Tobacco Buyout: Impacts on Manufacturers. Kelly Tiller. Agricultural Policy Analysis Center The University of Tennessee. 42 nd Tobacco Workers Conference Charleston, South Carolina January 17, 2006. - PowerPoint PPT Presentation

Agricultural Policy Analysis Center - University of Tennessee - 310 Morgan Hall - Knoxville, TN 37996-4519 www.agpolicy.org - phone: (865) 974-7407 - fax: (865) 974-7298 Tobacco Buyout: Tobacco Buyout: Impacts on Impacts on Manufacturer Manufacturer s s 42 nd Tobacco Workers Conference Charleston, South Carolina January 17, 2006 A A P P A A P P C C A A C C A A Kelly Tiller Agricultural Policy Analysis Center The University of Tennessee

Transcript

Agricultural Policy Analysis Center - University of Tennessee - 310 Morgan Hall - Knoxville, TN 37996-4519

• Tobacco manufacturer and importer assessments(-$10b)

• Domestic leaf cost savings (+$3.1b to $6.5b)

• Imported leaf cost savings (+?)– Savings for domestic leaf purchases for use in

international manufacturing operations (+?)

• Phase II payment savings (+$2.1b)

• Responsiveness to future market changes (+?)

• Net financial burden: 1.3¢ to 2.7¢ per pack

AAPP CCAA

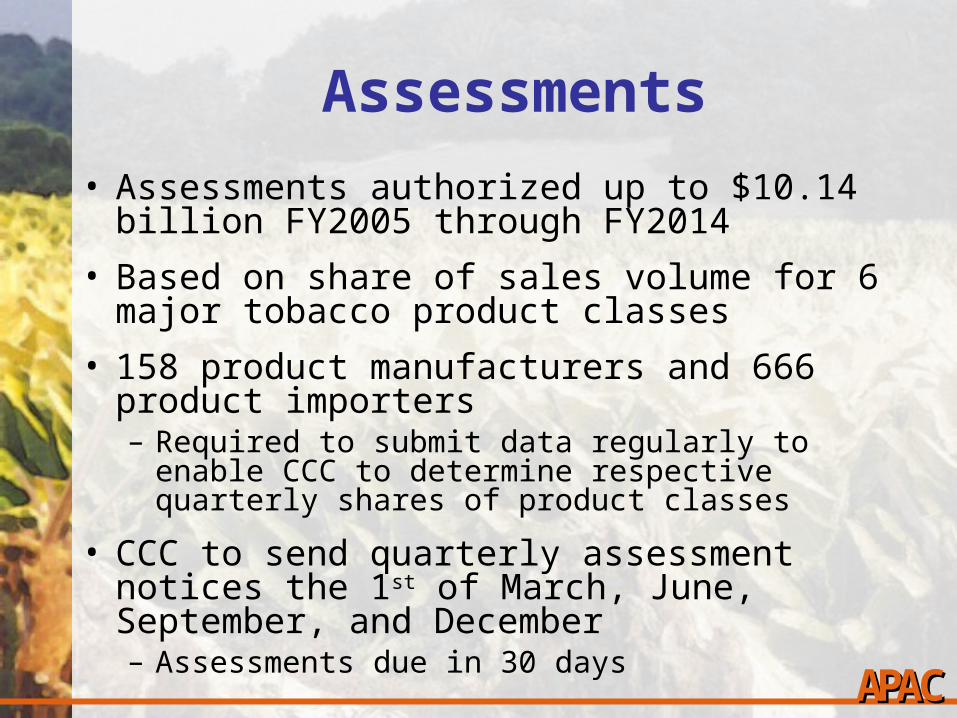

Assessments

• Assessments authorized up to $10.14 billion FY2005 through FY2014

• Based on share of sales volume for 6 major tobacco product classes

• 158 product manufacturers and 666 product importers– Required to submit data regularly to enable CCC

to determine respective quarterly shares of product classes

• CCC to send quarterly assessment notices the 1st of March, June, September, and December– Assessments due in 30 days AAPP CCAA

Assessments

AAPP CCAA

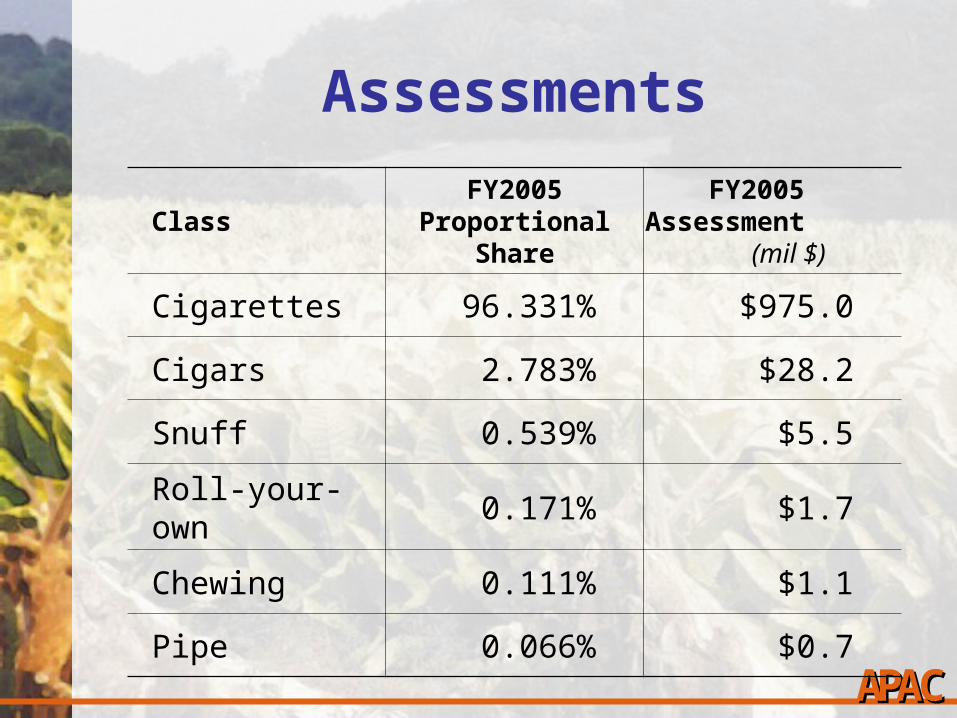

ClassFY2005

Proportional Share

FY2005 Assessment

(mil $)

Cigarettes 96.331% $975.0

Cigars 2.783% $28.2

Snuff 0.539% $5.5

Roll-your-own 0.171% $1.7

Chewing 0.111% $1.1

Pipe 0.066% $0.7

Market Responsiveness

• Absent the federal tobacco program, U.S. tobacco industry can exert more control over the tobacco production sector– Mere existence of former program influenced

the incentive structure surrounding contracting

– Growers now have a much stronger incentive to quickly adjust production, curing, and market prep practices to meet customer demands

• Highly beneficial in the event of future FDA authority

AAPP CCAA

Measuring Mfgr Impacts

• Event study methodology– Predicated upon the efficient markets hypothesis– All available information is impounded in current

stock prices– The value of a firm changes as the result of

unexpected events that cause investors to revise estimates of future cash flows and/or risk

• Calculate a measure of “normal” returns

• Calculate “actual” returns around event dates

• Estimate abnormal returns, the difference between actual and normal returns AAPP CCAA

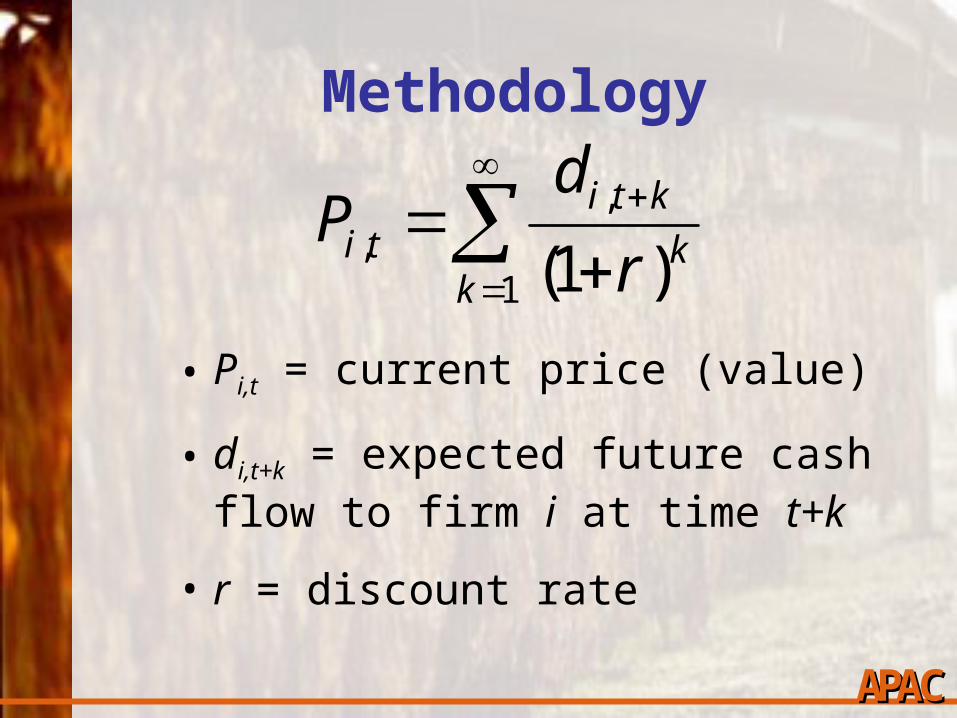

Methodology

• Pi,t = current price (value)

• di,t+k = expected future cash flow to firm i at time t+k

• r = discount rate

AAPP CCAA

1

,, )1(k

k

ktiti r

dP

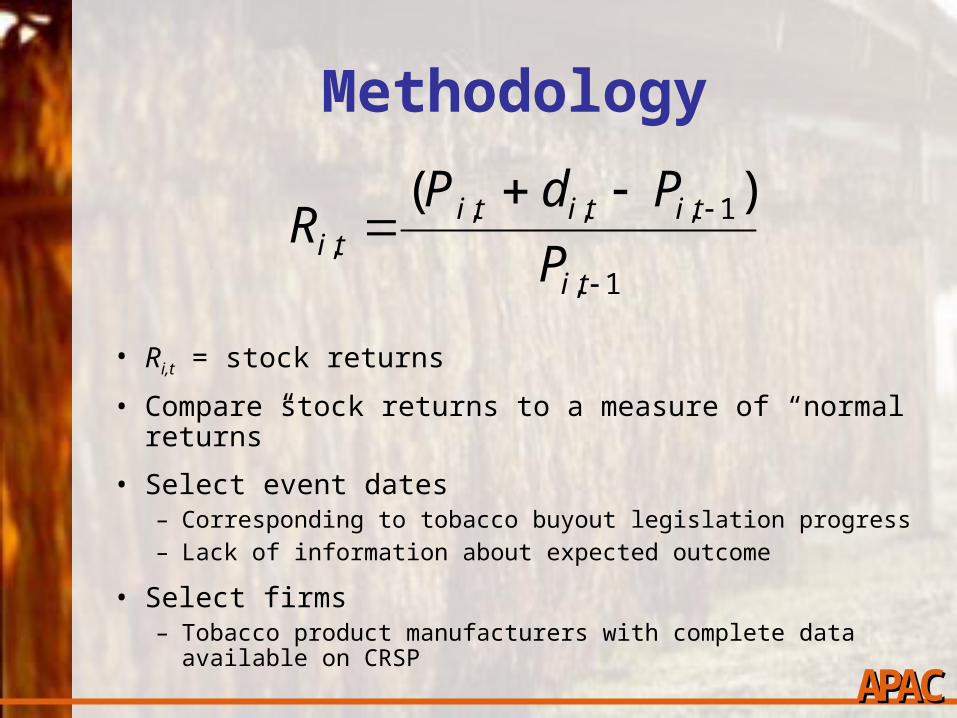

Methodology

• Ri,t = stock returns

• Compare stock returns to a measure of “normal returns”

• Select event dates– Corresponding to tobacco buyout legislation progress– Lack of information about expected outcome

• Select firms– Tobacco product manufacturers with complete data

available on CRSP AAPP CCAA

1,

1,,,,

)(

ti

titititi P

PdPR

Methodology

• Rm,t = value-weighted return on a portfolio of all marketable securities at time t

• ei,t = error term for firm i at time t; expected value of zero; variance = σ2

ei

• Estimated over the period 200 trading days before the event to 11 days before the event

AAPP CCAA

titmiiti eRR ,,,

Methodology

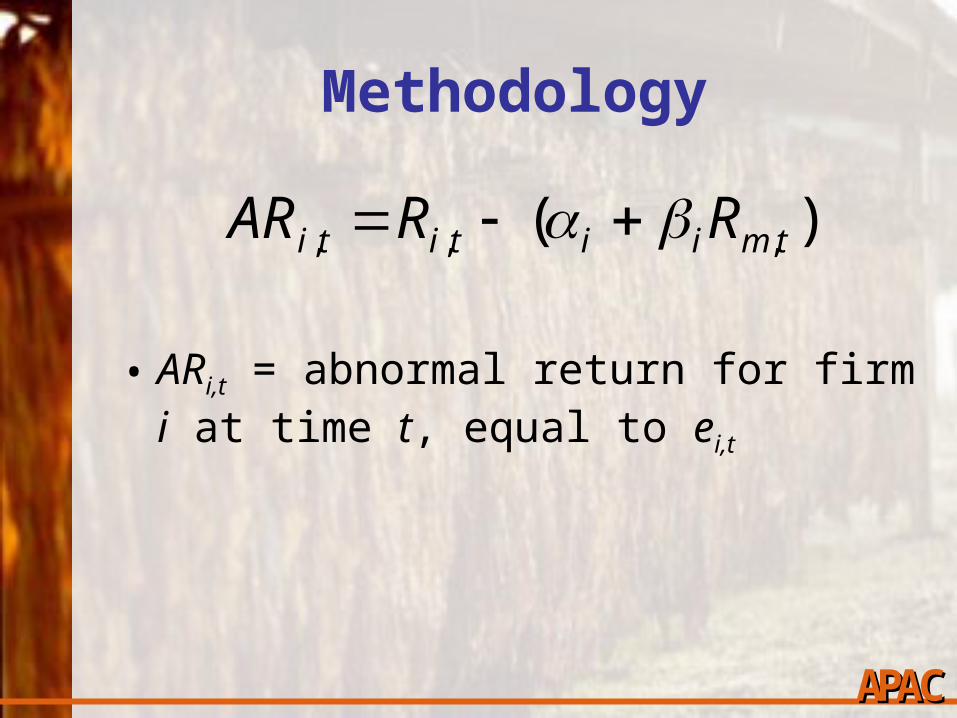

• ARi,t = abnormal return for firm i at time t, equal to ei,t

AAPP CCAA

)( ,,, tmiititi RRAR

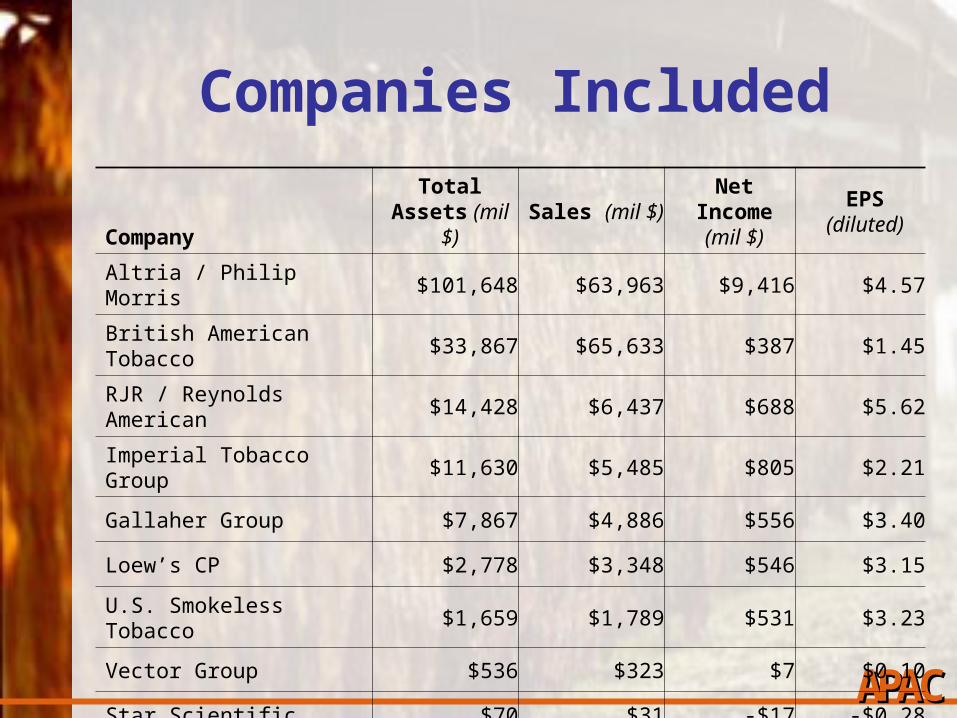

Companies Included

AAPP CCAA

Company

Total Assets (mil

$)

Sales (mil $)

Net Income (mil $)

EPS (diluted)

Altria / Philip Morris $101,648 $63,963 $9,416 $4.57

British American Tobacco

$33,867 $65,633 $387 $1.45

RJR / Reynolds American $14,428 $6,437 $688 $5.62

Imperial Tobacco Group $11,630 $5,485 $805 $2.21

Gallaher Group $7,867 $4,886 $556 $3.40

Loew’s CP $2,778 $3,348 $546 $3.15

U.S. Smokeless Tobacco $1,659 $1,789 $531 $3.23

Vector Group $536 $323 $7 $0.10

Star Scientific $70 $31 -$17 -$0.28

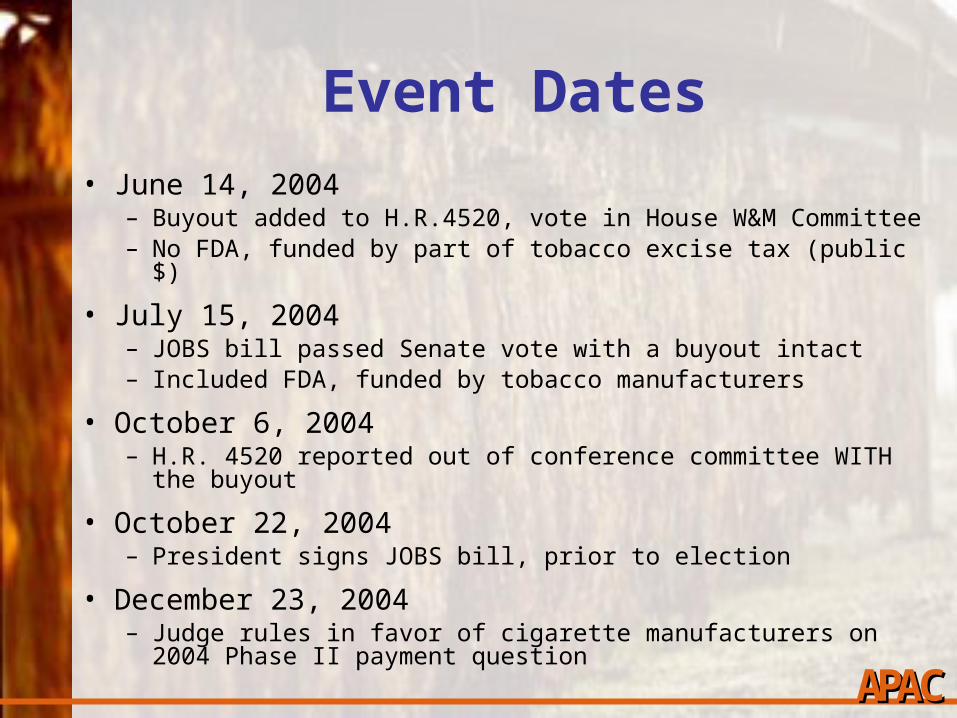

Event Dates

• June 14, 2004– Buyout added to H.R.4520, vote in House W&M Committee– No FDA, funded by part of tobacco excise tax (public $)

• July 15, 2004– JOBS bill passed Senate vote with a buyout intact– Included FDA, funded by tobacco manufacturers

• October 6, 2004– H.R. 4520 reported out of conference committee WITH the

buyout

• October 22, 2004– President signs JOBS bill, prior to election

• December 23, 2004– Judge rules in favor of cigarette manufacturers on 2004

Phase II payment questionAAPP CCAA

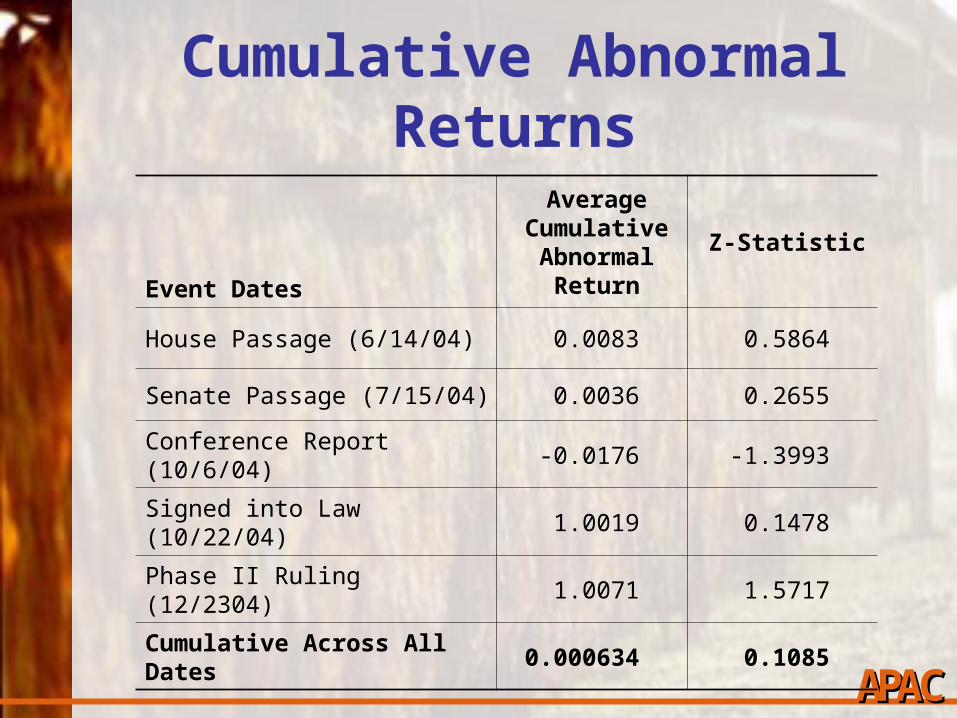

Cumulative Abnormal Returns

AAPP CCAA

Event Dates

Average Cumulative Abnormal

Return

Z-Statistic

House Passage (6/14/04) 0.0083 0.5864

Senate Passage (7/15/04) 0.0036 0.2655

Conference Report (10/6/04) -0.0176 -1.3993

Signed into Law (10/22/04) 1.0019 0.1478

Phase II Ruling (12/2304) 1.0071 1.5717

Cumulative Across All Dates 0.000634 0.1085

Summary & Conclusions

• No evidence that the buyout negatively affected tobacco product manufacturers

• Cumulative impact on expected returns was positive, 0.0006%, not statistically significant– Passage of conference report had a negative

impact, -0.02%, significant at 10%

– Phase II ruling was statistically significant, positive impact, 1.01%

• Weak evidence that non-market benefits of terminating the tobacco program outweighed net economic costs to manufacturers

AAPP CCAA

Summary & Conclusions

• Hypothesized that individual firms may be affected differently across event dates– No statistical evidence found

• The overall legislation (corporate tax overhaul) affects some multinational firms simultaneously in multiple ways

• May consider alternative event sets– Excluding signing bill into law

– Pulling out Phase II ruling and doing a separate event study on Phase II impacts