41

ISSP Conference Denver Trends in Sustainability Reporting November 2014

ISSP Conference

Denver

Trends in Sustainability Reporting

November 2014

What’s in store

1.

Emerging Standards

4.

What’s driving the need

3.

Assurance readiness and assurance

Achieving credible reporting

2.

Developing trends in measurement5.

Page 2 Moving toward credible reporting

1. What’s driving the need

Page 3 Moving toward credible reporting

Not adopted► May perform some

actions that are sustainable, but does not coordinate or communicate these actions

Early stage► Encourages and

collects environmental or social activities for reporting externally

► Focus on public relations

► Limited or no stakeholder engagement

Middle pack► Operations-focused

sustainability initiative improves efficiency, such as reduced energy consumption

► Sustainability initiative outcome reported publicly via metrics

► Cost savings from initiatives may be documented

► Early relationship with stakeholders

Advanced► Well-developed

materiality process

► Beginning to integratesustainability in business processes

► Sustainability linked to enterprise strategy

► Reporting on key metrics internally as well as externally

► Closely linked financial and non-financial reporting

► Limited assurance covers reported metric data, principles

2015 leaders► Enterprise-wide

sustainability strategy ties to business objectives

► Sustainability engages the value chain to drive business objectives

► Sustainability principles embedded in key areas of business strategy, operations

► Key metrics reported internally and externally, tied to compensation

► Formal controls and processes for metric data management

► Reasonable assurance covers metric data, principles

Leaders 1995 Leaders 2005 Leaders 2015+

What it takes to be a sustainabilityleader in 2015

Page 4 Moving toward credible reporting

Wide variety of stakeholders are asking for increased transparency

Socially

responsible

investment

(SRI) groups

Certifications

Global

reporting

initiative

CDP

Climate

change and

sustainability

lawsuits

increasing

Expectations

for more

sustainable

products

SEC –

disclosure

guidance

FTC – green

guides

Corporate

initiatives

Human

Rights

Watch

EPA – GHG

reporting

Government

NGOs

Investors

Recruiting

and

retention

Industry

associations

(ACC, NAIC,

ICMM,

AAFA)

Employee

engagement

programs

EmployeesSupply chain

and industry

Customers

Communities

Permitting or

expansion

challenges

“license to

operate”

Shareholder

resolutions

Dow Jones

sustainability

index,

Bloomberg’s

ESG terminal

Customer

surveys/

questionnaires

Page 5 Moving toward credible reporting

Page 6 Moving toward credible reporting

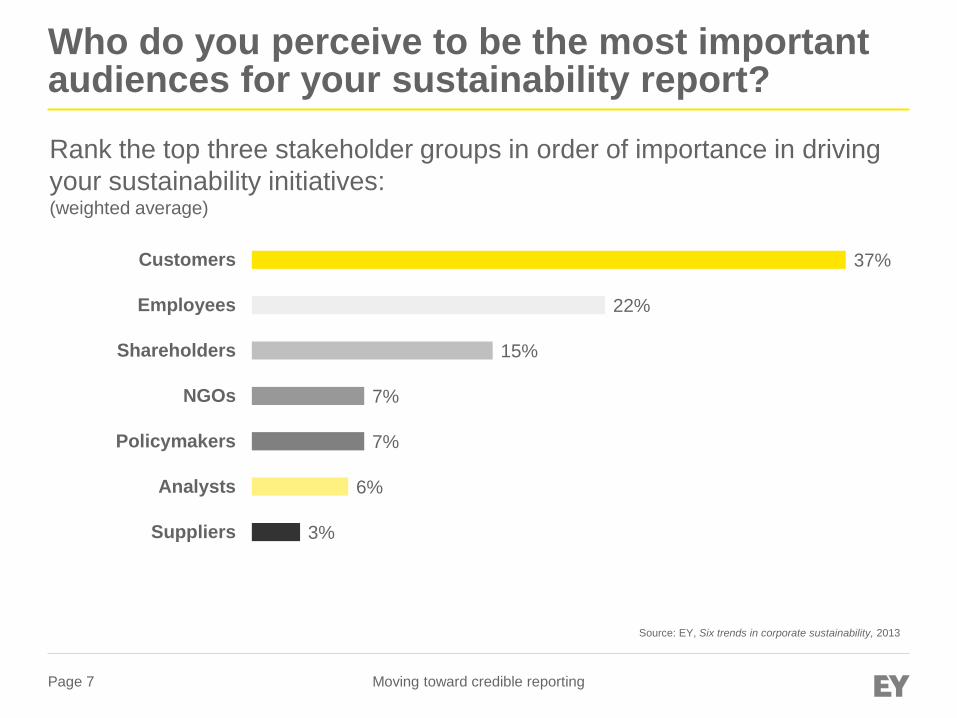

37 is

A. The age of my oldest child

B. The number of NGO’s that are focused on

carbon

C. The current temperature outside

D. The % of companies that say that their

customers are the primary audience for

their sustainability report

Page 7 Moving toward credible reporting

Who do you perceive to be the most important audiences for your sustainability report?

Rank the top three stakeholder groups in order of importance in driving

your sustainability initiatives:(weighted average)

3%

6%

7%

7%

15%

22%

37%

Suppliers

Analysts

Policymakers

NGOs

Shareholders

Employees

Customers

Source: EY, Six trends in corporate sustainability, 2013

Page 8 Moving toward credible reporting

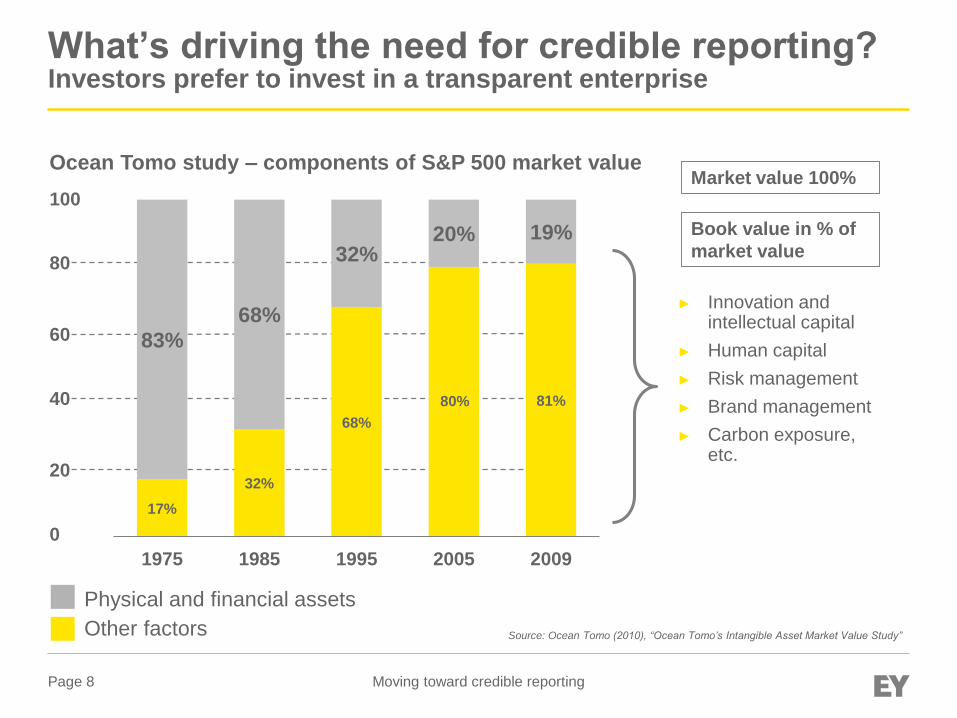

What’s driving the need for credible reporting?Investors prefer to invest in a transparent enterprise

0

20

40

60

80

100

► Innovation and intellectual capital

► Human capital

► Risk management

► Brand management

► Carbon exposure, etc.

Market value 100%

Book value in % of

market value

Physical and financial assets

Other factors Source: Ocean Tomo (2010), “Ocean Tomo’s Intangible Asset Market Value Study”

Ocean Tomo study – components of S&P 500 market value

17%

32%

68%

80% 81%

83%

68%

32%20% 19%

1975 1985 1995 2005 2009

Page 9 Moving toward credible reporting

Page 10 Moving toward credible reporting

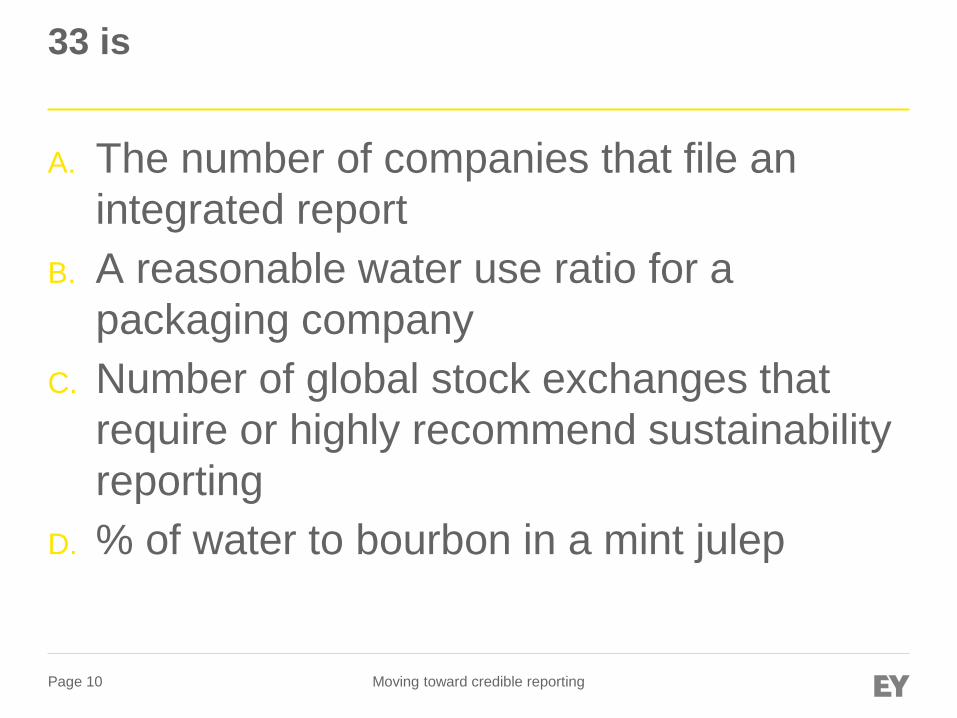

33 is

A. The number of companies that file an

integrated report

B. A reasonable water use ratio for a

packaging company

C. Number of global stock exchanges that

require or highly recommend sustainability

reporting

D. % of water to bourbon in a mint julep

Page 11 Moving toward credible reporting

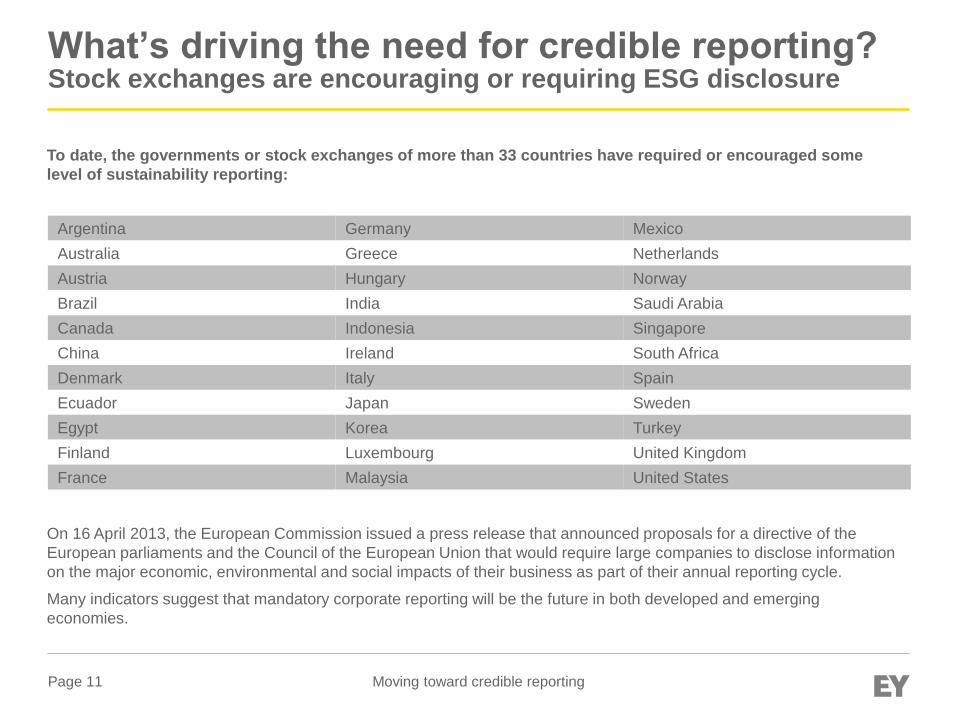

What’s driving the need for credible reporting?Stock exchanges are encouraging or requiring ESG disclosure

To date, the governments or stock exchanges of more than 33 countries have required or encouraged some

level of sustainability reporting:

On 16 April 2013, the European Commission issued a press release that announced proposals for a directive of the

European parliaments and the Council of the European Union that would require large companies to disclose information

on the major economic, environmental and social impacts of their business as part of their annual reporting cycle.

Many indicators suggest that mandatory corporate reporting will be the future in both developed and emerging

economies.

Argentina Germany Mexico

Australia Greece Netherlands

Austria Hungary Norway

Brazil India Saudi Arabia

Canada Indonesia Singapore

China Ireland South Africa

Denmark Italy Spain

Ecuador Japan Sweden

Egypt Korea Turkey

Finland Luxembourg United Kingdom

France Malaysia United States

Page 12 Moving toward credible reporting

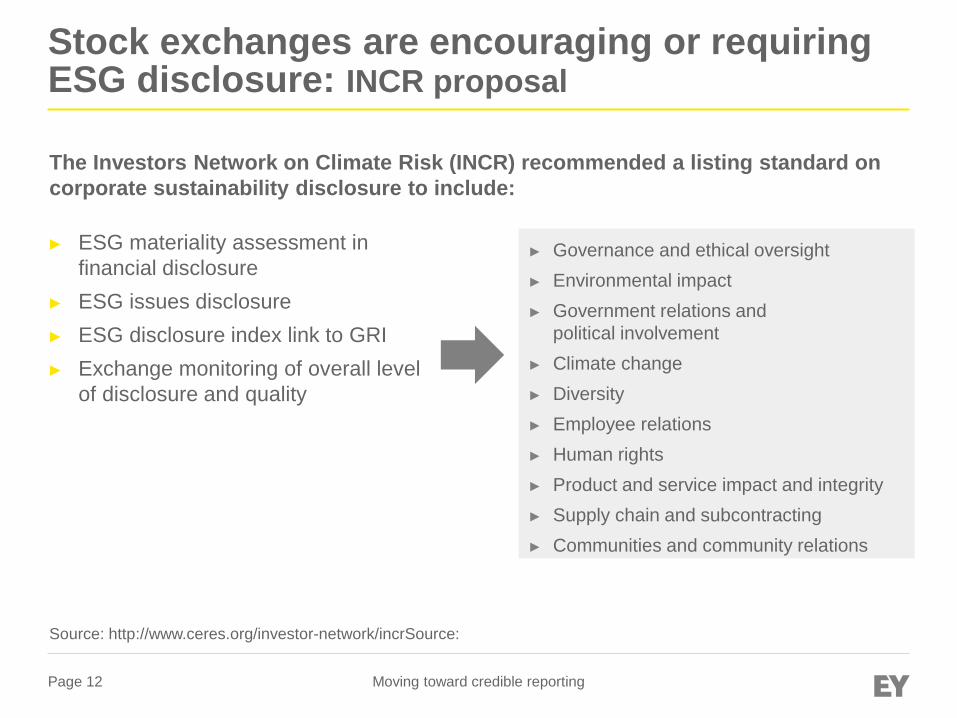

Stock exchanges are encouraging or requiring ESG disclosure: INCR proposal

► ESG materiality assessment in

financial disclosure

► ESG issues disclosure

► ESG disclosure index link to GRI

► Exchange monitoring of overall level

of disclosure and quality

► Governance and ethical oversight

► Environmental impact

► Government relations and

political involvement

► Climate change

► Diversity

► Employee relations

► Human rights

► Product and service impact and integrity

► Supply chain and subcontracting

► Communities and community relations

The Investors Network on Climate Risk (INCR) recommended a listing standard on

corporate sustainability disclosure to include:

Source: http://www.ceres.org/investor-network/incrSource:

Page 13 Moving toward credible reporting

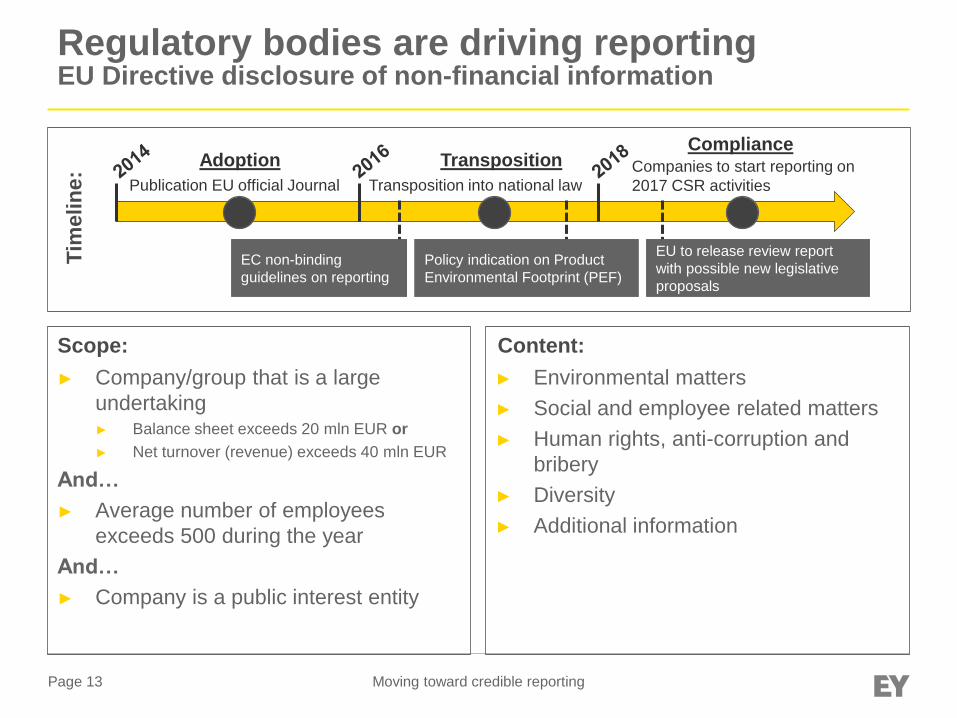

Regulatory bodies are driving reportingEU Directive disclosure of non-financial information

Tim

eli

ne

:

AdoptionCompliance

Transposition

Publication EU official Journal Transposition into national law

Companies to start reporting on

2017 CSR activities

EC non-binding

guidelines on reporting

Policy indication on Product

Environmental Footprint (PEF)

EU to release review report

with possible new legislative

proposals

Scope:

► Company/group that is a large

undertaking► Balance sheet exceeds 20 mln EUR or

► Net turnover (revenue) exceeds 40 mln EUR

And…

► Average number of employees

exceeds 500 during the year

And…

► Company is a public interest entity

Content:

► Environmental matters

► Social and employee related matters

► Human rights, anti-corruption and

bribery

► Diversity

► Additional information

Page 14 Moving toward credible reporting

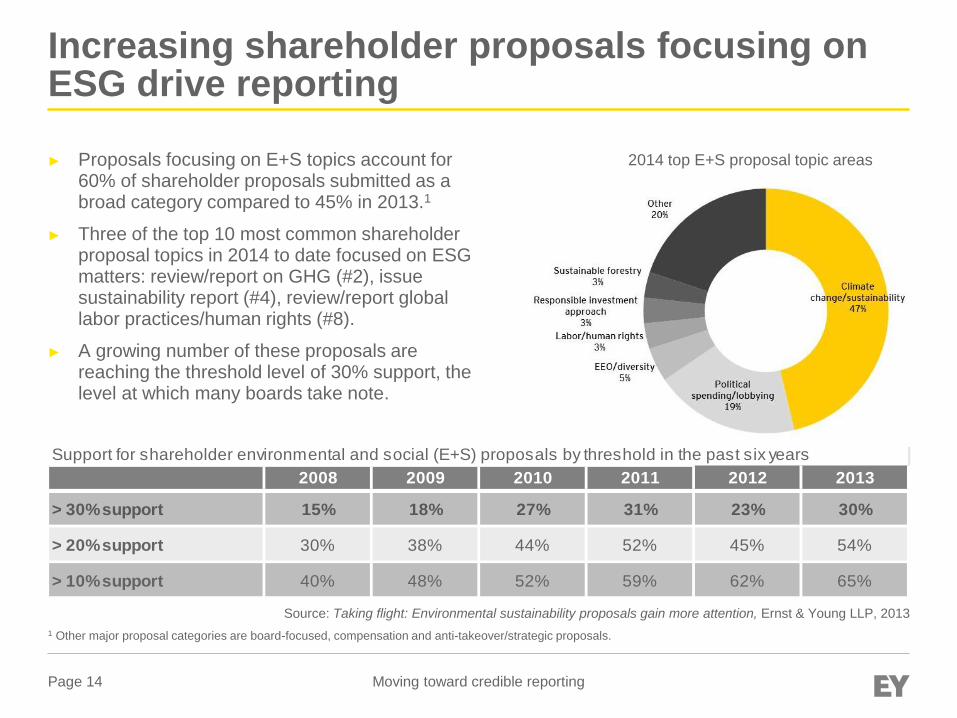

Support for shareholder environmental and social (E+S) proposals by threshold in the past six years

2008 2009 2010 2011 2012 2013

> 30% support 15% 18% 27% 31% 23% 30%

> 20% support 30% 38% 44% 52% 45% 54%

> 10% support 40% 48% 52% 59% 62% 65%

Increasing shareholder proposals focusing on ESG drive reporting

► Proposals focusing on E+S topics account for 60% of shareholder proposals submitted as a broad category compared to 45% in 2013.1

► Three of the top 10 most common shareholder proposal topics in 2014 to date focused on ESG matters: review/report on GHG (#2), issue sustainability report (#4), review/report global labor practices/human rights (#8).

► A growing number of these proposals are reaching the threshold level of 30% support, the level at which many boards take note.

Source: Taking flight: Environmental sustainability proposals gain more attention, Ernst & Young LLP, 2013

1 Other major proposal categories are board-focused, compensation and anti-takeover/strategic proposals.

2014 top E+S proposal topic areas

Page 15 Moving toward credible reporting

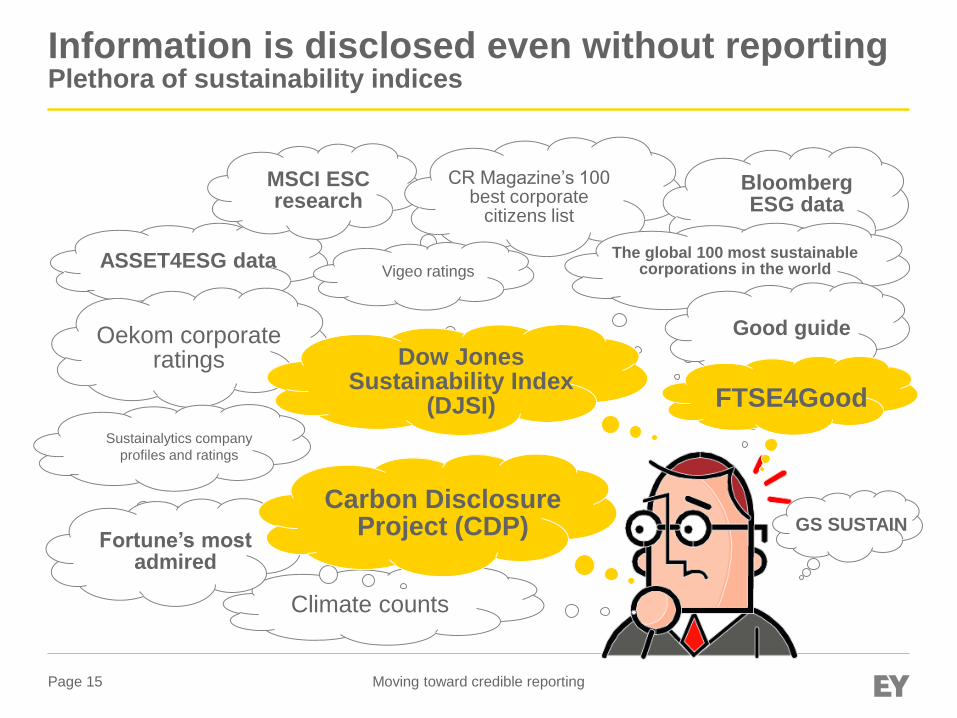

ASSET4ESG data

MSCI ESC research

Information is disclosed even without reportingPlethora of sustainability indices

CR Magazine’s 100 best corporate

citizens list

Oekom corporate ratings

BloombergESG data

The global 100 most sustainable corporations in the world

GS SUSTAIN

Vigeo ratings

Climate counts

Good guide

Sustainalytics company

profiles and ratings

Fortune’s most admired

Dow Jones Sustainability Index

(DJSI)

Carbon Disclosure Project (CDP)

FTSE4Good

Page 16 Moving toward credible reporting

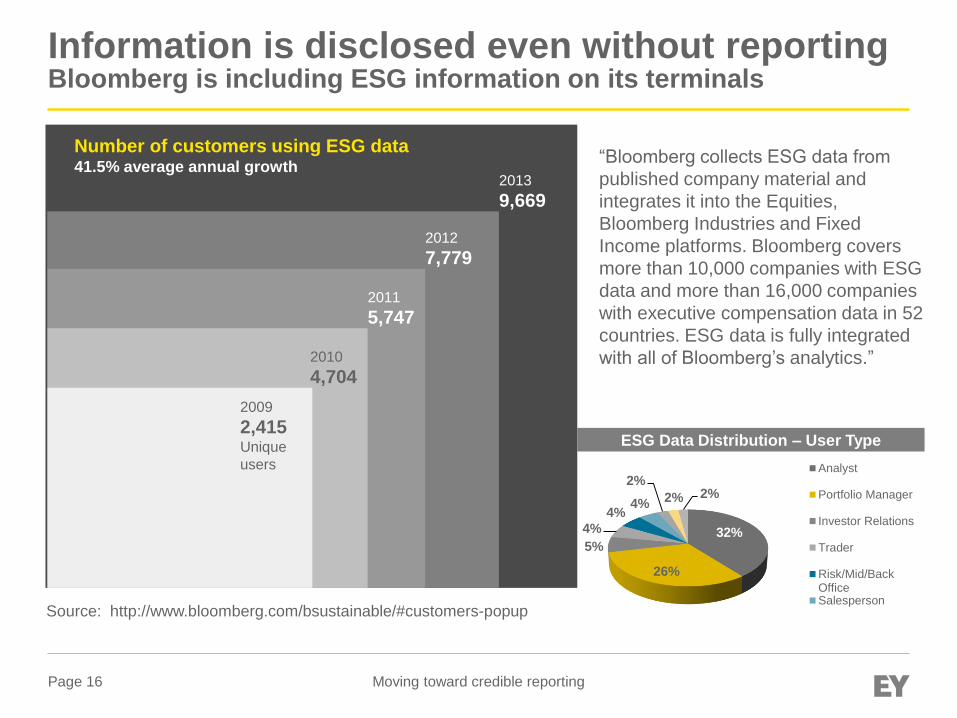

Number of customers using ESG data41.5% average annual growth

Information is disclosed even without reportingBloomberg is including ESG information on its terminals

“Bloomberg collects ESG data from

published company material and

integrates it into the Equities,

Bloomberg Industries and Fixed

Income platforms. Bloomberg covers

more than 10,000 companies with ESG

data and more than 16,000 companies

with executive compensation data in 52

countries. ESG data is fully integrated

with all of Bloomberg’s analytics.”

Source: http://www.bloomberg.com/bsustainable/#customers-popup

2012

7,779

2011

5,747

2010

4,704

2009

2,415Unique

users

32%

26%

5%

4%

4%4%

2%

2% 2%

Analyst

Portfolio Manager

Investor Relations

Trader

Risk/Mid/BackOfficeSalesperson

ESG Data Distribution – User Type

2013

9,669

Page 17 Moving toward credible reporting

Information is disclosed even without reportingImpact of social media and proactive response

What is being said about your company and its products?

By who? Why?

Where do your customers go to validate information about you?

Page 18 Moving toward credible reporting

2. Emerging Reporting Standards

Page 19 Moving toward credible reporting

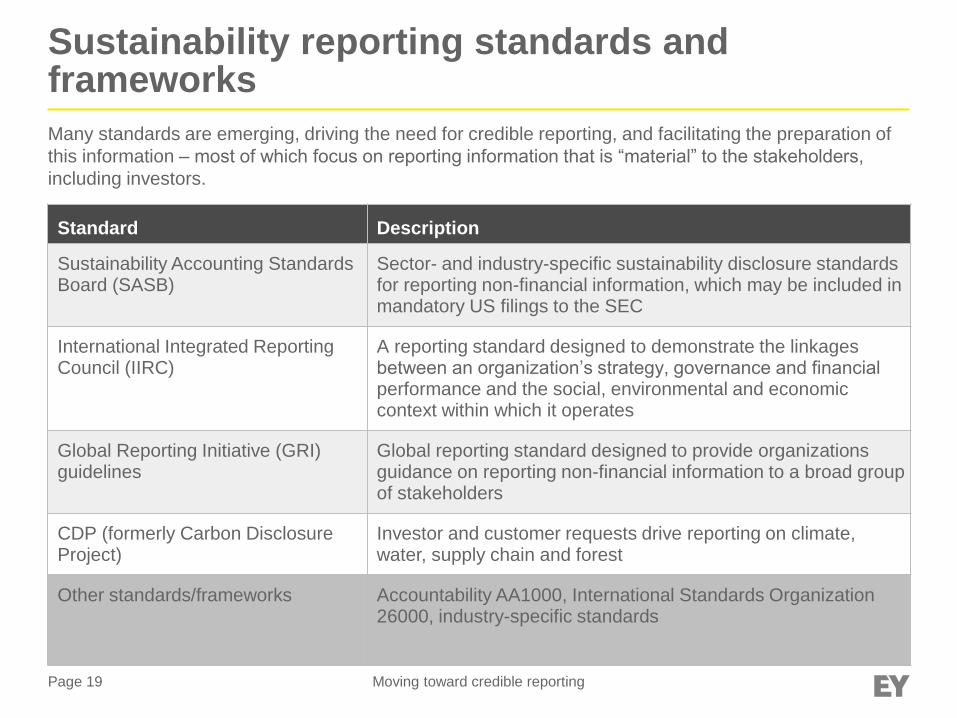

Sustainability reporting standards and frameworks

Many standards are emerging, driving the need for credible reporting, and facilitating the preparation of

this information – most of which focus on reporting information that is “material” to the stakeholders,

including investors.

Standard Description

Sustainability Accounting Standards Board (SASB)

Sector- and industry-specific sustainability disclosure standards for reporting non-financial information, which may be included in mandatory US filings to the SEC

International Integrated Reporting Council (IIRC)

A reporting standard designed to demonstrate the linkages between an organization’s strategy, governance and financial performance and the social, environmental and economic context within which it operates

Global Reporting Initiative (GRI) guidelines

Global reporting standard designed to provide organizations guidance on reporting non-financial information to a broad group of stakeholders

CDP (formerly Carbon Disclosure Project)

Investor and customer requests drive reporting on climate, water, supply chain and forest

Other standards/frameworks Accountability AA1000, International Standards Organization 26000, industry-specific standards

Page 20 Moving toward credible reporting

Legend:

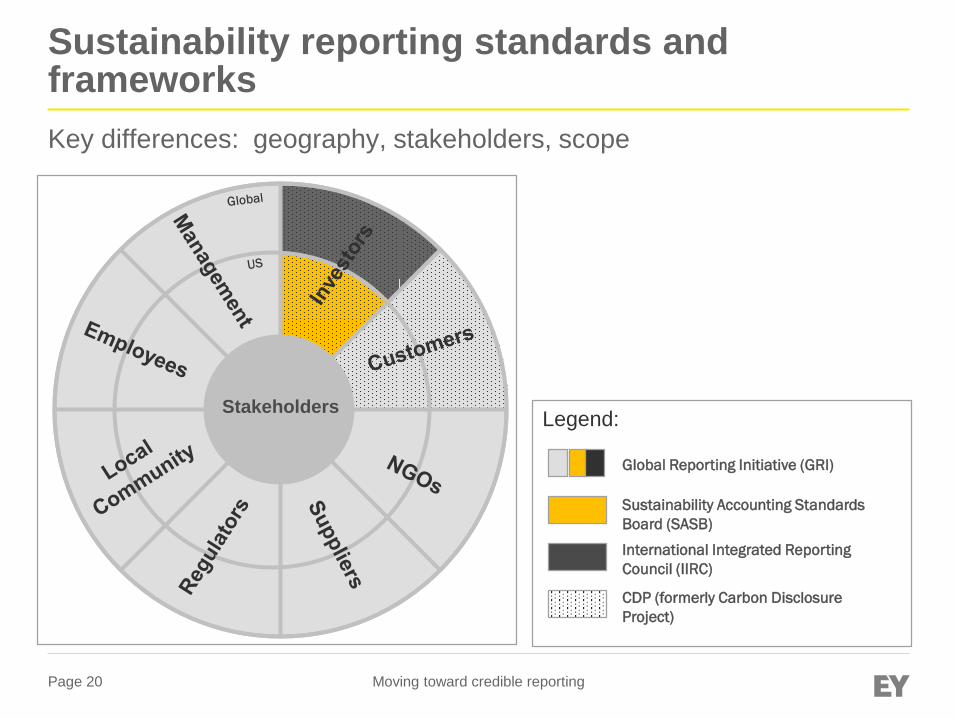

Sustainability reporting standards and frameworks

Key differences: geography, stakeholders, scope

Global Reporting Initiative (GRI)

Sustainability Accounting Standards

Board (SASB)

International Integrated Reporting

Council (IIRC)

CDP (formerly Carbon Disclosure

Project)

Stakeholders

Page 21 Moving toward credible reporting

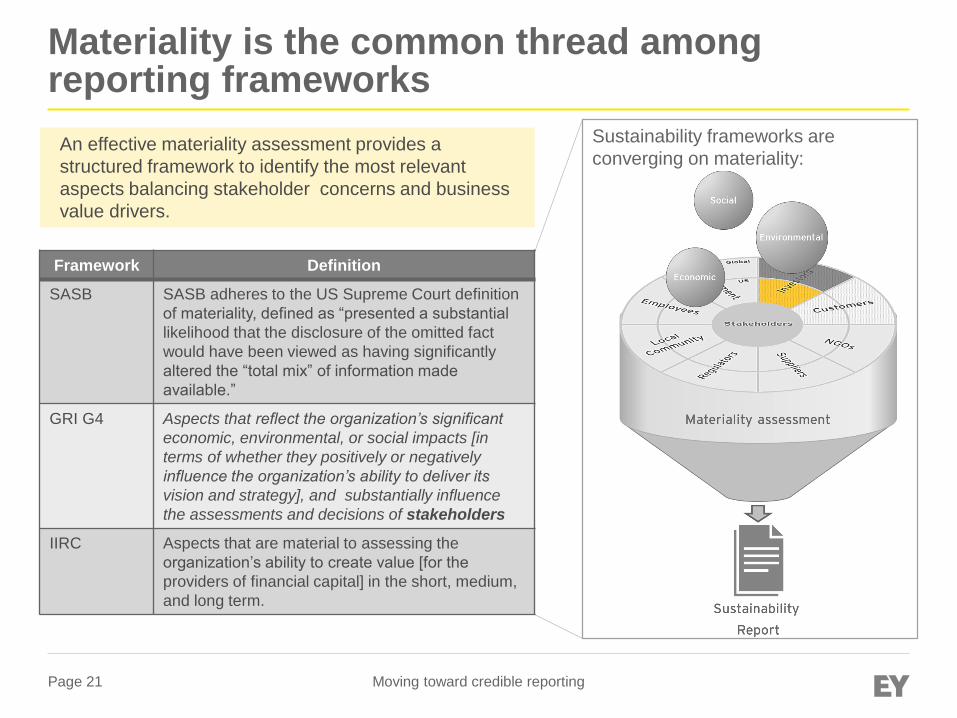

Materiality is the common thread among reporting frameworks

An effective materiality assessment provides a

structured framework to identify the most relevant

aspects balancing stakeholder concerns and business

value drivers.

Sustainability frameworks are

converging on materiality:

Framework Definition

SASB SASB adheres to the US Supreme Court definition

of materiality, defined as “presented a substantial

likelihood that the disclosure of the omitted fact

would have been viewed as having significantly

altered the “total mix” of information made

available.”

GRI G4 Aspects that reflect the organization’s significant

economic, environmental, or social impacts [in

terms of whether they positively or negatively

influence the organization’s ability to deliver its

vision and strategy], and substantially influence

the assessments and decisions of stakeholders

IIRC Aspects that are material to assessing the

organization’s ability to create value [for the

providers of financial capital] in the short, medium,

and long term.

Page 22 Moving toward credible reporting

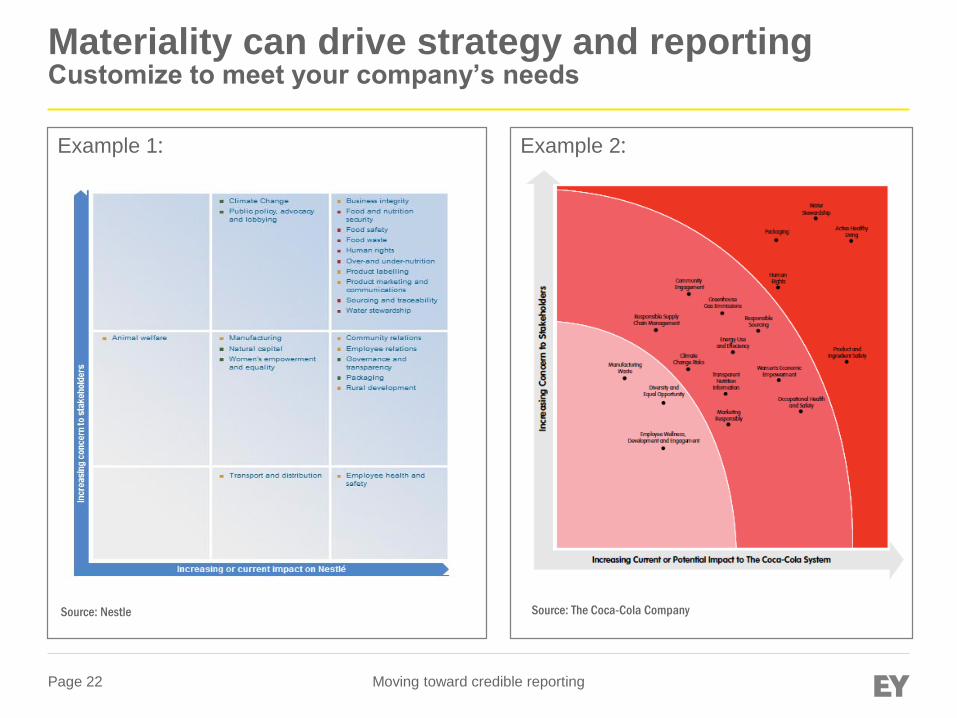

Example 1:

Materiality can drive strategy and reportingCustomize to meet your company’s needs

Source: Nestle

Example 2:

Source: The Coca-Cola Company

Page 23 Moving toward credible reporting

Page 24 Moving toward credible reporting

72 is

A. A reasonable lost days number for a

manufacturing company

B. My age in dog years

C. % of global 50 that have a focus on water

D. % of S&P 500 companies published a

sustainability report in 2013

Page 25 Moving toward credible reporting

Current reporting trends

► 72% of S&P 500 companies published a sustainability

report in 2013, compared with 20% in 2011

► 90% of the world’s largest 250 companies issued a

Corporate Responsibility report, 82% of which refer to the

GRI guidelines

► The number of US companies reporting with GRI

Guidelines has doubled in the past 5 years up to 266

reports in total

► In 2013, approximately 16% of US-based companies

published a third-party assured, GRI-based sustainability

report, as opposed to 10% in 2011

Source: GRI, Trends in External Assurance of Sustainability Reports: Update on the USA, July 2014

Page 26 Moving toward credible reporting

3. Achieving Credible Reporting

Page 27 Moving toward credible reporting

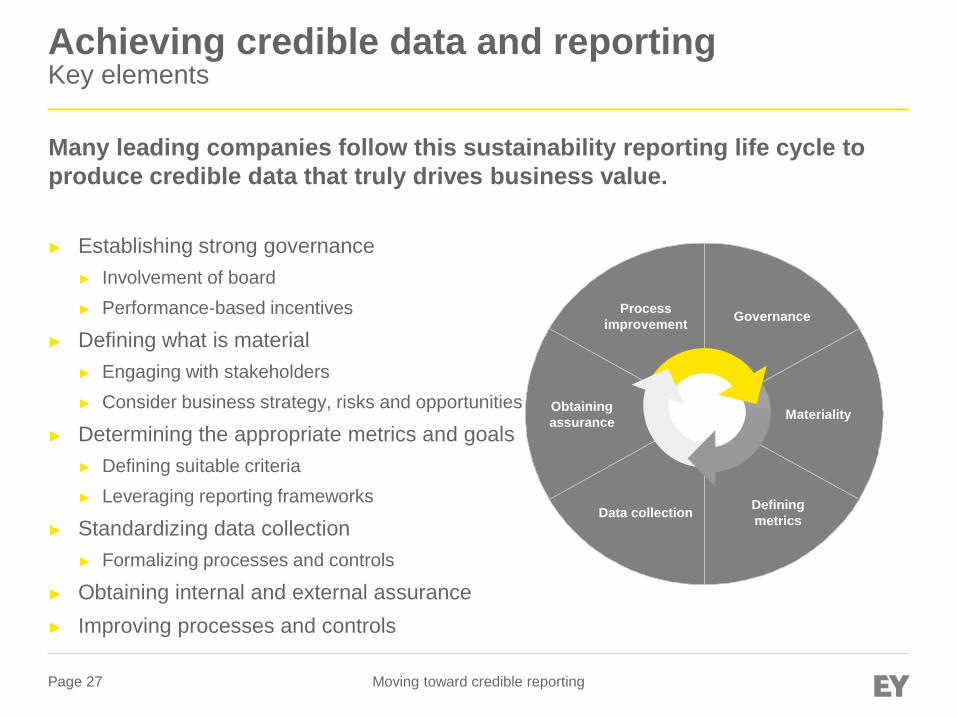

Achieving credible data and reportingKey elements

► Establishing strong governance

► Involvement of board

► Performance-based incentives

► Defining what is material

► Engaging with stakeholders

► Consider business strategy, risks and opportunities

► Determining the appropriate metrics and goals

► Defining suitable criteria

► Leveraging reporting frameworks

► Standardizing data collection

► Formalizing processes and controls

► Obtaining internal and external assurance

► Improving processes and controls

Many leading companies follow this sustainability reporting life cycle to

produce credible data that truly drives business value.

Obtaining

assuranceMateriality

Defining

metricsData collection

Governance Process

improvement

Page 28 Moving toward credible reporting

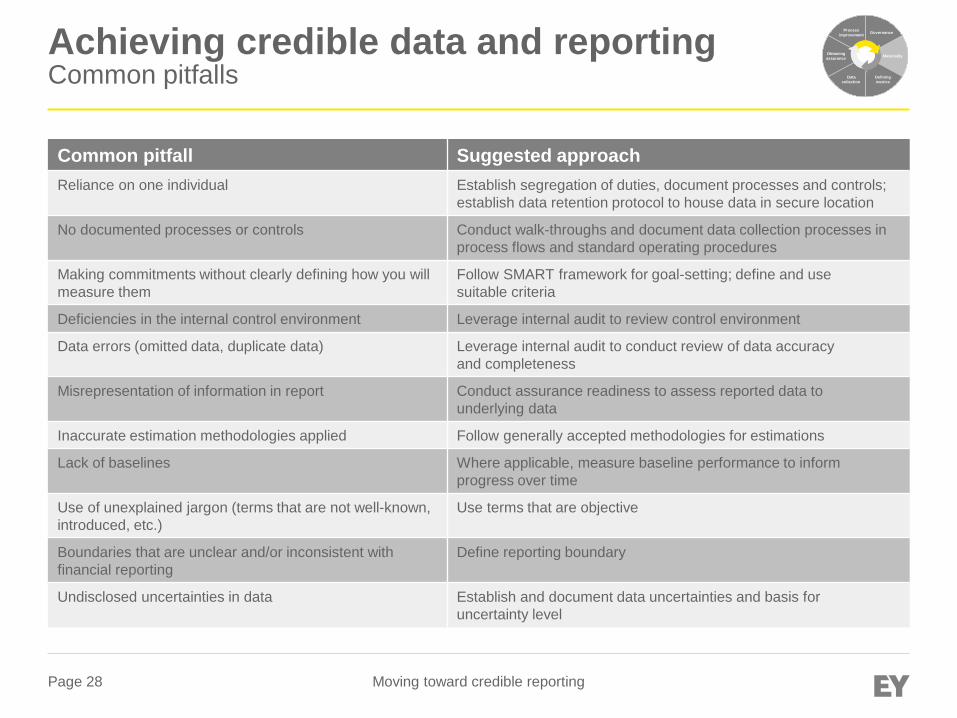

Achieving credible data and reportingCommon pitfalls

Common pitfall Suggested approach

Reliance on one individual Establish segregation of duties, document processes and controls;

establish data retention protocol to house data in secure location

No documented processes or controls Conduct walk-throughs and document data collection processes in

process flows and standard operating procedures

Making commitments without clearly defining how you will

measure them

Follow SMART framework for goal-setting; define and use

suitable criteria

Deficiencies in the internal control environment Leverage internal audit to review control environment

Data errors (omitted data, duplicate data) Leverage internal audit to conduct review of data accuracy

and completeness

Misrepresentation of information in report Conduct assurance readiness to assess reported data to

underlying data

Inaccurate estimation methodologies applied Follow generally accepted methodologies for estimations

Lack of baselines Where applicable, measure baseline performance to inform

progress over time

Use of unexplained jargon (terms that are not well-known,

introduced, etc.)

Use terms that are objective

Boundaries that are unclear and/or inconsistent with

financial reporting

Define reporting boundary

Undisclosed uncertainties in data Establish and document data uncertainties and basis for

uncertainty level

Obtaining

assuranceMateriality

Defining

metrics

Data

collection

Governance Process

improvement

Page 29 Moving toward credible reporting

Achieving credible data and reportingAssurance readiness

► As you drive toward preparing credible data, consider conducting

assurance readiness to understand the level of assurance and

completeness in the existing data, as well as potential process and

control gaps that are causing material misstatements.

► Inquiry about the nature of significant judgments and estimates made by management

► Inquiry about any uncertainties regarding measurements

► Evaluation of whether assumptions have a reasonable basis

► Walk-through of data collection process

► Site visits

► Tracing information to supporting documents

► Analytical procedures (e.g., year-over-year fluctuations)

Obtaining

assuranceMateriality

Defining

metrics

Data

collection

Governance Process

improvement

Page 30 Moving toward credible reporting

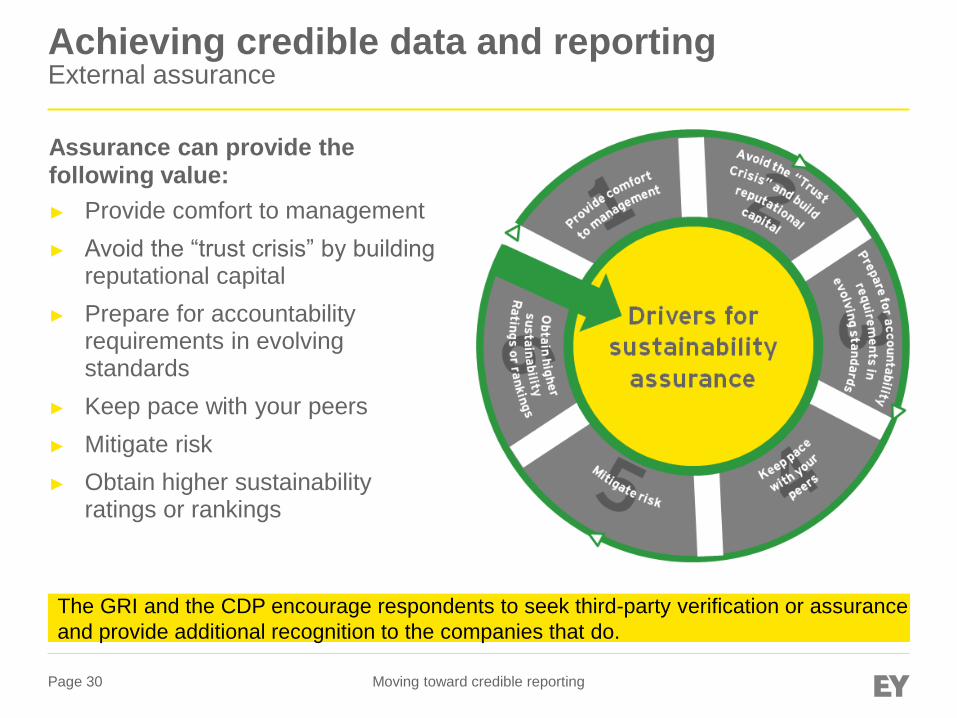

Achieving credible data and reportingExternal assurance

The GRI and the CDP encourage respondents to seek third-party verification or assurance

and provide additional recognition to the companies that do.

Assurance can provide the following value:

► Provide comfort to management

► Avoid the “trust crisis” by building reputational capital

► Prepare for accountability requirements in evolving standards

► Keep pace with your peers

► Mitigate risk

► Obtain higher sustainability ratings or rankings

Page 31 Moving toward credible reporting

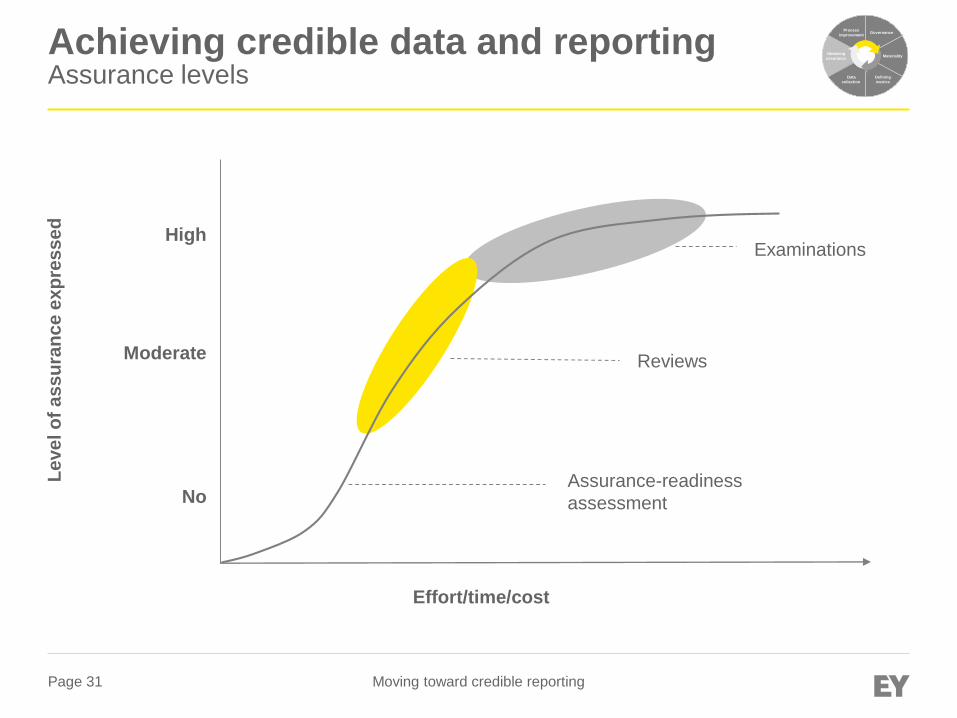

Achieving credible data and reportingAssurance levels

High

Moderate

No

Effort/time/cost

Level o

f assu

ran

ce e

xp

ressed

Examinations

Reviews

Assurance-readiness

assessment

Obtaining

assuranceMateriality

Defining

metrics

Data

collection

Governance Process

improvement

Page 32 Moving toward credible reporting

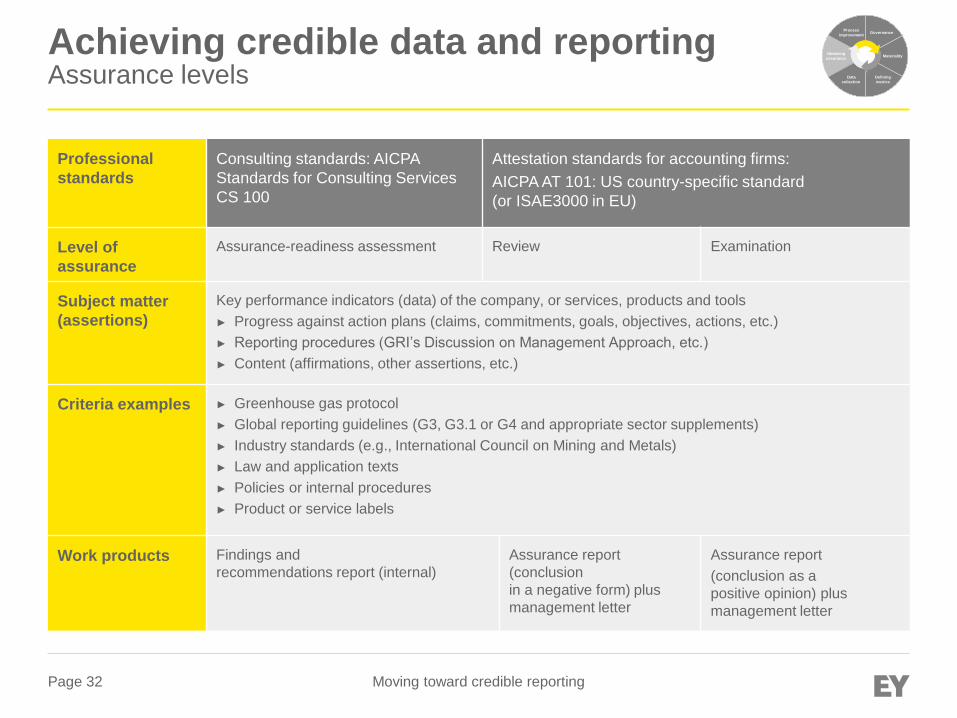

Professional

standards

Consulting standards: AICPA

Standards for Consulting Services

CS 100

Attestation standards for accounting firms:

AICPA AT 101: US country-specific standard

(or ISAE3000 in EU)

Level of

assurance

Assurance-readiness assessment Review Examination

Subject matter

(assertions)

Key performance indicators (data) of the company, or services, products and tools

► Progress against action plans (claims, commitments, goals, objectives, actions, etc.)

► Reporting procedures (GRI’s Discussion on Management Approach, etc.)

► Content (affirmations, other assertions, etc.)

Criteria examples ► Greenhouse gas protocol

► Global reporting guidelines (G3, G3.1 or G4 and appropriate sector supplements)

► Industry standards (e.g., International Council on Mining and Metals)

► Law and application texts

► Policies or internal procedures

► Product or service labels

Work products Findings and

recommendations report (internal)

Assurance report

(conclusion

in a negative form) plus

management letter

Assurance report

(conclusion as a

positive opinion) plus

management letter

Achieving credible data and reportingAssurance levels

Obtaining

assuranceMateriality

Defining

metrics

Data

collection

Governance Process

improvement

Page 33 Moving toward credible reporting

Characteristics of a credible report

► Follows an established framework

► Presents transparent and balanced disclosure

► Offers context-based reporting

► Focuses on material topics

► Aligns with stakeholder expectations and significant impacts

by and to the business

► Shows how goals and commitments significantly influence and drive the

strategy and operations of the business

► Includes content that has been externally assured to build both internal and

external confidence and credibility

A credible report:

Page 34 Moving toward credible reporting

4. Trends in measurement

Page 35 Moving toward credible reporting

What’s developing in measurement and reporting

► Outcome vs. input or output measures

► More expansive social impact

measurement

► Natural Capital Valuation

► 3BL (triple bottom line) capital allocation

and decision making

Page 36 Moving toward credible reporting

Let’s talk: sustainabilityA new point of view for business leaders

Sustainability on the go

Access our thought

leadership anywhere with

EY Insights, our new

mobile app.

Visit

ey.com/us/sustainability

to download the report

Page 37 Moving toward credible reporting

Continue the conversation

Chris Hagler

SE Leader, Climate Change and Sustainability

ISSP member and certificate holder

Atlanta, GA

+1 404 817 5799

EY | Assurance | Tax | Transactions | Advisory

About EY

EY is a global leader in assurance, tax, transaction and

advisory services. The insights and quality services we

deliver help build trust and confidence in the capital

markets and in economies the world over. We develop

outstanding leaders who team to deliver on our

promises to all of our stakeholders. In so doing, we play

a critical role in building a better working world for our

people, for our clients and for our communities.

EY refers to the global organization, and may refer to

one or more, of the member firms of Ernst & Young

Global Limited, each of which is a separate legal entity.

Ernst & Young Global Limited, a UK company limited by

guarantee, does not provide services to clients. For more

information about our organization, please visit ey.com.

Ernst & Young LLP is a client-serving member firm of

Ernst & Young Global Limited operating in the US.

© 2014 Ernst & Young LLP.

All Rights Reserved.

1403-1213903

ED None

This material has been prepared for general informational purposes

only and is not intended to be relied upon as accounting, tax, or other

professional advice. Please refer to your advisors for specific advice.

ey.com

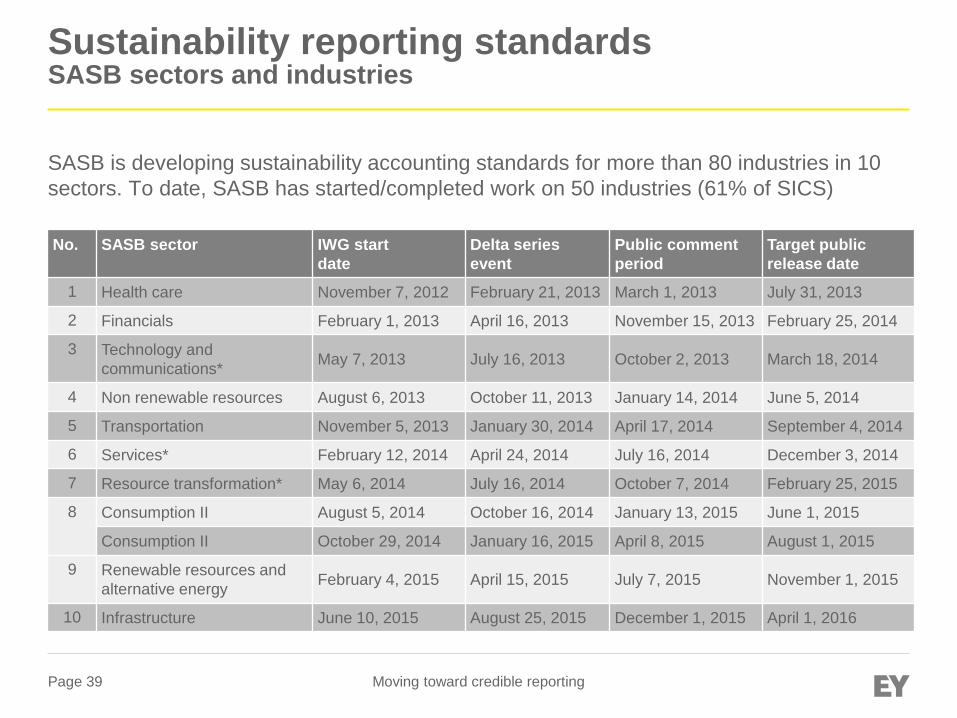

Page 39 Moving toward credible reporting

Sustainability reporting standards SASB sectors and industries

SASB is developing sustainability accounting standards for more than 80 industries in 10

sectors. To date, SASB has started/completed work on 50 industries (61% of SICS)

No. SASB sector IWG start

date

Delta series

event

Public comment

period

Target public

release date

1 Health care November 7, 2012 February 21, 2013 March 1, 2013 July 31, 2013

2 Financials February 1, 2013 April 16, 2013 November 15, 2013 February 25, 2014

3 Technology and

communications*May 7, 2013 July 16, 2013 October 2, 2013 March 18, 2014

4 Non renewable resources August 6, 2013 October 11, 2013 January 14, 2014 June 5, 2014

5 Transportation November 5, 2013 January 30, 2014 April 17, 2014 September 4, 2014

6 Services* February 12, 2014 April 24, 2014 July 16, 2014 December 3, 2014

7 Resource transformation* May 6, 2014 July 16, 2014 October 7, 2014 February 25, 2015

8 Consumption II August 5, 2014 October 16, 2014 January 13, 2015 June 1, 2015

Consumption II October 29, 2014 January 16, 2015 April 8, 2015 August 1, 2015

9 Renewable resources and

alternative energyFebruary 4, 2015 April 15, 2015 July 7, 2015 November 1, 2015

10 Infrastructure June 10, 2015 August 25, 2015 December 1, 2015 April 1, 2016

Page 40 Moving toward credible reporting

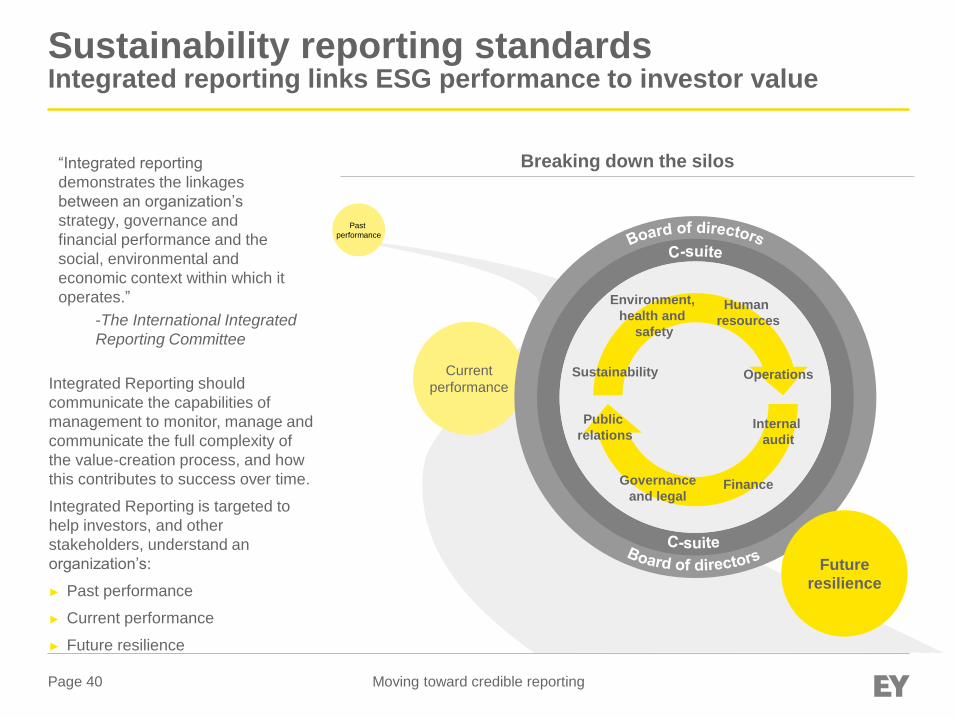

Integrated Reporting should

communicate the capabilities of

management to monitor, manage and

communicate the full complexity of

the value-creation process, and how

this contributes to success over time.

Integrated Reporting is targeted to

help investors, and other

stakeholders, understand an

organization’s:

► Past performance

► Current performance

► Future resilience

Breaking down the silos

Past

performance

Current

performance

Environment,

health and

safety

Finance

Public

relations

Operations

Human

resources

Sustainability

Governance

and legal

Internal

audit

Futureresilience

“Integrated reporting

demonstrates the linkages

between an organization’s

strategy, governance and

financial performance and the

social, environmental and

economic context within which it

operates.”

-The International Integrated

Reporting Committee

Sustainability reporting standardsIntegrated reporting links ESG performance to investor value