• How many bottles of L’Oréal Elvive Triple Resist Reinforcing Shampoo would you get for the global brand value of L’Oréal?

1 billion

3 billion

5 billion

• How many Amazon delivery trucks would you need to get them to your home?

40,000

100,000

300,000

• How long would the supply last an average family?

10 years

99 years

250m years

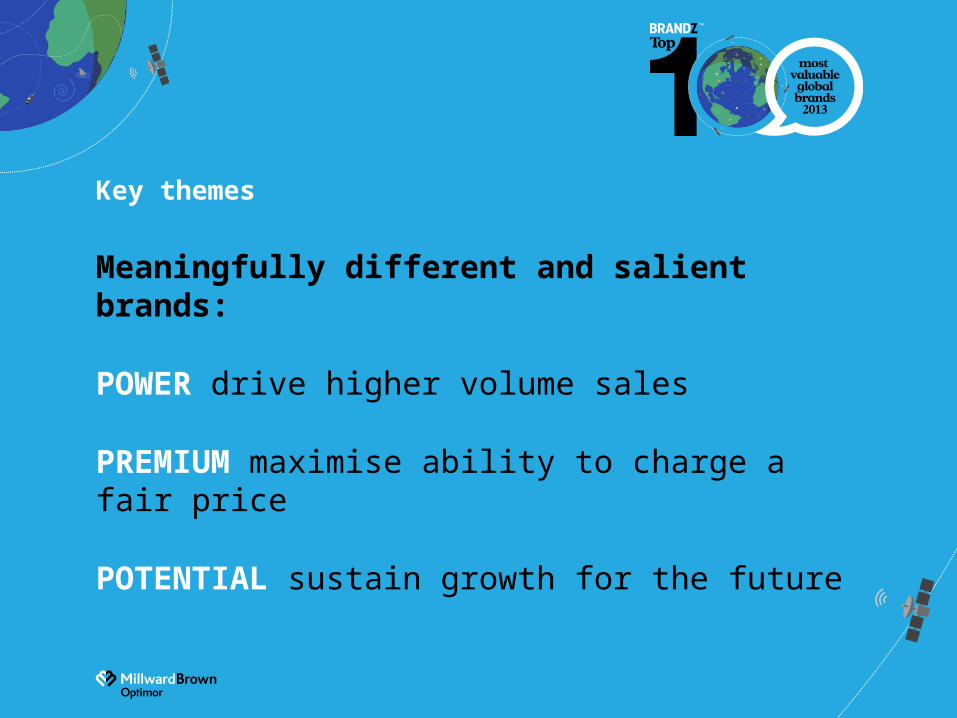

Key themes

Meaningfully different and salient brands:

POWER drive higher volume sales

PREMIUM maximise ability to charge a fair price

POTENTIAL sustain growth for the future

Top 100 Brands

MEANINGFUL 115

DIFFERENT 120

SALIENT 131

Average for all brands 100

Eight Years, Eight Top Risers

BRAND BRAND VALUE($M)

BRAND VALUE CHANGE

Subway 16,700 +5,798%

Apple 185,071 +1,058%

Amazon 45,700 +664%

Hermès 19,129 +296%

Zara 20,167 +295%

SAP 34,365 +259%

Verizon 53,004 +256%

IBM 112,536 +212%

Up

+425%Top 100 up

+77%

Eight Success Trends

Great Value Proposition

Relevant for today

Harnessing technology

Getting abroad and about

Reputation

Meaningfully Different

Personality

A great branded experience

Asia leads growth

Top 10 vs 2012

Asia +13%

Continental Europe +5%

UK +4%

US +2%

LatAm -13%

Rankings: Top 10 Asia

BRAND BRAND VALUE($M)

BRAND VALUE CHANGE

China Mobile 55,368 +18%

ICBC 41,115 -1%

Tencent 27,273 +52%China Construction Bank 26,859 +10%

Toyota 24,497 +12%

Samsung 21,404 +51%

Baidu 20,443 -16%Agriculture Bank of China 19,975 +12%

Commonwealth Bank of Australia 17,745 +36%

ANZ 16,565 New

+13%

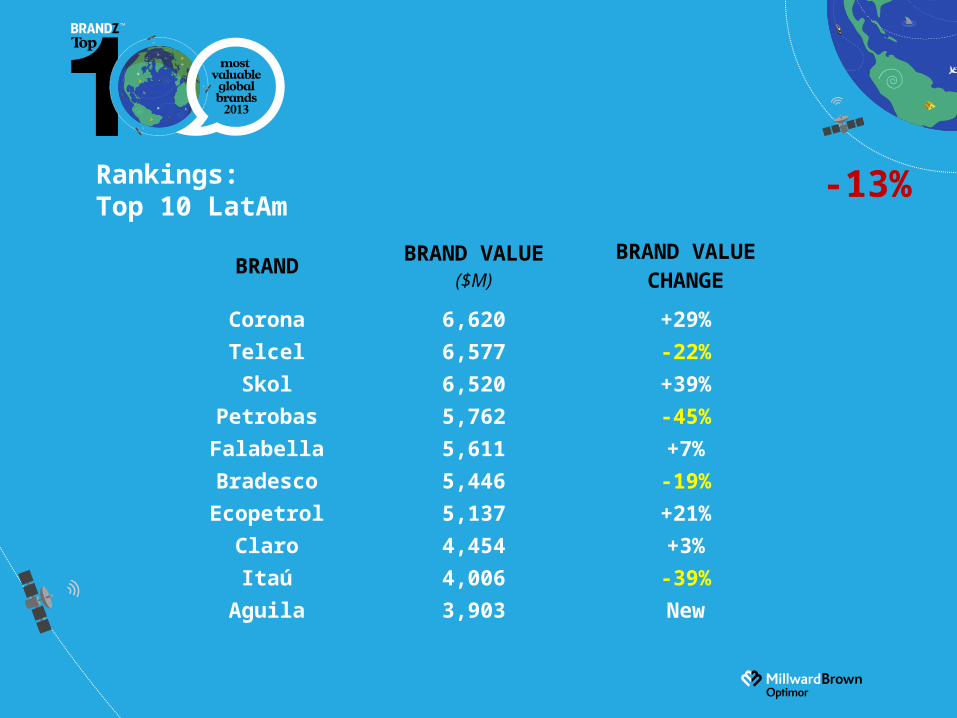

Rankings: Top 10 LatAm

BRAND BRAND VALUE($M)

BRAND VALUE CHANGE

Corona 6,620 +29%

Telcel 6,577 -22%

Skol 6,520 +39%

Petrobas 5,762 -45%

Falabella 5,611 +7%

Bradesco 5,446 -19%

Ecopetrol 5,137 +21%

Claro 4,454 +3%

Itaú 4,006 -39%

Aguila 3,903 New

-13%

Fast Growing markets: Other

BRAND BRAND VALUE($M)

BRAND VALUE CHANGE

ICICI Bank (India) 14,196 +12%

Sberbank (Russia) 12,655 +19%

MTN (Africa) 11,448 +23%

MTS (Russia) 10,633 +11%

Airtel (India) 10,054 -13%

Gazprom (Russia) 6,182 -8%

Lukoil (Russia) 5,011 New

Rankings: Top 10 North America

BRAND BRAND VALUE($M)

BRAND VALUE CHANGE

Apple 185,071 +1%

Google 113,669 +5%

IBM 112,536 -3%

McDonald’s 90,256 -5%

Coca-Cola 78,415 +6%

AT&T 75,507 +10%

Microsoft 69,814 -9%

Marlboro 69,383 -6%

Visa 56,060 +46%

GE 55,357 +21%

(Canada: RBC 38th, TD 46th, Scotiabank 85th)

+2%

Rankings: Top 10 UK

BRAND BRAND VALUE($M)

BRAND VALUE CHANGE

Vodafone 39,712 -8%

HSBC 23,970 +24%

Shell 17,678 -1%

Tesco 16,303 -9%

BP 11,520 +11%

Standard Chartered 10,160 +1%

BT 9,531 New

Barclays 7,989 +34%

O2 5,965 -30%

Dove 4,927 +5%

+4%

Rankings: Top 10 Continental Europe

BRAND BRAND VALUE($M)

BRAND VALUE CHANGE

SAP 34,365 +34%

BMW 24,015 -2%

Deutsche Telekom 23,893 -11%

Louis Vuitton 22,719 -12%

Zara 20,167 +60%

Hermès 19,129 0%

L'Oréal 17,971 +30%

Mercedes-Benz 17,952 +11%

Orange 13,829 -10%

Movistar 13,336 -22%

+5%

BRAND BRAND VALUE($M)

BRAND VALUE

CHANGE

Amazon 45,727 +34%

Walmart 36,220 +5%

The Home Depot 18,488 +43%

eBay 17,749 +40%

Tesco 16,303 -9%

IKEA 12,040 +31%

Target 11,879 +13%

Woolworths 11,039 -

ALDI 8,885 -5%

Lowe’s 7,559 +26%

Consumer: Top 20 Retail 2013

BRAND BRAND VALUE($M)

BRAND VALUE

CHANGE

Carrefour 7,372 -6%

Costco 6,789 +33%

Whole Foods 6,728 -

Walgreens 5,925 -

CVS 5,620 -

Falabella 5,611 +7%

M&S 4,649 +7%

Asda 4,617 +19%

Lidl 4,524 -2%

Coles 4,416 -

Key Take Aways

PURPOSE

CONSUMERS

COMMUNICATION

GROWTH

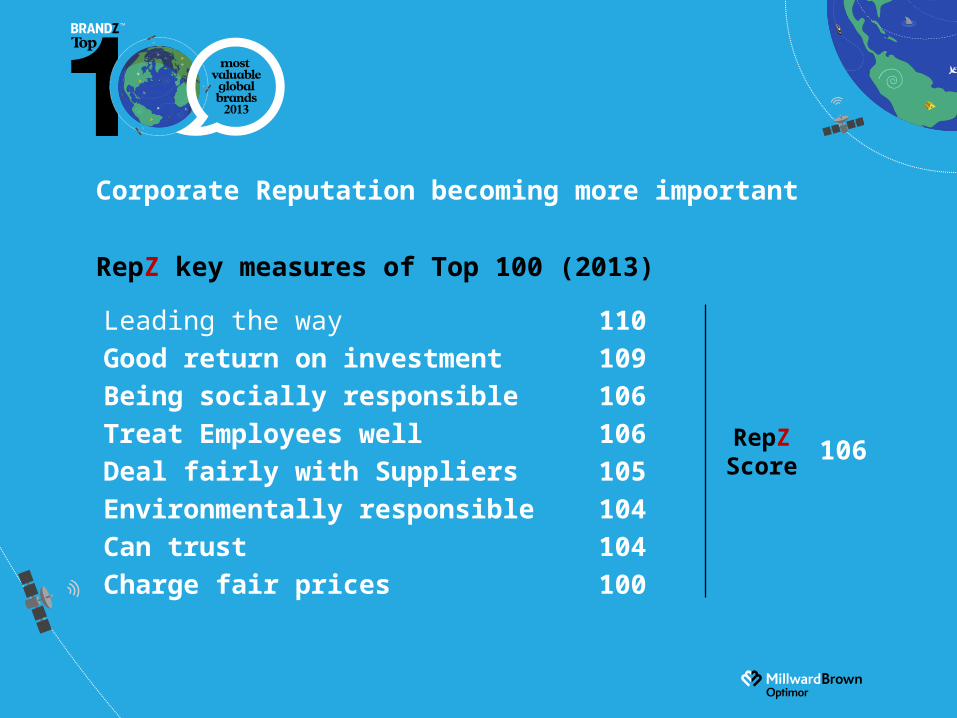

Corporate Reputation becoming more important

RepZ key measures of Top 100 (2013)

Leading the way 110Good return on investment 109Being socially responsible 106Treat Employees well 106Deal fairly with Suppliers 105Environmentally responsible 104Can trust 104Charge fair prices 100