I E-BANKING LOYALTY Submission of a project report summer internship Submitted By: Kundan Prajapati (20044311071) Submitted To: Prof.Dhara Jha Ganpat University-V M INSTITUTE OF MANAGEMENT August-4-2021

Transcript

I

E-BANKING LOYALTY

Submission of a project report

summer internship

Submitted By:

Kundan Prajapati (20044311071)

Submitted To:

Prof.Dhara Jha

Ganpat University-V M INSTITUTE OF MANAGEMENT

August-4-2021

II

SUMMER INTERNSHIP PROGRAMME 2020

MBA Semester-II

Joining Report

Date:

To,

Sub: Joining Report for Summer Internship Programme

Dear Sir / Madam,

As per the schedule for commencement of Summer Internship Programme in your esteemed Organization, I report

to the duty on DT 2020, At . . AM. My present address for communication and contact numbers are

as mentioned below. I shall abide by the rules and regulations of the Organization during the entire project period.

I solicit your active guidance and kind co-

operation. Thank You.

Yours Truly,

Students Name & Signature Corporate Mentor

NAME

MBA Sem II Name:

Enrolment No.

Contact No.

Signature:

Address for Communication

Email Id:

Copy to: The Concerned Corporate Mentor & Faculty Mentor.

III

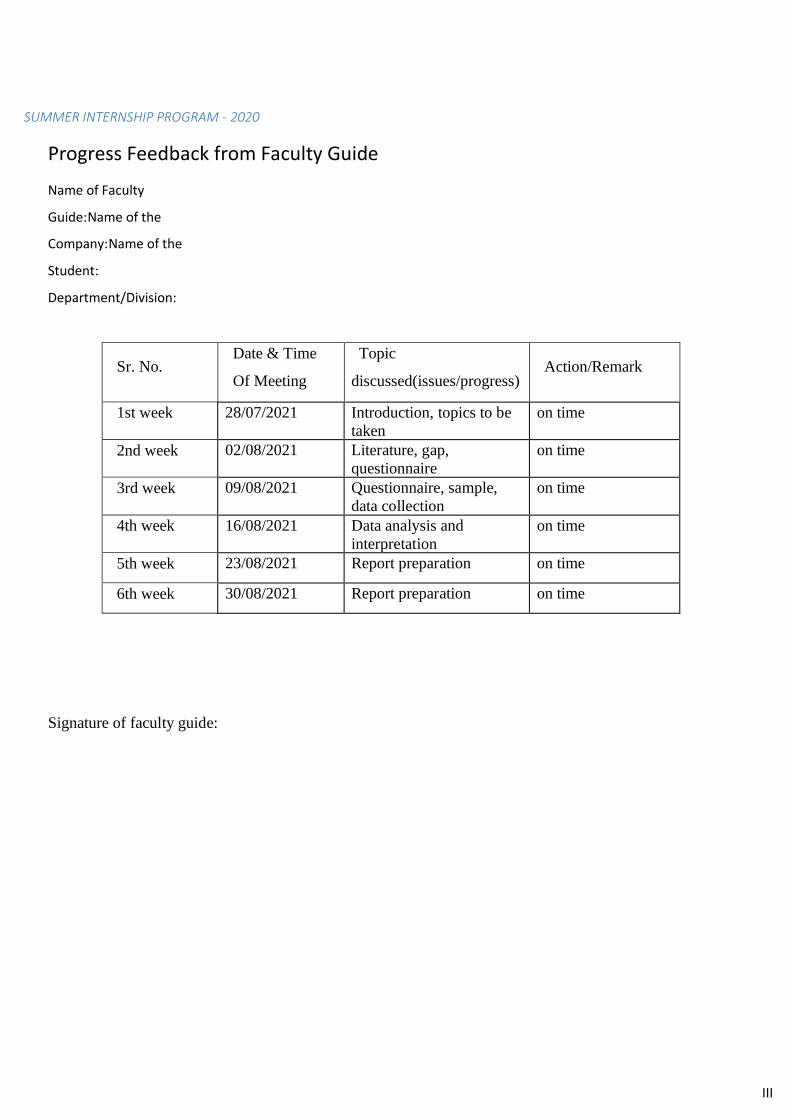

SUMMER INTERNSHIP PROGRAM - 2020

Progress Feedback from Faculty Guide

Name of Faculty

Guide: Name of the

Company: Name of the

Student:

Department/Division:

Sr. No. Date & Time

Of Meeting

Topic

discussed(issues/progress)

Action/Remark

1st week 28/07/2021 Introduction, topics to be

taken

on time

2nd week 02/08/2021 Literature, gap,

questionnaire

on time

3rd week 09/08/2021 Questionnaire, sample,

data collection

on time

4th week 16/08/2021 Data analysis and

interpretation

on time

5th week 23/08/2021 Report preparation on time

6th week 30/08/2021 Report preparation on time

Signature of faculty guide:

IV

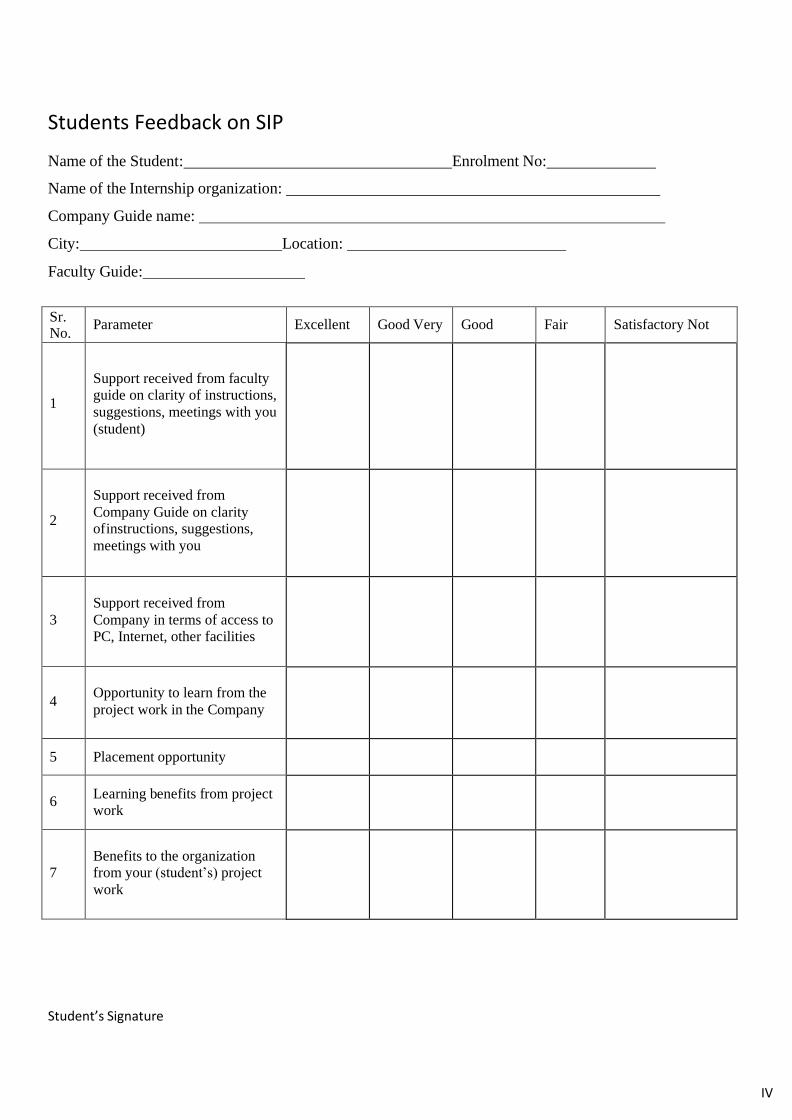

Students Feedback on SIP

Name of the Student: Enrolment No:

Name of the Internship organization:

Company Guide name:

City: Location:

Faculty Guide:

Sr. No.

Parameter Excellent Good Very Good Fair Satisfactory Not

1

Support received from faculty

guide on clarity of instructions,

suggestions, meetings with you

(student)

2

Support received from

Company Guide on clarity

of instructions, suggestions,

meetings with you

3

Support received from

Company in terms of access to

PC, Internet, other facilities

4

Opportunity to learn from the

project work in the Company

5 Placement opportunity

6 Learning benefits from project

work

7

Benefits to the organization

from your (student’s) project

work

Student’s Signature

V

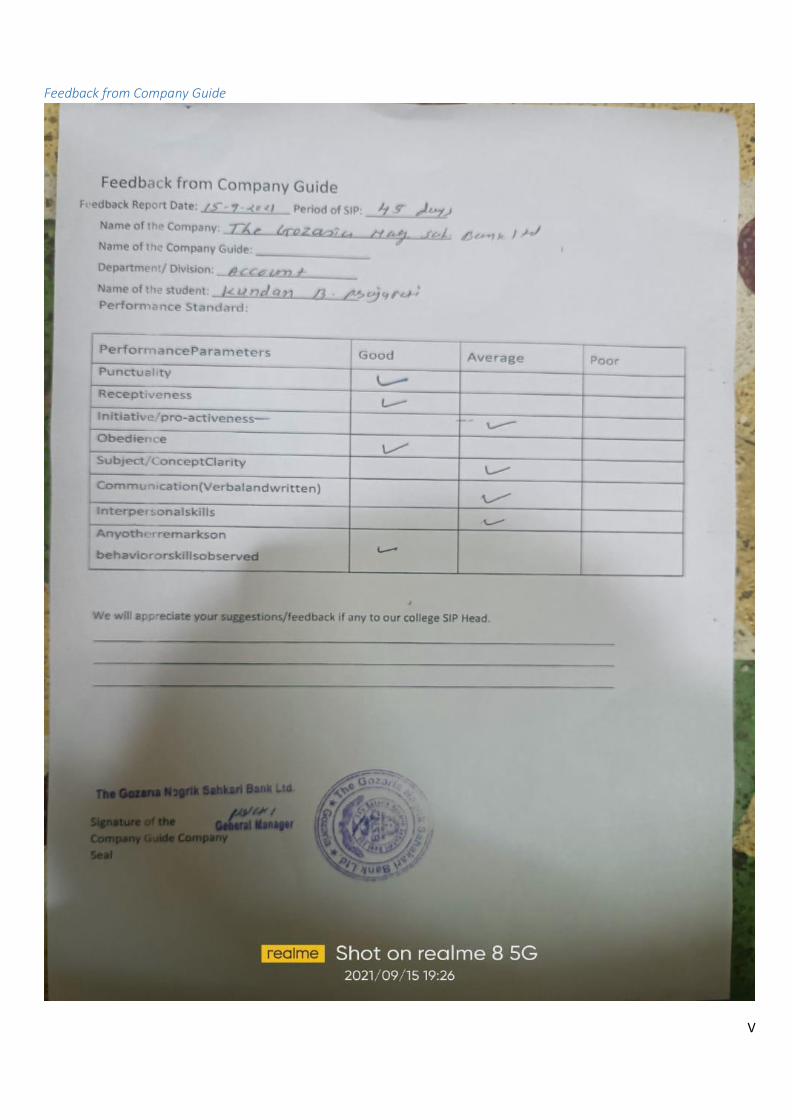

Feedback from Company Guide

VI

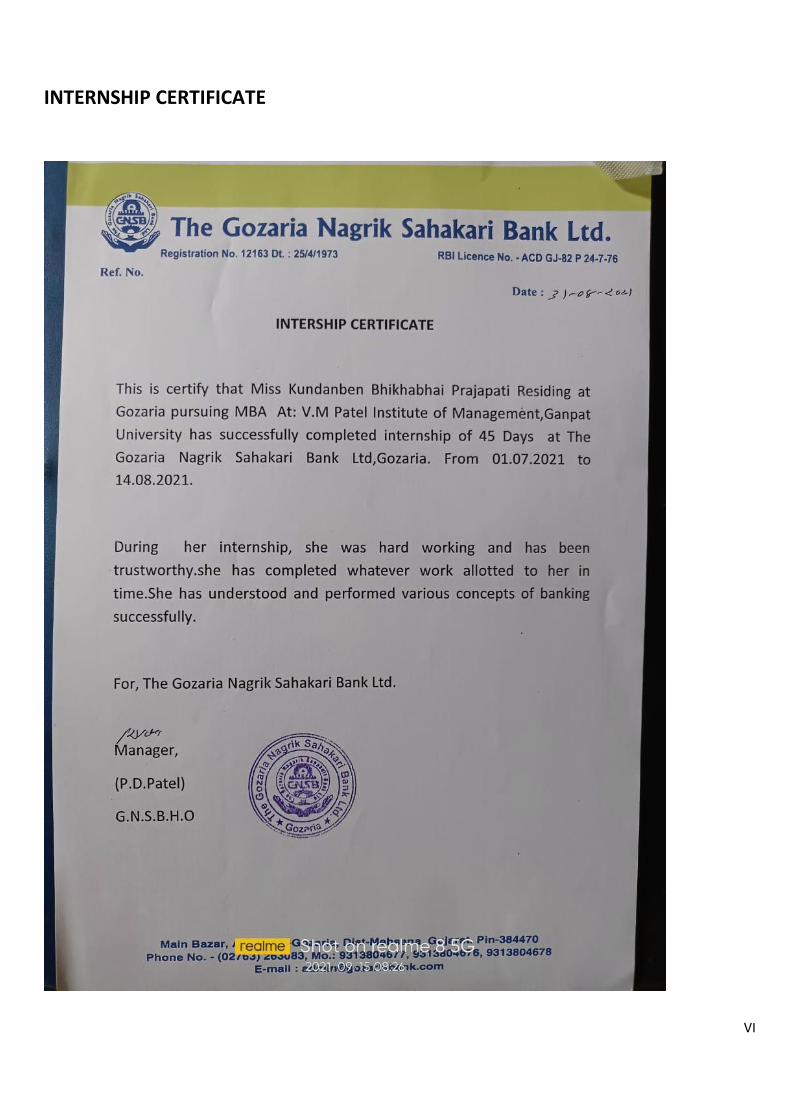

INTERNSHIP CERTIFICATE

VII

CANDIDATE STATEMENT

I hereby declare that in this research project I have worked hard on the

Topic.

“E-BANKING” This project is a individual project report and I have worked constantly worked on this topic under the guidance of prof.dhara jha maam.in inchoate of the requirement for the finder of award of MASTER OF BUSINESS ADMINISTRATION(SEM 3)is the of original study undertaken by me and it has not been submitted earlier to any university or institute for finder a d the degree diploma.

Kundan Prajapati (20044311071)

VIII

PREFACE

This project report has been prepared in full fulfillment of the requirement for the assignment of subject SUMMER INTERNSHIP. For preparing the project report. I have received different papers on the subject of E-BANKING and customer loyalty blend of learning and knowledge acquired during our practical studies in the field of research presented in this project report.

Mine main focus and study were on the topic of e-banking, in which my focus was on the role of customer loyalty, reliability and etc.I have put up my best efforts and enumerated every possible information after concluding the research, to make this report a satisfactory report.

It was great opportunity and memorable experience to learn new facets practical knowledge about research through carrying out a research, collecting information about the above-mentioned subject interacting with people for data collection.

Lastly, I have tried our level best to prepare the best informative report.

Kundan Prajapati (20044311071)

IX

ACKNOWLEDGEMENT

It was indeed an opportunity for us to carry out a research and prepare a report on the topic of e-banking during the semester 3 as a part of study. I would hereby take this opportunity to show our gratitude towards all our mentors for what we have learnt during the research. And we would also like to thank all our respondents for their co- operation and for providing valuable information for our research project. The successful completion of this project could not have been possible without the co-operation and support of our faculty guide who have given complete information, support & guidance for the project. I feel immense pleasure to thank our faculty guide Prof.Dhara jha ma’am for making available all facilities in fulfilling the requirements for the project work. I forward our appreciation to the Project Coordinator of the VMPIM.

Kundan Prajapati

X

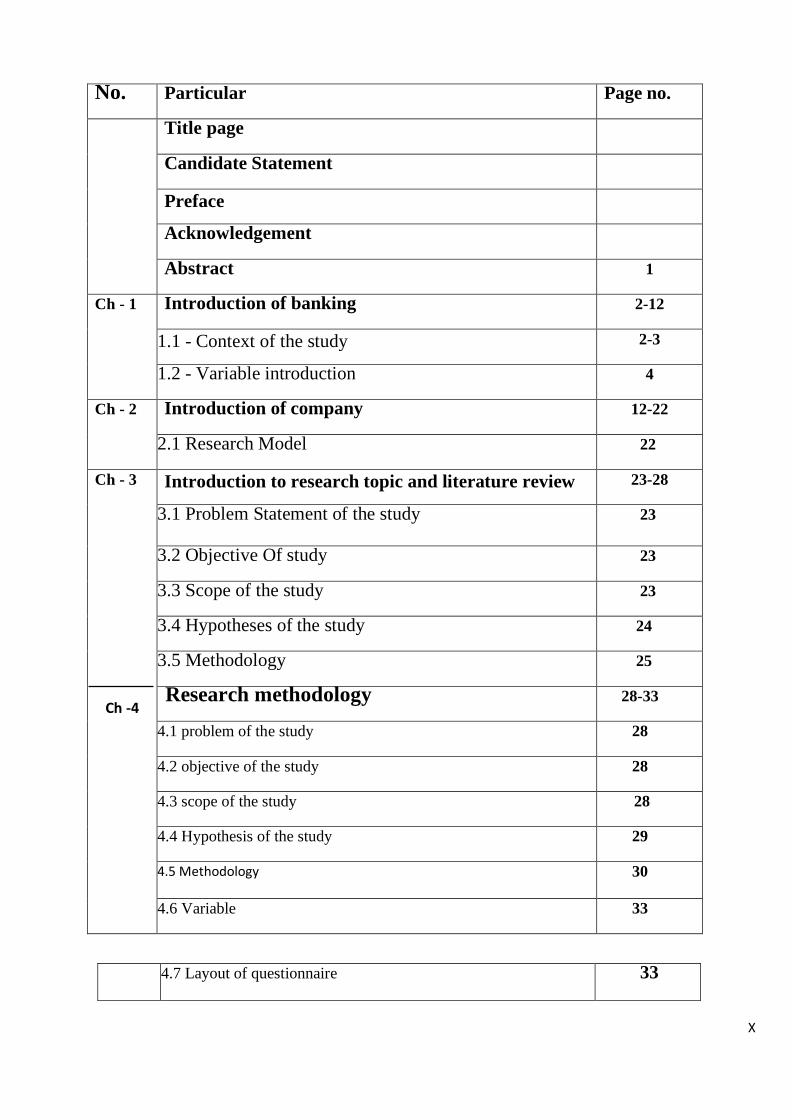

No. Particular Page no.

Title page

Candidate Statement

Preface

Acknowledgement

Abstract 1

Ch - 1 Introduction of banking 2-12

1.1 - Context of the study 2-3

1.2 - Variable introduction 4

Ch - 2 Introduction of company 12-22

2.1 Research Model 22

Ch - 3

Ch -4

Introduction to research topic and literature review 23-28

3.1 Problem Statement of the study 23

3.2 Objective Of study 23

3.3 Scope of the study 23

3.4 Hypotheses of the study 24

3.5 Methodology 25

Research methodology 28-33

4.1 problem of the study 28

4.2 objective of the study 28

4.3 scope of the study 28

4.4 Hypothesis of the study 29

4.5 Methodology 30

4.6 Variable 33

4.7 Layout of questionnaire 33

XI

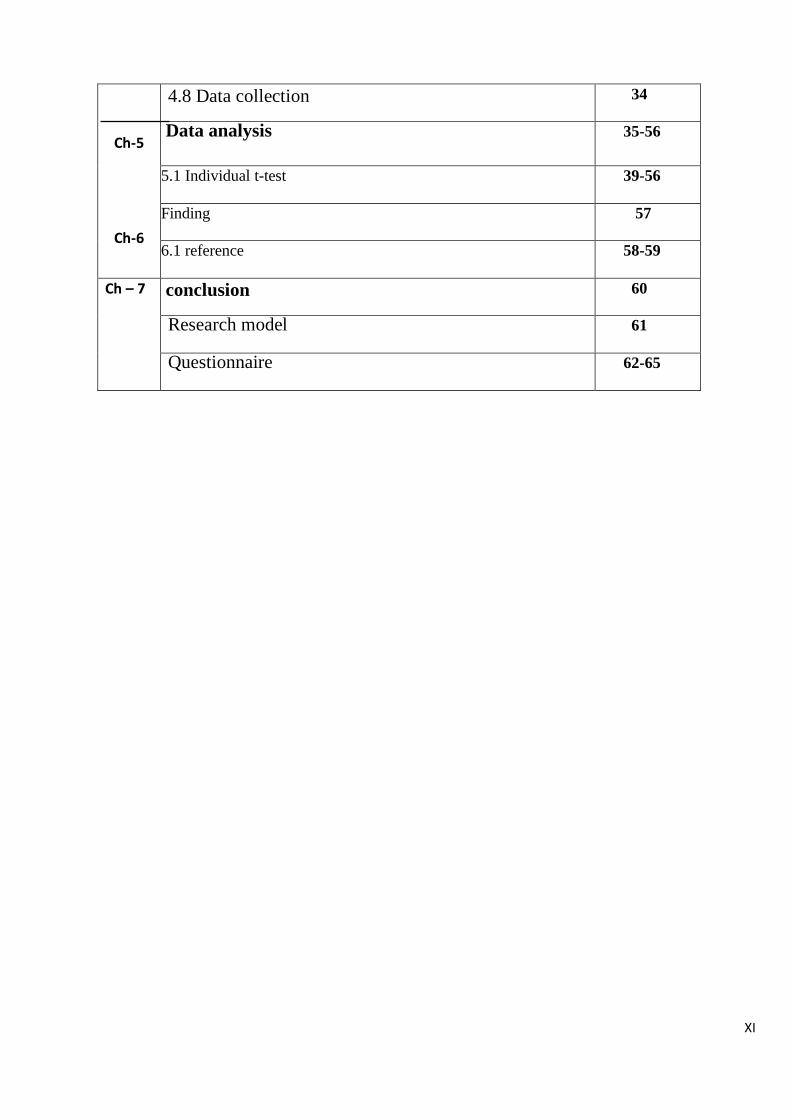

Ch-5

Ch-6

4.8 Data collection 34

Data analysis 35-56

5.1 Individual t-test 39-56

Finding 57

6.1 reference 58-59

Ch – 7 conclusion 60

Research model 61

Questionnaire 62-65

1

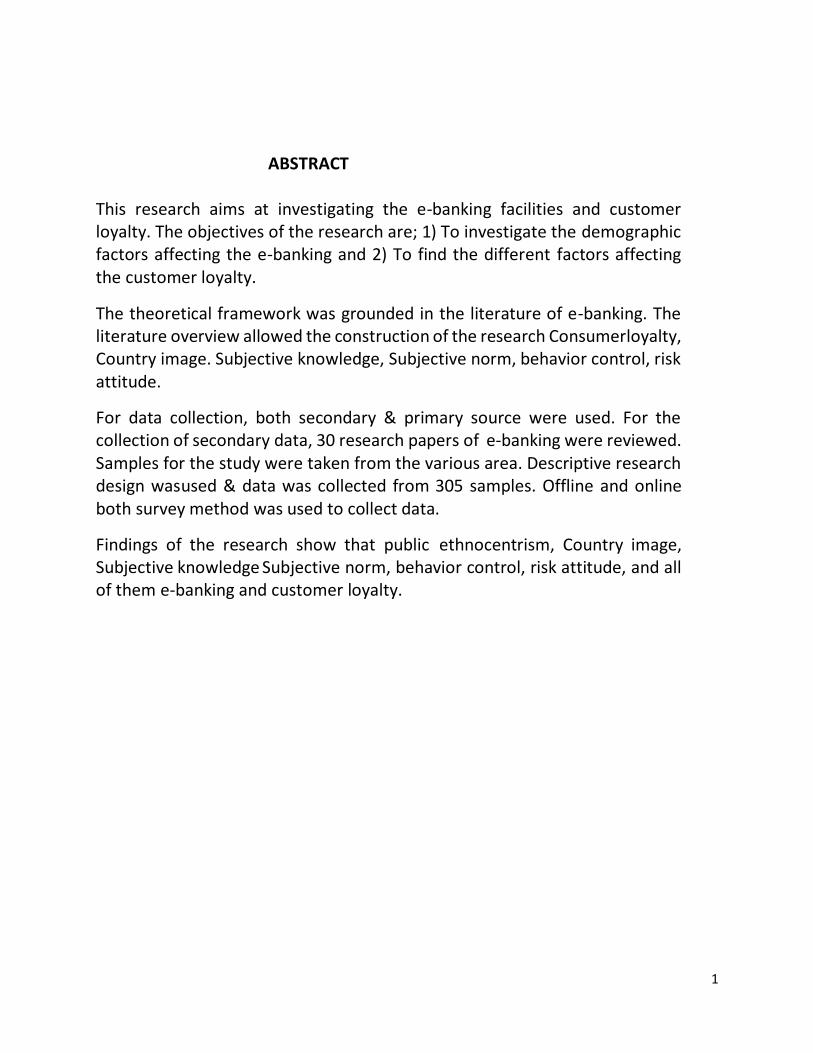

ABSTRACT This research aims at investigating the e-banking facilities and customer loyalty. The objectives of the research are; 1) To investigate the demographic factors affecting the e-banking and 2) To find the different factors affecting the customer loyalty.

The theoretical framework was grounded in the literature of e-banking. The literature overview allowed the construction of the research Consumer loyalty, Country image. Subjective knowledge, Subjective norm, behavior control, risk attitude.

For data collection, both secondary & primary source were used. For the collection of secondary data, 30 research papers of e-banking were reviewed. Samples for the study were taken from the various area. Descriptive research design was used & data was collected from 305 samples. Offline and online both survey method was used to collect data.

Findings of the research show that public ethnocentrism, Country image, Subjective knowledge Subjective norm, behavior control, risk attitude, and all of them e-banking and customer loyalty.

2

1.Introduction of banking The banking sector is the lifeline of any modern economy.it is one of the financial pillars of the financial sectors, which plays a vital role in the functioning of an economy.it is very important for economic development of a country that its financing requirements of trade, industry and agriculture are met with higher of commitment and responsibility. They play an important role in the mobilization of deposits and disbursement of credit to various sectors of the country. the strength of an economy depends on a sound and solvent banking system. A sound banking system efficiently mobilized savings in productive sectors and a solvent banking system ensures that the bank is capable of meeting its obligation to the depositors.

In India ,banks are playing a crucial role in socio-economic progress of the country after independence. the banking sector is dominant in india as it accounts for more than half the assets of the fianancial sector. indian banks have been going through a fascinating phase through rapid changes brought about by financial sector reforms, which are being implemented in a phased manner.

The current process of transformation should be viewed as an opportunity to convert indian banking into a sound , strong and vibrant system capable of playing its role efficiently and effectively on their own without imposing any burden on government. after the liberalization of the indian economy. the government has announced a number of reform measures on the basis of the recommendation of the Narasimhan committee to take the banking sector economically viable and competitively strong.

Modern banking in India originated in the last decade of the 18th century. Among the first banks were the Bank of Hindustan, which was established in 1770 and liquidated in 1829–32; and the General Bank of India, established in 1786 but failed in 1791.

The largest and the oldest bank which is still in existence is the State Bank of India (SBI). It originated and started working as the Bank of Calcutta in mid-June 1806. In 1809, it was renamed as the Bank of Bengal. This was one of the three banks founded by a presidency government, the other two were the Bank of Bombay in 1840 and the Bank of Madras in 1843. The three banks were merged in 1921 to form the Imperial Bank of India, which upon India's independence, became the State Bank of India in 1955. For many years, the presidency banks had acted as quasi-central banks, as did their successors, until the Reserve Bank of India was established in 1935, under the Reserve Bank of India Act, 1934.

In 1960, the State Banks of India was given control of eight state-associated banks under the State Bank of India (Subsidiary Banks) Act, 1959. These are now called its associate banks. In 1969, the Government of India nationalised 14 major private banks; one of the big banks was Bank of India. In 1980, 6 more private banks were nationalised. These nationalised banks are the majority of lenders in the Indian economy. They dominate the banking sector because of their large size and widespread networks.

The Indian banking sector is broadly classified into scheduled and non-scheduled banks. The scheduled banks are those included under the 2nd Schedule of the Reserve Bank of India Act, 1934. The scheduled banks are further classified into: nationalised banks; State Bank of India and its associates; Regional Rural Banks (RRBs); foreign banks; and other Indian private sector banks. The SBI has merged its Associate banks into itself to create the largest Bank in India on 1 April 2017. With this merger SBI has a global ranking of 236 on Fortune 500 index. The term commercial banks refers to both scheduled and non-scheduled commercial banks regulated under the Banking Regulation Act, 1949.

Generally the supply, product range and reach of banking in India is fairly mature-even though reach in rural India and to the poor still remains a challenge. The government has developed initiatives to address this through the State Bank of India expanding its branch network and through the National Bank for Agriculture and Rural Development (NABARD) with facilities like microfinance.

• Make /Collect Payment in ALL INDIA instantly through RTGS (Real Time Gross Settlement) NEFT (National Electronic Funds Transfer) Facility.

2.1.3 RTGS

• The minimum amount to be remitted through RTGS is 2.00 lac. There is no upper ceiling for RTGS transactions. Transaction of RTGS settled instantly.

2.1.4 NEFT

• There is no limit of amount for remittance in NEFT transaction. Transaction of NEFT Settled as per Batchwise.

11

• For RTGS / NEFT transaction contact to your nearst Branch (Any Branch Banking under CBS)

• IFS (Indian Financial System ) Code for RTGS / NEFT transaction, is printed on the cheque book.

2.1.5 E-Payment (TDS/TCS/GVAT/CST/Excise & Service Tax)

• E-Payment (TDS/TCS/GVAT/CST/Excise & Service Tax) Services -e-Payment facilitates payment of direct taxes online by taxpayers. To avail of this facility the taxpayer is required to have a net-banking account with any of the Authorized Banks.

• If Our Customer Sufficient balance in the bank account to cover the amount of payment for immediate transfer via IDBI Bank. Please avoid using browsing centers for making e-payments / GVAT(Gujarat Value added Tax) / CST (Central Sales Tax)/ Excise and Service Tax.

• E-Payment (Tax Deducted at Source / Tax Collected at Source (TDS/TCS) from corporates or non-corporates);(payment of Income tax & Corporation Tax);(payment of Security Transaction Tax, Hotel Receipts Tax, Estate Duty, Interest Tax, Wealth Tax, Expenditure Tax /Other direct taxes & Gift tax) ;(payment of Banking Cash Transaction Tax and Fringe Benefits Tax) or Epayment/GVAT/CST/Excise and Service Tax transaction contact to your nearst Branch (Any Branch Banking under CBS).

2.1.6 Online E-payment:

• Income-tax

• TDS-TCS

• Security Transaction Tax

• Hotel Receipt Tax

• Estate Duty

• Expenditure Tax

• Interest Tax

• Other Direct Tax

• Central Sales Tax

12

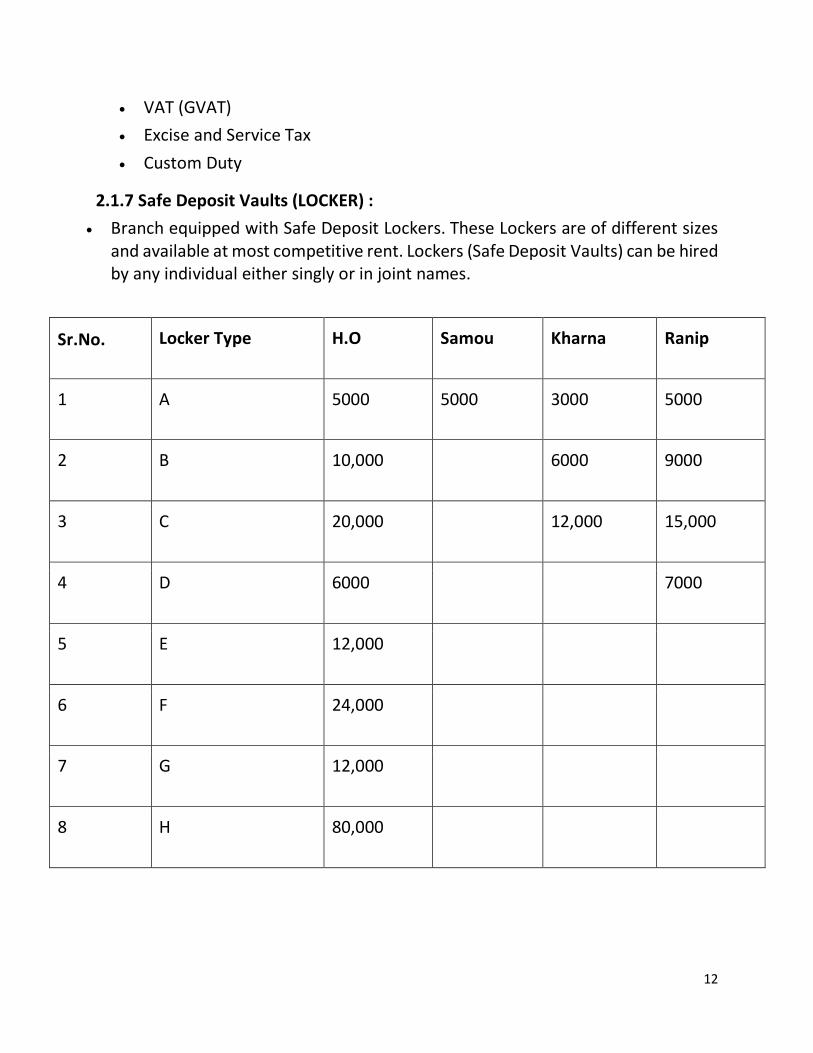

• VAT (GVAT)

• Excise and Service Tax

• Custom Duty

2.1.7 Safe Deposit Vaults (LOCKER) :

• Branch equipped with Safe Deposit Lockers. These Lockers are of different sizes and available at most competitive rent. Lockers (Safe Deposit Vaults) can be hired by any individual either singly or in joint names.

Sr.No. Locker Type H.O Samou Kharna Ranip

1 A 5000 5000 3000 5000

2 B 10,000

6000 9000

3 C 20,000

12,000 15,000

4 D 6000

7000

5 E 12,000

6 F 24,000

7 G 12,000

8 H 80,000

13

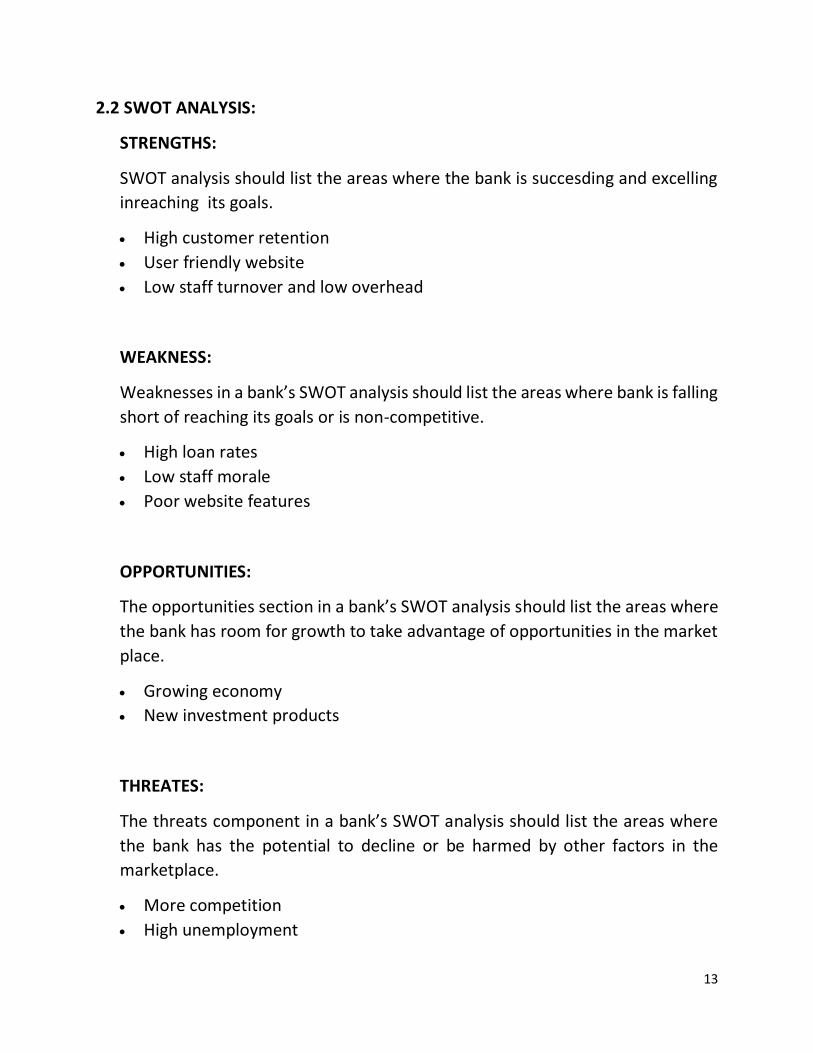

2.2 SWOT ANALYSIS:

STRENGTHS:

SWOT analysis should list the areas where the bank is succesding and excelling

inreaching its goals.

• High customer retention

• User friendly website

• Low staff turnover and low overhead

WEAKNESS:

Weaknesses in a bank’s SWOT analysis should list the areas where bank is falling

short of reaching its goals or is non-competitive.

• High loan rates

• Low staff morale

• Poor website features

OPPORTUNITIES:

The opportunities section in a bank’s SWOT analysis should list the areas where

the bank has room for growth to take advantage of opportunities in the market

place.

• Growing economy

• New investment products

THREATES:

The threats component in a bank’s SWOT analysis should list the areas where

the bank has the potential to decline or be harmed by other factors in the

marketplace.

• More competition

• High unemployment

14

3. INTRODUCTION TO RESEARCH TOPIC AND LITREATURE REVIEW

3.1 CONTEXT OF THE STUDY

Prior studies on E-banking have focused on how knowledgeable customers are about e-banking. Their findings have shown that customers possess inadequate knowledge about personal finance issues. However, the results of these studies are weakened because of several limitations. First, many of the past studies used surveys with only a limited number of 5 to 10 questions. Readers must question the reliability of the results. Second, there is little research and agreement among

researchers on what important questions should be included in a customer loyalty survey. Last, many previous studies have been conducted by financial service companies. These surveys focus on areas related to their business and fail to cover other areas in personal finance. These limitations have made the validity and reliability of past survey instruments questionable. If a person fails a five-question survey on mutual funds, the individual is not necessarily illiterate about mutual funds, let alone about the entire field of personal finance. There exists an urgent need to make improvements on these issues.

15

3.2 INTRODUCTION OF VARIABLES

3.2.1 GENDER

Every person, family, or household makes certain financial decisions relative to its activity. Currently, also due to societal or legal obligations, we are often obliged to use offers of the financial market. However, not every person is willing to use the relevant products or services in the same way. Moreover, the market for financial services is becoming increasingly complex and complicated, and the responsibility for taking financial decisions rests solely on the individual making choices in this regard. Meanwhile, a number of studies have shown that the state of personal finances, economic prosperity and financial behaviors differ significantly between men and women (Fisher, 2010; Theodor et al., 2014; Chen & Volpe, 2002; Lusardi & Mitchell, 2008). people’s behavior on the financial market is determined and conditioned also by other factors, such as, for instance age, employment status, place of residence, education income, number of people in the household, or experiencing financial management (Borden et al., 2008; Robb & Woodyard, 2011; Agarwal et al., 2009; Shiva pour, 2012; Carter et al., 2007). These variables affect actions taken by men and women. Also, experience gained in the use of financial services affect decisions about financial planning. Understanding the relationship between the knowledge of personal finance and specific behaviors in the financial market among women and men constitutes an increasingly important research problem.

3.2.2 Age: Population aging is a process that shapes the economic environment in most of the developed economies. Thus, understanding the dynamics between e-banking and the demographic variables enables policy-makers to adapt and to ameliorate their medium-term budgetary frameworks. The aim of this paper is to examine the fiscal implications of the demographic shift using panel data on 25 EU countries in the period from 1995 until 2014. In order to qualify the findings of previous literature, this paper considers the demographic variables as endogenous and applies the system GMM estimator to obtain the elasticity of several public finance categories with respect to population aging. The results indicate significant and positive impacts of the elderly share on expenditure for pensions and social

16

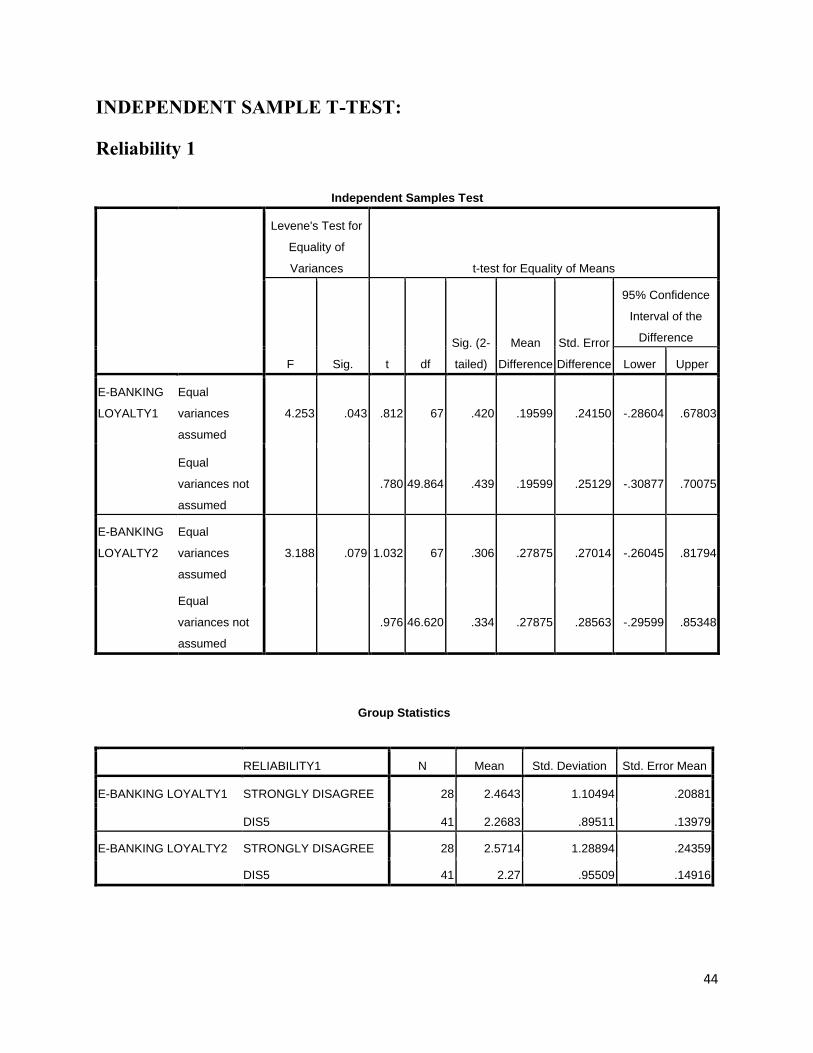

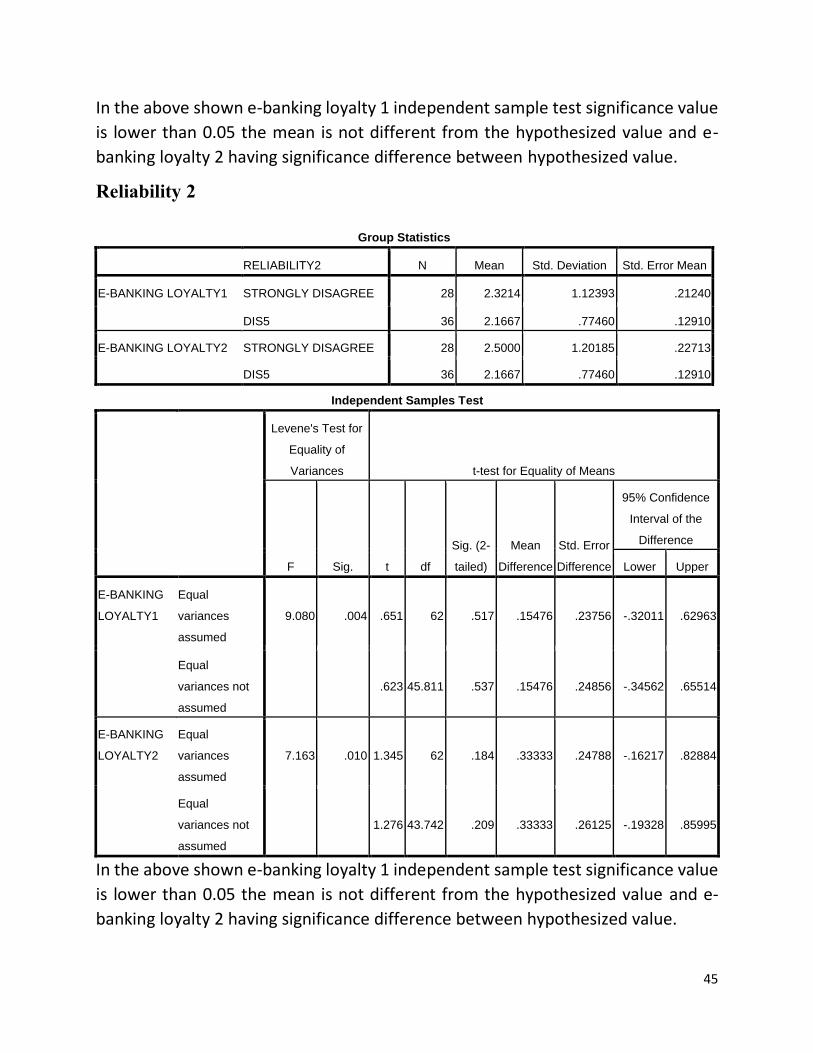

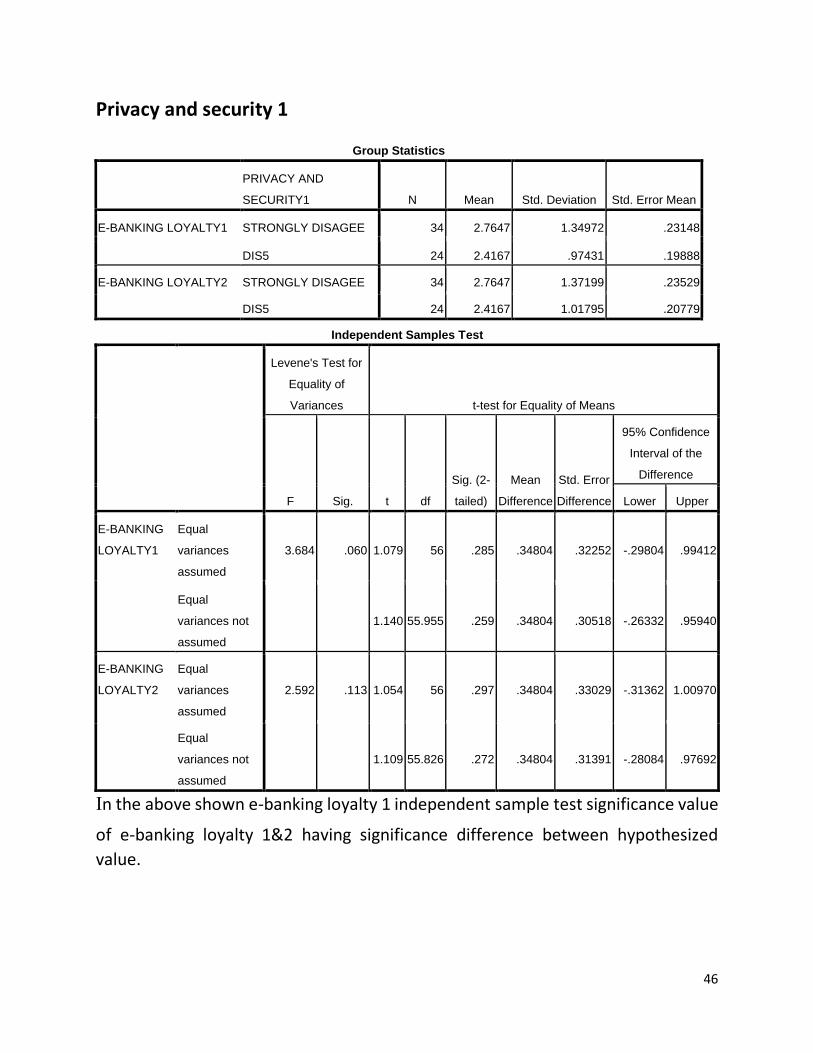

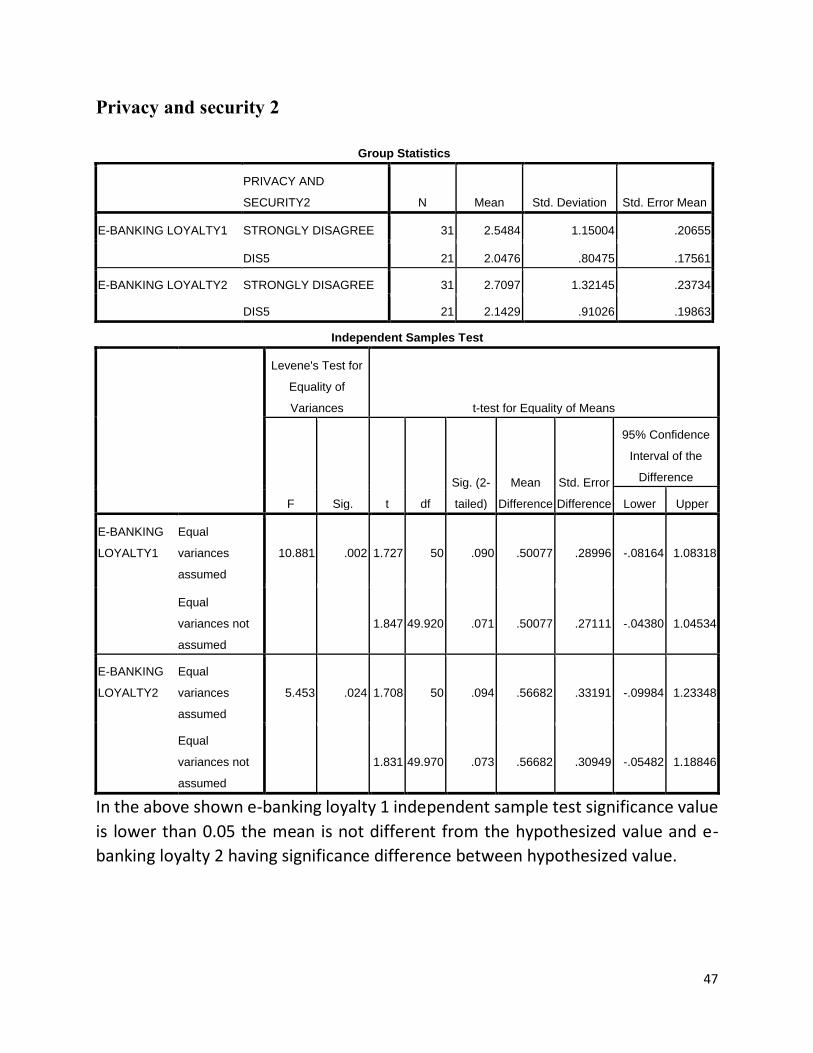

protection. The higher positive impact on overall public expenditure compared with total government revenue confirms the negative effect of population aging on budget balance. An increase in the young population has a significant impact only on health expenditure. The forecasted increase in the share of total public expenditure on elderly individuals is largely accounted for by expenditure on civilian pensions and other cash transfers, government services, and poverty and other social protection. Elderly individuals are found to be not very expensive in terms of public health expenditure. Tax revenues increase and result in a decline of debt-to-GDP ratio because population ageing does not lower tax buoyancy in the long run. Overall, the increasing total budget surplus and fiscal support ratio implies that the long-term impact of population ageing may be fiscally sustainable. 3.2.3 RELIABILITY Reliability concerns the extent to which a measurement of a phenomenon provides stable and consist result (Carmines and Zeller, 1979). Reliability is also concerned with repeatability. For example, a scale or test is said to be reliable if repeat measurement made by it under constant conditions will give the same result (Moser and Kalton, 1989). Testing for reliability is important as it refers to the consistency across the parts of a measuring instrument (Huck, 2007). A scale is said to have high internal consistency reliability if the itemsof a scale “hang together” and measure the same construct (Huck, 2007, Robinson, 2009). The most commonly used internal consistency measure is theCronbach Alpha coefficient. It is viewed as the most appropriate measure of reliability when making use of Likert scales (Whitley, 2002, Robinson, 2009). No absolute rules exist for internal consistencies, however most agree on a minimum internal consistency coefficient of .70 (Whitley, 2002, Robinson, 2009). For an exploratory or pilot study, it is suggested that reliability should be equal to or above 0.60 (Straub et al., 2004). Hinton et al. (2004) have suggested four cut-off points for reliability, which includes excellent reliability (0.90 and above), high reliability (0.70-0.90), moderate reliability (0.50-0.70) and low reliability (0.50 and below)(Hinton et al., 2004). Although reliability is important for study, it is not sufficient unless combined with validity. In other words, for a test to be reliable, it also needs to be valid (Wilson, 2010). Table 2 compares the validity components. 3.2.4 PRIVACY AND SECURITY

17

Privacy can be understood as a legal concept and as the right to be let alone (S.

Warren, et al 1890). Privacy can also mean “the claim of individuals, groups, or

institutions to determine for themselves when, how, and to what extent

information about them is communicated to others” (A.F.Westin, 1967). From a

privacy standpoint, trust can be viewed as the customer’s expectation that an

online business will treat the customer’s information fairly (V. Shankar et al, 2002).

There are four basic categories of privacy: information privacy, bodily privacy,

communications privacy, and territorial privacy (S. Davies, 1996). Internet privacy

is mostly information privacy. Information privacy means the ability of the

individual to control information about one’s self. Invasions of privacy occur when

individuals cannot maintain a substantial degree of control over their personal

information and its use. People react differently to privacy problems. One reason

for these differences might be a cultural viewpoint. For example, researchers have

pointed out that consumers in Germany react differently to marketing practices

than people in the USA might consider the norm (T.Singh et al, 2003). It is also

important to understand their views regarding privacy in general, their personal

expertise in Internet technologies, and how they view the role of the government

and the role of companies in protecting consumer privacy. An individual’s

perceptions of such external conditions will also vary with personal characteristics

and past experiences (N. K. Malhotra et al, 2004). Therefore, consumers often have

different opinions about what is fair and what is not fair in collecting and using

personal information. According to C.M.K.Cheung et al (2006) different threats in

e-commerce, like data transaction attacks and misuse of financial and personal

information, generate security threats. Thus, security is protection against such

threats (F. Belanger et al 2002). Information security consists of three main parts:

confidentiality, integrity, and availability. CIA as an abbreviation is a widely used

benchmark for evaluation of information system security also IJCSI International

Journal of Computer Science Issues, Vol. 9, Issue 4, No 3, July 2012 ISSN (Online):

1694-0814 www.IJCSI.org 438 Copyright (c) 2012 International Journal of Computer

Science Issues. All Rights Reserved. in the e-commerce environment (Parker et al,

2004). All three parts of security may be affected by purely technical issues, natural

phenomena, or accidental or deliberate human causes. Confidentiality refers to

limitations of information access and disclosure to authorized users and preventing

access by or disclosure to unauthorized users. In other words, confidentiality is an

assurance that information is shared only among authorized persons or

18

organizations. Authentication methods, like user IDs and passwords that identify

users can help to reach the goal of confidentiality. Other control methods support

confidentiality, such as limiting each identified user's access to the data system's

resources. Additionally, critical to confidentiality (also to integrity and availability)

are protection against malware, spyware, spam and other attackes.

3.2.5 WEBSITE DESIGN

Recently there has been a shift in the banking industry. The industry is rapidly

moving towards a click and bricks strategy that emphasize on an online supplement

to the conventional banking services (Miranda , F.J . Cortes, R and Barriuso, C. ,

2006) . Internet Banking and Internet Banks there are basically two different

strategies: First an existing bank with physical offices can establish a website and

offer Internet Banking to its customer as an additional delivery channel. A second

alternative is to establish an Internet only bank or virtual bank, almost without

physical offices (Miranda, F.J Cortes, R and Barriuso, C. , 2006 ). For the banks to go

in for internet banking, the websites play a very important role. (Diniz,1998)

reported that banks use the web to achieve main objectives like to market

information, to deliver banking products and services and also as a tool in order to

improve customer relationship. According to (Donlan, 1999), although delivery is

highly important in fulfilling customer needs, perceptions and expectations also

need to be managed and the website plays a main role in this. The design of a good

website should be based on a common ground between the site’s goals and the

customer’s goals; this reveals ideal customer experience (Good, 2000). According

to (Jayawardhena , 2004) today’s context of ebanking, is one whereby a customer

uses the internet to connect to the bank’s computer systems and there is no human

contact element as found in traditional banking services. In this process a very large

number of transactions between the bank and the customer are carried out by

digital means. Banks web sites can contain various features including the product

information, contact information to enable customer feedback, general company

information etc. If 80% of the users are using 20 % of your information then that

information should be most visible and easiest to access. (Bormann and Solms,

1993) were of the opinion that a website is unique in its hypermedia attributes.

Hypermedia integrates multimedia content with hypertext connection. Multimedia

19

content refers to information while hypertext connection appertains to navigation

Basic required information should be available on the home page and related

information should be easily traceable.(Miranda, F.J. Cortes, R and Barriuso, C ,

2006). In the past many banks were of the opinion that designing a website is a

technical job and it can be handled best by the engineers and the architects. Recent

research has proven that the design of the website is very important in attracting

the customer and improving the overall sales. Now, important website decisions

are more likely to be made in the boardroom than the cubicle (Brown, 2003). User

satisfaction depends on website features (Doll and Tozkzadeh , 1988) and hence it

is important to analyze web features of banking services delivered over the

internet.(Jayawardhena and Foley, 2002) suggested that the website features that

should be analysed are: speed of download, content, design, interactivity,

navigation and security features. (Cox and Dale, 2001) examined factors that can

contribute to delivering good service quality through a website are ease of use,

customer confidence, online resources and Relationship services.

20

3.3. LITREATURE

E-BANKING

The inherent properties of internet technology, such as facilitating customer

growth, cost saving, mass customization, innovation and many others, make it an

ideal channel to offer banking products and services (Chong et al., 2010;

Jayawardhena and Foley, 2000). Thus it is not surprising that banker’s strategic

emphasis on the provision of safe and secure web-based solutions has shifted the

focus of competition from a physical to a virtual environment. Moreover the

substantial strategic investment in online banking has not only reduced operational

costs for the banks but also provides greater convenience for customers (Mols,

2000; Rod et al., 2008). Online banking is the process through which a customer

digitally interacts with a bank through computers or other connecting devices

without the need of a human contact (Jayawardhena, 2004). Although the growth

rate remains exceptionally high as reflected by the number of online branches that

have doubled in last five years, the percentage of customers adopting these

services remains below expectations in developed as well as in developing

economies (SBP, 2011b). The lack of customer acceptance of online banking has led

to multiple investigations exploring factors that influence customer adoptability of

these services (Johnson and Marakas, 2000; Pikkarainen et al., 2004; Poon, 2008).

On the other hand, those who believe that the consumer acceptance of online

services is largely dependent on the quality of online services were focused on

measuring consumer perception of online service quality and its subsequent

consequences. Thus it is hardly surprising to see that e-service quality as a topic has

gained significant attention from researchers who believed that providing high-

quality online banking services can serve as a competitive advantage

(Jayawardhena, 2004; Joseph et al., 1999; Jun and Cai, 2001).

In a recent study, Riffat et al. (2012) investigated the dimension of online service

quality of Pakistani banks. Their results suggest that responsiveness, web interface,

web quality, reliability and connectivity are the five dimensions of e-service quality

of Pakistani banks. However, apart from few exceptions, most of these

investigations were descriptive in nature. For example, in a cross-cultural study,

Kassim and Abdullah (2010) compared the casual relationship between service

quality, trust, satisfaction and customer word of mouth among Qatari and

21

Malaysian online consumers. Their results suggested that apart from the effects of

satisfaction on trust, no significant differences were found between the causal

relationships in their model. Nonetheless, little or no attempt was made to

investigate causality between religious and market driven constructs.

E-CUSTOMER SATISFACTION

Even though the relationship between service quality and satisfaction is one of the

most rigorously studied associations in the business literature, it is also a fact that

this association has rarely been explored in an online banking context (Chau and

Ngai, 2010). Similar to service quality, satisfaction can also be defined from

expectation disconfirmation or perception alone paradigm. For example, according

to the expectation disconfirmation model, proposed by Oliver (1980), consumer

expectation before consuming a service serves as a standard to compare it with

actual performance. If a product or service exceeds customer expectations, he/she

will be satisfied. On the other hand, Tse and Wilton (1988), proposed a perceived

performance model. Contrary to the Oliver (1980) conceptualization, consumer

satisfaction is the outcome of the actual performance (Yoon and Uysal, 2005).

Similarly, Jin and Park (2006) also defined e-satisfaction as customer evaluation and

impression of a web site across a range of attributes. This research will also use

performance only definition of e-service satisfaction. Particularly in case of service

industries, survival of a provider heavily depends on the customer’s continuous

usage of its services. Therefore it is logical for a service provider to focus on

retention by providing excellent services (Anderson and Srinivasan, 2003). Banks,

being primarily service organizations, are inevitably compelled by the fact that

meeting and exceeding customer perceptions, regarding their service quality, helps

in avoiding customer churn (Brown and Gulycz, 2001). Lee and Hwan (2005) also

suggest that customer service quality perceptions are among the most important

predictors of satisfaction/dissatisfaction in a Taiwanese banking context.

E-CUSTOMER LOYALTY & E- BANKING QUALITY

22

Loyalty is defined as “a deeply held customer commitment with a product/service

reflected by his purchase repetitions of the same brand while ignoring any other

influences to leave that brand” (Oliver, 1999, p. 34). A strong attitudinal

commitment is a mandatory prerequisite for meaningful customer loyalty (Jacoby

and Chestnut, 1978). Acquiring new customers is primarily a costly exercise.

Therefore, retaining exiting customers by investing in enhancing brand value and

loyalty is still considered as one of the most effective business strategy (Kim et al.,

2004). For example, past research in traditional brick and mortar service context

suggests that improvements in quality of service delivery can directly generate

customer loyalty (Chu and Lu, 2009; Dick and Basu, 1994). In the e-commerce

context the proponents of a direct relationship between service quality and loyalty

argue that online service quality is more technical in its nature and thus can directly

affect customer loyalty. Several past studies empirically explored the direct relation

between service quality and loyalty. For example Oliveira (2007) reported a direct

and significant relationship between customer service quality perceptions and

loyalty in e-banking services. Similarly in a recent study, Lin and Sun (2009) reported

a direct relationship between service quality and e-loyalty in online shopping

context.

TRUST

Trust is a complex, multifaceted construct, making it extremely difficult for scholars

to agree on a common definition (Ibrahim et al., 2009; Rousseau et al., 1998).

Nonetheless, this does not deter researchers from devoting considerable time and

cognitive efforts to define and conceptualize it using diverse approaches (Chopra

and Wallace, 2003; Krauter-Grabner and Kaluscha, 2002). For example, in

marketing context, Rousseau et al. (1998) define trust as “a psychological state

composing the intention to accept vulnerability based on expectations about the

intentions or behaviour of another (p. 395). Cheung and Lee (2001) defined trust

as a customer degree of confidence in the exchange options. Based on this

definition of trust in traditional service industry, Ribbink et al. (2004) presented a

modified version that fits well within the online context. They defined e-trust as a

“degree of confidence a customer has in online exchanges or in the online exchange

channels” (p. 447). Previous studies have indicated that consumer trust remains

23

relevant and important in web-based environments and plays a vital role in

successful management of a firm’s e-businesses (Ibrahim et al., 2009; Kim et al.,

2009). Furthermore, lack of trust is one of the most cited reasons for not purchasing

from internet vendors (Lee and Turban, 2001). Thus it is hardly any surprise to find

that trust plays a very significant 12 IJBM 31,1 role in e-business context, where

consumers are primarily concern about their security and privacy (Anderson and

Swaminathan, 2011).

E-SERVICE QUALITY

Service quality remains a topic of focal interest for both academicians and practitioners. In the service industry, its definitions tend to focus on how well a service provider meets or exceed its customer expectations (Lewis and Booms, 1983). Service quality is defined as “a global judgment or attitude relating to the overall excellence or superiority of the service” (Parasuraman et al., 1988, p. 16). Nonetheless, the meaning and measurement of service quality significantly differs in an online context due to the unique nature of interactions between customer and a service provider (Ribbink et al., 10 IJBM 31,1 2004). In its most simplistic form e-service quality is defined as “As the consumer overall evaluation and judgement of the excellence and the quality of the e-services offering in the virtual marketplace” (Santos, 2003, p. 235). Marketers generally advocate a functional approach, when it comes to the issue of measuring service quality. Their major focus is on customer perception rather than measuring technical aspects of service quality. This is due to the fact that a customer normally analyses and perceives service quality differently as compared to an expert. Therefore, it is inappropriate to use technical measures for gauging customer perceptions about the quality of a service (Donabedian, 1980). This study will also follow the functional approach to measure the e-service quality of Islamic banks. Motivated by the significance of online service quality in contemporary business, several researchers have undertaken rigorous scale development efforts to capture multidimensional construct of e-service quality. For example, the results of a study by Joseph et al. (1999) suggested that online banking service quality has six dimensions. These include convenience and accuracy, feedback and compliant management, efficiency, queue management, accessibility and customization. In their initial research to identify the dimension of online service quality, Zeithaml et al. (2002) found that information availability, ease of use, privacy, web site graphics and

24

reliability are the key dimensions of online service quality (Herington and Weaven, 2007). Despite significant differences in the number and nature of e-service quality dimensions reported in previous literature, its relevance as an important antecedent for some of the most desired outcomes for a service firm, such as customer satisfaction, trust and loyalty, remain constant. The following section will explore the interrelation between e-service quality and e-satisfaction.

ONLINE RELATIONSHIP QUALITY

Introduced by Dwyer and Oh (1987), consolidated by Crosby et al. (1990) and

further refined by many researchers since 1995, relationship quality is an important

concept emerging from research on relationship marketing in a traditional context

(Athanasopoulou, 2009). “Relationship quality can be regarded as a metaconstruct

composed of several key components reflecting the overall nature of relationships

between companies and consumers” (Hennig-Thurau et al., 2002, p. 234). More

specifically, these key components are thought to reflect the extent to which the

relationship is appropriate and, in turn, to determine the extent to which the

relationship marketing outcomes are favorable (Ndubisi et al., 2012). Although the

examined components of relationship quality vary from one study to another,

several research groups in relationship marketing in a traditional context consider

satisfaction, trust and commitment to be the key indicators of this meta construct

or multidimensional construct (e.g. De Wulf et al., 2001; Hennig-Thurau et al., 2002;

Lang and Colgate, 2003; Palmatier et al., 2006; Vesel and Zabkar, 2010). Indeed,

these three dimensions are interrelated (Hennig-Thurau et al., 2002; Palmatier,

2008); more precisely, each dimension captures a different facet of the quality of

the relationship between the consumer and the company (Palmatier, 2008).

Moreover, in their article, De Wulf et al. (2001, p. 36) mention: “we prefer the

abstract relationship quality construct over its more specific dimensions because,

even though these various forms of attitude may be conceptually distinct,

consumers have difficulty making fine distinctions between them and tend to lump

them together.” In keeping with this view, the current study considers online

relationship quality as a multidimensional integrative construct.

25

ONLINE ATTRIBUTES OF THE E-BANKING WEB SITE

Balasubramanian et al. (2003) propose that the virtual attributes of the e-banking

web site create the situational normality which one uses to create trust in the

online environment. They add that attributes such as a well-designed customer

interface provide the cognitive cues for a sense of order. Past studies in this area

have classified online attributes into four factors: perceived security, perceived

privacy, perceived usefulness and perceived ease of use (Koufaris and Hampton-

Sosa, 2004; Hampton-Sosa and Koufaris, 2005; Casalo et al., 2007; Vatanasombut

et al., 2008). In the current study, the authors propose that these four factors

influence trust for e-banking.

In order for a customer to have trust in the online context, including e-banking, a

customer must be made to believe that the transactional medium is secure, and

that any information provided to those web sites are not being intercepted or given

to a third party (Suh and Han, 2003). Studies have found that perceptions of privacy

and security can be influenced by the use of third party assurances, privacy policies

and other security tools (Suh and Han, 2003), and it is these attributes which create

consumers’ perceptions of security and privacy. Such perceptions reinforce the

customer’s views that actions being performed online are the norm and build trust

for the online environment (Jarvenpaa et al., 2000; Koufaris and Hampton-Sosa,

2004; Liu et al., 2005; Casalo et al., 2007; Chen and Barnes, 2007; Vatanasombut et

al., 2008). The “usability” – or the effort required to use a computer system as

defined by Casalo et al. (2007) – of the e-banking web site can also influence a

customer’s confidence in it. It has been found that increased usability reduces the

likelihood of error, increases predictability of the web site’s behaviour, and creates

a comfortable environment which would positively influence customer disposition

towards the web site. Other studies have also purported that the factors of

usefulness and ease of use of a web site function in the same way as a salesperson’s

personal attributes in the creation of trust traditional retailing (Koufaris and

Hampton-Sosa, 2004; Hampton-Sosa and Koufaris, 2005).

TRADITIONAL ATTRIBUTES OF THE BANK

26

A significant proposition forwarded in this study is that trust in e-banking is derived

from structural assurances that a customer infers from the size and reputation of

the bank concerned. The size of an organisation is often regarded as a proxy for

security and trustworthiness. Doney and Cannon (1997) and Jarvenpaa et al. (2000)

purport that if a firm is large, it must have performed well in order to have grown

to such a size. They go further to suggest that customers making an initial decision

to engage in any transaction would expect that larger firms would have more

impetus to deliver, having more to lose if they were to engage in untrustworthy

behaviour. Chen and Dhillon (2003) argue that in the online environment where

the physical cues which consumers can draw trust from are absent, the size of a

firm behind the web site is one of the few ways in which a customer can base their

decision to trust the firm in an e-commerce setting. Moreover, a customer must be

able to believe that the seller has the capacity to deliver the goods or services and

firm size is one of the proxy indicators. Several studies have established the

relationship between firm size and trust for the firm (Doney and Cannon, 1997;

Jarvenpaa et al., 2000; Koufaris and Hampton-Sosa, 2004); nonetheless, a literature

review has not uncovered any study that has examined the relationship between

the size of a bank and trust for its e-banking web site.

27

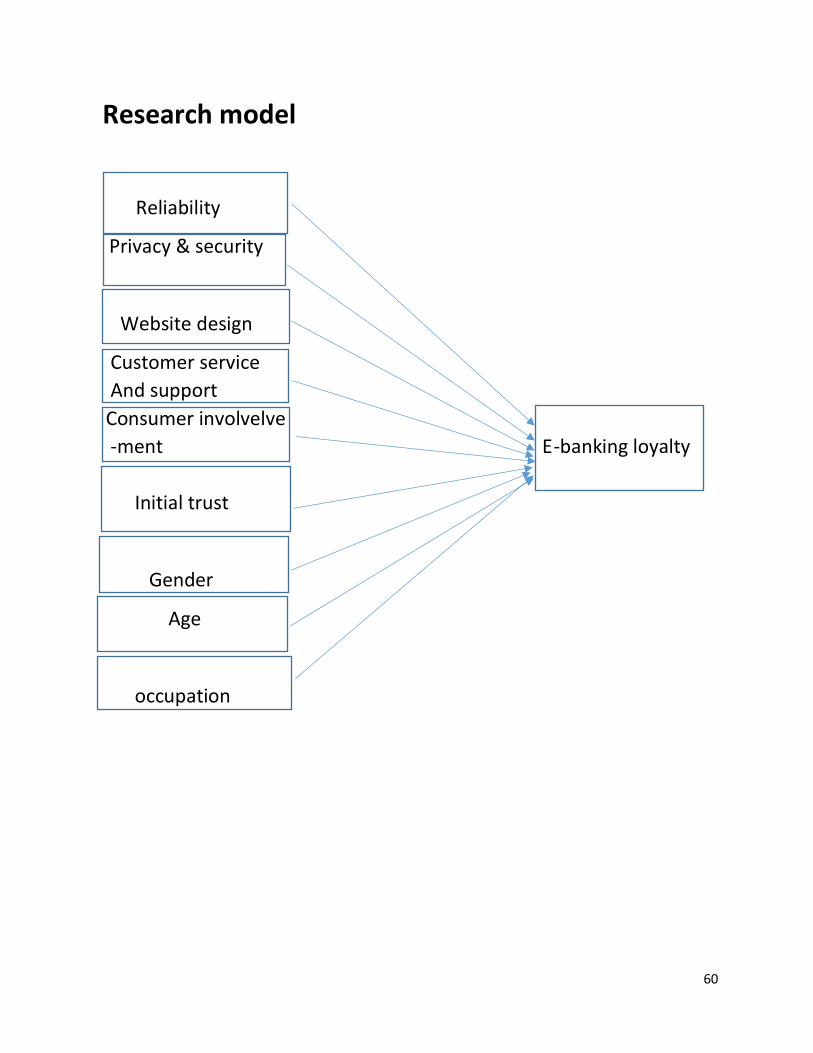

3.4 Research model

Reliability

Privacy & security

Website design

Customer service

And support

Consumer involvelve

-ment E-banking loyalty

Initial trust

Gender

Age

Education level

28

4.Research methodology:

4.1 Problem Statement of the study

This chapter basically describes the objectives of study. It also focuses on how

study has been conducted, the research design used for the study, methods of

selecting and approaching the samples, sources used for the collection of 3data. It

also describes hypothesis used to identify the relationship between variables and

tests applied with the help of statistical tools.

4.2 Objective of the study

To assess the e-banking loyalty

➢ To study and to analyze the awareness of e-banking among residents of India.

➢ To study and to analyze the attitude regarding e-banking loyalty among residents of India.

➢ To identify the factors influencing customer behavior towards e-banking loyalty

➢ To examine the need of e-banking by customers. 4.3 Scope of the Study

Study is designed to find awareness and attitude of customers for e-banking loyalty. Study also tries to identify factors influencing e-banking loyalty for customers. To conduct the study, a sample of 305 respondents has been chosen from four major villages from the State of Gujarat. These are branches of the Gozariya nagrik sahakari bank ltd: Ahmedabad, kharana, solaiya and gozariya. Scope of the study was limited to customers of bank of the Gozariya nagrik sahakari bank ltd.

29

4.4 Hypotheses of the study:

H1. Reliability of e-banking services positively influences customer loyalty to e-banking providers.

H2. Privacy and security of e-banking services positively influences customer loyalty to e-banking providers.

H3. Website design of e-banking services positively influences customer loyalty to e-banking providers.

H4. Customer service and support of e-banking services positively influence customer loyalty to e-banking providers.

H5. Initial trust in e-banking mediates the association between the (a) reliability, (b) privacy and security (c) website design and (d) customer service and support and customer loyalty to e-banking providers.

H6. The mediation effects of initial trust on the association between (a) reliability, (b) privacy and security, (c) website design and customer loyalty to e-banking are stronger at a high level of consumer involvement in e-banking than the low level of involvement and (d) the mediation effects of initial trust on the association between customer service and support and customer loyalty to e-banking are stronger at a low level of consumer involvement in e-banking than the high level of involvement.

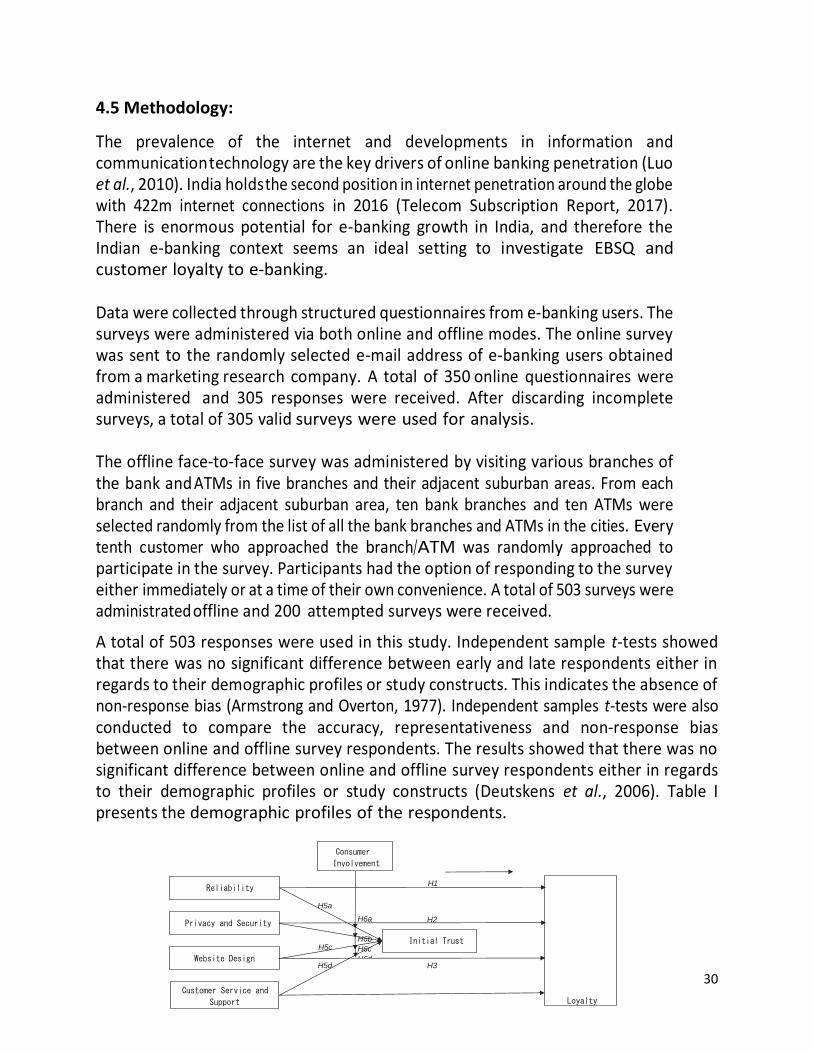

30

H1

H5a

H5c

H6a

H6b

H6c

H6d

H2

H5d H3

Customer Service and

Support

Website Design

Initial Trust

Privacy and Security

Loyalty

Reliability

Consumer

Involvement

4.5 Methodology:

The prevalence of the internet and developments in information and communication technology are the key drivers of online banking penetration (Luo et al., 2010). India holds the second position in internet penetration around the globe with 422m internet connections in 2016 (Telecom Subscription Report, 2017). There is enormous potential for e-banking growth in India, and therefore the Indian e-banking context seems an ideal setting to investigate EBSQ and customer loyalty to e-banking. Data were collected through structured questionnaires from e-banking users. The surveys were administered via both online and offline modes. The online survey was sent to the randomly selected e-mail address of e-banking users obtained from a marketing research company. A total of 350 online questionnaires were administered and 305 responses were received. After discarding incomplete surveys, a total of 305 valid surveys were used for analysis. The offline face-to-face survey was administered by visiting various branches of the bank and ATMs in five branches and their adjacent suburban areas. From each branch and their adjacent suburban area, ten bank branches and ten ATMs were selected randomly from the list of all the bank branches and ATMs in the cities. Every tenth customer who approached the branch/ATM was randomly approached to participate in the survey. Participants had the option of responding to the survey either immediately or at a time of their own convenience. A total of 503 surveys were administrated offline and 200 attempted surveys were received.

A total of 503 responses were used in this study. Independent sample t-tests showed that there was no significant difference between early and late respondents either in regards to their demographic profiles or study constructs. This indicates the absence of non-response bias (Armstrong and Overton, 1977). Independent samples t-tests were also conducted to compare the accuracy, representativeness and non-response bias between online and offline survey respondents. The results showed that there was no significant difference between online and offline survey respondents either in regards to their demographic profiles or study constructs (Deutskens et al., 2006). Table I presents the demographic profiles of the respondents.

31

4.5.1 sampling methodology used: 4.5.1.1 sample frame: For the research purpose following were characteristics of the ideal population:

➢ Person-must aware about e-banking ➢ Gender- Male &female ➢ Age- More than 18 years ➢ Education- At least literate

4.5.1.2 sample size determination:

I created online google form as well as offline questionnaire and circulate that questionnaire

to online platforms and offline customer involvement to collect the data.

4.5.1.3 Measures of the study:

Reliability

Privacy and security

Website design

Customer service and support

Consumer involvement

Initial trust

Gender

Age

Education level

e-banking loyalty

32

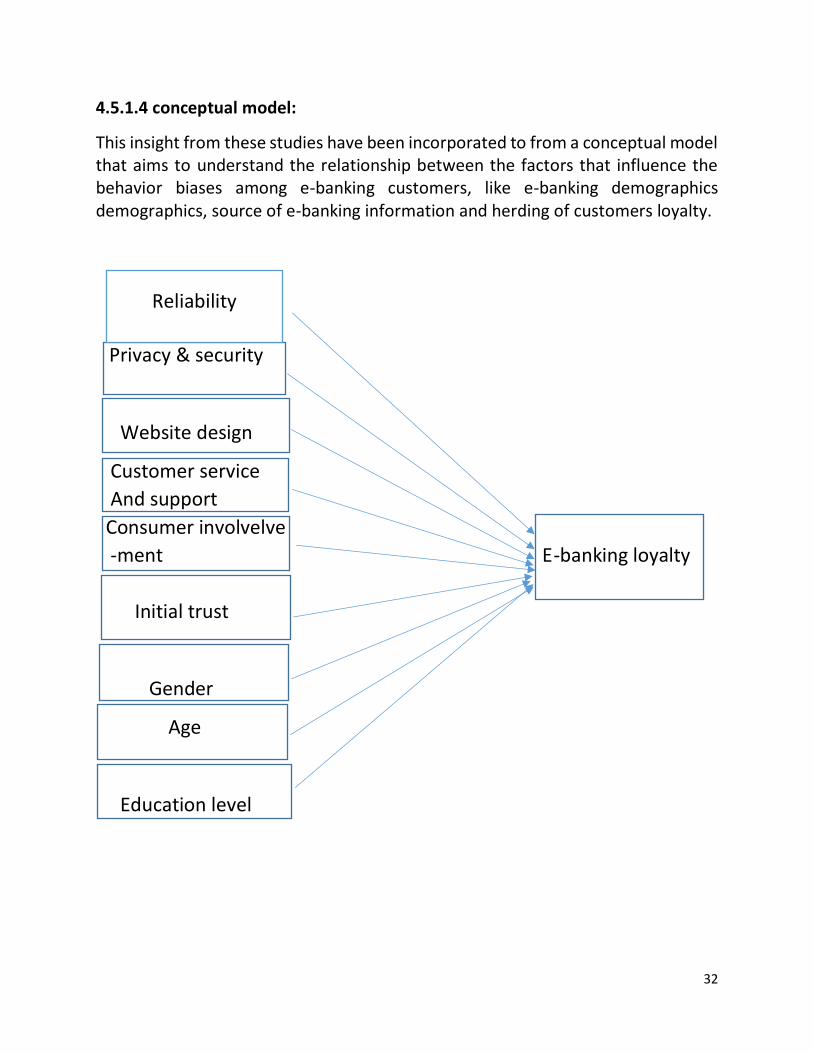

4.5.1.4 conceptual model:

This insight from these studies have been incorporated to from a conceptual model that aims to understand the relationship between the factors that influence the behavior biases among e-banking customers, like e-banking demographics demographics, source of e-banking information and herding of customers loyalty.

Reliability

Privacy & security

Website design

Customer service

And support

Consumer involvelve

-ment E-banking loyalty

Initial trust

Gender

Age

Education level

Reliability

33

4.6 Variable:

e-banking loyalty towards the customers as dependent variable whereas Age, gender, Reliability, privacy and security, monthly income, education level, customer service and support, consumer involvement, initial trust are the independent variables that influence the e-banking loyalty. The research model developed by the writers will serve as a basis for this research and it will help in analyzing and interpreting the empirical results.

4.7 layout of questionnaire:

The questionnaire is carefully designed to meet the requirements of the research. The questions are taken from previous literature on with a view to validate the research more. The questionnaire consists of two main parts; first is basic information of respondents & second is people responses which include the different responses given by the respondents.

In the first part basic information of respondents such as age, gender, Name Information source and use of e-banking loyalty were include, which were helpful in obtaining the demographic & personal information of the respondents. And for the answers of these questions different options were provided to respondents from which they need to select any one pertaining options.

Second part include people response. in second part different question regarding independent variable related data included. Second part in customer awareness about e-banking about e-banking loyalty data related data include. in sample data how much people keep track of banking websites on a regular basis.in sample data how much people put money aside for saving future purchases or emergences in the bank and how muchj they withdraw their money from the use of e-banking websites and services.in data how much people pay credit card bills on that time each month and am most never latter in uses of websites.in sample data how much people comparison shop or buy things on online basis scale .in sample data people interested are increasing your e-banking knowledge. in sample data people which topic would be interested in learning about e-banking loyalty .

34

4.8 Data collection:

4.8.1 Methods of data collection:

• Primary data:

Primary data was collected from the Various area and from 305 respondents. For

primary data collection online and offline questionnaire survey was conducted. Link

of the online questionnaire was sent to respondents using different social media.

• Secondary data:

For the purpose of secondary data collection, around 30 research papers related to

topic of e-banking loyalty.

35

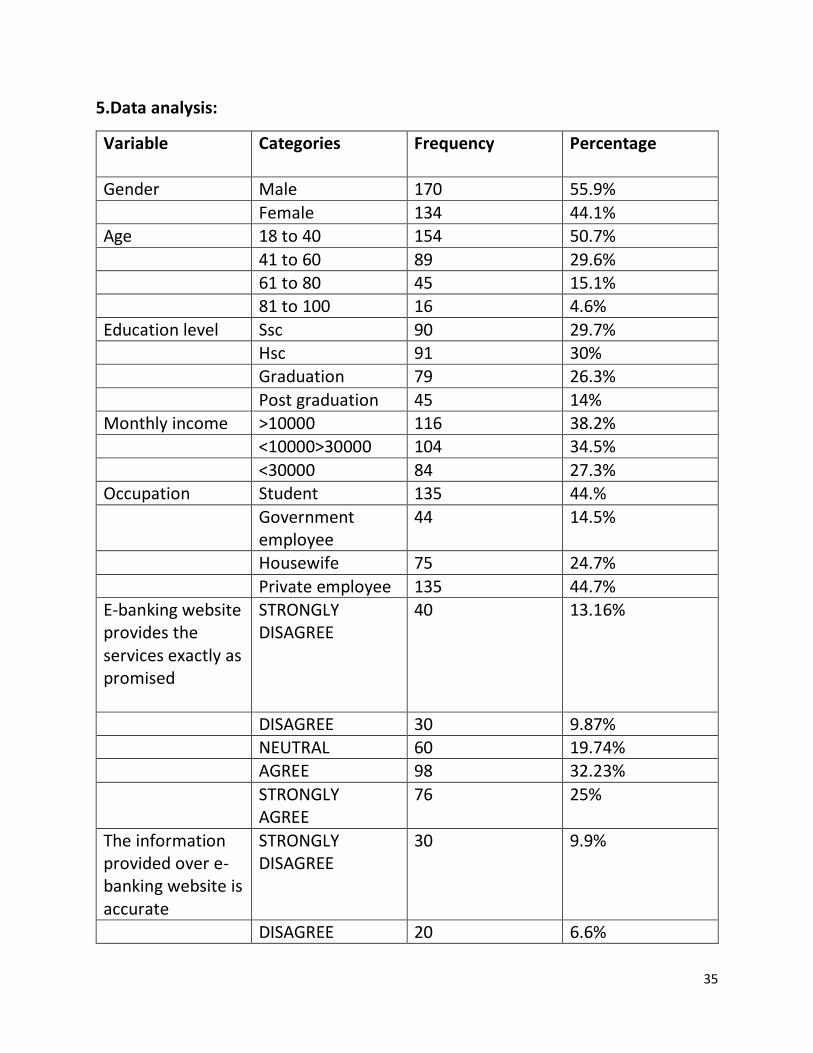

5.Data analysis:

Variable Categories Frequency Percentage

Gender Male 170 55.9%

Female 134 44.1% Age 18 to 40 154 50.7%

41 to 60 89 29.6% 61 to 80 45 15.1% 81 to 100 16 4.6%

Education level Ssc 90 29.7% Hsc 91 30%

Graduation 79 26.3%

Post graduation 45 14% Monthly income >10000 116 38.2% <10000>30000 104 34.5%

<30000 84 27.3% Occupation Student 135 44.%

Government employee

44 14.5%

Housewife 75 24.7%

Private employee 135 44.7% E-banking website provides the services exactly as promised

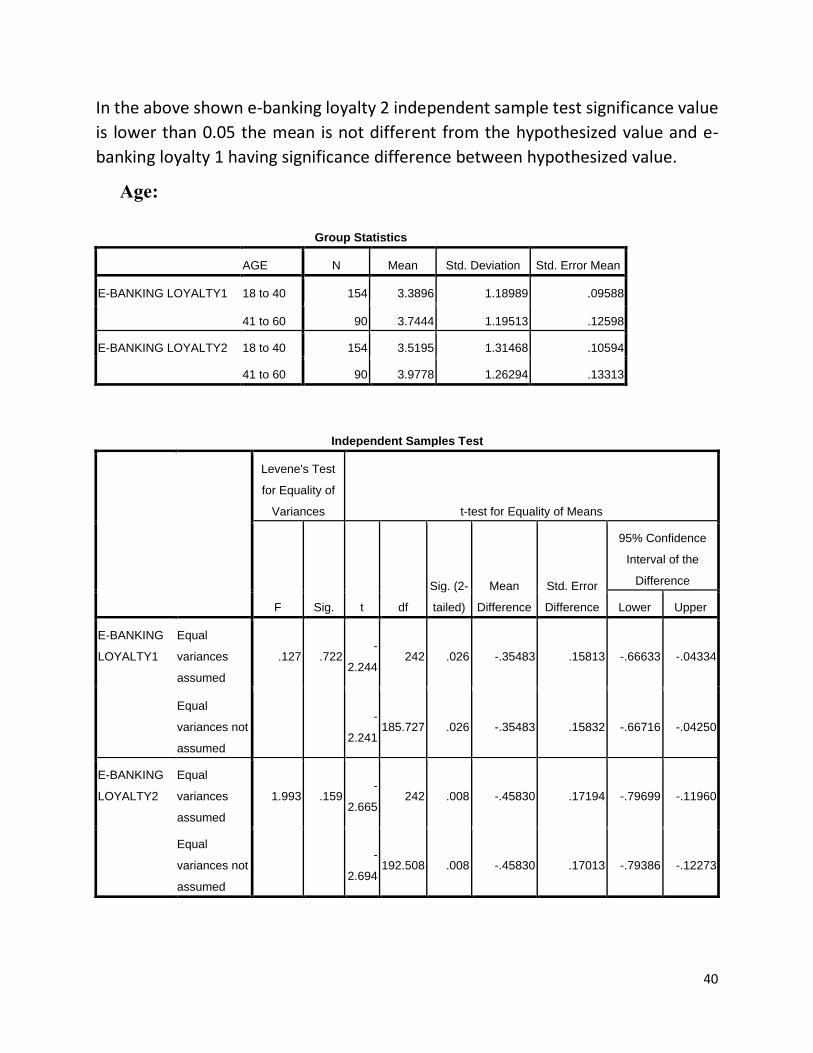

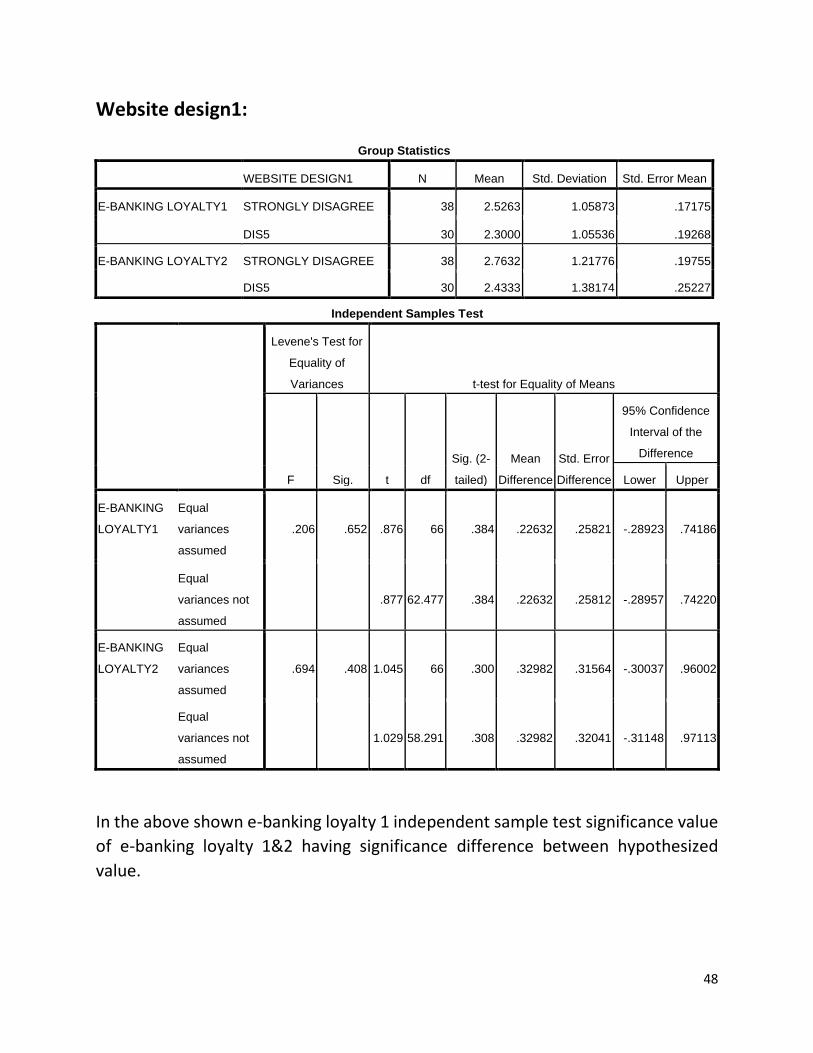

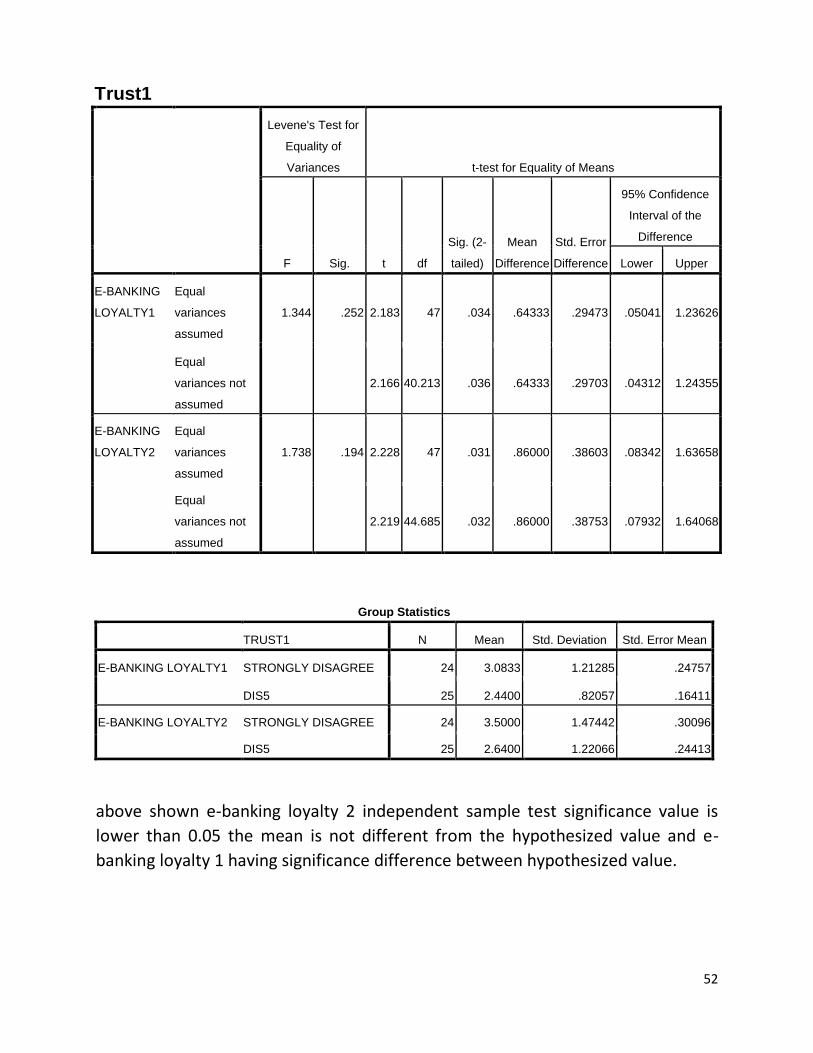

In the above shown e-banking loyalty independent sample test significance value

of e-banking loyalty 1&2 having no significance difference between hypothesized

value.

56

6.Finding:

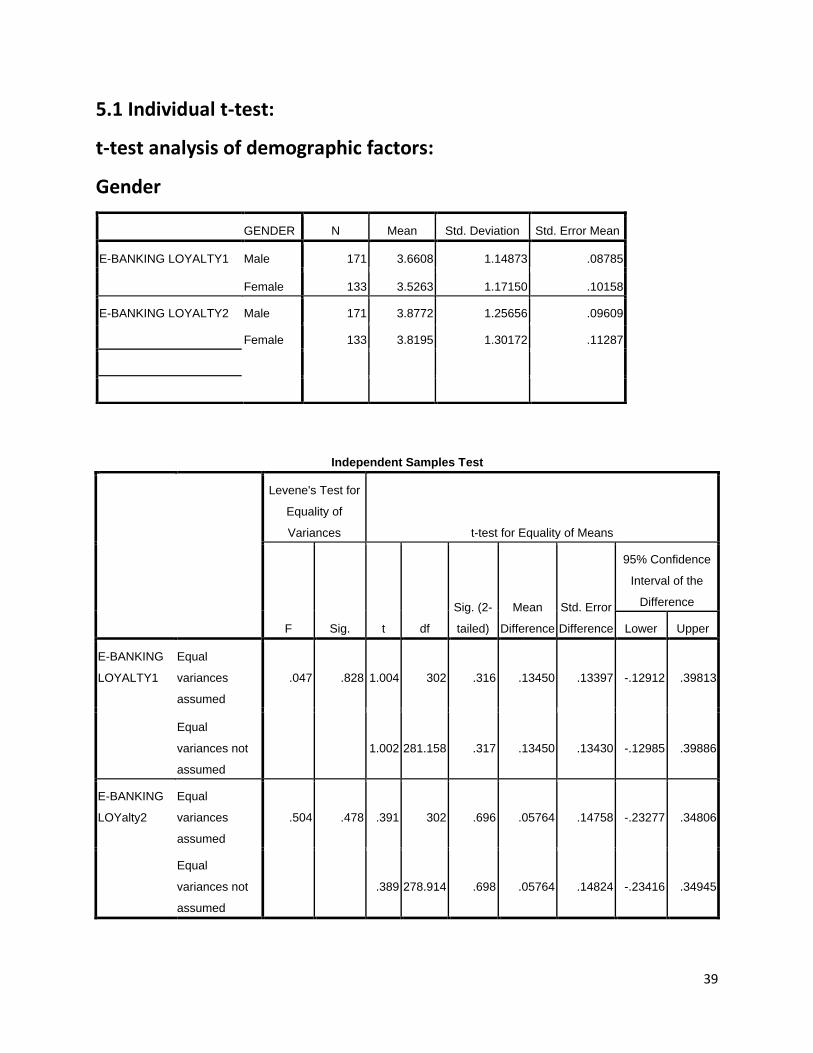

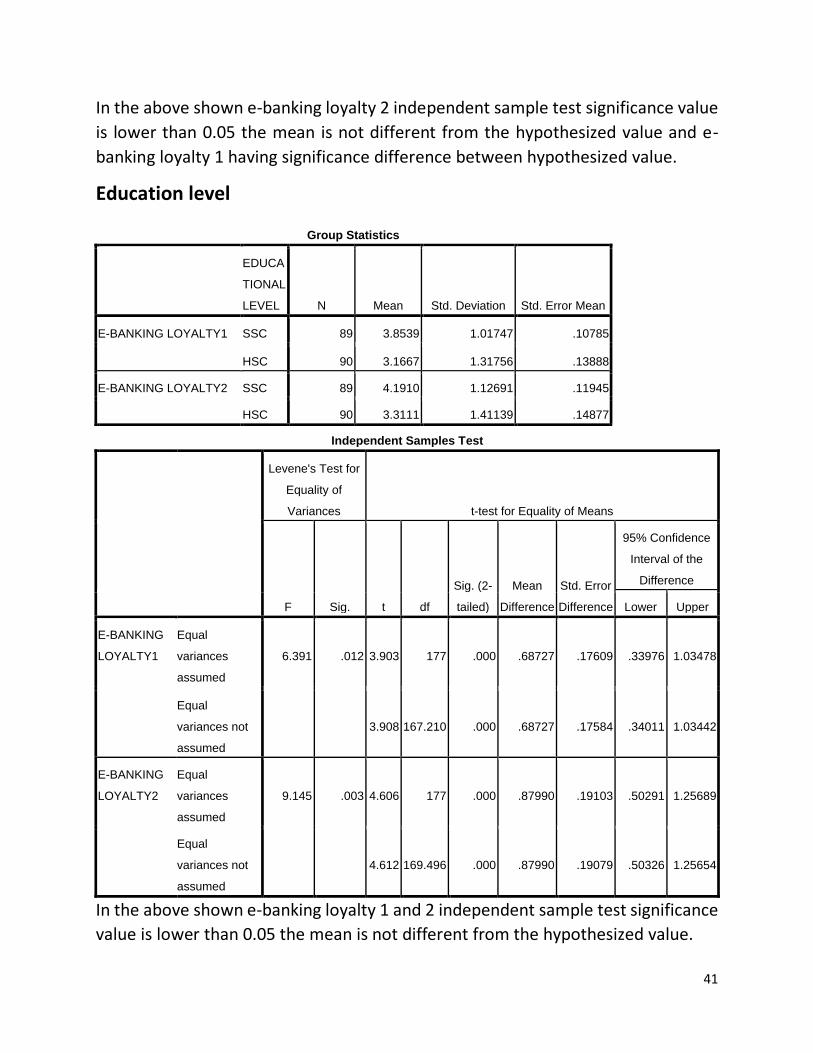

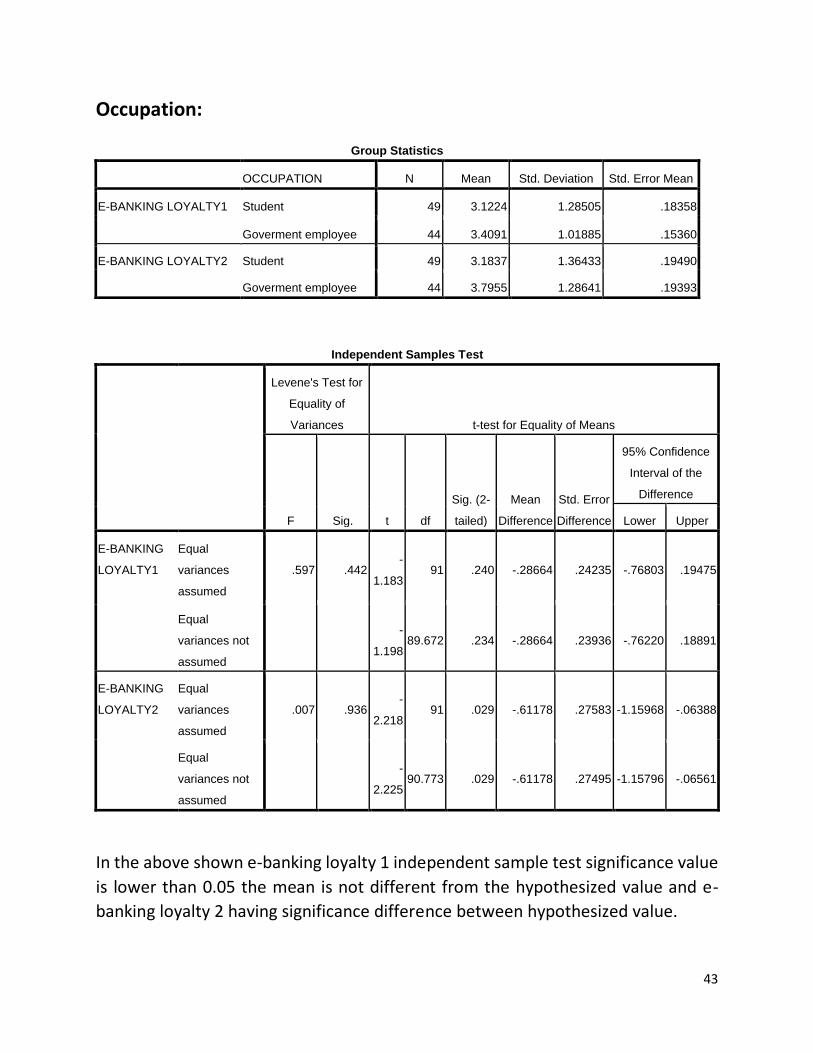

➢ Since p-value is less than 0.05,the null hypothesis (the ability of the service provider to performed the promised services accurately and consistently) is rejected at 5% level of significance with respect to education level (.12)(.003),but other dimensions are not associated with respect to occupation (.442)(.936), gender (.828)(.478), age(.722 )(159).

➢ Since p-value is less than 0.05,the null hypothesis (the ability of the service provider to performed the promised services accurately and consistently) is rejected at 5% level of significance with respect to reliability (0.43)(0.79),privacy and security (0.60)(0.112),but other dimensions are not associated with dimensions of e-banking loyalty with respect to website design (.652)(.408),trust (.252)(.194),customer service and support(.213)(.184).

➢ There is a greater number of males than females, who mostly aware about e-banking loyalty.

➢ P-value is (.000)is less than 0.01 which hypothesis is rejected hence there is a positive relationship between consumer involvement(.000) and e-banking loyalty.

➢ It is find that in research Younger generation has been found to using knowledge of e-banking than other age groups.

➢ Highest number of people is having the income below 10000 per month from the respondents.

➢ It is found that the gender of a person does not create any difference among the knowledge of e-banking. It means there will not be any differences in knowledge in males and females.

➢ It is found that age of a person does not creates a difference in the knowledge.

➢ Education level of people do have impact on the e-banking. It means that people having different education will have different knowledge of e-banking loyalty.

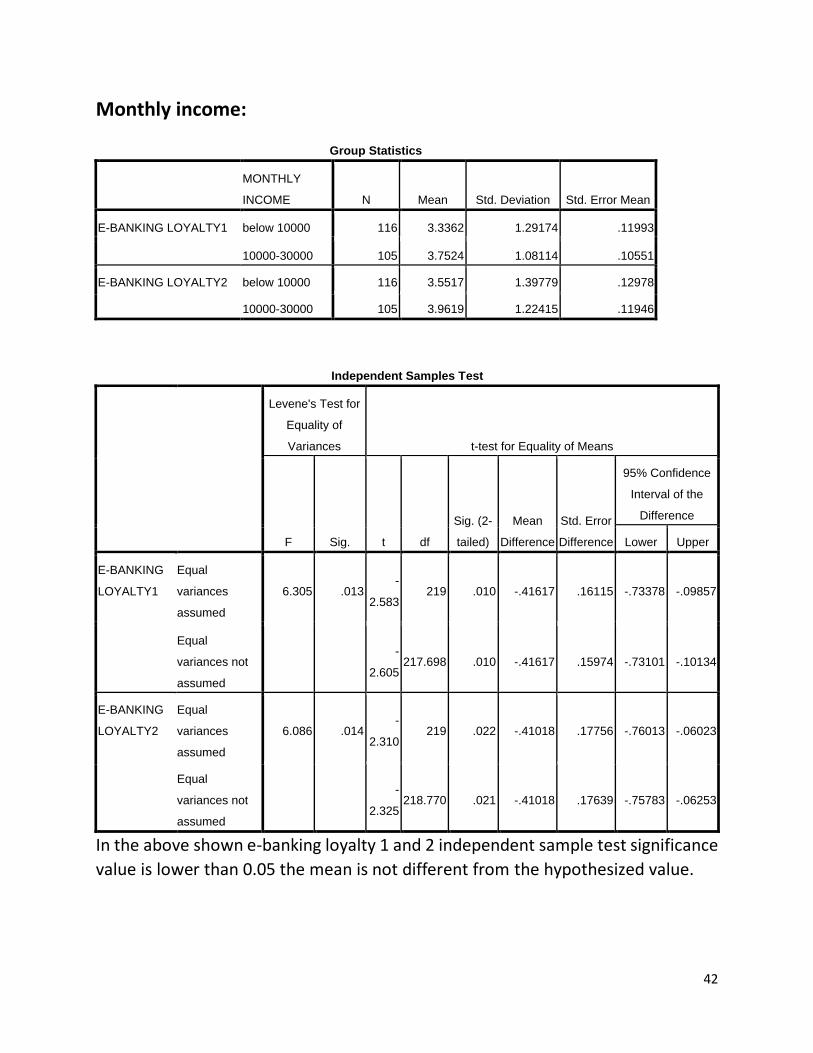

➢ It Found that Monthly income create differential impact on the e-banking. It means that there is difference in the people of different Monthly Income groups.

➢ Information Source does not create any differential impact on the importance of or knowledge of e-banking among working customers.

57

6.1 reference

➢ Ahmad Al-Hawari, M. (2014), “Does customer sociability matter? Differences

in e-quality, e-satisfaction, and e-loyalty between introvert and extravert online banking users”, Journal of Services Marketing, Vol. 28 No. 7, pp. 538-546.

➢ Akbar, M.M. and Parvez, N. (2009), “Impact of service quality, trust, and customer satisfaction on customers loyalty”, ABAC Journal, Vol. 29 No. 1, pp. 24-38.

➢ Al-Alak, B.A. (2014), “Impact of marketing activities on relationship quality in the Malaysian banking sector”, Journal of Retailing and Consumer Services, Vol. 21 No. 3, pp. 347-356.

➢ Algharabat, R., Rana, N.P., Dwivedi, Y.K., Alalwan, A.A. and Qasem, Z. (2018), “The effect of telepresence, social presence and involvement on consumer brand engagement: an empirical study of non-profit organizations”, Journal of Retailing and Consumer Services, Vol. 40 No. 1, pp. 139-149.

➢ Al-Hawari, M.A. (2015), “How the personality of retail bank customers interferes with the relationship between service quality and loyalty”, International Journal of Bank Marketing, Vol. 33 No. 1, pp. 41-57.

➢ Amin, M. (2016), “Internet banking service quality and its implication on e-customer satisfaction and e-customer loyalty”, International Journal of Bank Marketing, Vol. 34 No. 3, pp. 280-306.

➢ Arcand, M., PromTep, S., Brun, I. and Rajaobelina, L. (2017), “Mobile banking service quality and customer relationships”, International Journal of Bank Marketing, Vol. 35 No. 7, pp. 1068-1089.

➢ Armstrong, J.S. and Overton, T.S. (1977), “Estimating nonresponse bias in mail surveys”, Journal of Marketing Research, Vol. 14 No. 3, pp. 396-402.

➢ Ayo, C.K., Oni, A.A., Adewoye, O.J. and Eweoya, I.O. (2016), “E-banking users’ behaviour: e-service quality, attitude, and customer satisfaction”, International Journal of Bank Marketing, Vol. 34 No. 3, pp. 347-367.

➢ Bauer, H.H., Hammerschmidt, M. and Falk, T. (2005), “Measuring the quality of e-banking portals”,

➢ International Journal of Bank Marketing, Vol. 23 No. 2, pp. 153-175. ➢ Behe, B.K., Bae, M., Huddleston, P.T. and Sage, L. (2015), “The effect of

involvement on visual attention and product choice”, Journal of Retailing and Consumer Services, Vol. 24 No. 3, pp. 10-21.

➢ Blut, M., Beatty, S.E., Evanschitzky, H. and Brock, C. (2014), “The impact of service characteristics on the switching costs–customer loyalty link”, Journal of Retailing, Vol. 90 No. 2, pp. 275-290.

➢ Blut, M., Frennea, C.M., Mittal, V. and Mothersbaugh, D.L. (2015), “How procedural, financial and relational switching costs affect customer satisfaction, repurchase intentions, and repurchase behavior: a meta-analysis”, International Journal of Research in Marketing, Vol. 32 No. 2, pp. 226-229.

➢ Bowen, J.T. and Chen McCain, S.L. (2015), “Transitioning loyalty programs: a commentary on ‘the relationship between customer loyalty and customer satisfaction’ ”, International Journal of Contemporary Hospitality Management, Vol. 27 No. 3, pp. 415-430.

58

➢ Brady, M.K. and Robertson, C.J. (2001), “Searching for a consensus on the antecedent role of service quality and satisfaction: an exploratory cross-national study”, Journal of Business Research, Vol. 51 No. 1, pp. 53-60.

➢ Breugelmans, E. and Campo, K. (2011), “Effectiveness of in-store displays in a virtual store environment”, Journal of Retailing, Vol. 87 No. 1, pp. 75-89.

➢ Brun, I., Rajaobelina, L. and Ricard, L. (2014), “Online relationship quality: scale development and initial testing”, International Journal of Bank Marketing, Vol. 32 No. 1, pp. 5-27.

➢ Butt, M.M. and Aftab, M. (2013), “Incorporating attitude towards Halal banking in an integrated service quality, satisfaction, trust and loyalty model in online Islamic banking context”, International Journal of Bank Marketing, Vol. 31 No. 1, pp. 6-23.

➢ Byrne, B.M. (2009), Structural Equation Modeling with AMOS: Basic Concepts, Applications, and Programming, 2nd ed., Taylor & Francis, New York, NY.

➢ Cai, S. and Jun, M. (2003), “Internet users’ perceptions of online service quality: a comparison of online buyers and information searchers”, Managing Service Quality: An International Journal, Vol. 13 No. 6, pp. 504-519.

➢ Cases, A.S., Fournier, C., Dubois, P.L. and Tanner, J.F. (2010), “Web Site spill over to email campaigns: the role of privacy, trust and shoppers’ attitudes”, Journal of Business Research, Vol. 63 No. 9, pp. 993-999.

➢ Cheung, G.W. and Lau, R.S. (2008), “Testing mediation and suppression effects of latent variables: bootstrapping with structural equation models”, Organizational Research Methods, Vol. 11 No. 2, pp. 296-325.

➢ Coetzee, J., Van Zyl, H. and Tait, M. (2013), “Perceptions of service quality by clients and contact- personnel in the South African retail banking sector”, Southern African Business Review, Vol. 17 No. 1, pp. 1-22.

➢ CoX, J. and Dale, B.G. (2001), “Service quality and e-commerce: an exploratory analysis”, Managing Service Quality: An International Journal, Vol. 11 No. 2, pp. 121-131.

➢ Cronin, J.J. Jr and Taylor, S.A. (1992), “Measuring service quality: a reexamination and extension”,

➢ Journal of Marketing, Vol. 56 No. 3, pp. 55-68. ➢ Demirci-Orel, F. and Kara, A. (2015), “Assessing the role of service quality of retail

self-checkouts on customer satisfaction and loyalty: empirical evidence from an emerging market”, in Robinson, L. (Ed.), Marketing Dynamism & Sustainability: Things Change, Things Stay the Same, Springer

➢ International Publishing, Baltimore, MD, p. 226.

59

7.conclusion

As per research report, there are independent variables for one dependent

variable that E-BANKING LOYALTY as following;

➢ Gender

➢ Age

➢ Occupation

➢ Monthly income

➢ Educational level of individual

➢ Reliability

➢ Privacy and security

➢ Website design

➢ Customer service and support

➢ Consumer involvement

➢ Initial trust

➢ knowledge is also an important factor. So, people will have more

knowledge about e-banking.

➢ Education level of individual is also important for knowledge of e-

banking.

➢ In demographic factors age, education, income, type of functions use

are important factors for e-banking loyalty.

60

Research model

Reliability

Privacy & security

Website design

Customer service

And support

Consumer involvelve

-ment E-banking loyalty

Initial trust

Gender

Age

occupation

61

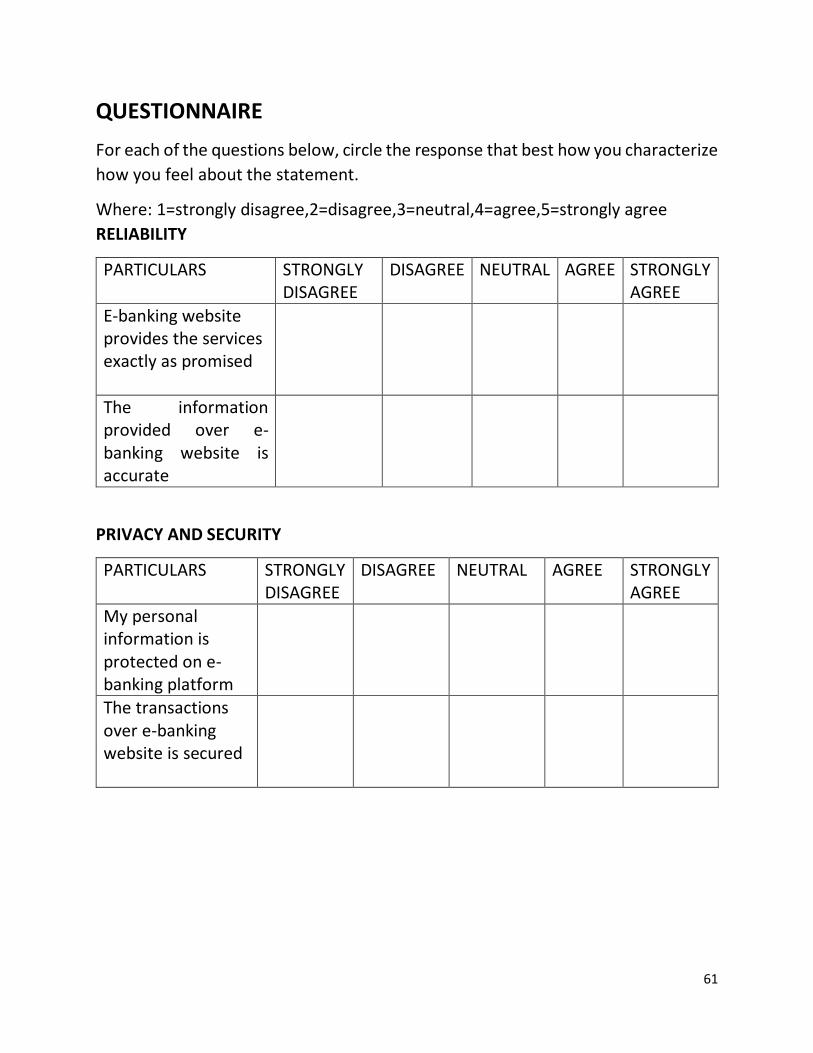

QUESTIONNAIRE

For each of the questions below, circle the response that best how you characterize