33

Strategy as Revolution James Oldroyd Kellogg Graduate School of Management Northwestern University [email protected] 801-422-7888 650 TNRB

| Date post: | 24-Dec-2015 |

| Category: |

Documents |

| Upload: | alexia-watkins |

| View: | 216 times |

| Download: | 1 times |

Strategy as Revolution

James OldroydKellogg Graduate School of ManagementNorthwestern University

[email protected] TNRB

2

Stock Performance

Radically Improving the Value Equation

Reconfigure the Value Chain and employ a completely new/different value chain

Value for Whom?

4

Separate Form and Function

Finding new uses for existing technologies

Credit Cards turned to hotel keys

5

Achieving Joy of Use

Products – services should be fun to use

6

Pushing the Bounds of Universality

Focus not only on the served market but on the entire imaginable market

http://www.polaroid.com/promotions/promo.jsp?FOLDER%3C%3Efolder_id=385651&FOLDER%3C%3EbrowsePath=385651&PRODUCT%3C%3Eprd_id=31111&PRDREG=

POL&bmLocale=en_US&bmUID=1017153506454

7

Striving for Individuality

Mass Customization/Striving for Individuality

http://www.us.levi.com/fal02a/levi/ospin/l_ospin_frame.jsp?FOLDER%3C%3Efolder_id=2357089&bmUID=1026829418909

8

Increase Accessibility

24/7365

Banking, Retail

9

Rescaling the Industry

Re-scale the Industry• Increasing scale, from local to national or

national to global (e.g., IKEA, Service Corporation [funerals] International)

• Downscaling to serve narrow or local customer segments (e.g., microbreweries, local bakeries, bed-breakfast inns).

PFIZER TO ACQUIRE PHARMACIA CORPORATION FOR $60 BILLION IN STOCK,

STRATEGICALLY POSITIONING COMPANY FOR LONG-TERM LEADERSHIP IN RAPIDLY

CHANGING PHARMACEUTICAL INDUSTRY

10

Licensee

Licensee

Licensee

Licensee

Intel IBM

PC Mfr

PC Mfr

PC Mfr

PC Mfr

PC Mfr

Structure of Microprocessor Market Before and After the 386

11

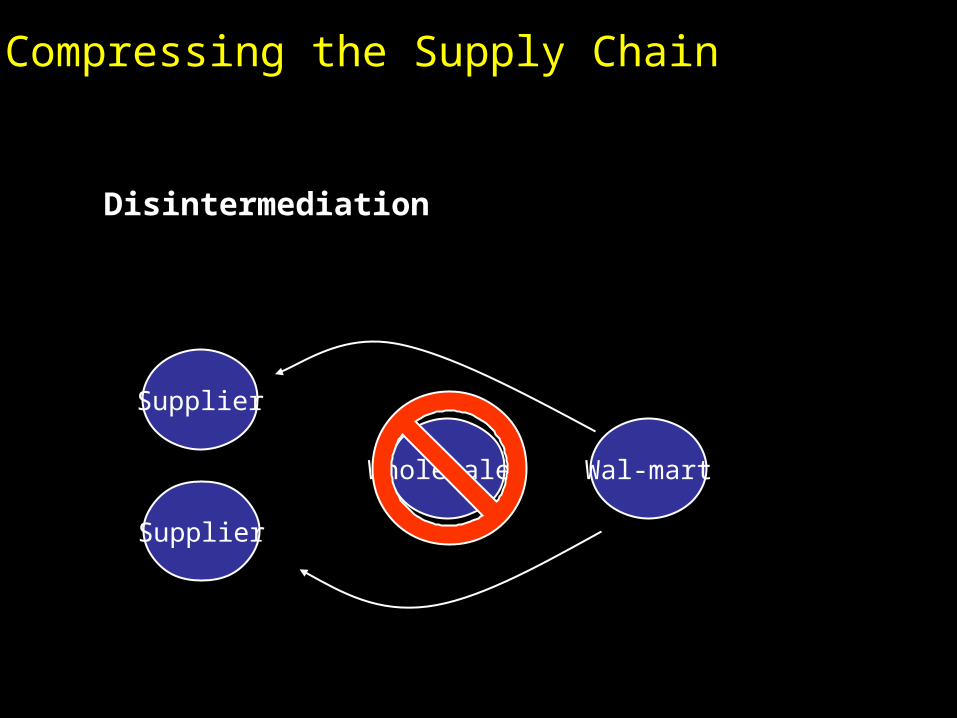

Compressing the Supply Chain

Disintermediation

Supplier

Supplier

Wholesaler Wal-mart

12

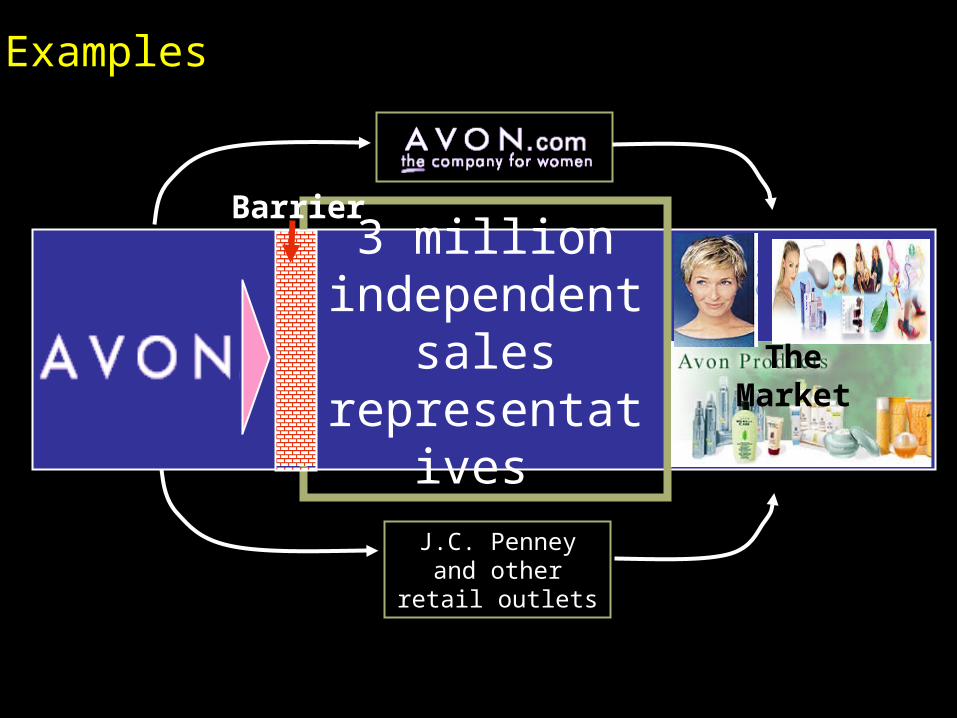

Examples

3 million independent

sales representatives

J.C. Penney and other retail outlets

The Market

Barrier

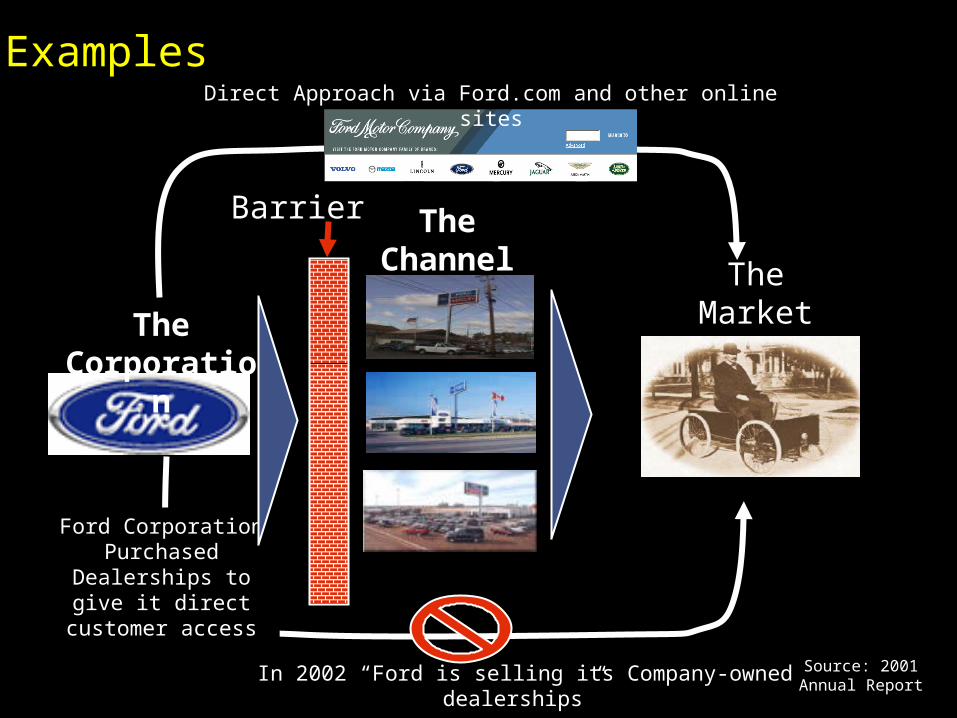

13

The Corporation

The Channel The

Market

Barrier

Ford Corporation Purchased

Dealerships to give it direct customer

access

In 2002 “Ford is selling its Company-owned dealerships” Source: 2001 Annual Report

Direct Approach via Ford.com and other online sites

Examples

14

Online access to account information– Account activity & balances– Portfolio holdings

Online access to Merrill Lynch research

Ability to e-mail with financial consultant

Online bill payment capabilities

Access to Merrill Lynch analytical tools

Ability to execute trades

Source: ml.com

Brokers The Market

ml.com

Merrill Lynch sought to involve brokers in the online process

to minimize dissatisfaction

Examples

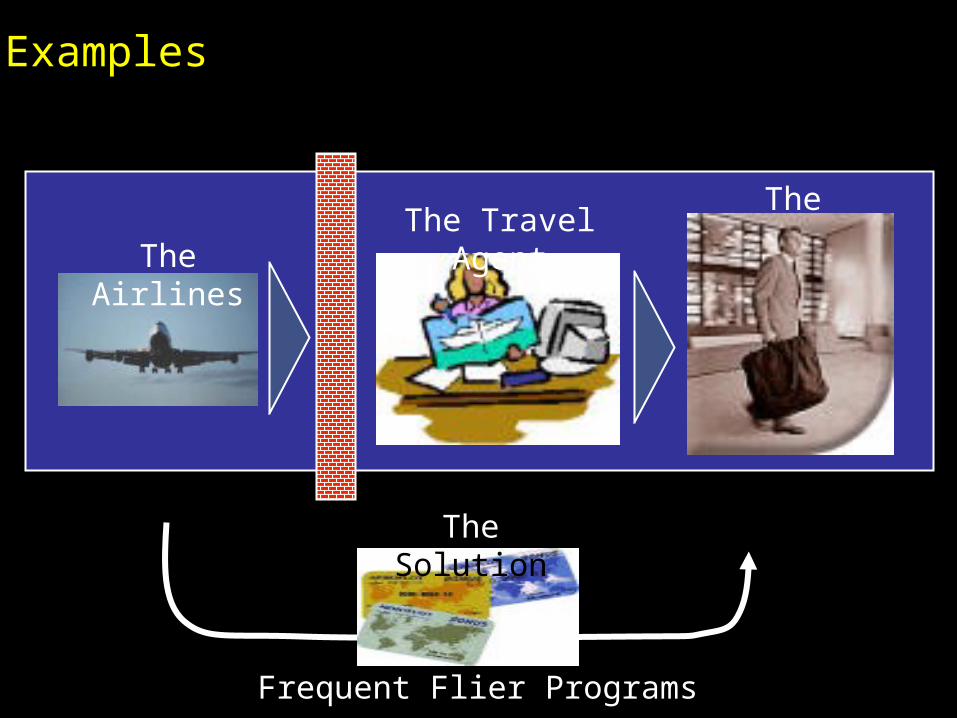

15

The MarketThe Travel Agent

The Airlines

The Solution

Frequent Flier Programs

Examples

16

Driving Convergence

Product/Service Bundling • Offer broader mix of related products along the

value chain beyond “core” product (e.g., software office suites, GM car loans/leasing)

• Swimming in other industry pools

17

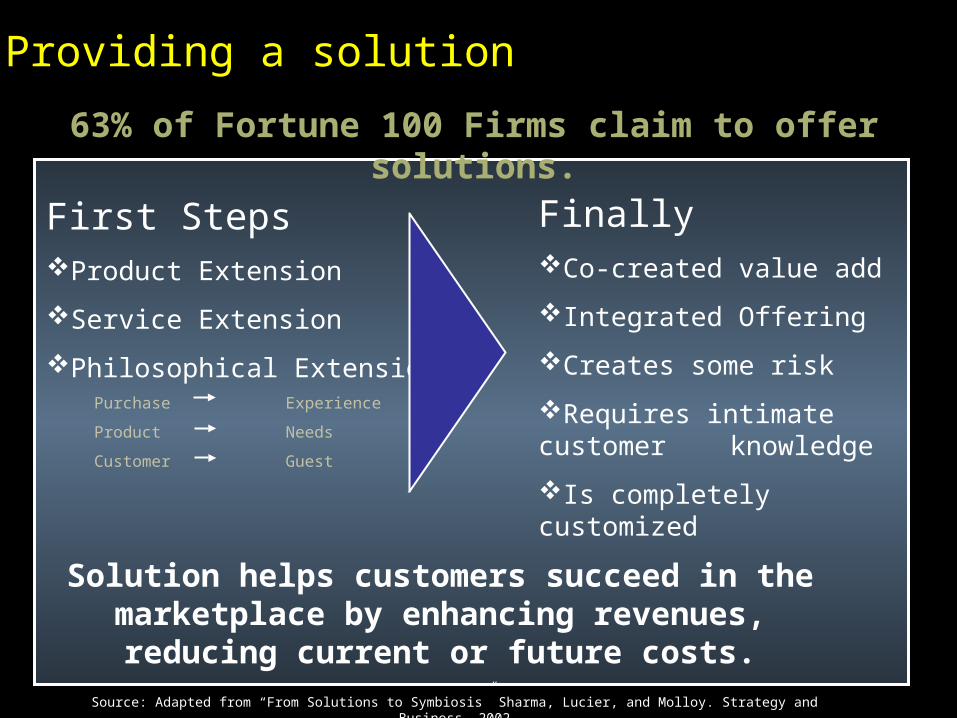

Providing a solution

First StepsProduct Extension

Service Extension

Philosophical ExtensionPurchase Experience

Product Needs

Customer Guest

63% of Fortune 100 Firms claim to offer solutions.

Solution helps customers succeed in the marketplace by enhancing revenues, reducing

current or future costs.

FinallyCo-created value add

Integrated Offering

Creates some risk

Requires intimate customer knowledge

Is completely customized

Source: Adapted from “From Solutions to Symbiosis” Sharma, Lucier, and Molloy. Strategy and Business, 2002

18

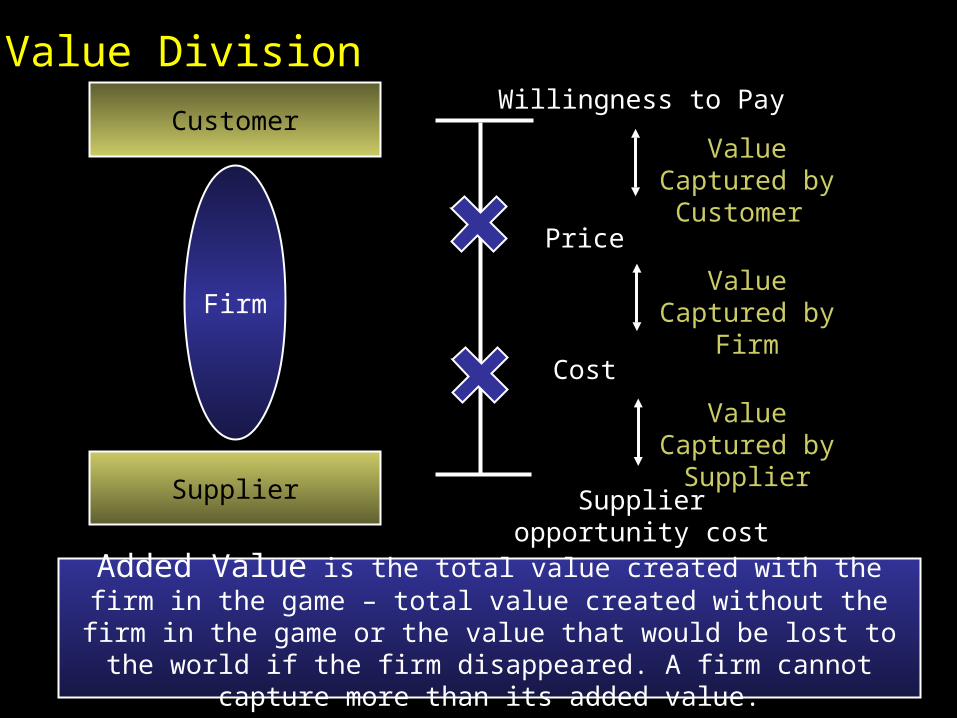

Value Division

Customer

Supplier

Firm

Willingness to Pay

Supplier opportunity cost

Cost

Price

Value Captured by Customer

Value Captured by Firm

Value Captured by Supplier

Added Value is the total value created with the firm in the game – total value created without the firm in the game or the value that would be lost to the world if the firm disappeared. A firm cannot capture more

than its added value.

19

The Opportunity and Threatof Disruptive Technologies

Clayton M. ChristensenHarvard Business School

20

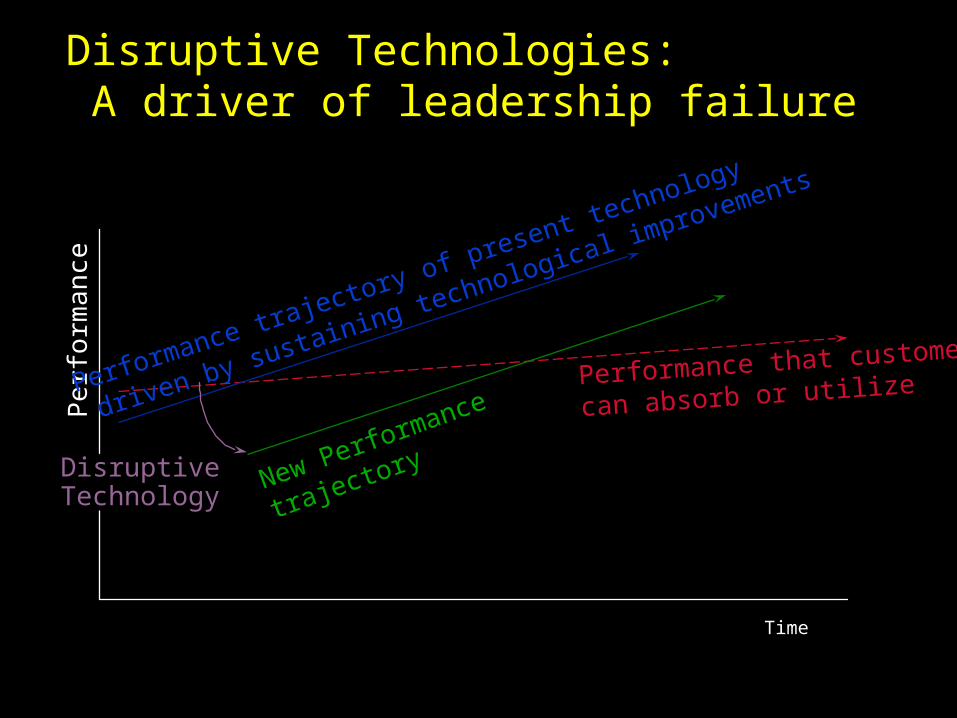

Disruptive Technologies: A driver of leadership failure

Performance that customers

can absorb or utilize

New Performance

trajectory

Per

form

ance

Time

DisruptiveTechnology

Performance trajectory of present technology

driven by sustaining technological improvements

21

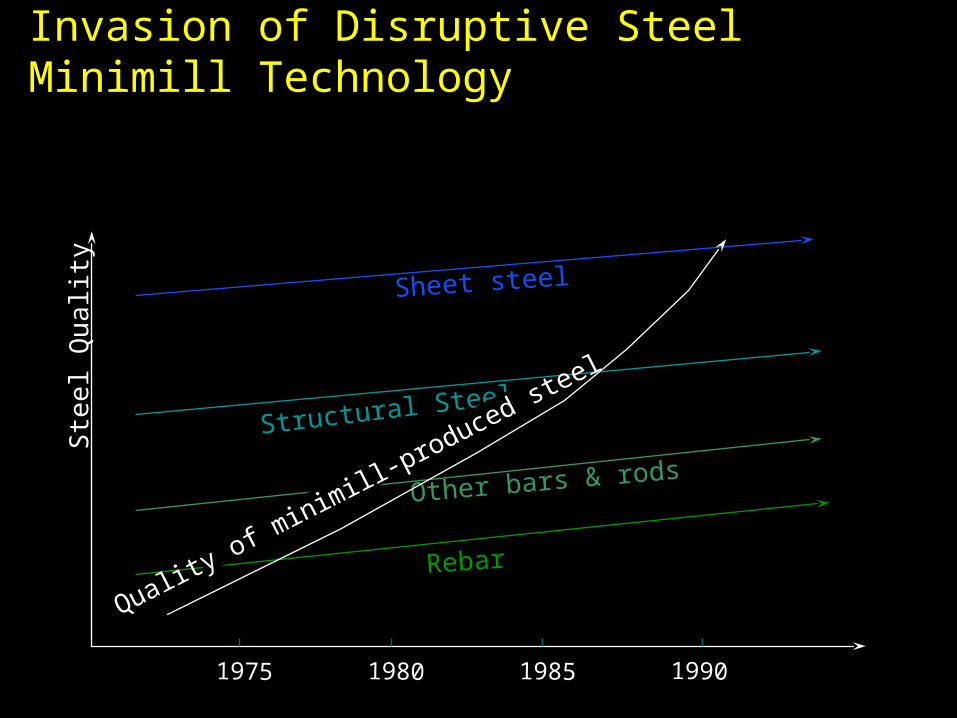

Invasion of Disruptive Steel Minimill Technology

Rebar

Other bars & rods

Structural Steel

Sheet steel

Ste

el Q

ualit

y

1975 1980 1985 1990

Quality of m

inimill-produced ste

el

22

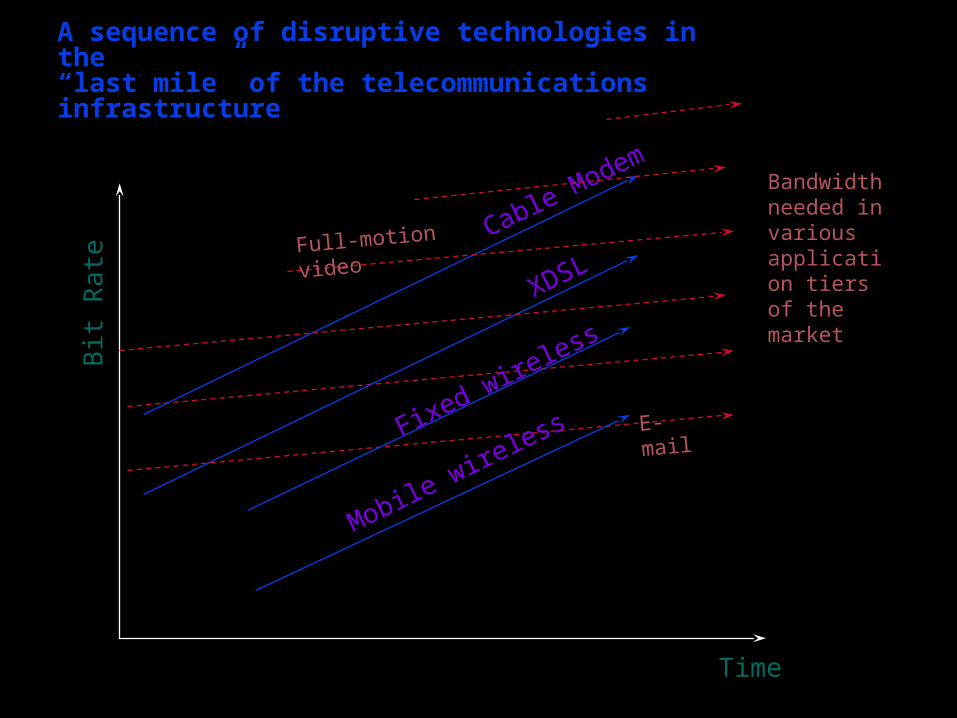

XDSL

Bit

Rat

e

Time

Cable Modem

Fixed wireless

Mobile wireless

Bandwidth needed in various application tiers of the market

Full-motion video

A sequence of disruptive technologies in the“last mile” of the telecommunicationsinfrastructure

23

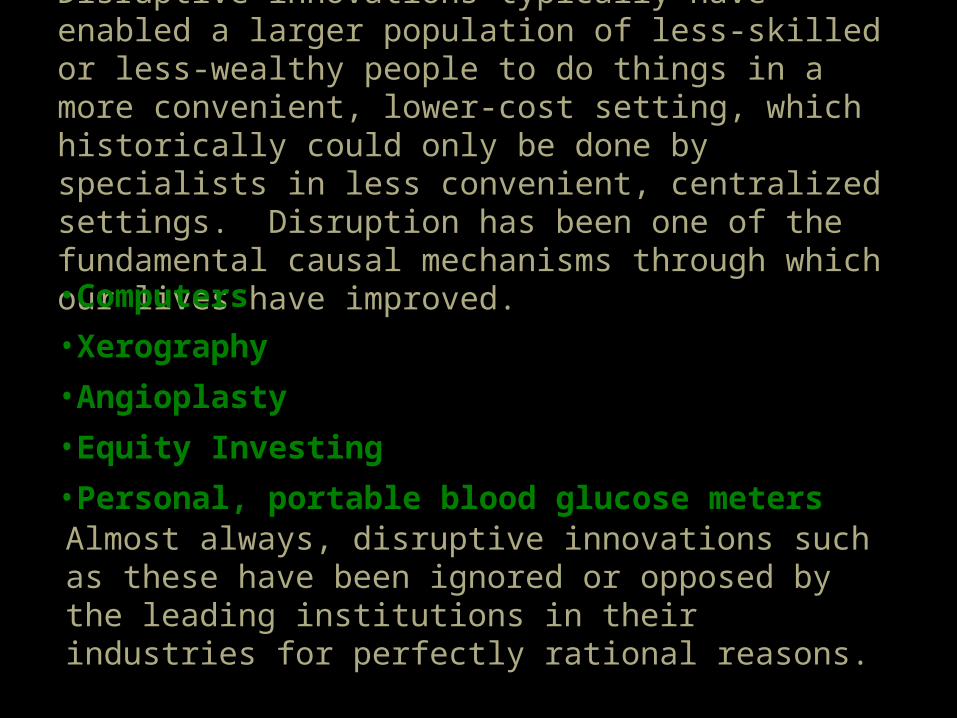

Disruptive innovations typically have enabled a larger population of less-skilled or less-wealthy people to do things in a more convenient, lower-cost setting, which historically could only be done by specialists in less convenient, centralized settings. Disruption has been one of the fundamental causal mechanisms through which our lives have improved.

•Computers

•Xerography

•Angioplasty

•Equity Investing

•Personal, portable blood glucose meters

Almost always, disruptive innovations such as these have been ignored or opposed by the leading institutions in their industries for perfectly rational reasons.

24

Many of our Economy’s Greatest Companies Began as Disruptive Innovators

Intel

Sun Microsystems

Compaq

Dell

EMC

Microsoft

Nucor

Merrill Lynch

Charles Schwab

Bloomberg

AT&T

Cisco

Sprint PCS

Nokia

Toyota

Honda

Sony

Barnes & Noble

Amazon

Sears

Wal-Mart

Established firms seem instinctively to force disruptive technologies into existing markets and business models.

Major Established Electronics Markets:

Tabletop radios, floor-standing televisions,

computers, telecomm. equipment, etc.

Path taken byestablished vacuumtube manufacturers

Disruptive Technology: Transistors vs. Vacuum Tubes

Hearing Aids

Path taken byentrant firms

Portable Radios &Televisions, etc.

26

What Is Digital Photography?

PresentApplications for

Silver HalideFilm Technology

ASustaining

Technology?

Enabling Technologies: CCDs, Ink Jet Printing, CMOS Sensors

Children’s Games

Professional /Archival

Recreational

ADisruptive

Technology?

A MajorGrowth

Opportunity?

27

Disruptions amongst health care professionals

Performance thatthe marketplaceneeds or utilizes

Com

plex

ity

of d

iagn

osis

& tr

eatm

ent

Time

Specialist & sub-specialist p

hysicians

Nurse practitioners

Self-care

Family / personal care physicians

28

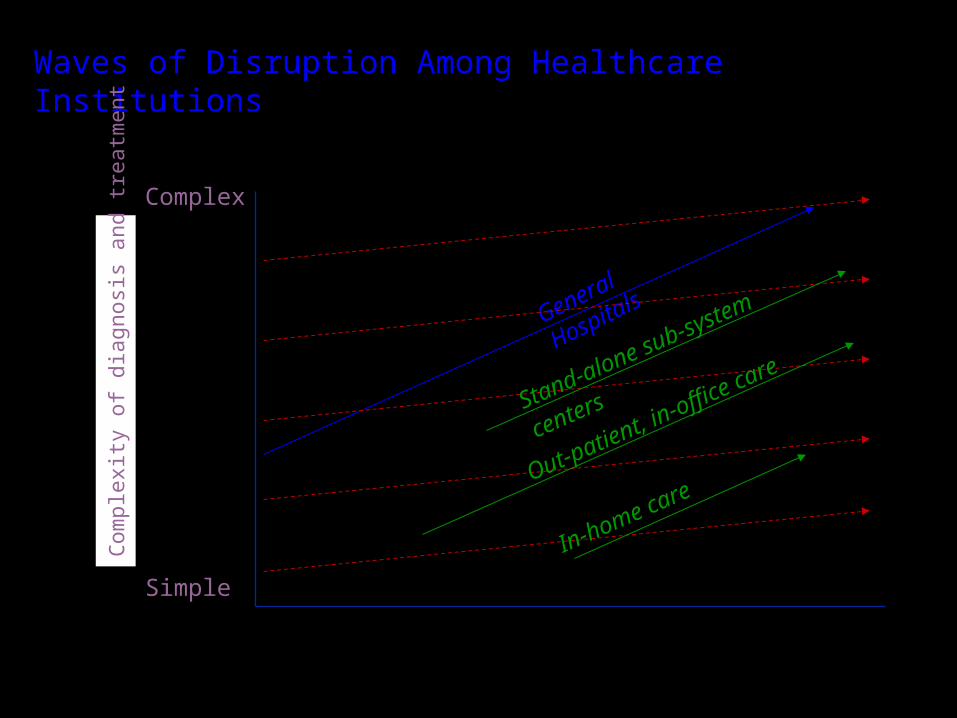

Waves of Disruption Among Healthcare Institutions

General Hospitals

Com

plex

ity

of d

iagn

osis

and

trea

tmen

t

Stand-alone sub-system centers

Complex

Simple

Out-patient, in-office care

In-home care

What Would Have to Happen for the Electric Vehicle to Be a Disruptive Technology?

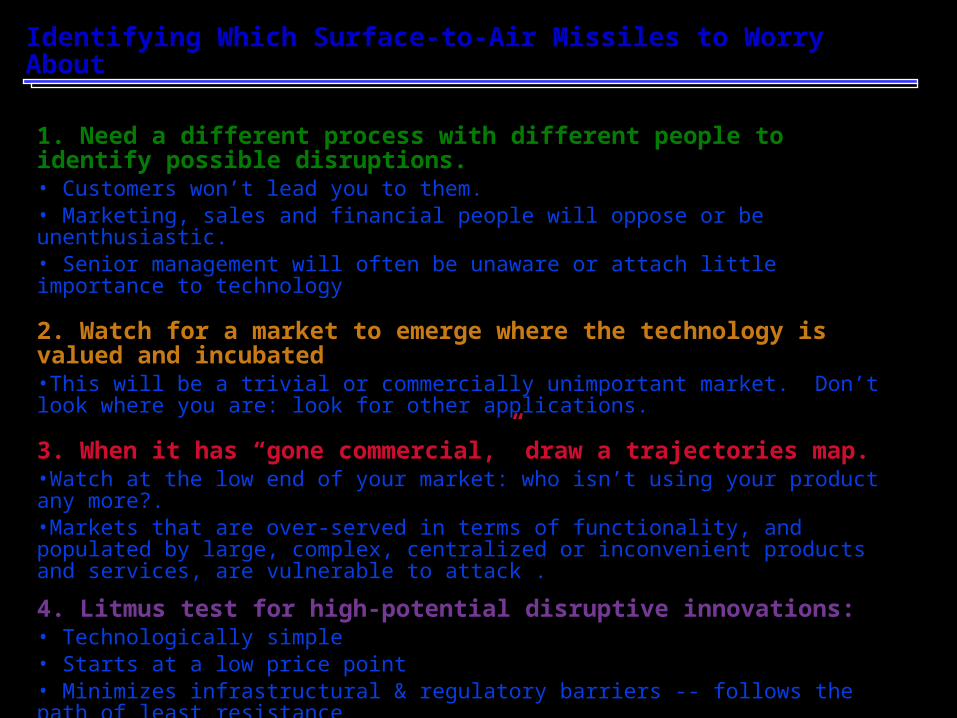

Identifying Which Surface-to-Air Missiles to Worry About

1. Need a different process with different people to identify possible disruptions.• Customers won’t lead you to them.• Marketing, sales and financial people will oppose or be unenthusiastic.• Senior management will often be unaware or attach little importance to technology

2. Watch for a market to emerge where the technology is valued and incubated•This will be a trivial or commercially unimportant market. Don’t look where you are: look for other applications.

3. When it has “gone commercial,” draw a trajectories map. •Watch at the low end of your market: who isn’t using your product any more?.•Markets that are over-served in terms of functionality, and populated by large, complex, centralized or inconvenient products and services, are vulnerable to attack .

4. Litmus test for high-potential disruptive innovations:• Technologically simple• Starts at a low price point• Minimizes infrastructural & regulatory barriers -- follows the path of least resistance• Success isn’t predicated upon customers’ behavioral change• Enables a larger population of less-skilled people to conveniently do something that only expensive specialists historically could do.

31

Region B:

Modular Architectures

Region A: Integral A

rchitectures

Per

form

ance

Time

Sustaining Technology

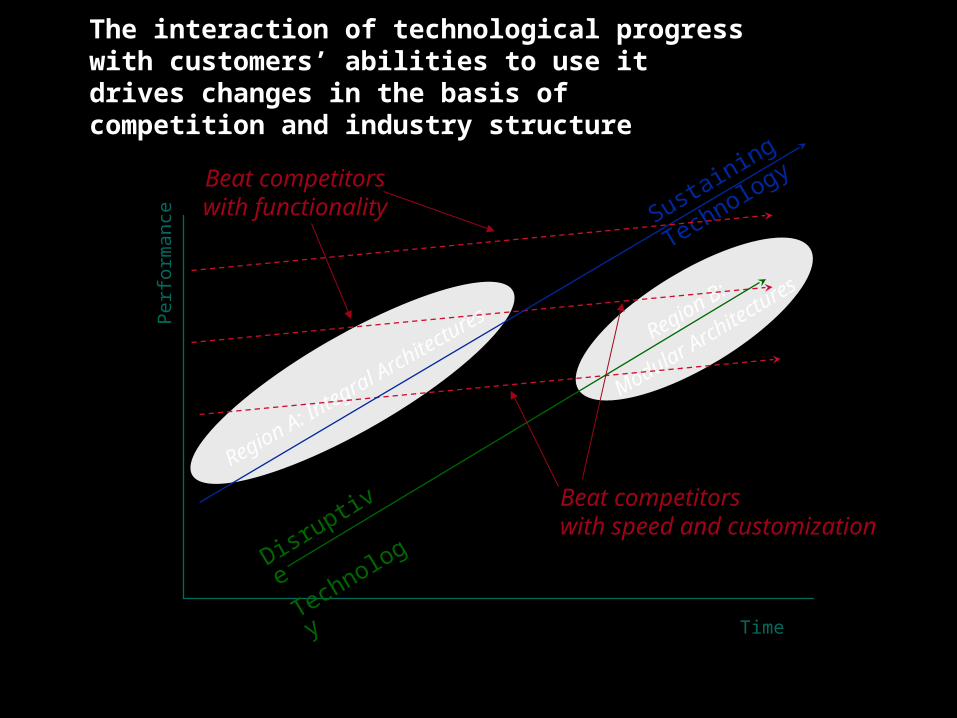

The interaction of technological progress with customers’ abilities to use it drives changes in the basis ofcompetition and industry structure

Disruptive

Technology

Beat competitorswith functionality

Beat competitorswith speed and customization

32

The Disruption of Traditional Campus-Based Management Education Programs

Traditional MBA Programs

Strategy consulting firms

Qua

lity

of

man

agem

ent e

duca

tion

Time

Self-administered

distance education

Large corporations

Small businesses

Corporate Universities

with live instructors

Corporate Universities

with on-line instruction

33

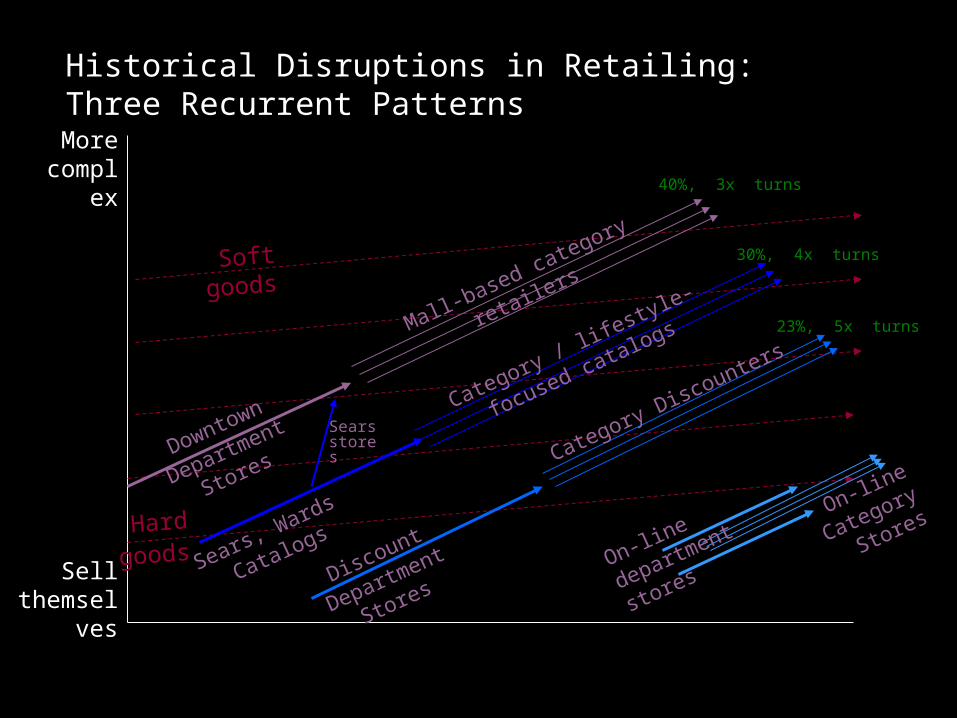

Downtown

Department Stores

Mall-based category retailers

Sears, Wards C

atalogs

Category / lifestyle-focused catalogs

Discount

Department Stores

Sears stores Category Discounters

On-line departm

ent

stores

On-line

Category Stores

Historical Disruptions in Retailing: Three Recurrent Patterns

More complex

Sell themselves

Soft goods

Hard

goods

40%, 3x turns

30%, 4x turns

23%, 5x turns