Transmission of Sovereign Risk in the Euro Crisis * Filippo Brutti † University of Zurich Study Center Gerzensee Philip Saur´ e ‡ Swiss National Bank January 2013 Abstract We assess the role of financial linkages in the transmission of sovereign risk in the Euro Crisis. Building on the narrative approach by Romer and Romer (1989), we use financial news to identify structural shocks in a vector autoregressive model of daily sovereign CDS premia for eleven European countries. To estimate how these shocks transmit across borders, we use data on cross-country bank exposures to sovereign debt. Our results indicate that cross-border financial exposures constitute important transmission channels. A 10-percent decrease in the exposure to Greek debt reduces, on average, the transmission rate of sovereign risk by 9.4 percent. Decomposing these effects, we find that exposures to sovereign constitute significant transmission channels, while we find no robust support for transmission through bank-to-bank lending. Keywords: Cross-country Transmission, Sovereign Risk, Financial Linkages, Euro Crisis, Narrative Approach JEL Classification: F36, F42, F21, C30 * We would like to thank Nathan Foley-Fisher, Matthias Gubler, Sylvia Kaufmann, Christian Kascha, Carlos Lenz, Dirk Niepelt and Fabrizio Zilibotti. We are also grateful to seminar participants at the Study Center Gerzensee, Swiss National Bank, University of Konstanz, University of Lausanne and University of Zurich for comments and suggestions. Filippo Brutti gratefully acknowledges financial support from the European Research Council (ERC Advanced Grant IPCDP-229883). The views expressed in this paper are the authors’ views and do not necessarily represent those of the Swiss National Bank. † Email: fi[email protected]‡ Email: [email protected]. 1

Transcript

Transmission of Sovereign Risk in the Euro Crisis∗

Filippo Brutti†

University of ZurichStudy Center Gerzensee

Philip Saure‡

Swiss National Bank

January 2013

Abstract

We assess the role of financial linkages in the transmission of sovereign risk in theEuro Crisis. Building on the narrative approach by Romer and Romer (1989), we usefinancial news to identify structural shocks in a vector autoregressive model of dailysovereign CDS premia for eleven European countries. To estimate how these shockstransmit across borders, we use data on cross-country bank exposures to sovereigndebt. Our results indicate that cross-border financial exposures constitute importanttransmission channels. A 10-percent decrease in the exposure to Greek debt reduces,on average, the transmission rate of sovereign risk by 9.4 percent. Decomposingthese effects, we find that exposures to sovereign constitute significant transmissionchannels, while we find no robust support for transmission through bank-to-banklending.

Keywords: Cross-country Transmission, Sovereign Risk, Financial Linkages, EuroCrisis, Narrative Approach

JEL Classification: F36, F42, F21, C30

∗We would like to thank Nathan Foley-Fisher, Matthias Gubler, Sylvia Kaufmann, Christian Kascha,Carlos Lenz, Dirk Niepelt and Fabrizio Zilibotti. We are also grateful to seminar participants at the StudyCenter Gerzensee, Swiss National Bank, University of Konstanz, University of Lausanne and University ofZurich for comments and suggestions. Filippo Brutti gratefully acknowledges financial support from theEuropean Research Council (ERC Advanced Grant IPCDP-229883). The views expressed in this paperare the authors’ views and do not necessarily represent those of the Swiss National Bank.†Email: [email protected]‡Email: [email protected].

1

1 Introduction

In late 2009, with the global economy inching out of the Great Recession, the sovereign

debt crisis hit Europe with a remarkable pace and vigor. Fears of sovereign insolvency

initially developed in one peripheral country, Greece, but quickly spread to other European

countries, forcing policymakers to take bold actions in order to stop the contagion.

Financial turmoil can spread across countries through different channels. We recognize

that the public debate about contagion in the Euro crisis has repeatedly stressed the im-

portance of financial linkages across the involved countries and, in particular, of financial

institutions operating across national borders.1 For example, a looming Greek sovereign

default may adversely affect banks in other countries according to their exposure to Greek

sovereign debt. Through implicit guarantees, a troubled national banking system consti-

tutes a liability of the respective sovereign, thereby increasing sovereign credit risk. By the

same token, cross-border interbank lending can matter: as the Greek sovereign debt crisis

stresses the Greek banking system, counterparty risk rises for foreign creditors, affecting

the financial health of the latter’s countries. However, the role played by cross-border ex-

posures of financial institutions for the transmission of shocks is still heavily debated (see

Van Wincoop (2011), among others).

The aim of this paper is to provide empirical evidence to assess the contribution of

cross-border exposures by financial institutions to the transmission of sovereign risk in

Euro Crisis. We distinguish, in particular, between transmission through exposure to public

debt and through cross-border bank linkages. To this end, we identify financial shocks that

originate in Greece and we analyze how the sovereign default risk of European countries,

measured by sovereign Credit Default Swap (CDS) premia, responds to these shocks. We

1Christine Lagarde, Managing Director of the International Monetary Fund, states that “[f]inancialexposures across the continent are transmitting weakness and spreading fear from market to market,country to country, periphery to core.” See also Financial Times: ”Greek contagion fears spread to otherEU banks”, June 15, 2011. For a careful discussion of the role of financial institution for the internationalpropagation of risk see Bolton and Jeanne (2011) and Guerrieri et al. (2012).

2

then use data on bilateral cross-border bank positions from the Bank of International

Settlements (BIS) to relate the responses of other countries to their aggregate exposure to

Greek public debt and debt of Greek banks, while controlling for other factors.

Our results indicate that a one-percent shock to Greek CDS causes a 0.36 percent in-

crease in the CDS of the average European country, which suggests economically important

transmission rates. Moreover, financial linkages contribute significantly to these spillovers.

In particular, a 10-percent decrease in cross-border financial exposures, corresponding to a

reduction of 0.075 percent of GDP for the average country, would decrease the spillover ef-

fects of sovereign risk by 3.4 percent. For the average country, this corresponds to about 9.4

percent of the overall transmission rate. Decomposing these effects, we find that bilateral

exposures to sovereign debt constitute economically and statistically significant transmis-

sion channels. Specifically, a 10-percent decrease in the exposure to foreign sovereign debt,

corresponding to a reduction of 0.05 percent of GDP, would decrease spillover effects by 1.8

percent. Again the average country, this corresponds to 5 percent of the overall transmission

rate. On the contrary, we find no robust support for transmission through bank-to-bank

lending.

Methodologically, we consider a vector autoregressive (VAR) model for country CDS

premia, which includes global financial factors as exogenous variables. We adopt the nar-

rative approach of Romer and Romer (1989) using financial news to identify exogenous

shocks in one country, with a specific focus on information innovations stemming from

Greece (“Greek shocks”). Within this framework, we then estimate whether the response

to Greek shocks varies over time with the exposure to Greek debt, controlling for country

and time fixed effects and within-country variation in trade linkages.2

2We acknowledge that the narrative approach exhibits some commonalities with a classic event-studymethodology, which has been previously applied to study the international transmission of financial crises(e.g., Forbes (2004)). This methodology usually considers a market model to explain the behavior of finan-cial assets during normal times and then compute within a specific event-window a measure of abnormalreturns, defined as the deviation of asset returns from the model predictions. In our study, we are forced

3

The narrative approach has the major advantage that identification is achieved without

imposing a specific pattern for cross-country spillovers on the VAR model. This virtue is

particularly important when analyzing cross-country transmission because standard iden-

tification assumptions, e.g., short-run, long-run or sign restrictions, are difficult to defend

in this context (see Rigobon (2002)). Some concerns need to be addressed, however. Im-

portantly, our estimates of cross-country spillovers might suffer of an endogeneity bias if

simultaneous shocks in other countries or to global factors occurred at the time of Greek

shocks. We have several reasons to think that this is not the case. First, with daily data

the problem of simultaneity is sensibly reduced. Second, we take special care in reviewing

financial news to exclude from our analysis those Greek events that occurred simultaneously

with relevant financial news in other countries.3 Third, by controlling for global financial

factors in the estimation, common shocks that affect sovereign risk through general market

conditions are accounted for.

The classic use of the narrative approach has also been disputed in the past. Romer and

Romer’s (1989) original identification strategy through episodes of monetary contraction

has been criticized. Concerned about reverse causality, Leeper (1997) argues that the

events considered may constitute an endogenous policy response to previous movements in

economic conditions (see Romer and Romer (1997) for a reply).4 Additionally, the effects

of the policy events selected using a narrative approach are said to be indistinguishable

from those of omitted economic fundamentals (Hoover and Perez (1995)). We argue that

these standard lines of critique do not apply to our setup. First, the high frequency of our

to use a VAR model to account for the strong autocorrelation of CDS premia during the Euro Crisis.Additionally, event studies are typically based on a single event-window of extended length rather than ona collection of daily events. Our definition of an event is thus more conservative since a clear identificationof the exact origin of the event is much easier to motivate for short-lived single-day events.

3A detailed description of the data and the selection procedure follows in Section 2.4Leeper (1997) notes that the events that Romer and Romer (1989) use to identify the response to

monetary shocks (contractions of the FED) are predictable by past macroeconomic variables and thatunpredictable changes do not generate responses that look like typical effects of monetary policy. Romerand Romer (1997) argue that the results in Leeper (1997) are due to overfitting.

4

data relieves us of the specific problem of reverse causality mentioned by Leeper (1997):

a daily blip in the CDS premium cannot reasonably be believed to cause major political

action in Greece on the same day (compare Table A1 in the Appendix). Second, unlike

Romer and Romer (1989), we measure the immediate daily response of CDS to the selected

Greek events instead of medium- and long-term effects that could be driven by omitted

macroeconomic fundamentals.5. In addition, we also argue that our identification is intact

even when events are partially anticipated as we measure the rate of transmission based

on the response of other European countries relative to the size of the contemporaneous

shock in Greece. A partial anticipation of future shocks thus has no effect on the estimates

of this relative transmission.

The potential endogeneity of cross-border financial linkages is another source of concern.

In particular, reverse causality may bias our estimates if deteriorating economic conditions

in the home country led banks to chase high risk, high return Greek debt in the attempt to

gamble for resurrection. In such a case, we would observe a contemporaneous increase in

sovereign risk in the home country and in the exposure to Greek debt, which has nothing

to do with the transmission of Greek turmoil through financial linkages. If this type of

reverse causality were affecting our estimates, we should also observe a positive correlation

between sovereign risk and the exposure to a general class of high-risk foreign assets. We

therefore replace the exposure to Greek debt with exposure to the debt of other troubled

European countries (namely Italy, Portugal and Spain; Ireland is not in our sample). We

find no significant relation between the change in exposure to other PIIGS debt and the

reaction of sovereign risk, which indicates that our estimates are unlikely to suffer from the

reverse causality bias described.

Another concern is that the market may interpret some of the Greek news as shocks to

global financial stability, which are not captured by our exogenous variables. Our estimates

5We also refer to the lag structure of the VAR here, which generally captures trends of the dependentdata. See the description of our autocorrelation tests in Section 4.

5

might then suffer an omitted variable bias if changes in the exposure to Greek debt correlate

with changes in their general exposure to global risk. We address this concern by controlling,

in addition, for changes in countries’ aggregate exposure to foreign debt. The estimates

of this extended model show that the previous results on the effect of exposure to Greece

remain intact, while no significant relation between the responses to Greek shocks and

the exposure to general foreign risk of countries is detected. We thus conclude that our

estimates are not affected by the presence of omitted variables.

1.1 Literature Review

The mechanism of cross-country transmission is at the core of a large empirical and the-

oretical literature. Calvo and Reinhart (1996) distinguish between three different sources

of spillovers: first, responses to common shocks; second, fundamental-based contagion,

which operates via direct trade or financial linkages; third, pure contagion, which operates

through the portfolio rebalancing of global investors and herding behavior.6 In testing

whether cross-country spillovers are determined by direct linkages across countries, our pa-

per is closer in spirit to Forbes (2004) and Forbes and Chinn (2004).7 Contrary to the latter

study, however, our results indicate that bank linkages are relatively more important than

trade linkages to explain the propagation of risk.8 We explain this difference in results as a

consequence of the large degree of financial integration existing among European countries.

Longstaff et al. (2011) focus on the role of global factors, such as the US stock market

return or the VIX index for market volatility, as a driver of co-movements in sovereign

CDS markets. They find that these factors explain a sizeable fraction of the total variation

6A necessarily incomplete list of papers includes Baig and Goldfajn (1999), Schinasi and Smith (2000),Kyle and Xiong (2001), Forbes and Rigobon (2002), Corsetti et al. (2005), Broner et al. (2006).

7See also Kaminsky and Reinhart (2000), Hernandez and Valdes (2001), Van Rijckeghem and Weder(2001, 2003).

8Analyzing stock market returns, Forbes and Chinn find that bank channels are significant only in someof their specifications.

6

and, in light of this evidence, conclude that global investors play a dominant role in these

markets. Borri and Verdelhan (2011) study the linkages across sovereign debt markets

that arise when countries borrow from a common risk averse lender.9 We see our results as

complementary to these studies insofar as we control for global factors in our estimations.10

The unfolding Euro crisis is currently stimulating rich academic output, which can be

covered here only partially. A large part of this literature has focused on the role of finan-

cial linkages in the spread of the crisis. Bolton and Jeanne (2011) develop a comprehensive

theoretical analysis of transmission of sovereign risk through an integrated banking system.

The authors note that, although “diversification generates risk diversification benefits ex

ante, it also generates contagion ex post.” Using sovereign and bank CDS premia between

2007 and 2010 and a series of bank bailouts, Acharya et al. (2011) provide evidence that a

weak banking sector increases the default risk of the sovereign, showing in particular “that

the announcement of financial sector bailouts was associated with an immediate, unprece-

dented widening of sovereign CDS spreads and narrowing of bank CDS spreads.”11 In line

with these findings, Dieckmann and Plank (2010) find “a private-to-public risk transfer

through which market participants incorporate their expectations about financial indus-

try bailouts and the potential burden of government intervention.” Focusing on the role of

financial news, Bhanot et al. (2011) report results that “point to the role of news announce-

ments and the banking channel as important transmission channels in the crisis period.”

Finally, Arezki et al. (2011) find that “sovereign rating downgrades have statistically and

economically significant spillover effects both across countries and financial markets.” The

authors discuss several channels of spillover of sovereign risk across countries, pointing es-

pecially to “the holding of foreign sovereign debt by domestic banks...” and to the claims

9See also Lizarazo (2010) and Arellano and Bai (2012).10Furthermore, in a VAR model, the response of risk premia to global factors can differ across countries,

as suggested by Borri and Verdelhan (2011).11Balteanu and Erce (2011) study the feedback effects between bank crises and sovereign defaults in

emerging economies.

7

of banks “on banks in other countries” (see also Blundell-Wignall and Slovik (2010) and

Sy (2010)).

Our contribution to this empirical literature is twofold. First, building on the docu-

mented roles of bank-to-bank and bank-to-sovereign linkages as transmission channels of

sovereign risk, we take the broader perspective of the country level and analyze cross-

country spillovers and the role the national exposure rates in the transmission of sovereign

risk. Second, we evaluate the transmission mechanism through the careful identification

of financial shocks that originated in Greece and through the time variation in national

exposure rates.

The remainder of this paper is structured as follows. Section 2 describes our data in

detail, and Section 3 lays out the empirical framework. Section 4 presents and discusses

our main findings, and Section 5 concludes.

2 Data

Our analysis requires us to combine three main types of data: (i) a measure of sovereign

default risk; (ii) a classification of shocks that identifies, in particular, those of Greek origin;

(ii) a measure of bilateral financial linkages. The key sources for the first and third types

of data are Datastream and the BIS, respectively. We compile the second one ourselves.

Sovereign default risk. Our measure of a country’s default risk is a five-year sovereign

Credit Default Swap (CDS) premium, collected by CMAN and provided by Bloomberg. A

CDS is essentially an insurance contract between two counterparties, typically traded over

the counter. It transfers credit risk from one party, the buyer of protection, who pays “a

regular fixed premium to the seller of protection in return for compensation contingent

on the occurrence of a specified credit event” (Barclays Capital 2010). Although CDS

premia do not capture default risk perfectly, recent literature has documented that they

8

are considered to be reliable and among the best measures of default risk available (Pan

and Singleton (2008), Stulz (2010) and Fontana and Scheicher (2010)). Our analysis thus

relies on CDS premia on five-year on-the-run government bonds as a measure of sovereign

risk.12

Figure 1: Sovereign CDS Premia0

50

01

00

0

01jan2008 01jan2009 01jan2010 01jan2011

Portugal Italy Greece

Spain

A: The 'PIIGS' Countries

01

00

20

03

00

01jan2008 01jan2009 01jan2010 01jan2011

Austria Belgium Germany France

UK Netherlands Sweden

B: The 'Northern' European Countries

Five-year sovereign CDS premia of selected European countries at daily frequencyfrom January 2008 to March 2011. Units of the vertical axis are basis points (a levelof 100 bp implies that it costs 0.01 Euro per year to protect one Euro of outstandingdebt over the five-year period). Source: Bloomberg.

Figure 1 plots daily five-year sovereign CDS premia separately for “PIGS” countries

12This type of CDS contracts are the most commonly traded and have commonly been monitored, quotedand commented on the course of the recent sovereign debt crisis (Packer and Suthiphongchai 2003).

9

(Portugal, Italy, Greece and Spain) and eight other “Northern” European countries for

the period from January 2008 to March 2011.13 These graphs are familiar to the reader

of financial news: the curves not only track financial troubles at the height of the Great

Recession, but also illustrate the buildup of the Euro crisis; in particular, the market’s

assessment of a potential Greek sovereign default following the budgetary announcements

by Greek authorities in fall 2009.

The figure exhibits strong co-movements of CDS premia across countries, which appear

also from the pairwise correlations of log-changes reported in Table 1. These pairwise

correlations range between 0.6011 (Sweden and Greece) and 0.8952 (Italy and Spain), with

an average of 0.7290. In addition to the obvious effects of common factors (see Fontana

and Scheicher (2010)), part of that correlation is likely to be generated by spillover effects

from one troubled country – e.g., Greece – to other countries in the sample.

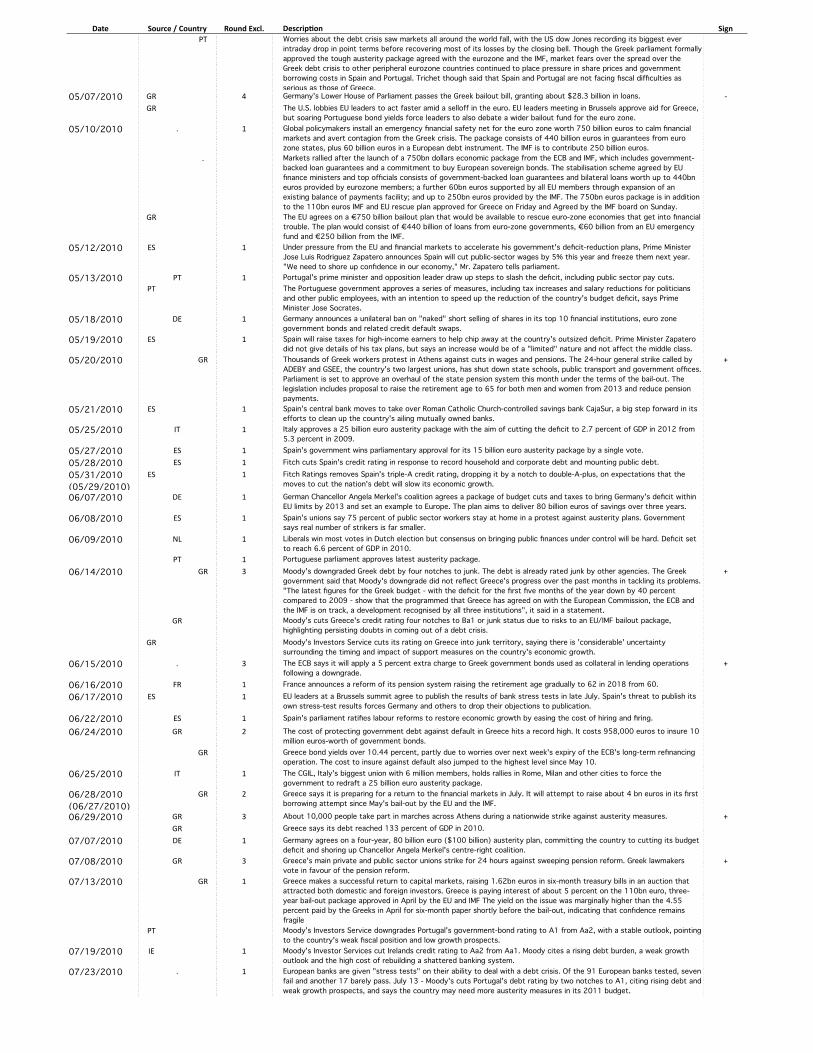

Greek Shocks. The second type of required information is a list of those days when

financially relevant information innovation came (almost) exclusively from Greece. For our

identification strategy, indeed, it is essential that we make sure that Greece is the only

origin of a relevant news shock. Pioneering the “narrative approach”, Romer and Romer

(1989) stress that severe problems can arise when isolating the shocks due to the judg-

mental and retrospective nature of the selection process. To prevent an unconscious bias

in this selection process, we rely entirely on external sources for a selection of ‘financially

relevant information shocks” during the Euro Crisis and keep the required selection process

of Greek events as mechanical as possible. Specifically, we first construct a timeline of the

Euro crisis by combining three external sources: the Financial Times (Interactive Timeline:

Greek Debt Crisis), the Wall Street Journal (Europe’s Debt Crisis - Timeline), and Reuters

13Ireland, the additional “I” in the usual PIIGS acronym, is excluded from our sample for the followingreason. In the last quarter of 2010 we observe a sharp decline in the exposure of Irish banks to Greekdebt. This drop is likely to be caused by the creation in late 2010 of a nationalized “bad bank” absorbingtroubled assets owned by Irish banks, without actually changing the exposure to Greece. We are concernedthat the inclusion of Ireland might bias our results.

10

(Europe’s Debt Crisis Timelines).14 The thus compiled joint timeline covers a period start-

ing October 9, 2009, and ending November 28, 2010. The list of these events is reported

in Table A1 in the Appendix. The first column of Table A1, labeled Date, reports the day

of the event or, in case the event falls on a weekend or a bank holiday, the first business

day after the event. In the latter case, the original date is reported in brackets. The list

includes 92 working days where news of any kind is reported in at least one of the three

timelines. The column in Table A2 labeled Source / Country provides information on the

original timeline as well as the country in which the news shock originated.15 Excluding

the days that contain news from other countries than Greece leaves us with 50 of these 92

days. The days excluded in this first step are marked with 1 in the third column of Table

A1 labeled Exclusion Round. In a second round, we exclude those of remaining days, in

which the news essentially consists of reported market sentiment, the evolution of bond

spreads and unspecific political statements. We are aware of the fact that this selection

is judgmental to some extent but argue that there is little room for ambiguity, as can be

verified by taking a close look at the third column of Table A2, where these days are marked

with a 2. After excluding these days from the list, we are left with 38 days of Greek events.

We label this list of events the raw set of Greek shocks. It reflects our broadest definition of

Greek shocks and will serve for robustness checks for our results. However, to prevent our

results to be driven by simultaneous shocks in other countries, we perform an additional

round of elimination. Specifically, for each of the remaining 38 days in the raw set of Greek

shocks, we search for potential overlapping shocks originating in other countries. This step

of exclusion is based on Lexis-Nexis, a comprehensive news database.16 For each of the 38

14See http://www.ft.com/intl/cms/s/0/003cbb92-4e2d-11df-b48d-00144feab49a.html#axzz1eQwHrlj,http://online.wsj.com/article/SB10001424052748704448304575195863350731920.html andhttp://www.reuters.com/article/2010/08/25/eurozone-crisis-events-idUSLDE67O0YD2010082515We re-date the very first shock, which appears to be misreported in the timeline of Reuters to October

9 2009. We don’t find other inconsistencies between the three original timelines and the news in theLexis-Nexis database.

16See www.lexisnexis.com.

11

days, we classify the events occurring in other countries into nine categories.17 The first

four comprise, respectively, information on monetary policy (MONP), policy action and

regulation (POLA), social unrest (SOCU) and a rating agency’s change of grading of a

country other than Greece (RATE). We view these events as too important for financial

markets and therefore exclude those days from our list of Greek events, where at least one

of these events is reported. The remaining five categories comprise general economic news

(ECON) the description of market developments and sentiment (MKT), event outside of

Europe (FORE) political statements regarding non-committal intentions (POLI), and news

on private companies (COMP). Days are not excluded from our list of Greek events based

on these events. In the third column of Table A2 the days excluded in this last round of

exclusion are marked with 3.

The final list of Greek events comprises 24 information shocks identified as Greek shocks

and is reported in Table A1 along with a short description of the corresponding event. These

24 pure Greek events are finally classified as generating positive or negative information

shocks, depending on whether we expect the Greek CDS premium to either increase or

decrease on that day. This last step is actually the only one relying on our judgement only.

We refer to Table A1 to check that there is little room for ambiguity at this stage.

To perform an additional robstness check, we also exclude those dates, at which, ac-

cording to the description in the Lexis-Nexis database, the general economic news (ECON)

were unexpected or surprising to market participants. This final round excludes 7 addi-

tional days (marked with a 4 in Table A1, third column) and leaves us with a set of 17

days, which we label the restricted set of Greek events.

Financial linkages. We now need a measure of bilateral financial linkages with Greece

which we can then relate to the response of each country to Greek shocks. In particular, we

focus on bilateral cross-border bank exposures using data from the Consolidated Banking

17We document this list of events in a supplementary appendix, which is available from the authors uponrequest. (This appendix is included in the submission.)

12

Statistics of the BIS. This dataset covers banks’ claims to non-residents, broken down by

nationality of borrower and creditor and four types of debt: (i) Public Debt; (ii) Private

Bank Debt; (iii) Private Non-Bank Debt; and (iv) Other Debt (see BIS (2006)). Report-

ing entities are bank head offices, including the exposures of their foreign affiliates (i.e.,

subsidiaries and branches); reported data cover financial claims on the balance sheet, con-

solidated on a worldwide basis within each banking group (i.e., inter-office positions are

netted out).18 The final dataset provides a matrix of cross-country bilateral (gross) bank

exposures, evaluated at market prices.19

The BIS reports the data in US dollars after converting the positions originally reported

in other currencies using end-of-quarter exchange rates. As most of the countries in our

sample belong to the Euro Area, we convert the data back into Euros using the end-of-

quarter exchange rate provided by the International Financial Statistics (IFS) of the IMF.

This conversion allows us to remove potential valuation effects that are common to all

countries, which might introduce an exogenous variation in our measure of financial linkages

and thus affect our estimates. Finally, we normalize banks’ exposure by the average GDP

between 2009 and 2010 to control for different country sizes. The data on GDP come from

the World Economic Outlook of the IMF.

Figure 2, top panel, illustrates gross cross-border exposure of BIS-reporting banks,

aggregated across the eleven European countries in our sample, by type of debt. It shows

that, during the height of the financial crisis, the total foreign positions were rewound,

in particular those of bank debt. With the onset of the year 2010, the downward trend

has continued, but moderately so. The picture is different when focusing on Greek foreign

18BIS (2006) specifies that balance-sheet relevant instruments include ”certificates of deposit (CDs),promissory notes and other negotiable paper issued by non-residents, banks’ holdings of international notesand coins, foreign trade-related credits, claims under sale and repurchase agreements with non-residents,deposits and balances placed with banks, loans and advances to banks and non-banks, holdings of securitiesand participations including equity holdings in unconsolidated banks or non-bank subsidiaries.”

19In addition, BIS (2006) reports a number of valuation practices recommended to reporting entities toensure the cross-country comparability of data. In addition to the use of market prices to evaluate claims,these practices specify how to report arrears, provisions and the write-off of claims.

13

Figure 2: Foreign Debt Exposure by Type

01000

2000

3000

4000

Bill

ion E

uro

s

2006q1 2007q1 2008q1 2009q1 2010q1 2011q1

A. Aggregate Cross-Border Debt

020

40

60

80

100

Bill

ion E

uro

s

2006q1 2007q1 2008q1 2009q1 2010q1 2011q1

Private Debt Bank Debt

Public Debt Other Debt

B. Greek Debt

Exposure of BIS reporting banks to European debt (top panel) and Greek debt (bot-tom panel) by type of debt: Public, Bank and Non-Bank Private, and Other. Quar-terly data are reported on an immediate borrower basis (for a comparison betweenimmediate and ultimate borrower bases, see the Appendix). The set of 11 countriesincludes: Austria, Belgium, France, Germany, Greece, Italy, Netherlands, Portugal,Spain, Sweden and UK. Source: BIS, Consolidated Banking Statistics.

debt to the remaining ten countries (bottom panel). Here, the largest decrease in debt

exposure occurred during the year 2010, with positions in sovereign debt dropping the

most in absolute terms.20

20In principle, the decrease in the exposure to Greek bonds may result from valuation effects. Thus,to ensure international comparability, the BIS recommends ”that banks’ international claims be valued atmarket prices” but acknowledges that, where ”market values are not appropriate, contractual or nominalvalues should be used.” Moreover, differences across countries arise because ”loans in the banking books,which in principle should be assigned nominal value, should be valued in accordance to the reportingcountries’ accounting standards.” (BIS 2006)

14

It is important to notice that neither the levels nor the trends in the exposure to Greek

debt are uniform across all countries. Table 2a shows that within the set of ten European

countries, average exposures vary between roughly 0.08 and 1.22 percent of GDP. Table 2b

reports summary statistics of the evolution of exposure to Greek debt staring in the fourth

quarter 2009, for which levels are normalized to 100.21 Panel A reports numbers for total

debt by quarter. The last column thus shows that, on average, the exposure to Greek debt

was 67.5% of the initial level. The country for which exposure changed the least reduced

its exposure by 0.2% (100-99.8), and the largest reduction amounted to 77.2%. Panel B

summarizes exposures for Greek public debt. Up to 2010Q4, the average country reduced

its exposure to 73.0% of the initial level. The maximum reduction was 82.3%, and one

country actually increased its exposure by 13.1%. Finally, panel C reports the numbers

based on Greek bank debt. Between 2009Q4 and 2010Q4, the average country reduced Its

exposure to 32.0% of the initial level. The maximum reduction reached 97.7%, and at least

one country increased its exposure by 4.2%. Our aim is to exploit the time variation of

each country to extract information about how sovereign risk is transmitted via exposure

to the different classes of Greek debt.

The data on financial linkages are reported on the immediate borrower basis and do not

include credit derivatives and guarantees, which could shift risk exposure across countries.

Thus, the accuracy of effective exposure is a potential source of concern. Unfortunately, the

availability of data on the ultimate risk basis is very limited. Not only would the use of the

ultimate borrower basis limit our sample, but Greece would drop out of it. A comparison

between the data on the immediate and ultimate basis shows that the two measures covary

very closely.

A first inspection of the data reveals two important aspects of CDS premia on the days

classified as Greek events. First, on these days, we observe large movements in the Greek

21The beginning of the Greek sovereign debt crisis can be dated to 2009Q4.

15

CDS premium relative to the rest of the sample. Table 3a reports summary statistics of

daily log-changes in the Greek CDS premium, partitioning the sample into days of positive

Greek shocks, days of negative Greek shocks and all remaining days, respectively. While

the average change in Greek CDS is 0.19% in the absence of Greek events, the table shows

an average increase of more than 7% on the days of “positive” Greek news, and a decline

of more than 4% on the days on “negative” Greek news. We also observe that the largest

increase in Greek CDS (27%) occurred on a day of positive Greek shocks. Similarly, the

second largest drop in the Greek CDS premium (-15.7%) is associated with a Greek event

with negative sign.22

Looking at the relation between exposure to Greek debt and the response of other

countries to Greek shocks, we find that a level of exposure above the country median is

on average associated with larger CDS responses. Table 3b reports summary statistics of

the log-changes in the CDS premia of the 10 European countries in our sample by rate

of exposure to Greek debt (above or below the country median) and by type of Greek

shock (positive or negative). As shown in Panel A, the average increase in the CDS of

other countries on the days of positive Greek shocks is equal to 3.99% when the exposure

to total Greek debt is above the median of each respective country, while it is equal to

2.64% when the exposure is below the median. Similarly, on the days of negative Greek

shocks the CDS of other countries decline on average by 1.66% when exposure is above the

country median and by 0.87% when exposure is below the country median. Panels B and

C show similar patterns in the cases of exposure to public debt and to private bank debt,

respectively. Overall, these numbers suggest that, controlling for country fixed effects, the

absolute response to Greek shocks tend to increase with the exposure to Greek debt. In the

next section, we describe the empirical framework that we adopt to test this hypothesis.

22Notice that the largest drop in the Greek CDS premium (-47.10%) coincides with the joint EU-IMFannouncement of a 110bn Euro bailout package for Greece. However, we had to exclude this announcementfrom the list of pure Greek events as the EU Council agreed on the same day to establish the first Europeanstabilization mechanism with the aim of safeguarding financial stability in all member states.

16

3 Empirical Framework

In this section, we discuss our approach to identifying sovereign risk spillovers across coun-

tries. We start by considering a n-dimensional vector autoregressive model

yt = Φy(L)yt−1 + Φxxt + ut,

where yt is a vector of CDS premia for each country, Φy(L) =∑J

j=1 Φy,jLj−1 is a polynomial

of n× n matrices in the lag operator, xt is a m-dimensional vector of exogenous variables

that includes the constant, and ut is a vector of innovations. In a more compact form, this

model can be written as

yt = Φzt + ut, (1)

where zt = [y′t−1, . . . , y′t−J , x

′t]′ is a p × 1 vector of both lagged endogenous and exogenous

variables with p = nJ +m and Φ = [Φy,1, . . . ,Φy,J ,Φx] is a n× p matrix of coefficients.

The innovations ut are jointly correlated reflecting cross-country spillovers. Following

standard practice, we assume

ut = Bεt, (2)

where εt is an i.i.d. vector of country-specific shocks with zero mean. The matrix B thus

reflects the rate of transmission of these shocks across countries. Without loss of generality,

we normalize the diagonal elements of B, which reflect the within-country transmission of

shocks, to one.

3.1 Identifying Spillovers using a Narrative Approach

We use a “narrative approach” similar to Romer and Romer (1989) to identify cross-country

spillovers, measured by the non-diagonal elements of the transmission matrix B. As part

of our specific approach, we first decompose each country-specific shock into a signed mean

17

shift, which shall reflects “exceptional” and to some extent observable events, and a residual

noise, which shall reflect “normal” shocks. Specifically, we assume for each country i that

εi,t = di,tξi + νi,t

where di,t ∈ −1, 0, 1 is a signed indicator for exceptional events in country i; ξi denotes

the size of exceptional events; νi,t reflects normal events; and di,t and νi,t are i.i.d. across

time and countries.23 Applying the same decomposition to each country, we can write

εt = Dtξ + νt

where Dt is a diagonal matrix with entries di,t.

The narrative account of Greek events described in the previous section allows us to

identify a specific set of dates with pure Greek shocks (i.e., days of exceptional events in

Greece but in no other country) and to determine the sign of the corresponding shock.

Using this information, we can define a signed indicator function 1gr,t for Greek events and

rearrange the vector of country-specific shocks as

εt = 1gr,tξgr + εt (3)

where ξgr = [0 ... ξgr ... 0]′ is a column vector of exceptional shocks in Greek events and

thus is zero except for the Greek component. Meanwhile, εt = (1 − |1gr,t|)Dngrt ξ + νt is a

residual shock that incorporates the possibility of exceptional non-Greek shocks in other

periods plus the normal noise νt.

23Despite being quite restrictive, the assumption that the effect of exceptional events is constant overtime does not affect our results but conveniently reduces notation.

18

Combining (3) and (2) yields

yt = Φzt + β · 1gr,t + ut, (4)

where ut is a modified residual defined as

ut ≡ 1gr,tugrt + (1− |1gr,t|)ungrt

ugrt ≡ Bνt (5)

ungrt ≡ B(Dngrt ξ + νt).

In model (4), the vector β measures the average response of sovereign risk in each

country to a shock in Greece, and is the coefficient of interest. To obtain efficient estimates

for this coefficient, however, we cannot use a standard Ordinary Least Squares (OLS)

estimator as the assumption of conditional homoskedasticity of the error term is clearly

violated. By construction, indeed, ut depends only on the normal shock νt in the days of

Greek events, while it depends on the sum of νt and, potentially, the non-Greek exceptional

shocks Dngrt ξ in all other days. Our strategy thus forces us to derive a Generalized Least

Squares (GLS) estimator that allows for the presence of two alternating regimes in the

variance-covariance matrix of the residuals. We refer to the Appendix for a technical

description of the GLS estimator used to estimate model (4).

One last step is required to test whether the transmission of Greek shocks is statistically

significant. By construction, indeed, the coefficient β is a reduced-form parameter that

depends on both the rate of cross-country transmission of Greek shocks and the average

19

size of the shocks, i.e.

β ≡ B · ξgr =

B(1,gr)

...

B(n,gr)

· ξgr

where B(i,gr) denotes the component of the transmission matrix B corresponding to the

position of country i and Greece. To be able to make inference about B(i,gr), we thus need

to normalize the vector β by the average size of Greek shocks ξgr. Exploiting the linearity

of our model and our previous normalization of the diagonal elements of B, we obtain

βiβgr≡

B(i,gr) · ξgrB(gr,gr) · ξgr

= B(i,gr).

As analytical confidence intervals for these ratios cannot be easily computed, we then rely

on bootstrapping techniques to construct empirically consistent confidence intervals for

B(i,gr).24

3.2 Inspecting the Role of Financial Linkages

We turn now to the contribution of financial linkages in the transmission of sovereign risk.

To deal with potential omitted variables, we adopt a difference-in-difference approach by

exploiting the within-country variation in the exposure to Greek debt. This identification

strategy allows us to control for a wide range of factors that may affect the response of

countries to Greek shocks independently of financial linkages. First, by including country-

fixed effects, slow-moving country characteristics such as political instability and structural

fiscal imbalances will be accounted for. Second, adding time-fixed effects allows us to remove

24In doing so, we take special care to resample the residuals only within each variance-covariance regime,not across them, to satisfy the assumption of invariance in distribution that underlies the bootstrappingtechnique.

20

all time-varying factors that have a common effect on all countries. Finally, we include a

measure of bilateral trade of each country with Greece to remove potential endogenous

responses of financial linkages through changes in trade linkages.

Specifically, we allow the spillover matrix B in (2) to vary over time, reflecting quarterly

changes in financial exposures and trade linkages. Using Bq to denote the transmission

matrix in quarter q, we assume

Bq = B0 + Tq + d1 · FINq + d2 · TRADEq, (6)

where B0 is a matrix of fixed effects for each country pair, Tq is a matrix of time-fixed

effects common to all country pairs, and FINq and TRADEq are the matrices of financial

and trade linkages for each country pair. The coefficients d1 and d2 measure the effects of

an increase in financial and trade linkages on cross-country spillovers, respectively. Both

coefficients are scalar, as we assume that financial and trade linkages have the same effect

independently of the country pair.25

Substituting for (6) into (2) and using our previous decomposition of country-specific

Thus, the response to Greek shocks now depends on a vector of fixed effects for each

country, β0 = B0ξgr, a vector of common time effects, τq, and the vectors of financial

and trade linkages of each country with Greece, FINgr,q and TRADEgr,q. The coefficients

δ1 ≡ d1 · ξgr and δ2 ≡ d2 · ξgr are scalar and measure the contribution of financial and trade

linkages to the transmission of the average Greek shock, respectively.

25In (6) we maintain our previous normalization of the diagonal entries of B, by setting the diagonalentries of B0 equal to one and those of Tq, FINq and TRADEq to zero.

21

The estimation of model (7) involves some technical complications. First, the coefficients

τq, δ1 and δ2 are equal for all countries, imposing a cross-equation restriction on the VAR

model. Second, implicit in this model is the fact that the residual ut now depends on Bq (see

(5)) and thus has a variance-covariance matrix that can vary both across regimes (Greek

and non-Greek) and across quarters q. We thus derive a restricted GLS estimator that

allows us to address these properties of the model, referring once again to the Appendix

for a detailed discussion.

Once again, to estimate the contribution of financial linkages to cross-country transmis-

sion independently of the size of Greek shocks, we need to take the following normalization

of the coefficient δ1,

δ1β0(gr)

=d1 · ξgr

B0(gr,gr)ξgr

= d1, (8)

where β0(gr) ≡ B0(gr,gr)ξgr denotes the Greek component of the vector of time-invariant

responses β0 and is equal to the size of Greek shocks by effects of our previous normalization

of B0. We then construct confidence intervals for coefficient d1 by estimating repeatedly

model (7) with bootstrapped residuals.

4 Results

This section reports GLS estimates of cross-country transmission rates of sovereign risk.

We begin by estimating model (4) to assess average, time-invariant transmission. We then

turn to model (7) to analyze the role of the financial linkages.

The dependent variable yt consists, in all specifications but for few explicitly indicated

cases, of a vector of five-year sovereign CDS premia of eleven European countries (in-

cluding Greece).26 Data are in logs and in first-differences. We take logs to focus on

26The eleven countries are Austria, Belgium, France, Germany, Greece, Italy, the Netherlands, Portugal,

22

percentage deviations rather than absolute deviations, which would give excessive weight

in the estimations to countries with relatively high levels of CDS premia (compare Figure

1). Intuitively, a jump from 30 to 50 basis points in the German CDS premium should

be considered much more dramatic than an increase from 450 to 470 basis points of the

Portuguese CDS premium. We take first-difference to ensure stationarity.27

The vector of regressors zt comprises the lags of the endogenous variable yt plus the

vector of exogenous variables xt. The latter control for common shocks affecting global

market conditions and consist of the following variables: sovereign CDS premia of the US

and Japan (logged and differentiated as all other CDS premia), the VIX index for the US

(logged), stock market returns for the US (defined as log changes of the S&P index), the

US federal fund rate, and seasonal dummies for each day of the week.28

Our measures of financial linkages, FINgr,q, and of trade linkages, TRADEgr,q, which

appear in the interaction terms of model (7), are normalized by average GDP between 2009

and 2010 to control for country size and are logged.29 We use logs to focus on percentage

variations in the linkages with Greece rather than absolute variations, as the latter may

depend on cross-country differences in average levels.

The data are reported on a daily basis, except for the data on financial and trade

linkages which have quarterly frequency. We include a total of 500 business days for the

calendar years 2009 and 2010.

Spain, Sweden and UK.27The estimation results remain intact when we use a Hodrick-Prescott filter.28Data on sovereign CDS premia for US and Japan are from the same source used for the other countries

and described in Section 2. Data for the VIX are taken from Bloomberg, while data on S&P500 stockmarket returns and the US federal fund rate are from the Federal Reserve Economic Data (FRED).

29We use average GDP to avoid that the indicators for financial and trade linkages depend spuriouslyon time variation in GDP. We refer to Section 2 for the definition of the indicator of financial linkages,FINgr,q. The indicator of trade linkages, TRADEgr,q is defined as the sum of bilateral exports and importsof each country from and to Greece. The source of these data is the Direction of Trade Statistics of theIMF. As for the data on bilateral exposures, these data, originally reported in US dollars, are convertedinto Euros using end-of-quarters exchange rates from IFS.

In our baseline specification, we estimate model (4). The coefficient β is constant over the

entire period and thus captures the time-average of the responses to the identified Greek

shocks by the other European countries.

Our tests of autocorrelation of the residuals prompt us to include eight lags of the

dependent variable and no lag of the exogenous variables. Moreover, we disregard het-

eroskedasticity within the set of days where Greek events occur.

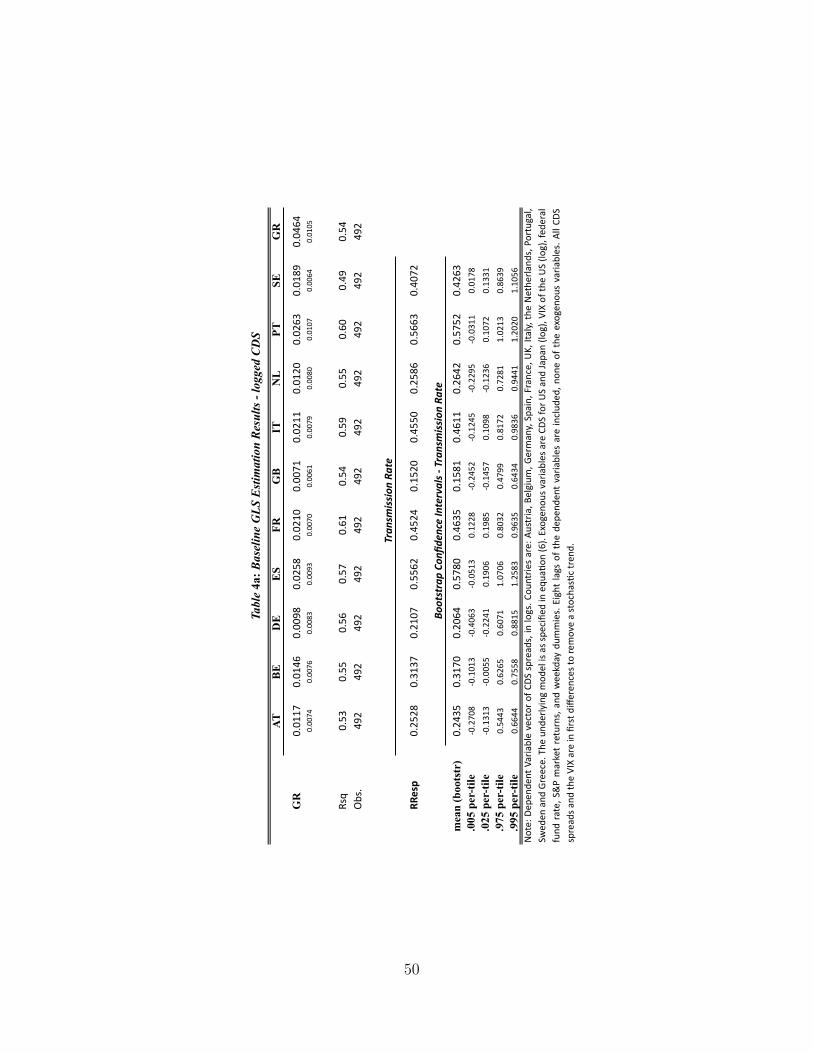

Table 4a reports the results for the baseline specification. The columns correspond to

the elements of the vector yt, i.e., to the eleven countries. In the upper panel, we report the

corresponding coefficients of the indicator for Greek events (GR), along with the standard

errors. All of the estimates of the eleven coefficients are positive, and the implied t-ratios

indicate that the coefficients are statistically significant on the five-percent level for more

than half of the countries.30 The point estimate for Greece itself is 0.0464, which indicates

that the events identified in Table A1 generated, on average, a jump in the Greek sovereign

CDS premium of over 4.6 percent. At a time-average of 679 basis points in 2010, this

average change in the CDS premium is roughly equivalent to a jump of more than 31 basis

points (679 ∗ .0464 = 31.53).

The coefficients corresponding to countries other than Greece itself vary from 0.0071

(UK) to 0.0263 (Portugal). Measured relative to the magnitude of the Greek coefficient

(lower panel), these estimates imply a rate of transmission that ranges from 15.20% to

56.63%, with a level of statistical significance that strongly matches that of the absolute

responses. On average, the rate of transmission is equal to 36.25%, suggesting economically

significant cross-country spillovers.

Table 4b repeats the estimates without prior logging the CDS premia to assess transmis-

30Namely, Spain, France, Italy, Portugal, Sweden and Greece. Increasing the confidence level to tenpercent, the response to Greek shocks is significant also for Belgium.

24

sion rates by levels rather than percentage deviations. Again, all estimates are positive and

with level of statistical significance comparable to those obtained before. The coefficient

for Greece indicates an average jump of 24.217 basis points in response to Greek events,

which is somewhat lower than, but in the same realm as, the benchmark computed using

the elasticities. The response of European sovereign CDS premia relative to the response

of the Greek CDS premium ranges between 1.11% and 34.30%.

Figure 3 plots the impulse response functions, including the five-percent confidence

bounds, for all eleven countries. The figure shows that a Greek shock generates a positive

contemporaneous response in the CDS premium of all countries, whose significance is com-

parable to the levels reported in Table 4a. In general, the induced change in CDS becomes

insignificant after one day. More importantly, the figure shows no negative response as the

lag increases, which indicates that the effects of Greek shocks are not transitory and the

sovereign CDS premia do not revert to their initial levels over time.31

Overall, the results from the baseline regression indicate substantial rates of transmis-

sion of sovereign risk across Europe. In the next step, we analyze the role of financial

linkages in that transmission.

4.2 Financial Linkages

We turn now to the estimation specified in (7). The coefficient δ1 on the interaction term

FINgr,q · 1gr,t captures the effect of financial linkages on the transmission of sovereign risk,

and is therefore the coefficient of interest. We use three different measures of financial

linkages: exposure (i) to Total Greek Debt (i.e. public plus private); (ii) to Greek Public

Debt; and (iii) to Debt of Greek Banks. Whenever there is no risk of confusion, we will

refer to these measures as exposure to Greece.

Column I in Table 5 shows the estimates corresponding to the specification where expo-

31The confidence bounds are derived from a bootstrap distribution based on 1000 replications.

25

Figure 3: Impulse Response Functions

0 2 4 6 8 10−0.02

00.020.04

at

0 2 4 6 8 10−0.02

00.020.04

be

0 2 4 6 8 10−0.02

00.020.04

de

0 2 4 6 8 10−0.02

00.020.04

es

0 2 4 6 8 10−0.02

00.020.04

fr

0 2 4 6 8 10−0.02

00.020.04

gb

0 2 4 6 8 10−0.02

00.020.04

it

0 2 4 6 8 10−0.02

00.020.04

nl

0 2 4 6 8 10−0.02

00.020.04

pt

0 2 4 6 8 10−0.02

00.020.04

se

0 2 4 6 8 10

0

0.05

0.1gr

Impulse response functions of CDS (log-changes) of eleven countries to a Greek shock of averagesize for the 10 business days after impact (blue line). The red lines indicate the 5% confidencebounds based on a bootstrap exercise with 1000 replications.

sure is measured in total Greek debt over GDP (Total). We choose to report only a small

set of the estimated coefficients for exigences of space: the first row reports the Greek

component of the vector of time-invariant coefficients on the Greek dummy (GR). This

coefficient, denoted by β0(gr) in (8), captures the average size of Greek shocks and is esti-

mated to be 0.0474, which is close to the point estimate in the baseline regression (Table

4a).32

32We do not report the fixed effects of the responses of other countries but nevertheless check that theimplied average rate of transmission is consistent with the baseline results.

26

The second and the third coefficient reported in Column I of Table 5 correspond to

the interaction terms GR ∗ Total and GR ∗ Trade, which relate the responses to Greek

shocks to the financial and trade linkages with Greece, respectively. The coefficient for the

first interaction term, which corresponds to δ1 in model (7), is 0.0163 and is significant at

the five-percent level, as indicated by the implied t-ratio. The coefficient on the second

interaction term is −0.0115 and is not statistically significant. We take these results as an

indication that financial linkages have been relatively more important than trade linkages

for the transmission of the Euro crisis and we further scrutinize their role.

We are interested in the rate of transmission, i.e. in the response relative to the size of

the original Greek shock. To this aim, the coefficient of GR ∗Total needs to be normalized

by the average size of the Greek shock, β0(gr) . The resulting ratio corresponds to the ratio

d1 in (6), which measures the elasticity, with respect to an increase in financial exposure,

of other countries’ responses to a one-percent increase of Greek sovereign risk. We will

therefore say that our coefficient of interest measures the impact of financial linkages on

the transmission rate of a normalized Greek shock.

The point estimate reported in Column I is equal to 0.3443 and is statistically significant

at the one-percent level as shown by the bootstrap confidence intervals reported in the lower

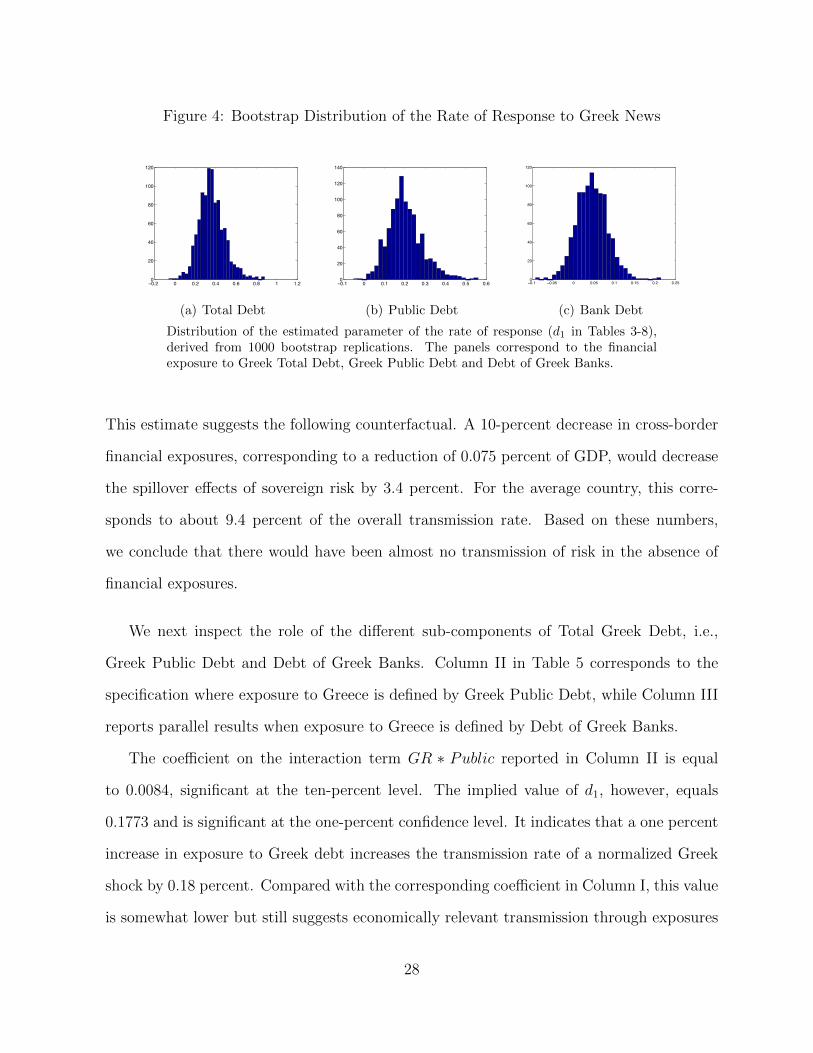

panel of the table.33 Figure 4 illustrates the bootstrap distributions for this coefficient for

the different measures of financial exposures to Greece. In all cases, the point estimates of

the coefficient lie, reassuringly, at the center of the respective bootstrap distribution.

The effect of financial linkages on transmission is not only statistically significant but

also economically relevant. Since CDS as well as financial exposure are logged, the point

estimate of 0.3443 suggests that a one percent increase in a country’s financial exposure

to Greece increases the transmission rate of a normalized Greek shock by 0.34 percent.

33As discussed in Section 3, we cannot derive a theoretical distribution for the estimator of d1 andresume to bootstrapping to assess statistical significance. The reported confidence bounds are based on1000 bootstrap replications and indicates that the estimates of d1 are strictly positive with a one-percentconfidence level.

27

Figure 4: Bootstrap Distribution of the Rate of Response to Greek News

−0.2 0 0.2 0.4 0.6 0.8 1 1.20

20

40

60

80

100

120

(a) Total Debt

−0.1 0 0.1 0.2 0.3 0.4 0.5 0.60

20

40

60

80

100

120

140

(b) Public Debt

−0.1 −0.05 0 0.05 0.1 0.15 0.2 0.250

20

40

60

80

100

120

(c) Bank Debt

Distribution of the estimated parameter of the rate of response (d1 in Tables 3-8),derived from 1000 bootstrap replications. The panels correspond to the financialexposure to Greek Total Debt, Greek Public Debt and Debt of Greek Banks.

This estimate suggests the following counterfactual. A 10-percent decrease in cross-border

financial exposures, corresponding to a reduction of 0.075 percent of GDP, would decrease

the spillover effects of sovereign risk by 3.4 percent. For the average country, this corre-

sponds to about 9.4 percent of the overall transmission rate. Based on these numbers,

we conclude that there would have been almost no transmission of risk in the absence of

financial exposures.

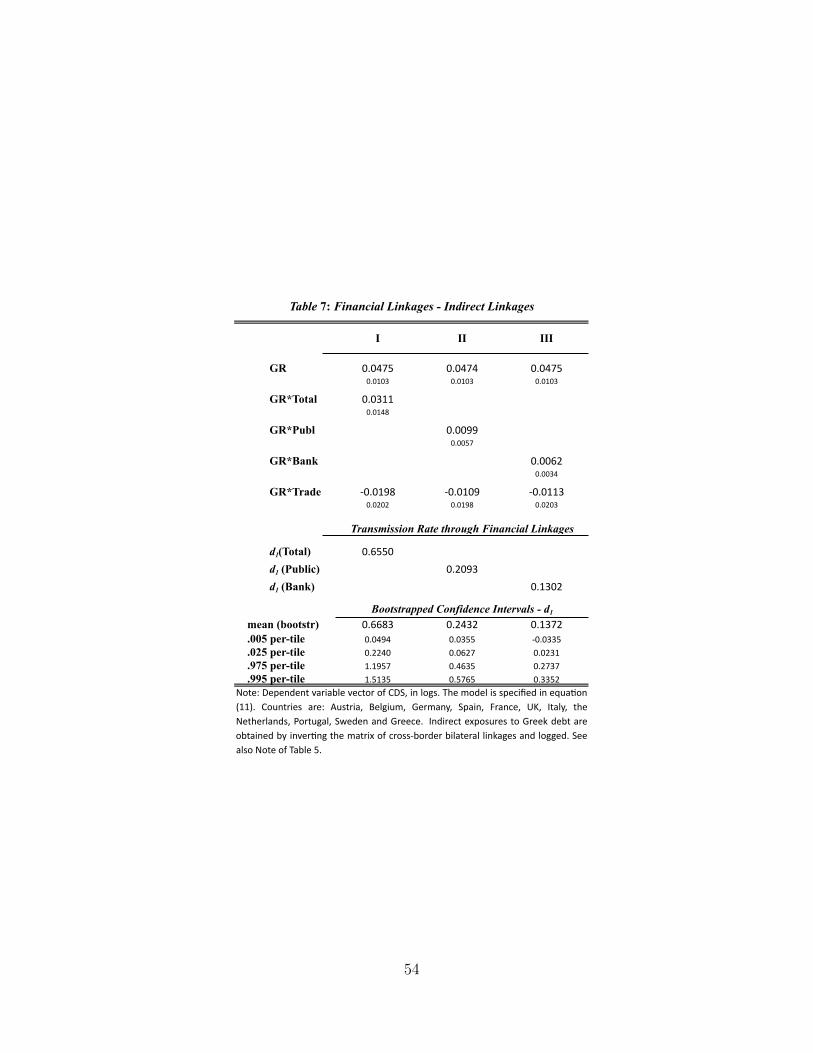

We next inspect the role of the different sub-components of Total Greek Debt, i.e.,

Greek Public Debt and Debt of Greek Banks. Column II in Table 5 corresponds to the

specification where exposure to Greece is defined by Greek Public Debt, while Column III

reports parallel results when exposure to Greece is defined by Debt of Greek Banks.

The coefficient on the interaction term GR ∗ Public reported in Column II is equal

to 0.0084, significant at the ten-percent level. The implied value of d1, however, equals

0.1773 and is significant at the one-percent confidence level. It indicates that a one percent

increase in exposure to Greek debt increases the transmission rate of a normalized Greek

shock by 0.18 percent. Compared with the corresponding coefficient in Column I, this value

is somewhat lower but still suggests economically relevant transmission through exposures

28

to public debt.

The coefficient on the interaction term GR ∗ Bank reported in Column III is equal to

0.0020 and is not statistically significant. The implied value of d1 is 0.0412, much lower than

in the previous two cases. In addition, the reported bootstrap confidence interval shows

that this coefficient is not statistically different from zero at a five-percent confidence level.

These results suggest that the role of exposure to debt of foreign banks is less important for

the transmission of sovereign risk: the elasticity of the spillover effects to bank debt exposure

is less than one fourth of the corresponding elasticity with respect to direct exposure to

Greek sovereign debt.

Finally, notice that the estimated coefficients on the Greek dummy and on the interac-

tion term GR ∗ Trade do not vary much across specifications.

Overall, the baseline estimates suggest that the rates of exposure to total Greek debt,

and in particular to Greek public debt, played important roles in the transmission of

sovereign risk across the Euro Area. Bank-to-bank lending, by contrast, did not seem

to play a major role for the transmission. We now conduct a number of robustness exer-

cises using alternative specifications and different variables than those used in our baseline

estimations.

4.3 Robustness

In the first robustness check, we repeat our estimations measuring CDS in basis points and

the exposure to Greek debt as percentage points of GDP (i.e., we do not log these variables).

While this linear specification, may consitute a more direct way of testing transmission,

the estimates may also be affected by the respective levels of CDS and exposure to Greece.

Specifically, countries with relatively large CDS premia and with relatively large exposures

to Greek debt will have higher weight in the estimation. Table 6 shows that the coefficients

on the interaction between the different measures of financial exposures and the Greek

29

dummy remain positive, although the coefficients involving the exposure to total Greek

debt and the exposure to Greek public debt are not statistically significant. When we nor-

malize the interaction coefficients by the size of Greek shocks, however, we find insignificant

estimates only in the specification with total Greek debt. We observe that the estimate of

the coefficient of interest, d1, in the specification involving the Debt of Greek Banks is now

larger than the estimate in the specification using Greek Public Debt. The estimates of the

coefficient d1 are 0.0625 and 0.2894, respectively. One must bear in mind, however, that

the exposure to bank debt (0.09% of GDP on average) is much lower than the exposure

to sovereign debt (0.48%) so that the total effect of the latter is bigger. Overall, the point

estimates reported in Table 6 suggest following interpretation of our results. According to

Column II, a reduction of exposure to Greek Public Debt of one percent of GDP implies

that the transmission rate of a normalized Greek shock decreases by roughly 0.06 percent.

Comparing these results with an average normalized response of 0.08912 basis point (com-

pare Table 4b), this value suggest that financial linkages were important for the observed

transmission of sovereign risk.

Next, we take an alternative measure of financial linkages that not only considers the

direct exposure to Greek debt but also the entire network of bilateral exposures across

the countries in our sample. In particular, if French banks are strongly exposed to Greek

sovereign debt but Spanish banks are not, the Spanish banks might nevertheless suffer

from an increase in Greek sovereign risk due to their indirect exposure through the French

banking system. To capture these indirect effects, we invert the matrix of bilateral financial

linkages and estimate the corresponding Greek column of the matrix of financial linkages.

The exposure now captures the overall – i.e., the direct and the indirect – transmission

of Greek shocks to the respective European countries. Table 7 shows that the estimates

for d1 have a level of statistical significance of at least five percent in all specifications.

Interestingly, the point estimates are larger than those reported in Table 5, especially in

30

the specification with total Greek debt and with Debt of Greek Banks. These numbers

demonstrate the importance of accounting for the entire network of cross-border financial

linkages when studying the propagation of sovereign risk, particularly in the context of the

highly integrated European countries.

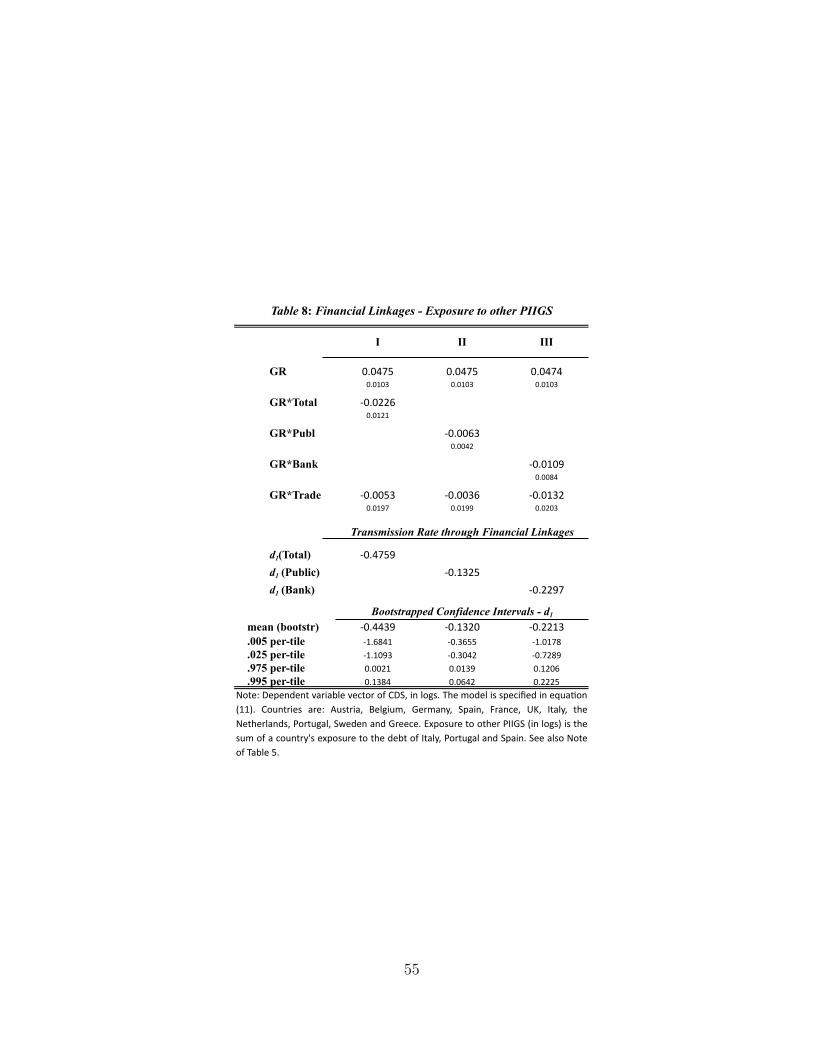

Further, we address potential concerns related to the possibility that financial institu-

tions in distress may raise their exposures to high risk, high return assets (including Greece)

to gamble for resurrection. In this case, vulnerable economies with strong responses to all

foreign (including Greek) shocks may actually increase their exposure to Greek debt so

that reverse causality could bias our estimates. To test for such effects, we re-estimate our

baseline model by replacing the exposure to Greek debt with the exposure to the debt of

the PIIGS. The results reported in Table 8 show that there is no clear association between

the change in responses to Greek shocks and the exposures to the debt of the PIIGS. In par-

ticular, the coefficient on the interaction with the different measures of financial exposures

are all negative and statistically insignificant. The same result applies when normalizing

the interaction coefficients by the size of average Greek shocks, as indicated by the fact that

the bootstrap confidence intervals for d1 are centered around zero. We confidently dismiss

the possibility of gambling for resurrection and the associated reverse causality bias in the

results showed in Table 5.

An additional concern is that the days of Greek news might be interpreted by the

market as days of deteriorating global economic conditions.34 In this case, our estimate

would be biased if changes in exposure to Greek debt correlate within countries’ changes in

the exposure to aggregate foreign debt, defined as the sum of claims on each foreign country.

Specifically, the coefficient on the interaction term with financial exposures would reflect

the response of sovereign risk to changes in the general exposure to risk rather than changes

34More specifically, these event could be perceived as changes in global conditions not captured in ourexogenous variables.

31

in the exposure to Greece. To address this concern, we add as a control the interaction

between the Greek dummy and three measures of aggregate exposure to foreign debt (i.e.,

total, public and bank debt), each referring to the corresponding measure considered in the

exposure to Greek debt. At the cost of generating some confusion, we denote in Table 9

this additional interaction term as GR ∗ FOREIGN , irrespectively of the specific class of

asset it refers. The results in Table 9 show that both the coefficient on the interaction term

with exposure to Greek debt and the implied value of d1 barely change in magnitude or in

significance relative to our baseline results in Table 5. The coefficient on the interaction

with aggregate foreign exposure, instead, enters with a negative sign and is not significant

in any of the three specification. Overall, these results shows that the aggregate exposure

to foreign debt has no effect on the transmission rate of Greek shocks.

Finally, we conduct a number of additional checks to verify whether our results are

robust to different definitions of Greek shocks. In the first check, we take a narrower set

of events which was labeled the restricted set of Greek events in section 2. As described

in that section, this set is obtained after taking an additional round of elimination, where

we adopt a more conservative definition of relevant financial news in other countries. The

results are shown in Table 10. Relative to our baseline results, the coefficient on the Greek

dummy (GR) rises to approximately 0.053 in all specifications and remains significant at

the one-percent level. Column I and II show that the coefficients on the interaction terms

GR∗Total and GR∗Publ increase in magnitude and are significant at the one-percent and

at the five-percent confidence level, respectively. The coefficient on GR ∗ Bank reported

in Column III remains insignificant. A similar pattern is maintained for the normalized

coefficient d1, which is strongly significant in the first two specifications while it is not so in

the third one. In addition, the values of this coefficient in the first two columns is roughly

equivalent to the ones reported in Table 5. We can therefore conclude that our results do

not change significantly when we base the selection of Greek shocks on a narrow definition.

32

Similarly, the general pattern of our results does not change when we expand the defi-

nition of Greek events to include all dates that survive the first two rounds of elimination

(see Table A2). In particular, this raw set of Greek events includes also those events that

overlap with information shocks stemming from outside Greece. Using this noisy measure

of Greek shocks should thus result in an attenuation bias of both the coefficients on the

Greek dummy and on the two interaction terms. Consistently with our expectations, the

results reported in Table 11 show that almost all estimated coefficient have lower absolute

magnitude but there is no meaningful change in the respective sign. The estimated size

of Greek shocks reported in the first row of the table is approximately equal to 0.03 in

all specifications, remaining statistically significant at the one-percent level. As for the

interaction with the measures of financial linkages, we observe a much lower coefficient in

the specification with the exposure to total Greek debt (0.0106) and only a small variation

in the coefficient corresponding to the exposure to Greek public debt (0.0086). These val-

ues results in an estimate for the normalized coefficient d1 that equals 0.3567 in the first

specification and 0.2911 in the second one, with a level of significance of five-percent in

the worst case. The value of d1 instead close to zero and statistically insignificant in the

specification with the exposure to Debt of Greek Banks. Overall, these results indicate

that our estimates of the effect of financial linkages on the transmission of sovereign risk

are very robust to the specific set of Greek events considered.

5 Conclusion

This paper has shown that financial linkages matter for the transmission of sovereign risk

in the Euro crisis. Our preferred estimates show that a 10-percent decrease in cross-

border financial exposures, corresponding to a reduction of 0.075 percent of GDP, would

decrease the spillover effects of sovereign risk by 3.4 percent. For the average country,

this corresponds to about 9.4 percent of the overall transmission rate. Similarly, a 10-

33

percent decrease in the exposure to foreign sovereign debt, corresponding to a reduction

of 0.05 percent of GDP, would decrease spillover effects by 1.8 percent. Again the average

country, this corresponds to 5 percent of the overall transmission rate. These estimates are

statistically significant and economically relevant. On the contrary, bank-to-bank lending

does not appear to matter for the transmission of sovereign risk.

Methodologically, we follow the narrative approach of Romer and Romer (1989), iden-

tifying financially relevant news shocks that can be attributed to Greece’s problems ser-

vicing its sovereign debt. These shocks are used to assess the response of sovereign risk of

other European countries. We further relate the latter responses to cross-border financial

linkages, controlling for alternative transmission channels using country-fixed effects and

within-country variation in trade linkages.

34

A The Estimator

We derive the estimator used in main body of the paper. To do so, we will proceed in

several steps. First, we state a technical result on matrix inversion, which we use later.

Second, we derive a multi-variate generalized least squares (GLS) estimator under the type

of heteroskedasticity described in the main text. Third, we describe our bootstrapping

techniques.

A.1 Matrix Algebra

Claim 1 Let Σk be a collection of n × n matrices with full rank, for k = 1, ..., K. Let

further Ik denote m × m matrices of the following form: all off-diagonal elements equal

to zero, all diagonal elements are either zero or one and the Ik sum to the unit matrix:∑k Ik = 1m. Then, (

K∑k=1

Σk ⊗ Ik

)−1=

K∑k=1

Σ−1k ⊗ Ik (9)

holds, where ⊗ symbolizes the Kronecker matrix multiplication.

Proof. Multiplication of∑

k Σk ⊗ Ik and the right hand side in (9) and exploiting the

basic properties of the Kronecker multiplication yields

(∑k

Σk ⊗ Ik

)∑k

Σ−1k ⊗ Ik =∑k

(Σk ⊗ Ik)(Σ−1k ⊗ Ik

)+∑k 6=j

(Σk ⊗ Ik)(Σ−1j ⊗ Ij

)=

∑k

ΣkΣ−1k ⊗ IkIk +∑k 6=j

ΣkΣ−1j ⊗ IkIj

=∑k

1n ⊗ Ik +∑k 6=j

ΣkΣ−1j ⊗ 0m

= 1n ⊗∑k

Ik = 1nm

35

A.2 GLS Estimator – Time-Invariant Transmission

Defining zt = [z′t,1gr,t]′ and Φ = [Φ, β], we can reformulate model (4) in the main text as

yt = Φzt + ut, (10)

where the residuals ut satisfy

Et(ut) = 0, Et(utu′t) =

Σgr if t ∈ T gr

Σngr if t 6∈ T gr

, Et(utu′s) = 0 for s 6= t (11)

with T gr being the set of greek events and Σgr and Σngr being full-ranked and thus invert-

ible. Here and in the following, Et denotes the expected value given the information set

available at period t.

Further assumptions are required to guarantee the asymptotic normality of the GLS

estimator. Following Lutkepohl (2007, p. 397), we assume throughout that the matrix Φ of

autoregressive coefficients satisfies a stability condition, and that the vector of exogenous

variables xt, which appears among the elements of zt, is generated by a stationary, stable

VAR process which is independent of the process ut.

For a model dimension n and sample size T , model (10) can be written compactly as

y = (In ⊗ Z ′)φ + u, (12)

where y is the nT × 1 vector obtained by stacking the vectors y(k) of time series for each

kth component of yt, u is similarly defined by stacking the vectors u(k) of time series of

each component of ut, In is a n-dimensional identity matrix and Z = [z1, . . . , zT ] is the

(p+ 1)× T matrix formed by the time series of vector zt. Here, p+ 1 denotes the number

of regressors in each equation of model (10), which include p = nJ + m variables plus the

36

Greek dummy. φ = [Φ′(1), Φ′(2), . . . , Φ

′(n)]′ is the n(p+ 1)× 1 vector obtained from stacking

the rows Φ(k) of matrix Φ.

Consistently with the assumptions in (11), the variance-covariance of the vector of

residuals ut satisfies

Σu = Σgr ⊗ IgrT + Σngr ⊗ IngrT .

Here IgrT is a T -dimensional diagonal matrix whose diagonal entries corresponds to the

entries of the vector [1gr,1, . . . ,1gr,T ] and IngrT = IT − IgrT . The GLS estimator of φ thus

minimizes u′(Σu)−1u and equals

φ = [(In ⊗ Z)Σ−1u (In ⊗ Z ′)]−1(In ⊗ Z)Σ−1u y. (13)

Under the assumption in (11) and the regularity conditions discussed above, we can

show

Claim 2 The GLS estimator of β converges in distribution according to

√T(φ− φ

)d−→ N(0,Q−1VQ−1),

where Q ≡ plim(T−1(In ⊗ Z)Σ−1u (In ⊗ Z ′)

)is well-defined, symmetric and non-singular

and V ≡ (In ⊗ Z)Σ−1u (In ⊗ Z ′).

Proof. Rearranging (13) we obtain

√T(φ− φ

)=

[(In ⊗ Z)Σ−1u (In ⊗ Z ′)

T

]−1(In ⊗ Z)Σ−1u u√

T. (14)

37

Expanding the term within squared brackets yields

(In ⊗ Z)Σ−1u (In ⊗ Z ′)T

=1

T

ZΩ11Z′ ZΩ12Z

′ . . . ZΩ1nZ′

ZΩ21Z′ ZΩ22Z

′ . . . ZΩ2nZ′

......

. . ....

ZΩn1Z′ ZΩn2Z

′ . . . ZΩnnZ′