Top 8 Retail Banking Trends and Predictions For 2021 It’s been more than seven months since the coronavirus first made its presence. Lot has changed in these past seven months. And, one thing that is quite evident is life has never been the same since then. With ongoing restrictions, lockdowns, and social distancing – digital ways have become the new norm. Even the so-called self-proclaimed luddites have migrated much of their day-to-day life online. CEO’s and managers who never planned meetings remotely have mastered the art of looking professional from the waist up on Zoom calls. Tenured college professors have let go of the usual ways and started conducting classes virtually. Adding, customers have traded strolling grocery aisles with scrolling through Amazon for all their shopping needs. This sudden and rapid transition to digital ways had a ripple effect on many industries, including the banking and finance industry. As a result of this new shift to digital compulsion, banking customers started to seek the same in-branch experiences in their online interactions. Banks and financial institutions felt tremendous pressure to innovate and provide seamless digital services that

Transcript

Top 8 Retail Banking Trendsand Predictions For 2021It’s been more than seven months since the coronavirusfirst made its presence. Lot has changed in these pastseven months. And, one thing that is quite evident is lifehas never been the same since then.

With ongoing restrictions, lockdowns, and socialdistancing – digital ways have become the new norm.Even the so-called self-proclaimed luddites have migratedmuch of their day-to-day life online.

CEO’s and managers who never planned meetingsremotely have mastered the art of looking professionalfrom the waist up on Zoom calls. Tenured collegeprofessors have let go of the usual ways and startedconducting classes virtually. Adding, customers havetraded strolling grocery aisles with scrolling throughAmazon for all their shopping needs.

This sudden and rapid transition to digital ways had aripple effect on many industries, including the bankingand finance industry. As a result of this new shift to digitalcompulsion, banking customers started to seek the samein-branch experiences in their online interactions.

Banks and financial institutions felt tremendous pressureto innovate and provide seamless digital services that

replicate the same digital experience that a tech companyprovides to stay relevant to current times. As a matter offact, even before Covid-19, tech-shy segments of thepopulation started turning to Fintech apps to managetheir banking needs.

As we advance, even after life returns to “normal,” it islikely that most of the behavioral changes due to thepandemic will persist. Including the ways that customersbank, pay bills, and conduct transactions.

Moreover, many emergent tech companies have big plansto disrupt the industry by providing banking alternativesthat address broader personal finance issues – like payingdown debt, credit saving, and budgeting.

Based on our research and findings, here are eightpandemic-sparked retail banking trends worth keeping aneye on for 2021 and beyond.

Let’s get started.

1. Digital-only banking is looming

The temporary closures or reduced hours of brick-and-mortar bank branches forced many customers todownload their financial institution’s app finally.

According to a CNBC report, “Fidelity National InformationServices (FIS), which works with 50 of the world‘s largestbanks saw a 200% increase in new mobile bankingregistrations in early April, and mobile banking trafficballooned 85%.”

The same report states that among some specific userdemographics, the adoption of Fintech and other digitalservices has soared. For example, many older Americansare now more comfortable paying bills online over the pastsix months to eight months. In the pre-pandemic times,according to the Financial Health Network study in2019, “two-thirds of smartphone users over the age of 50were reluctant to use their devices for their banking

Though there is no official verdict on how these numbershave changed in 2020, the earlier studies suggest thatBaby Boomers’ mindsets were shifting even before thepandemic.

Another study by the National Retail Federation statedthat nearly half (45%) of Baby Boomers are shoppingonline more due to the pandemic.

Key takeaways:

Digital banking or digital-only bank is part of thebroader context for moving to online banking, wherebanking services are delivered over the internet

Digital-only banks are looming for several reasons;one of the primary reason is convenience As a result of digital-only banks, visits to traditionalbrick and mortar banks will drop by nearly 40% Still, traditional banks will have the edge over digitalbanks when customers need to settle ongoingproblems by visiting the nearest bank location

2. Rapid adaptation of Blockchain byRetail Bankers

Traditional money transfer solutions have beenproblematic in both the B2B and P2P areas, plagued byslow transfer times and high costs.

The clearing firms involved in the transactions haveindependent processing systems. Each party involved inthat process will keep their own copy of that record of agiven transaction, making it stringent.

The lack of standardization between these bodies andcorrespondent banks means that costs are high, andsettlement periods are longer. But, thanks to Blockchain.

Blockchain has the potential to solve these challenges byoffering faster transaction times, more transparency, andlower costs, changing the money transfer equation.

According to Forbes, Blockchain brings the followingbenefits:

Blockchain records and validates every transaction. Blockchain does not require third-partyauthorization. Blockchain is decentralized.

Another benefit from Blockchain that has got largebanks excited is keeping track of trades and bonds orstocks by ensuring that the payments are correctlymade.

At present, this is a complex process involving banks,traders, exchanges, clearinghouses, and others. It takestwo days to verify the seller and buyers and then arrangethe movement of funds. But, with Blockchain, all this workcan be done in minutes.

Key takeaways:

Blockchain is still a new technology and will soonbecome the future of banking

Blockchain is a powerful and secure technology forthe banking sector as security is of utmostimportance for the financial domain It is worth considering for Payment processing firms,Stock Exchange and Share Trading, Accounting,

With financial institutions revenues exceeding theincomes of nations, it comes as no surprise that they arethe first to embrace A.I. and Data Science technologies.Of all other advanced technologies, bankers and leadersin the banking industry firmly believe that ArtificialIntelligence will be game-changing.

Banks and financial institutions are further fine-tuningtheir A.I. solution strategies to strengthen overall portfoliomanagement.

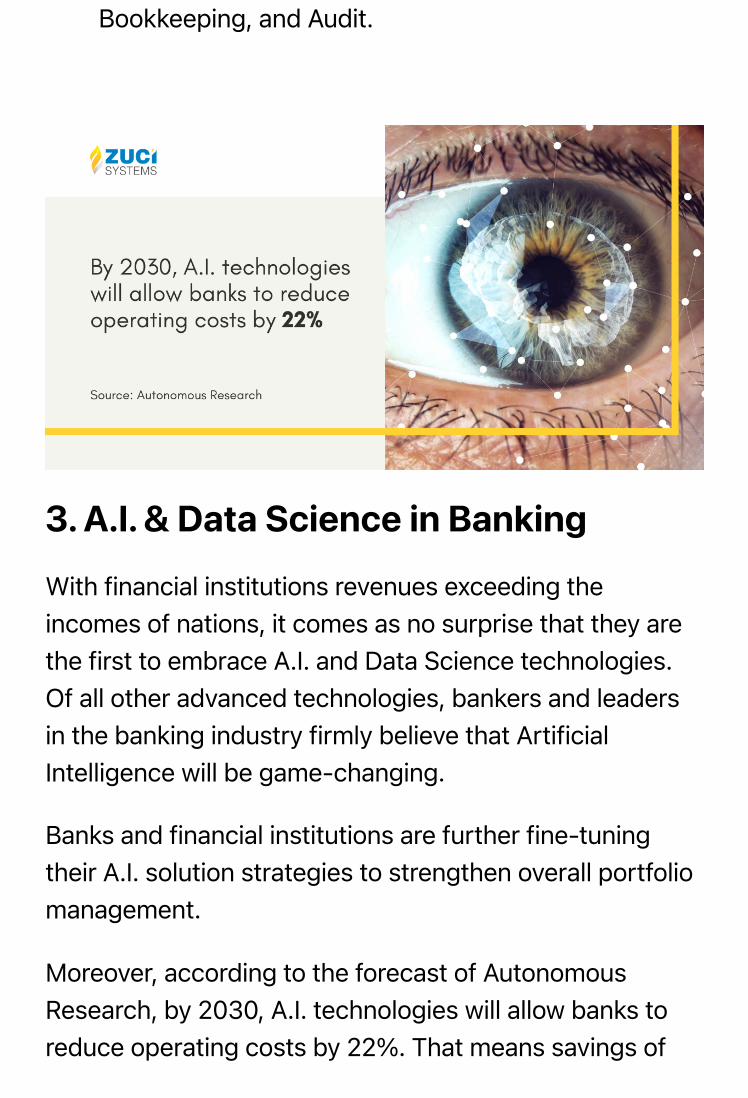

Moreover, according to the forecast of AutonomousResearch, by 2030, A.I. technologies will allow banks toreduce operating costs by 22%. That means savings of

financial institutions can reach to $1 trillion in the longrun.

However, the path to this outlook is not straightforward. Areport from Tencent Research Institute states there areonly 300,000 AI researchers and practitioners worldwide,with the market demanding millions of jobs to bridge theskills gap.

Key takeaways:

With its efficiency to work with unstructured data, A.I. iswell poised to deal with the rising incidence ofcybercrimes, financial fraud threats, and lots more. Someof the ways A.I. & Data Science can be used in banks are:

Fraud Preventions: Such as identity thefts & creditcards schemes Anomaly Detection: In detecting illegal insidertrading

Customer Analytics: Predicting customer behavioraltrends for strategizing the right marketing mix Risk Management: Minimizing human error byidentifying and predicting market trend, competition,customer creditworthiness, and customer loyalty Algorithmic Trading: High precise trades on themarket using a machine learning algorithm byreducing human errors

Banks & financial institutions with extensive customerdata can construct better models and get ahead of thecompetition.

4. Cyber-Security will be a top priority

The banking and financial sector is one of the heavilyregulated industries in the world. Banks and financialinstitutions have always been at the forefront of enterprisecybersecurity. The enormous stores of cash andconsumer data make them a top target for hackers. Thethreat of financial losses, regulatory consequences, andreputational damage has spurred them to innovate andaccelerate the field of cybersecurity.

Financial services executives are already depressinglyfamiliar and aware of the impact of cyber-threats on theindustry.

According to the PWC report, “69% of financial services’CEOs reported that they are either somewhat orextremely concerned about cyber-threats, compared to61% of CEOs across all sectors.“

In the digital banking age, one area that regulators wouldscrutinize closely is banks and financial institutions’ dataownership. Nations will address this question at their ownpace.

The ideal outcome is a set of national standardscomprehensive enough to calm businesses andconsumers’ nerves.

Key takeaways:

With the COVID-19 outbreak, cybercriminalsincreasingly are targeting organizations that nowhave more remote workers and fewer I.T. andsecurity, staff A well-defined security policy serves as a crucial roadmap for any bank I.T. team to maintain a trulyadaptive security architecture going forward Lastly, banks must continuously monitor theirnetwork for changes to configurations and ensurethat these changes are approved and compliant withpolicy

5. Open banking API’s

Before open banking and the rise of Fintech, most banksdid not extract any real value from the expensivecustomer data they held.

With Fintechs making waves in the finance and bankingindustries and open banking being a key factor propellingthem to the forefront in the banking industry,banks have to look for ways to infiltrate and conquer.

In the process, most banks realized that instead ofcompeting directly against Fintech and third-partyinstitutions, retail banks could leverage open banking topartner with the newer players instead, therebyremaining competitive in the rapidly evolving industry.

That said, Open banking is a secure way to have morecontrol over what matters to your customers. There ismoney, but it’s also your customers’ financial data.

Combining these two elements gives customers thefreedom to opt-out if they feel obligated and provide morepersonalized services for those interested.

According to Allied Market Research, “Open banking isreported to have generated $7.29 billion in 2018 and isexpected to reach $43.15 billion by 2026.”

To realize the full potential of open banking, the APIs arecritical in exposing the banking data to third parties. Notevery third party can have access to your customers’banking information. Indeed, PSD2 has identified twotypes of third-party providers.

AISP: Account Information Service Providers

AISP is a business that uses customer account data toprovide services such as aggregating financial informationin one place, tracking their spending, or planning theirfinance.

PISP: Payment Initiation Service Providers

PISP is a company that initiates additional payment onbehalf of the customer directly from their bank account,offering an alternative to debit and credit cards.

relationships and business models. But there is alsoan opportunity for incumbent banks by using theircurrent advantage of brand and customer base toprovide these aggregator services themselves. Thebanking landscape is changing, and it’s time toexplore open banking now.

6. Payment innovations

The concept of Instant Payment has become highlyimportant in both consumer and B2B payment areas,where settlement time has really been a challenge earlier.

The term “Instant Payment” refers to the ability to makepayments within a matter of seconds, which in turn will behighly beneficial for both parties throughout the paymentlandscape.

As we advance, mobile wallets will replace physicalwallets – a wallet with customer’s credit cards, rewardscards, and much more. In 2019 alone, there were alreadyabout 2.1 billion mobile wallet users.

As a result, Instant payments have become an integralpart of both financial institutions and regulators, driven bykey success stories in early deployments.

The SEPA (Single Euro Payments Area) scheme in theE.U. has significantly brought down settlement times,and the SEPA Instant Credit Transfer Scheme furtherreduced it. In SEPA Instant, the payment will be received in amatter of 10 seconds, which is dramatically fasterthan traditional methods. However, still much morework needs to be done. Adding, the U.S. Federal Reserve hasannounced FedNow. This service will processindividual credit transfers valued at $25000 or lesswithin seconds. But this service will not launch until2021.

Key takeaways:

Instant payment schemes will accelerate and focus oninternational interoperability in 2021, enabled bystandardization with ISO 20022 and cross-borderschemes. This will allow banks and financial services toupgrade to:

Faster and simpler accounts payable/receivableprocesses Less complicated B2B payment systems Increased payment volume for payment processors

Digital wallets, mobile payments will drive paymentinnovations from now on

In order to achieve these benefits, banks will need toupdate their systems because the whole chain needs tosupport the instantaneousness of payments.

7. From competitors to collaborators

Even though the industry is shifting towards convenienceand superior customer experience usingtechnology, it’s still a long way to go. The Fintech firms arestill only getting a slice of the entire banking

customers.

Both old and new financial players have something or theother to offer that each lacks in the long run. Thepartnership model is what each says is the best,but it‘s riddled with challenges.

But the value of FinTechs is in bringing new things to thebank – a new segment of customers the bank could notaccess earlier, or a new service to existing customers, or anew way to approach existing problems and workflows.

According to the CNBC report, US-based CBW Bank haspartnered with fintech Moven to provide real-time insightsto their users. And, Visa announced a Fintech partnershipto help companies eliminate $33 trillion in paper checks.

How far is this collaboration trend goingforward? According to PwC, “82% of current financialservice providers will be increasing partnerships withinthe next five years.“

Key takeaways:

Recognizing the need to work together, fintechstartups and established names will redefine thebanking and financial landscape Old names in the financial sector will opt to invest infintech startups to gain a foothold in the rising

Tech firms like Apple, Google & Samsung have beenproviding payment services for several years now, and fewhave started to coalesce to accelerate their financialservices movement.

The primary reason is the decreasing financial brandloyalty due to open banking, which has loosened the ropethat banks have on their customer data. Many countriesare mandating a streamlined switching service to movefrom one bank to another much more quickly.

Most importantly, banks have a limited ability to retaintheir users compared to traditional ones. Simultaneously,

technology companies have always had much moresuccess in developing in a closed ecosystem. And theyare now looking to bring finance under their banner.

Key takeaways:

With Apple Card showing its prominence. AndGoogle, Stripe, and PayPal are preparing to start orexpand banking and payment-related offerings. Theindustry is already shaken. Open Banking tools made available from PSD2guidelines give these companies the ability to bebank-like without banks.

We think that the partnership between banks and techcompanies are more likely than tech companies outrightbecoming banks.

Instead of viewing big tech companies as a threat,banking and financial institutions should embracepartnerships and collaboration with them.

The Bottom Line

The world has digitized, and your customers are seekinglow friction and immediacy over slower traditional ways ofbanking.

Moreover, when we look at banking as an industry andhow it has developed, you will understand that it’s not justabout inserting technology into banking. There is abroader shift here – and a significant part of the shift isaround the bank’s trust and utility.

Lastly, in order to sustain this banking transformation,listen to your customers, earn their trust by creatingtransparent and seamless experiences, respect their needfor privacy, look out for industry trends, and alwayschoose to make tech investments to align the recenttechnological developments with what people want.