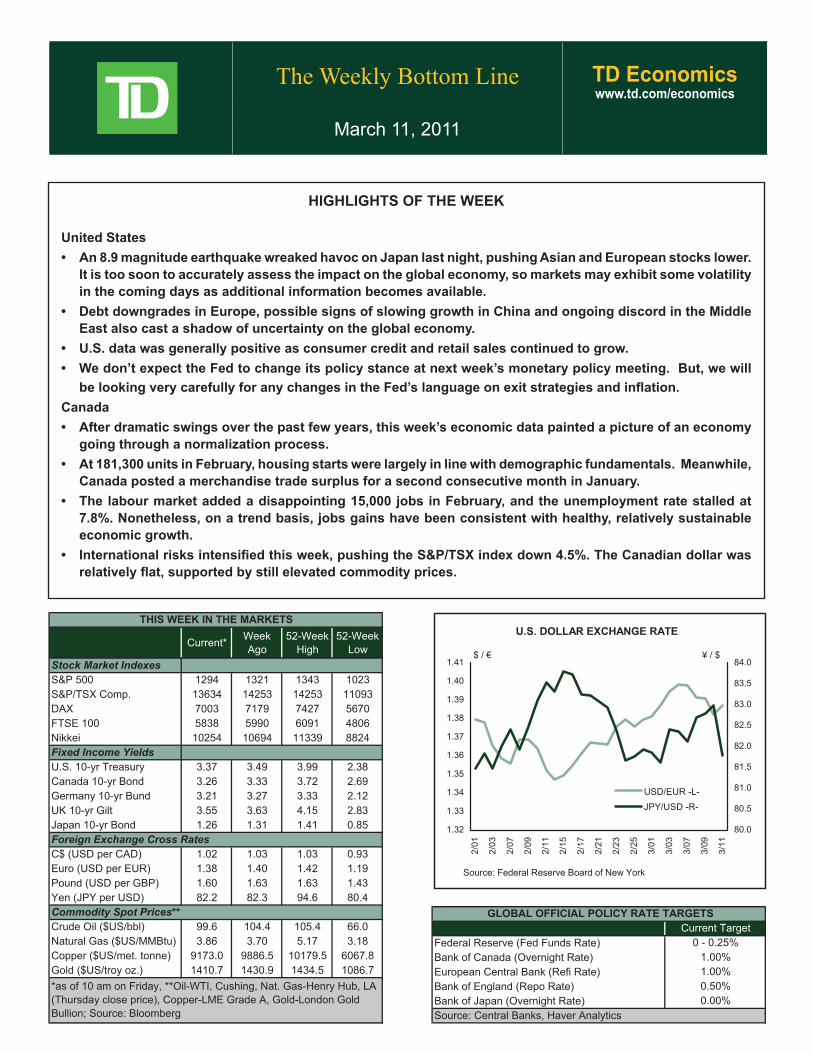

The Weekly Bottom Line TD Economics www.td.com/economics March 11, 2011 HIGHLIGHTS OF THE WEEK United States • An 8.9 magnitude earthquake wreaked havoc on Japan last night, pushing Asian and European stocks lower. It is too soon to accurately assess the impact on the global economy, so markets may exhibit some volatility in the coming days as additional information becomes available. • Debt downgrades in Europe, possible signs of slowing growth in China and ongoing discord in the Middle East also cast a shadow of uncertainty on the global economy. • U.S. data was generally positive as consumer credit and retail sales continued to grow. • We don’t expect the Fed to change its policy stance at next week’s monetary policy meeting. But, we will be looking very carefully for any changes in the Fed’s language on exit strategies and inflation. Canada • After dramatic swings over the past few years, this week’s economic data painted a picture of an economy going through a normalization process. • At 181,300 units in February, housing starts were largely in line with demographic fundamentals. Meanwhile, Canada posted a merchandise trade surplus for a second consecutive month in January. • The labour market added a disappointing 15,000 jobs in February, and the unemployment rate stalled at 7.8%. Nonetheless, on a trend basis, jobs gains have been consistent with healthy, relatively sustainable economic growth. • International risks intensified this week, pushing the S&P/TSX index down 4.5%. The Canadian dollar was relatively flat, supported by still elevated commodity prices. Current* Week Ago 52-Week High 52-Week Low Stock Market Indexes S&P 500 1294 1321 1343 1023 S&P/TSX Comp. 13634 14253 14253 11093 DAX 7003 7179 7427 5670 FTSE 100 5838 5990 6091 4806 Nikkei 10254 10694 11339 8824 Fixed Income Yields U.S. 10-yr Treasury 3.37 3.49 3.99 2.38 Canada 10-yr Bond 3.26 3.33 3.72 2.69 Germany 10-yr Bund 3.21 3.27 3.33 2.12 UK 10-yr Gilt 3.55 3.63 4.15 2.83 Japan 10-yr Bond 1.26 1.31 1.41 0.85 Foreign Exchange Cross Rates C$ (USD per CAD) 1.02 1.03 1.03 0.93 Euro (USD per EUR) 1.38 1.40 1.42 1.19 Pound (USD per GBP) 1.60 1.63 1.63 1.43 Yen (JPY per USD) 82.2 82.3 94.6 80.4 Commodity Spot Prices** Crude Oil ($US/bbl) 99.6 104.4 105.4 66.0 Natural Gas ($US/MMBtu) 3.86 3.70 5.17 3.18 Copper ($US/met. tonne) 9173.0 9886.5 10179.5 6067.8 Gold ($US/troy oz.) 1410.7 1430.9 1434.5 1086.7 THIS WEEK IN THE MARKETS *as of 10 am on Friday, **Oil-WTI, Cushing, Nat. Gas-Henry Hub, LA (Thursday close price), Copper-LME Grade A, Gold-London Gold Bullion; Source: Bloomberg Federal Reserve (Fed Funds Rate) Bank of Canada (Overnight Rate) European Central Bank (Refi Rate) Bank of England (Repo Rate) Bank of Japan (Overnight Rate) Source: Central Banks, Haver Analytics GLOBAL OFFICIAL POLICY RATE TARGETS Current Target 0.00% 0.50% 0 - 0.25% 1.00% 1.00% U.S. DOLLAR EXCHANGE RATE 1.32 1.33 1.34 1.35 1.36 1.37 1.38 1.39 1.40 1.41 2/01 2/03 2/07 2/09 2/11 2/15 2/17 2/21 2/23 2/25 3/01 3/03 3/07 3/09 3/11 80.0 80.5 81.0 81.5 82.0 82.5 83.0 83.5 84.0 USD/EUR -L- JPY/USD -R- $ / € ¥ / $ Source: Federal Reserve Board of New York

Transcript

The Weekly Bottom Line TD Economicswww.td.com/economics

March 11, 2011

HIGHLIGHTS OF THE WEEK

United States• An8.9magnitudeearthquakewreakedhavoconJapanlastnight,pushingAsianandEuropeanstockslower.

*as of 10 am on Friday, **Oil-WTI, Cushing, Nat. Gas-Henry Hub, LA (Thursday close price), Copper-LME Grade A, Gold-London Gold Bullion; Source: Bloomberg

Federal Reserve (Fed Funds Rate)Bank of Canada (Overnight Rate)European Central Bank (Refi Rate)Bank of England (Repo Rate)Bank of Japan (Overnight Rate)Source: Central Banks, Haver Analytics

GLOBALOFFICIALPOLICYRATETARGETSCurrent Target

0.00%0.50%

0 - 0.25%1.00%1.00%

U.S.DOLLAREXCHANGERATE

1.32

1.33

1.34

1.35

1.36

1.37

1.38

1.39

1.40

1.41

2/01

2/03

2/07

2/09

2/11

2/15

2/17

2/21

2/23

2/25

3/01

3/03

3/07

3/09

3/11

80.0

80.5

81.0

81.5

82.0

82.5

83.0

83.5

84.0

USD/EUR -L-JPY/USD -R-

$ / € ¥ / $

Source: Federal Reserve Board of New York

The Weekly Bottom LineMarch 11, 2011

TD Economicswww.td.com/economics

2

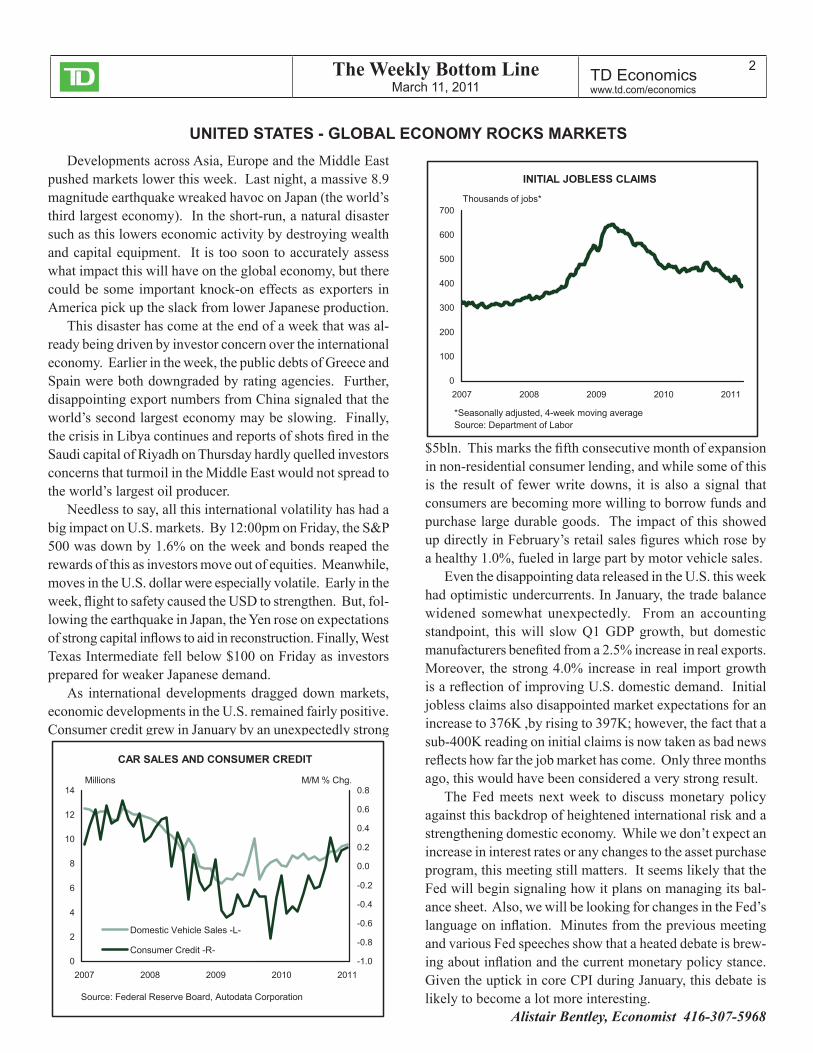

UNITEDSTATES-GLOBALECONOMYROCKSMARKETSDevelopments across Asia, Europe and the Middle East

pushed markets lower this week. Last night, a massive 8.9 magnitude earthquake wreaked havoc on Japan (the world’s third largest economy). In the short-run, a natural disaster such as this lowers economic activity by destroying wealth and capital equipment. It is too soon to accurately assess what impact this will have on the global economy, but there could be some important knock-on effects as exporters in America pick up the slack from lower Japanese production.

This disaster has come at the end of a week that was al-ready being driven by investor concern over the international economy. Earlier in the week, the public debts of Greece and Spain were both downgraded by rating agencies. Further, disappointing export numbers from China signaled that the world’s second largest economy may be slowing. Finally, the crisis in Libya continues and reports of shots fired in the Saudi capital of Riyadh on Thursday hardly quelled investors concerns that turmoil in the Middle East would not spread to the world’s largest oil producer.

Needless to say, all this international volatility has had a big impact on U.S. markets. By 12:00pm on Friday, the S&P 500 was down by 1.6% on the week and bonds reaped the rewards of this as investors move out of equities. Meanwhile, moves in the U.S. dollar were especially volatile. Early in the week, flight to safety caused the USD to strengthen. But, fol-lowing the earthquake in Japan, the Yen rose on expectations of strong capital inflows to aid in reconstruction. Finally, West Texas Intermediate fell below $100 on Friday as investors prepared for weaker Japanese demand.

As international developments dragged down markets, economic developments in the U.S. remained fairly positive. Consumer credit grew in January by an unexpectedly strong

$5bln. This marks the fifth consecutive month of expansion in non-residential consumer lending, and while some of this is the result of fewer write downs, it is also a signal that consumers are becoming more willing to borrow funds and purchase large durable goods. The impact of this showed up directly in February’s retail sales figures which rose by a healthy 1.0%, fueled in large part by motor vehicle sales.

Even the disappointing data released in the U.S. this week had optimistic undercurrents. In January, the trade balance widened somewhat unexpectedly. From an accounting standpoint, this will slow Q1 GDP growth, but domestic manufacturers benefited from a 2.5% increase in real exports. Moreover, the strong 4.0% increase in real import growth is a reflection of improving U.S. domestic demand. Initial jobless claims also disappointed market expectations for an increase to 376K ,by rising to 397K; however, the fact that a sub-400K reading on initial claims is now taken as bad news reflects how far the job market has come. Only three months ago, this would have been considered a very strong result.

The Fed meets next week to discuss monetary policy against this backdrop of heightened international risk and a strengthening domestic economy. While we don’t expect an increase in interest rates or any changes to the asset purchase program, this meeting still matters. It seems likely that the Fed will begin signaling how it plans on managing its bal-ance sheet. Also, we will be looking for changes in the Fed’s language on inflation. Minutes from the previous meeting and various Fed speeches show that a heated debate is brew-ing about inflation and the current monetary policy stance. Given the uptick in core CPI during January, this debate is likely to become a lot more interesting.

Alistair Bentley, Economist 416-307-5968

CARSALESANDCONSUMERCREDIT

0

2

4

6

8

10

12

14

2007 2008 2009 2010 2011-1.0

-0.8

-0.6

-0.4

-0.2

0.0

0.2

0.4

0.6

0.8

Domestic Vehicle Sales -L-

Consumer Credit -R-

Millions M/M % Chg.

Source: Federal Reserve Board, Autodata Corporation

INITIALJOBLESSCLAIMS

0

100

200

300

400

500

600

700

2007 2008 2009 2010 2011

Thousands of jobs*

*Seasonally adjusted, 4-week moving averageSource: Department of Labor

As we move further away from the 2008/2009 financial crisis, the Canadian economic data continue to paint a picture of an economy swiftly returning to normal. That doesn’t mean we should expect the heydays of the decade prior to the recession to return. Those days were characterized by an overinflated housing market, and booming commod-ity prices and employment markets, both of which have proven unsustainable. A more normal environment for the Canadian economy is one characterized by moderate, but healthy growth.

This week’s data helped underscore this view, with hous-ing starts and employment not too hot, and not too cold. In fact, at the current rate of 181,300 units, housing starts are largely inline with the 177,000 average units per month required to keep up with population growth, as estimated by CMHC. Meanwhile, Friday’s job figures showed that the recovery in the labour market has become well entrenched, with the level of employment eclipsing the pre-recession peak by 65,000 jobs in February. Admittedly, the details of the employment report in February were soft, but on a trend basis, the Canadian economy has turned out an average 20,000-25,000 jobs per month over the last six months, led by private, full-time positions. These jobs gains are consis-tent with healthy, steady economic growth in the range of 2.5-3.0%. The unemployment rate remains stuck at a lofty 7.8%, but with the labour market expected to continue chug-ging along at its current pace, the unemployment rate should continue to drift down, reaching 7.5% by end of 2011 and 7.3% by end of 2012.

The trade data this week were also encouraging with further evidence that Canada’s trade deficits caused by the recession is unwinding. Canada’s merchandise trade bal-ance was back in black for a second consecutive month in

January, and for the first time in two years. With the U.S. recovery becoming more entrenched, demand for Canadian exports is likely to remain firm through 2011 and 2012. As such, the Canadian economy should continue to enjoy a sustained recovery in its trade balance.

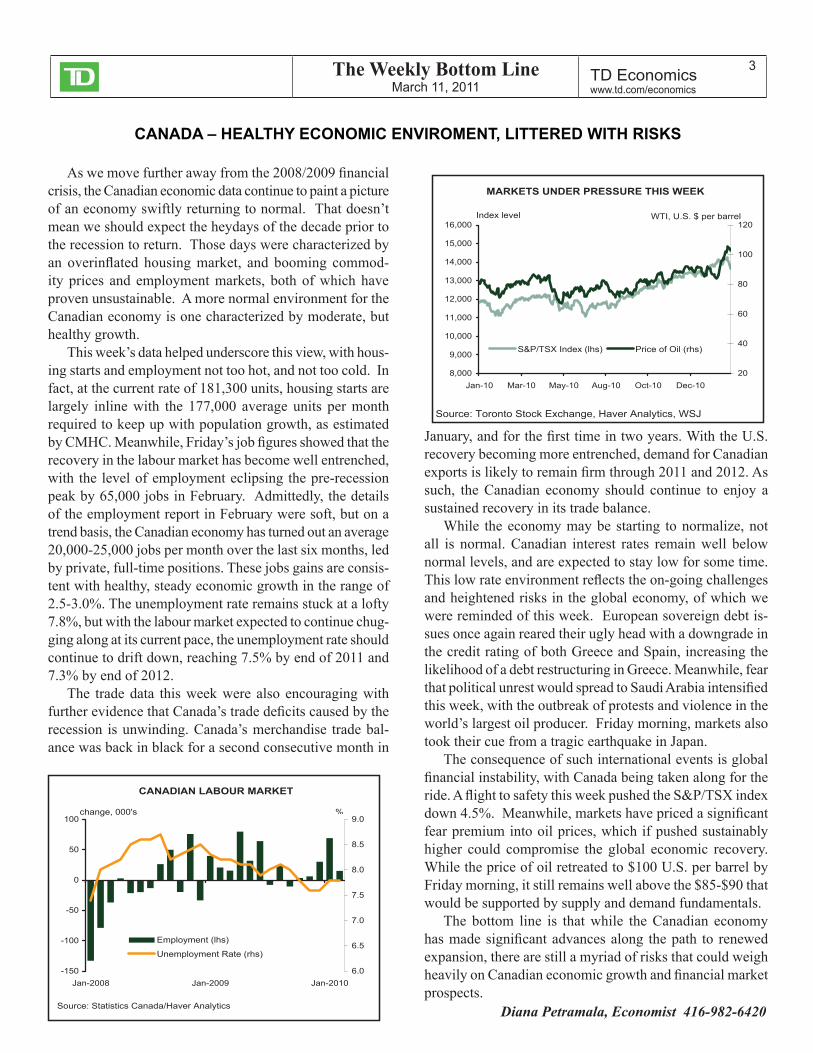

While the economy may be starting to normalize, not all is normal. Canadian interest rates remain well below normal levels, and are expected to stay low for some time. This low rate environment reflects the on-going challenges and heightened risks in the global economy, of which we were reminded of this week. European sovereign debt is-sues once again reared their ugly head with a downgrade in the credit rating of both Greece and Spain, increasing the likelihood of a debt restructuring in Greece. Meanwhile, fear that political unrest would spread to Saudi Arabia intensified this week, with the outbreak of protests and violence in the world’s largest oil producer. Friday morning, markets also took their cue from a tragic earthquake in Japan.

The consequence of such international events is global financial instability, with Canada being taken along for the ride. A flight to safety this week pushed the S&P/TSX index down 4.5%. Meanwhile, markets have priced a significant fear premium into oil prices, which if pushed sustainably higher could compromise the global economic recovery. While the price of oil retreated to $100 U.S. per barrel by Friday morning, it still remains well above the $85-$90 that would be supported by supply and demand fundamentals.

The bottom line is that while the Canadian economy has made significant advances along the path to renewed expansion, there are still a myriad of risks that could weigh heavily on Canadian economic growth and financial market prospects.

Diana Petramala, Economist 416-982-6420

CANADIANLABOURMARKET

-150

-100

-50

0

50

100

Jan-2008 Jan-2009 Jan-20106.0

6.5

7.0

7.5

8.0

8.5

9.0

Employment (lhs)

Unemployment Rate (rhs)

change, 000's %

Source: Statistics Canada/Haver Analytics

MARKETSUNDERPRESSURETHISWEEK

8,000

9,000

10,000

11,000

12,000

13,000

14,000

15,000

16,000

Jan-10 Mar-10 May-10 Aug-10 Oct-10 Dec-1020

40

60

80

100

120

S&P/TSX Index (lhs) Price of Oil (rhs)

Source: Toronto Stock Exchange, Haver Analytics, WSJ

Index level WTI, U.S. $ per barrel

The Weekly Bottom LineMarch 11, 2011

TD Economicswww.td.com/economics

4

U.S.:UPCOMINGKEYECONOMICRELEASES

*Forecast by Rates and FX Strategy Group. For further information, contact TDRates&[email protected].

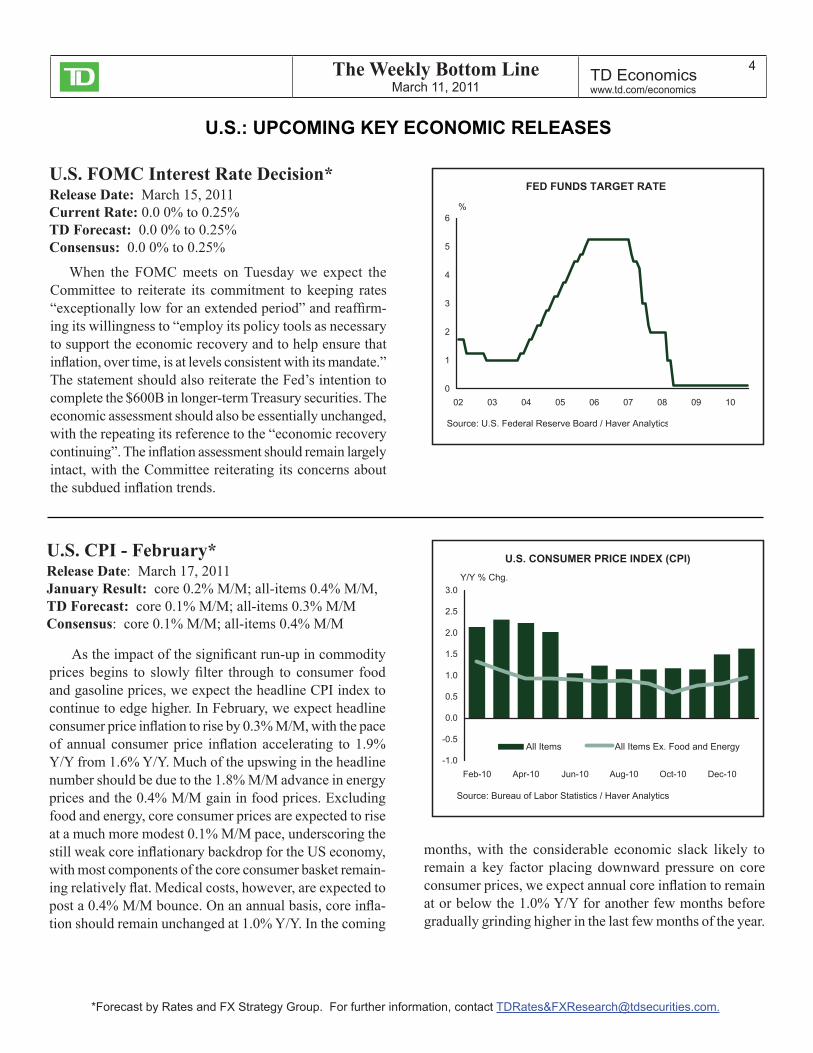

When the FOMC meets on Tuesday we expect the Committee to reiterate its commitment to keeping rates “exceptionally low for an extended period” and reaffirm-ing its willingness to “employ its policy tools as necessary to support the economic recovery and to help ensure that inflation, over time, is at levels consistent with its mandate.” The statement should also reiterate the Fed’s intention to complete the $600B in longer-term Treasury securities. The economic assessment should also be essentially unchanged, with the repeating its reference to the “economic recovery continuing”. The inflation assessment should remain largely intact, with the Committee reiterating its concerns about the subdued inflation trends.

As the impact of the significant run-up in commodity prices begins to slowly filter through to consumer food and gasoline prices, we expect the headline CPI index to continue to edge higher. In February, we expect headline consumer price inflation to rise by 0.3% M/M, with the pace of annual consumer price inflation accelerating to 1.9% Y/Y from 1.6% Y/Y. Much of the upswing in the headline number should be due to the 1.8% M/M advance in energy prices and the 0.4% M/M gain in food prices. Excluding food and energy, core consumer prices are expected to rise at a much more modest 0.1% M/M pace, underscoring the still weak core inflationary backdrop for the US economy, with most components of the core consumer basket remain-ing relatively flat. Medical costs, however, are expected to post a 0.4% M/M bounce. On an annual basis, core infla-tion should remain unchanged at 1.0% Y/Y. In the coming

months, with the considerable economic slack likely to remain a key factor placing downward pressure on core consumer prices, we expect annual core inflation to remain at or below the 1.0% Y/Y for another few months before gradually grinding higher in the last few months of the year.

U.S. FOMC Interest Rate Decision* Release Date: March 15, 2011Current Rate: 0.0 0% to 0.25%TD Forecast: 0.0 0% to 0.25%Consensus: 0.0 0% to 0.25%

*Forecast by Rates and FX Strategy Group. For further information, contact TDRates&[email protected].

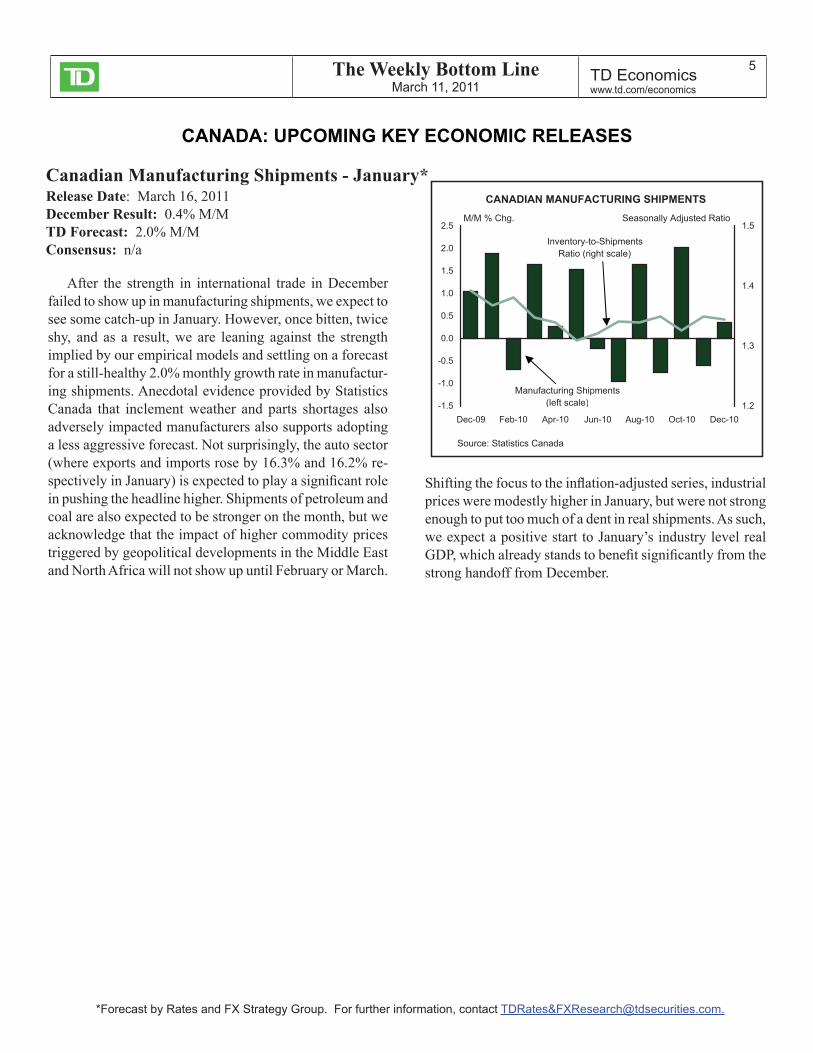

After the strength in international trade in December failed to show up in manufacturing shipments, we expect to see some catch-up in January. However, once bitten, twice shy, and as a result, we are leaning against the strength implied by our empirical models and settling on a forecast for a still-healthy 2.0% monthly growth rate in manufactur-ing shipments. Anecdotal evidence provided by Statistics Canada that inclement weather and parts shortages also adversely impacted manufacturers also supports adopting a less aggressive forecast. Not surprisingly, the auto sector (where exports and imports rose by 16.3% and 16.2% re-spectively in January) is expected to play a significant role in pushing the headline higher. Shipments of petroleum and coal are also expected to be stronger on the month, but we acknowledge that the impact of higher commodity prices triggered by geopolitical developments in the Middle East and North Africa will not show up until February or March.

Canadian Manufacturing Shipments - January*Release Date: March 16, 2011December Result: 0.4% M/M TD Forecast: 2.0% M/MConsensus: n/a

Shifting the focus to the inflation-adjusted series, industrial prices were modestly higher in January, but were not strong enough to put too much of a dent in real shipments. As such, we expect a positive start to January’s industry level real GDP, which already stands to benefit significantly from the strong handoff from December.

*Forecast by Rates and FX Strategy Group. For further information, contact TDRates&[email protected].

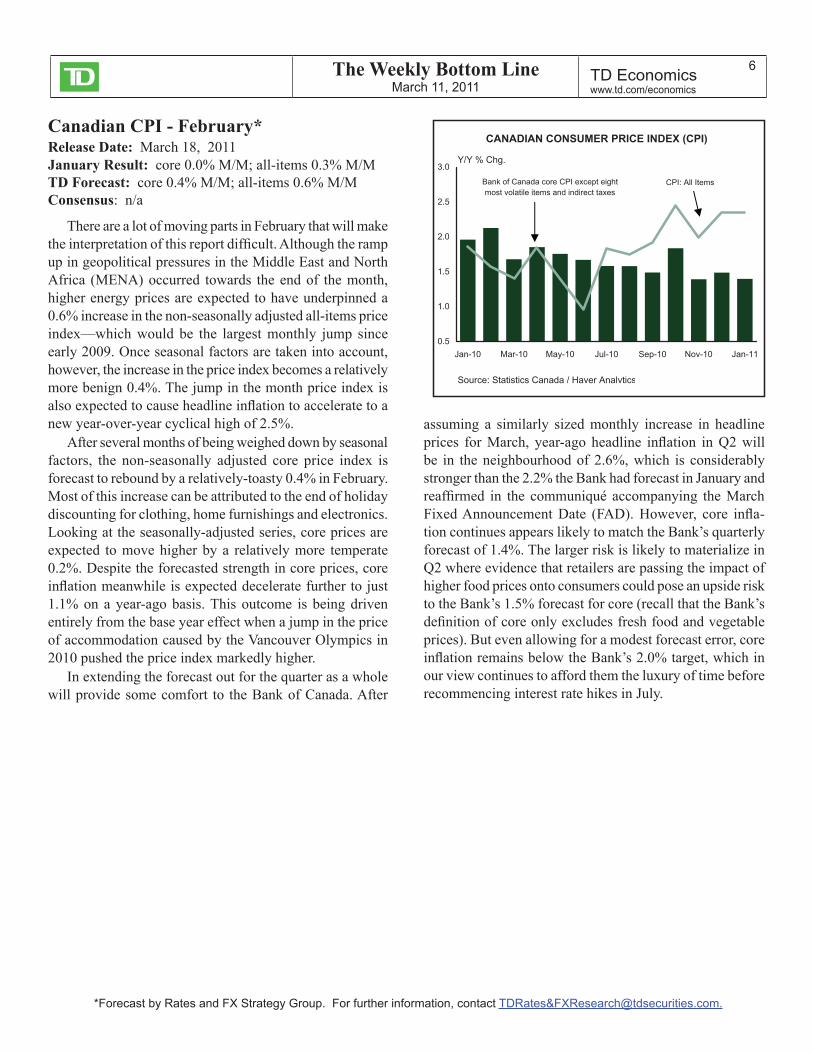

There are a lot of moving parts in February that will make the interpretation of this report difficult. Although the ramp up in geopolitical pressures in the Middle East and North Africa (MENA) occurred towards the end of the month, higher energy prices are expected to have underpinned a 0.6% increase in the non-seasonally adjusted all-items price index—which would be the largest monthly jump since early 2009. Once seasonal factors are taken into account, however, the increase in the price index becomes a relatively more benign 0.4%. The jump in the month price index is also expected to cause headline inflation to accelerate to a new year-over-year cyclical high of 2.5%.

After several months of being weighed down by seasonal factors, the non-seasonally adjusted core price index is forecast to rebound by a relatively-toasty 0.4% in February. Most of this increase can be attributed to the end of holiday discounting for clothing, home furnishings and electronics. Looking at the seasonally-adjusted series, core prices are expected to move higher by a relatively more temperate 0.2%. Despite the forecasted strength in core prices, core inflation meanwhile is expected decelerate further to just 1.1% on a year-ago basis. This outcome is being driven entirely from the base year effect when a jump in the price of accommodation caused by the Vancouver Olympics in 2010 pushed the price index markedly higher.

In extending the forecast out for the quarter as a whole will provide some comfort to the Bank of Canada. After

assuming a similarly sized monthly increase in headline prices for March, year-ago headline inflation in Q2 will be in the neighbourhood of 2.6%, which is considerably stronger than the 2.2% the Bank had forecast in January and reaffirmed in the communiqué accompanying the March Fixed Announcement Date (FAD). However, core infla-tion continues appears likely to match the Bank’s quarterly forecast of 1.4%. The larger risk is likely to materialize in Q2 where evidence that retailers are passing the impact of higher food prices onto consumers could pose an upside risk to the Bank’s 1.5% forecast for core (recall that the Bank’s definition of core only excludes fresh food and vegetable prices). But even allowing for a modest forecast error, core inflation remains below the Bank’s 2.0% target, which in our view continues to afford them the luxury of time before recommencing interest rate hikes in July.

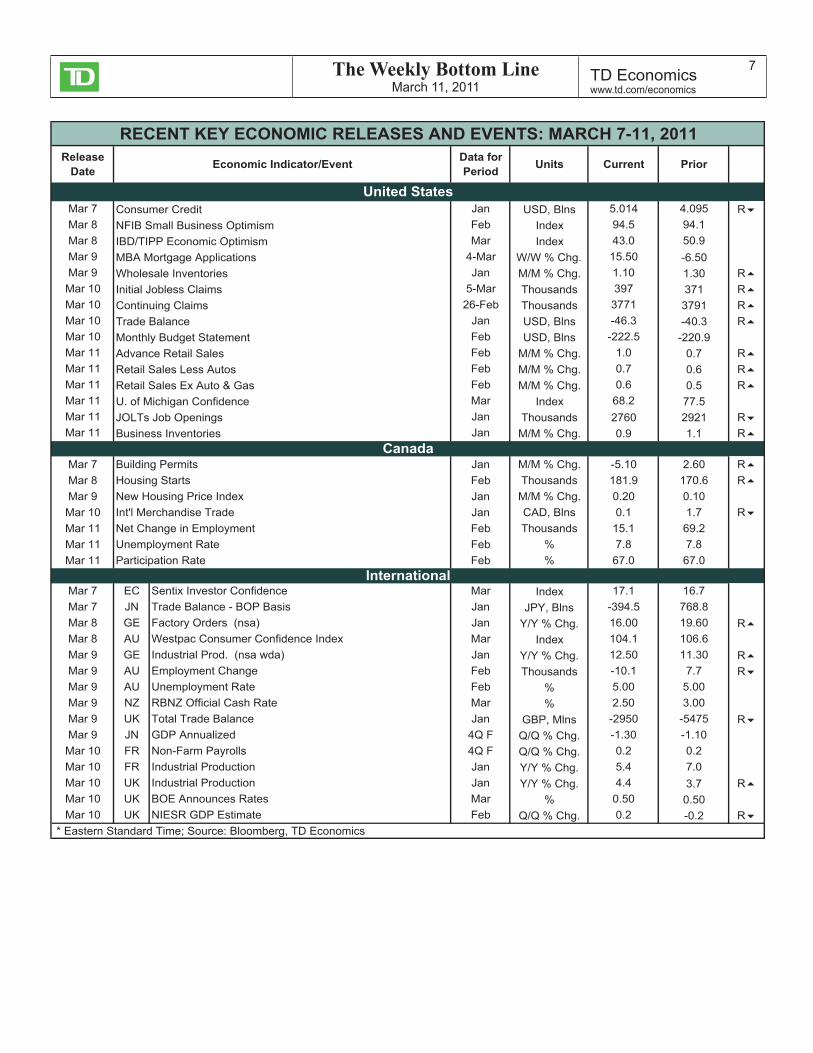

Mar 7 Consumer Credit Jan USD, Blns 5.014 4.095 RMar 8 NFIB Small Business Optimism Feb Index 94.5 94.1Mar 8 IBD/TIPP Economic Optimism Mar Index 43.0 50.9Mar 9 MBA Mortgage Applications 4-Mar W/W % Chg. 15.50 -6.50Mar 9 Wholesale Inventories Jan M/M % Chg. 1.10 1.30 RMar 10 Initial Jobless Claims 5-Mar Thousands 397 371 RMar 10 Continuing Claims 26-Feb Thousands 3771 3791 RMar 10 Trade Balance Jan USD, Blns -46.3 -40.3 RMar 10 Monthly Budget Statement Feb USD, Blns -222.5 -220.9Mar 11 Advance Retail Sales Feb M/M % Chg. 1.0 0.7 RMar 11 Retail Sales Less Autos Feb M/M % Chg. 0.7 0.6 RMar 11 Retail Sales Ex Auto & Gas Feb M/M % Chg. 0.6 0.5 RMar 11 U. of Michigan Confidence Mar Index 68.2 77.5Mar 11 JOLTs Job Openings Jan Thousands 2760 2921 RMar 11 Business Inventories Jan M/M % Chg. 0.9 1.1 R

Mar 7 Building Permits Jan M/M % Chg. -5.10 2.60 RMar 8 Housing Starts Feb Thousands 181.9 170.6 RMar 9 New Housing Price Index Jan M/M % Chg. 0.20 0.10Mar 10 Int'l Merchandise Trade Jan CAD, Blns 0.1 1.7 RMar 11 Net Change in Employment Feb Thousands 15.1 69.2Mar 11 Unemployment Rate Feb % 7.8 7.8Mar 11 Participation Rate Feb % 67.0 67.0

Mar 7 EC Sentix Investor Confidence Mar Index 17.1 16.7Mar 7 JN Trade Balance - BOP Basis Jan JPY, Blns -394.5 768.8Mar 8 GE Factory Orders (nsa) Jan Y/Y % Chg. 16.00 19.60 RMar 8 AU Westpac Consumer Confidence Index Mar Index 104.1 106.6Mar 9 GE Industrial Prod. (nsa wda) Jan Y/Y % Chg. 12.50 11.30 RMar 9 AU Employment Change Feb Thousands -10.1 7.7 RMar 9 AU Unemployment Rate Feb % 5.00 5.00Mar 9 NZ RBNZ Official Cash Rate Mar % 2.50 3.00Mar 9 UK Total Trade Balance Jan GBP, Mlns -2950 -5475 RMar 9 JN GDP Annualized 4Q F Q/Q % Chg. -1.30 -1.10Mar 10 FR Non-Farm Payrolls 4Q F Q/Q % Chg. 0.2 0.2Mar 10 FR Industrial Production Jan Y/Y % Chg. 5.4 7.0Mar 10 UK Industrial Production Jan Y/Y % Chg. 4.4 3.7 RMar 10 UK BOE Announces Rates Mar % 0.50 0.50Mar 10 UK NIESR GDP Estimate Feb Q/Q % Chg. 0.2 -0.2 R

* Eastern Standard Time; Source: Bloomberg, TD Economics

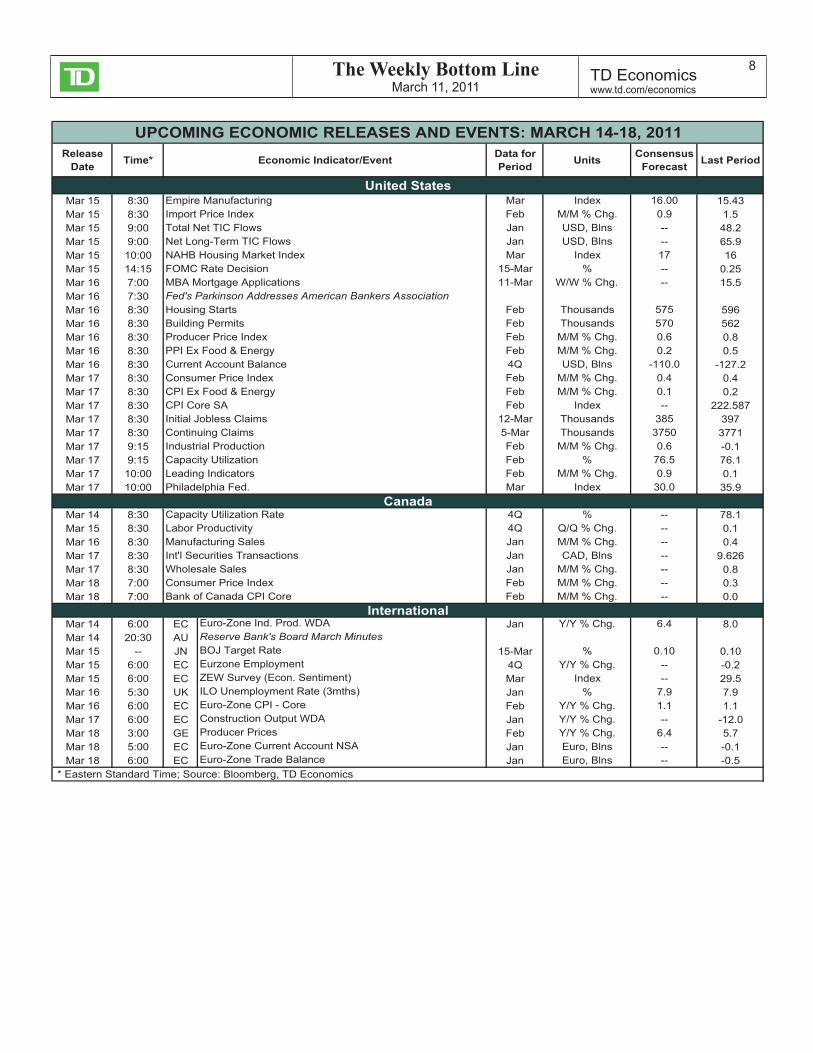

Date Time* EconomicIndicator/Event DataforPeriod Units Consensus

Forecast LastPeriod

United StatesMar 15 8:30 Empire Manufacturing Mar Index 16.00 15.43Mar 15 8:30 Import Price Index Feb M/M % Chg. 0.9 1.5Mar 15 9:00 Total Net TIC Flows Jan USD, Blns -- 48.2Mar 15 9:00 Net Long-Term TIC Flows Jan USD, Blns -- 65.9Mar 15 10:00 NAHB Housing Market Index Mar Index 17 16Mar 15 14:15 FOMC Rate Decision 15-Mar % -- 0.25Mar 16 7:00 MBA Mortgage Applications 11-Mar W/W % Chg. -- 15.5Mar 16 7:30 Fed's Parkinson Addresses American Bankers AssociationMar 16 8:30 Housing Starts Feb Thousands 575 596Mar 16 8:30 Building Permits Feb Thousands 570 562Mar 16 8:30 Producer Price Index Feb M/M % Chg. 0.6 0.8Mar 16 8:30 PPI Ex Food & Energy Feb M/M % Chg. 0.2 0.5Mar 16 8:30 Current Account Balance 4Q USD, Blns -110.0 -127.2Mar 17 8:30 Consumer Price Index Feb M/M % Chg. 0.4 0.4Mar 17 8:30 CPI Ex Food & Energy Feb M/M % Chg. 0.1 0.2Mar 17 8:30 CPI Core SA Feb Index -- 222.587Mar 17 8:30 Initial Jobless Claims 12-Mar Thousands 385 397Mar 17 8:30 Continuing Claims 5-Mar Thousands 3750 3771Mar 17 9:15 Industrial Production Feb M/M % Chg. 0.6 -0.1Mar 17 9:15 Capacity Utilization Feb % 76.5 76.1Mar 17 10:00 Leading Indicators Feb M/M % Chg. 0.9 0.1Mar 17 10:00 Philadelphia Fed. Mar Index 30.0 35.9

CanadaMar 14 8:30 Capacity Utilization Rate 4Q % -- 78.1Mar 15 8:30 Labor Productivity 4Q Q/Q % Chg. -- 0.1Mar 16 8:30 Manufacturing Sales Jan M/M % Chg. -- 0.4Mar 17 8:30 Int'l Securities Transactions Jan CAD, Blns -- 9.626Mar 17 8:30 Wholesale Sales Jan M/M % Chg. -- 0.8Mar 18 7:00 Consumer Price Index Feb M/M % Chg. -- 0.3Mar 18 7:00 Bank of Canada CPI Core Feb M/M % Chg. -- 0.0

InternationalMar 14 6:00 EC Euro-Zone Ind. Prod. WDA Jan Y/Y % Chg. 6.4 8.0Mar 14 20:30 AU Reserve Bank's Board March MinutesMar 15 -- JN BOJ Target Rate 15-Mar % 0.10 0.10Mar 15 6:00 EC Eurzone Employment 4Q Y/Y % Chg. -- -0.2Mar 15 6:00 EC ZEW Survey (Econ. Sentiment) Mar Index -- 29.5Mar 16 5:30 UK ILO Unemployment Rate (3mths) Jan % 7.9 7.9Mar 16 6:00 EC Euro-Zone CPI - Core Feb Y/Y % Chg. 1.1 1.1Mar 17 6:00 EC Construction Output WDA Jan Y/Y % Chg. -- -12.0Mar 18 3:00 GE Producer Prices Feb Y/Y % Chg. 6.4 5.7Mar 18 5:00 EC Euro-Zone Current Account NSA Jan Euro, Blns -- -0.1Mar 18 6:00 EC Euro-Zone Trade Balance Jan Euro, Blns -- -0.5

* Eastern Standard Time; Source: Bloomberg, TD Economics

The Weekly Bottom LineMarch 11, 2011

TD Economicswww.td.com/economics

9

This report is provided by TD Economics for customers of TD Bank Group. It is for information purposes only and may not be appropriate for other purposes. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. The report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.