Trump versus Clinton – the economic and financial implications of the 2016 US presidential election Follow us on Twitter @Danske_Research Important disclosures and certifications are contained from page 49 of this report. 7 October 2016 Investment Research www.danskebank.com/CI Mikael Olai Milhøj Senior Analyst [email protected]Thomas Harr Global Head of FICC Research [email protected]Arne Lohmann Rasmussen Chief Analyst [email protected]Christian Tegllund Blaabjerg Senior Strategist [email protected]Jakob Ekholdt Christensen Chief Analyst [email protected]Vladimir Miklashevsky Senior Analyst [email protected]Aila Mihr First Year Analyst [email protected]Las Olsen Chief Economist, Denmark [email protected]

Transcript

Trump versus Clinton – the economic and financial

implications of the 2016 US presidential election

Follow us on Twitter @Danske_Research

Important disclosures and certifications are contained from page 49 of this report.

TTIPPreviously called it an "economic NATO", no comments recently

No comments on TTIP but given his protectionist stance does not bode well

China Status quoMore aggressive against China as China breaks trade policy rules

OverallLikely she will abandon protectionist stance when elected, may face resistance from Congress

Aggressive protectionist trade policy, risking a global trade war

Stance Status quoAgainst low rate policy, Fed to become more hawkish to offset more expansionary fiscal policy

Fed chair Reappointment of Fed chair Yellen in 2018To replace Fed chair Yellen, uncertainty over independence

Foreign policy Status quoSubstantially more hawkish against free trade, significant regime shift

Immigration Status quo Substantially more hawkish vs immigrants

Fiscal policy

Trade policy

Monetary

policy

22

Ahead of Election Day, markets could move with opinion polls and the odds on the outcome being offered by

bookmakers. This will especially be the case if Trump gains momentum and takes the lead in the polls.

Key takeaways – market implications

Source: Danske Bank Markets estimates

3

Clinton ahead and gap is widening again

44

Hillary Clinton ahead in most polls and gap has widened again

Clinton leading but gap has closed significantly… … Clinton still seems to be the most likely winner

Note: the probability of winning the next presidential election is calculated by FiveThirtyEight in

their polls-only model based on state and national polls.

Source: fivethirtyeight.com

Source: realclearpolitics.com

55

538 electoral votes – 270 to win

Current US electoral map - green states indicate a close race in recent state polls

• Number of electoral voters in a given state is equal to the total number of seats in Congress => Populated states are hence most important

• Florida, Ohio, Virginia, Pennsylvania and Wisconsin (all toss-up states currently) hold 90 electoral votes.

• Since 1964, Ohio and Florida have voted for the winning candidate every time except in 1992 when Florida had a Republican majority and Bill Clinton won.

Note: Number indicates electoral votes. Hawaii and D.C. are solid Democratic and Alaska is solid Republican

Source: realclearpolitics.com

Division of electoral votes – Clinton

still missing 65 electoral votes

66Source: Bloomberg, Wikipedia

US election – timetable

08 November: Election Day

26 September: firstpresidential debate

04 October: vicepresidential debate

09 October: secondpresidential debate

19 October: third and final presidential debate

20 January 2017:

inauguration of the new president and vice president

In the meantime, markets are set to focus on opinion polls and odds on the

outcome being offered by bookmakers

(but be careful, they may send a false signal)

7

Check-and-balance system limits presidential

powers

88

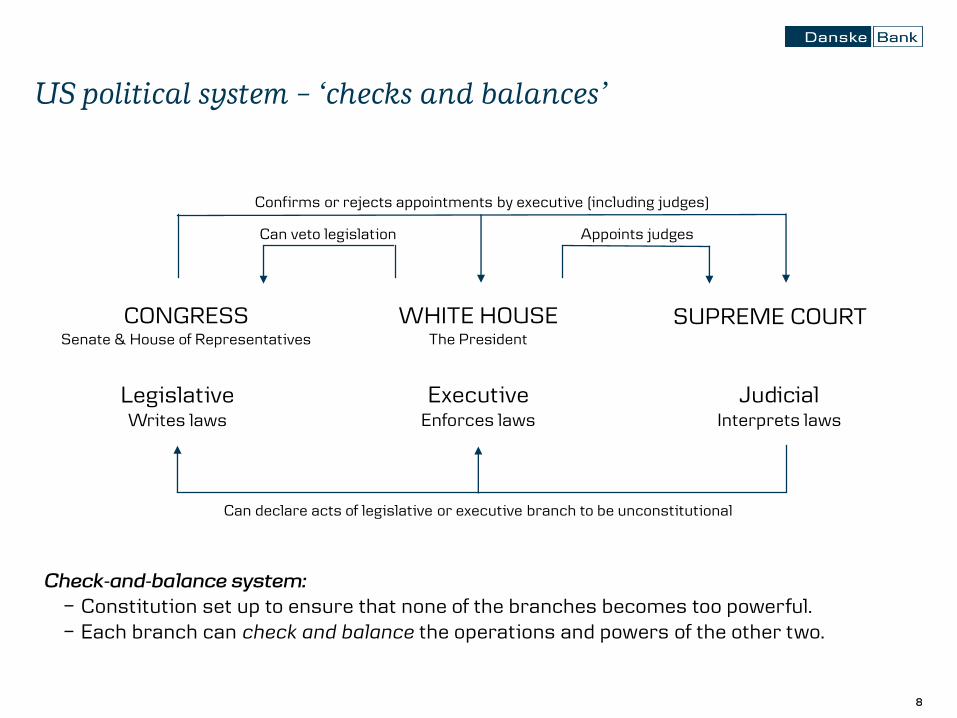

US political system – ‘checks and balances’

LegislativeWrites laws

ExecutiveEnforces laws

JudicialInterprets laws

Can veto legislation Appoints judges

Confirms or rejects appointments by executive (including judges)

Can declare acts of legislative or executive branch to be unconstitutional

Check-and-balance system: − Constitution set up to ensure that none of the branches becomes too powerful.− Each branch can check and balance the operations and powers of the other two.

CONGRESSSenate & House of Representatives

WHITE HOUSEThe President

SUPREME COURT

99

• Sign or veto legislation (return to Congress with a veto message suggesting changes – must approve all of a bill or none of it, cannot veto selectively).Veto can be overridden by two-thirds vote in both chambers (difficult and rare).

• Can issue executive orders (have the full force of a law but without Congressional approval) –subject to judicial review (Supreme Court has upheld all but two legal challenges). Congress has the power to overturn an executive order by passing legislation in conflict with it, which, however, the president can veto. The latter explains why this is extremely rare.

• Responsible for preparing the US budget although Congress must approve it.

• Can recommend legislation.

• State of the Union speech to a joint Congress (and the American people through television/media coverage).

Source: Wikipedia, US gov info

Powers of the president – legislation

1010

• Commander in Chief of the armed forces (defence budget set by Congress).

• Congress holds the power to declare war but as Commander in Chief the president can send troops without declaration (or make an executive order).

• The President holds summits with other world leaders.

• The President negotiates treaties with other countries, which need to be ratified by two-thirds of the Senate.

Source: Wikipedia, US gov info

Powers of the president – foreign affairs

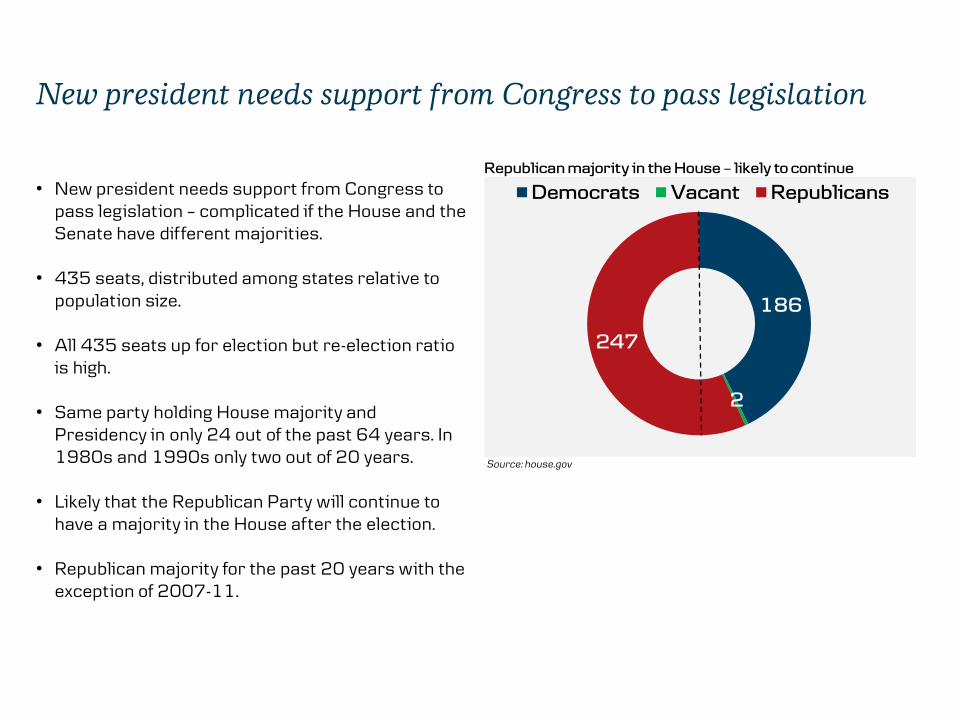

New president needs support from Congress to pass legislation

• New president needs support from Congress to pass legislation – complicated if the House and the Senate have different majorities.

• 435 seats, distributed among states relative to population size.

• All 435 seats up for election but re-election ratio is high.

• Same party holding House majority and Presidency in only 24 out of the past 64 years. In 1980s and 1990s only two out of 20 years.

• Likely that the Republican Party will continue to have a majority in the House after the election.

• Republican majority for the past 20 years with the exception of 2007-11.

Republican majority in the House – likely to continue

186

2

247

Democrats Vacant Republicans

Source: house.gov

1212

• 100 seats, two from each state. Republican majority currently. 34 seats up for election.

• 24 out of the 34 seats up for election are held by Republicans, 10 by Democrats.

• Still a long way to the so-called super majority of 60 seats, which makes the legislation process easier (prevents filibustering).

Majority in the Senate could shift to the Democrats

Republicans hold 24 of the 34 seats up for election

• Six out of seven toss-up states are currently held by Republicans.

• Democrats need to win 15 seats out of 34 to get majority, Republicans need 21 => likely that the majority could shift to the Democrats.

• Increases the likelihood of a divided Congress, which complicates legislation.

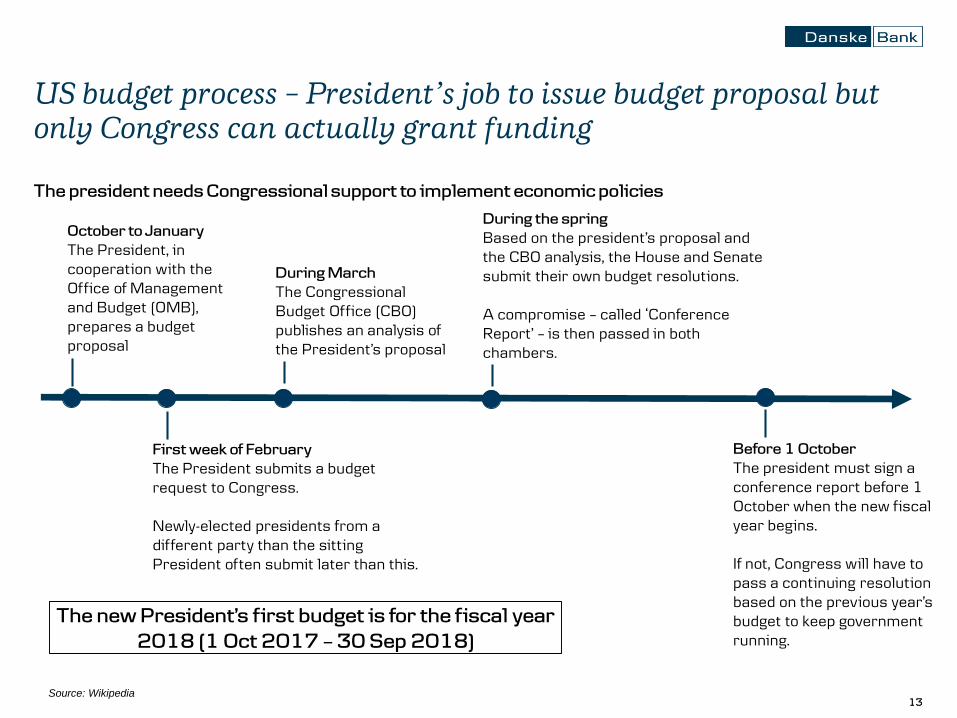

US budget process – President’s job to issue budget proposal but

only Congress can actually grant funding

First week of February

The President submits a budget request to Congress.

Newly-elected presidents from a different party than the sitting President often submit later than this.

During March

The Congressional Budget Office (CBO) publishes an analysis of the President’s proposal

During the spring

Based on the president’s proposal and the CBO analysis, the House and Senate submit their own budget resolutions.

A compromise – called ‘Conference Report’ – is then passed in both chambers.

Before 1 October

The president must sign a conference report before 1 October when the new fiscal year begins.

If not, Congress will have to pass a continuing resolution based on the previous year’s budget to keep government running.

October to January

The President, in cooperation with the Office of Management and Budget (OMB), prepares a budget proposal

The president needs Congressional support to implement economic policies

The new President’s first budget is for the fiscal year

2018 (1 Oct 2017 – 30 Sep 2018)

14

Trump vs Clinton – their power is limited by the

‘check and balances’ system

1515

• Hillary Clinton most likely faces either a Republican or a divided Congress.

• Would need to seek compromises to get her policy through.

• Not a new thing - same has been true for both Barack Obama and Bill Clinton.

• Do not expect significant changes to US politics, neither domestically nor globally.

Clinton vs Trump

Hillary Clinton - status quo candidate

• Hawkish views on immigration, fiscal policy, tradepolicy and foreign policy.

• His political views/statements differ from traditionalRepublican views.

• No political experience – we do not know what to expect if elected. Increases uncertainty.

• In reality, he may be more modest than currentretorics suggest.

Donald Trump - more hawkish views

1616

• Trump will need Republican support to pass legislation in Congress due to the check-and-balance system (unlikely he can pass all his policies as Executive Orders).

• Many Republican Congress members do not share his political views.

• Trump may be forced to be more pragmatic and seek more compromises as President on domestic affairs, especially if Congress is divided.

• Still more likely that Trump can get more of his policies through if the Republican Party wins both chambers.

• With respect to foreign policy, Donald Trump would have more power. Here lies the biggest uncertainty in case of a Trump win, in our view.

Trump may be forced to be more pragmatic if elected

Trump does not enjoy significant support in the Senate…

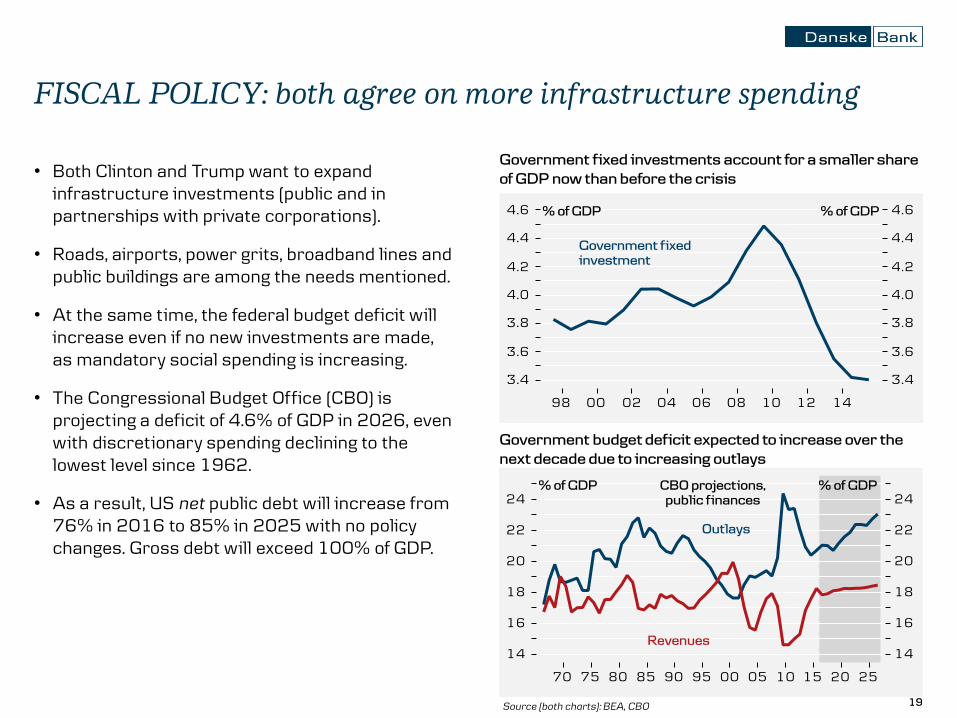

• Both Clinton and Trump want to expand infrastructure investments (public and in partnerships with private corporations).

• Roads, airports, power grits, broadband lines and public buildings are among the needs mentioned.

• At the same time, the federal budget deficit will increase even if no new investments are made, as mandatory social spending is increasing.

• The Congressional Budget Office (CBO) is projecting a deficit of 4.6% of GDP in 2026, even with discretionary spending declining to the lowest level since 1962.

• As a result, US net public debt will increase from 76% in 2016 to 85% in 2025 with no policy changes. Gross debt will exceed 100% of GDP.

FISCAL POLICY: both agree on more infrastructure spending

Government fixed investments account for a smaller share

of GDP now than before the crisis

Government budget deficit expected to increase over the

• Infrastructure programme of USD275bn over five years : approximately 0.3% of GDP each year.

• Many other expenditures, including:Broadband access, parental leave, better access to pre-school and childcare, more community colleges.

• Tax hikes on high incomes, lower threshold for inheritance tax, fewer deductions in corporate income and other hikes – estimated at USD1,100bn over 10 years, or approximately 0.6% of GDP each year.

• Expenditures could be advanced and income

measures postponed if the administration wants a

more expansionary policy in the first years – as some of its advisers are advocating.

• But over a longer horizon: more or less neutral.

FISCAL POLICY: widely different fiscal stance and tax policies

Clinton: expenses but also higher taxes

• Has promised to ‘at least double’ Clinton’s infrastructure spending, implying at least 0.6% of GDP. Has talked about ‘trillion-dollar rebuilding programme’, so potentially higher spending.

• Trump’s original tax proposal was estimated to cost USD10trn over 10 years.

• New proposal is more modest – perhaps USD3trn, or 1.6% of annual GDP.

In sum, fiscal easing of at least 2.2% of annual GDP.

• Trump has also talked about a balanced budget within eight years. According to his economic plan, it is possible due to dynamic effects – in reality, it is doubtful.

• Very difficult to estimate the actual effect of a Trump

victory but according to his economic plan, we should

Source (both charts): CBO, www.donaldjtrump.com, Danske Bank Markets

• Clinton’s economic plan is more or less neutral – in line with the CBO’s baseline projection.

• Using a simple debt model and assuming Trump gets all his policy proposals through (an unrealistic scenario), the US public net debt could increase to above 95% of GDP from about 75% today.

• As a result, we think that the US would lose the last two of its ‘AAA’ ratings (has already lost one).

• Less rosy assumptions imply that debt increasesmore (slower growth, lower fiscal multiplier, higherrates).

• US public sector needs to reform as projected fiscalpath is unsustainable in the long run.

FISCAL POLICY: implications of fiscal plans for US public debt

US government debt set to increase in case of a Trump win

US public debt to increase significantly in coming decades

• Fiscal policy is mainly a tool to increase employment – but unemployment gap nearly closed.

• Fiscal policy lag: more expansionary fiscal policy will not get through before late 2017 at the earliest (more likely in 2018).

• Remember the new President’s first budget is for the 2018 fiscal year (1 Oct 2017 – 30 Sep2018).

• More expansionary fiscal policy may be fullyoffset by a more hawkish Fed (higher Fed funds rate) if it thinks the economy risks overheating.

• In our view, focus should be on structuralreforms as the US struggles with very weakproductivity growth.

FISCAL POLICY: likely to be too late in the recovery to justify

more expansionary fiscal policyCould be too late in the recovery to justify more

expanionsary fiscal policy

Very weak productivity is a bigger problem in the medium

term for the US economy

Source (both charts: BLS, BEA

2323Source: www.donaldjtrump.com,

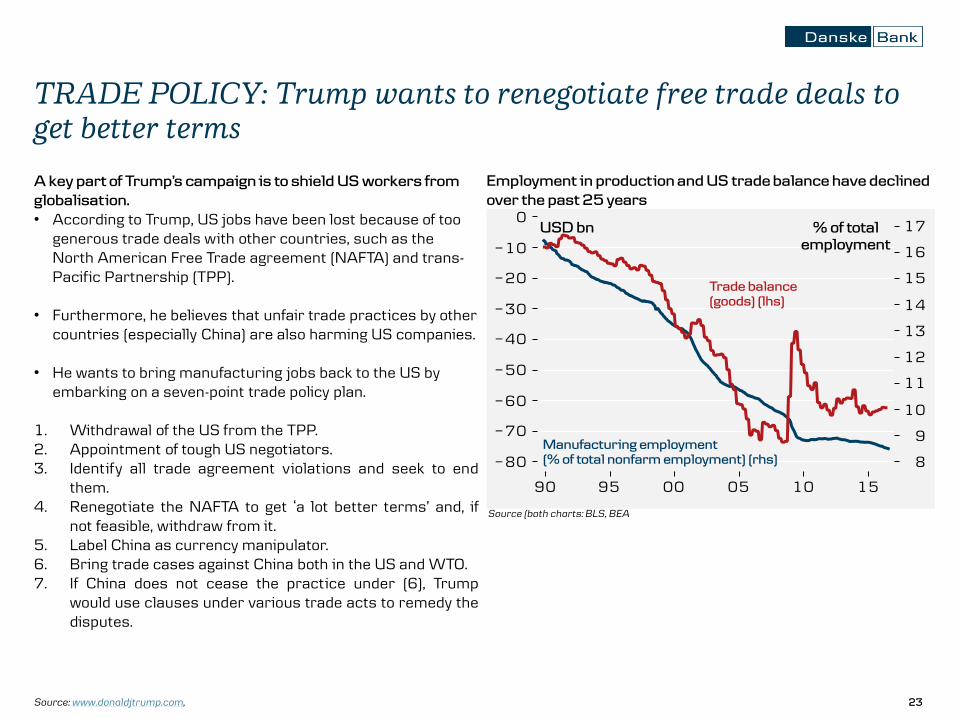

• According to Trump, US jobs have been lost because of too generous trade deals with other countries, such as the North American Free Trade agreement (NAFTA) and trans-Pacific Partnership (TPP).

• Furthermore, he believes that unfair trade practices by other countries (especially China) are also harming US companies.

• He wants to bring manufacturing jobs back to the US by embarking on a seven-point trade policy plan.

1. Withdrawal of the US from the TPP.2. Appointment of tough US negotiators.3. Identify all trade agreement violations and seek to end

them.4. Renegotiate the NAFTA to get ‘a lot better terms’ and, if

not feasible, withdraw from it.5. Label China as currency manipulator.6. Bring trade cases against China both in the US and WTO.7. If China does not cease the practice under (6), Trump

would use clauses under various trade acts to remedy thedisputes.

TRADE POLICY: Trump wants to renegotiate free trade deals to

get better terms

Employment in production and US trade balance have declined

over the past 25 years

A key part of Trump’s campaign is to shield US workers from

• Echoing concerns of the Sanders supporters of the Democratic party, Clinton has stressed that she will ‘stop any trade deal that kills jobs or holds down wages’.

• Clinton will say no to trade deals such as the TPP, which does not ‘meet her high standard of

raising wages, creating good-paying jobs, and enhancing our national security’.

• She has also expressed scepticism about NAFTA (her husband’s old trade agreement).

• Remains an open question whether she would pursue a more protectionist policy if elected, as she has previously been an advocator for free trade deals.

• Also, the Republicans Congress members are more pro free trade than Donald Trump – may try to prevent more protectionist policy.

TRADE POLICY: Clinton is also advocating more protectionism

• There is a significant risk that affected countries may take retaliatory trade measures, which could set inmotion a global trade war.

• This would hurt global trade, which has already been sluggish since 2014 and ultimately global economicgrowth.

• Neither Clinton nor Trump have said much explicitly on the Transatlantic Trade and Investment Partnership (TTIP – EU/US trade deal) but free trade reservations by both Clinton and Trump do not bode well for a deal.

• Given that both candidates call for more protectionism, most likely some protectionist measures will be taken on the back of the US election.

TRADE POLICY: aggressive protectionist US trade policy could

lead to global protectionism

-5

0

5

10

15

20

% of GDP Net exports to the US

1990 2015

TPP

NAFTA

Unilateral

2626

• The President nominates chairmanship and Governors (subject to Senate confirmation).

• Janet Yellen and Stanley Fischer’s chairmanships are due to end in 2018 – new President to appoint new chairs or reappoint the current.

• New chairmanship may be chosen by the President from among the sitting Governors for four-year terms.

• Daniel Tarullo and Stanley Fischer’s terms as Governors expire in 2020 – new President to appoint new Governors (14-year terms).

• Long terms to ensure independency but political views play a role when a president appoints new members.

• Currently, there are two vacant seats in the Board of Governors – not a given that the current nominees (Allan Landon and Kathryn Dominguez) will be approved before the inauguration of the new President.

Stanley Fischer (Vice-Chair) 20142018 (as Vice-Chair)2020 (as Governor)

Daniel Tarullo 2009 2020

Jerome H. Powell 2012 2028

Lael Brainard 2014 2026

Vacant

Vacant

Source: Federal Reserve, WIkipedia

2727Source: Federal Reserve, WIkipedia

• It is unusual to replace a sitting chair.

• Barack Obama (Democrat) reappointed Ben Bernanke (a Republican first nominated by George W. Bush) for a second term in 2009.

• Democrat Bill Clinton reappointed Alan Greenspan (a Republican) twice.

• Republican Ronald Reagan kept Paul Volcker (a Democrat).

• If Hillary Clinton wins, she is most likely to stick with Janet Yellen (assuming she wants a second term).

MONETARY POLICY: unusual to replace Fed chair – Clinton

would be likely to stick with Janet Yellen

2828

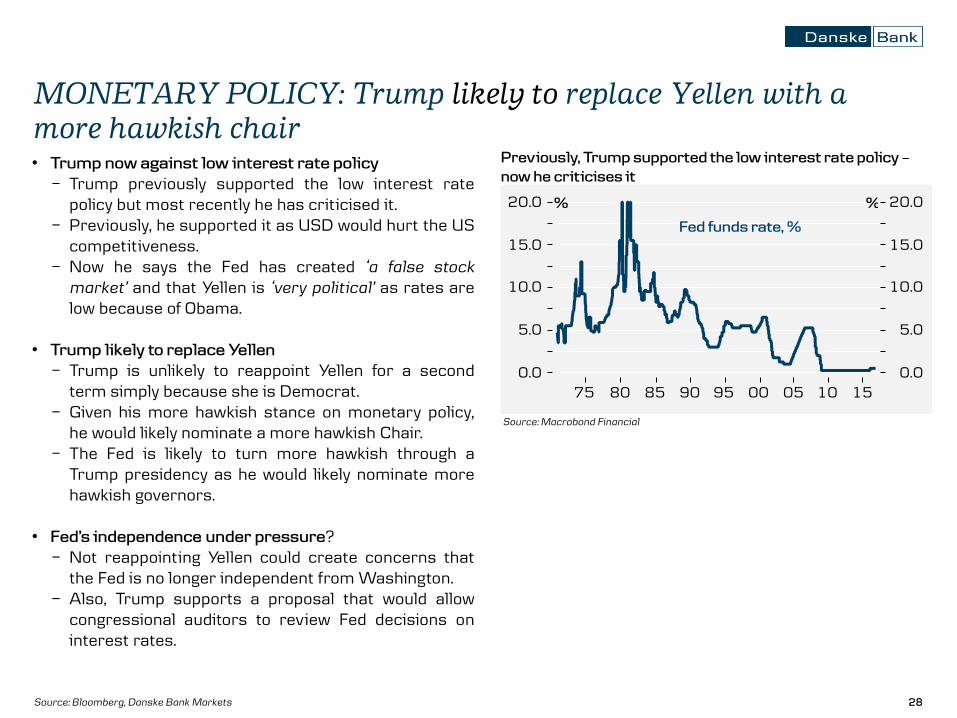

• Trump now against low interest rate policy

− Trump previously supported the low interest ratepolicy but most recently he has criticised it.

− Previously, he supported it as USD would hurt the UScompetitiveness.

− Now he says the Fed has created ‘a false stock

market’ and that Yellen is ‘very political’ as rates arelow because of Obama.

• Trump likely to replace Yellen

− Trump is unlikely to reappoint Yellen for a secondterm simply because she is Democrat.

− Given his more hawkish stance on monetary policy,he would likely nominate a more hawkish Chair.

− The Fed is likely to turn more hawkish through aTrump presidency as he would likely nominate morehawkish governors.

• Fed’s independence under pressure?− Not reappointing Yellen could create concerns that

the Fed is no longer independent from Washington.− Also, Trump supports a proposal that would allow

congressional auditors to review Fed decisions oninterest rates.

Source: Bloomberg, Danske Bank Markets

MONETARY POLICY: Trump likely to replace Yellen with a

more hawkish chair Previously, Trump supported the low interest rate policy –

now he criticises it

Source: Macrobond Financial

2929

0

0.5

1

1.5

2

2.5

3

3.5

4

2016E

NATO Guideline 2%

According to Trump’s statements, US foreign policy could see a significant shift – here lies the biggest uncertainty

1. Escalation of rhetoric towards China’s increasinggeopolitical presence and growing pressure on NorthKorea.

2. China is the main enemy, not Russia.3. NATO members will be asked to contribute more to

NATO if their contributions are below the 2% of GDPthreshold (see figure below). This could create possiblefrictions within NATO.

4. Improving dialogue with Russia – Trump says ‘Putin

has absolutely no respect for President Obama’.

5. Improving economic ties with Cuba.6. Being the key negotiator for an Israeli-

Palestinian deal while avoiding taking sides.7. Retreat from active rebels training, act as a

negotiator in the Syrian conflict and let Russiado the ground job.

8. More sanctions on Iran versus more support ofIsrael.

Defence expenditures as a share of GDP

(based on 2010 prices and exchange rates)

Trump will put pressure on NATO members to contribute 2% in line with NATO guidelines.

Source: Nato

FOREIGN POLICY: Clinton status quo – the US could see a

regime shift in US foreign policy under Trump

3030

0102030405060708090

2008 2012 2016

Importance of immigration issue (% of respondents saying immigration is 'very

important' to their vote)

Importance of "immigration, all"

Among republicans

Among democrats

Source (Both charts): Pew Research Center, Survey conducted June 15-26, 2016

IMMIGRATION: immigration is a key issue to voters

40

45

52

57

63

65

66

67

70

72

74

75

80

84

0 25 50 75 100

Treatment of sexualminorities

Abortion

Environment

Trade policy

Treatment of racial, ethnicminorities

Supreme court appointments

Education

Social security

Immigration

Gun policy

Health care

Foreign policy

Terrorism

Economy

Top voting issues in 2016 election (% of respondents saying the topic is

'very important')

Immigration is the sixthmost important issue for

voters

Trump oftenconnects

immigrationissues to terrorism

Both Republican and Democrat voters think immigration

is a more important issue than at previous elections

3131

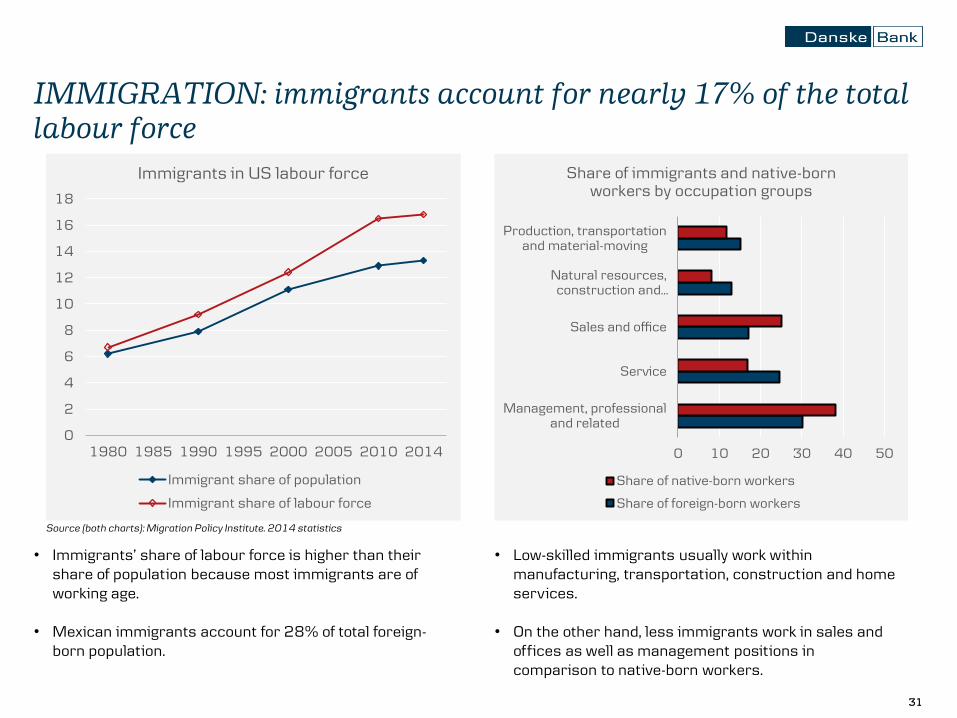

Source (both charts): Migration Policy Institute. 2014 statistics

• Immigrants’ share of labour force is higher than their share of population because most immigrants are of working age.

• Mexican immigrants account for 28% of total foreign-born population.

IMMIGRATION: immigrants account for nearly 17% of the total

labour force

0 10 20 30 40 50

Management, professionaland related

Service

Sales and office

Natural resources,construction and…

Production, transportationand material-moving

Share of immigrants and native-born workers by occupation groups

Share of native-born workers

Share of foreign-born workers

• Low-skilled immigrants usually work withinmanufacturing, transportation, construction and home services.

• On the other hand, less immigrants work in sales and offices as well as management positions in comparison to native-born workers.

0

2

4

6

8

10

12

14

16

18

1980 1985 1990 1995 2000 2005 2010 2014

Immigrants in US labour force

Immigrant share of population

Immigrant share of labour force

3232

IMMIGRATION: candidates’ immigration policies are worlds

apart

Hillary Clinton – comprehensive immigration reform Donald Trump – against illegal immigration

Key points:

• A comprehensive reform with a pathway to full and equalcitizenship within the first 100 days in office.

• Immigration enforcement must be humane, targeted and effective, focus resources on detaining and deportingindividuals that pose threat to public safety.

• Expansion of access to affordable healthcare.

• Creation of national Office of Immigrant Affairs, supportfor immigrant integration at community level.

Key points:

• Plans to build a wall to Mexico border to prevent illegalimmigrants from entering the country, legal immigrantsare welcome and will receive fair treatment.

• Immigration security = national security => carefulscreening of each individual entering the country and extreme vetting for immigrants from troubled parts of theworld.

• Temporary suspension of immigration entirely fromregions where safe and adequate screening cannot occur.

Source: Official campaign websites

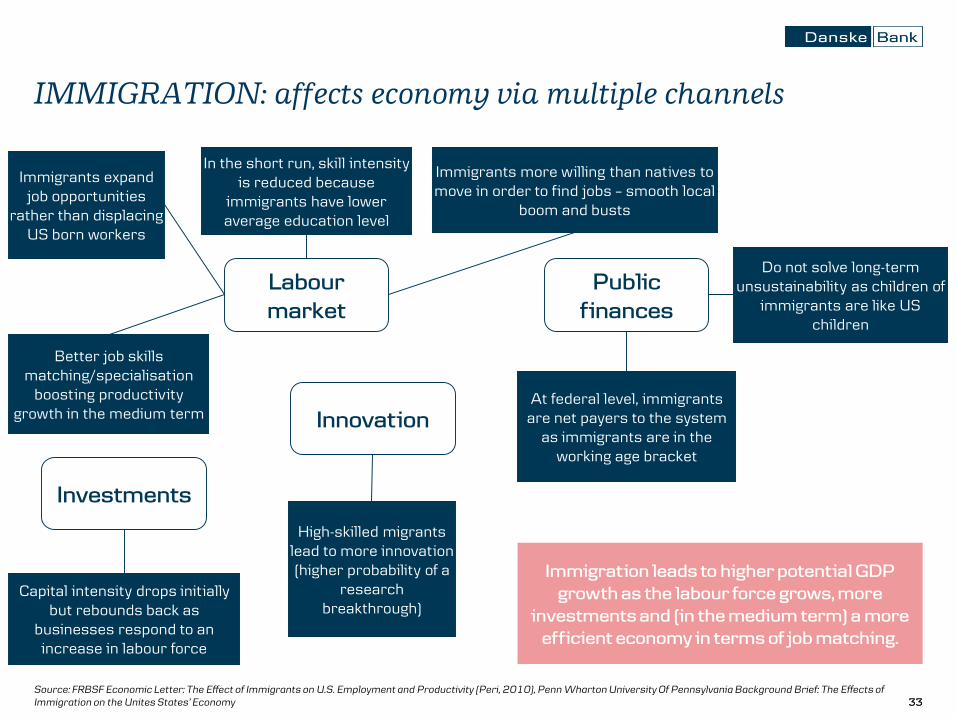

3333Source: FRBSF Economic Letter: The Effect of Immigrants on U.S. Employment and Productivity (Peri, 2010), Penn Wharton University Of Pennsylvania Background Brief: The Effects of

Immigration on the Unites States’ Economy

IMMIGRATION: affects economy via multiple channels

Labour

market

Public

finances

Investments

High-skilled migrantslead to more innovation(higher probability of a

researchbreakthrough)

In the short run, skill intensityis reduced because

immigrants have loweraverage education level

Immigrants expandjob opportunities

rather than displacingUS born workers

Capital intensity drops initiallybut rebounds back as

businesses respond to an increase in labour force

At federal level, immigrantsare net payers to the system

as immigrants are in theworking age bracket

Do not solve long-termunsustainability as children of

immigrants are like US children

Immigration leads to higher potential GDP

growth as the labour force grows, more

investments and (in the medium term) a more

efficient economy in terms of job matching.

Immigrants more willing than natives to move in order to find jobs – smooth local

boom and busts

Better job skillsmatching/specialisation

boosting productivitygrowth in the medium term

Innovation

3434

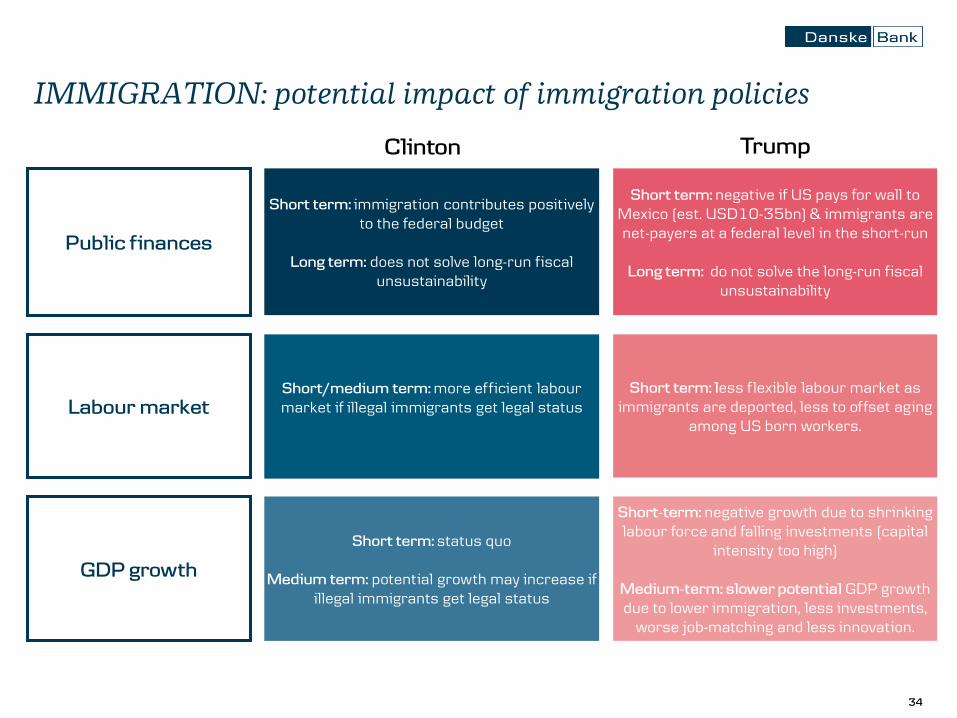

IMMIGRATION: potential impact of immigration policies

Short term: immigration contributes positivelyto the federal budget

Long term: does not solve long-run fiscalunsustainability

Short term: negative if US pays for wall to Mexico (est. USD10-35bn) & immigrants arenet-payers at a federal level in the short-run

Long term: do not solve the long-run fiscalunsustainability

Short/medium term: more efficient labour market if illegal immigrants get legal status

Short term: status quo

Medium term: potential growth may increase ifillegal immigrants get legal status

Short term: less flexible labour market as immigrants are deported, less to offset aging

among US born workers.

Short-term: negative growth due to shrinkinglabour force and falling investments (capital

intensity too high)

Medium-term: slower potential GDP growthdue to lower immigration, less investments,

worse job-matching and less innovation.

Public finances

Labour market

GDP growth

Clinton Trump

35

Market implications

3636

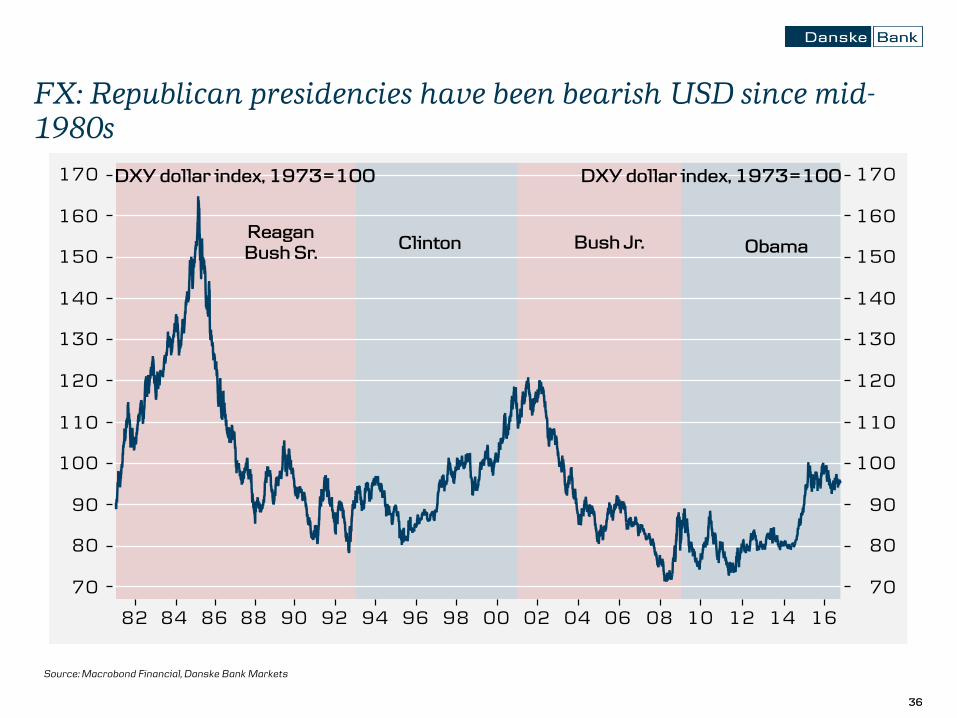

FX: Republican presidencies have been bearish USD since mid-

1980s

Source: Macrobond Financial, Danske Bank Markets

3737

FX: higher growth under Democratic presidencies may provide

part of the reason why the USD has been stronger

Source: BEA, Danske Bank Markets

3838

• Larger fiscal expansions have tended to drive USD weakness with the exception of Reagan’s first term in1981-84.

• During Reagan’s first term, the newly appointed Paul Volcker raised policy rates sharply whichsupported the dollar.

Source (both charts): Macrobond Financial, Danske Bank Markets

But higher real interest rates tend to drive USD strengthFiscal expansion has tended to drive USD weakness

FX: fiscal expansions drive USD weakness if they are not

accompanied by higher real interest rates

3939

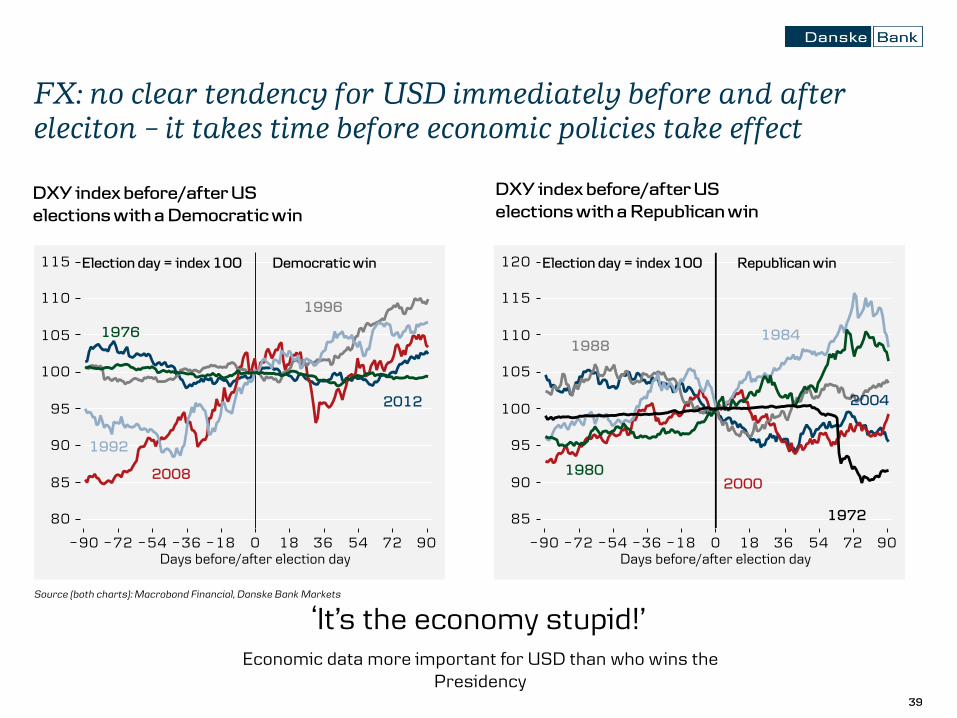

FX: no clear tendency for USD immediately before and after

eleciton – it takes time before economic policies take effect

DXY index before/after US

elections with a Democratic win

‘It’s the economy stupid!’

DXY index before/after US

elections with a Republican win

Economic data more important for USD than who wins the Presidency

Source (both charts): Macrobond Financial, Danske Bank Markets

4040

FX: USD is fundamentally overvalued vs the EUR, which will

drive the cross higher over the medium term

Eurozone-US current account differential at

Q4-2004 levels

Danske Bank’s G10 medium-term valuation (MEVA) model

indicates EUR/USD at 1.27 in the medium term

Source (both charts): Macrobond Financial, Bloomberg, Danske Bank Markets

4141

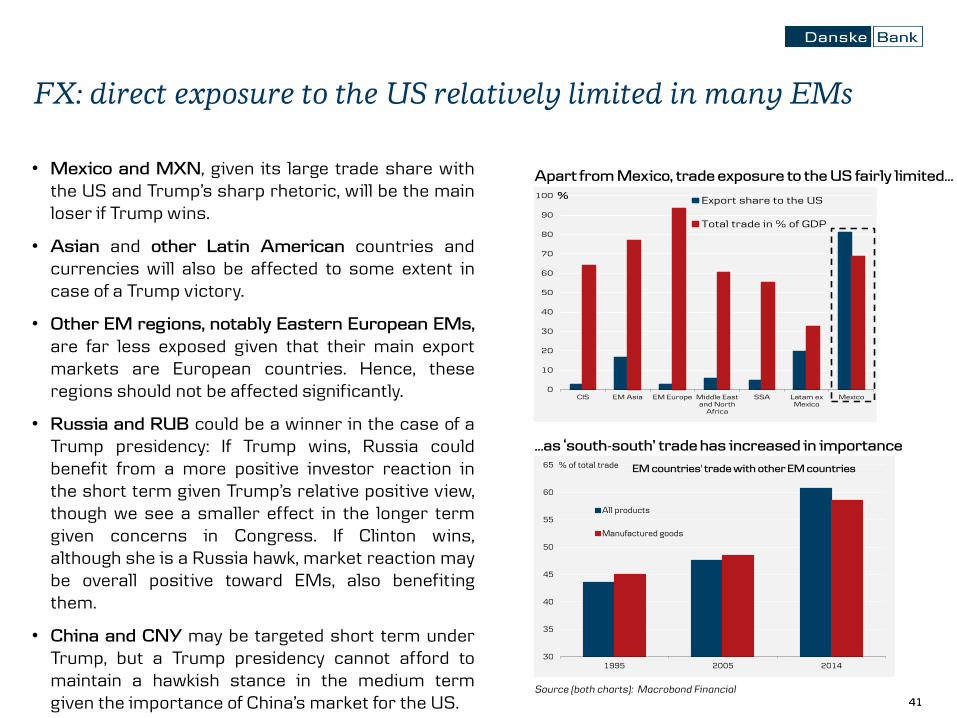

• Mexico and MXN, given its large trade share withthe US and Trump’s sharp rhetoric, will be the mainloser if Trump wins.

• Asian and other Latin American countries andcurrencies will also be affected to some extent incase of a Trump victory.

• Other EM regions, notably Eastern European EMs,

are far less exposed given that their main exportmarkets are European countries. Hence, theseregions should not be affected significantly.

• Russia and RUB could be a winner in the case of aTrump presidency: If Trump wins, Russia couldbenefit from a more positive investor reaction inthe short term given Trump’s relative positive view,though we see a smaller effect in the longer termgiven concerns in Congress. If Clinton wins,although she is a Russia hawk, market reaction maybe overall positive toward EMs, also benefitingthem.

• China and CNY may be targeted short term underTrump, but a Trump presidency cannot afford tomaintain a hawkish stance in the medium termgiven the importance of China’s market for the US.

Apart from Mexico, trade exposure to the US fairly limited…

FX: direct exposure to the US relatively limited in many EMs

…as ‘south-south’ trade has increased in importance

Source (both charts): Macrobond Financial

0

10

20

30

40

50

60

70

80

90

100

CIS EM Asia EM Europe Middle Eastand North

Africa

SSA Latam exMexico

Mexico

% Export share to the US

Total trade in % of GDP

30

35

40

45

50

55

60

65

1995 2005 2014

% of total trade

All products

Manufactured goods

EM countries' trade with other EM countries

4242Source: Macrobond Financial

• Emerging markets, notably Asian merchandise exporters, will be among the biggest losers from increased protectionism given their sizable foreign trade.

• Larger and more closed economies, such as the US, China, Russia and Canada, are more immune to global protectionism due to bigger home market and less export focus.

FX: EM biggest losers from possible global trade war

4343

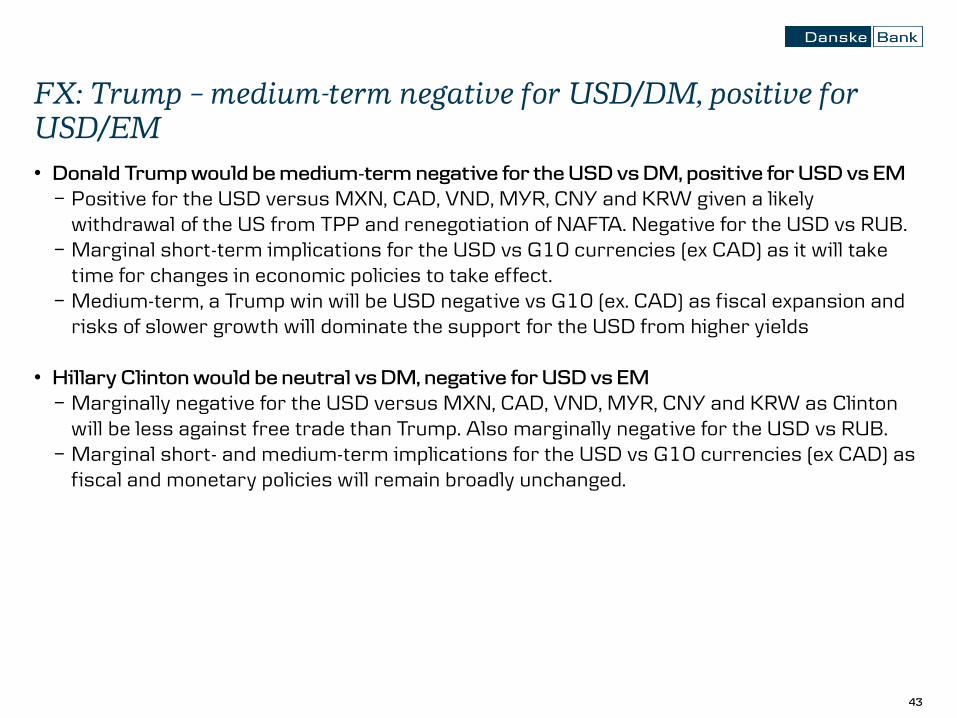

• Donald Trump would be medium-term negative for the USD vs DM, positive for USD vs EM

− Positive for the USD versus MXN, CAD, VND, MYR, CNY and KRW given a likely withdrawal of the US from TPP and renegotiation of NAFTA. Negative for the USD vs RUB.

− Marginal short-term implications for the USD vs G10 currencies (ex CAD) as it will take time for changes in economic policies to take effect.

− Medium-term, a Trump win will be USD negative vs G10 (ex. CAD) as fiscal expansion and risks of slower growth will dominate the support for the USD from higher yields

• Hillary Clinton would be neutral vs DM, negative for USD vs EM

− Marginally negative for the USD versus MXN, CAD, VND, MYR, CNY and KRW as Clinton will be less against free trade than Trump. Also marginally negative for the USD vs RUB.

− Marginal short- and medium-term implications for the USD vs G10 currencies (ex CAD) as fiscal and monetary policies will remain broadly unchanged.

FX: Trump – medium-term negative for USD/DM, positive for

USD/EM

4444

Source: Macrobond Financial, Danske Bank Markets

EQUITIES: US markets react to economy, ignore geopolitics

4545Source: Danske Bank Markets

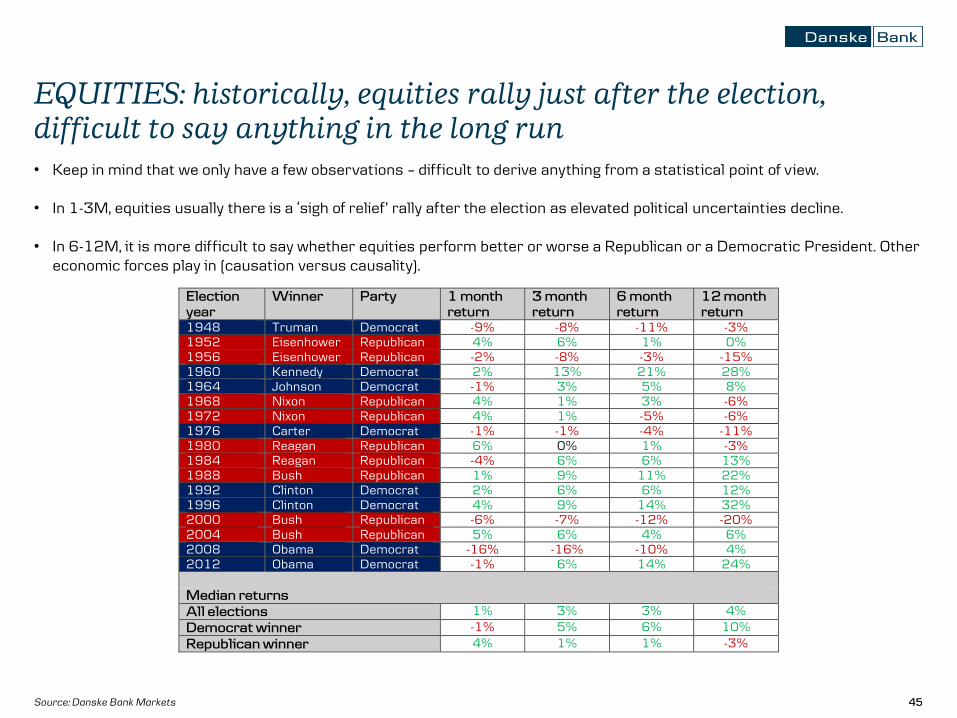

• Keep in mind that we only have a few observations – difficult to derive anything from a statistical point of view.

• In 1-3M, equities usually there is a ‘sigh of relief’ rally after the election as elevated political uncertainties decline.

• In 6-12M, it is more difficult to say whether equities perform better or worse a Republican or a Democratic President. Other economic forces play in (causation versus causality).

EQUITIES: historically, equities rally just after the election,

• In our view, the outcome of the upcoming US election is by no means trivial when it comes to global regional allocation and US sector allocation. Overall, we see a Clinton win as positive for global equities; Trump as negative for global equities.

• As prior US presidential elections have shown, uncertainty typically rises sharply ahead of the election and this time around we expect this pattern to be repeated. Hence, uncertainty will prevail until election day.

• If Hillary Clinton wins the upcoming US election, we would continue with our current position: long eurozone equities versus short US equities.

• Clinton has turned more protectionist but as explained previously, it is not a given how protectionist she would actually be if elected.

• In terms of US domestic sector exposure, we think the impact of fiscal easing would be negligible as she has proposed to increase taxes as well; hence, no particular emphasis on domestic sectors.

• We expect financials to underperform as they would face further regulation. Healthcare, on the other hand, is likely to outperform as we do not think Clinton will be able to get a price control mechanism passed through Congress.

EQUITIES: election outcome will be decisive for exposure

4747

• Under the assumption that Donald Trump wins, we would suggest entering a long US versusa short eurozone position. We will also be bullish on US equities relative to EM equities incase of a Trump win.

• Our view is largely driven by the protectionist policies advocated by Donald Trump that onrelative basis will benefit the US corporates more than their euro zone peers, as a largershare of their revenue stem from domestic sales.

• In terms of US sector exposure, we think that the expansionary fiscal policy should benefitsectors such as industrials and basic materials.

• The suggested regulation from Clinton on energy could lead to a sell-off in this sector.

EQUITIES: election outcome will be decisive for exposure

4848

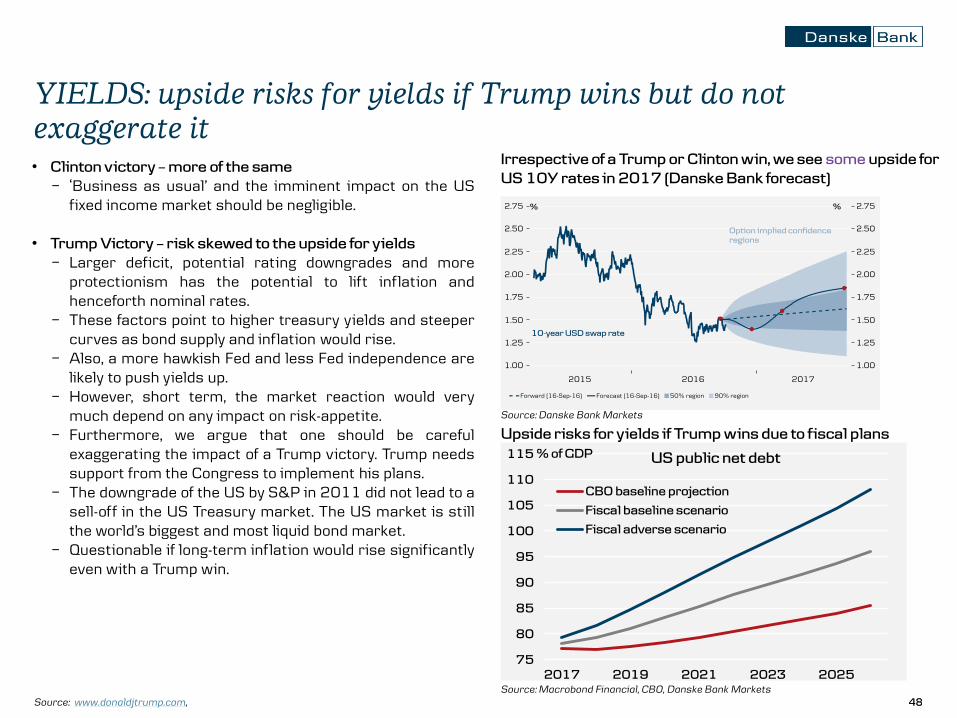

• Clinton victory – more of the same

− ‘Business as usual’ and the imminent impact on the USfixed income market should be negligible.

• Trump Victory – risk skewed to the upside for yields

− Larger deficit, potential rating downgrades and moreprotectionism has the potential to lift inflation andhenceforth nominal rates.

− These factors point to higher treasury yields and steepercurves as bond supply and inflation would rise.

− Also, a more hawkish Fed and less Fed independence arelikely to push yields up.

− However, short term, the market reaction would verymuch depend on any impact on risk-appetite.

− Furthermore, we argue that one should be carefulexaggerating the impact of a Trump victory. Trump needssupport from the Congress to implement his plans.

− The downgrade of the US by S&P in 2011 did not lead to asell-off in the US Treasury market. The US market is stillthe world’s biggest and most liquid bond market.

− Questionable if long-term inflation would rise significantlyeven with a Trump win.

Irrespective of a Trump or Clinton win, we see some upside for

US 10Y rates in 2017 (Danske Bank forecast)

YIELDS: upside risks for yields if Trump wins but do not

exaggerate it

Upside risks for yields if Trump wins due to fiscal plans

75

80

85

90

95

100

105

110

115

2017 2019 2021 2023 2025

% of GDP

CBO baseline projection

Fiscal baseline scenario

Fiscal adverse scenario

US public net debt

Source: www.donaldjtrump.com,

Source: Macrobond Financial, CBO, Danske Bank Markets

This research report has been prepared by Danske Bank Markets, a division of Danske Bank A/S (‘Danske Bank’). The authors of this presentation are listed on the first page.

Each research analyst responsible for the content of this research report certifies that the views expressed in this research report accurately reflect the research analyst’s personal view about the financial instruments and issuers covered by the research report. Each responsible research analyst further certifies that no part of the compensation of the research analyst was, is or will be, directly or indirectly, related to the specific recommendations expressed in the research report.

Regulation

Danske Bank is authorised and subject to regulation by the Danish Financial Supervisory Authority and is subject to the rules and regulation of the relevant regulators in all other jurisdictions where it conducts business. Danske Bank is subject to limited regulation by the Financial Conduct Authority and the Prudential Regulation Authority (UK). Details on the extent of the regulation by the Financial Conduct Authority and the Prudential Regulation Authority are available from Danske Bank on request.

The research reports of Danske Bank are prepared in accordance with the Danish Finance Society’s rules of ethics and the recommendations of the Danish Securities Dealers Association.

Conflicts of interest

Danske Bank has established procedures to prevent conflicts of interest and to ensure the provision of high-quality research based on research objectivity and independence. These procedures are documented in Danske Bank’s research policies. Employees within Danske Bank’s Research Departments have been instructed that any request that might impair the objectivity and independence of research shall be referred to Research Management and the Compliance Department. Danske Bank’s Research Departments are organised independently from and do not report to other business areas within Danske Bank.

Research analysts are remunerated in part based on the overall profitability of Danske Bank, which includes investment banking revenues, but do not receive bonuses or other remuneration linked to specific corporate finance or debt capital transactions.

Financial models and/or methodology used in this research report

Calculations and presentations in this research report are based on standard econometric tools and methodology as well as publicly available statistics for each individual security, issuer and/or country. Documentation can be obtained from the authors on request.

Risk warning

Major risks connected with recommendations or opinions in this research report, including a sensitivity analysis of relevant assumptions, are stated throughout the text.

Date of first publication

See the front page of this research report for the date of first publication.

General disclaimerThis research has been prepared by Danske Bank Markets (a division of Danske Bank A/S). It is provided for informational purposes only. It does not constitute or form part of, and shall under no circumstances be considered as, an offer to sell or a solicitation of an offer to purchase or sell any relevant

financial instruments (i.e. financial instruments mentioned herein or other financial instruments of any issuer mentioned herein and/or options, warrants,

rights or other interests with respect to any such financial instruments) (‘Relevant Financial Instruments’).

The research report has been prepared independently and solely on the basis of publicly available information that Danske Bank considers to be reliable.

While reasonable care has been taken to ensure that its contents are not untrue or misleading, no representation is made as to its accuracy or

completeness and Danske Bank, its affiliates and subsidiaries accept no liability whatsoever for any direct or consequential loss, including without limitation any loss of profits, arising from reliance on this research report.

The opinions expressed herein are the opinions of the research analysts responsible for the research report and reflect their judgement as of the date

hereof. These opinions are subject to change and Danske Bank does not undertake to notify any recipient of this research report of any such change nor of any other changes related to the information provided in this research report.

This research report is not intended for, and may not be redistributed to, retail customers in the United Kingdom or the United States.

This research report is protected by copyright and is intended solely for the designated addressee. It may not be reproduced or distributed, in whole or in part, by any recipient for any purpose without Danske Bank’s prior written consent.

Disclaimer related to distribution in the United StatesThis research report was created by Danske Bank A/S and is distributed in the United States by Danske Markets Inc., a U.S. registered broker-dealer and

subsidiary of Danske Bank A/S, pursuant to SEC Rule 15a-6 and related interpretations issued by the U.S. Securities and Exchange Commission. The

research report is intended for distribution in the United States solely to ‘U.S. institutional investors’ as defined in SEC Rule 15a-6. Danske Markets Inc. accepts responsibility for this research report in connection with distribution in the United States solely to ‘U.S. institutional investors’.

Danske Bank is not subject to U.S. rules with regard to the preparation of research reports and the independence of research analysts. In addition, the

research analysts of Danske Bank who have prepared this research report are not registered or qualified as research analysts with the NYSE or FINRA but satisfy the applicable requirements of a non-U.S. jurisdiction.

Any U.S. investor recipient of this research report who wishes to purchase or sell any Relevant Financial Instrument may do so only by contacting Danske

Markets Inc. directly and should be aware that investing in non-U.S. financial instruments may entail certain risks. Financial instruments of non-U.S. issuers may not be registered with the U.S. Securities and Exchange Commission and may not be subject to the reporting and auditing standards of the U.S.