19

| Date post: | 03-Apr-2018 |

| Category: |

Documents |

| Upload: | duongthuan |

| View: | 218 times |

| Download: | 0 times |

This is a brief overview of some interesting aspects of the WESM

A separate paper is available covering additional issues

1

The Philippine WESM

• Competitive wholesale spot market / over 5 years of operating history (since June 2006)

• Over 70% of assets and dispatch rights privatised

• Historical power purchase agreements honoured

• Energy-only market -- no formal capacity payments

• Independent regulation through ERC

• Retail competition scheduled to evolve from December 2011

• Recent expansion of WESM to include the Visayas (Dec 2010)

• And more is planned

– Ancillary services market

– Independent Market Operator

• And more is needed

2

Oil

Natural Gas

Coal

Geothermal

Hydro

• Local hydro and geothermal

• Locally developed, internationally priced

natural gas

• Some indigenous coal, but mostly imported

• Fuel is essentially at global market prices

– Maybe LNG in the future

– Coal is the currently growing generation source

• Renewables feed-in tariff

– But impact on total quantity unclear

3

Luzon fuel mix

Private sector, no industry subsidies

Power Plant

Rated

Capacity

(MW)

Winning Bidder Winning Price

(US$ million)

US$M/

MW

Pantabangan-Masiway 112.0 First Gen Hydropower 129.0 1.15

Magat Hydroelectric 360.0 SN Aboitiz Power 530.0 1.47

Masinloc 600.0 Masinloc Power Partners

Co. Ltd. 930.0 1.55

Ambuklao-Binga 175.0 SN Aboitiz Power 325.0 1.86

Tiwi-MakBan Geothermal 747.5 AP Renewables. 446.9 0.60

Batangas (Calaca) 600.0 DMCI Holdings,. 361.7 0.60

Palinpinon-Tongonan 305.0 Green Core Geothermal 220.0 0.72

Angat Hydro Electric * 218.0 Korea Water Resources

Development 440.9 2.02

Total 4,320.3 3,467.5

[*] Sale pending a dispute

4

Innovative Approach to Competition: IPPA

IPPA Opportunity

Contracted

Capacity

(MW)

Winning

Bidder

Winning Price

(USD MM)

USD

MM/MW

Pagbilao Coal Fired 700 Therma Luzon Inc. 691 0.98

Sual Coal Fired 1,000 San Miguel Corporation 1,107 1.11

San Roque Hydro 345 San Miguel Corporation 450 1.30

Bakun-Benguet Hydros * 100.75 Amlan Power Holdings 145 1.43

Ilijan Combined Cycle 1,200 San Miguel Corporation 870 0.73

Total 3,345 3,263

[*] Benguet IPPA subject to a dispute

5

IPPA Process puts merchant players in the WESM to while honoring existing

agreements

6

PSALM IPPA IPP

PPA, ECA, etc. New

Administration Agreement

7

Each IPPA structure deals with different underlying issues

• FOAK for Philippine WESM

• Coal procurement

• Excess capacity (plant output > PPA)

• Various market interface and metering

issues reduced value and added risks to

the structure

Sual and Pagbilao

• Hydrological uncertainty and poor data

complicated valuation

• Used generation payment approach to

reduce risk to bidders to achieve better

outcomes for PSALM

Hydro’s

• Long term fixed gas contract

• Unprofitable operation in the WESM

• Risk sharing agreement developed

Ilijan

• Peaking plant but significant fuel-related

constraints

• Must-run status and compensation

uncertainties

• Ultimately not sold

Malaya

8

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

Jan-

07

Mar

-07

May

-07

Jul-0

7

Sep-0

7

Nov

-07

Jan-

08

Mar

-08

May

-08

Jul-0

8

Sep-0

8

Nov

-08

Jan-

09

Mar

-09

May

-09

Jul-0

9

Sep-0

9

Nov

-09

Jan-

10

Mar

-10

May

-10

Jul-1

0

Sep-1

0

Nov

-10

Jan-

11

Mar

-11

De

ma

nd

(M

W)

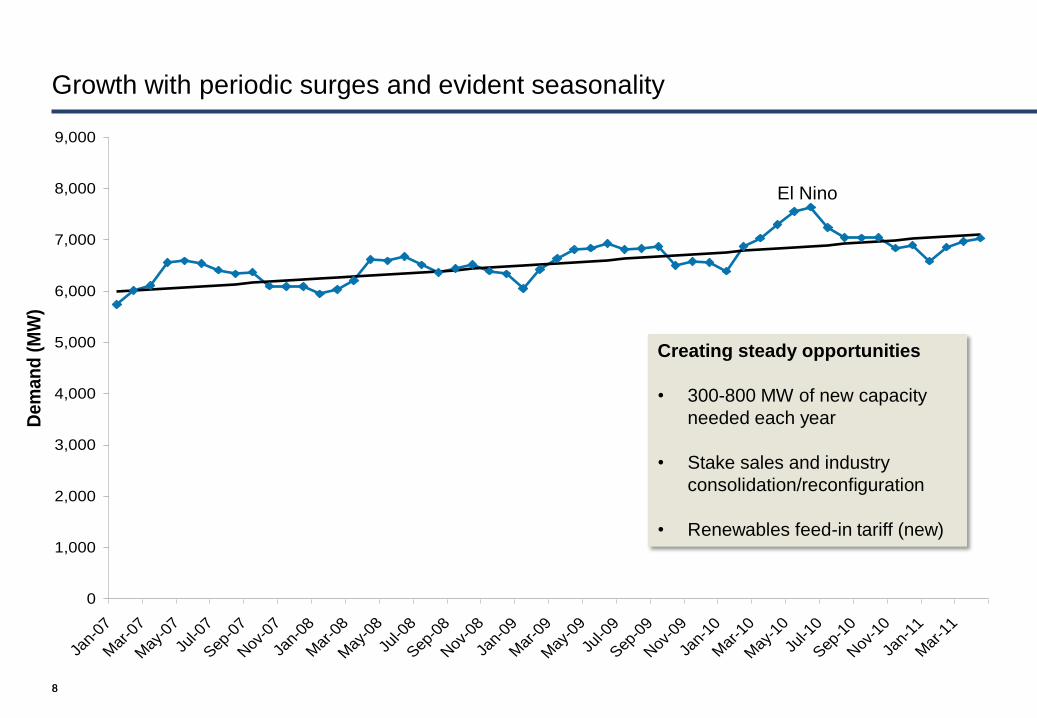

Creating steady opportunities

• 300-800 MW of new capacity

needed each year

• Stake sales and industry

consolidation/reconfiguration

• Renewables feed-in tariff (new)

Growth with periodic surges and evident seasonality

8

El Nino

Event Driven Market (WESM Spot Price) Outcomes

Monthly Average Ex-Post LWAP

0

2,000

4,000

6,000

8,000

10,000

12,000

Jul-0

6

Aug

-06

Oct-0

6

Dec

-06

Mar

-07

May

-07

Jul-0

7

Sep

-07

Nov

-07

Jan-

08

Mar

-08

May

-08

Jul-0

8

Sep

-08

Nov

-08

Jan-

09

Mar

-09

May

-09

Jul-0

9

Sep

-09

Nov

-09

Jan-

10

Mar

-10

May

-10

Jul-1

0

Sep

-10

Nov

-10

Jan-

11

Mar

-11

Pe

so

/kW

h

Gas

curtailment

s

Plant

outages

and coal

limitations

Plant

outages

Major typhoon

damage to plant

and lines

Gas

curtailments

and low

hydro

Low

hydro

9

High

Hydro

Load Weighted Average Prices

Volatility is driving investment in more capacity and flexibility

Recurring El Nino Effects are worth noting…

10

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

0% 10% 20% 30% 40% 50% 60% 70% 80% 90%

2007 2008 2009 2010

El Nino Year (2010)

MW Load Duration Curve

“El Niño and La Niña occur on average every 3

to 5 years. However, in the historical record the

interval between events has varied from 2 to 7

years.” http://www.elnino.noaa.gov/lanina_new_faq.html

Periodic El Nino effect is a boon to retention of older stand-by capacity and efficient flexible response

Until demand grows further, the plant mix puts dispatch pressure on coal

11

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

0% 10% 20% 30% 40% 50% 60% 70% 80% 90%

2007 2008 2009 2010

El Nino Year (2010)

Take or pay gas 2700 MW

Hydro+Geothermal about 4000 MW

Total 6,700 MW of “non-coal”

MW Load Duration Curve

5000

Main problem is to “digest” the surplus of “must take” generation, which displaces coal

12

Hydro variation is a key issue

Wet (2009)

Sorted Daily GWhs by fuel type

Dry (2010)

Sorted Daily GWhs by fuel type

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1

1

20

39

58

77

96

11

5

13

4

15

3

17

2

19

1

21

0

22

9

24

8

26

7

28

6

30

5

32

4

34

3

36

2Diesel/Oil

Hydro

Natural Gas

Coal

Wind

Geothermal

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1

1

20

39

58

77

96

11

5

13

4

15

3

17

2

19

1

21

0

22

9

24

8

26

7

28

6

30

5

32

4

34

3

36

2

Diesel/Oil

Hydro

Natural Gas

Coal

Wind

Geothermal

More Coal ON peak

More Oil OFF Peak

Difference between a dry and wet year depends on fuel and capacity availability

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Luzon Baseload

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Luzon Baseload

Luzon managed El Nino 2010 by calling upon its underutilised coal capacity

Much spare energy in 2009

at least relative to “theoretical” utilisation levels

Much less spare energy in 2010

due to El Nino, mainly

13

Unused coal capacity earned its reward in 2010 during higher temperatures and lower water availability

14

The ratio of price to “full-availability” SRMC varies with supply and demand

2009 2008

-4

-2

0

2

4

6

8

10

0.4 0.5 0.6 0.7 0.8

-4

-2

0

2

4

6

8

10

0.4 0.5 0.6 0.7 0.8

Relatively Wet Year San Jose Transformer Fault

Demand / “Capacity”

Price / “SRMC”

Demand / “Capacity”

Market prices in the WESM are highly responsive to conditions – very strong signals for investment

and responsiveness

Opportunity for “spare” capacity (Malaya Example)

Analysis of Malaya Must Run since August 2008

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

Aug-

08

Sep-

08

Oct-

08

Nov-

08

Dec-

08

Jan-

09

Feb-

09

Mar-

09

Apr-

09

May-

09

Jun-

09

Jul-

09

Aug-

09

Sep-

09

Oct-

09

Nov-

09

Dec-

09

Jan-

10

Feb-

10

Mar-

10

Apr-

10

May-

10

Mu

st

Ru

n E

ne

rgy

(M

Wh

)

Performance and Emissions Tests Outages and problems with other Gencos Low hydro/Malampya Outages

San Jose Transformer issues Transmission Problems (exc San Jose)

15

Older steam (oil) capacity proved essential during El Nino period

Profitable management of older capacity can depend heavily on the “must run”

compensation regime or on the future ancillary services market

0

50

100

150

200

250

300

0.0 0.5 1.0 1.5 2.0 2.5

Avg Peak Price to Dispatch Cost Ratio

Avg

Ho

url

y G

en

era

tio

n (

MW

)

Forced Generation

Economic Generation

"No" Generation

Breakeven Peak Price Ratio

SHOULD RUN SHOULD NOT RUN

“Forced Generation” is unprofitable generation that is required to meet ancillary services requirements

Compensation regime is crucial

Summary

• Sophisticated energy-only wholesale spot market in a developing country

• Over 5 years old, recently expanded to cover the Visayas region

• WESM has now operated during two presidential administrations

• Substantially privatized (more than Australia)

• Progressing to implement Ancillary Services Market

• Evaluating introduction of Independent Market Operator

• Survived El Nino 2010

• Incentivizing rehabilitation and plant improvement investment

• Reasonably competitive structure

• Independent regulation

• All fuel types represented (coal, gas, hydro, geothermal, renewables, oil)

• Mix of domestic and international investors

17

Thank you

18