71

20 19 WRAP-UP OUTLOOK 20 20 TAX

20 19 WRAP-UP OUTLOOK

20 20 TAX

PART I: GOVERNMENT POLICY AND TAX ADMINISTRATION

TABLE OF CONTENT

INTRODUCTION: THE TAX LANDSCAPE IN NIGERIA

The African Continental

Free Trade Agreement.

Revision of Excise Duty

for Specific Products by

the Federal Government.

The Executive Order 007: Road

Infrastructure Development

and Refurbishment Investment

Tax Credit Scheme Order 2019.

01 02 03

Federal Executive Council

Approval of New Import

Levy.

The Value Added Tax

(Exemption of Commission

on the Stock Exchange

Transaction) Order of 2014

Reached its Natural End.

Federal Inland Revenue

Service Suspension of

Application of Lien on

Customers’ Bank Account.

04 05 06

Public Notice on Deduction

at Source of Withholding

TAT/VAT on Compensation

paid to Agent, Dealers,

Distributors and Retailers by

Principal.

Lagos Internal Revenue Service

Public Notice Appointing Payers

of Capital Sums Inclusive of

Employers as Collecting Agent

of Capital Gains Tax.

Federal Inland Revenue

Service Circular on the

Claim of Tax Treaty

Benefits in Nigeria.

07 08 09

Lagos State Internal

Revenue Service Public

Notice on Tax

Identification Number

Integration.

Federal Inland Revenue

Service Guidelines on Mutual

Agreement Procedure in

Nigeria.

Establishment of non-

Resident Persons Tax

Office by the Federal

Inland Revenue Service.

10 11 12

The Introduction of the E-

form ‘NXP’

13

TABLE OF CONTENT

Communication of a Tax

Objection Via Electronic

Medium Is Valid: Earth

Moving Intl Ltd v. Federal

Inland Revenue Service

Validity of the imposition of

Consumption Tax by the Lagos

State Government: Registered

Trustees of Hotel Owners and

Managers Association of Lagos

v. Attorney General of Lagos

State and Federal Inland

Revenue Service

Local Government Cannot

Impose Taxes Not

Contained in The Taxes and

Levies Approved List for

Collection: Abuja Electricity

Distribution Company v.

Kuje Area Council

01 02 03

Federal Inland Revenue

Service Cannot Freeze

Taxpayer’s Bank Account

Without A Valid Court Order:

Ama Etuwewe v. Federal

Inland Revenue Service &

Anor.

04

The National Lottery Act 2015

(As Amended)

Nigerian Police Trust Fund

Establishment Act 2019 Creates

Additional Tax Burden on

Nigerian Companies for The

Next 6 Years

Deep Offshore and Inland

Basin Production Sharing

Contract (Amendment) Act

2019

01 02 03

The Finance Act 2019

04

PART II: LEGISLATIVE DEVELOPMENTS

PART III: JUDICIAL DEVELOPMENTS

Best of judgement

assessment based on the

value of property

inappropriate: Theodak

Nigeria Limited v. Federal

Inland Revenue Service.

06

Interest and penalties to accrue

from date of failure to remit

taxes: Shell Nigeria Exploration

and Production company

Limited v. Lagos State Internal

Revenue Service.

05

TABLE OF CONTENT

Voluntary Pension

Contribution is Tax Exempt

if not withdrawn for a

period of not less than 5

years from the day of

contribution

07

Reverse Charge of VAT

Applicable in Nigeria:

Vodacom Business Nigeria

Limited v. Federal Inland

Revenue Service.

Gratuities Not Liable to Income

Tax in Nigeria: Nigerian

Breweries Plc v. Abia State

Board of Internal Revenue &

Ors

Strict Application of Section

19 of the Companies

Income Tax Act- Excess

Dividend Tax:

08 09

10

Excess Dividends Taxation

Actis Africa Nigeria Limited v.

Federal Inland Revenue

Service;

Excess Dividends Taxation

United Capital Plc v. Federal

Inland Revenue Service.

Mortgage Banks Not Liable

to Value Added Tax: Infinity

Trust Mortgage Bank Plc v.

Federal Inland Revenue

Service.

11 12

13

Non-Registration of

Technology Transfer

Agreement with National

Office for Technology

Acquisition and Promotion

does not render the

agreement void and

unenforceable: Stanbic IBTC

Holdings Plc v. Financial

Reporting Council of Nigeria.

Limiting the Whims and

Caprices of the Tax

Authorities: Polaris Bank

Limited v. Abia State Board of

Internal Revenue.

Liability of Non-Resident

Entities to VAT in Nigeria:

Allan Gray Investment

Management Nigeria

Limited v. Federal Inland

Revenue Service

14 15

16

TABLE OF CONTENT

PART IV: THE 2020 TAX YEAR IN VIEW

The Finance Act 2019 Introduce E-Filing for Transfer

Pricing Returns In 2020

Increase in Tax Burden

01 02 03

Increase in Tax Drive Appeals to The Federal High

Court

Global Policy and

Developments in The Digital

Economy

04 05 06

GLOSSARY

OUR TEAM

CONTACT US

INTRODUCTION:THE TAX LANDSCAPE

IN NIGERIA

The tax space also experienced a series of initiatives deployed by the

Federal Inland Revenue Service (FIRS) and the Internal Revenue Services

(IRS) of various states of the Nigerian federation to enhance tax payment

and collection. There is a gradual shift towards automation and the

utilization of technology for the collection and remittance of taxes. These

developments demonstrate the commitment of the government to deploy

aggressive and innovative tools to broaden the tax net and increase tax

revenue. It also shows the increased focus on the financing of public

expenditure in Nigeria through taxation.

This 2019 Tax Review/2020 Outlook (the Report), has therefore been

designed to provide useful insight on the initiatives, policies, reforms, and

strategies formulated by the government and tax authorities to improve the

Nigerian tax system and increase tax revenue generation in the last one

year. The developments examined in this Report range from government

policy and tax administration to legislative intervention and judicial

decisions on tax issues. The Report also highlights predictions for the tax

landscape for the year 2020.

The

2019 fiscal year was dotted with ample

administrative, judicial

and regulatory

developments. The Nigerian fiscal

landscape is evolving due

to the continued drive by

the government to improve

and increase tax revenue.

5

PART I

GOVERNMENT POLICY AND

TAX ADMINISTRATION

Although Nigeria’s tax to Gross Domestic Product (GDP) ratio continues to hover around

6%, it was reported that the FIRS generated more than half of the revenue contribution to

the federation account for some months of 2019. With a projected tax revenue of N8

Trillion (Eight Trillion Naira), the FIRS realised the sums of N1,046,889,800(One Billion,

Forty Six Million, Eight hundred and Eighty-nine thousand, Eight hundred naira only),

N1,400,608,600 (One Billion, Four Hundred Million, Six Hundred and Eight Thousand, Six

Hundred Naira), and N1,564,568,900 (One Billion, Five Hundred and Sixty Four Million,

Five Hundred and Sixty Eight thousand, Nine hundred naira), as tax collections for the

first, second and third quarters respectively.[1] For the final quarter of 2019, FIRS is yet

to publish the details of its revenue collection but it is however unlikely that it will surpass

or be substantially different from the revenue recorded in the previous quarters.

Aside from the revenue generated by the government, 2019 also witnessed several

government policies and administrative directives from the tax authorities geared towards

enhancing revenue generation, collection, and remittance. Through the course of the year

2019, government policies and administrative directives were particularly high with both

the FIRS and the Lagos State Internal Revenue Service (LIRS) issuing circulars and public

notices clarifying several tax issues in Nigeria.

We have identified below some of these government policies and administrative directives

which were introduced in 2019, and which we consider relevant for the year 2020.

2019 also witnessed several government policies and administrative directives from the tax authorities geared towards enhancing revenue generation, collection, and remittance.

7

1. FIRS “Tax Statistics/Report” available at https://www.firs.gov.ng/TaxResources/TaxStatisticsReports accessed on 23.01.2020

THE AFRICAN CONTINENTAL

FREE TRADE AGREEMENT

The Agreement establishing the African Continental Free Trade Area (AfCFTA) was signed

on March 21, 2018 by 44 African Union member states in Kigali, Rwanda and came into

force on May 30, 2019 for the countries that deposited their instruments of ratification.

Nigeria became a signatory to the AfCFTA Agreement on July 07, 2019, bringing the total

number of countries that are signatories to the AfCFTA Agreement to 53 at the relevant

date.

The AfCFTA Agreement establishes a free trade area, and it is

envisaged that the AfCFTA will lay the foundation for the

establishment of a continental customs union in future.[2]

Continental customs union in this case means the adoption of a

common external tariff for goods entering the country of the

contracting parties to the AfCFTA Agreement.[3]

The overarching trade liberalization objectives of the AfCFTA includes the creation of a

single market for goods and services facilitated by movement of persons; establishment of

a liberalized market through successive rounds of negotiations; laying the foundation for

the establishment of a continental customs union; and facilitation of investments through

the movement of natural persons and capital. The economic development objectives of the

AfCFTA include; sustainable inclusive development and structural transformation,

enhancement of competitiveness, promotion of industrial development through

diversification, and acceleration of regional and continental integration.

Nigeria became a

signatory to the

AFCFTA

Agreement on

July 07, 2019

8

2. Article 3(d) of the AfCFTA Agreement 3. See Art. 1(j) of the AfCFTA Agreement

By a circular dated 2nd February 2019, the FGN revised the applicable excise duty for

“other fermented beverages (for example, Cider, Perry, Mead, Sake); mixture of

fermented beverages; and mixture of fermented beverages and non-alcoholic beverages

not elsewhere specified or included”.

The rate as prescribed by the circular for these products is ₦0.30K per centilitre and is

effective from June 04, 2018 to June 03, 2019 (i.e. the first year) and ₦0.35K per centilitre

from June 04 2019 (i.e. the start date of the second year). This is in effect a reduction in

the excise rate of ₦1.50 per centiliter previously applied to beverages with relatively lower

alcohol content than beer and stout. The imposition of a uniform excise duty rate for items

with similar alcohol contents is commendable as it displaces the pre-existing situation

where products with similar alcohol content were subjected to different rates.

Whilst it may appear that the implementation of this circular may result in the reduction of

the revenue of government, it however incentivizes the manufacturers as well as

increases the consumption of these products.

The rate as prescribed

by the circular for these

products is

₦0.30K per

centiliter…

REVISION OF EXCISE DUTY

FOR SPECIFIC PRODUCTS BY

THE FEDERAL GOVERNMENT

9

The President on 25th January 2019, signed

the Executive Order 007 tagged the “Road

Infrastructure Development and

Refurbishment Investment Tax Credit

Scheme Order 2019” (The 007 Order).

The 007 Order was issued pursuant to

Section 23(2) of CITA, which gives the

President the power to exempt by order,

any company or class of companies from all

or any of the provisions of CITA or exempt

any profit of any company or class of

companies from tax.

The Scheme was introduced to reduce

government budget with respect to capital

expenditure on road development. It

enables the Federal Government of Nigeria

(FGN) to leverage on private sector

funding for the construction or

refurbishment of eligible road infrastructure

projects in Nigeria for a period of 10 (ten)

years.

THE EXECUTIVE ORDER 007 :

ROAD INFRASTRUCTURE

DEVELOPMENT AND

REFURBISHMENT

INVESTMENT TAX CREDIT

SCHEME ORDER 2019

10

It also allows taxpayers to inter alia (a)

partner with the FGN on the development of

road infrastructure in Nigeria; (b) earn tax

credit on the value/cost of the road

construction; (c) trade their tax credit on the

stock exchange; (d) earn tax-free income on

the cost incurred in developing the road,

thereby increasing their revenue for the

relevant years; and (e) carry forward their

credit from year to year until it is fully utilized.

Following the 2016 Kigali Summit where African leaders agreed to implement a 0.2%

uniform levy on eligible imports into members states, the Federal Executive Council in May

2019 approved a new 0.2% import levy on eligible imports from African Union (AU)

member states.

The levy is to be calculated based on cost, insurance and freight values of the eligible

goods. This uniform levy is applicable to all goods save for the following:

FEDERAL EXECUTIVE

COUNCIL APPROVAL OF

NEW IMPORT LEVY

goods originating from outside the territory of a

member state for home consumption in a

member state, and re-exported to another

member state;

goods received as aid, gifts and non-repayable

grants by a state or by legal entities constituted

under public law and earmarked for charitable

works;

goods originating from non-member states,

imported as part of financing agreements with

foreign partners, subject to a clause expressly

exempting the said goods from any fiscal or para-

fiscal levy;

goods which have been imported prior to

commencement of the import levy;

goods that have been ordered and are under

importation process before approval of the import

levy;

goods on which the import levy had previously

been paid.

Revenues raised from the import levy is to be used to settle AU subscriptions and the

excess will be paid into a special account which will be used in settling subscriptions to

other multilateral organizations.

11

The Value Added Tax (VAT) exemption which was enjoyed on commissions: (a) earned on

traded value of shares; (b) payable to the Securities and Exchange Commission; (c)

payable to the Nigerian Stock Exchange; and (d) payable to the Central Securities Clearing

System pursuant to the Value Added Tax (Exemption of Commissions on Stock Exchange

Transactions) Order of 2014 (“the Order”) ceased to apply on July 24, 2019. The Order

was issued by Dr. Ngozi Okonjo-Iweala, the then Coordinating Minister for the Economy

and Honourable Minister of Finance, in line with Section 38 of the Value Added Tax Act

(VATA) which empowers the Minister to amend, vary or modify the list of exempt items

contained in the First Schedule to the VATA.

The Order was aimed at increasing investor activities in the Nigerian capital market as well

as to stimulate economic development. The exemption of stock exchange transactions

from VAT resulted in a significant reduction in transaction charges for investors in the

capital market. The Order also reduced the compliance cost for stockbrokers who by the

exemption were not required to account and remit VAT on capital market transactions.

THE VALUE ADDED TAX

(EXEMPTION OF COMMISSIONS

ON STOCK EXCHANGE

TRANSACTIONS) ORDER OF 2014

REACHED ITS NATURAL END

12

FIRS SUSPENSION OF THE

APPLICATION OF LIEN ON

CUSTOMERS’ BANK ACCOUNT

By a letter dated 15th February 2019, the FIRS informed all the banks in Nigeria of the

temporary suspension of the lien placed on customers’ bank accounts for a period of 30

(thirty) days effective from the date of the letter. In the letter, the FIRS stated that the

suspension was as a result of a large number of taxpayers visiting the FIRS office for

reconciliation, and also the inconvenience caused to taxpayers.

The FIRS in the last 2 (two) years has been exercising the power of lien and substitution

on taxpayers’ bank accounts pursuant to Section 49 of Companies Income Tax Act (CITA)

and Section 31 of the Federal Inland Revenue Service Establishment Act 2007 (FIRSEA).

The CITA and FIRSEA provide that the FIRS may by notice in writing, appoint any person

to be the agent of a taxable person where such person is in possession of any money

belonging to the taxpayer, and where such agent fails to comply, the tax due shall be

recoverable from such agent. As will be examined under the judicial development segment

of this Report, the manner in which this power has been exercised by the FIRS has been

held by the court as being outside the ambit of the law.

…the FIRS stated that the

suspension was as a result of a

large number of taxpayers visiting

the FIRS office for reconciliation,

and also as a result of the

inconvenience caused to

taxpayers.

13

PUBLIC NOTICE ON DEDUCTION

AT SOURCE OF WITHHOLDING

TAX/ VAT ON COMPENSATION

PAID TO AGENTS, DEALERS,

DISTRIBUTORS AND RETAILERS BY

PRINCIPAL COMPANIES.

commission and other trade

incentives earned by

distributors/dealers will be

subjected to WHT and VAT”.

The FIRS, by a notice[4], gave directives and guidance to taxpayers on Withholding Tax

(WHT) and VAT deductible on compensation/commission due to distributors/dealers

and/or agents.[5] By the notice, the FIRS noted that some companies do not deduct

WHT/VAT from the compensation and incentives paid to their distributors, which it said is

contrary to the provisions of the Companies Income Tax (Rates, Etc. Deduction at Source

(Withholding Tax) Regulations S. 1 10 1997 (the Regulation), and Paragraph 3.8 of

Federal Inland Revenue Service Information Circular No 2006/02 of February 2006 (the

Circular) which states that “commission and other trade incentives earned by

distributors/dealers will be subjected to WHT and VAT”.

14

4. Published in the Daily trust newspaper publication dated 14.08.19 5. The Notice was particularly directed to the Fast-Moving Consumer Goods companies

Commissions are generally rewards received by agents in an agency relationship for

services rendered by the agents to their principal. Where agents receive a commission for

services rendered or sales made on behalf of the principal, there is no doubt that VAT

applies on such commission and the principal would have an obligation to deduct WHT on

the commission payable to the agent. While the principal records such commission as

expense in its books, the commission received by the agent will constitute income in the

books of the agent.

It should be noted that trade incentives are income in the books of the customers who

receive them, and therefore taxable. However, the practicability of the application of VAT

and WHT on some of these incentives by the companies may be difficult. Taking discount

coupon as an example, where a discount coupon is issued as an incentive in a sale

transaction, International Financial Reporting Standard (IFRS) 15 provides that the entity

is considered to have sold two things: (a) the goods or services; and (b) the right to a free

or discounted good or service in the future. In recognising the applicable revenue in the

books of the entity, IFRS 15 provides for the allocation of the stand-alone price of the

items sold and the value of the applicable benefit as a percentage of the actual amount

received from the customer for the goods (in essence, the actual amount received from

the customer remains the turnover of the company, while the actual unit price of the

goods or services is reduced to accommodate the trade incentives). It becomes difficult in

this type of situation to determine the applicable VAT and WHT on this benefit to

customer, especially where such customers do not take the option of the discount coupon

in the future.

15

FIRS CIRCULAR ON THE

CLAIM OF TAX TREATY

BENEFITS IN NIGERIA

This Tax Treaty

Benefit Circular was

issued pursuant to

Sections 45 and

46 of the CITA and

similar provisions in

other tax laws.

16

The FIRS by its circular dated 4th December 2019 (the Tax Treaty Benefit

Circular) laid down rules and guidance on the application of treaty

benefits in Nigeria. This Tax Treaty Benefit Circular was issued pursuant

to Sections 45 and 46 of the CITA and similar provisions in other tax

laws.

any taxpayer (resident and

non-resident) who wishes to

claim treaty benefits must

complete the certificate of

residence form which is to be

endorsed by the FIRS where

the tax payer is a Nigerian

resident, or the tax authority

of the country of residence of

the taxpayer where such tax

payer is non-resident.

the certificate of residence and

a formal application to claim

treaty benefits must be

submitted to the Executive

Chairman of the FIRS through

the Director, Tax policy and

Advisory.

Notably, Nigeria has subsisting treaties with the following countries: Italy (Air and

shipping transport agreement only), United Kingdom, Belgium, Pakistan, Czech, Slovakia,

France, Netherland, Romania, Canada, South Africa, China, Philippines, Singapore and

Spain.

only residents of Nigeria and

other treaty countries can

claim treaty benefits.

the reduced WHT rates in the

treaty for passive income will

only be applicable where

payment is made to non-

residents and the payment is

not connected to the

permanent establishment that

the non-resident has in

Nigeria.

the beneficial owner of the

income must be resident in the

treaty partner country.

Key provisions to be noted in the circular are as follows;

17

treaty benefits will only be

granted in the following

instances; (i) the taxpayer is

liable to tax in the treaty

country in which it is resident;

(ii) the income in question is

not liable to tax in Nigeria; (iii)

the benefit sought is covered

by the treaty, and not

specifically exempted; and (iv)

the benefit is claimed within

the stipulated time (not later

than two years after the year

of assessment).

the availability of mutual

agreement procedures where

the tax treaties are interpreted

by competent authorities in a

manner not in line with the

provisions and intendment of

the law.

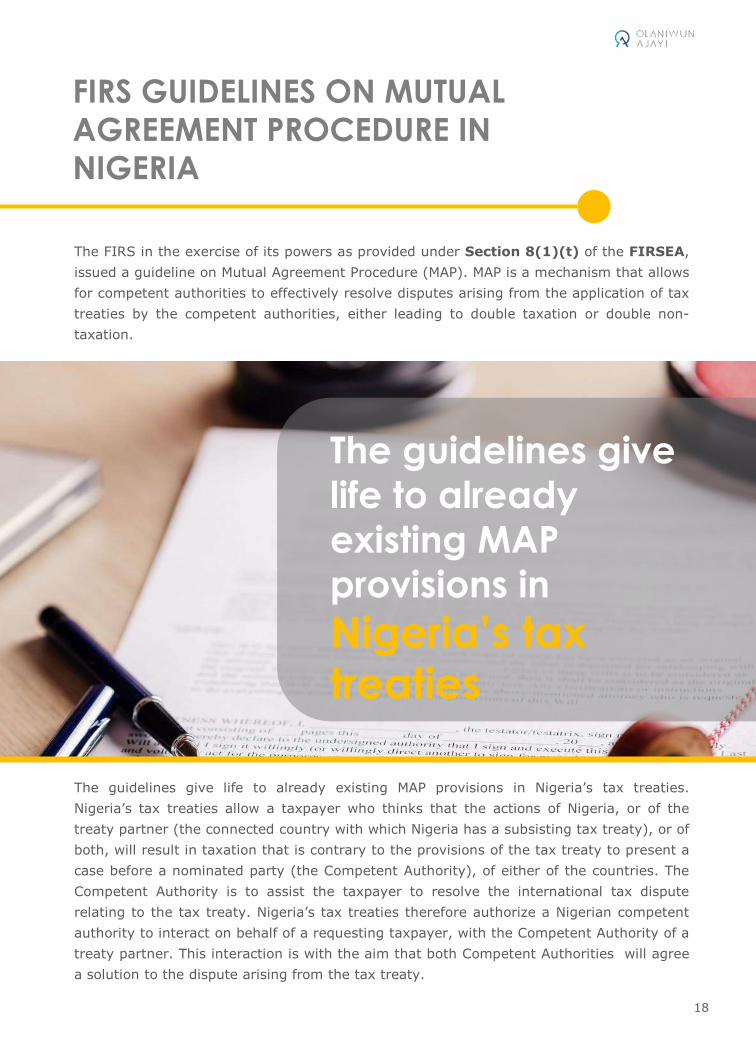

The FIRS in the exercise of its powers as provided under Section 8(1)(t) of the FIRSEA,

issued a guideline on Mutual Agreement Procedure (MAP). MAP is a mechanism that allows

for competent authorities to effectively resolve disputes arising from the application of tax

treaties by the competent authorities, either leading to double taxation or double non-

taxation.

The guidelines give

life to already

existing MAP

provisions in

Nigeria’s tax

treaties

The guidelines give life to already existing MAP provisions in Nigeria’s tax treaties.

Nigeria’s tax treaties allow a taxpayer who thinks that the actions of Nigeria, or of the

treaty partner (the connected country with which Nigeria has a subsisting tax treaty), or of

both, will result in taxation that is contrary to the provisions of the tax treaty to present a

case before a nominated party (the Competent Authority), of either of the countries. The

Competent Authority is to assist the taxpayer to resolve the international tax dispute

relating to the tax treaty. Nigeria’s tax treaties therefore authorize a Nigerian competent

authority to interact on behalf of a requesting taxpayer, with the Competent Authority of a

treaty partner. This interaction is with the aim that both Competent Authorities will agree

a solution to the dispute arising from the tax treaty.

FIRS GUIDELINES ON MUTUAL

AGREEMENT PROCEDURE IN

NIGERIA

18

By a public notice, the FIRS communicated the establishment of a non-resident tax office.

Non-resident persons are now required to submit every return, enquiry or correspondence

to the Non-Resident Persons Tax Office (NRPTO) located at 17B Awolowo Road, Ikoyi

Lagos.

The notice aims at devoting more attention to non-resident persons operating in Nigeria

and empowering the NRPTO to handle all the tax affairs of such persons. Pursuant to the

notice, once a determination is made that a taxable non-resident person is liable to tax in

Nigeria under the extant law, all interface which would have hitherto been done by FIRS

shall be undertaken by the NRPTO, a specialized unit of the FIRS. This will allow for a

quicker and potentially more effective system given that the NRPTO will be a specialized

office dedicated to the needs of non-resident taxpayers.

All non-resident taxpayers liable to tax in Nigeria are advised to deal with the NRPTO for all

purposes relating to their tax affairs in Nigeria. This will prevent administrative issues that

may be associated with non-compliance. It is also important to ensure that compliance

requirements are strictly adhered to given that the tax authority will be paying closer

attention to the activities of non-residents deriving income or profit in Nigeria.

ESTABLISHMENT OF NON-

RESIDENT PERSONS TAX

OFFICE BY THE FIRS

The notice clearly delineates its

scope of application and

defines non-resident persons to

include foreign companies as

defined in the CITA or an

individual (who is resident

outside Nigeria and derives

income or profits from Nigeria)

as defined in the PITA.

19

Central bank of Nigeria (CBN) by the introduction of E-Form NXP (which replaces hard

copy forms) has introduced automation into the export process. The CBN by its

circular dated 28 October 2019, requires exporters to log on to the trade monitoring

system website to acquire its NXP form. As a condition precedent to processing the form,

all exporters are to obtain a valid TIN from the FIRS or the Joint Tax Board (JTB).

While automation is good for the sector, the requirement of a TIN would also help the FIRS

to monitor tax compliance of exporters and ensure that relevant taxes are collected.

The CBN requires

exporters to log on to

the trade monitoring

system website to

acquire its NXP form.

THE INTRODUCTION

OF E-FORM ‘NXP’

20

LAGOS STATE INTERNAL

REVENUE SERVICE PUBLIC

NOTICE ON TAX IDENTIFICATION

NUMBER INTEGRATION

The LIRS released a public notice on its plans to merge its LASG-EBS Taxpayers

Identification Digit (PID) with the nationwide Tax Identification Number (TIN). The

notice further states that the Bank Verification Number (BVN) of taxpayers will be

required before the LASG-EBS platform can be accessed for all tax transactions such

as registration and creation of Payer ID for new taxpayers, payment of taxes and

validation of taxpayer’s profile.

Self-employed individuals were required to provide their BVN to the

LIRS in order to assist in the creation of PID. It also requires

corporate organisations to ensure that their employees who qualify for

tax clearance card include their BVN in individual e-TCC forms. Finally,

the notice assures taxpayers of the safety, security and strict

confidentiality of all data/information in the custody of the LIRS.

LASG-EBS is the Lagos State Government Electronic Banking System

which is a new tax administration system of the LIRS. LASG-EBS PID

is the unique code issued by the LIRS to taxpayers that are resident in

Lagos, while the TIN is a unique code issued by the FIRS to individuals

and corporate entities. The aim of the notice and the automation

initiative is to further guarantee the ease of doing business in Nigeria

as well as prevent multiplicity of taxes in Nigeria.

21

LIRS PUBLIC NOTICE APPOINTING

PAYERS OF CAPITAL SUMS INCLUSIVE

OF EMPLOYERS AS COLLECTING

AGENTS OF CAPITAL GAINS TAX

At the start of the year 2019, the LIRS issued a public notice pursuant to Section 50 of

the Personal Income Tax Act (PITA), and Sections 6, 11 and 43 of Capital Gains Tax Act

(CGTA) appointing all employers who pay “capital sums” (which is defined under the

CGTA as money or money’s worth that is paid to taxpayers in respect of transactions that

fall within the meaning of “disposal of assets”) as compensation for loss of office to

residents of Lagos State, as collecting agents of Capital Gains Tax (CGT) for the LIRS.

As agents of the LIRS, the employer in making such payment is required to withhold and

remit CGT on the “capital sum” paid to the employee. The notice requires the employer to

file annual returns together with statements showing all recipients of “capital sums” in a

prescribed format.

It is evident that the LIRS through this public notice aims to ensure that compensation for

loss of office is accounted for by employers who are already in the tax net as well as

prevents taxpayers who are unlikely to file tax returns, from holding on to the full “capital

sum” received. With the Finance Act 2019, the threshold for the tax base for compensation

for loss of office has been increased from NGN 10,000 (ten thousand naira) to NGN

10,000,000 (ten million naira).

The threshold for the tax base for

compensation for loss of office

has been increased from:

NGN 10,000 to

NGN 10,000,000

22

23

PART II

T H E N A T I O N A L L O T T E R Y A C T 2 0 1 5 ( A S

A M E N D E D )

LEGISLATIVE DEVELOPMENTS

The Nigerian National Assembly (NASS) passed the National Lottery (Amendment) Act

2017 (the Lottery Amendment Act), into law, amending the National Lottery Act, 2015

and introducing a new tax regime for lottery businesses in Nigeria. Prior to the passage of

this amendment Act by the NASS, lottery companies had been liable to pay taxes in line

with the provisions of the CITA. However, with the Lottery Amendment Act, the following

changes were introduced, thus heralding the new tax regime for lottery businesses in

Nigeria.

In addition to the long list of judicial and executive actions in the tax space, the legislature

also made giant strides in making the year 2019 a remarkable one. The year 2019 saw the

introduction of the following tax legislations:

24

25

6. Section 35B of the National Lottery Amendment Act, 2017. 7. Section 35B (2) of the National Lottery Amendment Act, 2017.

Imposition of Lottery Tax:

Section 35A of the Lottery Amendment Act imposes and charges a tax to be

known as the Lottery Companies Incomes Tax (the Lottery Tax) at a rate of 7%

on the net proceeds of the licensee at the end of each assessment year. The

Lottery Amendment Act requires that the lottery operator conduct a self-

assessment in every year of assessment and forward evidence of payment of the

computed taxes to the FIRS. The Lottery Amendment Act further provides that

where the FIRS is not satisfied with an assessment submitted by the licensee,

the FIRS may according to best of its judgement, assess the licensee to further

tax.

Deductible Expenses:

The Lottery Amendment Act6 makes provisions for deductible expenses for tax

purposes. These deductible expenses include: the 40% of the proceeds of the

lottery paid by the holder of a licence other than a fixed odds game licence into

the prize fund, and the 20% of the net proceeds of the lottery paid by the holder

of a fixed-odd licence to the Fixed-odd Prize Fund.

Tax Neutrality

The Lottery Amendment Act7 further provides that the prize fund shall be tax

neutral, and therefore all moneys accruing in, payments made from, and

transactions relating to the prize fund shall be exempted from all forms of taxes,

levies, duties, charges or imposition however described.

Tax Exemption

Where a licensee has been assessed for Lottery Tax in any year, the licensee

shall be exempted from the provisions of the CITA and the VATA. As such, lottery

companies will no longer be expected to charge, impose, and remit CIT and VAT

to the FIRS. It however remains to be seen whether the companies will be

required to file relevant CIT and VAT returns on a “nil” basis monthly.

Any payment made by a licensee prior to the commencement of the Lottery

Amendment Act under any existing arrangement with and accepted by the

National Lottery Commission (the Commission) is legal, valid, and binding on the

Commission, and shall be deemed to be the full and final settlement of any

liability or obligation of a licensee under the Lottery Amendment Act.7 As such,

licensees will not be required to pay any outstanding sums or undertake any

further obligations to the Commission which were due prior to the enactment of

the Lottery Amendment Act.

The provisions exempting the lottery industry from the application of VAT has settled the

controversies surrounding the “VATability” of takings by lottery operators. It is expected

that the FIRS will give guidance to lottery companies as to the operation of the Lottery

Amendment Act, and in the meantime, lottery companies are enjoined to comply with the

provisions of the new regime.

Prior Payments

26 7. Section 35D of the National Lottery (Amendment) Act 2017

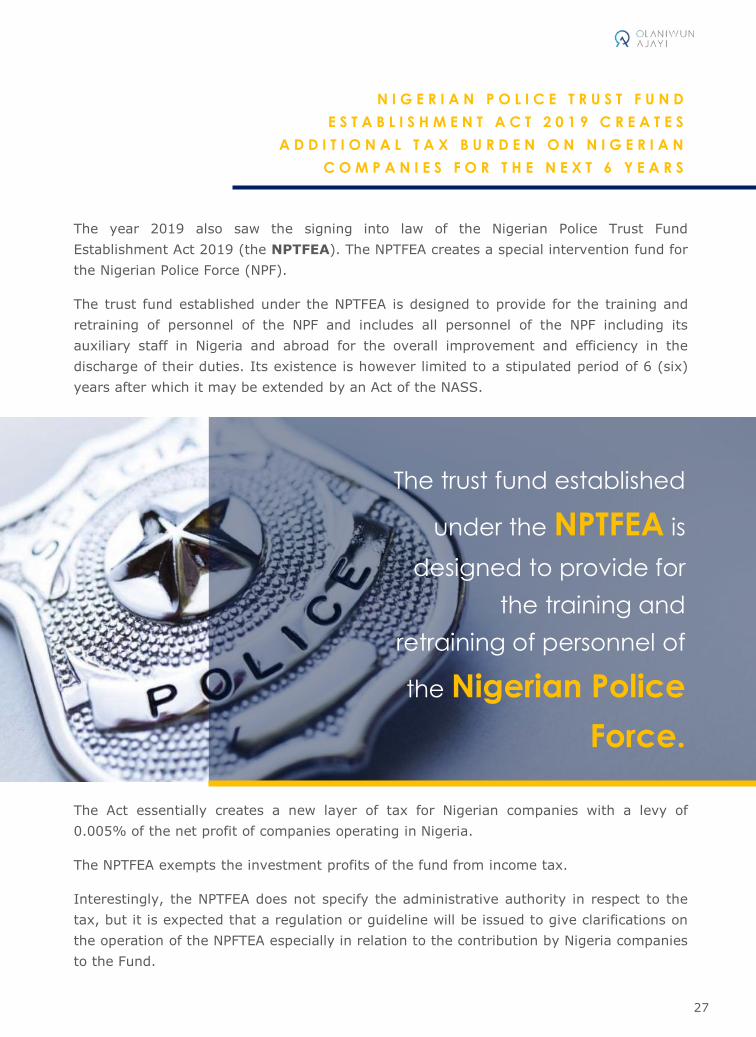

The year 2019 also saw the signing into law of the Nigerian Police Trust Fund

Establishment Act 2019 (the NPTFEA). The NPTFEA creates a special intervention fund for

the Nigerian Police Force (NPF).

The trust fund established under the NPTFEA is designed to provide for the training and

retraining of personnel of the NPF and includes all personnel of the NPF including its

auxiliary staff in Nigeria and abroad for the overall improvement and efficiency in the

discharge of their duties. Its existence is however limited to a stipulated period of 6 (six)

years after which it may be extended by an Act of the NASS.

The Act essentially creates a new layer of tax for Nigerian companies with a levy of

0.005% of the net profit of companies operating in Nigeria.

The NPTFEA exempts the investment profits of the fund from income tax.

Interestingly, the NPTFEA does not specify the administrative authority in respect to the

tax, but it is expected that a regulation or guideline will be issued to give clarifications on

the operation of the NPFTEA especially in relation to the contribution by Nigeria companies

to the Fund.

N I G E R I A N P O L I C E T R U S T F U N D

E S T A B L I S H M E N T A C T 2 0 1 9 C R E A T E S

A D D I T I O N A L T A X B U R D E N O N N I G E R I A N

C O M P A N I E S F O R T H E N E X T 6 Y E A R S

27

The trust fund established

under the NPTFEA is

designed to provide for

the training and

retraining of personnel of

the Nigerian Police

Force.

The Deep Offshore and Inland Basin Production Sharing Contract (Amendment) Act

(DOIBPSCAA) was signed into law in December 2019.

The DOIBPSCAA introduced the following amendments: (a) inclusion of a price-based

royalty (Royalty by Price) which requires the contractor to pay additional amounts as

royalty based on increasing prices of crude oil and condensates; (b) inclusion of periodic

mandatory review provisions for the Production Sharing Contracts (PSCs); and (c)

inclusion of offences and penalty clauses to deter persons from flouting the provisions of

the DOIBPSCAA.

The Fixed Royalty Rates in the DOIBPSCAA replaced the graduating/incremental royalty

rates based on water depth as formerly applicable under the Deep Offshore and Inland

Basin Production Sharing Contract Act (the Old Act), with a flat royalty rate of 10% for

deep offshore (any water depth beyond 200m), while frontier/inland basins would attract

7.5% royalty rates. In addition to this, a royalty payment based on the applicable price of

crude oil, condensates and natural gas will be applicable where the price of crude oil

exceeds USD20 (twenty dollars) per barrel. The graduated royalty rates are as follows;

D E E P O F F S H O R E A N D I N L A N D B A S I N

P R O D U C T I O N S H A R I N G C O N T R A C T

( A M E N D M E N T ) A C T 2 0 1 9

28

$0 to $20 per barrel,

royalty of 0%

Above $20 and up to

$60, royalty of 2.5%

Above $60 and up to

$100, royalty at 4%

Above $100 and up to

$150, royalty at 8%

Above $150, royalty at

10%

In a bid to ensure periodic reviews of PSCs, the DOIBPSCAA also imposes an obligation on the

Minister of Petroleum Resources (the Minister) to cause the Nigerian National Petroleum

Corporation (NNPC) to call for a review of PSCs every 8 (eight) years. The periodic review

obligation imposed on the Minister/NNPC in the DOIBPSCAA, is aimed at substituting section 16

of the Old Act, which mandated a periodic review of the Old Act by the legislature.

The Act imposes a penalty of not less than

₦500,000,000.00

(Five Hundred Million Naira) or imprisonment for a

period not less than 5 years or both upon conviction

by a court of competent authority, for failure to

carry out any obligation imposed by the Act.

29

…a royalty payment based

on the applicable price of

crude oil, condensates and

natural gas will be applicable

where the price of

crude oil exceeds

USD20 per barrel.

The last quarter of 2019 witnessed the introduction of the Finance Bill to the National

Assembly, which was subsequently assented by the President Muhammadu Buhari on

January 13, 2020 and became the Finance Act, 2019 (the Act). The passing of the Act is

part of government’s efforts to continually improve the ease of doing business in Nigeria

with the aim of increasing the contribution of non-oil revenue to the government.

The Act made sweeping changes to certain provisions of the existing tax laws. We have

identified below the various tax laws that were impact by the Act as well as their

implications.

Capital Gains Tax

Act Cap C1, LFN

2004

The Stamp

Duties Act Cap

S8, LFN 2004

Customs and Excise

Tariff Etc.

(Consolidation) Act,

Cap C49

Personal Income

Tax Act Cap P8,

LFN 2004 (as

amended)

Petroleum

Profit Tax Act

The Companies

Income Tax Act,

Cap. C21, LFN

2004

Value Added

Tax Act, Cap

V1, LFN 2004

T H E F I N A N C E A C T 2 0 1 9

30

1 C O M P A N I E S I N C O M E T A X A C T

A. EXPANSION OF THE DEFINITION OF INTEREST AND DIVIDEND

The Act has expanded the definition of interest and dividend to include compensating

payments between a lender and a borrower in a regulated security lending transaction.

The Act further provides that where securities are transferred from a lender and subsequently

returned by the borrower in a regulated securities lending transaction, such transfer shall not

be deemed to be a disposal. These dividend and interest received shall be deemed to be

franked investment income in the hands of the lender or borrower and will not be liable to

further tax.

B. WIDER BASE FOR THE TAXATION OF NON-RESIDENT COMPANIES IN NIGERIA.

The Act introduces the concept of “significant economic presence” to counter the challenges

of the digital economy by including in section 13 of the CITA activities relating to electronic

commerce to the extent that the non-resident company has significant economic presence in

Nigeria. This provision also extends to non-resident companies carrying on technical,

management, professional and consultancy services in Nigeria, provided those companies

have significant economic presence in Nigeria. Significant economic presence is required to

be determined by the Minister.

C. EXCESS DIVIDEND TAX PROVISIONS

The double tax implications of the application of the former section 19 of the CITA no longer

exists under the new regime. Under the former regime, excess dividend tax will be

applicable under the following instances;

i. where the dividend is paid out of retained earnings of company that has previously been

subjected to tax under the CITA, PPTA or the CGTA;

ii. where dividend is paid from profit of a company enjoying pioneer status incentive;

iii. where the dividend is paid from the profits of companies that are regarded as franked

investment income under the CITA;

iv. distribution made by a Real Estate Investment Company (REIC) to its shareholders from

rental income, and dividend income received on behalf of those shareholders.

31

Now, companies are free to pay dividend from their retained earnings, and would not be

subjected to excess dividend tax as long as the retained earnings has suffered income tax in

previous years or the retained earnings are from tax exempt income.

D. DIVIDEND DISTRIBUTED BY UNIT TRUST:

Dividend distributed by unit trust are now exempted from WHT.

E. EXEMPTION OF DIVIDEND AND RENTAL INCOME RECEIVED BY REIC:

Dividends and rental income received by REIC on behalf of its shareholders shall be

exempted from income tax provided that 75% of the dividend and rental income is

distributed and such distribution is made within 12 (twelve) months of the financial year.

F. EXEMPTION OF SMALL COMPANIES FROM INCOME TAX

Companies with turnover less than NGN 25,000,000 (Twenty-Five million Naira) in any year

of assessment shall not be liable to income tax. Also, companies with turnover of more than

NGN 25,000,000 (Twenty-Five million Naira) but less than NGN 100,000,000 (Hundred

Million Naira) will be taxed at the rate of 20%, while companies with turnover of more than

NGN 100,000,000 (Hundred Million Naira) will be taxed at the rate of 30%. This has

introduced a progressive or graduated income tax rate for companies in Nigeria.

G. DIVIDEND DISTRIBUTED BY SMALL COMPANIES IN THE MANUFACTURING

SECTOR

Dividend received from small companies in the manufacturing sector in the first 5 years of

commencement of business is exempt from tax.

H. TERMINATION OF THE COMMENCEMENT AND CESSATION RULE

The double taxation effect of commencement and cessation rule has been removed by the

new amendment. The rule has been replaced with a new basis for assessing new companies

and ceasing companies to tax, such that the profit of the same accounting period is not taxed

twice.

32

I. TAX PLANNING IN COMPANY RE-ORGANISATION

The gap in the CITA which allows companies to carry out fictitious tax neutral business

reorganisation has been closed. Under the CITA, unrelated companies will usually execute a

two-layer reorganization to enjoy the tax neutral considerations which applies to related

parties under section 29(9) of the CITA. Under the Act, related party companies undergoing a

reorganisation must have been so related for at least 365 days, and upon the reorganisation,

the acquiring party will lose the tax neutral advantage in the reorganisation if it makes

subsequent disposal within 365 days after the date of transaction.

J. LIMITATION ON CURRENT INCENTIVES ENJOYED BY COMPANIES ENGAGED

IN GAS UTILIZATION ACTIVITIES

Gas utilization companies that have enjoyed tax relief under the CITA will not be allowed to

enjoy the same relief under the Industrial Development and Income Tax Relief Act (IDITRA).

K. ADJUSTMENT ON THE APPLICATION OF MINIMUM TAX

i. Minimum tax is now a flat rate of 0.5% of turnover.

ii. Minimum tax will no longer apply to companies with turnover of NGN25,000,000 (Twenty-Five million) and below.

iii. Exemption from minimum tax for certain companies no longer exists.

L. INDEFINITE CARRY FORWARD OF LOSSES FOR INSURANCE COMPANIES

Restriction on the carry forward of losses for insurance companies has been removed. Before

now, insurance companies could only carry forward their losses for a limited period of 4

(four) years. Insurance companies can now carry losses indefinitely.

M. INTRODUCTION OF THIN CAPITALISATION RULES

Thin capitalisation rules have been introduced to Nigerian tax laws. This rule limits the

amount of related party interest payable to foreign lenders. The rule under the Act has

limited deductible foreign interest to a connected party to 30% of earnings before interest,

tax, depreciation and amortization (EBITDA).

33

Excess interest not deductible can be carried forward for a maximum period of 5 years only.

The provision on thin capitalisation shall not apply to Nigerian subsidiaries of foreign

companies engaged in the business of banking and insurance. The penalty for non-

compliance with this provision is 10% of any adjustment made by the FIRS and interest at

the CBN monetary rate plus a spread to be determined by the minister. This is in addition to

the effect that such adjustment shall not be allowed as deductible expense.

N. OTHER LIMITATIONS ON EXPENSE DEDUCTIONS

In addition to the conditions under the thin capitalisation rules, all expenses qualifying for

deduction must conform to the provisions of the Transfer Pricing Regulations 2018. Also,

expenses incurred in generating tax exempt income will not be allowed as deductible

expenses.

O. WITHHOLDING TAX ON INTERIM DIVIDEND

The complex provisions on interim dividends tax which are impractical to implement have

been removed from the CITA. Companies are now to withhold tax when dividends are paid.

P. BONUS FOR PROMPT FILING OF TAX RETURNS

The Act introduces a bonus of 2% for medium sized companies and 1% for any other

company where any such company pays its tax 90 (ninety) days before the due date.

Q. INVESTMENT TAX CREDIT ON OBSOLETE PLANT AND MACHINERY

Investment tax credit given for investment in replacing obsolete plant and machinery no

longer exists in the CITA.

R. WHT EXEMPTION ON QUALIFYING FOREIGN LOAN

There is no longer a 100% WHT exemption for foreign loans which meets the 7 years

repayment conditions. Maximum exemption for WHT is now pegged at 70%. The table below

shows the difference between the current regime and the new regime on tax exemptions for

foreign lenders.

34

Below 2 years

Moratorium Period:

Nil CITA

Exemption

Exemption under the

Act

0

0

2-4 years

5-7 years

Above 7 years

Moratorium Period:

Not less than 12 months

Moratorium Period:

Not less than 18 months

Moratorium Period:

Not less than 2 years

CITA Exemption

Exemption under the

Act

40%

10%

CITA Exemption

Exemption under the

Act

70%

40%

CITA Exemption

Exemption under the

Act

100%

70%

S. SPECIAL PROVISIONS FOR INSURANCE COMPANIES

Life Insurance

i. The discriminating minimum tax provision, which requires that life insurance companies

must have 20% of their gross income available for taxation after deduction of all

expenses has been abolished. Minimum tax for life insurance companies is now 0.5% of

gross income.

ii. Investment income of life insurance companies is now limited to returns on

shareholders’ fund. This means that revenue realised from investing subscriber’s

premium will not be taxable in the current year.

Non-life insurance

i. Reserve for unexpired risk is now to be calculated on a time apportionment basis. Under

the CITA, it is calculated as 45% and 25% of total premium for general and marine

insurance respectively.

ii. Under the CITA, tax deductible expense is capped at 25% of total premium. The Act has

eliminated this restriction.

iii. Minimum tax for non-life insurance companies is now 0.5% of its gross premium.

35

A. INCREASE IN VAT RATE.

VAT has been increased from 5% to 7.5%. The implication of this is that there will be

increase in the value of goods and services by 2.5%.

B. VAT EXEMPTION IN GROUP RE-ORGANISATIONS.

As a matter of practice, special application is required to be made to the FIRS to enjoy

VAT exemptions on the value of assets transferred in a re-organisation between related

parties. The Act has explicitly exempted the application of VAT on the transfer of assets in

a re-organisation, provided the re-organisation is between related parties who have been

so related for a period of not less than 365 days before the date of the transaction.

C. INCREASE IN PENALTIES FOR NON-REGISTRATION AND FILING OF RETURNS.

Penalties for non-registration for VAT has been increased to NGN50,000 (Fifty Thousand

Naira) in the first month of default, and NGN25,000(Twenty Five Thousand Naira) (for

each month in which the default continues). The same penalty also applies for failure to

submit VAT returns.

D. INCREASE IN PENALTY FOR NON-REMITTANCE OF VAT.

The penalty for failure to remit VAT has been increased from 5% to 10% plus interest at the

prevailing commercial rate.

E. VAT EXEMPTION FOR MICRO-FINANCE BANKS.

The services of micro-finance banks are now exempted from VAT under the Act. Previously,

the VATA did not specifically exempt micro-finance banks from VAT. However, the FIRS

accorded micro finance banks the same treatment as community banks whose services were

exempted from VAT under the VATA.

2 V A L U E A D D E D T A X A M E N D M E N T S A N D I M P L I C A T I O N

36

F. VAT ON TUITION

Tuition relating to nursery, primary, secondary and tertiary education are now to be

exempted from VAT.

G. THRESHOLD FOR VAT REGISTRATION

Only companies with turnover above NGN25,000,000 (Twenty-Five Million Naira) are

required to account for VAT.

H. CASH COLLECTION BASIS FOR ACCOUNTING FOR VAT

VAT is to be accounted based on the input VAT paid and the output VAT collected. What is

remitted should be the difference between the output collected and the input paid, and where

the input exceeds the output in any month, the excess should be utilized by the tax-payer in

the subsequent month.

I. NON-RESIDENT TO INCLUDE TAX ON ITS INVOICE

A non-resident entity carrying on business in Nigeria is required to register for VAT using the

address of the person with whom it has a subsisting contract. It is also required to include

VAT in its invoice for supply of vatable services. The recipient of the service is required to

withhold and remit VAT directly to the FIRS in the currency of the transaction.

J. CHANGES TO THE INTERPRETATION SECTION OF THE VATA

i. Exported Services: the Act defines exported services to mean “a service

rendered within or outside Nigeria by a person resident in Nigeria to a person

resident outside Nigeria provided, however, that a service provided to the fixed

base or permanent establishment of a non-resident person shall not qualify as

exported service”.

ii. Definition of goods: the Act provides that “Goods mean all forms of tangible

properties that are moveable at the point of supply but does not include money

or securities; and any intangible product, asset or property over which a person

has ownership or rights, or from which he derives benefits, and which can be

transferred from one person to the other excluding interest in land”.

37

iii. Definition of services: Services means anything other than goods, money or securities

which is supplied excluding services provided under a contract of employment .

iv. Commencement of business: For the purpose of registration for VAT, the Act defines

commencement as the date in which the business carries out its first transaction. This is the

day which is earlier between, when the entity begins to market or advertise its product in

Nigeria, or the date it obtains its operating license, or the date it executes its first trading

contract.

v. Definition of Basic Food: Basic food has always been exempted from VAT. However, the

term “basic food” was not defined under the VATA, and this has been a point of conflict over

the years between the FIRS and taxpayers. The Act has now defined basic food items to

include bread, cooking oil, flour, vegetables and additives.

38

3 P E T R O L E U M P R O F I T T A X A C T

Dividends paid by upstream oil and gas companies

will now be liable to WHT.

39

4 P E R S O N A L I N C O M E T A X A C T

Below are some of the changes to the PITA:

a) The reliefs that were generally believed to have been inadvertently retained after

the 2011 amendment to the PITA have finally been deleted by the Act. These

reliefs include personal allowance, children allowance, dependent allowance,

alimony etc.

b) Contribution to pension no longer requires the approval of the Board of the IRS.

c) There is a new requirement for banks to ensure that persons intending to open

bank account for the purpose of business operations must provide a “Tax

Identification Number” as a precondition for opening the bank account.

d) Recognition of electronic mail as a mode for the delivery of tax objection to the

tax authorities.

e) Functions previously carried out by the Joint Tax Board will now be carried out

by the FIRS.

40

40

5 C A P I T A L G A I N S T A X A C T

Exemption of Capital Gains Tax (CGT) in mergers and take overs has been

restricted to those that take place between related parties. Such related parties

must have been so related for a period of 365 days before the merger, and the

acquiring company shall not make a subsequent disposal of the assets arising

from the takeover within 365 days after the transaction is concluded. If these

conditions are not followed, the companies shall be treated as if they never

qualified for the concession from the date of the initial reorganisation.

The threshold for the payment of CGT in relation to compensation for loss of

office paid by an employer has been increased. Before now, compensation for

loss of office was not be a chargeable gain except the compensation is more

than NGN10,000 (Ten thousand Naira) in any year of assessment. This

threshold has been increased to NGN10,000,000 (Ten million Naira).

41

6 S T A M P D U T I E S A C T

The changes to the Stamp Duties Act (SDA) are as follows;

a) The Act now recognizes electronic stamping in addition to the other previously

accepted modes of stamping.

b) The amount of receipt that will trigger the imposition of stamp duties has been

increased from NGN 4 (Four Naira) to NGN 10,000 (Ten Thousand Naira) by the

Act, and the amount of stamp duties chargeable shall be N50 (Fifty Naira). This

has settled the controversy as to the legal basis for the imposition of stamp

duties of N50 (Fifty Naira) on every N1,000 (One Thousand Naira) previously

charged by the banks on the instructions of the CBN.

42

7 C U S T O M S A N D E X C I S E T A R I F F ( C O N S O L I D A T I O N ) A C T

43

The Act provides a level

playing field for locally

manufactured excisable goods

and imported excisable goods

by including imported

excisable goods as chargeable

to excise duties.

C O N C L U S I O N

The changes made by the Act are laudable. However, it is still important for the FIRS and

the Minister of Finance to give further clarification on the many ambiguous provisions in

the Act.

PART III

44

Through the course of 2019, the Nigerian Courts and the Tax Appeal Tribunal (TAT or “the

Tribunal”) delivered several judgements/rulings, some of which triggered a lot of debate

as to their alignment with the provisions of the Nigerian tax laws.

We have examined below, some of these notable judicial decisions during the year under

review.

JUDICIAL DEVELOPMENTS

The Nigerian Courts/Tax

Appeal Tribunal

delivered several

judgements/rulings,

some of which triggered

a lot of debate as to

their alignment with the

provisions of the

Nigerian tax laws.

45

In January 2019, the Federal High Court (FHC) held that the FIRS cannot assess taxpayers

to tax on a turnover basis, based on the value of the property.

Theodak challenged the powers of the FIRS to assess the company to tax based on the

value of the company’s property and deeming the value of the property as the turnover of

the company for the purpose of tax assessment. The issue for determination before the

court was “whether the FIRS acted within the provisions of Section 30(1)(a) of CITA in

assessing the Company to Income tax”. The court held that the FIRS cannot assess

taxpayers to tax on a turnover basis where the turnover is premised on the value of the

taxpayer’s property.

In arriving at its decision, the court defined turnover in Section 30(1)(a) of CITA as the

aggregate income of a business received in the normal business activities, and held that

the value of the property of the company does not constitute the company’s business

income.

The court declared the assessment to be unfair and unacceptable in law. The court further

stated that it would have taken a different view if the company was involved in the

business of selling properties. In such circumstances, it would have been appropriate for

the FIRS to tax the company on the value of the property, especially where such company

refuses to file its annual tax returns within the time stipulated by law.

BEST OF JUDGEMENT

ASSESSMENT BASED ON THE

VALUE OF PROPERTY

INAPPROPRIATE:

46

T H E O D A K N I G E R I A L I M I T E D v . F E D E R A L

I N L A N D R E V E N U E S E R V I C E

The TAT on 14th May 2019, held in Shell v.

LIRS that penalties and interest will accrue

from the date of the failure by the

taxpayer to remit outstanding taxes and

will become payable when the tax

assessments become final and conclusive.

47

INTEREST AND PENALTIES TO ACCRUE

FROM DATE OF FAILURE TO REMIT

TAXES:

S H E L L N I G E R I A E X P L O R A T I O N A N D

P R O D U C T I O N C O M P A N Y L I M I T E D v . L A G O S

S T A T E I N T E R N A L R E V E N U E S E R V I C E

The LIRS issued a demand notice on Shell Nigeria Exploration and Production Company

Limited (the Appellant or Shell) imposing interest and penalties for 2007 to 2012 years of

assessment. At the time the appeal was instituted, parties had reconciled on all the

grounds of objection save for the interest and penalties imposed for the outstanding taxes

for 2007 – 2012 years of assessment. The issues before the tribunal were;

The TAT agreed with the position of the Appellant that an assessment validly objected to

cannot under the law be final and conclusive, and interest and penalties ought not to

accrue. Notwithstanding this, the TAT held that interest and penalties should accrue from

the date in which the Appellant failed to deduct the relevant taxes, and upon the

assessment being final and conclusive, taxpayers will be required to pay interest and

penalties on outstanding tax liabilities.

48

whether the demand notice issued on the

Appellant was final and conclusive.

whether the Appellant is

liable to pay interest and

penalties on unremitted

WHT tax and Pay As You

Earn (PAYE) for 2007 –

2012 years of assessment.

whether interest and

penalties are applicable to

an assessment which is not

final and conclusive.

N E X E N P E T R O L E U M N I G E R I A L I M I T E D v .

L A G O S S T A T E I N T E R N A L R E V E N U E S E R V I C E

The TAT on 18th June 2019, held that: (a) the import of section 10(4) of the Pensions

Reform Act, 2014 (PRA 2014), is that for Voluntary Pension Contributions (VPC) to be tax

exempt, the VPC must not be withdrawn by the employee before the expiration of 5 (five)

years from the date the VPC was made; and (b) the onus solely rests on the LIRS to

ascertain whether a VPC has been withdrawn by an employee within the said period.

Upon the conduct of a tax audit by the LIRS for the 2013 and 2014 years of assessment,

additional tax liability was imposed on Nexen Petroleum Nigeria Limited (Nexen) on the

basis that withdrawals had been made from the VPC of Nexen employees. Dissatisfied with

the assessments, Nexen filed its Notice of Appeal before the TAT, against the LIRS’ Notice

of Refusal to Amend (NORA). The TAT in applying section 10(4) of the PRA 2014 and

other provisions held that all pension contributions, whether statutorily prescribed or

voluntarily contributed is expected to reduce the taxable income of the employees. It

further held that the PRA 2014 clearly exempts all classes of pension contributions and

does not limit the tax deductibility of pension contributions to the minimum 18%

prescribed by law. It held that the LIRS could not impose any additional liability on Nexen

based on the withdrawal by employees from their VPC.

The TAT expressed that the employees of Nexen withdrawing their VPC before the

expiration of 5 (five) years amounted to a gross violation of the extant provisions of the

PRA 2014, but agreed that Nexen could not have been privy to the dealings and

transactions of its employees making withdrawals before the required time.

VOLUNTARY PENSION

CONTRIBUTION IS TAX EXEMPT IF

NOT WITHDRAWN FOR A PERIOD

OF NOT LESS THAN 5 YEARS FROM

THE DAY OF CONTRIBUTION:

49

The Court of Appeal (CoA) on 24th June 2019, upheld the decisions of the TAT and the

FHC, to the effect that: (a) the supply of satellite network bandwidth capacities by a non-

resident company to the Vodacom Business Nigeria Limited (Vodacom) in Nigeria

constituted a VATable transaction; (b) that the Vodacom is liable to remit VAT even in the

absence of VAT in the invoice of the Non-resident Company; and (c) the provisions of the

VATA are in line with the Reverse Charge principle.

The CoA held that the integral construction of Sections 2, 10 and 46 of the VATA leads to

the indubitable conclusion that the transaction between Vodacom and the non-resident

foreign company is one for which the services were supplied in Nigeria, making it VATable.

It stated that the phrase “carries on” means “to continue doing something”. The foreign

company was thus held to carry on business in Nigeria as it continued doing business

within the meaning of Section 10(1) of the VATA.

The CoA also held that Section 10(2) of the VATA requires a person to whom goods or

services are supplied to in Nigeria to remit VAT. This obligation imposed under section

10(2) is similar to the Reverse Charge principle which requires that the buyer of goods or

services assumes the responsibility of paying the VAT.

V O D A C O M B U S I N E S S N I G E R I A L I M I T E D v . F E D E R A L I N L A N D R E V E N U E S E R V I C E

50

REVERSE CHARGE OF VAT

APPLICABLE IN NIGERIA:

The TAT ruled in favour of Nigerian Breweries that gratuities are tax exempt by virtue of

the Finance (Miscellaneous Taxation provisions) No. 3 Decree of 1996, which deleted

gratuities from the list of income chargeable to tax under the PITA.

The TAT sitting in Enugu on 20th June 2019 held that gratuities are not subject to income

tax. In this case, the Abia State Board of Internal Revenue (ABIR) assessed Nigerian

Breweries Plc (Nigerian Breweries) to additional taxes consisting of PAYE, which included

taxes on gratuities paid to the retired employees of Nigerian Breweries.

…gratuities

are not

subject to

income

tax…

N I G E R I A N B R E W E R I E S P L C v . A B I A S T A T E B O A R D O F I N T E R N A L R E V E N U E & O R S .

51

GRATUITIES NOT LIABLE TO

INCOME TAX IN NIGERIA:

The TAT on July 5, 2019 held that where a company pays dividends that exceeds its total

profit in any year of assessment, that dividend shall constitute its total profit for that year,

and it is immaterial if such dividend was paid from the retained earnings of the company

which has suffered income tax in previous years.

In this case, Actis Africa Nigeria Limited (Actis) paid dividends in 2014 out of its retained

profits to the tune of approximately N49,000,000 (forty nine million naira) even though no

profits had been declared. In relying on Section 19 of the CITA, the FIRS subjected the

dividends paid out in 2014 by Actis to Companies Income Tax (CIT).

The TAT in making its determination relied on the FHC and CoA decisions in Oando v.

FIRS, and concluded that Actis is liable to pay CIT on dividend paid out.

The provisions on excess dividend tax has been amended by the Finance Act 2019 to deal

with incidences of double taxation.

Strict

application of

Section 19

of the CITA

A C T I S A F R I C A N I G E R I A L I M I T E D v .

F E D E R A L I N L A N D R E V E N U E S E R V I C E

52

STRICT APPLICATION OF SECTION

19 OF THE CITA- EXCESS

DIVIDEND TAX:

The TAT sitting in Lagos restated the

principles on excess dividend tax as

provided in section 19 of the CITA.

The TAT held that the provision of

section 19 does not concern itself

with the source or origin of the

dividend paid. Rather, Section 19 is

applicable once the dividend

declared and paid is higher than

total profits in any year of

assessment.

U N I T E D C A P I T A L P L C v . F E D E R A L I N L A N D

R E V E N U E S E R V I C E

53

EXCESS

DIVIDEND TAX:

I N F I N I T Y T R U S T M O R T G A G E B A N K P L C v .

F E D E R A L I N L A N D R E V E N U E S E R V I C E

The TAT sitting in Abuja on 19th June 2019 held that mortgage institutions are not liable

to pay VAT on services rendered within the scope of their business. FIRS had issued a VAT

assessment notice on Infinity Trust Mortgage Bank Plc (the Bank). The Bank however,

objected to the notice on the basis that its services as a mortgage institution were exempt

from VAT. This narrow question as to whether the bank being a mortgage institution was

liable to VAT was submitted to the TAT for determination. The TAT held that mortgage

banks are not liable to remit VAT on its services to the extent that its services are

performed within the general scope of mortgage businesses under the Mortgage

Institutions Act and regulations/guidelines issued thereto.

The TAT also held that the FIRS had failed to prove that the bank’s income was generated

in the course of engaging in non-mortgage banking services, and discharged the FIRS’ VAT

Assessments on the bank.

The TAT held that

mortgage banks are

not liable to remit VAT

on its services.

54

MORTGAGE BANKS NOT

LIABLE TO VAT:

The CoA held that failure to obtain the National Office For Technology Acquisition And

Promotion (NOTAP) approval on a contract that requires NOTAP registration, does not

render the contract illegal and void. This is a reversal of the earlier FHC decision in the

same case in which the FHC held that the failure to obtain NOTAP approval (on a

registrable contract) rendered the contract illegal and void, and that payment could not be

made on an unregistered contract.

The matter arose from an investigation conducted by the Financial Reporting Council of

Nigeria (FRCN) in relation to a technology contract for software expensed by Stanbic IBTC

Holdings Plc (Stanbic) in its audited financial statements for 2013 and 2014 payable to its

South African parent company. The CoA confirmed that NOTAP’s scope does not cover

contracts for the exportation of technology out of Nigeria as held by the FHC. In addition,

the CoA held that failure to register an agreement under section 7 of the NOTAP Act is not

criminal and does not render the agreement void. However, payment of consideration with

respect to the agreement through the Ministry of Finance, Central Bank of Nigeria (CBN) or

any commercial bank will not be permitted.

Subsequent to this judgement, and via a public notice dated 5th August 2019, the FRCN

revoked the provisions of Rule 4 of the FRCN rules which requires that where an expense

requires regulatory approval, such expense shall not be recognized until such regulatory

approval is obtained. The implication of this judgement and the subsequent action of the

FRCN is that the approval of regulatory authorities will no longer be required for recognition

of business expenses.

the Court of Appeal held that failure to register an agreement under section 7 of the NOTAP Act is not criminal and does not render the agreement void.

S T A N B I C I B T C H O L D I N G S P L C v . F I N A N C I A L

R E P O R T I N G C O U N C I L O F N I G E R I A

55

NON-REGISTRATION OF

TECHNOLOGY TRANSFER

AGREEMENT WITH NATIONAL

OFFICE FOR TECHNOLOGY

ACQUISITION AND PROMOTION

DOES NOT RENDER THE AGREEMENT

VOID AND UNENFORCEABLE:

On 21st August 2019, the TAT gave its decision on the appeal of Polaris Bank Limited

(Polaris Bank) against a series of demand notices issued by the ABIR. Polaris bank had

approached the TAT contesting the demand notice of the ABIR, and the ABIR’s refusal to

follow statutory prescribed procedures on the finality of a tax assessment.

Several issues were raised and determined by the TAT, including (a) the propriety of

compelling payment of tax when assessment is not final and conclusive; (b) the power to

impose development and business premises levy based on the Taxes and Levies Act

(TLA); and (c) entitlement of the tax authority to issue interest and penalty in the instant

case.

On the first issue, the TAT restated the principle of fair hearing as enshrined in our laws

and especially as provided in sections 58 and 68(2) of the PITA which deal with the

procedure for the determination of tax objections and appeals, confirming that the ABIR

had failed to follow the outlined procedure under the law.

On the second issue, the TAT held that the TLA cannot be the statutory basis for the

collection of development and business premises levy. The TAT stated that the Abia state

government must specifically enact its laws to collect these taxes. The TAT took a more

dynamic approach to the last issue by stating clearly that labeling an exercise a tax

investigation does not protect its outcome against the statute of limitation. The court

further held that interest and penalties cannot be imposed on an undisputed tax liability

that is statute barred.

The decision of the TAT is merely another

leaf in a very uniformly coloured tree. It

has not attempted to change the law,

nor has it done anything outside the

ordinary. It merely restates the law on

the issues raised.

P O L A R I S B A N K L I M I T E D v . A B I A S T A T E

B O A R D O F I N T E R N A L R E V E N U E

56

LIMITING THE WHIMS AND CAPRICES

OF THE TAX AUTHORITIES:

The TAT in the case above considered the issue of VAT exemption on marketing and

distribution services rendered by a Nigerian entity to its South African related party in

relation to investment products sold to its Nigerian customers.

Following a desk review of Allan Gray Investment Management Nigeria Limited (Allan

Gray)’s tax returns by the FIRS, a notice of additional assessment with respect to its VAT

liabilities was issued. Upon receipt of the Notice of Assessment, Allan Grey objected on the

basis that the revenue for the relevant period was derived from its marketing and

distribution services rendered to its non-resident related party and hence exempted from

VAT. After several reconciliation meetings, the FIRS issued to Allan Grey a NORA. Allan

Grey rejected the assessments and subsequently filed this action on the ground that the nil

returns filed for the relevant period were valid as there was no obligation to remit VAT since

its services are exempted from VAT under Part II of the First Schedule to the VATA.

After considering the argument of parties, the TAT considered the following issues for

determination; (a) whether the activities of an agent to a foreign principal are exempted

from VAT being exported services; and (b) the impact of the Double Taxation Agreement

(“DTA”) between Nigeria and South Africa in determining whether an entity has a taxable

presence in Nigeria.

On the first issue, the TAT concluded that the non-resident related party was marketing and

distributing its financial services to its clients in Nigeria through Allan Grey, and therefore

carrying on business in Nigeria through it. On the issue of exported services, the TAT

emphasized that the definition of exported services requires the services to be performed

outside Nigeria, and the location of the consumer of the service is immaterial.

With respect to the second issue, the TAT did not refer to any provision of the Nigeria-

South Africa DTA in addressing this issue. Instead, the TAT relied on the agency principle by

referring to the marketing and distribution agreement executed between Allan Grey and the

non-resident related party as a basis for establishing a principal-agent relationship. The TAT

concluded that where an agent enters into a contract on behalf of third parties, such agent

would be responsible for any tax liability under such contract particularly where the

principal is a foreign entity.

A L L A N G R A Y I N V E S T M E N T M A N A G E M E N T

N I G E R I A L I M I T E D v . F E D E R A L I N L A N D

R E V E N U E S E R V I C E :

57

LIABILITY OF NON-RESIDENT

ENTITIES TO VAT IN NIGERIA:

The reasoning of the TAT does not align with the provisions of the VATA especially on the

definition of exported services. The TAT emphasized the importance of the location where

the services are carried out rather than the location of the recipient.

Section 46 of the VATA defines exported services as services performed by a Nigerian

resident or a Nigerian Company to a person outside Nigeria. While the TAT may hold that

the activities of Allan Grey may have constituted a fixed base for the non-resident related

party, and therefore may not qualify as exported service, it is erroneous to conclude that

an activity qualifying for exported service must have been carried out outside Nigeria. This

is a sharp deviation from the principles established by the CoA recognizing the destination

principle with respect to imported services.