23

The financing dimension in SHA 2011 A focus on the Revenue of Schemes Patricia Hernandez WHO HA Geneva

The financing dimension in SHA 2011

A focus on the Revenue of Schemes

Patricia Hernandez WHO HA Geneva

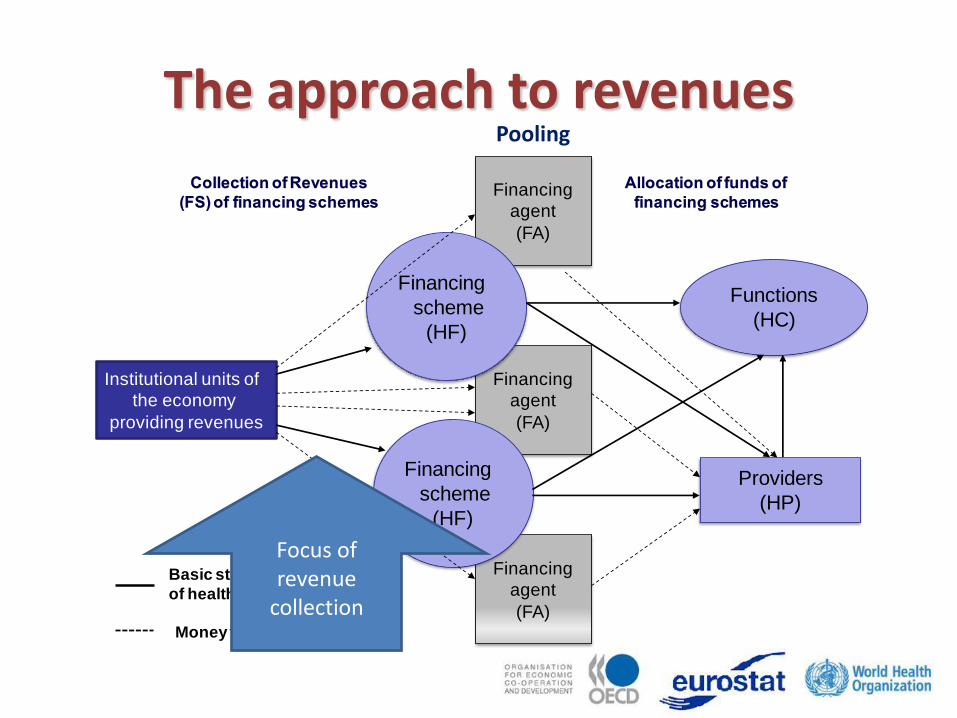

The approach to revenues

Financing

agent

(FA)

Financing

agent

(FA)

Institutional units of

the economy

providing revenues

Financing

agent

(FA)

Providers

(HP)

Functions

(HC)

Financing

scheme

(HF)

Financing

scheme

(HF)

Basic structural relationships

of health financing

Money flow

Pooling

Focus of revenue

collection

Revenues of health financing schemes (FS)

• Revenues vs. Expenditures – Revenue is an increase in the funds of a financing

scheme

– Expenditure is the amount spent by the institutional units providing resources.

• FS classification highlights the sources and the mechanisms of revenue raising for each financing scheme.

• PG tracked Financing Sources = expenditure by entities; whereas SHA 2011 track Revenues linked to expenditure by financing schemes.

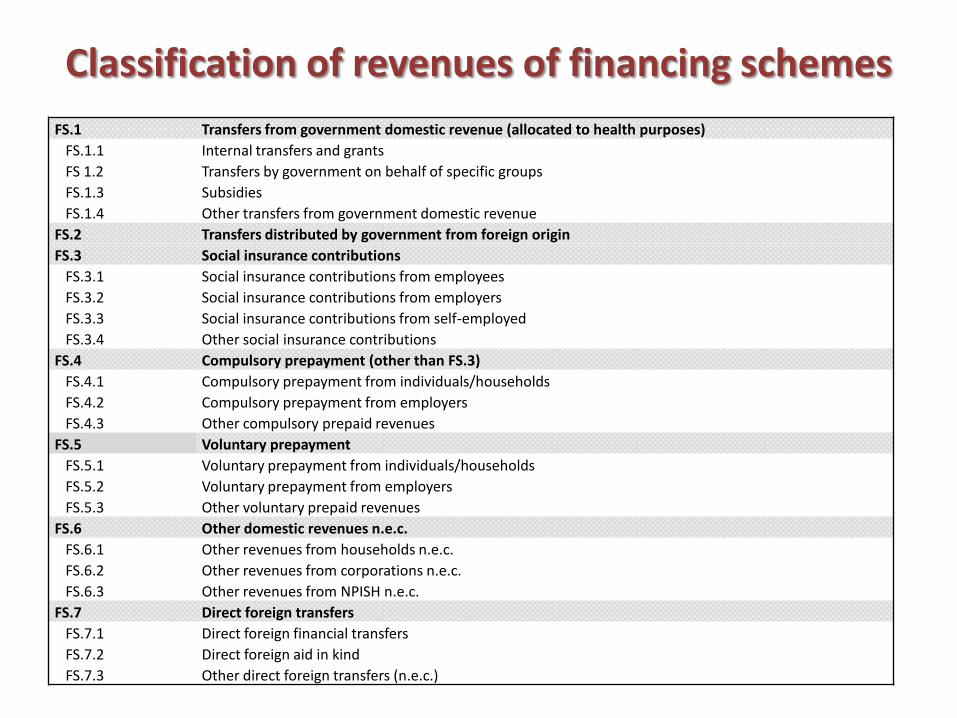

Classification of revenues of financing schemes (First digit)

FS.1Transfers from government domestic revenue (allocated to

health purposes)

FS.2 Transfers distributed by government from foreign origin

FS.3 Social insurance contributions

FS.4 Compulsory prepayment (other than FS.3)

FS.5 Voluntary prepayment

FS.6 Other domestic revenues n.e.c.

FS.7 Direct foreign transfers

Reporting items

FS.RI.1 Institutional units providing revenues to financing schemes

FS.RI.2 Total foreign revenues (FS.2 +FS.7)

FS Related

items

FSR.1 Loans

FSR.2 Aid in kind at donor value

Memorandum items

SNA based

Classification of revenues of financing schemes

FS.1 Transfers from government domestic revenue (allocated to health purposes)

FS.1.1 Internal transfers and grants

FS 1.2 Transfers by government on behalf of specific groups

FS.1.3 Subsidies

FS.1.4 Other transfers from government domestic revenue

FS.2 Transfers distributed by government from foreign origin

FS.3 Social insurance contributions

FS.3.1 Social insurance contributions from employees

FS.3.2 Social insurance contributions from employers

FS.3.3 Social insurance contributions from self-employed

FS.3.4 Other social insurance contributions

FS.4 Compulsory prepayment (other than FS.3)

FS.4.1 Compulsory prepayment from individuals/households

FS.4.2 Compulsory prepayment from employers

FS.4.3 Other compulsory prepaid revenues

FS.5 Voluntary prepayment

FS.5.1 Voluntary prepayment from individuals/households

FS.5.2 Voluntary prepayment from employers

FS.5.3 Other voluntary prepaid revenues

FS.6 Other domestic revenues n.e.c.

FS.6.1 Other revenues from households n.e.c.

FS.6.2 Other revenues from corporations n.e.c.

FS.6.3 Other revenues from NPISH n.e.c.

FS.7 Direct foreign transfers

FS.7.1 Direct foreign financial transfers

FS.7.2 Direct foreign aid in kind

FS.7.3 Other direct foreign transfers (n.e.c.)

Classification of revenues of financing schemes

Memorandum items Reporting items

FS.RI.1 Institutional units providing revenues to financing schemes

FS.RI.1.1 Government

FS.RI.1.2 Corporations

FS.RI.1.3 Households

FS.RI.1.4 NPISH

FS.RI.1.5 Rest of the world

FS.RI.2 Total foreign revenues (FS.2 +FS.7)

FS Related items

FSR.1 Loans

FSR.1.1 Loans taken by government

FSR.1.2 Loans taken by private organisations

FSR.2 Aid in kind at donor value

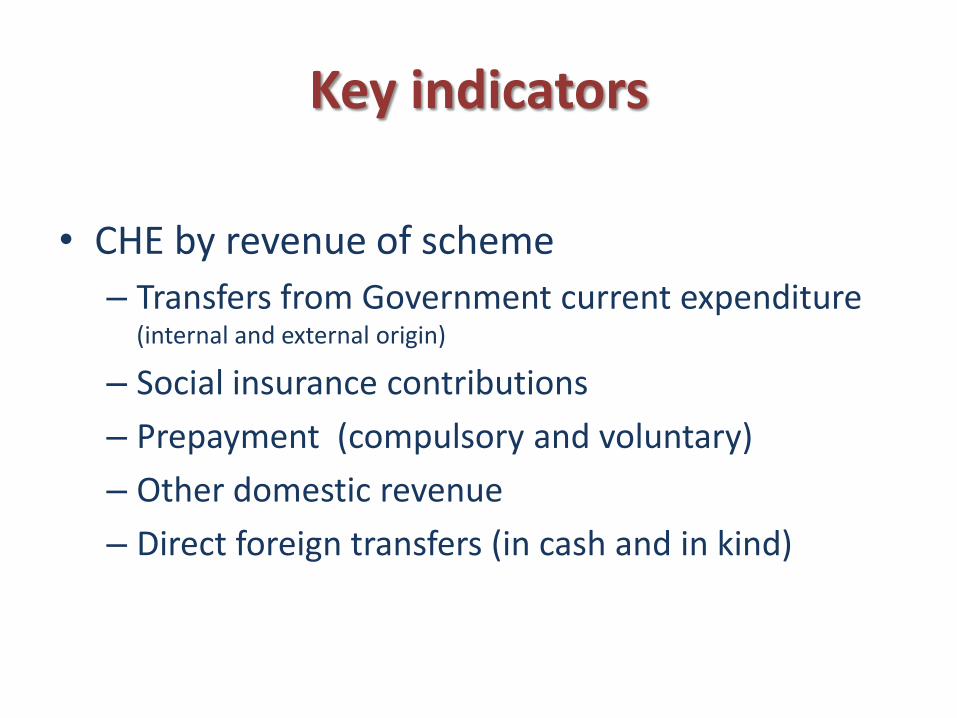

Key indicators

• CHE by revenue of scheme

– Transfers from Government current expenditure

(internal and external origin)

– Social insurance contributions

– Prepayment (compulsory and voluntary)

– Other domestic revenue

– Direct foreign transfers (in cash and in kind)

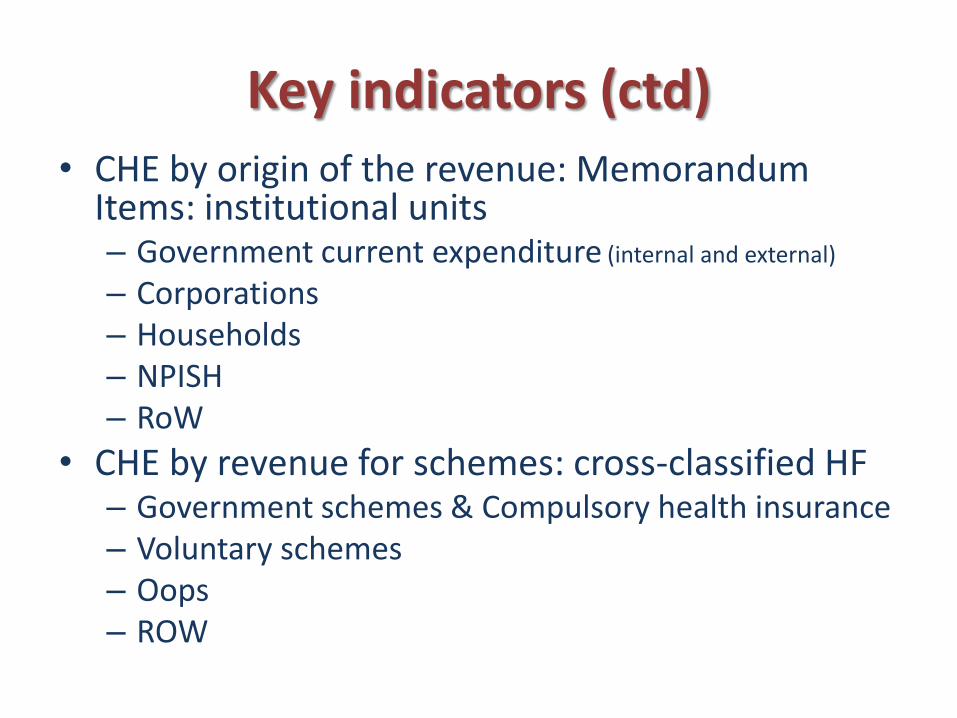

Key indicators (ctd) • CHE by origin of the revenue: Memorandum

Items: institutional units – Government current expenditure (internal and external)

– Corporations – Households – NPISH – RoW

• CHE by revenue for schemes: cross-classified HF – Government schemes & Compulsory health insurance – Voluntary schemes – Oops – ROW

Structure of the classification

• The classification refers to the mechanism directly channeling the resources to the scheme

– e.g. transfers by government from foreign origin

• Additional layers can be added to existing categories when needed

Example:

• FS.1.1 Internal transfers and grants – FS 1.1.2 Internal transfers and grants from general

revenues

– FS.1.1.3 Internal transfers and grants from earmarked tax

Multiple financing paths example of government flows

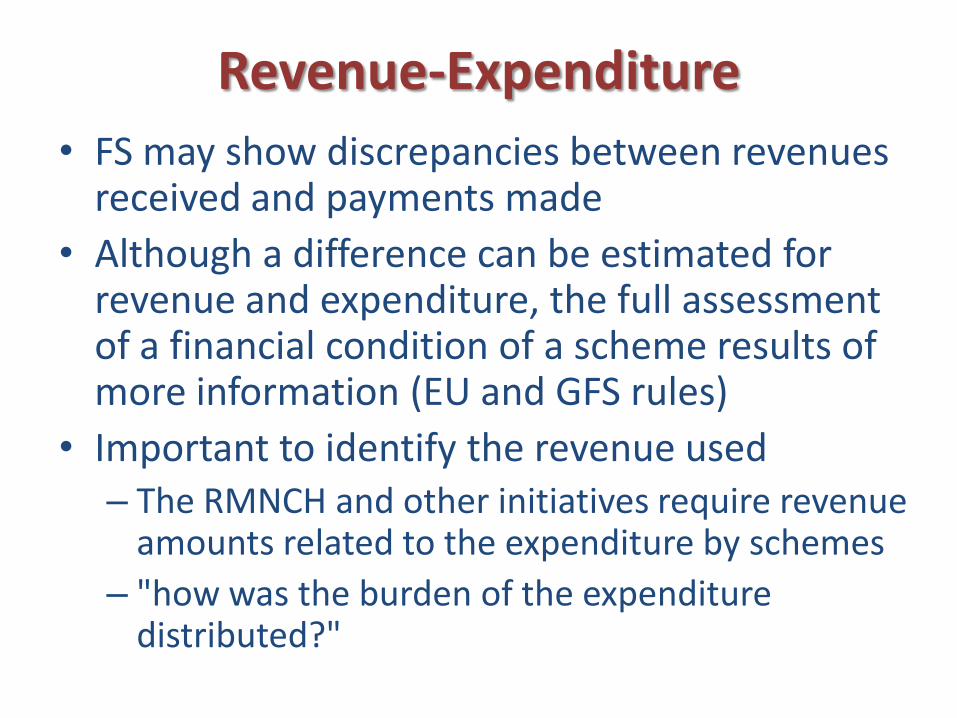

Revenue-Expenditure

• FS may show discrepancies between revenues received and payments made

• Although a difference can be estimated for revenue and expenditure, the full assessment of a financial condition of a scheme results of more information (EU and GFS rules)

• Important to identify the revenue used – The RMNCH and other initiatives require revenue

amounts related to the expenditure by schemes

– "how was the burden of the expenditure distributed?"

Public – Private mix

• "Compulsory" revenues are treated as governmental. – "Compulsory" reflects a public intervention resulting

in a regulated financial structure – Compulsory = public intervention

• "Voluntary" implies a discretionary use of resources, out of regulation, out of government direct intervention – Private decision on use of resources – It involves both public and private resources – Voluntary = non - governmental

• From the perspective of financing scheme:

– participation in a scheme is compulsory or voluntary

• From the perspective of the revenue:

– payment of revenue is compulsory or voluntary

• In SHA 2011 ownership is not the basis of analysis

Public – Private in SHA 2011

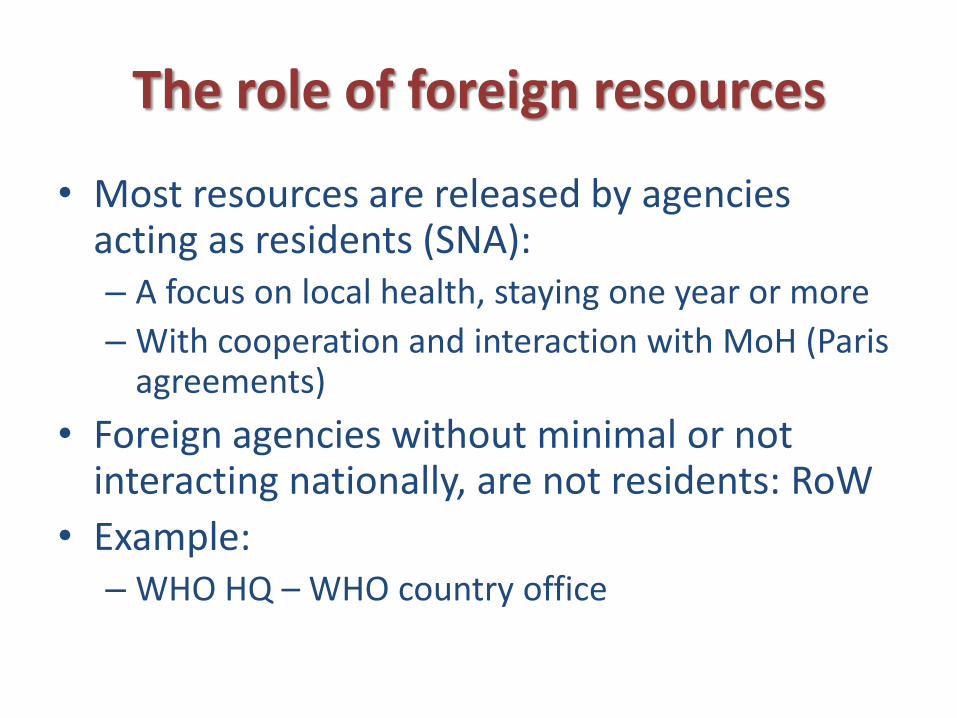

The role of foreign resources

• Most resources are released by agencies acting as residents (SNA): – A focus on local health, staying one year or more

– With cooperation and interaction with MoH (Paris agreements)

• Foreign agencies without minimal or not interacting nationally, are not residents: RoW

• Example: – WHO HQ – WHO country office

About loans • Loans are not a real increase of the funds

(they have to be repaid + they have a cost), they are reported as memorandum item

• Loans are recorded only on the amount used during the accounting period

• Debt forgiven as well as low interest loans (concessional and other quasi-grants) are recorded as RoW (FS.7)

About transfers • In kind transfers are included and valued at

current market prices. E.g. foreign technical assistance. The viewpoint of originators can be recorded below the line.

• Conditional health cash transfers are recorded as governmental, because recipient households cannot make a discretionary use of them

• Non conditional health transfers are excluded. They are recorded when spent / used by households on health care.

General Government – Public Sector

• Government = GFS public sector includes public corporations & other non budgetary entities

• National labels may not be equivalent to those in SHA 2011: – One "insurance" can nest several schemes – A label "insurance" can represent a governmental scheme

• NPIs are classified as part of government based on criteria (not only one, not all needed):

– Government appoints officers – Contractual agreements with government – Degree of financing by government – Other provisions (discretionary use of funds for other purposes) – Risk exposure

Coverage of the Government Sector reflected in reports

Source: GFS 2011 manual

Data Collection issues • Preparatory work for SHA 2011 framework • Data may still be collected from financing agents

• when there is third party involvement: shift from agent (SHA 1.0) to scheme (SHA 2011).

• Only health components are kept, and should be treated by scheme

• Surveys and other instruments need to be adjusted – added complexity and detail to the surveys/records to

cover from revenues to allocation, fund management and agents involved

– special effort to cover more relevant funds (size, role) – need of detail to allow the consolidation of flows.

Intermediation

• Agencies with no active role between allocation resources to health and paying for health services may operate, frequently to transfer resources

• Their intervention frequently involves an overhead or transaction costs important to capture

• Accounting for them is proposed based on documented reports or allocation based on administration costs

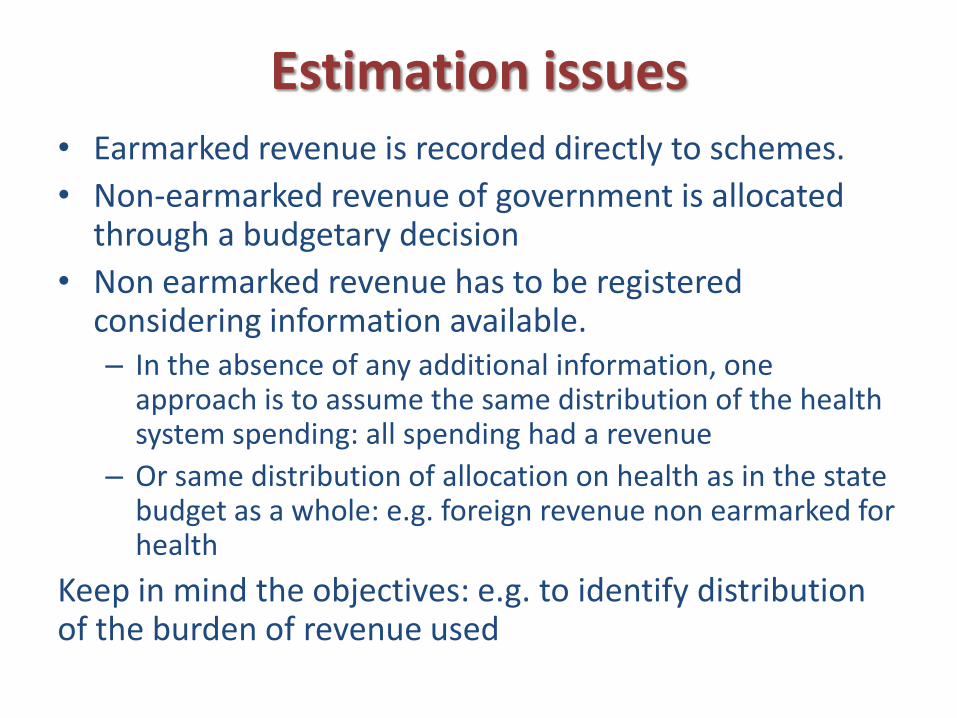

Estimation issues • Earmarked revenue is recorded directly to schemes.

• Non-earmarked revenue of government is allocated through a budgetary decision

• Non earmarked revenue has to be registered considering information available. – In the absence of any additional information, one

approach is to assume the same distribution of the health system spending: all spending had a revenue

– Or same distribution of allocation on health as in the state budget as a whole: e.g. foreign revenue non earmarked for health

Keep in mind the objectives: e.g. to identify distribution of the burden of revenue used

Guidelines / References

In addition to SHA 2011, PG, SHA 1.0

• Some revenue guidelines on the IMF Government Finance Statistics Manual (including compilation guide for developing countries)

Exercise

• Identify the revenue modalities existing in your country and mark those more relevant

• Continue the exercise for schemes and list the related revenue types for each scheme

• Identify their potential data sources

• Which revenues can be considered public, which private and which are external?