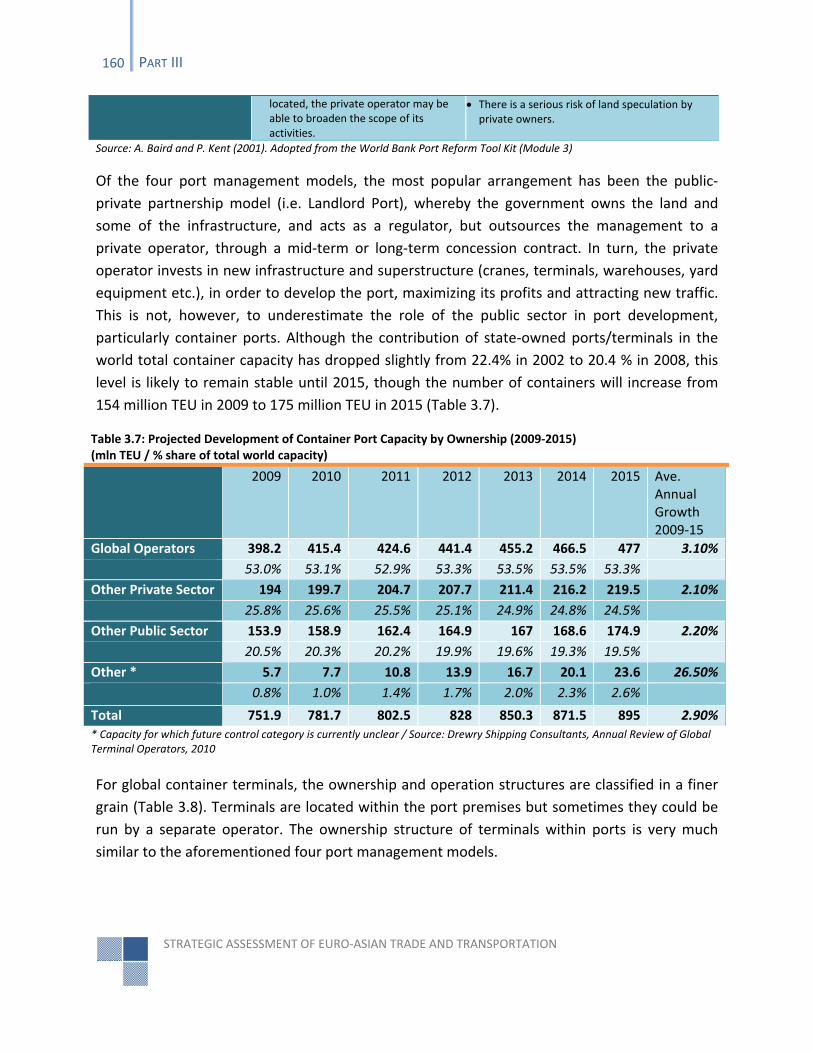

245

TALEH ZIYADOV JUNE 2011 Strategic Assessment of Euro‐Asian Trade & Transportation Azerbaijan as a Regional Hub in Central Eurasia

| Date post: | 08-Feb-2017 |

| Category: |

Documents |

| Upload: | hoangquynh |

| View: | 233 times |

| Download: | 9 times |

TALEH ZIYADOV

JUNE 2011

Strategic Assessment of Euro‐Asian Trade & Transportation

Azerbaijan as a Regional Hub in Central Eurasia

Strategic Assessment of Euro‐Asian Trade and Transportation

Azerbaijan as a Regional Hub in Central Eurasia

TALEH ZIYADOV

June 2011

Publisher Information (TBD): Azerbaijan Diplomatic Academy Baku, Azerbaijan Johns Hopkins University Washington, DC Please cite this work as: ….. ….

Cover Photo: Design Concept of New International Terminal at Heydar Aliyev International Airport in Baku, Azerbaijan. Courtesy of ARUP Engineering Company.

ISBN: Copyright ©

AZERBAIJAN AS A REGIONAL HUB IN CENTRAL EURASIA

TABLE OF CONTENTS

TABLE OF CONTENTS .......................................................................................................................................... V

PREFACE ........................................................................................................................................................... IX

ACKNOWLEDGEMENTS ................................................................................................................................... XIII

FOREWORD ...................................................................................................................................................... IX

EXECUTIVE SUMMARY ...................................................................................................................................... IX

ABBREVIATIONS ............................................................................................................................................. XVII

FIGURES & MAPS ............................................................................................................................................ XXI

TABLES .......................................................................................................................................................... XXIII

INTRODUCTION.................................................................................................................................................. 1

PART I: EURO‐ASIAN TRADE: THE BIG PICTURE ................................................................................................... 7

THE EURO‐ASIAN TRADE AND CENTRAL EURASIA ................................................................................................................. 9

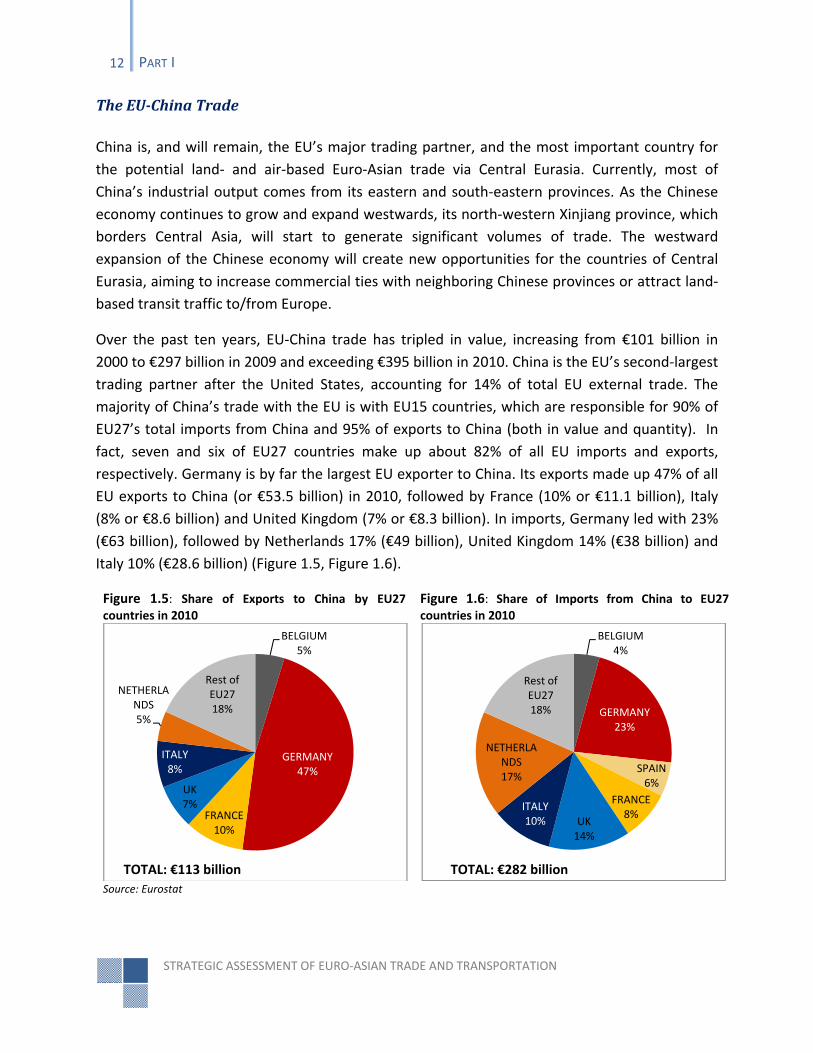

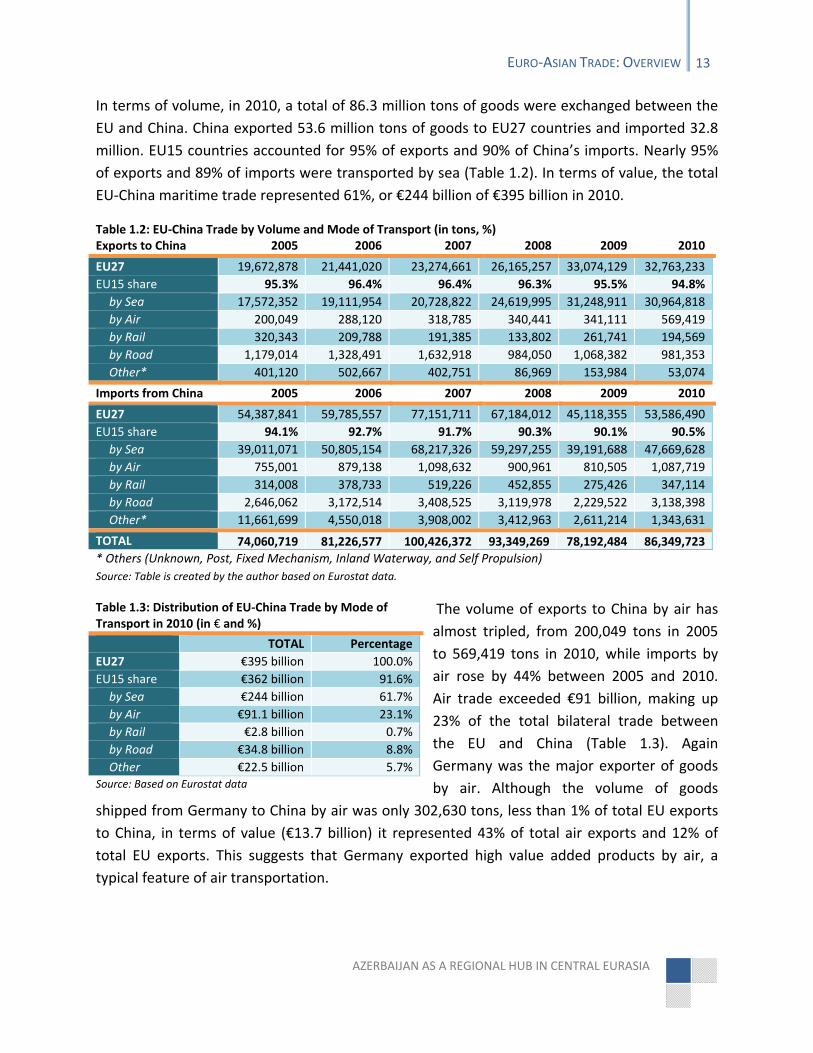

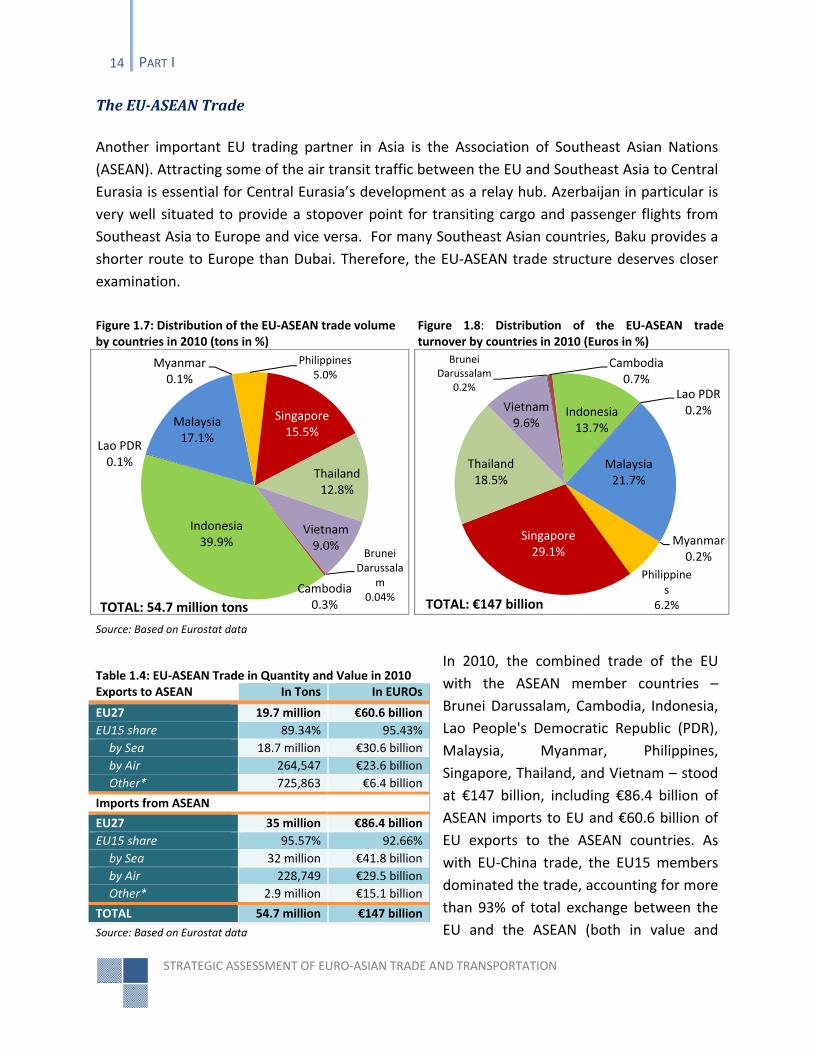

The Euro‐Asian Trade: Overview ........................................................................................................................... 9 The EU‐China Trade .......................................................................................................................................................... 12 The EU‐ASEAN Trade ........................................................................................................................................................ 14 The EU‐India Trade ........................................................................................................................................................... 15

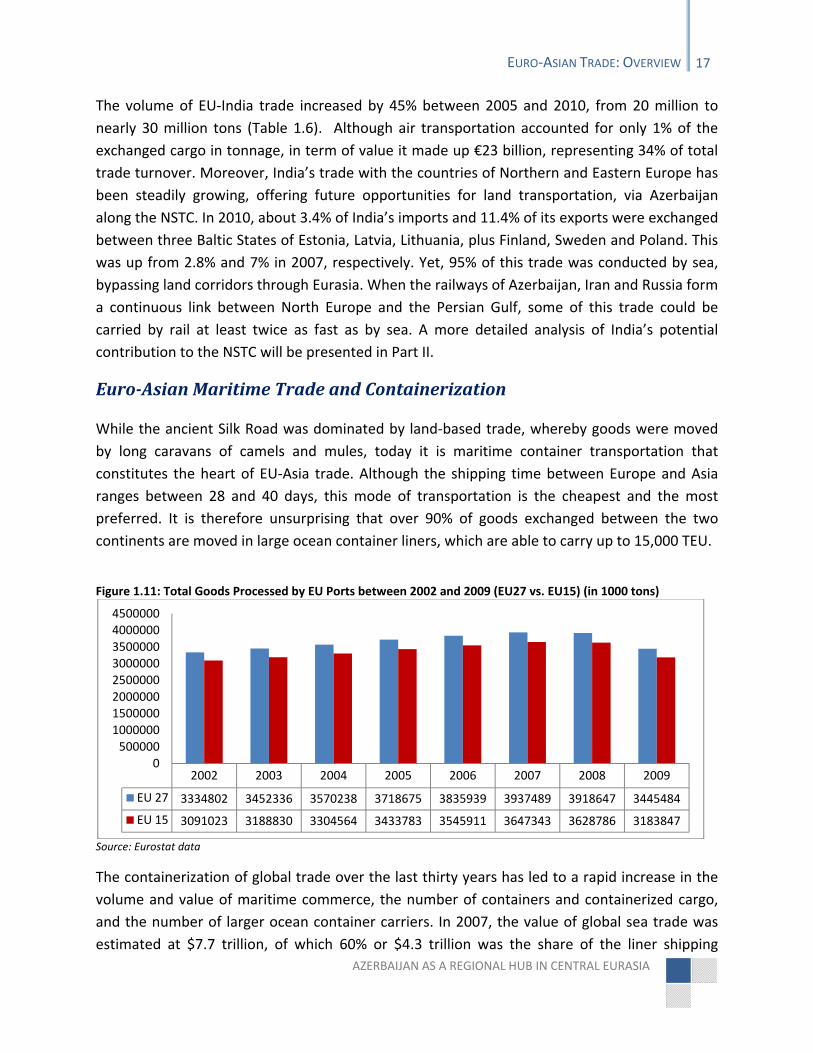

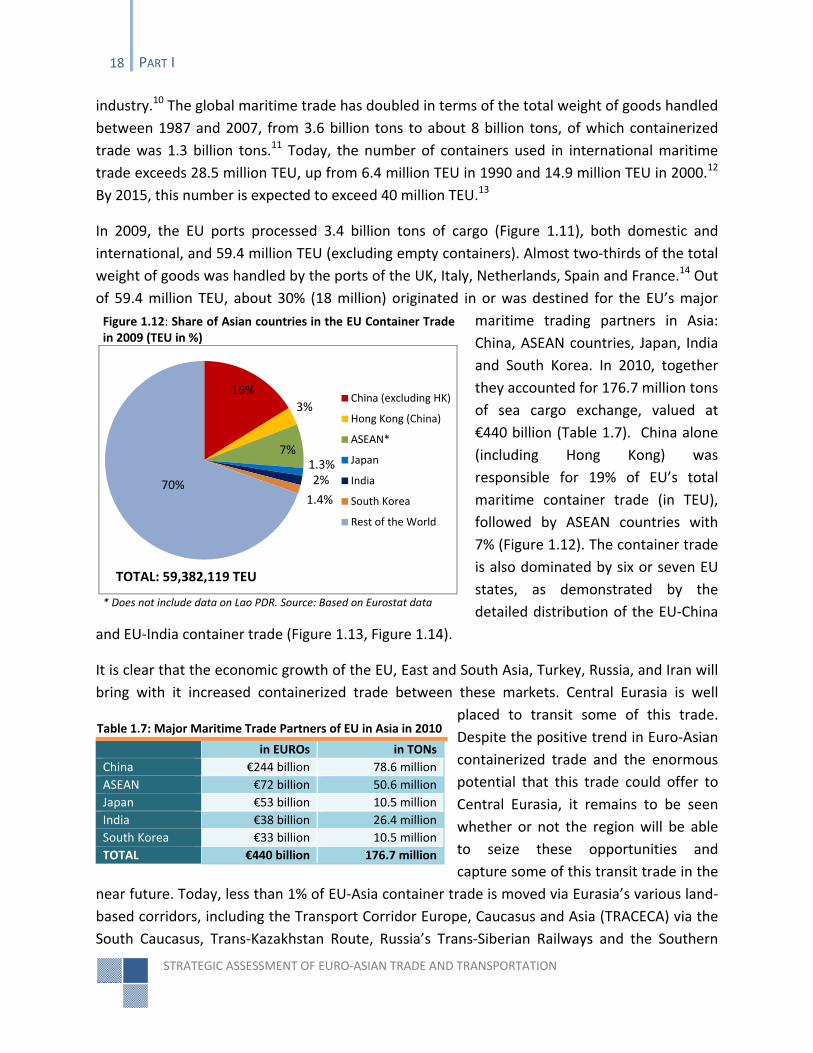

Euro‐Asian Maritime Trade and Containerization .............................................................................................. 17

PART II: ASSESSING THE PRESENT: TRANSPORT, CORRIDORS, AND LOGISTICS IN EURASIA ................................ 21

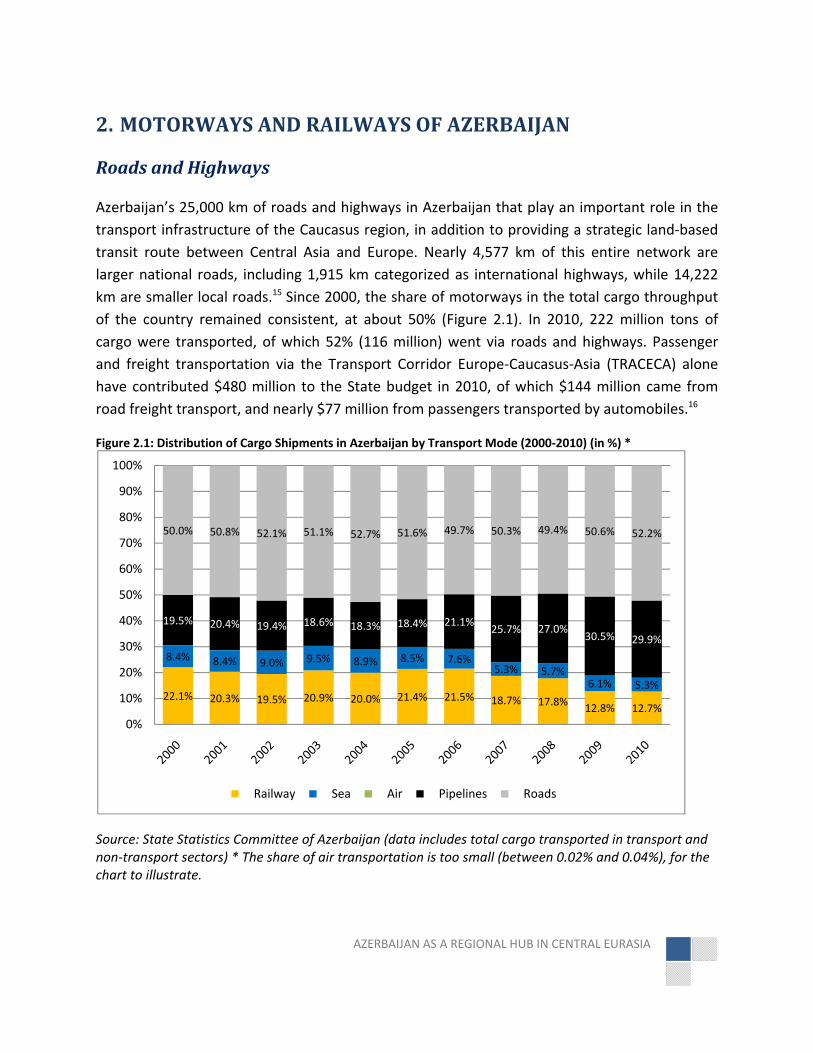

MOTORWAYS AND RAILWAYS OF AZERBAIJAN .................................................................................................................... 23

Roads and Highways ........................................................................................................................................... 23

Railways .............................................................................................................................................................. 26

EURASIAN TRANSPORT CORRIDORS .................................................................................................................................. 29

The Central Corridor: Transport Corridor Europe, Caucasus, Asia (TRACECA) .................................................... 29 A Limping Leg of the New Silk Road ................................................................................................................................. 29 Truck Transit via TRACECA vs. Alternatives ...................................................................................................................... 33

The Central Route to Afghanistan ............................................................................................................................... 33 The Southern Route ..................................................................................................................................................... 36 The Northern Route .................................................................................................................................................... 37 The Fastest Route ........................................................................................................................................................ 38 Advantages and Disadvantages of TRACECA for Trucking ........................................................................................... 38

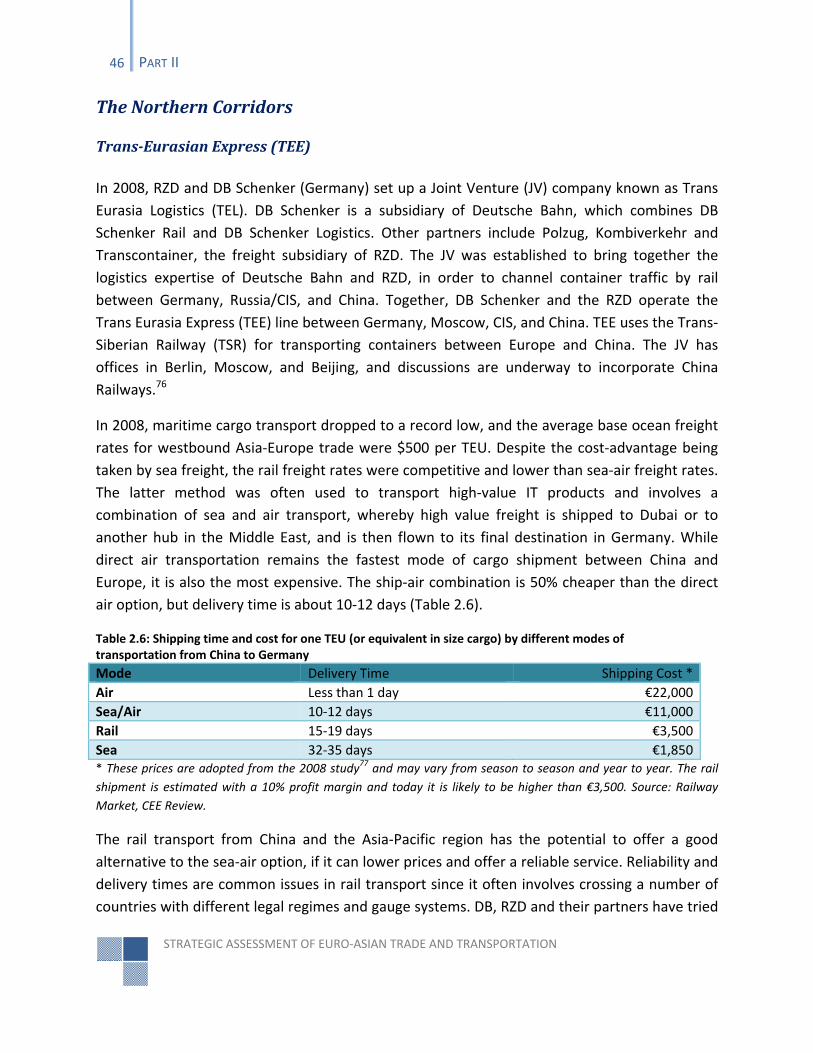

TRACECA and Rail Transportation .................................................................................................................................... 40 The Northern Corridors ....................................................................................................................................... 46

Trans‐Eurasian Express (TEE) ............................................................................................................................................ 46 Trans‐Siberian Railway (TSR) ............................................................................................................................................ 48 Trans‐Kazakhstan Routes ................................................................................................................................................. 55

The China Angle ........................................................................................................................................................... 64 The Southern Corridor ......................................................................................................................................... 66

STRATEGIC ASSESSMENT OF EURO‐ASIAN TRADE AND TRANSPORTATION

vi TABLE OF CONTENTS

The North‐South Transport Corridor (NSTC) ....................................................................................................... 74 The Western NSTC Route ................................................................................................................................................. 80

The western NSTC route: Highways ............................................................................................................................ 80 The western NSTC route: Railways .............................................................................................................................. 83

The Eastern NSTC Routes ................................................................................................................................................. 85 MARITIME TRANSPORTATION AND CASPIAN PORTS ............................................................................................................. 89

Overview ............................................................................................................................................................. 89

Caspian Ports ...................................................................................................................................................... 92 Baku .................................................................................................................................................................................. 92 Aktau ................................................................................................................................................................................ 95 Turkmenbashy .................................................................................................................................................................. 99 Astrakhan ....................................................................................................................................................................... 103 Ola .................................................................................................................................................................................. 105 Makhachkala .................................................................................................................................................................. 106 Iranian Ports ................................................................................................................................................................... 107 Anzali ............................................................................................................................................................................ 111 Amirabad ...................................................................................................................................................................... 112 Nowshahr ...................................................................................................................................................................... 113 Neka .............................................................................................................................................................................. 114

LOGISTICS & SUPPLY CHAIN ................................................................................................................................... 116

Logistics Market: Domestic vs. International .................................................................................................... 119

AIR TRANSPORTATION .......................................................................................................................................... 126

Passenger Traffic via Azerbaijan ....................................................................................................................... 127

Air Cargo Traffic via Azerbaijan ........................................................................................................................ 132 Baku Cargo Terminal & Silk Way Airlines ....................................................................................................................... 134

PART III: FREE ECONOMIC ZONES AND PORT DEVELOPMENT IN THE 21ST CENTURY .......................................... 141

FREE ECONOMIC ZONE DEVELOPMENT .......................................................................................................................... 143

FEZ Development in Azerbaijan ........................................................................................................................ 145

Strategic Planning for FEZ Development ........................................................................................................... 149

FEZ Administration and Operation Models ....................................................................................................... 151

Challenges in FEZ Development ........................................................................................................................ 152

THE ALYAT PORT AND 21ST CENTURY PORT DEVELOPMENT ................................................................................................ 155

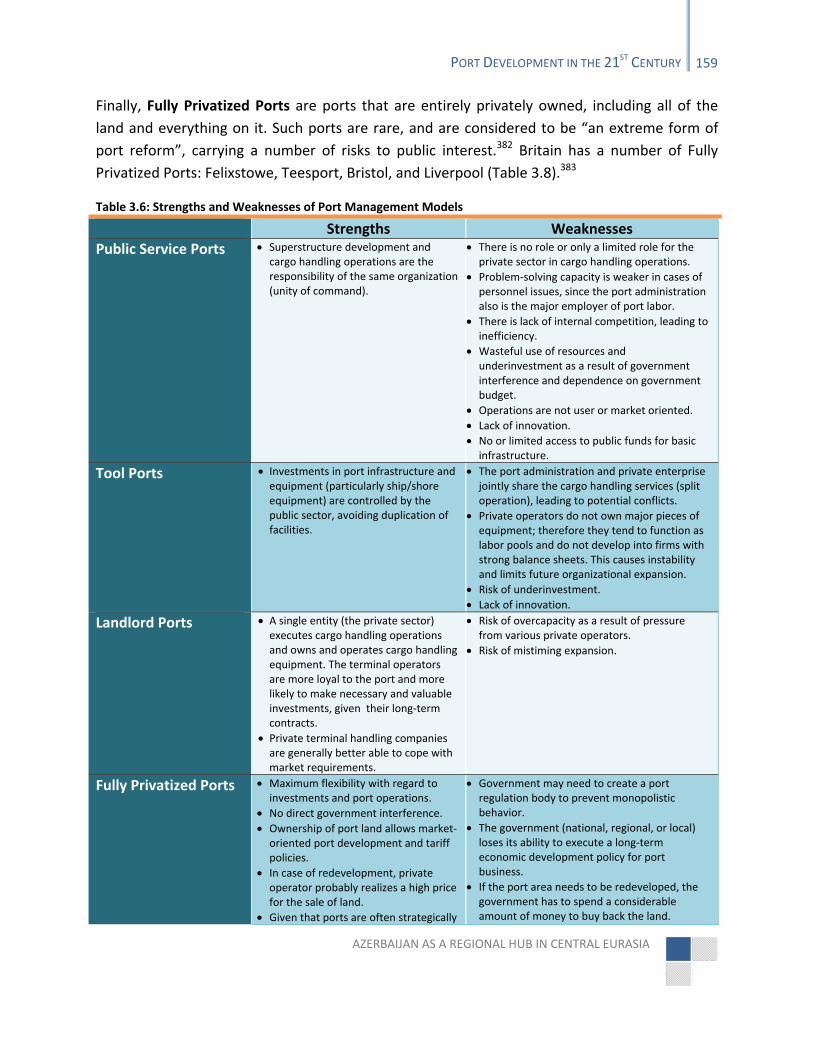

The Global Port Industry and Port Reform Process ........................................................................................... 156

Main Actors in Port Development ..................................................................................................................... 157

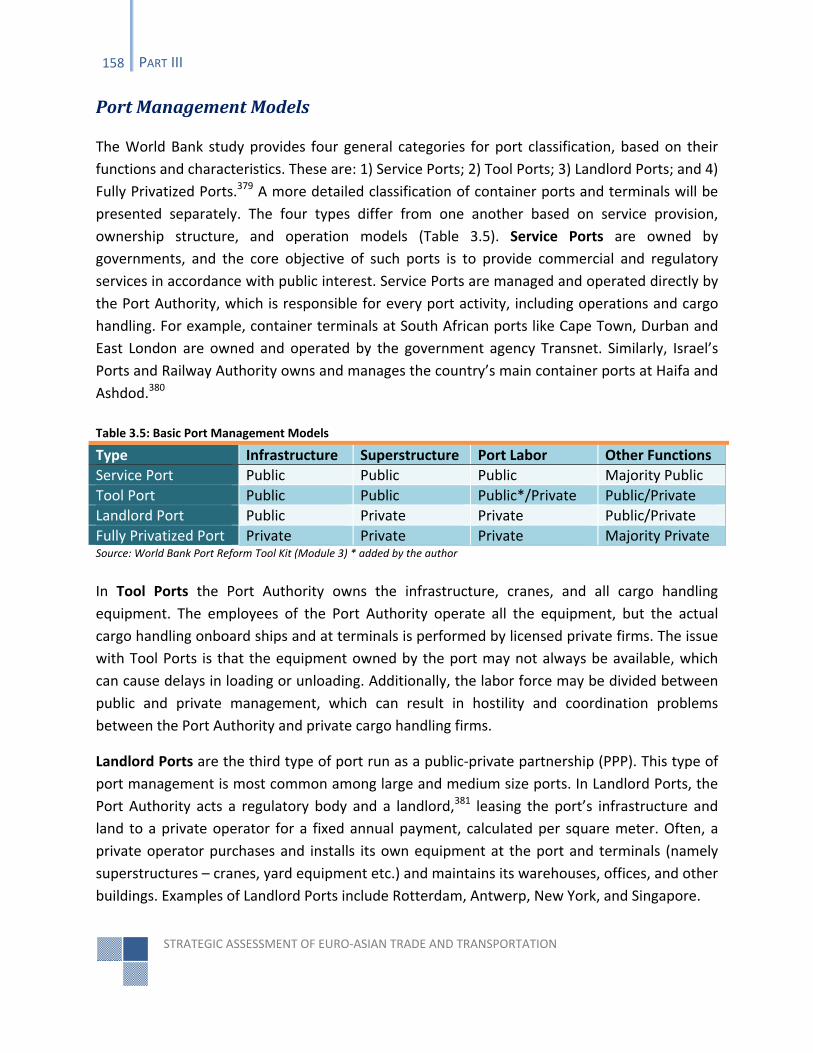

Port Management Models ................................................................................................................................ 158

Modes and Forms of Privatization .................................................................................................................... 161

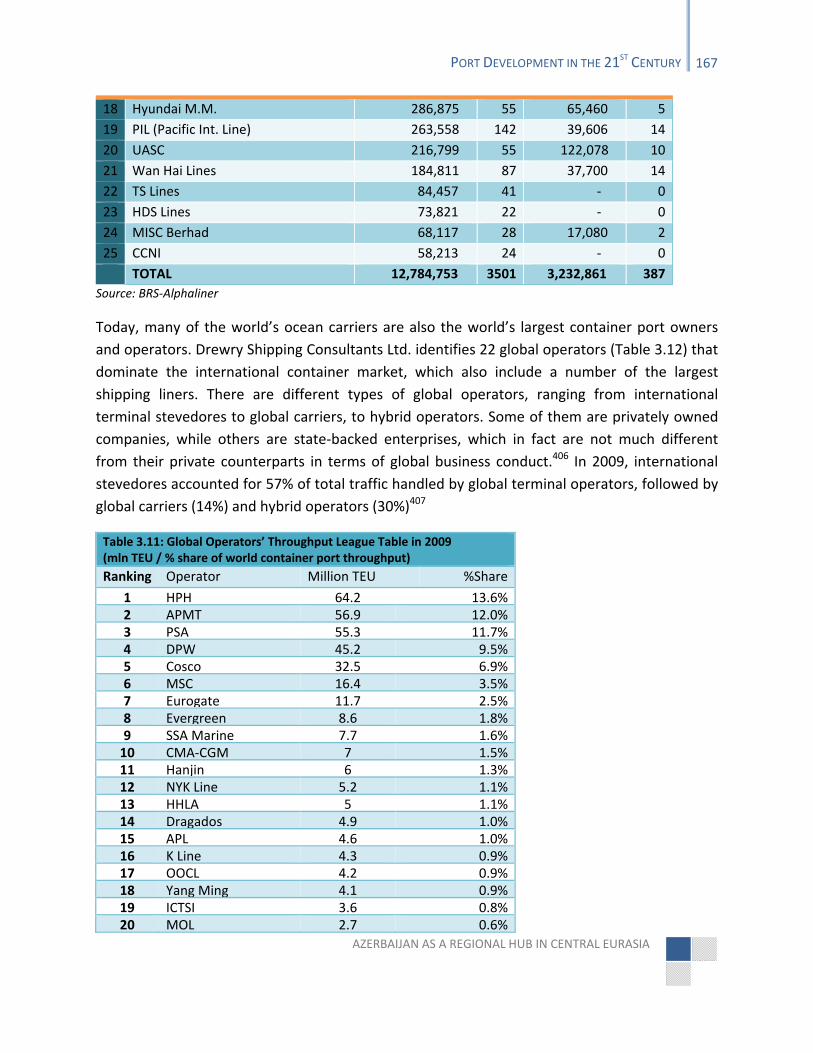

Global Operators and Global Shipping Lines ..................................................................................................... 165

The New Baku International Sea and Trade Port at Alyat ................................................................................ 169

The Alyat Port and Hinterland Development .................................................................................................... 172

PART IV: A PATH TO SUCCESS .......................................................................................................................... 177

VISION FOR AZERBAIJAN: A BIRD’S EYE VIEW .................................................................................................................. 179

Overview ........................................................................................................................................................... 179

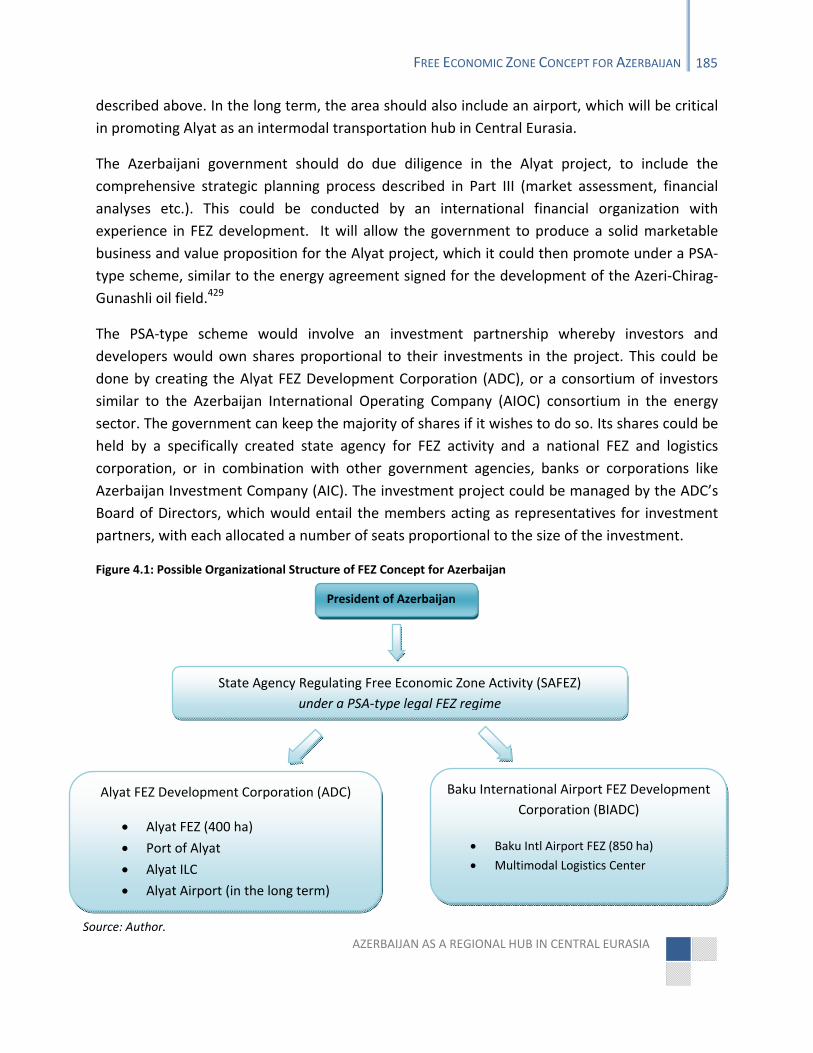

FREE ECONOMIC ZONE CONCEPT FOR AZERBAIJAN ........................................................................................................... 183

PSA‐type Legal Regime and FEZ Development .................................................................................................. 183

A Marketable Product/Project .......................................................................................................................... 184

AZERBAIJAN AS A REGIONAL HUB IN CENTRAL EURASIA

TABLE OF CONTENTS vii

The Jewel of the Caspian: The Alyat Project ................................................................................................................... 184 Eurasian Aviation & Logistics Hub: Baku International Airport FEZ ................................................................................ 186

Stability and Political Support ........................................................................................................................... 187

A FINAL WORD .......................................................................................................................................................... 187

ABOUT THE AUTHOR ....................................................................................................................................... 189

APPENDICES .................................................................................................................................................... 191

APPENDIX A: MAP OF AZERBAIJAN ............................................................................................................ 191

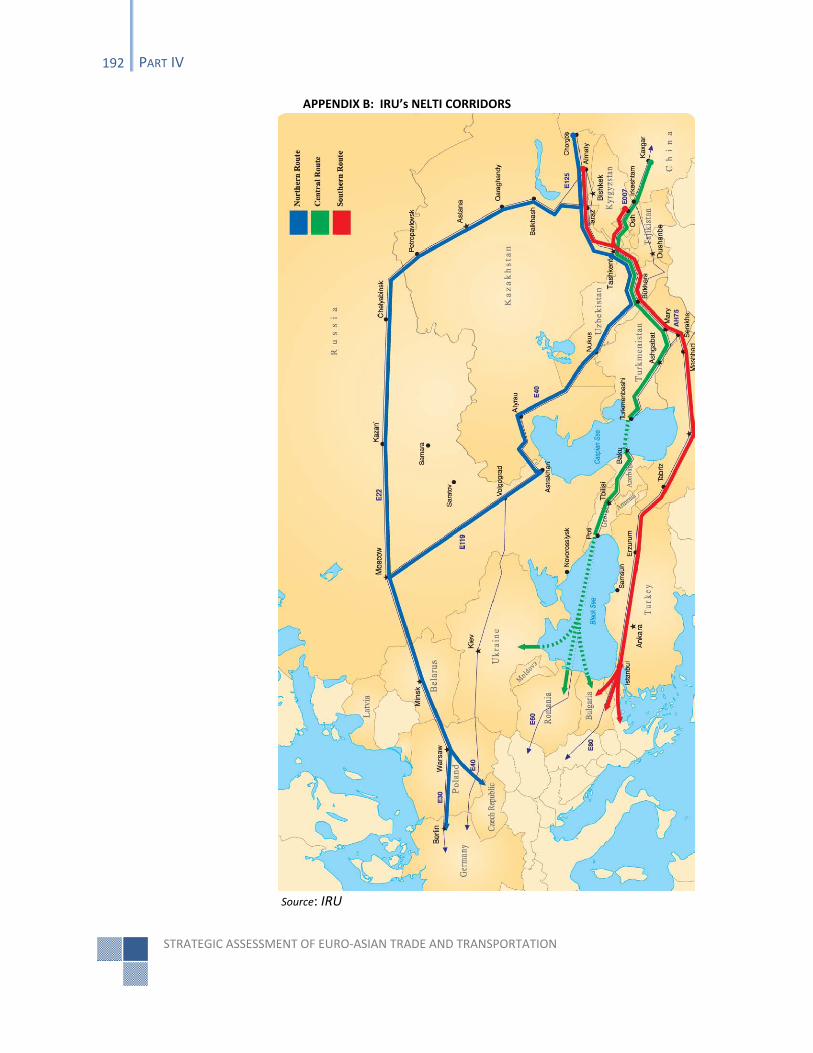

APPENDIX B: IRU’S NELTI CORRIDORS ........................................................................................................ 192

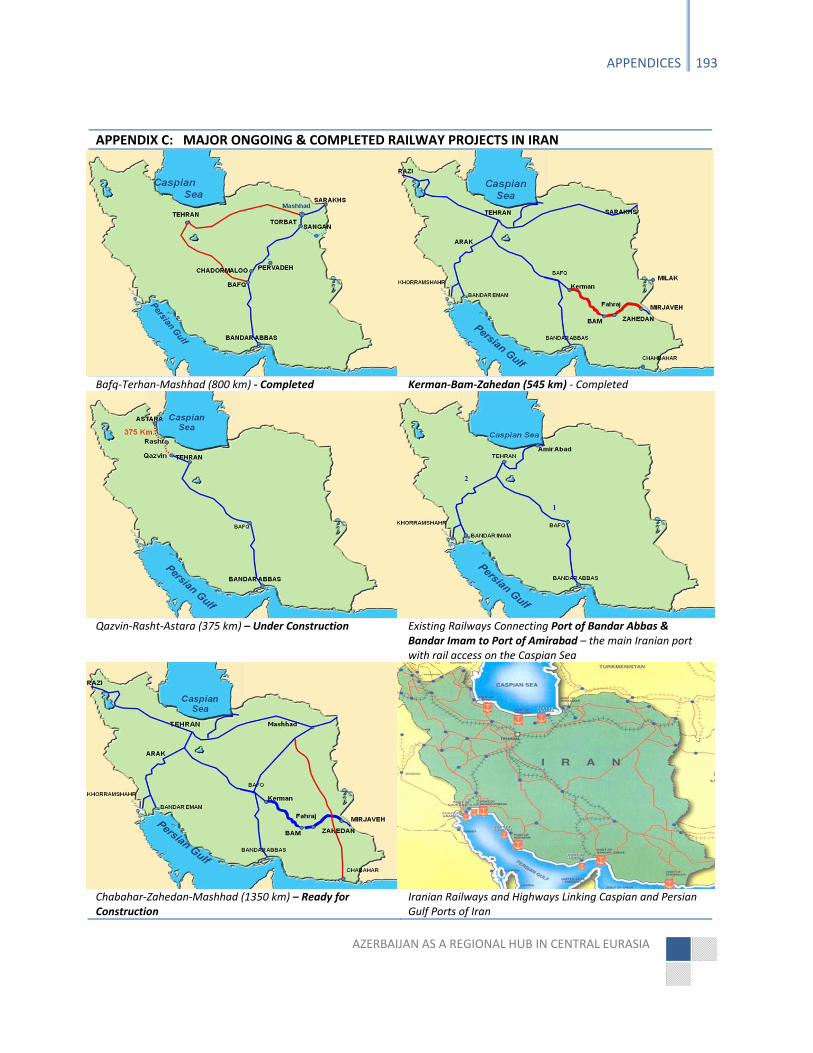

APPENDIX C: MAJOR ONGOING & COMPLETED RAILWAY PROJECTS IN IRAN .......................................... 193

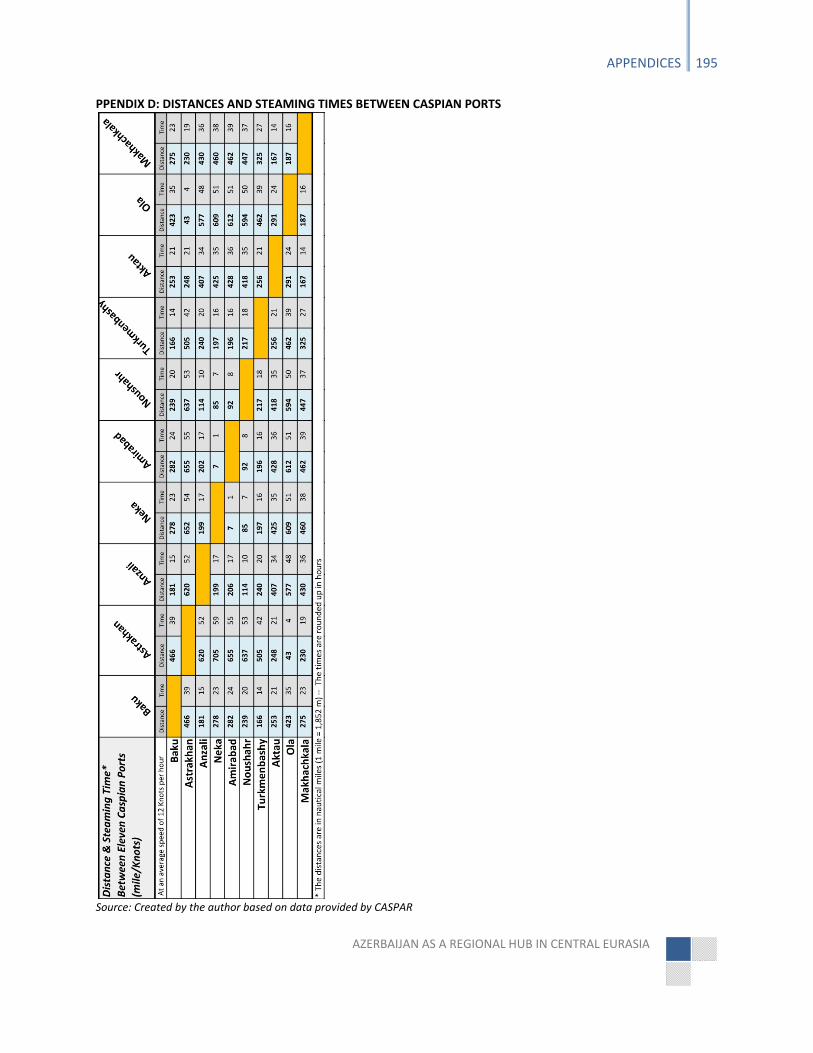

APPENDIX D: DISTANCES AND STEAMING TIMES BETWEEN CASPIAN PORTS ............................................ 195

NOTES............................................................................................................................................................. 197

STRATEGIC ASSESSMENT OF EURO‐ASIAN TRADE AND TRANSPORTATION

viii TABLE OF CONTENTS

AZERBAIJAN AS A REGIONAL HUB IN CENTRAL EURASIA

PREFACE

The present study is the result of a year‐long research project commissioned by the Azerbaijan

Diplomatic Academy as part of its “Azerbaijan 2025” series. The official start date of the

research is May 2010, though my personal interest in the subject goes back to 2006, when I first

authored a chapter on Azerbaijan’s transport sector for The New Silk Roads: Transport and

Trade in Greater Central Asia (published by the Central Asia‐Caucasus Institute at the Johns

Hopkins University in 2007). The initial goal of this study was to assess current and potential

Euro‐Asian trade and transportation links and answer one simple question: What are

Azerbaijan’s chances of becoming a transportation hub in Eurasia?

The aim was to do an in‐depth investigation of Euro‐Asian commerce and to produce an

independent and comprehensive work on how, if at all, Azerbaijan could be developed into a

transportation hub in Eurasia. Soon, as I got deeper into the research, I became convinced that

the issue of transportation cannot be studied in isolation from Azerbaijan’s overall

development strategy, in general, or from its non‐oil economy in particular. For this reason the

study you are about to read is no longer merely an assessment of the transportation sector per

se, but a comprehensive blueprint for Azerbaijan’s grand hub vision that goes beyond the issue

of transportation. This vision requires an integrated ‘bird’s eye approach’ in developing the

non‐oil economy in a way that mobilizes all of the country’s resources and projects towards

achieving one goal: Building Azerbaijan of 2030.

Once a vibrant route for the Silk Road trade, Central Eurasia is poised to regain its historical role

as a commercial bridge between east and west, north and south. Azerbaijan has the

ingredients to become one of the major commercial and transportation hubs in the region and

to be the country that facilitates regional transformation. Its location, abundance of natural

resources and dynamic new generation will help realize this vision. But for this vision to unfold,

one must have a clear understanding of the vision itself and how to achieve it. The present

study will offer one of many views about what this vision of the future might be and how it

could be successfully implemented. The ideas sketched out here are by no means set rules and

should not be viewed as fixed propositions. It is rather a logical framework analysis that has

been built upon a year‐long investigation in attempt to contribute to the understanding and

development of Azerbaijan’s hub vision.

The question of envisaging the future of Azerbaijan and the region of which it is part has been

at the heart of this study, thus, its main focus is on transportation, logistics and issues

associated with non‐oil sector development such as Free Economic Zones (FEZ). I hope that I

STRATEGIC ASSESSMENT OF EURO‐ASIAN TRADE AND TRANSPORTATION

x PREFACE

have done due diligence when drafting the hub strategy for Azerbaijan and while examining the

structure of Euro‐Asian commerce, comparing alternative Eurasian land corridors, transport

and logistics sectors and proposing the FEZ concept for the country.

Audience

The findings of the study are aimed at the decision makers in the Republic of Azerbaijan as well

as other countries of Central Eurasia. Although it focuses on a particular hub strategy for

Azerbaijan, the analyses presented here go beyond a single state and are equally relevant to

any other regional state that aspires to become a transportation hub in Eurasia. The sections of

the study that assess the Euro‐Asian trade and transportation linkages (Part I), Eurasian

corridors and the region’s land‐, air‐ and maritime‐based trade, transportation and logistics

networks (Part II) and the FEZ and port development (Part III) will be interesting for regional

specialists, transportation and logistics experts, government officials, business people, and

students of economics, area studies, and political science.

Methodology

The study has drawn on primary and secondary sources in English, Russian, Turkish, Persian and

Azerbaijani and has built its core empirical analysis on several field trips and more than 100

interviews (in person, by phone or by email) with transport and logistics experts, trade

specialists, representatives of international organizations and private sector, government

officials, academics, freight forwarders, truck drivers, port authorities, and ordinary citizens. A

considerable part of the study is dedicated to the interpretation of statistical data collected

from existing databases as well as from the interviews and surveys conducted during the

research.

Note on Statistics

Working with statistical data is challenging and doing so with the official data of regional

countries is even more so. Although little can be done to improve or guarantee the accuracy of

published official statistics, I have nonetheless tried to crosscheck official data with statistics

collected by myself from other government agencies, private institutions, or interviewees.

There are some discrepancies that I have addressed by adding explanatory footnotes. It is

important also to be aware that fiscal years of some countries differ. For example, the trade

statistics on EU‐India may appear to differ depending on the source of the data. While most

statistics cover the period from January 1 to December 31 of the year, the Indian financial

calendar (like the Iranian financial calendar) runs from April to March. Therefore, if trade data is

provided by the Indian government and indicated as “2008‐2009”, it implies the period from 1

AZERBAIJAN AS A REGIONAL HUB IN CENTRAL EURASIA

PREFACE xi

April 2008 till 31 March 2009. These differences have been noted at various points to minimize

the risk of confusion.

Definitions and Terminology

A few terms and definitions need clarification. Additional terms can be found in the Glossary.

Central Eurasia: Although the term “Central Eurasia” has a number of different definitions, in

this study it refers to eight Eurasian countries, namely the three South Caucasus states of

Armenia, Azerbaijan, and Georgia and the five Central Asian states of Kazakhstan, Kyrgyzstan,

Tajikistan, Turkmenistan, and Uzbekistan.

Hub: A hub here means simply a center or focal point of activity.

Hub Vision or Hub Strategy: Terms such as “grand hub strategy” or “future hub vision” are used

interchangeably to mean the strategy of developing the country as a major trade,

transportation and logistics center in the region. Such a strategy encompasses and includes

other sector‐specific hub strategies such as transportation, aviation or logistics. When referring

to a particular hub strategy, a specific limiting term will be used (e.g. transportation hub

strategy).

Relay Hub: The term “relay hub” is used to describe a place that acts as a transiting point for

cargo or passenger shipments.

Hub and Spoke: The term “hub and spoke” refers to an area that acts as a major distribution

center for freight or passenger traffic. Such centers operate as regional focal points for many

businesses and airline carriers. Services offered at the ‘hub and spoke’ center go beyond transit

shipments and could involve re‐distribution, consolidation, labeling, packaging and so on.

Intermodal or Multimodal Transportation: Transportation that involves more than one mode of

transport such as air, rail, sea and road.

Currency Signs

Several currency signs are used throughout the study. All “$” signs refer to US Dollars, while “€”

is for Euro. The national currency of Azerbaijan is “Azerbaijani manat” indicated as “AZN” (1

AZN = $1.25 or €0.87).

Taleh Ziyadov Cambridge, UK May 31, 2011

STRATEGIC ASSESSMENT OF EURO‐ASIAN TRADE AND TRANSPORTATION

AZERBAIJAN AS A REGIONAL HUB IN CENTRAL EURASIA

ACKNOWLEDGEMENTS

It was at the Azerbaijan Diplomatic Academy (ADA), an institution that is very close to my heart,

that the idea of this research was first conceived a few years ago. I am grateful for the support

and assistance I have received from the ADA while conducting this research. This study would

have been incomplete if not for the crucial interventions at different stages by the ADA Rector,

Ambassador Hafiz Pashayev. He acted as a facilitator, motivator, and mentor, never turning

down my frequent requests for help with setting up meetings or getting much‐needed

statistical data or interviewing important state officials. Moreover, Ambassador Pashayev was

the person who convinced me to undertake this important research when I hesitated. I

therefore thank him for his foresight and kind attention throughout the making of this study. I

am also grateful for the encouragement and support of other colleagues at the ADA, including

Galib Mammad, Fariz Ismailzade, Murad Ismayilov, and Turgut Mustafayev, and of ADA faculty,

including Elkin Nurmammadov, Elnur Soltanov, Kavus Abushov and Anar Valiyev.

Special thanks go to a regional guru, Professor Frederick Starr at the Johns Hopkins University,

who has acted as an academic advisor for this research. I have benefited greatly from his

constructive comments and interesting observations. In addition, a number of background case

studies have contributed to the conceptual framework of this work. I am especially grateful to

James Graham for his analysis on Europe‐China freight activity and for his comments and

reviews, and to Erdal Erkut, who investigated the opportunities for Azerbaijan in the logistics

sector and has commented on the logistics section of the study. I would like to express my

gratitude to Professor Gulshan Sachdeva at Jawaharlal Nehru University (India) for sharing his

work on EU‐South East Asia trade linkages and for assisting with finding statistics on EU‐India

trade. A number of people have reviewed parts of the study and have shared their opinions. In

particular, I am grateful to Pablo Ruiz Del Real, Michel Gueriot, Jan Tomczyk, Emin Huseynov,

Nijat Valiyev, Hadji Huseynov and Jamil Manizade for their comments and suggestions.

I would also like to acknowledge a number of individuals, institutions, and agencies that have

made this study possible. Several public agencies and private sector representatives in

Azerbaijan have provided valuable assistance during the research. I would like to mention Akif

Mustafayev, Azerbaijan’s National Secretary at the European Commission’s TRACECA program,

Elman Aliyev and Rafael Mirgulamov at the Port of Baku, Ilham Mammadov at CASPAR, Jamil

Manizade at AZAL, Ilgar Alekperov and Vugar Zeynalov at Baku Cargo Terminal; and Anar

Rzayev at Van der Wal Company – Azerbaijan. Despite their busy schedule, they have always

found time to discuss my questions and have been encouraging throughout the process. Thanks

STRATEGIC ASSESSMENT OF EURO‐ASIAN TRADE AND TRANSPORTATION

xiv ACKNOWLEDGMENTS

also go to Musa Panahov, Sadraddin Mamadov, Ravil Iskenderov, and Qafqaz Adigozelov (MoT);

Aqil Usubov (State Customs Committee); Niyazi Safarov and Fakhri Hasanov (MED); Elnur

Aslanov (Office of President); Ayaz Bayramov and Aysel Askerova (MCIT); Vahid Aliyev (Port of

Baku); Yusif Yusifov and Anar Orujov (State Statistical Committee); Mikayil Jabbarov and Samir

Nuriyev (Administration of State Historical‐Architectural Reserve Icherisheher); Nazim

Mammadov (CASPAR); Teymur Mammadov and Ilgar Mustafayev (ADY); Bulent Karani and

Ismet Kale (Azerinshaat); Nurid Aliyev and Movsum Muslum‐zada (Caspian Logistics); David H.

Watkins and Amin Melikzadeh (Royal Haskoning); Akif Babayev and Javanshir Askerov (A‐

Logistics), and Nigar Resulova (AZPROMO).

I have benefited greatly from the views of international experts and specialists in the field who

have contributed to my learning and knowledge. I would like to thank Gohkan Akinci at

International Finance Corporation (IFC) for his valuable insight about the FEZ development. A

word of thanks also goes to members and participants of UNECE and OSCE Inter‐Regional

Workshops on developing Euro‐Asian Transport Links (EATL), including Michalis Adamantiadis,

Robert Nowak, Jan Tomczyk, Azer Tagiyev, Anthony Pearce, Gabriel Leonte, Stig Nerdal, Erik

Evtimov, Professor Dimitrios A. Tsamboulas, Panayota Moraiti, Constantinos Alexopoulos,

Mohammad Mirzaei Kahagh, Tahir Aliyev and Abdusamad Muminov (Uzbekistan), Yazgeldi

Nazarov and Davut Pomanov (Turkmenistan), Alexey Alekseev (Russia), Murat Bekmagambetov

(TRACECA‐Kazakhstan), Abdulhakim Tohirov (Tajikistan), Marc Abeille, and Helmut Meelich.

In addition, I want to express my appreciation to Professor Mehmet Tanyaş, Jawad Kamel,

Fereydun Kousedghi, Hamed Kazemzadeh, Mehdi Hoseini Taghi Abad, Khalil Karimi, Abbas

Maleki, Brenda Shaffer, Nariman Mamedov, John Wensveen, Muzaffar Behlulov, Valerian

Akhalaia, Fariz Rzayev, George Katcharava, David Abesadze, Irakly Chkhenkely, Mamuka

Tsereteli, Udo Witulski, Yves Goulin, Marcel Sames, Radoslaw Wegrzyn, Christos Kostopoulos,

Svante Cornell, Solmaz Rustamova‐Tohidi, Goshqar Goshqarli, Azer Mursagulov, Afgan Isayev,

Fahrettin Yagci, Thomas Farole, Stephan Baertges, Nurzhan Zhambekov, Khayal Rahbarli, Ali

Gara, Said Ismayil, Ismayil Hasanov, Abbas Hummatov, Olga Smirnova, Olga Frolova, Vadim

Fedoseev, David Owens, Tolkyn Yerkinkyzy, Sally Marshak, Bayram Atayev, Jeyhun Mammadov

and Farid Ahmadov.

Finally, I am grateful to Celia Davies for her meticulous editing of the entire manuscript, which

has improved it greatly. Also thanks to Vincent Ercolano and James Graham for their editing

contributions to parts of this study. I claim responsibility for any oversights and shortcomings.

AZERBAIJAN AS A REGIONAL HUB IN CENTRAL EURASIA

FOREWORD

AZERBAIJAN AS A REGIONAL HUB IN CENTRAL EURASIA

EXECUTIVE SUMMARY

AZERBAIJAN AS A REGIONAL HUB IN CENTRAL EURASIA

ABBREVIATIONS

ABADA – Azerbaijan International Road Carriers Association ADA – Azerbaijan Diplomatic Academy ADB – Asian Development Bank ADC – Alyat FEZ Development Corporation ADDY – Azerbaijan State Railways Company (predecessor of ADY) ADIF – Administrator of Spanish Railway Infrastructures ADY – Azerbaijan Railways JSC AIC – Azerbaijan Investment Company AIOC – Azerbaijan International Operating Company ALG – Advanced Logistics Group AMTRAK – The US National Railroad Passenger Corporation ASK – Available Seat‐Kilometers ASEAN – Association of Southeast Asian Nations ATI – Air Transport Intelligence AZAL – Azerbaijan National Airlines AZN – Azerbaijani manat (currency code) AZPROMO – Azerbaijani Export & Investment Promotion Foundation BAH – Booz Allen Hamilton BAM – Baikal‐Amur Mainline BCT – Baku Cargo Terminal BIADC – Baku International Airport FEZ Development Corporation BISP – Baku International Sea Port BOO – Build‐Own‐Operate BOOT – Build‐Own‐Operate and Transfer BOT – Build‐Operate‐Transfer bpd – Barrels per day BRIC – Brazil, Russia, India and China BTC – Baku‐Tbilisi‐Ceyhan pipeline BTK – Baku‐Tbilisi‐Kars railway project CACI – Central Asia‐Caucasus Institute (CACI) at Johns Hopkins University CAREC – Central Asia Regional Economic Cooperation CASPAR – The Azerbaijan State Caspian Sea Shipping company CCTT – Coordinating Council on Transsiberian Transportation CFS – Container Freight Stuffing CIS – Commonwealth of Independent States CIM – Uniform Rules concerning the Contract of International Carriage of Goods by Rail CIT – International Rail Transport Committee CJSC – Closed Joint Stock Company CPC – Caspian Pipeline Consortium

STRATEGIC ASSESSMENT OF EURO‐ASIAN TRADE AND TRANSPORTATION

xviii ABBREVIATIONS

CPMM – CAREC Corridors Performance Measurement and Monitoring CRCT – China Railway Container Transport Corporation CRIMT – China Railway International Multimodal Transport CROS – Caspian Sea Republics’ Oil Swap Project DB – Deutsche Bahn DWT – Deadweight Tonnage EATL – Euro‐Asian Transport Links (UNECE) EBRD – European Bank for Reconstruction and Development EC – European Commission ECO – Economic Cooperation Organization EMS – Environmental Management System EPZ – Export Processing Zones EU – European Union EurAsEC – Eurasian Economic Community FCL – full container load FDI – Foreign Direct Investment FEZ – Free Economic Zone ft – feet FTK – Freight Ton‐Kilometers FTZ – Free Trade Zones GDP – Gross domestic product GPS – Global Positioning System GSP+ – Generalized System of Preferences plus GYD – Heydar Aliyev International Airport, Baku ha – hectare HPH – Hutchison Port Holdings IATA – International Air Transport Association IBRD – The International Bank for Reconstruction and Development ICD – inland container depot ICT – information and communications technology IGC – Intergovernmental Commission ILC – International Logistics Center IsDB – Islamic Development Bank IRU – International Road Transport Union ISO – International Organization for Standardization IT – Information Technology JSC – Joint Stock Company JV – Joint Venture km – Kilometer km/h – Kilometers per hour KMS – Kaveh Marine and Services of Islamic Republic of Iran KTS – Kaztransservice KTZ – Kazakhstan Temir Zholy (Kazakhstan Railways)

AZERBAIJAN AS A REGIONAL HUB IN CENTRAL EURASIA

ABBREVIATIONS xix

kV – Kilovolt LCL – less than container load LLC – Limited Liability Company LNG – Liquefied Natural Gas LP – Logistic Park LPI – Logistics Performance Index MCIT – Ministry of Communications and Information Technologies MED – Ministry of Economic Development mln – Million MoT – Ministry of Transport MoU – Memorandum of Understanding NATO – The North Atlantic Treaty Organization NAR – Nakhichevan Autonomous Republic of Azerbaijan NELTI – New Eurasian Land Transport Initiative NIOC – National Iranian Oil Company NSTC – The North‐South Transport Corridor OAG – Official Airline Guide OECD – Organization for Economic Co‐operation and Development OILCECA – Oil Corridor Europe, Caucasus, Asia OJSC – Open Joint Stock Company OSCE – Organization for Security and Co‐operation in Europe OSJD – Organization for Cooperation Railways PMO – Ports and Maritime Organization of Islamic Republic of Iran PPP – public‐private partnership PRD – Lao People's Democratic Republic PSA – Port of Singapore Authority PSA – Production Sharing Agreement RAI – Iranian Railways RENFE – Spanish National Railway Network RIZ – Regional Innovation Zone RO‐RO – Roll‐on Roll‐off RoPax – Roll On, Roll Off Passenger RPK – Revenue Passenger‐Kilometers RTK – Revenue Ton‐Kilometers RZD – Russian Railways SES – Single European Sky SEZ – Special Economic Zone SMGS – Agreement on International Freight Traffic by Rail SPM – Single Point Mooring SOCAR – State Owned Company of Azerbaijan Republic TAR – Trans‐Asian Railway (UNESCAP) TEE – Trans‐Eurasian Express TEL – Trans Eurasia Logistics

STRATEGIC ASSESSMENT OF EURO‐ASIAN TRADE AND TRANSPORTATION

xx ABBREVIATIONS

TEM – Trans‐European Motorways (UNECE) TEN – Trans‐European Transport Networks TER – Trans‐European Railway (UNECE) TEU – Twenty‐foot equivalent unit TIKA – Turkish International Cooperation & Development Agency TIR – Convention on International Transport of Goods Under Cover of TIR Carnets TKTR – Trans‐Kazakhstan Trunk Railway TSR – The Trans‐Siberian Railway TRACECA – Transport Corridor Europe, Caucasus, Asia UIC – The International Union of Railways UN – United Nations UNCTAD – United Nations Conference on Trade and Development UNECE – United Nations Economic Commission for Europe UNESCAP – United Nations Economic and Social Commission for Asia and the Pacific US – United States WTO – World Trade Organization XUAR – Xinjiang Uygur Autonomous Region of the People's Republic of China

AZERBAIJAN AS A REGIONAL HUB IN CENTRAL EURASIA

FIGURES & MAPS

FIGURE 1.1: EU EXTERNAL TRADE: TOP 10 EU TRADING PARTNERS PLUS ASEAN COUNTRIES IN 2010 (IN %) .................................. 10

FIGURE 1.2: REGIONAL SHARES IN WORLD MERCHANDISE EXPORTS (2000 AND 2008) (IN %) ...................................................... 11

FIGURE 1.3: SHARE OF NATIONAL EXPORTS IN WORLD EXPORTS (IN %)...................................................................................... 11

FIGURE 1.4: SHARE OF NATIONAL IMPORTS IN WORLD IMPORTS (IN %) ..................................................................................... 11

FIGURE 1.5: SHARE OF EXPORTS TO CHINA BY EU27 COUNTRIES IN 2010 .................................................................................. 12

FIGURE 1.6: SHARE OF IMPORTS FROM CHINA TO EU27 COUNTRIES IN 2010 .............................................................................. 12

FIGURE 1.7: DISTRIBUTION OF THE EU‐ASEAN TRADE VOLUME BY COUNTRIES IN 2010 (TONS IN %) .............................................. 14

FIGURE 1.8: DISTRIBUTION OF THE EU‐ASEAN TRADE TURNOVER BY COUNTRIES IN 2010 (EUROS IN %) ......................................... 14

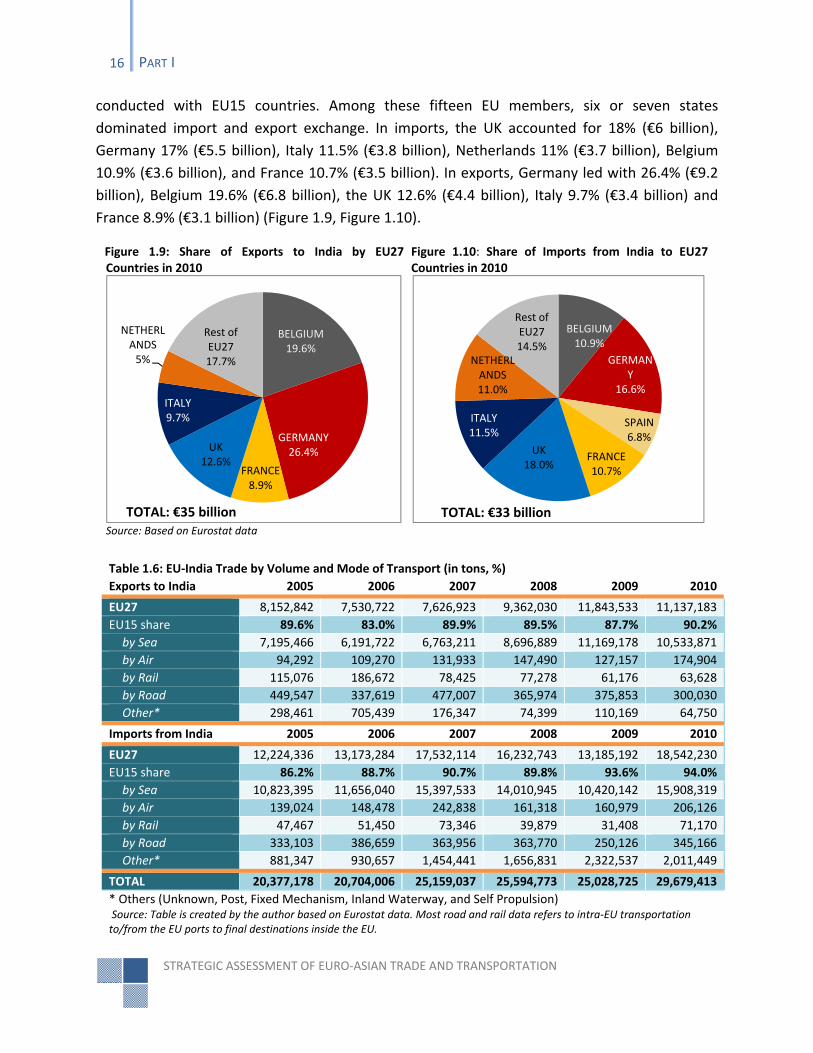

FIGURE 1.9: SHARE OF EXPORTS TO INDIA BY EU27 COUNTRIES IN 2010 ................................................................................... 16

FIGURE 1.10: SHARE OF IMPORTS FROM INDIA TO EU27 COUNTRIES IN 2010 ............................................................................ 16

FIGURE 1.11: TOTAL GOODS PROCESSED BY EU PORTS BETWEEN 2002 AND 2009 (EU27 VS. EU15) (IN 1000 TONS) ..................... 17

FIGURE 1.12: SHARE OF ASIAN COUNTRIES IN THE EU‐ASIA CONTAINER TRADE IN 2009 (TEU IN %) .............................................. 18

FIGURE 1.13: DISTRIBUTION OF THE EU‐CHINA (EXCLUDING HONG KONG) CONTAINER TRADE BY COUNTRIES IN 2009 (TEU IN %) ...... 19

FIGURE 1.14: DISTRIBUTION OF THE EU‐INDIA CONTAINER TRADE BY COUNTRIES IN 2009 (TEU IN %) ........................................... 19

FIGURE 2.1: DISTRIBUTION OF CARGO SHIPMENTS IN AZERBAIJAN BY TRANSPORT MODE (2000‐2010) (IN %) ................................ 23

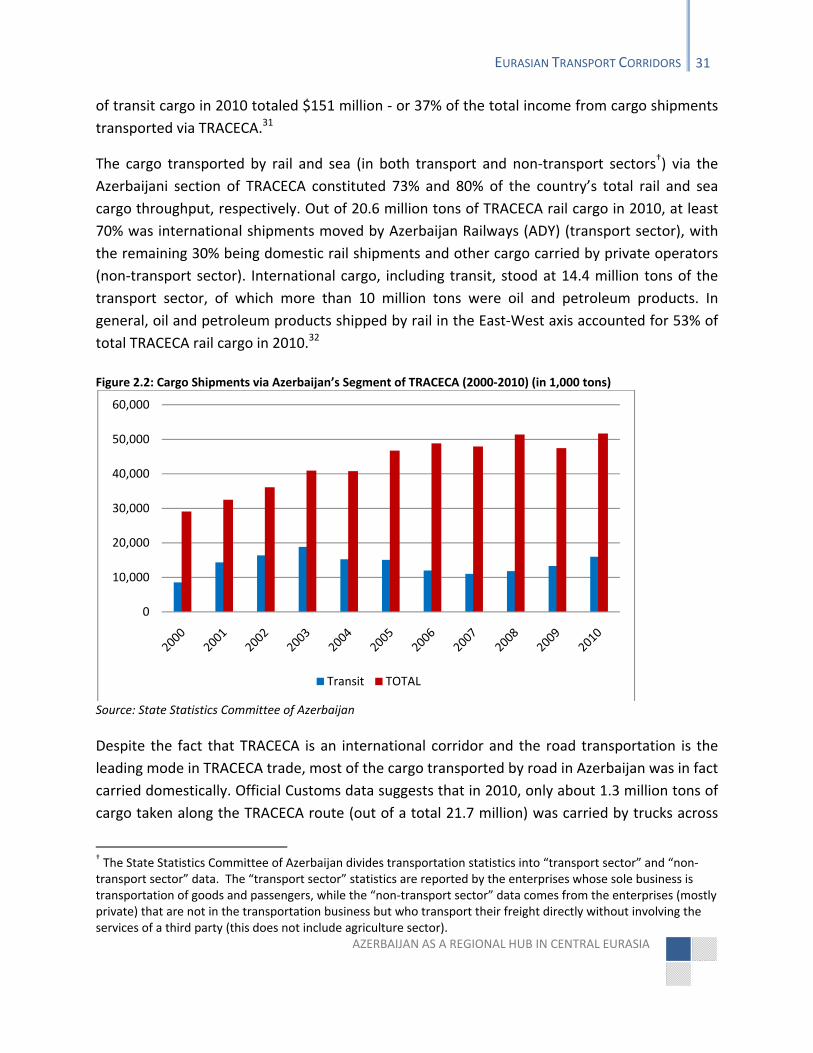

FIGURE 2.2: CARGO SHIPMENTS VIA AZERBAIJAN’S SEGMENT OF TRACECA (2000‐2010) (IN 1,000 TONS) ................................... 31

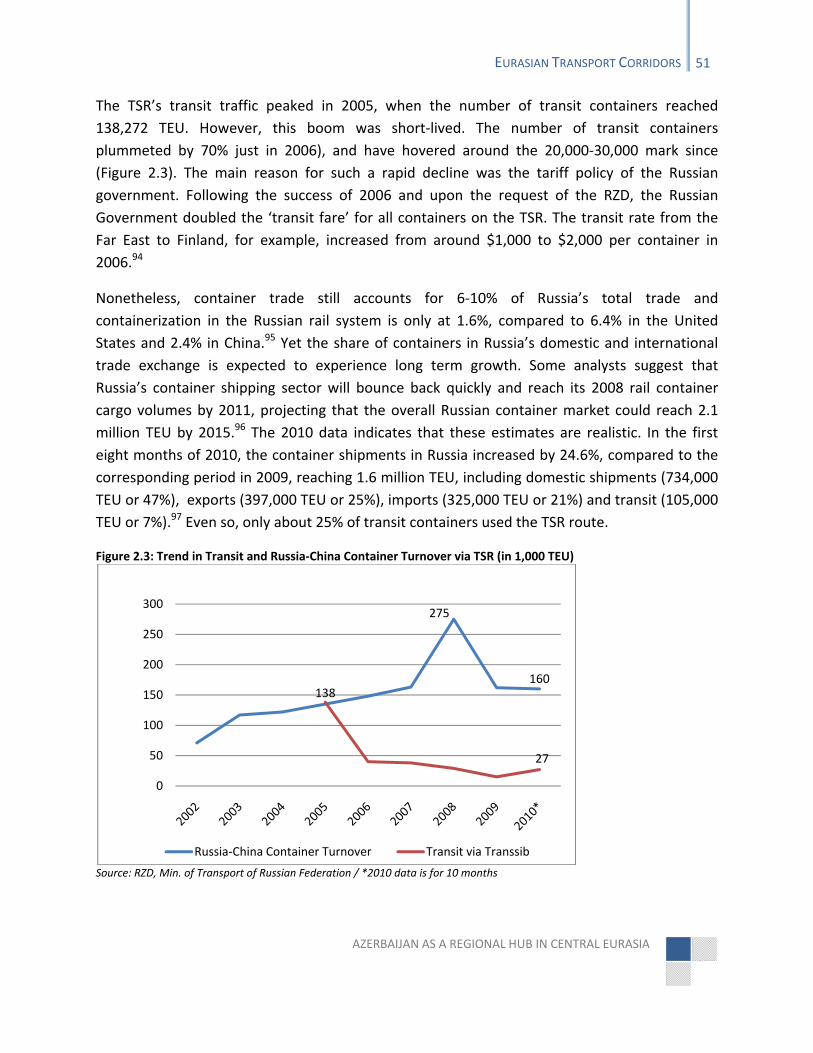

FIGURE 2.3: TREND IN TRANSIT AND RUSSIA‐CHINA CONTAINER TURNOVER VIA TSR (IN 1,000 TEU) ............................................. 51

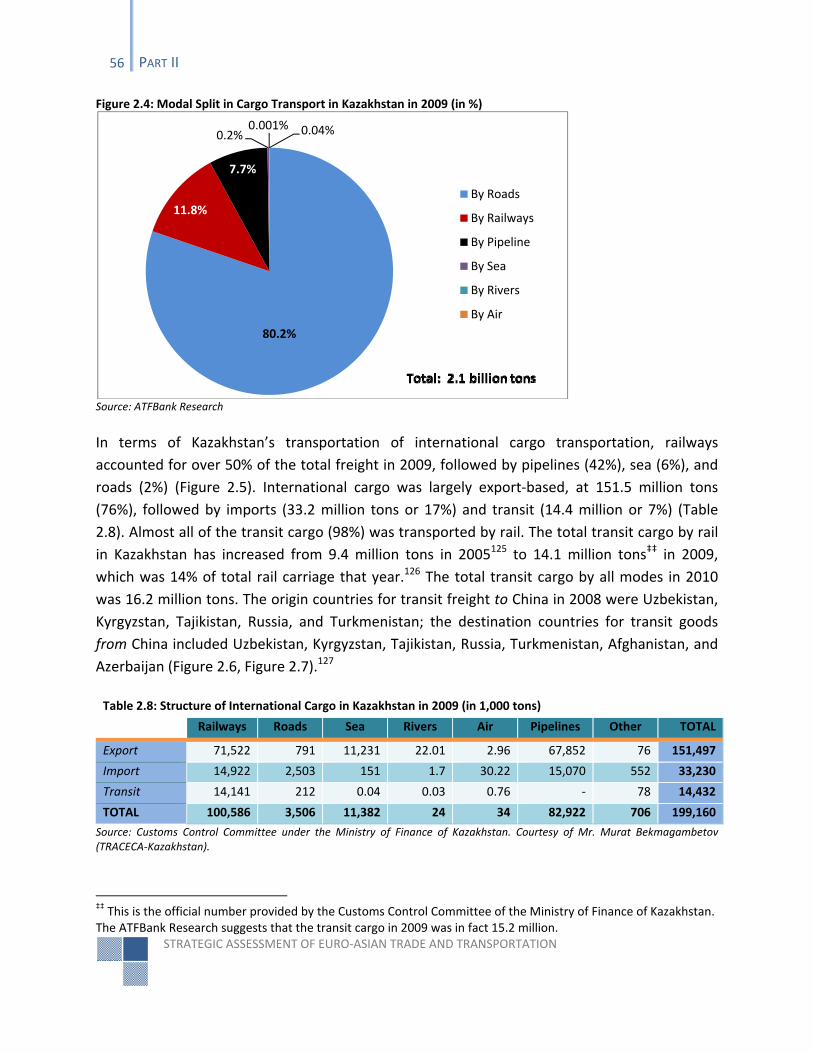

FIGURE 2.4: MODAL SPLIT IN CARGO TRANSPORT IN KAZAKHSTAN IN 2009 (IN %) ...................................................................... 56

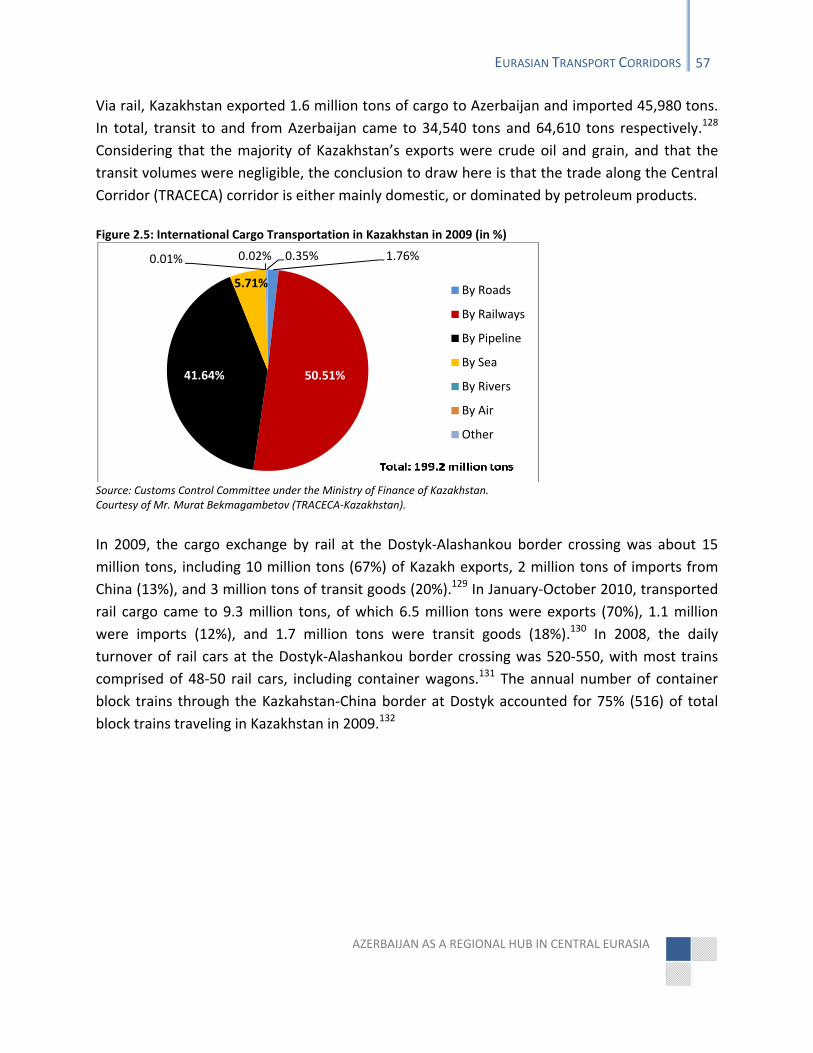

FIGURE 2.5: INTERNATIONAL CARGO TRANSPORTATION IN KAZAKHSTAN IN 2009 (IN %) ............................................................... 57

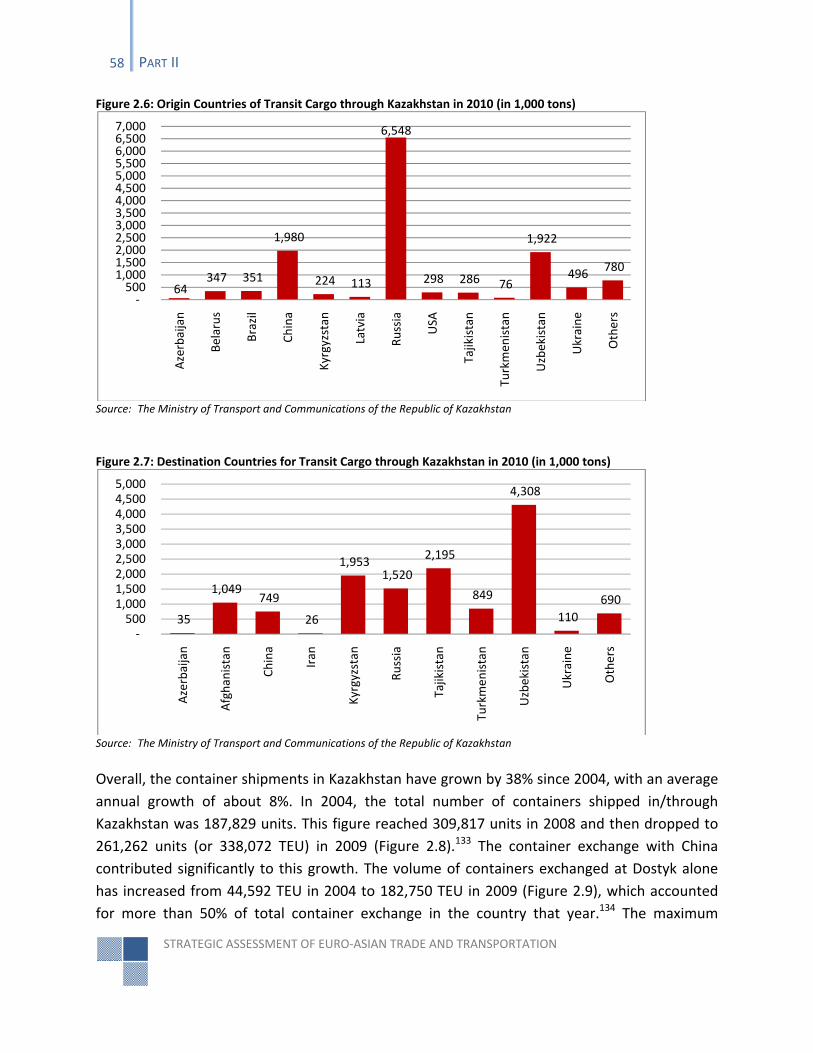

FIGURE 2.6: ORIGIN COUNTRIES OF TRANSIT CARGO THROUGH KAZAKHSTAN IN 2010 (IN 1,000 TONS) .......................................... 58

FIGURE 2.7: DESTINATION COUNTRIES FOR TRANSIT CARGO THROUGH KAZAKHSTAN IN 2010 (IN 1,000 TONS) ................................ 58

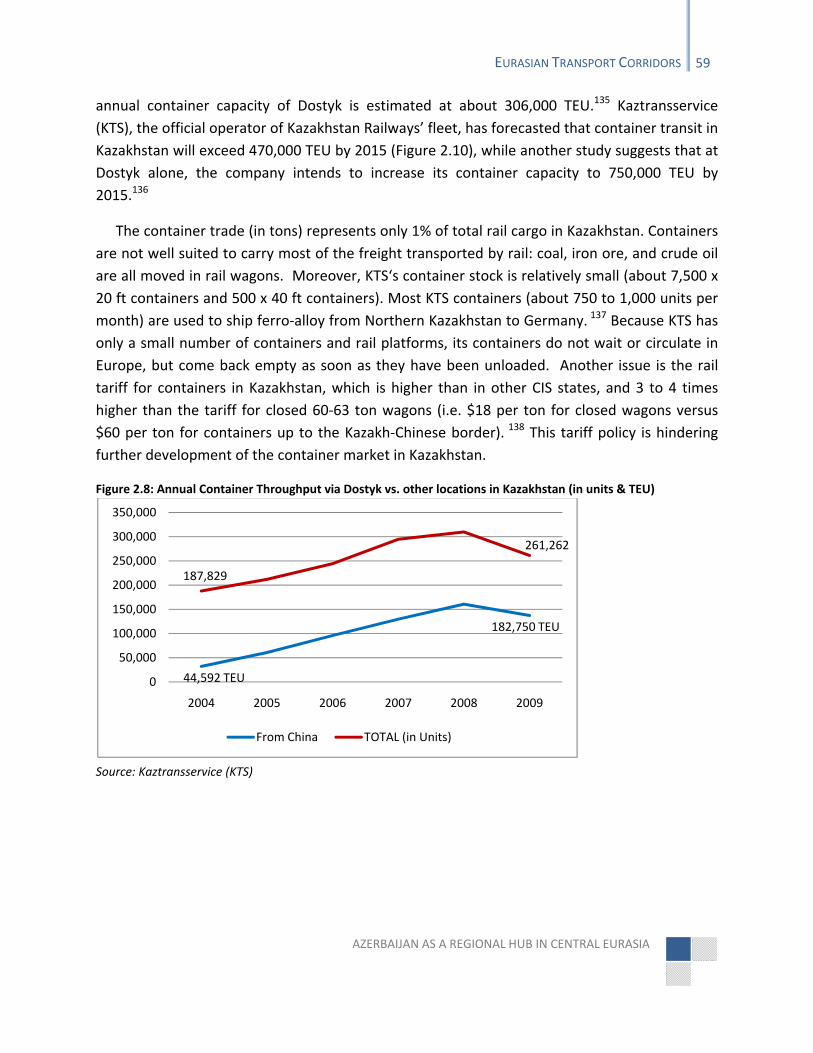

FIGURE 2.8: ANNUAL CONTAINER THROUGHPUT VIA DOSTYK VS. OTHER LOCATIONS IN KAZAKHSTAN (IN UNITS & TEU) ...................... 59

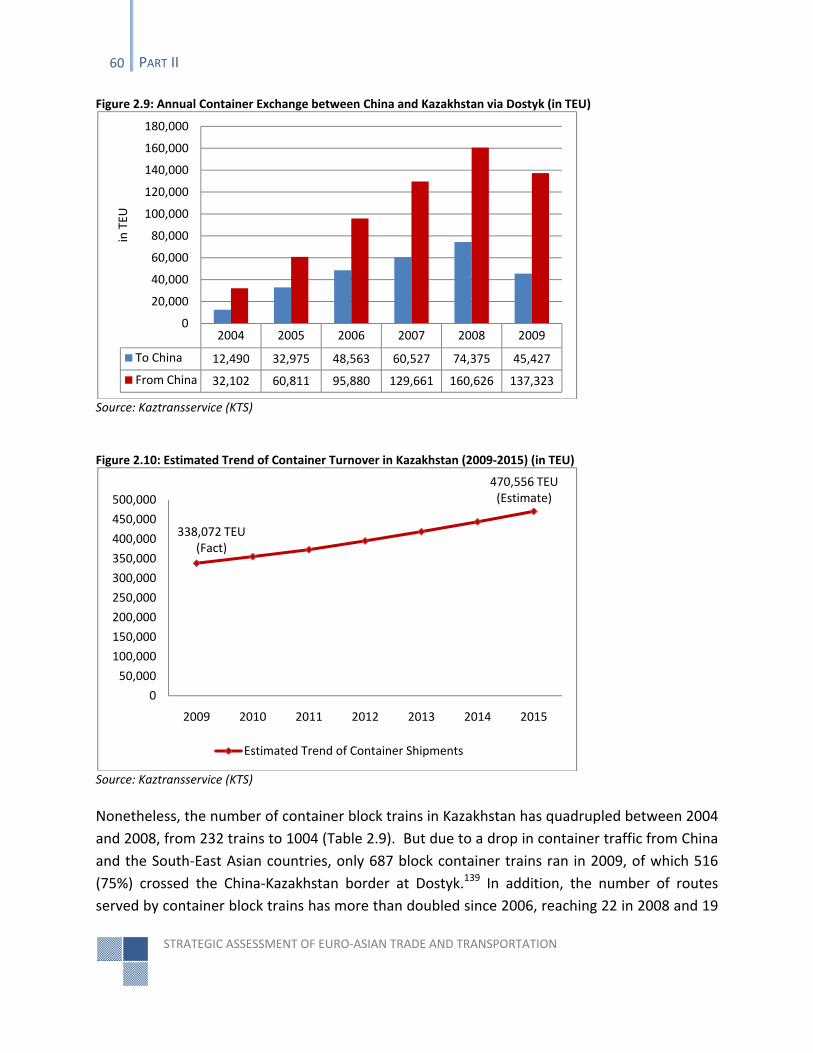

FIGURE 2.9: ANNUAL CONTAINER EXCHANGE BETWEEN CHINA AND KAZAKHSTAN VIA DOSTYK (IN TEU) .......................................... 60

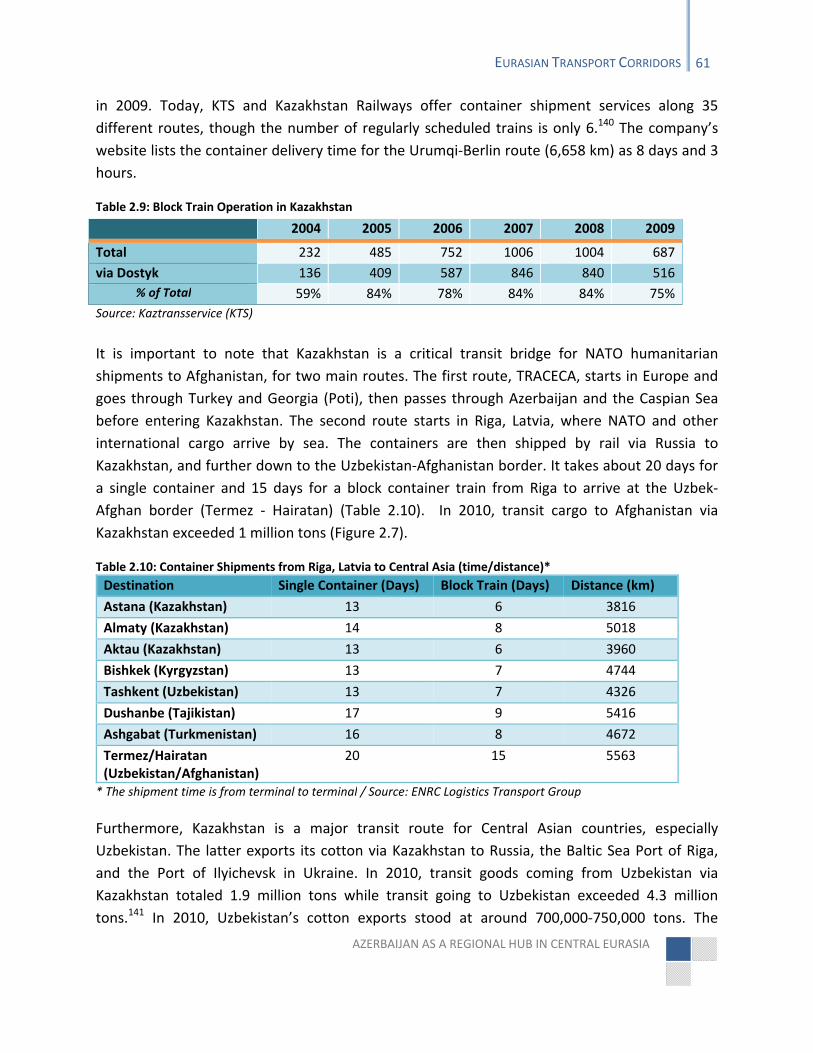

FIGURE 2.10: ESTIMATED TREND OF CONTAINER TURNOVER IN KAZAKHSTAN (2009‐2015) (IN TEU) ............................................ 60

FIGURE 2.11: AVERAGE SPEED OF THE ISLAMABAD‐TEHRAN‐ISTANBUL INAUGURAL TRAIN (AUGUST 14‐28, 2010) ........................... 70

FIGURE 2.12: CONTAINER SHIPPING COST FROM ISLAMABAD TO ISTANBUL (IN $) ........................................................................ 71

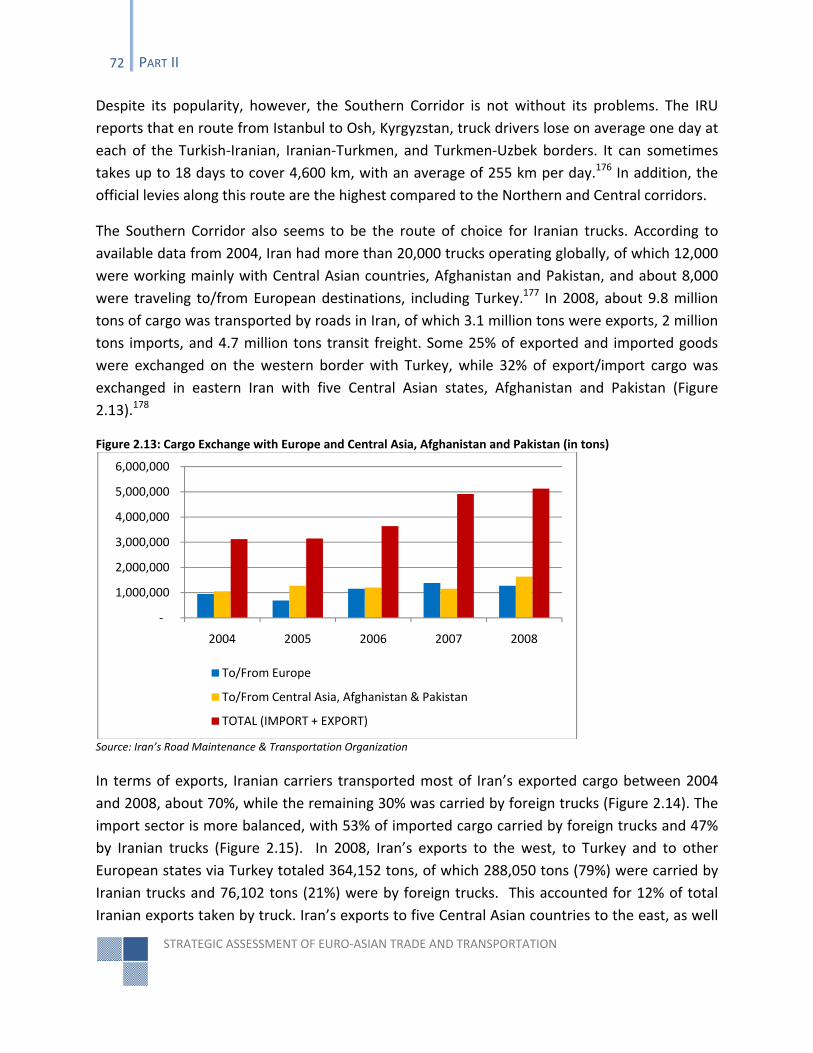

FIGURE 2.13: CARGO EXCHANGE WITH EUROPE AND CENTRAL ASIA, AFGHANISTAN AND PAKISTAN (IN TONS) ................................... 72

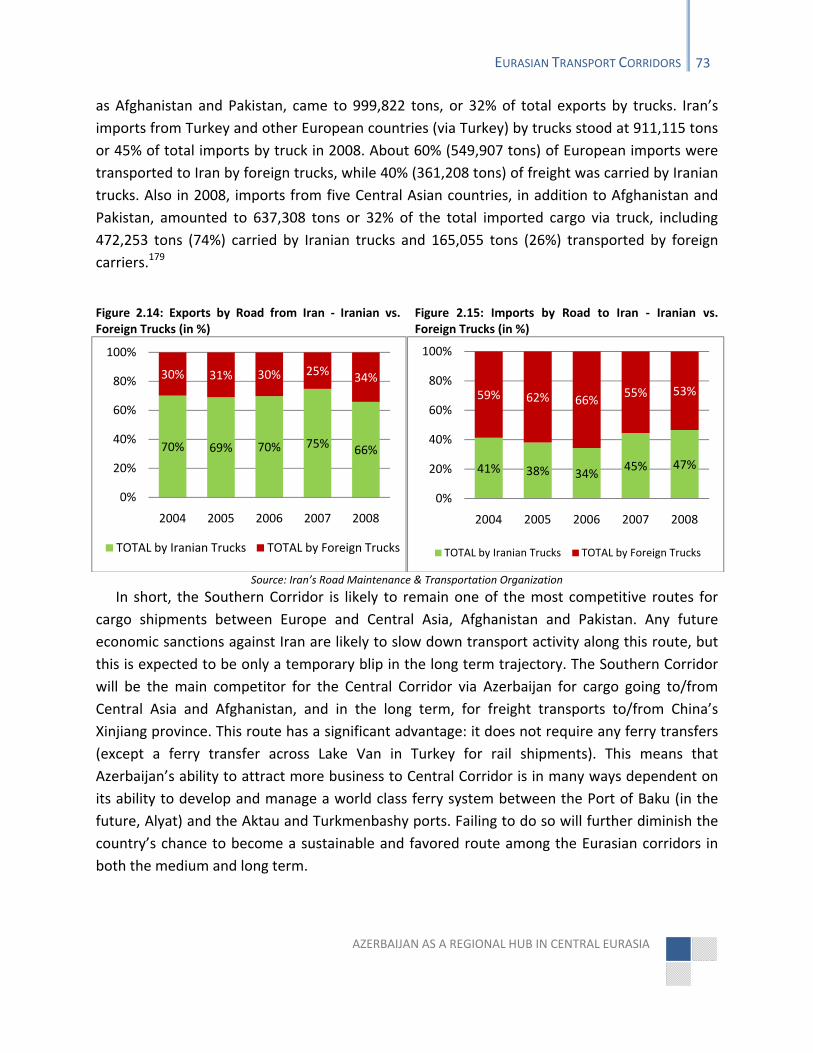

FIGURE 2.14: EXPORTS BY ROAD FROM IRAN ‐ IRANIAN VS. FOREIGN TRUCKS (IN %) .................................................................... 73

FIGURE 2.15: IMPORTS BY ROAD TO IRAN ‐ IRANIAN VS. FOREIGN TRUCKS (IN %) ........................................................................ 73

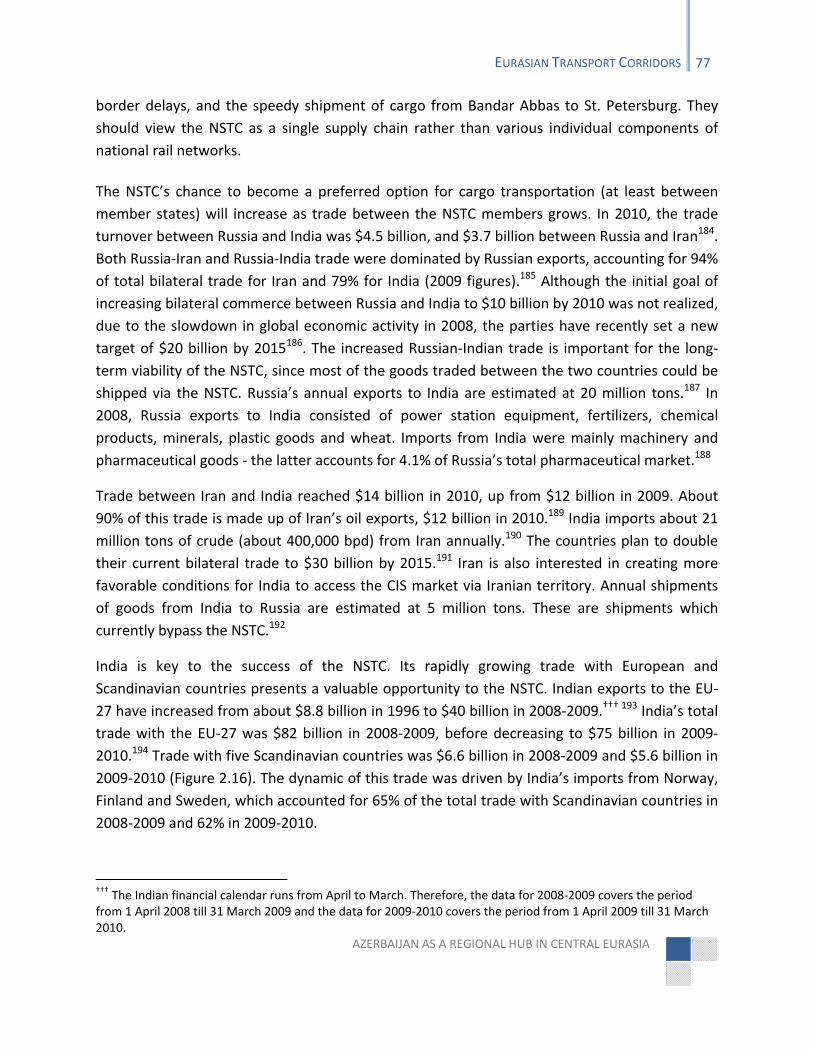

FIGURE 2.16: INDIAN TRADE WITH SCANDINAVIAN COUNTRIES (2008‐2009/2009‐2010) (IN MLN $) .......................................... 78

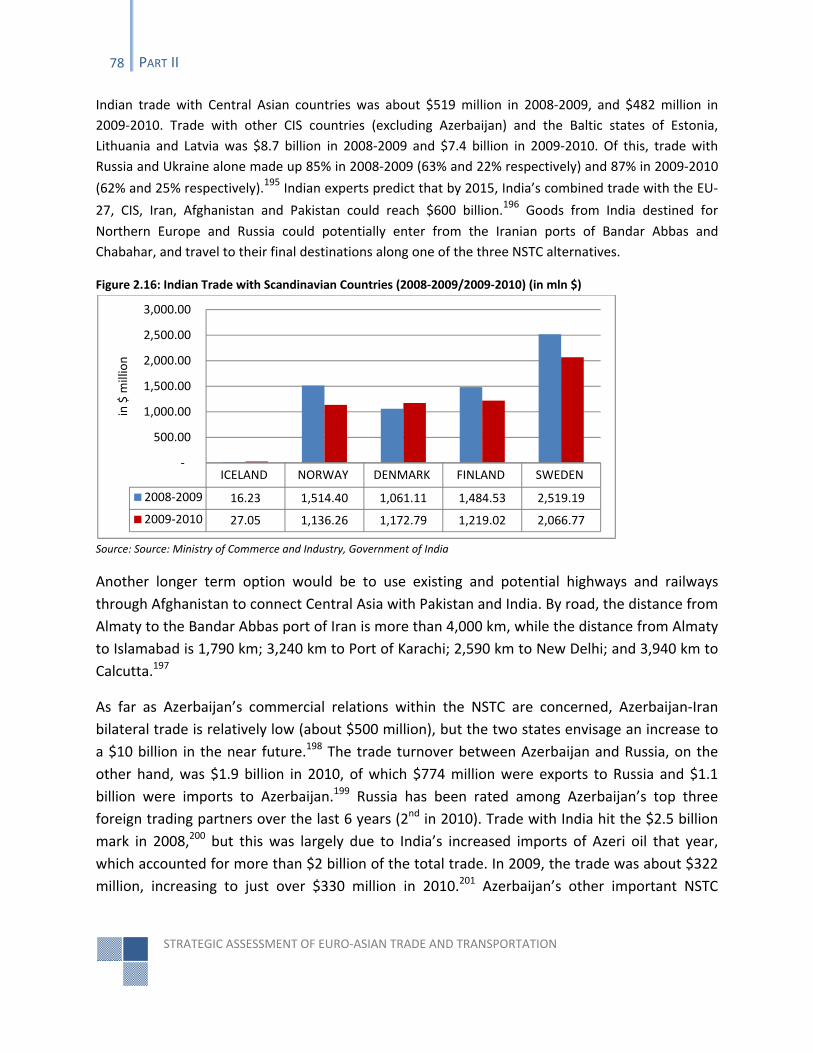

FIGURE 2.17: INDIAN TRADE WITH CIS (EXCLUDING CENTRAL ASIAN STATES AND AZERBAIJAN) & BALTIC STATES ............................... 79

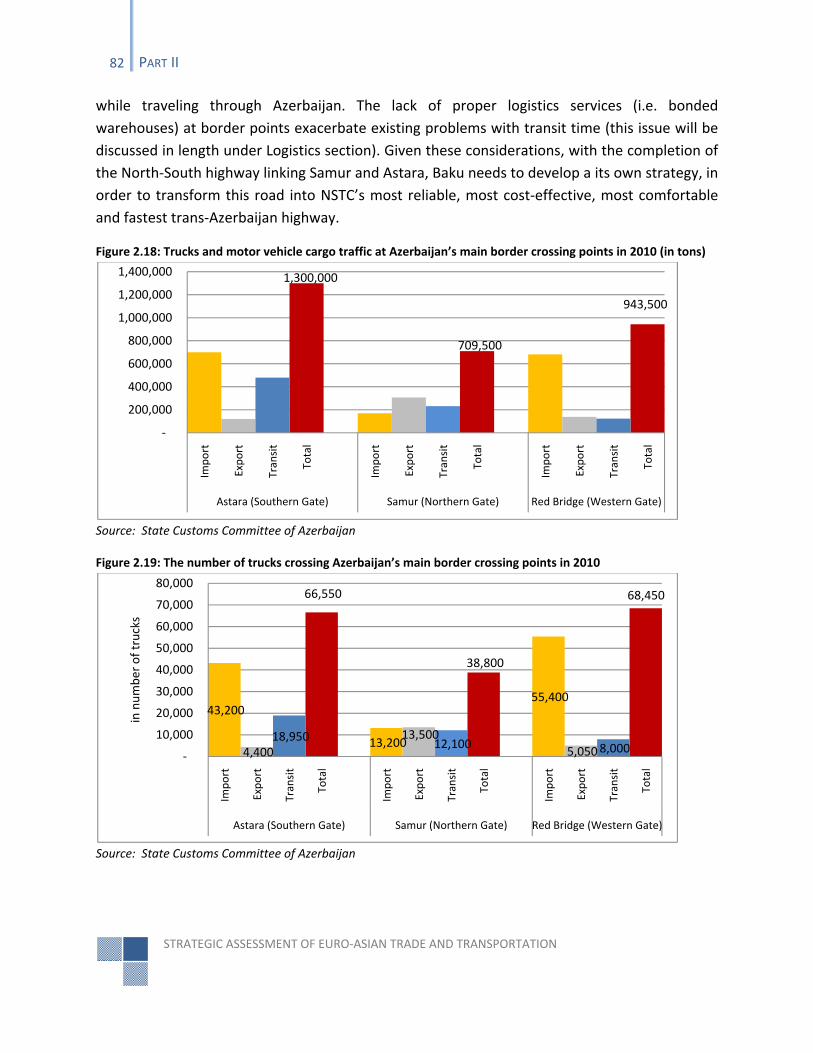

FIGURE 2.18: TRUCKS AND MOTOR VEHICLE CARGO TRAFFIC AT AZERBAIJAN’S MAIN BORDER CROSSING POINTS IN 2010 (IN TONS) ....... 82

FIGURE 2.19: THE NUMBER OF TRUCKS CROSSING AZERBAIJAN’S MAIN BORDER CROSSING POINTS IN 2010 ....................................... 82

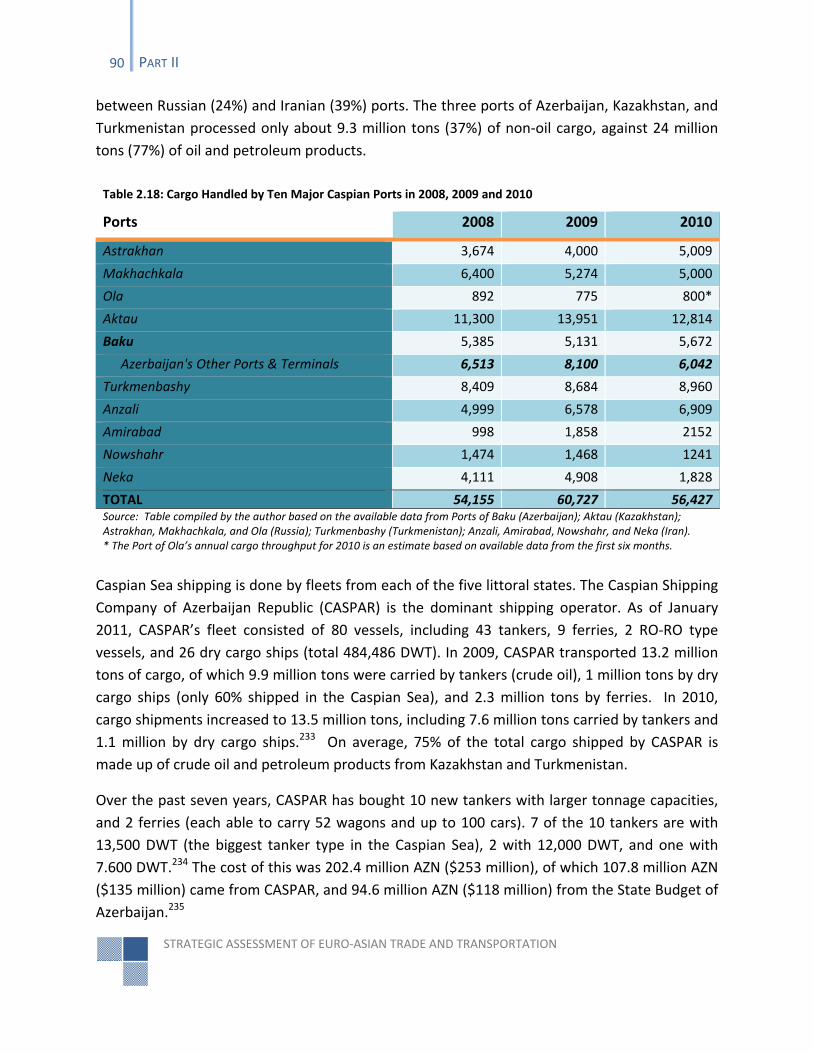

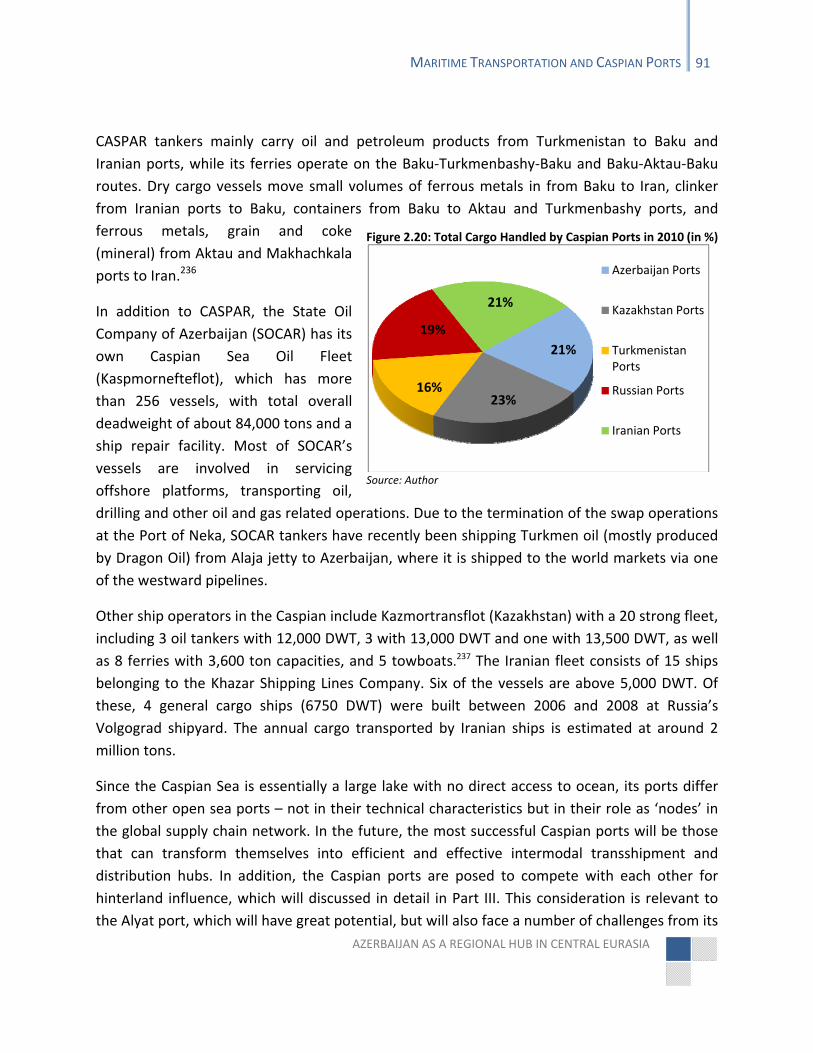

FIGURE 2.20: TOTAL CARGO HANDLED BY CASPIAN PORTS IN 2010 (IN %) ................................................................................ 91

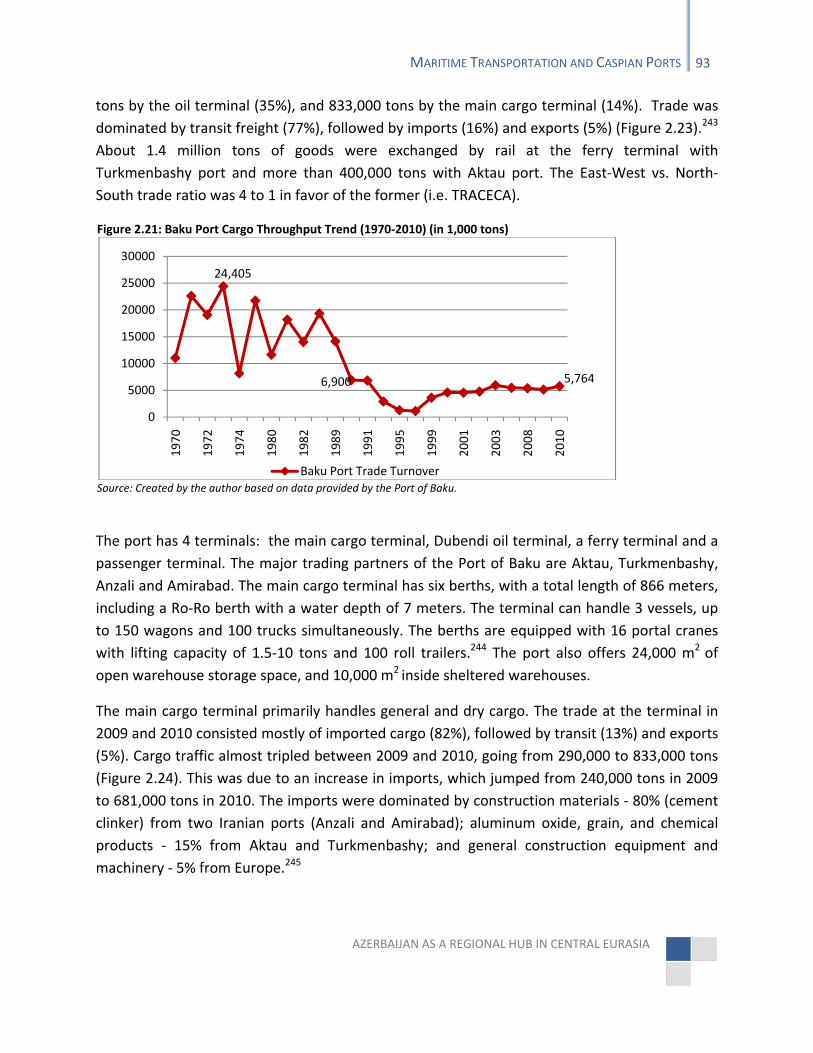

FIGURE 2.21: BAKU PORT CARGO THROUGHPUT TREND (1970‐2010) (IN 1,000 TONS).............................................................. 93

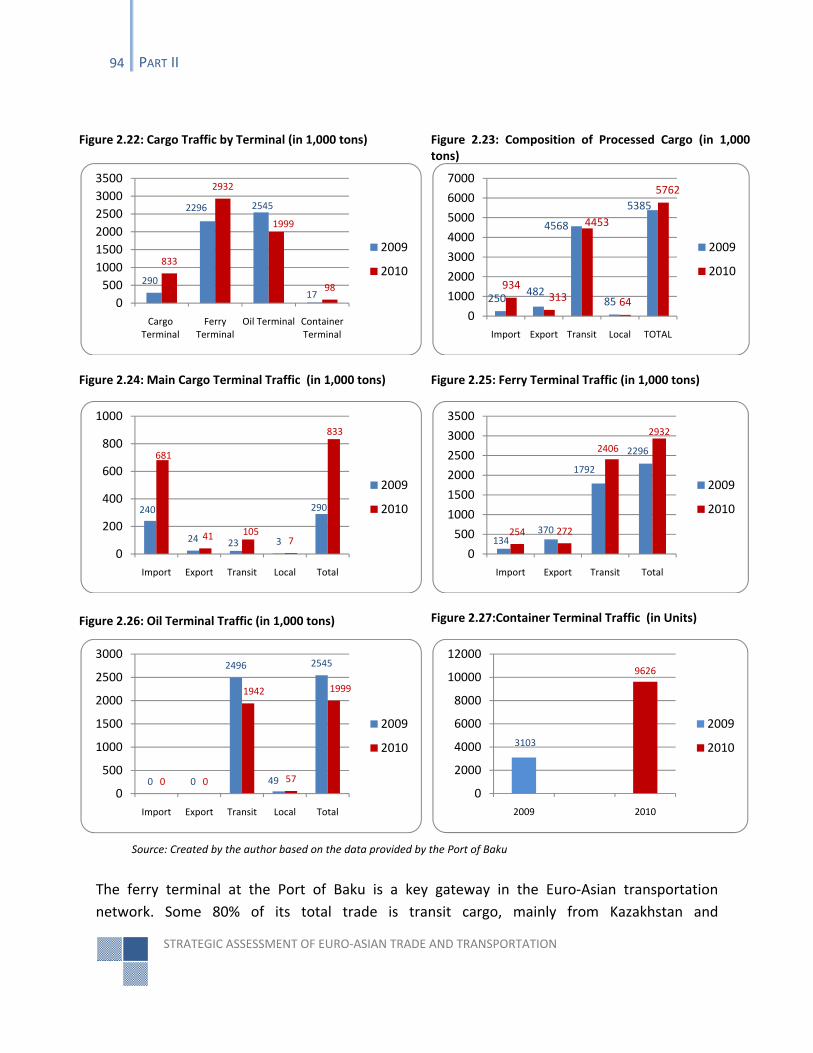

FIGURE 2.22: CARGO TRAFFIC BY TERMINAL (IN 1,000 TONS) .................................................................................................. 94

FIGURE 2.23: COMPOSITION OF PROCESSED CARGO (IN 1,000 TONS) ....................................................................................... 94

FIGURE 2.24: MAIN CARGO TERMINAL TRAFFIC (IN 1,000 TONS) ............................................................................................ 94

FIGURE 2.25: FERRY TERMINAL TRAFFIC (IN 1,000 TONS) ....................................................................................................... 94

FIGURE 2.26: OIL TERMINAL TRAFFIC (IN 1,000 TONS) ........................................................................................................... 94

FIGURE 2.27:CONTAINER TERMINAL TRAFFIC (IN UNITS) ........................................................................................................ 94

STRATEGIC ASSESSMENT OF EURO‐ASIAN TRADE AND TRANSPORTATION

xxii FIGURES & MAPS

FIGURE 2.28: AKTAU PORT CARGO COMPOSITION AND TRAFFIC (1996‐2010) (IN 1,000 TONS) ................................................... 97

FIGURE 2.29: TOTAL CARGO TRAFFIC AT AKTAU PORT: OIL VS. NON‐OIL CARGO (1996‐2010) (IN %) ........................................... 98

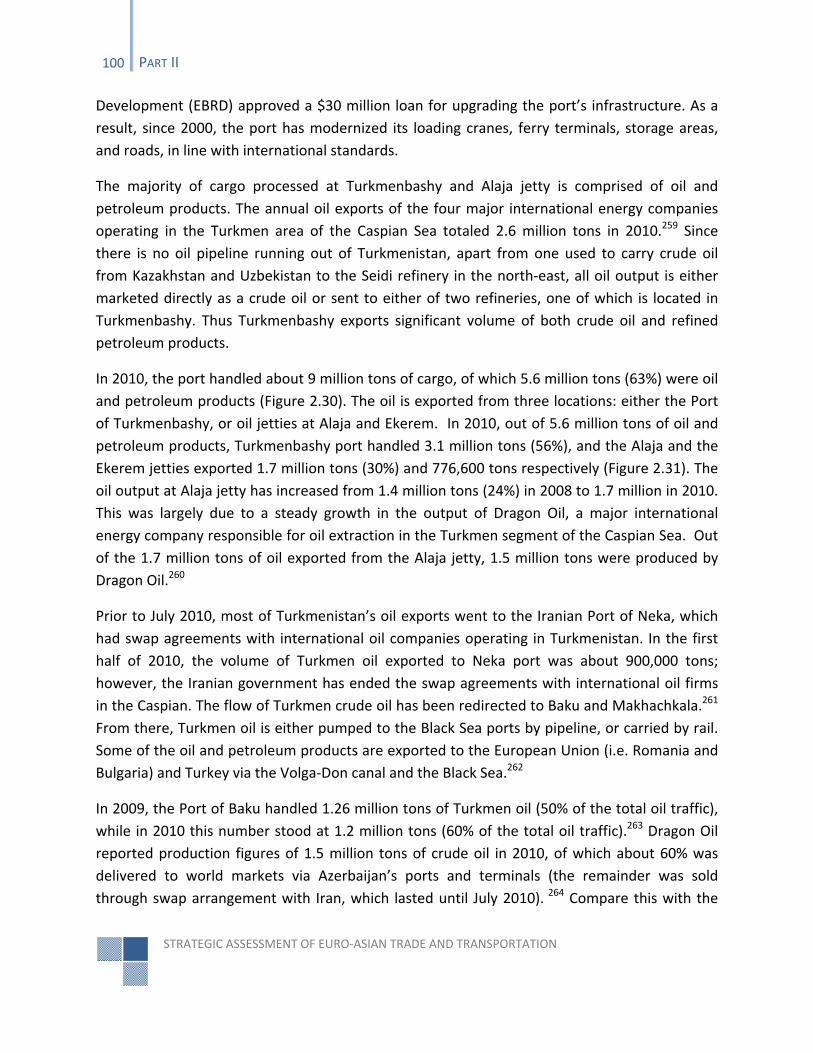

FIGURE 2.30: OIL VS. NON‐OIL CARGO TRAFFIC AT TURKMENISTAN’S PORTS (2008‐2010) (IN 1,000 TONS) ................................ 101

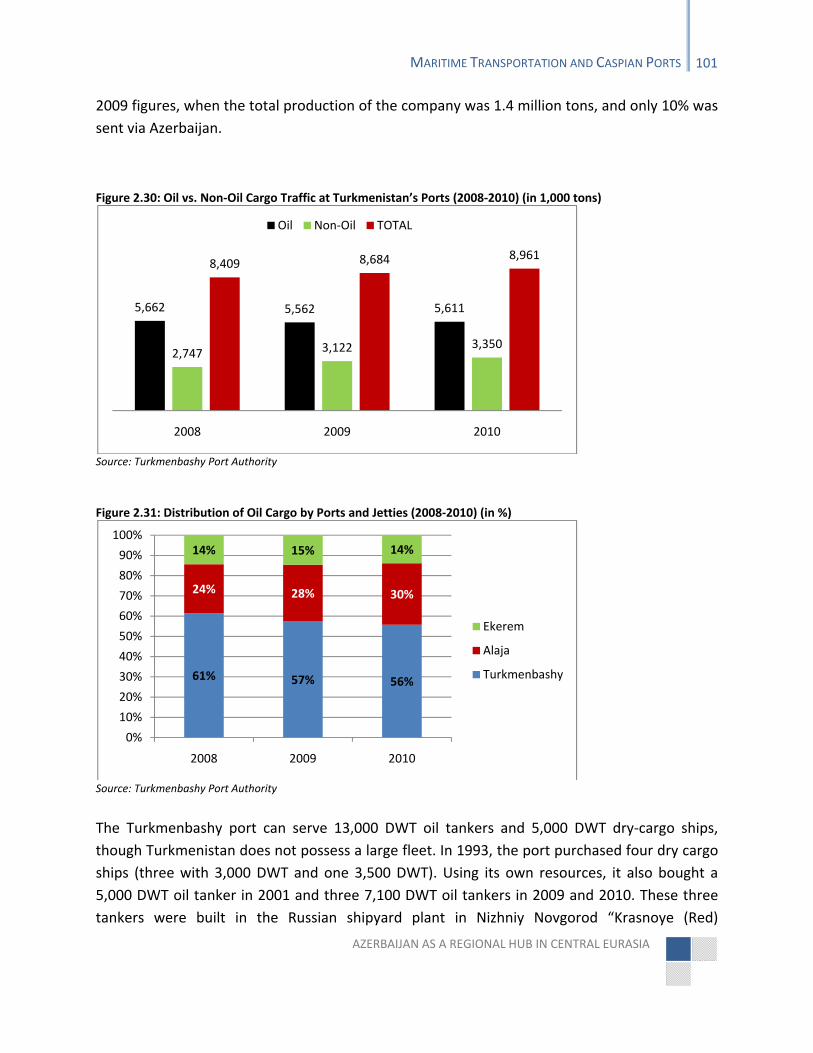

FIGURE 2.31: DISTRIBUTION OF OIL CARGO BY PORTS AND JETTIES (2008‐2010) (IN %) ............................................................ 101

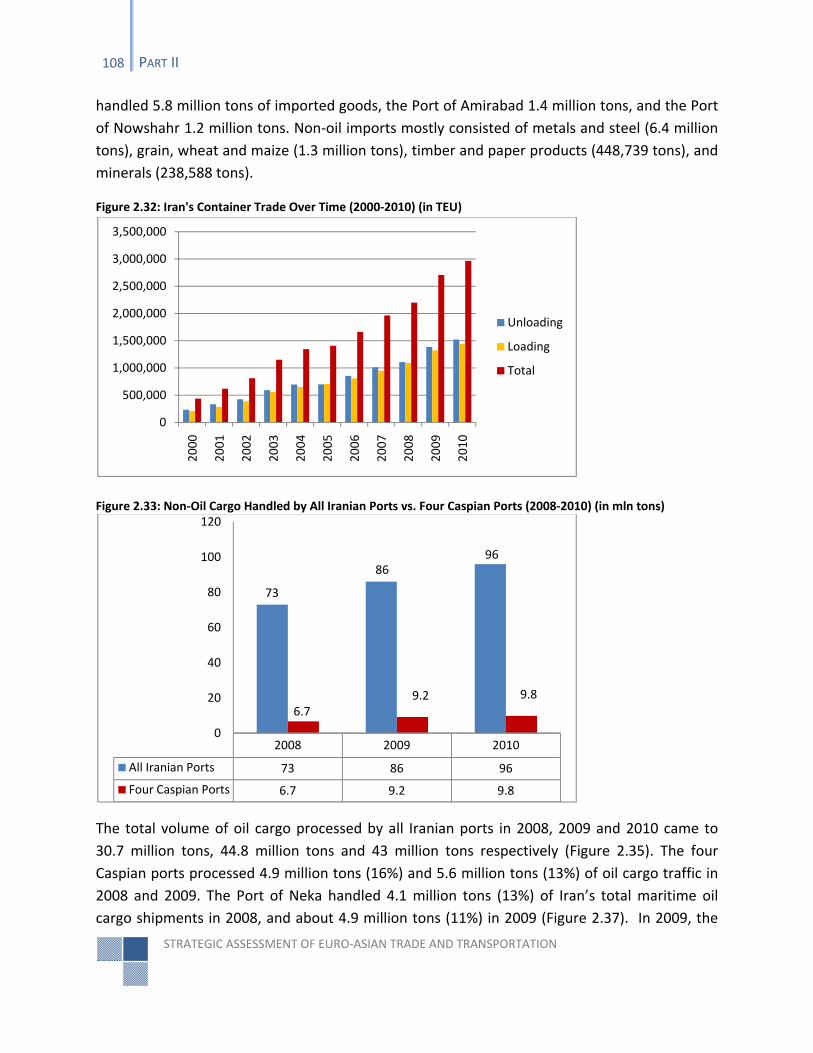

FIGURE 2.32: IRAN'S CONTAINER TRADE OVER TIME (2000‐2010) (IN TEU) ........................................................................... 108

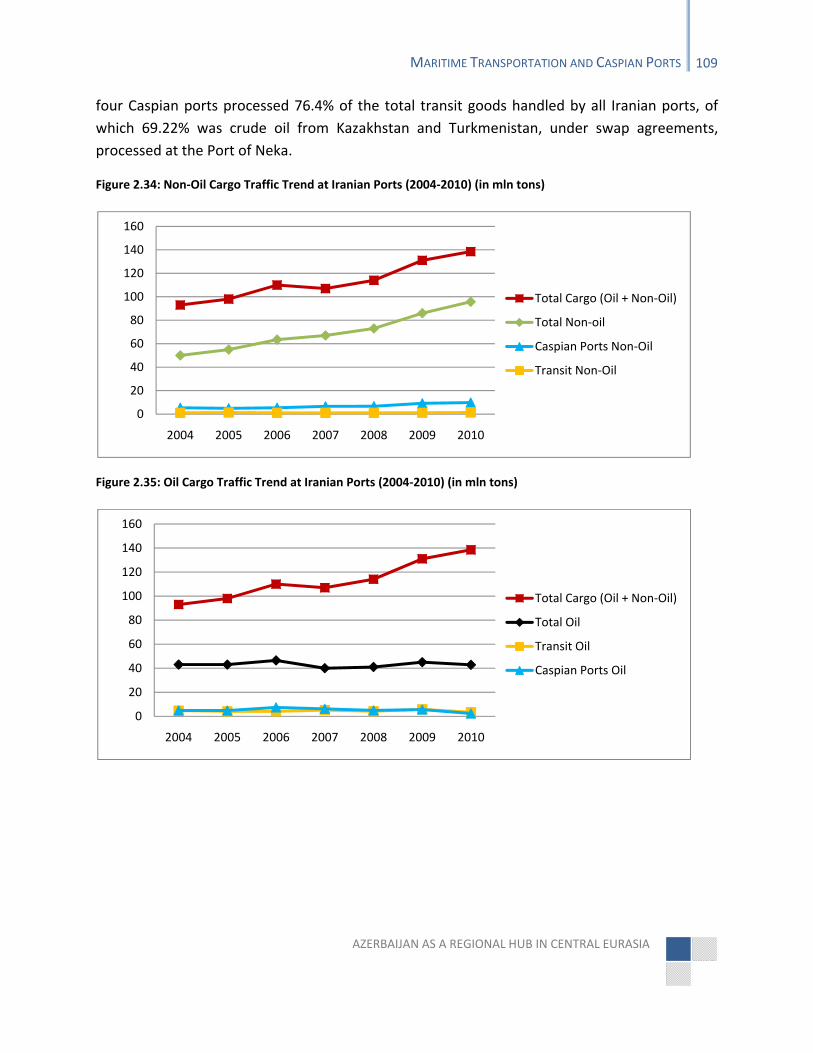

FIGURE 2.33: NON‐OIL CARGO HANDLED BY ALL IRANIAN PORTS VS. FOUR CASPIAN PORTS (2008‐2010) (IN MLN TONS) ............... 108

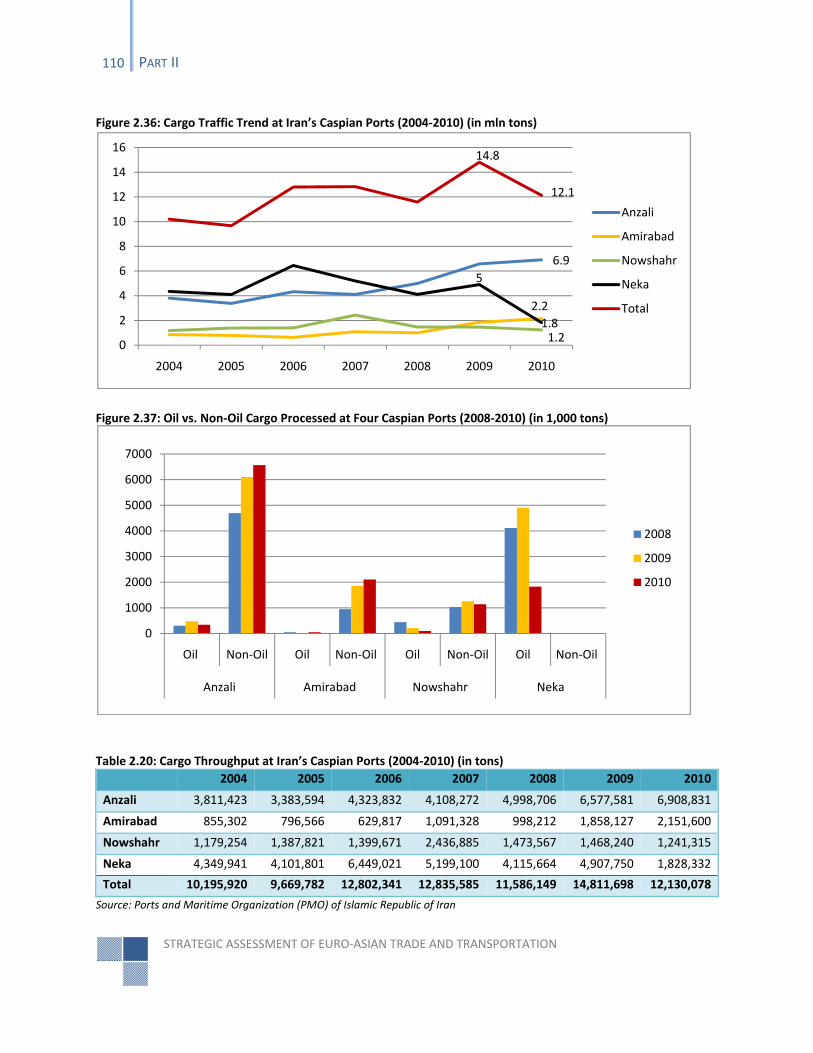

FIGURE 2.34: NON‐OIL CARGO TRAFFIC TREND AT IRANIAN PORTS (2004‐2010) (IN MLN TONS) ................................................ 109

FIGURE 2.35: OIL CARGO TRAFFIC TREND AT IRANIAN PORTS (2004‐2010) (IN MLN TONS) ........................................................ 109

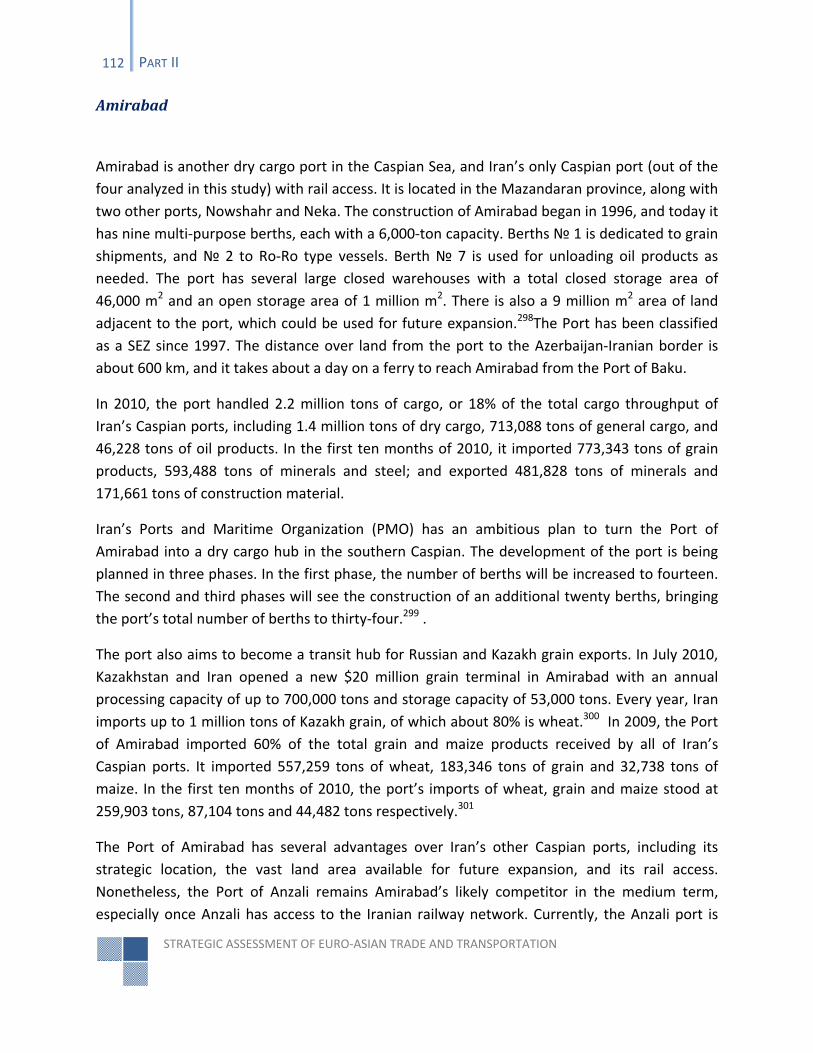

FIGURE 2.36: CARGO TRAFFIC TREND AT IRAN’S CASPIAN PORTS (2004‐2010) (IN MLN TONS) ................................................... 110

FIGURE 2.37: OIL VS. NON‐OIL CARGO PROCESSED AT FOUR CASPIAN PORTS (2008‐2010) (IN 1,000 TONS) ............................... 110

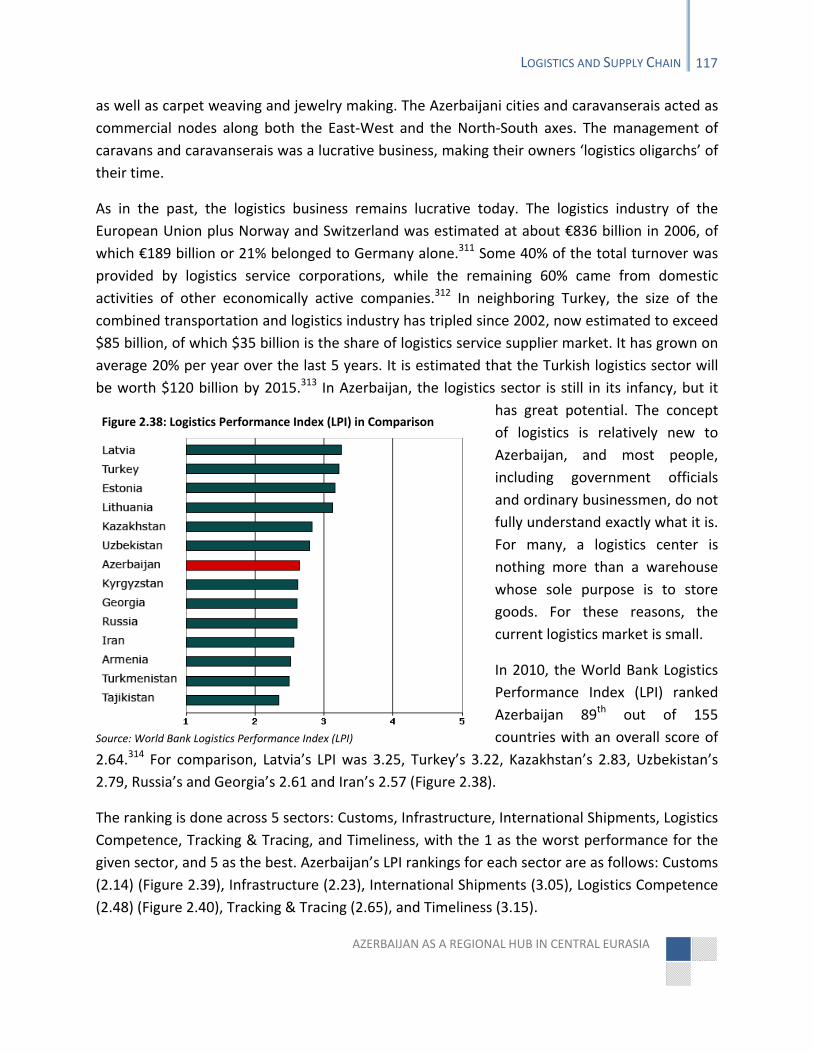

FIGURE 2.38: LOGISTICS PERFORMANCE INDEX (LPI) IN COMPARISON ..................................................................................... 117

FIGURE 2.39: LPI CUSTOMS ............................................................................................................................................. 118

FIGURE 2.40: LPI LOGISTICS COMPETENCE ......................................................................................................................... 118

FIGURE 2.41: A NODE‐LINK SYSTEM ................................................................................................................................... 123

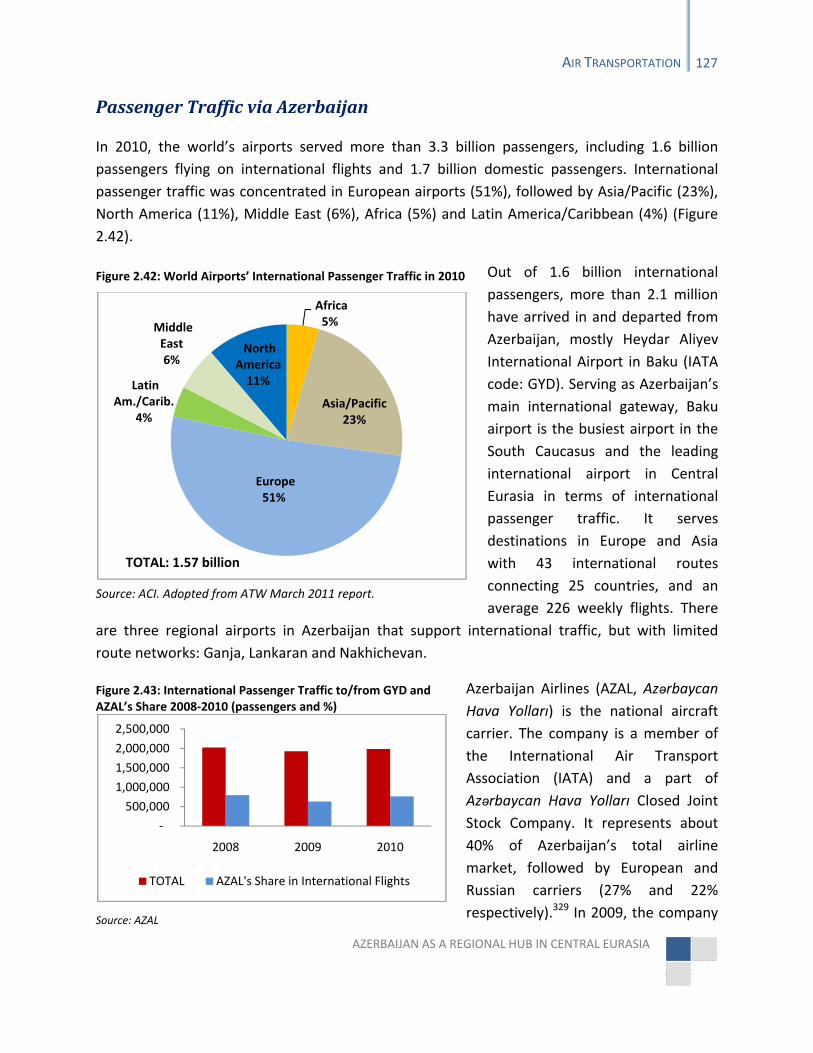

FIGURE 2.42: WORLD AIRPORTS’ INTERNATIONAL PASSENGER TRAFFIC IN 2010 ....................................................................... 127

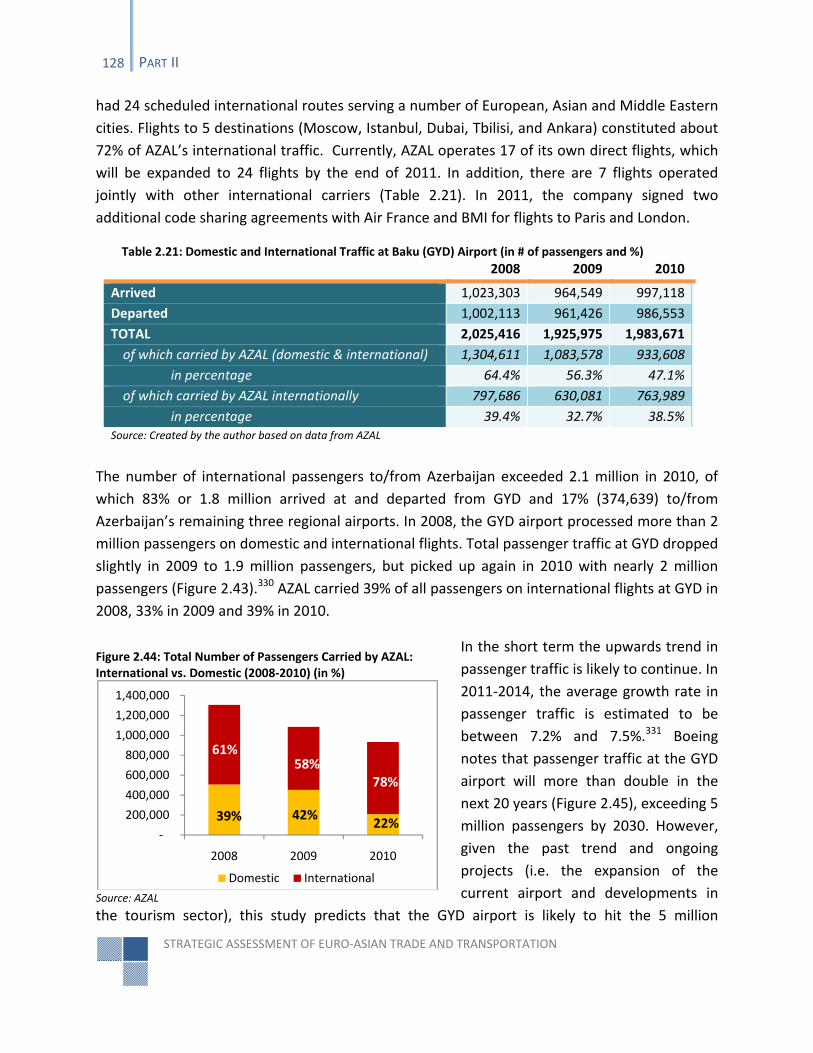

FIGURE 2.43: INTERNATIONAL PASSENGER TRAFFIC TO/FROM GYD AND AZAL’S SHARE 2008‐2010 (PASSENGERS AND %) ............. 127

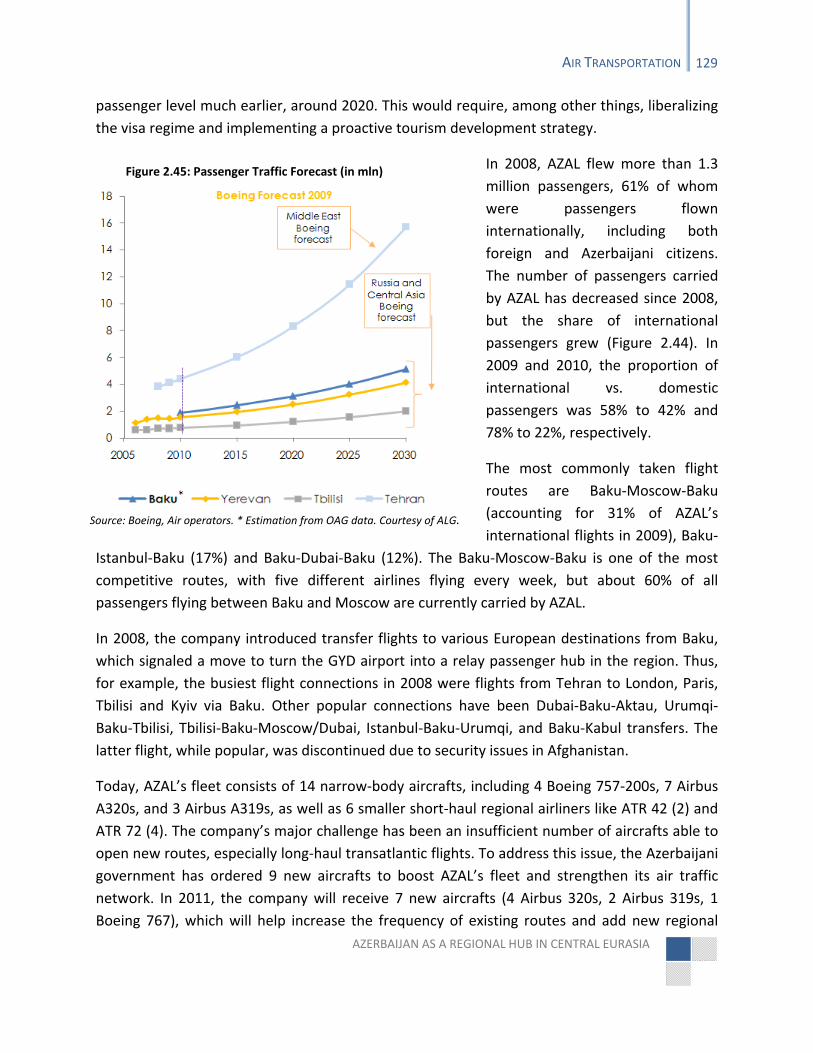

FIGURE 2.44: TOTAL NUMBER OF PASSENGERS CARRIED BY AZAL: INTERNATIONAL VS. DOMESTIC (2008‐2010) (IN %) ................. 128

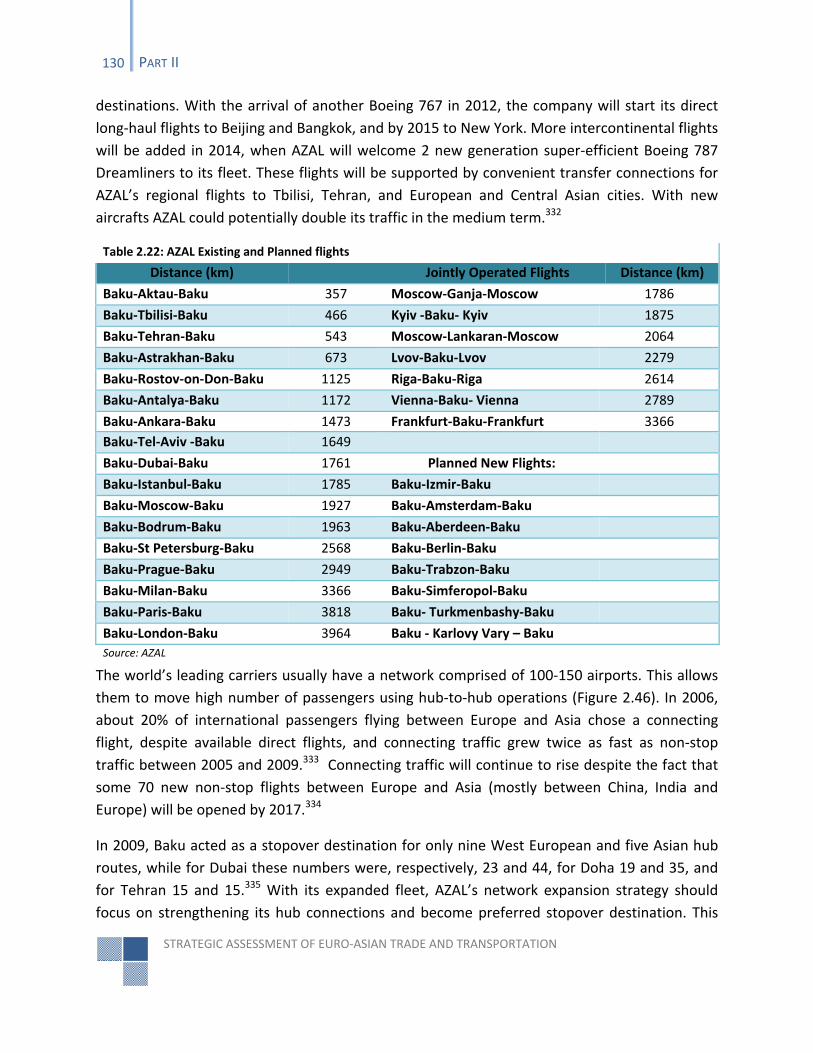

FIGURE 2.45: PASSENGER TRAFFIC FORECAST (IN MLN) ......................................................................................................... 129

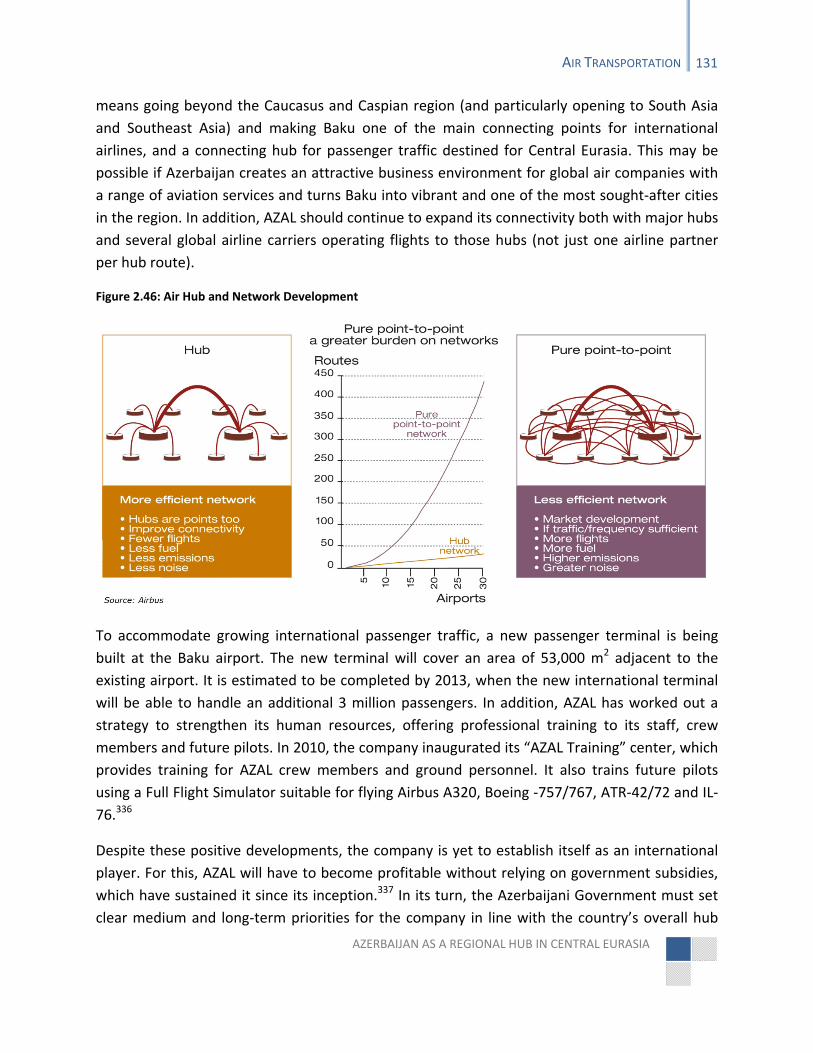

FIGURE 2.46: AIR HUB AND NETWORK DEVELOPMENT ......................................................................................................... 131

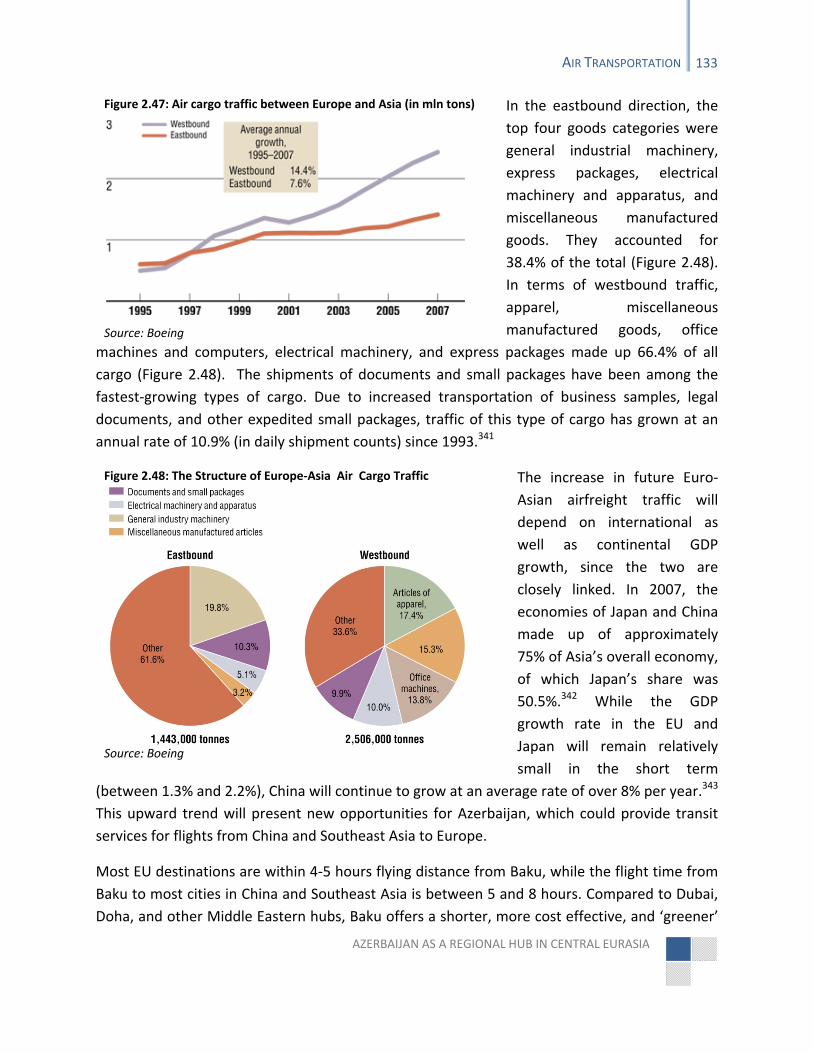

FIGURE 2.47: AIR CARGO TRAFFIC BETWEEN EUROPE AND ASIA (IN MLN TONS) .......................................................................... 133

FIGURE 2.48: THE STRUCTURE OF EUROPE‐ASIA AIR CARGO TRAFFIC ..................................................................................... 133

FIGURE 2.49: AIR CARGO TRAFFIC VIA BAKU CARGO TERMINAL (IN 1,000 TONS) ...................................................................... 136

FIGURE 2.50: AIR CARGO TRAFFIC VIA BAKU AND NAVOI (UZBEKISTAN) (IN 1,000 TONS) ........................................................... 137

FIGURE 2.51: THE PRICE OF JET FUEL ON APRIL 15, 2011 (PER METRIC TON) ........................................................................... 138

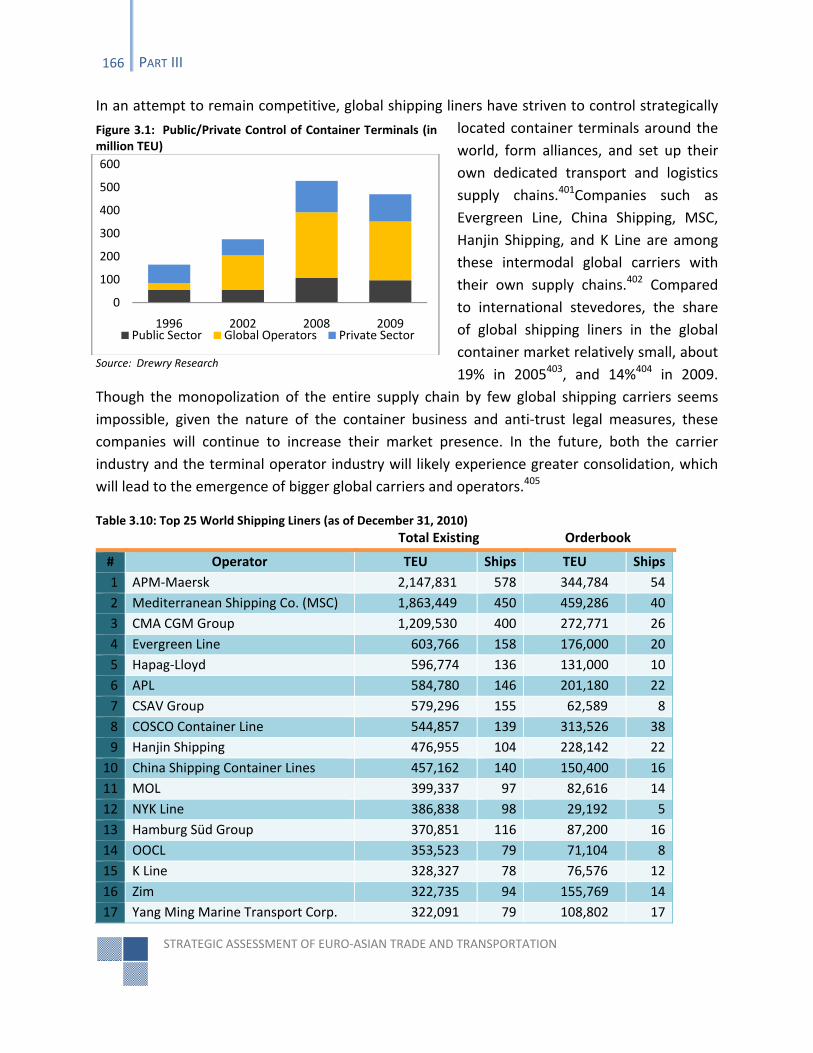

FIGURE 3.1: PUBLIC/PRIVATE CONTROL OF CONTAINER TERMINALS (IN MILLION TEU) ............................................................... 166

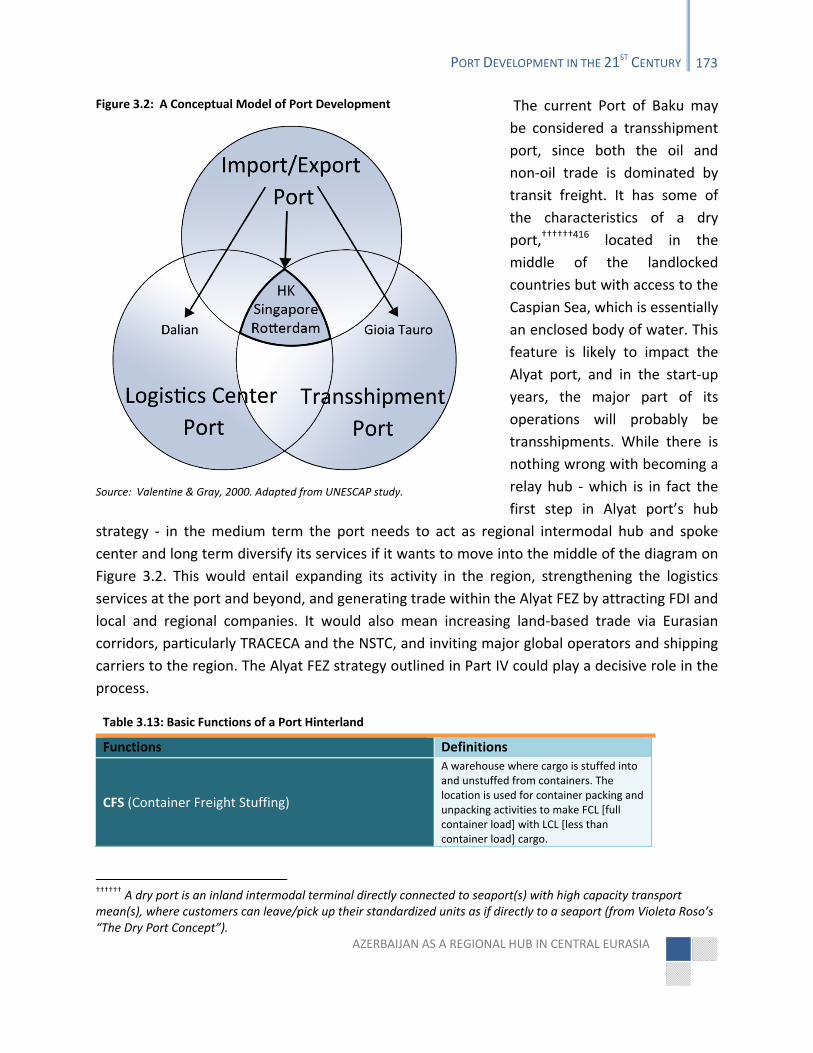

FIGURE 3.2: A CONCEPTUAL MODEL OF PORT DEVELOPMENT ............................................................................................... 173

FIGURE 3.3: PORT HINTERLAND CONCEPT ........................................................................................................................... 174

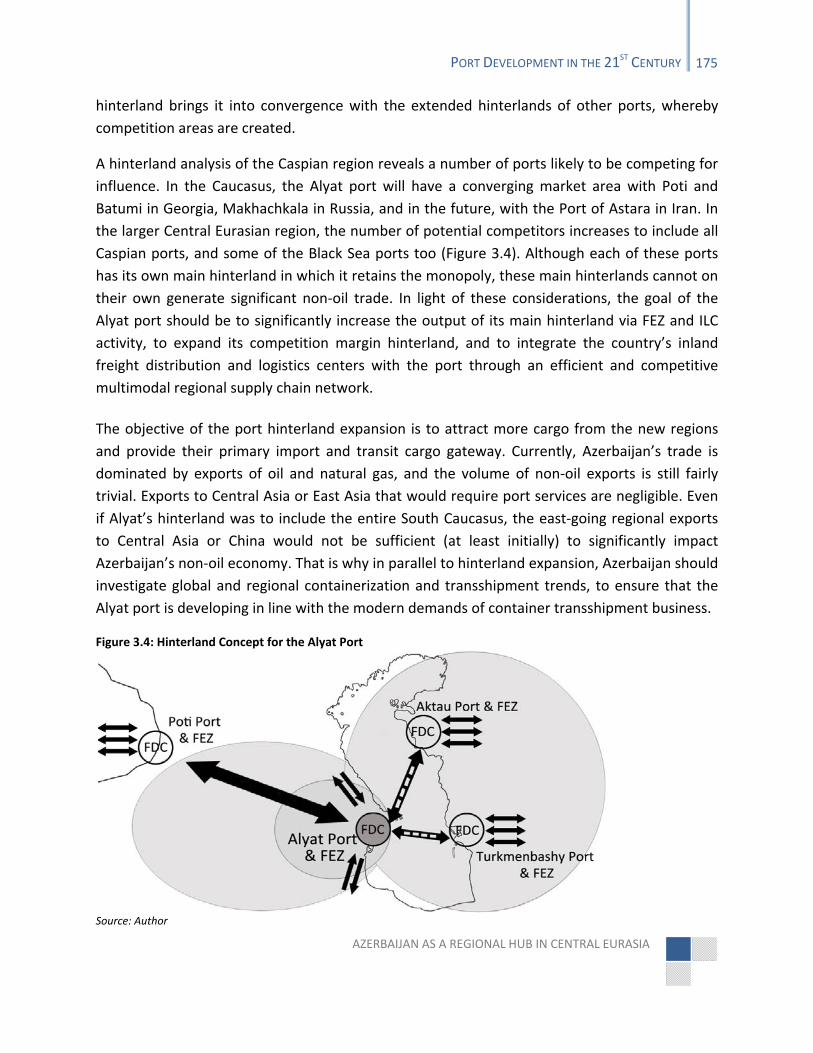

FIGURE 3.4: HINTERLAND CONCEPT FOR THE ALYAT PORT ...................................................................................................... 175

FIGURE 4.1: POSSIBLE ORGANIZATIONAL STRUCTURE OF FEZ CONCEPT FOR AZERBAIJAN ............................................................. 185

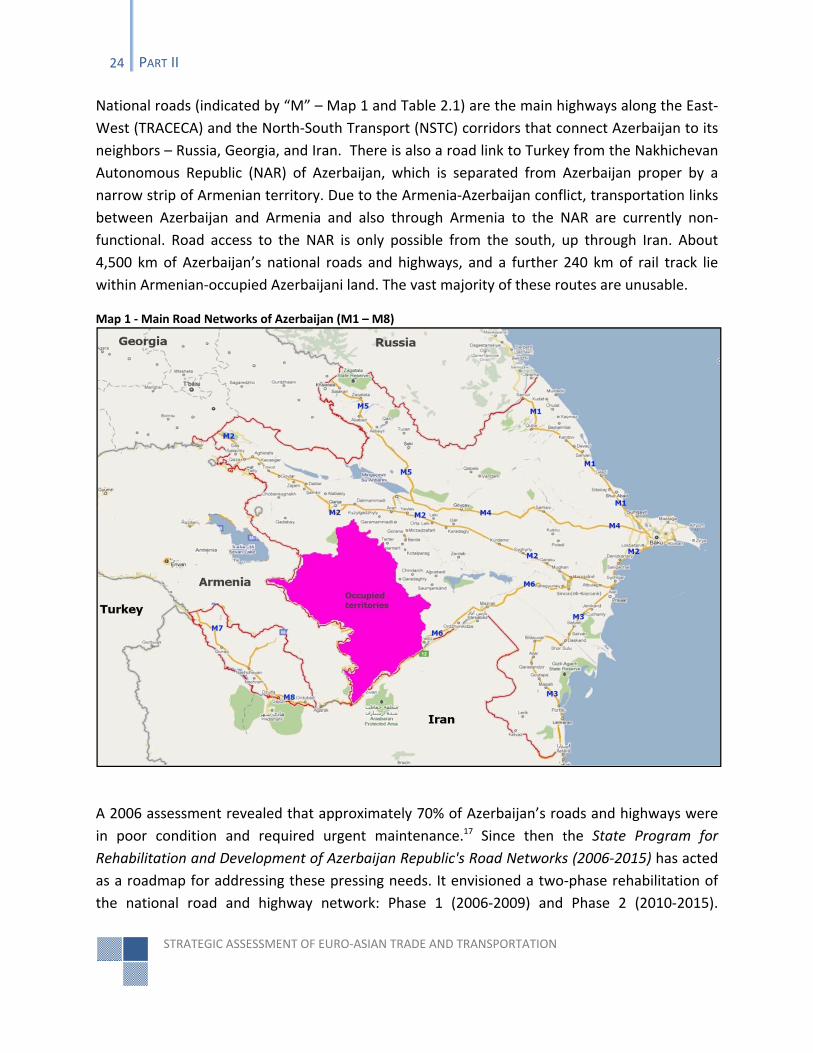

MAP 1 ‐ MAIN ROAD NETWORKS OF AZERBAIJAN (M1 – M8) ................................................................................................. 24

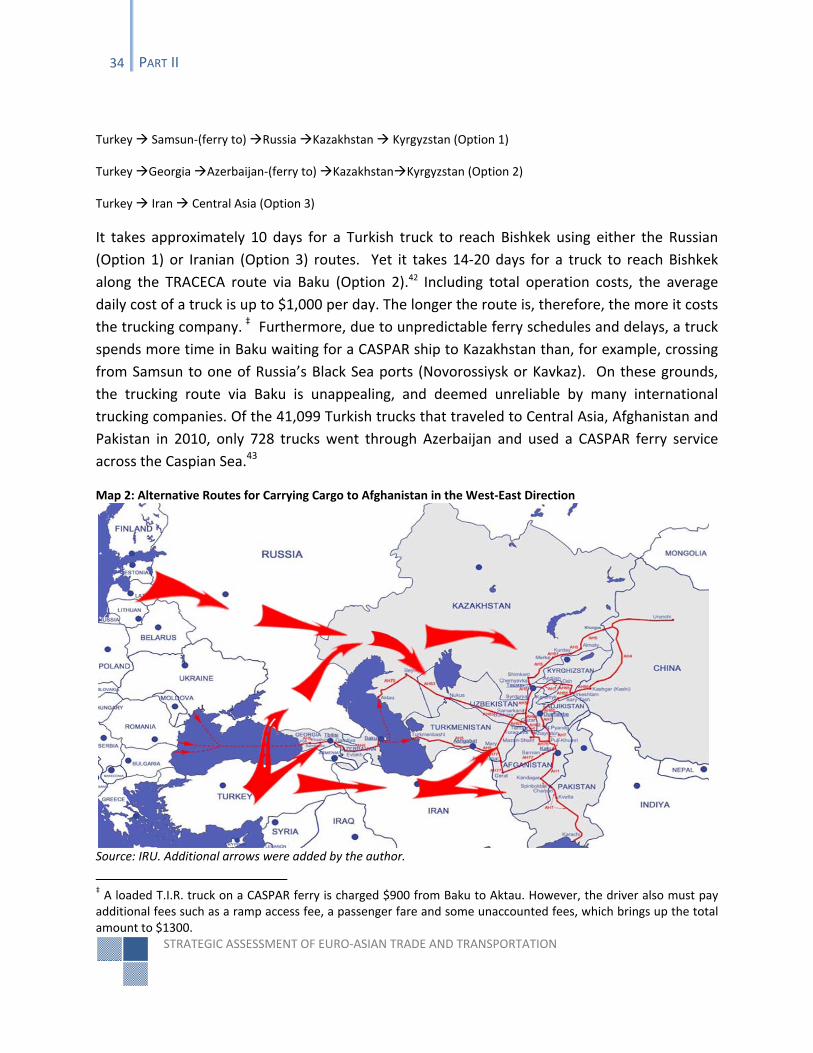

MAP 2: ALTERNATIVE ROUTES FOR CARRYING CARGO TO AFGHANISTAN IN THE WEST‐EAST DIRECTION ........................................... 34

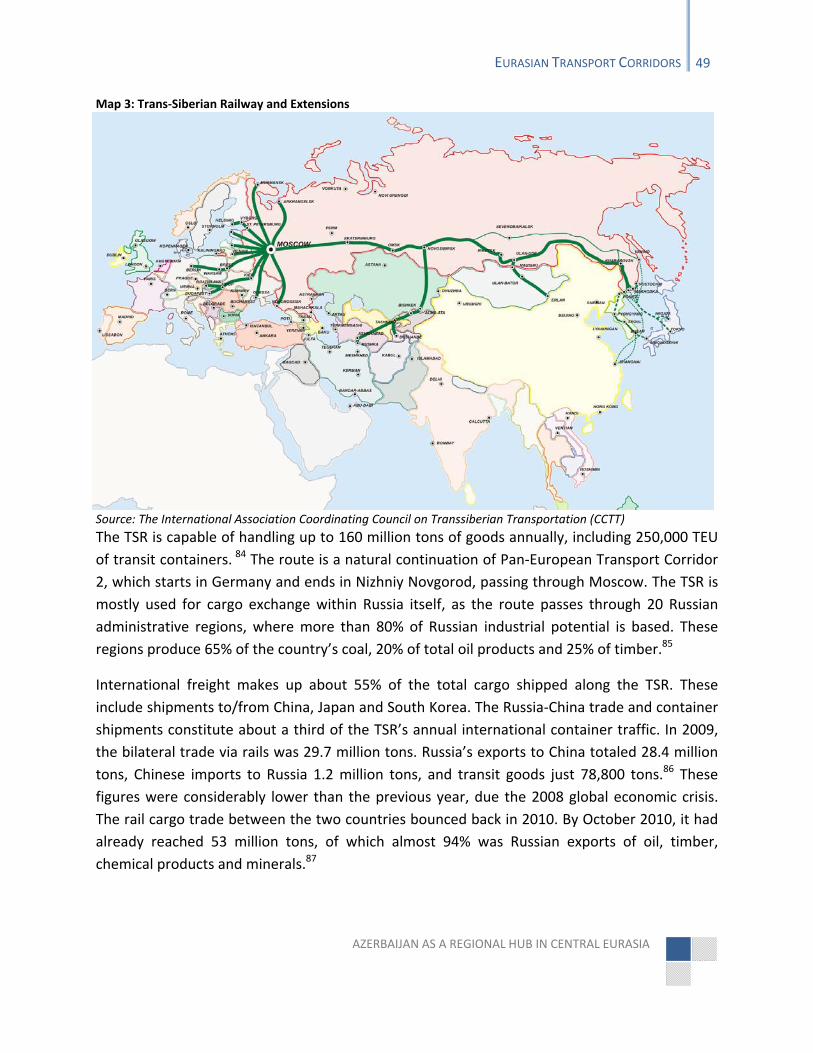

MAP 3: TRANS‐SIBERIAN RAILWAY AND EXTENSIONS .............................................................................................................. 49

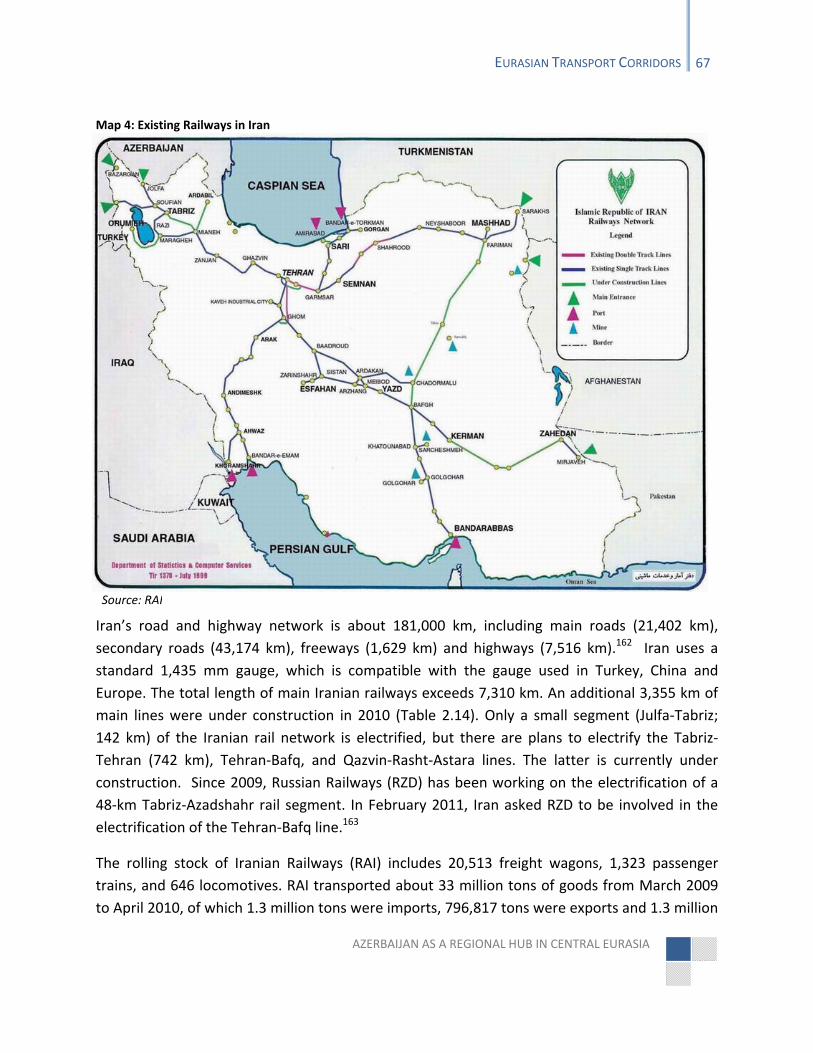

MAP 4: EXISTING RAILWAYS IN IRAN .................................................................................................................................... 67

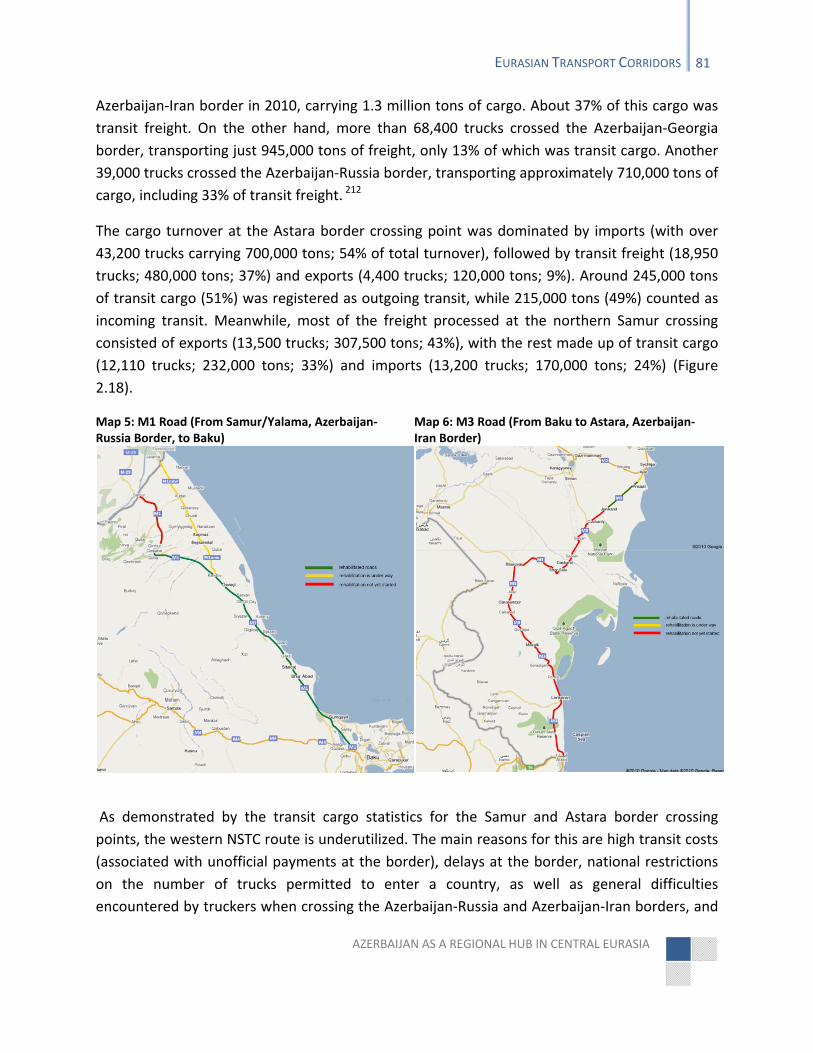

MAP 5: M1 ROAD (FROM SAMUR/YALAMA, AZERBAIJAN‐RUSSIA BORDER, TO BAKU) ................................................................. 81

MAP 6: M3 ROAD (FROM BAKU TO ASTARA, AZERBAIJAN‐IRAN BORDER) .................................................................................. 81

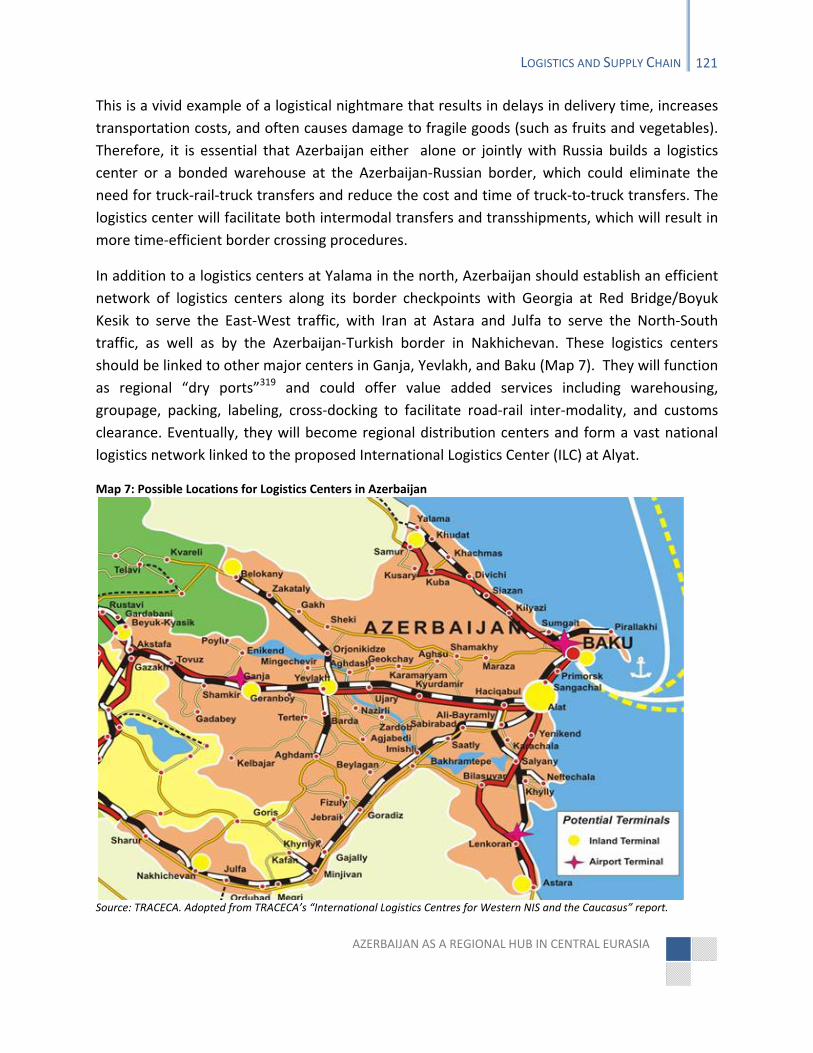

MAP 7: POSSIBLE LOCATIONS FOR LOGISTICS CENTERS IN AZERBAIJAN ...................................................................................... 121

MAP 8: ALYAT ILC AS MAJOR INTERMODAL HUB IN THE CASPIAN REGION ................................................................................ 124

MAP 10: SILK WAY AIRLINES FLIGHT ROUTES IN EUROPE AND ASIA ......................................................................................... 135

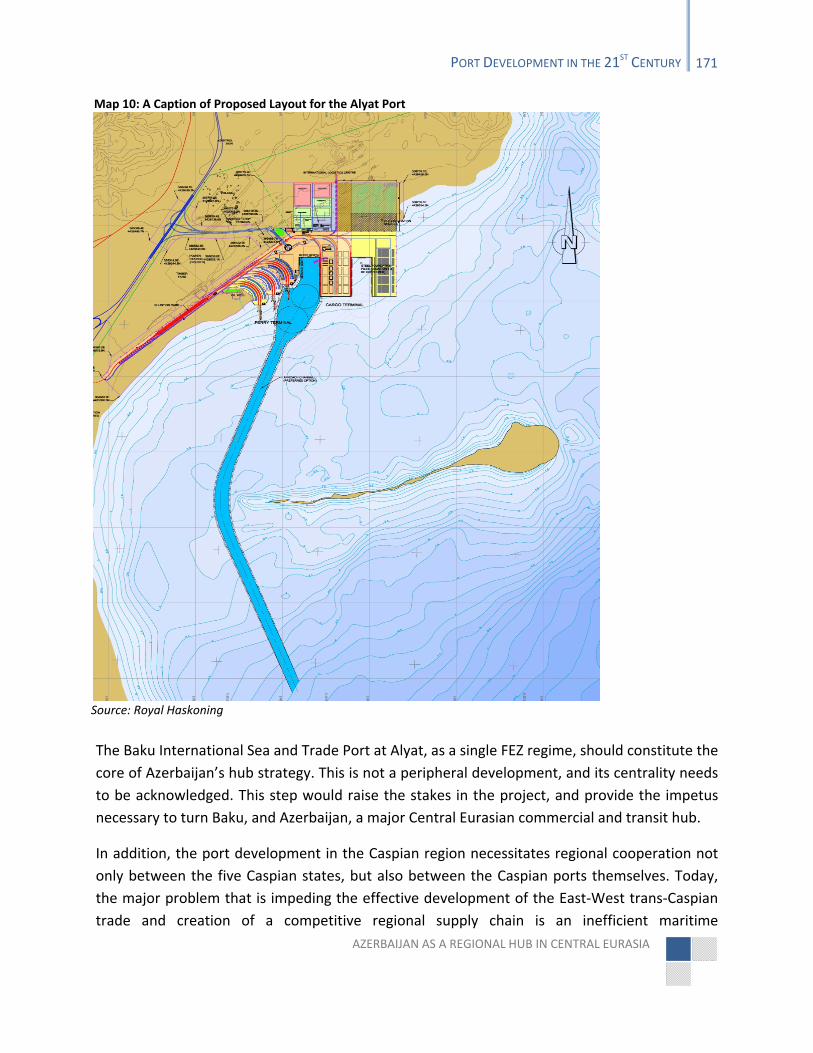

MAP 11: A CAPTION OF PROPOSED LAYOUT FOR THE ALYAT PORT .......................................................................................... 171

AZERBAIJAN AS A REGIONAL HUB IN CENTRAL EURASIA

TABLES

TABLE 1.1: WORLD EXPORTS OF MERCHANDISE AND COMMERCIAL SERVICES, 2005‐10 ($BLN & ANNUAL % CHANGE) ........................ 10

TABLE 1.2: EU‐CHINA TRADE BY VOLUME AND MODE OF TRANSPORT (IN TONS, %) .................................................................... 13

TABLE 1.3: DISTRIBUTION OF EU‐CHINA TRADE BY MODE OF TRANSPORT IN 2010 (IN € AND %) ................................................... 13

TABLE 1.4: EU‐ASEAN TRADE IN QUANTITY AND VALUE IN 2010 ............................................................................................ 14

TABLE 1.5: DISTRIBUTION OF EU‐INDIA TRADE BY MODE OF TRANSPORT IN 2010 (IN € AND %) .................................................... 15

TABLE 1.6: EU‐INDIA TRADE BY VOLUME AND MODE OF TRANSPORT (IN TONS, %) ...................................................................... 16

TABLE 1.7: MAJOR MARITIME TRADE PARTNERS OF EU IN ASIA IN 2010 ................................................................................... 18

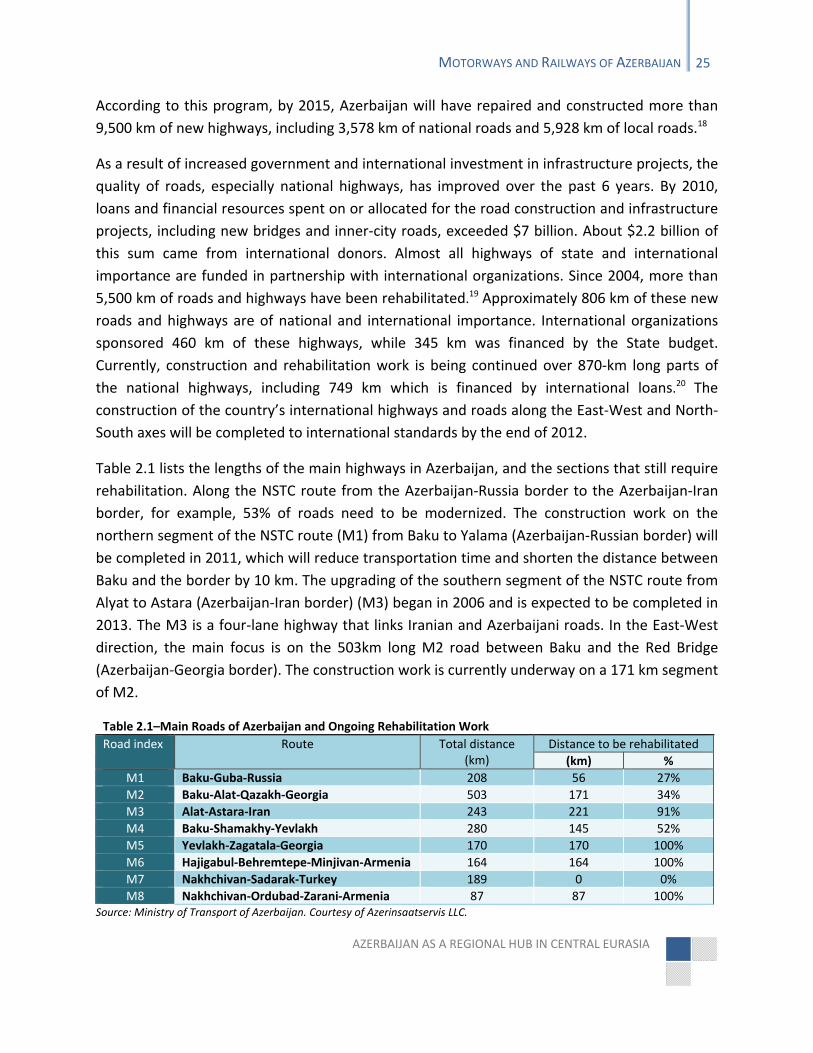

TABLE 2.1–MAIN ROADS OF AZERBAIJAN AND ONGOING REHABILITATION WORK ........................................................................ 25

TABLE 2.2: TRANSPORTATION OF CARGO ALONG AZERBAIJAN’S SEGMENT OF TRACECA (IN 1000 TONS) ........................................ 30

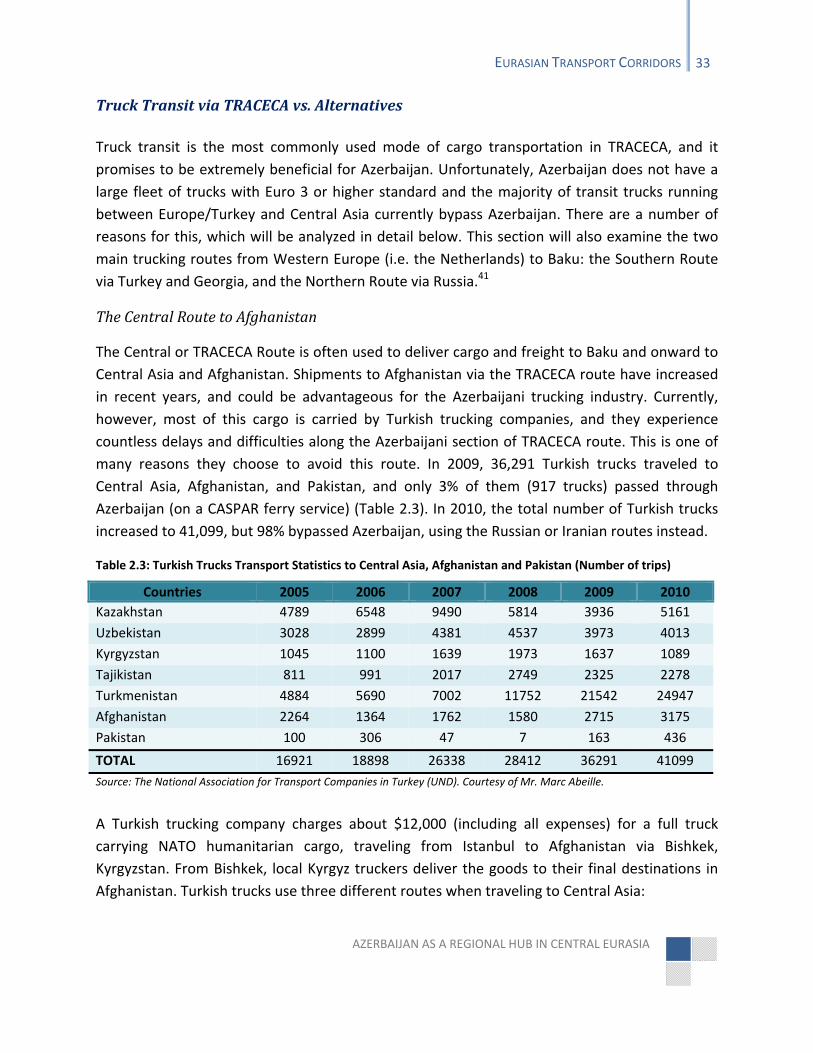

TABLE 2.3: TURKISH TRUCKS TRANSPORT STATISTICS TO CENTRAL ASIA, AFGHANISTAN AND PAKISTAN (NUMBER OF TRIPS) ................. 33

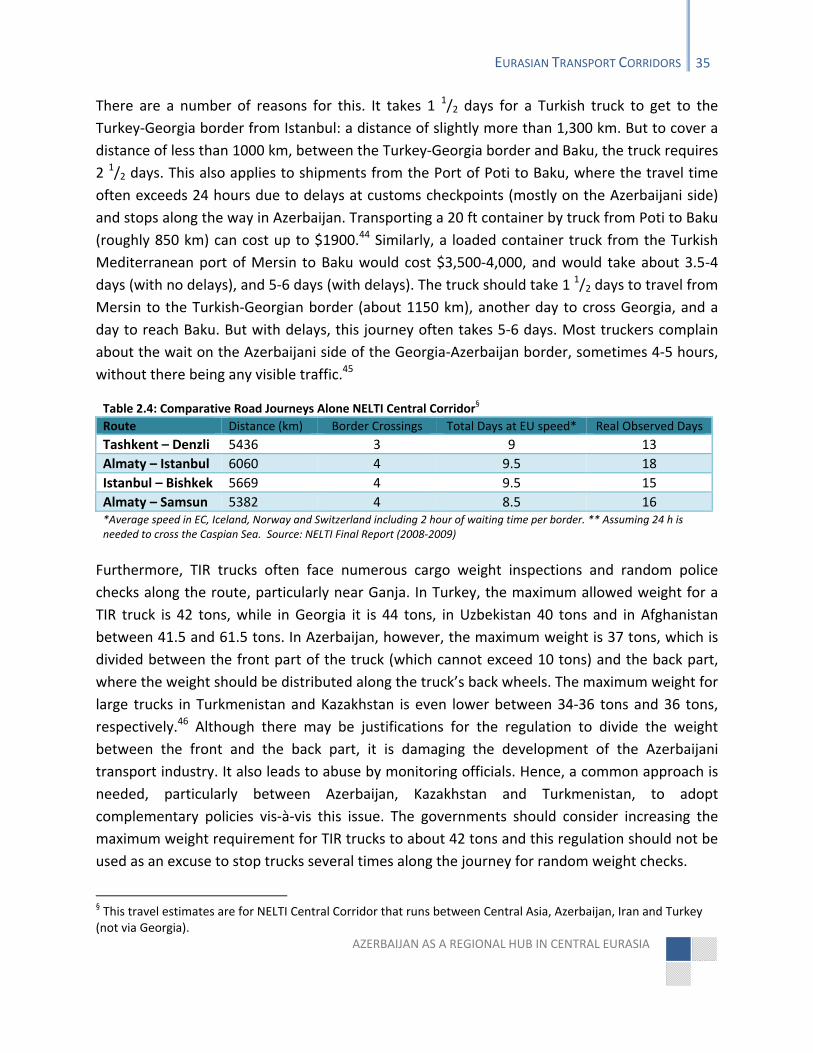

TABLE 2.4: COMPARATIVE ROAD JOURNEYS ALONE NELTI CENTRAL CORRIDOR .......................................................................... 35

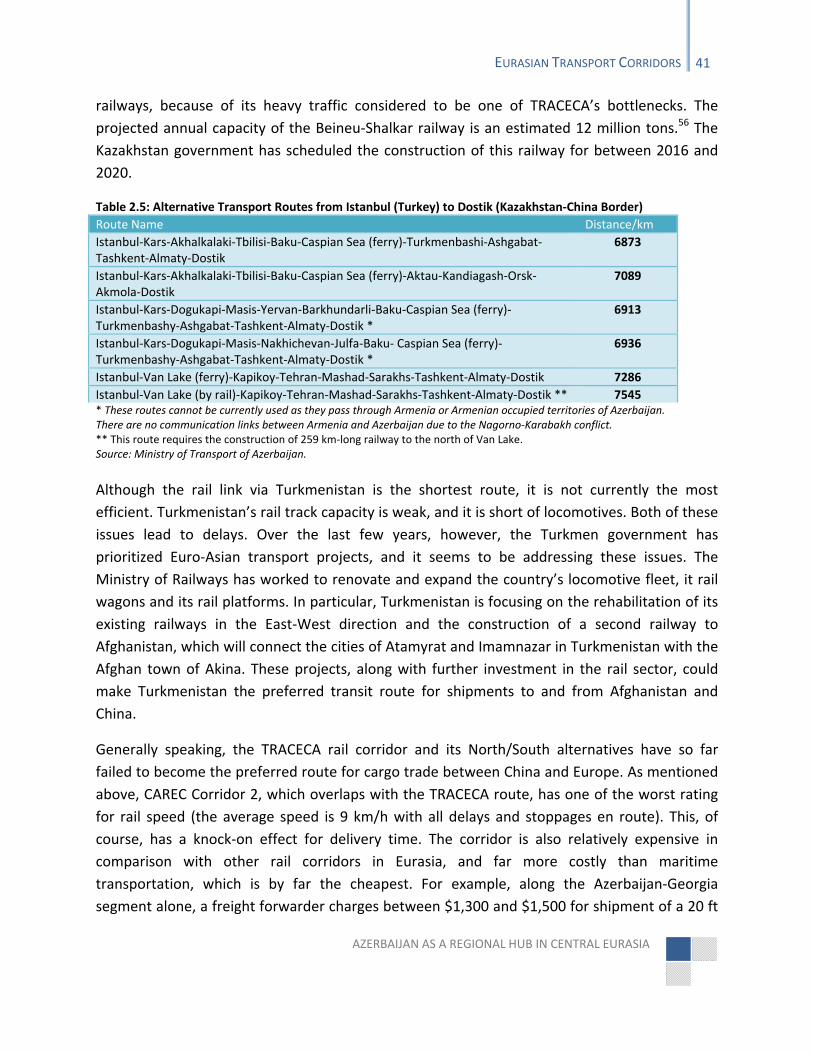

TABLE 2.5: ALTERNATIVE TRANSPORT ROUTES FROM ISTANBUL (TURKEY) TO DOSTIK (KAZAKHSTAN‐CHINA BORDER) ......................... 41

TABLE 2.6: SHIPPING TIME AND COST FOR ONE TEU (OR EQUIVALENT IN SIZE CARGO) FROM CHINA TO GERMANY ............................. 46

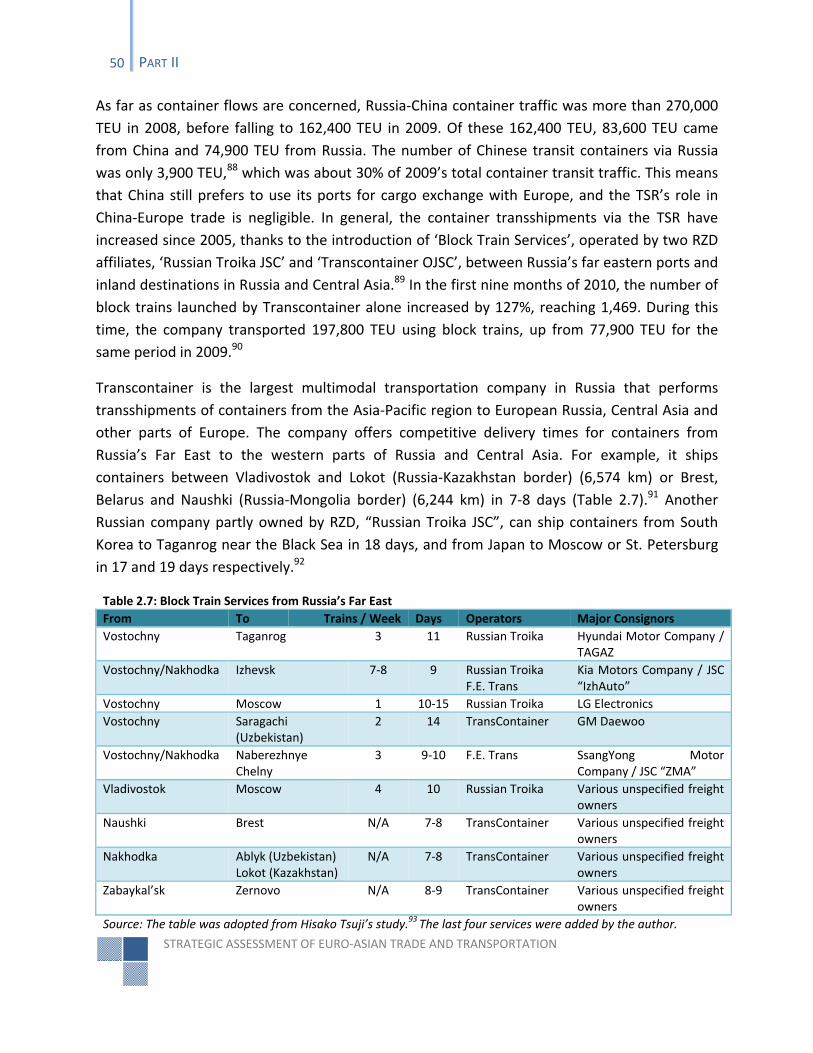

TABLE 2.7: BLOCK TRAIN SERVICES FROM RUSSIA’S FAR EAST ................................................................................................... 50

TABLE 2.8: STRUCTURE OF INTERNATIONAL CARGO IN KAZAKHSTAN IN 2009 (IN 1,000 TONS) ...................................................... 56

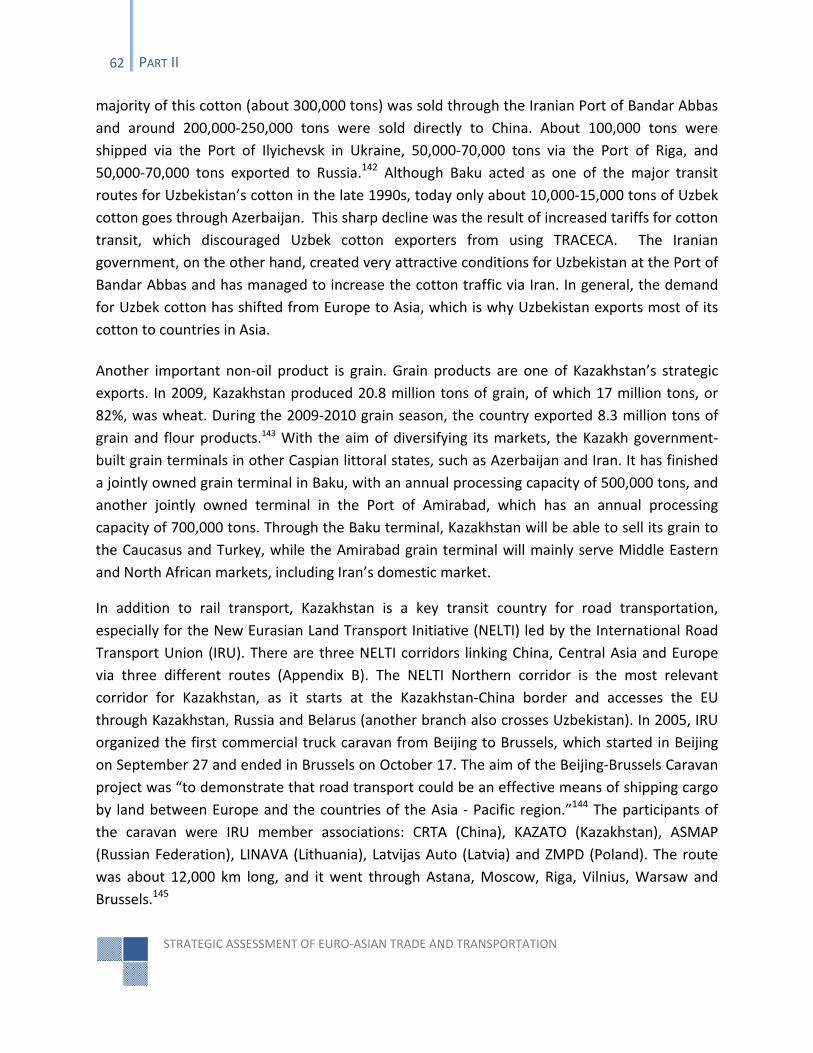

TABLE 2.9: BLOCK TRAIN OPERATION IN KAZAKHSTAN ............................................................................................................ 61

TABLE 2.10: CONTAINER SHIPMENTS FROM RIGA, LATVIA TO CENTRAL ASIA (TIME/DISTANCE) ....................................................... 61

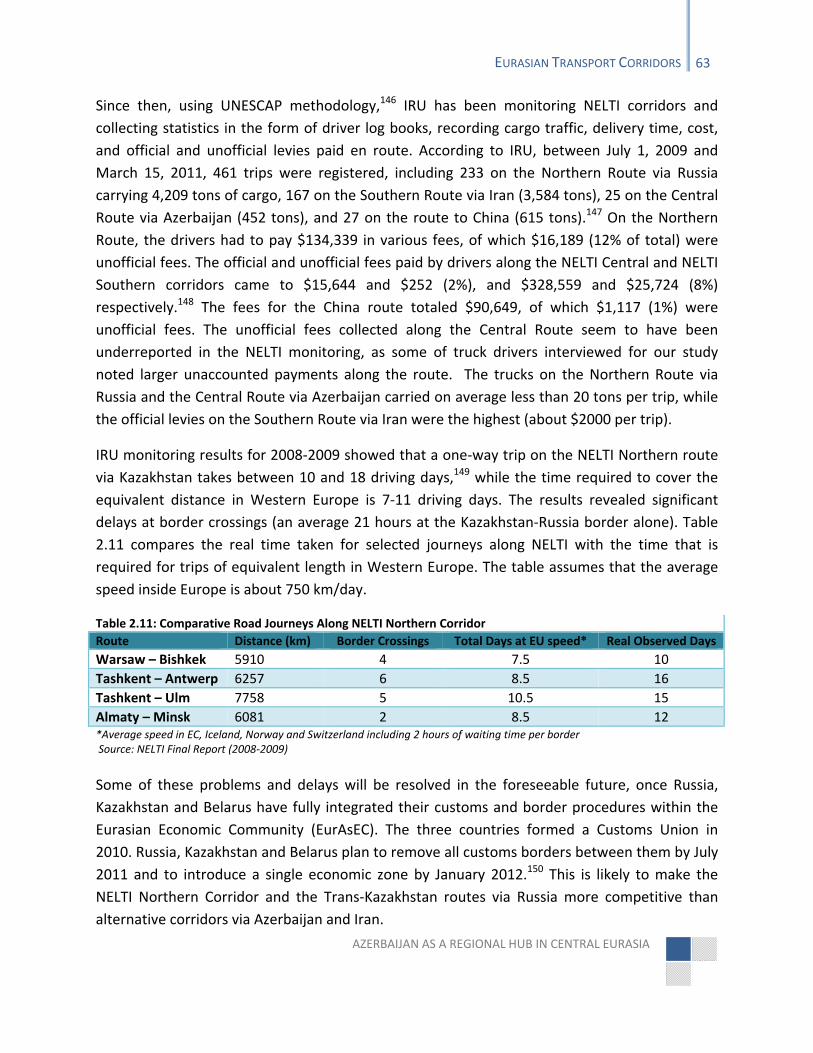

TABLE 2.11: COMPARATIVE ROAD JOURNEYS ALONG NELTI NORTHERN CORRIDOR ..................................................................... 63

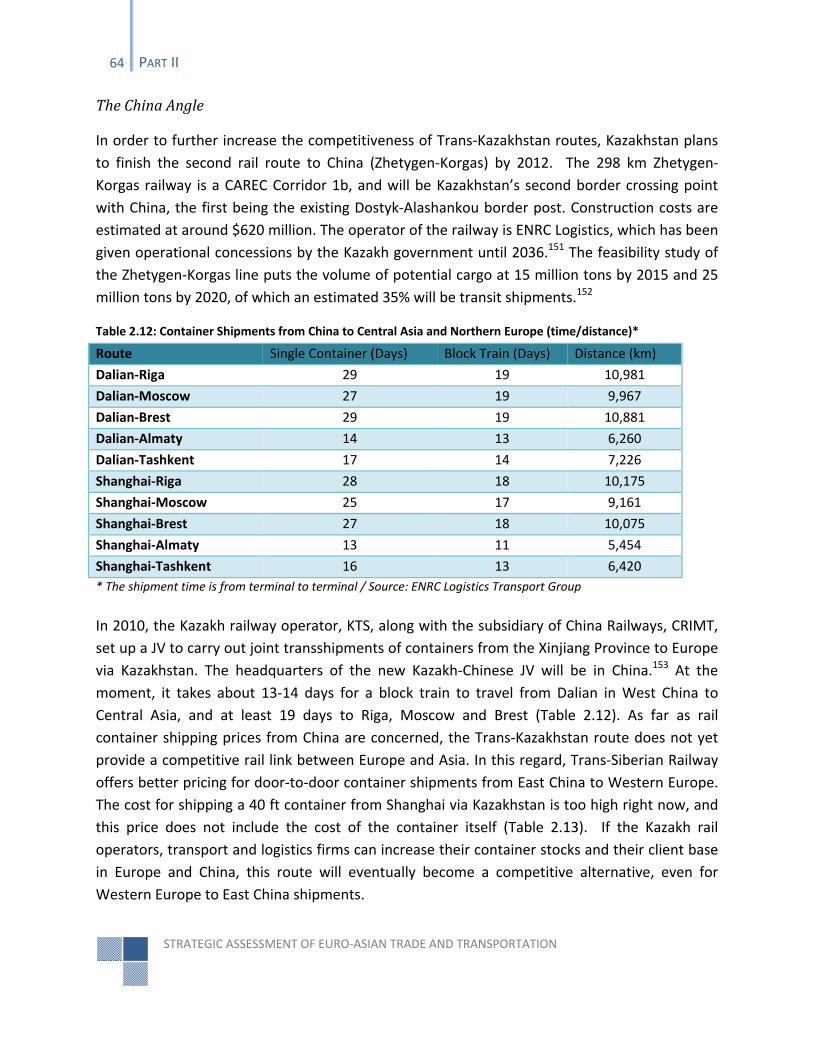

TABLE 2.12: CONTAINER SHIPMENTS FROM CHINA TO CENTRAL ASIA AND NORTHERN EUROPE (TIME/DISTANCE) .............................. 64

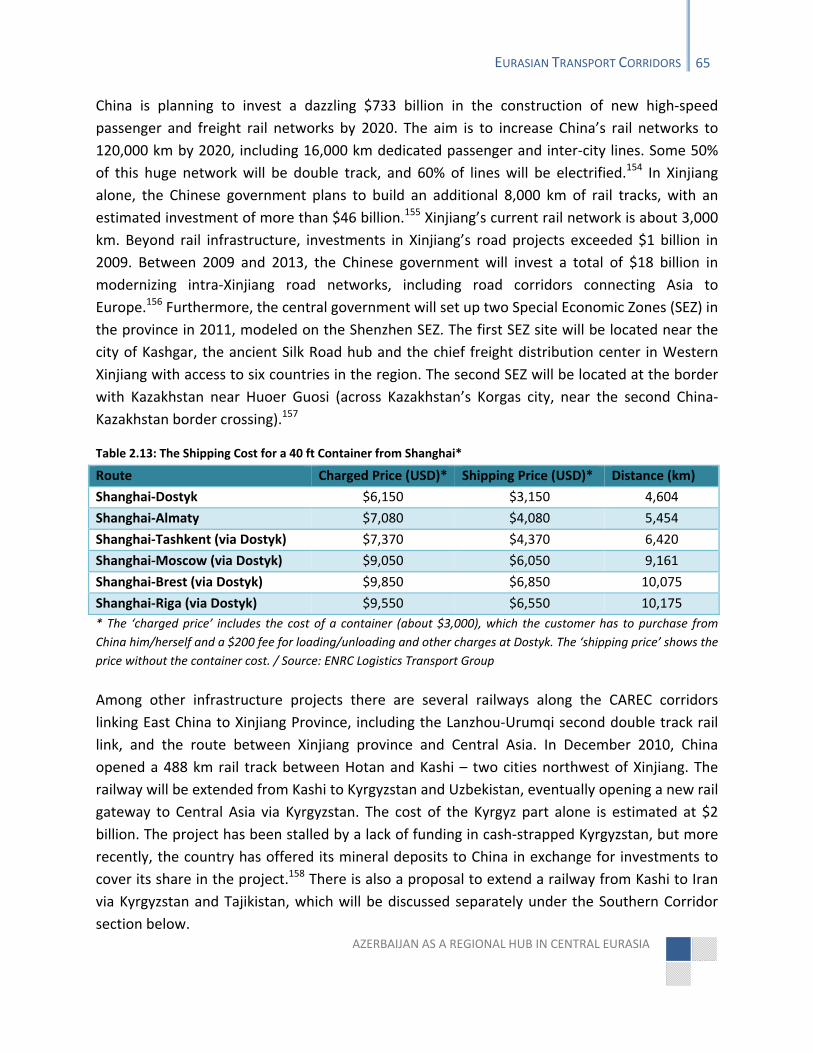

TABLE 2.13: THE SHIPPING COST FOR A 40 FT CONTAINER FROM SHANGHAI ............................................................................... 65

TABLE 2.14: IRANIAN RAIL LINES CONSTRUCTED SINCE THE 1990S ........................................................................................... 68

TABLE 2.15: NEW RAILWAYS TO BE BUILT BY CHINA ............................................................................................................... 68

TABLE 2.16: COMPARATIVE ROAD JOURNEYS ALONG NELTI SOUTHERN CORRIDOR ..................................................................... 71

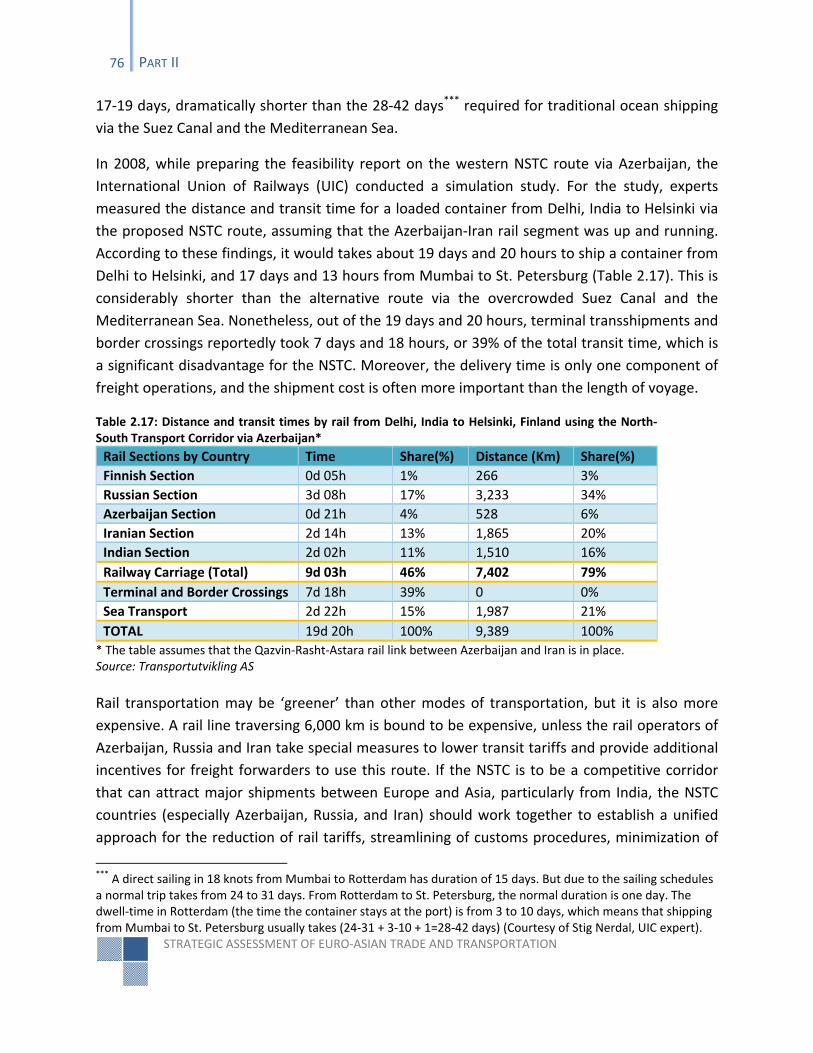

TABLE 2.17: DISTANCE AND TRANSIT TIMES BY RAIL FROM DELHI TO HELSINKI USING THE NSTC VIA AZERBAIJAN ............................... 76

TABLE 2.18: CARGO HANDLED BY TEN MAJOR CASPIAN PORTS IN 2008, 2009 AND 2010 ........................................................... 90

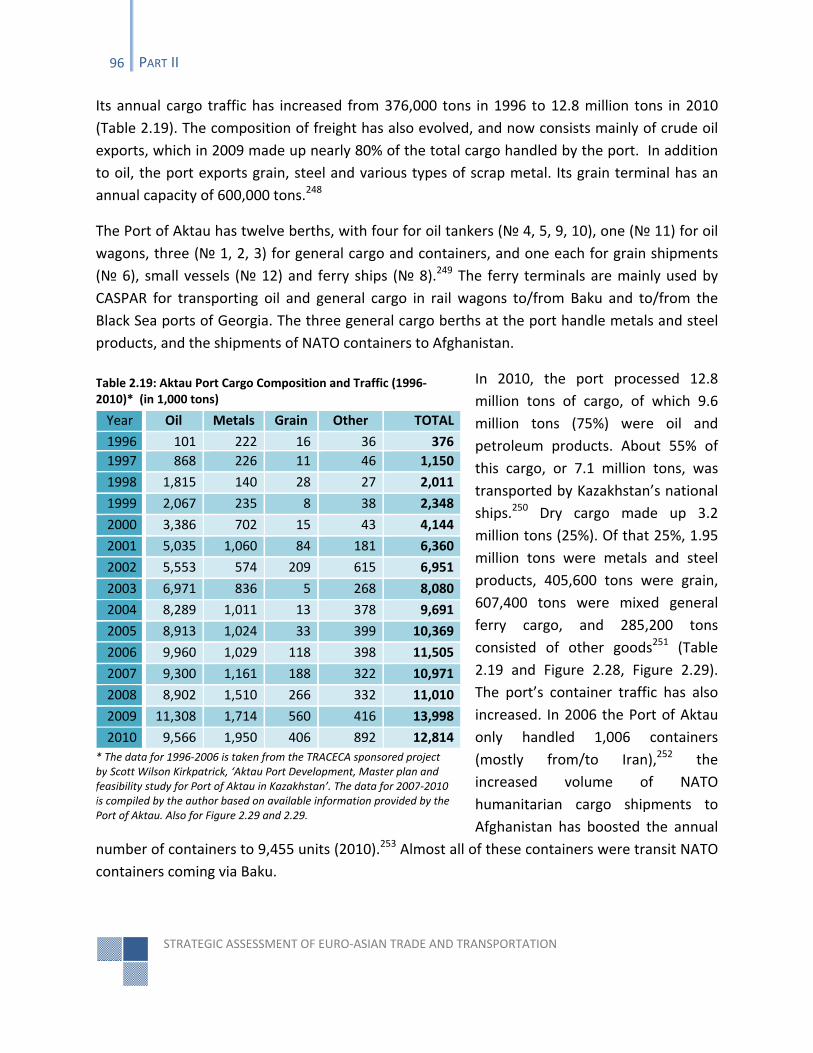

TABLE 2.19: AKTAU PORT CARGO COMPOSITION AND TRAFFIC (1996‐2010) (IN 1,000 TONS) .................................................... 96

TABLE 2.20: CARGO THROUGHPUT AT IRAN’S CASPIAN PORTS (2004‐2010) (IN TONS) ............................................................. 110

TABLE 2.21: DOMESTIC AND INTERNATIONAL TRAFFIC AT BAKU (GYD) AIRPORT (IN # OF PASSENGERS AND %) ............................... 128

TABLE 2.22: AZAL EXISTING AND PLANNED FLIGHTS ............................................................................................................. 130

TABLE 2.23: COMPARISON OF JET FUEL USAGE ON FLIGHT FROM SHANGHAI TO FRANKFURT VIA BAKU VS. DUBAI (IN TONS ) ............ 134

TABLE 2.24: DISTANCES BETWEEN MAJOR WEST EUROPEAN AND ASIAN CITIES (IN NAUTICAL MILES) ............................................ 134

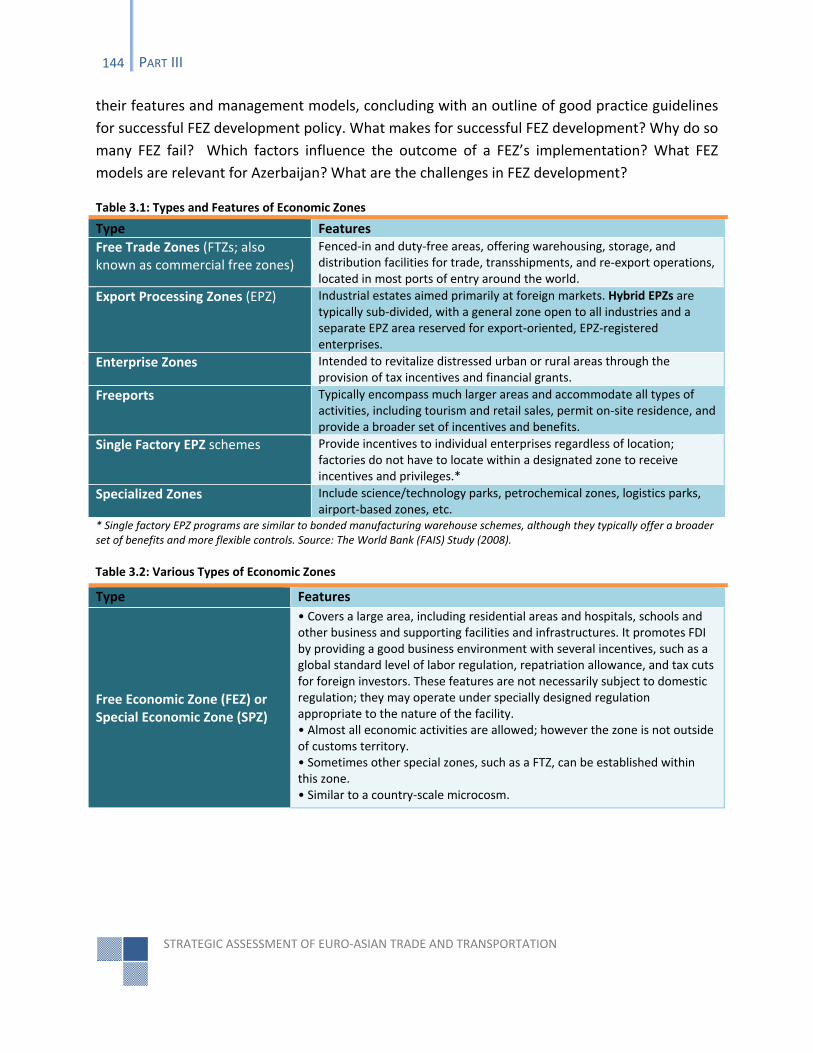

TABLE 3.1: TYPES AND FEATURES OF ECONOMIC ZONES ........................................................................................................ 144

TABLE 3.2: VARIOUS TYPES OF ECONOMIC ZONES ................................................................................................................ 144

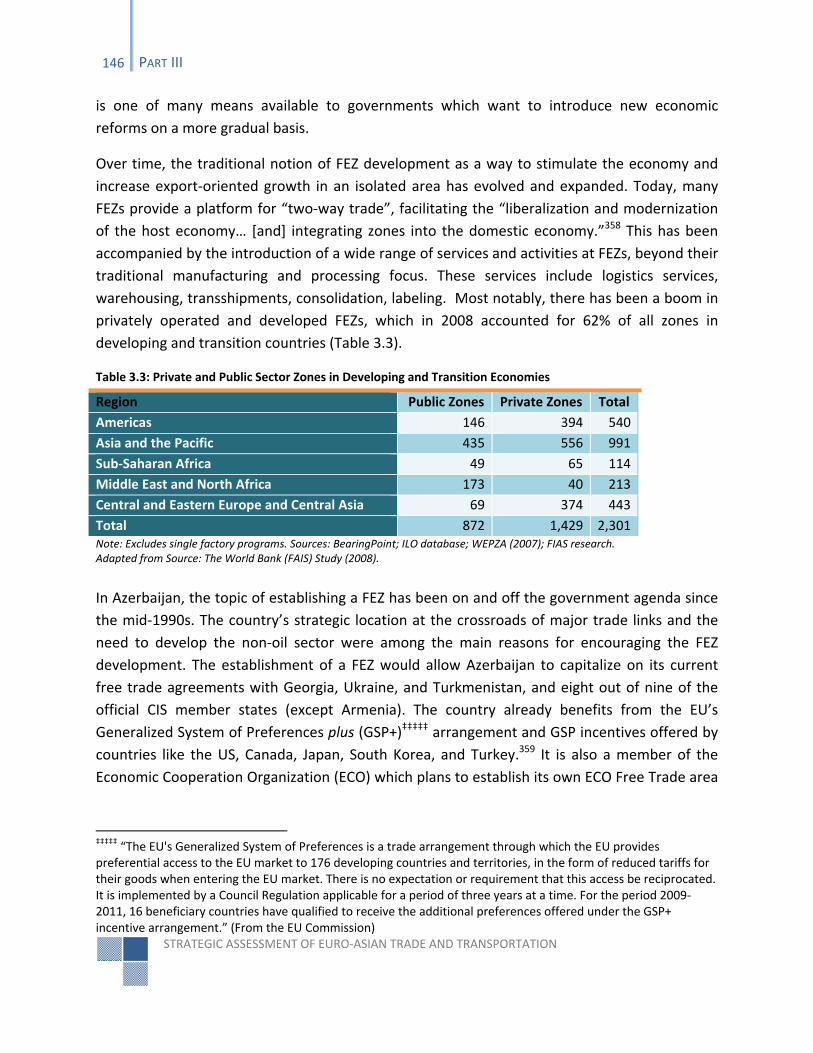

TABLE 3.3: PRIVATE AND PUBLIC SECTOR ZONES IN DEVELOPING AND TRANSITION ECONOMIES .................................................... 146

TABLE 3.4: EXAMPLES OF PUBLIC‐PRIVATE PARTNERSHIP IN ZONE DEVELOPMENT ...................................................................... 151

TABLE 3.5: BASIC PORT MANAGEMENT MODELS ................................................................................................................. 158

TABLE 3.6: STRENGTHS AND WEAKNESSES OF PORT MANAGEMENT MODELS ............................................................................ 159

TABLE 3.7: PROJECTED DEVELOPMENT OF CONTAINER PORT CAPACITY BY OWNERSHIP (2009‐2015) (MLN TEU / %) .................... 160

TABLE 3.8: TYPICAL OWNERSHIP AND OPERATING STRUCTURES IN GLOBAL CONTAINER PORT INDUSTRY ........................................ 161

TABLE 3.9 LISTS SOME EXAMPLES OF CONCESSION AGREEMENTS REACHED DURING 2009 AND 2010. ............................................ 164

TABLE 3.10: SELECTED CONCESSION ACTIVITY BY GLOBAL/INTERNATIONAL OPERATORS IN 2009/10 ............................................ 164

STRATEGIC ASSESSMENT OF EURO‐ASIAN TRADE AND TRANSPORTATION

xxiv TABLES

TABLE 3.11: TOP 25 WORLD SHIPPING LINERS (AS OF DECEMBER 31, 2010) ........................................................................... 166

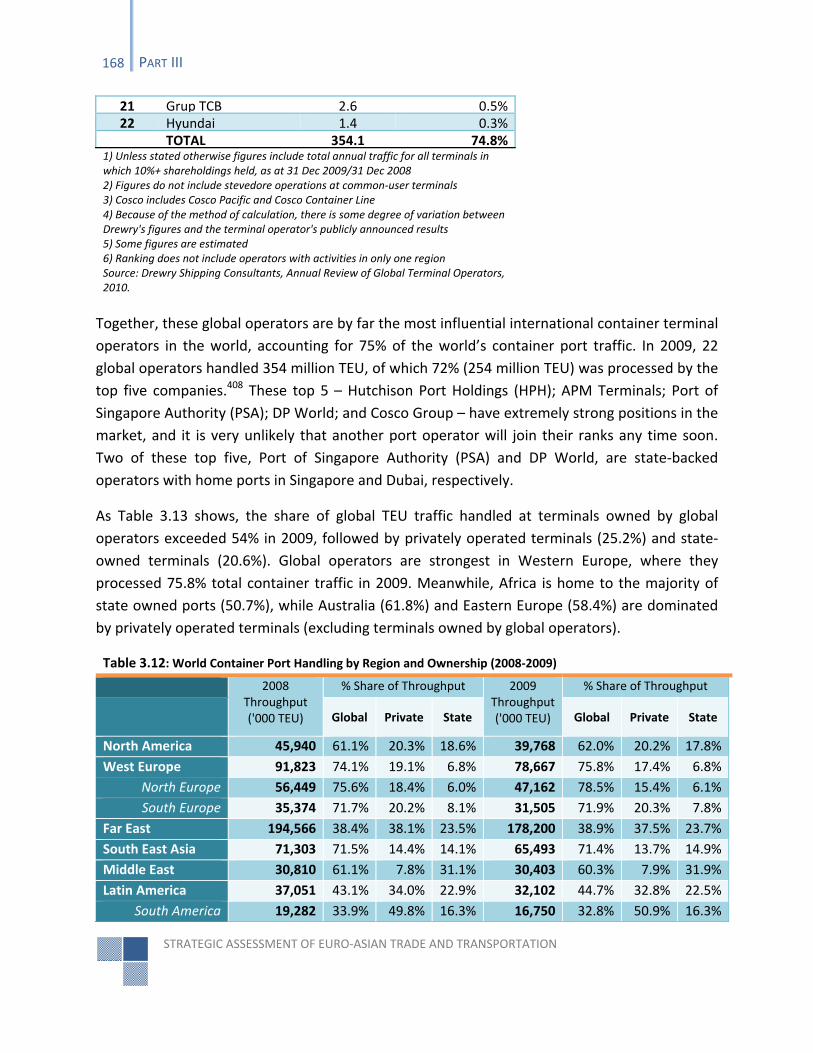

TABLE 3.12: GLOBAL OPERATORS’ THROUGHPUT LEAGUE TABLE IN 2009 ................................................................................ 167

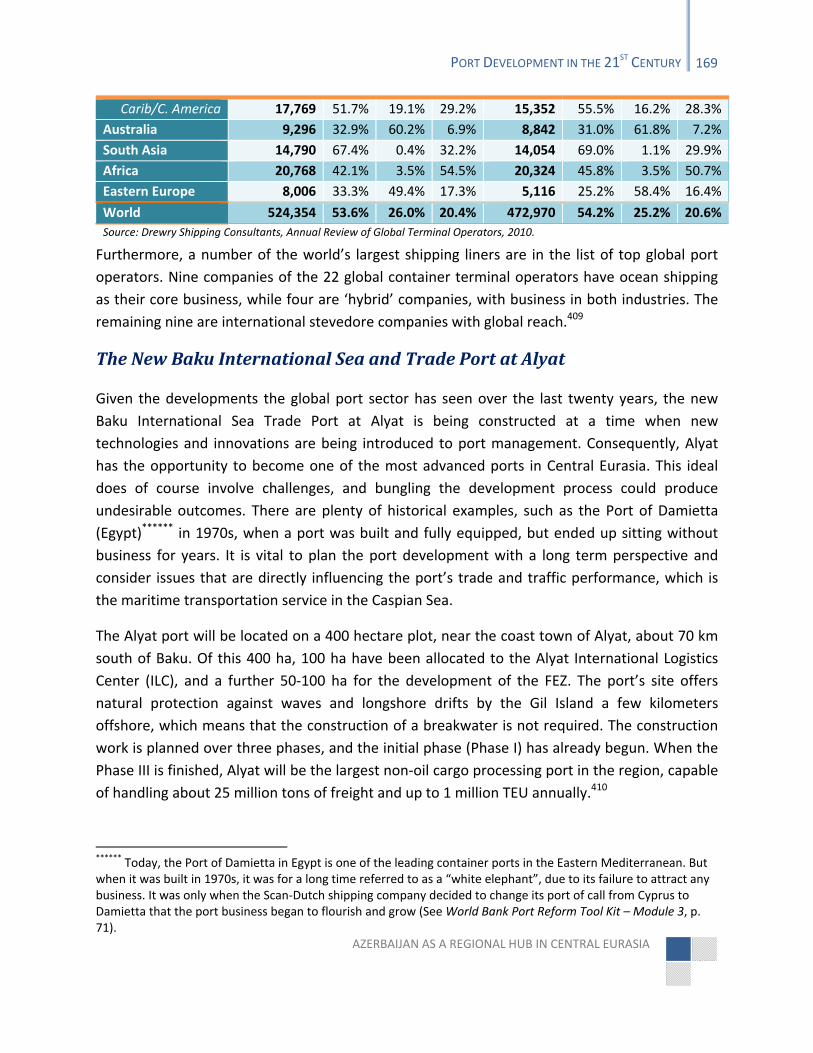

TABLE 3.13: WORLD CONTAINER PORT HANDLING BY REGION AND OWNERSHIP (2008‐2009) ................................................... 168

TABLE 3.14: BASIC FUNCTIONS OF A PORT HINTERLAND ........................................................................................................ 173

AZERBAIJAN AS A REGIONAL HUB IN CENTRAL EURASIA

INTRODUCTION

The Need for a Vision for the Future

In 1965, the late Sheikh Rashid bin Said Al‐Maktum, the visionary ruler of Dubai, asked his

British advisers to draw up a plan for the construction of a port. It took a British engineering

firm two years to complete a comprehensive master planning study for the proposed port site,

adjacent to the centuries‐old Al Shindagah neighborhood in downtown Dubai. Based on the

market assessment and future traffic forecasts, the advisers concluded that the new port would

need only four berths. Having carefully considered the proposal, Sheikh Rashid demanded that

the plan be altered to include sixteen berths instead of four. The British advisers reluctantly

complied. The port was finally opened in 1971, and all sixteen berths were oversubscribed by

the end of the first year of operation. Further expansions followed, and more berths were built

in subsequent years.1 Sheikh Rashid was convinced that Dubai was bound to become the most

important transport hub in the Middle East, and even beyond. Today, the Rashid Port, the Jabal

Ali Port and Free Zone, Dubai International Airport, and many other state‐of‐the‐art projects in

the Dubai emirate stand as testaments to Sheikh Rashid’s foresight and vision.

In a similar fashion, it was the vision of Lee Kuan Yew, one of the longest‐serving prime

ministers of the twentieth century, that transformed the tiny city‐state of Singapore from a

relatively underdeveloped former colonial settlement to a modern and competitive economy

and the major distribution hub in Southeast Asia. As early as 1973, just eight years after

independence, Singapore was being hailed as “the world’s fourth busiest port,” serving more

than 200 shipping carriers and some fifty maritime states.2 By becoming the region’s oil refining

and distribution center, Singapore managed to turn itself into an oil‐rich state even though it

was virtually devoid of any oil of its own. Capitalizing on its strategic location at the crossroads

of the major maritime routes between Europe and Asia, Lee Kuan Yew seized every opportunity

that came his way. He established an attractive business environment for foreign direct

investment (FDI) and pursued an aggressive diversification policy. Today, the country enjoys a

strong economy with a high level of FDI, and booming trade, manufacturing, and finance

sectors. In 2009, Singapore’s gross domestic product (GDP) per capita exceeded $36,000, up

from a mere $395 in 1960.3

Even though both Dubai and Singapore have undoubtedly benefited from their coastal locations

and the entrepôt trade generated by maritime traffic, the vision of their respective leaders was

essential to these cities’ resounding economic success, for without it they would be utterly

different places today. The paths taken by Sheikh Rashid in Dubai and Prime Minister Lee in

STRATEGIC ASSESSMENT OF EURO‐ASIAN TRADE AND TRANSPORTATION

2 INTRODUCTION

Singapore offer a lesson for every national leader and every country aspiring to make an

enduring mark in the world: it is necessary to possess a vision for the future.

Unlike the world’s great seaports, the prominent commercial cities of Central Eurasia have

historically been land‐based hubs. It took months and even years for the ancient Silk Road

traders to travel between Europe and Asia, and Central Eurasia’s hubs served as critical regional

logistics and distribution centers. Each of them had a number of caravanserais, where goods

and ideas exchanged hands, and people and cultures met and mixed. These trading centers

were connected with other regional hubs and megacities through a vast network of corridors

across Eurasia and the Middle East. The Silk Road corridors were for centuries the source of

prosperity for many nations in Central Eurasia.

As a result of technological advances in the twenty‐first century, Central Eurasia is poised to

regain its former prominence as a land‐based hub between Europe and Asia. By 2030, a tourist

will be able to jump on a high‐speed train in Istanbul and arrive in Baku the same day; he will

even have time to take a free bus tour of Tbilisi en route. He will continue his trip on an express

ferry to Turkmenbashy, from where another high‐speed train will take him all the way to

Urumqi in China’s Xinjiang Autonomous Region. The entire territory of Central Eurasia will be

covered with a great infrastructure of highways, railways, airports, and logistics centers that will

handle goods and passengers moving between Europe and Asia.

For many countries in Central Eurasia, however, envisioning the future is a complex matter.

Political, economic, and social crises caused by the sudden collapse of the Soviet Union have

dominated the relatively short history of independence enjoyed by these states. In 2011, they

celebrate only the twentieth anniversary of the end of Soviet rule. Memories of wars,

unresolved conflicts, economic hardships, and coups still haunt the generation old enough to

remember the days of communist control. Fortunately, the most difficult times have been left

behind, though a few crucial challenges persist. The countries of Central Eurasia are now at the

stage of development where they must complete their political and economic transitions and

choose a path that would lead them into the ranks of prosperous developed nations.

The Process of Becoming: Central Eurasia Twenty Years Later

In the 1990s, many people in the resource‐rich states of Central Eurasia, including Azerbaijan,

believed that their respective countries would soon become the “Kuwaits” and “Switzerlands”

of the twenty‐first century. The abundance of natural resources made this notion so alluring

and so palpable that few really thought about the process by which this goal would be realized,

if it were to be realized at all. Becoming another Kuwait or Switzerland would have required

AZERBAIJAN AS A REGIONAL HUB IN CENTRAL EURASIA

INTRODUCTION 3

different development strategies, with a strategic vision supported by the presence of other

essential components, such as a business friendly environment, political and economic

capabilities, the effective management of revenues from the sale of natural resource and an

advantageous location.

In the past twenty years, the regional countries, especially the resource‐rich ones, have

achieved a great deal. In 2009, the GDPs of Azerbaijan, Kazakhstan, Uzbekistan, and

Turkmenistan exceeded $43 billion, $115 billion, $32 billion, and $19 billion, respectively.4 On

the other hand, the combined GDP of the remaining four, more poorly endowed, states—

Armenia, Georgia, Kyrgyzstan, and Tajikistan—was less than $30 billion. Azerbaijan and

Kazakhstan have attracted billions of dollars in FDI and have completed key energy

infrastructure projects that guarantee their future development. A latecomer, Turkmenistan,

has started opening its doors to investors only recently, with the great expectations still to be

met. The most populous state in the region, Uzbekistan, has chosen a gradual domestic

demand‐led development path that does not seek external FDI, but it too promises to

contribute to the future hub vision of Central Eurasia.

There is no doubt that the chief engine of growth in the region has been the abundant natural

resources of Azerbaijan, Kazakhstan, Uzbekistan, and Turkmenistan. The governments of these

states, particularly Azerbaijan and Kazakhstan, have been mindful of the perils of resource

dependence and have tried to implement policies to minimize potential risks. They also have a

strategy as far as development of their energy sectors is concerned. Azerbaijan and Kazakhstan,

for example, have used Production Sharing Agreements (PSAs) to attract foreign energy

companies and inject the most needed investments into their economies. It was this energy

strategy that allowed Azerbaijan and its Western multinational partners to reach agreement on

the “Contract of the Century” in 1994 and subsequently to construct the Baku‐Tbilisi‐Ceyhan oil

pipeline in 2005 and the Baku‐Tbilisi‐Erzurum natural gas pipeline in 2006. Azerbaijan’s energy

sector alone has attracted more than $35 billion in FDI. Moreover, the revenues from these two

pipelines account for the lion’s share of the current state budget. In short, the resource‐rich

states are reaping the fruits of energy strategies they conceptualized in the 1990s.

Whether resource rich or resource poor, the countries of Central Eurasia share the same future,

and they are bound to find new synergies that will give their region a prominent place on the

economic and political map of the twenty‐first century. Indeed, each country in the region has

its own destiny, and each has reason to hope that one day it will become a prosperous and

developed state in its own right, like no other state but itself. To achieve this goal, however,

each of them would need a clear vision of itself as an individual state and also as a member of a

broader regional framework that could economically, and even politically, unite them by 2030.

STRATEGIC ASSESSMENT OF EURO‐ASIAN TRADE AND TRANSPORTATION

4 INTRODUCTION

They will have to cooperate, integrate, and adapt to the rapidly changing world around them

and forge a common vision for the years ahead. What is the common vision that one day these

mostly landlocked countries might share? Will it be a vision that will make the region a

periphery for another central power? Or a geopolitical playground for powers aiming to control

the region’s riches? Or will the ancient Silk Road be revived, with the region reclaiming its

status as a vibrant commercial hub between major economic blocs such as Europe, East Asia,

South Asia, and the Middle East? Whatever the answers to these questions, one thing is clear:

international trade will play a central role in the transformation of the region.

Azerbaijan: Potential Catalyst for Regional Dynamism

Azerbaijan is, and will remain, a pivotal state in Central Eurasia, helping to shape a common

vision for the region and facilitate its transformation. The country’s vast natural resources will

act as catalyst for developing its non‐oil economy and reviving the non‐oil trade of the region—

thus restoring Central Eurasia’s historical position as a commercial hub along the ancient Silk

Road. But for this to happen, Azerbaijan needs to formulate a comprehensive vision to guide its

development and lead it to the desired goal.

Azerbaijan is located at the crossroads of major Eurasian land and air transport corridors—a

feature that will play a vital part in its long‐term success, if utilized properly. Potentially, the

country could serve not only as a commercial bridge between Europe and Asia, but also as a

major distribution hub in Eurasia. Unlike its energy strategy, however, Azerbaijan’s vision for

development of its non‐oil economy is still a work in progress. Nearly 95% of the country’s

exports and more than 55% of GDP come from the sale of oil and natural gas—a situation that

is unlikely to change in the immediate future. The mid‐ and long‐term prospects of the country

are promising, albeit conditioned upon successful development of the non‐oil sector.

Looking Beyond Energy

Though many Azerbaijani government officials have repeatedly acknowledged that the country

is ideally situated to become a regional transportation hub between Europe and Asia, these

statements are yet to be translated into a long‐term strategic vision that is coherent and

sustainable. Nonetheless, the idea of “wanting to become a regional hub” at least is in place. In

fact, a number of transportation and infrastructure projects have already been launched to

advance this strategy. Among them is the strategic Kars‐Akhalkalaki railway, which will link the

Georgian and Turkish rail networks and thus create a rail corridor between China and Europe

via Azerbaijan. In addition, the government is investing billions of dollars in modernization of

AZERBAIJAN AS A REGIONAL HUB IN CENTRAL EURASIA

INTRODUCTION 5

the country’s international highways along the East‐West and North‐South axes in an attempt

to better prepare for anticipated land‐based traffic through Azerbaijani territory. Moreover, the

new state‐of‐the‐art Baku International Sea Trade Port and Logistics Center at Alyat and the

new Baku International Airport will both have a central place in the vision of Azerbaijan as a

global transport hub. Last, but not least, the government plans to establish Free Economic

Zones (FEZs) and invest more than $60 billion in real estate projects in and around Baku,

essentially aiming to transform the national capital into the “Dubai of the Caspian.”

These projects will genuinely strengthen Azerbaijan’s position in the region and enable it to

become a magnet for land‐ and air‐based trade between and among the states of Europe and

Asia. Baku will act as a gateway to Central Asia for Europe and a door to Europe for Central Asia

and China. It has the potential to become a “hub of hubs” on the Caspian Sea, but this will

require articulation of a clear vision today for the Azerbaijan of 2030.

The Need for an Integrated Development Strategy

Close examination of the ongoing and planned infrastructure and transportation projects in

Azerbaijan would reveal a lack of coherence in the country’s strategy for its non‐oil economy.

Important and useful projects are being planned and initiated independently of one another,

without the necessary cross‐sector and intra‐sector coordination. In other words, these projects

do not seem to be guided by a unified objective or directed by a cohesive state policy. Unless a

clear, integrated “big picture” strategy is set forth today, the development trajectory of

Azerbaijan, or of any other country in the region, for that matter, is likely to be halting and

subject to chance. This is not to say that Azerbaijan could not achieve high per capita income or

social‐welfare advancement without such a vision. The “trial and error” approach certainly

offers one type of problem‐solving strategy. But in addition to being risky, such an approach

would consume far more in terms of resources, time, and energy in the long run, and its success

would not be guaranteed.

The study you are about to read has been written in the hope of contributing to the vision of

the future of Azerbaijan. It focuses on Euro‐Asian trade, transportation and logistics, FEZ, and

port development, and draws some lessons for Azerbaijan and other countries in Central

Eurasia aspiring to become regional commercial hubs and take advantage of the growing trade

between two major economic blocs, namely Europe and Asia. In particular, it proposes a

specific development scheme for Azerbaijan’s hub strategy. As is noted throughout the study,

the opportunities for Azerbaijan are many, and the realization of this potential will benefit the

whole region, not just a single state. This means that for Azerbaijan to achieve its national

objectives, it needs to coordinate its efforts with those of neighboring countries in the region.

STRATEGIC ASSESSMENT OF EURO‐ASIAN TRADE AND TRANSPORTATION

6 INTRODUCTION

Most of the states of Central Eurasia are landlocked, and they depend on each other’s

transportation infrastructure. Building highways, railways, ports, and airports is a necessary

part of Azerbaijan’s hub strategy, but it is not a sufficient one. Without a bird’s‐eye approach

and a coherent policy, which will view all these projects as components of a single strategy, the

transportation and infrastructure projects are likely to have outcomes that will be insufficiently

efficacious, because they lack complementarity. Hence, the compartmentalized mindset has to

give way to an integrated vision that will direct each project towards a common goal.

An Overview of the Study

Part I of the present study will give a brief overview of the structure of the Euro‐Asian trade and

its major players and the means through which this trade is conducted. In particular, it looks at

the European Union’s commercial relations with a number of Asian states relevant to the future

hub strategy of Central Eurasia.

Part II assesses the current state of affairs in the transportation, infrastructure, and logistics

sectors of Azerbaijan and Central Eurasia. It illuminates a number of challenges in these sectors

and points to current and potential competition between the Euro‐Asian transport corridors

that bypass Azerbaijan and the Transport Corridor Europe‐Caucasus‐Asia (TRACECA), which

transits the country. In particular, it highlights the importance of establishing an effective trans‐

Caspian maritime transportation system, which is essential to the success of TRACECA. Part II

also stresses the importance of creating a well‐connected national and regional logistics

network and supply chain that will connect the nodes in the global land‐ and air‐based supply

chain via Azerbaijan.

Becoming a transportation and transit hub will not be sufficient for the successful development

of Azerbaijan as a non‐oil economy. Hence Part III discusses the FEZ and port development in

general and identifies best practices that could be applied in Azerbaijan and could help

establish a competitive and sustainable non‐oil sector. A gradual approach to implementing the

hub vision is advocated, one that entails focusing on two projects within the context of the FEZ

concept: the new Baku International Sea Trade Port and Logistics Center FEZ at Alyat and the

Baku International Airport FEZ.

The core of a successful hub strategy for Azerbaijan must include FEZ development within a

PSA‐type legal framework, as only under such an arrangement can Azerbaijan generate trade

and attract FDI on a level that could make a lasting difference in the non‐oil economy. This

specific vision is outlined in detail in Part IV.

AZERBAIJAN AS A REGIONAL HUB IN CENTRAL EURASIA

PART I

EURO‐ASIAN TRADE: THE BIG PICTURE

AZERBAIJAN AS A REGIONAL HUB IN CENTRAL EURASIA

1. THE EUROASIAN TRADE AND CENTRAL EURASIA

The countries of Central Eurasia have always acted as a land bridge along the major commercial

routes between Europe and Asia. The Silk Road trade brought wealth and prosperity to the

region’s inhabitants at different stages in history. The exchange of goods introduced new ideas

and technologies, enriching and advancing the development of these societies. The disruption

of the ancient trade routes, however, brought suffering and hardship to the region with long‐

lasting impact. Some regions were gradually able to recover, while others never did. Over time,

a number of commercial cities faded away as they lost the prominence they once held in the

Silk Road trade, and new vibrant megacities emerged in their places. Euro‐Asian trade was the

economic backbone of Central Eurasia for centuries.

Today, the majority of this trade bypasses the region, and so do the attendant benefits. Large

ships that can carry thousands of containers at a time have replaced the ancient caravans of the

Silk Road. Most of the trade between Europe and Asia is conducted by maritime transportation

via Suez Canal, which makes up more than 90% of total cargo exchanged between the two

continents. The success of Central Eurasian hub strategy largely depends on the ability of the

regional states to attract some of this Euro‐Asian continental container trade by creating

integrated and competitive intermodal transportation and logistics networks across Eurasia.

An assessment of the potential impact of land‐ and air‐based Euro‐Asian commerce on the

countries of Central Eurasia requires an analysis of its current structure. A closer look at Euro‐

Asian trade exposes a number of opportunities for the region, including Azerbaijan, and reveals

issues and challenges associated with attracting this commerce. This section will examine Euro‐

Asian trade and its structure in attempt to reveal the bigger picture: whether or not this trade

has prospects and whether Central Eurasia can benefit and once again become a conduit, which

would allow it to regain its historical position as a commercial hub between Europe and Asia.

The EuroAsian Trade: Overview*

Since the sharp decline in 2009, world trade has bounced back, with a record‐high 14.5%

increase in the volume of exports in 2010.5 The highest ever surge in the volume of exports was

recorded in developing economies and the Commonwealth of Independent States (CIS), which

together made up of 45% of all exports in 2010. The Asian economies, led by China and Japan,

saw the fastest real export growth with 23.1%. The world merchandise exports rose from $12.5

trillion in 2009 to $15.2 trillion in 2010 (up 22%), while exports of commercial services

* The statistical data used in this section is drawn primarily from the World Trade Organizations (WTO) and European Commission’s Eurostat databases, unless indicated otherwise.

STRATEGIC ASSESSMENT OF EURO‐ASIAN TRADE AND TRANSPORTATION

10 PART I

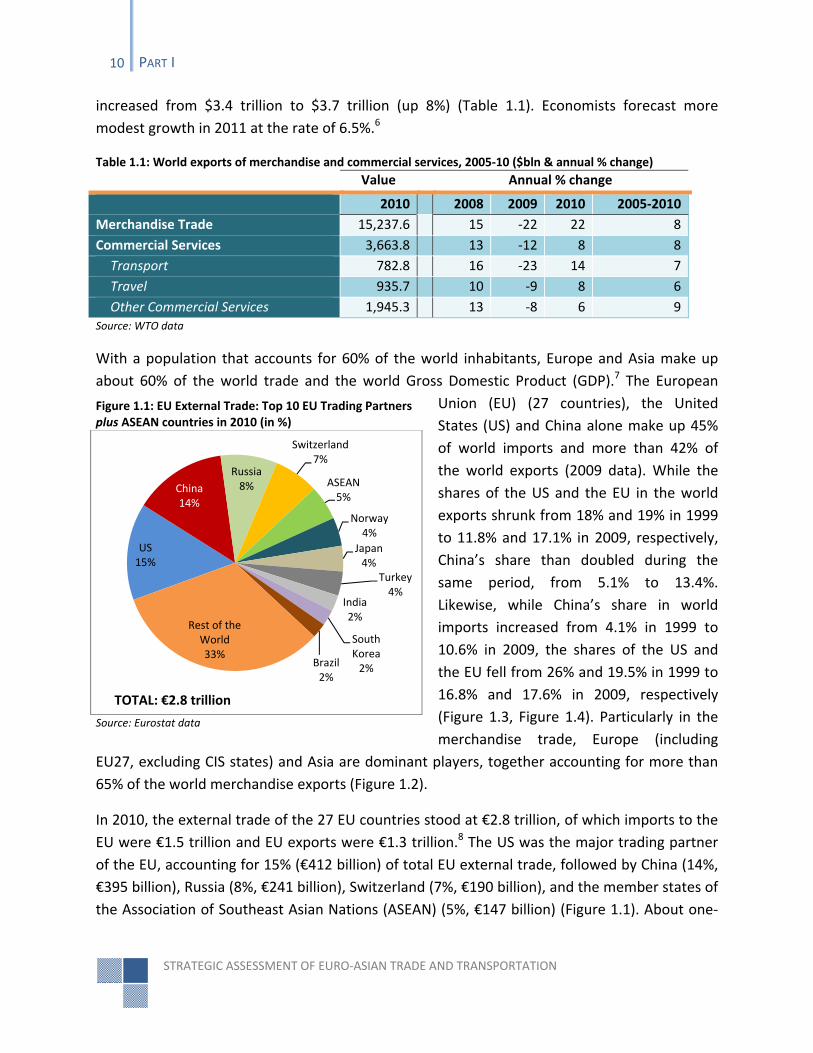

increased from $3.4 trillion to $3.7 trillion (up 8%) (Table 1.1). Economists forecast more

modest growth in 2011 at the rate of 6.5%.6

Value Annual % change

2010 2008 2009 2010 2005‐2010

Merchandise Trade 15,237.6 15 ‐22 22 8

Commercial Services 3,663.8 13 ‐12 8 8

Transport 782.8 16 ‐23 14 7

Travel 935.7 10 ‐9 8 6

Other Commercial Services 1,945.3 13 ‐8 6 9Source: WTO data

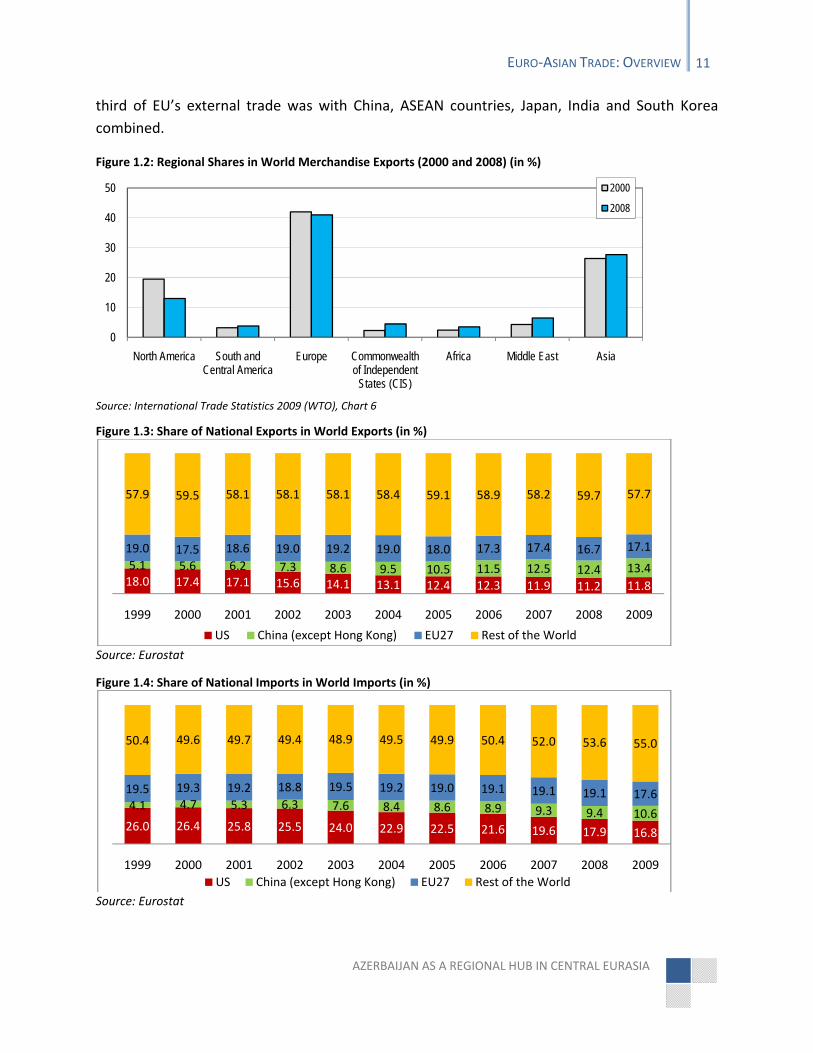

With a population that accounts for 60% of the world inhabitants, Europe and Asia make up

about 60% of the world trade and the world Gross Domestic Product (GDP).7 The European

Union (EU) (27 countries), the United

States (US) and China alone make up 45%

of world imports and more than 42% of

the world exports (2009 data). While the

shares of the US and the EU in the world

exports shrunk from 18% and 19% in 1999

to 11.8% and 17.1% in 2009, respectively,

China’s share than doubled during the

same period, from 5.1% to 13.4%.

Likewise, while China’s share in world

imports increased from 4.1% in 1999 to

10.6% in 2009, the shares of the US and

the EU fell from 26% and 19.5% in 1999 to

16.8% and 17.6% in 2009, respectively

(Figure 1.3, Figure 1.4). Particularly in the

merchandise trade, Europe (including

EU27, excluding CIS states) and Asia are dominant players, together accounting for more than

65% of the world merchandise exports (Figure 1.2).