The Reserving Actuary’s Role in Risk Assessment: Value Added by the Reserving Actuary in Identifying and Helping Mitigate Financial Risk Both on the Balance Sheet and in Underwriting and Financial Considerations Presented at the Casualty Loss Reserve Seminar By: Ronald T. Kuehn, FCAS, MAAA, CPCU, ARM, FCA Consulting Actuary September 12, 2005 1

Transcript

The Reserving Actuary’s Role in Risk Assessment:Value Added by the Reserving Actuary in Identifying

and Helping Mitigate Financial Risk Both on the Balance Sheet and in Underwriting and

Financial Considerations

The Reserving Actuary’s Role in Risk Assessment:Value Added by the Reserving Actuary in Identifying

and Helping Mitigate Financial Risk Both on the Balance Sheet and in Underwriting and

•Started in early 1980’s when insurers stopped offering occurrence policies

•Originally held as loss or unearned premium reserve

•Currently must be disclosed in opinion and displayed in Exhibit B

DDR Reserve

•Free tail for death disability and retirement

•Started in early 1980’s when insurers stopped offering occurrence policies

•Originally held as loss or unearned premium reserve

•Currently must be disclosed in opinion and displayed in Exhibit B

33

The Reserving Actuary’s Role in Risk Assessment:

Value Added by the Reserving Actuary

The Reserving Actuary’s Role in Risk Assessment:

Value Added by the Reserving Actuary

DDR Reserve

Items Required to Compute DDR Reserve (per insured)

•Age

•Policy Inception Date

•Premium

•Also need withdrawal rates by age, assumed retirement age, and decrement (death and disability) tables

DDR Reserve

Items Required to Compute DDR Reserve (per insured)

•Age

•Policy Inception Date

•Premium

•Also need withdrawal rates by age, assumed retirement age, and decrement (death and disability) tables

44

The Reserving Actuary’s Role in Risk Assessment:

Value Added by the Reserving Actuary

The Reserving Actuary’s Role in Risk Assessment:

Value Added by the Reserving Actuary

DDR Reserve

NAIC Accounting Practices and Procedures Manual

“Reserve is required to assure that amounts collected by insurers to pay for these benefits are not earned prematurely and that an insurer with an aging book of business will not show adverse operating results simply because an increasing portion of insureds is earning the benefits for which it has paid”

DDR Reserve

NAIC Accounting Practices and Procedures Manual

“Reserve is required to assure that amounts collected by insurers to pay for these benefits are not earned prematurely and that an insurer with an aging book of business will not show adverse operating results simply because an increasing portion of insureds is earning the benefits for which it has paid”

55

The Reserving Actuary’s Role in Risk Assessment:

Value Added by the Reserving Actuary

The Reserving Actuary’s Role in Risk Assessment:

Value Added by the Reserving Actuary

DDR Reserve- Steps in Modeling Accrued LiabilityDDR Reserve- Steps in Modeling Accrued Liability

•1. Develop current cost of tail benefit, adjusted for population

•2. Project cost by multiplying by annual growth in premiums

•3. Compute present value of step 2 at entry age based on mortality, interest and withdrawal

•4. Compute present value of step 2 at attained age based on mortality, interest and withdrawal

•5. Compute annuity factor from attained age to retirement, based on premium growth, mortality and withdrawal

•1. Develop current cost of tail benefit, adjusted for population

•2. Project cost by multiplying by annual growth in premiums

•3. Compute present value of step 2 at entry age based on mortality, interest and withdrawal

•4. Compute present value of step 2 at attained age based on mortality, interest and withdrawal

•5. Compute annuity factor from attained age to retirement, based on premium growth, mortality and withdrawal

66

The Reserving Actuary’s Role in Risk Assessment:

Value Added by the Reserving Actuary

The Reserving Actuary’s Role in Risk Assessment:

Value Added by the Reserving Actuary

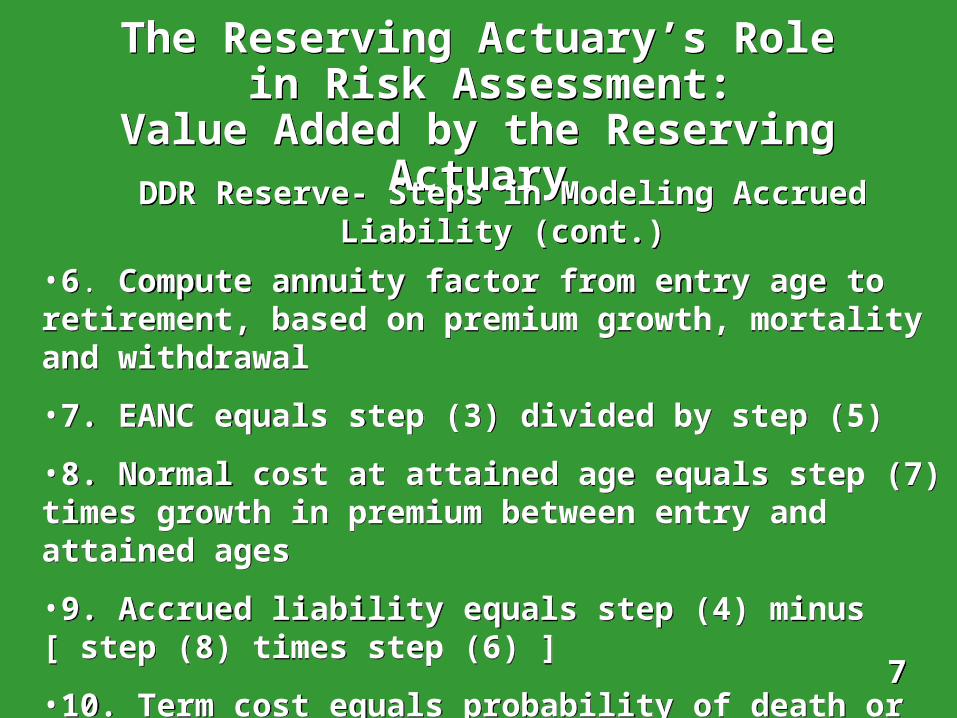

DDR Reserve- Steps in Modeling Accrued Liability (cont.)DDR Reserve- Steps in Modeling Accrued Liability (cont.)

•6. Compute annuity factor from entry age to retirement, based on premium growth, mortality and withdrawal

•7. EANC equals step (3) divided by step (5)

•8. Normal cost at attained age equals step (7) times growth in premium between entry and attained ages

•9. Accrued liability equals step (4) minus [ step (8) times step (6) ]

•10. Term cost equals probability of death or disability times step (1)

•6. Compute annuity factor from entry age to retirement, based on premium growth, mortality and withdrawal

•7. EANC equals step (3) divided by step (5)

•8. Normal cost at attained age equals step (7) times growth in premium between entry and attained ages

•9. Accrued liability equals step (4) minus [ step (8) times step (6) ]

•10. Term cost equals probability of death or disability times step (1)

77

The Reserving Actuary’s Role in Risk Assessment:

Value Added by the Reserving Actuary

The Reserving Actuary’s Role in Risk Assessment:

Value Added by the Reserving Actuary

DDR Reserve-Entry Age Normal Funding

•EANC- Level percent of future malpractice premiums (from physician’s original date of insurance) equal to present value of projected retirement benefits

•Accrued Liability-Present value of future projected retirement benefits less present value of future normal costs

•Term Cost- Cost of providing benefit to the insureds who die or become disabled during the current year

DDR Reserve-Entry Age Normal Funding

•EANC- Level percent of future malpractice premiums (from physician’s original date of insurance) equal to present value of projected retirement benefits

•Accrued Liability-Present value of future projected retirement benefits less present value of future normal costs

•Term Cost- Cost of providing benefit to the insureds who die or become disabled during the current year

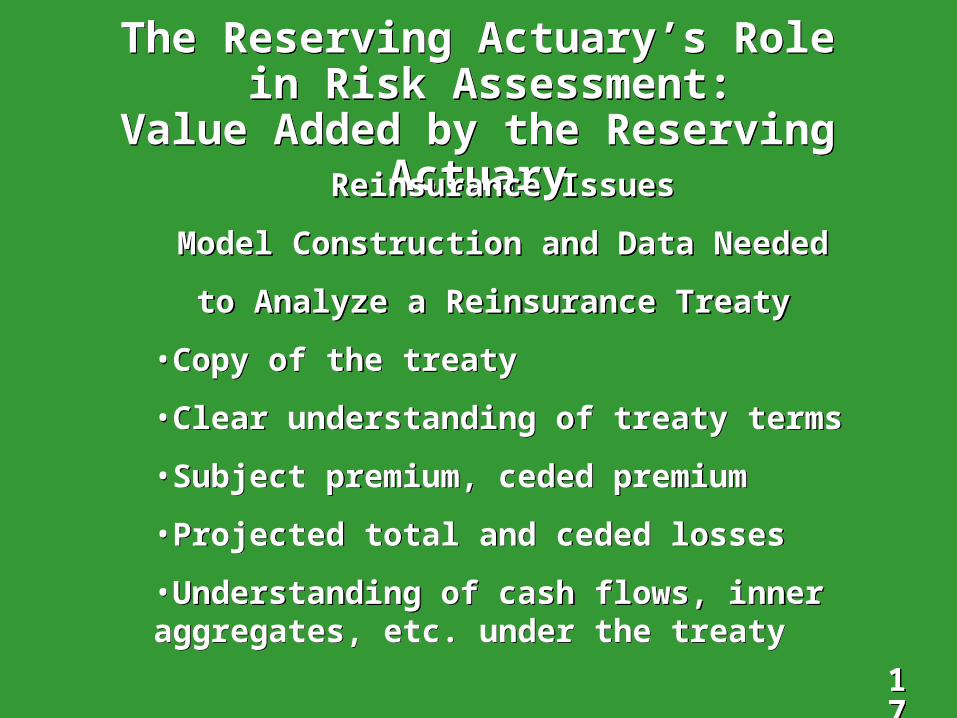

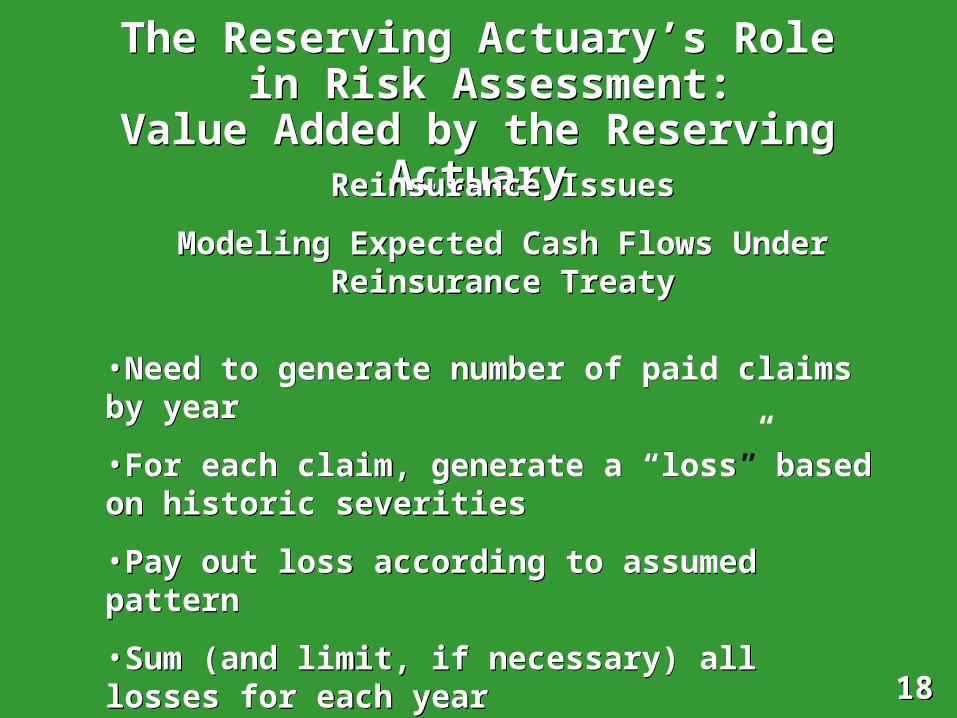

Value Added by the Reserving ActuaryReinsurance Issues

Net Cost of Reinsurance

•Difference between ceded premium and ultimate ceded loss (and LAE, if applicable) on a present value basis, divided by premiums ceded

•Ceded losses may be estimated directly or as difference of gross and net

•Actuary can show management if ceding certain losses is profitable or is accomplished at relatively low cost. If not, management may want to commute the treaty.

Reinsurance Issues

Net Cost of Reinsurance

•Difference between ceded premium and ultimate ceded loss (and LAE, if applicable) on a present value basis, divided by premiums ceded

•Ceded losses may be estimated directly or as difference of gross and net

•Actuary can show management if ceding certain losses is profitable or is accomplished at relatively low cost. If not, management may want to commute the treaty.

2121

The Reserving Actuary’s Role in Risk Assessment:

Value Added by the Reserving Actuary

Reinsurance Issues

The Reserving Actuary’s Role in Risk Assessment:

Value Added by the Reserving Actuary

Reinsurance Issues

Treaty

Prob. of

Reins Loss

Loss to Reinsurer

Proj. Net Cost

of Reins.

A 10% 5% 3.0%

B 10% 15% 3.0%

C 10% 20% 4.5%

D 10% 25% 7.0%

2222

The Reserving Actuary’s Role in Risk Assessment:

Value Added by the Reserving Actuary

The Reserving Actuary’s Role in Risk Assessment:

Value Added by the Reserving Actuary

Reinsurance Issues-Recoverability

•Determine Best’s rating of company’s reinsurers

•Discuss collectibility problems with management

•May need to perform additional investigation if any reinsurers are in financial difficulty and may not be able to meet obligations

Reinsurance Issues-Recoverability

•Determine Best’s rating of company’s reinsurers

•Discuss collectibility problems with management

•May need to perform additional investigation if any reinsurers are in financial difficulty and may not be able to meet obligations