24

Wind energy Stefan Karlsson Global Segment Manager, Renewable Energy Capital Markets Day 2009

Wind energy

Stefan Karlsson

Global Segment Manager, Renewable Energy

Capital Markets Day 2009

19 May 2009 © SKF Group

The dynamicwind energy market

Wind energy business development snapshot

Global Wind Power StatusCumulative MW by end of 2002, 2005 & 2008

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

Europe USA Asia Rest of World2002 (32,037 MW) 2005 (59,399 MW) 2008 (122,158 MW)Source: BTM Consult ApS - March 2009

Year: Installed MW Increase % Cumulative MW Increase %2003 8,344 40,3012004 8,154 -2% 47,912 19%2005 11,542 42% 59,399 24%2006 15,016 30% 74,306 25%2007 19,791 32% 94,005 27%2008 28,190 42% 122,158 30%

27.6% 24.8%Source: BTM Consult ApS - March 2009

Average growth - 5 years

Global Wind Power ForecastCumulative MW by end of 2007 & Forecast 2012

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

160,000

Europe USA Asia Rest of World

2008 (122,158 MW) 2013 (343,153 MW)Source: BTM Consult ApS - March 2009

Wind development activity is shifting from Europe to North America and Asia-Pacific. By 2020, Europe is expected to account for 27% of new capacity added worldwide, compared to 31% for North America and 42% for Asia-Pacific.

19 May 2009 © SKF Group

Wind energy market development

Actual

2003-2008

Trend

Next

12 months

Trend

After 12 months and

forward

Wind energy

Globally

• Speed of growth globallyexpected to fall from >30% to around 10% during 2009.

Europe • Limited effect on investments by credit crunch.

North America

• Delay in new windfarm projects2009 due to limited financing. ARRA expected to give effect by Q4 2009.

AsianMarkets

• Explosive growth continuing in China. India suffering from effectsof financial crisis.

+++

+++

++ +++

+++ ++ +++

+++

+++

+++

+++=

+++ annual growth > 15%++ annual growth 10 to 15%+ annual growth 5 to 10%= 0 to + 5%- annual decline 0 to -5%

19 May 2009 © SKF Group

The macroeconomy effects on wind energy

• Wind energy at an early stage of a long term growth phase, business fundamentals for the industry are strong. Long term growth >20%/year.

• The present credit crunch has resulted in postponement and cancellationof some externally financed windfarm projects, mainly in USA and India.

• Manufacturers affected by this downturn are mainly producers with high exposure in the US market, as well as their sub-system suppliers.

• The recently approved stimulus package for the US economy, includingareas for renewable energy, will create renewed dynamic growth;– ”American Recovery and Reinvestment Act 2009”

– Proposed legislation for USD 20 billion in tax cuts to support growth of renewableenergy, including a multiyear extenstion of PTC. (Production Tax Credit)

– A total of USD 8 billion proposed to be allocated for Renewable Energy Loan Guarantees.

• MRO-service market not affected – windfarm service activities as normal

19 May 2009 © SKF Group

Expectations of a quick business recovery

Source: Vestas annual report 2008

19 May 2009 © SKF Group

Globalisation of wind energy market

• Environmentally concerns, security of fuel supply and demand for additional electricity output are driving the establishment of renewable energy support systems in several new markets.

• Windturbine manufacturing base expanding rapidly from a few countries, to form a truly global market.

• China has in just a few years expanded to become the global market leader of wind turbines in a few years.

• Korea on the brink of taking off as a major windturbinemanufacturing base, Canada and Latinamerica to follow.

19 May 2009 © SKF Group

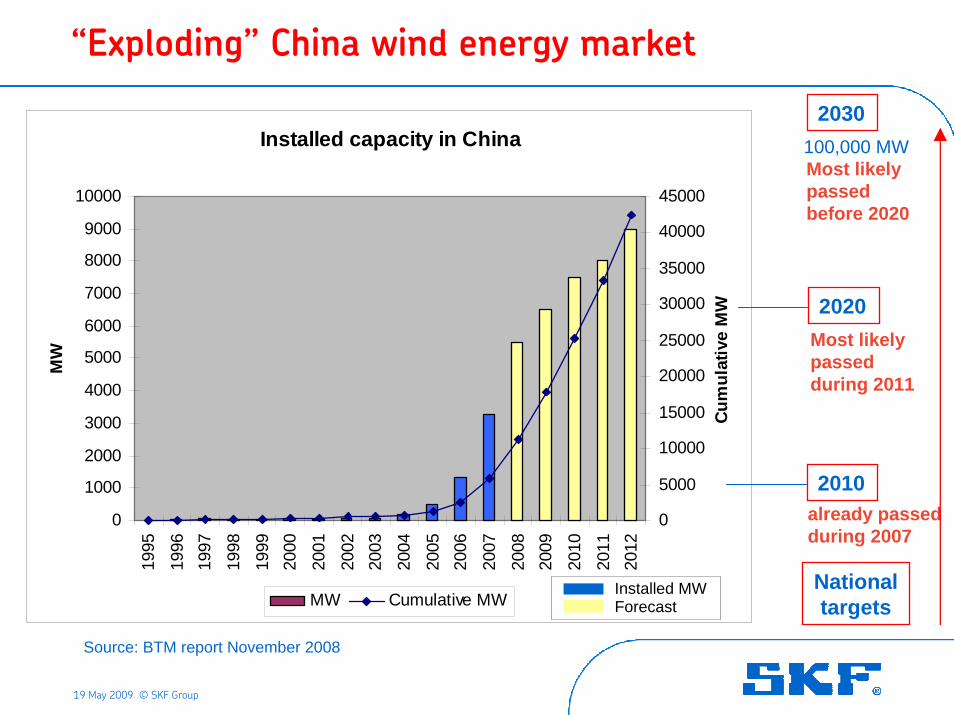

“Exploding” China wind energy market

Installed capacity in China

0

1000

2000

3000

4000

5000

6000

7000

8000

9000

10000

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

MW

0

5000

10000

15000

20000

25000

30000

35000

40000

45000

Cum

ulat

ive

MW

MW Cumulative MWInstalled MWForecast

National targets

2020

2010already passedduring 2007

Most likelypassedduring 2011

2030100,000 MWMost likelypassedbefore 2020

Source: BTM report November 2008

19 May 2009 © SKF Group

19 May 2009 © SKF Group

SKF in wind energy

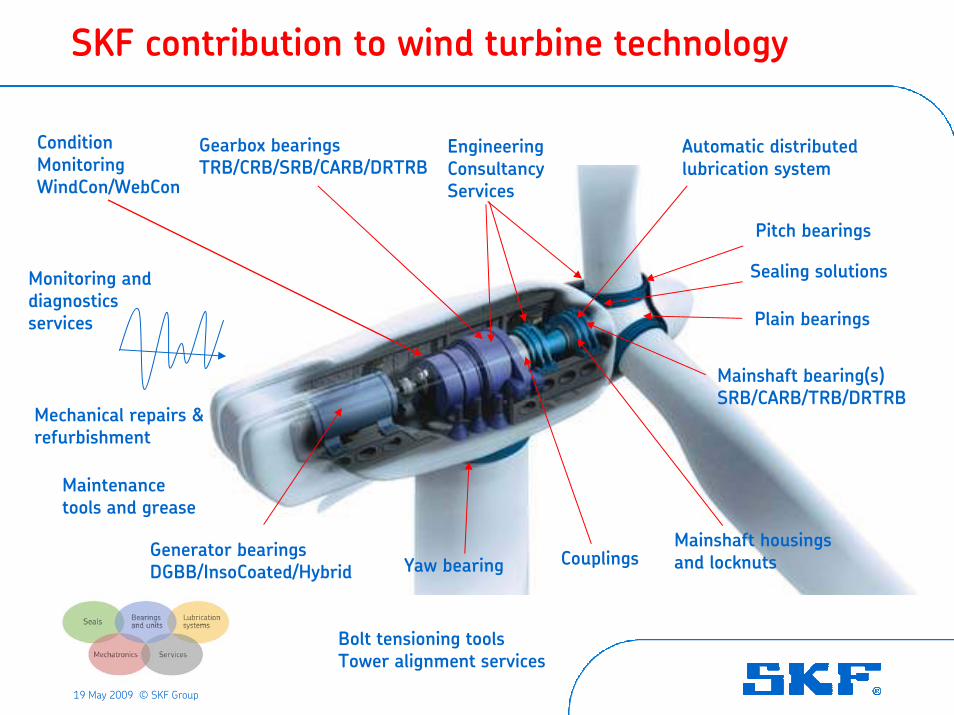

SKF contribution to wind turbine technology

19 May 2009 © SKF Group

Pitch bearings

Yaw bearingMainshaft housingsand locknuts

ConditionMonitoringWindCon/WebCon

Couplings

Automatic distributedlubrication system

Monitoring and diagnosticsservices

Mechanical repairs &refurbishment

Sealing solutions

EngineeringConsultancyServices

Plain bearings

Maintenancetools and grease

Gearbox bearingsTRB/CRB/SRB/CARB/DRTRB

Generator bearingsDGBB/InsoCoated/Hybrid

Mainshaft bearing(s)SRB/CARB/TRB/DRTRB

Bolt tensioning toolsTower alignment services

SKF is a supplier to all major manufacturers

Wind turbine manufacturers (global ranking)Rank Manufaturer Homebase MW-output 2008

1 Vestas Denmark 5,5812 GE-Wind USA 5,2393 Gamesa Spain 3,3734 Enercon Germany 2,8065 Suzlon India 2,5266 Siemens Denmark 1,9477 Sinovel China 1,4038 Acciona Spain 1,2909 Goldwind China 1,132

10 Nordex Germany 1,07511 Dong Fang China 1,05312 REpower Germany 943

Wind-gearbox manufacturers (global ranking)Rank Manufaturer Homebase

1 Winergy Germany2 Hansen Belgium3 Bosch-Rexroth Germany4 Moventas Finland5 Nanjing GC China

Source: BTM Consult ApS March 2009:

19 May 2009 © SKF Group

SKF business development beyond market growth

Annual Wind Power DevelopmentActual 1990-2008 & Forecast 2009-2013

0

10,000

20,000

30,000

40,000

50,000

60,000

1990 1995 2000 2008 2013

MW

Europe USA Asia Rest of World ExistingSource: BTM Consult ApS - March 2009

19 May 2009 © SKF Group

Recent SKF market launches - wind energy industry

New pitch bearingdesign with improvedcorrosion protection

DRTRB-unit Nautilus™with segmented cagefor minimized friction

New CRB-design withextra-high carrying capacityfor wind-gearboxes.

XL Hybrid bearingswith ceramic ballsfor superior insulation

SKF WindCon 3.0/WebconIntranet supervisedcondition monitoring

Automatic centralizedlubrication kits for reduced maintenance cost

19 May 2009 © SKF Group

19 May 2009 © SKF Group

Business Case: SKF Nautilus™

The new wind-mainshaft DRTRB-unit Nautilus™

Patented segmented PEEK cage developed by SKF.

19 May 2009 © SKF Group

The unique benefits of SKF Nautilus™

The SKF test-rig for the large

mainshaft ”Nautilus™” bearing.

Nautilus™ key features;• Designed for heavy, complex loads.• Only pure torque load is being

transmitted to the drivetrain.• Segmented cage for improved

performance also under misalignment.• Extremely low friction coefficient.• Can be either oil or grease lubricated• Available for cold-climate locations

19 May 2009 © SKF Group

Milestones in Nautilus™ business development

• Developed to fulfill the challenging conditions and the specific requirements for a radical new turbine design (2002-2003).

• Officially market launched also for other turbine models (2005).

• 3 different windturbine manufacturers selected Nautilus™ as mainshaftarrangement for new turbine models (2006).

• 12 different windturbine models with Nautilus™ selected. Customers in Denmark, Germany, Belgium, Italy, India, Japan, China and Korea (2008).

• Several new upcoming windturbine models evaluating Nautilus™ (2009).

• Manufacturing capacity expansion in Schweinfurt, Germany and investment decision to start up manufacturing in Dalian, China (2009).

19 May 2009 © SKF Group

19 May 2009 © SKF Group

SKF Intelligence Center Wind

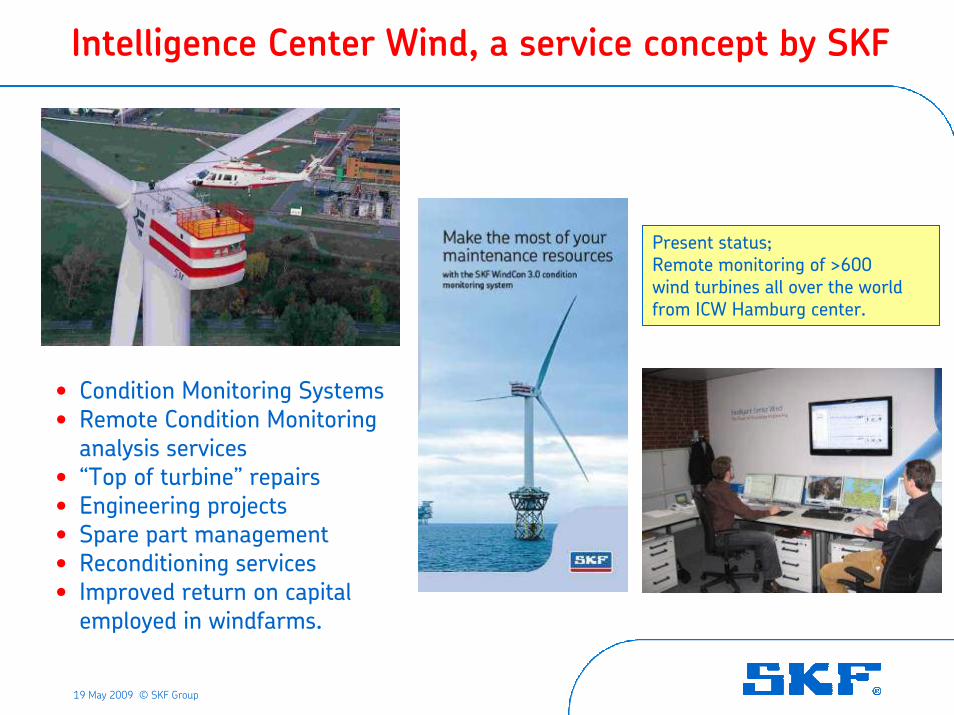

Intelligence Center Wind, a service concept by SKF

19 May 2009 © SKF Group

• Condition Monitoring Systems• Remote Condition Monitoring

analysis services • “Top of turbine” repairs• Engineering projects • Spare part management• Reconditioning services• Improved return on capital

employed in windfarms.

Present status;Remote monitoring of >600wind turbines all over the worldfrom ICW Hamburg center.

SKF Windfarm Service (ICW) • Europe-NAM-Asia

19 May 2009 © SKF Group

19 May 2009 © SKF Group

Summary & Conclusions

Renewable energy high on the agendas

19 May 2009 © SKF Group

”15% in 2020” ”20% by 2020”(some 34% of electricity)

*14% renewables in electricity 2006Actual: 7% renewables in 2007 Actual: 8% renewables in 2007

”10% in 2012””25% in 2025”

*) target on all prime energy

Key business message

• Speed of growth of wind energy industry temporarilyslowing down to some 10% during 2009. Back to ”normal”predicted already during 2010.

• Quick globalisation of the industry at present. New manufacturers in emerging markets. SKF already in place.

• SKF is well positioned with most leading manufacturers. • Nautilus™ well received by the market. Massive business

growth foreseen with Nautilus™ on new turbine models.• Intelligence Center Wind is positioning SKF as a partner

and a competence provider in windfarm service market. • SKF is actively involved in the development of the wind-

turbine technology of the future (onshore and offshore).

19 May 2009 © SKF Group