23

Macroeconomics in the Global Economy Session 3. The Open Economy Trade and Capital Flows Balance of Payments Saving, Investment and the Current Account

Macroeconomics in the Global Economy

Session 3. The Open Economy

Trade and Capital Flows

Balance of Payments

Saving, Investment and the Current Account

Macroeconomics in the Global Economy

1. Trade Flows

020406080

100120140160180

Singapore Ireland Mexico Italy Turkey Japan USA Brazil

% o

f GD

P

Exports Imports

2015

Macroeconomics in the Global Economy

3. Capital Flows

Foreign Direct Investment. Involves significant ownership in foreign company or establishment of foreign operations.

Portfolio investment: foreign debt and equity (without control).

Change in official (foreign) reserves: portfolio investment under the control of the government or central bank.

2. Income Flows: Net Factor Payments

Worker’s remittances

Unilateral government transfers.

Repatriation of profits.

Macroeconomics in the Global Economy

Exports (+)

Imports (-)

Net factor payments

Current Account Capital and Financial Account

Changes in foreign reserves**

Change in domestic holdings of foreign assets

Change in foreign holdings of domestic assets

Acquisition (-)Sale (+)

Acquisition (+)Sale (-)

Acquisition (-)Sale (+)

Balance of payments: stylized version

** See definition in next slide

Macroeconomics in the Global Economy

Foreign Reserves

Foreign (Official) Reserves: Liquid assets owned by the monetary authority (or government) for international payments, liquidity needs, foreign exchange intervention, current account crisis.

Traditionally Foreign Reserves only included cash, foreign bank deposits and foreign government securities.

As foreign reserves grew fast in the last 15 years, these assets get treated as any other investment. Sovereign Wealth Funds take over the management of these assets. Assets become illiquid.

There is therefore some uncertainty about what qualifies as “foreign reserves” when you compare countries’ balance of payments.

Macroeconomics in the Global Economy

A country’s balance of payments accounts keep track of both its payments to and its receipts from foreigners.

All transactions produce two records of opposite sign and the balance is always zero:

Current account + Capital and Financial Account = 0

For example, a current account deficit can be financed by either

In all cases these changes appear as a surplus in the Capital and Financial Account.

FDI inflow orBorrowing from foreigners orSale of foreign assets orDecrease of foreign reserves

Balance of Payments: A Balanced Imbalance

Macroeconomics in the Global Economy

Exports of goods (+)Imports of goods (-)

Goods Trade Balance

Exports of services (+)Imports of services (-)

Services Trade Balance

Net exports

Net Factor Payments

Current Account

Other financial flows

Change in Foreign Reserves

Foreign direct investment

Private Capital Flows

223

15

238

287

-472

186

Negative numbers mean an increase in reserves!

-185Capital and Financial AccountErrors and Omissions -53

Balance of PaymentsChina 2010 – Billions USD

101

246

-23

Macroeconomics in the Global Economy

Exports of goods (+)Imports of goods (-)

Goods Trade Balance

Exports of services (+)Imports of services (-)

Services Trade Balance

Net exports

Net Factor Payments

Current Account

Other financial flows

Change in Foreign Reserves

Foreign direct investment

Private Capital Flows

385

-54

331

-485

342

62

Positive numbers mean a decrease in reserves!

-143Capital and Financial AccountErrors and Omissions -188

Balance of PaymentsChina 2015 – Billions USD

-547

567

-182

Macroeconomics in the Global Economy

In an open economy saving does not need to be equal to investment:

GDP = C + G + I + NX(GDP+NFP) - C – G = I + (NX + NFP)

S = I + CA, or(Sprivate- Iprivate) + (Sgovernment – Igovernment)= CA

As an example: An increase in the government budget deficit must be accompanied by:

An increase in private saving orA decline in investment orA current account deficit

Saving, Investment and the Current Account

Macroeconomics in the Global Economy

(SPrivate- IPrivate) + (SGovernment – IGovernment) = CASaving, Investment and the Current Account

(% of GDP) Private SectorBalance

GovernmentBalance

CurrentAccount

2007 United States -2.2 -2.8 -5.0

Japan 7.0 -2.1 4.9

Greece -7.7 -6.7 -14.4

2012 United States 5.6 -8.3 -2.7

Japan 11.1 -10.1 1.0

Greece 2.9 -6.3 -3.4

2016 United States 1.6 -4.1 -2.5

Japan 8.9 -5.2 3.7

Greece 3.4 -3.4 0

Macroeconomics in the Global Economy

-16

-12

-8

-4

0

4

8

12

1960 1965 1970 1975 1980 1985 1990 1995 2000 2005 2010 2015

(% o

f GD

P)

Current Account Govt. Budget balance Net private saving

Saving, Investment and the Current Account (US)

Macroeconomics in the Global Economy

r

Saving, Investment

Investment

Saving

WorldReal interestrate

CA surplus

Saving and Investment in a Small Open EconomyCountries with excess saving (relative to investment) run current account surpluses. Remember that when S > I, it means that spending (C + I +G) is smaller than income (GDP+NFP).

Macroeconomics in the Global Economy

r

Saving, Investment

Investment

Saving

WorldReal interestrate

CA deficit

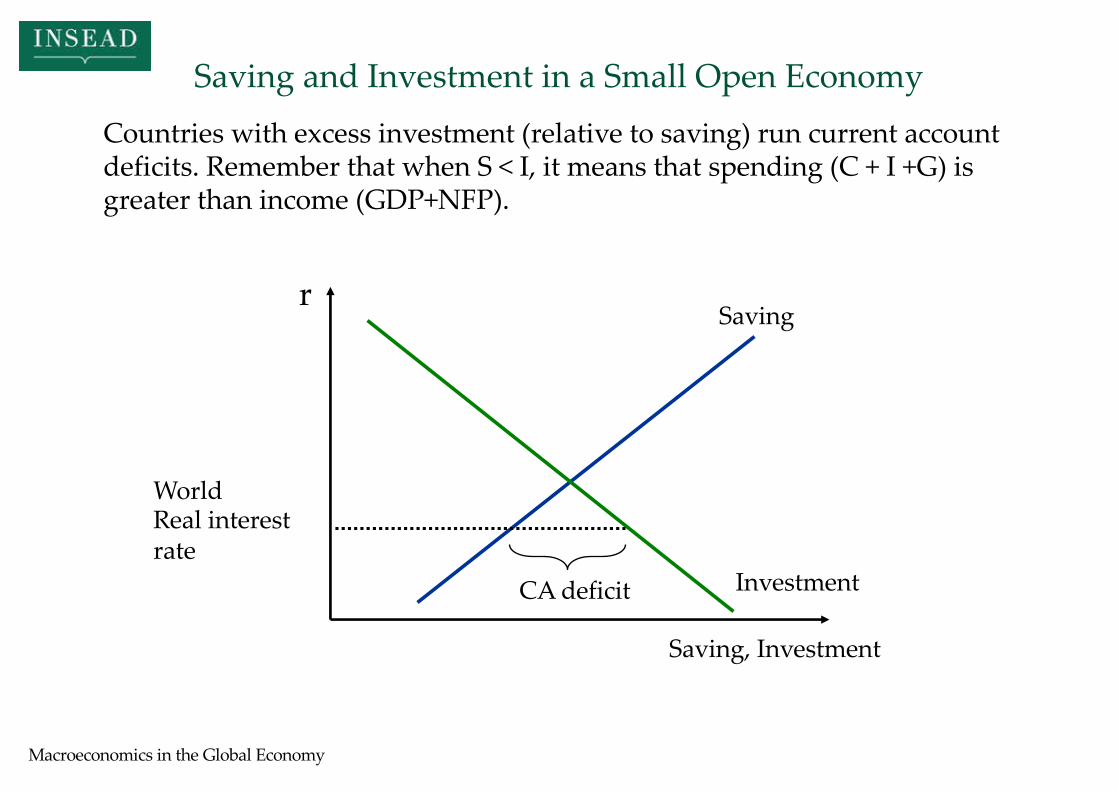

Saving and Investment in a Small Open EconomyCountries with excess investment (relative to saving) run current account deficits. Remember that when S < I, it means that spending (C + I +G) is greater than income (GDP+NFP).

Macroeconomics in the Global Economy

r

Saving, Investment

Investment

Saving

WorldReal interestrate

CA surplusr

Saving, Investment

Investment

Saving

CA deficit

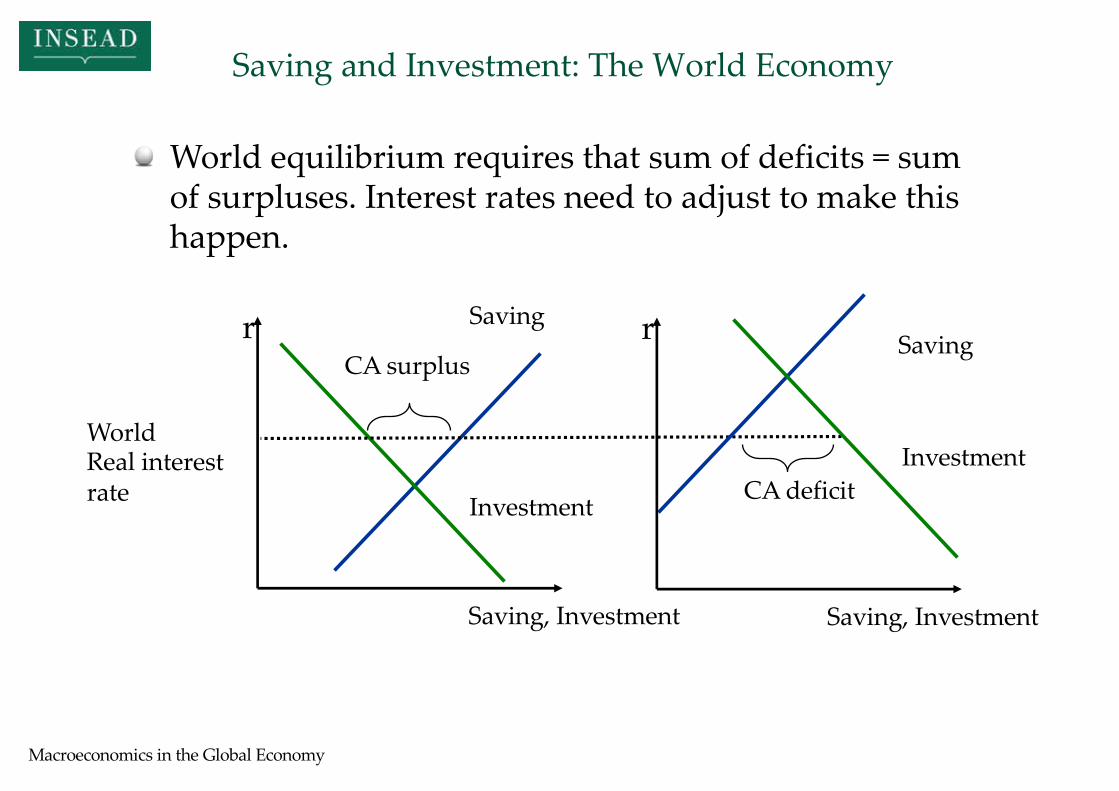

Saving and Investment: The World Economy

World equilibrium requires that sum of deficits = sum of surpluses. Interest rates need to adjust to make this happen.

Macroeconomics in the Global Economy

r

Saving, Investment

Investment

Saving

Real interestrate (1990s)

CA surplusr

Saving, Investment

Investment

Saving

CA deficit

Real interestrate (2000s)

Saving (New)

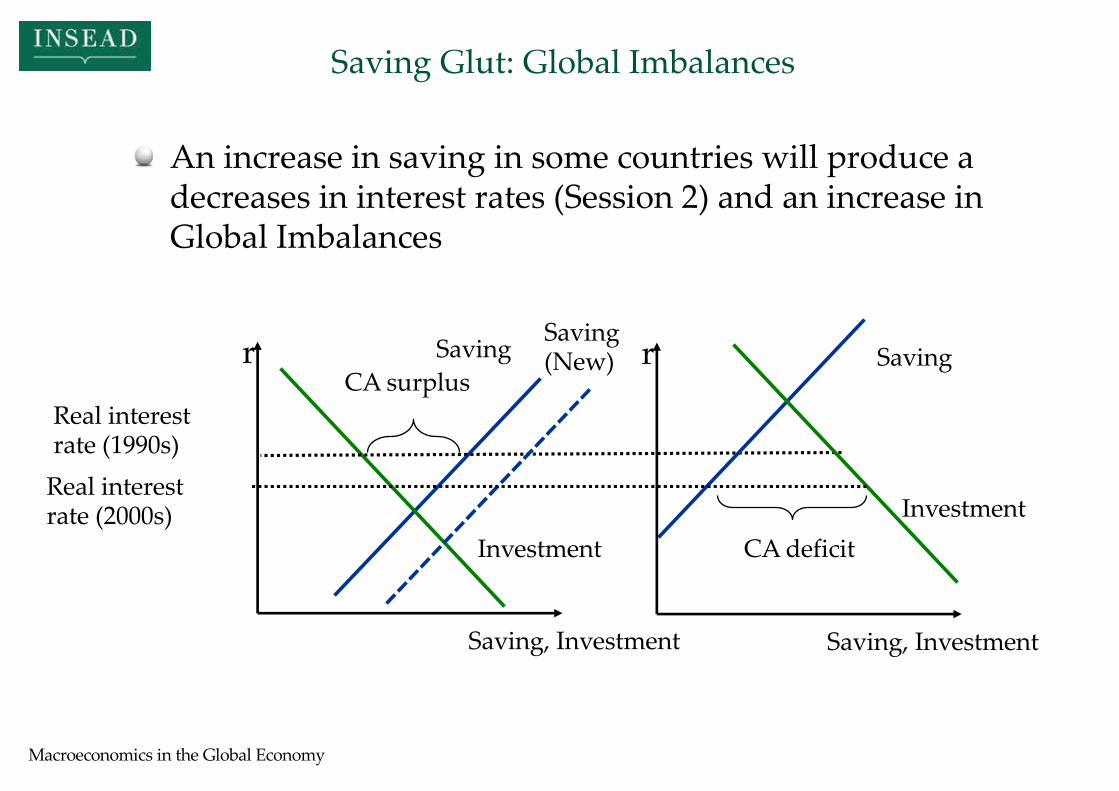

Saving Glut: Global Imbalances

An increase in saving in some countries will produce a decreases in interest rates (Session 2) and an increase in Global Imbalances

Macroeconomics in the Global Economy

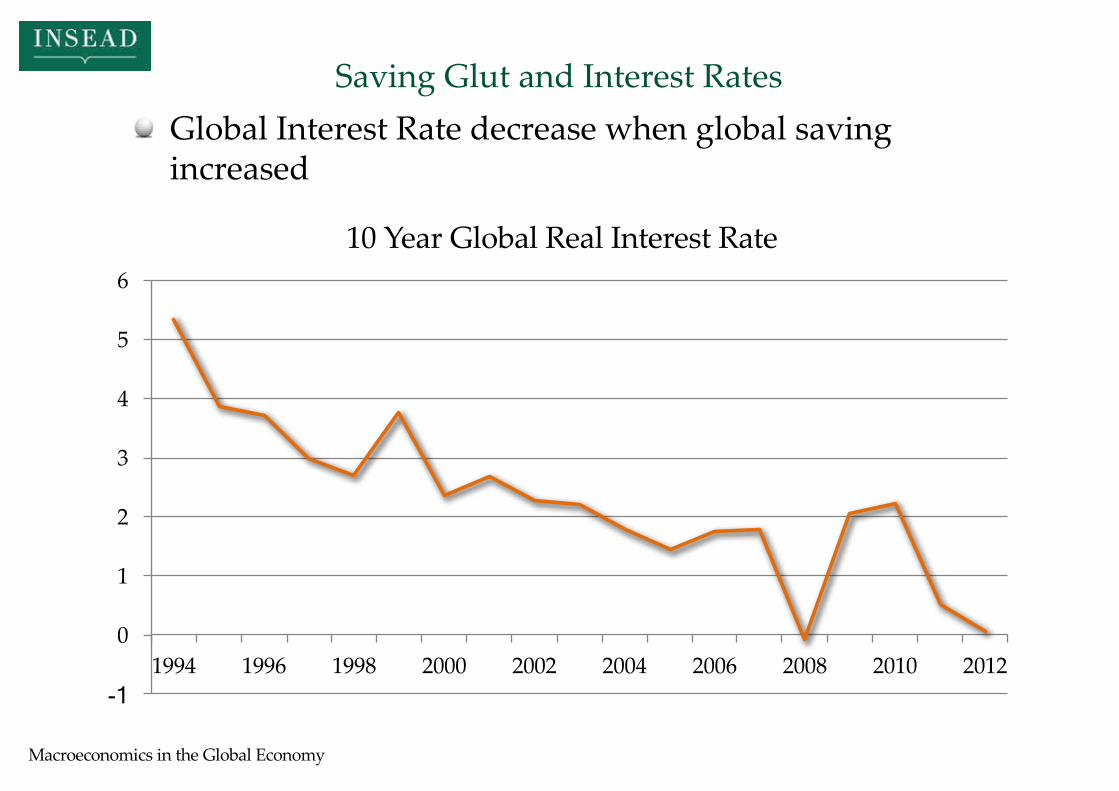

Saving Glut and Interest Rates

-1

0

1

2

3

4

5

6

1994 1996 1998 2000 2002 2004 2006 2008 2010 2012

10 Year Global Real Interest Rate

Global Interest Rate decrease when global saving increased

Macroeconomics in the Global Economy

-3

-2

-1

0

1

2

3

1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007

Cur

rent

Acc

ount

as %

of W

orld

GD

P

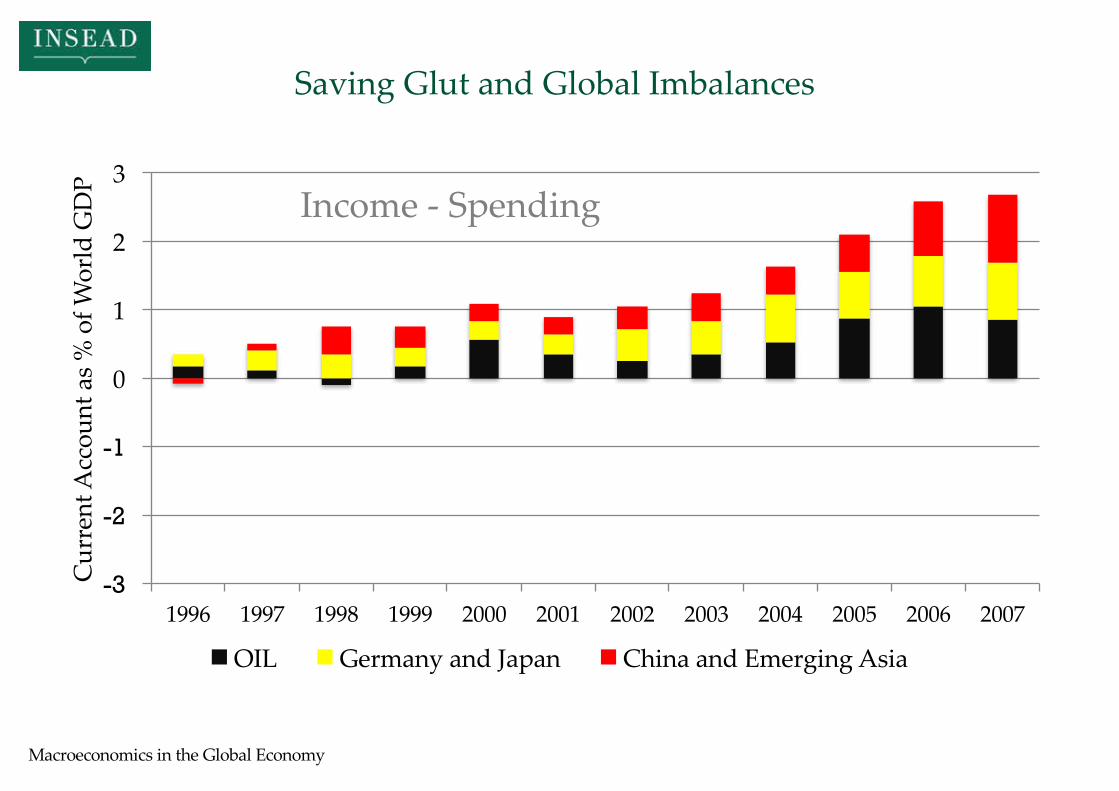

OIL Germany and Japan China and Emerging Asia

Income - Spending

Saving Glut and Global Imbalances

Macroeconomics in the Global Economy

-3

-2

-1

0

1

2

3

1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007

Cur

rent

Acc

ount

as %

of W

orld

GD

P

US Europe Deficit

Income - Spending

Europe Deficit: Bulgaria, Greece, Hungary, Ireland, Portugal, Spain, UK,…

Saving Glut and Global Imbalances

Macroeconomics in the Global Economy

-3

-2

-1

0

1

2

3

419

96

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

Cur

rent

Acc

ount

as %

of W

orld

GD

P

US Europe Deficit OIL Ger and Jap China and Em. Asia Others

Income - Spending

Saving Glut and Global Imbalances

Macroeconomics in the Global Economy

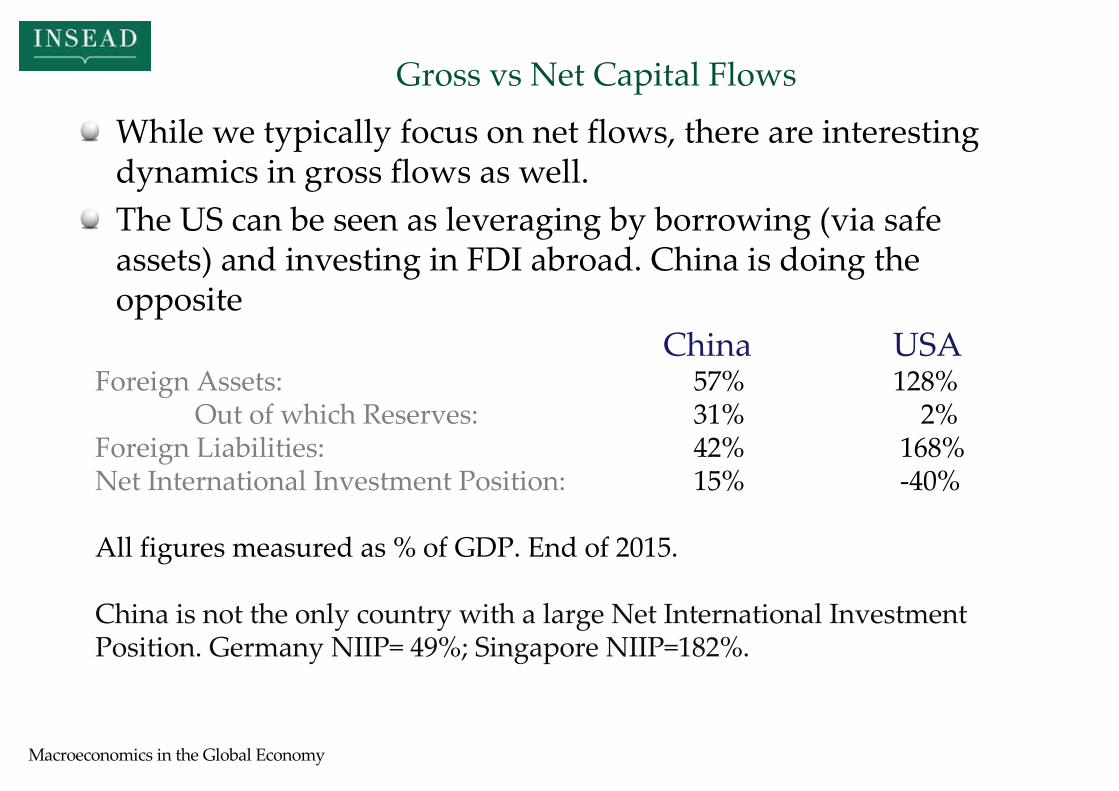

Gross vs Net Capital Flows

China USAForeign Assets: 57% 128%

Out of which Reserves: 31% 2%Foreign Liabilities: 42% 168%Net International Investment Position: 15% -40%

All figures measured as % of GDP. End of 2015.

China is not the only country with a large Net International Investment Position. Germany NIIP= 49%; Singapore NIIP=182%.

While we typically focus on net flows, there are interesting dynamics in gross flows as well.The US can be seen as leveraging by borrowing (via safe assets) and investing in FDI abroad. China is doing the opposite

Macroeconomics in the Global Economy

Session 3. Summary

Financial transactions and commercial transactions are linked by the balance of payments identity.

Current Account balance must match Capital and Financial Account balance.

In an open economy Saving – Investment = Current Accountbalance. The interest rate is determined by the rest of the world.

Saving Glut caused both a decrease in interest rates and an explosion of global imbalances. Both phenomena are related.

Macroeconomics in the Global Economy

v Example:

Nikon (a Japanese company) sells to a US customer a digital camera for $1000. Suppose the buyer pays by depositing a check to the US-based account of Nikon. Then the transaction is recorded in Japan’s Balance of Payments as:

Export of goods for 1000 USD Purchase of a foreign asset 1000 USD

CURRENT ACCOUNT: +1000 CAPITAL and FIN. ACCOUNT: -1000

Appendix: Balance of payments: Examples

Macroeconomics in the Global Economy

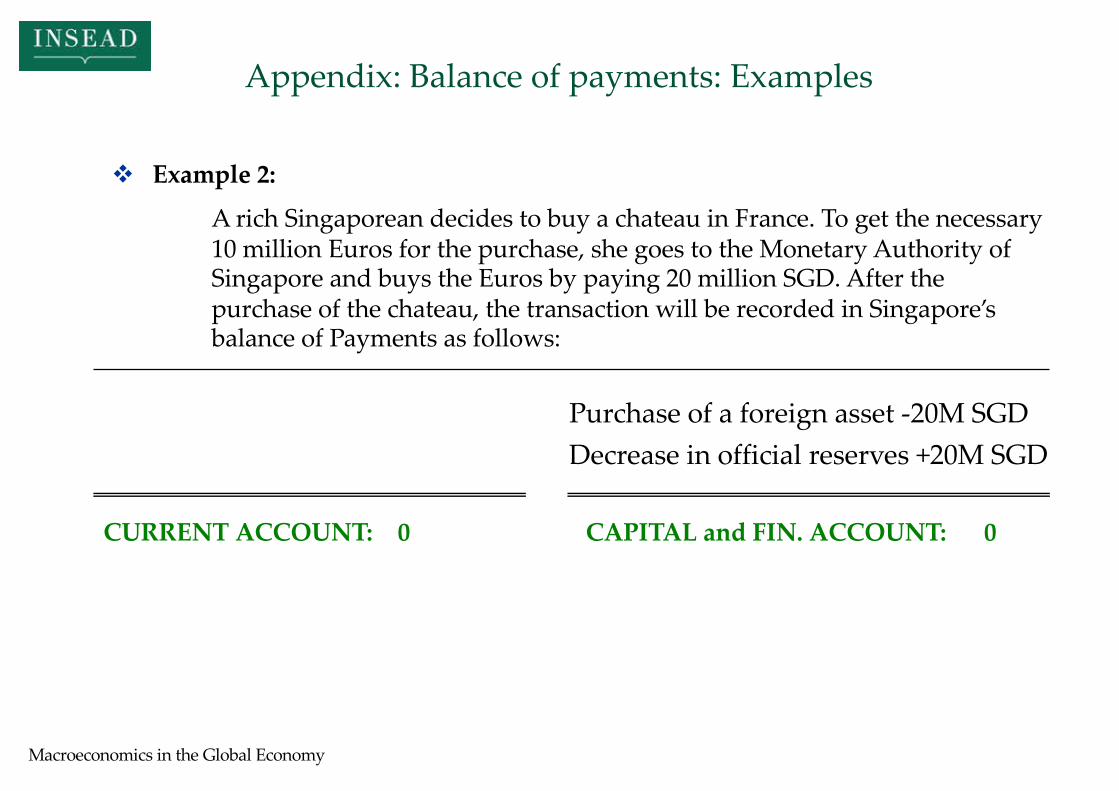

v Example 2:

A rich Singaporean decides to buy a chateau in France. To get the necessary 10 million Euros for the purchase, she goes to the Monetary Authority of Singapore and buys the Euros by paying 20 million SGD. After the purchase of the chateau, the transaction will be recorded in Singapore’s balance of Payments as follows:

CAPITAL and FIN. ACCOUNT: 0

Purchase of a foreign asset -20M SGDDecrease in official reserves +20M SGD

CURRENT ACCOUNT: 0

Appendix: Balance of payments: Examples