2015 2015 ANNUAL REPORT INDUSTRIAL BANK CO.,LTD. Green Finance , Better Tomorrow Add: No. 154 Hudong Road, Fuzhou, Fujian, P.R.C T e l : (86)591-87839338 F a x : (86)591-87842633 P. C : 350003 www.cib.com.cn THE FIRST EQUATOR BANK IN CHINA

Transcript

2015

2015ANNUAL REPORT

IND

USTR

IAL BANK C

O.,LTD

.

Green Finance , Better Tomorrow

Add: No. 154 Hudong Road, Fuzhou, Fujian, P.R.CT e l : (86)591-87839338F a x : (86)591-87842633P. C : 350003www.cib.com.cn

Overthepastfiveyears, the industrypositionfurther improvedwiththekeyperformanceindicatorsdoubled.Asat theendof2015,theCompany’s totalassets,balanceofdeposits ,balanceof loans,equity interestattributable to theordinaryshareholdersof theparentcompanyamounted toRMB5.30trillion,RMB2.48trillion,RMB1.78trillion,andRMB287.743billionrespectively,being2.86times,2.19times,2.08times,and3.13timesofthoseoftheendof2010respectively,enablingittorankthetop10DomesticBanks,Top50GlobalBanks,Top500WorldEnterprises,andtakethe6thplaceinallAsianbankswithregardtocompetitivenessofAsianbanks.TheBankactivelyandfullydisclosedrisks.ThebalanceofNPLswrittenoffandtransferredduringthepastfiveyearsaccumulatedtoapproximatelyRMB80billion,andtheNPLratioattheendof2015was1.46%.Theassetsqualitywasoverallcontrollable.Onthatbasis,netprofitattributabletotheshareholdersoftheparentcompanyaccumulatedtoapproximatelyRMB200billion,cashdividendsdistributedwereoverRMB40billion,averagerateofreturnontotalassetswas1.17%,andaveragerateofreturnonnetassetswas22.72%duringthepastfiveyears.TheBankmaintainedastableandsoundfinancialpositionandwontheawardofthe“Asian Bank Offering the GreatestReturntoShareholders”.

Over thepast fiveyears, thepositionasamainbankinggroupwasestablishedwith thesmoothprogressofcomprehensiveoperating layout.FollowingtheestablishmentofIndustrialBankFinancialLeasingCo.,Ltd.in2010,theCompanymergedUnionTrustLimitedandrenameditasChinaIndustrialInternationalTrustLimitedin2011,establishedCIBFundManagementCo.,Ltd.in2013,andIndustrialConsumerFinanceCo.,Ltd.in2014,andpurchasedNingboShanliFuturesBrokerCo.,Ltd.andrenameditasCIBFuturesCo.,Ltd.in2014,establishedChinaIndustryDigitalFinancialService(Shanghai)Co.,Ltd.andIndustrialEconomicResearchandConsultingCo.,Ltd. in2015.Meanwhile, theCompanyconstantlyexpandeditsbusinessscopeviareinvestmentofsubsidiaries,andtheCompanyhasbecomeoneofthefewdomesticbankholdinggroupsthatpossessfullfinanciallicenses.TheBankinsistedongivingfullplaytotheadvantageofmulti-licenseoperation,andcontinuedtoexpandthescopeofthecollaborationandlinkagebetweenparentcompanyandsubsidiariesandbetweensubsidiaries,whileenablingthetheGrouptoimproveitsoverallcompetitioncapability,customerserviceabilityandbusinesscomprehensiverevenue.Meanwhile,theGroupwonthe“AnnualFinancialHoldingGroupAward2015”.

Over thepastfiveyears, theeffectivenessofoperational transformationgradually revealedwith theconsensusreachedoncapitalsavingconcept.Adheringtothecapitalsupplementationprincipleof“givingprioritytointernalaccumulationwithexternalsourcesasthesupplement”,theCompanysupplementedcoretieronecapitalofoverRMB150billionbyprofitretentionduringthepastfiveyears.TheCompanyfurtheroptimizedshareholderstructureandraisedcoretieronecapitalofRMB23.532billionthroughprivateplacementtoshareholdersincludingPICCandChinaNationalTobaccoCorporation.TheCompanyactivelycarriedoutcapital instrument innovation,became thefirstbatchofpreferredsharepilotbanks, raised tieronecapitalofRMB25.905billion,andcompletedtwosupplementationoftiertwocapitalofRMB30billionintotal, therebypromotingthesustainableandhealthydevelopmentof itsvariousbusinesses.Attheendof2015,theCompany’snetcapitalreachedRMB383.504billion,being3.43timesofthatof theendof2010,withcapitaladequacy ratioof11.19%andadequacy ratioofcore tieronecapitalof8.43%.TheCompanyestablished theall-roundandactivecapitalmanagementconcept,promoted transformationofoperationmodeandcultivationofstrategickeybusiness throughcapitalmanagement,builtcharacterizedoperationanddifferentiatedcompetitionadvantages.Currently,theCompanyhasbecomeamainstreamcompetitorin thedomesticurbanizationfinance,apioneer in thegreenfinance,a forerunner in the interbankbusinessfinanceandanadvocatorofpensionfinance.Moreover,theCompanytooktheleadinpositioningitselfformultiplemarkets,suchasmoneymarket,capitalmarket,preciousmetalsmarket,foreignexchangemarket,andderivativesmarket,etc.,therebyenjoyingfirst-moveradvantages.

Over thepastfiveyears, the reformofbusinessgovernancesystemconstantlydeepenedwith thestableoperationofcorporategovernance.TheCompanysmoothlycompleted theworkhandoverof thepresidentand two termsofchairmenof theboardofsupervisors,appointed fournewvicepresidents, thereby realizingastable transitionof theseniormanagement teamwhile following itsoperationstrategies.TheCompanysuccessfullycompleted thechangesof the8thsessionof theboardofdirectorsand resignandadditionofpartofdirectorsduringsuchsession,continued tostrengthen theconstructionofprofessionalabilityanddecision transmissionmechanismof theboardofdirectors, therebyenhancing thestrategymanagementandcontrolabilityaswellasstrategy implementationability.TheCompanywasconsecutivelygranted the“Award of the Board of Directors”byShanghaiStockExchange in2011and2012.Basedon thedevelopment trendofbanking industryandactualconditionsof theCompany, theCompanysuccessfully implemented theprofessional reformsoncorporatefinanceandfinancialmarket, furtherdeepened thereformof retailfinanceandsupporting reforms including the reformon riskmanagementsystem,enabling theBankatall levels toexperiencesignificantchangesintheorganizationsystemandpromotionmodeoftheoperationalmanagementandfurtherimprovetheprofessionaloperationability,internalgrowth impetusandrefinedmanagement level.TheCompanyadapted to thereformrequirementsbyestablishingHongKongBranch,which isoneessentialsteptointernationaldevelopment.Meanwhile,theCompanyadvancedstocknetworktransformationandcommunitybankconstructionafterbasicallycompletingthedeploymentofnationwidenetwork,accelerated integrated innovationof traditionalphysicalchannelsandInternetchannels,therebyfurtherenhancingitsspecializedservicescapability.

Lookingaheadintothe“13thFive-Year”,thedevelopmentenvironmentathomeandabroadwillremaincomplicated,theworldeconomyrecoverywillbeatortuousprocessinprofoundadjustment,thedomesticeconomywilldeepenreformtorealizeashift fromolddevelopmentmomentumintothenewoneand the industry transformationandupgrading.TheCompanywillproactivelyservenationalstrategies, insiston theoveralldirectionofmarketization, integrationand internationalization,adapt to thenewnormaleconomy, integrate itself intonewfinancialpattern, furtheremphasizesoundness, innovation,coordination, refinementandreformsofsystemsandmechanisms,consolidateandexpand thepositionandadvantagesoftraditionalbusinesses,andcultivateandexpandemergingstrategicbusinessboundaryandspace,aimingtofurtherenhancetheoverallstrengthoftheGroup,andcreategreatervalueforrelevantstakeholdersincludingcustomers,employeesandshareholders.

Chairman:

Chairman’s Statement

3

2 0 1 5 ANNUAL REPORT

Chairman:Gao Jianping

4

In2015,domesticmacroeconomycontinuedtoslide,financialmarketfluctuatedintensively,commercialbanksfacedgreatchallengesinitsoperationandmanagement.Facingthecomplexandseverebusinessenvironment,andcenteringonoperationtargetsdeterminedbytheboardofdirectorsatthebeginningoftheyear,theCompanyflexiblyadjusteditsoperatingstrategy,profoundlypromotedreformandtransformation,vigorouslyconsolidatedthedevelopment foundation,successfullywithstoodvarious internalandexternal tests,achievingoperating resultswhicharegenerallybetter thanexpectedandsuccessfullyconcluding this roundofFive-yearPlan.Asat theendof the reportingperiod, the totalassetsof theCompanyreachedRMB5,298.880billion,up20.25%fromthebeginningof the reportingperiod.Netprofitattributable toshareholdersof theparentcompany for theyearreachedRMB50.207billion,representingayear-on-yearincreaseof6.51%.Stickingtobroadensourcesofincomeandreduceexpenditurewhilestrengtheningcostcontrolandmanagement, theCompanymaintainedacost-to-incomeratioat21.59%,remainingata relatively lower levelwithintheindustry.Influencedbythedownturnofmacroeconomyandriskdisclosureofcertainindustriesandareas,theassetsqualitydecreasedslightly,withtheratioofNPLsattheendofthereportingperiodstandingat1.46%,representinganincreaseof0.36percentagepointascomparedwiththebeginningofthereportingperiod.However,theoverallassetsqualityremainedreasonableandcontrollable.TheCompanyincreasedprovision,withprovisionimpairmentlossesofassetsmadeduringthereportingperiodofRMB45.260billion,representingayear-on-yearincreaseof74.72%,whileprovisioncoveragewasadequateoverall,withprovisioncoverageratioat210.08%,andprovision-to-loanratioat3.07%.

In2015,theCompanyprofoundlypromotedgroupoperationsandfurtherstrengthenedmulti-marketoperationandcomprehensiveservicecapability.IndustrialEconomicResearchandConsultingCo.,Ltd.openedsmoothly,CIBDigitalFinancialServiceCo.,Ltd.officiallyestablished,and thesubsidiaries furtherdiversified.TheCompanyhasbecomeoneof thedomesticbankgroupswithmostabundantfinancial license resources.Eachsubsidiarymaintainedarapidbusinessdevelopment,andtheindustrialpositionandprofitcontributiontotheGroupcontinuedtoincrease.Supportingmechanismssuchasexaminationandassessment further improved,and intra-groupcooperationand linkagebecamesmoother.Trans-department,trans-line,trans-institution,andtrans-businesssegmentcooperationandlinkagehavebeenmoreintimateandefficient,andcooperationandlinkagebetweenparent-subsidiarycorporationsandamongsubsidiariescontinued toexpand.Theconstructionofcorebusinessclusterof theGroupmadesignificantachievement,and thebusiness formatof“sizeable investment,sizeableassetmanagementandsizeablewealthmanagement” further shaped.

In2015, theCompanysteadilypromotedvariousreforms,and furtherconsolidated the foundation fordevelopment.TheCompanycomprehensivelydeployedanddeepenedthereformofriskmanagementsystemsandmechanisms,andorderlypromotedthereformofthecreditcardoperationandmanagementsystemsandmechanisms,comprehensivelyoptimized the labororganizationmodeofbusinesshalls,and further improved thereformof the franchisedmechanismof the inter-bankbusiness, therebyobviouslyenhancing theeffectivenessofmanagement.TheCompanysparednoeffortstopreventandcontrolnon-performingassets,soastoachieveoverallstableassetqualityatalllevelsoftheBank.TheCompanycontinuouslyenhanced innovations in riskmanagementmodeandoperation,andvigorouslysupported innovationbusinessdevelopment.TheCompanysolidlycarried out the “two enhancements, two containment” and “lookingback”special inspections,andprofoundlycarriedoutcheckingofemployeebehaviorrisk,therebyfurtherimprovingtheeffectivenessofcomplianceinternalcontrolmanagement.TheCompanycontinuedtoincreaseinvestmentin informationtechnologyconstruction,exploredtheleadingrolesofapplyingscienceandtechnologiesinthebusinessdevelopment,andconstantlyimprovedtheelectronic,informationandintelligentlevelsofthebusinessoperation.

Chairman of the Board of Supervisors :JiangYunming

7

2 0 1 5 ANNUAL REPORT

TheCompany’s board of directors, board of supervisors, directors, supervisors and senior management membersherebywarrant that the informationcontained in this report is free fromfalserepresentation,misleadingstatementormaterialomission,andassumejointandseveralliabilities.

TheCompany’sannual report2015and itsabstractwerereviewedandapprovedat the18thmeetingof the8thsessionof theboardofdirectorsonApril27,2016.Therewerenodirectors,supervisorsorseniormanagementmemberswhocouldnotwarrantordisagreedwith the truthfulness,accuracyandcompletenessofthecontentsofthisannualreport.

The financialdataand indicatorscontained in thisannual reportwereprepared incompliancewiththePRCGenerallyAcceptedAccountingPrinciples.Unlessotherwisespecified, they represented theconsolidateddata.ThemonetarysumsexpressedinRMBinthisannualreport.

DeloitteToucheTohmatsuCertifiedPublicAccountantsLLPhasaudited theCompany’s financialstatements2015 inaccordancewith theChineseAuditingStandards (“CAS”) and has issued a standard auditor’sreportwithunqualifiedopinions.

TheCompany’schairmanGaoJianping,presidentTaoYipingandgeneralmanagerof the financialdepartmentLi Jianherebywarrant that the financial statements in theannual report2015are true,accurateandcomplete.

Theplanofdividendsdistributionforordinaryshareforthereportingperiodconsideredbytheboardofdirectors:basedon the totalcapitalof19,052,336,751shares,cashdividendofRMB6.10(inclusiveoftax)shouldbedistributedforevery10ordinaryshares.

Theplanofdividendsdistribution forpreferredshares isas follows:proposeddividends forpreferredsharesareRMB1.147billion in total.Ofwhich, the total nominal valueof thepreferredsharesof“IndustrialBankP1”isRMB13billion,theinterestperiodwasfromJanuary1toDecember31,2015,proposeddividendsareRMB780millionwithanannualdividendyieldof6%;thetotalnominalvalueofthe preferred shares of “IndustrialBankP2”isRMB13billion,theinterestperiodwasfromJune24toDecember31,2015,proposeddividendsareRMB367millionwithanannualdividendyieldof5.40%.

Investorsareadvised to read the fullcontentof thisannual reportcarefully.Perspectiveand forward-lookingstatements regarding futurefinancialconditions,operatingperformance,businessdevelopmentandbusinessplancontainedinthisreportdonotconstituteanysubstantivecommitmentoftheCompanytoinvestors.Investorsshouldpayattentiontoinvestmentrisks.

Theboardofdirectorsspecially reminds investors that therisk factors theCompany issubject tohavebeen listed indetail in this report.Please refer to“ManagementDiscussionandAnalysis” for risk factortheCompanyissubjecttoandtheriskmanagementanalysis.

Note:1.BasicEPSandweightedaverageROEwerecalculatedbasedon“PreparationRulesforInformationDisclosurebyCompaniesOfferingSecurities to thePublicNo.9-CalculationandDisclosureofReturnonNetAssetsandEarningsPerShare” (2010Revision).

business areas and opens its own “blueocean”,withdistinctoperationcharacteristics.TheCompanyhasbuilttheentireIndustrialBankbrandbybusinessinnovationandestablishedawell-recognizedproductandservicebrandsystem.Abathofproductsandservicebrandsincluding“NaturalLife”, “EnjoyableLife”, “UniversalLife”, “IB Business Express”, “IBFortuneStar”, “IndustrialBankSesameBlooming”, “GreenFinance”, “theEquatorPrinciples”, “Bank-to-BankPlatform”, “E-banking”, “Hotline IB”, “QianDaMoneyManager” and “Direct Banking”arewidely recognized in thedomesticfinancialmarket.TheCompany followed themarketdevelopmenttrend, made great efforts in creating “onebodyand twowings” specializedservicesystem, centralized theresourceadvantagesof thegroupand focusingonurbanizationfinancialbusiness,environmentfinancebusiness,pension financebusiness,comprehensiveservicesbusiness forsmallandmediumbanking institutionsandnon-bankfinancial institutions,directfinancingbusiness incapitalmarket, investmentandcustodybusinessofassetsmanagementandtransactionbankingbusiness, itcreatedafinancialproductsystemwithclearpositioning,distinctcharacteristics,outstandingadvantagesandcomplete functions, formingadvantageousbrandandproductclusterwiththecharacteristicsofthegroup.

Promotingbusiness transformationbycomprehensiveoperation.TheCompanyhasbeenpersisting in themulti-market,multi-productandcomprehensivedevelopmentpathandactivelycreating itscapabilityoffinancialservicesformulti-market. Ithas formeda relativelycompletebusinesssystemcovering interbankbusiness,capital trading,assetsmanagementandassetscustody,andhas taken the lead inplanning itsbusiness in themonetarymarket,capitalmarket,bondmarket, inter-bankmarket,non-bank financial institutionmarket,preciousmetals, foreignexchangeandderivativeproducts trading.Through thecomprehensive layoutof recentyears, theCompanyhasbeen transformed fromasinglebank to“amoderncomprehensivefinancialservicegroupwithbankingbusinessas thecore,coveringbusinessareas including trust, leasing, funds, futures,assetmanagement, internet financeandresearchandconsultation”.TheHongKongbranchwasofficiallyopened in2014,markingakeystepfor theinternationalizationstrategiesof theCompany.Relyingon linkagebetween investmentand loan, linkagebetweenbusinessinandoutsidethestatements,linkagebetweenparentcompanyandsubsidiaries,theCompanyhasmetthediversifiedfinancialservicedemandofcustomers,andthebusinesscoordinationandlinkagedevelopmentcapabilitybetweenbranchesandsubsidiariesbothathomeandabroadhasbeenconstantlyimproved.

Promotingcontinuous improvementofoperationsupportingcapabilitybyscienceand technology.“Building theBank throughScienceandTechnology” is listedasoneof thekeystrategies for thebankingoperation.TheCompanyvaluedtracingandgraspedthedevelopmenttrendofmodernfinancialtechnology.Itincreasedinvestmentinscienceandtechnology topromote innovation infinancial technologiesandconstantly improvethe technologicalcontentoffinancialservice.TheCompanyisamongthefirstbatchofbanksbuildingmodernmanagementsystemsinaccordancewiththeprocessbankconcept,anditscentralizedbackofficeoperationsystemholdsaleadingpositionin the industry.Thecoreproductionsystemconstructionof theCompany isamongthebest in the industry,makingitoneofthefewbanksinthecountrythathaveindependentcoresystemresearchanddevelopmentcapabilityandproprietaryintellectualpropertyrights,aswellastheonlydomesticbankexportingcoresystemtechnology.Itisthefirst tobuildan integrateddisaster recoverysystem integrating themasterdatacenter,same-citydisaster recoveryanddifferent-citydisasterrecovery,andoneofthefirstbanksinthecountrythatcomplywiththeinternationaldisasterrecoverystandard(level-5)andtherequirementsofthedisasterrecoverystipulationsofPBOC.TheCompany’skeyindicators,suchaskey informationsystemavailabilityandgoldcardsystem transactionsuccess rate,havebeenamongthebestintheindustryovertheyears.

Creatingsoftcompetitivepowerbythepragmaticanddedicatedcorporateculture.Tofulfilltheenterprisemissionof“SincereWin-WinService”,adhering to thecorevalueof“Ration, Innovation,PeopleFirstandSharing” and theoperationpolicyof“operatinginaccordancewithlaw,steadyoperationandcivilizedoperation”,theCompanyimplements thestrategyofstrictbankingoperation,bankingoperationbyexperts,developingbankbyscienceandtechnologyandbankingestablishmentbyservice,upholds thecorporatespiritsof“Pragmatism,ProfessionalDedication, Entrepreneurship and Teamwork”, graduallybuildsasimpleandharmonious“homeculture”, a prudent and sound “riskculture”,ahard-working“diligenceculture”andasincerewin-win“serviceculture”, thereby formingstrongsoftcompetitivepowerand improving internalmanagement level inallaspects,effectivelyimprovingcorecompetitivenessandpromotingthehealthydevelopmentofallundertakings.

During the reportingperiod, facing the complicatedand fiercebusinessenvironment, theCompany rationallycoordinated thegoals in relation to“scale,qualityandefficiency”, flexiblyadjusted thebusinessstrategy,andpromotedbusinessstructureadjustmentand transformationandupgrading, therebymeetingexpectationsof itsoveralloperations.

(2)Profitabilitycapabilitymaintainedrelativelygoodstatus.Duringthereportingperiod,therealizedoperatingincomewasRMB154.348billion,up23.58%year-on-year,ofwhichfeeandcommissionincomereachedRMB33.592billion,up18.23%year-on-year.NetprofitattributabletotheshareholdersoftheparentcompanyforthewholeyearreachedRMB50.207billion,representingayear-on-yearincreaseof6.51%.Duringthereportingperiod,weightedaveragenetassets returns ratiowere18.89%, representingayear-on-yeardecreaseof2.32percentagepoints, total returnonassetsreached1.04%,representingayear-on-yeardecreaseof0.14percentagepoint.

(3)Thequalityofassetswascontrollableoverall.Asattheendofthereportingperiod,thebalanceofnon-performingloansof theCompanywasRMB25.983billion,upRMB8.439billion; the ratioofnon-performing loansstandingat1.46%, representingan increaseof0.36percentagepoint fromthefigureat thebeginningof the reportingperiod.Duringthereportingperiod,theprovision-to-loanratiowas3.07%attheendofthereportingperiod,andtheprovisioncoverageratiowas210.08%.

(4)Marketstatusandbrand imagewerecontinuouslyenhanced.TheCompanycontinued tobeamong the top50worldbanks,global500companies,and top150 listedworldenterpriseswith rankingssteadilyclimbing.Over thepastyear, theCompanywonhonors including the“AnnualFinancialHoldingGroupAward2015”, “The Most InfluentialNationalBank”, “AsianBankOfferingtheGreatestReturn toShareholders”, “The Best Green Bank Award”inaseriesofappraisalactivitiesofauthoritiesbothathomeandabroad.

(1)TheCompanydivided its regionalbranches into tensegmentsby importanceandcomparability,namely,headoffice(includingtheheadquartersanditsaffiliatedoperatingunits),Fujian,Beijing,Shanghai,Guangdong,Zhejiang,Jiangsu,Northeastandother regions inNorthernChina,WesternChinaandCentralChina.Operating incomeandoperatingprofitofvariousregionsaresetoutasfollows:

24

Unit:RMBmillion

Region Operating income Change over previousyear(%) Operatingprofit Change over

previousyear(%)

Headoffice 55,861 95.92 31,871 87.04

Fujian 16,229 1.30 1,988 (72.92)

Beijing 7,465 (2.82) 2,781 (45.52)

Shanghai 8,226 5.66 5,658 24.98

Guangdong 9,184 (4.18) (540) (117.87)

Zhejiang 5,811 9.72 1,259 418.11

Jiangsu 6,930 18.81 3,258 14.96

Northeast and other regions 15,017 3.20 5,672 (20.03)

Note: (1) Included the financialassetsat fairvalue throughprofitor loss,available-for-sale financialassets, receivableaccountinvestments,held-to-maturityinvestmentsandlong-termequityinvestments.

Asat theendof the reportingperiod, theproportionofcorporate loanswas67.30%,down6.74percentagepointsfromthefigureatthebeginningoftheperiod.Theproportionofpersonalloansincreasedby4.54percentagepointsto28.77%,and theproportionofdiscountedbills increasedby2.20percentagepoints to3.93%,comparedwiththatatthebeginningoftheperiod.TheCompanyproactivelydealtwiththenewnormaleconomyandnewfinancialpattern,adheredtothemainprinciplesofstabilizingdevelopment,ensuringsafety,andpromotingtransformation” in itswork,rationallycoordinatedthegoalsinrelationto“scale,qualityandefficiency”,flexiblyadjustedthebusinessstrategy, furtherdeepened reformand transformation,vigorouslydevelopedandconsolidated the foundation fordevelopment,rationallydeterminedthedirectionandtempoforcreditgrant,soastomaintainasteadyandbalanceddevelopmentofvariousbusinesses.

Following theprincipleof“riskcontrollable, resourceconservationandsustainabledevelopment”, theCompanypromoted the reasonablearrangementandbalanceddevelopmentofcredit resources in the industry,customers,products,etc.,continuouslyexecuted the“protected,controlledandstressful”difference loanpolicy,speededup thedevelopmentofsmallandmedium-sized,microandretailbusinessesunder thepremiseofmeetingaccessconditionsandeffectivelycontrolling risks, fullyuncoveredbusinessopportunities in free tradezones, industrialparks,reformtestareasandotherareaswithspecialsupportpoliciesgrantedbythecountry, increasedsupportforenvironmentalprotection,medicalcare,education, tourism,communicationsandotherweakperiodicandgreenfinance,andpeople’slivelihoodconsumptionindustries,effectivelycompressedandwithdrewbackwardproductivityprojects,andcontinuouslyadjustedandoptimizedthecreditassetstructure.

NPLratios for themanufacturing,wholesaleand retail industriesslightly increased from thoseat thebeginningoftheperiod,mainlyattributabletotheimpactsoftheslowdowninmacroeconomicgrowth,theadjustmentofindustrialstructureand thedecrease inmarketdemand.Certainenterprisessuffered fromoperationdifficultyanddecreaseof repaymentability, certain industrieswithexcesscapacityandbulkcommodity tradesuffered from increasedrisks,whilenegative factorsofprivate lendingandguaranteed financing repaymentdidnot show fundamentalimprovements,resultinginincreasedcreditrisks.

Northeast and other regions 237,929 13.37 197,426 12.38

WesternChina 277,343 15.59 235,395 14.78

CentralChina 295,794 16.62 256,751 16.12

total 1,779,408 100 1,593,148 100

TheCompany’s loan distribution by geographical region remained stable.TheCompany encouragedeachbranch combining thenational regional development strategybyexecuting the regional differential policy of“helpandcontrol”,gave fullplay to the regionalcomparativeadvantage, formulatedcreditpolicywith regionalcharacteristics, adjustedandoptimized regional credit structureunder theunifiedcredit policyofheadoffice,according tocomprehensive factors including thecharactersof region, industryecology, industrialstructureandcreditenvironment.

Asat theendof the reportingperiod, the loanbalanceof theCompany’s largestsingleborrowerwasRMB7,600million,accountingfor2.11%oftheCompany’snetcapitalbeforeconsolidation,whichconformedtotherequirementby the regulatorydepartments that theproportionof loanbalanceofasingleborrowercouldnotexceed10%ofabank’snetcapital.

TheCompany further adjustedandoptimized its structureof personal loansand steppedup support for thedevelopmentof personalmortgage loanbusiness. Influencedby the slowdown in thegrowthof thedomesticeconomy,theNPLratioofpersonal loansslightlywentupasat theendof thereportingperiod,but theoverall riskremainedcontrollable.

During the reportingperiod, theCompanyseized themarketopportunities.Firstly, theCompanystressedon theincreaseofholdinggovernmentbondsand localgovernmentbondswith taxdeductionandexemption, riskcapitalsavingandhighliquidity.Secondly,theCompanyincreasedtheinvestmentsthathadrelativelyhigherabsoluteyieldsandcontrollablerisks.

Asat theendof the reportingperiod, theCompany recordedabalanceofRMB48,016million in financialassetssoldunderrepurchaseagreements,representingadecreaseofRMB50,555millionor51.29%fromthefigureatthebeginningof theperiod,mainlydue to thecompanyadjusted liabilitiesallocationand reducedselling repurchaseassets.

Unit:RMBmillion

TypeDecember31,2015 December31,2014

Balance Percentage(%) Balance Percentage(%)

Bonds 39,980 83.26 78,188 79.32

Bills 8,036 16.74 19,864 20.15

Others - - 519 0.53

total 48,016 100 98,571 100

37

2 0 1 5 ANNUAL REPORT

(III)AnalysisoftheincomestatementDuring the reportingperiod, theCompanydeliveredsteadyandhealthygrowth invariousbusinesses,withsteadygrowth in interest-bearingassets.TheCompany flexiblyallocatedassetsbycapturingmarketopportunitiesandincreasedtheyieldsofinterest-bearingassets,withstablenetincreasemargin.Therewasasustainedgrowthinfeeandcommissionincome.Thecost-to-incomeratiowasmaintainedatarelativelylowlevel.ThenetprofitattributabletoshareholdersoftheparentcompanyreachedRMB50,207million,up6.51%year-on-year.

Unit:RMBmillion

Item 2015 2014 Increase/DecreaseYoY(%)

Operating income 154,348 124,898 23.58

Net interest income 119,834 95,560 25.40

Netnon-interestincome 34,514 29,338 17.64

Business tax and surcharges (12,955) (9,105) 42.28

Operating and administrative expense (32,849) (29,451) 11.54

Duringthereportingperiod,thenetinterestincomeoftheCompanywasRMB119,834million,upRMB24,274millionor25.40%year-on-year,mainlybecause interest-bearingassetsgrowth.Ononehand, the interestmarginof theCompanydecreasedslightly,thenetinterestmargindownby0.03percentagepointto2.45%.Ontheotherhand,thebusinessmaintainedasteadyandrapidgrowth,dailyaveragescaleof interest-bearingassetsup26.71%year-on-year.

TheinterestincomeincreasedRMB36,558millionor16.66%year-on-year.TheinvestmentinterestincomeincreasedbyRMB58,205millionor116.84%year-on-year,mainlydue to the investmentdailyaveragescaleup135.90%year-on-yearandholding resale interest incomedecreasedbyRMB28,953millionor51.39%year-on-year,mainlybecausedailyaveragescaleunderrepurchaseagreementsdown43.43%year-on-year.

During the reportingperiod, thenetnon-interest incomeof theCompanywasRMB34,514million,accounting for22.36%oftheoperatingincome,representinganincreaseofRMB5,176millionor17.64%year-on-year.Thespecificcompositionissetoutasfollows:

Unit:RMBmillion

Item 2015 2014

Net fee and commission income 32,190 27,041

Gainandlossfrominvestment 3,482 (96)

Gainandlossfromchangesinfairvalue 1,378 1,631

Gainandlossfromexchange (2,850) 692

Income from other businesses 314 70

total 34,514 29,338

Duringthereportingperiod,theCompanyrealizedfeeandcommissionincomeofRMB32,190million,upRMB5,149millionor19.04%year-on-year. Items likegainand loss from investment,gainand loss fromchanges in fairvalueandgainandlossfromexchangewerehighlyinterrelated.Afterthereclassificationbasedontheirbusinessnature,thegainrecognizedreachedRMB2,010million,downRMB217millionyear-on-year.

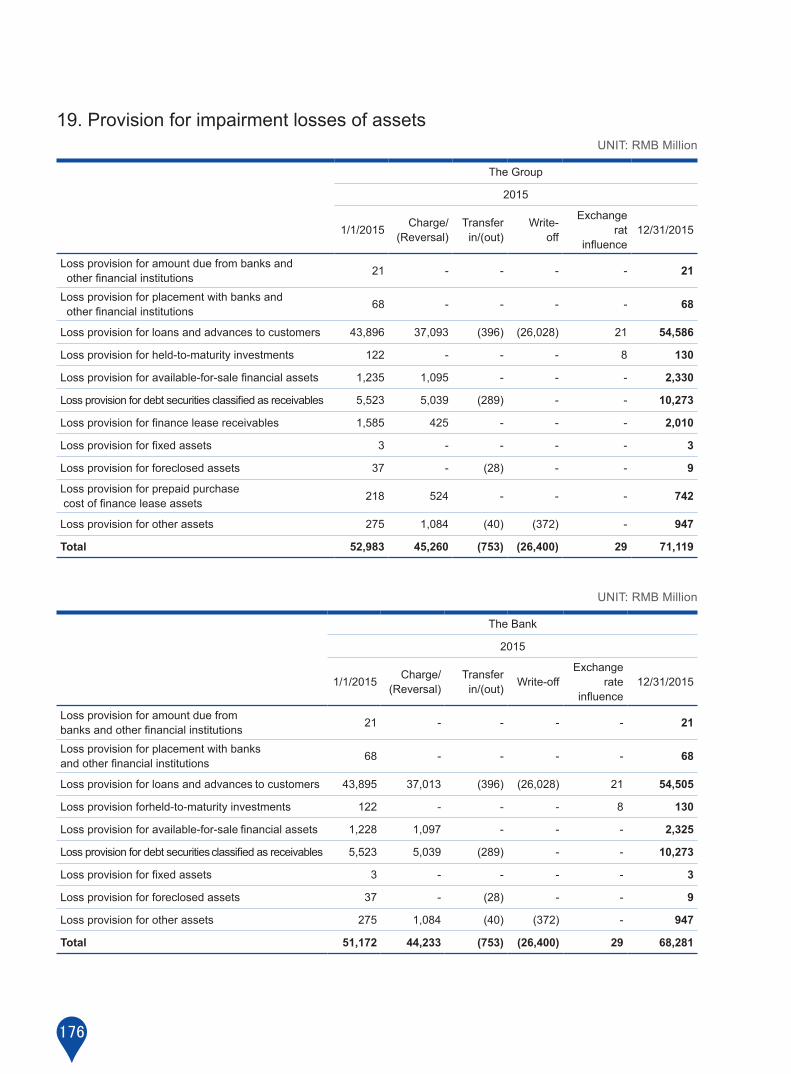

During the reportingperiod, theCompanyaccrueda loan impairment lossofRMB37,093million,upRMB17,442millionyear-on-year,mainlybecauseoftheincreaseinscaleofloans.TheCompanymadeprovisionforimpairmentbasedonthepredictedpresentvalueofdiscountedfuturecashflowsdeterminedaspertheoriginaleffectiveinterestratesoftheloans,pursuanttotherelevantrequirementsoftheAccountingStandardsforBusinessEnterpriseswithindustryriskstakenintoaccount.

Adheringtothefive-yearplanningstrategicobjective,theCompanyfurtherstrengthenedthemanagementconceptofconstraintsoncapital,andearnestly implementedvariouscapitalmanagementpoliciesaccordingtotheregulationsof theCapitalRules forCommercialBanks (Provisional)ofCBRC.Started from themanagementstrategy, riskconditionsand regulatory requirements, according to changes in externalmacroeconomicenvironment, andcombined with the “IndustrialBankMedium-termCapitalManagementPlanning (2014-2016)”, theCompanyformulatedcapitalmanagementplanof2015.Onthebasisofbalancingassetsgrowth,capitaldemandandcapitalsupplychannels,theCompanyfullyprovedthenecessityandfeasibilityofcapitalsupplement,ascertainedthecapitaladequacyratiomanagementgoal,soastorealizeahealthy,sustainableandsteadydevelopment.

Ininternalmanagement,theCompanyreinforceditscapitalallocationfunctionbyfocusingonthereturnontargetriskassetsandarrangementsonthescaleofrisk-weightedassetsineachbusinessdepartmentandbusinesssegment,soastooptimizecapitalallocationandstrivetomaximizethereturnonrisk-weightedassets.TheCompanyfurtherunleashedtheadvantageofgroup-orientedandintegratedmanagement,strengthenedthemanagementofcapitalofsubsidiaries,andgraduallyestablishedtheinvestmentallocationpolicyandprocesswhichareinfavoroffund-raisingandallocation,operationmanagement,performanceappraisal,andinvestmentallocation,soastomeetthedemandofcollectivizationand the integratedmanagement forcapitalmanagement.According to relatedguidelinesof theCapitalRulesforCommercialBanks(Provisional)ofCBRCandprovisionsofotherdocuments,theGroupmonitorsitscapitaladequacyandcapitalapplicationinrealtime.

2.Implementationofthenewcapitalaccord

TheCompanyalwaysattachesgreat importance to the implementationof thenewcapitalaccord,andproactivelypromotes theworkunder thenewcapitalaccordbystageandwithemphasisaccording to relevant regulatoryrequirementsofCBRC.TheCompanyconstructedbasicallycompleteworkingsystemof thefirstpillarof thenewcapitalaccord,makinggreatachievementsinconstructionofthenewcapitalaccord.

In respectof systembuildingandworkguarantee, theCompanybasically setupasystem framework for theimplementationof thenewcapitalaccord,coveringcapitaladequacy ratiomanagement, internal ratingprocessand frameworkconstruction,model validation, internal ratingapplicationmanagement, stress testing,anddatamanagementandsoon,carriedoutcompletebank-wide trainingandbanking industry research formany timeseveryyear,andpromoted theapplicationof thenewcapitalaccordsystem idea in thewholebank. In respectofprojectconstruction,non-retailinternalrating,retailinternalrating,creditriskweightedasset(RWA),themarketriskmanagementsystem,theoperationalriskmanagementsystemandthemodellaboratorywereapplied.In2015,theCompanycarriedout theSelf-assessmentonComplianceofAdvancedCapitalMeasurementMethods for theFirstPillar, theAuditProjectofAdvancedCapitalMeasurementMethods, theCreditRisk InternalRatingSystemProjectand theVerificationProjectofMarketRisk InternalModelSystem for the first time. In respectofmeasurementinstrumentapplication, theCompanygraduallyexpandedthebreadthanddepthofapplicationof the internal ratingsystem,whichwasmainlyusedforauthorizationmanagement,industrylimitmanagement,customerlimit,provisionassessment,comprehensiveappraisalandcapitalallocationmanagementandsoon.

TheapplicationofnewcapitalaccordprojectoftheCompanypaidmoreattentiontothefurtherapplicationofprojectresults inbusinessmanagementand riskmanagementbasedon theactualneeds toperfect riskmanagement,effectively improved the standardization and refined levels of riskmanagement, andmeanwhile sped upimplementationofthenewcapitalaccordoftheCompanyrelyingonthefirstpillarcompliance.

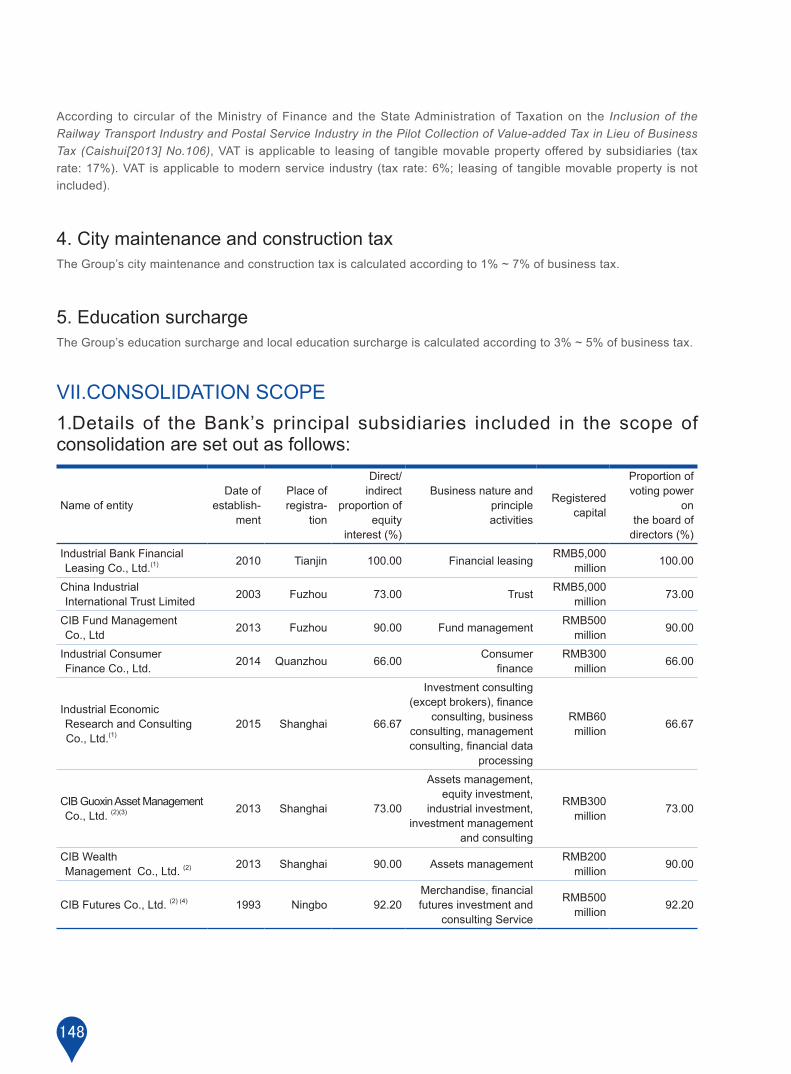

Thecalculation range for theconsolidatedcapitaladequacy ratioof theCompany included the IndustrialBankCo.,Ltd.andfinancial institutionscomplyingwith requirementson thecalculationrangeof theconsolidatedcapitaladequacy ratio inSection I,Chapter IIof theCapitalRules forCommercialBanks (Provisional)ofCBRC.Tobespecific, thisapplied to thebankinggroup jointlycomprisedof IndustrialBankCo.,Ltd., IndustrialBankFinancialLeasingCo., Ltd,China Industrial InternationalTrust Limited,CIBFundManagementCo., Ltd. and IndustrialConsumerFinanceCo.,Ltd.

Secondly, layingmoreemphasison innovation.TheCompanywill further increase the innovation intensityofbusinessproductsandbusinessmodes,paymoreattention to the innovationanddevelopmentof theOff-BalanceSheetActivities (OBS),anddevelopnewchannelsofbusinessesandprofit growth.TheCompanywill furtheraccelerateinnovationofthoughts,methods,meansandtoolsforriskmanagement,andeffectivelygraspthematerialrisks,soastopromotetheimplementationofnewbusinesses.

Thirdly,layingmoreemphasisonlinkage.TheCompanywillunswervinglydeepengroup-orientedandcomprehensiveoperations,andcontinuouslyenlargecooperationand linkageamong lines,agencies,andsegments, soas toimprovetheefficiencyandability forobtainingcustomers,andfurtherexplore thecustomers’value.TheCompanywillcontinue to integratebusiness resources includingcommercialbanks, investmentbanks,capitalmanagementandwealthmanagement,improvetheservicechain,andincreasecomprehensiveincome.

Fourthly, layingmoreemphasison refinement.Adhering to theperspectiveof theentireGroup, theCompanywillmakeoverallplanningandpromote theconstructionof refinedmanagement tools including the internal transferpricing,managementaccounting, resourcesandprofit distribution,evaluationmanagement, soas toprovideapowerfulbasicmeanssupport for internalbusiness linkageof theGroup.TheCompanywill enrichdigitalandintelligentbuildingof thebusinessoperationandmanagement,andplay theroleofboostingandevendrivingandleadingofscienceand technology tobusinessdevelopment.TheCompanywillprofoundlypromote theapplicationofmobile internet,bigdata, cloudcomputing,artificial intelligenceandotheradvanced technologies, transformbusinessesandpromoteinnovationwithscienceandtechnology,andcontinuouslyimprovethedigitalandintelligentlevelsofbusinessoperations.

IndustrialLeasingcontinued topromote innovations infinancingbusiness,andsuccessfully issued two tranchesoffinancialbondsofRMB5billion in total.Thecompanycontinued topromotecross-borderfinancingbusiness,andcompletedtwocross-borderRMBloanbusinesses in theQianHaiShenzhen-HongKongCrossBorderCooperationZone.Thecompanyobtainedthequalificationsforcarryingoutleasingassetsecuritizationbusiness,furtherenrichedthefinancingtools,andimprovedassetmanagementcapabilities.

51

2 0 1 5 ANNUAL REPORT

(2)ChinaIndustrialInternationalTrustLimited

China Industrial InternationalTrustLimited isaholdingsubsidiaryof theCompanywith registeredcapitalofRMB5billionandtheCompanyholds73%ofthecapital.Thebusinesscoversfundtrust,movablepropertytrust,immovableproperty trust,negotiablesecurities trust,otherpropertyorproperty right trustandotherbusinessesstipulatedbylawsandregulationsorapprovedbytheChinabankingregulatoryagencies.IndustrialTrust’s own assets, gains and losseswereincludedintheCompany’sconsolidatedfinancialstatements,butitstrustassets,gainsandlosseswerenotincluded.

During the reportingperiod, closelyadopting the strategic target of cultivating itself intoa“comprehensive, diversified,andfeaturedtopnationaltrustcompany”andstickingtothedevelopmentdirectionof“stabilizingscale,adjustingstructure,preventing risks,enhancingefficiencyandemphasizing innovation”, IndustrialTrustactivelypushedforwardbusinesstransformationandstructuraladjustment,comprehensivelystrengthenedriskmanagementand internalcontrol,continuously improvedcomprehensiveoperationalstrategies, realized rapiddevelopmentofallbusinesses,made itsmajoroperation targets rank thefirst tireofnational trust industryandmaintainedsoundassetsquality.Asat theendof thereportingperiod, IndustrialTrust’sownassetsamounted toRMB16.035billion,up29.49%fromthebeginningoftheperiod,owners’equitywasRMB12.426billion,up11.97%fromthebeginningoftheperiod,andtheassetundermanagementincreased49.02%toRMB1,046.027billion,whichwasthefirsttimetoexceedone trillion.During the reportingperiod, the realized revenuewasRMB2.944billion,ofwhich the trustbusiness incomewasRMB1.632billion, fixedbusiness incomeandotherbusinesses income totaledRMB1.312billion, therealized totalprofitwasRMB2.122billion, thenetprofitwasRMB1.611billion,up14.62%year-on-year.ROEwas13.74%,andcost-to-incomeratiowas22.75%.Asattheendofthereportingperiod,thebusinesssizeofsubsistingtrustofIndustrialTrustwasRMB908.482billion,up40.92%fromthefigureatthebeginningoftheperiod.

IndustrialTrust continuouslypromoted thebusiness transformationandstructuraladjustment, soas to furtherimprove theproactivemanagementandbusiness innovationcapabilities.Asat theendof the reportingperiod,collection trust business scale of IndustrialTrust reachedRMB229,663million, representing an increaseofRMB81,347millioncomparedtothefigureatthebeginningoftheperiod;propertyrighttrustbusinessscalereachedRMB107,072million, representingan increaseofRMB78,970million.The trustbusinessstructurecontinued tobe improved. Internationalbusinessmadebreakthroughs,assetsecuritizationbusinesswas rapidlypromoted, thefirstactivemanagement industrial fundwasestablished,and thefirstaccumulation fundandpersonal loanassetsecuritizationproductwas issued. IndustrialTrustsmoothlyobtained thequalification for foreignexchange trustbusiness,registeredbytheprivateequityfundmanagersoftheAssetManagementAssociationofChina,andsteadilypromotedbusinessesincludingfamilytrust,pensiontrust,publictrust,consumertrust,mixedownershipreformandsoon.

IndustrialTruststrictlyimplementednationalmacropoliciesandfinancialregulatoryrequirements,adheredtosoundcompliancemanagement idea, andst rengthened comprehensive r isk management and internal control, soas tomaintaingoodassetqualityandmakeall themain indexesconform toregulatory requirements.Asat theendof the reportingperiod, IndustrialTrusthadnosurvivalornewnon-performingassets, all trust planswith liquidationweretimelypaid inasafemanner,andsurvival trust property operationwasinnormal condition. It also increasedinvestment in foreignfinancialequities,and made new b reak th roughs in

52

comprehensiveoperation.

Comprehensivemanagement layouthasbeen involved inassetmanagement, futuresservices,securitiesservices,financial researches,enterprisegroup financialmanagement,andother fields.Comprehensive financial servicecapabilityhasbeenfurtherimproved.IndustrialTrustwhollyownsCIBGuoxinAssetManagementCo.,Ltd.It isthecontrollingshareholderofCIBFuturesCo.,Ltd. It invests IndustrialEconomicResearchandConsultingCo.,Ltd.,ZijinMiningGroupFinanceCo.,Ltd.,HuafuSecuritiesCo.,Ltd.,andChongqingMachineryandElectronicsHoldingGroupFinanceCo.,Ltd., realizedprofitsduring the reportingperiodofeachequity investmentproject,andgainedgoodequityinvestmentincome.

(3)CIBFundManagementCo.,Ltd.

The registered capital of CIB FundManagementCo., Ltd. wasRMB500millionand theCompanyheld90%of its total capital.Asof yet,CIBFundManagementhas set up tenbranches inChina,includingShanghai,BeijingandShenzhenandwhollyownedthefundsubsidiarycompany-CIBWealthManagementCo.,Ltd.During thereportingperiod,CIBWealthManagementCo.,Ltd. investedequityandestablishedChina IndustryDigitalFinancialService (Shanghai)Co.,Ltd.andheld51%ofitstotalcapital.TheregisteredaddresswasatChina (Shanghai)PilotFreeTradeZoneand the registrationwithIndustrialandCommercialAuthoritywascompetedinNovember2015.

CIBFund has followed the business philosophy of“Within theLaw, Innovation,PlateLinkageandBrandBuilding”, persisted in developingpublic offeringandnon-public offering simultaneouslyandactivelyadopted thebusinessstrategyofmaintainingabalancebetweenmanagerial businessand investment consultation. It hasadhered to the mission of “Establishing characteristics throughbuilding thebrandwithpublicofferingproducts, improving thescalewith constant returns with active management”, realizing rapidand steady development in all businesses.As at the end of thereportingperiod,CIBFundhad totalassetsofRMB1.783billion,up46.65% from thebeginningof theperiod.Owners’ equity reachedRMB1.039billion,up63.58%fromthebeginningoftheperiod.Duringthe reportingperiod, the realizedoperating income totaledRMB728millionandthenetprofittotaledRMB244million,increasedby103.34%year-on-year.Asattheendofthereportingperiod,thetotalassetsmanagementsizereachedRMB412.653billion,increasedby111.86%fromthebeginningoftheperiod,ofwhichpublicofferingof fundaccounted forRMB73.481billion,specialaccountof the fundcompanywasRMB36.865billion, thespecialaccountof thesubsidiary fundcompanyaccounted forRMB302.308billion. InNovember2015,CIBFundwasofficiallyapproved tobe theQualifiedDomestic Institutional Investors (QDII)byCSRC.

IndustrialConsumerFinanceconstantlypromoted innovationofsystemsandmechanisms,established three linesofdepartments inaccordancewith theprincipleofdelayeringand intensification,andclarified theoperationalmechanism of “reporting line+delegation”;setupbusinessdepartment fornetworkbusiness,specialbusiness,E-businessandsecurities trader in the incubatormodetopromote thedevelopmentofonlinebusiness;proactivelyoptimizedtheITsupportingplatformbasedonmobileinternettechnology,independentlyresearchedanddevelopedPADmobilemarketingsystem,and realizedpaperlessoperations from loanmaterial submission toexaminationandapproval; successfully launchedonlineexhibition channels includingempty-handaccess to thewebsite,WeChatclient-sideandmobileAPP,and launchedFamousCompanyTrainandPOSflow loanandother Internetproductsofmanyscenarios;successfully researchedanddevelopedself-service loanmachineswith independentintellectualpropertyrights,plannedtobearrangedin2016inlargequantities.Madeeffortstoimproveandintegratethe traditional riskcontroland the riskmanagementmechanismbasedon thenewriskcontrolby the lawof largenumbers,establishedandimprovedtheriskcontrolmechanismsincludingthethree-personloanreviewmechanism,the five-persongroupsecuritymechanism, the risk fundmechanism, themultidimensionalcollectionsystemandaccountabilitysystem,paidattention tocombining the thirdpartycredit informationandbigdatamanagementwayto identify thecustomer risk,andcontinued to improve the risk identificationcapabilityandpost-loanmanagementcapability.

IndustrialEconomicResearchandConsultingCo.,Ltd.was founded inJune2015and is the firstprofessionalresearchinstitutionoperatedincorporateforminthedomesticbankingindustry.IndustrialResearchhaspreliminarilyestablished researchsystemsofsuch fourfieldsasmacro (incl. interest rates,exchangeratesandcommodities),industryandcredit,financialengineeringandproducts,anddatamining.Sinceitsestablishment,IndustrialResearchreleasedover560regularreports(daily,weekly,andmonthly),fastassessment,andspecialreportsandsoon;heldlectures, forums,business training,specialconference, research,and thecustomerpromotionconferenceandsoon,over90intotal;theservicescopecoveredheadofficedepartments,branchesandsubsidiariesintheGroupandagenciesofthesametradeandregulators,etc.outsidetheGroup.

IndustrialResearch’sresearchresultscloselyfollowedthetrendofdomesticandforeignfinancialmarkets,accuratelyforecasted the inflectionpointof interest rates in thecurrencymarket inmiddle2015,andaccuratelypredicted thetrendofRMBexchangerates; industrialspecial researcheswerehighlyeffective,credit researches tightlygraspedthechanges incredit risk,andbonddefaultexceeded70%. IndustrialResearchdevelopedandstarted financialengineeringquantitativeproductsandstrategies,and implemented investmentadvisoryservices.Each researchresultwasfit formarketdevelopment, followed theGroup’s business needs, made important contributions to the operation of the Group’sbusinesses,enablingitsresearchservicestopromotebusinessgrowth.

Adheringtotheoperationalstrategyof“stabilizingdevelopment,ensuringsecurityandpromotingtransformation”, theCompany responded to thechangesofsituation,activelyandproperlyhandled risksand realizedsteadyandhealthydevelopmentof thecorporate financebusiness throughstrengtheningstructuraladjustment,speedinguptransformationandupgradingandenhancingbasismanagement.

Firstly, theasset-liability structuremaintainedbalanceddevelopmentandcustomer foundationcontinued tobestrengthened.Asat theendof the reportingperiod, thebalanceofcorporatefinancedeposits in localand foreigncurrenciesamountedtoRMB2,109.799billion,upRMB212.508billionfromthebeginningoftheperiod,dailybalance

54

ofcorporatefinancedeposits in localandforeigncurrencieswasRMB2,090.1billion,upRMB359.6billionfromthebeginningoftheperiod,andthebalanceofcorporatefinanceloansinlocalandforeigncurrencieswasRMB1,267.502billion,upRMB60.304billion from thebeginningof theperiod,and the total corporate financecustomerswere469,520,ofwhich137,751werebasiccustomers.Secondly, theCompanyadapted to the typeofoperations toaccelerateinnovation,withoutstandingfeaturesandobviousadvantages.Complyingwiththenationaldevelopmentstrategy,basedonthecustomerservicerequirementchangesandthevigorousdevelopmentoftheInternetfinance,theCompanystrivedtopromoteinnovationandupgradingofproducts,servicesandprocess,andmadeinnovationsandbreakthroughsinthecapitalmarket,greenfinance,Internetfinanceandotherfields.UnderwritingscaleofdebtfinancingtoolsrankedNo.1forfourconsecutiveyearsamongjoint-stockbanks;totalscaleofreleaseofcreditassetsecuritizationproductsrankedNo.1amongjoint-stockbanks,andcreatedsuchinnovativecasesasthefirstshort-termsecuritizationproductinthemarket,thefirstdomesticCLOproductinvestedbyQFIIandthesuccessfulmarketof thefirstassetsecuritizationproduct in the inter-bankbondmarket;financingbalanceofenvironmentalfinancialbusiness increased40%,breaking throughRMB300,000million;dealsumof the“three Internet through trains” of receiptandpayment, financing,and treasury reachedRMB150,000million.Thirdly, theCompanyhighlightedcomprehensiveoperationadvantagesby linkagewithin theGroup. Incooperationwith IndustrialTrust, IndustrialLeasing,IndustrialFundandothersubsidiaries,theCompanyobtainedmaterialoperationalresultsinindustryfunds,assetsecuritization,bondunderwritingandinvestmentlinkage,operationandleaseintegration,moneymanagement,futures,proprietary investment,warehousewarranthedgingfinancing in theoperationalperiodandotheraspects,promoted formationof thecooperationmodeofdivisionof laborandorderly linkagewithin thegroup,andmet therequirementsfordiversifiedfinancialservicesofenterpriseswhilemaximizingtheinterestsoftheGroup.

(2) Investment banking business

Investmentbankingwasbasedon themain lineofnationaleconomicdevelopment,grasped thedevelopmentopportunitiesofdirectfinancingtoproactivelypromotetheenterprisemergingandreorganization,privateplacement,mixedownership reform,enterpriseassetsecuritization, localgovernmentbondunderwriting,andPPPandotherinnovationbusinesseswhileacceleratingthedevelopmentofnon-financialcorporatedebtfinancingtools,corporatebonds,directfinancing tools formoneymanagementandotherbusinesses.Firstly, theCompanyaccelerated thedevelopmentofcapitalfinancingbusiness.Itgraspedthetrendofthecoordinateddevelopmentofthedebtinvestmentandcapital investmentbyapplicationofcombinationsofanumberof investmentbankingproducts,andfocusedonsolving the“pain points” and “difficultpoints”of improving thedebtstructureandreducing thefinancingcostbycustomers,soas toattractnumerous largehigh-qualitycustomers.Secondly, theCompanyspedup innovationandupgradingofinvestmentbankingservices,andlaunchedaseriesofinnovativeproductsofinvestmentbanksinthecreditassetsecuritizationbusiness,corporateassetsecuritizationbusinessand innovativebondbusinessandotheraspects,obtaininggoodmarketresponse.Itprovidedperpetualcapitalsecuritiesandotherfinancialproductsfor the high rating corporate customers to meet customers’ requirementsforoptimizingthestructureofassetsandliabilitiesand transforming to the light-assetoperation.Thirdly, theCompanybuiltacompleted investmentbankingsystem,andcontinuouslyexpandedthesaleschannelsofinvestmentbanks.Asofyet,theCompanyhasestablishedfavourablebusinesscooperation relationswithmostdomesticbanks,and reachedcooperation intentionswithanumberofnon-bankingfinancial institutionsrankinginfront inthemarket,realizingfullcoverageofmaininter-bankmarketinstitutionalinvestors.

During the reportingperiod, theCompanyservedas theunderwriter fordebt financing instrumentsamounting toRMB384.245billion,accumulativelyunderwrotefourissuesofcredit-and-assetbackedsecurities,whoseunderwritingamounttotalingRMB23.2billion,andwonthetenderoflocalgovernmentbondstotalingRMB192.3billion.

(3)Tradefinancingbusiness

Tradefinancialbusinessfollowedthenationaldevelopmentstrategiesincluding“OneBeltOneRoad”and free trade zoneconstruction.Firstly, theCompany reconstructed theproductsystemwith thevisionof“big tradefinance” to form four categoriesof businesses includingcorporatemulti-level financing, supply chain financing, cross-borderfinanceandcapitalhedgingappreciation,enriched the functionsofcustomerservices,and formedunique

Cashmanagementbusinesswasfit for the trendof interest rateliberalizationand Internet finance,enrichedcashmanagementproduct line,andbuiltnew Internet financestate tostrengthenthe ability of precisemarketing and differentiated services,thereby realizing thegreat increaseofcustomers,andenlargingof customers’ fundmanagementscale ina leap type.Asat theend of the reporting period, cash management customers reached 17,597,representinganincreaseof5,616comparedtothefigureatthebeginningofthereportingperiod.AveragedailyoutstandingofdepositsofthecashmanagementcustomersreachedRMB835billion, accounting for 40.3% in the average daily depositsof corporate finance, and total assets of average daily cashmanagementreachedRMB603.1billion.

Firstly, theCompanystrived tobuild thepyramid-typeproductsystemsurrounding thecash flowprocessof thecorporateandcash management customers, based on the idea of combining services and technologies, and promote the“three Internet through trains”ofreceiptandpayment,financing,andtreasury.Itcontinuouslydevelopedandupgradedtargetedproductsfromtheperspectiveof featuredsettlementbusiness tomeetcustomers’ practicalneeds,captured thepotentialneedsof thecustomers,and promoted product construction from customers’ needs.Secondly, theCompanyprepared correspondingstandardizedcashmanagementserviceschemebasedon thescaleofall kindsofcustomers, launchedserviceschemesofmedicine,educationandenergy industries,andpersonalize theschemescombinedwith theneedsofcustomers.Smartmedicalproductshavecovered49regionsin27branches,andservicedmorethan300hospitals.Thirdly,theCompanybuiltacompletebusinesschaincenteringoncapitalcollection,allocation,settlement,storageandapplicationofcorporatecustomers,andexplored toprovidecashmanagementservicesofdifferentcategoriesandlevelsfordifferentcustomers,applyingcashmanagementservicesineachprofessionalfield.

(5)Environmentfinancebusiness

Regarding the construction of “Green China”as itsownresponsibility,environmentalfinancialbusinesscoverednumerousprojects including improvingenergyefficiency,newenergyand renewableenergydevelopmentandutilization,carbonemission reduction,wastewater treatmentandwaterareamanagement,sulfurdioxideemissionreduction,andsolidwasterecycling,becomingthemostdistinctivebusinessareaunderdifferentiatedoperations.As

56

attheendofthereportingperiod,theCompanyaccumulatively providedRMB804.6billion offinancing to no less than 6,000 enterprisesand thebalanceof financing ingreen financereachedRMB394.2billion.

Firstly, theCompany listed theenvironmentalfinancial business as the core business andoneof theannual businesseswithemphasison development, and established the groupl inkage and coord inat ion mechanism forenvironmental finance to transfer the“green bank” to the “green f inancia l group” .Secondly, environmental protection benefitswere more obvious.As at the end of thereportingperiod,annualsavedstandardcoalofprojectssupportedbytheenvironmentfinancialbusiness reachedabout25,538.6 thousand tonnes,annualcarbondioxideemission reductions reached71,619.9thousandtonnes,annualemissionreductionsofchemicaloxygendemand(COD)reached1,387.4thousandtonnes,annualcomprehensivelyusedsolidwaste reached17,290.4 thousand tonnes,andannualwater-savingamountreached285,650.6 thousand tonnes.Thirdly, theCompanycontinued topromoteenvironment finance innovationandexploration.Withrespecttothecarbonfinance,itestablishedrelationshipwithsevendomesticcarbonemissiontradingpilotprovincesandcities,signedacooperationagreementwithsixof them,andbecamethemainclearingandservicebank inmost regions.With respect toemission rightfinance, itsignedacooperationagreementwith10of the11domesticemission right tradingpilotprovincesandcities,andconductedbusinesscooperationsuchasemission rightmortgage loans, trading fundstorageandsettlement,and financialchargingaccountopening.Fourthly,theCompanycontinuouslypromotedmarketinfluenceandpublicrecognition.Itwonthefifth“AnnualBestGreenFinanceAward”appraisedbytheChinaBankingAssociation,receivedtheinvitationtoparticipatein“EnergyEfficiencyCreditGuideTrainingSeminar” of the CBRC, “EnergyEfficiencyFinancing InnovationMechanismResearch Topic” of theWorldBank,andproject researchongreen financial reformandgreen transformationpromotionoftheChinaCouncilforInternationalCo-operationonEnvironmentandDevelopment.

(6)Smallenterprisebusiness

Businesses of small enterprises kept providing better service to the general public of traditional business,continuouslypromoted theconstructionof“sixspecialmechanisms”ofsmallandmicrobusinesses focusingonexclusiveorganizationsystem,exclusive risk technology,exclusivebusinessprocess,exclusiveproductseries,exclusive incentiveandconstraint,andexclusive resourceallocationbasedon theprofessionaloperations,andcontinuously improvedtheprofessionalandrefinedmanagement levelsofsmallandmicrofinancialservices.Asattheendofthereportingperiod,thenumberofcustomizedsmallandmicroenterpriseoftheCompanytotaled372.2thousand,andthebalanceofloansforsmallandmicrobusinessesamountedtoRMB104.212billion.

TheCompanystrivedtostrengthentheconstructionofsmallandmicroenterprises’exclusiveproductsandfeaturecluster,createdfinancialservicesanddifferentiatedcompetitiveadvantagescoveringthewholelifecycleofsmallandmicroenterprises,withmoredistinctbusinesscharacteristics.Firstly,basedonregionalcharacteristics,theCompanyachievedprominentclusterconstructioneffects.Asattheendofthereportingperiod,729smallbusinessindustrialclustersof theCompanywereconstructed,up45.51%fromthebeginningof thereportingperiod,and thebalanceof loansof theclustersreachedRMB35.3billion,up79.37%fromthebeginningof thereportingperiod.Secondly,“TheThreeLoanServices”brandandscaleeffectforsmallandmicroenterprisesgivenpriorityto“Easy&FastLoan”,followedby“TransactionLoan” and cooperated with “ConsecutiveLoan”wasfurtherhighlighted.Asattheendofthereportingperiod,loansamountedtoRMB24.88billion,providingfinancingservicesforapproximately

57

2 0 1 5 ANNUAL REPORT

7,000small andmicroenterprisecustomers.Thirdly, smallandmicro Internetfinanceof“Internet+Bank+Platform” madebreakthrough in development.As at the end of thereportingperiod, online financing customers reached208,and thebalanceof loans reachedRMB474million.Fourthly,the “EntrepreneurialFinance” servicesystem integrating“debt financing, equity financing, settlement andmoneymanagement,andadvisoryserviceswasofficially launchedin the market, and “EntrepreneurialLoan”,“Three-BoardSeries Products” and “VCreation” small andmicroenterprises’specialactionplanswereinnovativelylaunched.

(7)Institutionalbusiness

In termsof institutionalbusiness,adhering to taking root infinance,social insurance,publicutilities,healthcare,cultureandeducationandother fields, theCompany implemented“big infrastructure, health, and culture”developmentstrategy, and strengthened industry service ability.As atthe end of the reporting period, theCompany obtained423central, provincial,municipal, anddistrict-levelagencyqualifications, increasing by 83 from thebeginning of thereportingperiod.Technologicalcapabilitiesprovidedastrongsupport for institutionalcustomers,“Thecentralgovernmentnon-tax revenuecollectionsystemof theMinistryofFinance”waspassedby theentireacceptancegroupof theMinistryofFinance;after thecross-provincial trafficviolationfinepaymentsystemof theMinistryofPublicSecuritywas launched, itwasacceptedandapprovedby the threeministriesof theMinistryofPublicSecurity, theMinistryofFinanceand theCentralBank.With respect to theconstructionof theprovincial treasuryconcentratedpaymentelectronicbusinesssystem,itwasdevelopedandintegratedinFujian,HebeiandLiaoning,anditwasconnectedtonearly400budgetunitsinFujian.

Asat theendof the reportingperiod, thenumberof institutionalcustomers reached21,627,up1,481 from thebeginningof theperiod; thebalanceofcustomerdepositswasRMB552.989billion,upRMB37.063billion fromthebeginningoftheperiod,andthedailybalanceofinstitutionaldepositswasRMB529.465billion,upRMB63.504billionyear-on-year.

2.Retailfinancebusinesssegment

(1)Overview

Under thecircumstanceofeconomicdownturn,especiallywhenChinawaspromoting“de-capacity,de-stocking,de-leveraging”andthepressureofbankassetsqualityconstantly increased,theCompanyimplementedthe“one bodyand twowings”specializedservicesystemand thedevelopmentconceptofsizeable investment,sizeableassetmanagement,andsizeablewealthmanagementdevelopment layout toseekprogressamidstability,activelyplanned transformationdevelopment in itsoperationaldirection,marketingpromotion,businesscapability,productinnovationandcoordination,continuedtostrengthenthereformoftheworkmodeofbusinesshallsandcreditcardsystemmechanism,speededup the transformationof traditionalbranchnetwork,enhanced thebrandbuildingof“FourLife”, thereby realizing the improvementofspecializedbusinesscapability.Asat theendof the reportingperiod,therewere36.505millionretailbankingcustomers(includingcreditcardcustomers),increased4.977millioncustomersfromthebeginningoftheperiod.ThebalanceofcomprehensivefinancialassetsofretailcustomerswasRMB1,209.4billion,upRMB198.9billion fromthebeginningof theperiod.Duringthereportingperiod, therealized

58

reta i l in termediary business income wasRMB14.111 billion, up 21.14%year-on-year.Thenet incomeof retailbankingbusinesswasRMB27.733billion,up15.32%year-on-year.

With respect to management, f i rs t ly, theCompanyadhered to focusingon“customer, comprehensivefinancialassetandrevenue”as i ts primary business direction to optimizebusiness resources allocationmanagement,strengthenbusiness inputandoutputaswellas riskmanagement.Secondly, theCompanystrengthened the transformation of branch networkandchannel integrationcoordination,to speedup the constructionof a communitybank for it togohand inhandwith traditionalbranch network reconstruct ion, so as to promotethesmaller,smarter,andmorecommunity-orienteddevelopmentmodel.Thirdly,theCompanyimplementedthedevelopmentstrategyofbusinessbrands,promoted thebrandcultivationandconstructionof“FourLife”, continuing todevelop the“EnjoyableLife”servicebrand in thepensionfinancefield,promoted themarketingof“DynamicLife”CIBDynamiccreditcardandbracelets;centeredoncustomers,“WealthyLife”cultivated thetrust of customers toward “WealthyLifeBrand”;TheCompany launched theoverseas financialservicebrand“UniversalLife”withbusinessessuchasvisacourierserviceandoverseasstudy loansasentry to fosterandaccumulatequalityretailcustomers.Fourthly,theCompanylaunchedthereformofoperatinghalllabororganizationmodel,vigorouslyreinforcedthereformandimplementationofcreditcardsystemmechanism,promotedtheplanof“onepositionwithvariouscapabilities”ofoperatinghallstaff,perfectedandcarriedoutseparationmodelofhigh-lowcounter,soas toenhancecapability increaseandpersonnel transformation.Fifthly, theCompanycontinued toenhance the implementationofbasicwork,promoted theconstructionof retailcustomersseparationmanagementsystem, perfected themechanismof developing customer system, continuously optimizedVIP value-addedservicesolutions,strengthened thebuildingofservicestandardizationsystem,activelypromoted thestandardizedmanagementofbranchnetworkstaff,improvedthestaffefficiencyofretaillinesacrosstheBank,strengthenedcostcontroloverall,activelyorganized thepromotedconstructionof technologyplatform relating tomobilepayment,promotedbranchnetwork transformationandcapability lifting,andstrengthened the internaldevelopmentabilityofretailbusinesses.

(2)Retailbankingbusiness

With respect to retail liabilities, theCompanykeptupwith the trendof interest rate liberalization,andcontinuouslystrengthened themanagementof interest rates,guidedandencouragedbranches toenhanceexpansion intensityofcurrentdepositsandshort-termfixeddepositsthroughinterestrateauthorizationmanagement,windowguidance,etc.,achievinggoodresultswith thebalanceof individualdeposits reachingRMB374,124millionat theendof thereportingperiod.TheCompanygraduallydividedtheoriginalstructuraldeposits,andproactivelyreducedthecostofdebt;innovatedthelargeamountdepositcertificates,withthebalanceoflargeamountindividualdepositcertificatesatoverRMB8billionattheendofthereportingperiod,whichmadeupfortheshortcomingsoftheshort-termfixeddepositproductstructure.

With respect to the retail credit business, theCompanyproactively responded to the call of thegovernment,increasedsupportforloanstoowner-occupiedproperties,andpromotedthedevelopmentofhousingmortgageloanbusiness.Meanwhile, inorder toadapt to thechangesof themarketconditions, theCompanyconstantly improvedandupgraded the retail credit product system,enrichedand innovated retail credit products, accelerated thepromotion of the “flourishing”characteristicindustrialloans,strengthenedthelinkagemarketingofretailproducts,

Withrespecttotheretailwealthbusiness,theCompanycontinuedtopromotethetransformationoftheretailwealthbusiness,andvigorouslydeveloped theagencybusiness, thus forming themulti-categoryandmulti-channel retailwealthproductsupplyandsalessystem;carriedout the retailwealthbusinessmainlycenteringon theproductstructurechange:firstly, thewealthmanagementbusinessemphasiswas transferred toagencybusiness,and theagencyproduct salesgrew17%compared to thepreviousyear; secondly, financingproductswere transferredto theopennetvalueproducts, theclosed-endproductsales fell30% from thepreviousyear,and theopen-endproductsalesgrew113%.Thecontributionoftheagencybusinessintermediarybusinessincomeintheretailwealthintermediatebusiness incomebroke through20% for the first time,and the incomestructure tended tobemorereasonable.Agencybusinessofpreciousmetals,insurance,etc.madebreakthroughindevelopment,andsalesscalejumpedtothefrontamongsimilarjoint-stockcommercialbanks.Withrespecttotheretailwealthbusiness,thesalesvolume(excludingprivatebanking)offinancialproducts in localand foreigncurrencieswasRMB3,654.390billion,increasedbyRMB1,418.705billionyear-on-year,ofwhichthevolumeofopen-endproductsstoodatRMB3,110.976billion and volumeof closed-end productswasRMB543.414 billion.Sales volumeof agency productswasRMB146.247billion,upRMB21.203billionyear-on-year,ofwhichsalesvolumeoffundproducts(includingsecuritiescompanies), insuranceproductsand trustproductswereRMB122.926billion,RMB12.883billionandRMB10.438billion respectively.Accumulative transactionvolumeof tradingbusinesswasRMB142.789billion,ofwhich thetransactionvolumeofpreciousmetalsamounted toRMB136.190billionandaccumulated transactionvolumeofforeigncurrencywasRMB6,599million.

With respect to the retailchannels,communitybanksweresteadilydeveloped,and theoutlet transformationwasfully implemented.Asoneof thebankswhichstarted tobuildcommunitybanksearlier, theCompanyproactivelypromoted the “intelligentandstandardized”projectsofcommunitybranches facedwith the impactof interestrateliberalizationandInternetfinance,adheredtobecustomer-orientedtotakethecharacteristicanddifferentiatedoperationalpath,established theoveralldevelopmentstrategyof“promotingdevelopmentwith thesystem,andbuildingbrandwithservices”,andpromoted thehealthyandstabledevelopmentofcommunitybanks from theperspectivesofperfectingmanagementmechanism,settingupthemarketingplatform,optimizingproductallocation,and innovatingservicepatternandsoon.Asat theendof the reportingperiod, the licensedcommunitybranchesamountedto772,smallandmicrobranchesamountedtofive,andmorethantwothirdscommunitybranchesmadeprofits.

TheCompany fully implementedoutlet transformation,andgraduallyachieved the transformationof traditionaloutlets from the“transactionprocessing type” to the “efficiency-oriented servicemarketing type” in the “intelligent,small,community-based,andstandardized” direction and centered on the three nodes of “burden reduction,highreductionand lowreduction”with theaim toenhanceoperation,serviceandmarketingefficiency,

The credit card business focusedon the frontier of industry development, grasped the opportunity of rapiddevelopmentof internet financeandmobilepayment,endeavored topush forwardbusiness transformationandupgrading,continuouslyprovidedsafe,convenientandpersonalizedconsumptionandfinanceservicetocreditcardcustomers.Asat theendof the reportingperiod, theCompany issuedcreditcardsamounting to15.4952million,ofwhich2.1831millionwerenewly issuedcardsduring theperiod.During the reportingperiod, theaccumulatedtransactionamountofcredit cardbusiness totaledRMB451.975billion, representingayear-on-year increaseof22.73%.

Grasping thedevelopment trendof the“movement” and “health” industries, theCompanycomprehensivelypromoted the construction of the core brand of “DynamicLife”credit card to form differentiated competitive capabilities.TheCompanyissued“CIBDynamic”creditcard, integratingthephilosophyof“vitality,healthyandgreen” into theproductdesign,combinedfinancialpaymentproductswith thehealthy life ideaby the innovativemethodofexchangingcreditcardpointwithcalorieburningbyexercise.Thesynchronouslylaunchedmobilepaymentsportsbraceletoptionalaccessorieswere thefirstdomesticwearablemobilepaymentequipmentandwereon thedomesticleadingposition.Centeringonthesportsandhealthidea,theCompanysteadilypromotedtheexpansionofpreferencemerchantsandconstructionofmobilepaymentacceptanceenvironment,creatinggoodenvironment forthecardholdertousethecard.

(4) Private banking business

Centering on “consultation-driven”work in termsof theprivatebankingbusiness, theCompanyvigorouslypromotedbusinessinnovationandriskmanagementandcontrol,continuouslyenhancedcapabilitiesofresearchandanalysisandprofessionalinvestmentconsultingservices,improvedthehigh-endservicesystem,setuptheoverseasplatform,andeffectivelyenhancedmarketinfluenceandscalemerit.Asattheendofthereportingperiod,theprivatebankingcustomerstotaled18,381,up24%fromthebeginningoftheperiod,andtheconsolidatedfinanceassetsofprivatebankingcustomersamountedtoRMB263.9billion,up20%fromthebeginningoftheperiod.Theaccumulatedfinancialproducts issuedby theCompanyover thewholeyear totaledRMB167billion, representinga13%year-on-year increase.During the reportingperiod, theCompanyheld fourquarterlystrategicconferencesonfinancialmarketanalysisandallocationofgeneralcategories,andinvitedleadingexpertsandcustomerstosharetheirlatest

TheCompanyhasconstructedsoundprofessionalbusinessmanagement systemandunified financialmarketserviceplatformat theheadquarters level.Under theheadquartersmarketdepartment,sixfirst-classdepartmentsweresetup, including the inter-bankbusinessdepartment, fundoperationcenter,assetmanagementdepartment,assetcustodydepartment,bankcooperationcenterandfinancialmarketriskmanagementdepartment,allofwhichwerewith clearpositionsandduties,mutual cooperation,alongwith furtherenhancementof theconstructionofaprofessional talent team,soas toprovidecustomerswithmoreprofessional, comprehensiveandefficientcomprehensivefinancialproductsandservices.

Activelypushing forward thedevelopment strategyof“sizeable investment, sizeableassetmanagementandsizeablewealthmanagement” , theCompany took full advantageof its specialized talent teamwith financialmarketandcomparativelyfull licensestofurtherstrengthenitssharpmarketandinnovationawareness,strengthenthe linkagesof thebusinessesamong lineswithin theGroup,actively respond to thechangesandchallengesfrommarketization, facilitate the steadydevelopmentof various financialmarketbusinessesandenhance itsmarket influence.The fundoperationcenteraccuratelypredicted the trendofmarket interest rate,adoptedflexibletransactionstrategyof foreignexchangeandderivativeproducts,achieved remarkableself-operatingeconomicresults,andcontinuedtomaintainthemarketpositionofthemostactivemarketmaker.Promotingthetransformationand innovationof financialproducts, theCompany’sscaleof financialproductscontinuouslyexpended,makingthedailyaveragestockbalanceof financialproductsamount toRMB1,347.641billion,up60.27%year-on-year,accumulatedfinancing fund totalledRMB11,690.862billion, representingayear-on-year increaseof88.46%.Whiletheindustrycompetitionwasincreasinglyfierce,thescaleofassetcustodybusinessrealizedsubstantialgrowth,withtheclosingbalanceofRMB7,213.948billion,up52.64%fromthebeginningoftheperiod,therebyenablingthescaleofcustodybusiness to rise toNo.2 in themarket.Characteristic inter-bankbusinesses including theBank-to-BankPlatform, technological inputcontinued todevelop, functionalsystemof“QianDaMoneyManager”continuouslyimproved,andfinancialcloudserviceplatformbegantoconstruct.

(2)Inter-bankbusiness

During the reportingperiod, the totalnumberofonlinesecuritiesfirmsnetworked for thirdpartydepositoryservicewas98,with the industrycoverageratioof99%and the totalnumberofonlinesecuritiesfirms formargin trading,securitieslendinganddepositoryserviceswas52.Theend-usercustomersofthird-partydepositoryreached3,644.2thousand.TheCompany innovatively launched the transferserviceofstock, futuresandderivativebankproducts,with22security companieswith transfer serviceof stock, futuresandderivativebankproducts inoperation. Itcollaboratedwith67trustcompanieswithmarketcoverageratioof98.5%.Theaccumulatednumberofdirectonlinebankingwealthmanagementcustomerswithfinancecompanieswas121,with the industrycoverageratioof56%.TheCompanyestablishedagentrelationshipswith1,509institutions,coveringover100countriesandregions.Duringthereportingperiod, theCompanybecameanaffiliatememberof the InsuranceAssetManagementAssociationofChina;obtainedthequalificationforoptionfundsettlementbanksfromtheChinaSecuritiesDepositoryandClearingCo.,Ltd.;obtainedcomprehensivelyqualifiedbusinessauthorityoftheparticipantsoftheinter-agencyprivatemarketand theofferbusinesssystem,qualification for fundsettlementsystemof theoffersystem,andqualification forplatformfundsettlementbusinessoftheChinaSecuritiesJintong;becameamemberforcomprehensiveclearingofnetbondsoftheShanghaiClearingHouse.

62

(3)Bank-to-bankcooperation

As the Company’s f i rs t brand in China’s bank- to-bankcooperation, theBank-to-BankPlatform isan integratedservicesystemof the Internet finance and offline finance, providingvariouscollaborativebankswithcomprehensivefinancialservicesolutionscoveringwealthmanagement,paymentandsettlement,technological output, training services, financing services,optimizationofcapital,asset-liabilitystructure,etc.Asat theendof the reportingperiod, thenumberof collaborated customersofBank-to-BankPlatformwas653, ofwhich254werewealthmanagementgatewaycooperationcustomers,withsoldproductstotalingRMB2,163.370 billion, up 51.24% year-on-year.Theaccumulatedtotalnumberofnetworkedoutletsforcounteragencysettlementexceeded36.2 thousand.During theperiod,a totalof41,630.8 thousandaccumulatedsettlement transactionswerecompletedon theBank-to-BankPlatform, representingayear-on-year increaseof 56.77%.TheaccumulatedsettlementwasRMB2,904.144billion,up42.22%year-on-year.TheBank-to-BankPlatform’s single-year settlement transactionsand settlementamount both hit a record high.TheCompany accumulativelycooperatedwith270commercialbanks in termsofestablishmentof information systems, amongwhich 146banksmanaged tooperatewithonline informationsystems.TheCompanyhasbecomeoneof the largestprovidersof informationsystemsforcommercialbanksinChina.

Wealthmanagementbusinessrefers to theCompany’s investmentandassetmanagement in thewayagreedwiththe customer in advance upon the customer’sentrustmentandauthorization,and thecustomer’s undertaking correspondingrisksandenjoyingcorrespondingearningsasagreed,coveringsuchproductsaswealthmanagementproducts forretail,wealthmanagementproducts forcorporatecustomers, inter-bankwealthmanagementproducts,andetc.Thewealthmanagementbusiness involvesmultiple links like investmentmanagement,productR&D,issuanceandsalesandbackgroundoperation,withspecificworkflowsmainly includingproductcreation,productapproval,marketabilityapprovalandschedulearrangement,supervisionreportandinformationregistration,productsales,productinvestmentmanagementanddurationmanagement,andetc.

Wealthmanagementbusinesscontinuedtomaintainarapidgrowth,withthescaleandincomehittingtherecordhighandgrowingspeedexceedingthatoflastyear.Asattheendofthereportingperiod,thebalanceoftheCompany’s wealthmanagementproductswasRMB1,438.558billion,up72.26%year-on-year,ofwhichthebalanceofopen-endproductsandclosed-endproductswasRMB668.286billionandRMB770.272billionrespectively, takingup46.46%and53.54% respectively.Thebalanceofprinciple-guaranteedproduct includedandcalculated in the formwasRMB395.045billion,takingup27.46%,balanceofremainingnon-principle-guaranteedwealthmanagementproductsissuedandmanagedbytheCompanywasRMB1,043.513billion,takingup72.54%.Duringtheperiod,averagedailybalanceofwealthmanagementproductswasRMB1,347.641billion,up60.27%year-on-year,accumulated raisedwealthmanagement fundwasRMB11,690.862billion,up88.46%year-on-year,and the intermediary incomeofwealthmanagementbusinesswasRMB9.528billion,up22.37%year-on-year.

TheCompanycarriedout itsassetcustodybusinessbyeffectively responding to thechangesofcapitalmarket,furtherreinforcedinnovation,spedupoptimizationofproductstructureandrealizedsustainabledevelopmentoftheassetcustodybusiness.Allbusiness targetssteadily rose,and themarketpositionwas furtherconsolidated.Asattheendof thereportingperiod, thenumberofonlinecustodyproductsof theCompanywas18,799,with thescaleofassetcustodybusinesstotalingRMB7,213.948billion,upRMB2,487.907billionor52.64%fromthebeginningoftheperiod.Whileduring theperiod, therealized total incomeof intermediarybusinessesofassetcustodyreachedRMB4.316billion,upRMB105millionor2.49%year-on-year.

TheCompanyproceeded tostrengthen traditional custodybusiness toensure itsdominantpositionwithin theindustry.At thesame time, in thewakeofcapitalmarkethotspots, theCompany focusedon threemajorcustodybusinesses including thebank financialproducts, securities investment fundandcustomerassetmanagementproductsof fundcompanies,and it alsocultivatednewoperationgrowthpoint.Asat theendof the reportingperiod, thecustodybusinessofbank financialproductswasRMB1,463.563billion,upRMB701.628billion fromthebeginningof theperiod, thecustodybusinessofassetmanagementproductsof fundfirmswasRMB769.099billion,upRMB388.403billion fromthebeginningof theperiod, thecustodybusinessofsecurities investment fundwasRMB288.318billion,upRMB159.025billion from thebeginningof theperiod, thecustodybusinessof trustassetmanagementproductswasRMB1,804.582billion,upRMB496.595billion from thebeginningof theperiod,

64

thecustodybusinessofassetmanagementproductsofsecuritiesfirms’customerswasRMB1,566.627billion,upRMB395.917billionfromthebeginningoftheperiod,thecustodybusinessofinsuranceassetmanagementproductswasRMB638.298billion,upRMB117.058billionfromthebeginningoftheperiodandthecustodybusinessofprivateassetmanagementproductwasRMB213.698billion, increasedbyRMB109.169billion from thebeginningof theperiod.

(7)Futuresfinancialbusiness

During the reportingperiod, theCompanywasdesignatedby the Shanghai Futures Exchange as the depositorybank for futuresmargin.Meanwhile, it served as thedepository bankdesignatedbyChinaFinancial FuturesExchange,DalianCommodityExchangeandZhengzhouCommodityExchange.TheCompanyconstantly improvedfuturesmargin custodybusinessand technical systemsmanagement mechanism to ensure the compl ianceandstableoperationof thebusiness.On thisbasis, theCompanyactivelycarriedout thecooperationwith futuresexchangeandfuturescompaniesbusinessandrealizedthestablegrowthofthebusiness.Asattheendofthereportingperiod, theCompany’s balance of deposits of futuresfirmsand futuresexchangeswasRMB56.328billion, upRMB3.984billionor7.61%fromthebeginningoftheperiod.Amongthem,thebalanceofdepositsoffuturesmarginswasRMB49.607billion,upRMB4.243billionfromthebeginningof the period.During the period, theCompany’s dailybalanceofdepositsof futures fundswasRMB55.6billion,up119.85%year-on-year.Asat theendof the reportingperiod, therewere84 Internet futuresfirmsofbank-futurestransferoftheCompany,126futuresfirmscooperatingwiththeCompany,up14firmsfromthebeginningoftheperiod.228futuresguaranteeaccountswereopenedforfuturesfirms,ofwhich125wereearmarkedfundaccounts.Duringtheperiod,therewere10,784completedtransactionswithfuturesexchangesettlement,withatotalsettlementamountofRMB1,912.499billion.Therewere232,903completedbank-futures transfer transactions,witha totalamountofRMB292.335billion.Thecompanycontinued topromotebusinesscooperationwithfuturesfirmsinvariousareasincludingpledgeandcreditofstandardwarehousereceipts,subordinateddebtcredit,assetmanagementandassetcustody.Asat theendof the reportingperiod, therewere111assetmanagementproductsoffuturesfirmsunderonlinecustodyoftheCompany,withtotalassetofRMB2.078billion.

4.E-banking

Following the trendof“marketization,disintermediation,networkingandcustomization”of finance,E-bankingbusiness focused on“opening, focusing, execution and customer experience” tospeedup thepaceofe-financeinnovation.TheCompanystrivedtoperformwellinoperation,service,innovationanddevelopmentofonlinechannelsincludingdirectbanking, Internetbanking (onlinebanking,mobilebanking,SMSbankandWeChatbank), remotebank(telephonebanking95561;VIPspecialline4008895561).Besides,theCompanyintegratedintothewholelifecycleofcustomersofvariousecologicalscenarios,formedafullyinteractedbusinessserviceclosed-loopwithofflineoutletsandcommunitybanksand fullyexcavatedandpromoted the innovationservicevalueofnetworkfinancialchannelsandimprovedtheproductivityandcompetitivenessalongwiththeformationofnewmarketbreakthrough.

65

2 0 1 5 ANNUAL REPORT