Page 1

The audio portion of the conference may be accessed via the telephone or by using your computer's

speakers. Please refer to the instructions emailed to registrants for additional information. If you

have any questions, please contact Customer Service at 1-800-926-7926 ext. 10.

Presenting a live 90-minute webinar with interactive Q&A

Structuring Private Equity Funds

for Investment in Renewable Energy

Projects: A New Financing Option

Today’s faculty features:

1pm Eastern | 12pm Central | 11am Mountain | 10am Pacific

WEDNESDAY, JUNE 14, 2017

John J. McDonald, Partner, Troutman Sanders, New York

Justin Boose, Partner, Troutman Sanders, New York

Adam C. Kobos, Partner, Troutman Sanders, Portland & San Francisco

Page 2

Tips for Optimal Quality

Sound Quality

If you are listening via your computer speakers, please note that the quality

of your sound will vary depending on the speed and quality of your internet

connection.

If the sound quality is not satisfactory, you may listen via the phone: dial

1-866-570-7602 and enter your PIN when prompted. Otherwise, please

send us a chat or e-mail [email protected] immediately so we can

address the problem.

If you dialed in and have any difficulties during the call, press *0 for assistance.

Viewing Quality

To maximize your screen, press the F11 key on your keyboard. To exit full screen,

press the F11 key again.

FOR LIVE EVENT ONLY

Page 3

Continuing Education Credits

In order for us to process your continuing education credit, you must confirm your

participation in this webinar by completing and submitting the Attendance

Affirmation/Evaluation after the webinar.

A link to the Attendance Affirmation/Evaluation will be in the thank you email

that you will receive immediately following the program.

For additional information about continuing education, call us at 1-800-926-7926

ext. 35.

FOR LIVE EVENT ONLY

Page 4

Program Materials

If you have not printed the conference materials for this program, please

complete the following steps:

• Click on the ^ symbol next to “Conference Materials” in the middle of the left-

hand column on your screen.

• Click on the tab labeled “Handouts” that appears, and there you will see a

PDF of the slides for today's program.

• Double click on the PDF and a separate page will open.

• Print the slides by clicking on the printer icon.

FOR LIVE EVENT ONLY

Page 5

STRUCTURING PRIVATE EQUITY FUNDS FOR INVESTMENT IN RENEWABLE ENERGY PROJECTS:

A NEW FINANCING OPTION

John McDonald

Partner

Troutman Sanders LLP

John.McDonald@

TroutmanSanders.com

Strafford National Webinar

June 14, 2017

Justin Boose

Partner

Troutman Sanders LLP

Justin.Boose@

TroutmanSanders.com

Adam Kobos

Partner

Troutman Sanders LLP

Adam.Kobos@

TroutmanSanders.com

Page 6

A NEW AND CREATIVE STRUCTURE…

• The emerging trend of energy private equity (EPE) funds is revolutionizing the

renewable energy field, as renewable energy joins leveraged buyouts, venture

capital and hedge funds as asset classes that institutional investors and high net

worth investors are using to deploy their capital in a diversified manner, with the

added “social good” of investing in a sustainable energy future.

• Sophisticated energy sponsors are increasingly eschewing the traditional project

finance structure, in which capital stacks are created for each deal, in favor of a

private equity fund structure in which committed capital is deployed by the

sponsor in accordance with a specified investment strategy.

• From the sponsors’ perspective, the goal is the “holy grail” of all private equity

sponsors – permanent capital. This trend can be seen as further evidence of

renewable energy maturing as an asset class within the larger investment world.

• Since this trend is so new, the terms of EPE funds vary tremendously. However,

some common terms have emerged….

6

Page 7

COMMITTED CAPITAL

• Committed Capital

EPE funds typically employ a traditional private equity fund structure in

which LP investors sign subscription agreements requiring them to make

capital contributions in response to capital calls issued by the sponsor to

fund investments made by the fund in accordance with the investment

strategy.

This contrasts with traditional project finance structure in which the sponsor

creates a project company for each investment and then sources investors to

provide equity capital for that investment (like the “fundless sponsor” LBO

model).

U.S. renewable energy “tax equity” investments are still predominantly done

utilizing the traditional project finance structure, rather than a committed

capital structure.

7

Page 8

INVESTMENT STRATEGY; CARRIED INTEREST

• Investment Strategy

EPE funds are typically focused on investments in a particular sector –

renewable energy, waste-to-value, etc. – and consent of a majority-in-

interest of the LP investors (or, less frequently, the LPAC) is required for the

fund to make deviating investments.

• Carried Interest & Management Fees

Carried interest and management fees in EPE funds vary significantly based

upon relative negotiating strength of the parties, which is often a function of

the sponsor’s track record and the sophistication of the LP investors.

Some EPE funds employ traditional “2&20” private equity fund structure, in

which the sponsor receives a 2% management fee on committed capital

(stepping down to apply to invested capital once it is deployed), along with a

20% “carried interest” share of the profits on investments made by the fund.

8

Page 9

DISTRIBUTION STRUCTURE

• Distribution Structure

Waterfall distribution structures vary considerably across EPE funds, but

many employ a traditional private equity distribution structure in which the

LP investors receive back their invested capital, plus a preferred return on

that invested capital, and then the profits are split.

Profit are split between the LP investors and the sponsor in accordance with

the traditional 80/20 “carried interest” split ratio. This “hard pref” approach,

in which the split is only of the excess over the pref, is commonly used in US

real estate private equity funds.

However, as with US LBO funds, there is sometimes a “disappearing pref”

structure in which, once the LP investors receive back their invested capital

plus the preferred return, there is a “GP catch up” so that all profits in excess

of invested capital are split 80/20 between the LP investors and the sponsor.

9

Page 10

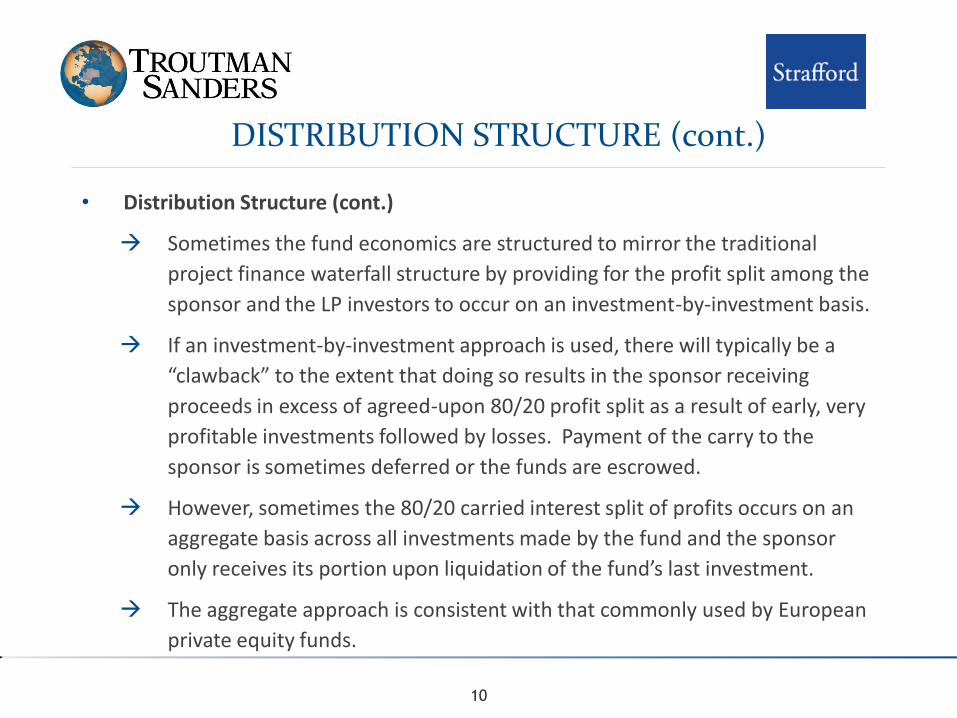

DISTRIBUTION STRUCTURE (cont.)

• Distribution Structure (cont.)

Sometimes the fund economics are structured to mirror the traditional

project finance waterfall structure by providing for the profit split among the

sponsor and the LP investors to occur on an investment-by-investment basis.

If an investment-by-investment approach is used, there will typically be a

“clawback” to the extent that doing so results in the sponsor receiving

proceeds in excess of agreed-upon 80/20 profit split as a result of early, very

profitable investments followed by losses. Payment of the carry to the

sponsor is sometimes deferred or the funds are escrowed.

However, sometimes the 80/20 carried interest split of profits occurs on an

aggregate basis across all investments made by the fund and the sponsor

only receives its portion upon liquidation of the fund’s last investment.

The aggregate approach is consistent with that commonly used by European

private equity funds.

10

Page 11

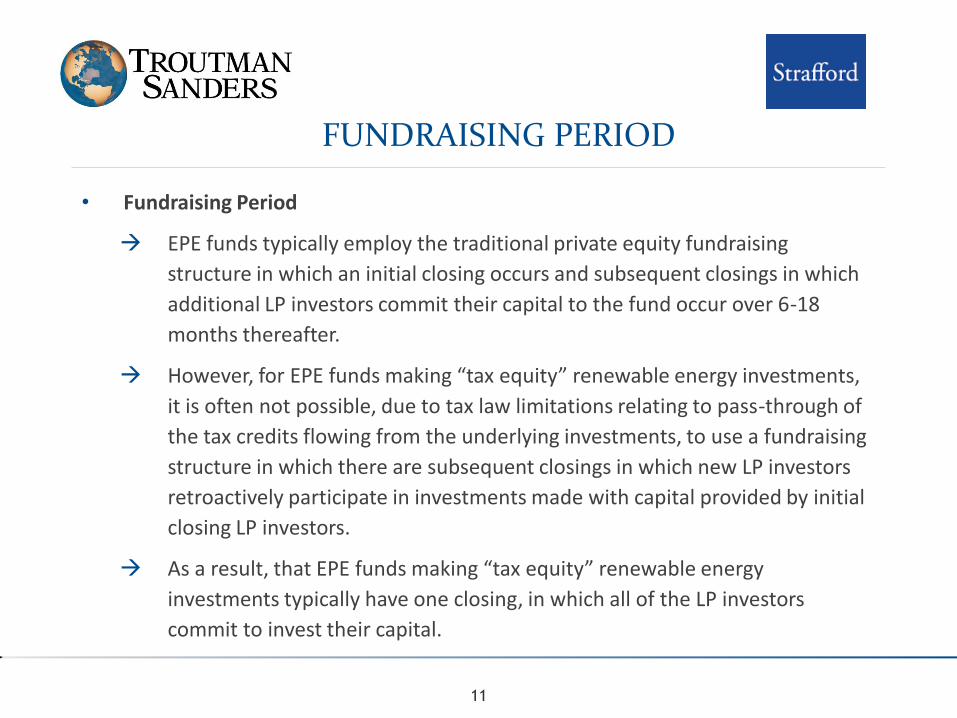

FUNDRAISING PERIOD

• Fundraising Period

EPE funds typically employ the traditional private equity fundraising

structure in which an initial closing occurs and subsequent closings in which

additional LP investors commit their capital to the fund occur over 6-18

months thereafter.

However, for EPE funds making “tax equity” renewable energy investments,

it is often not possible, due to tax law limitations relating to pass-through of

the tax credits flowing from the underlying investments, to use a fundraising

structure in which there are subsequent closings in which new LP investors

retroactively participate in investments made with capital provided by initial

closing LP investors.

As a result, that EPE funds making “tax equity” renewable energy

investments typically have one closing, in which all of the LP investors

commit to invest their capital.

11

Page 12

INVESTMENT PERIOD

• Investment Period

In EPE funds that provide capital to construct renewable energy facilities that

will, upon completion, be sold to long-term investors, the fund’s investment

period often follows the approach customarily used in private equity funds.

In those types of funds, there is a stated investment period, in which the

fund sponsor identifies investment opportunities, calls capital from LP

investors to make the investments, and the capital is used to construct the

facility.

Upon completion of the facility, cashflow from the facility and sometimes

sale proceeds from sale of the facility, are used to repay LP investors. Upon

realization of all investments made by the fund, it is liquidated.

However, the investment period can vary considerably for EPE funds making

other types of renewable energy investments, including those that invest in

completed projects.

12

Page 13

INFORMATION RIGHTS

• Information Rights

EPE fund investors typically receive the following information from the fund

sponsor:

- Quarterly and annual financial statements, with the annual financial

statements often being required to be audited

- Form K-1s and other documents necessary for investors to complete their

tax filings

- Annual reports to investors summarizing the fund’s performance

In addition to receiving the documents listed above, EPE fund investors

typically have the right to inspect the fund’s books and records and

sometimes have the right to meet with the sponsor to discuss fund

performance.

13

Page 14

REGULATORY ASPECTS

• Regulatory Aspects

Like other private equity funds, energy private equity funds are required to

comply with federal and state securities laws:

- The Securities Act of 1933

- State Blue Sky laws

- The Investment Advisors Act of 1940

- The Investment Company Act of 1940

14

Page 15

CONCLUSION

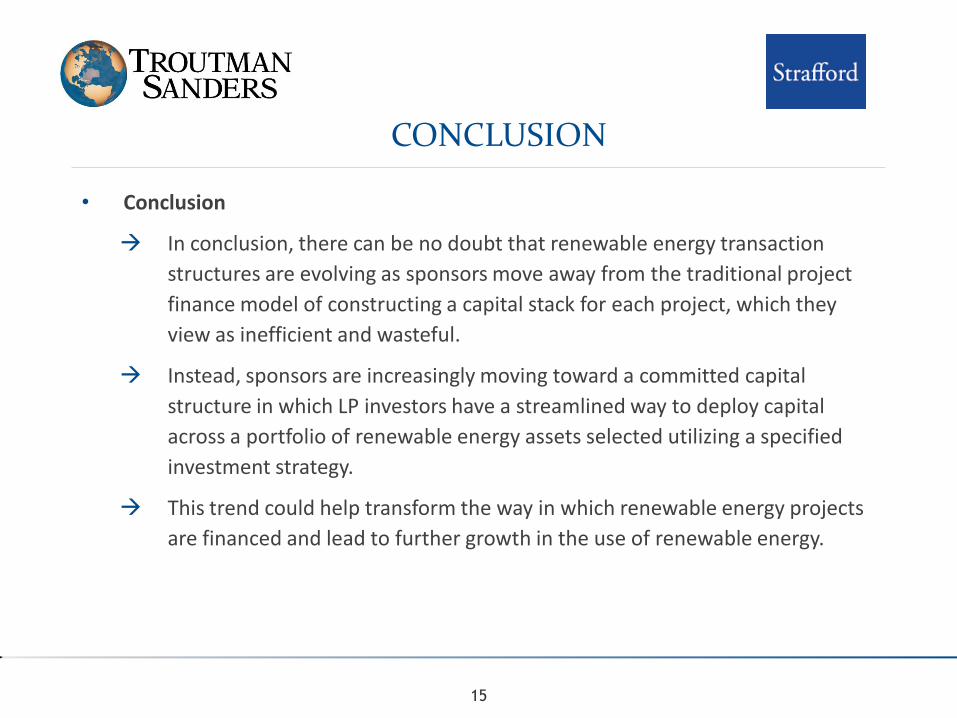

• Conclusion

In conclusion, there can be no doubt that renewable energy transaction

structures are evolving as sponsors move away from the traditional project

finance model of constructing a capital stack for each project, which they

view as inefficient and wasteful.

Instead, sponsors are increasingly moving toward a committed capital

structure in which LP investors have a streamlined way to deploy capital

across a portfolio of renewable energy assets selected utilizing a specified

investment strategy.

This trend could help transform the way in which renewable energy projects

are financed and lead to further growth in the use of renewable energy.

15

Page 16

QUESTIONS?

16

John McDonald

Partner

Troutman Sanders LLP

(212) 704-6234

John.McDonald@

TroutmanSanders.com

Justin Boose

Partner

Troutman Sanders LLP

(212) 704-6349

Justin.Boose@

TroutmanSanders.com

Adam Kobos

Partner

Troutman Sanders LLP

(503) 290-2321

Adam.Kobos@

TroutmanSanders.com