56

THE 2016 HOME SHOPPING A COMPREHENSIVE REVIEW OF 2015 HOME SHOPPING TRENDS TRENDS REPORT

| Date post: | 28-Jul-2016 |

| Category: |

Documents |

| Upload: | epsilon-abacus |

| View: | 220 times |

| Download: | 0 times |

THE 2016 HOME SHOPPING

A COMPREHENSIVE REVIEW OF 2015 HOME SHOPPING TRENDS

TRENDS REPORT

Executive Summary

How This Report Was Compiled

Home Shopping Overview

Spending Patterns by Acorn Category

Clothing Overview

Interview: Dara O’Malley, JD Williams

Clothing: High-End & Contemporary

Interview: Rob McMahon, Madeleine

Clothing: Mature

Interview: Lynn Cordall, Damart

Clothing: Mid Market

Food & Wine

Gardening

Generalist Retail

Interview: Arun Mundle, Easylife

Gifts, Gadgets & Entertainment

Home Interiors & Household Goods

Interview: Jo Whitworth, Plumbs

Positive Uk Economy Creating Retail Success by Mark Pragnell

How Weather Influences Customers Demand

Consumer Indicators

How We Consume Entertainment In The Home

About Us: Epsilon

About Us: The Abacus Alliance

How To Get More Insight

04-05

06-07

08-09

10-11

12-13

14-15

16-17

18-19

20-21

22-23

24-25

26-27

28-29

30-31

32-33

34-35

36-37

38-39

42-43

44-45

46-47

48-49

50

51

52-53

CONTENTS

EXECUTIVESUMMARY

04

05

Introduction & Executive Summary Lara Bonney, UK Country Director Epsilon Abacus Welcome to the 2016 Epsilon Abacus Annual Trends

report, which reviews consumer spending patterns

across the home shopping sector in 2015. This report is

now in its sixth year and for six years running we see

overall growth in the market year on year. It shows a

vibrant, well established sector that is firmly embedded

in the retail landscape. Many home shopping businesses

have worked hard to put the customer at the forefront

of everything they do and are seeing the return in the

form of revenue growth. This report is made possible

by Abacus Alliance members sharing transactional

information on their customers. It is their willingness

to provide monthly updates of new purchases that

creates a dataset unparalleled in depth and breadth,

making it a reliable and robust platform for research that

can be trusted. To give value back to the contributing

members and their marketing partners, we invest our

analytical time and expertise to give relevant insight into

specific home shopping sectors to help future planning.

Key trends in 2015 were an overall revenue growth

of 11.9% year on year, with a highlight of 18.1% revenue

growth in September. The spike in September is possibly

due to a delay in sales from August and an exaggeration

in comparison to the year on year revenue decline we

saw in September 2014 due to unseasonably warm

weather. Despite minimal UK price inflation, the Average

Order Value across the Home Shopping Sector grew by

3.0% from £57.10 in 2014 to £58.80 in 2015.

In addition to showing revenue trends, we include

monthly direct mail volumes provided by Ebiquity to add

insight into some of the marketing activity that went

into generating the revenue. This of course just reports

on one part of the marketing spectrum but gives a little

perspective. Mailing volumes were down year on year

according to Ebiquity by 7.1% in 2015. An overview

of the economy and wider UK retail market in 2015

adds context to the home shopping revenue trends

in this report so we are delighted to include

Consumer Indicators created by Step Solutions

and commentary from Mark Pragnell from Capital

Economics. While postal catalogues still play a vital

role in driving sales, having a seamlessly integrated

online and offline marketing strategy is the foundation

for successful Home Shopping businesses. To shed light

on how online devices compete for attention in the

modern living room, we are pleased to showcase the

Real Living research from the Internet Advertising Bureau

(IAB). Many home shopping businesses reported that

in recent years unusual weather patterns impacted

spending trends so in this report we include research

from Planalytics. This adds some science to the

speculation that weather has an influence on sales. For

an extra dimension, we asked business owners and

senior directors for their views on the trends they saw

in their own home shopping businesses and the sector as

a whole in 2015. Our thanks go to Lynn Cordall (Damart),

Arun Mundle (Easylife), Jo Whitworth (Plumbs), Dara

O’Malley (JD Williams) and Robert McMahon (Madeleine)

for their time and contributions.

I hope you find something in this report that resonates

and gives insight that can help you better understand

consumer trends in the home shopping market. I’m keen

to hear your feedback on our findings so please email me

directly at [email protected].

Executive Summary Key Findings: • Sales in the home shopping market

increased by 11.9% YOY

• Q2 growth rate was highest of year at 14.8% YOY

• Highest growth in a single month was September at 18.1% YOY

• 3.0% growth in Ave Order Value, from £57.10 in 2014 to £58.80 in 2015

EXECUTIVE SUMMARY

06

HOW THIS REPORT WAS COMPILED

In order to qualify for this analysis sample, the selected

members had to be trading actively throughout the

calendar years of 2014 and 2015, and have provided

up-to-date transactional information to the end of

December 2015. For ease of presentation we have

aggregated Abacus merchandise categories into six

macro categories; Clothing, Food and Wine, Gardening,

Generalist Retail, Gifts Gadgets & Entertainment and

Home Interiors & Household Goods. The following

clothing sub-categories are large enough to allow

independent analysis and have been presented

separately: Contemporary & High-End, Mature and

Mid-Market. Trends are presented using indices to the

two-year monthly average. The revenue in each month

of 2014/2015 is compared to the average monthly

revenue for the analysis period. This allows us to

examine seasonal trends, as well as year on year

growth or decline. Mailing volume data for the industry

was supplied by Ebiquity (www.ebiquity.com) who collect

information monthly from their UK panel. This content has

been reproduced with their kind permission. Throughout

this report we will present mailing volume trends by

macro category and the overall home shopping sample.

We reconfigured Ebiquity’s mailing volume figures to

produce indices to the two-year monthly average. Please

note that only mailing volumes for the Alliance members

selected for this year’s Annual Trends Report sample

have been included in the mailing trends analysis. The

allocation of a member and the related Ebiquity mailing

volumes to a specific macro category was conducted by

Abacus. Mailing trends are not presented for the Food

& Wine category due to insufficient coverage.

Over 500 multi-channel retail brands have joined the Abacus Alliance, contributing 500 million transactions and approximately £20 billion spend. We identified a sample of members from each of the categories listed opposite:

“The revenue in each month of 2014/2015 is compared to the average monthly revenue for the analysis period.

This allows us to examine seasonal trends, as well as year on year growth or decline”

CLOTHINGChildren’s: Casual and dress fashion.

Contemporary: Quality contemporary clothing and accessories.

High-End: Upmarket and High-End clothing and accessories.

Mature: Products aimed at the over-50s selling classic and casual

clothing and accessories.

Men’s: Business suits, dress shirts, ties, cufflinks, scarves,

some casual clothing and shoes.

Mid-Market: Mid-priced clothing and accessories.

FOOD AND WINE Direct food purchases and wine clubs.

GARDENING Garden gates/fencing, tables and chairs,

sheds, garden accessories and plants & seeds.

GENERALIST RETAIL

Traditional large brand selling all kind of products including clothing,

furniture, home interior, appliances, collectibles etc.

GIFTS, GADGETS & ENTERTAINMENTBooks & Collectibles: Books and collectible items for the home.

Gadgets & Gifts: Sporting gadgets, binoculars, radio, stereo & home theatre

equipment, mobile phones & accessories & gift products aimed at all ages.

Home Gifts: Decorative homewares and gifts for the home.

Music & Entertainment: CDs and DVDs.

Sentimental Gifts: Artificial & cut flowers, chocolates and jewellery.

HOME INTERIORS & HOUSEHOLD GOODSHome Interiors: Practical furnishings for the home, from sofas

to cookware to shelves and storage.

Household Goods: Convenience products for the home,

including small home appliances, time saving products,

light exercise equipment and small tools.

07

08

Sales in the sample covered by the Annual Trends

Report grew 11.9% year-on-year (YOY) in 2015. This

follows three years of growth at an average rate of

10.4%, showing the continued strength in the sector.

The growth rate for the home shopping brands covered

by this report is in-line with the 15.7% increase in

non-store retail sales repored by Office for National

Statistics. The year got off to a good start with January

and February both exhibiting strong growth (+12.6%

and +13.1% YOY respectively).

Growth slowed somewhat in March (+8.4% YOY)

resulting in Q1 growth of 11.2%. April (+15.9% YOY)

and May (+15.1% YOY) were stronger than June

(+13.4% YOY) replicating the pattern seen in the first

quarter. The growth rate of 14.8% in Q2 was the

highest of the year. Q3 started with growth just below the

annual average in July (+11.2% YOY) before slowing

substantially in August (+5.9% YOY), the lowest point

of the year for sales growth. There was a strong

recovery in September (+18.1% YOY), resulting in overall

Q3 growth of 12.1%. Q4 started with above average

growth in October (+12.3%) before slowing slightly in

the final two months of the year (November +10.3%;

December +8.6%). Average Order Value (AOV was

up 3.0% compared to the previous year, going from

£57.1 in 2014 to £58.8 in 2015. The year started

with a substantial increase in AOV (+6.9% YOY in

January). This was predominantly driven by the

Gifts, Gadgets & Entertainment category (+22.1%

YOY in January) and may be the result of consumers

delaying larger purchases until after Christmas to

take advantage of January sales. The AOV growth rate

gradually reduced in February and March reaching

+0.8% in April, which showed the lowest increase

for the year. In June the AOV growth rate picked-up

again (+3.3% YOY) and remained around the annual

average until October. AOV growth accelerated in

November (+4.7% YOY), and then slowed

substantially in the last month of the year (+0.8%

YOY). Mailing Volumes were down 7.1% YOY

in 2015. This follows a decline of 8.1% in 2014.

REVENUE AND MAILING VOLUMES, 2014-2015

HOME SHOPPING OVERVIEW

09

The year started with increased mailing volumes in

both January (+11.9% YOY) and February (+12.0%

YOY) before declining in March (-13.4% YOY). As March

is the largest mailing month in Q1, this resulted in

mailing volumes increasing by 1.7% in Q1. The trend

for declining mailing volumes continued into Q2 with

a drop of 26.3% in April. This was the biggest decline

throughout the year, and with a drop in May (-16.3%

YOY) and a flat June (+0.0% YOY) Q2 was down 15.1%

YOY. The trend continued into Q3 with a decline of 17.1%.

October saw a decline of 7.8% YOY before an increase

towards the end of the year (November +5.2% YOY;

December +17.5% YOY). This resulted in an overall

increase of 2.2% in Q4.

AOV YEAR-ON-YEAR CHANGE, 2014-2015

REVENUE-ON-YEAR CHANGE, 2014-2015

SPENDING PATTERNS BY ACORN CATEGORY

10

Acorn, created by CACI, is a geodemographic segmentation of the UK’s population. It segments households, postcodes and neighbourhoods into 6 categories, 18 groups and 62 types. By analysing significant social factors and population behaviour, it provides precise information and an in-depth understanding of the different types of people. For the purposes of this report we have excluded the sixth category, Not Private Households. Below you can find descriptions for each Acorn category.

Affluent AchieversThese are some of the most financially successful people in the UK. They live in wealthy, high status rural, semi-rural and suburban areas of the country. Middle aged or older people, the ‘baby-boomer’ generation, predominate with many empty nesters and wealthy retired. Some neighbourhoods contain large numbers of well-off families with school age children, particularly the more suburban locations. Usually confident with new technology and managing their finances, these people are established at the top of the social ladder. They are healthy, wealthy and confident consumers.

Rising ProsperityThese are generally younger, well educated, and mostly prosperous people living in our major towns and cities. Most are singles or couples, some yet to start a family, others with younger children. Often these are highly educated younger professionals moving up the career ladder. Most live in converted or modern flats, with a significant proportion of these being recently built executive city flats. Some will live in terraced town houses. While some are buying their home, occasionally through some form of shared equity scheme, others will be renting. These people have a cosmopolitan outlook and enjoy their urban lifestyle. They like to eat out in restaurants, go to the theatre and cinema and make the most of the culture and nightlife of the big city.

Comfortable CommunitiesThis category contains much of middle-of-the-road Britain, whether in the suburbs, smaller towns or the countryside. All lifestages are represented in this category. Many areas have mostly stable families and empty nesters, especially in suburban or semi-rural locations. There are also comfortably off pensioners, living in retirement areas around the coast or in the countryside and sometimes younger couples just starting out on their lives together. Generally people own their own home. Most houses are semi-detached or detached, overall of average value

for the region. Incomes overall are average, some will earn more, the younger people a bit less than average. Those better established might have built up a degree of savings or investments. Most people are comfortably off. They may not be very wealthy, but they have few major financial worries.

Financially StretchedThis category contains a mix of traditional areas of Britain. Housing is often terraced or semi-detached, a mix of lower value owner occupied housing and homes rented from the council or housing associations, including social housing developments specifically for the elderly. This category also includes student term-time areas. There tends to be fewer traditional married couples than usual and more single parents, single, separated and divorced people than average. These people are less likely than average to use new technology or to shop online or research using the internet, although will use the internet socially. Overall, while many people in this category are just getting by with modest lifestyles a significant minority are experiencing some degree of financial pressure.

Urban AdversityThis category contains the most deprived areas of large and small towns and cities across the UK. Household incomes are low, nearly always below the national average. The level of people having difficulties with debt or having been refused credit approaches double the national average. The numbers claiming Jobseeker’s Allowance and other benefits is well above the national average. Levels of qualifications are low and those in work are likely to be employed in semi-skilled or unskilled occupations. The housing is a mix of low rise estates, with terraced and semi-detached houses, and purpose built flats, including high rise blocks. These are the people who are finding life the hardest and experiencing the most difficult social and financial conditions.

SPENDING PATTERNS BY ACORN CATEGORY

11

SPEND GROWTH BY ACORN CATEGORY, 2014-2015

SPENDING PATTERNS BY ACORN CATEGORY, 2014-2015REV TOTAL CH

70

90

110

130

150

170

Affluent Achievers Rising Prosperity Comfortable Commnunities Financially Stretched Urban Adversity

16.5%15.9%

13.2%12.7%

10.2%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

16.0%

18.0%

Urban Adversity Financially Stretched Comfortable Communities Affluent Achievers Rising Prosperity

As in the previous two years, in 2015 growth was higher in the less-affluent Acorn categories with both Urban Adversity and Financially Stretched showing an increase in spend of over 15% compared to 2014. Consumers in these categories tend to spend more of their annual budget in the pre-Christmas period (July to November), while consumers in more affluent categories spend proportionally more in the first six months of the year.

CLOTHINGOVERVIEW

12

Clothing has been one of the most successful

categories in home shopping over the last five years,

with an astonishing average growth rate of 13.3% per

annum. The trend continued in 2015, with the category

up 10.7% Year-On-Year (YOY) making this the sixth year

of continuous growth. The year kicked-off with sales up

9.7% YOY in Q1 led by a very positive January (+11.0%

YOY). The pace of growth increased going into Q2

(+13.1% YOY) with the strongest performance in April

(+14.0% YOY) and June (+13.4% YOY). Growth slowed

going into Q3, with July (+7.4% YOY) and August (+7.0%

YOY) both below the average for the year. September

was particularly strong (+17.2% YOY), possibly due to

a poor September in 2014. As this is the largest month

of Q3 in terms of revenue, the strong growth in sales in

September resulted in Q3 being up 12.1% overall. Q4 grew

in-line with the annual rate (+9.2% YOY) led by a strong

performance in November (+12.1%). December was the

worst performing month of the quarter with a growth of

“just” 5.2%. The Average Order Value (AOV) in the category

declined compared to the previous year, although

very marginally (-0.1% YOY). This is the third year in

a row that the AOV has declined in Clothing (-2.7%

in 2013 and -0.5% in 2014). However, the rate of

decline has now slowed significantly. This means

that the growth experienced in the category in 2015

and the previous two years was driven by existing

customers placing more transactions and/or more

consumers coming to the marketplace. Mailing

volumes were down quite significantly in 2015 (-14.5% YOY)

There were particular declines in May (-29.4% YOY), August

(-27.3%) and September (-31.1%). The biggest increase

was in November (+14.1% YOY), possibly indicating that

retailers are pushing larger campaigns “deeper” into

the Autumn/Winter season. In the following

pages we will examine trends for the main

Clothing sub-categories: High-End & Contemporary,

Mid-Market and Mature.

CLOTHING OVERVIEW

13

REVENUE AND MAILING VOLUMES, 2014-2015

0000

Over time we are starting to see changing patterns in

customer loyalty. Older age customers are more loyal

than new younger age customers so when older age

customers move on, we have to work harder to get new

younger age customers to become loyal. To respond to

this, we have put a stronger focus on segmentation so we

can treat and talk to customers differently. It is becoming

apparent that we have to become much more shrewd

and knowledgeable in the way we segment, communicate

with and promote to our customer. Our aim is one to one

customer marketing but until we can truly make this

happen, clever segmentation is the next best thing. We

want to think of our customers as individuals and not a

number. For us, getting contact frequency right, product

customisation and making everything we do relevant to

the customer is key.

Dara O’Malley, Head of Marketing at JD Williams

In 2015 we saw our more mature customers continuing

to become more digitally aware with the online channel

becoming more important. We found that the tablet was

the fastest growing online order device for our older

customers (age 55 – 75), whilst for those under 50s

the fastest growing device is mobile. Whilst the digital

channel was strong for us and it is becoming increasingly

more important, we are conscious not to take our eye

off the more traditional channels such as direct mail and

press which have been the bedrock of our marketing. We

believe that whatever channel we use, we need to give a

consistent experience for the customer.

We were more promotional in 2015 because we feel we

have to work harder to get the older customer to spend

money with us. We seem to be competing with spend

on experience activity such as eating out and travel as

well as spend on products and we found that we had to

generate more orders per customer to gain the same

value as previous years. Promotions are not responding

as well as they used to, and I think it’s because there is

so much choice and noise in the market. The customer is

exposed to a variety of style, price and promotion offered

by specialist retailers as well as traditional retailers. We

have more to compete against and need to respond

by adding variety to our product and making our brand

something that our customers really connect with.

INTERVIEW WITH…

14

“Our aim is one to one customer marketing but until we can

truly make this happen, clever

segmentation is the next best thing”

000015

This calendar year has been challenging for our market

and our impression is that consumer confidence in the

mature market, especially from those who rely on fixed

incomes from stocks and shares has been affected by

the recent stock market downturn and the uncertainty

created by the EU Referendum. Some older customers

seem to be reigning in spend as a result.

In 2015, Black Friday and Cyber Monday had the effect

of pulling Christmas sales forward for us so going into

the future we will plan our business slightly differently

to accommodate it. The use of digital gives a window

of opportunity to get extra sales before Christmas from

those people who order during the promotional period.

Last year Cyber Monday immediately followed Black

Friday but there is a separation in 2016 so it would be

interesting to see if this affects spending patterns.

In my view, the biggest thing for multi channel retailers

to focus on going into 2016 is to put customers at the

heart of their marketing strategy, make sure they are

being relevant to customers and ensure that they are

maximising the ROI on marketing spend. If you can get

the right mix of traditional higher cost paper led marketing

activities with lower cost digital activity, you have more

chance of communicating with customers in the right

way for them and giving them a personalised experience

of your brand.

“The use of digital gives a window of opportunity to get extra sales before

Christmas from those people who order during the Black Friday and Cyber

Monday promotional period”

CLOTHINGHIGH END & CONTEMPORARYThe High-End & Contemporary Clothing category grew 13.4% Year-On-Year (YOY) in 2015. This follows growth of 8.5% YOY in 2014, showing that demand in this sector continues to be very robust. There was strong growth across all quarters, with Q4 showing the biggest increase in sales YOY (+17.5%). The biggest month of the year for the category is November and there was very strong growth during this month (+24.5%). September was the best performing month in terms of growth (+30.9% YOY). This might be due to the month performing poorly in 2014 (-8.4% YOY compared to 2013). The Average

Order Value (AOV) in the High-End & Contemporary Clothing category was marginally higher in 2015 (+0.7%) compared to the previous year. This indicates that the majority of the revenue growth was driven by a higher number of transactions in the category rather than an increase in spend per order. Mailing volumes were very similar to the previous year with a very slight decline (-1.2% YOY). There was a significant decline in mailings between April and June (-56.9% YOY), but this was contrasted by significant increases in February (+61.5% YOY) and December (+120.2% YOY).

16

REVENUE AND MAILING VOLUMES, 2014-2015

HIGH-END & CONTEMPORARY: Clothing

17

0%

2%

4%

6%

8%

10%

12%

18-24 25-29 30-34 35-39 40-44 45-49 50-54 55-59 60-64 65-69 70-74 75-79 80-84 85+0%

10%

20%

30%

40%

50%

60%

Less than £10,000

£10,000 -£14,999

£15,000 -£19,999

£20,000 -£24,999

£25,000 -£29,999

£30,000 -£39,999

£40,000 -£49,999

£50,000 -£59,999

£60,000 & Over

HIGH-END & CONTEMPORARY CLOTHING GREW

BY 13.4% YOY IN 2015

Contemporary & High End Clothing UK Contemporary & High End Clothing UK

AGE DISTRIBUTION INCOME DISTRIBUTION

30.9GROWTH%YOY

SEPTEMBER SHOWED

00

segmentation to understand what our customers buy

across the home shopping sector. We were able to

use the share of wallet information to tailor customer

vouchers and targeted incentives in a more intelligent

way for more impact and a greater return. When offering

incentives and promotions to customers, we are always

mindful of the impact they have on brand perception and

identity. It’s important to maintain our brand values, while

understanding that we need to offer relevant and targeted

incentives and promotions to remain competitive and

provide what customers would like and expect. We are

very engaged with Black Friday promotions and we will

continue to use this as an activity to gain market share.

We believe that we would lose out if we didn’t run any

promotions during this time; anyone in our sector who

ignores this opportunity would find themselves left out

in the cold. By developing these offers we have managed

to carve out a better level of customer service, including

a dedicated free-phone line, which has resulted in our

customers becoming more loyal. We provide free returns

on all orders – this is no longer seen as an offer, but

just an expectation by consumers who are now used to

Rob McMahon, Director UK, Marketing and Sales at Madeleine

The main purchasing trend we saw in 2015 was an

increase in seasonal buying. Customers continued

to buy products from our spring and summer

collection well into autumn due to the delay of the

colder weather. It seems that people buy for the

weather at the moment rather than planning ahead

for the next season. 2015 saw the continued shift

towards people buying online, we’re not alone in

saying that online is becoming the order channel of

choice. However, we understand the importance of

the catalogue in getting people onsite and because

of this the catalogue remains an integral part of our

marketing strategy, enabling us to convey the quality

of our brand effectively and it is a strong motivator

to purchase. By making our catalogue a high end

printed item with coffee table appeal, it stays in

the home much longer and serves as a continuing

reminder of our brand. We often receive orders

four or five months after someone has received the

catalogue. In terms of sending the catalogue to the

right people to attract new customers, we have had

great success through our work with Abacus.

We had an explosive growth year through a

combination of using Abacus solutions to target

catalogues at high quality prospective customers

and then making it simple for them to order online.

We also used Abacus customer segmentation

solutions such as data tagging and share of wallet

18

“We provide free returns on all orders.

This is no longer seen as an offer,

but an expectation by consumers

who are used to seeing this across clothing retailers”

INTERVIEW WITH…

seeing this across clothing retailers. We saw a positive

performance across most of our marketing channels

in 2015 and this led to year on year revenue growth.

Online advertising, banner adverts and classic DR

adverts all continued to work well for us. We strive to

speak to our customers with a single voice, making sure

that at every touch point the messages are consistent.

We adapt our messages appropriately to the different

channels to ensure we are communicating in the best

way to the customer. The main challenge we face is

attribution. It is difficult to understand the role that each

channel played in driving a customer to order and to

know how we allocate response to each channel. This

is something we will continue to work on in 2016 and

beyond. In 2016 we will focus our efforts on a greater

push for cross channel and cross platform marketing with

the goal to become more specialised in the marketing

we use to reach our customers. We would like to create

mobile and online advertising messaging consistent

with our offline messaging to ensure that the brand is

communicated cohesively to maintain the brand offering.

The main challenge is to stay up to date with the trends

and technology and continuing to communicate well

with our customer. Our long term aim is for Madeleine

to be a quality brand that is not perceived as a fad or

passing trend. Our mantra is “Fashion is the challenge of

standing out of the crowd whilst staying on trend”.

“By making our catalogue a high end printed item with coffee table appeal, it stays in the

home much longer and serves as a continuing reminder of our brand”

19

CLOTHINGMATUREThe Mature Clothing category grew by 6.8% in 2015, a lower rate compared to 2014 which saw sales growth of 12.1% Year-On-Year (YOY). Growth was consistent in the first half of the year (+8.3% in Q1 and +8.4% in Q2) before it accelerated in Q3 (+10.4% YOY). The worst performing quarter was Q4, with growth of just 1.0% YOY. The best performing month was September which saw growth of 20.2% whilst December was particularly poor with a decline of 11.9%. This is in stark contrast to 2014 which had seen September growth below the average for the year (+7.7 YOY v 12.1% for 2014 overall) and

very strong growth in December 2014 (+19.1% YOY). These changes may be caused by unusually warm weather depressing winter clothing sales in September 2014 and December 2015. The Average Order Value (AOV) in the category was marginally higher than in the 2014 (+0.7% YOY). This indicates that the majority of the revenue growth was driven by a higher number of transactions rather than an increase in spend per order. Mailing volumes were significantly lower than in the previous year (-24.2% YOY), with the biggest decline being in May (-42.5% YOY).

20

MATURE: Clothing

21

REVENUE AND MAILING VOLUMES, 2014-2015

IN 20156.8% YOY GROWTH

SEPTEMBERYOY GROWTH IN

Mature Clothing UK Mature Clothing UK

AGE DISTRIBUTION INCOME DISTRIBUTION

0%

2%

4%

6%

8%

10%

12%

14%

16%

18-24 25-29 30-34 35-39 40-44 45-49 50-54 55-59 60-64 65-69 70-74 75-79 80-84 85+0%

5%

10%

15%

20%

25%

Less than £10,000

£10,000 -£14,999

£15,000 -£19,999

£20,000 -£24,999

£25,000 -£29,999

£30,000 -£39,999

£40,000 -£49,999

£50,000 -£59,999

£60,000 & Over

22

grew and media inserts performed exceptionally well.

“Off the Page ads” performed a little more patchily over

the year but are still strong. A key focus for us in 2015

was to reduce our lead-time to market and get quicker at

doing things. It’s no longer acceptable to take 18 weeks

to put a catalogue out like it was years ago so we are

shaving time from all parts of the process. We are also

trying to be more effective with our marketing by using

more segmentation and differentiated contact plans to

give the customers what they really want while reducing

paper and postage costs.

The biggest initiative that we invested in is our customer

service. We invested in our people by carrying out

extensive customer service training. We went through

accreditation for customer service and we compared well

against John Lewis.

A big challenge we faced in 2015 was the discounting

mentality across the board. Customers shopping any

channel now expect a deal or to be incentivised. How

the market has traded online has trained the customers

to expect this, whether it’s online or offline, distance

or store.

Lynn Cordall, Commercial Director at Damart

As a home shopping clothing retailer aimed at the

older age customer, we saw a few interesting trends

in 2015. While in the past customers used to order

early in the season, we saw the “buy now, wear now”

concept speeding up; I think due to commoditisation

on the high street for some product areas, but also

due to the uncertain weather patterns we have

seen in recent years. Customers don’t really want to

spend until they need it. This presented a challenge

around service and delivery expectations because

customers want things to arrive much more quickly,

so we are offering more flexible options. Our

customers with an average age of 70 are becoming

more comfortable with online purchasing because

we saw an acceleration of orders coming through

on tablets and mobiles. The dominant device is the

tablet but mobile purchasing is growing rapidly and

while our overall percentage of online sales is still

small, I think mobile sales may catch up or exceed

tablet sales in the next few years.

With regard to marketing channels, most of them

worked well in 2015. Catalogues have always

performed well for us, our online channel activity

“We understand that a customer aged 55 will have a different

outlook to a customer who is 80”

INTERVIEW WITH…

It’s an established habit now, not just a recession impact

behaviour that we think will continue. This doesn’t

necessarily mean money off so we have to be more

creative with our offers. We found high street retailers

gaining ground into the home shopping space by offering

discounts. Black Friday and Cyber Monday had a big

impact on sales; we noticed 87% of similar companies

to ours were offering an average of 30% discount over

this period. We felt that the impact of Black Friday

brought the sales forwards which then effected the

last 4 weeks of the year. After testing we found that

some of our customers did not like Black Friday so next

year we will group our customers to ensure that we

tailor these offers in a different way. It is important for

Home Shopping companies to look at promotions and

incentives that work across different channels.

The future for us is personalisation, as one size doesn’t

fit all. We are doing a lot of research into how customers

react to incentives and promotions. For example, we

understand that a customer aged 55 will have a different

outlook to a customer who is 80. We would like to

automate the personalisation process in the future

and building a Single Customer View database is key to

helping us to understand and segment our customers

for a one to one experience. We plan to test everything.

Small changes can have big impacts.

Going into 2016 we understand that while differentiation

and personalisation is something we want to focus on in

2016, we mustn’t lose sight that people are buying the

product and brand and we need to get this right. We will

be ramping up testing around differentiated content and

focusing on a contact strategy for different customer

segmentations. We want to remove the fact that price

or promotion is the determining factor, we want the

customer to buy because of the brand. Buying online

is very much about price and there is always someone

who can undercut you. Differentiation is crucial.

“Black Friday and Cyber Monday had

a big impact on sales; we noticed

87% of similar companies to

ours were offering an average of 30%

discount over this period”

23

CLOTHINGMID MARKETThe Mid-Market Clothing category grew by 12.5%

Year-On-Year (YOY) in 2015. This was a similar rate of

growth to the previous year (+12.9% YOY in 2014). There

was growth across all months of the year, with June

exhibiting the strongest YOY growth (+21.1%) followed

by September and November (both at +17.0% compared

to 2014). This makes it the second year in a row that

November has had strong growth (+16.1% YOY in 2014).

The weakest sales growth was in July, with revenue up

“just”+4.0% YOY. The Average Order Value (AOV) in the

Mid-Market Clothing category was exactly the same YOY.

This indicates that the revenue growth was driven by a

higher number of transactions rather than an increase in

spend per order. Mailing volumes were down 11.6% YOY.

At the beginning of the year mailing volumes increased,

with January and February volumes up 33.5%, but from

March until October there was a decline in every month,

resulting in a drop of 24.5% during this period. There was

a significant increase in November (+48.9% YOY), but this

didn’t continue in December as mailing volumes were up

only marginally in that month (+0.5% YOY).

24

MID MARKET: Clothing

25

REVENUE AND MAILING VOLUMES, 2014-2015

12.5% GROWTH

IN 2015

YO

Y

JUNE HAD THE GROWTH OFSTRONGEST

21.1%YOY

Mid Market Clothing UK Mid Market Clothing UK

AGE DISTRIBUTION INCOME DISTRIBUTION

0%

2%

4%

6%

8%

10%

12%

18-24 25-29 30-34 35-39 40-44 45-49 50-54 55-59 60-64 65-69 70-74 75-79 80-84 85+0%

5%

10%

15%

20%

25%

30%

Less than £10,000

£10,000 -£14,999

£15,000 -£19,999

£20,000 -£24,999

£25,000 -£29,999

£30,000 -£39,999

£40,000 -£49,999

£50,000 -£59,999

£60,000 & Over

FOOD & WINEThe Food & Wine category had a very strong 2015 with sales growth of 17.5% Year-On-Year (YOY). As you can see in the graph, the category is heavily weighted towards the end of the year due to increased demand during the pre-Christmas period. November, the second biggest month of the year behind December, saw exceptional sales growth of 28.4% YOY. December also exhibited very strong growth (+18.0% YOY) which contributed to Q4 being the strongest quarter of the year (+22.0% YOY). Q4 makes up nearly 40% of the annual revenue in

the Food & Wine category, so the performance during this quarter deeply affects (in this case positively) the performance of the entire year. The first three quarters of the year saw fairly consistent YOY growth of around 15% (+14.6% in Q1, +14.7% in Q2 and +15.5% in Q3). The Average Order Value (AOV) in the Food & Wine category was marginally higher in 2015 compared to the previous year (+1.3% YOY). This indicates that the majority of the revenue growth was generated by a higher number of transactions rather than an increase in spend per order.

26

FOOD & WINE

27

REVENUE AND MAILING VOLUMES, 2014-2015

17.5%

GROWTHYOY

28.4YOY

PE

RC

EN

T

DECEMBERGROWTH IN

Food & Wine UK Food & Wine UK

AGE DISTRIBUTION INCOME DISTRIBUTION

0%

2%

4%

6%

8%

10%

12%

14%

18-24 25-29 30-34 35-39 40-44 45-49 50-54 55-59 60-64 65-69 70-74 75-79 80-84 85+0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

Less than £10,000

£10,000 -£14,999

£15,000 -£19,999

£20,000 -£24,999

£25,000 -£29,999

£30,000 -£39,999

£40,000 -£49,999

£50,000 -£59,999

£60,000 & Over

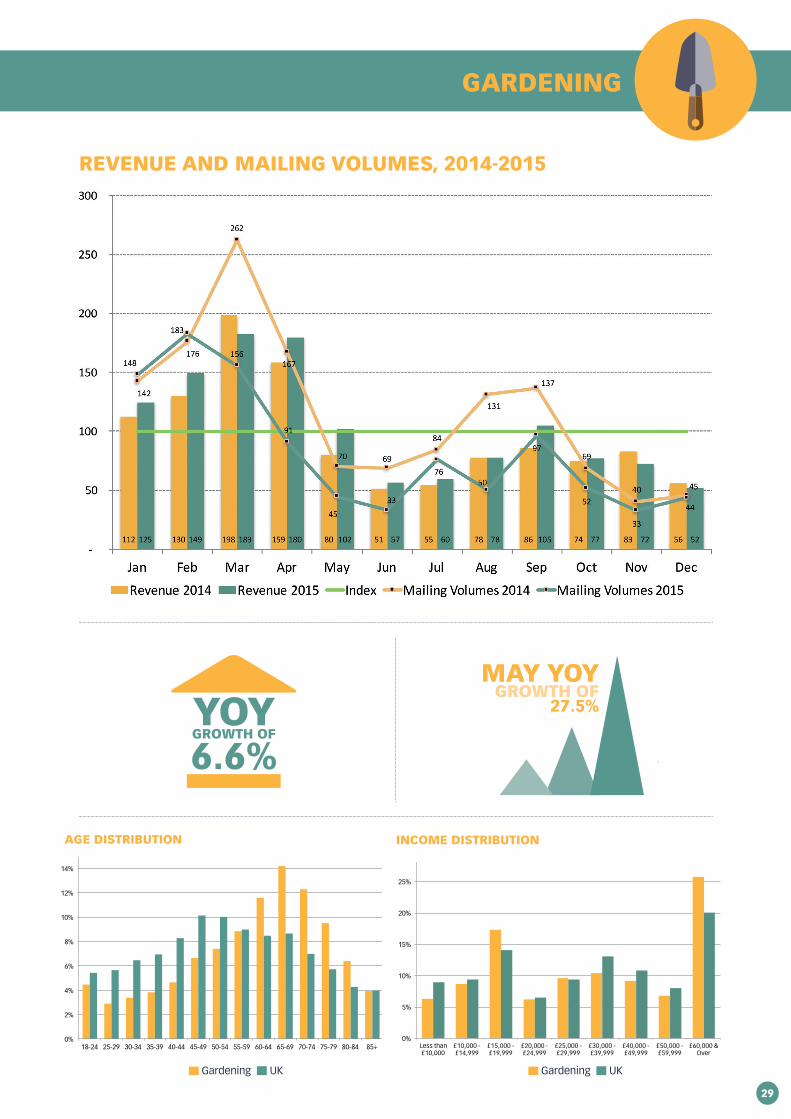

GARDENINGSales in the Gardening category grew by 6.6% Year-On-Year (YOY) in 2015. This represented a marked improvement over the previous two years which had seen declines in revenue (-9.4% YOY in 2013 and -0.3% in 2014). The growth was concentrated in the first nine months of the year (Q1 +3.7% YOY, Q2 +16.7% YOY and Q3 +11.2%) whereas the end of the year was more of a struggle with revenue down 5.7% in Q4. May saw the strongest annual growth (+27.5% YOY) while November saw the biggest decline (-13.3% YOY). The YOY decline we saw in November might be due to the seasonal pattern reverting to the

long term average after the exceptionally strong growth we saw in that month the previous year (+17.4% YOY in November 2014). There was a small increase in Average Order Value (AOV) in 2015 compared to the previous year (+2.1% YOY) which indicates that the revenue growth was mostly due to a greater number of transactions being made in the category. Mailing volumes were up in January (+4.2% YOY) and February (+4.0% YOY) but down significantly in the March to June period. This translated in an overall decline of -27.8% YOY in 2015.

28

GARDENING

29

YOYGROWTH OF

6.6%

REVENUE AND MAILING VOLUMES, 2014-2015

MAY YOY GROWTH OF

27.5%

Gardening UK Gardening UK

AGE DISTRIBUTION INCOME DISTRIBUTION

0%

2%

4%

6%

8%

10%

12%

14%

16%

18-24 25-29 30-34 35-39 40-44 45-49 50-54 55-59 60-64 65-69 70-74 75-79 80-84 85+0%

5%

10%

15%

20%

25%

30%

Less than £10,000

£10,000 -£14,999

£15,000 -£19,999

£20,000 -£24,999

£25,000 -£29,999

£30,000 -£39,999

£40,000 -£49,999

£50,000 -£59,999

£60,000 & Over

GENERALIST RETAILThe Generalist Retail category grew by 7.5% in 2015. This makes it the fifth year in a row of increased revenue in the category. There was growth across all quarters, although the first half of the year was stronger than the second half. Q2 had the biggest Year-On-Year (YOY) growth at 15.3% whilst the weakest growth was in Q4 (+2.2% YOY). The strongest month was April (+28.8% YOY) but there was growth across all months with the exception of August (-5.7% YOY) and November (-3.1% YOY). In 2014 November had 18.3% growth so this slight decline may be

the result of returning to normal revenue levels. The Average Order Value (AOV) in the Generalist Retail category was quite significantly higher in 2015 (+7.2% YOY). This can explain a large part of the YOY growth in this category. Mailing volumes grew by 6.9% YOY. The timing of mailing campaigns changed quite significantly, with more being mailed towards the end of the year than in 2014. Between July and October there was a decline of 36.7% in mailing volumes but in the final two months of the year mailings more than double (+102.3% YOY).

30

GENERALIST RETAIL

31

REVENUE AND MAILING VOLUMES, 2014-2015

7.5% YOY GROWTH

IN 2015

APRIL HAD THE

GROWTH OFSTRONGEST

28.8%YOY

Generalist Retail UK Generalist Retail UK

AGE DISTRIBUTION INCOME DISTRIBUTION

0%

2%

4%

6%

8%

10%

12%

18-24 25-29 30-34 35-39 40-44 45-49 50-54 55-59 60-64 65-69 70-74 75-79 80-84 85+0%

5%

10%

15%

20%

25%

Less than £10,000

£10,000 -£14,999

£15,000 -£19,999

£20,000 -£24,999

£25,000 -£29,999

£30,000 -£39,999

£40,000 -£49,999

£50,000 -£59,999

£60,000 & Over

0000

and this worked with a fairly high degree of success. This

success, as well as new customer recruitment mailings

using Abacus Alliance data, grew our customer file

exponentially and we saw a clean profit on our campaigns

as a result.

We explored a lot more dynamic and analytical targeting

in 2015 and this led to significant increases in conversion.

We wanted to increase website conversion without

negating the appeal for digitally recruited customers

from channels such as organic search, PPC and affiliates.

This process involved singling out individual segments

based on source and customer type and giving each

one its unique dynamic proposition and journey. New

customers who were labelled as not digitally savvy

would get more confidence statements and slightly more

clicks to checkout. The returning customer would have a

reduced path to checkout with product selections based

on previous viewing history. By combining these tactics,

we improved our overall conversion rate by 30%.

National press insertions are still the heart of our media

buying for the business. In 2015 this channel seemed

to be erratic which without close supervision could

have affected us badly. Managing our media booking in-

house provided us with the critical relationship with the

publications and insights to navigate successfully through

these pendulum swings of distribution.

We saw consumer spend dip in the run up to the

general election, but we recovered well with very good

performance in quarter three. The suspicion is that the

Arun Mundle, Managing Director at Easylife

In 2015 we saw consumer spending make a significant

recovery compared to the past 5 years, in terms of

physical demand and average spend which improved

significantly across all sectors. The overall increase was

not quite back to pre-recession response, but a great leap

forward. We saw a growth in online trade, however, our

proportionate organic traffic remained static; ultimately

our offline activity is still the driving force behind the sales.

The website is simply being used more as the channel

of preference to make the purchase. With consumer

spending on the increase, we altered our customer direct

mail strategy by putting more emphasis on contacting

customers with recent purchases rather than focusing on

how much they spent. We assumed the general increase

in consumer confidence and increased spending power

would naturally increase the average order value anyway

32

“In 2015 we saw consumers spending

make a significant recovery compared to the past 5 years”

INTERVIEW WITH…

00000033

demand was merely delayed. Cold weather is one of

the critical ingredients in increasing the propensity to

spend and the warm autumn did have a huge effect on

demand. Overall demand was lower than anticipated,

but it did create a healthy spread across the quarter.

Normally, we see a big scramble for weather related

products in a condensed period of time as soon as the

weather turns. This puts a lot of pressure on stock control

and fulfilment operations. As this didn’t happen it gave

us a better opportunity to spread resources across the

period, achieving better efficiency to counter balance the

reduction in demand. It was these events or lack of them

in early October that led us not to put too much emphasis

on Black Friday/Cyber Monday or flash sales generally.

The need for promotions seems self-fulfilling. Once

consumers get used to a promotion, the expectation is

set. On that basis, we tend to stay away from clearance

or knocked down prices unless we are clearing obsolete

stock. I would say that promotions do work, but you must

be committed to a long-term strategy because dipping

in and out can have a negative effect on the overall

bottom line.

In 2016 we will continue to focus on our core business,

making it work harder and more efficiently. While

consumer demand has been on the rise, the last five

years of lean trade has taught us to continue the same

strict monitoring but benefit from an increased response

to generate an increased net operating profit. We have

been quite ruthless in removing all the activities that

were “nice to have” but added no real value to the

business, as this was creating unnecessary distractions.

We will be looking to revisit everything we do well and do

it even better.

“The website is simply being used as the channel of

preference to make the purchase”

GIFTS, GADGETS & ENTERTAINMENT

The Gifts, Gadgets and Entertainment category grew by 12.8% in 2015. There was increased sales growth across the first three quarters of the year (+25.3% in Q1; +25.5% in Q2; +18.0% in Q3) but there was a small decline in Q4 (-0.5% Year-On-Year), the biggest revenue quarter of the year and accounting for over 40% of 2015 sales. This was driven by a decline in November (-7.5% YOY), the biggest month of the year in terms of revenue. The largest growth was in May (+35.7% YOY). The first half of the year in 2014 saw a decline in revenues, so the 2015 increase during this period may in part be a

recovery from then. The Average Order Value (AOV) in the Gifts, Gadgets & Entertainment category was significantly higher in 2015 than in 2014 (+16.6% YOY). This indicates that there were actually fewer transactions in 2015 than the previous year, and that revenue growth was driven entirely by the increased spend per order. Mailing volumes were up 10.7% YOY. There were significant increases in mailing volumes in June (+47.1% YOY) and July (+55.5% YOY), but also some declines in April (-12.0% YOY) and November (-10.0% YOY).

34

GIFTS, GADGETS & ENTERTAINMENT

35

REVENUE AND MAILING VOLUMES, 2014-2015

35.7%YOY

IN MAYGROWTH

Gadgets, Gifts and Entertainment UK Gadgets, Gifts and Entertainment UK

AGE DISTRIBUTION INCOME DISTRIBUTION

YOYGROWTH

12.8PERCENT

IN 2015

0%

2%

4%

6%

8%

10%

12%

18-24 25-29 30-34 35-39 40-44 45-49 50-54 55-59 60-64 65-69 70-74 75-79 80-84 85+0%

5%

10%

15%

20%

25%

30%

Less than £10,000

£10,000 -£14,999

£15,000 -£19,999

£20,000 -£24,999

£25,000 -£29,999

£30,000 -£39,999

£40,000 -£49,999

£50,000 -£59,999

£60,000 & Over

HOME INTERIORS & HOUSEHOLD GOODSThe Home Interiors & Household Goods category grew by 13.6% in 2015. This is slightly lower than the previous year (+15.1% Year-On-Year) and is the fifth successive year of category growth. There was growth across all months, with the biggest growth seen in September (+24.2% YOY) and October (+22.2% YOY.) The lowest level of growth was in August (+4.5% YOY) and January (+5.0% YOY.) In 2014 there was exceptional growth in January (+27.2% YOY,) which may explain why the growth in January 2015 was

more restrained compared to other months. There was a decline in the Average Order Value (AOV) for the Home Interiors & Household Goods category of 2.8%. This indicates that the revenue growth was a result of an increase in the volume of transactions rather than a higher spend per order. Mailing volumes were marginally higher in 2015 (+1.6% YOY.) The biggest decline in mailings was in April (-28.0% YOY), whilst the biggest increase was in February (+24.3% YOY) closely followed by January (+21.1% YOY).

HOME INTERIORS & HOUSEHOLD GOODS

36

HOME INTERIORS & HOUSEHOLD GOODS

37

REVENUE AND MAILING VOLUMES, 2014-2015

HOME INTERIORS & HOUSEHOLD

GOODS SAW 24.2% YOY GROWTH

IN SEPTEMBER13.6%

GROWTHYOY

Home Interiors & Household Goods UK Home Interiors & Household Goods UK

AGE DISTRIBUTION INCOME DISTRIBUTION

0%

2%

4%

6%

8%

10%

12%

14%

18-24 25-29 30-34 35-39 40-44 45-49 50-54 55-59 60-64 65-69 70-74 75-79 80-84 85+0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

Less than £10,000

£10,000 -£14,999

£15,000 -£19,999

£20,000 -£24,999

£25,000 -£29,999

£30,000 -£39,999

£40,000 -£49,999

£50,000 -£59,999

£60,000 & Over

0000000038

has been positive we are also taking part in one hour

programmes on a TV shopping channel that explains the

process of the re-upholstering. We are also testing some

video marketing which is proving to be a good way to

communicate a more involved product. Going into 2016,

the digital channels will be a focus for us with tests via

Affiliate and Facebook advertising.

To support our service objectives, in 2015 we used data

to understand and communicate with our customers

more frequently through the buying cycle and after

dispatch. We called more customers to talk them through

the ordering process and afterwards sent them a thank

you pack with incentives to order again, coupled with a

phone call to ask how the order process was for them.

We find that our customers really appreciate this more

Jo Whitworth, Marketing Development Manager at Plumbs

A recent trend I have seen is that more people seem to

be looking for personalised and niche items and I believe

that home shopping businesses are in a good position

to offer those things. As a bespoke furniture covers and

re-upholstery business, we offer a very hands-on, face–to-

face service which gives us a positive point of difference.

For our target market, which is the over 50’s, the

emphasis on giving friendly advice and having someone

to help you through the buying process can create a good

buying experience for the customer and consequently

good advocacy.

We recently reviewed our processes and found that our

customers value service and quality above everything

when deciding on a large item purchase. There is a lot

of good brand imagery from furniture home shopping

businesses in the market at the moment which makes

things look high quality, fresh and easy to purchase. This is

attractive to consumers and is good for all of us in raising

awareness that quality products are available from home

shopping businesses at affordable prices.

Bespoke furniture covers aren’t something you usually

just order through the website, so our marketing objective

is to get people to ask for a home visit. Our best channel

in 2015 to achieve this was PPC (pay per click) but we

know there was a halo effect from other marketing

activity. We tried TV sponsorship last year for the first

time and we believe this had a positive effect on

response from all media channels. As a direct marketing

company we usually look at every pound and try to work

out how many leads we got from it. TV sponsorship

is more brand awareness orientated but because it

“We tried TV sponsorship last year for the first time and we believe this had a positive effect on response from all media channels”

INTERVIEW WITH…

000000000039

personalised service. Customers often refer us to their

friends and encouraging this is at the forefront of our

thinking. “Recommend a friend” is very important for us

and simple incentives like vouchers for recommending a

friend work well.

Customers still expect incentives and promotion is still

king in the home shopping world. We are competing with

high street furniture retailers who regularly have half

price sales so we have to give some sort of offer. Over

the years we have tested many type of incentives as well

as testing giving an offer versus giving no offer. Giving an

offer works every time and if you want instant response,

a time limit to the offer works even better. Added value

order incentives are effective such as M&S vouchers. The

Brand people say that the brand should speak for itself but

I don’t think there is anything like a promotion or an offer

to make someone act there and then.

Going into 2016, we would like to be more adventurous

and creative with our marketing by testing new media

and approaches. To stimulate ideas and mitigate the

risks, we plan to network with other companies, as often

it is not what you are doing but how you are doing it

that can be critical for success. Understanding what has

worked and what hasn’t for similar businesses could

give us the confidence to try things. Also, knowing the

right agencies and third parties to work with for each

marketing discipline can make all the difference for

strong campaign execution and performance.

“Giving an offer works every time and if you want instant response, a time limit to the offer

works even better”

40

OTHER THINGSTO KEEP IN MIND

41

By Mark Pragnell Head of Commissioned Projects at Capital Economics Ltd

The British economic recovery is on the right track, largely

because of consumers, and Brexit is unlikely to derail it.

Britain’s economy grew by its fastest pace since the

global financial crisis and was the fastest growing G7

economy in 2014. Last year, it lost out on first place to

the United States. But despite a soft first quarter, the

economy still expanded by a respectable 2.2 per cent in

2015 as a whole. While some areas of the economy lost

momentum in 2015, the consumer recovery gained pace.

Although in the early phase of the recovery retail sales

led the way, 2015 saw strong growth in spending on and

off the high street.

Consumers benefitted from falling oil prices which have

plunged since their peak in mid-2014. The slump in

energy prices has saved consumers the equivalent of 0.2

per cent of Gross Domestic Product on their fuel bills.

This increased households’ annual real income.

Falling gas and electricity prices and food prices have

also boosted households’ income. Indeed, real disposable

income rose by an average of 3.5 per cent in the

first three quarters of the year after contracting in both

2013 and 2014. This was one of the main reasons why

household spending rose by its fastest pace in over

a decade last year. Households were also given by a fillip

by the continued improvement in the labour market.

The number of people employed is currently at a record

high and the unemployment rate has continued its slide.

It fell from 5.6 per cent in January 2015 to just 5.1 per

cent at the end of the year. This led to a rise in pay growth

whilst inflation remained subdued boosting household’s

real earnings which rose by 2.4 per cent.

There are concerns that the consumer recovery is

unsustainable because it is in part being driven by

unsecured credit growth. However, debt and interest

payments as a share of incomes are well below their

previous peaks. In 2016 downward pressure on inflation

from lower oil prices and sterling’s previous appreciation

is set to fade.

“The economy expanded by a respectable

2.2% in 2015”

42

POSITIVE UK ECONOMY CREATING RETAIL SUCCESS

43

What’s more, employment growth is slowing now that

the labour market is nearing full employment and we

expect the Bank of England to hike interest rates for the

first time in nine years later in the year. However, the

tightening cycle is set to be very gradual and is unlikely

to deter spending. The British economy should still grow

strongly this year, by about 2.2 per cent in 2016, similar

to last year’s rate.

Admittedly, a number of factors threaten to undermine

the recovery including the resumption of the fiscal

squeeze and the uncertainty ahead of the European

Union referendum. But we think that the economy should

weather these relatively well. The Chancellor managed to

soften the pace of fiscal tightening in his latest Budget,

but the big picture remains that fiscal policy will be

tightened more this year than last. That said, rising real

earnings leaves households far better placed to deal with

this stage of austerity than the last one.

There are few signs yet that the referendum on Brexit

is having any adverse impact on firms’ investment

intentions and we do not think the vote will have a major

impact on consumer spending either way. Unlike firms,

we doubt that households would delay their spending.

Consumers may be affected by Brexit if it hits domestic

firms hard, but we doubt this would be the case. We

continue to think that the United Kingdom’s prospects

are good whether in or outside the European Union. As

such, whatever happens, consumers won’t be flustered.

“Household spending rose at its fastest

pace in over a decade last year”

HOW WEATHER INFLUENCES CUSTOMERS DEMAND

44

Weather is a critically important external factor for

consumer-focused businesses. This is because no other

outside variable shifts consumer buying behaviour as

frequently, directly, immediately, or meaningfully as the

weather. The climate outside affects decisions every day:

from the clothing people wear to their food and drink

choices, from the leisure activities they pursue to the

chores that need to be done in their homes, gardens, and

garages. The challenge for businesses is that the weather

is always changing and the trends rarely seem to be the

same from one year to the next. As the conditions change

so does the consumer response and 2015 proved to be

another year with glaringly different weather and sales

patterns. The following summary highlights how the

year-on-year weather changes affected retail businesses

and the demand for specific product categories.

Planalytics’ Weather-Driven Demand values are

measurements of how much the weather (and only the

weather) positively or negatively impacted demand for a

product or overall transactions.

The first half of 2015 was stubbornly cooler in comparison

to both “normal” and the prior year. Whilst the chillier

temperatures helped clear some winter merchandise in

January and in early February, the trend did businesses

no favours during the important spring selling season.

March is a particularly important period for fashion

retailers along with DIY chains and garden stores as

springtime officially arrives and the focus of consumer

activities and shopping changes. These retailers were

already facing strong turnover comparisons produced

by a very warm March 2014 (7th warmest in 54 years)

and Mother Nature was decidedly less generous

in 2015. Cooler temperatures throughout the UK

delayed the start of spring purchases and stormy

weather across the north in the first half of the month

made things even worse. Weather-Driven Demand

(March 2015 v March 2014): Lawn Mowers -25%,

Gardening Products -9%, Skirts -11%, and Casual

Trousers -6%. The less than favourable trend continued

into April and into the run up to Easter, but warmer

weather did arrive over the two weeks after Easter.

Although this is not apparent on the monthly map, the

long awaited warmup along with much drier conditions

for Wales and the southern half of England finally

helped kickoff spring spending in earnest and resulted

in stronger demand for seasonal categories. Weather-

Driven Demand (April 2015 v April 2014): Garden Hoses

+10%, Beer +3%, and Shorts +5%. The conditions were

not as good for some categories such as Sleeveless

Tops, which were down 11%. May turned less favourable

YEAR-TO-YEAR TEMPERATURE VARIATION (JAN-JUN)

45

The year-on-year weather volatility continued in the

second half of 2015. The core of summer featured a much

colder July that hurt seasonal businesses followed by a

warmer August that helped some companies rebound.

As autumn arrived, clothing and department stores were

greeted by weather that encouraged consumers to think

about updating the fall-winter wardrobes. October’s cooler

temperatures and clear skies supported footfall on high

street and stimulated seasonal buying. Weather-Driven

Demand (October 2015 v October 2014): Knitwear +5%,

Outerwear +11%, Soup +3%, and Cough-Cold Products

+4%. It is said all good things must come to an end and

from a weather standpoint that definitely happened as

the calendar flipped to November. Overall, November

2015 ended up being the 4th warmest in 55 years and

this significantly slowed demand for winter items.

Weather-Driven Demand (November 2015 v November

2014): Hats, Scarves & Gloves -15%, Fleece -11%, and

Long-Sleeve Shirts -13%. The month also registered as

the 7th wettest November, hurting footfall for many

retailers. Clothing Store Transactions fell 2% due to

weather. December proved to be even worse for fashion

and winter-focused businesses. It was the warmest

December on record and this coming on the heels of a

challenging November led to heavy discounting as retailers

faced mountains of winter stocks that needed to be moved.

Making matters worse, many locations in Ireland, Scotland,

and northern England faced record-breaking rainfall and

flooding, further altering typical purchasing patterns.

Weather-Driven Demand (December 2015 v December

2014): Heaters -38%, Women’s Boots -13%, and Winter

Coats -18%. For several winter clothing categories

it was the worst demand environment for the

November-December period in at least 10 years.

Planalytics calculated that the unfavourable weather

hurt topline sales by £-83 million at clothing store chains

during the last two months.

David Frieberg, [email protected],

http://www.planalytics.com/

overall with the UK overall experiencing an even stronger

cold variance to 2014 than the first two spring months.

London and other locations in southern England fared

better with temperatures closer to normal and less

rainfall. A couple of Weather-Driven Demand examples

(May 2015 v May 2014) highlight the regional differences

– Women’s Sandals were -36% in Manchester whilst only

-1% in London, Exterior Paint was -19% in Glasgow versus

+14% in Bournemouth.

YEAR-TO-YEAR TEMPERATURE VARIATION (JUL-DEC)

By Tim Morris Managing Director, Planalytics Europe

CONSUMER INDICATORS

2015 - review of the year

Digest of Consumer Behaviour

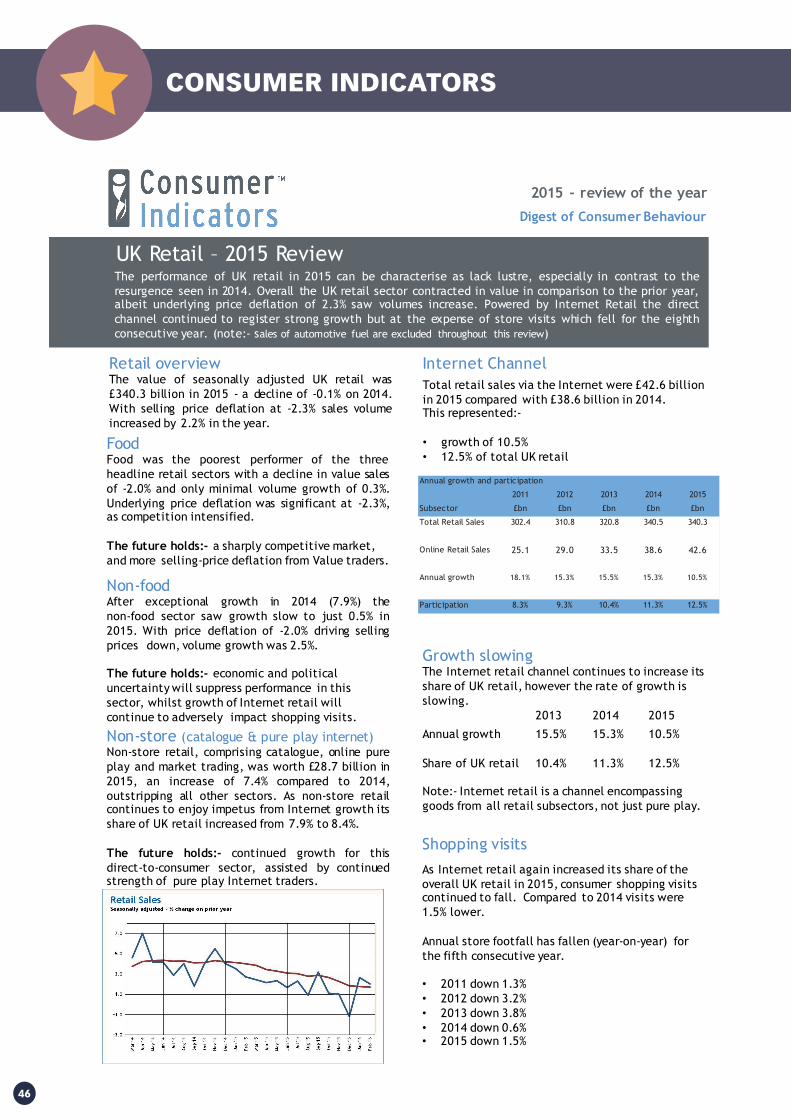

Retail overviewThe value of seasonally adjusted UK retail was£340.3 billion in 2015 - a decline of -0.1% on 2014.With selling price deflation at -2.3% sales volumeincreased by 2.2% in the year.

UK Retail – 2015 ReviewThe performance of UK retail in 2015 can be characterise as lack lustre, especially in contrast to theresurgence seen in 2014. Overall the UK retail sector contracted in value in comparison to the prior year,albeit underlying price deflation of 2.3% saw volumes increase. Powered by Internet Retail the directchannel continued to register strong growth but at the expense of store visits which fell for the eighthconsecutive year. (note:- sales of automotive fuel are excluded throughout this review)

Growth slowing The Internet retail channel continues to increase its share of UK retail, however the rate of growth is slowing.

2013 2014 2015

Annual growth 15.5% 15.3% 10.5%

Share of UK retail 10.4% 11.3% 12.5%

Note:- Internet retail is a channel encompassinggoods from all retail subsectors, not just pure play.

Published by Step Solutions www.stepsolutions.co.uk

FoodFood was the poorest performer of the threeheadline retail sectors with a decline in value salesof -2.0% and only minimal volume growth of 0.3%.Underlying price deflation was significant at -2.3%,as competition intensified.

The future holds:- a sharply competitive market,and more selling-price deflation from Value traders.

Non-foodAfter exceptional growth in 2014 (7.9%) thenon-food sector saw growth slow to just 0.5% in2015. With price deflation of -2.0% driving sellingprices down, volume growth was 2.5%.

The future holds:- economic and politicaluncertainty will suppress performance in thissector, whilst growth of Internet retail willcontinue to adversely impact shopping visits.

Non-store (catalogue & pure play internet)Non-store retail, comprising catalogue, online pureplay and market trading, was worth £28.7 billion in2015, an increase of 7.4% compared to 2014,outstripping all other sectors. As non-store retailcontinues to enjoy impetus from Internet growth itsshare of UK retail increased from 7.9% to 8.4%.

The future holds:- continued growth for thisdirect-to-consumer sector, assisted by continuedstrength of pure play Internet traders.

Total retail sales via the Internet were £42.6 billion in 2015 compared with £38.6 billion in 2014. This represented:-

• growth of 10.5% • 12.5% of total UK retail

Internet Channel

Annual growth and participation

2011 2012 2013 2014 2015

Subsector £bn £bn £bn £bn £bn

Total Retail Sales 302.4 310.8 320.8 340.5 340.3

Online Retail Sales 25.1 29.0 33.5 38.6 42.6

Annual growth 18.1% 15.3% 15.5% 15.3% 10.5%

Participation 8.3% 9.3% 10.4% 11.3% 12.5%

As Internet retail again increased its share of the overall UK retail in 2015, consumer shopping visits continued to fall. Compared to 2014 visits were 1.5% lower.

Annual store footfall has fallen (year-on-year) for the fifth consecutive year.

• 2011 down 1.3%• 2012 down 3.2%• 2013 down 3.8%• 2014 down 0.6%• 2015 down 1.5%

Shopping visits

46

By Tony Lahert Managing Director at ‘Step solutions’

www.stepsolutions.co .uk

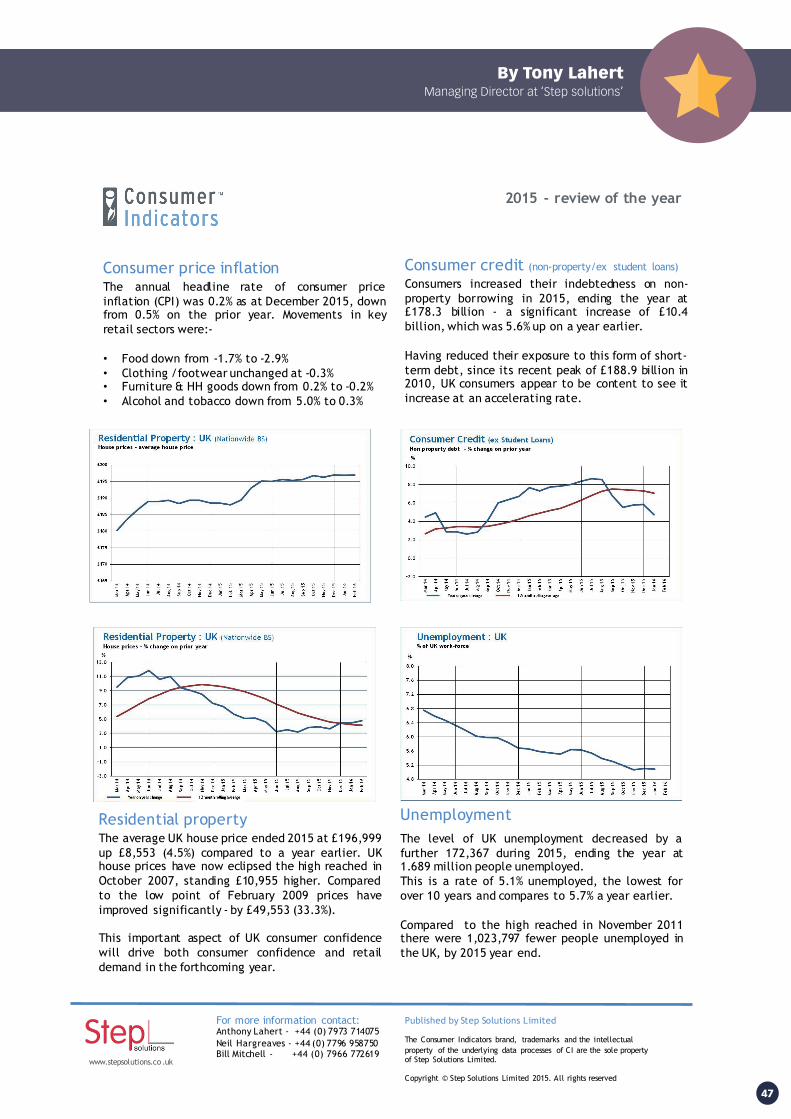

The annual headline rate of consumer priceinflation (CPI) was 0.2% as at December 2015, downfrom 0.5% on the prior year. Movements in keyretail sectors were:-

• Food down from -1.7% to -2.9%• Clothing /footwear unchanged at -0.3% • Furniture & HH goods down from 0.2% to -0.2% • Alcohol and tobacco down from 5.0% to 0.3%

Consumer price inflation

The average UK house price ended 2015 at £196,999up £8,553 (4.5%) compared to a year earlier. UKhouse prices have now eclipsed the high reached inOctober 2007, standing £10,955 higher. Comparedto the low point of February 2009 prices haveimproved significantly - by £49,553 (33.3%).

This important aspect of UK consumer confidencewill drive both consumer confidence and retaildemand in the forthcoming year.

Residential propertyThe level of UK unemployment decreased by afurther 172,367 during 2015, ending the year at1.689 million people unemployed.This is a rate of 5.1% unemployed, the lowest forover 10 years and compares to 5.7% a year earlier.

Compared to the high reached in November 2011there were 1,023,797 fewer people unemployed inthe UK, by 2015 year end.

Unemployment

For more information contact:Anthony Lahert - +44 (0) 7973 714075Neil Hargreaves - +44 (0) 7796 958750Bill Mitchell - +44 (0) 7966 772619

Published by Step Solutions Limited

The Consumer Indicators brand, trademarks and the intellectual property of the underlying data processes of CI are the sole property of Step Solutions Limited.

Copyright © Step Solutions Limited 2015. All rights reserved

2015 - review of the year

Consumers increased their indebtedness on non-property borrowing in 2015, ending the year at£178.3 billion - a significant increase of £10.4billion, which was 5.6% up on a year earlier.

Having reduced their exposure to this form of short-term debt, since its recent peak of £188.9 billion in2010, UK consumers appear to be content to see itincrease at an accelerating rate.

Consumer credit (non-property/ex student loans)

47

HOW WE CONSUME ENTERTAINMENT IN THE HOME

48

The average UK home contains 8.3 connected devices (smart phones, TVs, tablets

laptops etc). This is 12% more than a year ago according to YouGov (Omnibus,

Feb 2016). And with time spent online about 3 hours and TV viewing about 3 and

a half hours, how does the average household, divide its screen time?

78%57% 50%

Mobile technology has changed the way we consume entertainment in the home

…agree that mobile technology has changed the way they consume entertainment in

the home

…of people would now say their TV set is the main focal point of their living room

Total 16-34’s Only

To gain a picture of this new media world in the living room,

the IAB (Internet Advertising Bureau) commissioned its

Real Living research, conducted by Sparkler in November

2015. The research combined a quantitative online study

with passive monitoring of app and online usage with

in-home ethnography. This short abstract draws on data

from the quantitative and passive monitoring elements to

shed light on how devices compete for attention in the

modern living room.

How do they really divide this attention between different screens?

What really happens in the modern living room?

But people only have a finite amount of attention

People use devices for 2 hours, 59 minutes a day*

People watch TV for 3 hours, 35 minutes a day**

Research Objectives:

*UKOM data provided by comScore H2 2015

**BARB - Average daily viewing calculated by total weekly viewing figures sourced from http://www.barb.co.uk/whats-new/monthly-viewing-summary

Source: Quantitative Survey, Question Q13 “Please read the following staments about watching TV or online video content in this context and tick any that you personally agree with” and Q23 “Thinking more generally about the role of technology in your life, which of the following do you agree or disagree with?”

Base: Total–n=1010, 16-34’s–n=323.

HOW WE CONSUME ENTERTAINMENT IN THE HOME

49

Over half (57%) of those surveyed agreed that ‘mobile

technology has changed the way that I consume

entertainment in the home’. This increased to over

three quarters (78%) of 16 – 34 year olds. These changes

mean that only half (50%) of those surveyed now think

of the TV as the main focal point in the living room.The

use of connected devices at home whilst watching TV is

so prevalent that access to multiple screens should be

considered the norm. 70% of online UK adults said they

ordinarily use a connected device whilst watching TV

content at home. This increases to almost nine out of ten

(87%) of 16 – 34 year olds.

87%70%

Access to multi-screens is now the norm

…of people claim to ordinarily use a second screen whilst watching their

television set

…of those aged 16-34 years old claim to ordinarily use a second screen while watching their television set

Source: Quantitave Survey, Question Q14 “Over the course of the evening, would you ordinarily use one of your mobile devices whilst watching TV or online video content at home?”. Base: Total–n=1010, 16-34s–n=323.

The Full Real Living resultsThe full results available from www.iabuk.net/real_living

also include bio-metric data gathered two respondents

over two evenings and emphasise the variety of sources

that account for ‘high attention’ moments in the living

room – for example from connected devices – smart-

phones, tablets and laptops – in addition to the TV.

Recommendations Given the massive changes in consumer behaviour and

the disruption to the way we consume entertainment

in the home it’s vital that advertisers think about the

implications that these finding have, for example:

• There is no hierarchy of screens in the living room, only

fragmentation of attention. Connected devices should

be regarded as equals to TV when trying to connect

with highly attentive people in the home.