56

ihs.com © 2015 IHS US Economic Outlook IHS The US Economic Outlook 17 December 2015 Patrick Newport, Director of Long Term Forecasting +1 781 301 9125, [email protected] ECONOMICS

ihs.com

© 2015 IHS

US Economic Outlook

IHS

The US Economic Outlook 17 December 2015

Patrick Newport, Director of Long Term Forecasting

+1 781 301 9125, [email protected]

ECONOMICS

© 2015 IHS

The US economy on a moderate growth path

• Real GDP growth will pick up from 2.5% in 2015 to 2.7% in 2016.

• Consumer spending is supported by solid gains in employment, real

disposable income, and housing asset values.

• Housing construction will steadily recover in response to rising

employment, easing credit, and a higher household formation rate.

• Business investment in equipment, software, and commercial

structures will post robust growth.

• A two-year federal budget agreement and suspension of the debt

ceiling boosts near-term spending and reduces policy uncertainty.

• Interest rates will gradually increase from late 2015 through 2018 as

monetary accommodation is withdrawn.

2

US Economic Outlook / December 2015

© 2015 IHS

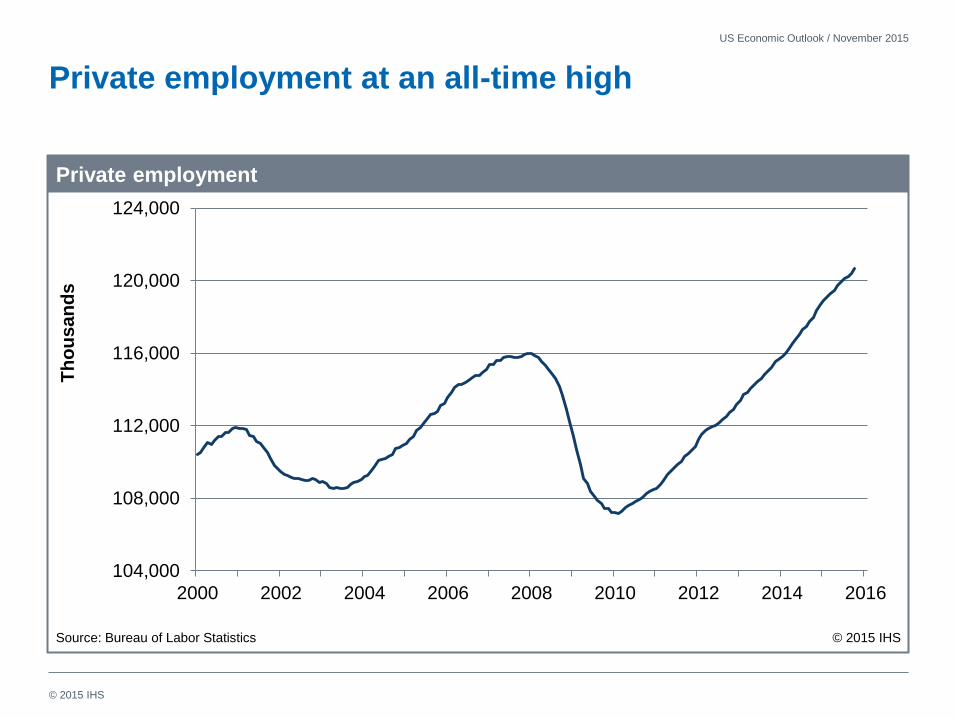

Private employment at an all-time high

US Economic Outlook / November 2015

104,000

108,000

112,000

116,000

120,000

124,000

2000 2002 2004 2006 2008 2010 2012 2014 2016

Private employment

Source: Bureau of Labor Statistics © 2015 IHS

Th

ou

sa

nd

s

© 2015 IHS

Jobs!

Indiana Presentation / December 2015

-8

-6

-4

-2

0

2

4

2000 2002 2004 2006 2008 2010 2012 2014

United States Indiana

Payroll employment growth

Source: Bureau of Labor Statistics © 2015 IHS

Y/y

pe

rce

nt

ch

an

ge

© 2015 IHS

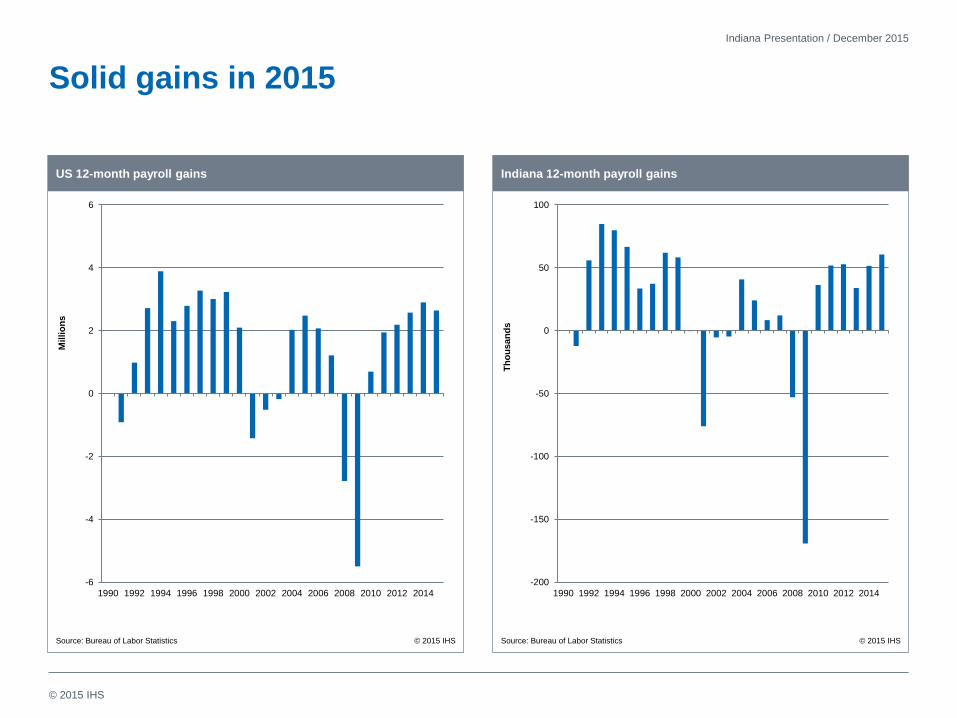

Solid gains in 2015

Indiana Presentation / December 2015

-6

-4

-2

0

2

4

6

1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014

US 12-month payroll gains

Source: Bureau of Labor Statistics © 2015 IHS

Millio

ns

-200

-150

-100

-50

0

50

100

1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014

Indiana 12-month payroll gains

Source: Bureau of Labor Statistics © 2015 IHS

Th

ou

san

ds

© 2015 IHS

Close to full employment!!!

Indiana Presentation / December 2015

2

3

4

5

6

7

8

9

10

11

2000 2002 2004 2006 2008 2010 2012 2014

United States Indiana

Unemployment rate

Source: Bureau of Labor Statistics © 2015 IHS

Pe

rce

nt

© 2015 IHS

Participation rate: at 1978 levels

US Economic Outlook / November 2015

62

63

64

65

66

67

68

2000 2002 2004 2006 2008 2010 2012 2014 2016

Labor force paticipation rate

Source: Bureau of Labor Statistics © 2015 IHS

Pe

rce

nt

© 2015 IHS

Little Wage inflation

US Economic Outlook / November 2015

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

2000 2002 2004 2006 2008 2010 2012 2014 2016

Employment cost index, wages and salaries

Source: Bureau of Labor Statistics © 2015 IHS

Year-

ove

r-ye

ar

pe

rce

nt

ch

an

ge

© 2015 IHS

Stagnant productivity growth

US Economic Outlook / November 2015

-1

0

1

2

3

4

5

6

2000 2002 2004 2006 2008 2010 2012 2014 2016

Nonfarm business output per hour

Source: Bureau of Labor Statistics © 2015 IHS

Year-

ove

r-ye

ar

pe

rce

nt

ch

an

ge

© 2015 IHS

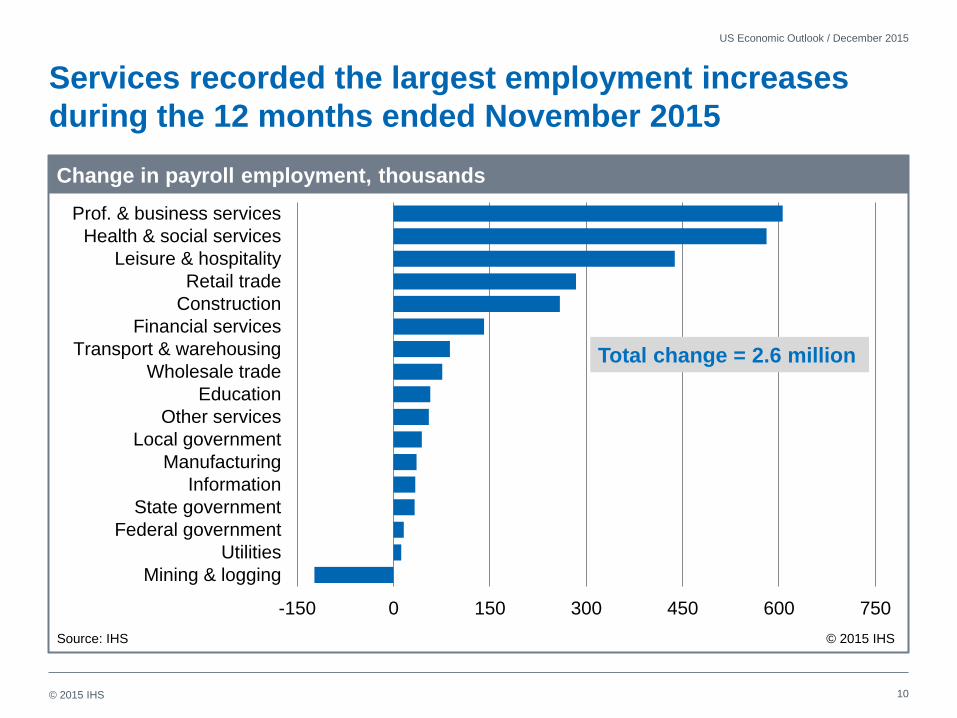

-150 0 150 300 450 600 750

Mining & logging

Utilities

Federal government

State government

Information

Manufacturing

Local government

Other services

Education

Wholesale trade

Transport & warehousing

Financial services

Construction

Retail trade

Leisure & hospitality

Health & social services

Prof. & business services

10

Services recorded the largest employment increases

during the 12 months ended November 2015

US Economic Outlook / December 2015

Change in payroll employment, thousands

Total change = 2.6 million

Source: IHS © 2015 IHS

© 2015 IHS 11

The dollar’s real exchange value is appreciating,

reaching a 12-year high against major currencies

US Economic Outlook / November 2015

Real trade-weighted dollar index

0.6

0.8

1.0

1.2

1.4

1.6

1980 1984 1988 1992 1996 2000 2004 2008 2012 2016 2020

Ind

ex,

2009 =

1.0

Major trading partners Other important trading partners

Source: IHS © 2015 IHS

© 2015 IHS 12

The Institute for Supply Management’s indexes signal a

stall in manufacturing and moderate growth in services

US Economic Outlook / December 2015

30

35

40

45

50

55

60

65

2000 2002 2004 2006 2008 2010 2012 2014

Ove

r 5

0 i

nd

ica

tes

ex

pa

ns

ion

Manufacturing index Nonmanufacturing index

ISM indexes

Source: Institute for Supply Management (ISM) © 2015 IHS

© 2015 IHS 13

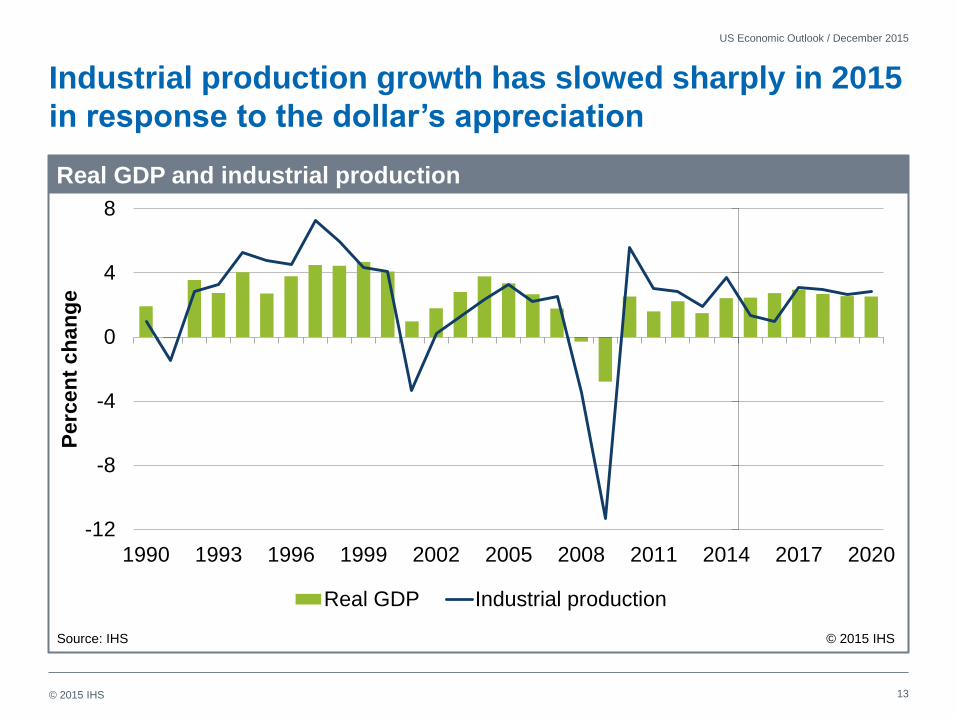

Industrial production growth has slowed sharply in 2015

in response to the dollar’s appreciation

US Economic Outlook / December 2015

Real GDP and industrial production

-12

-8

-4

0

4

8

1990 1993 1996 1999 2002 2005 2008 2011 2014 2017 2020

Perc

en

t ch

an

ge

Real GDP Industrial production

Source: IHS © 2015 IHS

© 2015 IHS 14

Sources of growth in US real GDP

US Webcast / November 2015

-1

0

1

2

3

4

2012 2013 2014 2015 2016 2017 2018

Real GDP Consumer spending Nonresidential investmentResidential investment Inventories ExportsImports Government Domestic demand

Perc

en

tag

e p

oin

ts

Contribution to real GDP growth

Source: IHS © 2015 IHS

© 2015 IHS 15

US economic growth by sector

US Economic Outlook / December 2015

Real GDP and its components

Percent change 2014 2015 2016 2017

Real GDP 2.4 2.5 2.7 3.0

Consumption 2.7 3.1 3.1 3.2

Residential investment 1.8 8.4 9.0 10.3

Business fixed investment 6.2 3.3 5.3 5.1

Federal government -2.4 -0.4 3.6 -0.8

State & local government 0.6 1.5 1.4 1.2

Exports 3.4 1.0 2.5 5.4

Imports 3.8 4.8 4.8 7.5

© 2015 IHS 16

The US economy is near full employment: Real GDP

growth and the unemployment rate

US Economic Outlook / November 2015

Real GDP and unemployment

4

5

6

7

8

9

10

-10.0

-7.5

-5.0

-2.5

0.0

2.5

5.0

2007 2009 2011 2013 2015 2017

Perc

en

t o

f la

bo

r fo

rce

An

nu

al

perc

en

t ch

an

ge

Real GDP growth (Left scale) Unemployment rate (Right scale)

Source: IHS © 2015 IHS

© 2015 IHS 17

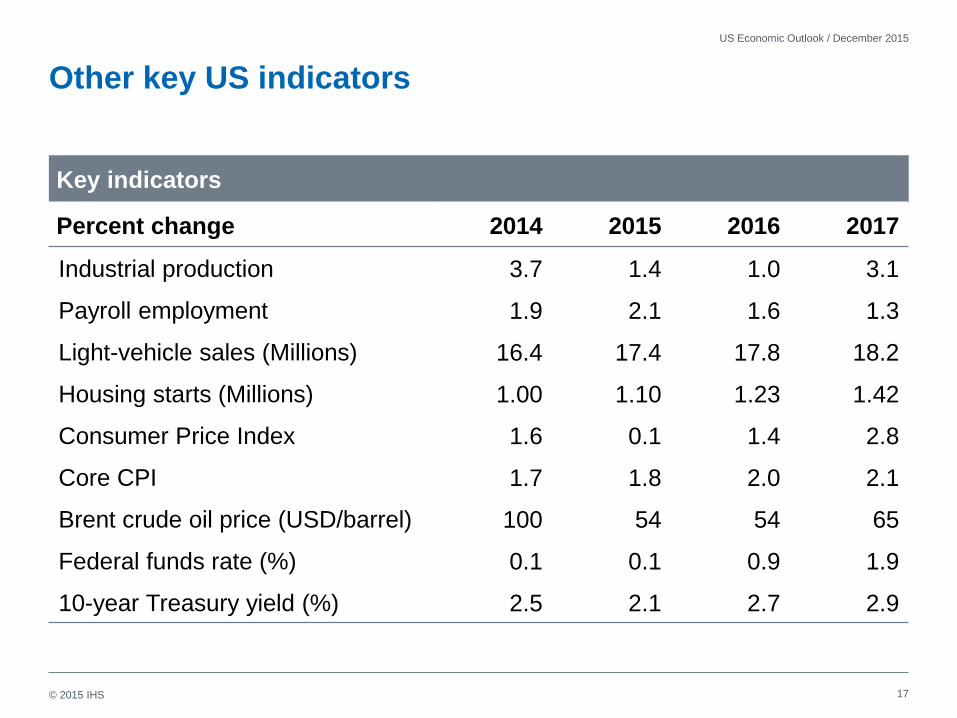

Other key US indicators

US Economic Outlook / December 2015

Key indicators

Percent change 2014 2015 2016 2017

Industrial production 3.7 1.4 1.0 3.1

Payroll employment 1.9 2.1 1.6 1.3

Light-vehicle sales (Millions) 16.4 17.4 17.8 18.2

Housing starts (Millions) 1.00 1.10 1.23 1.42

Consumer Price Index 1.6 0.1 1.4 2.8

Core CPI 1.7 1.8 2.0 2.1

Brent crude oil price (USD/barrel) 100 54 54 65

Federal funds rate (%) 0.1 0.1 0.9 1.9

10-year Treasury yield (%) 2.5 2.1 2.7 2.9

© 2015 IHS 18

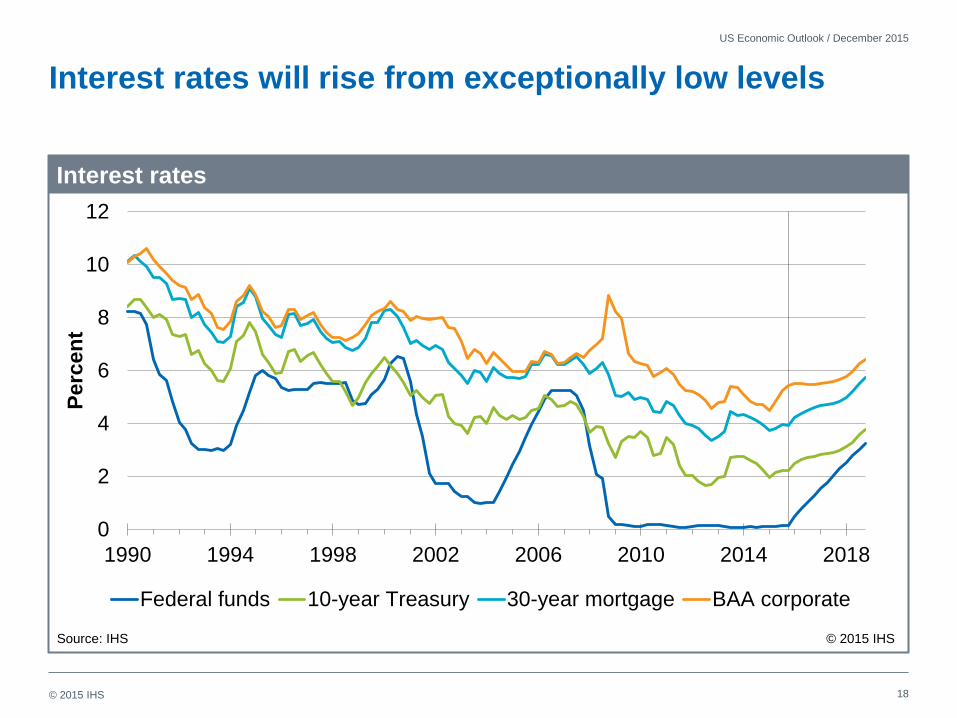

Interest rates will rise from exceptionally low levels

US Economic Outlook / December 2015

Interest rates

0

2

4

6

8

10

12

1990 1994 1998 2002 2006 2010 2014 2018

Pe

rce

nt

Federal funds 10-year Treasury 30-year mortgage BAA corporate

Source: IHS © 2015 IHS

© 2015 IHS 19

Job growth will slow as the US economy approaches full

employment

US Economic Outlook / November 2015

Payroll employment

-8

-6

-4

-2

0

2

4

2000 2002 2004 2006 2008 2010 2012 2014 2016 2018

Perc

en

t ch

an

ge,

an

nu

al

rate

Source: IHS © 2015 IHS

© 2015 IHS 20

After an inventory correction in late 2015 and early 2016,

manufacturing production growth will rebound

US Economic Outlook / December 2015

Industrial production and real GDP

-4

-2

0

2

4

6

8

2011 2012 2013 2014 2015 2016 2017 2018

Year-

over-

year

perc

en

t ch

an

ge

All manufacturing Excluding information technologies Real GDP

Source: IHS © 2015 IHS

© 2015 IHS 21

US industrial production growth

US Economic Outlook / November 2015

Industrial production

Percent change 2014 2015 2016 2017

All manufacturing 2.8 2.1 2.2 3.2

Motor vehicles & parts 10.4 9.2 6.5 3.6

Computers & electronics 2.9 1.4 3.8 6.6

Electrical equip. & appliances 2.1 3.6 2.5 3.3

Machinery 4.7 -0.3 -1.7 4.7

Textiles 3.4 -0.6 0.0 -1.3

Furniture 6.5 3.6 2.1 3.7

Chemicals 1.8 3.4 2.1 4.2

© 2015 IHS 22

Consumer price inflation will pick up as commodity

prices recover

US Economic Outlook / December 2015

Inflation rates

-2

-1

0

1

2

3

4

5

6

2000 2002 2004 2006 2008 2010 2012 2014 2016 2018 2020

Year-

over-

year

perc

en

t ch

an

ge

All-urban CPI Core CPI (excluding food and energy)

Source: IHS © 2015 IHS

© 2015 IHS 23

Worker compensation will accelerate as labor markets

tighten and the Affordable Care Act is implemented

US Economic Outlook / December 2015

Labor compensation

0

1

2

3

4

5

6

7

8

2000 2002 2004 2006 2008 2010 2012 2014 2016 2018 2020

Year-

over-

year

perc

en

t ch

an

ge

Total compensation Wages & salaries Benefits

Source: IHS © 2015 IHS

© 2015 IHS 24

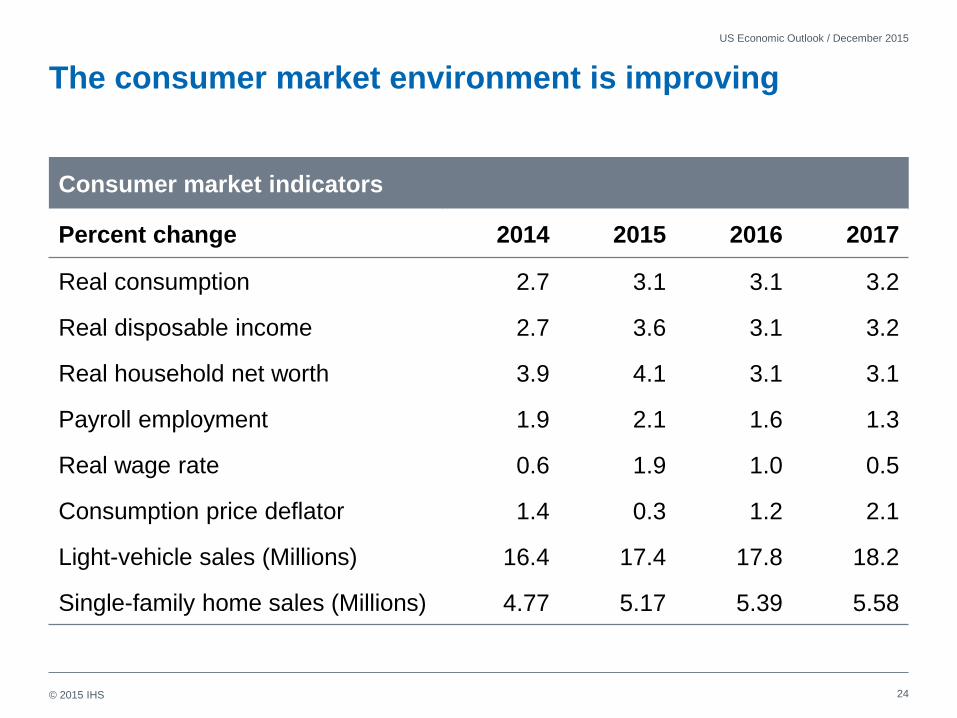

The consumer market environment is improving

US Economic Outlook / December 2015

Consumer market indicators

Percent change 2014 2015 2016 2017

Real consumption 2.7 3.1 3.1 3.2

Real disposable income 2.7 3.6 3.1 3.2

Real household net worth 3.9 4.1 3.1 3.1

Payroll employment 1.9 2.1 1.6 1.3

Real wage rate 0.6 1.9 1.0 0.5

Consumption price deflator 1.4 0.3 1.2 2.1

Light-vehicle sales (Millions) 16.4 17.4 17.8 18.2

Single-family home sales (Millions) 4.77 5.17 5.39 5.58

© 2015 IHS 25

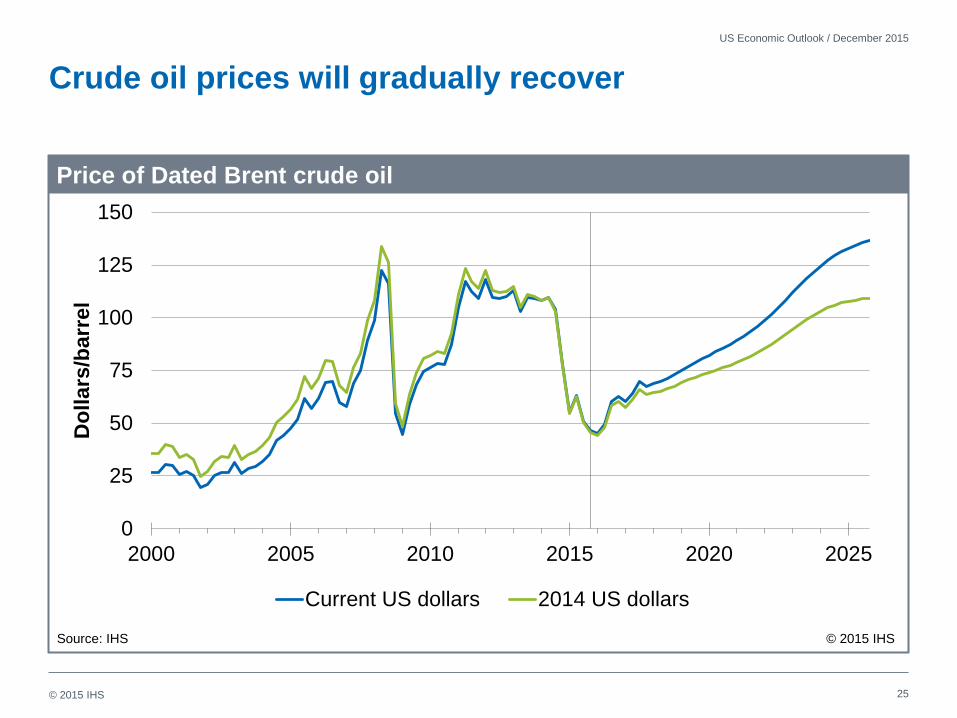

Crude oil prices will gradually recover

US Economic Outlook / December 2015

0

25

50

75

100

125

150

2000 2005 2010 2015 2020 2025

Do

llars

/barr

el

Current US dollars 2014 US dollars

Price of Dated Brent crude oil

Source: IHS © 2015 IHS

© 2015 IHS 26

Consumer spending growth depends on disposable

income growth, which has strengthened in 2015

US Economic Outlook / November 2015

Real consumer spending and disposable income

-2

0

2

4

6

2000 2002 2004 2006 2008 2010 2012 2014 2016 2018

Perc

en

t ch

an

ge

Real consumer spending Real disposable income

Tax increases under-

mined growth in 2013

Source: IHS © 2015 IHS

© 2015 IHS 27

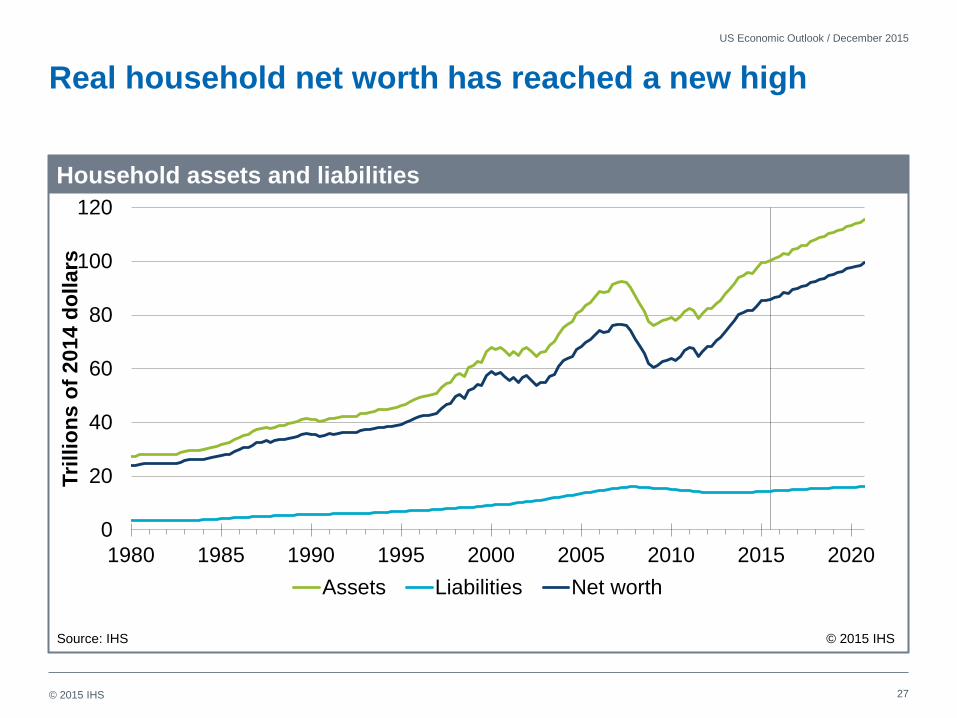

Real household net worth has reached a new high

US Economic Outlook / December 2015

Household assets and liabilities

0

20

40

60

80

100

120

1980 1985 1990 1995 2000 2005 2010 2015 2020

Tri

llio

ns

of

20

14

do

llars

Assets Liabilities Net worth

Source: IHS © 2015 IHS

© 2015 IHS 28

Light-vehicle sales will peak in 2017; low gasoline prices

boost demand for light trucks

US Economic Outlook / December 2015

Light-vehicle sales

0

4

8

12

16

20

1980 1985 1990 1995 2000 2005 2010 2015 2020

Millio

ns o

f u

nit

s,

an

nu

al

rate

s

Total Cars Light trucks

Source: IHS © 2015 IHS

© 2015 IHS

The recovery in housing markets is gaining momentum

• Sustained job growth will support increases in housing demand.

• Credit availability is improving for home buyers and builders.

• Supplies of new and existing homes are tight, driving up prices.

• Multifamily units will account for about one-third of housing starts.

• Young adults have postponed homeownership, resulting in pent-up

demand.

• Sales to first-time buyers are rising rapidly.

• Baby boomers are starting to downsize.

29

US Economic Outlook / December 2015

© 2015 IHS 30

A recovery in household formation will support further

gains in housing starts

US Economic Outlook / December 2015

Housing starts and formation

0.0

0.3

0.6

0.9

1.2

1.5

1.8

2.1

1980 1985 1990 1995 2000 2005 2010 2015 2020 2025

Mil

lio

ns

Housing starts Household formation

Source: IHS © 2015 IHS

© 2015 IHS 31

Single-family home sales and construction are not

expected to regain 2005 peaks

US Economic Outlook / December 2015

Single-family housing starts and sales

1

2

3

4

5

6

7

8

0.25

0.50

0.75

1.00

1.25

1.50

1.75

2.00

1970 1975 1980 1985 1990 1995 2000 2005 2010 2015 2020

Millio

ns o

f u

nit

s

Millio

ns o

f u

nit

s

Housing starts (Left scale) Home sales (Right scale)

Source: IHS © 2015 IHS

© 2015 IHS

Nonresidential fixed investment has slowed

• Most companies are investing at steady rates

• However, companies exposed to foreign competition (manufacturing),

low oil and gas prices, and falling agricultural prices have cut capital

spending sharply

• Agricultural machinery is down 48% year-over-year, due to falling agricultural

prices

• Mining and oilfield machinery equipment is down 48% year-over-year—blame

low oil prices

• Railroad equipment is down 56% year-over-year

• Special industrial machinery is down 20% year-over-year, thanks to the

strong dollar

• Mine and well structures are down 44% year-over-year

US Webcast / November 2015

32

© 2015 IHS

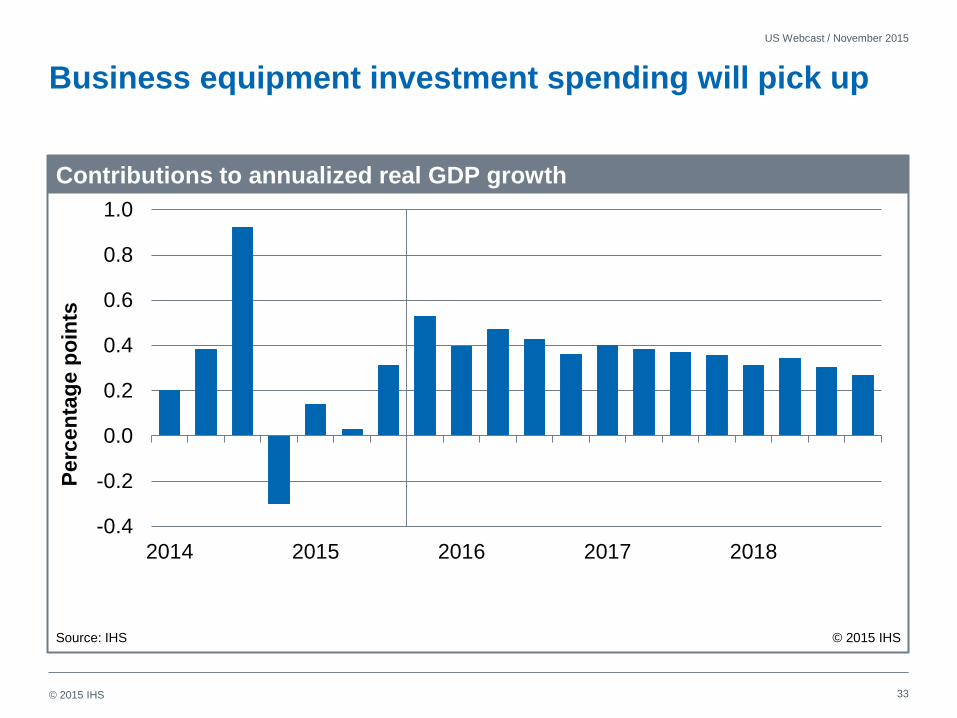

Business equipment investment spending will pick up

-0.4

-0.2

0.0

0.2

0.4

0.6

0.8

1.0

2014 2015 2016 2017 2018

Contributions to annualized real GDP growth

Source: IHS © 2015 IHS

Perc

en

tag

e p

oin

ts

US Webcast / November 2015

33

© 2015 IHS

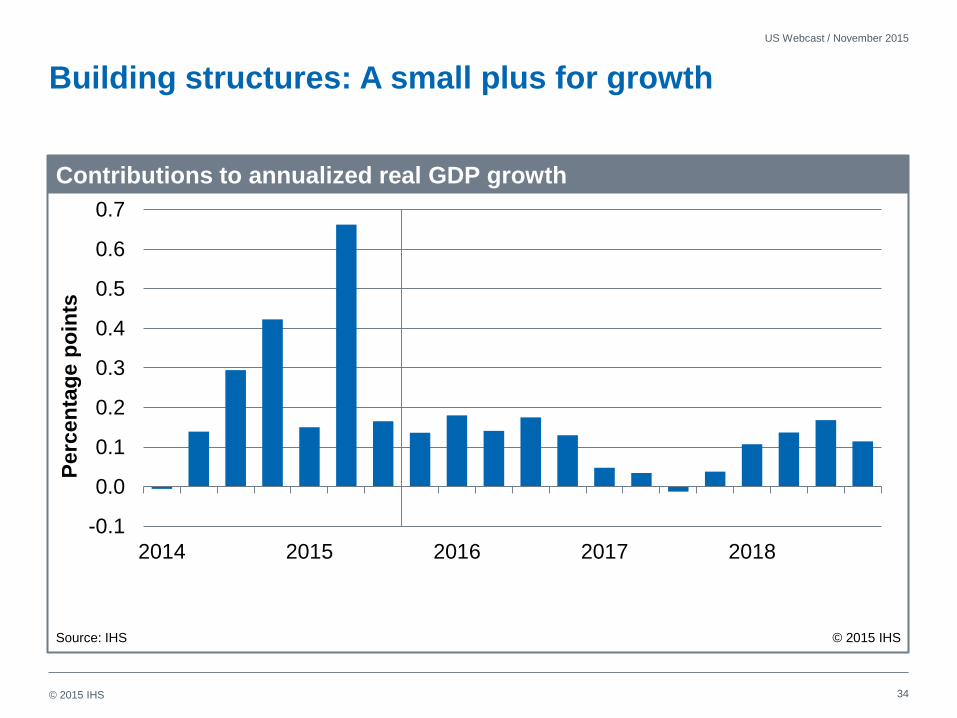

Building structures: A small plus for growth

-0.1

0.0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

2014 2015 2016 2017 2018

Contributions to annualized real GDP growth

Source: IHS © 2015 IHS

Perc

en

tag

e p

oin

ts

US Webcast / November 2015

34

© 2015 IHS

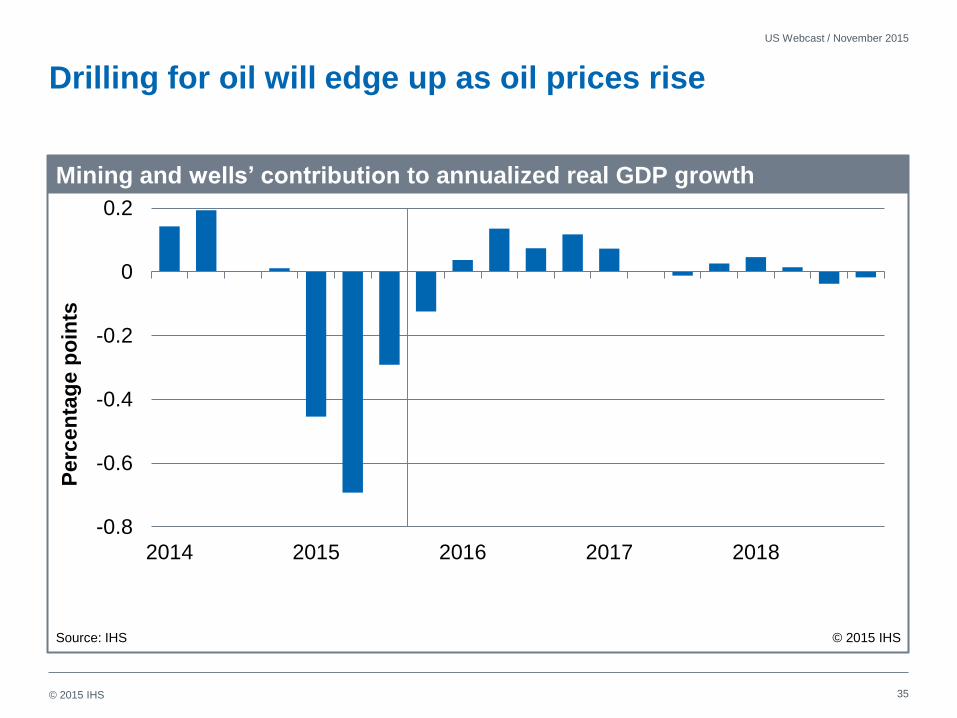

Drilling for oil will edge up as oil prices rise

-0.8

-0.6

-0.4

-0.2

0

0.2

2014 2015 2016 2017 2018

Mining and wells’ contribution to annualized real GDP growth

Source: IHS © 2015 IHS

Perc

en

tag

e p

oin

ts

US Webcast / November 2015

35

© 2015 IHS 36

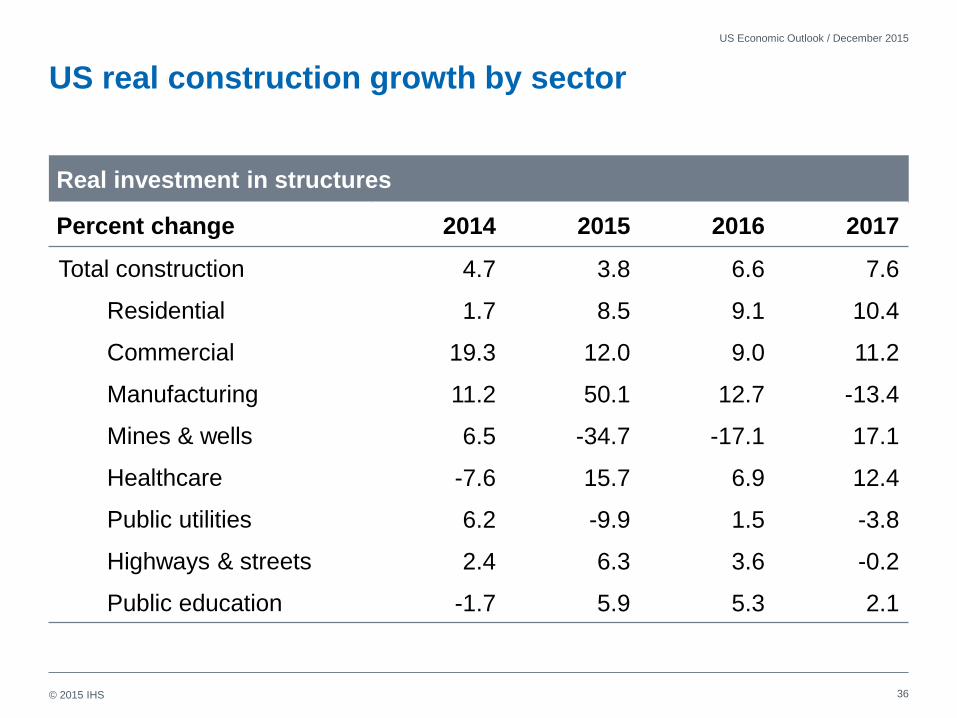

US real construction growth by sector

US Economic Outlook / December 2015

Real investment in structures

Percent change 2014 2015 2016 2017

Total construction 4.7 3.8 6.6 7.6

Residential 1.7 8.5 9.1 10.4

Commercial 19.3 12.0 9.0 11.2

Manufacturing 11.2 50.1 12.7 -13.4

Mines & wells 6.5 -34.7 -17.1 17.1

Healthcare -7.6 15.7 6.9 12.4

Public utilities 6.2 -9.9 1.5 -3.8

Highways & streets 2.4 6.3 3.6 -0.2

Public education -1.7 5.9 5.3 2.1

© 2015 IHS

The Bipartisan Budget Act of 2015 brings some clarity to

federal fiscal policy

• The federal debt ceiling is suspended through March 2017.

• The federal government is funded through September 2017.

• Budget authority is increased by $50 billion in fiscal 2016 and $30 billion in

fiscal 2017 from previous budget caps.

• These increments are divided equally between defense and nondefense

discretionary spending.

• An omnibus appropriations bill must still be enacted by 11 December.

• Consistent with Congressional Budget Office estimates, we assume that

outlays are increased by $30 billion in both 2016 and 2017, and the

remainder is spread through 2021.

• The agreement is expected to raise the level of real GDP by 0.2% in

2016 and 0.1% in 2017.

37

US Economic Outlook / November 2015

© 2015 IHS 38

The US federal budget will remain in deficit

US Economic Outlook / November 2015

US federal budget balance

-12

-9

-6

-3

0

3

-2,000

-1,500

-1,000

-500

0

500

1980 1985 1990 1995 2000 2005 2010 2015 2020 2025

Billio

ns o

f U

SD

, fi

scal

years

Unified budget balance (Left scale) Balance as percent of GDP (Right scale)

Source: IHS © 2015 IHS

© 2015 IHS 39

The gap between federal expenditures and revenues will

stay in the 2–3% range of GDP

US Economic Outlook / November 2015

Federal revenues and expenditures*

14

16

18

20

22

24

26

1970 1975 1980 1985 1990 1995 2000 2005 2010 2015 2020 2025

Perc

en

t o

f G

DP

Federal revenues Federal expenditures

* Fiscal years, unified budget

Source: IHS © 2015 IHS

© 2015 IHS

A gradual acceleration in the global economy

• The world economy remains in low gear; only a modest pickup in

growth is expected in 2016.

• Eurozone growth will improve slightly, aided by monetary stimulus,

currency depreciation, and pent-up demand.

• China’s economic growth will slow further in 2016 because of

imbalances in credit, housing, and industrial markets.

• The plunge in materials prices is restraining growth in the commodity-

exporting countries of the Americas, Africa, and Asia-Pacific.

• Prospects for emerging markets depend on structural reforms that raise

productivity and allocate capital more efficiently.

40

US Economic Outlook / December 2015

© 2015 IHS

-1

0

1

2

3

4

5

6

NAFTA OtherAmericas

WesternEurope

EmergingEurope

Mideast-N. Africa

Sub-Saharan

Africa

Japan OtherAsia-

Pacific

An

nu

al

perc

en

t ch

an

ge

2014 2015 2016 2017 2018-22

41

Asia-Pacific (excluding Japan) will achieve the fastest

growth in real GDP

US Economic Outlook / December 2015

Real GDP

Source: IHS © 2015 IHS

© 2015 IHS 42

The US current account will remain in deficit

US Economic Outlook / December 2015

Current-account balance

-7.5

-6.0

-4.5

-3.0

-1.5

0.0

1.5

-1,250

-1,000

-750

-500

-250

0

250

1980 1985 1990 1995 2000 2005 2010 2015 2020 2025

Current-account balance (Left scale, billion US dollars)

Balance as percent of GDP (Right scale)

Source: IHS © 2015 IHS

© 2015 IHS

Bottom line for the US economy

• Consumer spending will be supported by gains in employment, real

disposable income, and household net worth.

• Homebuilding will rise as credit availability improves and demand from

young adults strengthens.

• Foreign trade will be a drag on US economic growth through 2018, due

to a strong dollar and sluggish growth in major export markets.

• Real business fixed investment will post solid gains, led by information

technology equipment and commercial structures.

• The Federal Reserve will likely begin to raise the federal funds rate in

December; it will reach an equilibrium at 3.25% in late 2018.

• Core inflation will edge upward to the central bank’s 2% target.

• Forecast risks are weighted to the downside.

43

US Economic Outlook / December 2015

© 2015 IHS

Regional and Indiana Economic Outlook

44 Indiana Economic Outlook / December 2015

© 2015 IHS

U.S. Regional Outlook

• States in the West and Sunbelt will continue to growth fastest.

• These states saw the worst housing busts.

• Population growth fastest in these regions.

• People go where the jobs are, but jobs also go where the people are.

• Weaker service-sector growth in states with low population growth.

• Manufacturing gains, especially from the auto sector supply chain, have

been a key to the improving Midwestern economy.

• Drop in oil prices, combined with weakness in natural gas and coal, has

slammed the brakes on natural resource and mining sector.

• Demand for steel pipe, machinery, transportation, construction cut.

45

Indiana Economic Outlook / December 2015

© 2015 IHS 46

Indiana Economic Outlook / December 2015

2015 jobs growth concentrated in West, Southeast Resource-heavy states in a struggle; Indiana ranks 13th

Percent

-1.1 to 0.9

1.0 to 1.5

1.6 to 2.2

2.3 to 3.9

© 2015 IHS 47

Indiana Economic Outlook / December 2015

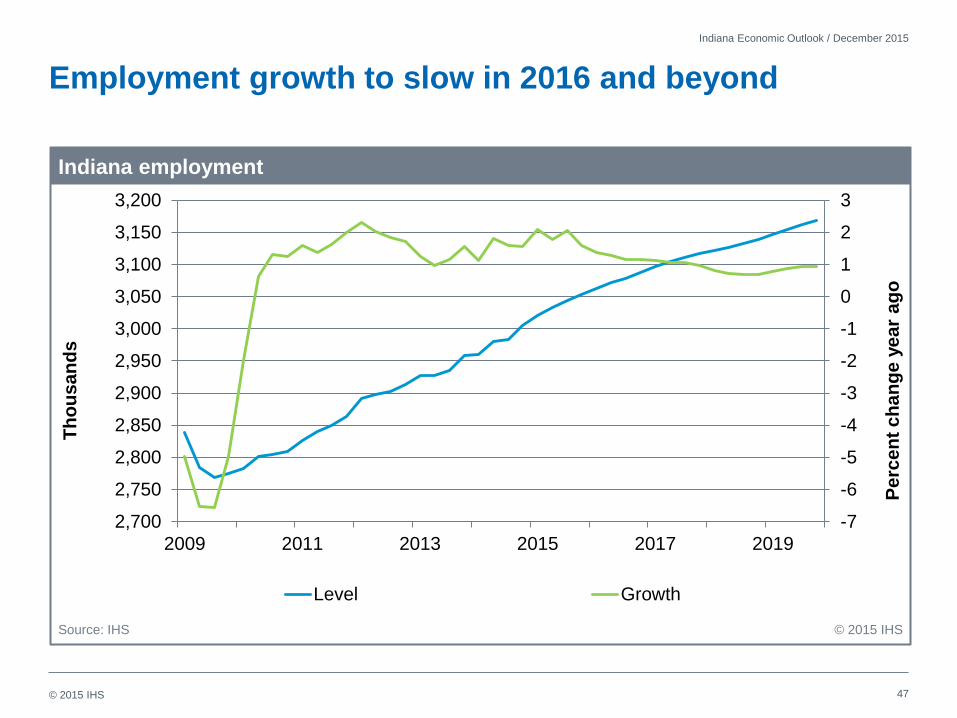

Employment growth to slow in 2016 and beyond

-7

-6

-5

-4

-3

-2

-1

0

1

2

3

2,700

2,750

2,800

2,850

2,900

2,950

3,000

3,050

3,100

3,150

3,200

2009 2011 2013 2015 2017 2019

Level Growth

Indiana employment

Source: IHS © 2015 IHS

Th

ou

sa

nd

s

Pe

rce

nt

ch

an

ge

ye

ar

ag

o

© 2015 IHS 48

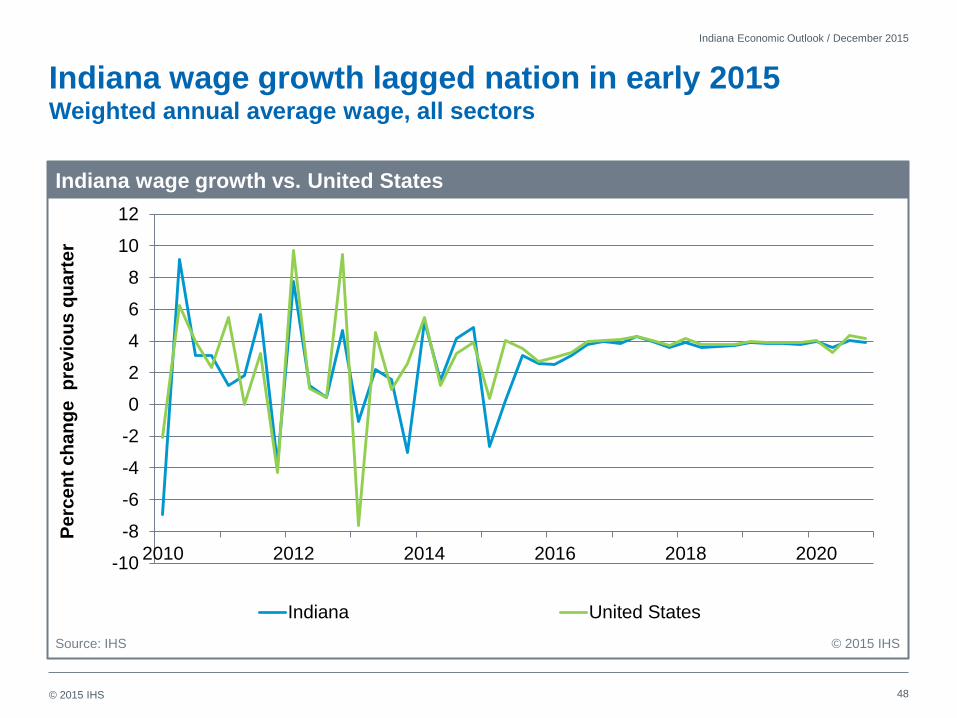

Indiana Economic Outlook / December 2015

Indiana wage growth lagged nation in early 2015 Weighted annual average wage, all sectors

-10

-8

-6

-4

-2

0

2

4

6

8

10

12

2010 2012 2014 2016 2018 2020

Indiana United States

Indiana wage growth vs. United States

Source: IHS © 2015 IHS

Pe

rce

nt

ch

an

ge

p

revio

us

qu

art

er

© 2015 IHS 49

Indiana Economic Outlook / December 2015

Indiana housing starts will increase in 2016 and beyond Auto sales growth to slow as recovery matures

0

5

10

15

20

25

30

0

50

100

150

200

250

300

2010 2012 2014 2016 2018 2020

New car registrations, left axis Total housing starts, right axis

Indiana total housing starts and new car registrations

Source: IHS © 2015 IHS

Th

ou

sa

nd

Th

ou

sa

nd

Pre-recession peak was

40,000 starts in 2003.

© 2015 IHS

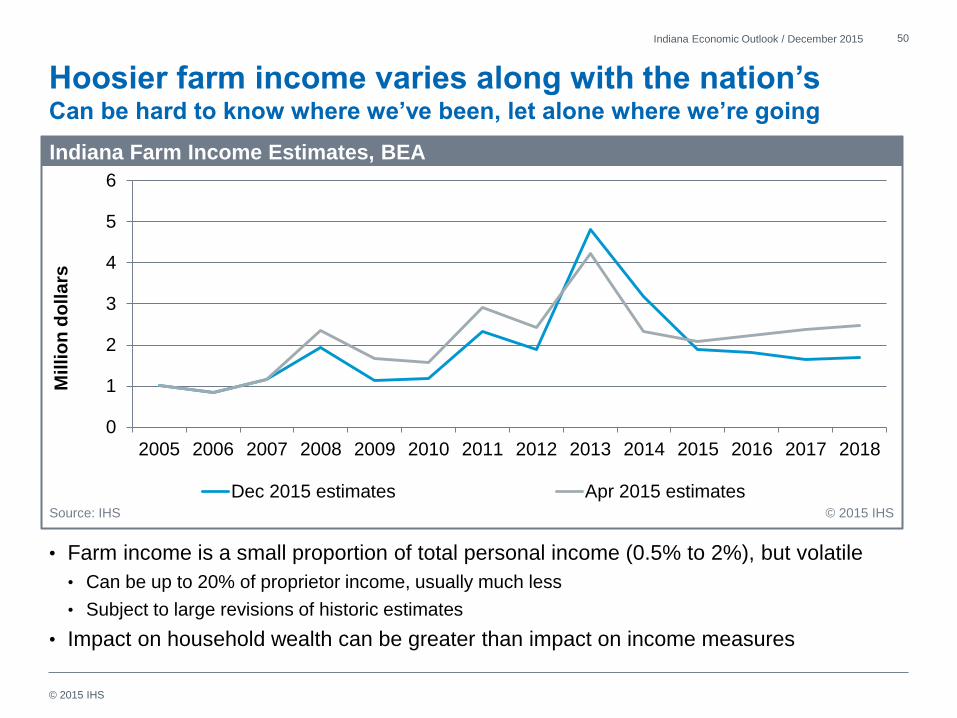

Hoosier farm income varies along with the nation’s Can be hard to know where we’ve been, let alone where we’re going

• Farm income is a small proportion of total personal income (0.5% to 2%), but volatile

• Can be up to 20% of proprietor income, usually much less

• Subject to large revisions of historic estimates

• Impact on household wealth can be greater than impact on income measures

50 Indiana Economic Outlook / December 2015

0

1

2

3

4

5

6

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

Dec 2015 estimates Apr 2015 estimates

Indiana Farm Income Estimates, BEA

Source: IHS © 2015 IHS

Millio

n d

oll

ars

© 2015 IHS 51

Indiana Economic Outlook / December 2015

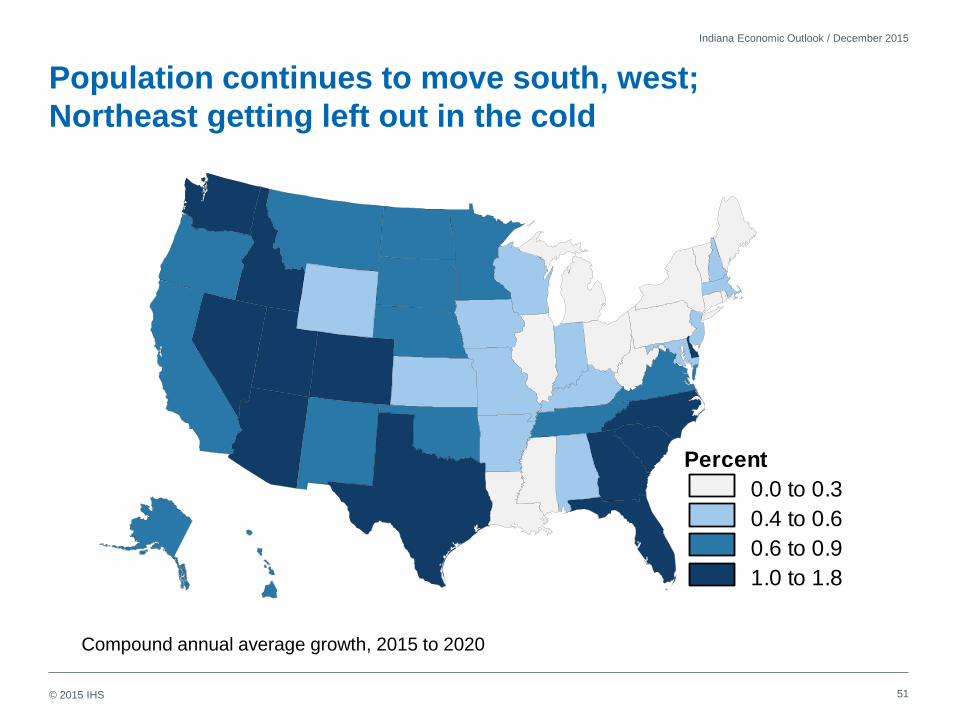

Population continues to move south, west;

Northeast getting left out in the cold

Compound annual average growth, 2015 to 2020

Percent

0.0 to 0.3

0.4 to 0.6

0.6 to 0.9

1.0 to 1.8

© 2015 IHS

Indiana Forecast Summary

52

Indiana Economic Outlook / December 2015

Key indicators

Percent change 2014 2015 2016 2017

Total employment 1.5 2.2 1.5 1.2

Unemployment rate (%) 5.9 5.0 4.5 4.5

Real personal Income 2.3 3.6 2.9 2.8

Real gross state product 0.4 1.5 2.5 2.8

Personal consumption

expenditures 3.1 2.9 4.1 5.4

Housing starts (Thousands) 17.5 15.9 19.8 23.8

Share of multi-family (%) 28.5 22.8 22.6 18.8

© 2015 IHS

IHS Forecast Track Record

• Income estimate for 2015 and beyond lowered slightly by lower expected wages

• Largely due to revisions in BLS data in early 2015

• Transportation, manufacturing, construction most affected

53 Indiana Economic Outlook / December 2015

U.S. GDP

Indiana

Employment

Indiana

Income

Percent change

Forecast

Date

2014

2015

2014

2015

2014

2015

Dec 2013 2.4 3.2 1.6 1.7 4.4 4.6

Dec 2014 2.2 2.7 1.8 1.7 2.1 4.0

Apr 2015 2.4 2.8 1.5 1.9 2.5 4.0

Dec 2015 2.4 2.5 1.5 2.2 3.8 3.8

© 2015 IHS

Bottom line for the Indiana economy

• Near-term economic growth will continue to be favorable.

• Manufacturing, especially related to the transportation sector, has

spurred Indiana’s economic recovery over the past five years.

• Manufacturing provides 17% of state’s payroll jobs, first in the nation.

• National average is 9%.

• Sales of cars and light trucks a huge factor; demand from oil and gas industry

for steel pipe, machinery, etc., has also helped.

• Domestic demand maturing, strong dollar reduces competitiveness.

• Expanding service employment is key to long-run economic growth.

• High-tech area is where value is being added.

• Requires ongoing investment in education, R&D, infrastructure.

• Long-term slow population growth a potential drag on economy.

54

Indiana Economic Outlook / December 2015

IHS Customer Care:

• Americas: +1 800 IHS CARE (+1 800 447 2273); [email protected]

• Europe, Middle East, and Africa: +44 (0) 1344 328 300; [email protected]

• Asia and the Pacific Rim: +604 291 3600; [email protected]

© 2014 IHS. No portion of this report may be reproduced, reused, or otherwise distributed in any form without prior written consent, with the exception of any internal client distribution as may be permitted in the license agreement between client and IHS.

Content reproduced or redistributed with IHS permission must display IHS legal notices and attributions of authorship. The information contained herein is from sources considered reliable but its accuracy and completeness are not warranted, nor are the

opinions and analyses which are based upon it, and to the extent permitted by law, IHS shall not be liable for any errors or omissions or any loss, damage or expense incurred by reliance on information or any statement contained herein. For more

information, please contact IHS at Customer Care (see phone numbers and email addresses above). All products, company names or other marks appearing in this publication are the trademarks and property of IHS or their respective owners.

Thank you!

IHSTM

COPYRIGHT NOTICE AND DISCLAIMER © 2015 IHS. For internal use of IHS clients only.

No portion of this report may be reproduced, reused, or otherwise distributed in any form without prior written consent, with the exception of any internal client distribution as may be permitted in the license agreement between client and IHS. Content

reproduced or redistributed with IHS permission must display IHS legal notices and attributions of authorship. The information contained herein is from sources considered reliable, but its accuracy and completeness are not warranted, nor are the

opinions and analyses that are based upon it, and to the extent permitted by law, IHS shall not be liable for any errors or omissions or any loss, damage, or expense incurred by reliance on information or any statement contained herein. In particular,

please note that no representation or warranty is given as to the achievement or reasonableness of, and no reliance should be placed on, any projections, forecasts, estimates, or assumptions, and, due to various risks and uncertainties, actual events

and results may differ materially from forecasts and statements of belief noted herein. This report is not to be construed as legal or financial advice, and use of or reliance on any information in this publication is entirely at client’s own risk. IHS and the

IHS logo are trademarks of IHS.

IHS Customer Care:

Americas: +1 800 IHS CARE (+1 800 447 2273); [email protected]

Europe, Middle East, and Africa: +44 (0) 1344 328 300; [email protected]

Asia and the Pacific Rim: +604 291 3600; [email protected]

ECONOMICS