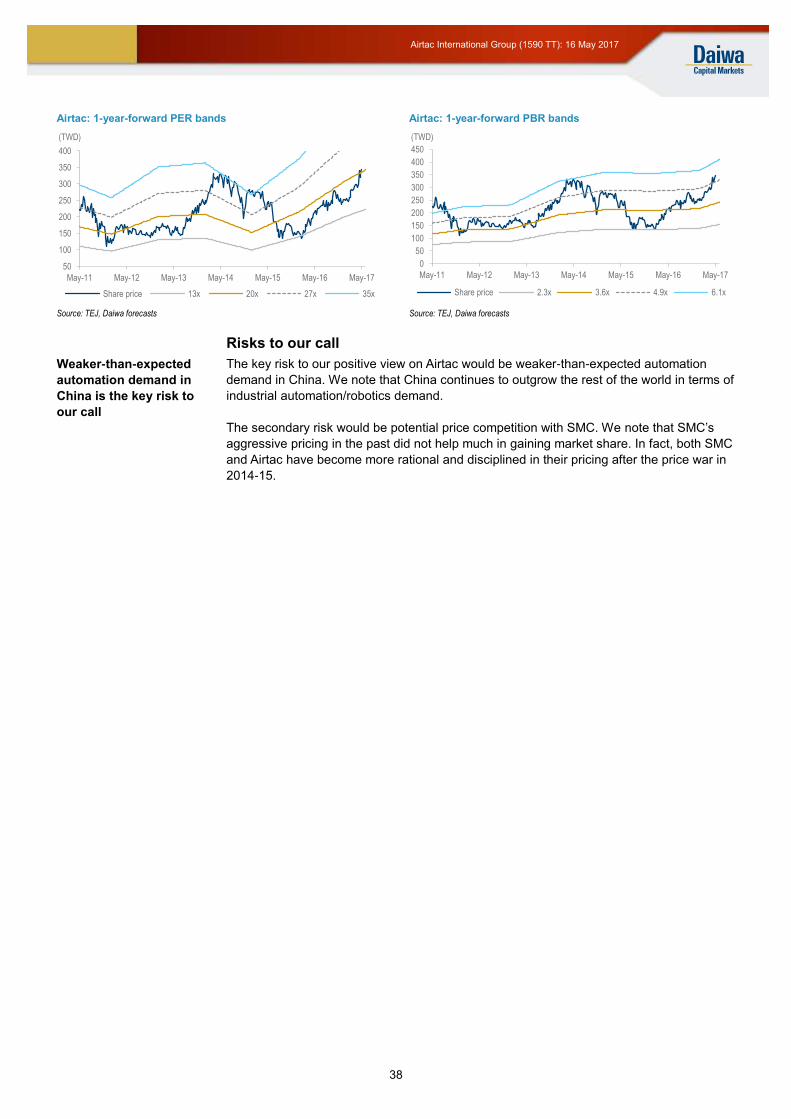

Page 1

See important disclosures, including any required research certifications, beginning on page 65

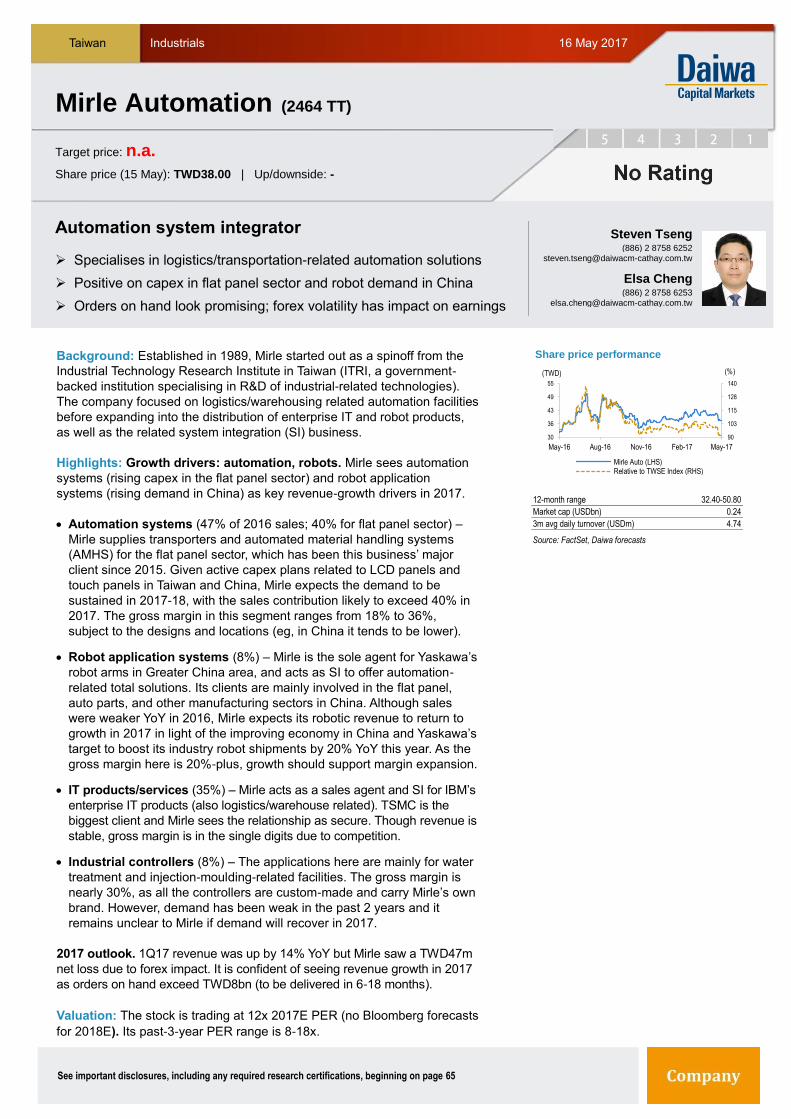

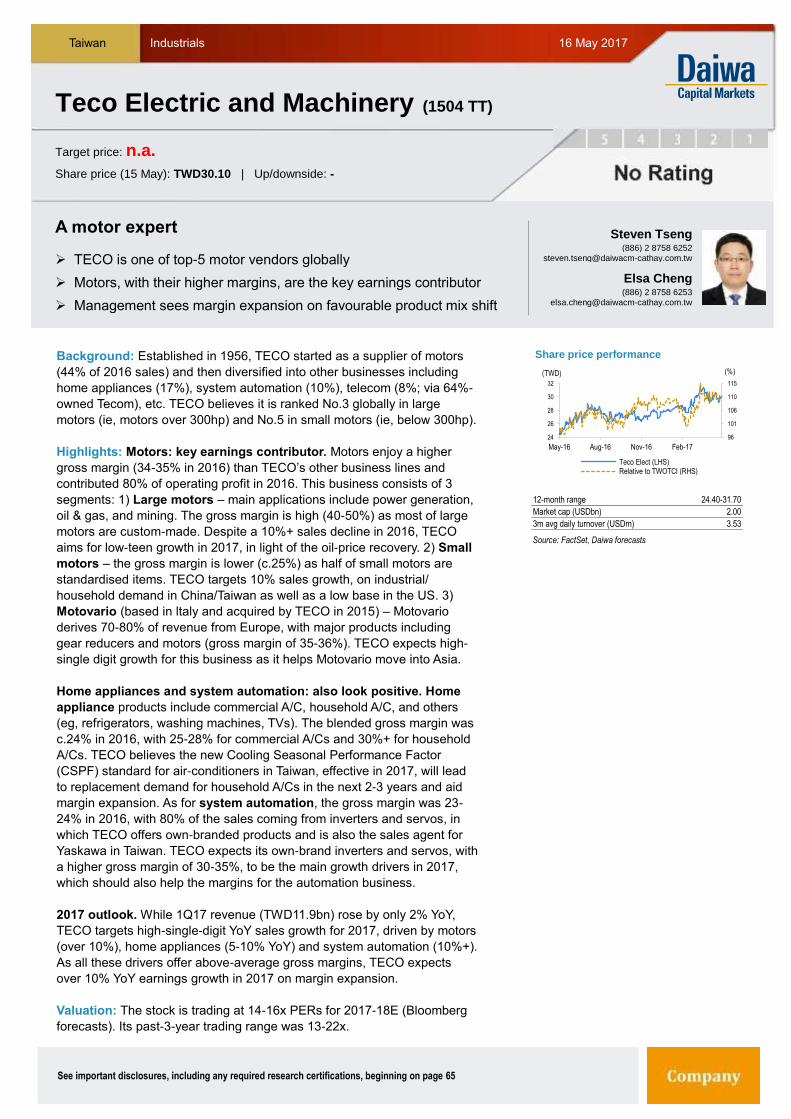

Taiwan Industrials

16 May 2017

Taiwan Industrial Robotics

Initiation: You’re hired!

Demand outlook for industrial robots positive, on rising penetration and more diverse applications in different sectors

Industrial robot supply chain in Taiwan looks to have strong upside thanks to automation demand in China and the local electronics sector

We favour Airtac and Delta for their market positions and earnings upside; cautious on Hiwin due to the drag from its subsidiary loss

Steven Tseng(886) 2 8758 6252

[email protected]

Elsa Cheng(886) 2 8758 6253

[email protected]

Page 2

See important disclosures, including any required research certifications, beginning on page 65

Taiwan Industrials

Investment case: We initiate coverage of Taiwan’s Industrial Robotics

Sector with a Positive rating. In our view, investors stand to benefit from

promising upside for the sector, given ample opportunities arising from

automation/robotics demand in China and the Taiwan electronics industry.

Catalysts: China: the key growth engine. China has been the largest

market for industrial robots since 2013, and is set for a 2015-19E CAGR of

23% in terms of units, according to the International Federation of Robotics

(IFR). With robot density still below the global average in China, the country

offers strong opportunities for robot demand growth.

Electronics sector: catching up fast. The electronics sector makes up c.

20% of the global robot installation base, trailing the automotive sector’s

38%. However, we expect the electronics sector to catch up and outpace

other major sectors in robot adoption, driven by the shortening product life

cycles of electronic products and rising labour costs in China.

Proliferation of robot applications. With robots becoming more powerful

and increasingly affordable, the types of robot use looks set to continue to

expand, ie, collaborative robots (cobots) (which can interact and work with

humans and are cheaper/easier to set up than industrial robots),

professional service robots, and personal/household robots for consumers.

Market indicators also look favourable. Improving PMIs in all major

regions globally, particularly in China, from mid-2016 point to positive

sentiment for industrial robot demand. Rising machine-tool production

value in Japan, China and Taiwan also supports this trend.

Valuation: We expect the favourable trends highlighted above to support

sustained earnings growth for the industrial automation/robot sector in

Taiwan. We initiate on Airtac (1590 TT, TWD431) with a Buy (1) call, as we

expect its market-share gains in China to continue, while favourable

operating leverage and effective opex control ensure operating-margin

expansion. We also like Delta (2308 TT, TWD194) and reiterate our Buy (1)

call, as we remain positive on its growth outlook in industrial automation,

passive components, and advanced power solution-related areas. And we

initiate coverage on Hiwin (2049 TT, TWD205) with a Hold (3) rating. We

like Hiwin’s competitiveness in linear motion components, but expect its

investment in solar energy to be an increasing drag on its earnings.

Risks: 1) Potential price competition in some areas of the robot supply

chain, and 2) worse-than-expected opex for robot related players, due to

higher R&D and client-service related inputs.

16 May 2017

Taiwan Industrial Robotics

Initiation: You’re hired!

Demand outlook for industrial robots positive, on rising penetration and more diverse applications in different sectors

Industrial robot supply chain in Taiwan looks to have strong upside thanks to automation demand in China and the local electronics sector

We favour Airtac and Delta for their market positions and earnings upside; cautious on Hiwin due to the drag from its subsidiary loss

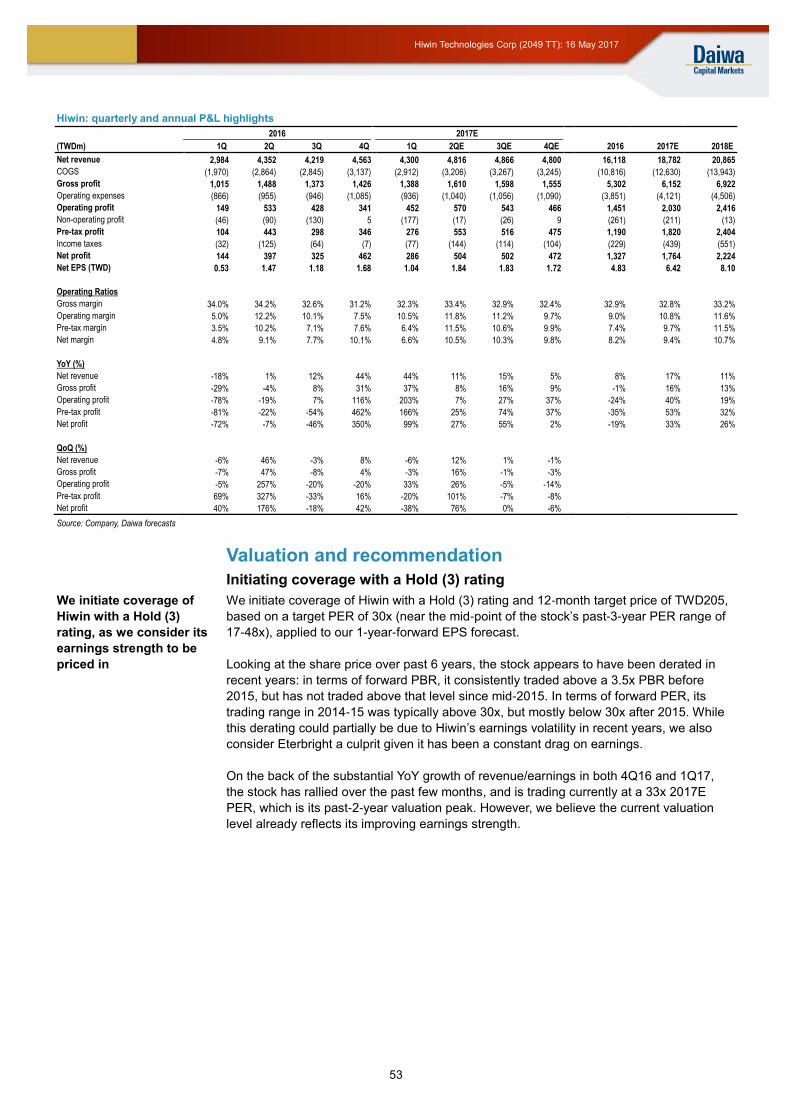

Key stock calls

Source: Daiwa forecasts

Steven Tseng(886) 2 8758 6252

[email protected]

Elsa Cheng(886) 2 8758 6253

[email protected]

New Prev.

Airtac International Group (1590 TT)Rating Buy

Target 431.00

Upside p 25.8%

Delta Electronics (2308 TT)Rating Buy Buy

Target 194.00 194.00

Upside p 14.8%

Hiwin Technologies Corp (2049 TT)Rating Hold

Target 205.00

Downside q 1.9%

Page 3

3

Taiwan Industrial Robotics: 16 May 2017

How do we justify our view?

Growth outlook Valuation Earnings revisions

Growth outlook Annual shipments of industrial robots worldwide

According to the IFR, global industrial robot shipments are

expected to increase from 254k in 2015 to 414k in 2019, a

CAGR of 13.0% over the period. Another research firm,

ABI Research, expects the global industrial robot market to

exceed USD30bn in 2020, suggesting that the size of the

global market could almost triple in 5 years, with a CAGR

of over 20%. All these forecasts indicate a very promising

growth outlook for the global industrial robot market, in our

view.

Source: IFR

Valuation Taiwan Automation/Robot Sector: PER bands

Taiwan’s automation/robot sector has seen a gradual

rerating, from trading in a PER range of 13-24x before

2014 towards 18-30x in recent years. With the steady

market-share expansion of several robot-related

components suppliers, coupled with the launches of

industrial robots by several Taiwanese companies in recent

years, we see further upside potential for sector earnings

and valuations.

Source: Bloomberg

Earnings revisions Taiwan Automation Sector: Bloomberg consensus 2017-18E earnings revisions

According to Bloomberg data, notwithstanding the

consensus’s occasional upward and downward revisions to

the earnings forecasts for Taiwan’s automation/robot

sector, it is noteworthy that the gap between 2017 and

2018 earnings forecasts is getting wider. This situation

indicates to us that the market is turning more positive on

the earnings growth outlook for this sector in the long run.

Source: Bloomberg

(60%)

(30%)

0%

30%

60%

90%

120%

50

150

250

350

450

2005 2007 2009 2011 2013 2015 2017E 2019E

Annual shipments (LHS) YoY (RHS)

('000 of units)

0

10

20

30

40

50

Jan-09 Jan-10 Jan-11 Jan-12 Jan-13 Jan-14 Jan-15 Jan-16 Jan-17

(USDbn)

Market Cap 13x 18x

22x 25x 30x

90

95

100

105

110

115

120

125

130

135

Apr

-15

Jun-

15

Aug

-15

Oct

-15

Dec

-15

Feb

-16

Apr

-16

Jun-

16

Aug

-16

Oct

-16

Dec

-16

Feb

-17

Apr

-17

2017 Index 2018E Index

Page 4

4

Taiwan Industrial Robotics: 16 May 2017

Sector stocks: key indicators

Source: Bloomberg, Daiwa forecasts

Worldwide operational stock of industrial robots Annual shipments of industrial robots by region

Source: IFR Source: IFR

Annual shipments of industrial robots in China PMI of major regions worldwide

Source: IFR Source: Markit, ISM, China official

Worldwide operational stock of industrial robots by main industries

Source: IFR Note: percentages in the chart refer to the YoY growth in 2015

Share

Company Name Stock code Price New Prev. New Prev. % chg New Prev. % chg New Prev. % chg

Airtac International Group 1590 TT 342.50 Buy 431.00 15.351 19.210

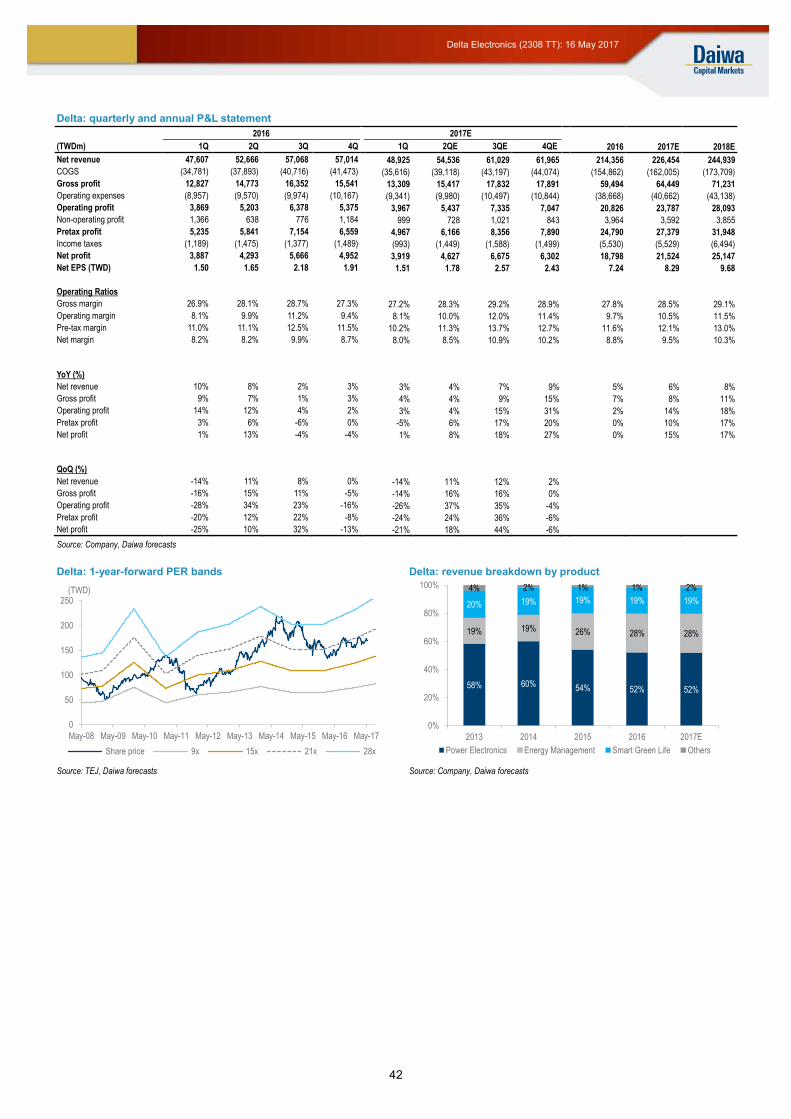

Delta Electronics 2308 TT 169.00 Buy Buy 194.00 194.00 0.0% 8.286 8.286 0.0% 9.681 9.681 0.0%

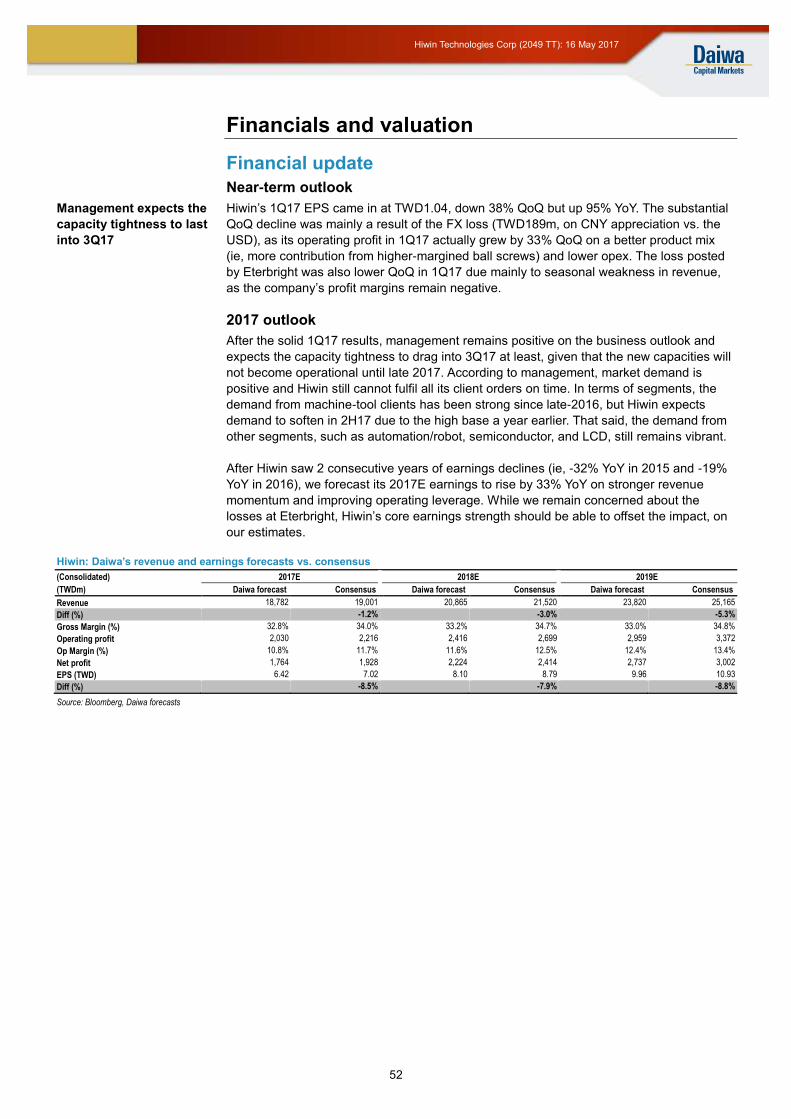

Hiwin Technologies Corp 2049 TT 209.00 Hold 205.00 6.421 8.097

Rating Target price (local curr.) FY1

EPS (local curr.)

FY2

0

500

1,000

1,500

2,000

2,500

3,000

1973

1983

1990

1995

2000

2005

2010

2014

2015

2016

E

2019

E

('000 of units)

0

50

100

150

200

250

300

350

2014 2015 2016E 2017E 2018E 2019E

Asia/Australia Europe America

('000 of units)

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

0

30

60

90

120

150

180

2010 2011 2012 2013 2014 2015 2016E 2017E 2018E 2019E

Annual shipments (LHS) China % to the world (RHS)

('000 of units)

30

35

40

45

50

55

60

65

Jan-

07

Jul-0

7

Jan-

08

Jul-0

8

Jan-

09

Jul-0

9

Jan-

10

Jul-1

0

Jan-

11

Jul-1

1

Jan-

12

Jul-1

2

Jan-

13

Jul-1

3

Jan-

14

Jul-1

4

Jan-

15

Jul-1

5

Jan-

16

Jul-1

6

Jan-

17

US China Eurozone

(Index)

0 100 200 300 400 500 600 700

Not specifled by industries

Others

Food

Chemical and plastics

Metal

Electrical/ electronics

Automotive

2015 2014 2013

('000 of units)+10%

+18%

+16%

+11%

+13%

Page 5

5

Taiwan Industrial Robotics: 16 May 2017

Table of contents

Overview of the global industrial robot sector ...................................................... 6

Robots – a compelling driver of automation .......................................................................6

Key trend 1: China a key engine for global demand ...........................................................8

Key trend 2: Electronics sector should offer the best potential ......................................... 10

Key trend 3: Proliferation of robot applications ................................................................. 12

Key trend 4: Industry indicators show favourable trends .................................................. 14

Industrial robot supply chain in Taiwan ................................................................16

Not a big sector, but likely a hidden gem ......................................................................... 16

Overview of the industrial robot supply chain in Taiwan ................................................... 16

Taiwan’s strength and opportunities ................................................................................. 17

Valuation and recommendations ...........................................................................20

Solid sector outlook suggests more valuation upside ....................................................... 20

Stock recommendations .................................................................................................. 21

Appendix ..................................................................................................................23

Major components of industrial robots ............................................................................. 23

Major types of industrial robots ........................................................................................ 26

Company Section

Airtac International Group ................................................................................................ 28

Delta Electronics .............................................................................................................. 39

Hiwin Technologies Corp ................................................................................................. 43

Chieftek Precision ............................................................................................................ 55

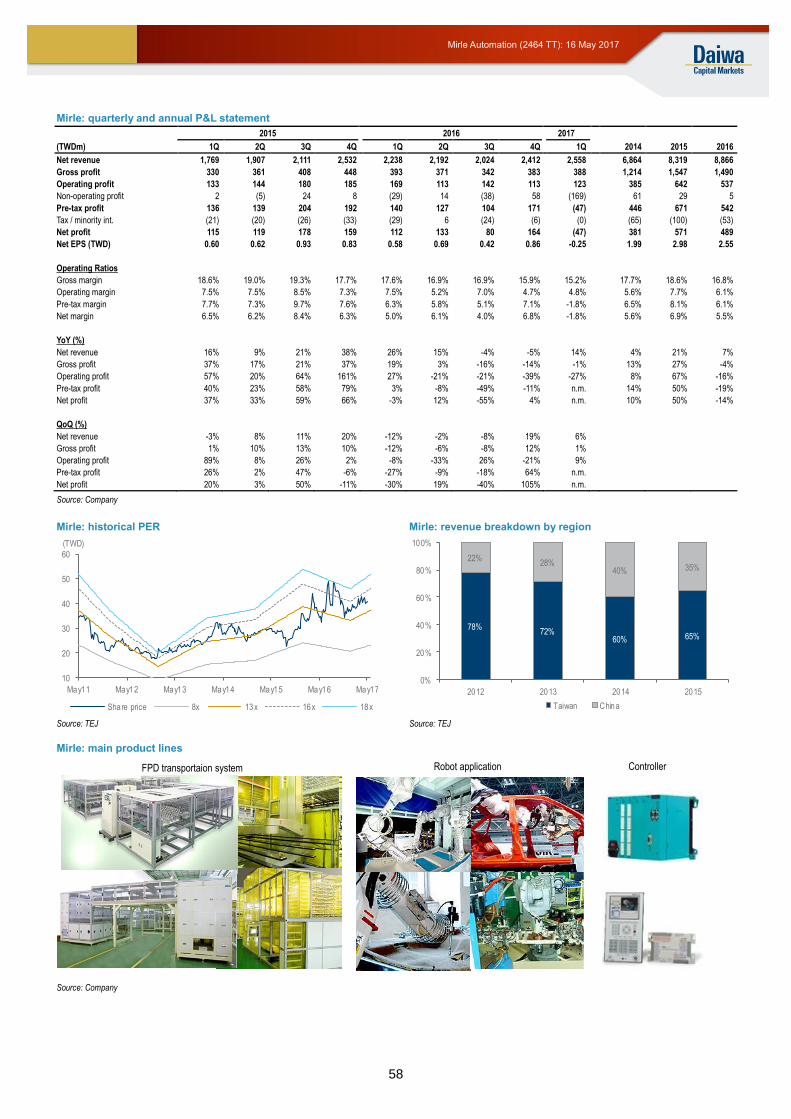

Mirle Automation .............................................................................................................. 57

Quanta Storage ............................................................................................................... 59

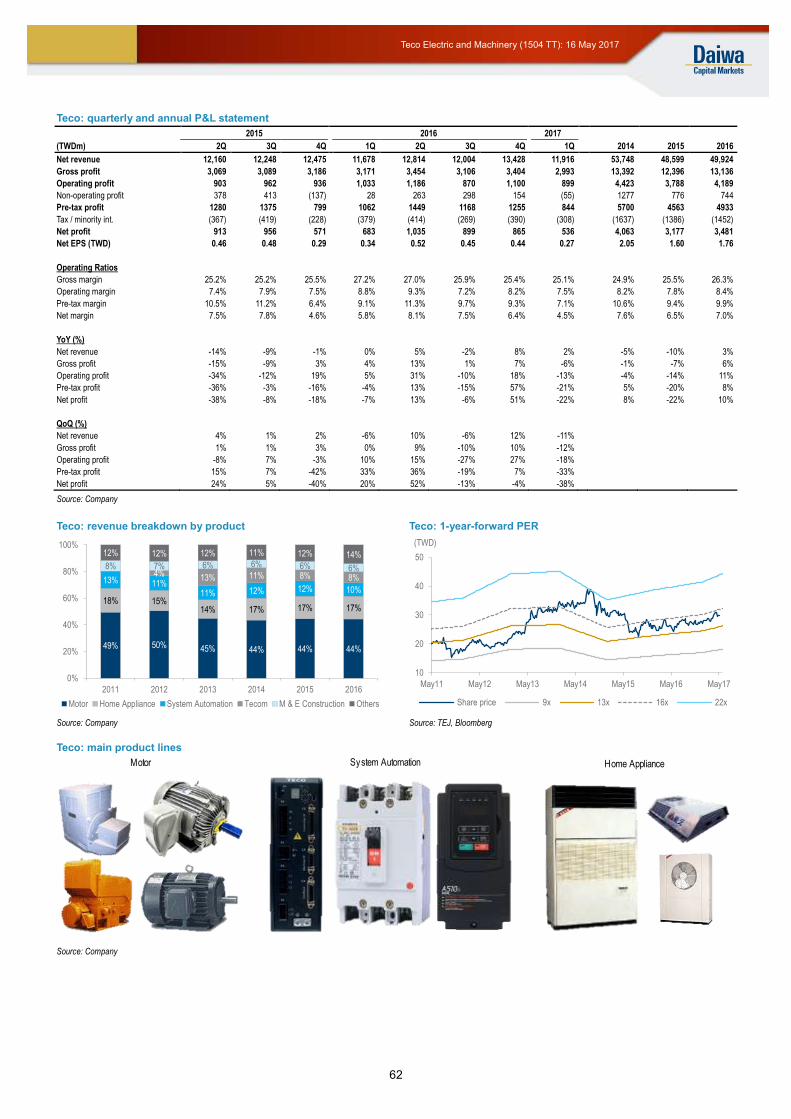

Teco Electric and Machinery ............................................................................................ 61

Page 6

6

Taiwan Industrial Robotics: 16 May 2017

Overview of the global industrial robot sector

Robots – a compelling driver of automation

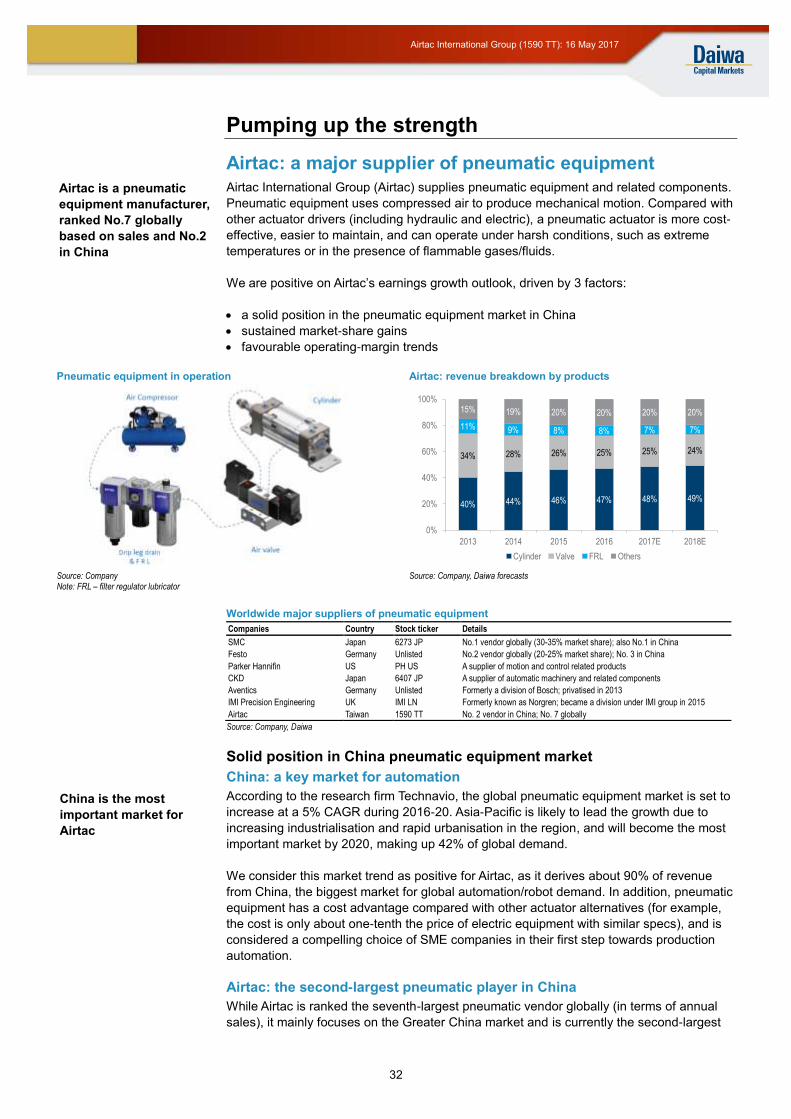

Industrial robots and automation Industrial automation has been an ongoing trend in the manufacturing industry worldwide

for the past decade. The advance of industrial technologies, the aging of the Baby Boomer

population, and rising labour costs in major manufacturing countries (China in particular)

have all helped drive demand for industrial automation worldwide.

Amid the promising trend of automation, rising adoption of industrial robots is becoming a

compelling driver. Also, as industrial automation has become “smarter”, along with the

growing applications for Industrial IoT and Big Data, industrial robots have become more

intelligent and as such we see vast potential unfolding for various industries.

Industrial robots

Source: Company data

According to the IFR, an industrial robot is defined as “an automatically controlled,

reprogrammable, multipurpose manipulator programmable in three or more axes, which

can be either fixed in place or mobile for use in industrial automation applications.” In this

definition, key words like “reprogrammable”, “multipurpose”, “three or more axes” suggest

that industrial robots can be highly flexible, versatile, and adaptive tools to meet diverse

needs in industrial processes.

There are some obvious advantages to using industrial robots. They can handle tasks in

hazardous environments, and those which are physically challenging or monotonous for

humans, and are often seen as being more efficient and producing more consistent quality

than humans.

The use of industrial robots also has disadvantages. They usually involve high initial setup

costs, while a lack of proper maintenance can cause serious interruptions to the industrial

processes. Also, currently not all tasks can be performed by robots, or are economically

viable to use robots, although this could change over time.

Industrial robots, with

their flexibility and

versatility, are a key

driver of automation

Page 7

7

Taiwan Industrial Robotics: 16 May 2017

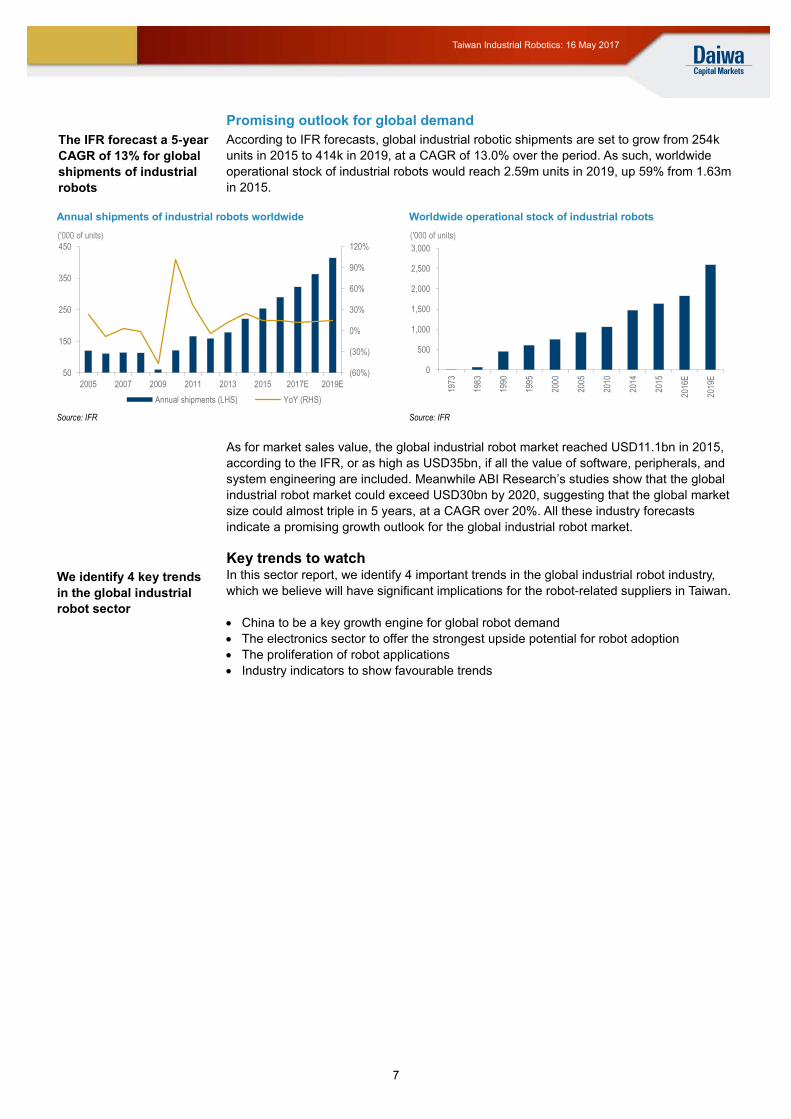

Promising outlook for global demand

According to IFR forecasts, global industrial robotic shipments are set to grow from 254k

units in 2015 to 414k in 2019, at a CAGR of 13.0% over the period. As such, worldwide

operational stock of industrial robots would reach 2.59m units in 2019, up 59% from 1.63m

in 2015.

Annual shipments of industrial robots worldwide Worldwide operational stock of industrial robots

Source: IFR Source: IFR

As for market sales value, the global industrial robot market reached USD11.1bn in 2015,

according to the IFR, or as high as USD35bn, if all the value of software, peripherals, and

system engineering are included. Meanwhile ABI Research’s studies show that the global

industrial robot market could exceed USD30bn by 2020, suggesting that the global market

size could almost triple in 5 years, at a CAGR over 20%. All these industry forecasts

indicate a promising growth outlook for the global industrial robot market.

Key trends to watch In this sector report, we identify 4 important trends in the global industrial robot industry,

which we believe will have significant implications for the robot-related suppliers in Taiwan.

China to be a key growth engine for global robot demand

The electronics sector to offer the strongest upside potential for robot adoption

The proliferation of robot applications

Industry indicators to show favourable trends

(60%)

(30%)

0%

30%

60%

90%

120%

50

150

250

350

450

2005 2007 2009 2011 2013 2015 2017E 2019E

Annual shipments (LHS) YoY (RHS)

('000 of units)

0

500

1,000

1,500

2,000

2,500

3,000

1973

1983

1990

1995

2000

2005

2010

2014

2015

2016

E

2019

E

('000 of units)

The IFR forecast a 5-year

CAGR of 13% for global

shipments of industrial

robots

We identify 4 key trends

in the global industrial

robot sector

Page 8

8

Taiwan Industrial Robotics: 16 May 2017

Key trend 1: China a key engine for global demand

Asia strength backed by China, Korea, and Japan According to IFR statistics, Asia is the world’s strongest growth market in terms of industrial

robot shipments. This region’s new robot shipments increased by 19% YoY in 2015,

followed by the Americas’ 17% and Europe’s 10%. In terms of individual countries, 5

countries represented 75% of total industrial robots sold globally in 2015 – China (27%),

South Korea (15%), Japan (14%), the US (11%), and Germany (8%) – while 3 Asian

countries make the top-5 list and together account for over half of global robot shipments.

China: the biggest market for industrial robots

China is a key reason behind the strength of Asia’s robotic demand. The country has been

the biggest market for industrial robots since 2013, with new robot shipments up 20% YoY

in 2015. In fact, IFR expects China to claim 40% of global robot demand by 2019, up from

27% in 2015, suggesting a CAGR of 23% in terms of units. South Korea and Japan are

also important drivers in Asia, with 2015 shipment growth reaching 55% YoY and 20% YoY,

respectively. Other Asian countries, like Taiwan (3% of global robot shipments in 2015) and

Thailand (1%), also provide meaningful contributions to global industrial robot demand.

Annual shipments of industrial robots by region Annual shipments of industrial robots in China

Source: IFR Source: IFR

Annual shipments of industrial robots by region/country

(Unit) 2014 2015 2016E 2019E

America 32,616 38,134 40,200 50,700 North America 31,029 36,444 38,000 46,000 Brazil 1,266 1,407 1,800 3,500 Rest of South America 321 283 400 1,200

Asia 134,444 160,558 190,200 285,700 China 57,096 68,556 90,000 160,000 Japan 29,297 35,023 38,000 43,000 South Korea 24,721 38,285 40,000 46,000 Taiwan 6,912 7,200 9,000 13,000 Thailand 3,657 2,556 3,000 4,500 India 2,126 2,065 2,600 6,000 Others 10,635 6,873 7,600 13,200

Europe 45,559 50,073 54,200 68,800 Germany 20,051 20,105 21,000 25,000 Italy 6,215 6,657 7,200 9,000 France 2,944 3,045 3,300 4,500 Spain 2,312 3,766 4,100 5,100 UK 2,094 1,645 1,800 2,500 Central/Eastern Europe 4,643 5,976 7,550 11,300 Others 7,300 8,879 9,250 11,400

Africa 428 348 400 800 Not specified by countries 7,524 4,635 5,000 8,000 Worldwide total 220,571 253,748 290,000 414,000

Source: IFR

0

50

100

150

200

250

300

350

2014 2015 2016E 2017E 2018E 2019E

Asia/Australia Europe America

('000 of units)

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

0

30

60

90

120

150

180

2010 2011 2012 2013 2014 2015 2016E 2017E 2018E 2019E

Annual shipments (LHS) China % to the world (RHS)

('000 of units)

Asia tops the world in

robot shipment growth

China set to claim 40%

of global robot demand

by 2019E (vs. 27% in

2015), according to IFR

Page 9

9

Taiwan Industrial Robotics: 16 May 2017

Robot density: a key parameter to watch

Simply comparing robot shipments in each region/country can be misleading, in our view,

as it fails to take into account the difference in size of the manufacturing segment in

different areas. As such, the IFR has come up with the concept of robot density, which is

defined as the number of industrial robots per 10,000 persons employed in the

manufacturing industry in a country/region.

According to the IFR, average robot density worldwide was 69 in 2015. Among all the

major regions, Europe had the highest average robot density at 92, followed by 86 in the

Americas and 57 in Asia. As mentioned earlier, Asia accounts for the highest growth than

other regions in terms of robot demand. Its lower robot density than other regions suggests

to us that such growth strength will continue in the next few years.

Robot density in major countries

Source: IFR (data as of 2015)

When we look at robot density by country, the most “automated” countries (ie, those with

high robot density) appear to be Korea, Singapore, Japan, and Germany, as shown in the

chart below. Robot density in China, the biggest market for industrial robots since 2013,

was only 49 in 2015.

As part of the targets set out in the China Government’s “Made in China 2025” strategy,

China aims to boost its robot density to 300 by 2025. If we assume no change in the

number of employees in China’s manufacturing sectors, the target robot density of 300

suggests a CAGR of nearly 20% for the number of industrial robots installed in China up to

2025. This figure reflects promising growth potential for China’s industrial robot market.

531

398

305 301

212 190 188 176 169 160 150 136 128 127 126 120 119 110 93 86 79 71 49

0

100

200

300

400

500

600

Kor

ea

Sin

gapo

re

Japa

n

Ger

man

y

Sw

eden

Tai

wan

Den

mar

k

US

Bel

gium Ita

ly

Spa

in

Can

ada

Aus

tria

Fra

nce

Fin

land

Net

herla

nds

Sw

itzed

land

Slo

veni

a

Cze

ch R

ep.

Aus

tral

ia

Slo

vaki

a

UK

Chi

na

(units per 10,000 employees)

Average robot density worldwide: 69

Asia’s lower robot

density suggests a

sustained strength of

robot demand

China’s robot density is

still much lower than the

global average level

Page 10

10

Taiwan Industrial Robotics: 16 May 2017

Key trend 2: Electronics sector should offer the best potential

Auto sector the biggest user, but electronics sector catching up fast While we expect rising interest in robot adoption from pretty much all manufacturing

sectors, for the time being about 70% of industrial robots installed worldwide are

concentrated on 3 major industries – automotive (38.2% as of 2015, according to IFR),

electrical/electronics (20.1%), and metal (9.9%). The automotive industry was an early

adopter and is the biggest user of industrial robots, but the electronics sector is catching up

fast. IFR data indicated that the electronic sector showed the strongest growth in 2015

among all the major sectors. In fact, the IFR expects the electronics sector will continue to

outperform other sectors in the unit growth of operational robots and new robots installed.

In terms of installed base, the total number of operational industrial robots worldwide

rose by 11% YoY for 2015. Among all the major sectors, the electronics sector posted

the highest growth of 18% YoY, followed by the metal/machinery sector’s 16%, the food

sector’s 13%, and the automotive sector’s 10%.

In terms of new robots sold worldwide, the total number of industrial robots rose by 15%

YoY for 2015. The electronics sector also showed the strongest growth of 41% YoY,

followed by the metal/machinery sector’s 39% and the chemical/plastic sector’s 16%

YoY. The automotive sector only post single-digit growth.

Worldwide operational stock of industrial robots by main industries

Source: IFR Note: percentages in the chart refer to the YoY growth in 2015

Drivers of robot demand in the electronics sector

Shortening product life cycle

We consider the fast-rising volume and shortening product life cycles of most consumer

electronic products, particularly mobile devices like smartphones, to be key drivers of

robotic adoption in the electronics sector, as robotic automation can shorten the retooling

process to cope with different products/models and help enhance manufacturing efficiency

and product quality. Furthermore, with the applications of Big Data, robotic production lines

can become highly flexible in terms of reacting to end-market demand, which helps reduce

the risk of a product shortage or inventory pile-up.

Among the electronics supply chain, we expect stronger growth of robot adoption from

downstream players, such as EMS and ODM companies, which traditionally have lower

levels of production automation than those of upstream players, such as semiconductor

and flat panel related producers.

0 100 200 300 400 500 600 700

Not specifled by industries

Others

Food

Chemical and plastics

Metal

Electrical/ electronics

Automotive

2015 2014 2013

('000 of units)+10%

+18%

+16%

+11%

+13%

The automotive sector is

currently the biggest

robot user, but the

electronics sector

should show much

stronger growth in robot

demand

We deem the shortening

product life cycle and

rising labour costs to be

the main factors

underpinning robot

demand in the

electronics sector

Page 11

11

Taiwan Industrial Robotics: 16 May 2017

Cost consideration due to rising labour costs

Another main driver of robotic demand evolves around cost reduction. Ever-rising labour

costs in China in recent years (typically up 10-15% pa over the past decade; sometimes

higher) have forced most companies to look for alternatives for cost-savings, one of which

is automation. As a general rule of thumb, in developed countries, the cost of a robot is

roughly equivalent to one worker’s salary over 2 years, so rising labour costs imply a

shorter payback period for robot-related investments, hence attract more incentive for

robot adoption.

Hon Hai/Foxconn group, the largest EMS in the world, announced its ambition for factory

automation back in 2011. According to press reports, so far it has installed over 40,000

units of robots in China, and the ultimate goal is to set up “unmanned factories” at its major

manufacturing sites in Chengzhou, Kunshan and Shenzhen. We expect most of Hon Hai’s

EMS/ODM peers to follow suit, which implies promising demand for automation/robots

going forward.

Page 12

12

Taiwan Industrial Robotics: 16 May 2017

Key trend 3: Proliferation of robot applications

Improving cost/performance leads to widening robot applications According a study by The Boston Consulting Group (BCG) in 2015, prices of robotic

hardware and enabling software are expected to drop by more than 20% over the next

decade; meanwhile, the performance of robotic systems will improve by 5% each year.

This means that robots will become increasingly powerful but also more affordable at the

same time. Such a trend will attract a widening range of new applications for robots.

Rising traction of collaborative robots

Cobots have been gaining traction in the past 3-4 years. The traditional concept of

automation typically involves big and fixed robotic equipment which can churn out large

volume output but are costly to set up and complicated to adjust or redeploy. Cobots are

designed to work around human workers (hence the term “collaborative”) and are easy to

adjust and re-programme for different tasks.

More importantly, cobots are much more affordable than traditional industrial robots,

according to Universal Robots (one of the early developers of cobots), as the all-in cost of

a cobot can be near a quarter of that of an industrial robot used for similar purposes. This

lower cost is mainly because cobots are highly integrated robots, which do not usually

need the involvement of system integrators. As such, cobots could become an attractive

option for automation for a broad range of potential customers, particularly when the tasks

involved are highly flexible and need reprograming on a regular basis.

According to ABI Research, the global cobot market is set to expand from USD95m in

2015 to USD1.0bn in 2020E, a 60% CAGR. Other market forecasts from Research and

Markets even call for the global cobot market to reach USD3.8bn by 2021E. Regardless of

the vast difference in terms of market value forecasts, they all expect exponential growth in

market revenue in this very promising sub-segment of industrial robots.

Example of a cobot Global cobot market forecasts

Source: Universal Robots Source: ABI Research

Non-manufacturing applications also very promising

It is not so uncommon nowadays to find robots in a variety of applications beyond the

factory floor, such as service robots, medical robots, household robots, etc. IFR provides

some pretty upbeat forecasts on different types of robots:

Professional service robots: These robots refer to industrial-grade robots for non-

manufacturing purposes, such as medical, logistics, defence, etc. Worldwide shipments

of such professional service robots, according to IFR, will rise to 333.2k units in 2019E

from only 41k in 2015, with sales value reaching USD23.1bn, from USD4.6bn in 2015.

Personal/household robots: These robots are mainly for consumer and household

related applications, such as vacuum cleaning, education, entertainment, elderly/

handicap companions, etc. IFR expects the worldwide shipments of personal and

household robots to rise to 30.8m units by 2019E (from 3.7m in 2015), with sales value

reaching USD22.3bn (vs. USD2.2bn in 2015).

0

200

400

600

800

1,000

1,200

2015 2016E 2017E 2018E 2019E 2020E

2015-20E CAGR: 60%

(USDm)

The global cobots

market is projected to

grow at a CAGR of 60%

Page 13

13

Taiwan Industrial Robotics: 16 May 2017

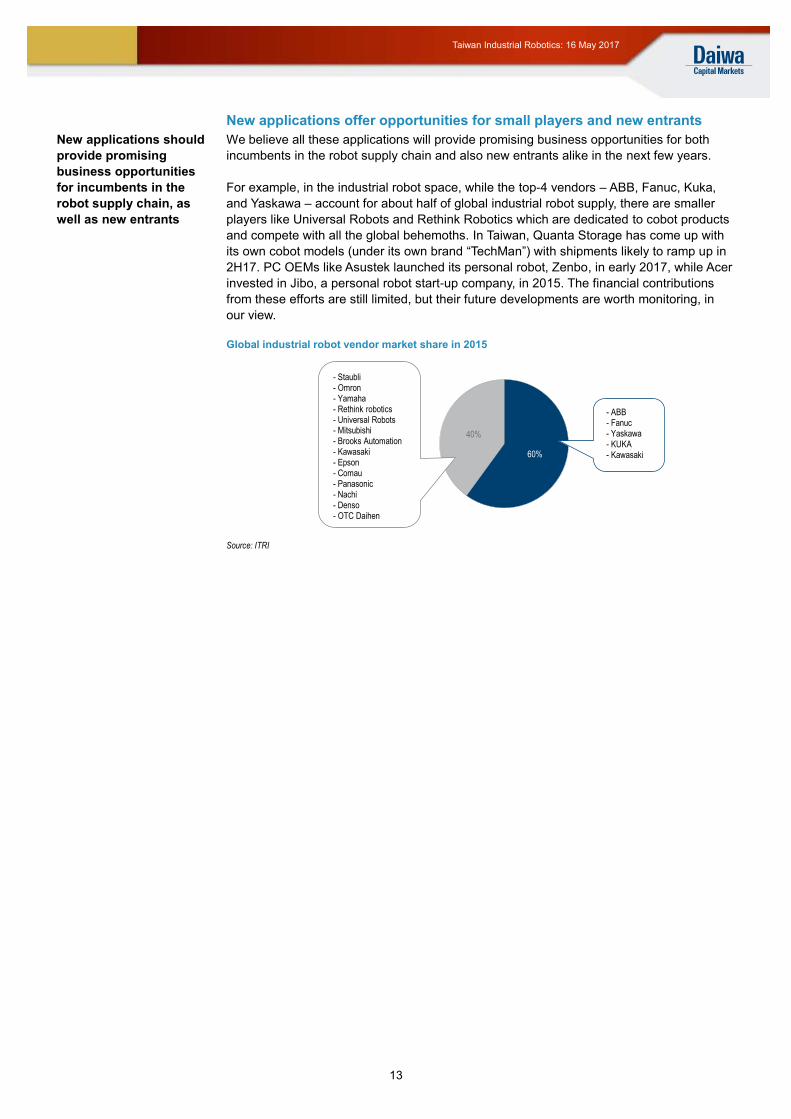

New applications offer opportunities for small players and new entrants

We believe all these applications will provide promising business opportunities for both

incumbents in the robot supply chain and also new entrants alike in the next few years.

For example, in the industrial robot space, while the top-4 vendors – ABB, Fanuc, Kuka,

and Yaskawa – account for about half of global industrial robot supply, there are smaller

players like Universal Robots and Rethink Robotics which are dedicated to cobot products

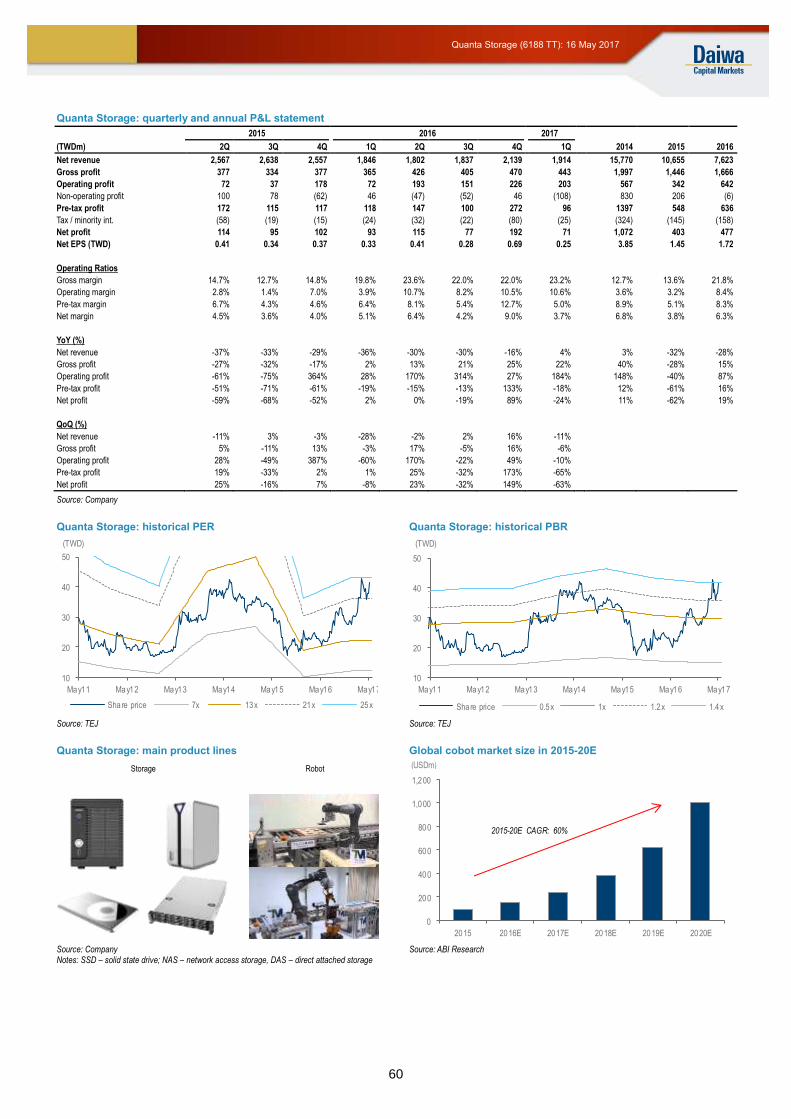

and compete with all the global behemoths. In Taiwan, Quanta Storage has come up with

its own cobot models (under its own brand “TechMan”) with shipments likely to ramp up in

2H17. PC OEMs like Asustek launched its personal robot, Zenbo, in early 2017, while Acer

invested in Jibo, a personal robot start-up company, in 2015. The financial contributions

from these efforts are still limited, but their future developments are worth monitoring, in

our view.

Global industrial robot vendor market share in 2015

Source: ITRI

60%

40%

- ABB- Fanuc- Yaskawa- KUKA- Kawasaki

- Staubli- Omron- Yamaha- Rethink robotics- Universal Robots- Mitsubishi- Brooks Automation- Kawasaki- Epson- Comau- Panasonic- Nachi- Denso- OTC Daihen

New applications should

provide promising

business opportunities

for incumbents in the

robot supply chain, as

well as new entrants

Page 14

14

Taiwan Industrial Robotics: 16 May 2017

Key trend 4: Industry indicators show favourable trends

The Purchasing Managers Index (PMI) has long been considered a leading indicator for

the economy and a sentiment barometer for overall manufacturing activities. The global

PMI bottomed out around mid-2016 after a steady decline since early 2014. In fact, the

PMI in all the major regions, including the US, Eurozone and China, all saw a similar

recovery during 2016, and has remained above the 50 level since September 2016. This

level suggests that manufacturing activities in all major regions should have been in

expansion mode since 4Q16, which we consider a positive indicator for automation and

robotic demand worldwide.

In addition, we observe regular cyclicality in the global PMI in the past decade, as historical

data shows that each upward or downward cycle of the global PMI tends to last for 1.5 to 2

years. As the most recent cycle trough was around 2Q16, we expect the favourable trend

to continue over the next 12 months or so.

PMI of major regions worldwide Cyclicality of the global PMI

Source: Markit, ISM, China official Source: Markit, Daiwa research

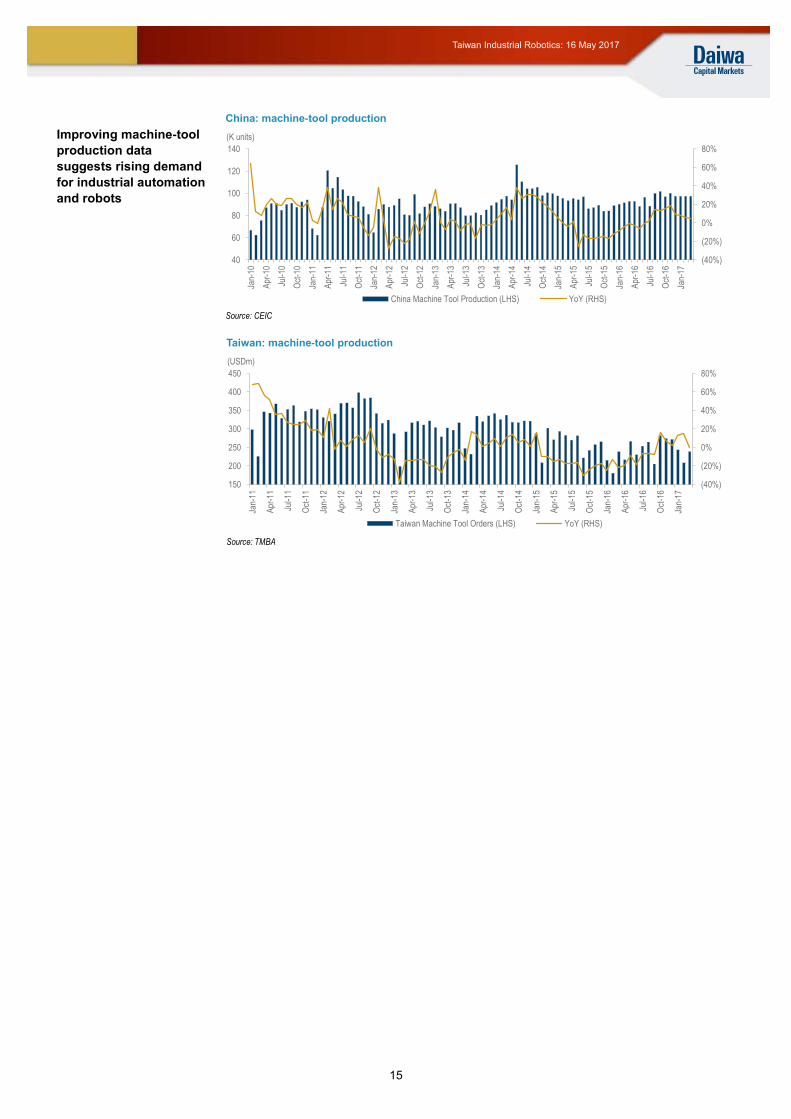

Machine-tool demand also trending up Another industry data point related to automation/robot demand is machine-tool

production, which is basically the industrial machines and related components for

manufacturing activities. While these are not all about industrial automation/robot demand,

they are obviously related. If we look at the monthly data from Japan, China and Taiwan,

both China and Taiwan’s monthly machine-tool production have reported positive YoY

growth since 3Q16. As for Japan, its growth just turned positive in 4Q16, but jumped

significantly in recent months. In short, we believe the improving machine-tool production

data also suggests growing demands for automation and industrial robots.

Japan: machine-tool production

Source: JMTBA

30

35

40

45

50

55

60

65

Jan-

07

Jul-0

7

Jan-

08

Jul-0

8

Jan-

09

Jul-0

9

Jan-

10

Jul-1

0

Jan-

11

Jul-1

1

Jan-

12

Jul-1

2

Jan-

13

Jul-1

3

Jan-

14

Jul-1

4

Jan-

15

Jul-1

5

Jan-

16

Jul-1

6

Jan-

17

US China Eurozone

(Index)

30

35

40

45

50

55

60

65

Jun-

08

Dec

-08

Jun-

09

Dec

-09

Jun-

10

Dec

-10

Jun-

11

Dec

-11

Jun-

12

Dec

-12

Jun-

13

Dec

-13

Jun-

14

Dec

-14

Jun-

15

Dec

-15

Jun-

16

Dec

-16

26 months

18 months

18 months

24 months

(Index)up cycle up cycle

down cycle down cycle

up cycle

? months

(40%)

(20%)

0%

20%

40%

60%

80%

100%

60

80

100

120

140

160

Jan-

11

Apr

-11

Jul-1

1

Oct

-11

Jan-

12

Apr

-12

Jul-1

2

Oct

-12

Jan-

13

Apr

-13

Jul-1

3

Oct

-13

Jan-

14

Apr

-14

Jul-1

4

Oct

-14

Jan-

15

Apr

-15

Jul-1

5

Oct

-15

Jan-

16

Apr

-16

Jul-1

6

Oct

-16

Jan-

17

Japan Machine Tool Orders (LHS) YoY (RHS)

(JPYbn)

PMI bottomed out

around mid-2016, a

positive indicator for

automation and robotic

demand worldwide

Page 15

15

Taiwan Industrial Robotics: 16 May 2017

China: machine-tool production

Improving machine-tool

production data

suggests rising demand

for industrial automation

and robots

Source: CEIC

Taiwan: machine-tool production

Source: TMBA

(40%)

(20%)

0%

20%

40%

60%

80%

40

60

80

100

120

140

Jan-

10

Apr

-10

Jul-1

0

Oct

-10

Jan-

11

Apr

-11

Jul-1

1

Oct

-11

Jan-

12

Apr

-12

Jul-1

2

Oct

-12

Jan-

13

Apr

-13

Jul-1

3

Oct

-13

Jan-

14

Apr

-14

Jul-1

4

Oct

-14

Jan-

15

Apr

-15

Jul-1

5

Oct

-15

Jan-

16

Apr

-16

Jul-1

6

Oct

-16

Jan-

17

China Machine Tool Production (LHS) YoY (RHS)

(K units)

(40%)

(20%)

0%

20%

40%

60%

80%

150

200

250

300

350

400

450

Jan-

11

Apr

-11

Jul-1

1

Oct

-11

Jan-

12

Apr

-12

Jul-1

2

Oct

-12

Jan-

13

Apr

-13

Jul-1

3

Oct

-13

Jan-

14

Apr

-14

Jul-1

4

Oct

-14

Jan-

15

Apr

-15

Jul-1

5

Oct

-15

Jan-

16

Apr

-16

Jul-1

6

Oct

-16

Jan-

17

Taiwan Machine Tool Orders (LHS) YoY (RHS)

(USDm)

Page 16

16

Taiwan Industrial Robotics: 16 May 2017

Industrial robot supply chain in Taiwan

Not a big sector, but likely a hidden gem

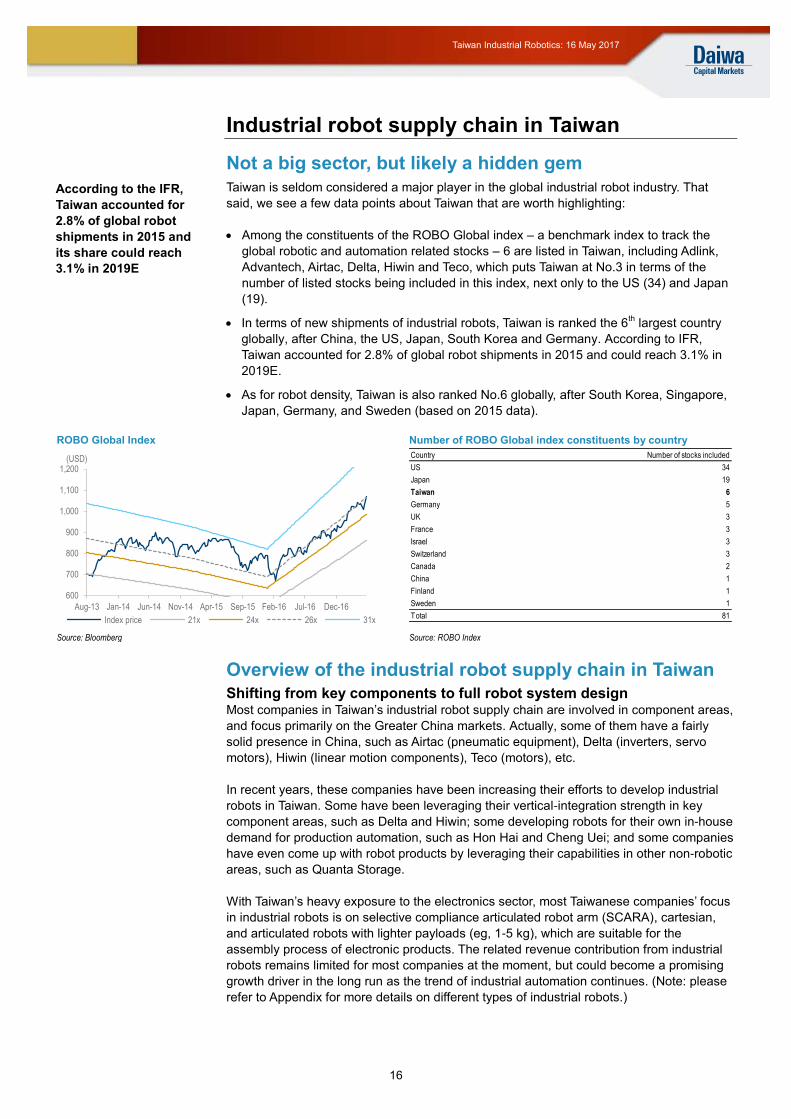

Taiwan is seldom considered a major player in the global industrial robot industry. That

said, we see a few data points about Taiwan that are worth highlighting:

Among the constituents of the ROBO Global index – a benchmark index to track the

global robotic and automation related stocks – 6 are listed in Taiwan, including Adlink,

Advantech, Airtac, Delta, Hiwin and Teco, which puts Taiwan at No.3 in terms of the

number of listed stocks being included in this index, next only to the US (34) and Japan

(19).

In terms of new shipments of industrial robots, Taiwan is ranked the 6th largest country

globally, after China, the US, Japan, South Korea and Germany. According to IFR,

Taiwan accounted for 2.8% of global robot shipments in 2015 and could reach 3.1% in

2019E.

As for robot density, Taiwan is also ranked No.6 globally, after South Korea, Singapore,

Japan, Germany, and Sweden (based on 2015 data).

ROBO Global Index Number of ROBO Global index constituents by country

Source: Bloomberg Source: ROBO Index

Overview of the industrial robot supply chain in Taiwan

Shifting from key components to full robot system design Most companies in Taiwan’s industrial robot supply chain are involved in component areas,

and focus primarily on the Greater China markets. Actually, some of them have a fairly

solid presence in China, such as Airtac (pneumatic equipment), Delta (inverters, servo

motors), Hiwin (linear motion components), Teco (motors), etc.

In recent years, these companies have been increasing their efforts to develop industrial

robots in Taiwan. Some have been leveraging their vertical-integration strength in key

component areas, such as Delta and Hiwin; some developing robots for their own in-house

demand for production automation, such as Hon Hai and Cheng Uei; and some companies

have even come up with robot products by leveraging their capabilities in other non-robotic

areas, such as Quanta Storage.

With Taiwan’s heavy exposure to the electronics sector, most Taiwanese companies’ focus

in industrial robots is on selective compliance articulated robot arm (SCARA), cartesian,

and articulated robots with lighter payloads (eg, 1-5 kg), which are suitable for the

assembly process of electronic products. The related revenue contribution from industrial

robots remains limited for most companies at the moment, but could become a promising

growth driver in the long run as the trend of industrial automation continues. (Note: please

refer to Appendix for more details on different types of industrial robots.)

600

700

800

900

1,000

1,100

1,200

Aug-13 Jan-14 Jun-14 Nov-14 Apr-15 Sep-15 Feb-16 Jul-16 Dec-16

Index price 21x 24x 26x 31x

(USD) Country Number of stocks included

US 34

Japan 19

Taiwan 6

Germany 5

UK 3

France 3

Israel 3

Switzerland 3

Canada 2

China 1

Finland 1

Sweden 1

Total 81

According to the IFR,

Taiwan accounted for

2.8% of global robot

shipments in 2015 and

its share could reach

3.1% in 2019E

Page 17

17

Taiwan Industrial Robotics: 16 May 2017

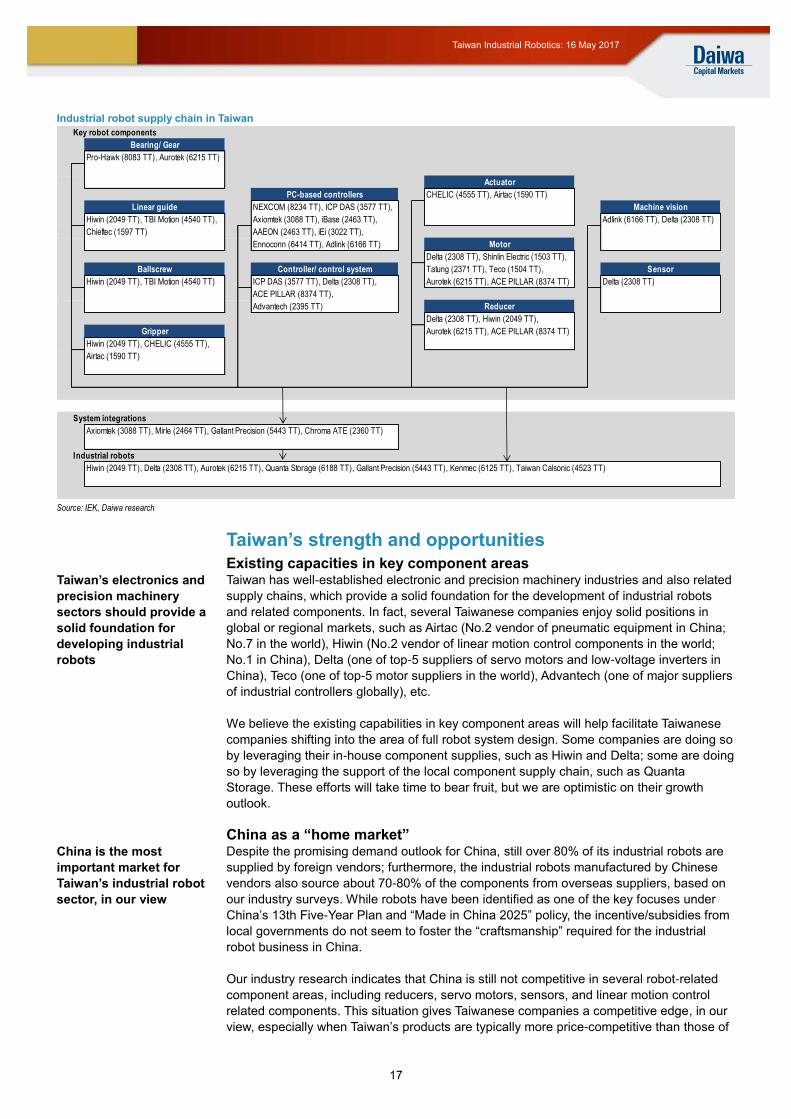

Industrial robot supply chain in Taiwan

Source: IEK, Daiwa research

Taiwan’s strength and opportunities

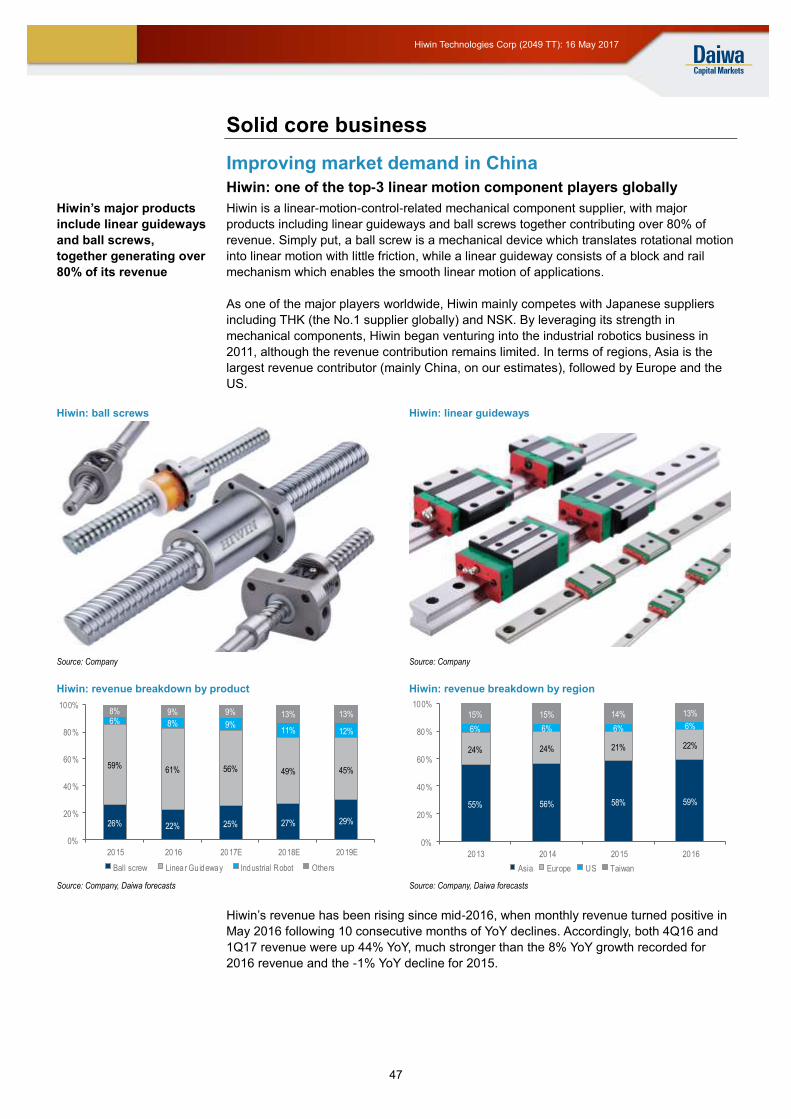

Existing capacities in key component areas Taiwan has well-established electronic and precision machinery industries and also related

supply chains, which provide a solid foundation for the development of industrial robots

and related components. In fact, several Taiwanese companies enjoy solid positions in

global or regional markets, such as Airtac (No.2 vendor of pneumatic equipment in China;

No.7 in the world), Hiwin (No.2 vendor of linear motion control components in the world;

No.1 in China), Delta (one of top-5 suppliers of servo motors and low-voltage inverters in

China), Teco (one of top-5 motor suppliers in the world), Advantech (one of major suppliers

of industrial controllers globally), etc.

We believe the existing capabilities in key component areas will help facilitate Taiwanese

companies shifting into the area of full robot system design. Some companies are doing so

by leveraging their in-house component supplies, such as Hiwin and Delta; some are doing

so by leveraging the support of the local component supply chain, such as Quanta

Storage. These efforts will take time to bear fruit, but we are optimistic on their growth

outlook.

China as a “home market” Despite the promising demand outlook for China, still over 80% of its industrial robots are

supplied by foreign vendors; furthermore, the industrial robots manufactured by Chinese

vendors also source about 70-80% of the components from overseas suppliers, based on

our industry surveys. While robots have been identified as one of the key focuses under

China’s 13th Five-Year Plan and “Made in China 2025” policy, the incentive/subsidies from

local governments do not seem to foster the “craftsmanship” required for the industrial

robot business in China.

Our industry research indicates that China is still not competitive in several robot-related

component areas, including reducers, servo motors, sensors, and linear motion control

related components. This situation gives Taiwanese companies a competitive edge, in our

view, especially when Taiwan’s products are typically more price-competitive than those of

Key robot components

Pro-Hawk (8083 TT), Aurotek (6215 TT)

CHELIC (4555 TT), Airtac (1590 TT)

NEXCOM (8234 TT), ICP DAS (3577 TT),

Hiwin (2049 TT), TBI Motion (4540 TT), Axiomtek (3088 TT), iBase (2463 TT), Adlink (6166 TT), Delta (2308 TT)

Chieftec (1597 TT) AAEON (2463 TT), iEi (3022 TT),

Ennoconn (6414 TT), Adlink (6166 TT)

Delta (2308 TT), Shinlin Electric (1503 TT),

Tatung (2371 TT), Teco (1504 TT),

Hiwin (2049 TT), TBI Motion (4540 TT) ICP DAS (3577 TT), Delta (2308 TT), Aurotek (6215 TT), ACE PILLAR (8374 TT) Delta (2308 TT)

ACE PILLAR (8374 TT),

Advantech (2395 TT)

Delta (2308 TT), Hiwin (2049 TT),

Aurotek (6215 TT), ACE PILLAR (8374 TT)

Hiwin (2049 TT), CHELIC (4555 TT),

Airtac (1590 TT)

System integrations

Axiomtek (3088 TT), Mirle (2464 TT), Gallant Precision (5443 TT), Chroma ATE (2360 TT)

Industrial robots

Hiwin (2049 TT), Delta (2308 TT), Aurotek (6215 TT), Quanta Storage (6188 TT), Gallant Precision (5443 TT), Kenmec (6125 TT), Taiwan Calsonic (4523 TT)

Bearing/ Gear

Linear guide

Ballscrew

PC-based controllers

Controller/ control system

Machine vision

Sensor

Gripper

Actuator

Motor

Reducer

Taiwan’s electronics and

precision machinery

sectors should provide a

solid foundation for

developing industrial

robots

China is the most

important market for

Taiwan’s industrial robot

sector, in our view

Page 18

18

Taiwan Industrial Robotics: 16 May 2017

overseas major vendors, but have consistently better quality than local suppliers in China.

We believe Taiwanese players stand a good chance of embracing the vast growth potential

in China, before the local supply chain in China starts to take shape.

Rising automation demand from local industries According to our industry surveys, the main target sectors in Taiwan’s industrial robot

supply chain include electronic, machinery, and auto parts. The electronics sector is no

doubt the most promising area, given Taiwan’s strong presence in the global IT industry

and the increasing automation demand for many technology companies.

Among all major sub-sectors in Taiwan’s electronics industry, we consider downstream

tech companies to be under more pressure to accelerate their automation, given their

lower penetration of production automation (than those of upstream tech companies) and

also the rising labour costs in China. The disclosure of these companies’ automation

roadmaps remains limited, but some companies appear more aggressive than others. For

example, Hon Hai’s chairman, Terry Guo, targets to achieve 30% automation by 2020,

while Delta aims to install 10-20k robot arms in China in the next 5 years, which could lead

to a 90% reduction in its workforce.

We conducted a quick estimate on the likely robot demand from these Taiwanese

downstream tech companies. If we assume all these companies achieve 10-20%

automation in the next 3 years, this could imply a 10-20% reduction in their workforces in

China. As a general rule of thumb in developed countries, the cost of a robotic arm is

equivalent to 2 workers’ full-year salaries. For our exercise we assumed the robot cost is

equivalent to 3 workers in China (although this might be a bit conservative give the ever-

rising labour costs there).

Potential robot demands from major EMS/ODM players in Taiwan

2016 revenue China workforce Likely robot demands in 3 years ('000 units)

Company (TWDbn) ('000 persons) 10% automation 20% automation

Hon Hai Precision 4,359 1,000 33.3 66.7 Pegatron 1,158 115 3.8 7.7 Quanta Computer 894 76 2.5 5.1 Delta Electronics 214 60 2.0 4.0 Compal Electronics 767 59 2.0 3.9 Wistron 660 36 1.2 2.4 Lite-On Technology 230 47 1.6 3.1 Inventec 428 15 0.5 1.0 Qisda Corp. 130 9 0.3 0.6 Total 47.2 94.5 Total robot demand in China from 2017E-19E (IFR forecast) 400.0 400.0 Contribution from Taiwan downstream tech companies 11.8% 23.6%

Source: Company data, Daiwa research

Based on these assumptions, as summarised in the table above, the major downstream

tech companies in Taiwan could create total robot arm demand of 47,200-94,500 units in

the next 3 years, equivalent to 11.8-23.6% of total industrial robot demand in China, based

on IFR’s forecast. While this is a rough estimate, it does represent a promising opportunity

for Taiwan’s industrial robot sector, in our view. In fact, the potential industrial robot

demand should be more substantial if we also include the potential demand from other

sub-segments in Taiwan’s electronic industry, as well as other industries like machinery,

auto parts and food & beverage.

New applications The new applications beyond traditional industrial automation related areas will also

provide growth opportunities, such as applications related to industrial IoT and Big Data, or

new types of robots like professional and personal robots (eg, robots for service, medical,

household related applications).

Nevertheless, all these new applications will require more than just robot-related know-

how. For IoT/Big Data related robotic solutions, they will involve a wide range of knowledge

(such as vertical domain know-how, big data software tools, etc), which could require

We expect downstream

tech to accelerate its

automation moves,

given its relatively low

penetration currently

and the rising labour

costs in China

New robot-related

applications could

benefit incumbents and

newcomers alike — but

new skills are required

too

Page 19

19

Taiwan Industrial Robotics: 16 May 2017

strategic alliances or even M&A. As for service/personal robots, aside from hardware

design, such businesses will require proper software support and feasible business

models. All these factors will mean that both newcomers and incumbents in the robot

supply chain will have a good chance of embracing the new opportunities, but they will also

need to develop/acquire the capabilities which they did not necessarily have in the first

place.

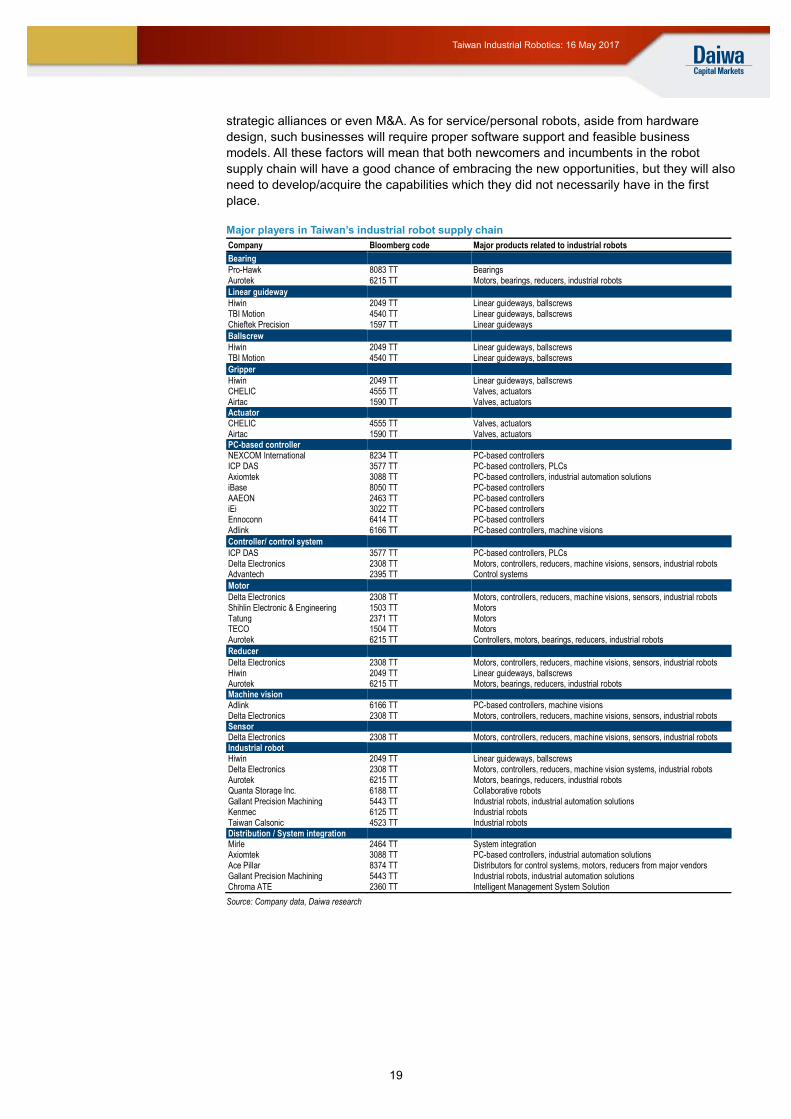

Major players in Taiwan’s industrial robot supply chain

Company Bloomberg code Major products related to industrial robots

Bearing

Pro-Hawk 8083 TT Bearings Aurotek 6215 TT Motors, bearings, reducers, industrial robots

Linear guideway

Hiwin 2049 TT Linear guideways, ballscrews TBI Motion 4540 TT Linear guideways, ballscrews Chieftek Precision 1597 TT Linear guideways

Ballscrew

Hiwin 2049 TT Linear guideways, ballscrews TBI Motion 4540 TT Linear guideways, ballscrews

Gripper

Hiwin 2049 TT Linear guideways, ballscrews CHELIC 4555 TT Valves, actuators Airtac 1590 TT Valves, actuators Actuator CHELIC 4555 TT Valves, actuators Airtac 1590 TT Valves, actuators PC-based controller NEXCOM International 8234 TT PC-based controllers ICP DAS 3577 TT PC-based controllers, PLCs Axiomtek 3088 TT PC-based controllers, industrial automation solutions iBase 8050 TT PC-based controllers AAEON 2463 TT PC-based controllers iEi 3022 TT PC-based controllers Ennoconn 6414 TT PC-based controllers Adlink 6166 TT PC-based controllers, machine visions

Controller/ control system

ICP DAS 3577 TT PC-based controllers, PLCs Delta Electronics 2308 TT Motors, controllers, reducers, machine visions, sensors, industrial robots Advantech 2395 TT Control systems

Motor

Delta Electronics 2308 TT Motors, controllers, reducers, machine visions, sensors, industrial robots Shihlin Electronic & Engineering 1503 TT Motors Tatung 2371 TT Motors TECO 1504 TT Motors Aurotek 6215 TT Controllers, motors, bearings, reducers, industrial robots

Reducer

Delta Electronics 2308 TT Motors, controllers, reducers, machine visions, sensors, industrial robots Hiwin 2049 TT Linear guideways, ballscrews Aurotek 6215 TT Motors, bearings, reducers, industrial robots Machine vision

Adlink 6166 TT PC-based controllers, machine visions Delta Electronics 2308 TT Motors, controllers, reducers, machine visions, sensors, industrial robots Sensor

Delta Electronics 2308 TT Motors, controllers, reducers, machine visions, sensors, industrial robots Industrial robot

Hiwin 2049 TT Linear guideways, ballscrews Delta Electronics 2308 TT Motors, controllers, reducers, machine vision systems, industrial robots Aurotek 6215 TT Motors, bearings, reducers, industrial robots Quanta Storage Inc. 6188 TT Collaborative robots Gallant Precision Machining 5443 TT Industrial robots, industrial automation solutions Kenmec 6125 TT Industrial robots Taiwan Calsonic 4523 TT Industrial robots Distribution / System integration

Mirle 2464 TT System integration Axiomtek 3088 TT PC-based controllers, industrial automation solutions Ace Pillar 8374 TT Distributors for control systems, motors, reducers from major vendors Gallant Precision Machining 5443 TT Industrial robots, industrial automation solutions Chroma ATE 2360 TT Intelligent Management System Solution

Source: Company data, Daiwa research

Page 20

20

Taiwan Industrial Robotics: 16 May 2017

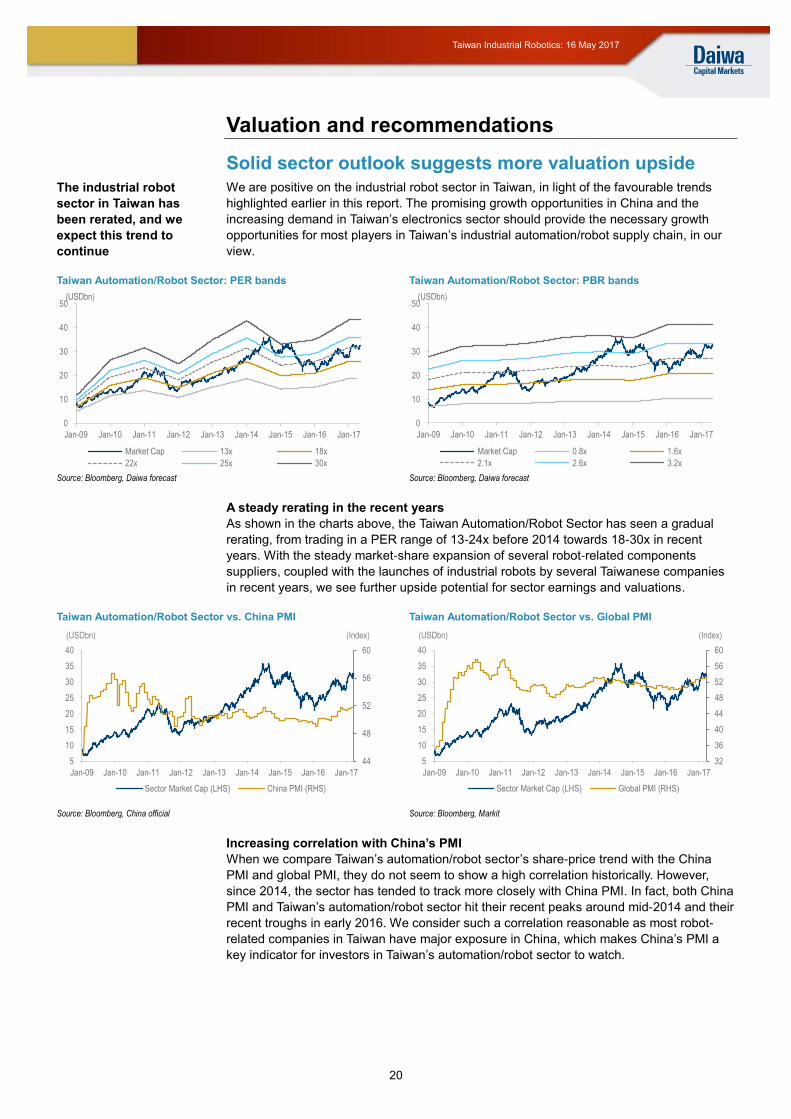

Valuation and recommendations

Solid sector outlook suggests more valuation upside

We are positive on the industrial robot sector in Taiwan, in light of the favourable trends

highlighted earlier in this report. The promising growth opportunities in China and the

increasing demand in Taiwan’s electronics sector should provide the necessary growth

opportunities for most players in Taiwan’s industrial automation/robot supply chain, in our

view.

Taiwan Automation/Robot Sector: PER bands Taiwan Automation/Robot Sector: PBR bands

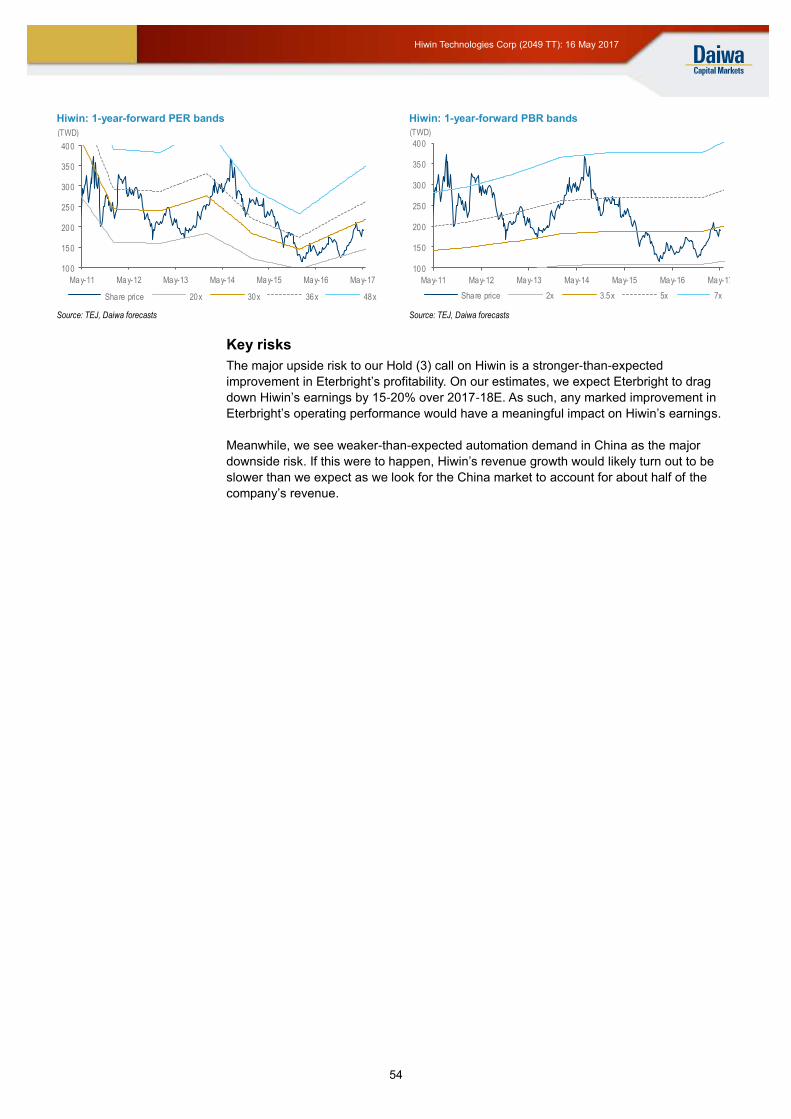

Source: Bloomberg, Daiwa forecast Source: Bloomberg, Daiwa forecast

A steady rerating in the recent years

As shown in the charts above, the Taiwan Automation/Robot Sector has seen a gradual

rerating, from trading in a PER range of 13-24x before 2014 towards 18-30x in recent

years. With the steady market-share expansion of several robot-related components

suppliers, coupled with the launches of industrial robots by several Taiwanese companies

in recent years, we see further upside potential for sector earnings and valuations.

Taiwan Automation/Robot Sector vs. China PMI Taiwan Automation/Robot Sector vs. Global PMI

Source: Bloomberg, China official Source: Bloomberg, Markit

Increasing correlation with China’s PMI

When we compare Taiwan’s automation/robot sector’s share-price trend with the China

PMI and global PMI, they do not seem to show a high correlation historically. However,

since 2014, the sector has tended to track more closely with China PMI. In fact, both China

PMI and Taiwan’s automation/robot sector hit their recent peaks around mid-2014 and their

recent troughs in early 2016. We consider such a correlation reasonable as most robot-

related companies in Taiwan have major exposure in China, which makes China’s PMI a

key indicator for investors in Taiwan’s automation/robot sector to watch.

0

10

20

30

40

50

Jan-09 Jan-10 Jan-11 Jan-12 Jan-13 Jan-14 Jan-15 Jan-16 Jan-17

(USDbn)

Market Cap 13x 18x

22x 25x 30x

0

10

20

30

40

50

Jan-09 Jan-10 Jan-11 Jan-12 Jan-13 Jan-14 Jan-15 Jan-16 Jan-17

(USDbn)

Market Cap 0.8x 1.6x

2.1x 2.6x 3.2x

44

48

52

56

60

5

10

15

20

25

30

35

40

Jan-09 Jan-10 Jan-11 Jan-12 Jan-13 Jan-14 Jan-15 Jan-16 Jan-17

Sector Market Cap (LHS) China PMI (RHS)

(USDbn) (Index)

32

36

40

44

48

52

56

60

5

10

15

20

25

30

35

40

Jan-09 Jan-10 Jan-11 Jan-12 Jan-13 Jan-14 Jan-15 Jan-16 Jan-17

Sector Market Cap (LHS) Global PMI (RHS)

(USDbn) (Index)

The industrial robot

sector in Taiwan has

been rerated, and we

expect this trend to

continue

Page 21

21

Taiwan Industrial Robotics: 16 May 2017

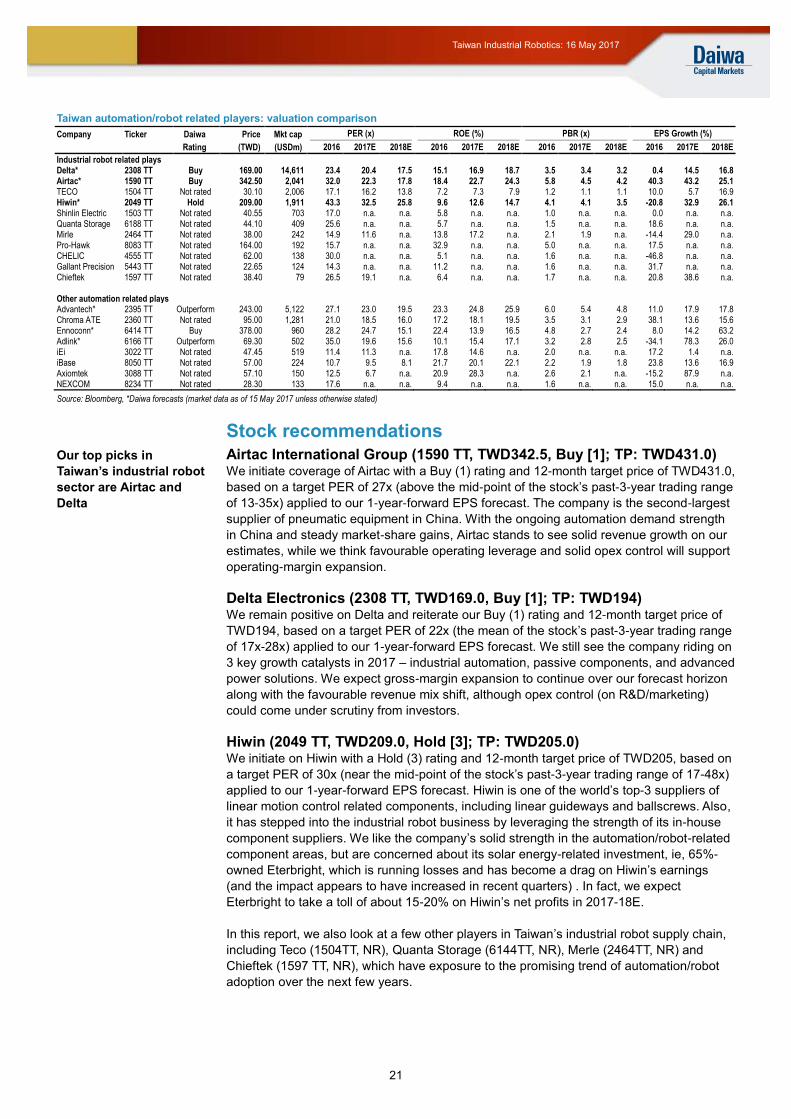

Taiwan automation/robot related players: valuation comparison

Company Ticker Daiwa Price Mkt cap PER (x) ROE (%) PBR (x) EPS Growth (%)

Rating (TWD) (USDm) 2016 2017E 2018E 2016 2017E 2018E 2016 2017E 2018E 2016 2017E 2018E

Industrial robot related plays Delta* 2308 TT Buy 169.00 14,611 23.4 20.4 17.5 15.1 16.9 18.7 3.5 3.4 3.2 0.4 14.5 16.8 Airtac* 1590 TT Buy 342.50 2,041 32.0 22.3 17.8 18.4 22.7 24.3 5.8 4.5 4.2 40.3 43.2 25.1 TECO 1504 TT Not rated 30.10 2,006 17.1 16.2 13.8 7.2 7.3 7.9 1.2 1.1 1.1 10.0 5.7 16.9 Hiwin* 2049 TT Hold 209.00 1,911 43.3 32.5 25.8 9.6 12.6 14.7 4.1 4.1 3.5 -20.8 32.9 26.1 Shinlin Electric 1503 TT Not rated 40.55 703 17.0 n.a. n.a. 5.8 n.a. n.a. 1.0 n.a. n.a. 0.0 n.a. n.a. Quanta Storage 6188 TT Not rated 44.10 409 25.6 n.a. n.a. 5.7 n.a. n.a. 1.5 n.a. n.a. 18.6 n.a. n.a. Mirle 2464 TT Not rated 38.00 242 14.9 11.6 n.a. 13.8 17.2 n.a. 2.1 1.9 n.a. -14.4 29.0 n.a. Pro-Hawk 8083 TT Not rated 164.00 192 15.7 n.a. n.a. 32.9 n.a. n.a. 5.0 n.a. n.a. 17.5 n.a. n.a. CHELIC 4555 TT Not rated 62.00 138 30.0 n.a. n.a. 5.1 n.a. n.a. 1.6 n.a. n.a. -46.8 n.a. n.a. Gallant Precision 5443 TT Not rated 22.65 124 14.3 n.a. n.a. 11.2 n.a. n.a. 1.6 n.a. n.a. 31.7 n.a. n.a. Chieftek 1597 TT Not rated 38.40 79 26.5 19.1 n.a. 6.4 n.a. n.a. 1.7 n.a. n.a. 20.8 38.6 n.a. Other automation related plays Advantech* 2395 TT Outperform 243.00 5,122 27.1 23.0 19.5 23.3 24.8 25.9 6.0 5.4 4.8 11.0 17.9 17.8 Chroma ATE 2360 TT Not rated 95.00 1,281 21.0 18.5 16.0 17.2 18.1 19.5 3.5 3.1 2.9 38.1 13.6 15.6 Ennoconn* 6414 TT Buy 378.00 960 28.2 24.7 15.1 22.4 13.9 16.5 4.8 2.7 2.4 8.0 14.2 63.2 Adlink* 6166 TT Outperform 69.30 502 35.0 19.6 15.6 10.1 15.4 17.1 3.2 2.8 2.5 -34.1 78.3 26.0 iEi 3022 TT Not rated 47.45 519 11.4 11.3 n.a. 17.8 14.6 n.a. 2.0 n.a. n.a. 17.2 1.4 n.a. iBase 8050 TT Not rated 57.00 224 10.7 9.5 8.1 21.7 20.1 22.1 2.2 1.9 1.8 23.8 13.6 16.9 Axiomtek 3088 TT Not rated 57.10 150 12.5 6.7 n.a. 20.9 28.3 n.a. 2.6 2.1 n.a. -15.2 87.9 n.a. NEXCOM 8234 TT Not rated 28.30 133 17.6 n.a. n.a. 9.4 n.a. n.a. 1.6 n.a. n.a. 15.0 n.a. n.a.

Source: Bloomberg, *Daiwa forecasts (market data as of 15 May 2017 unless otherwise stated)

Stock recommendations

Airtac International Group (1590 TT, TWD342.5, Buy [1]; TP: TWD431.0) We initiate coverage of Airtac with a Buy (1) rating and 12-month target price of TWD431.0,

based on a target PER of 27x (above the mid-point of the stock’s past-3-year trading range

of 13-35x) applied to our 1-year-forward EPS forecast. The company is the second-largest

supplier of pneumatic equipment in China. With the ongoing automation demand strength

in China and steady market-share gains, Airtac stands to see solid revenue growth on our

estimates, while we think favourable operating leverage and solid opex control will support

operating-margin expansion.

Delta Electronics (2308 TT, TWD169.0, Buy [1]; TP: TWD194) We remain positive on Delta and reiterate our Buy (1) rating and 12-month target price of

TWD194, based on a target PER of 22x (the mean of the stock’s past-3-year trading range

of 17x-28x) applied to our 1-year-forward EPS forecast. We still see the company riding on

3 key growth catalysts in 2017 – industrial automation, passive components, and advanced

power solutions. We expect gross-margin expansion to continue over our forecast horizon

along with the favourable revenue mix shift, although opex control (on R&D/marketing)

could come under scrutiny from investors.

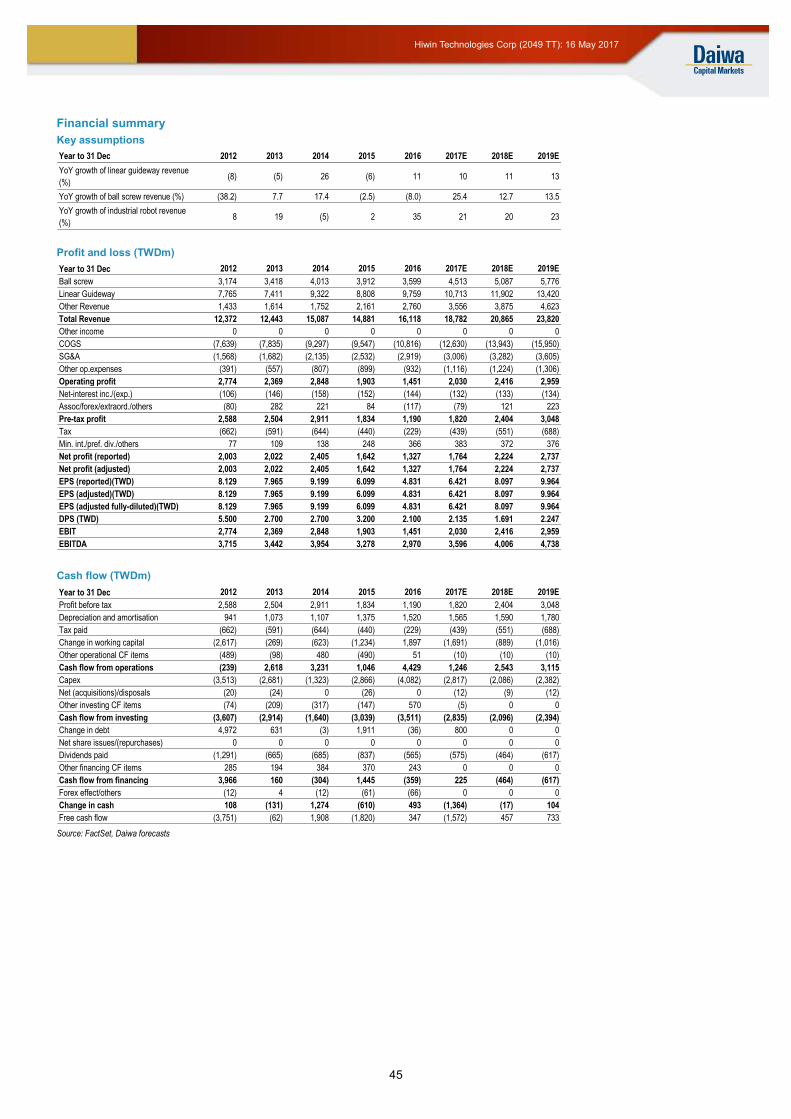

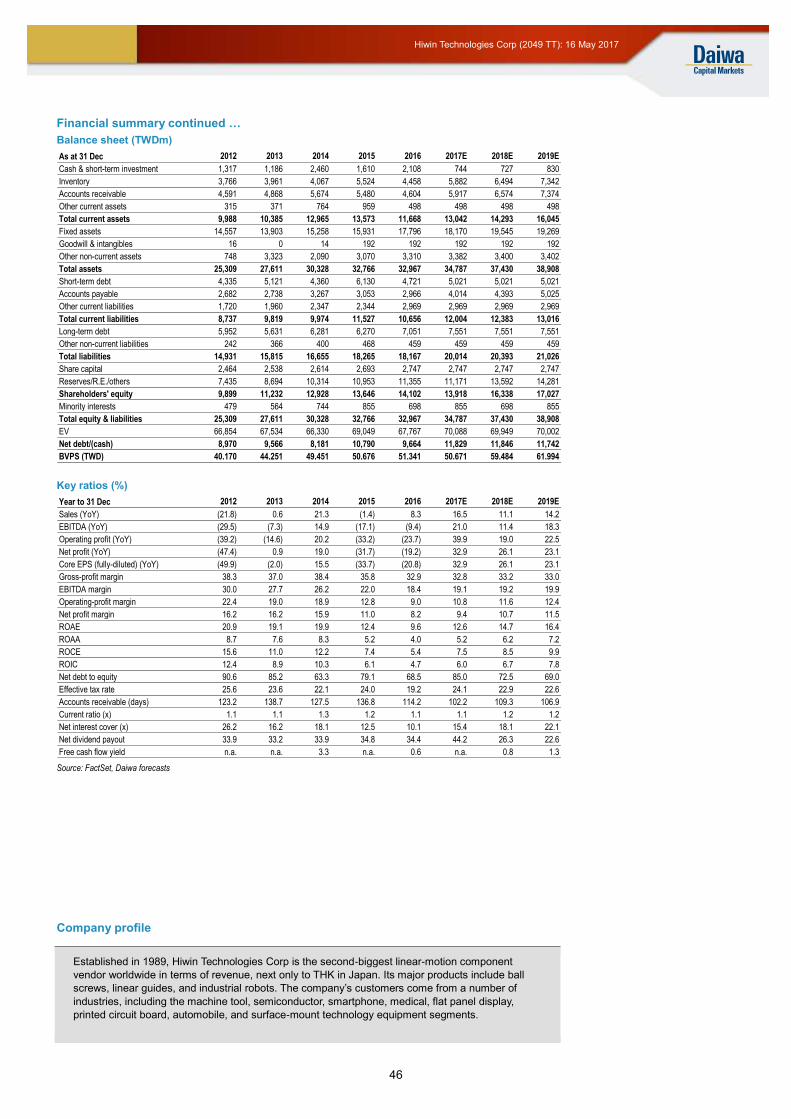

Hiwin (2049 TT, TWD209.0, Hold [3]; TP: TWD205.0) We initiate on Hiwin with a Hold (3) rating and 12-month target price of TWD205, based on

a target PER of 30x (near the mid-point of the stock’s past-3-year trading range of 17-48x)

applied to our 1-year-forward EPS forecast. Hiwin is one of the world’s top-3 suppliers of

linear motion control related components, including linear guideways and ballscrews. Also,

it has stepped into the industrial robot business by leveraging the strength of its in-house

component suppliers. We like the company’s solid strength in the automation/robot-related

component areas, but are concerned about its solar energy-related investment, ie, 65%-

owned Eterbright, which is running losses and has become a drag on Hiwin’s earnings

(and the impact appears to have increased in recent quarters) . In fact, we expect

Eterbright to take a toll of about 15-20% on Hiwin’s net profits in 2017-18E.

In this report, we also look at a few other players in Taiwan’s industrial robot supply chain,

including Teco (1504TT, NR), Quanta Storage (6144TT, NR), Merle (2464TT, NR) and

Chieftek (1597 TT, NR), which have exposure to the promising trend of automation/robot

adoption over the next few years.

Our top picks in

Taiwan’s industrial robot

sector are Airtac and

Delta

Page 22

22

Taiwan Industrial Robotics: 16 May 2017

Global automation/robot sector: valuation comparison

Company Ticker Daiwa Price Mkt cap PER (x) ROE (%) PBR (x) EPS Growth (%)

Rating (lc) (USDm) 2016 2017E 2018E 2016 2017E 2018E 2016 2017E 2018E 2016 2017E 2018E

Industrial robots ABB ABB SS Not-rated 218.40 54,794 191.4 176.6 156.9 13.6 18.8 20.5 32.5 34.1 32.8 -3.6 8.4 12.5 Denso 6902 JP Neutral 4882.00 34,125 15.9 18.8 17.1 7.6 6.6 7.1 1.2 1.2 1.2 -5.2 -15.7 10.3 FANUC* 6954 JP Outperform 22595.00 40,590 27.7 34.3 29.2 11.8 9.5 10.8 3.3 3.2 3.1 -23.0 -19.4 17.5 Krones KRN GR Not-rated 110.71 3,838 20.5 19.4 17.9 14.6 13.6 13.5 2.8 2.6 2.3 12.3 5.5 8.4 Kawasaki Heavy Industries* 7012 JP Neutral 339.00 4,986 12.3 21.6 13.0 10.7 6.0 9.6 1.3 1.3 1.2 -10.8 -43.0 65.6 Nachi* 6474 JP Neutral 606.00 1,329 32.8 30.8 n.a. 3.9 4.9 n.a. 1.5 1.5 n.a. -60.6 6.5 n.a. Panasonic* 6752 JP Neutral 1341.50 28,968 16.1 20.9 16.5 11.0 - 10.3 1.8 1.8 1.6 7.4 -22.9 26.7 Omron 6645 JP Not-rated 4535.00 8,541 20.7 21.8 19.8 10.1 9.7 10.0 2.2 2.0 1.9 -22.9 -5.0 10.1 Mitsubishi Heavy Industries* 7011 JP Neutral 453.50 13,468 23.8 17.4 14.4 3.7 5.1 5.9 0.9 0.9 0.8 -42.2 37.2 21.1 Siasun 300024 CH Not-rated 18.18 4,121 69.1 54.4 41.0 7.6 10.9 10.6 5.1 4.5 4.1 -3.6 27.0 32.6 Brooks Automation BRKS US Not-rated 28.34 1,974 60.3 25.8 23.1 -11.7 11.0 11.1 3.5 3.3 3.1 4.4 134.0 11.5 KUKA KU2 GR Not-rated 113.13 4,938 39.1 36.2 29.9 11.0 14.1 15.6 5.4 4.8 4.2 13.5 8.1 21.1 Yaskawa* 6506 JP Neutral 2190.00 5,141 25.9 33.5 30.8 12.7 9.3 9.5 3.2 3.0 2.8 -14.0 -22.9 8.7 Service robots iRobot IRBT US Not-rated 92.37 2,533 58.5 48.1 32.4 10.4 14.1 12.8 6.5 5.9 5.2 7.0 21.7 48.6 Intuitive Surgical ISRG US Not-rated 850.67 31,339 45.9 35.9 31.4 14.6 15.0 17.4 5.7 6.3 5.7 17.5 27.7 14.4 Toyota* 7203 JP Outperform 6009.00 172,600 8.1 9.9 10.2 13.8 10.5 9.5 1.1 1.0 0.9 7.8 -18.3 -2.3 Panasonic* 6752 JP Neutral 1341.50 28,968 16.1 20.9 16.5 11.0 - 10.3 1.8 1.8 1.6 7.4 -22.9 26.7 Honda* 7267 JP Neutral 3194.00 50,930 16.7 9.3 9.9 5.0 8.8 7.7 0.9 0.8 0.7 -34.1 79.0 -5.9 Samsung Electronics* 005930 KS Buy 2305000.00 288,454 14.8 8.4 7.4 12.5 19.0 17.9 1.9 1.6 1.3 22.7 76.1 13.1 MSI 2377 TT Not-rated 71.40 2,008 12.3 10.9 9.7 18.6 19.4 20.3 2.2 2.1 2.0 31.9 13.6 12.1 ASUSTek* 2357 TT Hold 280.00 6,922 10.8 11.7 11.2 11.0 9.6 9.7 1.1 1.1 1.1 12.3 -7.4 4.2 Actuators SMC* 6273 JP Outperform 33660.00 19,962 24.5 20.0 20.1 9.9 10.5 10.5 2.4 2.2 2.0 -15.8 22.7 -0.5 Yaskawa* 6506 JP Neutral 2190.00 5,141 25.9 33.5 30.8 12.7 9.3 9.5 3.2 3.0 2.8 -14.0 -22.9 8.7 IMI Plc IMI LN Not-rated 1270.00 4,459 21.4 20.6 18.4 24.0 27.6 29.0 6.7 5.9 5.3 26.9 4.0 11.5 Rotork ROR LN Not-rated 234.40 2,633 23.4 21.9 19.9 16.0 19.3 20.0 4.7 4.5 4.1 -3.8 7.0 10.3 Flowserve FLS US Not-rated 49.68 6,489 22.7 28.0 21.9 8.8 12.7 14.9 3.9 3.7 3.5 -28.7 -19.0 28.1 Omron 6645 JP Not-rated 4535.00 8,541 20.7 21.8 19.8 10.1 9.7 10.0 2.2 2.0 1.9 -22.9 -5.0 10.1 Siemens SIE GR Not-rated 129.94 121,209 20.2 16.0 15.2 15.9 17.7 17.3 3.1 2.7 2.5 0.6 26.6 5.4 Sensors Olympus* 7733 JP Neutral 4360.00 13,152 23.8 19.1 27.6 17.0 19.3 11.6 3.9 3.3 3.0 n.a. 24.9 -30.9 Sensata ST US Not-rated 39.74 6,800 13.8 12.7 11.7 14.5 22.9 19.6 3.5 2.9 2.5 5.1 8.6 8.4 Keyence 6861 JP Not-rated 48710.00 52,142 43.1 34.0 30.3 14.0 13.8 13.7 5.7 4.4 3.9 13.3 26.6 12.4 Delta* 2308 TT Buy 169.00 14,611 23.4 20.4 17.5 15.1 16.9 18.7 3.5 3.6 3.4 0.4 14.5 16.8 Rockwell Automation ROK US Not-rated 158.02 20,359 26.6 23.7 22.0 34.3 39.6 42.0 10.2 9.4 9.3 -7.3 12.3 7.8 Omron 6645 JP Not-rated 4535.00 8,541 20.7 21.8 19.8 10.1 9.7 10.0 2.2 2.0 1.9 -22.9 -5.0 10.1 Robot arms and end-effectors Yamaga Motor* 7272 JP Outperform 2807.00 8,646 15.5 11.7 10.2 12.3 14.9 15.2 1.8 1.6 1.5 5.2 33.0 14.3 ABB ABB SS Not-rated 218.40 54,794 191.4 176.6 156.9 13.6 18.8 20.5 32.5 34.1 32.8 -3.6 8.4 12.5 Omron 6645 JP Not-rated 4535.00 8,541 20.7 21.8 19.8 10.1 9.7 10.0 2.2 2.0 1.9 -22.9 -5.0 10.1 FANUC* 6954 JP Outperform 22595.00 40,590 27.7 34.3 29.2 11.8 9.5 10.8 3.3 3.2 3.1 -23.0 -19.4 17.5 Yaskawa* 6506 JP Neutral 2190.00 5,141 25.9 33.5 30.8 12.7 9.3 9.5 3.2 3.0 2.8 -14.0 -22.9 8.7 Controllers Omron 6645 JP Non-rated 4535.00 8,541 20.7 21.8 19.8 10.1 9.7 10.0 2.2 2.0 1.9 -22.9 -5.0 10.1 Kawasaki Heavy Industries* 7012 JP Neutral 339.00 4,986 12.3 21.6 13.0 10.7 6.0 9.6 1.3 1.3 1.2 -10.8 -43.0 65.6 Epson* 6724 JP Outperform 2329.00 8,193 18.2 17.0 13.7 9.5 10.1 11.8 1.8 1.7 1.6 -59.3 6.9 23.9 IMI Plc IMI LN Not-rated 1270.00 4,459 21.4 20.6 18.4 24.0 27.6 29.0 6.7 5.9 5.3 26.9 4.0 11.5 Sulzer SUN SW Not-rated 114.50 3,936 32.6 27.2 20.9 3.1 7.5 10.5 2.5 2.5 2.4 -10.6 19.8 30.3 Olympus* 7733 JP Neutral 4360.00 13,152 23.8 19.1 27.6 17.0 19.3 11.6 3.9 3.3 3.0 n.a. 24.9 -30.9 Hollysys HOLI US Not-rated 16.62 994 8.2 11.7 8.8 18.9 11.6 13.1 1.5 1.3 1.2 17.4 -29.6 33.2 Sensata ST US Not-rated 39.74 6,800 13.8 12.7 11.7 14.5 22.9 19.6 3.5 2.9 2.5 5.1 8.6 8.4 Schneider SU FP Not-rated 70.58 46,011 18.7 18.0 16.4 8.5 10.4 11.1 2.0 1.9 1.8 1.1 3.8 10.1 Rockwell Automation ROK US Not-rated 158.02 20,359 26.6 23.7 22.0 34.3 39.6 42.0 10.2 9.4 9.3 -7.3 12.3 7.8 Siemens SIE GR Not-rated 129.94 121,209 20.2 16.0 15.2 15.9 17.7 17.3 3.1 2.7 2.5 0.6 26.6 5.4 Advantech* 2395 TT Outperform 243.00 5,122 27.1 23.0 19.5 23.3 24.8 25.9 6.0 5.4 4.8 11.0 17.9 17.8 Yaskawa* 6506 JP Neutral 2190.00 5,141 25.9 33.5 30.8 12.7 9.3 9.5 3.2 3.0 2.8 -14.0 -22.9 8.7 Linear motion THK* 6481 JP Neutral 3015.00 3,553 28.1 22.8 18.9 5.5 6.7 7.8 1.5 1.5 1.4 -40.2 23.3 20.7 NSK* 6471 JP Buy 1465.00 7,109 12.1 17.0 12.4 14.3 9.9 12.8 1.7 1.7 1.5 10.6 -29.1 37.4 Danaher DHR US Not-rated 83.28 57,806 23.1 21.2 19.4 10.9 10.8 10.7 2.5 2.2 2.0 -16.0 8.8 9.3 Hiwin* 2049 TT Hold 209.00 1,911 43.3 32.5 25.8 9.6 12.6 14.7 4.1 4.1 3.5 -20.8 32.9 26.1 System Integration FANUC* 6954 JP Outperform 22595.00 40,590 27.7 34.3 29.2 11.8 9.5 10.8 3.3 3.2 3.1 -23.0 -19.4 17.5 ABB ABB SS Not-rated 218.40 54,794 191.4 176.6 156.9 13.6 18.8 20.5 32.5 34.1 32.8 -3.6 8.4 12.5 Emerson EMR US Not-rated 58.34 37,599 19.6 22.5 20.4 20.9 21.3 23.1 5.0 5.0 4.9 -6.0 -12.9 10.3 Rotork ROR LN Not-rated 234.40 2,633 23.4 21.9 19.9 16.0 19.3 20.0 4.7 4.5 4.1 -3.8 7.0 10.3 Yokogawa* 6841 JP Neutral 1919.00 4,538 16.8 19.9 22.2 13.2 10.4 8.7 2.1 2.0 1.9 70.5 -15.4 -10.4 Omron 6645 JP Not-rated 4535.00 8,541 20.7 21.8 19.8 10.1 9.7 10.0 2.2 2.0 1.9 -22.9 -5.0 10.1 Hollysys HOLI US Not-rated 16.62 994 8.2 11.7 8.8 18.9 11.6 13.1 1.5 1.3 1.2 17.4 -29.6 33.2 GE GE US Not-rated 28.18 244,714 18.9 17.2 15.0 9.4 18.3 21.8 3.2 3.3 3.2 13.7 9.8 15.2 Siemens SIE GR Not-rated 129.94 121,209 20.2 16.0 15.2 15.9 17.7 17.3 3.1 2.7 2.5 0.6 26.6 5.4 Motors Ametek AME US Not-rated 59.72 13,742 26.0 24.1 22.0 15.7 16.5 16.6 4.2 3.8 3.6 -9.8 7.6 9.9 Teco 1504 TT Not-rated 30.10 2,006 17.1 16.2 13.8 7.2 7.3 7.9 1.2 1.1 1.1 10.0 5.7 16.9 Delta* 2308 TT Buy 169.00 14,611 23.4 20.4 17.5 15.1 16.9 18.7 3.5 3.6 3.4 0.4 14.5 16.8 Machine vision 16.9 18.7 3.5 3.6 3.4 0.4 14.5 16.8 Cognex CGNX US Not-rated 91.65 7,941 53.3 46.0 39.0 16.7 18.0 18.4 8.2 7.3 6.4 41.0 15.8 18.0 Keyence 6861 JP Not-rated 48710.00 52,142 43.1 34.0 30.3 14.0 13.8 13.7 5.7 4.4 3.9 13.3 26.6 12.4 Delta* 2308 TT Buy 169.00 14,611 23.4 20.4 17.5 15.1 16.9 18.7 3.5 3.6 3.4 0.4 14.5 16.8 Valves Airtac* 1590 TT Buy 342.50 2,041 32.0 22.3 17.8 18.4 22.7 24.3 5.8 4.5 4.2 40.3 43.2 25.1 Flowserve FLS US Not-rated 49.68 6,489 22.7 28.0 21.9 8.8 12.7 14.9 3.9 3.7 3.5 -28.7 -19.0 28.1 Idex IEX US Not-rated 104.19 7,951 27.8 25.5 23.6 18.2 18.7 17.9 5.2 4.4 3.8 5.6 8.8 8.3 Roper ROP US Not-rated 222.40 22,692 33.9 24.5 22.3 11.9 13.1 13.9 3.9 3.5 3.2 -1.6 38.3 9.6 IMI Plc IMI LN Not-rated 1270.00 4,459 21.4 20.6 18.4 24.0 27.6 29.0 6.7 5.9 5.3 26.9 4.0 11.5 Rotork ROR LN Not-rated 234.40 2,633 23.4 21.9 19.9 16.0 19.3 20.0 4.7 4.5 4.1 -3.8 7.0 10.3

Source: Bloomberg, *Daiwa forecasts (market data as of 15 May 2017 unless otherwise stated)

Page 23

23

Taiwan Industrial Robotics: 16 May 2017

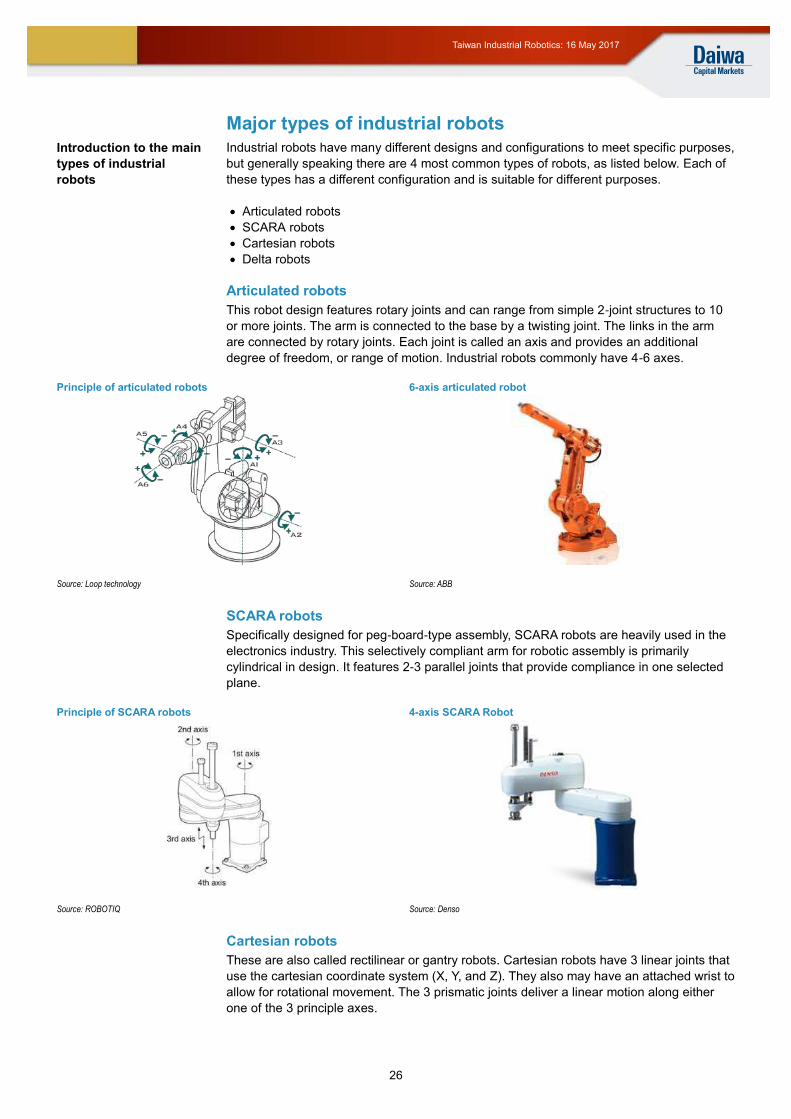

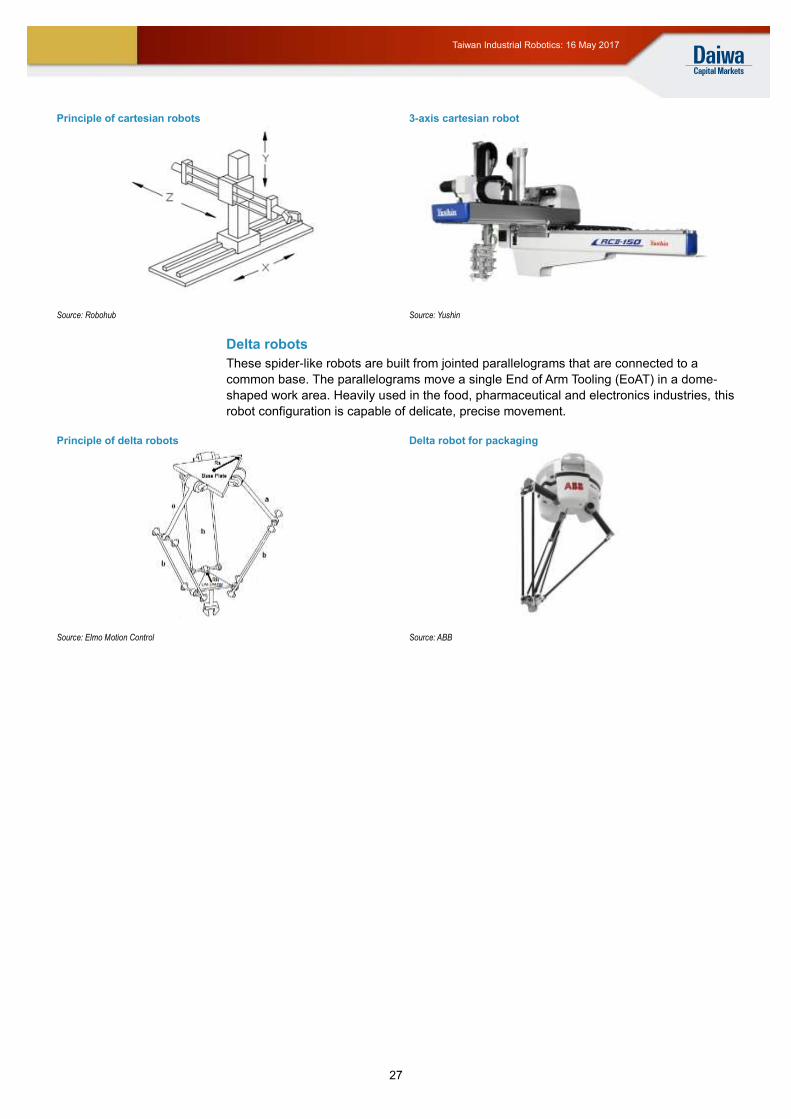

Appendix

Major components of industrial robots

An industrial robot typically consists of 5 major components: an actuator, robot arms, an

end-effector (the robot arms and end-effectors are sometimes also known as

manipulators), sensors, and a controller.

Major components of a typical industrial robot

Source: Fanuc

Actuators

An actuator is the mechanical device that converts energy into motion. Based on the

source of energy, the actuator can use one of the 3 common types: hydraulic, electric or

pneumatic. Each type of source has its advantage (see table below). For example,

hydraulic drive systems usually provide much greater speed and strength, followed by

electric ones (eg, motors), and then pneumatic.

Actuator

Motor

Gripper

Sensor

Reducer

Controller

Introduction to the major

components of industrial

robots

Actuators are the

“engines” of industrial

robots

Page 24

24

Taiwan Industrial Robotics: 16 May 2017

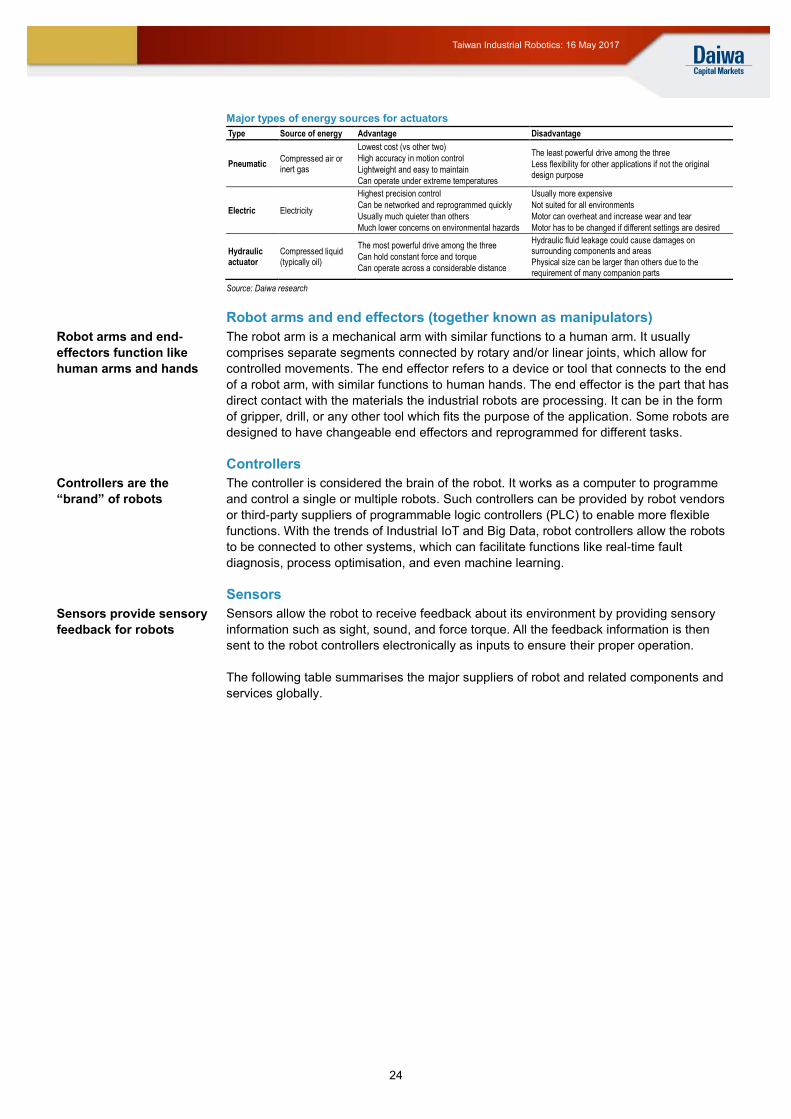

Major types of energy sources for actuators

Type Source of energy Advantage Disadvantage

Pneumatic Compressed air or inert gas

Lowest cost (vs other two)

High accuracy in motion control

Lightweight and easy to maintain

Can operate under extreme temperatures

The least powerful drive among the three

Less flexibility for other applications if not the original design purpose

Electric Electricity

Highest precision control

Can be networked and reprogrammed quickly

Usually much quieter than others

Much lower concerns on environmental hazards

Usually more expensive

Not suited for all environments

Motor can overheat and increase wear and tear

Motor has to be changed if different settings are desired

Hydraulic actuator

Compressed liquid (typically oil)

The most powerful drive among the three

Can hold constant force and torque

Can operate across a considerable distance

Hydraulic fluid leakage could cause damages on surrounding components and areas

Physical size can be larger than others due to the requirement of many companion parts

Source: Daiwa research

Robot arms and end effectors (together known as manipulators)

The robot arm is a mechanical arm with similar functions to a human arm. It usually

comprises separate segments connected by rotary and/or linear joints, which allow for

controlled movements. The end effector refers to a device or tool that connects to the end

of a robot arm, with similar functions to human hands. The end effector is the part that has

direct contact with the materials the industrial robots are processing. It can be in the form

of gripper, drill, or any other tool which fits the purpose of the application. Some robots are

designed to have changeable end effectors and reprogrammed for different tasks.

Controllers

The controller is considered the brain of the robot. It works as a computer to programme

and control a single or multiple robots. Such controllers can be provided by robot vendors

or third-party suppliers of programmable logic controllers (PLC) to enable more flexible

functions. With the trends of Industrial IoT and Big Data, robot controllers allow the robots

to be connected to other systems, which can facilitate functions like real-time fault

diagnosis, process optimisation, and even machine learning.

Sensors

Sensors allow the robot to receive feedback about its environment by providing sensory

information such as sight, sound, and force torque. All the feedback information is then

sent to the robot controllers electronically as inputs to ensure their proper operation.

The following table summarises the major suppliers of robot and related components and

services globally.

Robot arms and end-

effectors function like

human arms and hands

Controllers are the

“brand” of robots

Sensors provide sensory

feedback for robots

Page 25

25

Taiwan Industrial Robotics: 16 May 2017

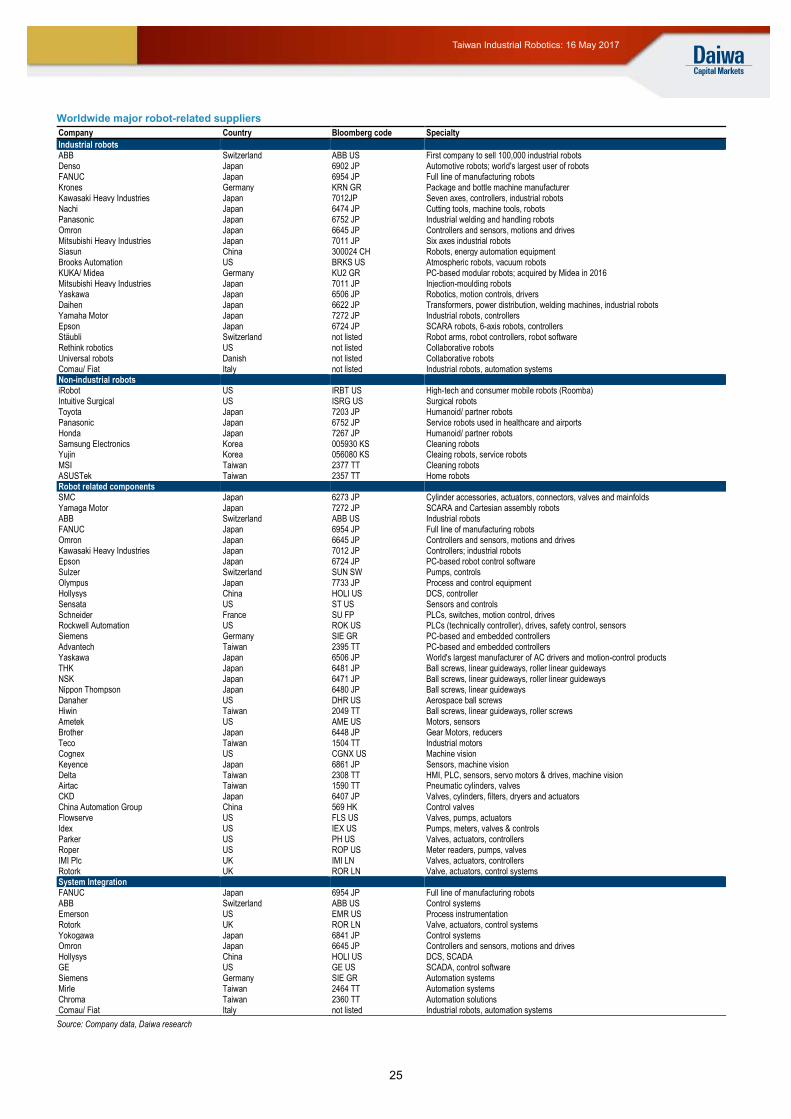

Worldwide major robot-related suppliers

Company Country Bloomberg code Specialty

Industrial robots ABB Switzerland ABB US First company to sell 100,000 industrial robots Denso Japan 6902 JP Automotive robots; world's largest user of robots FANUC Japan 6954 JP Full line of manufacturing robots Krones Germany KRN GR Package and bottle machine manufacturer Kawasaki Heavy Industries Japan 7012JP Seven axes, controllers, industrial robots Nachi Japan 6474 JP Cutting tools, machine tools, robots Panasonic Japan 6752 JP Industrial welding and handling robots Omron Japan 6645 JP Controllers and sensors, motions and drives Mitsubishi Heavy Industries Japan 7011 JP Six axes industrial robots Siasun China 300024 CH Robots, energy automation equipment Brooks Automation US BRKS US Atmospheric robots, vacuum robots KUKA/ Midea Germany KU2 GR PC-based modular robots; acquired by Midea in 2016 Mitsubishi Heavy Industries Japan 7011 JP Injection-moulding robots Yaskawa Japan 6506 JP Robotics, motion controls, drivers Daihen Japan 6622 JP Transformers, power distribution, welding machines, industrial robots Yamaha Motor Japan 7272 JP Industrial robots, controllers Epson Japan 6724 JP SCARA robots, 6-axis robots, controllers Stäubli Switzerland not listed Robot arms, robot controllers, robot software Rethink robotics US not listed Collaborative robots Universal robots Danish not listed Collaborative robots Comau/ Fiat Italy not listed Industrial robots, automation systems Non-industrial robots iRobot US IRBT US High-tech and consumer mobile robots (Roomba) Intuitive Surgical US ISRG US Surgical robots Toyota Japan 7203 JP Humanoid/ partner robots Panasonic Japan 6752 JP Service robots used in healthcare and airports Honda Japan 7267 JP Humanoid/ partner robots Samsung Electronics Korea 005930 KS Cleaning robots Yujin Korea 056080 KS Cleaing robots, service robots MSI Taiwan 2377 TT Cleaning robots ASUSTek Taiwan 2357 TT Home robots Robot related components SMC Japan 6273 JP Cylinder accessories, actuators, connectors, valves and mainfolds Yamaga Motor Japan 7272 JP SCARA and Cartesian assembly robots ABB Switzerland ABB US Industrial robots FANUC Japan 6954 JP Full line of manufacturing robots Omron Japan 6645 JP Controllers and sensors, motions and drives Kawasaki Heavy Industries Japan 7012 JP Controllers; industrial robots Epson Japan 6724 JP PC-based robot control software Sulzer Switzerland SUN SW Pumps, controls Olympus Japan 7733 JP Process and control equipment Hollysys China HOLI US DCS, controller Sensata US ST US Sensors and controls Schneider France SU FP PLCs, switches, motion control, drives Rockwell Automation US ROK US PLCs (technically controller), drives, safety control, sensors Siemens Germany SIE GR PC-based and embedded controllers Advantech Taiwan 2395 TT PC-based and embedded controllers Yaskawa Japan 6506 JP World's largest manufacturer of AC drivers and motion-control products THK Japan 6481 JP Ball screws, linear guideways, roller linear guideways NSK Japan 6471 JP Ball screws, linear guideways, roller linear guideways Nippon Thompson Japan 6480 JP Ball screws, linear guideways Danaher US DHR US Aerospace ball screws Hiwin Taiwan 2049 TT Ball screws, linear guideways, roller screws Ametek US AME US Motors, sensors Brother Japan 6448 JP Gear Motors, reducers Teco Taiwan 1504 TT Industrial motors Cognex US CGNX US Machine vision Keyence Japan 6861 JP Sensors, machine vision Delta Taiwan 2308 TT HMI, PLC, sensors, servo motors & drives, machine vision Airtac Taiwan 1590 TT Pneumatic cylinders, valves CKD Japan 6407 JP Valves, cylinders, filters, dryers and actuators China Automation Group China 569 HK Control valves Flowserve US FLS US Valves, pumps, actuators Idex US IEX US Pumps, meters, valves & controls Parker US PH US Valves, actuators, controllers Roper US ROP US Meter readers, pumps, valves IMI Plc UK IMI LN Valves, actuators, controllers Rotork UK ROR LN Valve, actuators, control systems System Integration FANUC Japan 6954 JP Full line of manufacturing robots ABB Switzerland ABB US Control systems Emerson US EMR US Process instrumentation Rotork UK ROR LN Valve, actuators, control systems Yokogawa Japan 6841 JP Control systems Omron Japan 6645 JP Controllers and sensors, motions and drives Hollysys China HOLI US DCS, SCADA GE US GE US SCADA, control software Siemens Germany SIE GR Automation systems Mirle Taiwan 2464 TT Automation systems Chroma Taiwan 2360 TT Automation solutions Comau/ Fiat Italy not listed Industrial robots, automation systems

Source: Company data, Daiwa research

Page 26

26

Taiwan Industrial Robotics: 16 May 2017