31

SUNTRUST SAVINGS & LOANS LIMITED ANNUAL REPORT AND ACCOUNTS December 31 2012 Aminu Ibrahim & Co Chartered Accountants

SUNTRUST SAVINGS & LOANS LIMITED

ANNUAL REPORT AND ACCOUNTS December 31 2012

Aminu Ibrahim & Co Chartered Accountants

SUNTRUST SAVINGS AND LOANS LIMITED

REPORT OF THE DIRECTORS AND AUDITED FINANCIAL STATEMENTS

FOR THE YEAR ENDED DECEMBER 31, 2012

CONTENTS PAGE

Financial Highlights 1

Directors and Advisers 2

Report of the Directors 3

Audited Financial Statements:

-Report of the Independent Auditors 6

-Statement of Significant Accounting Policies 8

-Balance Sheet 12

-Profit and Loss Account 13

-Statement of Cash Flows 14

-Notes to the Financial Statements 15

-Statement of Value Added 26

-Financial Summary 27

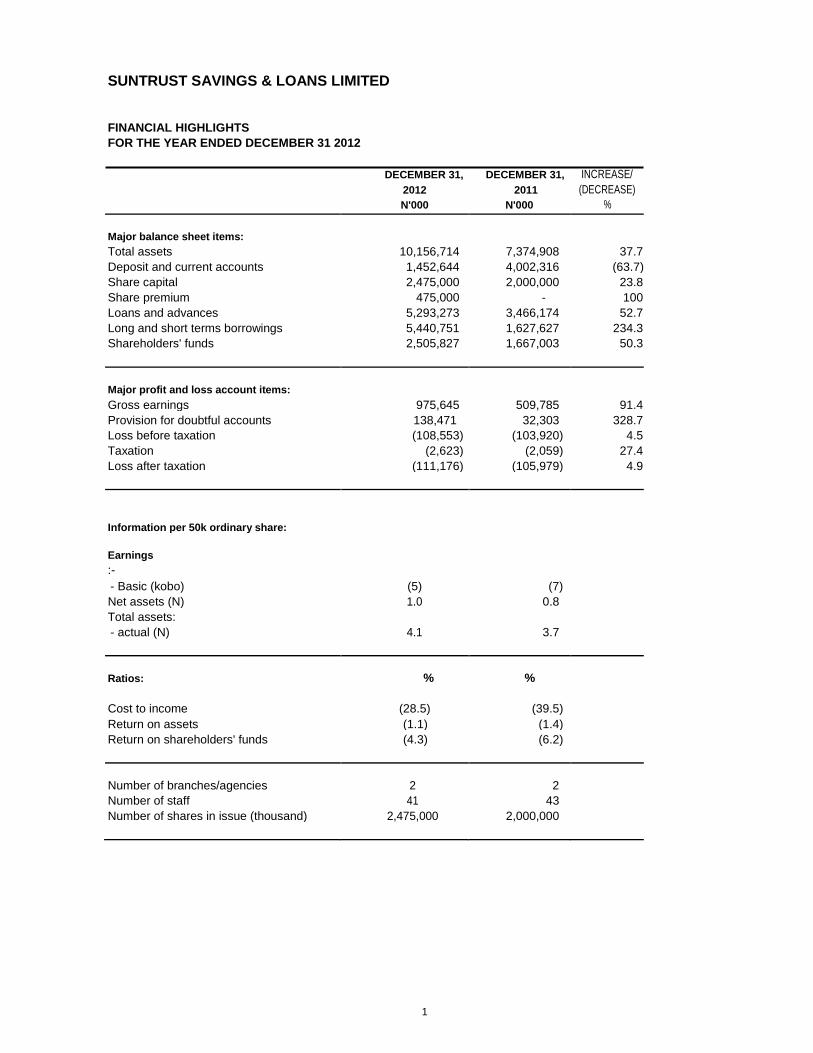

SUNTRUST SAVINGS & LOANS LIMITED FINANCIAL HIGHLIGHTS FOR THE YEAR ENDED DECEMBER 31 2012 DECEMBER 31, DECEMBER 31, INCREASE/ 2012 2011 (DECREASE) N'000 N'000 %

Major balance sheet items: Total assets 10,156,714 7,374,908 37.7 Deposit and current accounts 1,452,644 4,002,316 (63.7) Share capital 2,475,000 2,000,000 23.8 Share premium 475,000 - 100 Loans and advances 5,293,273 3,466,174 52.7 Long and short terms borrowings 5,440,751 1,627,627 234.3 Shareholders' funds 2,505,827 1,667,003 50.3

Major profit and loss account items: Gross earnings 975,645 509,785 91.4 Provision for doubtful accounts 138,471 32,303 328.7 Loss before taxation (108,553) (103,920) 4.5 Taxation (2,623) (2,059) 27.4 Loss after taxation (111,176) (105,979) 4.9

Information per 50k ordinary share:

Earnings :-

- Basic (kobo) (5) (7)

Net assets (N) 1.0 0.8

Total assets:

- actual (N) 4.1 3.7

Ratios: % %

Cost to income (28.5) (39.5) Return on assets (1.1) (1.4)

Return on shareholders' funds (4.3) (6.2)

Number of branches/agencies 2 2 Number of staff 41 43

Number of shares in issue (thousand) 2,475,000 2,000,000

1

SUNTRUST SAVINGS AND LOANS LIMITED

DIRECTORS AND ADVISERS FOR THE YEAR ENDED DECEMBER 31, 2012

DIRECTORS: Kenneth Ofili - Chairman Muhammad Jibrin - Managing Director/CEO

Yunusa Yakubu - Director Abubakar Sadiq Mohammed - Director Nasiru A. Dantata - Director

COMPANY SECRETARY Omega Reigns Chambers

REGISTERED OFFICE: 6, Dar-Es-Salaam Street

Off Aminu Kano Crescent Wuse II Abuja

AUDITORS: Aminu Ibrahim & Co. [Chartered Accountants] City Plaza, 3rd Floor Plot 596 Ahmadu Bello Way Garki II, Abuja

2

SUNTRUST SAVINGS AND LOANS LIMITED

REPORT OF THE DIRECTORS FOR THE YEAR ENDED DECEMBER 31, 2012

The Directors have pleasure in presenting to the members of mortgage bank their report and the audited financial statements for the year ended December 31, 2012. CORPORATE STRUCTURE AND BUSINESS

The Bank was incorporated on February 12, 2009 as a Private Limited Liability Company in accordance with the provisions of the Companies and Allied Matters Act. It was licensed to operate as a Mortgage Institution in March 2009 and commenced operations in January 2010. It is wholly owned by Nigerian corporate and individual citizens.

RESULT

The Bank’s results are shown as follows: 2012 N ’000

Loss after taxation (111,176)

Less: Appropriations

Transfer to statutory reserve - ------------ Loss for the period transferred to general reserve (111,176)

======= PRINCIPAL ACTIVITIES

The Bank engages in the business of mortgage banking.

STATE OF AFFAIRS

In the opinion of the Directors, the state of the mortgage bank's affairs is satisfactory and no event

has occurred since the balance sheet date, which would affect the financial statements as presented.

FIXED ASSETS

Information relating to changes in fixed assets is given in Note 8 to the financial statements.

3

SUNTRUST SAVINGS AND LOANS LIMITED REPORT OF THE DIRECTORS (CONTINUED) FOR THE YEAR ENDED DECEMBER 31, 2012 DIRECTORS' INTERESTS

The interest of the Directors in the issued share capital of the mortgage bank as recorded in the register of Director’s holding as at December 31, 2012 are as follows:

Names 2012 (units) 2011 (units)

Abubakar Saddiq Mohammed 50,000,000 50,000,000

Kenneth Ofili 50,000,000 50,000,000

Muhammad Jibrin 5,000,000 -

SIGNIFICANT SHAREHOLDERS

Names % holdings % holdings

(2012) (2011)

Midland Corporate Investments Limited 54 67

Afric Capital Limited 13 -

Pinnacle Prime Concepts & Investments Limited 10 12

Suntrust Real Estate Investment Limited 6 -

Tijara Resources Limited 4 5

Various individuals having less than 4% each 13 16

RESPONSIBILITIES OF DIRECTORS In accordance with the provisions of sections 334 and 335 of the Companies and Allied Matters Act and the requirements of Bank and Other Financial Institutions Act 2004. Directors are responsible for the preparation of financial statements which give a true and fair view of the state of affairs of the Bank as at the end of the financial year and of its financial performance for the year and comply with the provisions of the Act. These responsibilities include ensuring that:

i) adequate internal control procedures are instituted to safeguard assets and prevent and detect

fraud and other irregularities; ii) proper accounting records are maintained and applicable accounting standards followed; iii) suitable accounting policies are used and consistently applied; iv) the financial statements are prepared on a going concern basis unless it is inappropriate to

presume that the Company will continue in business.

4

SUNTRUST SAVINGS AND LOANS LIMITED REPORT OF THE DIRECTORS (CONTINUED) FOR THE YEAR ENDED DECEMBER 31, 2012

EMPLOYEES INVOLVEMENT The mortgage bank is committed to keeping employees fully informed as far as possible regarding the mortgage bank’s performance and progress and seeking their views wherever practicable on matters, which particularly affect them as employees.

Management, professional and technical expertise are the mortgage bank’s major assets and investment in developing such skills continues.

EMPLOYMENT OF PHYSICALLY CHALLENGED PERSONS No physically challenged person was employed by the mortgage bank during the year. It is however the mortgage bank's policy to consider such persons for employment if academically and medically qualified.

HEALTH, SAFETY OF EMPLOYEES

Health and safety regulations are enforced within the mortgage bank’s premises and employees are aware of the safety regulations.

DONATION

The mortgage bank did not make any donation during the year.

AUDITORS

Messrs Aminu Ibrahim & Co. have expressed their willingness to continue in office as auditors in accordance with Section 357(2) of the Companies and Allied Matters Act. BY ORDER OF THE BOARD

5

City Plaza, 3rd Floor

Aminu Ibrahim & Co Plot 596, Ahmadu Bello Way

P.O. Box 971, Garki II,

Abuja, Nigeria

Chartered Accountants Tel: +234 9 8706058, 3145724

www.aminuibrahim.com

REPORT OF THE INDEPENDENT AUDITORS TO THE MEMBERS OF SUNTRUST SAVINGS & LOANS LIMITED Report on the Financial Statements We have audited the accompanying financial statements of Suntrust Savings & Loans Limited which comprise the balance sheets as at December 31, 2012 and the profit and loss accounts and cash flow statements for the year then ended and a summary of significant accounting policies and other explanatory notes. Directors' Responsibility for the Financial Statements The Directors are responsible for the preparation and fair presentation of these financial statements. This responsibility includes designing, implementing and maintaining internal controls relevant to the preparation and fair presentation of financial statements that are free of material misstatement, whether due to fraud or error; selecting and applying appropriate accounting policies; and making accounting estimates that are reasonable in the circumstances. Auditors’ Responsibility Our responsibility is to express an opinion on these financial statements based on our audit. We conducted our audit in accordance with International Standards on Auditing and Nigerian Standards on Auditing issued by the Institute of Chartered Accountants of Nigeria, which require that we comply with ethical requirements and plan and perform the audit to obtain reasonable assurance whether the financial statements are free of material misstatement. An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the financial statements. The procedures selected depend on the auditors’ judgment, including the assessment of the risks of material misstatement of the financial statements, whether due to fraud or error. In making those risk assessments, the auditors consider internal control relevant to the entity's preparation and fair presentation of the financial statements in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the entity's internal control. An audit also includes evaluating the appropriateness of accounting policies

used and the reasonableness of accounting estimates made by directors, as well as evaluating the overall presentation of the financial statements. We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinion. Opinion In our opinion, the financial statements give a true and fair view of the financial position of Suntrust Savings & Loans Limited as at 31 December 2012, and of its financial performance and its cash flows for the year then ended in accordance with relevant accounting standards issued by the Financial Reporting Council of Nigeria, relevant circulars issued by the Central Bank of Nigeria, Companies and Allied Matters Act and the Banks and Other Financial Institutions Act.

6

Aminu Ibrahim & Co Chartered Accountants

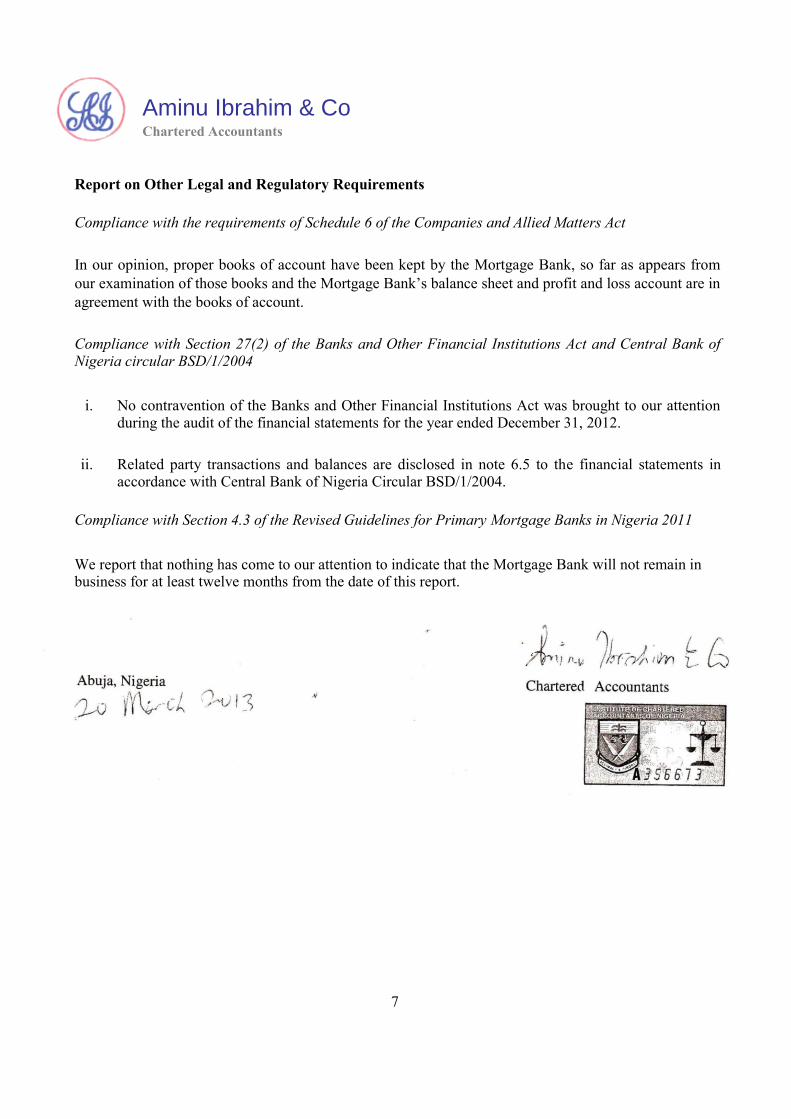

Report on Other Legal and Regulatory Requirements

Compliance with the requirements of Schedule 6 of the Companies and Allied Matters Act

In our opinion, proper books of account have been kept by the Mortgage Bank, so far as appears from

our examination of those books and the Mortgage Bank’s balance sheet and profit and loss account are in

agreement with the books of account.

Compliance with Section 27(2) of the Banks and Other Financial Institutions Act and Central Bank of Nigeria circular BSD/1/2004

i. No contravention of the Banks and Other Financial Institutions Act was brought to our attention during the audit of the financial statements for the year ended December 31, 2012.

ii. Related party transactions and balances are disclosed in note 6.5 to the financial statements in accordance with Central Bank of Nigeria Circular BSD/1/2004.

Compliance with Section 4.3 of the Revised Guidelines for Primary Mortgage Banks in Nigeria 2011 We report that nothing has come to our attention to indicate that the Mortgage Bank will not remain in business for at least twelve months from the date of this report.

7

SUNTRUST SAVINGS & LOANS LIMITED STATEMENT OF SIGNIFICANT ACCOUNTING POLICIES FOR THE YEAR ENDED DECEMBER 31, 2012 The accounting policies adopted in the preparation of these financial statements are set out below:

a) Basis of accounting

The financial statements have been prepared under the historical cost convention and comply with the Statements of Accounting Standards issued by the Nigerian Accounting Standards Board (now Financial Reporting Council of Nigeria).

b) Fixed Assets

Fixed assets are stated at costs less accumulated depreciation. Depreciation is calculated on straight line basis to write-off the cost of assets over their estimated useful lives as following:

%

Office furniture, fitting and equipment 20 Computer hardware 33.3 Motor vehicles 25 Plant and machinery 20

No depreciation is provided on assets under construction. Gain or loss arising from the disposal of fixed assets is included in the profit and loss account.

c) Loans and advances

Loans and advances are carried at cost less provision for impairment and are recognised when cash is advanced to borrowers. Loan impairment provision is made in accordance with the Revised Guidelines for Primary Mortgage Banks in Nigeria 2011 issued by the Central Bank of Nigeria for each account that is not performing in accordance with the terms of the related facility as follows:

Mortgage loans:

Interest and/or Principal outstanding for over Classification Provision 3 months but less than 6 months Watchlist 1% 6 months but less than 1 year Substandard 10% 1 year but less than 2 years Doubtful 100% less 50% of the estimated net realizable value of security 2 years and over Lost 100%

8

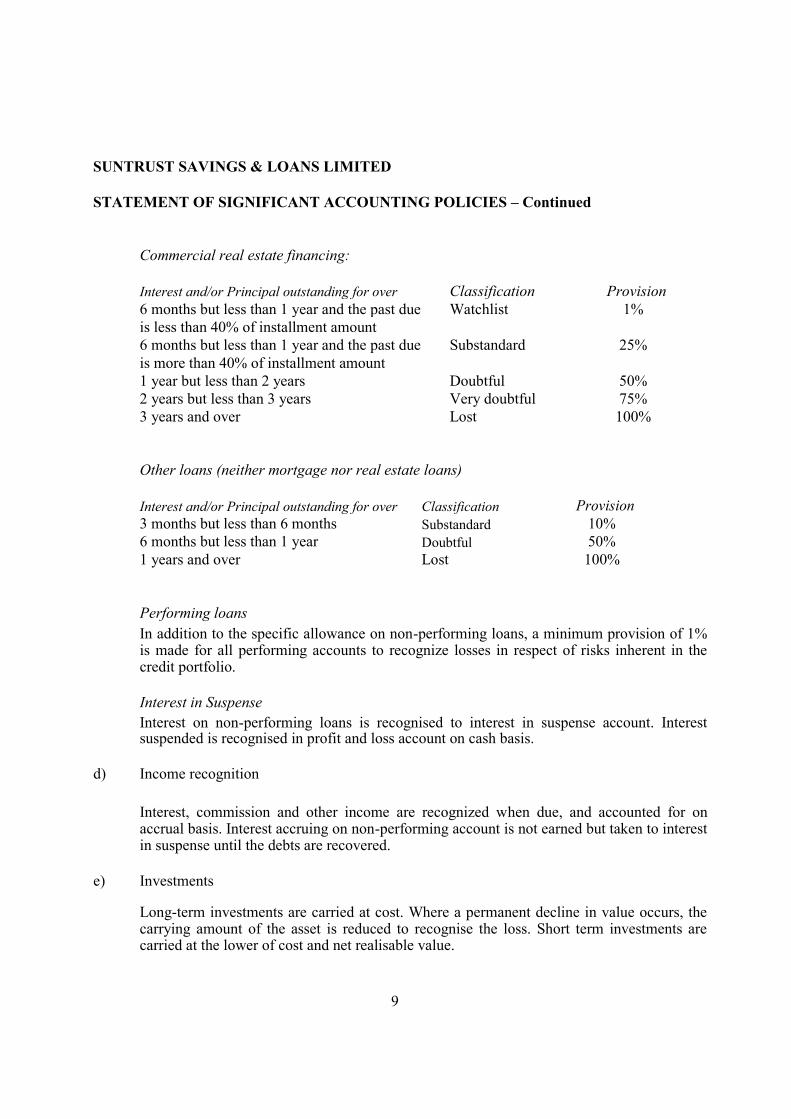

SUNTRUST SAVINGS & LOANS LIMITED STATEMENT OF SIGNIFICANT ACCOUNTING POLICIES – Continued

Commercial real estate financing:

Interest and/or Principal outstanding for over Classification Provision 6 months but less than 1 year and the past due Watchlist 1% is less than 40% of installment amount

6 months but less than 1 year and the past due Substandard 25% is more than 40% of installment amount

1 year but less than 2 years Doubtful 50% 2 years but less than 3 years Very doubtful 75% 3 years and over Lost 100%

Other loans (neither mortgage nor real estate loans)

Interest and/or Principal outstanding for over Classification Provision 3 months but less than 6 months Substandard 10% 6 months but less than 1 year Doubtful 50% 1 years and over Lost 100%

Performing loans In addition to the specific allowance on non-performing loans, a minimum provision of 1% is made for all performing accounts to recognize losses in respect of risks inherent in the credit portfolio.

Interest in Suspense Interest on non-performing loans is recognised to interest in suspense account. Interest suspended is recognised in profit and loss account on cash basis.

d) Income recognition

Interest, commission and other income are recognized when due, and accounted for on accrual basis. Interest accruing on non-performing account is not earned but taken to interest in suspense until the debts are recovered.

e) Investments

Long-term investments are carried at cost. Where a permanent decline in value occurs, the carrying amount of the asset is reduced to recognise the loss. Short term investments are carried at the lower of cost and net realisable value.

9

SUNTRUST SAVINGS & LOANS LIMITED STATEMENT OF SIGNIFICANT ACCOUNTING POLICIES – Continued f) Foreign Currency Transactions

Transactions in foreign currencies are translated to the Naira at the rates of exchange ruling at the dates of the transactions. Foreign currency balances are converted to the Naira at the rate of exchange ruling at the balance sheet date and resultant profit and loss on exchange is taken to the profit and loss account.

g) Taxation

i. Current income tax

Income tax expenses/credits are recognized in the profit and loss account. Current income tax is the expected tax payable on the taxable income for the year, using statutory tax rates at the balance sheet date, and any adjustment to tax payable in respect of previous years.

ii. Deferred taxation Deferred income tax is provided in full, using liability method, on all temporary timing differences arising between the tax bases of assets and liabilities and their carrying values for financial reporting purposes. Deferred income tax is determined using rates that are expected to apply when the related deferred income tax liability is settled.

Deferred income tax assets are recognized only to the extent that is probable that future taxable profits will be available against which the temporary differences can be utilised

h) Retirement benefits

Arrangements for retirement benefits for members of staff are based on the provisions of the

National Pension Reform Act. The matching contribution by the Company is based on

current basic salaries and designated allowances and it is charged to profit and loss account.

i) Investment properties

Investment properties which are held for capital appreciation and subsequent disposal are measured initially at their cost, including transaction costs. Subsequent to initial recognition, investment properties are carried at their valuation amount and revalued periodically on a systematic basis at least once in every three years. Investment properties are not subject to periodic charge for depreciation. An increase in the carrying amount arising from the revaluation of investment property is credited to the shareholders’ fund as revaluation surplus.

10

SUNTRUST SAVINGS & LOANS LIMITED STATEMENT OF SIGNIFICANT ACCOUNTING POLICIES – Continued

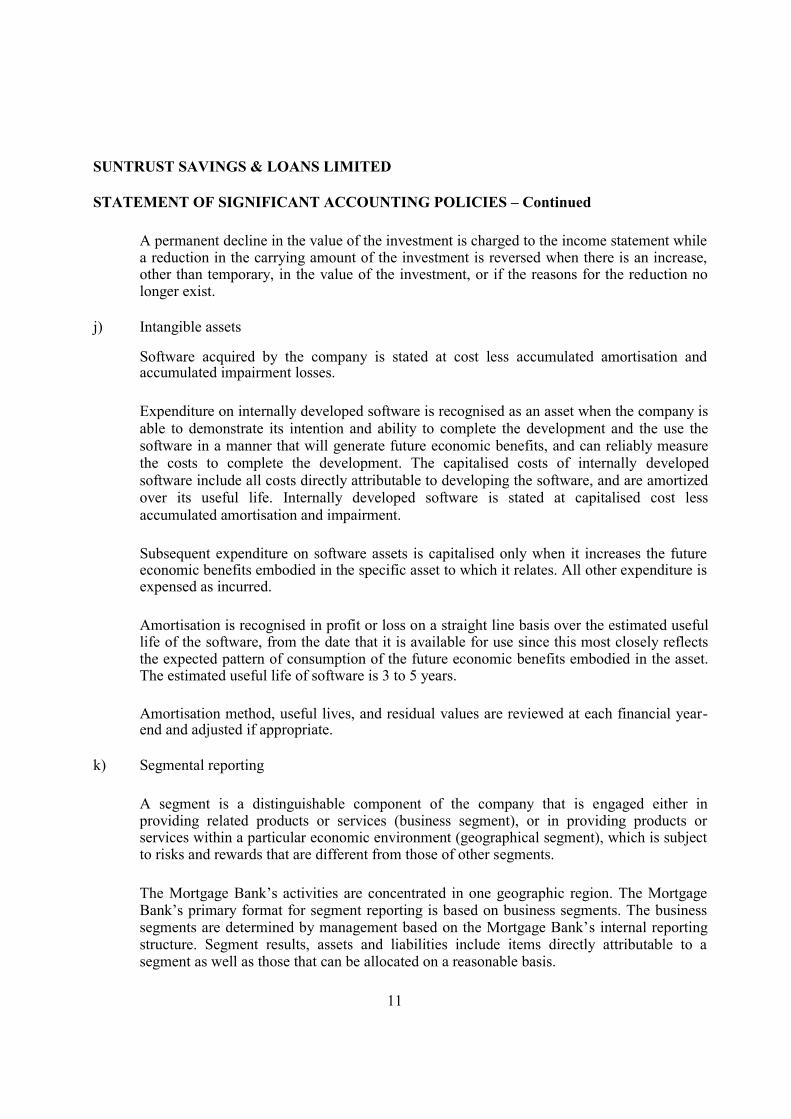

A permanent decline in the value of the investment is charged to the income statement while a reduction in the carrying amount of the investment is reversed when there is an increase, other than temporary, in the value of the investment, or if the reasons for the reduction no longer exist.

j) Intangible assets

Software acquired by the company is stated at cost less accumulated amortisation and accumulated impairment losses.

Expenditure on internally developed software is recognised as an asset when the company is able to demonstrate its intention and ability to complete the development and the use the software in a manner that will generate future economic benefits, and can reliably measure the costs to complete the development. The capitalised costs of internally developed software include all costs directly attributable to developing the software, and are amortized over its useful life. Internally developed software is stated at capitalised cost less

accumulated amortisation and impairment.

Subsequent expenditure on software assets is capitalised only when it increases the future economic benefits embodied in the specific asset to which it relates. All other expenditure is expensed as incurred.

Amortisation is recognised in profit or loss on a straight line basis over the estimated useful life of the software, from the date that it is available for use since this most closely reflects the expected pattern of consumption of the future economic benefits embodied in the asset. The estimated useful life of software is 3 to 5 years.

Amortisation method, useful lives, and residual values are reviewed at each financial year-end and adjusted if appropriate.

k) Segmental reporting

A segment is a distinguishable component of the company that is engaged either in providing related products or services (business segment), or in providing products or services within a particular economic environment (geographical segment), which is subject to risks and rewards that are different from those of other segments.

The Mortgage Bank’s activities are concentrated in one geographic region. The Mortgage Bank’s primary format for segment reporting is based on business segments. The business segments are determined by management based on the Mortgage Bank’s internal reporting structure. Segment results, assets and liabilities include items directly attributable to a segment as well as those that can be allocated on a reasonable basis.

11

SUNTRUST SAVINGS & LOANS LIMITED BALANCE SHEET AS AT DECEMBER 31 2012 DECEMBER 31 DECEMBER 31

2012 2011

Note N'000 N'000

ASSETS

Cash in hand 2 820 9,023

Due from banks and other financial institutions 3 647,611 117,022

Placements 4 803,754 1,790,193

Investment properties 5 2,272,673 1,540,526

Loans and advances 6 5,293,273 3,466,174

Other assets 7 1,047,581 228,409

Property, plant and equipment 9 69,697 103,037

Intangible assets 8 21,305 120,524

TOTAL ASSETS 10,156,714 7,374,908

LIABILITIES

Deposit and current accounts 10 1,452,644 4,002,316

Short-term borrowings 11 500,000 -

Taxation 12 2,623 2,059

Other liabilities 13 754,869 75,903

Long term borrowings 18 4,940,751 1,627,627

7,650,887 5,707,905

CAPITAL AND RESERVES

Share capital 14 2,475,000 2,000,000

Share premium 15 475,000 -

General reserve 17 (444,173) (332,997)

SHAREHOLDER'S FUNDS 2,505,827 1,667,003

TOTAL LIABILITIES AND SHAREHOLDERS'

FUNDS 10,156,714 7,374,908

The Accounting Policies and Notes to the financial statements form integral part of these financial statements

12

SUNTRUST SAVINGS & LOANS LIMITED PROFIT AND LOSS ACCOUNT FOR THE YEAR ENDED DECEMBER 31 2012

DECEMBER 31, DECEMBER 31,

2012 2011

Note N'000 N'000

Gross earnings 975,645 509,785

Interest income 19 694,344 374,816

Interest expense 20 (506,996) (233,188)

Interest margin 187,349 141,628

Commissions and other income 21 281,301 134,969

Operating income 468,649 276,597

Operating expenses 22 (278,152) (201,493)

Depreciation 9 (55,985) (47,457)

Amortisation of intangible assets 8 (104,594) (99,264)

Provision for doubtful accounts 23 (138,471) (32,303)

Loss before taxation (108,553) (103,920)

Taxation 12 (2,623) (2,059)

Loss after taxation (111,176) (105,979)

Appropriations:

Transfer to statutory reserve 16 - -

Transfer to general reserve 17 (111,176) (105,979)

(111,176) (105,979)

Earning per share (kobo)

-Basic 25 (5) (7)

The Accounting Policies and Notes to the financial statements form integral part of these financial

statements 13

SUNTRUST SAVINGS & LOANS LIMITED

STATEMENT OF CASH FLOWS FOR THE YEAR ENDED DECEMBER 31 2012

DECEMBER 31, DECEMBER 31, 2012 2011 Note N'000 N'000

Cash flows from operating activities

Interest received 694,344 374,816 Commission and other income received 281,301 134,969 Interest expenses paid (506,996) (233,188) Cash payment to employees and suppliers (278,152) (201,493) Tax paid (2,059) - Operating profit before changes in operating

assets and liabilities 188,438 42,801

Changes in operating assets/liabilities

Loans and advances (1,965,570) (2,456,640) Other assets (819,172) 31,549 Deposit and current accounts (2,549,671) 797,283 Other liabilities 678,966 (84,366)

Net cashflow from operating activities 26 (4,467,009) (1,669,373)

Cash flows from investing activities

Change in investments properties (732,147) (387,189) Acquistion of intangible assets 8 (5,375) (17,480) Purchase of fixed assets 9 (22,645) (44,975)

Net cash used in investing activities (760,167) (449,645)

Cash flows from financing activities

Proceeds from issue of shares 950,000 1,000,000 Short-term borrowings 500,000 - Long term borrowings 3,376,992 1,637,323 Repayment of long term loans (63,869) (9,693)

Net cashflow from financing activities 4,763,123 2,627,630

Net increase in cash and cash equivalents (464,053) 508,612 Cash and cash equivalents at 1 January 1,916,239 1,407,627

Cash and cash equivalents at year end 4.1 1,452,186 1,916,239

The Accounting Policies and Notes to the financial statements form integral part of these financial statements

14

SUNTRUST SAVINGS & LOANS LIMITED

NOTES TO THE FINANCIAL STATEMENTS

1. The mortgage bank

Sun Trust Savings & Loans Plc was incorporated on 12 February 2009 as a Private Limited Liability

Company in accordance with the provisions of the Companies and Allied Matters Act, 1990. It was

licensed to operate as a Mortgage Institution in March 2009 and commenced operations in January

2011.

December 31, December 31, 2012 2011 N'000 N'000

2. Cash and short term funds

Cash 820 9,023

3. Due from banks and other financial institutions

Local banks 647,611 117,022

4. Placements

Placements with banks in Nigeria 803,754 1,790,193

4.1 Cash and cash equivalents

Cash and short-term funds (note 2) 820 9,023

Balances with banks and other financial institutions (note 3) 647,611 117,022

Placements (note 4) 803,754 1,790,193

1,452,186 1,916,239

5 Investment Properties

Cost at 1 January 1,540,526 1,153,337

Additions during the year 3,984,169 387,189

Reclassification to other assets (321,090) -

Disposal during the year (2,930,932) -

Balance at year end 2,272,673 1,540,526

These are real estates acquired for resale at a later date and are stated at cost

15

SUNTRUST SAVINGS & LOANS LIMITED NOTES TO THE FINANCIAL STATEMENTS

December 31, December 31,

2012 2011 N'000 N'000

6. Loans and advances 6.1 Analysis of loans and advances by quality

Performing 5,122,727 3,475,350 Watchlist 180,722 - Sub-standard 19,144 21,658 Doubtful 51,310 - Lost 100,846 12,172 5,474,749 3,509,180 Less Provision

- General (51,224) (34,753) - Watchlist (1,807) - - Sub-standard (1,944) (2,166) - Doubtful (25,655) (6,086) - Lost (100,846) -

(181,476) (43,005)

5,293,273 3,466,174

6.2 Analysis of loans and advances by security

Real estate 4,778,933 2,182,856 Otherwise secured 695,816 1,326,324

Gross loans 5,474,749 3,509,180

6.3 Maturity profile of loans and advances

Under 1 month 1,002,569 1,002,569 1 - 3 months 248,171 248,171 Over 12 months 4,224,010 2,258,440 5,474,749 3,509,180

6.4 Analysis of loans and advances by nature

Term loans 83,356 323,755 Overdrafts 551,135 1,002,416 Mortgage 4,840,259 2,183,009

5,474,749 3,509,180

6.5 Insider-related credits

Aggregate amount of insider related credits outstanding at year-end 55,000 -

There were no non-performing insider-related credits as at December 31, 2012.

16

SUNTRUST SAVINGS & LOANS LIMITED NOTES TO THE FINANCIAL STATEMENTS (Continued) 2012 2011 N'000 N'000

7. Other assets

Interest receivable 28,257 10,850 Deposit for property 321,090 - Prepayments 131,952 173,873 Receivable from sales of investment properties 553,966 - Stationery stock 11,323 5,590 Accounts receivable & clearing house 994 15,202 Sundry debtors - 22,894

1,047,581 228,409

8. Intangible assets

The company adopted Statement of Accounting Standards 31: On Intangible Assets, which became operative for financial

statements covering years beginning on or after 1 January 2011. As a result, the carrying amount of the cost of its

acquired software, which does not form part of a related hardware and previously classified as Computer Equipment and

software, was reclassified to intangible assets. The movement on intangible asset account during the year was as follows:

Computer Software Cost: At 1 January 2012 (Note 35) Additions during the year At 31 December 2012

Accumulated Amortisation: At 1 January 2012 (Note 35) Additions during the year At 31 December 2012

Net book Value: At 31 December 2012

At 31 December 2011

9. Property, plant and equipment

Plants & Furniture & Computer Motor Office

Machinery Fittings equipment vehicles Equipment

N'000 N'000 N'000 N'000 N'000

Cost:

At January 01, 2012 20,933 39,302 97,673 27,605 4,775

Acquired during the year - 3,715 9,419 8,300 1,211

At December 31, 2012 20,933 43,017 107,092 35,905 5,986

Depreciation:

At January 01, 2012 6,126 12,055 59,998 8,228 843

Charge during the year 4,169 8,507 35,280 6,901 1,128

At December 31, 2012 10,295 20,562 95,279 15,130 1,972

Net Book Value

At December 31, 2012 10,638 22,455 11,813 20,776 4,014

At December 31, 2011 14,807 27,247 37,675 19,376 3,932

2012 N'000 310,421

5,375 315,796

(189,896) (104,594) (294,491)

21,305 120,524

Total

N'000

190,288 22,645

212,933

87,251 55,985

143,236

69,697 103,037

17

SUNTRUST SAVINGS & LOANS LIMITED NOTES TO THE FINANCIAL STATEMENTS (Continued)

December 31, December 31, 2012 2011

N'000 N'000

10. Deposit, current and other accounts

.1 Summary

In Nigeria:

Term 186,516 2,626,253

Demand 1,262,163 1,364,406

Savings 3,965 11,657

1,452,644 4,002,316

.2 The maturity profile of deposit liabilities is as

follows:

Under 1 month 1,262,163 1,364,406

6 - 12 months 97,223 1,324,783

Over 12 months 93,259 1,313,126

1,452,644 4,002,316

11. Short-term borrowings

The mortgage bank secured a loan of N500 million from Skye Bank Plc with a tenor of 4 years at

variable annual interest rate of 16% for onward lending to its customers to part-finance the acquisition of

an housing estate in Abuja. The loan is secured by a legal mortgage over the estate being acquired. The

mortgage bank has primary responsibility to service the loan but will recover from the customers.

12. Taxation

Company income tax 2,218 1,716 Education tax 405 343 Information technology development levy - -

Per Profit and loss account 2,623 2,059 Balance brought forward 2,059 - Payment during the year (2,059) - Per Balance sheet 2,623 2,059

The charge for taxation in these financial statements is based on the provisions of the Companies Income Tax Act. The charge for education tax is based on the provisions of the Education Tax Act.

Section 12(2a) of the Nigerian Information Technology Development Agency (NITDA) Act 2007 stipulates that, specified companies contribute 1% of their profit before tax to the Nigerian Information Technology Development Agency.

18

18

SUNTRUST SAVINGS & LOANS LIMITED NOTES TO THE FINANCIAL STATEMENTS (Continued) December 31, December 31,

2012 2011

N'000 N'000

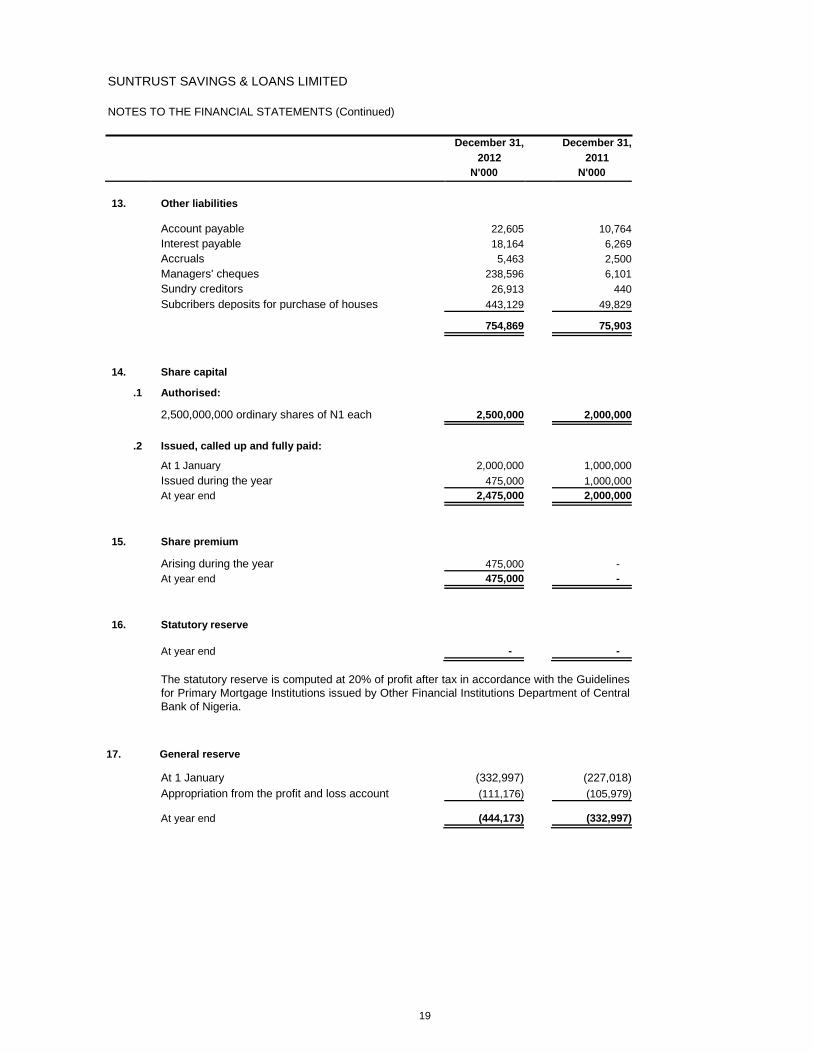

13. Other liabilities

Account payable 22,605 10,764

Interest payable 18,164 6,269

Accruals 5,463 2,500

Managers' cheques 238,596 6,101

Sundry creditors 26,913 440

Subcribers deposits for purchase of houses 443,129 49,829

754,869 75,903

14. Share capital

.1 Authorised:

2,500,000,000 ordinary shares of N1 each 2,500,000 2,000,000

.2 Issued, called up and fully paid:

At 1 January 2,000,000 1,000,000

Issued during the year 475,000 1,000,000

At year end 2,475,000 2,000,000

15. Share premium

Arising during the year 475,000 -

At year end 475,000 -

16. Statutory reserve

At year end - -

The statutory reserve is computed at 20% of profit after tax in accordance with the Guidelines

for Primary Mortgage Institutions issued by Other Financial Institutions Department of Central

Bank of Nigeria.

17. General reserve

At 1 January (332,997) (227,018) Appropriation from the profit and loss account (111,176) (105,979)

At year end (444,173) (332,997)

19

SUNTRUST SAVINGS & LOANS LIMITED

NOTES TO THE FINANCIAL STATEMENTS (Continued)

December 31, December 31, 2012 2011 N'000 N'000

18 Long Term Borrowings

At January 1 1,627,627 - Borrowings during the year 3,376,992 1,637,323 Repayments during the year (63,869) (9,695) At year end 4,940,751 1,627,627

18.1 This represents funds obtained from Federal Mortgage Bank at interest rate of 4% and disbursed to

beneficiaries of National Housing Fund. Interest and principal are payable monthly.

19. Interest earnings

a. This is analysed by source and income type as follows:

Bank sources:

- Interest on placements 154,267 66,686

Non-Bank sources:

- Interest on loans and advances 540,077 308,130

694,344 374,816

b. Geographical location:

Earned in Nigeria 694,344 374,816

20. Interest expense

.a Interest expense comprises:

- Demand 81,129 7,605

- Time deposits 291,344 189,287

- Savings 158 151

- NHF 134,364 36,145

506,996 233,188

.b Geographical location:

Paid in Nigeria 506,996 233,188

21. Commissions and other income

Commission on turnover 31,210 39,384

Loans management fees 20,946 92,679

Gain from sale of investment properties 229,045 -

Administrative and processing charges 101 2,907

281,301 134,969

20

SUNTRUST SAVINGS & LOANS LIMITED

NOTES TO THE FINANCIAL STATEMENTS (Continued)

December 31, December 31, 2012 2011 N'000 N'000

22. Operating expenses

1. Summary:

Staff and other related costs 49,310 52,521 Auditors remuneration 3,500 2,500 Share capital increase cost 10,941 - Other operating expenses 214,401 146,473 278,152 201,493

23. Provision for doubtful accounts Loans and advances

- General (note 6.1 ) 16,471 24,051

- Watchlist 1,807 -

- Sub-standard (note 6.1) (222) 2,166

- Doubtful (note 6.1) 19,569 6,086

- Lost (note 6.1) 100,846 -

138,471 32,303

Other assets 0 -

138,471 32,303

24. Loss before tax

This is stated after charging:

Directors' fees 850 -

Auditors remuneration 3,500 2,500

25. Earnings per share

Loss for the year attributable to shareholders (N'000) (111,176) (105,979)

Weighted average number of ordinary shares in issue ('000 units) 2,118,750 1,583,333

Adjusted weighted average number of ordinary shares ('000 units) 2,118,750 1,583,333

Earnings per share (Kobo) - basic

(5.25) (6.69)

Earnings per share (Kobo) - adjusted

(5.25) (6.69)

The weighted average number of ordinary shares in issue as stated above is less than the actual number of ordinary shares in issue at the year end because the shares issued during the year included in the weighted average number of shares reflect the date the consideration was received.

21

SUNTRUST SAVINGS & LOANS LIMITED

NOTES TO THE FINANCIAL STATEMENTS (Continued)

December 31, December 31,

2012 2011

N'000 N'000

26. Reconciliation of profit/(loss) after tax to net

cash provided by operating activities

Loss after taxation (111,176) (105,979)

Adjustments to reconcile profit after tax to net cash (utilised)/provided by operating activities:

Amortisation of intangible assets 104,594 47,457

Provision on doubtful balances 138,471 32,303

Depreciation of property, plant and equipment 55,985 99,264

Changes in assets and liabilities

Increase in loans and advances (1,965,570) (2,456,640)

Increase in other assets (819,172) 31,549

Increase in deposit and other current accounts (2,549,671) 797,283

Increase in tax payable 564 2,059

(Decrease)/increase in other liabilities 678,966 (84,366)

Net cash flow from operating activities (4,467,009) (1,669,373)

27. Emolument of Directors

.1 Emoluments:

Fees 850 -

Allowances 450 450

Aggregate emoluments 1,300 450

The Chairman's fees amounted to

250 -

Highest paid Director (Executive)

3,000 3,000

22

SUNTRUST SAVINGS & LOANS LTD

NOTES TO THE FINANCIAL STATEMENTS (Continued)

December 31, December 31

2012 2011

N'000 N'000

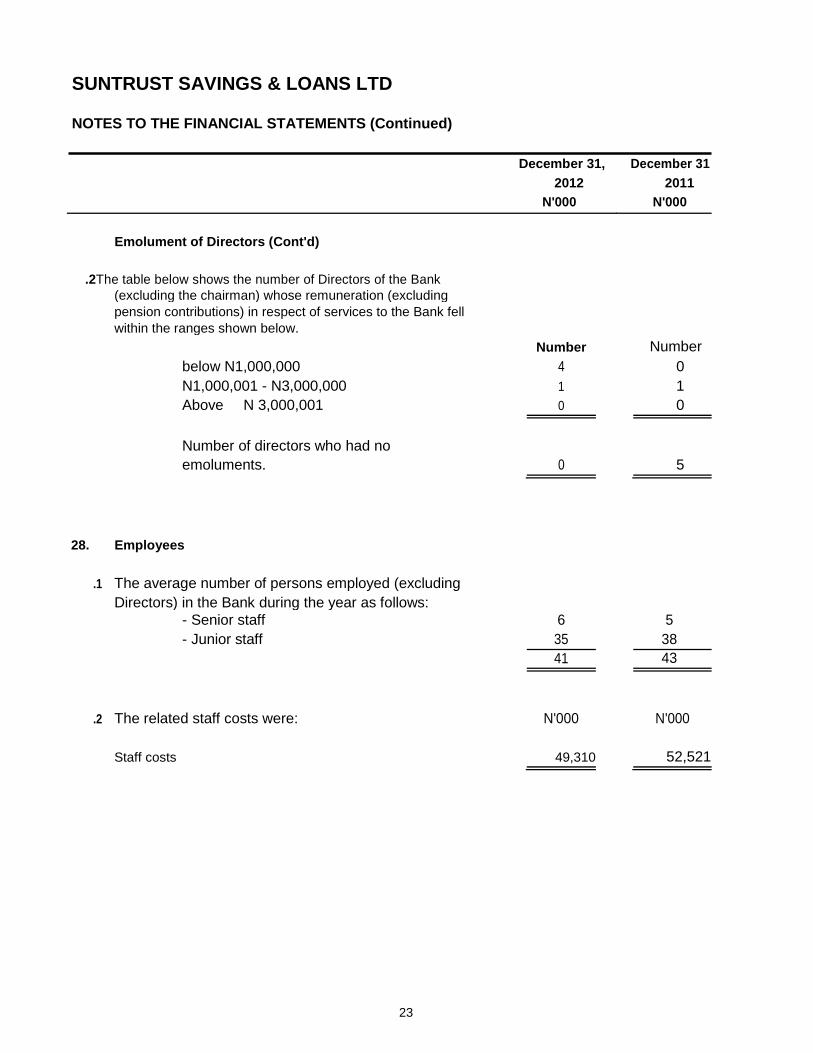

Emolument of Directors (Cont'd)

.2The table below shows the number of Directors of the Bank

(excluding the chairman) whose remuneration (excluding

pension contributions) in respect of services to the Bank fell

within the ranges shown below.

Number Number

below N1,000,000 4 0

N1,000,001 - N3,000,000 1 1

Above N 3,000,001 0 0

Number of directors who had no

emoluments. 0 5

28. Employees

.1 The average number of persons employed (excluding

Directors) in the Bank during the year as follows:

- Senior staff 6 5

- Junior staff 35 38

41 43

The related staff costs were:

.2 N'000 N'000

Staff costs 49,310 52,521

23

SUNTRUST SAVINGS & LOANS LIMITED

NOTES TO THE FINANCIAL STATEMENTS (Continued)

December 31,

2012 29. Post balance sheet events

There are no significant post balance sheet events which could have had a material effect on the state of affairs of the Bank as at 31 December, 2012 and on the loss for the year ended on that date which have not been adequately provided for or disclosed.

30. Claims and litigations

The Directors are of the opinion that no contingent liability will arise in respect of claims and litigation against the Bank as at 31 December 2012.

31. Guarantees and other financial commitments

The Directors are of the opinion that all known liabilities and commitments which are relevant in the assessment of the state of financial affairs of the mortgage bank have been taken into consideration in the preparation of these financial statements.

32. Comparative figures

Certain changes have been made to comparative figures to reflect current year presentations.

33. Contraventions

The Bank was not penalised for contravention of any section of the Banks and Other Financial Institutions Act during the year.

34. Sections 355 (8) and (9) of the Companies and Allied Matters Act

In accordance with banking traditions, the assets and liabilities have been shown in decreasing order of

liquidity and without sub-classifications as between fixed and current assets unlike the formats applied by

the Act. Subject to the foregoing, the format used gives the information required by the Act substantially in

accordance therewith. 24

SUNTRUST SAVINGS & LOANS LIMITED

NOTES TO THE FINANCIAL STATEMENTS (Continued)

December 31,

2012

35. Restatement of Property, Plant and Equipment prior year comparative

This is the first set of financial statements after the implementation of the Statement of

Accounting Standards number 31: On Intangible Assets, which became effective for

annual years beginning on or after 1 January 2011. The implementation of the

accounting policy resulted to a reclassification of computer software from Property,

Plant & Equipment (Note 9). The impact of this is shown below:

Cost: Opening balance as previously

stated Reclassification to intangible

assets Opening balance as re-stated

Accumulated Depreciation: Opening balance as previously

stated Reclassification to intangible

assets Opening balance as re-stated

Net Book Value: Opening balance as previously stated Opening balance as re-stated

2011 N'000

500,709

(310,421) 190,288

277,148 (189,896)

87,251

223,561

103,037

25

SUNTRUST SAVINGS & LOANS LIMITED

STATEMENT OF VALUE ADDED FOR THE YEAR ENDED 31 DECEMBER 2012

December 31, December 31,

2012 2011

N'000 N'000

- Gross earnings 975,645 509,785

- Interest expense (506,996) (233,188)

468,649 276,597

Administrative and other expenses - Local (228,842) (148,973)

Provision for doubtful debts (138,471) (32,303)

VALUE ADDED 101,337 100 95,322 100

DISTRIBUTED AS FOLLOWS:

In payment to employees:

- Salaries, wages and other allowances 49,310 49 52,521 55

In payment to government:

-Taxation 2,623 3 2,059 2

Retained for future replacement of assets

and expansion of business:

- Depreciation and amortisation 160,580 158 146,721 154

- Loss carried forward (111,176) (110) (105,979) (111)

101,337 100 95,322 100

Value added represents the additional wealth which the Bank has been

able to create by its own and its employees' efforts. This statement

shows the allocation of that wealth among employees, shareholders,

government and that retained for future creation of more wealth. 26

SUNTRUST SAVINGS & LOANS LIMITED FINANCIAL SUMMARY

DECEMBER 31 2012 2011 2010

N'000 N'000 N'000

ASSETS

Cash in hand 820 9,023 12,059

Due from banks and other financial institutions 647,611 117,022 580,092

Placements 803,754 1,790,193 815,476

Investment properties 2,272,673 1,540,526 1,153,337

Loans and advances 5,293,273 3,466,174 1,009,534

Other assets 1,047,581 228,409 259,958

Property, plant and equipment 69,697 103,037 307,827

Intangible assets 21,305 120,524 -

TOTAL ASSETS 10,156,714 7,374,908 4,138,283

LIABILITIES

Deposit and current accounts 1,452,644 4,002,316 3,205,032

Short-term borrowings 500,000 - -

Taxation 2,623 2,059 -

Other liabilities 754,869 75,903 160,269

Long term borrowings 4,940,751 1,627,627 -

7,650,887 5,707,905 3,365,301

Shareholders' funds 2,505,827 1,667,003 772,982

TOTAL LIABILITIES AND SHAREHOLDERS'

FUNDS 10,156,714 7,374,908 4,138,283

Gross Earnings 975,645 509,785 250,061

Loss before taxation (108,553) (103,920) (227,018)

Loss after taxation (111,176) (105,979) (227,018)

Earnings/(loss) per share

- Basic (Kobo) (5) (7) (23)

Net assets per share

- Actual (kobo) 1.0 0.8 0.8

Note: Earnings / (loss) per share (basic) are based on profit after taxation and the number of issued ordinary shares at the end of each year. Net assets per share are based on the number of issued share capital at the end of each year.

27

SUNTRUST SAVINGS AND LOANS LIMITED RC 800311

SUMMARISED FINANCIAL STATEMENTS

BALANCE SHEET AS AT DECEMBER 31, 2012

2012 2011

USE OF FUNDS N ’000 N ’000

Cash and short-terms funds 820 9,023

Due from banks and other financial

Institutions 647,611 117,022

Placements 803,754 1,790,193

Investment properties 2,272,673 1,540,526

Loans and advances 5,293,273 3,466,174

Other assets 1,047,581 228,409

Fixed and intagible assets 91,002 223,561

TOTAL ASSETS 10,156,714 7,374,908

LIABILITIES

Deposit and current accounts 1,452,644 4,002,316

Taxation 2,623 2,059

Other liabilities & short-term borrowing 1,254,869 75,903

Long term borrowings 4,940,751 1,627,627

TOTAL LIABILITIES 7,650,887 5,707,905

CAPITAL AND RESERVES

Paid-up share capital 2,475,000 2,000,000

Share premium and reserves 30,827 (332,997)

SHAREHOLDERS’ FUNDS 2,505,827 1,667,003

TOTAL LIABILITIES & SHAREHOLDERS’

FUNDS 10,156,714 7,374,908

PROFIT AND LOSS ACCOUNT FOR THE YEAR ENDED DECEMBER 31, 2012 2012 2011 N’000 N ’000

Gross earnings 975,645 509,785

Interest and similar income 694,344 374,816 Interest and similar expenses (506,996) (233,188)

Net Interest income 187,349 141,628 Commissions & other income 281,301 134,969

Operating income 468,649 276,597 Operating expenses (278,152) (201,493) Depreciation of fixed assets (55,985) (146,721) Provision for risk assets (138,471) (32,303) Amortisation of intangible assets (104,594) -

Loss before taxation (108,553) (103,920) Taxation (2,623) (2,059)

Loss after taxation (111,176) (105,979)

APPROPRIATIONS Transferred to statutory reserve - - Transferred to general reserve (111,176) (105,979)

(111,176) (105,979) The full financial statements were approved by the Board of Directors on March 20, 2013 and signed on its behalf by:

Kenneth Ofili (Chairman)

Muhammad Jibrin (Managing Director/CEO)

INDEPENDENT AUDITORS’ REPORT ON THE SUMMARISED FINANCIAL STATEMENTS We have audited the full financial statements of Suntrust Savings and Loans Limited for the year ended December 31,

2012 in accordance with International Standards on Auditing. In our report dated March 20, 2013, we expressed an

unqualified opinion on the full financial statements from which these summarised financial statements were derived. In our opinion, the summarised financial statements are consistent, in material respects, with the full financial statements from which they were derived. For a better understanding of the company’s financial position and the results of the operations for the year ended December 31, 2012 and the scope of our audit, the summarised financial statements should be read in conjunction with the full financial statements. Report on other legal and regulatory requirements The related party transactions and balances as defined in Central Bank of Nigeria Circular BSD/1/2004 during the year are reported in the Notes to financial statements. No contravention of the Banks and Other Financial Institutions Act, CAP B3 Laws of the Federation of Nigeria 2004 was brought to our attention during the audit of the full financial statements for the year ended December 31, 2012.

Abuja, Nigeria. March 20, 2013 Chartered Accountants

DIRECTORS: Kenneth Ofili (Chairman), Muhammad Jibrin (Managing Director/ Chief Executive Officer),

Yunusa Yakubu, Abubakar Sadiq Mohammed, Nasiru A. Dantata