Supervisory Development and Capacity Building By Olivier Frécaut Senior Financial Sector Expert Monetary and Financial Systems Department IMF World Bank/IMF/Federal Reserve System Seminar for Senior Bank Supervisors from Emerging Economies October 18, 2005

Transcript

Supervisory Developmentand Capacity Building

ByOlivier Frécaut

Senior Financial Sector ExpertMonetary and Financial Systems Department

IMF

World Bank/IMF/Federal Reserve System Seminar for Senior Bank Supervisors from Emerging Economies

October 18, 2005

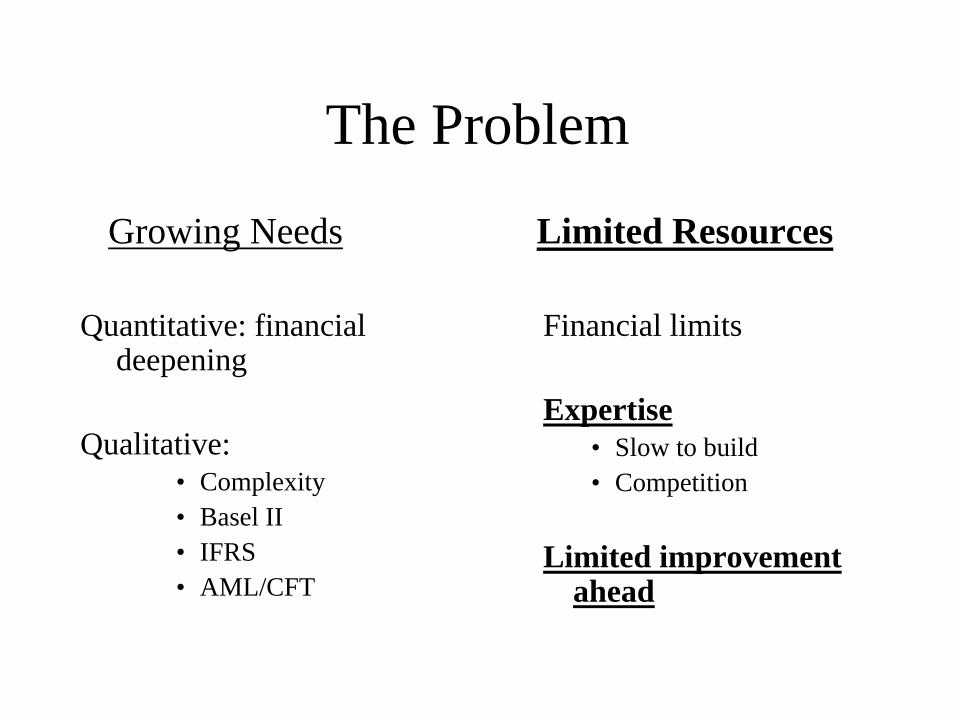

The Problem

Growing Needs

Quantitative: financial deepening

Qualitative:• Complexity• Basel II• IFRS• AML/CFT

Limited Resources

Financial limits

Expertise• Slow to build• Competition

Limited improvement ahead

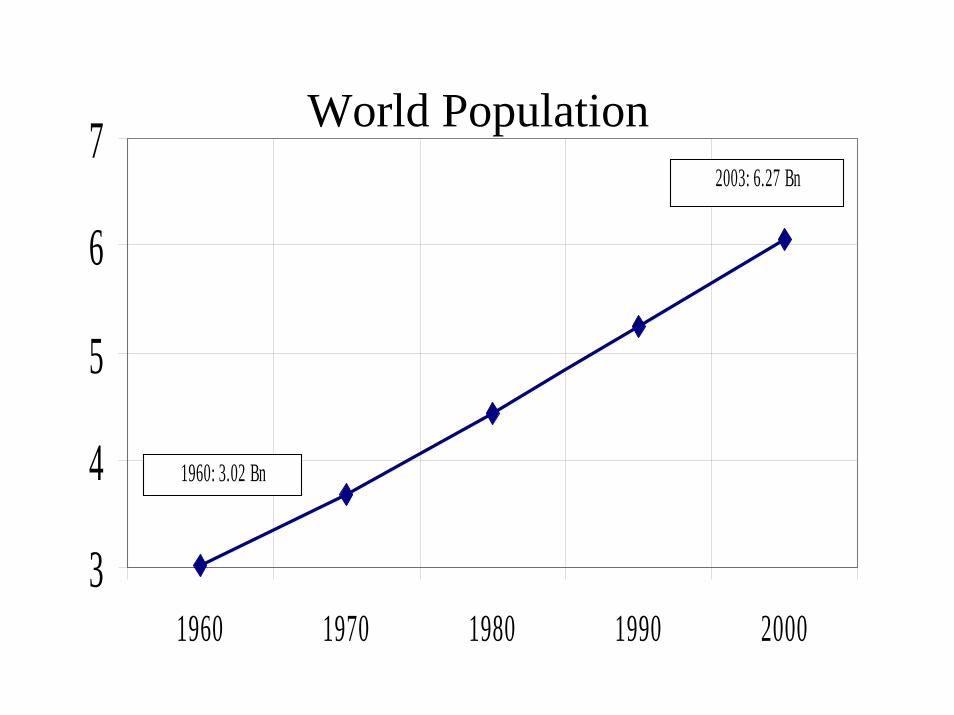

World Population

3

4

5

6

7

1960 1970 1980 1990 2000

1960: 3.02 Bn

2003: 6.27 Bn

World GDP Per Capita

$2,000

$3,000

$4,000

$5,000

1960 1970 1980 1990 2000

Constant 2000 $

2003: $ 5,345

1960: $ 2,417

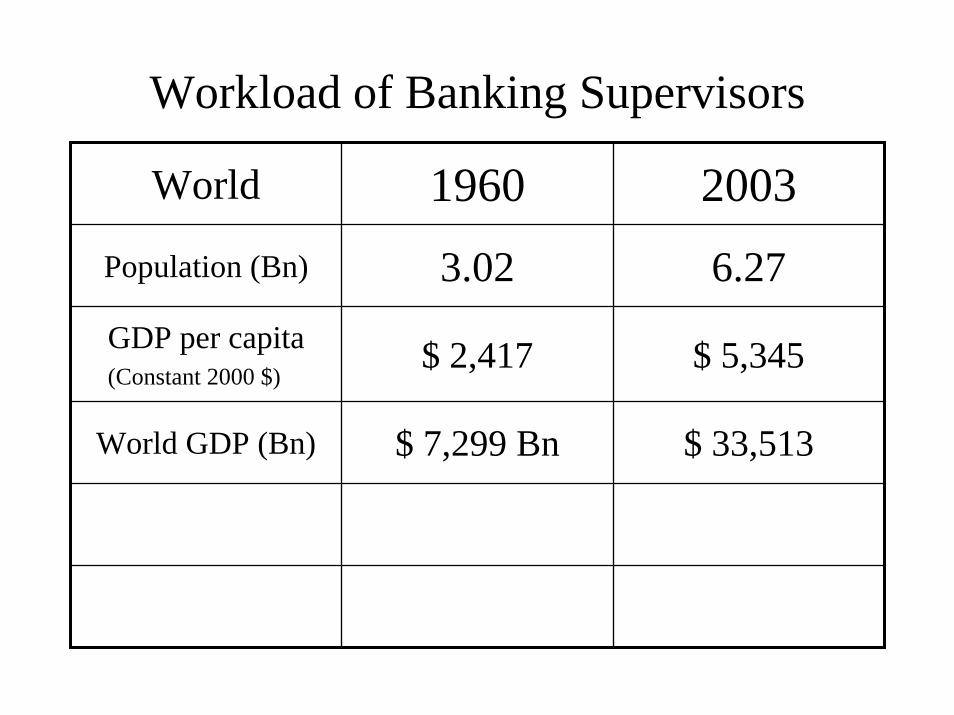

Workload of Banking Supervisors

World 1960 2003Population (Bn) 3.02 6.27GDP per capita(Constant 2000 $)

$ 2,417 $ 5,345

World GDP (Bn) $ 7,299 Bn $ 33,513

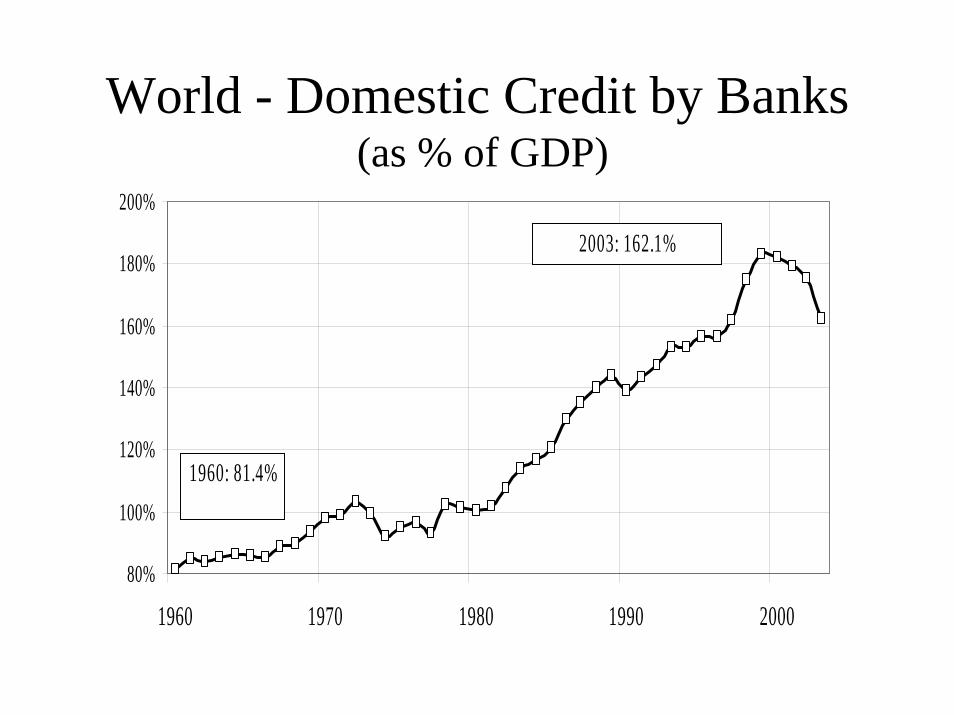

World - Domestic Credit by Banks(as % of GDP)

80%

100%

120%

140%

160%

180%

200%

1960 1970 1980 1990 2000

1960: 81.4%

2003: 162.1%

Workload of Banking SupervisorsWorld 1960 2003

Population (Bn) 3.02 6.27GDP per capita(Constant 2000 $)

$ 2,417 $ 5,345

World GDP (Bn) $ 7,299 Bn $ 33,513Banks Domestic Credit(% of GDP) 81.4 % 162.1 %Banks Domestic Credit(Bn of constant 2000 $) $ 5,941 Bn $ 54,325 Bn

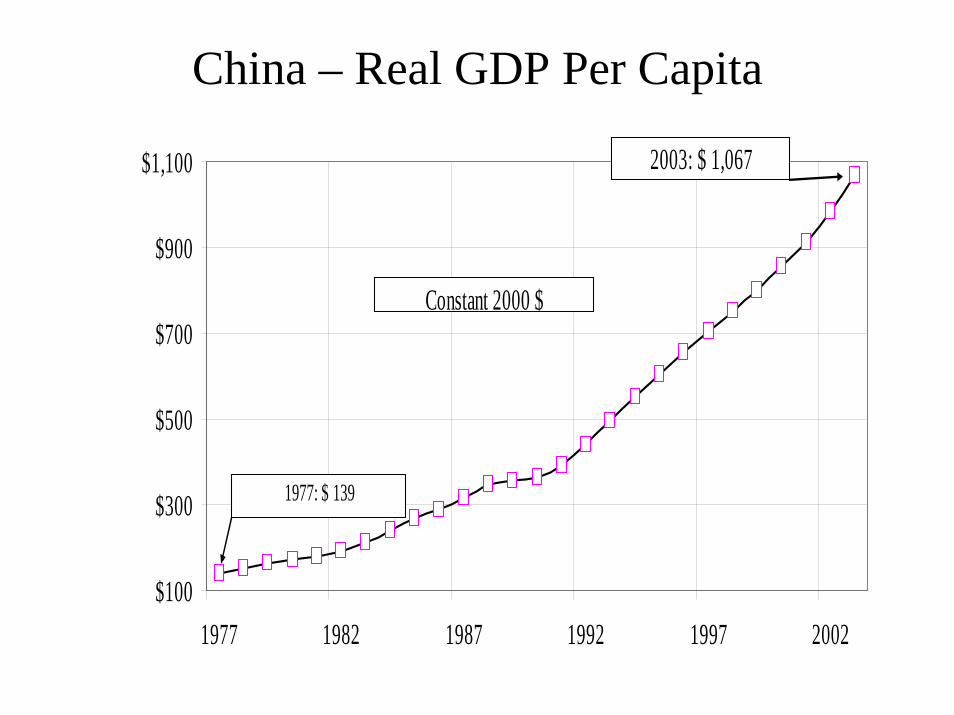

China – Real GDP Per Capita

$100

$300

$500

$700

$900

$1,100

1977 1982 1987 1992 1997 2002

Constant 2000 $

2003: $ 1,067

1977: $ 139

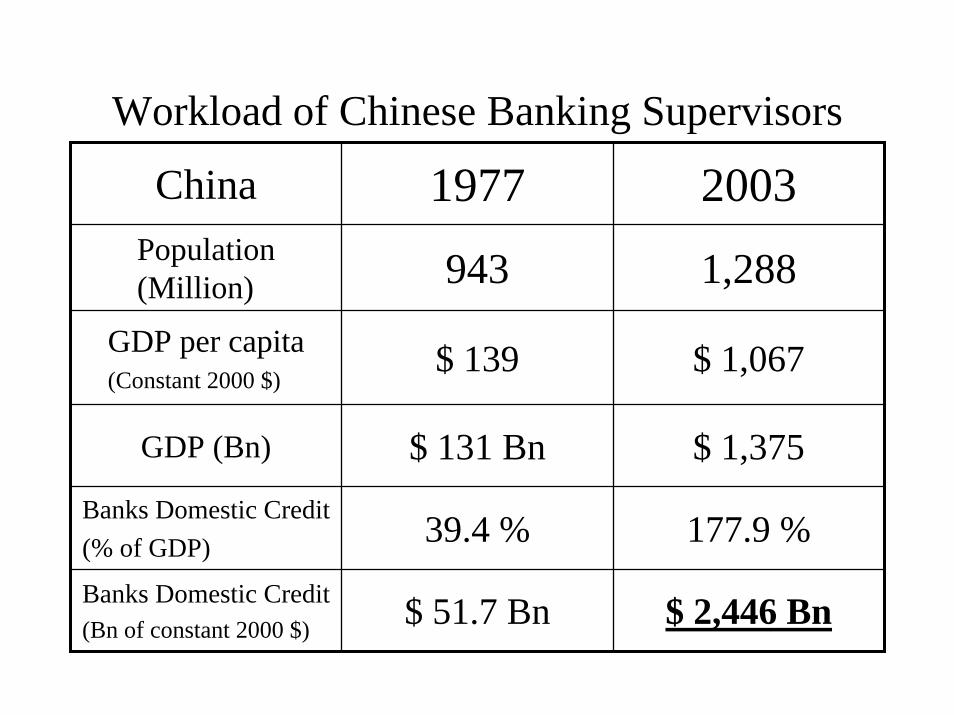

Workload of Chinese Banking Supervisors

China 1977 2003Population (Million) 943 1,288

GDP per capita(Constant 2000 $)

$ 139 $ 1,067

GDP (Bn) $ 131 Bn $ 1,375Banks Domestic Credit(% of GDP) 39.4 % 177.9 %Banks Domestic Credit(Bn of constant 2000 $) $ 51.7 Bn $ 2,446 Bn

The Problem

Growing Needs

Quantitative: financial deepening

Qualitative:• Complexity• Basel II• IFRS• AML/CFT

Limited Resources

Financial limits

Expertise• Slow to build• Competition

Limited improvement ahead

The Problem

Growing Needs

Quantitative: financial deepening

Qualitative:• Complexity• Basel II• IFRS• AML/CFT

Limited Resources

Financial limits

Expertise• Slow to build• Competition

Limited improvement ahead

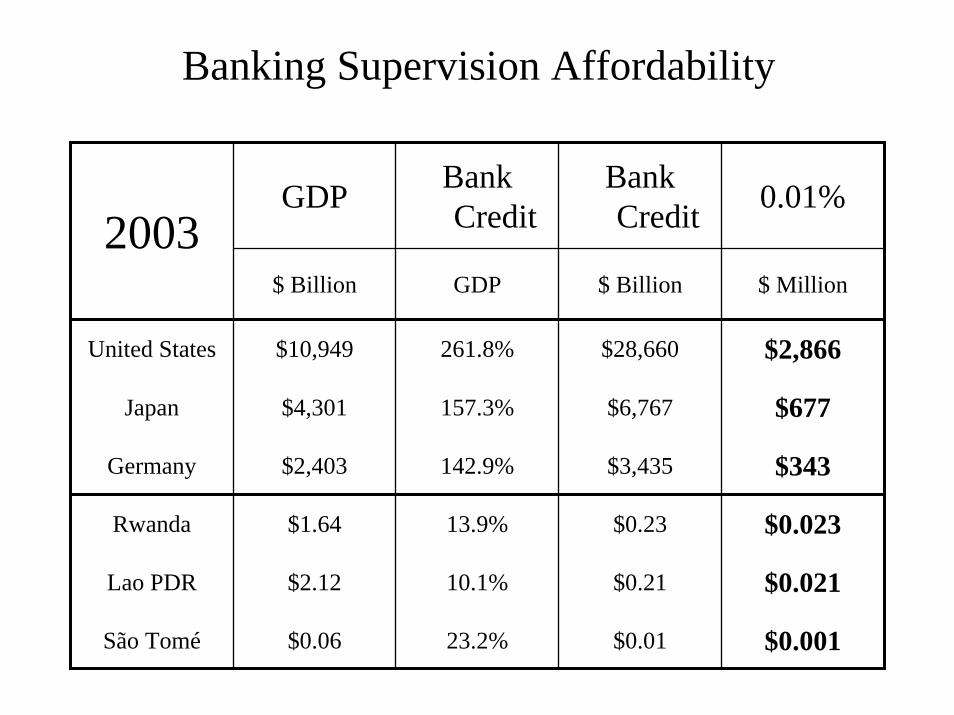

Banking Supervision Affordability

GDP Bank Credit

Bank Credit 0.01%

$ Billion GDP $ Billion $ Million

United States $10,949 261.8% $28,660 $2,866

Japan $4,301 157.3% $6,767 $677

Germany $2,403 142.9% $3,435 $343

Rwanda $1.64 13.9% $0.23 $0.023

Lao PDR $2.12 10.1% $0.21 $0.021

São Tomé $0.06 23.2% $0.01 $0.001

2003

Some Participating Countries

0.01% of credit $ million 0.01% of credit $ million

China $252 Philippines $4.8

India $34 Czech Republic $4.4

Malaysia $16 Morocco $3.7

Saudi Arabia $15 Lebanon $3.6

Turkey $13 Croatia $1.9

Egypt $10 Tunisia $1.8

Singapore $8.1 Slovak Republic $1.5

Chile $5.1 Nigeria $1.4

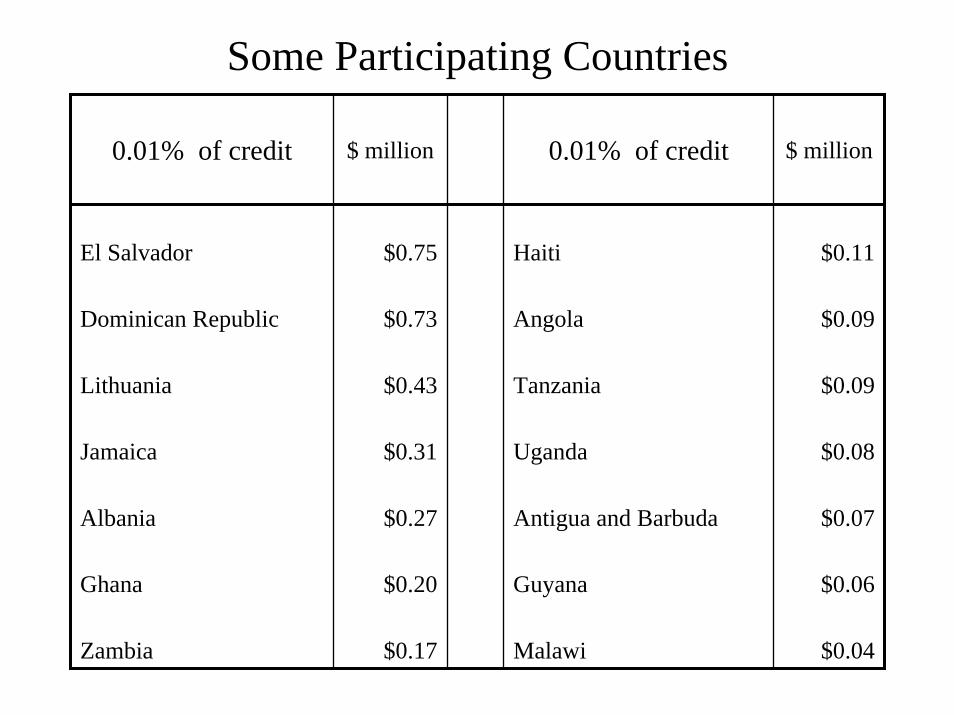

Some Participating Countries

0.01% of credit $ million 0.01% of credit $ million

El Salvador $0.75 Haiti $0.11

Dominican Republic $0.73 Angola $0.09

Lithuania $0.43 Tanzania $0.09

Jamaica $0.31 Uganda $0.08

Albania $0.27 Antigua and Barbuda $0.07

Ghana $0.20 Guyana $0.06

Zambia $0.17 Malawi $0.04

The Problem

Growing Needs

Quantitative: financial deepening

Qualitative:• Complexity• Basel II• IFRS• AML/CFT

Limited Resources

Financial limits

Expertise• Slow to build• Competition

Limited improvement ahead

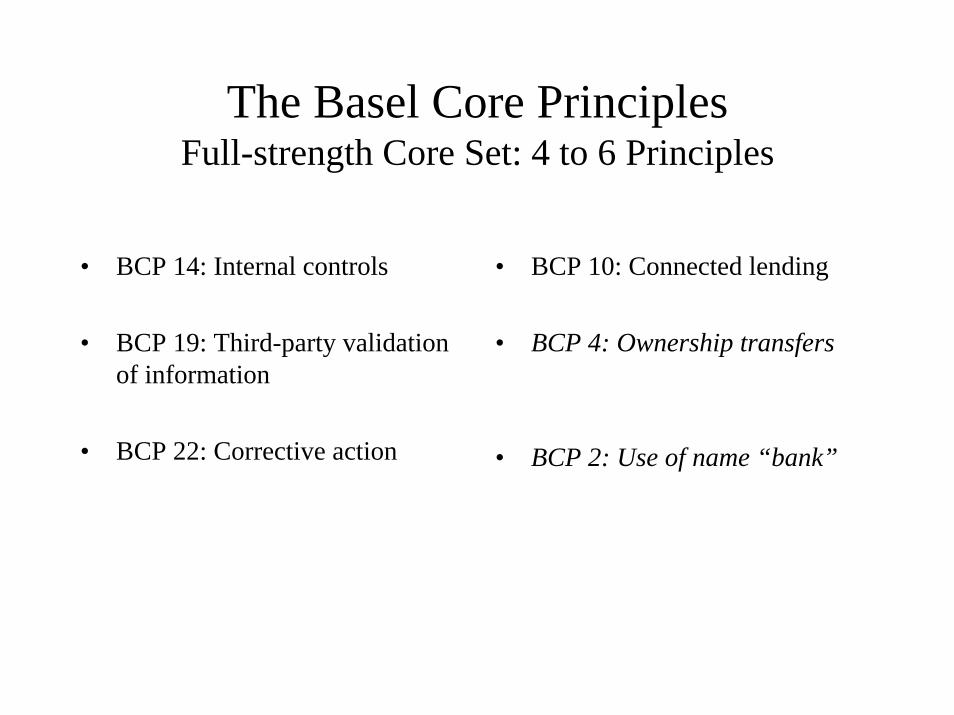

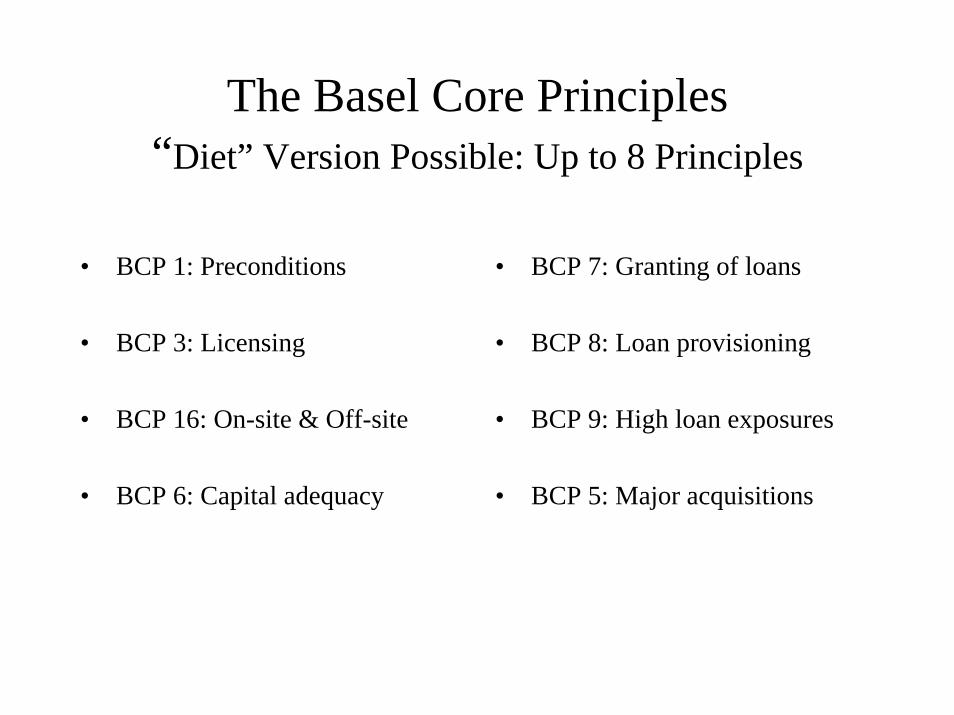

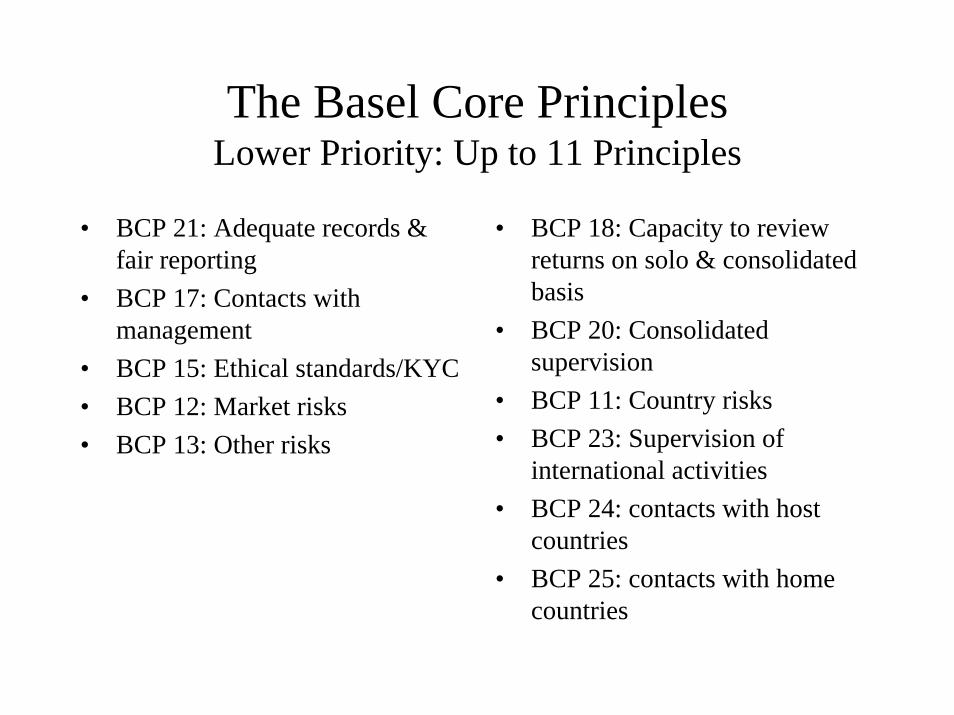

The Solution: Setting Priorities

• Strategic Thinking

• Guiding Principles

• Cost-extraction Approach

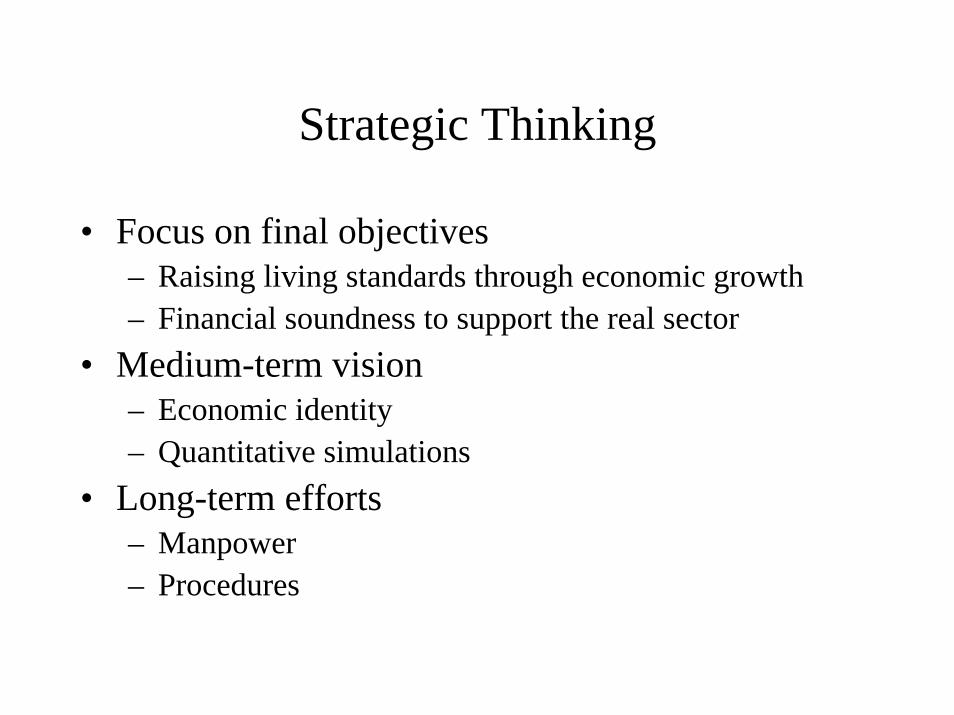

Strategic Thinking

• Focus on final objectives– Raising living standards through economic growth– Financial soundness to support the real sector