ISA 700 Issued December 2007 International Standard on Auditing The Auditor’s Report on Financial Statements The Malaysian Institute Of Certified Public Accountants (Institut Akauntan Awam Bertauliah Malaysia) (3246-U)

Transcript

ISA 700

Issued December 2007

International Standard on Auditing

The Auditor’s Report on Financial Statements

The Malaysian Institute Of Certified Public Accountants (Institut Akauntan Awam Bertauliah Malaysia) (3246-U)

ISA 700

1

INTERNATIONAL STANDARD ON AUDITING

The Auditor’s Report on Financial Statements

Foreword

The Council of The Malaysian Institute of Certified Public Accountants has approved this Foreword for publication.

The status of International Standards on Auditing is set out in the Council’s Statement of Policy on Approved Standards on Quality Control, Auditing, Review, Other Assurance and Related Services.

International Standards on Auditing (ISAs) are to be applied in the audit of financial statements. ISAs are also to be applied, adapted as necessary, to the audit of other information and to related services.

ISAs contain the basic principles and essential procedures (identified in bold type black lettering) together with related guidance in the form of explanatory and other material. The basic principles and essential procedures are to be interpreted in the context of the explanatory and other material that provide guidance for their application.

To understand and apply the basic principles and essential procedures together with the related guidance, it is necessary to consider the whole text of the ISA including explanatory and other material contained in the ISA not just that text which is black lettered.

In exceptional circumstances, an auditor may judge it necessary to depart from an ISA in order to more effectively achieve the objective of an audit. When such a situation arises, the auditor should be prepared to justify the departure. ISAs need only be applied to material matters.

ISA 700

2

Notes and Exceptions 1. The Council would like to highlight the following provisions in the

Companies Act 1965 concerning reporting on financial statements:

(a) Auditors’ report

Section 174(2) stipulates the matters that an auditor is required to report on in connection with the audit of a company’s financial statements.

(b) Accounts

Section 4 defines accounts to comprise profit and loss accounts and balance sheets and include notes or statements required by the Act (other than auditors’ reports or directors’ reports). Pursuant to paragraph 4 of the Nineth Schedule, the statement of changes in financial position is an integral part of the accounts.

Thus, the term “accounts” should be taken as synonymous with “financial statements” referred to in ISA 700.

(c) Responsibility for Accounts

Paragraph 9 of ISA 700 states that the auditor’s report should include a statement that the financial statements are the responsibility of the company’s management.

Section 169(15) of the Companies Act requires the directors of a company to attach a statement to the accounts of the company stating whether in their opinion:

(i) the accounts have been drawn up so as to give a true and fair view of the results of the business and the state of affairs of the company;

(ii) the accounts have been made out in accordance with the applicable approved accounting standards.

Thus, the directors are held primarily responsible for the accounts of the company.

For a foreign company having a place of business or is carrying on business within Malaysia pursuant to section 329 of the Companies Act 1965, the Council is of the view that the agent of the company, as defined in section 330(1) of the Companies Act, should be responsible for the financial statements of the foreign company.

ISA 700

3

Statutory Requirements 2. Section 174(2) of the Companies Act requires the auditor to state in his

report:

(a) whether the accounts and if the company is a holding company for which consolidated accounts are prepared, the consolidate accounts are in his opinion properly drawn up –

(i) so as to give a true and fair view of the matters required by section 169 to be dealt with in the accounts and, if there are consolidated accounts, in the consolidated accounts;

(ii) in accordance with the provisions of this Act so as to give a true and fair view of the company’s affairs; and

(iii) in accordance with the applicable approved accounting standards;

(aa) if in his opinion the accounts, and where applicable the consolidated accounts, have not been drawn up in accordance with a particular applicable approved accounting standard –

(i) whether in his opinion the accounts or consolidated accounts, as the case may be, would, if drawn up in accordance with that approved accounting standard, have given a true and fair view of the matters required by section 169 to be dealt with in the accounts or consolidated accounts;

(ii) if in his opinion the accounts or consolidated accounts, as the case may be, would not, if so drawn up, have given a true and fair view of those matters, his reasons for holding that opinion;

(iii) if the directors have given the particulars of the quantified financial effect under section 166A(5), his opinion concerning the particulars; and

(iv) in a case to which neither subparagraph (ii) nor (iii) applies, particulars of the quantified financial effect on the accounts or consolidated accounts of the failure to so drawn up the accounts or consolidated accounts, as the case may be;

(b) whether the accounting and other records and the registers required by this Act to be kept by the company and, if it is a holding company, by the subsidiaries other than those of which he has not acted as auditor

ISA 700

4

have been, in his opinion, properly kept in accordance with the provisions of this Act;

(c) in the case of consolidated accounts –

(i) the names of the subsidiaries (if any) of which he has not acted as auditor;

(ii) whether he has considered the accounts and auditor’s reports of all subsidiaries of which he has not acted as auditor, being accounts that are included (whether separately or consolidated with other accounts) in the consolidated accounts;

(iii) whether he is satisfied that the accounts of the subsidiaries that are consolidated with other accounts are in form and content appropriate and proper for the purposes of the preparation of the consolidated accounts, and whether he has received satisfactory information and explanations as required by him for those purposes; and

(iv) whether the auditor’s report on the accounts of any subsidiary was made subject to any qualification (other than a qualification that is not material in relation to the consolidated accounts), or included any comment made under subsection (3), and, if so, particulars of the qualification or comment;

(d) any effect or irregularity in the accounts or consolidated accounts and any matter not set out in the accounts or consolidated accounts without regard to which a true and fair view of the matters dealt with by the accounts or consolidated accounts would not be obtained; and

(e) if he is not satisfied as to any matter referred to in paragraph (a), (b) or (c), his reasons for not being so satisfied.

3. Additionally, the auditor is required by section 174(3) to report on the following circumstances:

(a) whether he has obtained all the information and explanations that he required;

(b) whether proper accounting and other records (including registers) have been kept by the company as required by this Act;

(c) whether the returns received from branch offices of the company are adequate; and

ISA 700

5

(d) whether the procedures and methods used by a holding company o a subsidiary in arriving at the amount taken into any consolidated accounts were appropriate to the circumstances of the consolidation,

and he shall state in his report of any deficiency, failure or shortcoming in respect of any matter referred to in this subsection.

This report is to be made on the basis of exception reporting i.e. the auditor only makes reference to the circumstances if there is some default.

Scope of Auditor’s Report under the Companies Act 1965 4. (a) Opinion on Directors’ Report

The Council is of the view that the directors’ report is not required to be specifically included in the auditor’s opinion under section 174(2) since the auditor’s opinion under section 174(2) centralises on the concerns only “the accounts”.

This view is supported by the definition of the term “accounts” in section 4 of the Companies Act [see paragraph 1(b) above] where the directors’ reports are specifically excluded from the definition of “accounts”.

The Council has obtained legal opinion that the auditor, in expressing his opinion on the accounts and the matters required to be dealt with in the accounts, is not required to express his opinion on the directors’ reports. However, under section 174(8) [see paragraph 4(b) below], the auditor may have to report a breach or non-observance of any provisions of the Act including, inter alia, the directors’ report.

(b) Compliance with the provisions of the Companies Act 1965

Section 174(8) states if an auditor, in the course of the performance of his duties as auditor of a company, is satisfied that:

(i) there has been a breach or non-observance of any of the provisions of this Act; and

(ii) the circumstances are such that in his opinion the matter has not been or will not be adequately dealt with by comment in his report on the accounts or consolidated accounts or by bringing

ISA 700

6

the matter to the notice of the directors of the company or, if the company is a subsidiary, of the directors of its holding company,

he shall forthwith report the matter in writing to the Registrar.

Council has obtained legal opinion that the onus of reporting to the Registrar in such circumstances has no legal limit as regards the breach or non-observance and the decision lies entirely with the reporting auditor.

Thus, all breaches encountered in an audit, whether relating to the accounts, accounting records or other aspects of the Act will have to be reported to the Registrar if the auditor feels the alternative actions referred to in section 174(8)(b) are inadequate to deal with the matter.

Therefore in his judgement on whether to report a breach or non-observance of provisions of the Act to the Registrar the auditor should:

(i) consider the evidence of a breach or non-observance, and be satisfied that a breach or non-observance has actually occurred; and

(ii) form an opinion on whether in the circumstances of a particular case the matter has been or will be adequately dealt with in the manner prescribed in section 174(8)(b) other than by reporting to the Registrar.

The exercise of this judgement will necessarily be on a case by case basis.

A major difficulty remains in that the Act does not define what constitutes performance of an auditor’s duties. The Act simply states that the auditor must report on the accounts and other matters under section 174.

(c) Exempt Private Companies:

Exempt private companies are required to include in or attach to its annual return to be filed under section 165 a statement relating to the accounts of the company required to be laid before the company at its annual general meeting held on the date to which the return is made up or if an annual general meeting is not held on that date, the annual general meeting last preceding that date, signed by the auditor of the company:

ISA 700

7

(i) stating whether the company has in his opinion kept proper accounting records and other books during the period covered by those accounts;

(ii) stating whether the auditor’s report on the accounts have been audited in accordance with this Act;

(iii) stating whether the auditor’s report on the accounts was made subject to any qualification, or included any comment made under section 174(3), and, if so, particulars of the qualification or comment; and

(iv) stating whether as at the date to which the profit and loss account has been made up, the company appeared to have been able to meet its liabilities as and when they fall due.

It should be noted that this requirement relates to a statement by the auditor rather than an auditor’s report as such. Auditors’ reports are normally addressed to a specified person or group of persons (usually the shareholders). The section 165A requirement is for a general statement in addition to the auditor’s report under section 174 to the shareholders. However, the general principles concerning auditors’ reports and qualifications as set out in the Standard generally apply to this auditor’s statement under section 165A.

The statement is required in addition to certification of exempt private company status by a director, the company secretary and the auditor carried on the Annual Return.

(d) Foreign Companies

Concerning foreign companies, section 336(6) of the Companies Act specifies that the provisions of the Act concerning auditor’s reports contained in section 174 apply to the accounts required to be filed with the Registrar of Companies in respect of a foreign company’s operations in Malaysia.

Examples of Auditor’s Report 5. The Council has set out in Appendix II examples of auditor’s reports

which comply with the requirements of section 174 as well as ISA 700. The examples illustrate circumstances that may result in unqualified opinion, qualified opinion, disclaimer of opinion and adverse opinion.

ISA 700

8

6. The Council would like to point out that a situation of significant uncertainty (other than a going concern problem) is not considered to be a matter that would affect the auditor’s opinion under this Standard, and it would be adequate if the auditor’s report is being modified to include an emphasis of matter paragraph. However, in extreme cases, such as situations involving multiple uncertainties that are significant to the financial statements, the auditor may consider it appropriate to express a disclaimer of opinion instead of adding on an emphasis of matter paragraph.

7. The examples of auditor’s reports in respect of going concern uncertainty are set out in Appendix I to ISA 570, Going Concern.

Effective Date in Malaysia The Standard is effective for audits of financial statements for periods ending on or after December 31, 2002. Early application of the Standard is encouraged.

Circumstances That May Result in Other Than an Unqualified Opinion .............................................................. 41 – 46

Appendix I : Form of Auditors’ Report

Appendix II : Examples of Auditor’s Report

ISA 700

10

Introduction

1. The purpose of this International Standard on Auditing (ISA) is to establish standards and provide guidance on the form and content of the auditor's report issued as a result of an audit performed by an independent auditor of the financial statements of an entity. Much of the guidance provided can be adapted to auditor reports on financial information other than financial statements.

2. The auditor should review and assess the conclusions drawn from the audit evidence obtained as the basis for the expression of an opinion on the financial statements.

3. This review and assessment involves considering whether the financial statements have been prepared in accordance with an acceptable financial reporting framework11 being either International Accounting Standards (IASs) or relevant national standards or practices. It may also be necessary to consider whether the financial statements comply with statutory requirements.

4. The auditor's report should contain a clear written expression of opinion on the financial statements taken as a whole.

Basic Elements of the Auditor's Report 5. The auditor's report includes the following basic elements, ordinarily in

the following layout:

(a) title,

(b) addressee,

(c) opening or introductory paragraph

(i) identification of the financial statements audited,

(ii) a statement of the responsibility of the entity's management and the responsibility of the auditor,

(d) scope paragraph (describing the nature of an audit)

1 The Framework of International Standards on Auditing and Related Services also identifies another authoritative and comprehensive financial reporting framework. Reporting in accordance with this third type of framework is covered in ISA "The Auditor's Report on Special Purpose Audit Engagements."

ISA 700

11

(i) a reference to the ISAs or relevant national standards or practices,

(ii) a description of the work the auditor performed,

(e) opinion paragraph containing an expression of opinion on the financial statements,

(f) date of the report,

(g) auditor's address, and

(h) auditor's signature.

A measure of uniformity in the form and content of the auditor's report is desirable because it helps to promote the reader's understanding and to identify unusual circumstances when they occur.

Title 6. The auditor's report should have an appropriate title. It may be

appropriate to use the term "Independent Auditor" in the title to distinguish the auditor's report from reports that might be issued by others, such as by officers of the entity, the board of directors, or from the reports of other auditors who may not have to abide by the same ethical requirements as the independent auditor.

Addressee 7. The auditor's report should be appropriately addressed as required

by the circumstances of the engagement and local regulations. The report is ordinarily addressed either to the shareholders or the board of directors of the entity whose financial statements are being audited.

Opening or Introductory Paragraph 8. The auditor's report should identify the financial statements of the

entity that have been audited, including the date of and period covered by the financial statements.

9. The report should include a statement that the financial statements are the responsibility of the entity's management2, and a statement

2

The level of management responsible for the financial statements will vary according to the legal

ISA 700

12

that the responsibility of the auditor is to express an opinion on the financial statements based on the audit.

10. Financial statements are the representations of management. The preparation of such statements requires management to make significant accounting estimates and judgments, as well as to determine the appropriate accounting principles and methods used in preparation of the financial statements. In contrast, the auditor's responsibility is to audit these financial statements in order to express an opinion thereon.

11. An illustration of these matters in an opening (introductory) paragraph is:

"We have audited the accompanying3 balance sheet of the ABC Company as of December 31, 19X1, and the related statements of income, and cash flows for the year then ended. These financial statements are the responsibility of the Company's management. Our responsibility is to express an opinion on these financial statements based on our audit."

Scope Paragraph 12. The auditor's report should describe the scope of the audit by

stating that the audit was conducted in accordance with ISAs or in accordance with relevant national standards or practices as appropriate. "Scope" refers to the auditor's ability to perform audit procedures deemed necessary in the circumstances. The reader needs this as an assurance that the audit has been carried out in accordance with established standards or practices. Unless otherwise stated, the auditing standards or practices followed are presumed to be those of the country indicated by the auditor's address.

13. The report should include a statement that the audit was planned and performed to obtain reasonable assurance about whether the financial statements are free of material misstatement.

14. The auditor's report should describe the audit as including:

(a) examining, on a test basis, evidence to support the financial statement amounts and disclosures;

situation in each country.

3 The reference can be by page numbers.

ISA 700

13

(b) assessing the accounting principles used in the preparation of the financial statements;

(c) assessing the significant estimates made by management in the preparation of the financial statements; and

(d) evaluating the overall financial statement presentation.

15. The report should include a statement by the auditor that the audit provides a reasonable basis for the opinion.

16. An illustration of these matters in a scope paragraph is:

"We conducted our audit in accordance with International Standards on Auditing (or refer to relevant national standards or practices). Those Standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement. An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements. An audit also includes assessing the accounting principles used and significant estimates made by management, as well as evaluating the overall financial statement presentation. We believe that our audit provides a reasonable basis for our opinion."

Opinion Paragraph 17. The auditor's report should clearly state the auditor's opinion as to

whether the financial statements give a true and fair view (or are presented fairly, in all material respects,) in accordance with the financial reporting framework and, where appropriate, whether the financial statements comply with statutory requirements.

18. The terms used to express the auditor's opinion are "give a true and fair view" or "present fairly, in all material respects," and are equivalent. Both terms indicate, amongst other things, that the auditor considers only those matters that are material to the financial statements.

19. The financial reporting framework is determined by IASs, rules issued

by professional bodies, and the development of general practice within a country, with an appropriate consideration of fairness and with due regard to local legislation. To advise the reader of the context in which "fairness" is expressed, the auditor's opinion would indicate the framework upon which the financial statements are based by using

ISA 700

14

words such as "in accordance with (indicate IASs or relevant national standards)."

20. In addition to an opinion on the true and fair view (or fair presentation, in all material respects,), the auditor's report may need to include an opinion as to whether the financial statements comply with other requirements specified by relevant statutes or law.

21. An illustration of these matters in an opinion paragraph is:

"In our opinion, the financial statements give a true and fair view of (or 'present fairly, in all material respects,') the financial position of the Company as of December 31, 19X1, and of the results of its operations and its cash flows for the year then ended in accordance with ...4 (and comply with ...5)."

22. In any situation where it is not evident which country's accounting principles have been used, the country should be stated. When reporting on financial statements that are distributed extensively outside the country of origin, it is recommended that the auditor refer to the standards of the country of origin in the auditor's report, such as:

..". in accordance with accounting principles generally accepted in country A ... ."

This designation will help the user to better understand which accounting principles were used in preparing the financial statements. When reporting on financial statements that are prepared specifically for use in another country (e.g., where the statements have been translated into the language and currency of another country in a cross-border financing), the auditor will consider the need to refer to the accounting principles of the country of origin where prepared, and consider whether appropriate disclosure has been made in the statements.

Date of Report 23. The auditor should date the report as of the completion date of the

audit. This informs the reader that the auditor has considered the effect on the financial statements and on the report of events and transactions of which the auditor became aware and that occurred up to that date.

4 Indicate IASs or relevant national standards. 5 Refer to relevant statutes or law.

ISA 700

15

24. Since the auditor's responsibility is to report on the financial statements as prepared and presented by management, the auditor should not date the report earlier than the date on which the financial statements are signed or approved by management.

Auditor's Address 25. The report should name a specific location, which is ordinarily the

city where the auditor maintains the office that has responsibility for the audit.

Auditor's Signature 26. The report should be signed in the name of the audit firm, the

personal name of the auditor or both, as appropriate. The auditor's report is ordinarily signed in the name of the firm because the firm assumes responsibility for the audit.

The Auditor's Report 27. An unqualified opinion should be expressed when the auditor

concludes that the financial statements give a true and fair view (or are presented fairly, in all material respects,) in accordance with the identified financial reporting framework. An unqualified opinion also indicates implicitly that any changes in accounting principles or in the method of their application, and the effects thereof, have been properly determined and disclosed in the financial statements.

28. The following is an illustration of the entire auditor's report incorporating the basic elements set forth and illustrated above. This report illustrates the expression of an unqualified opinion.

"AUDITOR'S REPORT

(APPROPRIATE ADDRESSEE)

We have audited the accompanying6 balance sheet of the ABC Company as at December 31, 19X1, and the related statements of income, and cash

6See footnote 3.

ISA 700

16

flows for the year then ended. These financial statements are the responsibility of the Company's management. Our responsibility is to express an opinion on these financial statements based on our audit.

We conducted our audit in accordance with International Standards on Auditing (or refer to relevant national standards or practices). Those Standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement. An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements. An audit also includes assessing the accounting principles used and significant estimates made by management, as well as evaluating the overall financial statement presentation. We believe that our audit provides a reasonable basis for our opinion.

In our opinion, the financial statements give a true and fair view of (or 'present fairly, in all material respects,') the financial position of the Company as at December 31, 19X1, and of the results of its operations and its cash flows for the year then ended in accordance with ...7 (and comply with ...8 ).

AUDITOR Date

Address"

Modified Reports 29. An auditor's report is considered to be modified in the following situations:

Matters That Do Not Affect the Auditor's Opinion

(a) emphasis of a matter

7 See footnote 4. 8 See footnote 5.

ISA 700

17

Matters That Do Affect the Auditor's Opinion

(a) qualified opinion,

(b) disclaimer of opinion, or

(c) adverse opinion.

Uniformity in the form and content of each type of modified report will further the user's understanding of such reports. Accordingly, this ISA includes suggested wording to express an unqualified opinion as well as examples of modifying phrases for use when issuing modified reports.

Matters That Do Not Affect the Auditor's Opinion 30.In certain circumstances, an auditor's report may be modified by adding

an emphasis of matter paragraph to highlight a matter affecting the financial statements which is included in a note to the financial statements that more extensively discusses the matter. The addition of such an emphasis of matter paragraph does not affect the auditor's opinion. The paragraph would preferably be included after the opinion paragraph and would ordinarily refer to the fact that the auditor's opinion is not qualified in this respect.

31. The auditor should modify the auditor's report by adding a paragraph to highlight a material matter regarding a going concern problem.

32. The auditor should consider modifying the auditor's report by adding a paragraph if there is a significant uncertainty (other than a going concern problem), the resolution of which is dependent upon future events and which may affect the financial statements. An uncertainty is a matter whose outcome depends on future actions or events not under the direct control of the entity but that may affect the financial statements.

33. An illustration of an emphasis of matter paragraph for a significant uncertainty in an auditor's report follows:

"In our opinion ... (remaining words are the same as illustrated in the opinion paragraph - paragraph 28 above).

Without qualifying our opinion we draw attention to Note X to the financial statements. The Company is the defendant in a lawsuit alleging infringement of certain patent rights and claiming royalties and punitive damages. The Company has filed a counter action, and

ISA 700

18

preliminary hearings and discovery proceedings on both actions are in progress. The ultimate outcome of the matter cannot presently be determined, and no provision for any liability that may result has been made in the financial statements."

(An illustration of an emphasis of matter paragraph relating to going concern is set out in ISA "Going Concern.")

34. The addition of a paragraph emphasizing a going concern problem or significant uncertainty is ordinarily adequate to meet the auditor's reporting responsibilities regarding such matters. However, in extreme cases, such as situations involving multiple uncertainties that are significant to the financial statements, the auditor may consider it appropriate to express a disclaimer of opinion instead of adding an emphasis of matter paragraph.

35. In addition to the use of an emphasis of matter paragraph for matters that affect the financial statements, the auditor may also modify the auditor's report by using an emphasis of matter paragraph, preferably after the opinion paragraph, to report on matters other than those affecting the financial statements. For example, if an amendment is necessary to other information in a document containing audited financial statements and the entity refuses to make the amendment, the auditor would consider including in the auditor's report an emphasis of matter paragraph describing the material inconsistency. An emphasis of a matter paragraph may also be used when there are additional statutory reporting responsibilities.

Matters That Do Affect the Auditor's Opinion 36. An auditor may not be able to express an unqualified opinion when either

of the following circumstances exist and, in the auditor's judgment, the effect of the matter is or may be material to the financial statements.

(a) There is a limitation on the scope of the auditor's work; or (b) There is a disagreement with management regarding the acceptability

of the accounting policies selected, the method of their application or the adequacy of financial statement disclosures.

The circumstances described in a) could lead to a qualified opinion or a disclaimer of opinion. The circumstances described in b) could lead to a qualified opinion or an adverse opinion. These circumstances are discussed more fully in paragraphs 41-46.

37. A qualified opinion should be expressed when the auditor concludes that an unqualified opinion cannot be expressed but that the effect of

ISA 700

19

any disagreement with management, or limitation on scope is not so material and pervasive as to require an adverse opinion or a disclaimer of opinion. A qualified opinion should be expressed as being 'except for' the effects of the matter to which the qualification relates.

38. A disclaimer of opinion should be expressed when the possible effect of a limitation on scope is so material and pervasive that the auditor has not been able to obtain sufficient appropriate audit evidence and accordingly is unable to express an opinion on the financial statements.

39. An adverse opinion should be expressed when the effect of a disagreement is so material and pervasive to the financial statements that the auditor concludes that a qualification of the report is not adequate to disclose the misleading or incomplete nature of the financial statements.

40. Whenever the auditor expresses an opinion that is other than unqualified, a clear description of all the substantive reasons should be included in the report and, unless impracticable, a quantification of the possible effect(s) on the financial statements. Ordinarily, this information would be set out in a separate paragraph preceding the opinion or disclaimer of opinion and may include a reference to a more extensive discussion, if any, in a note to the financial statements.

Circumstances That May Result in Other Than an Unqualified Opinion Limitation on Scope 41. A limitation on the scope of the auditor's work may sometimes be imposed

by the entity (for example, when the terms of the engagement specify that the auditor will not carry out an audit procedure that the auditor believes is necessary). However, when the limitation in the terms of a proposed engagement is such that the auditor believes the need to express a disclaimer of opinion exists, the auditor would ordinarily not accept such a limited engagement as an audit engagement, unless required by statute. Also, a statutory auditor would not accept such an audit engagement when

ISA 700

20

the limitation infringes on the auditor's statutory duties. 42. A scope limitation may be imposed by circumstances (for example when

the timing of the auditor's appointment is such that the auditor is unable to observe the counting of physical inventories). It may also arise when, in the opinion of the auditor, the entity's accounting records are inadequate or when the auditor is unable to carry out an audit procedure believed to be desirable. In these circumstances, the auditor would attempt to carry out reasonable alternative procedures to obtain sufficient appropriate audit evidence to support an unqualified opinion.

43. When there is a limitation on the scope of the auditor's work that requires expression of a qualified opinion or a disclaimer of opinion, the auditor's report should describe the limitation and indicate the possible adjustments to the financial statements that might have been determined to be necessary had the limitation not existed.

44. Illustrations of these matters are set out below.

Limitation on Scope—Qualified Opinion "We have audited ... (remaining words are the same as illustrated in the

introductory paragraph—paragraph 28 above). Except as discussed in the following paragraph, we conducted our audit

in accordance with ... (remaining words are the same as illustrated in the scope paragraph—paragraph 28 above).

We did not observe the counting of the physical inventories as at December 31, 19X1, since that date was prior to the time we were initially engaged as auditors for the Company. Owing to the nature of the Company's records, we were unable to satisfy ourselves as to inventory quantities by other audit procedures.

In our opinion, except for the effects of such adjustments, if any, as might have been determined to be necessary had we been able to satisfy ourselves as to physical inventory quantities, the financial statements give a true and ... (remaining words are the same as illustrated in the opinion paragraph—paragraph 28 above)."

Limitation on Scope—Disclaimer of Opinion "We were engaged to audit the accompanying balance sheet of the ABC

Company as at December 31, 19X1, and the related statements of income, and cash flows for the year then ended. These financial statements are the responsibility of the Company's management. (Omit the sentence stating the responsibility of the auditor).

ISA 700

21

(The paragraph discussing the scope of the audit would either be omitted or amended according to the circumstances.)

(Add a paragraph discussing the scope limitation as follows:) We were not able to observe all physical inventories and confirm

accounts receivable due to limitations placed on the scope of our work by the Company.

Because of the significance of the matters discussed in the preceding paragraph, we do not express an opinion on the financial statements."

Disagreement with Management 45. The auditor may disagree with management about matters such as the

acceptability of accounting policies selected, the method of their application, or the adequacy of disclosures in the financial statements. If such disagreements are material to the financial statements, the auditor should express a qualified or an adverse opinion.

46. Illustrations of these matters are set out below.

Disagreement on Accounting Policies-Inappropriate Accounting Method—Qualified Opinion

"We have audited ... (remaining words are the same as illustrated in the introductory paragraph—paragraph 28 above).

We conducted our audit in accordance with ... (remaining words are the same as illustrated in the scope paragraph—paragraph 28 above).

As discussed in Note X to the financial statements, no depreciation has been provided in the financial statements which practice, in our opinion, is not in accordance with International Accounting Standards. The provision for the year ended December 31, 19X1, should be ... based on the straight-line method of depreciation using annual rates of 5% for the building and 20% for the equipment. Accordingly, the fixed assets should be reduced by accumulated depreciation of ..... and the loss for the year and accumulated deficit should be increased by ...... and ......, respectively.

In our opinion, except for the effect on the financial statements of the matter referred to in the preceding paragraph, the financial statements give a true and ... (remaining words are the same as illustrated in the opinion paragraph—paragraph 28 above)."

ISA 700

22

Disagreement on Accounting Policies—Inadequate Disclosure—Qualified Opinion

"We have audited ... (remaining words are the same as illustrated in the introductory paragraph—paragraph 28 above).

We conducted our audit in accordance with ... (remaining words are the same as illustrated in the scope paragraph—paragraph 28 above).

On January 15, 19X2, the Company issued debentures in the amount of for the purpose of financing plant expansion. The debenture agreement restricts the payment of future cash dividends to earnings after December 31, 19X1. In our opinion, disclosure of this information is required by ...9 .

In our opinion, except for the omission of the information included in the preceding paragraph, the financial statements give a true and ... (remaining words are the same as illustrated in the opinion paragraph—paragraph 28 above)."

Disagreement on Accounting Policies—Inadequate Disclosure— Adverse Opinion

"We have audited ... (remaining words are the same as illustrated in the introductory paragraph—paragraph 28 above).

We conducted our audit in accordance with ... (remaining words are the same as illustrated in the scope paragraph—paragraph 28 above).

(Paragraph(s) discussing the disagreement).

In our opinion, because of the effects of the matters discussed in the preceding paragraph(s), the financial statements do not give a true and fair view of (or do not 'present fairly') the financial position of the Company as at December 31, 19X1, and of the results of its operations and its cash flows for the year then ended in accordance with ...10 (and do not comply with ...11)."

Public Sector Perspective 1. While the basic principles contained in this ISA apply to the audit of

financial statements in the public sector, the legislation giving rise to the

9 See footnotes 4 and 5. 10 See footnote 4. 11See footnote 5.

ISA 700

23

audit mandate may specify the nature, content and form of the auditor's report.

2. This ISA does not address the form and content of the auditor's report in circumstances where financial statements are prepared in conformity with a disclosed basis of accounting, whether mandated by legislation or ministerial (or other) directive, and that basis results in financial statements which are misleading.

ISA 700

24

Appendix I

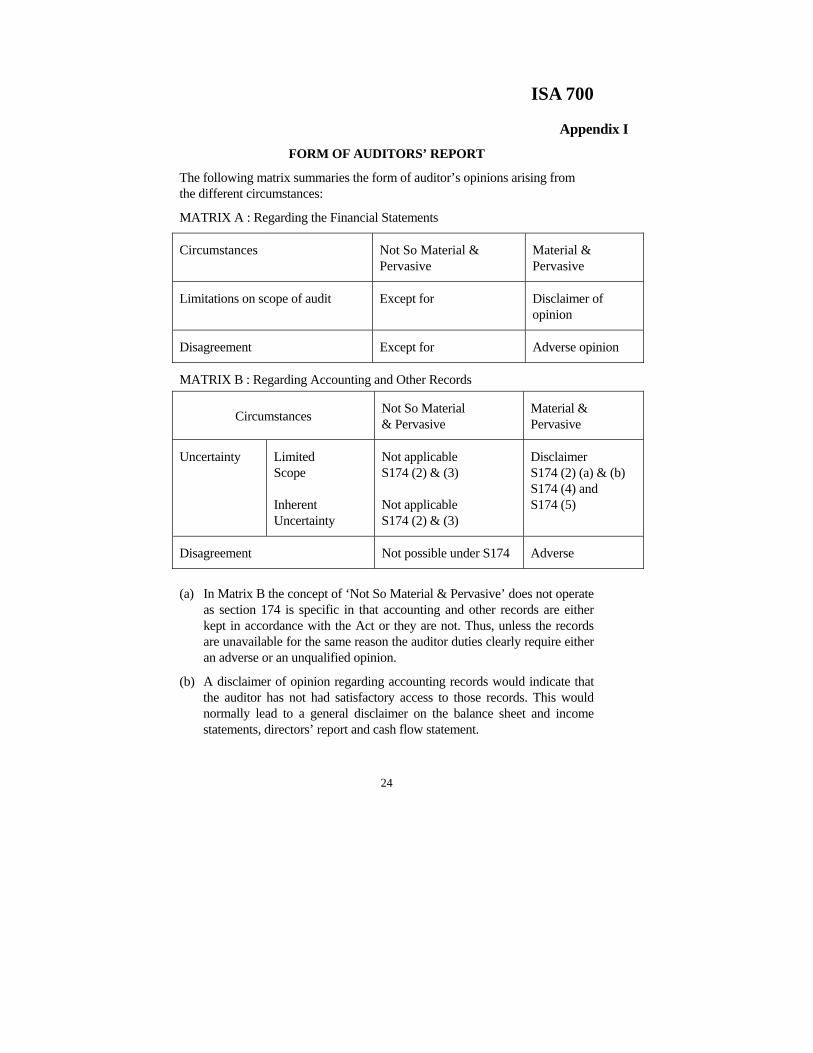

FORM OF AUDITORS’ REPORT

The following matrix summaries the form of auditor’s opinions arising from the different circumstances:

MATRIX A : Regarding the Financial Statements

Circumstances Not So Material & Pervasive

Material & Pervasive

Limitations on scope of audit Except for Disclaimer of opinion

Disagreement Except for Adverse opinion

MATRIX B : Regarding Accounting and Other Records

Circumstances Not So Material & Pervasive

Material & Pervasive

Uncertainty Limited Scope Inherent Uncertainty

Not applicable S174 (2) & (3) Not applicable S174 (2) & (3)

(a) In Matrix B the concept of ‘Not So Material & Pervasive’ does not operate as section 174 is specific in that accounting and other records are either kept in accordance with the Act or they are not. Thus, unless the records are unavailable for the same reason the auditor duties clearly require either an adverse or an unqualified opinion.

(b) A disclaimer of opinion regarding accounting records would indicate that the auditor has not had satisfactory access to those records. This would normally lead to a general disclaimer on the balance sheet and income statements, directors’ report and cash flow statement.

ISA 700

25

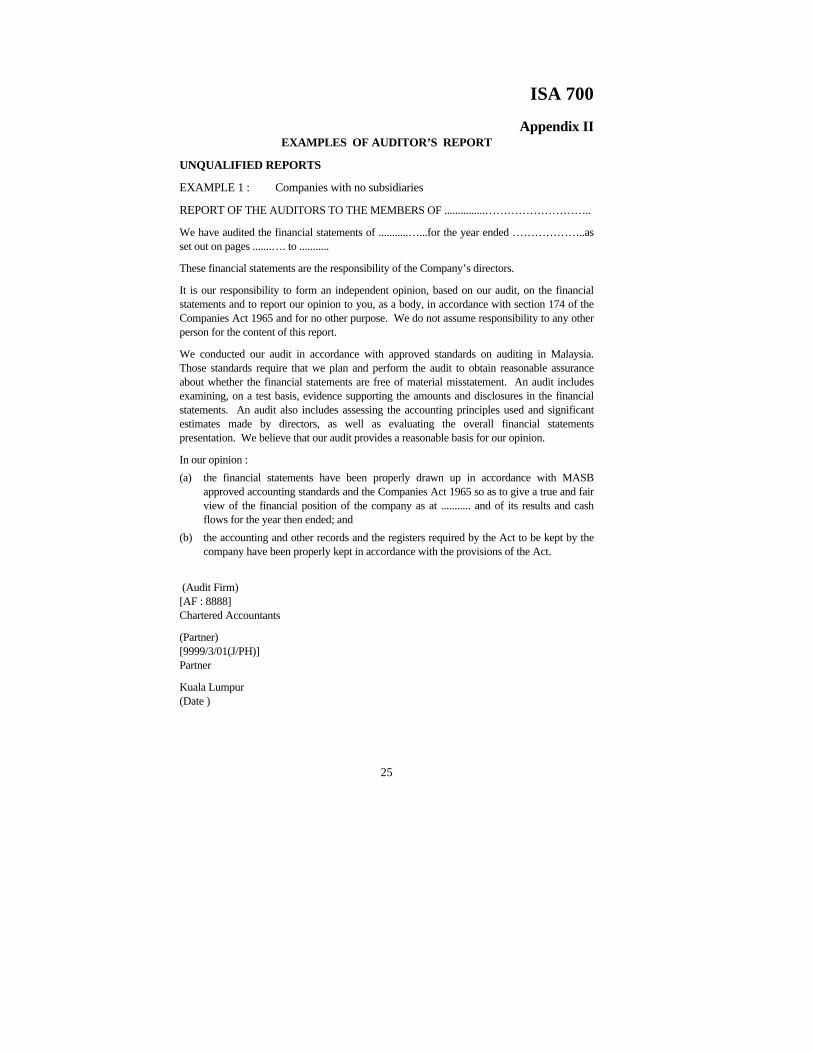

Appendix II EXAMPLES OF AUDITOR’S REPORT

UNQUALIFIED REPORTS

EXAMPLE 1 : Companies with no subsidiaries

REPORT OF THE AUDITORS TO THE MEMBERS OF ...............………………………..

We have audited the financial statements of ...........…...for the year ended ………………..as set out on pages .......…. to ...........

These financial statements are the responsibility of the Company’s directors.

It is our responsibility to form an independent opinion, based on our audit, on the financial statements and to report our opinion to you, as a body, in accordance with section 174 of the Companies Act 1965 and for no other purpose. We do not assume responsibility to any other person for the content of this report.

We conducted our audit in accordance with approved standards on auditing in Malaysia. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement. An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements. An audit also includes assessing the accounting principles used and significant estimates made by directors, as well as evaluating the overall financial statements presentation. We believe that our audit provides a reasonable basis for our opinion.

In our opinion : (a) the financial statements have been properly drawn up in accordance with MASB

approved accounting standards and the Companies Act 1965 so as to give a true and fair view of the financial position of the company as at ........... and of its results and cash flows for the year then ended; and

(b) the accounting and other records and the registers required by the Act to be kept by the company have been properly kept in accordance with the provisions of the Act.

(Audit Firm) [AF : 8888] Chartered Accountants

(Partner) [9999/3/01(J/PH)] Partner

Kuala Lumpur (Date )

ISA 700

26

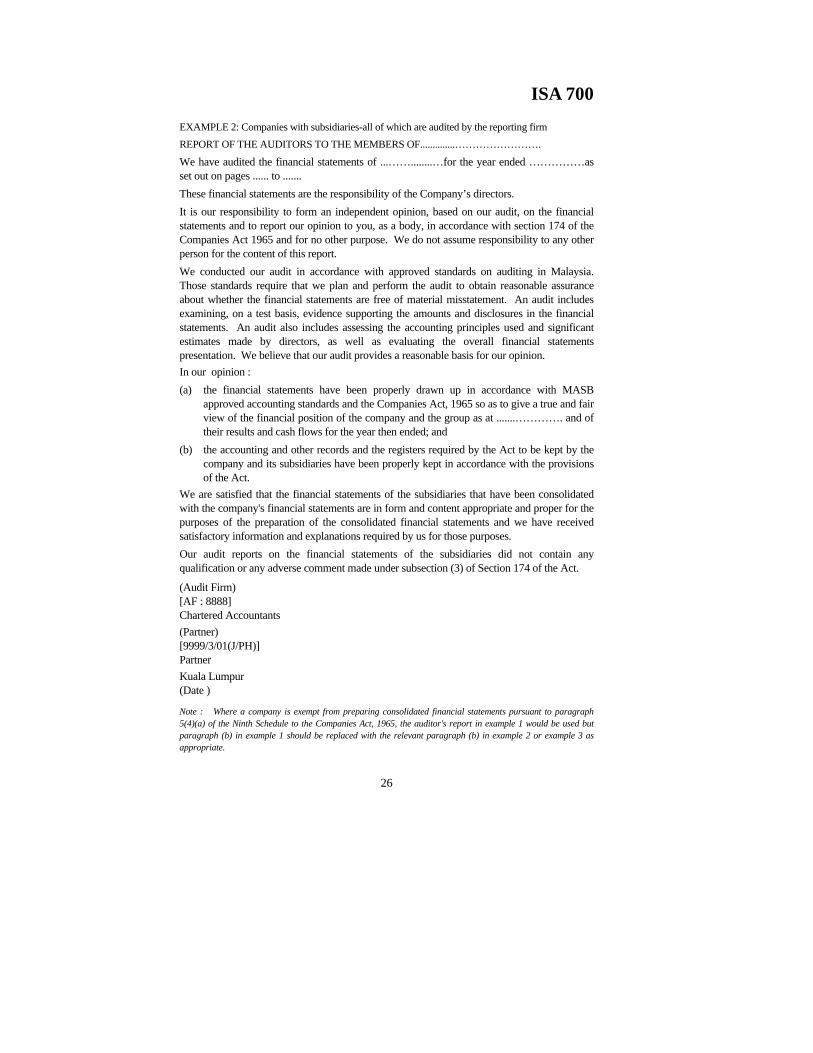

EXAMPLE 2: Companies with subsidiaries-all of which are audited by the reporting firm REPORT OF THE AUDITORS TO THE MEMBERS OF..............…………………….

We have audited the financial statements of ...……........…for the year ended ……………as set out on pages ...... to ....... These financial statements are the responsibility of the Company’s directors. It is our responsibility to form an independent opinion, based on our audit, on the financial statements and to report our opinion to you, as a body, in accordance with section 174 of the Companies Act 1965 and for no other purpose. We do not assume responsibility to any other person for the content of this report. We conducted our audit in accordance with approved standards on auditing in Malaysia. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement. An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements. An audit also includes assessing the accounting principles used and significant estimates made by directors, as well as evaluating the overall financial statements presentation. We believe that our audit provides a reasonable basis for our opinion. In our opinion : (a) the financial statements have been properly drawn up in accordance with MASB

approved accounting standards and the Companies Act, 1965 so as to give a true and fair view of the financial position of the company and the group as at .......…………. and of their results and cash flows for the year then ended; and

(b) the accounting and other records and the registers required by the Act to be kept by the company and its subsidiaries have been properly kept in accordance with the provisions of the Act.

We are satisfied that the financial statements of the subsidiaries that have been consolidated with the company's financial statements are in form and content appropriate and proper for the purposes of the preparation of the consolidated financial statements and we have received satisfactory information and explanations required by us for those purposes. Our audit reports on the financial statements of the subsidiaries did not contain any qualification or any adverse comment made under subsection (3) of Section 174 of the Act.

(Audit Firm) [AF : 8888] Chartered Accountants (Partner) [9999/3/01(J/PH)] Partner Kuala Lumpur (Date )

Note : Where a company is exempt from preparing consolidated financial statements pursuant to paragraph 5(4)(a) of the Ninth Schedule to the Companies Act, 1965, the auditor's report in example 1 would be used but paragraph (b) in example 1 should be replaced with the relevant paragraph (b) in example 2 or example 3 as appropriate.

ISA 700

27

EXAMPLE 3 : Companies with subsidiaries - not all of which are audited by the reporting firm REPORT OF THE AUDITORS TO THE MEMBERS OF ............…………………………. We have audited the financial statements of .......……....… .for the year ended ……………….as set out on pages .......…. to ...........

These financial statements are the responsibility of the Company’s directors.

It is our responsibility to form an independent opinion, based on our audit, on the financial statements and to report our opinion to you, as a body, in accordance with section 174 of the Companies Act 1965 and for no other purpose. We do not assume responsibility to any other person for the content of this report.

We conducted our audit in accordance with approved standards on auditing in Malaysia. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement. An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements. An audit also includes assessing the accounting principles used and significant estimates made by directors, as well as evaluating the overall financial statements presentation. We believe that our audit provides a reasonable basis for our opinion.

In our opinion :

(a) the financial statements have been properly drawn up in accordance with MASB approved accounting standards and the Companies Act, 1965 so as to give a true and fair view of the financial position of the company and the group as at .......... and of their results and cash flows of the group for the year then ended; and

(b) the accounting and other records and the registers required by the Act to be kept by the company and its subsidiaries of which we have acted as auditors have been properly kept in accordance with the provisions of the Act.

*We have considered the financial statements and the auditors' reports of all the subsidiaries of which we have not acted as auditors, which are as follows :

*(See note on alternative wording)

We are satisfied that the financial statements of the subsidiaries that have been consolidated with the company's financial statements are in form and content appropriate and proper for the purposes of the preparation of the consolidated financial statements and we have received satisfactory information and explanations required by us for those purposes.

ISA 700

28

The auditors' reports on the financial statements of the subsidiaries did not contain any qualification or any adverse comment made under subsection (3) of Section 174 of the Act.

(Audit Firm) [AF : 8888] Chartered Accountants

(Partner) [9999/3/01(J/PH)] Partner

Kuala Lumpur (Date )

Note: *Alternative method of reporting by referring to the list of subsidiaries set out in the notes to the financial statements.

“We have considered the financial statements and the auditors’ reports of all the subsidiaries of which we have not acted as auditors, and which are indicated in note …………….to the financial statements.”

ISA 700

29

EXAMPLE 4 : Exempt Private Company Statement by the auditors under Section 165A accompanying the annual return

PQR SENDIRIAN BERHAD (Exempt Private Company)

We have audited the financial statements of ..............……….. for the year ended ……………….as set out on pages .......…. to ...........

These financial statements are the responsibility of the Company’s directors.

It is our responsibility to form an independent opinion, based on our audit, on the financial statements and to report our opinion to you, as a body, in accordance with section 174 of the Companies Act 1965 and for no other purpose. We do not assume responsibility to any other person for the content of this report.

(a) contained our opinion that the accounting and other records and the registers required by the Act to be kept by the company have been properly kept in accordance with the provisions of the Act; and

(b) did not contain any qualification or included any adverse comment made under section 174(3) of the Act.

As at the date to which the income statement has been made up, the company appeared to have been able to meet its liabilities as and when they fall due.

(Audit Firm) [AF : 8888] Chartered Accountants

(Partner) [9999/3/01(J/PH)] Partner

Kuala Lumpur (Date )

ISA 700

30

EXAMPLE 5 : Foreign incorporated company carrying on business in Malaysia.

REPORT OF THE AUDITORS ON THE COMPANY’S OPERATIONS IN MALAYSIA

PURSUANT TO SECTION 336 OF THE COMPANIES ACT, 1965 .............………

We have audited the financial statements of ...........……….. for the year ended ……………….as set out on pages .......…. to ...........

These financial statements are the responsibility of the Company’s directors. It is our responsibility to form an independent opinion, based on our audit, on the financial statements and to report our opinion to you, as a body, in accordance with section 174 of the Companies Act 1965 and for no other purpose. We do not assume responsibility to any other person for the content of this report. We conducted our audit in accordance with approved standards on auditing in Malaysia. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement. An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements. An audit also includes assessing the accounting principles used and significant estimates made by the agents, as well as evaluating the overall financial statements presentation. We believe that our audit provides a reasonable basis for our opinion. In our opinion :

(a) the financial statements have been properly drawn up in accordance with applicable approved accounting standards1 and the Companies Act, 1965 so as to give a true and fair view of the financial position of the company's operations in Malaysia as at ........... and of the results of those operations and cash flows for the year then ended; and

(b) the accounting and other records2 examined by us relating to the company's operations have been properly kept in accordance with the provisions of the Act.

(Audit Firm) [AF : 8888] Chartered Accountants

(Partner) [9999/3/01(J/PH)] Partner

Kuala Lumpur (Date )

1 Approved accounting standards is defined in the Financial Reporting Act 1997 to include: (a) new accounting standards issued by the MASB under paragraph 7(1)(a) (b) existing accounting standards adopted by the MASB under paragraph 7(1)(b) (c) in relation to foreign companies listed on a stock exchange in Malaysia, acceptable

internationally recognised accounting standards.

ISA 700

31

Section 26B of the Financial Reporting Act 1997 states that financial statements which are required to be prepared or lodged under any law administered by the Securities Commission, the Central Bank or the Registrar of Companies by foreign companies listed on a stock exchange in Malaysia shall comply in their entirety with either:

(a) any acceptable internationally recognised accounting standards; or (b) MASB approved accounting standards.

The Malaysian Accounting Standards Board (MASB) has approved the accounting standards issued by the following standards issuing bodies as acceptable international accounting standards:

(a) International Accounting Standards Board (b) Financial Accounting Standards Board, United States of America (c) Accounting Standards Board, United Kingdom (d) Australian Accounting Standards Board, Australia

2 Where an auditor is required to report on a register which is kept pursuant to the Companies Act, 1965, paragraph (b) would require the addition of the words “and the registers” after the word “records”.

ISA 700

32

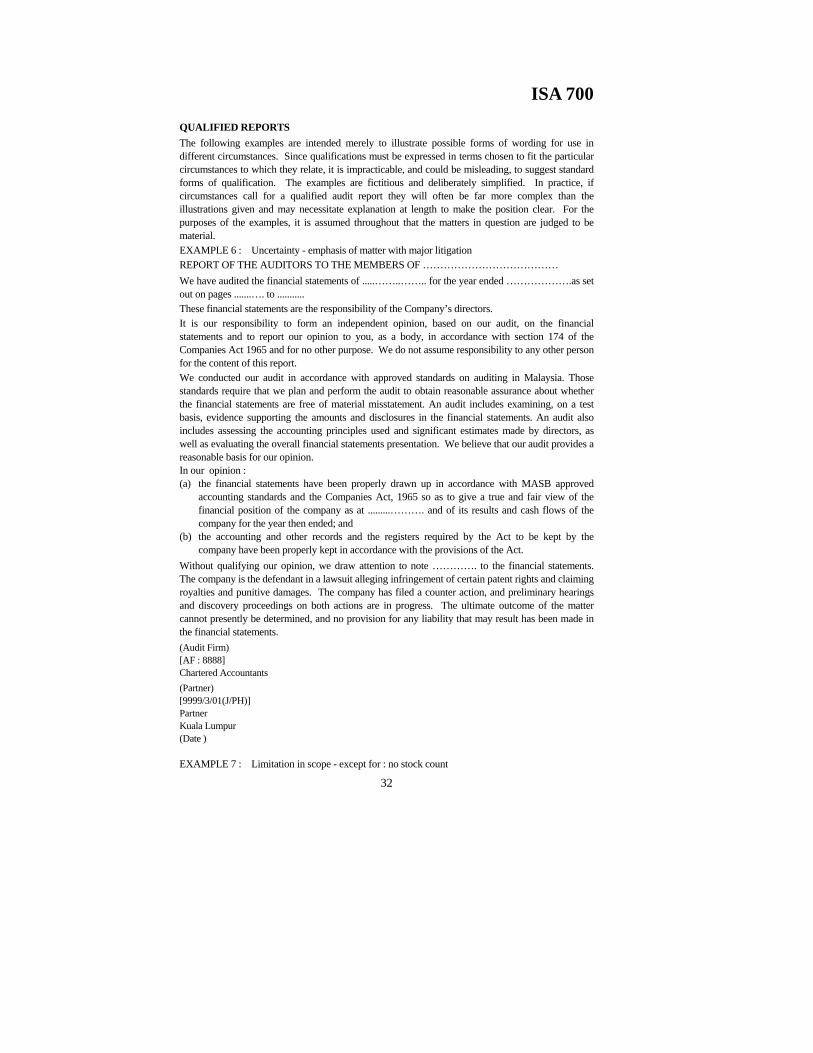

QUALIFIED REPORTS The following examples are intended merely to illustrate possible forms of wording for use in different circumstances. Since qualifications must be expressed in terms chosen to fit the particular circumstances to which they relate, it is impracticable, and could be misleading, to suggest standard forms of qualification. The examples are fictitious and deliberately simplified. In practice, if circumstances call for a qualified audit report they will often be far more complex than the illustrations given and may necessitate explanation at length to make the position clear. For the purposes of the examples, it is assumed throughout that the matters in question are judged to be material. EXAMPLE 6 : Uncertainty - emphasis of matter with major litigation REPORT OF THE AUDITORS TO THE MEMBERS OF ………………………………… We have audited the financial statements of .....……..…….. for the year ended ……………….as set out on pages .......…. to ........... These financial statements are the responsibility of the Company’s directors. It is our responsibility to form an independent opinion, based on our audit, on the financial statements and to report our opinion to you, as a body, in accordance with section 174 of the Companies Act 1965 and for no other purpose. We do not assume responsibility to any other person for the content of this report. We conducted our audit in accordance with approved standards on auditing in Malaysia. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement. An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements. An audit also includes assessing the accounting principles used and significant estimates made by directors, as well as evaluating the overall financial statements presentation. We believe that our audit provides a reasonable basis for our opinion. In our opinion : (a) the financial statements have been properly drawn up in accordance with MASB approved

accounting standards and the Companies Act, 1965 so as to give a true and fair view of the financial position of the company as at .........………. and of its results and cash flows of the company for the year then ended; and

(b) the accounting and other records and the registers required by the Act to be kept by the company have been properly kept in accordance with the provisions of the Act.

Without qualifying our opinion, we draw attention to note …………. to the financial statements. The company is the defendant in a lawsuit alleging infringement of certain patent rights and claiming royalties and punitive damages. The company has filed a counter action, and preliminary hearings and discovery proceedings on both actions are in progress. The ultimate outcome of the matter cannot presently be determined, and no provision for any liability that may result has been made in the financial statements. (Audit Firm) [AF : 8888] Chartered Accountants (Partner) [9999/3/01(J/PH)] Partner Kuala Lumpur (Date ) EXAMPLE 7 : Limitation in scope - except for : no stock count

ISA 700

33

REPORT OF THE AUDITORS TO THE MEMBERS OF …………………………………..

We have audited the financial statements of ...........……….. for the year ended ……………….as set out on pages .......…. to ...........

These financial statements are the responsibility of the Company’s directors.

It is our responsibility to form an independent opinion, based on our audit, on the financial statements and to report our opinion to you, as a body, in accordance with section 174 of the Companies Act 1965 and for no other purpose. We do not assume responsibility to any other person for the content of this report.

Except as discussed in the following paragraph, we conducted our audit in accordance with approved standards on auditing in Malaysia. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement. An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements. An audit also includes assessing the accounting principles used and significant estimates made by directors, as well as evaluating the overall financial statements presentation. We believe that our audit provides a reasonable basis for our opinion.

We did not observe the counting of the physical stocks as at .......…….., since that date was prior to the time we were initially engaged as auditors for the company. Owing to the nature of the company's records, we were unable to satisfy ourselves as to stock quantities by other audit procedures.

In our opinion, except for the effects of such adjustments, if any, as might have been determined to be necessary had we been able to satisfy ourselves as to physical stock quantities :

(a) the financial statements have been properly drawn up in accordance with MASB approved accounting standards and the Companies Act, 1965 so as to give a true and fair view of the financial position of the company as at ..........…………. and of its results and cash flows of the company for the year then ended; and

(b) the accounting and other records and the registers required by the Act to be kept by the company have been properly kept in accordance with the provisions of the Act.

(Audit Firm) [AF : 8888] Chartered Accountants

(Partner) [9999/3/01(J/PH)] Partner

Kuala Lumpur (Date )

ISA 700

34

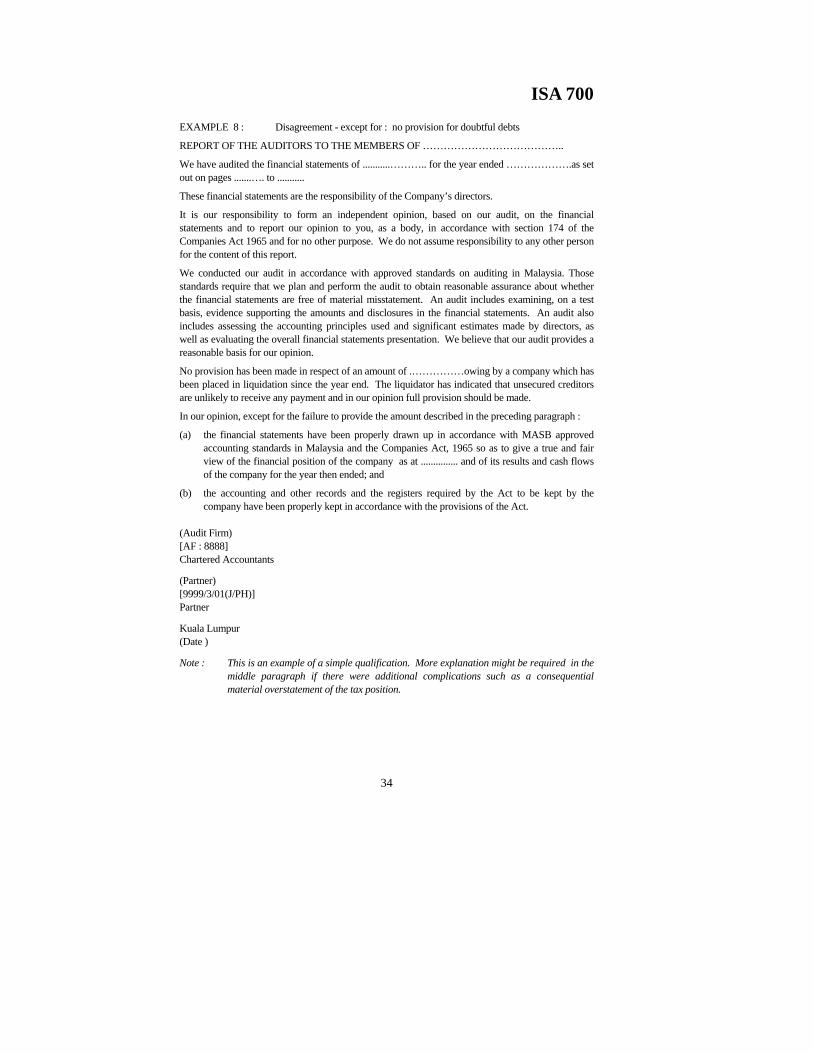

EXAMPLE 8 : Disagreement - except for : no provision for doubtful debts

REPORT OF THE AUDITORS TO THE MEMBERS OF …………………………………..

We have audited the financial statements of ...........……….. for the year ended ……………….as set out on pages .......…. to ...........

These financial statements are the responsibility of the Company’s directors.

It is our responsibility to form an independent opinion, based on our audit, on the financial statements and to report our opinion to you, as a body, in accordance with section 174 of the Companies Act 1965 and for no other purpose. We do not assume responsibility to any other person for the content of this report.

We conducted our audit in accordance with approved standards on auditing in Malaysia. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement. An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements. An audit also includes assessing the accounting principles used and significant estimates made by directors, as well as evaluating the overall financial statements presentation. We believe that our audit provides a reasonable basis for our opinion.

No provision has been made in respect of an amount of .……………owing by a company which has been placed in liquidation since the year end. The liquidator has indicated that unsecured creditors are unlikely to receive any payment and in our opinion full provision should be made.

In our opinion, except for the failure to provide the amount described in the preceding paragraph :

(a) the financial statements have been properly drawn up in accordance with MASB approved accounting standards in Malaysia and the Companies Act, 1965 so as to give a true and fair view of the financial position of the company as at ............... and of its results and cash flows of the company for the year then ended; and

(b) the accounting and other records and the registers required by the Act to be kept by the company have been properly kept in accordance with the provisions of the Act.

(Audit Firm) [AF : 8888] Chartered Accountants

(Partner) [9999/3/01(J/PH)] Partner

Kuala Lumpur (Date )

Note : This is an example of a simple qualification. More explanation might be required in the middle paragraph if there were additional complications such as a consequential material overstatement of the tax position.

ISA 700

35

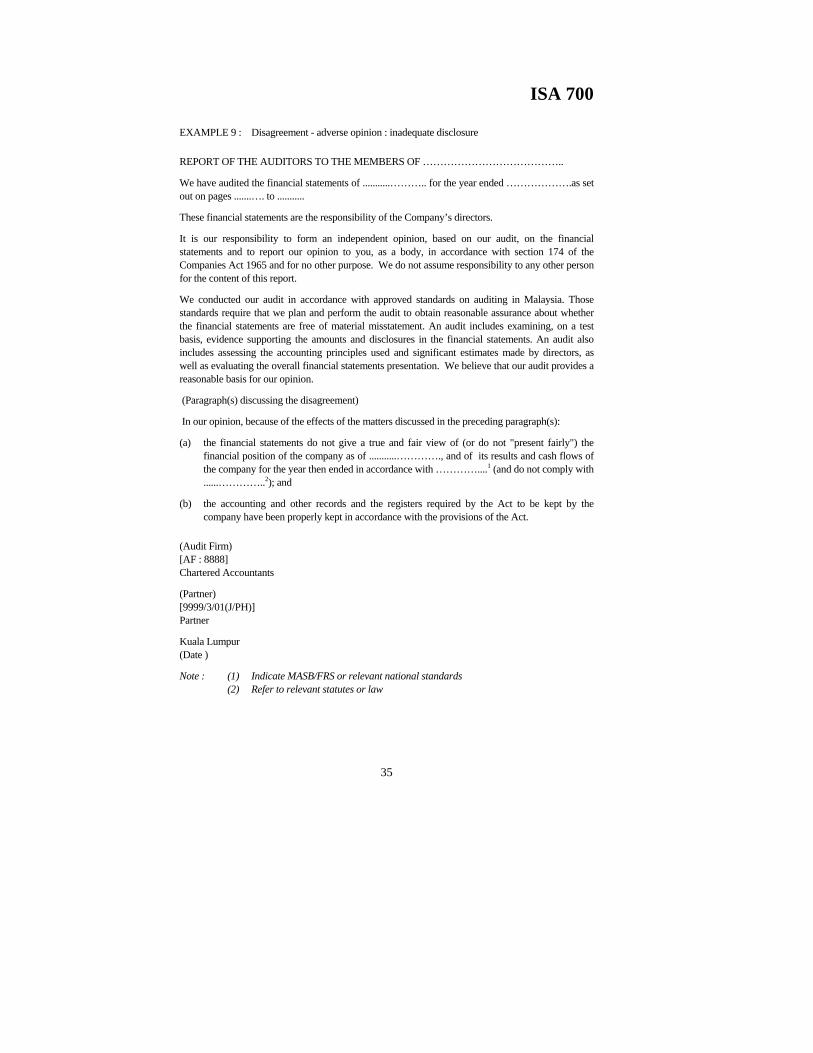

EXAMPLE 9 : Disagreement - adverse opinion : inadequate disclosure

REPORT OF THE AUDITORS TO THE MEMBERS OF …………………………………..

We have audited the financial statements of ...........……….. for the year ended ……………….as set out on pages .......…. to ...........

These financial statements are the responsibility of the Company’s directors.

It is our responsibility to form an independent opinion, based on our audit, on the financial statements and to report our opinion to you, as a body, in accordance with section 174 of the Companies Act 1965 and for no other purpose. We do not assume responsibility to any other person for the content of this report.

We conducted our audit in accordance with approved standards on auditing in Malaysia. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement. An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements. An audit also includes assessing the accounting principles used and significant estimates made by directors, as well as evaluating the overall financial statements presentation. We believe that our audit provides a reasonable basis for our opinion.

(Paragraph(s) discussing the disagreement)

In our opinion, because of the effects of the matters discussed in the preceding paragraph(s):

(a) the financial statements do not give a true and fair view of (or do not "present fairly") the financial position of the company as of ...........…………., and of its results and cash flows of the company for the year then ended in accordance with …………....1 (and do not comply with ......…………..2); and

(b) the accounting and other records and the registers required by the Act to be kept by the company have been properly kept in accordance with the provisions of the Act.

(Audit Firm) [AF : 8888] Chartered Accountants

(Partner) [9999/3/01(J/PH)] Partner

Kuala Lumpur (Date )

Note : (1) Indicate MASB/FRS or relevant national standards (2) Refer to relevant statutes or law

ISA 700

36

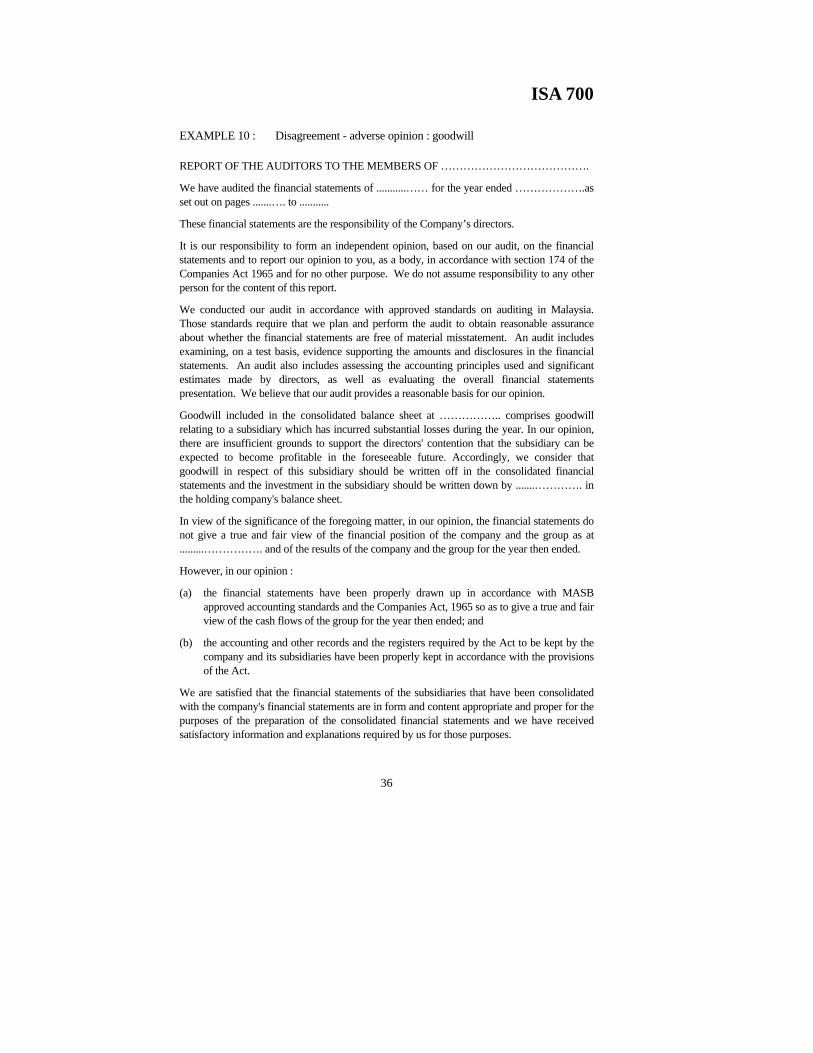

EXAMPLE 10 : Disagreement - adverse opinion : goodwill

REPORT OF THE AUDITORS TO THE MEMBERS OF ………………………………….

We have audited the financial statements of ...........…… for the year ended ……………….as set out on pages .......…. to ...........

These financial statements are the responsibility of the Company’s directors.

It is our responsibility to form an independent opinion, based on our audit, on the financial statements and to report our opinion to you, as a body, in accordance with section 174 of the Companies Act 1965 and for no other purpose. We do not assume responsibility to any other person for the content of this report.

We conducted our audit in accordance with approved standards on auditing in Malaysia. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement. An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements. An audit also includes assessing the accounting principles used and significant estimates made by directors, as well as evaluating the overall financial statements presentation. We believe that our audit provides a reasonable basis for our opinion.

Goodwill included in the consolidated balance sheet at …………….. comprises goodwill relating to a subsidiary which has incurred substantial losses during the year. In our opinion, there are insufficient grounds to support the directors' contention that the subsidiary can be expected to become profitable in the foreseeable future. Accordingly, we consider that goodwill in respect of this subsidiary should be written off in the consolidated financial statements and the investment in the subsidiary should be written down by .......…………. in the holding company's balance sheet.

In view of the significance of the foregoing matter, in our opinion, the financial statements do not give a true and fair view of the financial position of the company and the group as at .........……………. and of the results of the company and the group for the year then ended.

However, in our opinion :

(a) the financial statements have been properly drawn up in accordance with MASB approved accounting standards and the Companies Act, 1965 so as to give a true and fair view of the cash flows of the group for the year then ended; and

(b) the accounting and other records and the registers required by the Act to be kept by the company and its subsidiaries have been properly kept in accordance with the provisions of the Act.

We are satisfied that the financial statements of the subsidiaries that have been consolidated with the company's financial statements are in form and content appropriate and proper for the purposes of the preparation of the consolidated financial statements and we have received satisfactory information and explanations required by us for those purposes.

ISA 700

37

Our audit reports on the financial statements of the subsidiaries did not contain any qualification or any adverse comment made under subsection (3) of section 174 of the Act.

(Audit Firm) [AF : 8888] Chartered Accountants

(Partner) [9999/3/01(J/PH)] Partner

Kuala Lumpur (Date )

Notes : (1) In this case it has been assumed that, as the writing off of goodwill does not affect the total funds generated from operations, the cash flow statement has not been affected. The validity of this assumption will need to be considered in the light of individual circumstances.

(2) It is assumed that all subsidiaries are audited by the holding company's auditors.

ISA 700

38

EXAMPLE 11 : Uncertainty - disclaimer of opinion : accounting breakdown

REPORT OF THE AUDITORS TO THE MEMBERS OF …………………………...

We have audited the financial statements of ........…….……for the year ended ………..……….as set out on pages .......…. to ...........

These financial statements are the responsibility of the Company’s directors.

It is our responsibility to form an independent opinion, based on our audit, on the financial statements and to report our opinion to you, as a body, in accordance with section 174 of the Companies Act 1965 and for no other purpose. We do not assume responsibility to any other person for the content of this report.

We conducted our audit in accordance with approved standards on auditing in Malaysia. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement. An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements. An audit also includes assessing the accounting principles used and significant estimates made by directors, as well as evaluating the overall financial statements presentation. We believe that our audit provides a reasonable basis for our opinion.

As stated in note ……... , a fire at the company's computer centre destroyed many of the accounting records. The financial statements consequently include significant amounts based on estimates. In these circumstances, we have been unable to carry out all the auditing procedures, or to obtain all the information and explanations we have considered necessary.

In view of the significance of the matter referred to in the preceding paragraph, we are unable to form an opinion as to whether :

(a) the financial statements have been properly drawn up in accordance with MASB approved accounting standards and comply with the Companies Act, 1965 so as to give a true and fair view of the financial position of the company as at ..........……………and of the results and cash flows of the company for the year then ended; and

(b) the accounting and other records required by the Act to be kept by the company have been properly kept in accordance with provisions of the Act.

In our opinion, the registers required by the Act to be kept by the company have been properly kept in accordance with the provisions of the Act.

(Audit Firm) [AF : 8888] Chartered Accountants

(Partner) [9999/3/01(J/PH)] Partner

Kuala Lumpur (Date )

Notes : (1) This disclaimer of opinion would apply irrespective of the accounting convention adopted. (2) The notes to the financial statements should clearly identify which amounts are estimated.

(3) It is assumed that the registers were not burnt. EXAMPLE 12 : Limitation in scope - disclaimer of opinion : no stock count and unable to

confirm accounts receivable

ISA 700

39

REPORT OF THE AUDITORS TO THE MEMBERS OF ………………………….... We have audited the financial statements of ...........…………...…for the year ended …………….as set out on pages .......…. to ...........

These financial statements are the responsibility of the Company’s directors.

It is our responsibility to form an independent opinion, based on our audit, on the financial statements and to report our opinion to you, as a body, in accordance with section 174 of the Companies Act 1965 and for no other purpose. We do not assume responsibility to any other person for the content of this report.

(The paragraph discussing the scope of the audit would either be omitted or amended according to the circumstances.)

We were not able to observe all physical stocks and confirm accounts receivable due to limitations placed on the scope of our work by the company.

In view of the significance of the matters discussed in the preceding paragraph, we are unable to form an opinion as to whether the financial statements have been properly drawn up in accordance with MASB approved accounting standards and comply with the Companies Act, 1965 so as to give a true and fair view of the financial position of the company as at ..........……………and of the results and cash flows of the company for the year then ended.

However, in our opinion, the accounting and other records and the registers required by the Act to be kept by the company have been properly kept in accordance with the provisions of the Act.

(Audit Firm) [AF : 8888] Chartered Accountants

(Partner) [9999/3/01(J/PH)] Partner

Kuala Lumpur (Date )

ISA 700

40

EXAMPLE 13 : Non-compliance with MASB approved accounting standard Disagreement - except for: non-compliance with approved accounting standard on depreciation

REPORT OF THE AUDITORS TO THE MEMBERS OF …………………………

We have audited the financial statements of ...........………….. for the year ended ……………….as set out on pages .......…. to ...........

These financial statements are the responsibility of the Company’s directors.

It is our responsibility to form an independent opinion, based on our audit, on the financial statements and to report our opinion to you, as a body, in accordance with section 174 of the Companies Act 1965 and for no other purpose. We do not assume responsibility to any other person for the content of this report.

We conducted our audit in accordance with approved standards on auditing in Malaysia. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement. An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements. An audit also includes assessing the accounting principles used and significant estimates made by directors, as well as evaluating the overall financial statements presentation. We believe that our audit provides a reasonable basis for our opinion.

As discussed in note …………. to the financial statements, no depreciation has been provided in the financial statements in respect of the buildings and this is not in accordance with the approved accounting standard, FRS XXX or MASB XXX. The provision for the year ended .........………, if based on the straight line method of depreciation over management's estimate of their useful lives would amount to ...........……. On this basis, the carrying amount of fixed assets would be reduced by accumulated depreciation of ...........… and the profit for the year and accumulated profit would be decreased by .........…..and .............., respectively. In our opinion : (a) except for the non-compliance with the applicable approved accounting standard and the effect

on the financial statements of the matter referred to in the preceding paragraph, the financial statements have properly drawn up in accordance with MASB approved accounting standards and the Companies Act 1965 so as to give a true and fair view of the financial position of the company as at ...........………. and of the results and cash flows of the company for the year then ended and

(c) the accounting and other records and the registers required by the Act to be kept by the company have been properly kept in accordance with the provisions of the Act.

(Audit Firm) [AF : 8888] Chartered Accountants

(Partner) [9999/3/01(J/PH)] Partner

Kuala Lumpur (Date )

ISA 700

41

EXAMPLE 14 : Non-compliance with MASB approved accounting standard Disagreement – adverse opinion: contract losses not provided for in accordance with approved accounting standard on construction contracts

REPORT OF THE AUDITORS TO THE MEMBERS OF …………………………… We have audited the financial statements of ......…...……….. for the year ended ……………….as set out on pages .......…. to ...........

These financial statements are the responsibility of the Company’s directors.

It is our responsibility to form an independent opinion, based on our audit, on the financial statements and to report our opinion to you, as a body, in accordance with section 174 of the Companies Act 1965 and for no other purpose. We do not assume responsibility to any other person for the content of this report.

We conducted our audit in accordance with approved standards on auditing in Malaysia. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement. An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements. An audit also includes assessing the accounting principles used and significant estimates made by directors, as well as evaluating the overall financial statements presentation. We believe that our audit provides a reasonable basis for our opinion.