10

Image courtesy of Beckhoff Automation, Saugatuck Brewing Top 100 System Integrators | More than $7 billion in revenue represented inside

Image courtesy of Beckhoff Automation, Saugatuck Brewing

Top 100 System Integrators | More than $7 billion in revenue represented inside

System Integrator Giants of 2013

In its second year of production, the 2013 System Integrator Giants (SI Giants) program has assembled the 100 largest system integrators based on system integration revenue for the most recently completed fi scal year. Compared to

last year’s data, the 2013 metrics have signifi cantly increased in response to the number of participating fi rms, making the group even more “giant” in many ways.

For 2013, all 2,387 system integrators listed in the Control Engineering Automation Integrator Guide (AIG) were asked to provide details about annual revenues, head count, client base, industries and areas served, technical skills, professional affi liations, and product experience. They also were asked about the educational opportunities available to employees and

the biggest challenges they face as a company. Respondents reporting the largest system integration-related revenue are shown in the accompanying table (see pages 53 to 56).

In the early days of the computer industry, it was said that no one ever got fi red for buying IBM, meaning that the largest vendor in the business was never a bad choice. Some would say the same is true in today’s industrial automation industry when it comes to system integrators. Bigger integrators with more personnel and a broader geographic presence are arguably more adept than smaller competitors at implementing large-scale automation systems spread over multiple locations.

In practice, the advantages of hiring a larger integrator versus a smaller one probably depend on the particulars of each project, so the question of whether or not bigger is always better can never be defi nitively answered. Even the question of which integrators are the largest in the automation industry was a topic of debate before the 2013 System Integrator Giants survey.

The biggest change from last year is the addition of M+W Automation—the No. 1 system integrator for 2013—moving

Vance VanDoren, PhD, PE

The 100 largest system integrators in the industrial automation business—who they are and what they do.

46

More � rms with larger total revenue and larger system integration revenue replied to the SI Giants survey for 2013 than in 2012. Year-to-year total revenue increased 215% to $7.1 billion, and system integration revenue increased 41% to $1.2 billion. As a percent of total revenue, the revenue for system integration is less in 2013 at 17% compared to 39% in 2012. However, just excluding M+W alone (among new respondents with an unusually disproportionate amount of non-system integration revenue) increases the percentage of system integration income for 2013 to more than 30%.

System Integrator Giants: 2013 to 2012 revenue comparisonsTotal gross revenue

for � scal year($ U.S.)

Total system integration revenue

($ U.S.)

% of revenuefrom systemintegration

Median (50th ranked � rm) total

revenue

Median (50th ranked � rm):

SI revenue

% revenue from system

integration

2013 $7,097,250,184 $1,238,430,068 17% $8,500,000 $7,600,000 89%

2012 $2,251,284,436 $875,824,751 39% $5,000,000 $4,400,000 88%

2012 vs. 2013

Change in total rev-enue among those

ranked

Change in total SI revenue among those

ranked

Change in median (50th ranked � rm)

total revenue

Change in median (50th ranked � rm) total SI revenue

215% 41% 70% 73%

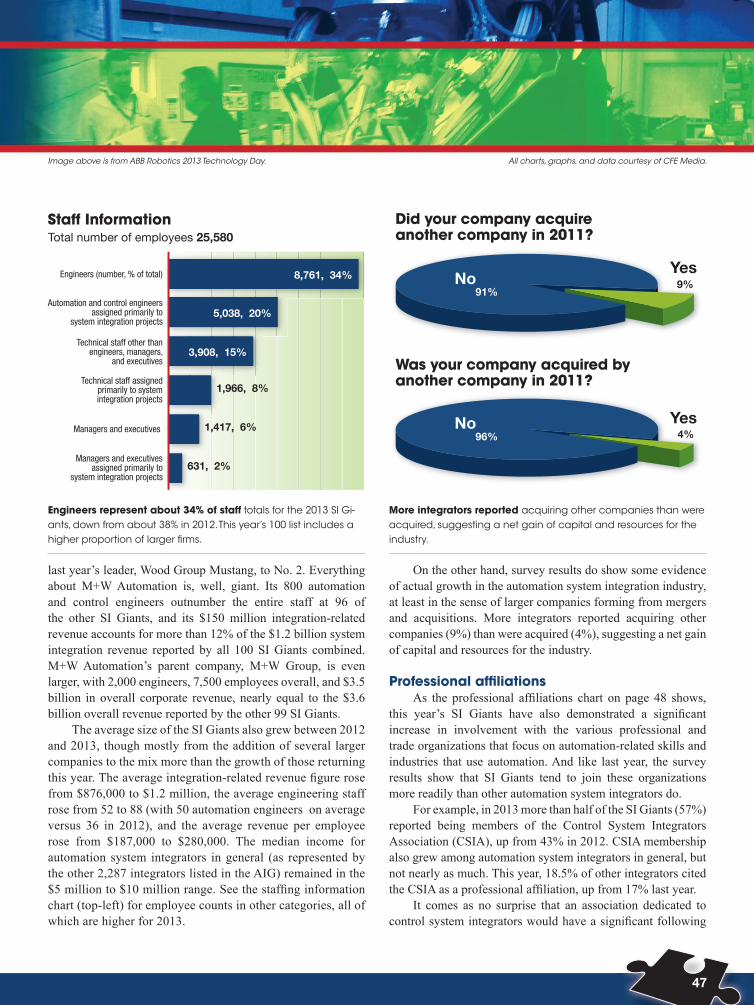

last year’s leader, Wood Group Mustang, to No. 2. Everything about M+W Automation is, well, giant. Its 800 automation and control engineers outnumber the entire staff at 96 of the other SI Giants, and its $150 million integration-related revenue accounts for more than 12% of the $1.2 billion system integration revenue reported by all 100 SI Giants combined. M+W Automation’s parent company, M+W Group, is even larger, with 2,000 engineers, 7,500 employees overall, and $3.5 billion in overall corporate revenue, nearly equal to the $3.6 billion overall revenue reported by the other 99 SI Giants.

The average size of the SI Giants also grew between 2012 and 2013, though mostly from the addition of several larger companies to the mix more than the growth of those returning this year. The average integration-related revenue fi gure rose from $876,000 to $1.2 million, the average engineering staff rose from 52 to 88 (with 50 automation engineers on average versus 36 in 2012), and the average revenue per employee rose from $187,000 to $280,000. The median income for automation system integrators in general (as represented by the other 2,287 integrators listed in the AIG) remained in the $5 million to $10 million range. See the staffi ng information chart (top-left) for employee counts in other categories, all of which are higher for 2013.

On the other hand, survey results do show some evidence of actual growth in the automation system integration industry, at least in the sense of larger companies forming from mergers and acquisitions. More integrators reported acquiring other companies (9%) than were acquired (4%), suggesting a net gain of capital and resources for the industry.

Professional af� liationsAs the professional affi liations chart on page 48 shows,

this year’s SI Giants have also demonstrated a signifi cant increase in involvement with the various professional and trade organizations that focus on automation-related skills and industries that use automation. And like last year, the survey results show that SI Giants tend to join these organizations more readily than other automation system integrators do.

For example, in 2013 more than half of the SI Giants (57%) reported being members of the Control System Integrators Association (CSIA), up from 43% in 2012. CSIA membership also grew among automation system integrators in general, but not nearly as much. This year, 18.5% of other integrators cited the CSIA as a professional affi liation, up from 17% last year.

It comes as no surprise that an association dedicated to control system integrators would have a signifi cant following

47

Staff InformationTotal number of employees 25,580

Engineers (number, % of total)

Automation and control engineersassigned primarily to

system integration projects

Technical staff other thanengineers, managers,

and executives

Technical staff assignedprimarily to systemintegration projects

Managers and executives

Managers and executivesassigned primarily to

system integration projects

8,761, 34%

5,038, 20%

3,908, 15%

1,966, 8%

1,417, 6%

631, 2%

Engineers represent about 34% of staff totals for the 2013 SI Gi-ants, down from about 38% in 2012. This year’s 100 list includes a higher proportion of larger � rms.

More integrators reported acquiring other companies than were acquired, suggesting a net gain of capital and resources for the industry.

All charts, graphs, and data courtesy of CFE Media.

Did your company acquireanother company in 2011?

Was your company acquired byanother company in 2011?

4%4%

9%Yes

Yes

No91%

No96%

Image above is from ABB Robotics 2013 Technology Day.

48

among both SI Giants and automation system integrators in general, but exactly why the CSIA should appeal so much more to larger fi rms is not altogether obvious. There was a time that the CSIA required a minimum annual revenue before a prospective member could join, but that requirement has been lifted. Perhaps smaller integrators still think of the CSIA as an organization just for the “big guys.”

Robotics vs. controlsThe organization for robotic system integrators, the

Robotics Industry Association (RIA), was cited by 3% of both

SI Giants and other integrators. At the 2013 Automate Show, the vast majority of system integrators exhibiting were RIA members (the event was sponsored in part by the RIA), yet only one belonged to the CSIA. Control system integration and robotic system integration industries seem to have little overlap, even though both cover industrial automation.

This divide is also evident in engineering specialties performed by the 2013 SI Giants (see table on page 52). Robotics (32%), vision systems (33%), and automated assemblies (33%) are the three least-common specialties performed, while automation and control engineering (95%), installation and start-up (93%), and HMI and operator interfaces (92%) round out the top three. Among automation system integrators in general, automation and programmable logic controller (PLC) skills were not so dominant (56% and 63%, respectively), but still well ahead of robotics and vision systems (32% and 30%, respectively).

Other professional organizations that gained popularity among the SI Giants included Underwriters Laboratories (UL), the Project Management Institute (PMI), and the National Society of Professional Engineers (NSPE). Comparing the 2012 and 2013 SI Giants data, UL increased from 19% to 39%; PMI increased from 11% to 24%; and NSPE increased from 10% to 24%. The International Society of Automation (ISA) remained in the top fi ve as the third most-cited professional affi liation, with 34% in 2013 vs. 38% in 2012. Rounding out the top 10 affi liations were the National Fire Protection Association (NFPA, 25%), the Control Systems Society (CSS, 20%), the International Society of Pharmaceutical Engineers (ISPE, 18%), the Institute of Electrical & Electronics Engineers (IEEE, 17%), and the American Society of Mechanical Engineers (ASME, 17%).

Most of these professional/third-party organizations are dedicated to the practice of various technical disciplines, which makes sense considering what automation system integrators do for a living. The list of most-cited professional affi liations among other integrators was similar: ISA, IEEE, CSIA, UL, CSS, NFPA, ASME, NSPE, and PMI.

Industries servedISPE was the 2013 SI Giants’ only top 10 professional

affi liation associated with a specifi c industry. It did not make the top 10 list for automation system integrators in general, but even for that group, ISPE was still the most popular of all professional organizations that focus on an industry rather than a technology. Ironically, pharmaceuticals as an industry

Professional and Third-party Af�liationsControl System

Integrators Association

UnderwritersLaboratories

International Societyof Automation

National FireProtection Association

Project ManagementInstitute

National Society of Professional Engineers

Control SystemsSociety (IEEE)

International Society ofPharmaceutical Engineers

Institute of Electrical &Electronics Engineers

American Society ofMechanical Engineers

Instrumentation andMeasurement Society (IEEE)

Industry ApplicationsSociety (IEEE)

American Institute ofChemical Engineers

Society of ManufacturingEngineers

OPC Foundation

FieldbusFoundation

American WaterWorks Association

AmericanPetroleum Institute

Robotic IndustriesAssociation

t

f

f

&

f

f

r

57%

39%

34%

25%

24%

24%

20%

18%

17%

17%

13%

13%

13%

7%

6%

6%

5%

5%

3%

The 2013 SI Giants are more involved in professional and trade organizations focusing on automation-related skills and industries that use automation. Majority of respondents belong to CSIA; RIA has the largest growth opportunity among the 2013 SI Giants.

was not as popular with the 2013 SI Giants or the other integrators listed in the AIG. Only 5% of the 2013 SI Giants serve the pharmaceutical manufacturing industry (see the chart on page 50), up 2% from 2012. Despite the industry’s increased popularity, pharmaceuticals still only accounted for half as much revenue as the most-served industry on the list: food and beverage (10%). The formerly most-served industry, oil and gas, dropped from 11% in 2012 to 8% in 2013. Rounding out the top fi ve were chemicals and petrochemicals (6%), automotive (6%), and water/wastewater (6%), about thesame as last year.

It is interesting to note that only one of these top fi ve industries served, automotive, is discrete, and of the top 10, there’s only one more, material handling (4%). The remaining industries are process or hybrid industries: metals (4%), consumer products (4%), and processing (3%). Perhaps the simplest explanation is that the refi neries, foundries, and processing plants of process industries generally operate on a much larger scale, with the exception of automotive plants of discrete industries, requiring the largest system integrators.

Product experienceThe divide between the SI Giants and robotic system

integrators came up again when the SI Giants were asked about vendor’s products they have integrated in the past 12 months. The most-cited robotics vendors were ABB with 55% popularity and Mitsubishi Electric Automation with 32%. But even those results are probably overestimates of the SI Giants’ involvement in robotics since ABB and Mitsubishi offer other automation products, and the product experience question did not specify divisions.

Which brands proved popular with the SI Giants? The Product Experience table (only online at www.controleng.com/giants) shows that Rockwell Automation’s Allen-Bradley brand from 71% in 2012 to 92% this year. The Rockwell

Automation brand itself increased to 89%, and Rockwell Software completed the Rockwell hat trick at 86%, up from 55% in 2012.

While the defending champion, Siemens Industry, fell to beneath the three Rockwell Automation brands with 79% this year, that popularity score improved from 71% in 2012. Invensys Wonderware also increased to 80%, up from 68% last year. The biggest gainers in this year’s product experience list were Microsoft (82%) and Dell (81%). Last year, they were 53% and 42%, respectively. These results would suggest that the SI Giants have become even more partial to product vendors offering PLCs, HMI software, and the personal computers (PCs) required to program PLCs and host HMI software.

Engineering specialtiesThe Engineering Specialties table on page 52

indicates that HMIs (92%) as a speciality are only slightly more selected by the 2013 SI Giants than PLCs (91%). Only the more generic skills of automation and control engineering (95%) and installation/start-up (93%)placed higher.

Ironically, the SI Giants did not identify PCs as a particularly popular engineering specialty, in spite of their affi nity for Dell and Microsoft. In 2013, only 58% of fi rms listed PCs as an engineering specialty, up 30% from 2012. Keeping consistent with the 2013 SI Giants’ top fi ve ranking of PMI, project management is an engineering speciality offered by 90% of the fi rms, up from 52% in 2012.

50

Food and beverage, oil and gas, chemicals and petrochemi-cals, automotive, and water and wastewater are the top � ve industries for the 2013 SI Giants.

Food, beverage, and allied industries (including baking, confections, and snack foods) ....... 10%Oil and gas (including exploration, production, transportation, and distribution) ........................ 8%Chemicals and petrochemicals (products and processing) .............................................. 6%Automotive (components and manufacturing) ................................................................... 6%Water and wastewater .............................................................................................. 6%Pharmaceuticals manufacturing ................................................................................ 5%

Industries Served - Big 6

More than half (56%) of 2013 SI Giants derive 76% to 100% of current business from existing clients.

Business from Existing ClientsWhat percentage of business in 2012 was from

existing clients? (not �rst-time clients)

0-10% 11-30% 31-50% 51-75% 76-90% 91-100%

3%3%

9%

12%30%

44%

52

The 2012 SI Giants’ top 10 engineering specialties were virtually identical as were the 2013 top 10 engineering specialties cited by other integrators in the AIG, though this year’s popularity scores for SI Giants were considerably higher than both.

These results also were consistent with the SI Giants’ affi nity for the CSIA and Rockwell Automation. All of the top 10 engineering specialties are integral to the practice of automation system integration, Rockwell Automation has signifi cant market share for the products involved (at least in North America), and the CSIA is the control system integrators’ most popular association, just as its name implies.

Challenges and opportunitiesIn a open-ended response, by far the challenges most often

cited by the survey’s respondents focused on fi nding, training,

and compensating the skilled labor they need. Last year’s top issue, the economy, came in a distant second for 2013. This result seems to refl ect the overall optimism about the economy in general and the automation industry in particular as reported by the CSIA in its own recent survey. (See “System integrators worldwide expect revenue growth in 2013” at www.controleng.com.)

Business seems to be so good that business-growth issues barely registered in respondents’ comments this year. Perhaps the 2013 SI Giants already have their hands full, but there’s a hidden danger in complacency. In response to a separate survey question, the SI Giants estimated their business percentage from existing clients, which showed that a whopping 86% of all respondents rely on existing clients for at least half of their revenue, and 12% rely on existing clients almost exclusively.

Repeat business is desirable, but what happens when projects run out? Presumably, there must come a time when even the most loyal client fi nds that everything that can be automated has been. But only three of the 2013 SI Giants cited “fi nding new customers” as a current challenge. Apparently, the rest of the SI Giants plan to cross that bridge when they come to it. Another challenge was geographical expansion. One SI Giant expressed interest in offering more services in more places, compared to 21 in 2012. It could be argued that trying to cover additional territory without opening new offi ces could be futile since clients would rather hire an integrator that can be on site within a matter of hours rather than days. (See the Areas Served charts online at www.controleng.com/giants.)

In conclusion, after two years worth of data collection from the System Integrator Giants, it remains apparent that system integrators continue to be a key component in the ever-evolving industrial manufacturing landscape. ce

- Vance VanDoren, PhD, PE, edits the Control EngineeringAutomation Integrator Guide. Patrick Lynch, project manager, provided data collection/analysis. Edited by Mark T. Hoske, content manager, Control Engineering, [email protected] and Amanda McLeman, project manager.

95% Automation and control engineering (including designs and implementation)

93% Installation and start-up92% Human-machine interfaces and operator interfaces91% Programmable logic controllers (including installation and programming)

90% Process control and automation90% Project management87% Data collection and reporting (including historians)

85% Control panels (including fabrication, installation, and UL listing)

85% Networking and communications (including � eldbus, Ethernet, and telemetry)

85% Systems engineering (including design and integration)

82% Computer engineering - software and programming82% SCADA (supervisory control and data acquisition)

81% Instrumentation and data acquisition81% Training and education80% Turnkey systems79% Discrete and sequential control79% Factory automation79% Field service79% Motors, drives, and motion control (including ac, dc, and variable frequency drives)

77% Batch control (including recipe management)

75% Project planning and consulting74% CAD/CAM, drafting, and documentation74% Data processing and database management (including SQL programming)

72% Supervisory control70% Designs and speci� cations (including P&ID development)

59% Distributed control systems (DCSs)

59% Electrical/electronics engineering (including electrical contracting)

59% Product tracking and identi� cation (including bar codes and radio frequency tags)

58% Personal computers (PCs)

49% Machine design and controls42% Water, wastewater, and groundwater systems33% Automated assembly33% Vision systems (including image processing and OCR)

32% Robotics

Engineering Specialties

Automation and controls, PLCs, installation and start-up, HMIs and operator interfaces (OIs) are among leading engineering specialties for the 2013 SI Giants.

At www.controleng.com/archive: � Take a survey about system integration with this article June 2013� See more tables, read more from system integrators about challenges� See the SI Giants for 2012 at www.controleng.com/giantsA no-cost listing in www.controleng.com/integrators is the first step for any automation, controls, instrumentation system integrator to be considered for SI Giants in 2014.

Go Online

53

1. M+W Automation Private $3,500,000,000 $150,000,000 4% Lotterbergstr. 30, 70499 Stuttgart, Germany www.mwgroup.net

2. Wood Group Mustang ** 1 Public $102,000,000 $95,000,000 93% 16001 Park Ten Pl., Houston, TX, 77084, USA www.mustangeng.com

3. Maverick Technologies ** 3 Private $80,000,000 $64,800,000 81% 265 Admiral Trost Dr., Columbia, IL, 62236, USA www.mavtechglobal.com

4. Prime Controls L.P. Private $65,235,302 $45,956,701 70% 815 Of� ce Park Cir., Lewisville, TX, 75057, USA www.prime-controls.com

5. Optimation Technology Inc. 4 Private $61,208,000 $45,500,000 74% 50 High Tech Dr., Rush, NY, 14543, USA www.optimation.us

6. Mangan Inc. ** 11 Employee $52,000,000 $41,600,000 80% 1500 W. Carson St., Ste. 100, Long Beach, CA, 90810, USA www.manganinc.com

7. EKB Public $36,976,989 $36,976,989 100% Wijkermeerweg 31, 1948 NT, Beverwijk, The Netherlands www.ekb.nl

8. Callisto Integration (Aseco **, PS2 merged) Private $32,000,000 $30,000,000 94% 635 Fourth Line, Unit 16, Oakville, Ontario, L6L 5B3, Canada www.callistointegration.com

9. Avanceon 6 Private $32,000,000 $24,000,000 75% 180 Sheree Blvd., Ste. 1400, Exton, PA, 19341, USA www.avanceon.com

9. Averna Private $37,000,000 $24,000,000 65% 87 Prince, Montreal, Quebec, H3C 2M7, Canada www.averna.com

11. Intech Process Automation Private $38,124,319 $23,447,318 62% 4903 W. Sam Houston Pkwy., North, Ste. A-100, Houston, TX, 77041, USA www.intechww.com

12. Matrix Technologies Inc. ** 10 Private $29,006,654 $23,205,323 80% 1760 Indian Wood Cir., Maumee, OH, 43537, USA www.matrixti.com

13. Nidec Avtron Automation Inc. 22 Public $35,000,000 $20,000,000 57% 7555 E. Pleasant Valley Rd., Bldg. 100, Independence, OH, 44131, USA www.avtron-ia.com

14. Premier System Integrators Private $29,500,000 $19,800,000 67% 140 Weakly Lane, Smyrna, TN, 37167, USA www.premier-system.com

15. EN Engineering LLC 14 Private $62,300,540 $17,078,045 27% 28100 Torch Pkwy., Ste. 400, Warrenville, IL, 60555, USA www.enengineering.com

16. E-Technologies Group Private $17,000,000 $17,000,000 100% 5530 Union Centre Dr., West Chester, OH, 45069, USA www.etech-group.com

16. SAIC Energy, Environment & Infrastructure LLC ** 48 Private $659,075,000 $17,000,000 3% 9400 N. Broadway, Oklahoma City, OK, 73114, USA www.saic.com/engineering

16. Testengeer Inc. 13 Employee $26,000,000 $17,000,000 65% 3777 Hwy. 35 South, Port Lavaca, TX, 77979, USA www.Testengeer.com

19. Concept Systems Inc. ** Private $16,700,000 $16,700,000 100% 1957 Fescue St. SE, Albany, OR, 97322, USA www.conceptsystemsinc.com

20. Applied Control Engineering Inc. 16 Private $15,900,000 $15,900,000 100% 700 Creek View Rd., Newark, DE, 19711, USA www.ace-net.com

21. Masmec SpA Private $15,700,000 $15,700,000 100% Via dei Gigli, 21, Modugno, 70026, Bari, Italy www.masmec.com

21. Thermo Systems LLC Private $25,500,000 $15,700,000 62% 84 Twin Rivers Dr., East Windsor, NJ, 08520, USA www.thermosystems.com

23. Barry-Wehmiller

Design Group Private $196,544,057 $14,163,937 7% 8020 Forsyth Blvd., St. Louis, MO, 63105, USA www.bwdesigngroup.com

24. Indicon Corp. Private $38,000,000 $14,000,000 37% 6125 Center Dr., Sterling Heights, MI, 48312, USA www.indicon.com

25. Interstates Control Systems Inc. ** 19 Private $18,500,000 $14,000,000 76% 444 12th St. NE, Sioux Center, IA, 51250, USA www.interstates.com

2013

rank

Compa

ny na

me

2012

rank

*

Owne

rship

type

Perce

ntage

of re

venu

e

fro

m syste

m integ

ration

Corp

orate

addr

ess

Web ad

dres

s

Total

gros

s rev

enue

for

� s

cal y

ear (

$ US

)

Total

syste

m integ

ration

rev

enue

( $ US

)

2013 SI Giants (by system integration revenue)

In the second year of CFE Media SI Giants, 65 companies that didn’t respond last year are ranked in the 2013 list of 100 largest by automation system integration revenue,

providing a much larger set of companies, overall. Until the 94th ranking, all the 2013 � rms have greater system integration revenue than those in the 2012 list. Only those

ranked 96-100 had less system integration revenue than those 2012 rankings.

1 - as Mustang Automation & Control22 - as Avtron Industrial Automation

2012 rank notes

54

26. Five Star Electric Private $68,000,000 $13,600,000 20% 4729 Shavano Oak, San Antonio, TX, 78249, USA www.vfd.com

27. Champion Technology Services Inc. 20 Private $22,720,000 $12,950,000 57% 11824 Market Place Ave., Baton Rouge, LA, 70816, USA www.champtechnology.com

28. Insist Avtomatika 17 Private $14,837,000 $12,218,741 82% 18-1A Marx St., Omsk, 644042, Russia www.industrialsystems.ru

29. Hollander Techniek Private $85,241,278 $12,000,000 14% Boogschutterstraat 30, Apeldoorn, 7324 AG GLD, The Netherlands www.hollandertechniek.nl

29. ICS Healy-Ruff Private $15,000,000 $12,000,000 80% 13005 16th Avenue North, Ste. 100, Plymouth, MN, 55441, USA www.icshealyruff.com

29. Integrity Integration Resources (I2R) ** Private $29,500,000 $12,000,000 41% 4001 E. Plano Pkwy., Ste. 500, Plano, TX, 75074, USA www.i2r.com

29. Kahler Automation Corp. Private $14,000,000 $12,000,000 86% 808 Timberlake Rd., Fairmont, MN, 56031, USA www.kahlerautomation.com

33. JMP Engineering ** 8 Private $19,245,000 $11,850,000 62% 4026 Meadowbrook Dr., Unit 143, London, Ontario, N6L 1C9, Canada www.jmpeng.com

34. Matrix Design Inc. Private $11,200,000 $10,990,000 98% 1627 Louise Dr., South Elgin, IL, 60177, USA www.getmatrixed.com

35. MLR System GmbH Employee $15,641,333 $10,948,933 70% Voithstrasse 15, Ludwigsburg, 71640, Germany www.mlr.de

36. Faith Technologies 28 Private $261,000,000 $10,535,000 4% 225 Main St., Menasha, WI, 54952, USA www.faithtechnologies.com

37. SpiraTec Private/ Employee $12,185,000 $10,525,000 86% 1839 Ygnacio Valley Road, #390, Walnut Creek, CA, 94598, USA www.spiratec-solutions.com

38. Avid Solutions Private $15,236,000 $10,281,000 67% 2875 Ridgewood Park Dr., Winston-Salem, NC, 27107, USA www.avidsolutionsinc.com

39. Innovative Controls Employee $104,000,000 $10,200,000 10% 624 Reliability Cir., Knoxville, TN, 37932, USA www.innovativecontrols.com

40. TriCore Inc. Private $10,173,595 $10,173,595 100% 6921 Mariner Dr., Racine, WI, 53406, USA www.tricore.com

41. Ausenco Public $633,500,000 $10,120,544 2% 1320 Willow Pass Rd., Ste. 300, Concord, CA, 94520, USA www.ausenco.com

42. aeSolutions Private $29,000,000 $9,396,000 32% 250 Commonwealth Dr., Ste. 200, Greenville, SC, 29615, USA www.aesolns.com

43. Superior Controls Inc. ** Private $9,400,000 $9,000,000 96% 135 Folly Mill Rd., Seabrook, NH, 03874, USA www.SuperiorControls.com

44. Alliant Technologies Private n/a $8,800,000 n/a 2080 Nelson Miller Pkwy., Louisville, KY, 40223, USA www.atcss.com

45. Automation & Control Concepts Inc. 37 Private $8,353,000 $8,353,000 100% 1310 Papin St., St. Louis, MO, 63129, USA www.a-cc.com

46. ESCO Automation 18 Private $38,100,000 $8,100,000 21% 3450 3rd St., Marion, IA, 52302, USA www.theescogroup.com

47. Cal-Bay Systems Private $8,000,000 $8,000,000 100% 3070 Kerner Blvd., Ste. B, San Rafael, CA, 94901, USA www.calbay.com

47. Direct Automation LLC Private $10,000,000 $8,000,000 80% 408 N. Hwy. 77, Dell Rapids, SD, 57022, USA www.direct-automation.com

47. Zarpac Inc. Public $11,000,000 $8,000,000 73% 1185 North Service Rd. East, Oakville, Ontario, L6H 1A7, Canada www.zarpac.com

50. Malisko Engineering Inc. 40 Private $8,500,000 $7,600,000 89% 707 N. 2nd St., Ste. 650, St. Louis, MO, 63102, USA www.malisko.com

51. Cotmac Electronics Pvt Ltd. Private $37,735,849 $7,547,169 20% S-168, MIDC, Bhosari, Pune, Maharashtra, 411026, India www.cotmacelectronics.com

2013

rank

Compa

ny na

me

2012

rank

*

Owne

rship

type

Perce

ntage

of re

venu

e

fro

m syste

m integ

ration

Corp

orate

addr

ess

Web ad

dres

s

Total

gros

s rev

enue

for

� s

cal y

ear (

$ US

)

Total

syste

m integ

ration

rev

enue

( $ US

)

2013 SI Giants (by system integration revenue)

55

52. R+D Custom Automation Employee $8,200,000 $6,970,000 85% 23411 W. Wall St., Lake Villa, IL, 60046, USA www.rdcustomautomation.com

53. Cougar Automation Ltd. 41 Private $8,253,968 $6,603,174 80% Birch House, Forest Rd., Waterlooville, Hampshire, PO7 6XP, U.K. www.cougar-automation.com

54. Dynamic Design Solutions Inc. Private $6,150,000 $6,150,000 100% 3565 Centre Cir., Fort Mill, SC, 29715, USA www.dynamicdesignsolutionsinc.com

55. Patti Engineering Inc. ** Private $6,700,000 $5,900,000 88% 2110 E. Walton Blvd., Auburn Hills, MI, 48326, USA www.pattieng.com

56. Stratus Automation Private $7,260,000 $5,780,000 80% 22613 68th Ave S., Kent, WA, 98032, USA www.stratusauto.com

57. IASTech Automacao de Rua Sansao Alves dos Santos, 76 - 4 andar - Brooklin Novo, Sistemas Ltda. Private $7,500,000 $5,625,000 75% Sao Paulo, SP, 04571-090, Brazil www.iastech.com.br

58. Industrial Automation Group 55 Private $7,400,000 $5,600,000 76% 1340 Coldwell Ave., Modesto, CA, 95350, USA www.automationgroup.com

59. Integro Technologies Corp. 38 Private $5,500,000 $5,500,000 100% 305 N. Lee St., Salisbury, NC, 28144, USA www.integro-tech.com

60. Booth Welsh Private $22,700,000 $5,150,000 23% First Ave., Stevenston Industrial Estate, Ayrshire, KA20 3LR, Scotland www.boothwelsh.co.uk

61. Advanced Integration

Group Inc. 53 Private $7,082,560 $5,052,000 71% 1 McCormick Rd., McKees Rocks, PA, 15136, USA www.advancedintegrationgroup.net

62. Industrial TurnAround Corp. (ITAC) Private $42,000,000 $4,600,000 11% 13141 N. Enon Church Rd., Chester, VA, 23836, USA www.itac.us.com

63. Nexjen Systems LLC 76 Private $5,500,000 $4,500,000 82% 5933 Brookshire Blvd., Charlotte, NC, 28216, USA www.nexjen.com

64. Cogent Industrial Unit 180 - 13091 Vanier Pl.,

Technologies Ltd. Private $4,400,000 $4,400,000 100% Richmond, British Columbia, V6V 2J1, Canada www.cogentind.com

65. Phantom Technical Services Inc. Private $3,896,536 $3,896,536 100% 111 Outerbelt St., Columbus, OH, 43213, USA www.PhantomTechnical.com

66. Custom Controls Technology Inc. 84 Private $4,275,250 $3,785,900 89% 705 W. 20th St., Hialeah, FL, 33010, USA www.customcontrol.net

67. Mikro Kontrol Doo. Private $7,800,000 $3,600,000 46% Vase Pelagica 30, Belgrade, 11040, Serbia www.mikrokontrol.rs

68. Electro Controles del Boulevard Paseo Rio Sonora Sur No. 69, Noroeste, S.A. de C.V. Private $19,400,000 $3,560,000 18% Hermosillo, Sonora, 83270, Mexico www.ecn.com.mx

69. Mertek Solutions Inc. Employee $4,000,000 $3,500,000 88% 3913 Hawkins Ave., Sanford, NC, 27330, USA www.merteknc.com

70. Optima Control Solutions Ltd. Private $3,336,000 $3,336,000 100% Blakewater Rd., Blackburn, Lancashire, BB1 5QR, U.K. www.optimacs.com

71. Trimax Systems Inc. Private $5,199,518 $3,328,239 64% 565 Explorer St., Brea, CA, 92821, USA www.trimaxsystems.com

72. Machine Vision Consulting Inc. 64 Private $3,200,000 $3,200,000 100% 69 Milk St., Ste. 217, Westborough, MA, 01581, USA www.machinevc.com

73. Loman Control Systems Inc. 68 Private $3,900,000 $3,128,000 80% 143 E. 28th Division Hwy., Lititz, PA, 17543, USA www.lomancsi.com

74. Aaron Associates of Connecticut Inc. 74 Private $3,330,000 $3,000,000 90% 478 W. Main St., Waterbury, CT, 06723, USA www.aaronct.com

75. Industrial Process Group LLC Private $3,738,644 $2,845,185 76% 111 E. Mildred St., Logansport, IN, 46947, USA www.indpg.com

76. Pro-AT BV Private $3,200,000 $2,800,000 88% Kubus 70, Sliedrecht, Zuid-Holland, 3364 DG, Netherlands www.pro-at.nl

2013

rank

Compa

ny na

me

2012

rank

*

Owne

rship

type

Perce

ntage

of re

venu

e

fro

m syste

m integ

ration

Corp

orate

addr

ess

Web ad

dres

s

Total

gros

s rev

enue

for

� s

cal y

ear (

$ US

)

Total

syste

m integ

ration

rev

enue

( $ US

)

2013 SI Giants (by system integration revenue)

Private/

77. Process Plus LLC 87 Employee $16,100,000 $2,660,757 17% 1340 Kemper Meadow Dr., Cincinnati, OH, 45240, USA www.processplus.com

78. River Consulting LLC 97 Private $27,392,098 $2,591,479 9% 445 Hutchinson Ave., Ste. 740, Columbus, OH, 43235, USA www.riverconsulting.com

79. Adaptive Resources Inc. Private $3,500,000 $2,500,000 71% 104 Broadway St., Carnegie, PA, 15106, USA www.adaptiveresources.com

79. Synergy Systems Inc. 67 Private $3,100,000 $2,500,000 81% 1982 Ohio St., Lisle, IL, 60532, USA www.synsysinc.com

81. Control Associates Inc. Employee n/a $2,400,000 n/a 20 Commerce Dr., Allendale, NJ, 07401, USA www.control-associates.com

82. Jordan Engineering Inc. Private $2,316,361 $2,316,361 100% 4516 Mountainview Rd., Beamsville, Ontario, L0R 1B3, Canada www.jordansynergist.com

83. Kaier Engineering Private $3,000,000 $2,250,000 75% 106 Commerce Blvd., P.O. Box 503, Lawrence, PA, 15055, USA www.kaier.net

84. Next Automation -

Focus Solution Group Employee $3,600,000 $2,200,000 61% Av Angelica 2223, São Paulo, 01227-20, Brazil www.nextautomation.com.br

84. The Fitch Company Private $4,100,000 $2,200,000 54% 631 Hammond St., Bangor, ME, 04401, USA www.� tchcompany.com

86. Smith Controls Private $2,900,000 $1,980,000 68% 1839 Route 9H, Hudson, NY, 12534, USA www.smithcontrols.net

87. George T. Hall Co. Inc. 81 Private $15,500,000 $1,900,000 12% 1605 Gene Autry Way, Anaheim, CA, 92805, USA www.georgethall.com

88. Apex Manufacturing Solutions 63 Private $1,963,747 $1,842,730 94% 408 E. Parkcenter Blvd., Ste. 200, Boise, ID, 83706, USA www.apexmfgsolutions.com

89. CQS Innovation Inc. Private $2,300,000 $1,650,000 72% 2390 Pipestone Rd., Benton Harbor, MI, 49022, USA www.cqsinnovation.com

90. Genesys Controls Corp. Private $3,500,000 $1,500,000 43% 1917 Olde Homestead Ln., Lancaster, PA, 17601, USA www.genesyscontrols.com

91. Automation Engineering 91 Private $6,294,586 $1,434,820 23% 100 North Main, Hackett, AR, 72937, USA www.auto-eng.net

92. NorthWind Technical Services Private $2,600,000 $1,350,000 52% 2751 Antelope Rd., Sabetha, KS, 66534, USA www.northwindts.com

93. Agatos Software Blk 67, Ayer Rajah Crescent, #07-18,

Engineering Pte. Ltd. Private $2,500,000 $1,300,000 52% Singapore, 139950, Singapore www.agatos.com

94. Project S.R.L. Private $1,300,000 $1,000,000 77% Via Don Lorenzo Perosi, 50, Firenze, 50127, Italy www.projectweb.it

95. Plant Werx Pte. Ltd. Private $1,200,000 $960,000 80% 51 Bukit Batok Crescent, #09-02, Singapore, 658077, Singapore www.plantwerx.com.sg

96. Synergetech Co. Ltd. Private $2,000,000 $500,000 25% 31/65 Moo 6 Pracharaj Rd., Taladkwan, Muang, Nonthaburi, 11000, Thailand www.synergetech.com

97. Flow Dynamics and Automation Private $8,000,000 $400,000 5% 1024 11th Court West, Birmingham, AL, 35204, USA www.� owdynamics.net

98. ESR-Systemtechnik GmbH Private $1,950,000 $300,000 15% Waiblinger Strasse 56, Fellbach, 70734, Germany www.esr-systemtechnik.de

99. KCC Software Private $225,000 $225,000 100% 830 Eldorado Ave. SE, Huntsville, AL, 35802, USA www.kccsoftware.com

100. Avison Electrical Private $850,000 $90,000 11% 592 Collins Dr., North Bay, Ontario, P1B 8G3, Canada www.avisonelectrical.com

2013

rank

Compa

ny na

me

2012

rank

*

Owne

rship

type

Perce

ntage

of re

venu

e

fro

m syste

m integ

ration

Corp

orate

addr

ess

Web ad

dres

s

Total

gros

s rev

enue

for

� s

cal y

ear (

$ US

)

Total

syste

m integ

ration

rev

enue

( $ US

)

2013 SI Giants (by system integration revenue)

* 2013 rank could be lower and system integration revenue higher: 65 names are new to the rank-ing in 2013. See the 2012 SI Giants listing at www.controleng.com/giants.

** Control Engineering named three � rms System Integrator of the Year annually since 2007 in three revenue classes; 12 are included here.

After deadline, two � rms asked that their total revenue not be reported. Firms not allowing requested data points will not be included in the 2014 ranking.

Notes

56

ONLINE: More graphics, links to related content at June 2013, www.controleng.com/archiveNot here? Process starts with a listing at www.controleng.com/integrators.System Integrator of the Year deadline is Aug. 1: www.controleng.com/SIY

![GT48 Integrators Manual_P1C[1]](https://static.documents.pub/doc/80x56/577d358c1a28ab3a6b90c114/gt48-integrators-manualp1c1.jpg)