TeamLease Employment Outlook Report Quarter-23, July-September 2012 A comprehensive and in-depth analysis of Employment and Business Outlook for the forthcoming quarter. Includes statistics for 8 cities and 8 sectors, literature review insights and depth-survey findings inTouch analytics http://be-in-touch.com

Transcript

TeamLease Employment Outlook Report Quarter-23, July-September 2012

A comprehensive and in-depth analysis of Employment and Business Outlook for the forthcoming quarter. Includes statistics for 8 cities and 8 sectors, literature review insights and depth-survey findings

inT

ou

ch an

alytics http://be-in-touch.com

Team

Leas

eEm

ploy

men

tOut

look

Repo

rt

1

Preface

The quarterly TeamLease Employment Outlook Report is a forward looking tool for human resource policy and decision makers, reflecting business sentiment for hiring across cities and sectors. The report carries a snapshot of business hiring sentiment for the immediate next three months with survey and analysis being carried out in the preceding quarter.

The Employment Outlook Survey spans eight industry sectors and eight cities across India. The survey covers small, medium and large companies across these sectors, studies attrition and employment trends, and gleans information on hiring sentiments, all this covering different locations, hierarchical levels and functional areas.

The current edition of the Employment Outlook Report revisits and validates the forecasts made in the immediate past reports, with the help of an extensive secondary research exercise. In addition to this, we have set out to invite thoughts on hiring and talent retention from respondents that go beyond hiring and business sentiment inputs we usually solicit from them.

With the most critical drivers that influence hiring being tracked quarter on quarter, the Employment Outlook Report is the only one of its kind seeking to deliver high impact hiring decision support to its stakeholders – Business & HR heads, Senior Management as well as industry policy makers.

Team

Leas

eEm

ploy

men

tOut

look

Repo

rt

2

Contents

1. Executive Summary 2. Project Objectives 3. Index definitions

3.1. Employment Outlook Index 3.2. Business Outlook Index

4. Employment Outlook 4.1. Net Employment Outlook 4.2. Net Employment Outlook Growth – by sector 4.3. Net Employment Outlook Growth – by city

5. Business Outlook 5.1. Net Business Outlook 5.2. Net Business Outlook Growth – by sector 5.3. Net Business Outlook Growth – by city

6. Hiring Intent 6.1. Hiring Intent by Location 6.2. Hiring Intent by Hierarchy 6.3. Hiring Intent by Functional Area

7. Other Trends 7.1. Employment Outlook Index – city-sector drilldown 7.2. Business Outlook Index – city-sector drilldown 7.3. Attrition trends by sector 7.4. Attrition trends by city

8. Annexure: Research Methodology 8.1. Sample Design 8.2. Respondent Selection 8.3. Data Collection 8.4. Secondary Sources

9. Sample Distribution 9.1. City-wise breakup 9.2. Business size-wise breakup

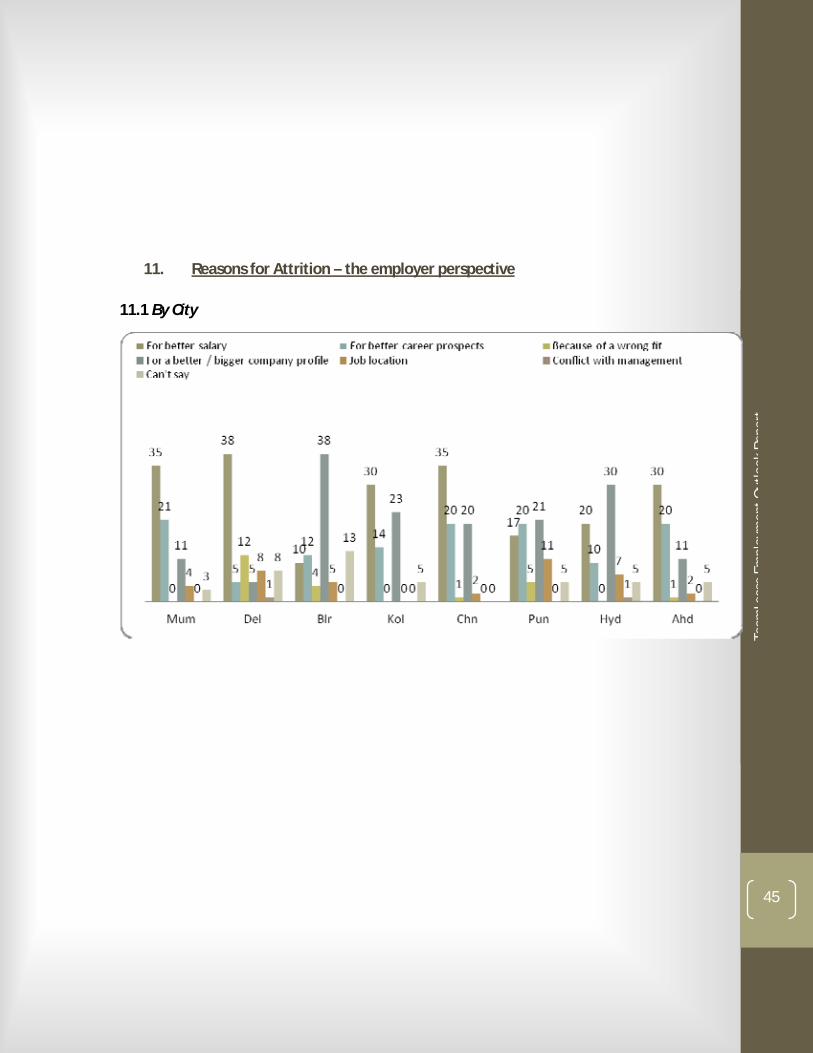

10. Literature Research findings – Business Growth trends 11. Reasons for Attrition – the employer perspective

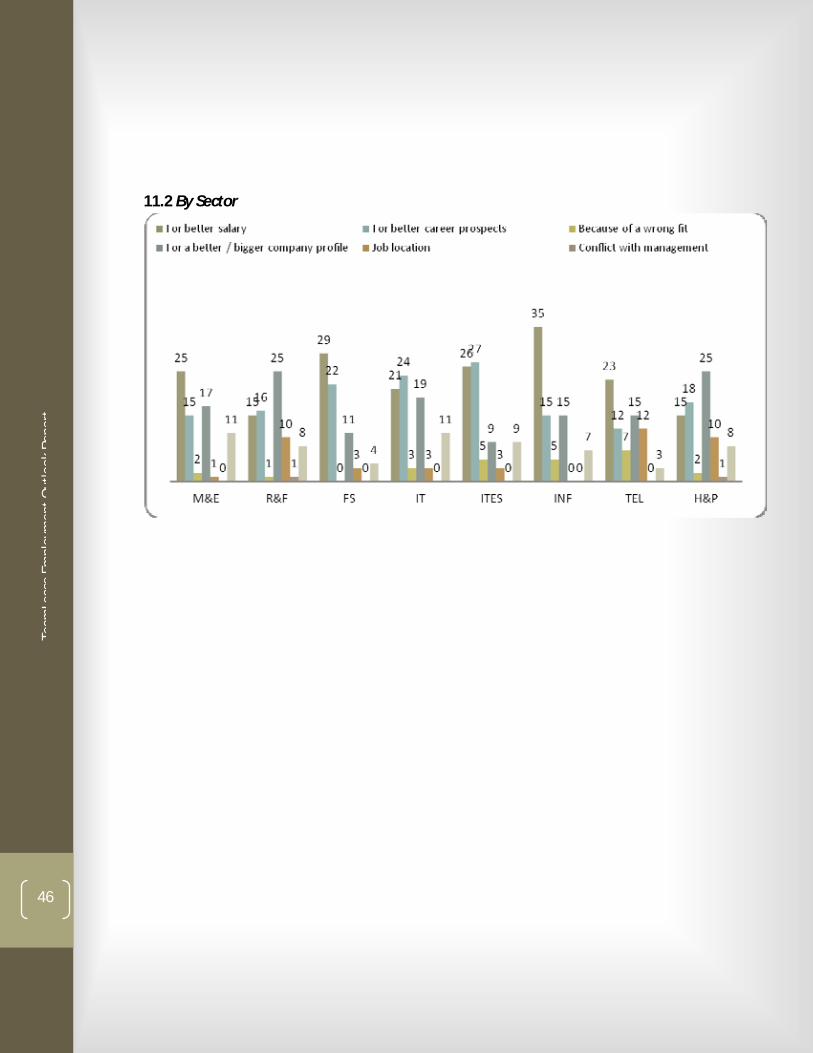

11.1. By city 11.2. By sector

Team

Leas

eEm

ploy

men

tOut

look

Repo

rt

3

Executive Summary Hiring sentiment continues to trend upwards in spite of the business sentiment

slipping. The Net Employment Outlook increments (by 1 point) for the third subsequent quarter this financial year and touches a high it had reached in the quarter ending July 2011. While hiring manages to stay up, the Net business Outlook rolls back by 2 pointsto +72- a low it had reached during the quarter, October-December 2011.

Manufacturing (+2 points), Infrastructure and Healthcare &Pharma (+1point each) are

reasons this quarter has seen steadfast employment sentiment. Similar Employment and Business Outlook trends are observed in Manufacturing and Infrastructure. Gloomy predictions for IT and ITES continue, with a dip of 1 & 2 points for employment outlook and a dip of 1 point each for business outlook respectively.

City wise Employment Outlook, likewise, fares better than its counterpart, Business

Outlook. Bangalore, Pune & Ahmedabad witness an increase of 1 point each in the employment outlook but post a flat trend in the business outlook. Both indexes decline by 1 pointfor Mumbai & Kolkata. Delhi, gains by 1 point in the employment outlook but loses as much in the business outlook. Chennai leads the business outlook, witnessing an increase of 2 points; however the index remains flat in the employment outlook.

While there’s not much to report for Geographical trends – with Metros continuing to

hog the limelight – hierarchical hiring preferences witness a huge upheaval. There is a steep increase in hiring for Middle level(+7 points) and a marginal increase for Senior level(+1 point). This, however, comes at the cost ofsignificant decline of 5 and 3 points each in hiring patterns for Entry and Junior levels.

Hard-to-wither optimism continues to hold sway with functional areas as well. Four out

of eight functional areas report an increase in hiring intent in the present quarter. Engineering, registers a significant increase of 4 points, IT and Sales and Marketing witness an incremental increase of 2 points. Laggards include Administration/HR/Office Service losing 3 points and others category declining by 2 points.

Our new literature research section includes analysis that shows up a fairly good match

between the forecasts and the actual trends for all sectors except one. The business growth analysis also reveals that our forecasts are almost in sync with the actual 4 out of 7 times across sectors for Q2 & Q3 of 2011-12.

Depth survey findings reveal a sense of uncertainty organizations have over acquiring the right talent and therefore making geographical preferences redundant for some, while most step on the gas even more, as far as retention measures go.

Team

Leas

eEm

ploy

men

tOut

look

Repo

rt

4

Project ObjectivesThe Employment Outlook Report aims at –

Providing forward looking estimates of hiring sentiment and thus enabling its users with a tool to make effective hiring / people decisions for the immediate next quarter.

Providing *Hiring Sentiment Intelligence* for different industry sectors, business sizes and geographies, as well as across hierarchical levels and functional areas.

Index Definitions Employment Outlook Index: The Employment Outlook Index is computed as the

difference in the proportion of respondents who report an increase in hiring needs and those who report a decline in hiring needs over the next three months.

Business Outlook Index: The Business Outlook Index is computed by subtracting the percentage respondents who say business in the next three months is likely to decrease from the percentage who say it will increase.

Team

Leas

eEm

ploy

men

tOut

look

Repo

rt

5

Team

Leas

eEm

ploy

men

tOut

look

Repo

rt

6

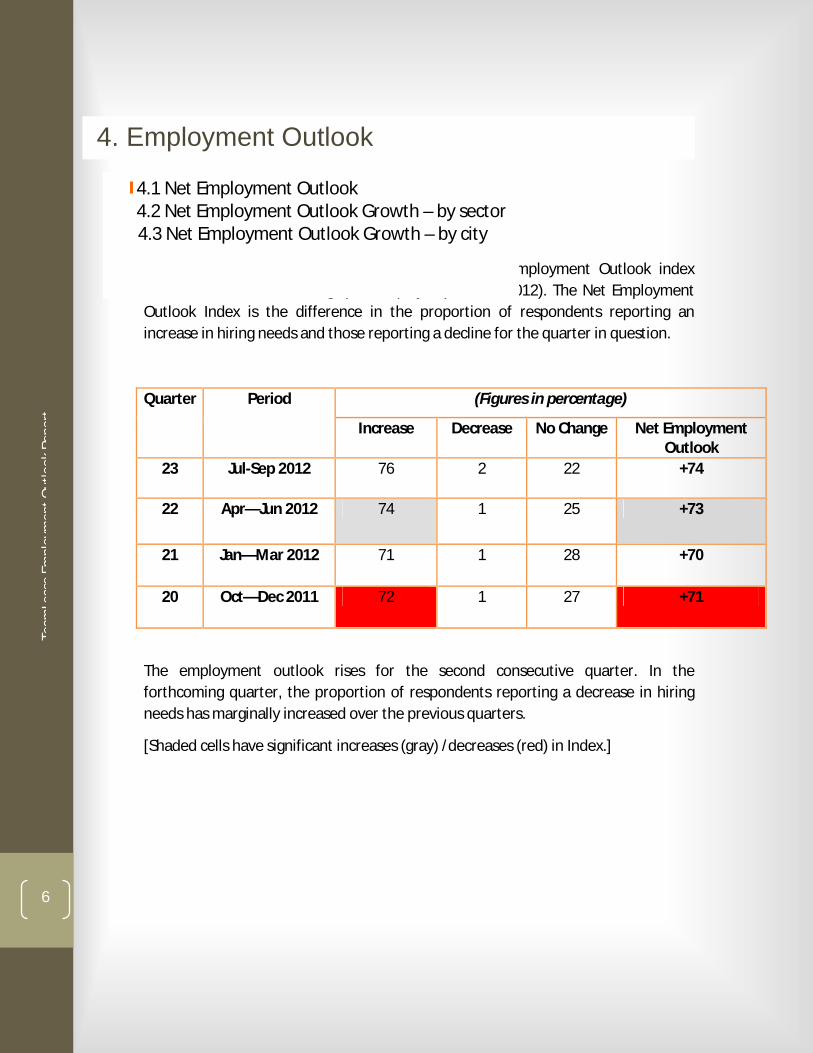

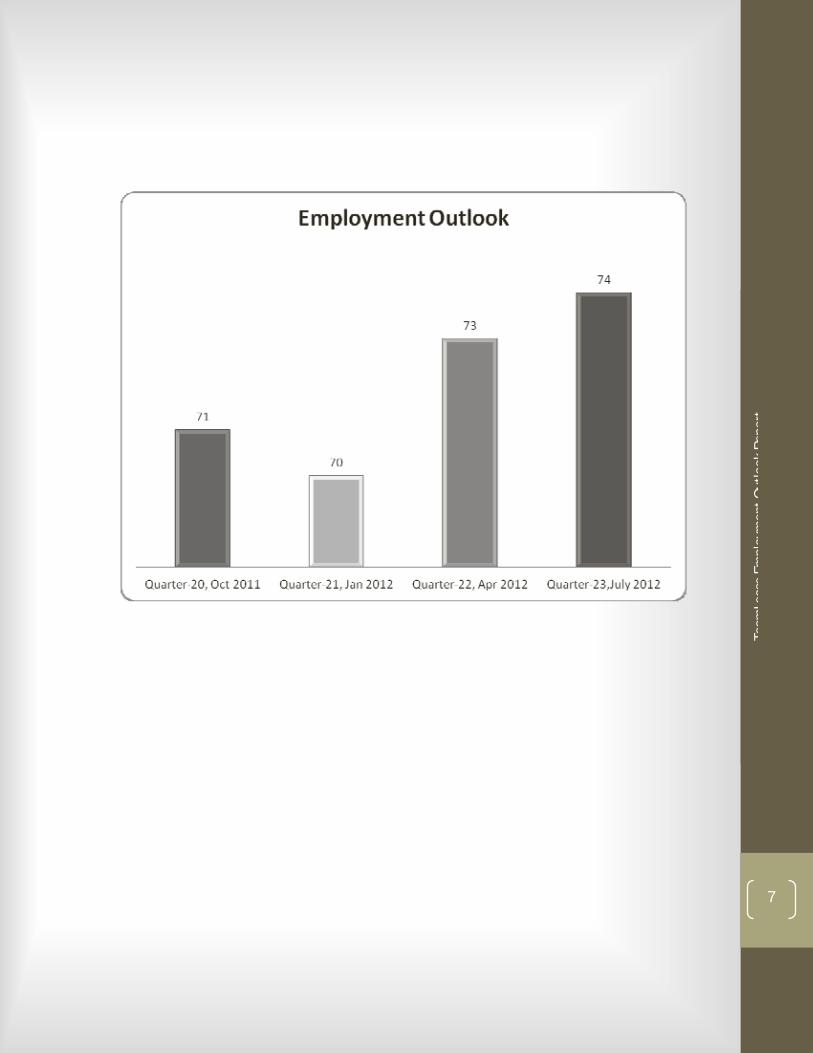

4.1 Net Employment Outlook

There is a 1 percentage point increase in the Net Employment Outlook index forecast for the forthcoming quarter (July-September 2012). The Net Employment Outlook Index is the difference in the proportion of respondents reporting an increase in hiring needs and those reporting a decline for the quarter in question.

(Figures in percentage) Quarter Period

Increase Decrease No Change Net Employment Outlook

23 Jul-Sep 2012 76 2 22 +74

22 Apr—Jun 2012 74 1 25 +73

21 Jan—Mar 2012 71 1 28 +70

20 Oct—Dec 2011 72 1 27 +71

The employment outlook rises for the second consecutive quarter. In the forthcoming quarter, the proportion of respondents reporting a decrease in hiring needs has marginally increased over the previous quarters.

[Shaded cells have significant increases (gray) /decreases (red) in Index.]

4. Employment Outlook

4.1 Net Employment Outlook4.2 Net Employment Outlook Growth – by sector

4.3 Net Employment Outlook Growth – by city

Team

Leas

eEm

ploy

men

tOut

look

Repo

rt

7

Team

Leas

eEm

ploy

men

tOut

look

Repo

rt

8

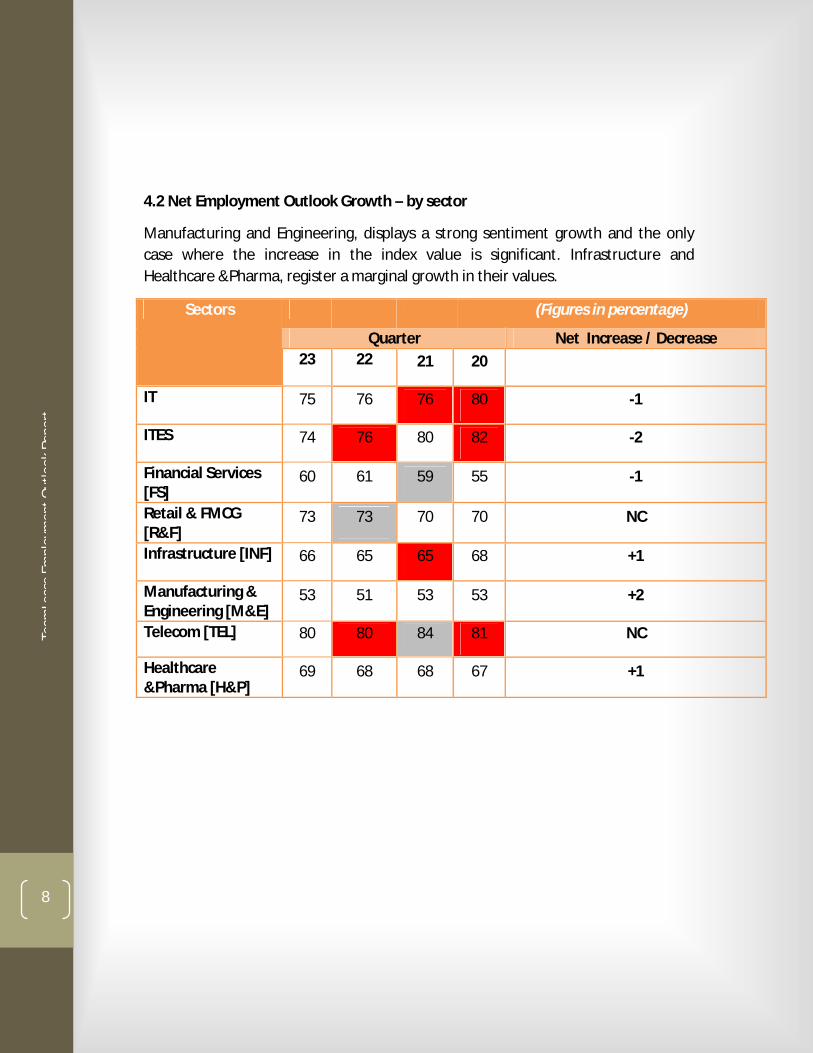

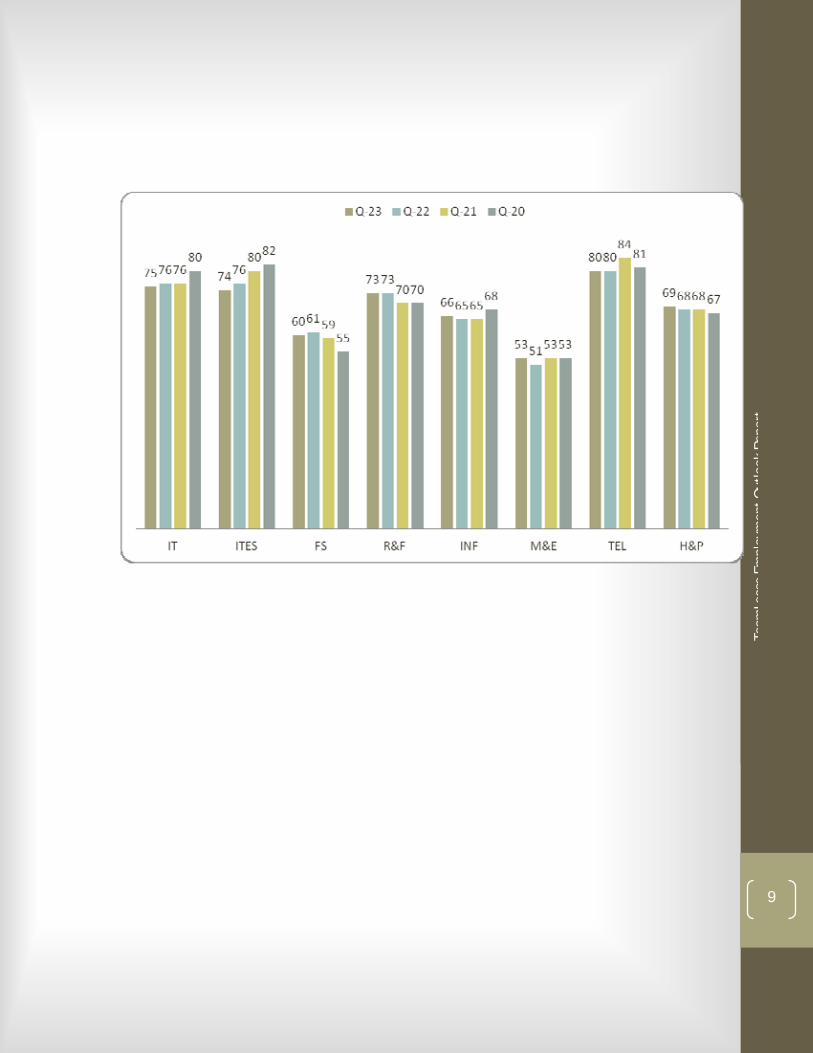

4.2 Net Employment Outlook Growth – by sector

Manufacturing and Engineering, displays a strong sentiment growth and the only case where the increase in the index value is significant. Infrastructure and Healthcare &Pharma, register a marginal growth in their values.

(Figures in percentage)

Quarter Net Increase / Decrease

Sectors

23 22 21 20

IT 75 76 76 80 -1

ITES 74 76 80 82 -2

Financial Services [FS]

60 61 59 55 -1

Retail & FMCG [R&F]

73 73 70 70 NC

Infrastructure [INF] 66 65 65 68 +1

Manufacturing & Engineering [M&E]

53 51 53 53 +2

Telecom [TEL] 80 80 84 81 NC

Healthcare &Pharma [H&P]

69 68 68 67 +1

Team

Leas

eEm

ploy

men

tOut

look

Repo

rt

9

Team

Leas

eEm

ploy

men

tOut

look

Repo

rt

10

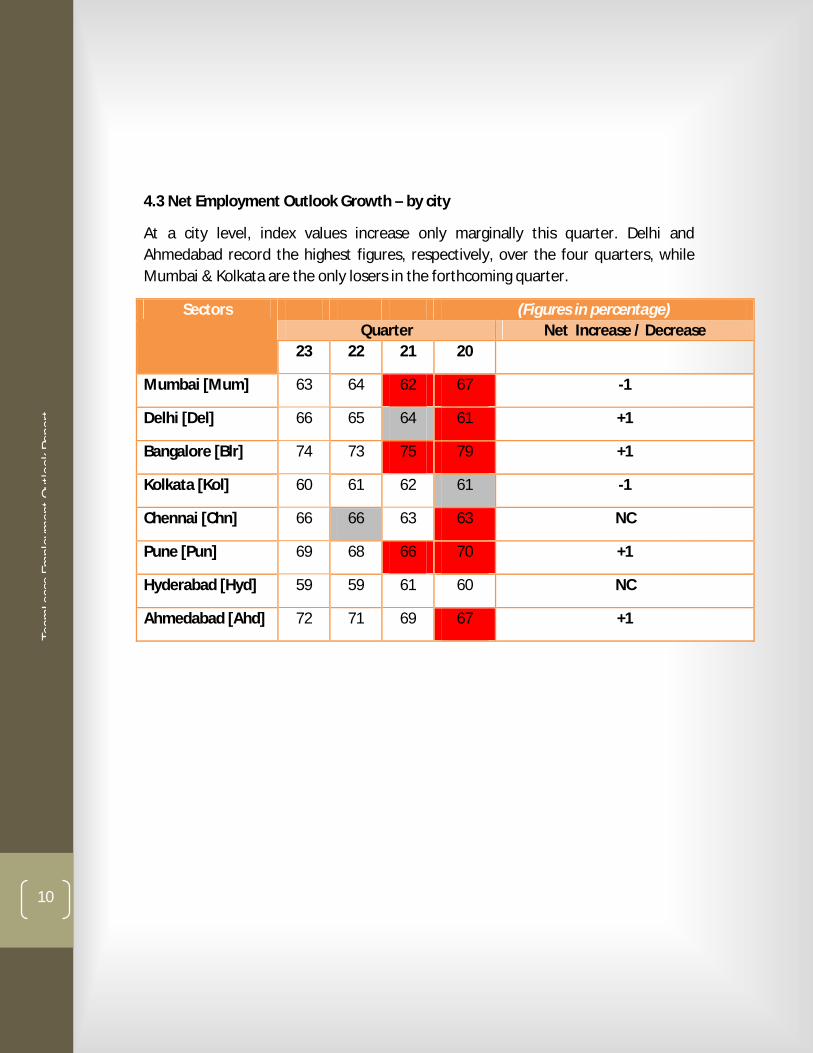

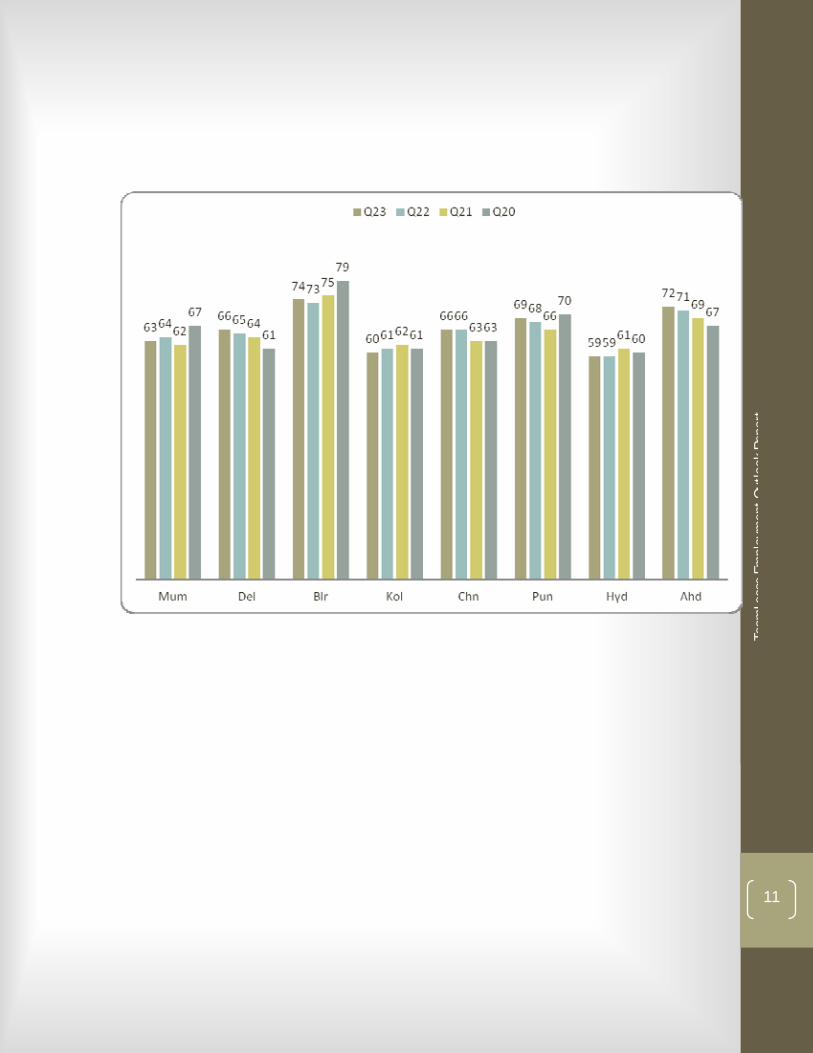

4.3 Net Employment Outlook Growth – by city

At a city level, index values increase only marginally this quarter. Delhi and Ahmedabad record the highest figures, respectively, over the four quarters, while Mumbai & Kolkata are the only losers in the forthcoming quarter.

(Figures in percentage) Quarter Net Increase / Decrease

Sectors

23 22 21 20

Mumbai [Mum] 63 64 62 67 -1

Delhi [Del] 66 65 64 61 +1

Bangalore [Blr] 74 73 75 79 +1

Kolkata [Kol] 60 61 62 61 -1

Chennai [Chn] 66 66 63 63 NC

Pune [Pun] 69 68 66 70 +1

Hyderabad [Hyd] 59 59 61 60 NC

Ahmedabad [Ahd] 72 71 69 67 +1

Team

Leas

eEm

ploy

men

tOut

look

Repo

rt

11

Team

Leas

eEm

ploy

men

tOut

look

Repo

rt

12

5. Business Outlook

5.1 Net Business Outlook5.2 Net Business Outlook Growth – by sector

5.3 Net Business Outlook Growth – by city

Team

Leas

eEm

ploy

men

tOut

look

Repo

rt

13

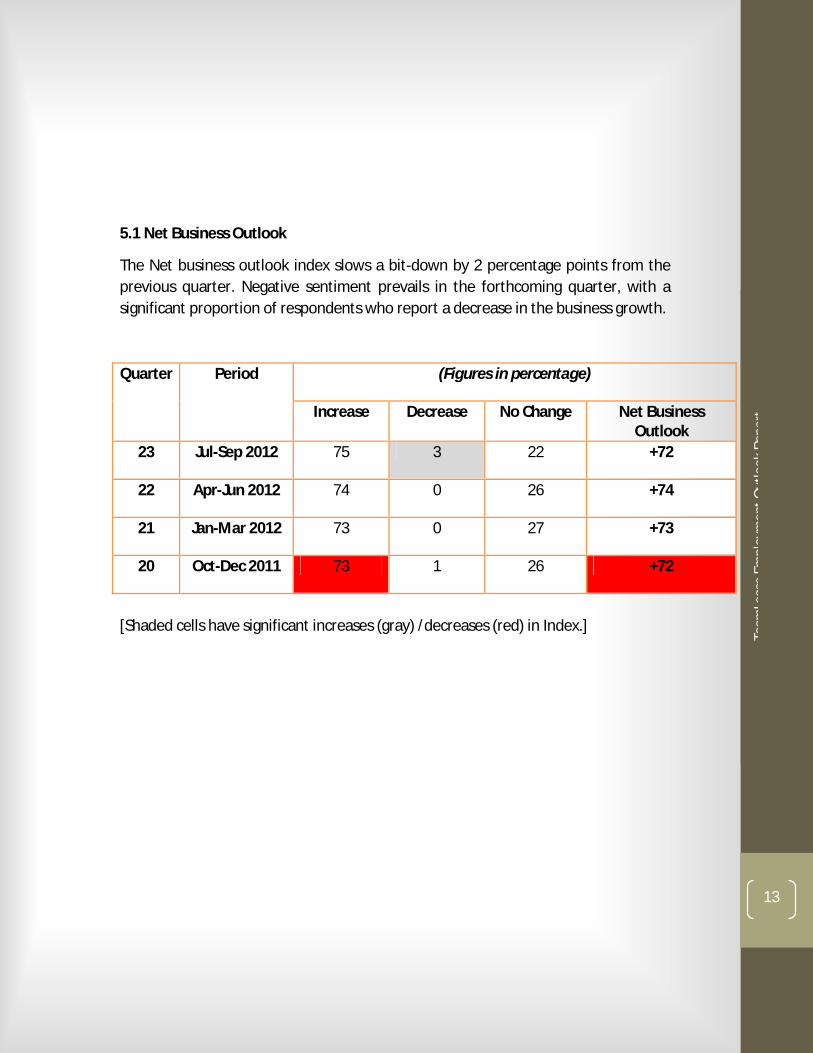

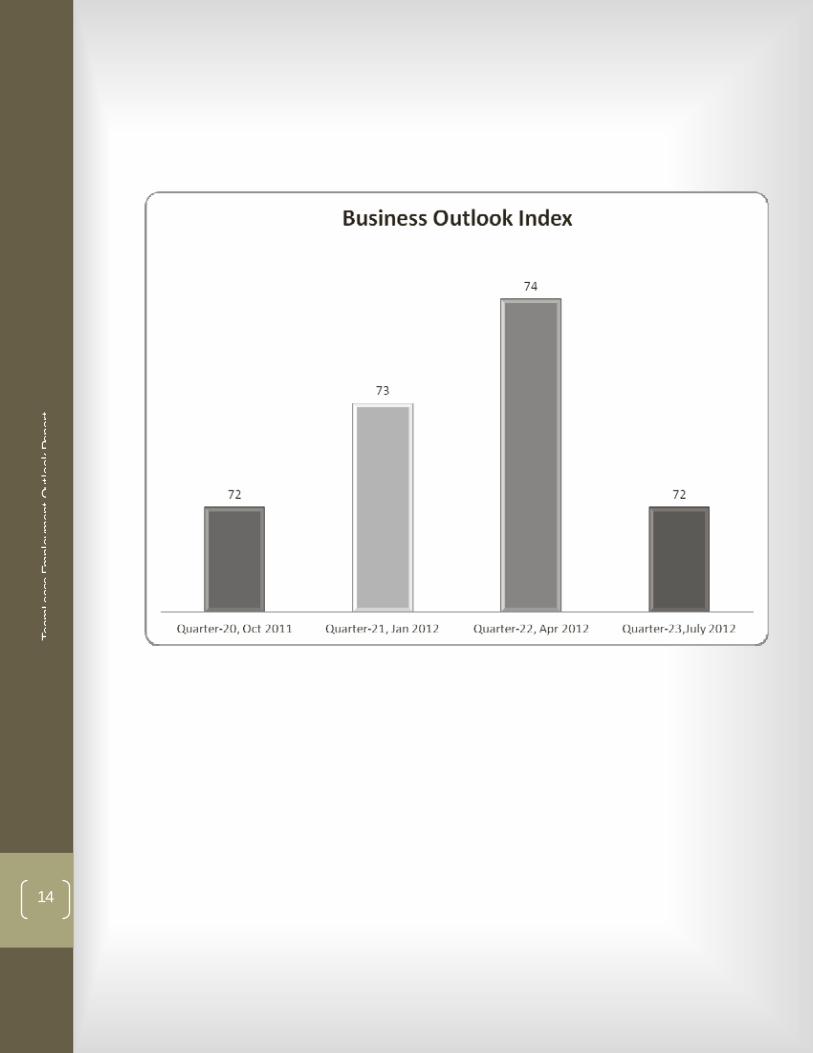

5.1 Net Business Outlook

The Net business outlook index slows a bit-down by 2 percentage points from the previous quarter. Negative sentiment prevails in the forthcoming quarter, with a significant proportion of respondents who report a decrease in the business growth.

(Figures in percentage) Quarter Period

Increase Decrease No Change Net Business Outlook

23 Jul-Sep 2012 75 3 22 +72

22 Apr-Jun 2012 74 0 26 +74

21 Jan-Mar 2012 73 0 27 +73

20 Oct-Dec 2011 73 1 26 +72

[Shaded cells have significant increases (gray) /decreases (red) in Index.]

Team

Leas

eEm

ploy

men

tOut

look

Repo

rt

14

Team

Leas

eEm

ploy

men

tOut

look

Repo

rt

15

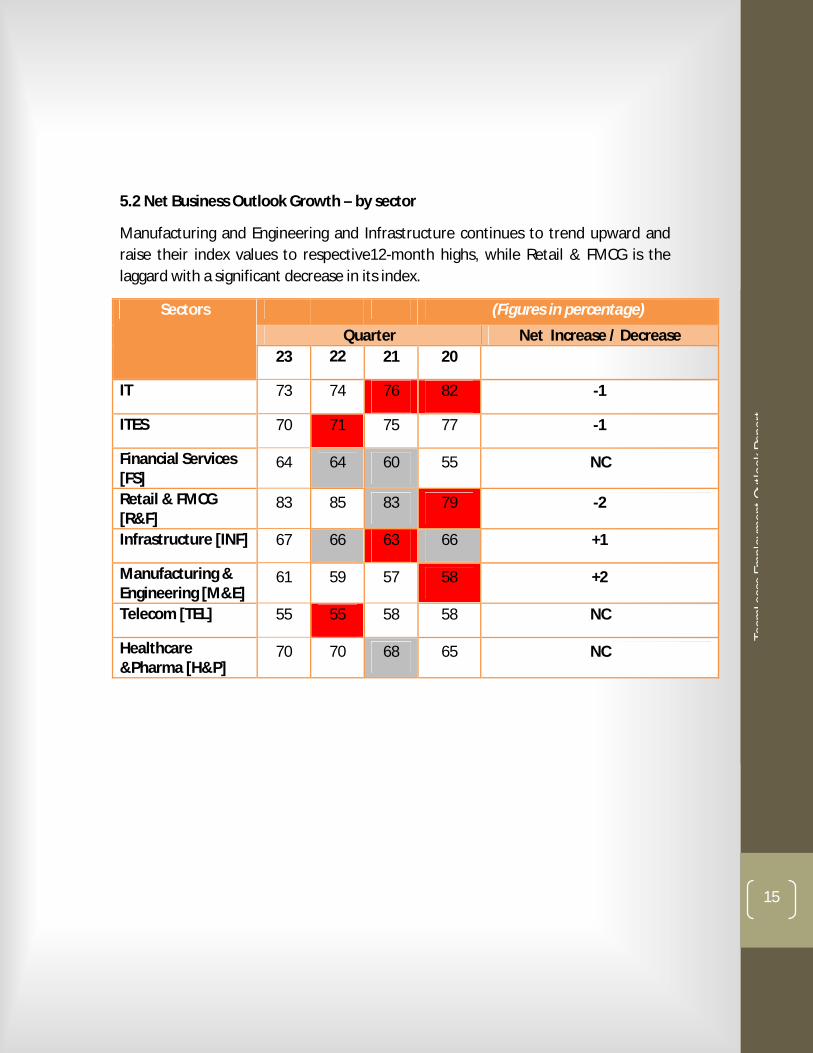

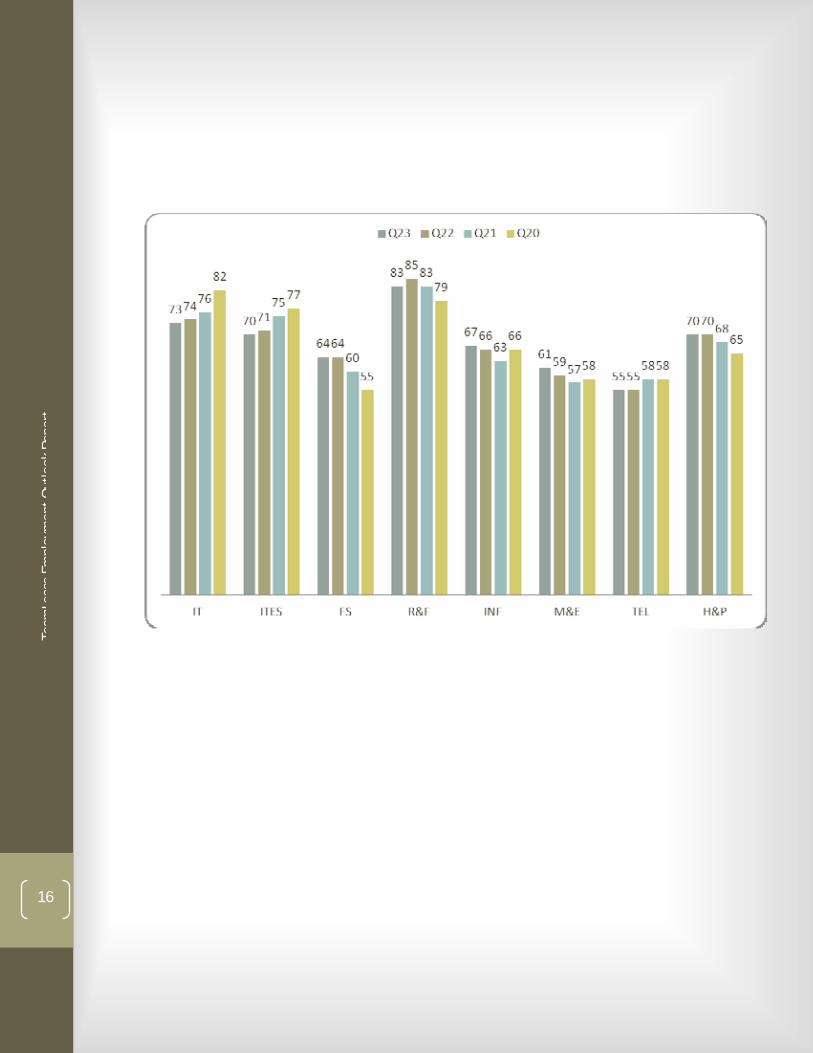

5.2 Net Business Outlook Growth – by sector

Manufacturing and Engineering and Infrastructure continues to trend upward and raise their index values to respective12-month highs, while Retail & FMCG is the laggard with a significant decrease in its index.

(Figures in percentage)

Quarter Net Increase / Decrease

Sectors

23 22 21 20

IT 73 74 76 82 -1

ITES 70 71 75 77 -1

Financial Services [FS]

64 64 60 55 NC

Retail & FMCG [R&F]

83 85 83 79 -2

Infrastructure [INF] 67 66 63 66 +1

Manufacturing & Engineering [M&E]

61 59 57 58 +2

Telecom [TEL] 55 55 58 58 NC

Healthcare &Pharma [H&P]

70 70 68 65 NC

Team

Leas

eEm

ploy

men

tOut

look

Repo

rt

16

Team

Leas

eEm

ploy

men

tOut

look

Repo

rt

17

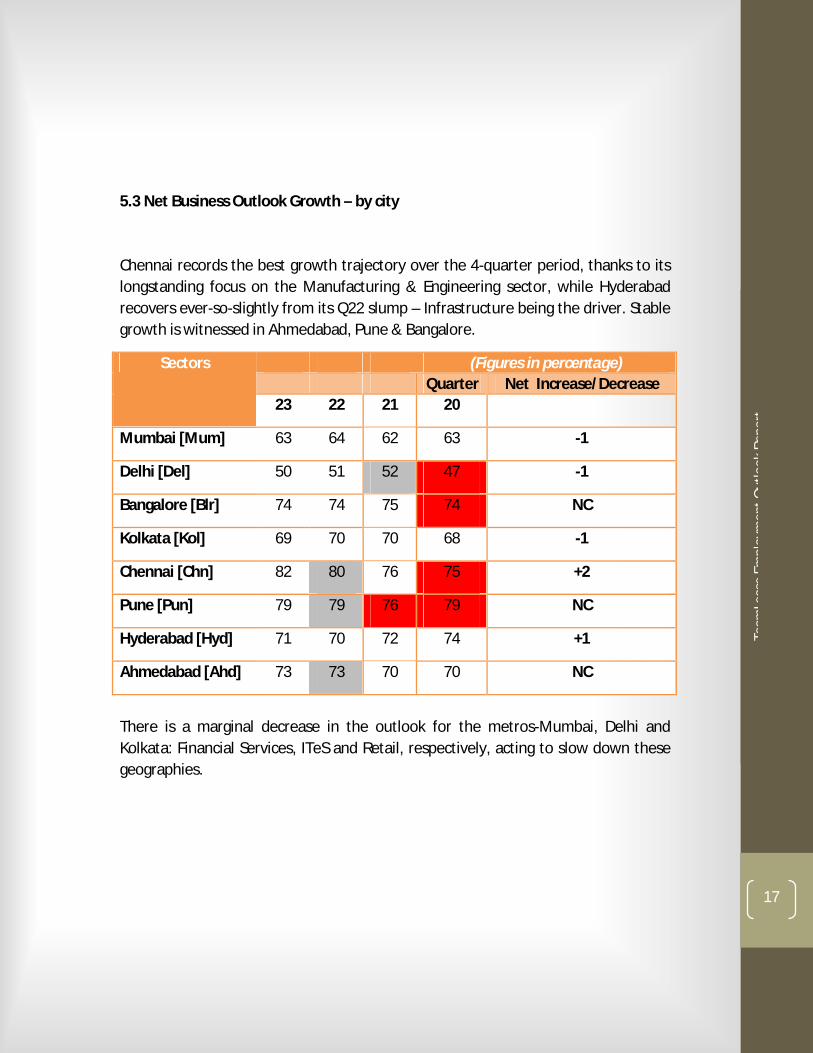

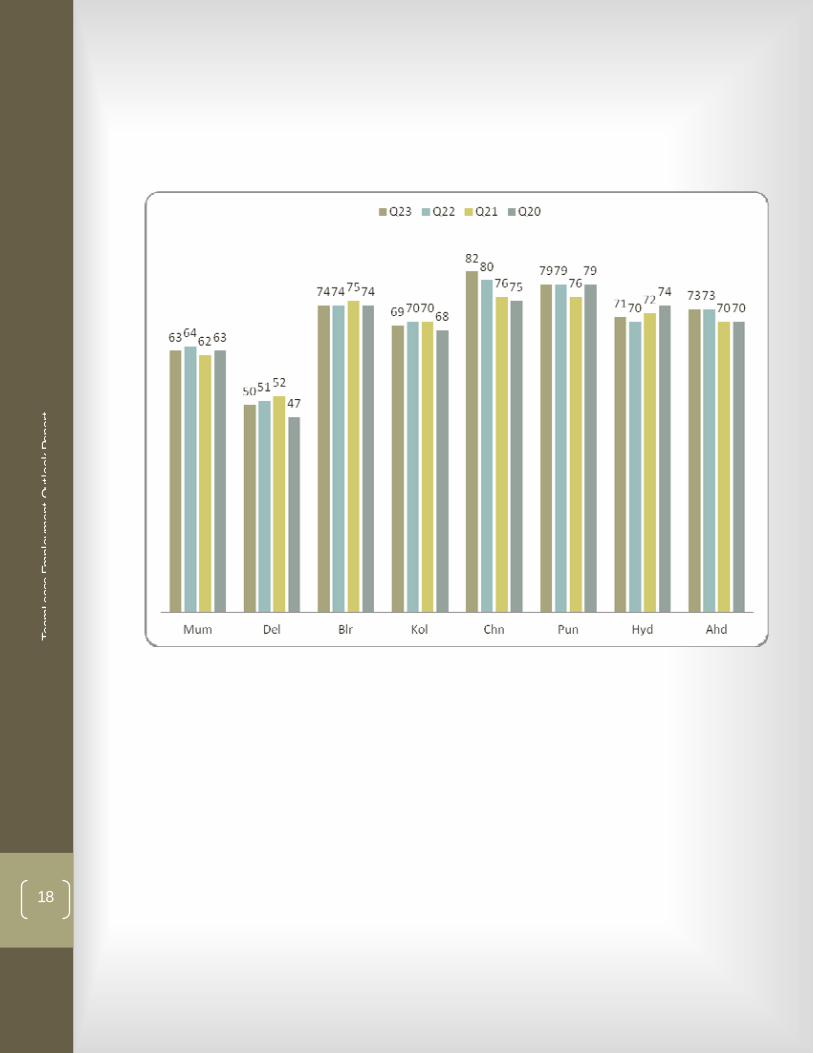

5.3 Net Business Outlook Growth – by city

Chennai records the best growth trajectory over the 4-quarter period, thanks to its longstanding focus on the Manufacturing & Engineering sector, while Hyderabad recovers ever-so-slightly from its Q22 slump – Infrastructure being the driver. Stable growth is witnessed in Ahmedabad, Pune & Bangalore.

(Figures in percentage) Quarter Net Increase/Decrease

Sectors

23 22 21 20

Mumbai [Mum] 63 64 62 63 -1

Delhi [Del] 50 51 52 47 -1

Bangalore [Blr] 74 74 75 74 NC

Kolkata [Kol] 69 70 70 68 -1

Chennai [Chn] 82 80 76 75 +2

Pune [Pun] 79 79 76 79 NC

Hyderabad [Hyd] 71 70 72 74 +1

Ahmedabad [Ahd] 73 73 70 70 NC

There is a marginal decrease in the outlook for the metros-Mumbai, Delhi and Kolkata: Financial Services, ITeS and Retail, respectively, acting to slow down these geographies.

Team

Leas

eEm

ploy

men

tOut

look

Repo

rt

18

Team

Leas

eEm

ploy

men

tOut

look

Repo

rt

19

6. Hiring Intent

6.1 Hiring Intent by Geography6.2 Hiring Intent by Hierarchy 6.3Hiring Intent by Functional Area

Team

Leas

eEm

ploy

men

tOut

look

Repo

rt

20

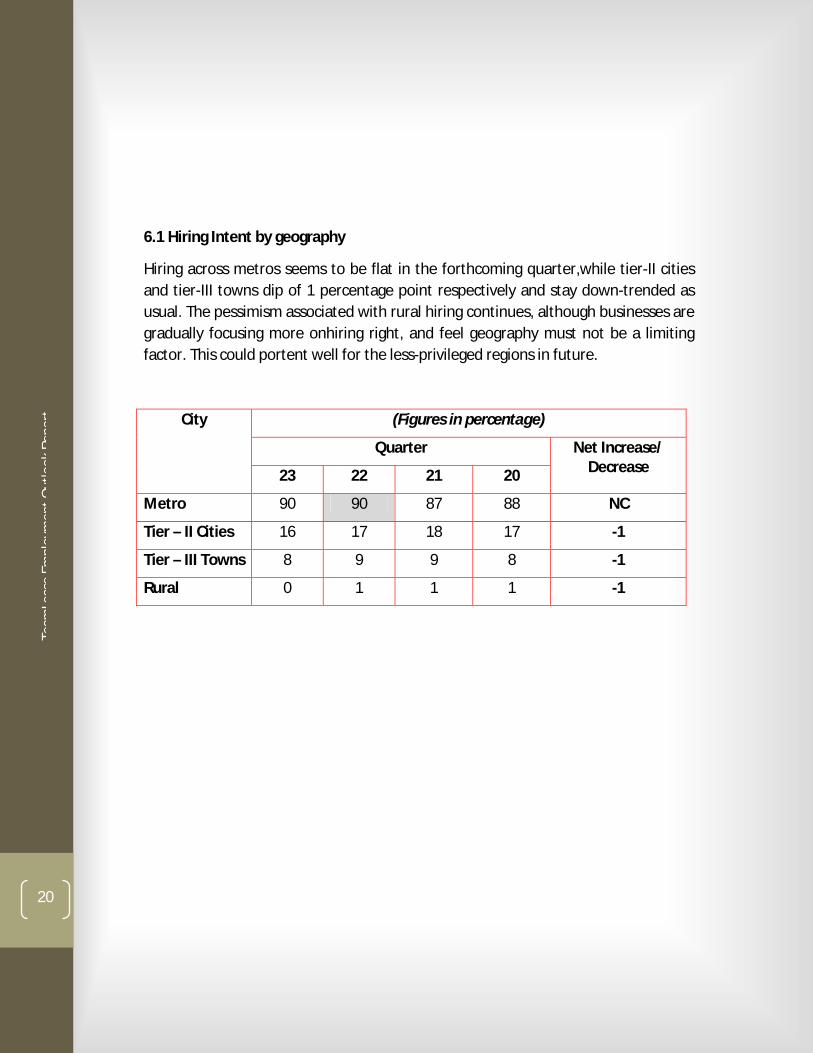

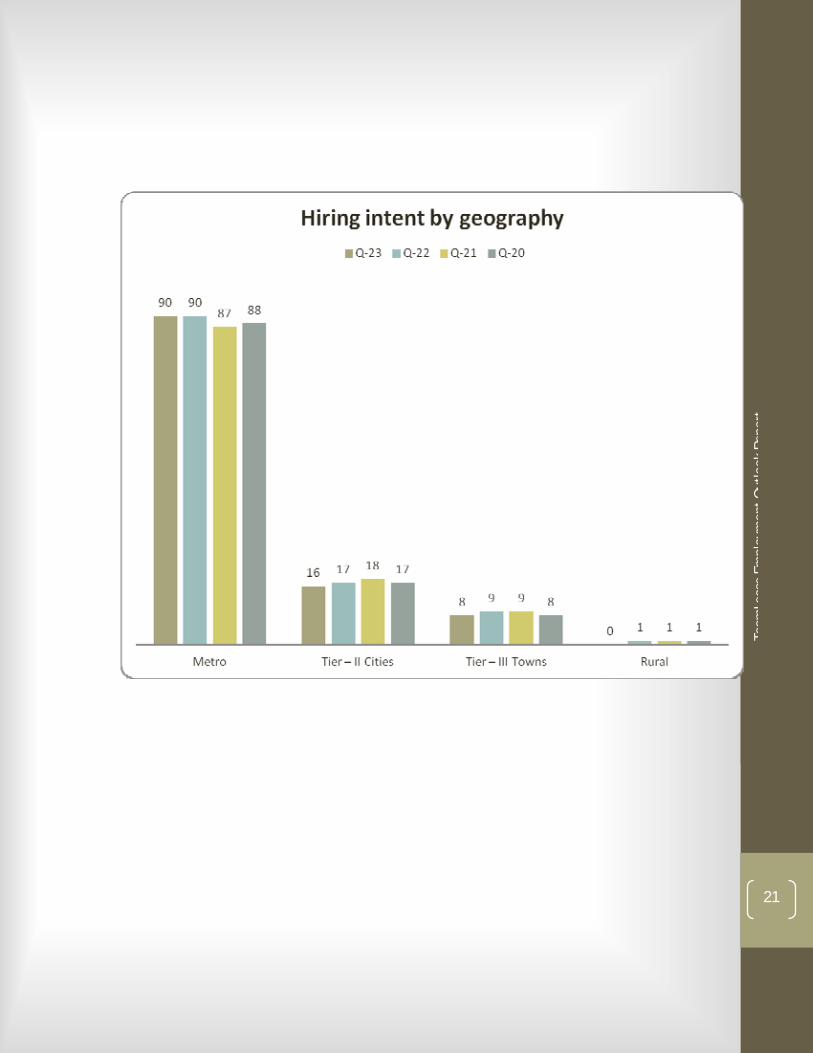

6.1 Hiring Intent by geography

Hiring across metros seems to be flat in the forthcoming quarter,while tier-II cities and tier-III towns dip of 1 percentage point respectively and stay down-trended as usual. The pessimism associated with rural hiring continues, although businesses are gradually focusing more onhiring right, and feel geography must not be a limiting factor. This could portent well for the less-privileged regions in future.

(Figures in percentage)

Quarter

City

23 22 21 20

Net Increase/ Decrease

Metro 90 90 87 88 NC

Tier – II Cities 16 17 18 17 -1

Tier – III Towns 8 9 9 8 -1

Rural 0 1 1 1 -1

Team

Leas

eEm

ploy

men

tOut

look

Repo

rt

21

Team

Leas

eEm

ploy

men

tOut

look

Repo

rt

22

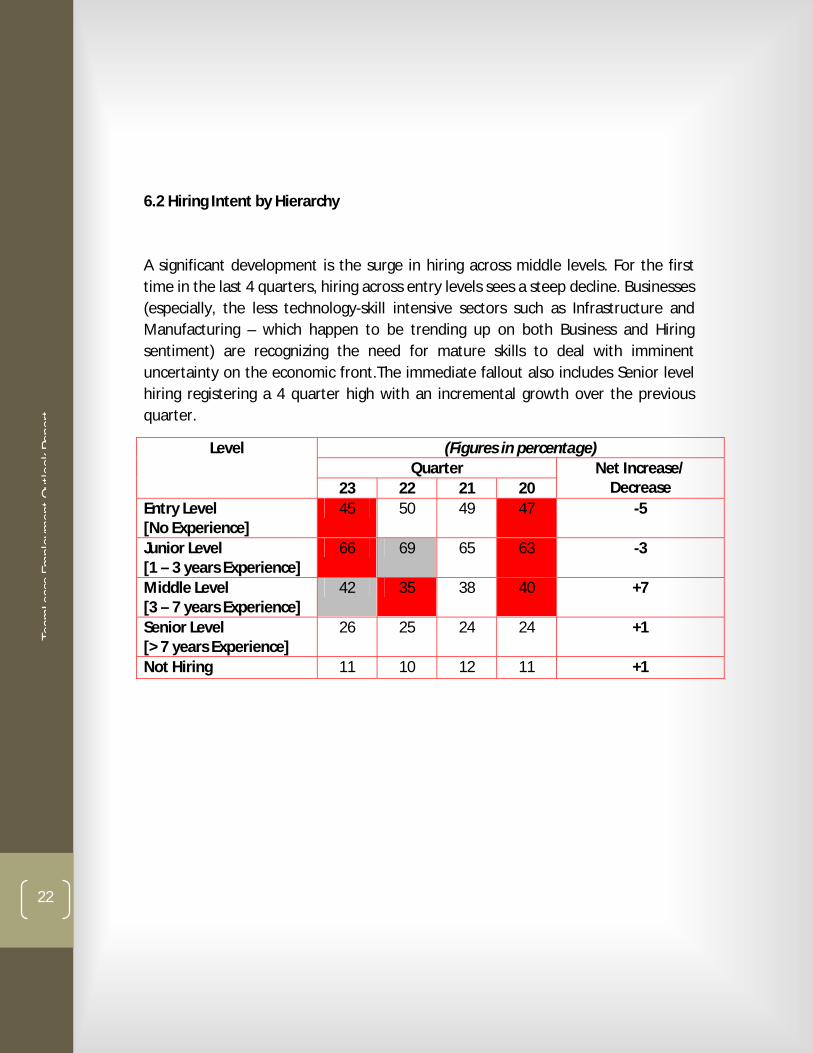

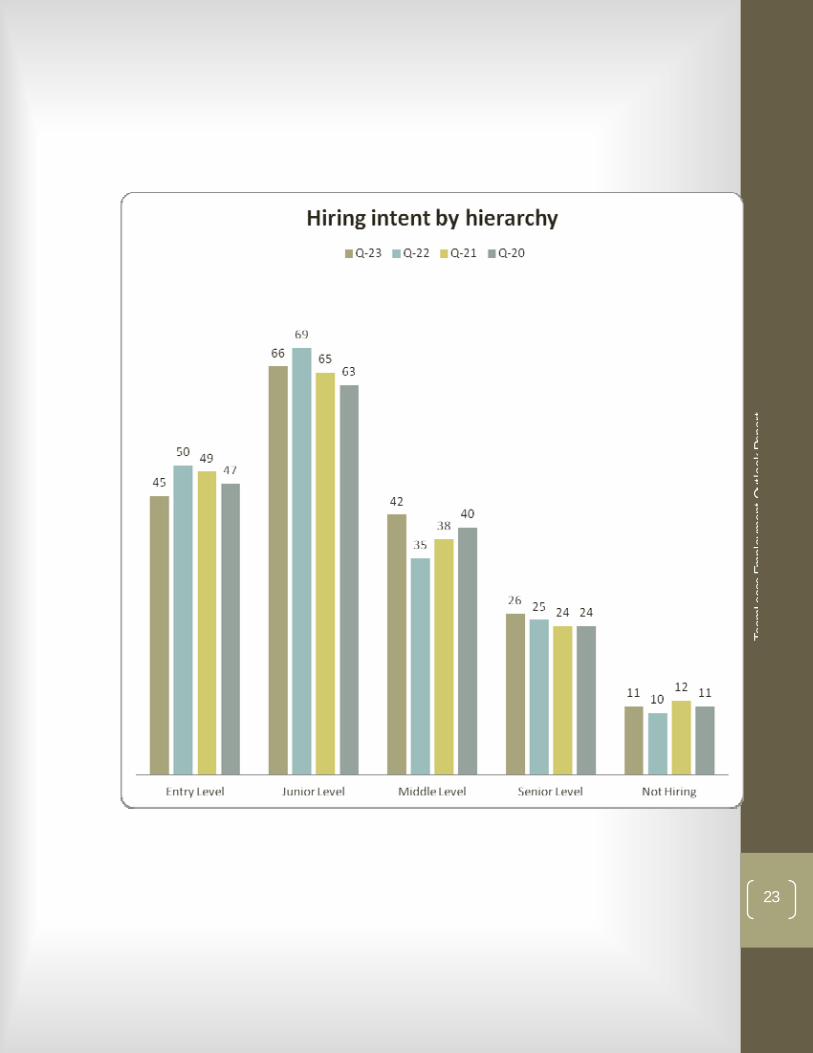

6.2 Hiring Intent by Hierarchy

A significant development is the surge in hiring across middle levels. For the first time in the last 4 quarters, hiring across entry levels sees a steep decline. Businesses (especially, the less technology-skill intensive sectors such as Infrastructure and Manufacturing – which happen to be trending up on both Business and Hiring sentiment) are recognizing the need for mature skills to deal with imminent uncertainty on the economic front.The immediate fallout also includes Senior level hiring registering a 4 quarter high with an incremental growth over the previous quarter.

(Figures in percentage) Quarter

Level

23 22 21 20 Net Increase/

Decrease Entry Level [No Experience]

45 50 49 47 -5

Junior Level [1 – 3 years Experience]

66 69 65 63 -3

Middle Level [3 – 7 years Experience]

42 35 38 40 +7

Senior Level [> 7 years Experience]

26 25 24 24 +1

Not Hiring 11 10 12 11 +1

Team

Leas

eEm

ploy

men

tOut

look

Repo

rt

23

Team

Leas

eEm

ploy

men

tOut

look

Repo

rt

24

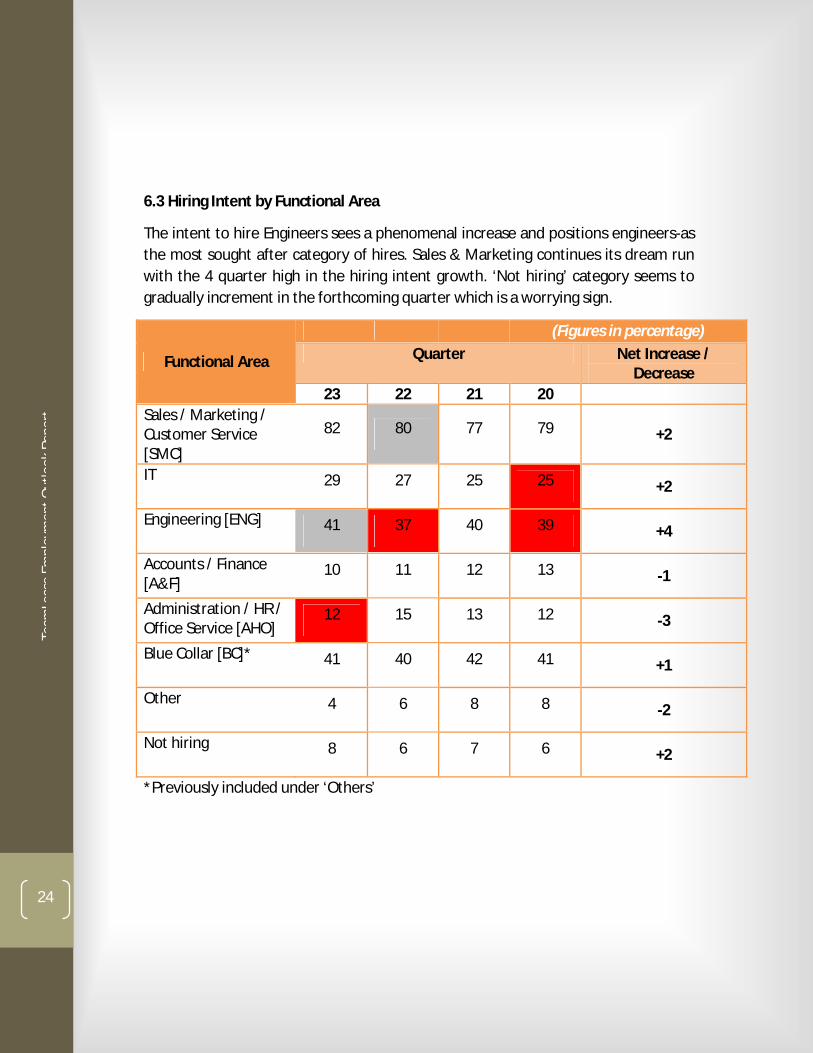

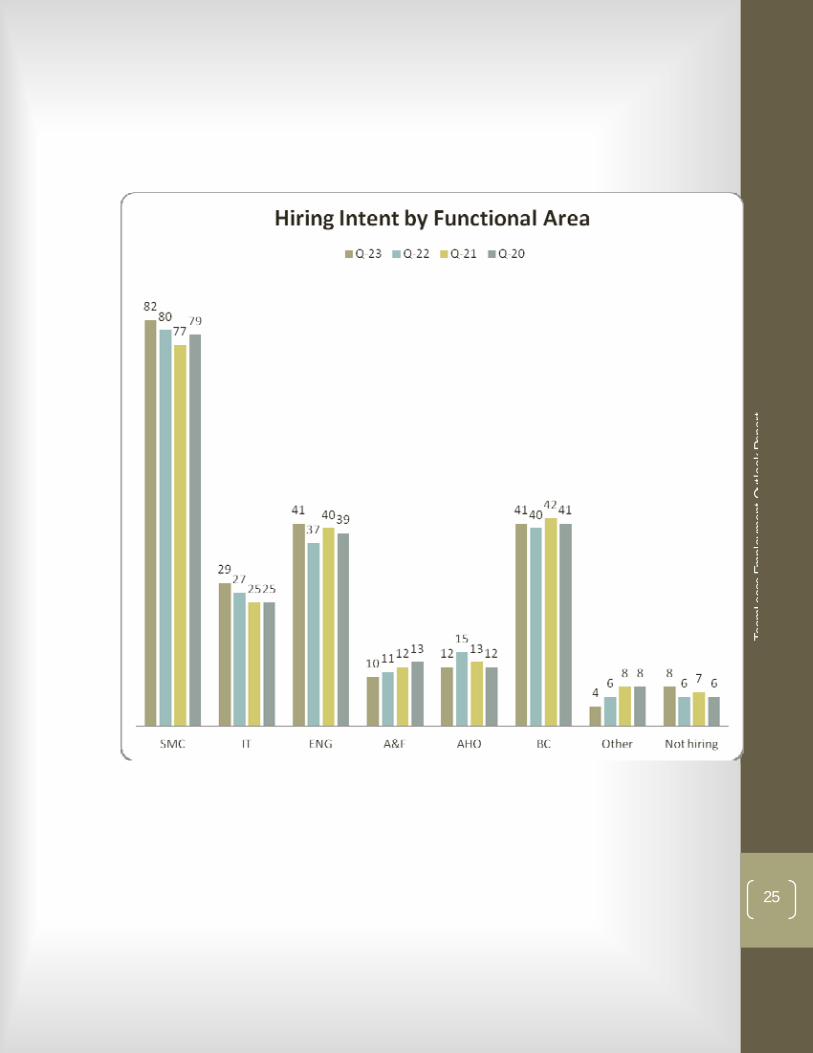

6.3 Hiring Intent by Functional Area

The intent to hire Engineers sees a phenomenal increase and positions engineers-as the most sought after category of hires. Sales & Marketing continues its dream run with the 4 quarter high in the hiring intent growth. ‘Not hiring’ category seems to gradually increment in the forthcoming quarter which is a worrying sign.

7.1 Employment Outlook Index – city-sector drilldown 7.2 Business Outlook Index – city-sector drilldown 7.3 Attrition trends by sector 7.4 Attrition trends by city

Team

Leas

eEm

ploy

men

tOut

look

Repo

rt

27

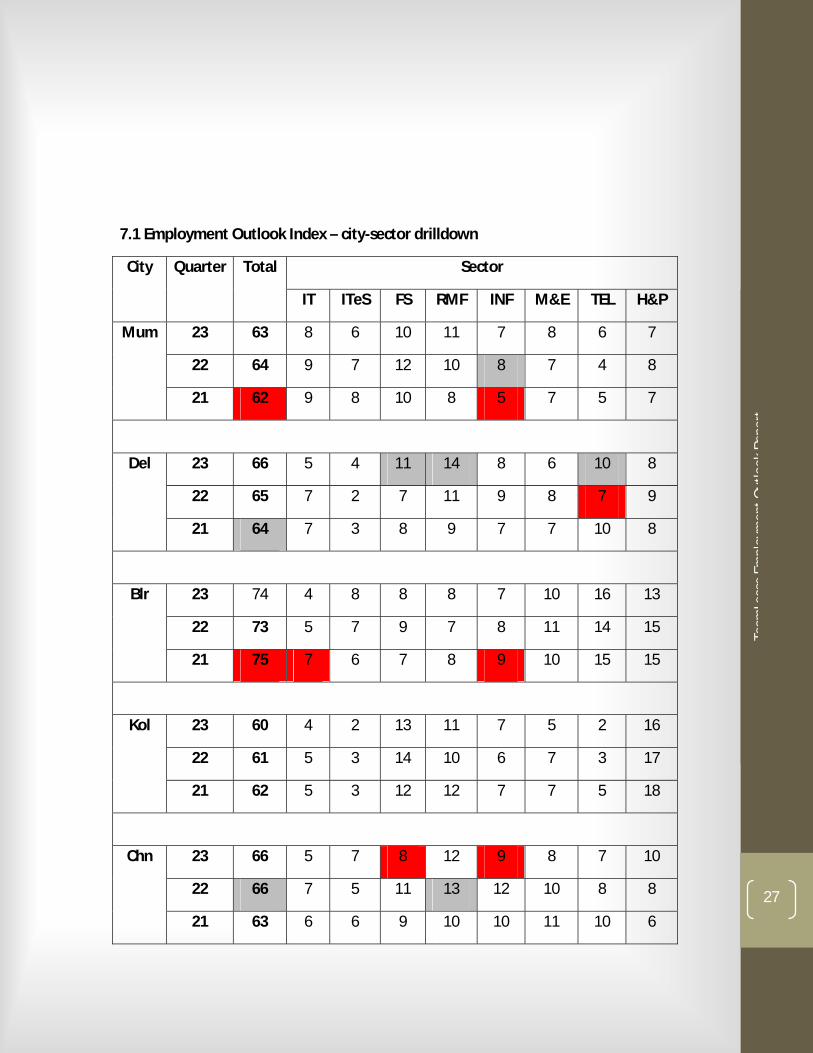

7.1 Employment Outlook Index – city-sector drilldown

Sector City Quarter Total

IT ITeS FS RMF INF M&E TEL H&P

23 63 8 6 10 11 7 8 6 7

22 64 9 7 12 10 8 7 4 8

Mum

21 62 9 8 10 8 5 7 5 7

23 66 5 4 11 14 8 6 10 8

22 65 7 2 7 11 9 8 7 9

Del

21 64 7 3 8 9 7 7 10 8

23 74 4 8 8 8 7 10 16 13

22 73 5 7 9 7 8 11 14 15

Blr

21 75 7 6 7 8 9 10 15 15

23 60 4 2 13 11 7 5 2 16

22 61 5 3 14 10 6 7 3 17

Kol

21 62 5 3 12 12 7 7 5 18

23 66 5 7 8 12 9 8 7 10

22 66 7 5 11 13 12 10 8 8

Chn

21 63 6 6 9 10 10 11 10 6

Team

Leas

eEm

ploy

men

tOut

look

Repo

rt

28

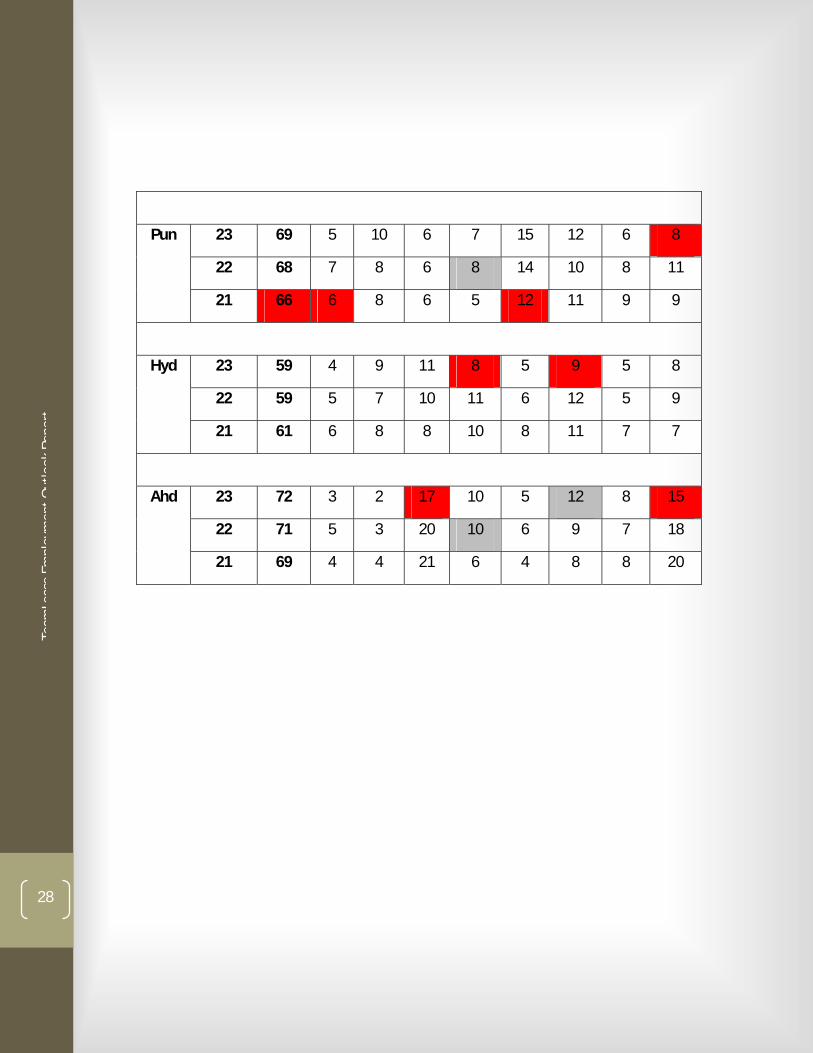

23 69 5 10 6 7 15 12 6 8

22 68 7 8 6 8 14 10 8 11

Pun

21 66 6 8 6 5 12 11 9 9

23 59 4 9 11 8 5 9 5 8

22 59 5 7 10 11 6 12 5 9

Hyd

21 61 6 8 8 10 8 11 7 7

23 72 3 2 17 10 5 12 8 15

22 71 5 3 20 10 6 9 7 18

Ahd

21 69 4 4 21 6 4 8 8 20

Team

Leas

eEm

ploy

men

tOut

look

Repo

rt

29

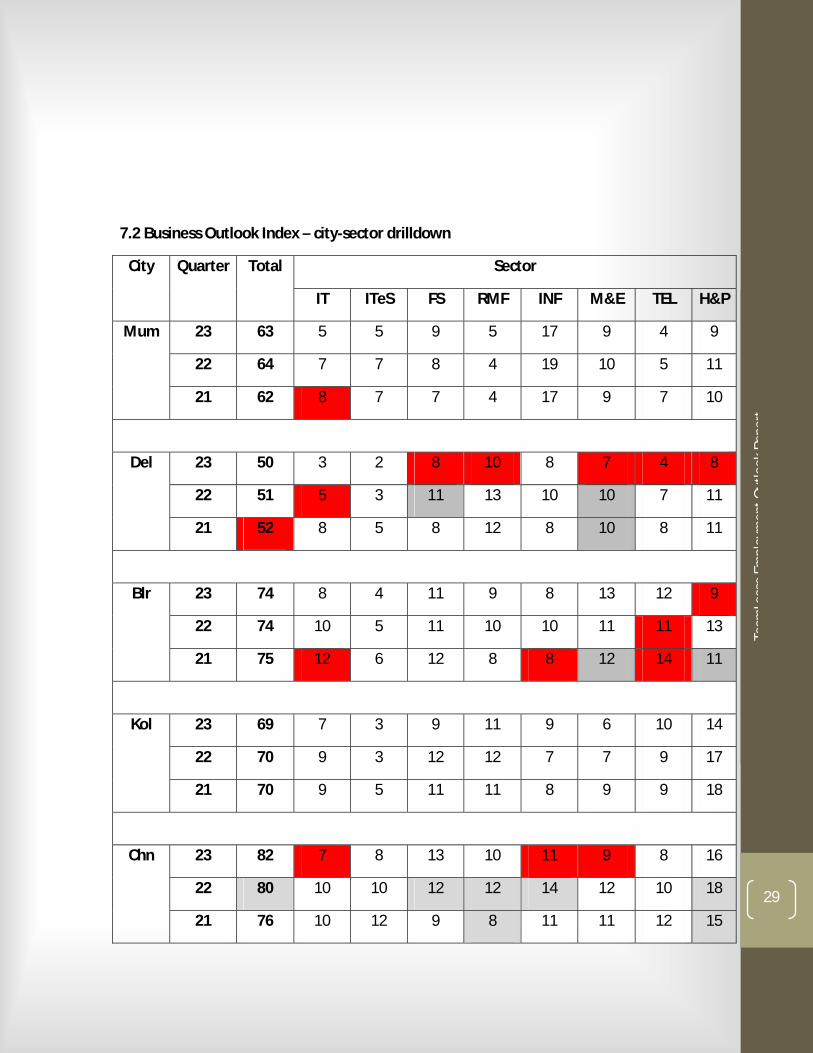

7.2 Business Outlook Index – city-sector drilldown

Sector City Quarter Total

IT ITeS FS RMF INF M&E TEL H&P

23 63 5 5 9 5 17 9 4 9

22 64 7 7 8 4 19 10 5 11

Mum

21 62 8 7 7 4 17 9 7 10

23 50 3 2 8 10 8 7 4 8

22 51 5 3 11 13 10 10 7 11

Del

21 52 8 5 8 12 8 10 8 11

23 74 8 4 11 9 8 13 12 9

22 74 10 5 11 10 10 11 11 13

Blr

21 75 12 6 12 8 8 12 14 11

23 69 7 3 9 11 9 6 10 14

22 70 9 3 12 12 7 7 9 17

Kol

21 70 9 5 11 11 8 9 9 18

23 82 7 8 13 10 11 9 8 16

22 80 10 10 12 12 14 12 10 18

Chn

21 76 10 12 9 8 11 11 12 15

Team

Leas

eEm

ploy

men

tOut

look

Repo

rt

30

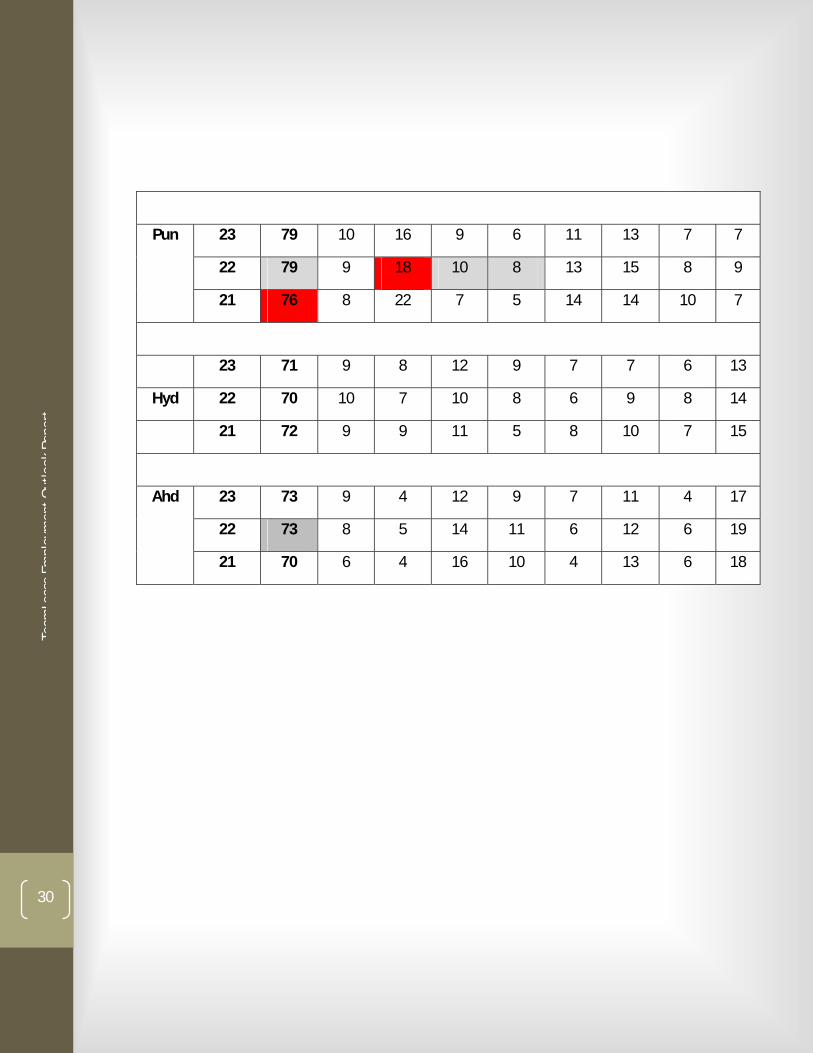

23 79 10 16 9 6 11 13 7 7

22 79 9 18 10 8 13 15 8 9

Pun

21 76 8 22 7 5 14 14 10 7

23 71 9 8 12 9 7 7 6 13

Hyd 22 70 10 7 10 8 6 9 8 14

21 72 9 9 11 5 8 10 7 15

23 73 9 4 12 9 7 11 4 17

22 73 8 5 14 11 6 12 6 19

Ahd

21 70 6 4 16 10 4 13 6 18

Team

Leas

eEm

ploy

men

tOut

look

Repo

rt

31

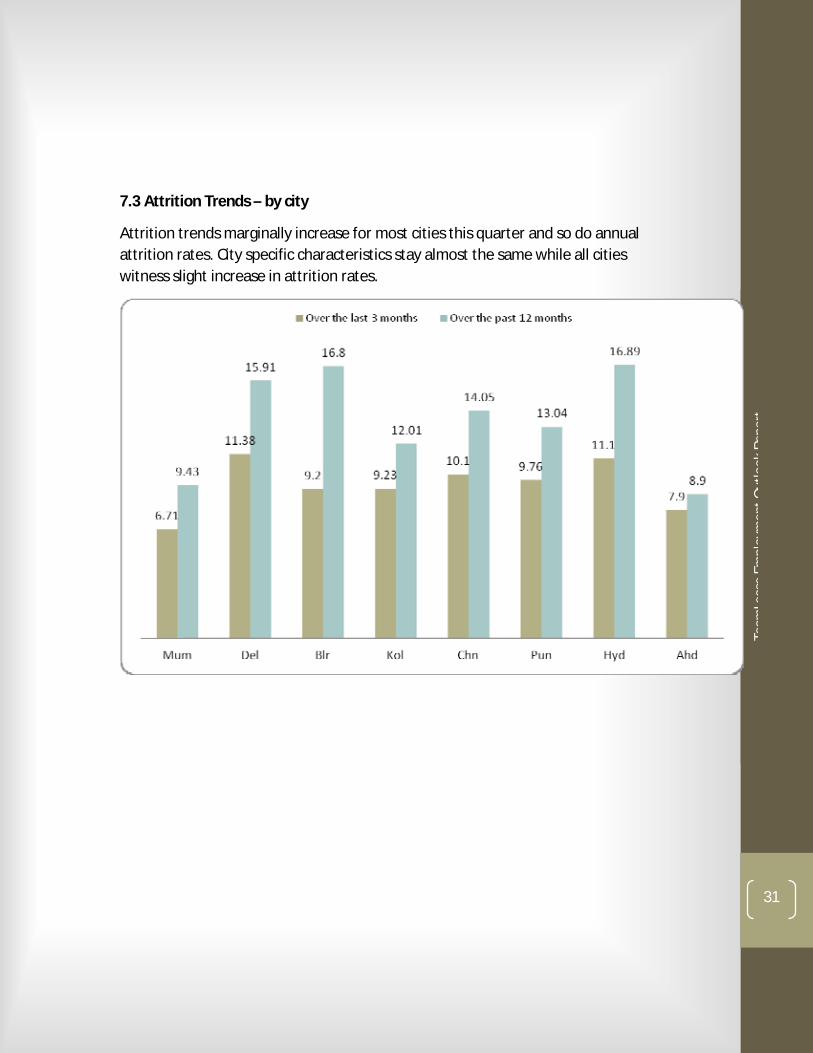

7.3 Attrition Trends – by city

Attrition trends marginally increase for most cities this quarter and so do annual attrition rates. City specific characteristics stay almost the same while all cities witness slight increase in attrition rates.

Team

Leas

eEm

ploy

men

tOut

look

Repo

rt

32

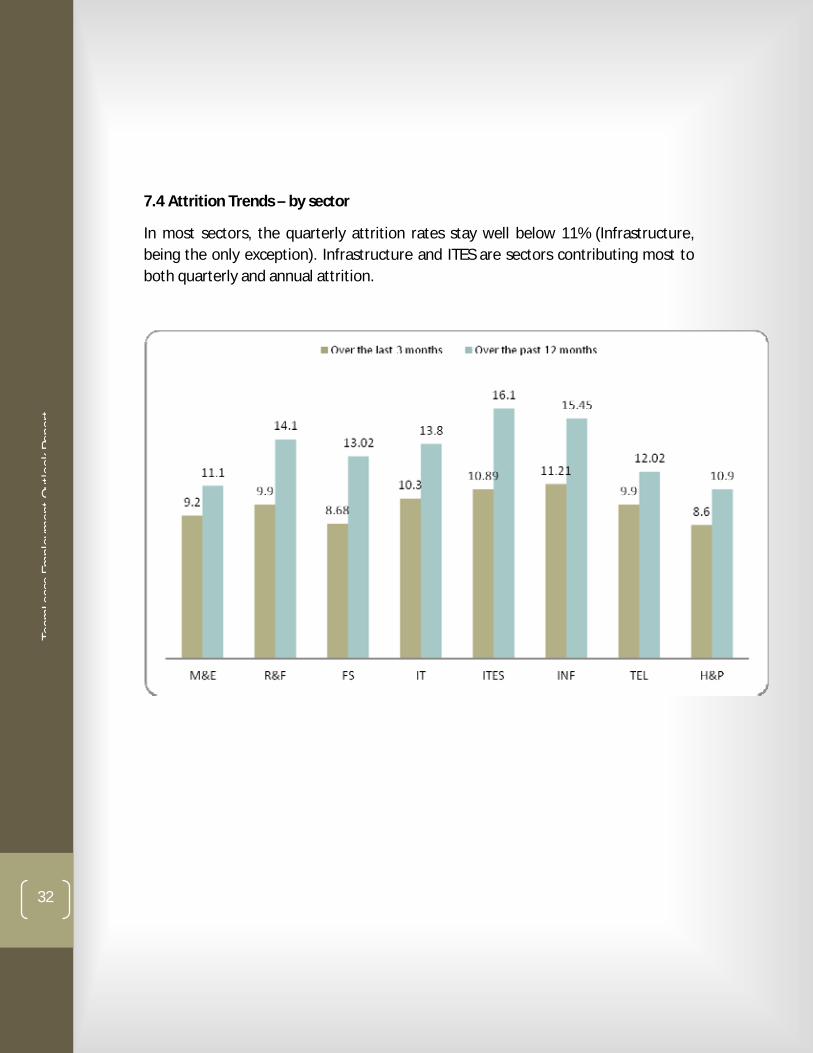

7.4 Attrition Trends – by sector

In most sectors, the quarterly attrition rates stay well below 11% (Infrastructure, being the only exception). Infrastructure and ITES are sectors contributing most to both quarterly and annual attrition.

Team

Leas

eEm

ploy

men

tOut

look

Repo

rt

33

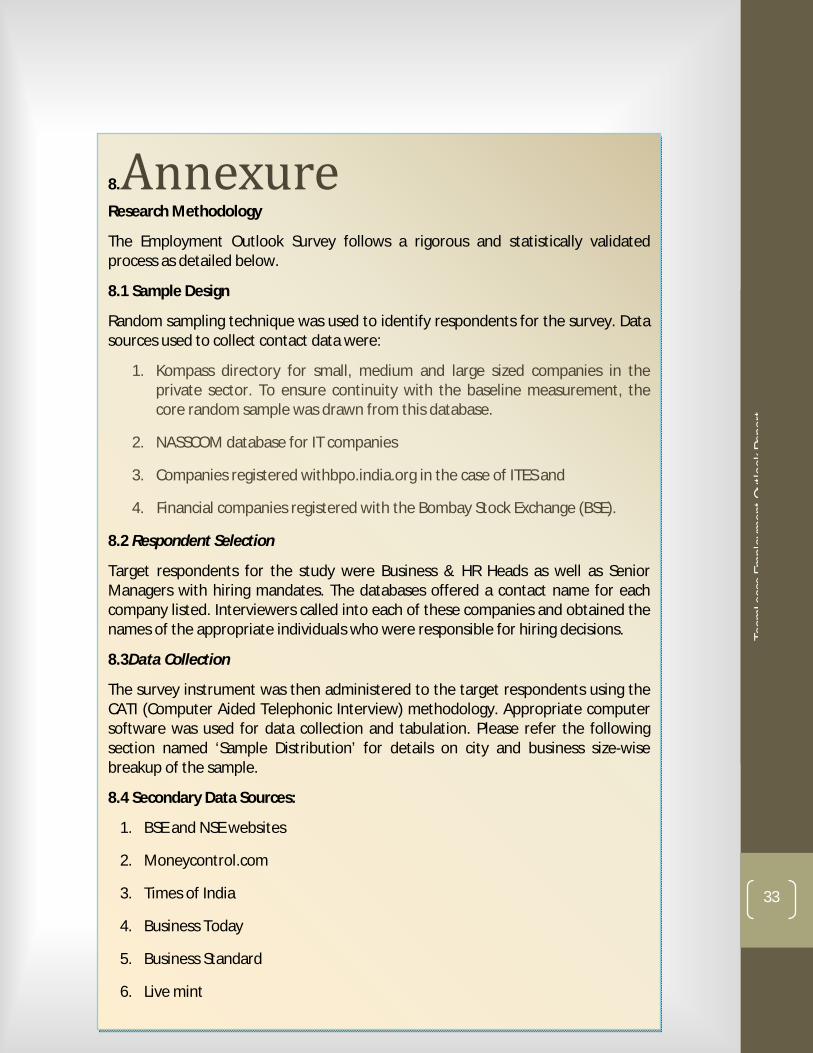

8.AnnexureResearch Methodology

The Employment Outlook Survey follows a rigorous and statistically validated process as detailed below.

8.1 Sample Design

Random sampling technique was used to identify respondents for the survey. Data sources used to collect contact data were:

1. Kompass directory for small, medium and large sized companies in the private sector. To ensure continuity with the baseline measurement, the core random sample was drawn from this database.

2. NASSCOM database for IT companies

3. Companies registered withbpo.india.org in the case of ITES and

4. Financial companies registered with the Bombay Stock Exchange (BSE).

8.2 Respondent Selection

Target respondents for the study were Business & HR Heads as well as Senior Managers with hiring mandates. The databases offered a contact name for each company listed. Interviewers called into each of these companies and obtained the names of the appropriate individuals who were responsible for hiring decisions.

8.3Data Collection

The survey instrument was then administered to the target respondents using the CATI (Computer Aided Telephonic Interview) methodology. Appropriate computer software was used for data collection and tabulation. Please refer the following section named ‘Sample Distribution’ for details on city and business size-wise breakup of the sample.

8.4 Secondary Data Sources:

1. BSE and NSE websites

2. Moneycontrol.com

3. Times of India

4. Business Today

5. Business Standard

6. Live mint

Team

Leas

eEm

ploy

men

tOut

look

Repo

rt

34

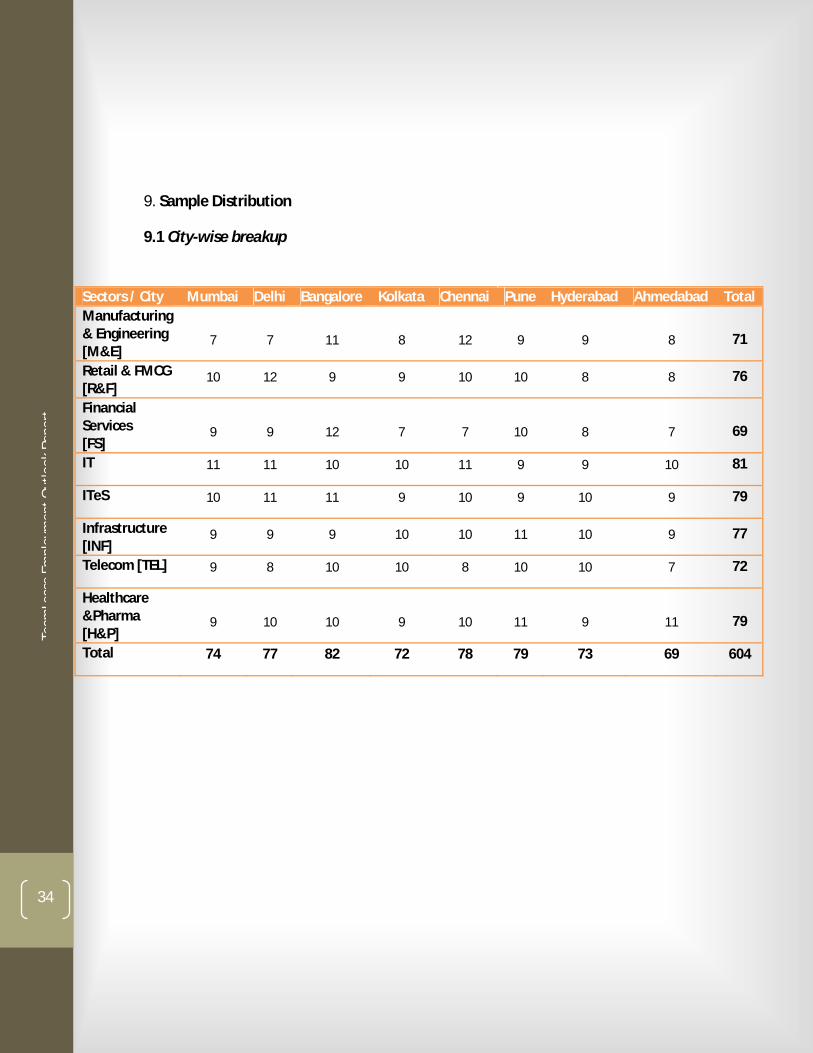

9. Sample Distribution

9.1 City-wise breakup

Sectors / City Mumbai Delhi Bangalore Kolkata Chennai Pune Hyderabad Ahmedabad Total Manufacturing & Engineering [M&E]

7 7 11 8 12 9 9 8 71

Retail & FMCG [R&F]

10 12 9 9 10 10 8 8 76

Financial Services [FS]

9 9 12 7 7 10 8 7 69

IT 11 11 10 10 11 9 9 10 81

ITeS 10 11 11 9 10 9 10 9 79

Infrastructure [INF]

9 9 9 10 10 11 10 9 77

Telecom [TEL] 9 8 10 10 8 10 10 7 72

Healthcare &Pharma [H&P]

9 10 10 9 10 11 9 11 79

Total 74 77 82 72 78 79 73 69 604

Team

Leas

eEm

ploy

men

tOut

look

Repo

rt

35

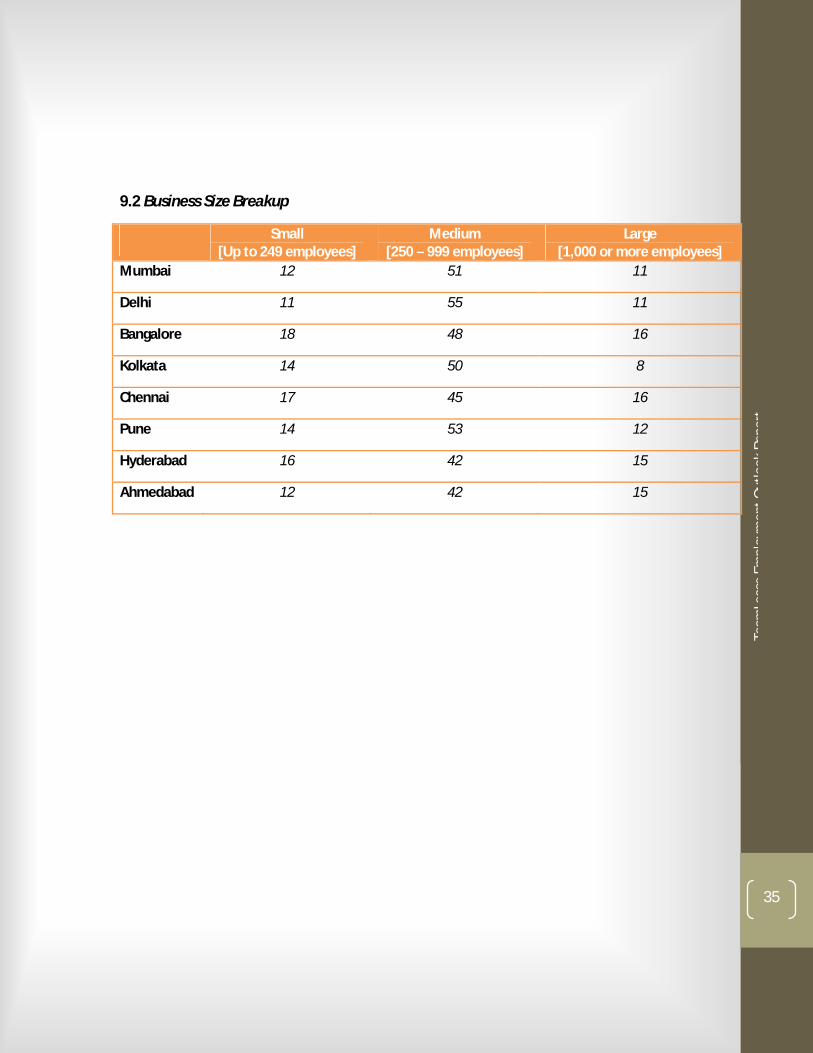

9.2 Business Size Breakup

Small [Up to 249 employees]

Medium [250 – 999 employees]

Large [1,000 or more employees]

Mumbai 12 51 11

Delhi 11 55 11

Bangalore 18 48 16

Kolkata 14 50 8

Chennai 17 45 16

Pune 14 53 12

Hyderabad 16 42 15

Ahmedabad 12 42 15

Team

Leas

eEm

ploy

men

tOut

look

Repo

rt

36

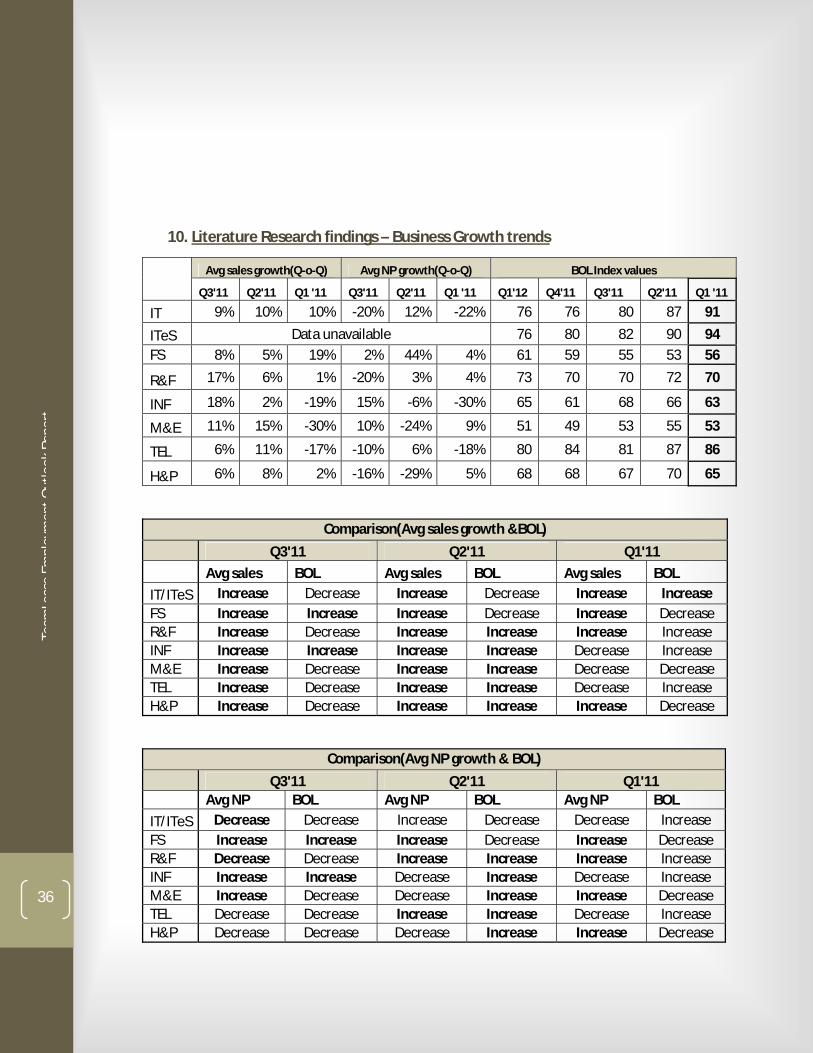

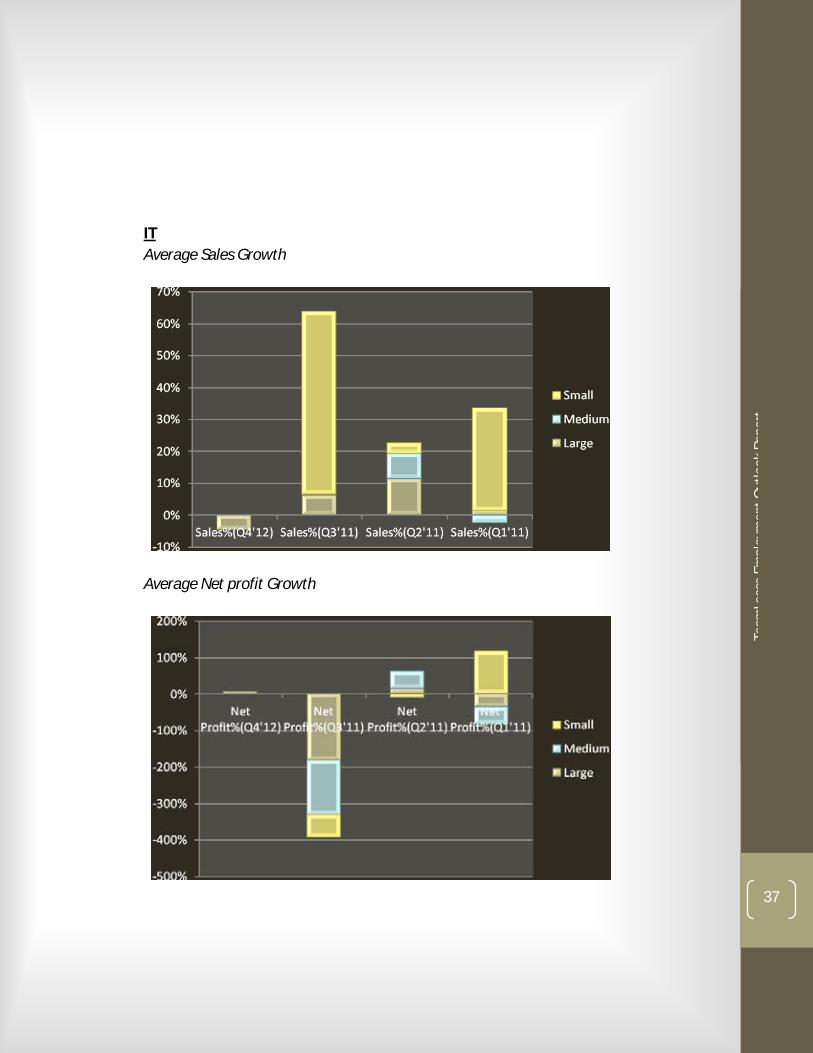

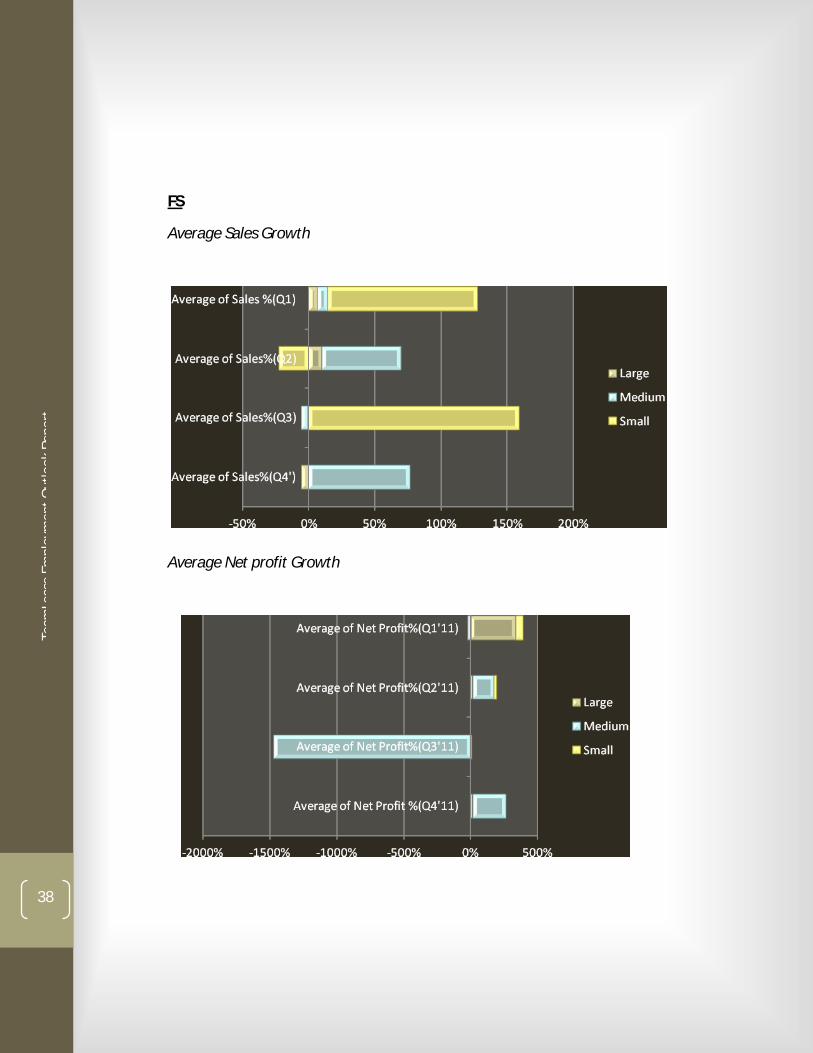

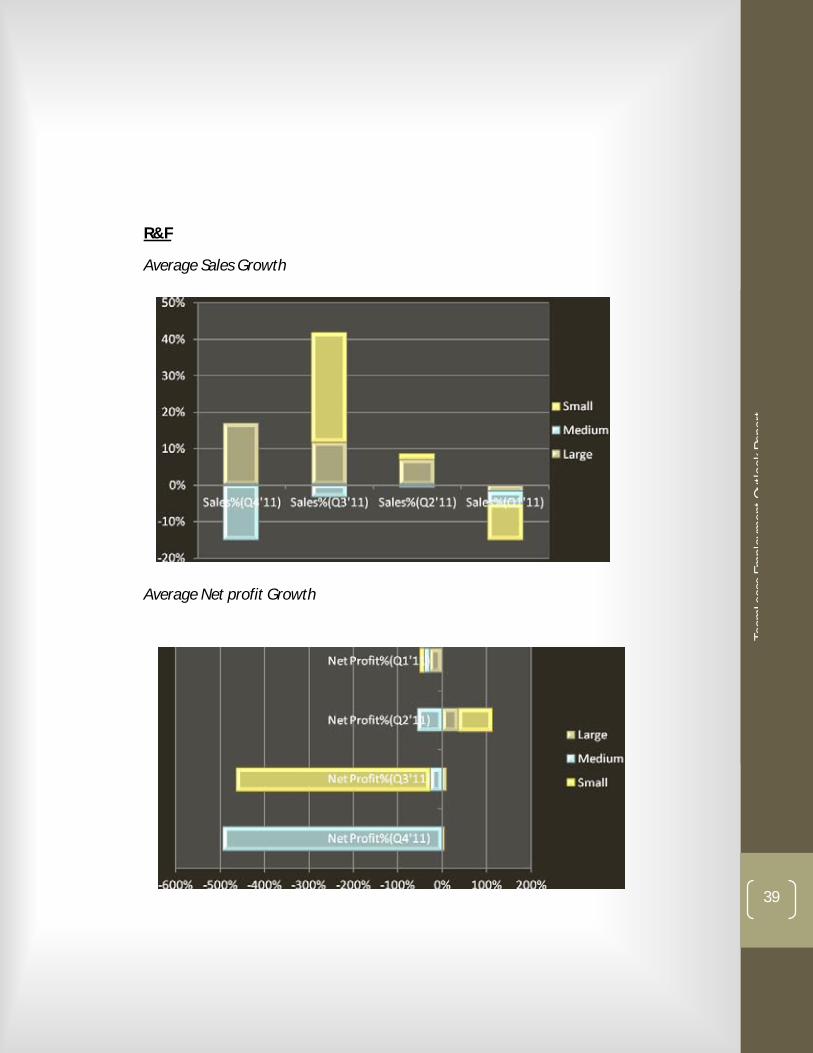

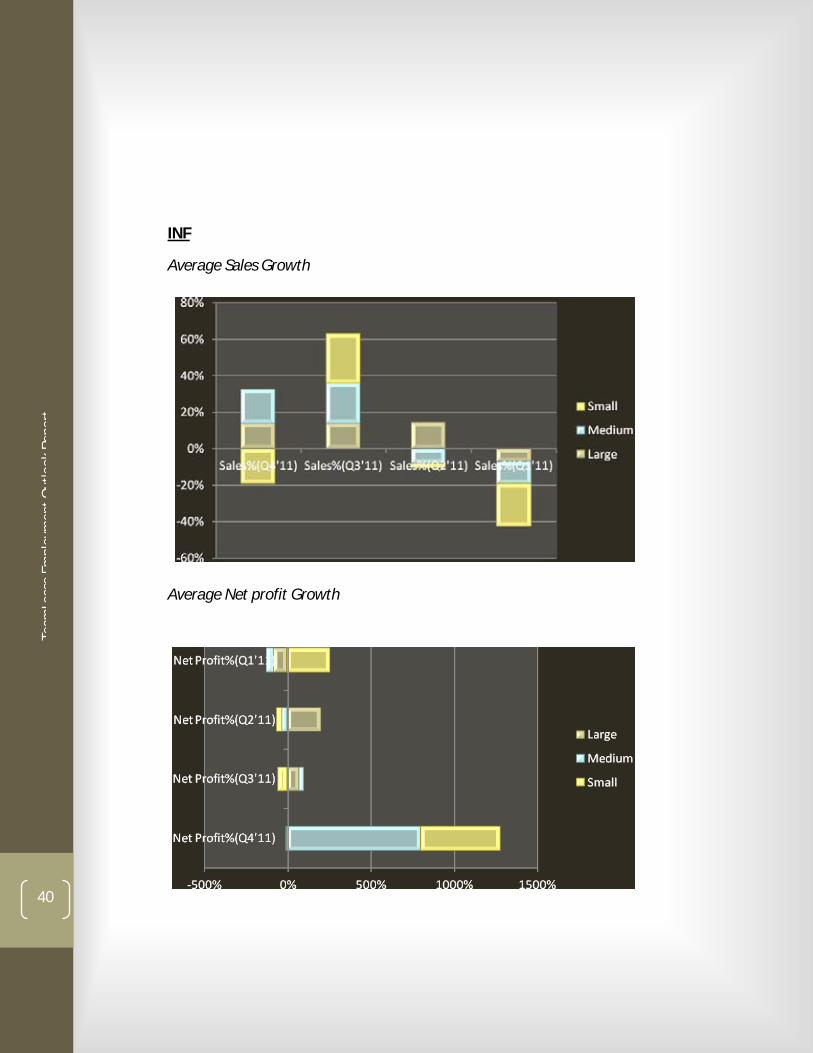

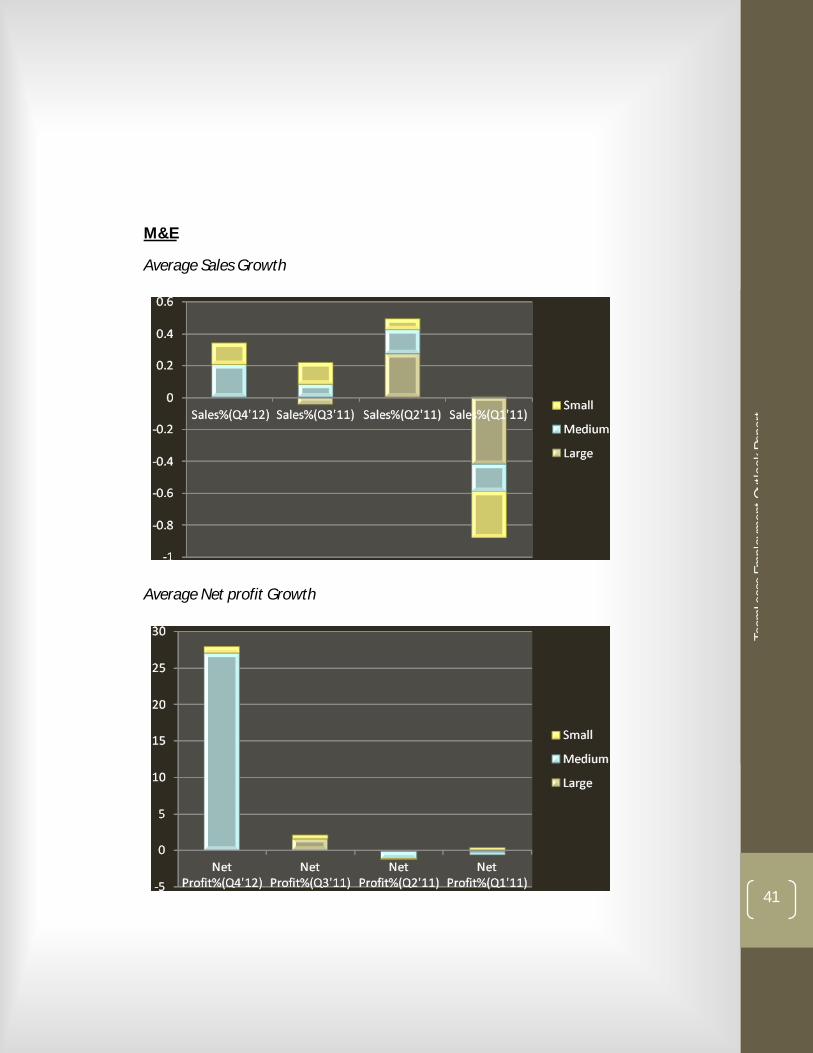

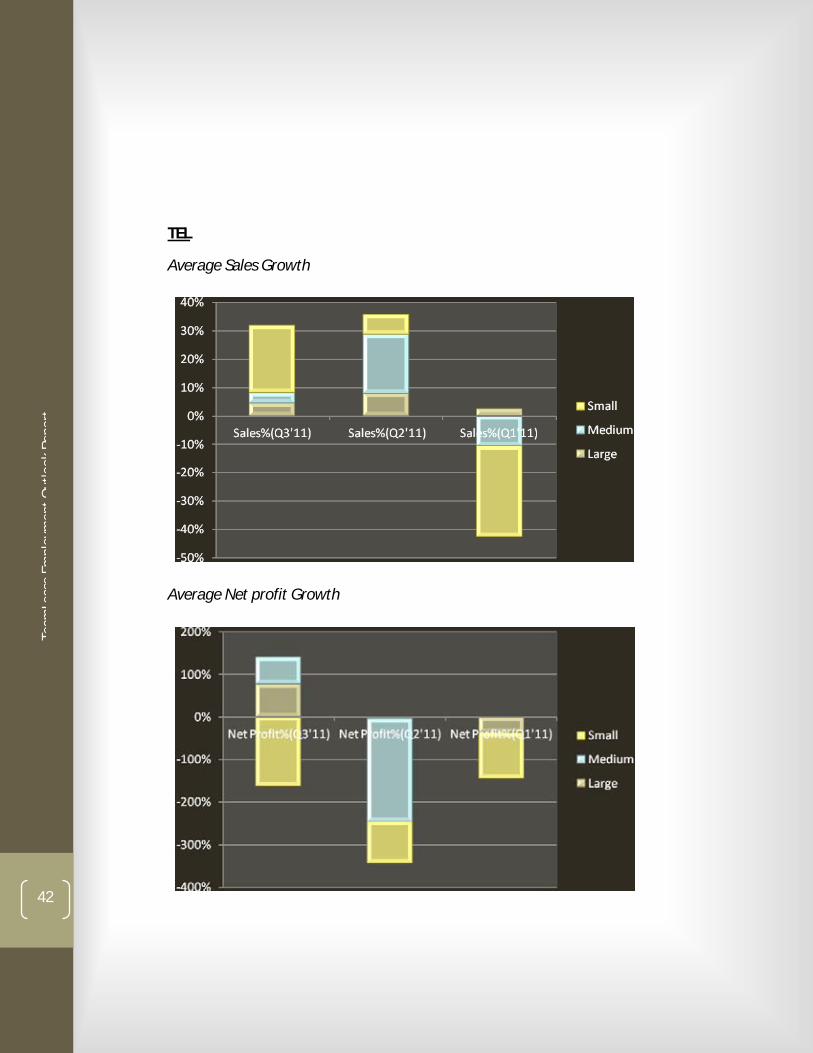

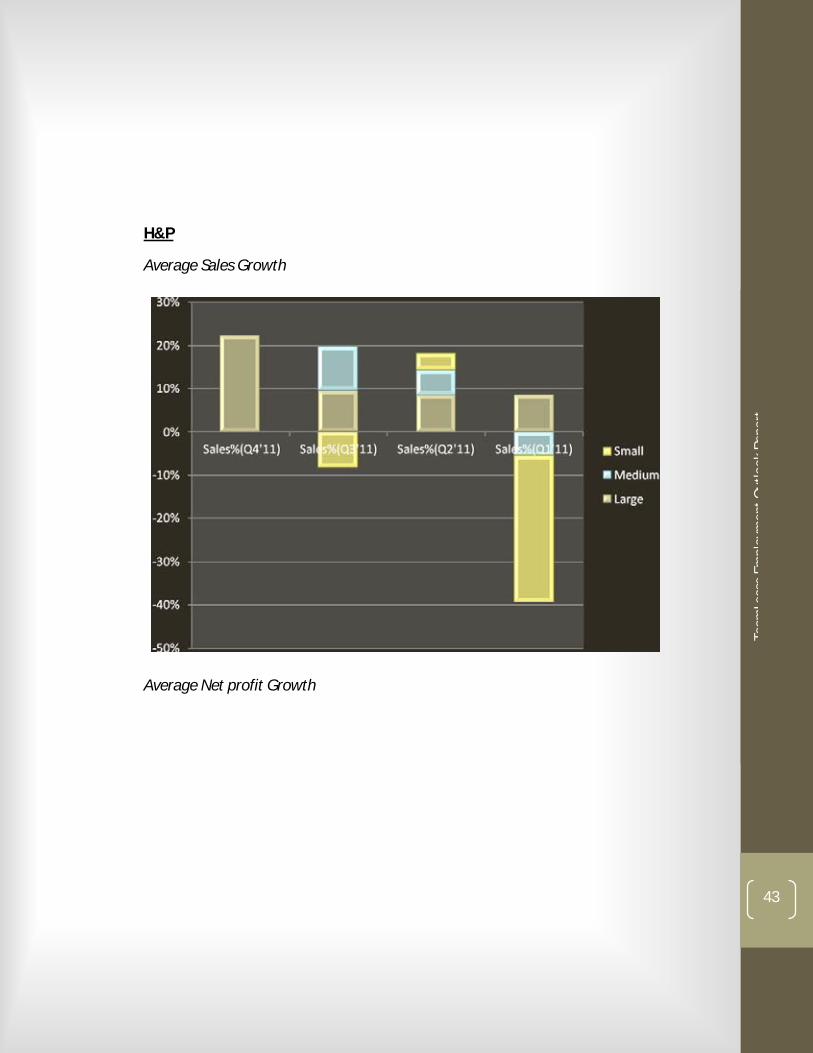

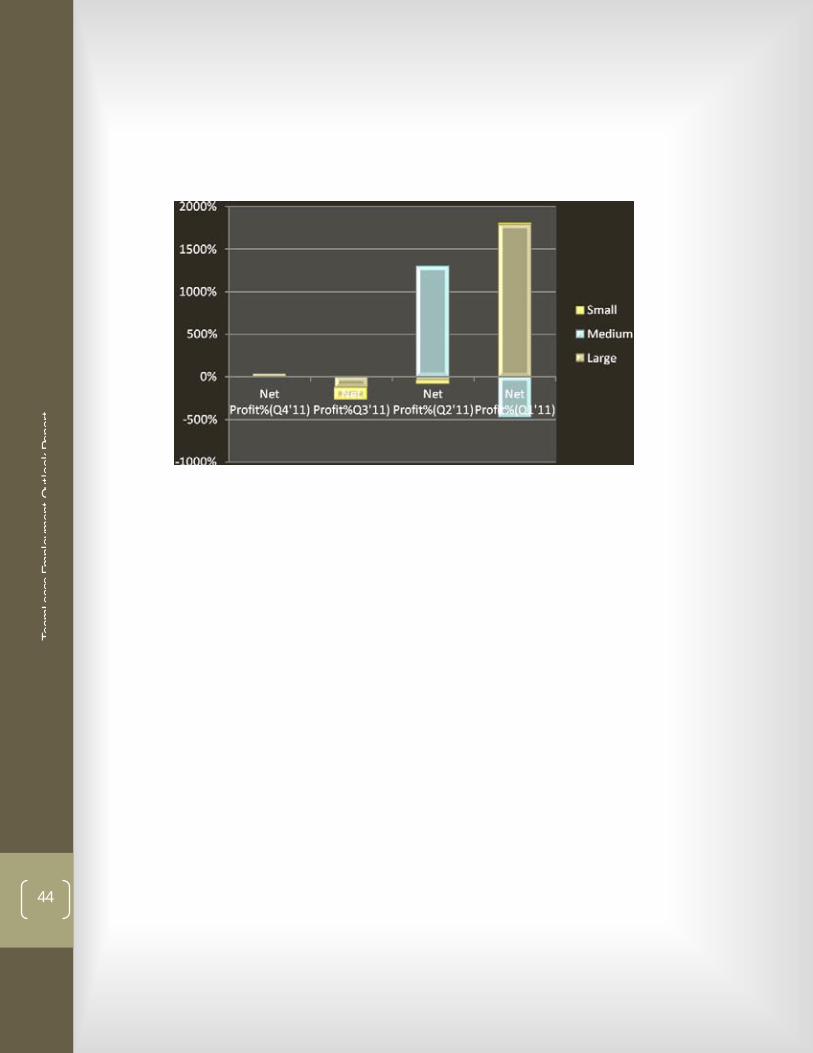

10. Literature Research findings – Business Growth trends

Avg sales growth(Q-o-Q) Avg NP growth(Q-o-Q) BOL Index values