26

Steering Through Turbulence Transfer pricing Dispute resolution Ho Chi Minh City, July 2019

Steering Through Turbulence

Transfer pricingDispute resolution

Ho Chi Minh City, July 2019

1© 2019 KPMG Limited, KPMG Tax and Advisory Limited, KPMG Legal Limited, all Vietnamese limited liability companies and member firms of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Document Classification: KPMG Confidential

Result on tax audit/

inspection

Procedures on Tax Audit/Inspection

- Send out to tax payers the decision within 15 days from issuance date- Tax payers are allowed to request a delay of on-site tax audit/inspection review, subject to tax authority’s decision

Minutes on tax audit/

inspection- Tax audit: 5 - 10 days

- Tax inspection:+ By provincial level: 30 -45 days+ By the General Department of Taxation (“GDT”): 45 - 70 days

- Tax audit: within 7-30 days after completion of on-site review: issue Decision on tax audit- Tax inspection: within 30 days from the tax inspection: issue Decision on tax inspection

On-site tax audit/inspection

review

Decision on tax audit/ inspection

(i) Announce the draft Minutes on tax audit/ inspection within 5 days after finishing on-site review(ii) Conclude/sign up the Minutes(iii) Tax payer still can provide more explanation between (i) and (ii)

2© 2019 KPMG Limited, KPMG Tax and Advisory Limited, KPMG Legal Limited, all Vietnamese limited liability companies and member firms of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Document Classification: KPMG Confidential

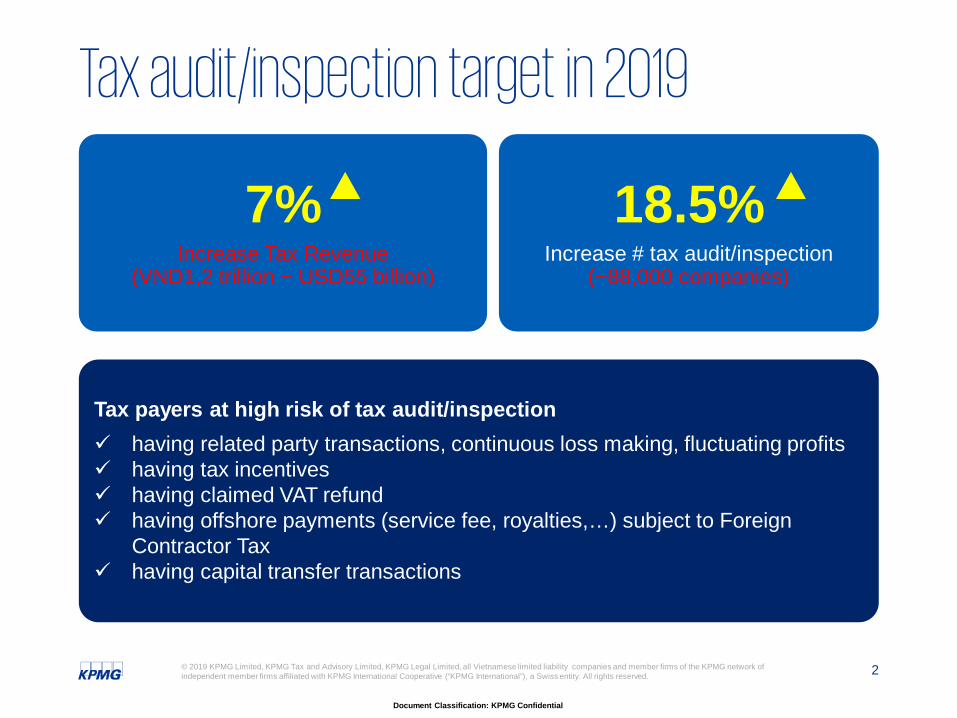

Tax audit/inspection target in 2019

Tax payers at high risk of tax audit/inspection having related party transactions, continuous loss making, fluctuating profits having tax incentives having claimed VAT refund having offshore payments (service fee, royalties,…) subject to Foreign

Contractor Tax having capital transfer transactions

7%Increase Tax Revenue

(VND1,2 trillion ~ USD55 billion)

18.5% Increase # tax audit/inspection

(~88,000 companies)

3© 2019 KPMG Limited, KPMG Tax and Advisory Limited, KPMG Legal Limited, all Vietnamese limited liability companies and member firms of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Document Classification: KPMG Confidential

Areas of TP focus / challenge

COMPLIANCE

DATA REPORTING (Accuracy & consistency)

COMPARABLE DATA

4© 2019 KPMG Limited, KPMG Tax and Advisory Limited, KPMG Legal Limited, all Vietnamese limited liability companies and member firms of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Document Classification: KPMG Confidential

Areas of TP focus / challenge

Art 9-2(d) Art 12-3 of Decree 20:

“Tax authorities have the right to make TP assessment (using database of tax authorities, i.e., ‘secret’ data)…if taxpayer commits the following violations:

- Failure to submit RPT declaration (Form 1) or submitting incomplete forms- Failure to provide TP documentation within the permitted time limited as

requested by tax authority; or submitting “insufficient” information- Providing untruthful / unlawful information- Inappropriate application of safe harbor / exemption rules (Article 11)”

5© 2019 KPMG Limited, KPMG Tax and Advisory Limited, KPMG Legal Limited, all Vietnamese limited liability companies and member firms of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Document Classification: KPMG Confidential

Areas of TP focus / challenge

Compliance

• Failure to file Related Party Transactions Disclosure Forms, or filing of incomplete forms

• TP documentation was not “contemporaneous” (not prepared in reasonable time when RPTs occurred (Cir 66) or by the CIT filing date(Decree 20)

• TP documentation not submitted to the tax authorities within the prescribed timeline, or submission of incomplete TP documentation

6© 2019 KPMG Limited, KPMG Tax and Advisory Limited, KPMG Legal Limited, all Vietnamese limited liability companies and member firms of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Document Classification: KPMG Confidential

Areas of TP focus / challenge

Data reporting

(Accuracy & consistency)

• Inaccurate figures disclosed (inconsistency with audited financials, source data, etc.)

• Inconsistent disclosure of RPTs between TP forms and TP documentation

• Inconsistent disclosure of TP methods between TP forms and TP documentation

7© 2019 KPMG Limited, KPMG Tax and Advisory Limited, KPMG Legal Limited, all Vietnamese limited liability companies and member firms of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Document Classification: KPMG Confidential

Areas of TP focus / challenge

Comparable data

• Tax officials will attempt to scrutinize the taxpayer’s benchmarking analysis. Common challenges include

‒ No Vietnamese comparables‒ Data of comparables not reliable (i.e., no audited financials)‒ No evidence to prove comparables enter into transactions at

arm’s length‒ Comparables having different functions, products, etc.

• By discrediting the comparable data, tax official will assert that taxpayer was non-compliant and make TP adjustment using “secret” data.

8© 2019 KPMG Limited, KPMG Tax and Advisory Limited, KPMG Legal Limited, all Vietnamese limited liability companies and member firms of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Document Classification: KPMG Confidential

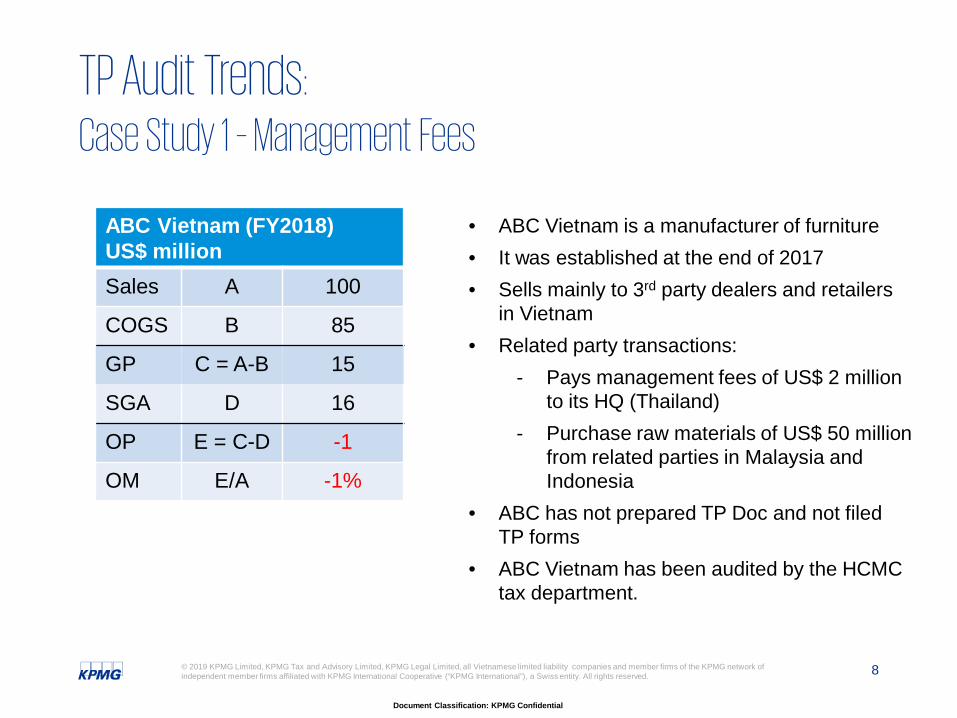

TP Audit Trends: Case Study 1 – Management Fees

ABC Vietnam (FY2018)US$ millionSales A 100

COGS B 85

GP C = A-B 15

SGA D 16

OP E = C-D -1

OM E/A -1%

• ABC Vietnam is a manufacturer of furniture• It was established at the end of 2017 • Sells mainly to 3rd party dealers and retailers

in Vietnam• Related party transactions:

- Pays management fees of US$ 2 million to its HQ (Thailand)

- Purchase raw materials of US$ 50 million from related parties in Malaysia and Indonesia

• ABC has not prepared TP Doc and not filed TP forms

• ABC Vietnam has been audited by the HCMC tax department.

9© 2019 KPMG Limited, KPMG Tax and Advisory Limited, KPMG Legal Limited, all Vietnamese limited liability companies and member firms of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Document Classification: KPMG Confidential

TP Audit Trends: Case Study 1 – Management Fees

Tax authority challenged two issues:1. Management fees paid are non-deductible

2. ABC Company incurred loss, so the transfer pricing is not arm’s length. Tax authority wants to make a TP adjustment to increase taxable profits of taxpayer

10© 2019 KPMG Limited, KPMG Tax and Advisory Limited, KPMG Legal Limited, all Vietnamese limited liability companies and member firms of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Document Classification: KPMG Confidential

TP Audit Trends: Case Study 1 – Management Fees

Management fees paid are non-deductible Have services actually been rendered? Do the services provide benefit to taxpayer? Is the amount of the service charge reasonable / reliable?

Before – tax / TP adjustmentUS$ millionSales A 100

COGS B 85

GP C = A-B 15

SGA D 16

OP E = C-D -1

OM E/A -1%

After adjustment of management feeUS$ millionSales A 100

COGS B 85

GP C = A-B 15

SGA D 14

OP E = C-D 1

OM E/A 1%

11© 2019 KPMG Limited, KPMG Tax and Advisory Limited, KPMG Legal Limited, all Vietnamese limited liability companies and member firms of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Document Classification: KPMG Confidential

TP Audit Trends: Case Study 1 – Management Fees

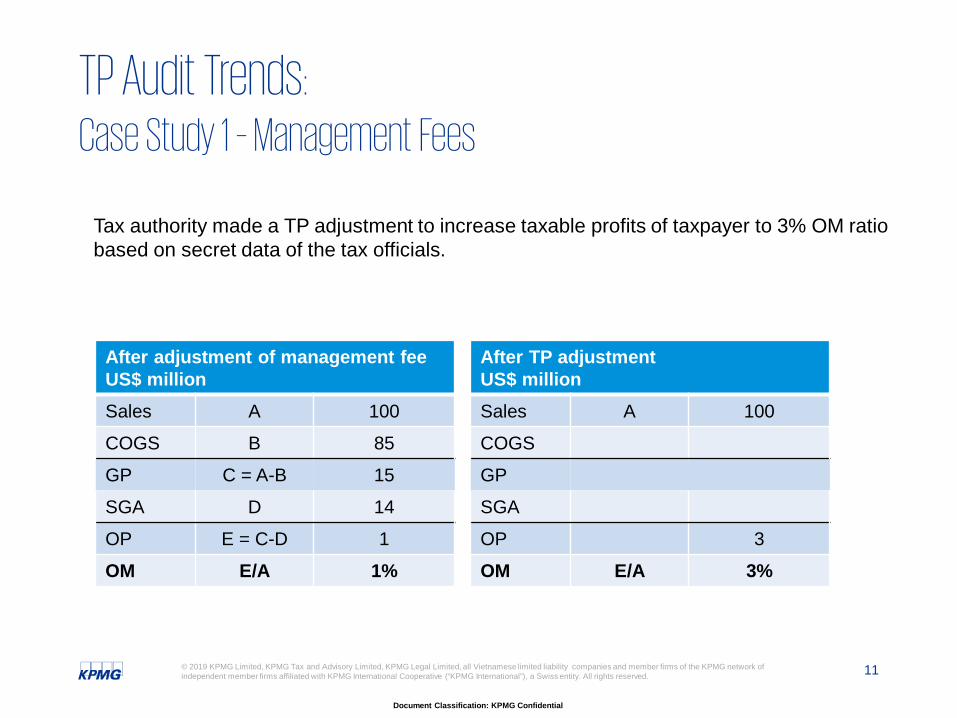

Tax authority made a TP adjustment to increase taxable profits of taxpayer to 3% OM ratio based on secret data of the tax officials.

After adjustment of management feeUS$ millionSales A 100

COGS B 85

GP C = A-B 15

SGA D 14

OP E = C-D 1

OM E/A 1%

After TP adjustmentUS$ millionSales A 100

COGS

GP

SGA

OP 3

OM E/A 3%

12© 2019 KPMG Limited, KPMG Tax and Advisory Limited, KPMG Legal Limited, all Vietnamese limited liability companies and member firms of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Document Classification: KPMG Confidential

TP Audit Trends: Case Study 1 – Management Fees

• Key issues:

Without TP Doc / TP forms, taxpayer does not have strong position to defend the audit

Intra-group services fee is the key focus of tax authority, and is extremely difficult to defend if not well prepared and without supporting documents.

Loss-making companies are often challenged by tax authority. Key arguments to support losses:

- Commercial reasons for the loss (start-up, high fixed costs, market entry strategy, etc.)

- External factors (loss of key customer, market downturn, competition, etc.)- Consider ‘appropriate’ benchmarking analysis

13© 2019 KPMG Limited, KPMG Tax and Advisory Limited, KPMG Legal Limited, all Vietnamese limited liability companies and member firms of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Document Classification: KPMG Confidential

TP Audit Trends: Case Study 2 – ‘True-down’ adjustment

ABC Vietnam (FY2018)US$ millionSales A 100

COGS B 50

GP C = A-B 50

SGA D 5

OP E = C-D 45

OM E/A 45%

• ABC Company is a trading company.

• Purchases all finished good from Parent Company (Thailand) and sells to 3rd party dealers and retailers.

• ABC Company achieved ‘super’ profits.

• Parent Company wants to make a downward profit adjustment to a “reasonable” level

14© 2019 KPMG Limited, KPMG Tax and Advisory Limited, KPMG Legal Limited, all Vietnamese limited liability companies and member firms of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Document Classification: KPMG Confidential

TP Audit Trends: Case Study 2 – ‘True-down’ adjustment

Key issues:

• Accounting & reporting - How / timing to actually book the adjustment? - Will the financial auditor agree to this?

• Tax / TP audit- What are the risks / challenges from tax authority?

• Other issues- Customs risks?- Cash remittance?

15© 2019 KPMG Limited, KPMG Tax and Advisory Limited, KPMG Legal Limited, all Vietnamese limited liability companies and member firms of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Document Classification: KPMG Confidential

Tax / TP audits in Vietnam- No standardized process for transfer pricing audit is available, leading to

inconsistent approaches among local tax authorities

- Taxpayers should pay attention to the timeline request for the submission or supplement/ explanation of information during tax audit

- Tax authorities are under pressure of conducting and completing audits in tight time frame.

- Content in draft Audit Minutes can be revised and negotiated several times before taxpayers and tax authorities reach an agreement.

- Recourse / appeal available to taxpayer, including review from high-level authority (MoF/GDT), court / litigation and mutual agreement procedures (MAP).

16© 2019 KPMG Limited, KPMG Tax and Advisory Limited, KPMG Legal Limited, all Vietnamese limited liability companies and member firms of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Document Classification: KPMG Confidential

Before the tax audit/inspection Comprehensive review of tax returns and payment

In case of incorrect declarations (or positions that can not be supported), consider to self-declare additional tax liability before receiving Decision on tax audit/inspection (to avoid penalty)

Understand and ask tax authority about reasons for tax audit/inspection and a list of documents to be prepared/provided for tax audit/inspection

Arrange time to fully and well prepare before tax audit/inspection; may request the tax authorities to postpone the tax audit/inspection time in order to prepare carefully

Notice to relevant departments (for example, regional/head quarter finance director)

Involve external advisors to review tax issues for timely adjustments and/or reporting

Tips for preparing for tax audit/inspection

17© 2019 KPMG Limited, KPMG Tax and Advisory Limited, KPMG Legal Limited, all Vietnamese limited liability companies and member firms of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Document Classification: KPMG Confidential

During on-site tax audit/inspection review Appoint qualified/experience staff to work with tax audit/inspection teams (e.g.

head of tax administration, chief accountant)

Try to resolve issues through dialogue before being recorded in Minutes on taxaudit/inspection

Be prepared to negotiate and accept “win-win” solutions that benefit bothparties

Consult the board of directors' opinions on important issues, actively seek helpand update all employees

Pre-discussion with tax officials that companies can appeal/dispute tax audit/inspection results to avoid their surprises

When requested to sign Memorandum of Facts, ensure the documents havebeen reviewed and approved by the Board of Directors. If not, only "confirm" butnot "agree" the adjustments made by tax audit/inspection team

Tips for preparing for tax audit/inspection

18© 2019 KPMG Limited, KPMG Tax and Advisory Limited, KPMG Legal Limited, all Vietnamese limited liability companies and member firms of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Document Classification: KPMG Confidential

Upon completion of the on-site tax audit/inspection review Carefully review Memorandum of Facts and Minutes on tax audit/inspection

and consider consulting with tax consultants

Decide which adjustments are acceptable or unacceptable

Prepare comments to include in the minutes and sign the minutes on time;apply for an extension, if needed

If there is still a dispute, consider putting a conservative opinion in theminutes and ask for guidance from the GDT/MOF

When Decision on tax audit/inspection is issued by the tax authority, pay thetax collection and penalties while carrying out the dispute procedures to avoidinterest penalties for late payment and enforcement measures

Submit dispute documents on time (within 90 days for the 1st dispute and 30days for the 2nd dispute). If you have any doubts about the tax treatment plan,make a dispute first and then accept it

Tips for preparing for tax audit/inspection

19© 2019 KPMG Limited, KPMG Tax and Advisory Limited, KPMG Legal Limited, all Vietnamese limited liability companies and member firms of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Document Classification: KPMG Confidential

KPMG’s experience in tax audit/inspection support

The only Big 4 who have a dedicated and experienced tax audit and controversy working team

In just 3 years

..large FDI companies assisted with their tax audit under the MOF, GDT and

provincial tax audit programs

100+

Corp

orat

e Ta

x

Transfer Pricing

Co-Team:9 Partners, 8 Directors

20 Associate Directors & Managers

Core team:01 Director, 02

Associate Directors, 01 Manager, 01

Senior Consultant

20© 2019 KPMG Limited, KPMG Tax and Advisory Limited, KPMG Legal Limited, all Vietnamese limited liability companies and member firms of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Document Classification: KPMG Confidential

KPMG’s experience in tax audit/inspection support Being the largest tax consulting firm in Vietnam

Have a close and good relationship with the Ministry of Finance, General Department

of Taxation and local tax departments

Well anticipate tax issues/adjustments that may arise before and during the tax

audit/inspection process

Can assist your company in providing professional opinions on issues raised by tax

authorities

Have extensive expertise and experience to help you get the best results in the

process of negotiating/resolving disputes with tax authorities

Can provide package services to you from pre, during and post tax audit/inspections

21© 2019 KPMG Limited, KPMG Tax and Advisory Limited, KPMG Legal Limited, all Vietnamese limited liability companies and member firms of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Document Classification: KPMG Confidential

KPMG’s tax audit/inspection support services

Develop a tax risk management strategy (e.g. tax policy formulation, or review the implementation of tax plans)

Study trends of tax issues and hot issues in new or developing areas

Advising on tax risks and tax strategy proposals

Review tax compliance for tax audit/ inspection

Assist in preparing/ presenting information and documents to provide tax audit/ inspection teams

Support to review before tax inspection to prevent and minimize tax and penalty costs incurred

Participate in the explanation of the required information for the tax audit/ inspection team

Advise explanation contents for tax audit/ inspection teams

Attend the meeting with the tax audit/ inspection team

Professional support and strategic advice throughout the tax audit/ inspection period to obtain the most favorable results

Reviewing Minutes on tax audit/inspection

Suggest appropriate feedback

Advising and analyzing which tax issues in the Minutes and Decisions on tax collection should consider making dispute

Strategic advice on tax risk management

Preparation before tax audit/ inspection

Technical support in tax audit/ inspection

Post tax audit/ inspection review

22© 2019 KPMG Limited, KPMG Tax and Advisory Limited, KPMG Legal Limited, all Vietnamese limited liability companies and member firms of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Document Classification: KPMG Confidential

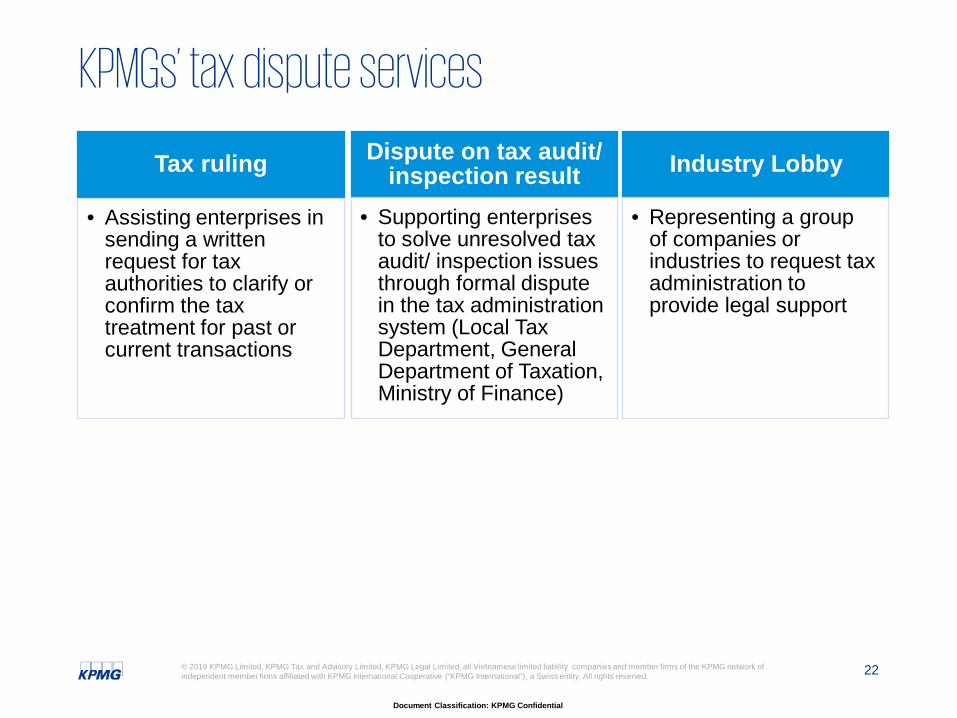

KPMGs’ tax dispute services

Tax ruling

• Assisting enterprises in sending a written request for tax authorities to clarify or confirm the tax treatment for past or current transactions

Dispute on tax audit/ inspection result

• Supporting enterprises to solve unresolved tax audit/ inspection issues through formal dispute in the tax administration system (Local Tax Department, General Department of Taxation, Ministry of Finance)

Industry Lobby

• Representing a group of companies or industries to request tax administration to provide legal support

Q&A

24© 2019 KPMG Limited, KPMG Tax and Advisory Limited, KPMG Legal Limited, all Vietnamese limited liability companies and member firms of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Document Classification: KPMG Confidential

Curriculum vitae – Joseph Vu

Joseph VuPartner,Transfer Pricing Services

Mobile: +84 918571771Email: [email protected]

Education, Licenses and Certifications• Bachelor of Arts, University of

California, Los Angeles• AICPA

Background

Joe has recently joined KPMG as a partner in our transfer pricing services. Joe brings tremendousknowledge and experience through his 17 years of transfer pricing consulting with another Big 4 firm.Over his professional career, he worked in the US, Japan and China before relocating to his nativeVietnam in 2015.Joe maintains strong working relationship with the GDT, and has frequently been invited as guest speakerin various forums and events held by the government to share insights on transfer pricing matters,including commentary on legislative reforms, providing technical training, and sharing of internationalpractices. Notably, Joe was invited by the delegation from Vietnam’s Ministry of Finance / GDT to meetwith the OECD, UN and World Bank representatives in Europe to share insights on administration oftransfer pricing for developing countries

Selected Experience:

• Joe has been involved in wide range of transfer pricing engagements, including compliance,developing group pricing policies, and tax dispute resolution.

• Joe specializes in tax controversy services and is experienced in formulating strategies andnegotiating with tax officials on difficult cases.

• He supported high-profile clients to lodge the first five (5) bilateral APAs in Vietnam, and workedclosely with Vietnam’s General Department of Taxation (GDT) on the first MAP case involving cross-border transfer pricing dispute, which is near conclusion.

• Joe maintains strong working relationship with the GDT, and has frequently been invited as guestspeaker in various forums and events held by the government to share experience and insights.

25© 2019 KPMG Limited, KPMG Tax and Advisory Limited, KPMG Legal Limited, all Vietnamese limited liability companies and member firms of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Document Classification: KPMG Confidential

Contact usKPMG Tax and Advisory Limited

Warrick Cleine Chairman & CEOVietnam and Cambodia Tax Managing Partner

HanoiDo Thi Thu Ha, Senior PartnerHoang Thuy Duong, PartnerLe Thi Kieu Nga, PartnerNguyen Thu Huong, PartnerNguyen Ngoc Thai, DirectorNguyen Hai Ha, DirectorPham Thi Quynh Ngoc, Director Ho Dang Thanh Huyen, Director Nguyen Huong Giang, Director Nguyen Manh Cuong, Director Le Minh Thu, Director Tran Thi Thuy Ha, Director Tran Van Trung, Director Pham Quynh Oanh, Director Tran Thi Thanh Minh, Director Ryosuke Okado, Japanese Desk

46th Floor, Keangnam Hanoi Landmark Tower, 72 Building, Plot E6, Pham Hung Street, Cau Giay New Urban Area, Me Tri Ward, South Tu Liem District, Hanoi, VietnamT: +84 (24) 3946 1600F: +84 (24) 3946 1601E: [email protected]

Ho Chi Minh CityNguyen Cong Ai, Partner Richard Stapley-Oh, Partner Ninh Van Hien, PartnerTa Hong Thai, PartnerHo Thi Bich Hanh, Partner Huynh Ngoc Nhan, Partner Dean Rolfe, PartnerJoseph Vu, PartnerAndrea Godfrey, Executive Director Nguyen Thanh Hoa, Director Nguyen Thanh Tam, Director Tran Duy Binh, DirectorBui Thi Thanh Ngoc, Director Pham Thi Thuy Hong, Director Nguyen Quang Phuc, Director Punnika Kaewsrion, Thai Desk

10th Floor, Sunwah Tower, No. 115, Nguyen Hue Street, Ben NgheWard, District 1, Ho Chi Minh City, VietnamT: +84 (28) 3821 9266F: +84 (28) 3821 9267E: [email protected]