Understanding and Assessing the Costs of the Federal Retail Excise Tax on the Department of Defense Edward G. Keating, Chad Pino, Sara H. Bana Prepared for the Office of the Secretary of Defense Approved for public release; distribution unlimited NATIONAL DEFENSE RESEARCH INSTITUTE

Transcript

Understanding and Assessing the Costs of the Federal Retail Excise Tax on the Department of Defense

Edward G. Keating, Chad Pino, Sara H. Bana

Prepared for the Office of the Secretary of DefenseApproved for public release; distribution unlimited

This document and trademark(s) contained herein are protected by law. This representation of RAND intellectual property is provided for noncommercial use only. Unauthorized posting of this publication online is prohibited. Permission is given to duplicate this document for personal use only, as long as it is unaltered and complete. Permission is required from RAND to reproduce, or reuse in another form, any of its research documents for commercial use. For information on reprint and linking permissions, please visit www.rand.org/pubs/permissions.

The RAND Corporation is a research organization that develops solutions to public policy challenges to help make communities throughout the world safer and more secure, healthier and more prosperous. RAND is nonprofit, nonpartisan, and committed to the public interest.

RAND’s publications do not necessarily reflect the opinions of its research clients and sponsors.

Support RANDMake a tax-deductible charitable contribution at

www.rand.org/giving/contribute

www.rand.org

For more information on this publication, visit www.rand.org/t/RR1635

Published by the RAND Corporation, Santa Monica, Calif.

The U.S. Department of Defense (DoD) pays a 12-percent Federal Retail Excise Tax (FRET), which ultimately benefits the U.S. Department of Transportation’s Highway Trust Fund, on many of its purchases of large trucks. Along with its direct costs, the FRET also imposes indi-rect (e.g., administrative, working capital) costs on DoD and its vehicle manufacturers.

The Office of the Under Secretary of Defense for Acquisition, Technology, and Logistics, Manufacturing and Industrial Base Policy (MIBP) asked the RAND Corporation to describe how the FRET affects DoD. This document fulfills that request. It provides an estimate of DoD FRET payments in recent years and reviews administrative and related issues associated with its payment.

RAND’s Human Subjects Protection Committee determined that this study does not involve “human subjects” as defined by the regulations and therefore was not subject to review.

This research should be of interest to DoD personnel involved with weapon system acqui-sition cost issues. It was sponsored by MIBP and conducted within the Acquisition and Tech-nology Policy Center of the RAND National Defense Research Institute, a federally funded research and development center sponsored by the Office of the Secretary of Defense, the Joint Staff, the Unified Combatant Commands, the Navy, the Marine Corps, the defense agencies, and the defense Intelligence Community.

For more information on the RAND Acquisition and Technology Policy Center, see www.rand.org/nsrd/ndri/centers/atp or contact the director (contact information is provided on the web page).

A. An Indifference Curve–Based Portrayal of U.S. Department of Defense Vehicle Choice . . . . 25B. Challenges in Collection and Tabulation of FRET’s Direct Costs to the U.S. Department

Certain types of medium and heavy tactical wheeled vehicles purchased by the U.S. Depart-ment of Defense (DoD) are subject to a 12-percent Federal Retail Excise Tax (FRET). The FRET is also due on vehicle refurbishments with costs in excess of 75 percent of vehicle pur-chase prices. The vehicle’s original equipment manufacturer (OEM) pays the FRET to the Internal Revenue Service (IRS) and the U.S. Department of the Treasury but is then reim-bursed for payment by DoD. The IRS and Treasury pass FRET proceeds on to the Department of Transportation’s Highway Trust Fund (HTF). This arrangement is depicted in Figure S.1.

The FRET is due to the IRS when the OEM delivers the trucks to the DoD customer. Once the OEM has made its FRET payment, the payment becomes a Contract Line Item Number, which the OEM uses to apply to DoD for reimbursement. Vehicles that are first used abroad are to be exempt from the FRET. The Army has made the preponderance of DoD FRET payments.

The FRET imposes two types of costs on DoD. First, there is a direct cost as DoD reim-burses its OEMs for their FRET payments. These direct costs vary considerably from year to

Figure S.1A Graphical Depiction of U.S. Department of Defense Vehicle FRET

RAND RR1635-S.1

OEM

IRS/Treasury

HTF

DoD

Trucks

$ for trucks

FRET $ fromtruck sales

FRET $ fromtruck sales

x Understanding and Assessing the Costs of the Federal Retail Excise Tax

year. FRET payments were especially sizable (more than $200 million per year) from fiscal years 2007 to 2011. Second, the FRET imposes indirect costs on DoD. There are increased administrative costs, both within DoD and on OEMs as they strive to comply with FRET regulations. Also, the FRET increases OEM working capital costs because OEMs must pay the FRET before they are reimbursed for it. It is logical to assume that at least some por-tion of elevated OEM administrative and working capital costs are ultimately passed on to DoD. Finally, if DoD responds to the incentive distortions the FRET provides, those distorted choices (relative to choices that would have been made absent the FRET) would be an addi-tional indirect cost of the FRET.

The indirect costs of the FRET are noteworthy in that they represent social costs of the mechanism. Whereas direct costs of the FRET are transfers within the federal government to the HTF, indirect costs are losses to society without offsetting gains to the HTF.

We consider three prospective options to reform the FRET that could reduce the indirect or social costs of the current arrangement.

1. DoD could receive a blanket exemption from vehicle FRET.2. DoD could provide a direct financial offset on vehicles purchased or substantially refur-

bished to the HTF. OEMs would make no FRET payments on DoD vehicles under this option.

3. DoD could make an annual payment, perhaps indexed for inflation, to the HTF unre-lated to annual DoD vehicle purchases or refurbishments.

Under any of these options, OEMs would no longer be involved with DoD vehicle FRET collection, so the prices they charge DoD would not include the FRET or its associated admin-istrative and working capital costs. Under options 2 and 3, DoD would still make payments to the HTF, but those payments would not go through vehicle OEMs.

xi

Acknowledgments

We thank Colonel Mary Beth Taylor, who has served as an active and engaged action officer. We also thank her predecessor, Colonel Christopher Day, who was tenacious in seeing this project come to fruition. We also thank their Manufacturing and Industrial Base Policy col-leagues Lirio Aviles, Jerry McGinn, Robert Read, and Sally Sleeper.

We thank the subject-matter experts we interviewed from the Defense Contract Man-agement Agency, Defense Logistics Agency, Oshkosh Corporation, U.S. Army’s Tank–Auto-motive and Armaments Command (TACOM), U.S. Department of Transportation, U.S. Department of the Treasury, and the U.S. Marine Corps.

We also thank Joel Slemrod and Mary Ceccanese of the University of Michigan and Phil-lip Dolan of the University of Western Australia for their assistance.

At RAND, we thank program director Cynthia Cook and her deputies, Christopher Mouton and Marc Robbins, for their assistance. We thank Steven Garber of RAND and Harry Hallock of the Army for constructive reviews of an earlier version of this report. Blair Smith edited this report. Clifford Grammich assisted with the exposition. We also thank our RAND colleagues Christopher Dirks, Ingrid Maples, Catherine Matty, Sarah Meadows, Judith Mele, Ellen Pint, Nancy Pollock, John Schank, Leslie Thornton, Rosalyn Velasquez, and Sachi Yagyu for their support.

xiii

Abbreviations

ARFF Airport Rescue Firefighting

CLIN Contract Line Item Number

CONUS continental United States

DoD U.S. Department of Defense

FHTV Family of Heavy Tactical Vehicles

FMTV Family of Medium Tactical Vehicles

FPDS-NG Federal Procurement Data System–Next Generation

FRET Federal Retail Excise Tax

FY fiscal year

GVW gross vehicle weight

HTF Highway Trust Fund

IRS Internal Revenue Service

LMTV Light Medium Tactical Vehicle

LVSR Logistics Vehicle System Replacement

MIBP Manufacturing and Industrial Base Policy

MMPV Medium Mine Protected Vehicle

MRAP Mine Resistant Ambush Protected

MTVR Medium Tactical Vehicle Replacement

OCONUS outside the Continental United States

OEM original equipment manufacturer

OUSD(AT&L) Office of the Under Secretary of Defense for Acquisition, Technology, and Logistics

xiv Understanding and Assessing the Costs of the Federal Retail Excise Tax

PEO Program Executive Officer

PLS Palletized Loading System

SME subject-matter expert

TACOM U.S. Army Tank-automotive and Armaments Command

WACC Weighted average cost of capital

1

CHAPTER ONE

Introduction and Background

Introduction

Many heavy trucks and trailers sold at retail for use on highways in the United States are sub-ject to a 12-percent Federal Retail Excise Tax (FRET). Proceeds from the FRET are paid into the Department of Transportation’s Highway Trust Fund (HTF). The HTF pays for road con-struction, maintenance, and other surface transportation projects.

Because the U.S. Department of Defense (DoD), and particularly the Army, purchases many heavy trucks and trailers that could be used on U.S. highways, it is one of the largest payers of the FRET. Indeed, between fiscal years (FYs) 2007 and 2011, DoD paid more than $200 million in FRET annually, and accounted for 5 to 25 percent of HTF truck retail tax revenue each year. Because such payments can affect DoD and its original equipment manu-facturers (OEMs) in many ways, the Office of the Under Secretary of Defense for Acquisi-tion, Technology, and Logistics (OUSD[AT&L]), Manufacturing and Industrial Base Policy (MIBP) asked the RAND Corporation to describe how DoD is affected by the FRET.

This document fulfills the OUSD(AT&L)’s request. It provides an overview of the FRET and how it works, the direct and indirect costs imposed by the FRET on DoD and its OEMs, and differing options DoD may wish to pursue to reduce its costs.

Application of the FRET

The FRET is assessed on vehicle OEMs when they sell or refurbish some types of highway-capable heavy vehicles to DoD. Internal Revenue Service (IRS) regulations stipulate a 12-per-cent excise tax on the sales price of highway-capable vehicles with a gross vehicle weight (GVW) rating of more than 33,000 pounds, as well as trailers with a GVW rating of more than 26,000 pounds, irrespective of whether the vehicles are sold to commercial firms or to DoD. For exam-ple, for a truck with a pre-tax price of $100,000, customers pay $112,000 to the OEM. The OEM, in turn, owes $12,000 to the IRS. The FRET is also due on vehicle refurbishments with costs in excess of 75 percent of vehicle purchase prices. DoD ultimately reimburses its OEMs for the FRET that its OEMs pay to the HTF.

The FRET is due to the IRS when the OEM delivers the truck to the DoD customer. Delivery officially occurs when the DoD Form 250, Material Inspection and Receiving Report, is signed. Once the OEM has paid the FRET, the payment becomes a Contract Line Item Number (CLIN), which the OEM uses to apply to DoD for reimbursement.

2 Understanding and Assessing the Costs of the Federal Retail Excise Tax

The vehicle’s OEM is the taxpayer of record, i.e., the OEM must remit the appropriate FRET payment to the IRS. Indeed, DoD does not have legal standing to negotiate directly with the IRS as to whether a given vehicle is taxable or what its tax basis (the portion of the price subject to the FRET) is. Nevertheless, DoD must reimburse OEMs for the FRET that OEMs pay. Figure 1.1 depicts how the FRET is applied. OEMs provide trucks to DoD, which pays a vehicle price including the FRET. The OEM gives the FRET portion of the price to the IRS, which in turn places it in the HTF.

In addition to its direct cost, the FRET imposes indirect costs to both OEMs and DoD. These include administrative costs, OEM financing costs between the time of the FRET pay-ment and reimbursement, and possible distortions caused by the FRET on DoD decision-making. More broadly, indirect costs of the FRET represent social costs of the mechanism relative to a regime in which these vehicles were not so-taxed. While direct costs of the FRET are transfers within the federal government from DoD to the HTF, indirect costs are losses to society without offsetting gains to the HTF.

MIBP asked RAND to estimate the total cost burden, both direct and indirect, borne by DoD because of the FRET. To do so, RAND researchers

• examined published work on the FRET and relevant legislation and regulations• interviewed subject-matter experts (SMEs)• analyzed available data on DoD FRET payments.

The SMEs we interviewed held a variety of positions with DoD, other federal agencies, and OEMs. We asked our interviewees if they knew of other experts on the FRET and we in

Figure 1.1A Graphical Depiction of U.S. Department of Defense Vehicle FRET

RAND RR1635-1.1

OEM

IRS/Treasury

HTF

DoD

Trucks

$ for trucks

FRET $ fromtruck sales

FRET $ fromtruck sales

Introduction and Background 3

turn interviewed those additional experts. Indeed, given that DoD payment of the FRET is a little -understood topic, our interviews ultimately encompassed the entirety of expertise on DoD FRET, with our interviewees representing, to our knowledge, a census rather than a sample of expertise on this topic.

The seminal report on DoD FRET is a 2001 Naval Postgraduate School thesis by Harry Hallock, a civilian employee of the United States Army. At the time of our work, Hallock was the Deputy Assistant Secretary of the Army (Procurement). He kindly agreed to be inter-viewed for our research, and provided us with a tranche of documents he used in writing his thesis, as well as contact information for other experts whom we later interviewed. Hallock also served as a reviewer of an earlier version of this report. However, Hallock’s views were not determinative of ours in that we complemented his perspectives with discussions with many other SMEs. Additionally, the document was reviewed by a disinterested RAND reviewer and others within RAND.

How the FRET Affects U.S. Department of Defense Vehicle Purchases

When DoD purchases heavy vehicles, it chooses among multiple providers offering somewhat differentiated products. OEMs submit bids specifying vehicle prices and capabilities; DoD must then decide which bid offers the best value to fulfill the military requirement.

A key issue for our analysis is whether DoD considers the post-FRET, tax-inclusive price or whether it chooses vehicles without considering the FRET. If DoD were to not consider the FRET, then the FRET would not matter: DoD would make the same choices with or without FRET.

It is more realistic, however, to assume that DoD decisionmakers do consider tax- inclusive prices and that such considerations may influence the choices they make. In Appendix A, we present an indifference curve–based portrayal of DoD vehicle choice.

The intuition is straightforward. If DoD were to receive two equally capable vehicle bids, then, absent the tax, it would choose the vehicle with the lower price. If, however, one vehicle were to have weight slightly below the tax threshold while weight for the other vehicle was slightly above it, then the heavier vehicle would be made more expensive (by the magnitude of the rate of the tax). We might then expect DoD to purchase the lighter vehicle at the lower tax-inclusive cost, even if it was not the lower-priced vehicle absent the tax. In this hypothetical case, the FRET would be distorting DoD decisionmaking.

Because there are no progress payments for the FRET, there is a period between when the OEM has made the FRET payment to the IRS and when the DoD customer reimburses the OEM for the FRET payment. We estimate that this delay, or “float time,” typically spans a few weeks. Obviously, the OEM has incentive to minimize this delay, given that it is effectively lending interest-free money to DoD during it.

This arrangement of the OEM paying the FRET before being paid for it by the DoD is a relatively new approach. In the 1980s and early 1990s, FRET payments were rolled into vehicle prices, with the government purchaser not knowing how much and whether the contractor paid the FRET. This approach generated widespread controversy and litigation. This contro-versy included different OEMs having differing views on whether their vehicles were subject to the FRET, disputes between OEMs and the IRS on whether the FRET was due on specific vehicles, and disputes between OEMs and the Army on whether an agreed price included

4 Understanding and Assessing the Costs of the Federal Retail Excise Tax

the FRET.1 Since then, vehicle acquisition contracts have had reimbursable CLINs for OEM FRET payments. Creating such CLINs improved transparency and reduced controversy and litigation costs.

The application of the FRET is governed by 26 CFR 145.4051-1: Imposition of tax on heavy trucks and trailers sold at retail.2 The FRET applies to any self-propelled vehicle designed to carry a load over public highways, whether or not it is also designed to perform other func-tions (e.g., drive off-road). A vehicle is not treated as a highway vehicle if its capability to transport a load over a public highway is substantially limited or impaired (e.g., if it cannot be driven above 25 miles per hour) by special design. The FRET, as noted, is applied to vehicles and trailers exceeding specified GVW ratings. While a DoD customer may not generally oper-ate a vehicle at its maximum weight-bearing capacity, capacity, not typical usage, determines FRET applicability.

The taxable sales price of the vehicle does not include amounts charged for machinery or equipment that does not contribute to the highway transportation function of the vehicle. IRS Publication 510 presents the example of a sewer-cleaning vehicle where the price of the high-pressure water pump, hose components, and the vacuum pipe are excluded from the FRET. From this, we surmise that the price of a weapon mounted on a vehicle would not be subject to the FRET, as the weapon would not contribute to the vehicle’s highway transportation function. Nevertheless, SMEs told us that the determination of which equipment on a vehicle should not be subject to the FRET is an area of uncertainty and contention.

FRET-eligible DoD vehicles include vehicles in the Family of Heavy Tactical Vehicles (FHTV), vehicles in the Family of Medium Tactical Vehicles (FMTV), the Logistics Vehi-cle System Replacement (LVSR), the Mine Resistant Ambush Protected (MRAP) All Terrain Vehicle, and the Medium Tactical Vehicle Replacement (MTVR).3 The FRET is not due on vehicles sent overseas, either for use by field units or for storage, because vehicle FRET is a user tax for U.S. highways.4 The IRS requires the specific Vehicle Identification Numbers of vehicles sent overseas. As a result, OEMs must be informed where vehicles go, and when—an exported vehicle must leave the United States within six months of delivery to DoD, i.e., immediately after the signing of the DD250 Form, in order to ascertain whether the FRET is due on a vehicle. An OEM SME noted that sometimes DoD fails to provide evidence of export, resulting in the FRET being paid unnecessarily.

1 Chapter 3 of Harry P. Hallock, A DoD Conundrum: The Handling of Federal Retail Excise Tax on the Army’s Medium & Heavy Truck Fleet, Monterey, Calif.: Naval Postgraduate School, June 2001, describes FRET-related disputes involving the Oshkosh Truck Corporation, AM General Corporation, BMY Corporation, and Stewart & Stevenson Services, Inc. (i.e., almost every manufacturer who sold a FRET-covered vehicle to DoD in the 1980s and 1990s). 2 This paragraph and the next draw on IRS, Excise Taxes (Including Fuel Tax Credits and Refunds), Publication 510, revised January 2016.3 U.S. Army, “About the Army: Support Vehicles” web site, undated, provides overviews of many of these vehicles and their missions.4 The FRET is also not due if a vehicle shipped overseas is later returned to the United States. John Klecha notes that “even though taxable vehicles escape the actual payment of tax due to their being exported, their return to the U.S. does not give rise to an obligation to pay any tax.” John E. Klecha, “Opinion as to the Applicability of Federal Retail Excise Tax to Used Vehicles Inducted into Army Reset Programs after Being Returned to the United States by the Army from OCONUS Loca-tions,” Memorandum of Law to Mr. Vince Faggioli, Command Counsel, Headquarters, U.S. Army Materiel Command, January 31, 2011, p. 3.

Introduction and Background 5

IRS Publication 510 notes that the FRET is also not due on sales to a state or local gov-ernment for its exclusive use, e.g., vehicles sold to the National Guard should be tax-exempt.5 We learned, however, that the FRET has been paid on some Army National Guard vehicles. A manufacturer told us that it would need to contract directly with the National Guard to make vehicles FRET-exempt. There would be FRET savings if future National Guard vehicles were purchased under a separate contracting arrangement, though the net cost savings are unclear given the additional DoD and OEM contracting costs that might be associated with such an approach.

Several DoD vehicles are not assessed the FRET. These include the Abrams tank (because its track largely precludes use on highways), the Joint Light Tactical Vehicle (which is below the GVW threshold), the Light Medium Tactical Vehicle (LMTV, also below the GVW thresh-old), and the Palletized Loading System (PLS) truck (which the IRS ruled was FRET-exempt).6

Identifying vehicles subject to the FRET is not always straightforward. Klecha (1996, p. 6) notes that FRET determination depends “on Gross Vehicle Weight calculations; on design characteristics, which may or may not qualify the configuration as a ‘highway’ vehicle; and numerous other variables that make it very difficult to determine that a vehicle is or is not subject to FRET with absolute certainty.”7

This difficulty is illustrated in Figure 1.2, showing the MTVR, and Figure 1.3, showing the PLS truck, both manufactured by Oshkosh. While the vehicles may appear similar to non-experts, the former is subject to the FRET while the latter is not.

Large-scale vehicle refurbishment or upgrade (sometimes termed “recap”) can also trig-ger the FRET. If a refurbishment or upgrade of a FRET-eligible vehicle exceeds 75 percent of the price of a new vehicle, FRET is owed on the entire cost of the refurbishment. Because refurbishment costing less than 75 percent of the new-vehicle price is FRET-exempt, buyers and suppliers have an incentive to refurbish vehicles only up to 75 percent of the cost of a new vehicle.

The FRET is also due if refurbishment transforms a non-FRET vehicle such as the LMTV, which falls below the GVW threshold, into a vehicle exceeding the FRET weight

5 See Chris Day, “Exemption of Federal Retail Excise Tax on Military Vehicles” briefing, Department of Defense, Manu-facturing and Industrial Base Policy (MIBP), November 21, 2014.6 The IRS noted that the PLS truck’s “chassis is equipped with a high strength frame, suspension system on all axles, intricate steering system, off-road tires and inflation system, all-wheel drive type transmission, and five ‘hub reduction’ drive axles that allow for high ground clearance. These features indicate a special design for transporting cargo off high-way…By virtue of its design and substantial highway limitation, [it] is not a highway vehicle and is not subject to the tax imposed by section 4051(a)(1) of the Code.” IRS, U.S. Department of the Treasury, Letter to Oshkosh Truck Company, TIN 39-0520270, Index No. 4051.00-00, December 19, 1990, pp. 5–6. Klecha describes how the PLS source-selection process was complicated by one bidder obtaining a private letter ruling that its unique design configuration was exempt from taxation: “The Ruling was limited to the requester and could not be used as precedent by any other competitor. The Government was faced with the possibility that it would have to award a technically inferior offeror based on a lower price which was only low by virtue of the ‘private’ tax exemption. As it happened, award was made to the technically superior offeror at the higher price and the awardee was able to subsequently obtain a tax exemption.” John E. Klecha, “More Than Just One Pocket to Another: Federal Excise Taxation of Military Medium and Heavy Trucks,” Warren, Mich.: U.S. Army Tank-automotive and Armaments Command, August 21, 1996, p. 6.7 There has also been extensive litigation about FRET applicability to specific nonmilitary vehicles, e.g., Worldwide Equip-ment versus United States of America, a long-running dispute over whether a specific coal-hauler truck is a “highway vehicle” subject to FRET.

6 Understanding and Assessing the Costs of the Federal Retail Excise Tax

Figure 1.2The FRET-Eligible Medium Tactical Vehicle Replacement

SOURCE: Promotional photo from Oshkosh Defense, “Medium Tactical Vehicle Replacement (MTVR),” web page, 2016.RAND RR1635-1.2

Figure 1.3The FRET-Exempt Palletized Loading System Truck

SOURCE: U.S. Army, “Military Palletized Load System (PLS) Loads Container Ready to Transport to Hawthorne, Nev.,” (Photo Credit: Kathy Anderson), July 28, 2011.RAND RR1635-1.3

Introduction and Background 7

threshold. Hence, buyers and suppliers have an incentive to keep vehicles below the GVW rating of 33,000 pounds.

FRET Costs and Options

FRET imposes two types of costs on DoD. First, as we discuss in Chapter Two, the FRET imposes a direct cost by increasing tax-inclusive prices, with manufacturers using the reim-bursable CLIN to pass on FRET costs to DoD. Such revenue, as noted, is passed on to the Department of Transportation’s HTF. This is an intragovernmental transfer from DoD to the HTF made through the OEM’s payment of FRET proceeds to the IRS.

Second, as we discuss in Chapter Three, the FRET imposes an indirect cost on DoD in the form of increased administrative costs, both within DoD and by OEMs as they strive to comply with FRET regulations. The FRET also increases OEM working capital costs as OEMs must pay FRET before being reimbursed for it. We assume that some portion of elevated OEM administrative and working capital costs are ultimately passed on to DoD.8 Finally, DoD responses to FRET incentive distortions (relative to choices that would have been made absent FRET) would be an additional indirect cost of the FRET.

DoD does have some options. Through legislation, it may pursue mitigating some of the distortions resulting from the FRET. We discuss prospective options to reform the FRET in Chapter Four, and present our conclusions in Chapter Five.

We also provide three appendixes. Appendix A presents an indifference curve-based exposition of how the FRET may distort DoD decisions. In Appendix B, we discuss alterna-tive approaches to estimating the direct costs of the FRET. Appendix C discusses the finances of the HTF, placing DoD FRET payments in a broader perspective.

8 It is possible that there is tax burden–sharing between DoD and its OEMs, with DoD only bearing a portion of increased costs, both direct and indirect. The reimbursable CLIN structure, however, suggests that DoD fully bears the burden of direct FRET costs. It is more plausible that OEMs bear some share of indirect costs. Our central point is that there are additional indirect costs associated with the FRET, irrespective of who ultimately bears such costs. These are costs to society because of the FRET.

9

CHAPTER TWO

Direct Costs of the FRET

Direct costs of the FRET are those that DoD’s OEMs directly pay. Such costs are passed on to DoD as a reimbursable CLIN. These costs vary each year by DoD purchases of taxable vehi-cles. They are also challenging to tabulate for all of DoD because FRET payments are made by individual program offices with no single point of contact for a tabulation of such payments. As a result, to tabulate FRET payments across all of DoD, data must be gathered from each program office that purchases FRET-eligible vehicles. (Table B.1 in Appendix B enumerates 13 programs for which we have FRET payment data.)

The data we present in this chapter reflect our tally of FRET payments by fiscal year across DoD program offices. As we discuss in Appendix B, our tally excludes some programs that make FRET payments, but we do not believe that any of the missing programs paid large amounts of the FRET. (Table B.1 notes three programs for which we know the FRET was paid, but we do not have annual total payments.) We discuss other methods we explored, including analysis of Federal Procurement Data System—Next Generation data and Army procurement data in Appendix B. We concluded that our tabulations by program office are fairly complete with only modest understatement of these costs and are the most accurate we can derive from existing sources.

Figure 2.1 shows estimated FRET payments in millions of then-year dollars, for all of DoD and for each military service from FYs 2003 to 2013. FRET payments were greatest from FYs 2007 to 2011, when they exceeded $200 million each year. Payments from FYs 2007 to 2011 far exceeded the roughly $40 million (in then-year dollars) per year in FRET DoD paid from FYs 1981 to 1995.1 The Army has made the preponderance of DoD FRET payments.

Figure 2.2 shows FRET paid by program in recent years, as well as total DoD FRET payments. Here, we see the Army’s FHTV and FMTV programs pay far more FRET than other programs or services. In FY 2008, when DoD FRET payments peaked, the FHTV pro-gram paid more than half of the DoD FRET. In three of the four most-recent years for which we have data, when FRET payments have decreased, FMTV FRET payments have exceeded those for the FHTV.

Our data on FRET payments for the MRAP include only those made by Navistar. While other MRAP vendors also paid the FRET, we were not able to tabulate their MRAP FRET payments by fiscal year, and hence we exclude them from the figures. (A considerable number of MRAPs were sent abroad and, therefore, were FRET-free. Thus, we cannot use total MRAP spending to estimate MRAP FRET payments.) In Figure 2.1, we attributed all Navistar MRAP

1 Hallock, 2001.

10 Understanding and Assessing the Costs of the Federal Retail Excise Tax

Figure 2.1Estimated U.S. Department of Defense FRET Payments by Military Service, FYs 2003–2013

NOTE: Data we received merged payments for FYs 2003 through 2005. The data only included Army FRETpayments for FY 2013. USMC = U.S. Marine Corps.RAND RR1635-2.1

payments to the U.S. Marine Corps because the Marine Corps was the lead contracting service on the program.

Figures 2.1 and 2.2 understate DoD FRET payments (in part because of our underesti-mation of MRAP FRET payments). Nevertheless, as we discuss in Appendix B, we believe that we have captured the preponderance of FRET payments. The systems we do not include, for example, the Army’s Medium Mine Protected Vehicle, are relatively small programs. Again, we believe this is the best estimate that can be derived. Nevertheless, we share Hallock’s (2001, p. 45) earlier lament on compiling FRET data:

Detailed data on the actual cost of FRET are difficult to compile because the Army does not specifically identify FRET when calculating its proposed budgets. . . Although indi-vidual programs that are subject to FRET do include a line item within their respective budget submissions. . . just as any other cost, the difficulty in accounting lies in the execu-tion phase of a program. Once funding has been obligated on a DOD contract, tracking the amount of actual FRET paid is impacted by contract management actions such as delivery changes (OCONUS [outside the continental United States] vs. CONUS [con-tinental United States]2) and the incorporation of Engineering Change Proposals. This makes efforts to reconstruct FRET payments to our contractors difficult. . .. Thus, detailed cost estimates in regard to FRET payments are not routinely included in overall Army pro-gram budgets.

The FRET imposes costs beyond the direct payments it requires. In the next section, we discuss the indirect costs of the FRET, including administrative costs, capital costs, and costs resulting from distorted decisions.

2 This phrasing is somewhat imprecise. A vehicle delivered to Alaska or Hawaii would be taxable. It would be more proper to classify vehicles for delivery outside the United States and domestic delivery than to delineate by OCONUS or CONUS.

13

CHAPTER THREE

Indirect Costs of the FRET

The direct costs of the FRET that DoD incurs result in a transfer within the federal govern-ment, effectively from DoD to the HTF. By contrast, indirect costs of the FRET—costs borne by DoD and its OEMs that do not translate into revenue for the HTF—are losses to society. Indirect costs represent productive resources that are consumed in the process, without offset-ting transfer to other parts of the federal government.

Taxpayers may be indifferent to a transfer from DoD to the HTF, or from one govern-mental agency to another. By contrast, taxpayers may be concerned about costs or losses to a government agency or an OEM that are not offset by gains elsewhere.

Unfortunately, it is difficult to quantify the indirect costs of the FRET. Nevertheless, we can identify categories of these. Table 3.1 summarizes these, and we discuss each further below.

First, the FRET results in greater administrative costs for the government. The military services and the IRS incur increased administrative costs because of the FRET. For example, DoD must track export of vehicles to provide accurate FRET information to OEMs. Without the FRET, government administrative costs could be lower or government employees could perform other functions.

Second, the FRET increases OEM administrative costs. Because the OEM is the payer of record for the FRET, it must devote costly effort to comply with the FRET. OEM prices to the government ultimately include a portion of such increased administrative costs. One of

Table 3.1Categories of Indirect Costs of the FRET

Category Explanation Comment

Increased government administrative costs

The military services and the IRS incur increased administrative costs doing things they would not otherwise do

May increase budgets or distract efforts from other activities

Increased OEM administrative costs

Since the OEM is the taxpayer of record, OEMs make efforts to ensure compliance

OEM prices ultimately build in such elevated administrative costs (“We pay FRET on FRET”)

Increased OEM working capital costs

OEMs must pay the FRET before being reimbursed for it

Like elevated administrative costs, elevated working capital costs for OEMs ultimately increase prices paid by DoD

Costs of distorted DoD decisions

FRET provides incentive to DoD decisionmakers to avoid buying taxable vehicles

We have not found evidence of DoD buying smaller vehicles to avoid the FRET

14 Understanding and Assessing the Costs of the Federal Retail Excise Tax

our SMEs noted that “we pay FRET on FRET,” i.e., the FRET increases OEM administrative costs and therefore prices on which the FRET is assessed.

Third, the FRET increases OEM working capital costs. OEMs must pay the FRET before being reimbursed for it, so OEMs must either borrow more money or use shareholder-provided funds to cover the financing delay between when they pay the FRET and when they receive reimbursement for it. OEMs pass such increased costs, like administrative costs, to DoD through increased prices.

Fourth, the FRET may distort DoD decisions. In Chapter One and Appendix A, we discuss how the FRET could distort DoD choices, for example, by encouraging purchase of vehicles just below the taxable threshold weight. To the extent that DoD changes its choices because of the FRET, it incurs an indirect cost (relative to the “better” choice that would have been made absent FRET). Most SMEs we interviewed, however, did not believe that DoD has made different decisions (e.g., choosing smaller vehicles or less costly refurbishments) because of the FRET.

Elevated Administrative Costs

We do not have good estimates of the increased administrative costs resulting from the FRET. We might, however, surmise that the FRET increases both government and OEM demands for

One OEM SME we interviewed described compliance with DoD FRET rules as a “heavy lift,” i.e., firms expend considerable effort to ensure that they fully comply with FRET rules. Firms failing to pay the appropriate FRET may risk IRS penalties and interest payments. OEMs are subject to IRS audit of FRET years after vehicle delivery.

To be sure, many administrative costs related to the FRET are fixed costs that OEMs would incur even if DoD were to receive a FRET exemption. A vehicle manufacturer must pay the FRET on vehicles sold to commercial customers. Nevertheless, to the extent that FRET on DoD vehicles increases or complicates OEM workload, OEMs are likely to pass administrative costs to DoD through higher prices.

Another SME suggested that FRET-driven administrative costs were comparatively minor once stable procedures were in place to manage them, but that there would be surges in administrative costs for FRET-related litigation. Seltzer (1997, p. 487) also found that “a large U.S. multinational company can complete an accurate corporate tax return with the

Indirect Costs of the FRET 15

functional equivalent of three full-time tax professionals,” possibly suggesting that an OEM’s incremental administrative cost associated with FRET compliance is modest.1

At the same time, SMEs noted that the FRET adds complexity to contracting. The FRET requires monitoring, for instance, of vehicle delivery locations (domestic or foreign) that are otherwise not relevant to a DoD acquisition contract. Contract negotiations must also clarify how the FRET will be handled, for example, whether quoted prices include the FRET. It is hard to quantify the incremental cost associated with these issues.

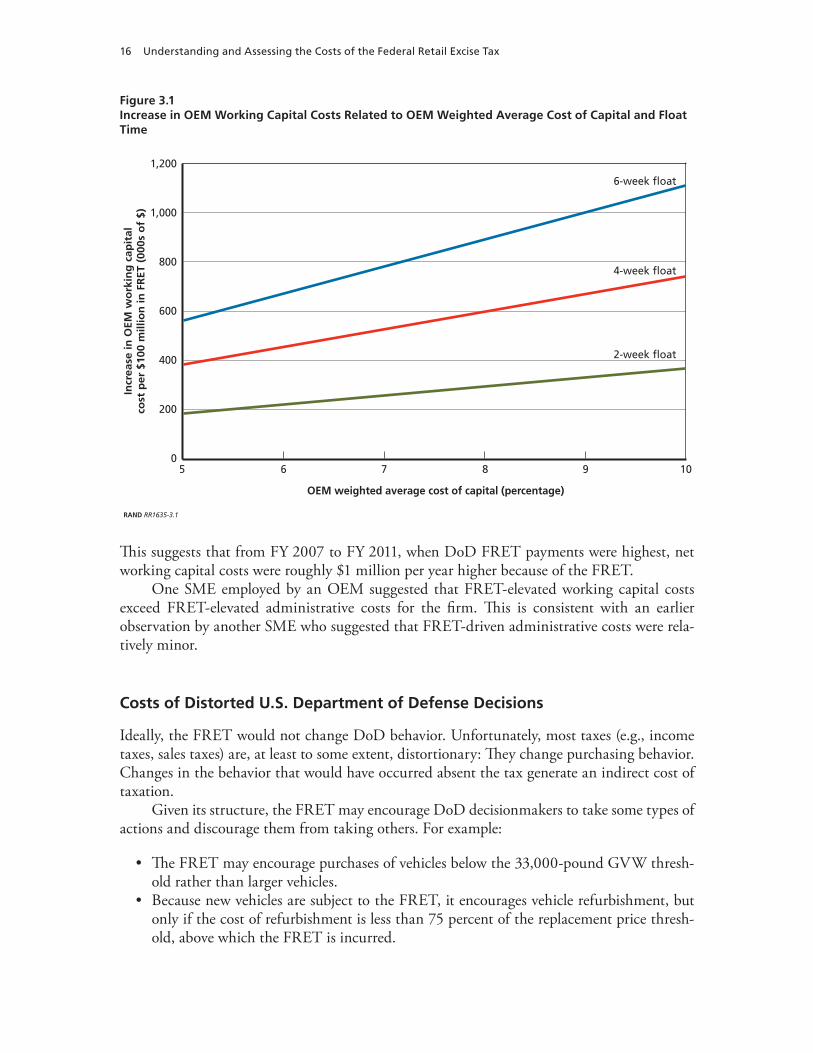

Elevated Working Capital Costs

The increase in OEM working capital costs resulting from the FRET can be calculated from the OEM’s weighted average cost of capital (WACC) and the float time, i.e., the duration of the delay between when the OEM pays the FRET and when DoD reimburses it. Weighted average cost of capital refers to the weighted average cost of different financing sources a firm uses.2 A firm’s WACC is a corporate proprietary piece of information. However, Damodaran (2015) estimates that, in 2015, a typical U.S. aerospace or defense firm had a 7.78-percent WACC, a typical auto and truck firm had a 5.09-percent WACC, and a typical machinery manufacturer had a 7.98-percent WACC.

In Figure 3.1, we show how OEM working capital costs in thousands of dollars per $100 million in annual FRET payments vary by WACC for a two-week, four-week, and six-week float. For example, with a four-week float and an 8-percent WACC, OEM annual work-ing capital costs increase by about $595,000 per $100 million in annual FRET payments. Higher WACCs and longer float times increase OEM working capital costs.

Figure 3.1’s costs are gross, not net, costs from the government’s perspective. The costs are offset, in part, by reduced government borrowing during the float time. During the float time, the OEM effectively lends the government money. Nevertheless, the government’s cost of capital is surely lower than the WACCs shown in Figure 3.1; indeed, perhaps one-fourth the level of the OEM’s WACC.3

Given that we do not know specific WACCs for OEMs or the typical float time, Figure 3.1 should only be viewed as suggestive. Nevertheless, an estimate of $500,000 in working capital costs for $100 million in annual FRET payments appears to be reasonable for discussion here.

1 Joel Slemrod and Varsha Venkatesh, in analyzing the costs of corporate tax compliance, (i.e., the costs of preparing for and filing corporate taxes, as well as responding to audits), found that large heavy manufacturing and transportation firms averaged about $1.6 million in annual average compliance costs. Tax issues that were especially complex and, there-fore, costly included the Alternative Minimum Tax, depreciation, and foreign source income. Unfortunately, these studies explicitly omit time and effort involved in dealing with matters not related to the business income tax and therefore exclude excise tax compliance costs. See Joel B. Slemrod and Varsha Venkatesh, “The Income Tax Compliance Cost of Large and Mid-Size Businesses,” University of Michigan, Ross School of Business Working Paper No. 914, September 2002.2 Suppose, for instance, that an OEM has a target capital structure of using 40-percent equity (stock) financing and 60-percent debt (borrowing) financing. If the OEM’s marginal cost of equity is 10 percent and its marginal, after-tax cost of debt is 6 percent, its WACC would be 7.6 percent (0.4 × 0.1 + 0.6 × 0.06). 3 Suppose, for instance, there is a four-week float and a 2.0-percent government cost of borrowing (per the Office of Man-agement and Budget Circular A-94’s prescribed nominal short-run interest rate for 2016). Then the government saves about $150,000 per $100 million in annual FRET payments, but that is considerably outweighed by the $595,000 in increased OEM working capital costs.

16 Understanding and Assessing the Costs of the Federal Retail Excise Tax

This suggests that from FY 2007 to FY 2011, when DoD FRET payments were highest, net working capital costs were roughly $1 million per year higher because of the FRET.

One SME employed by an OEM suggested that FRET-elevated working capital costs exceed FRET-elevated administrative costs for the firm. This is consistent with an earlier observation by another SME who suggested that FRET-driven administrative costs were rela-tively minor.

Costs of Distorted U.S. Department of Defense Decisions

Ideally, the FRET would not change DoD behavior. Unfortunately, most taxes (e.g., income taxes, sales taxes) are, at least to some extent, distortionary: They change purchasing behavior. Changes in the behavior that would have occurred absent the tax generate an indirect cost of taxation.

Given its structure, the FRET may encourage DoD decisionmakers to take some types of actions and discourage them from taking others. For example:

• The FRET may encourage purchases of vehicles below the 33,000-pound GVW thresh-old rather than larger vehicles.

• Because new vehicles are subject to the FRET, it encourages vehicle refurbishment, but only if the cost of refurbishment is less than 75 percent of the replacement price thresh-old, above which the FRET is incurred.

Figure 3.1Increase in OEM Working Capital Costs Related to OEM Weighted Average Cost of Capital and Float Time

RAND RR1635-2.2

RAND RR1635-3.1

Incr

ease

in O

EM w

ork

ing

cap

ital

cost

per

$10

0 m

illio

n in

FR

ET (

000s

of

$)

5 6 7 8 9 100

200

400

600

800

1,000

1,200

OEM weighted average cost of capital (percentage)

6-week �oat

4-week �oat

2-week �oat

Indirect Costs of the FRET 17

• The FRET provides an incentive to move FRET-subject vehicles overseas, where they will not incur the tax.

• DoD has an incentive to separate spare parts from initial vehicle purchases so as to reduce the FRET, even if separating contract actions this way increases contracting costs.

The mere fact that the FRET encourages some types of behavior while discouraging others does not mean that DoD decisionmakers have actually changed behavior and choices because of the FRET. Many DoD SMEs argued that, while incentive distortions may exist, they had not generally been acted upon. Other DoD SMEs, however, noted that time had been spent discussing options and the ramifications of the FRET, and that it may have changed past behavior or might change future behavior.

When we asked DoD SMEs how the FRET might have changed DoD choices, they focused on two issues. First, because the FRET increases the per-unit cost of taxable vehicles, some SMEs thought that acquisition programs may have been stretched out, for example, vehi-cles might be acquired over six years rather than five. Second, some acquisition SMEs thought that the increase in per-unit costs may have reduced fleet sizes. Either of these responses (delayed fielding or reduced fielding) to the FRET ultimately implies that DoD had less operational capability, either temporarily or permanently, because of the FRET.

To the extent that the SMEs are correct that the FRET has not yet much changed DoD behavior, the incentives enumerated are latent, not realized, risks. Future decisionmakers may still choose to purchase smaller-than-optimal vehicles so as to avoid the FRET.

19

CHAPTER FOUR

Options for Reform

In this chapter, we discuss three options for reform of the FRET. Option 1, making DoD-pur-chased vehicles FRET-exempt, has been, not surprisingly, widely advocated by DoD personnel.

In the interest of not limiting ourselves to solely the DoD’s preferred approach, the RAND research team developed two other options. Option 2 would be to have DoD make direct payments to the HTF for each vehicle purchased rather than flowing payments through OEMs and the FRET. Option 3 would have the DoD make an annual payment to the HTF unrelated to the number of vehicles it purchases in a given year; Option 3 is intended to be revenue-neutral for the HTF while increasing the stability of HTF revenue. Of course, no reform at all, the status quo, is also possible.

Any of the three reform options could be implemented legislatively. Option 1, making DoD-purchased vehicles FRET-exempt, could potentially be implemented through regulatory relief from the Department of the Treasury, as we discuss in Chapter Five.

Table 4.1 summarizes these options, which we discuss further below.In Option 1, DoD would receive a blanket exemption from vehicle FRET. Such an

exemption would completely eliminate indirect costs. It would probably be fairer than the status quo, given limited DoD use of public highways. As we discuss in Appendix B, Klecha (1996), Hallock (2001), and many SMEs emphasized how few miles DoD FRET-eligible vehi-cles operate on public highways, resulting in DoD paying disproportionately high FRET on a per-highway-mile basis. A disadvantage of a blanket exemption is that it would reduce funding

Table 4.1FRET Reform Options

Option Approach Advantages Relative to Status Quo Disadvantages

1 DoD receives a blanket exemption from vehicle FRET

Completely eliminates indirect costs;Probably fairer due to limited DoD use of public highways

Reduces funding for the HTF

2 DoD provides a direct financial offset on vehicles purchased or substantially refurbished to the HTF; OEMs make no FRET payments on DoD vehicles

Eliminates FRET-related OEM administrative and working capital costs;No change in (intrinsically variable) level of DoD funding to the HTF

Increases DoD administrative costs

3 DoD makes an annual payment (indexed for inflation?) to the HTF unrelated to annual DoD vehicle purchases or refurbishments

Eliminates FRET-related OEM administrative and working capital costs;Increases stability in HTF funding;Eliminates possible DoD incentive problems

Annual payment to the HTF would be a “must pay” bill that DoD cannot reduce even if it buys or refurbishes no vehicles in a year

20 Understanding and Assessing the Costs of the Federal Retail Excise Tax

for the HTF. Personnel we interviewed at the Department of Transportation indicated that they might accept process reforms that preserve HTF-funding levels but would oppose those that do not.

In Option 2, DoD, not OEMs, would make payments to the HTF for DoD purchases and vehicle refurbishments. This approach would eliminate FRET-related OEM administra-tive and working capital costs while not changing the (intrinsically variable) level of DoD funding to the HTF.1 The disadvantage of this approach is that it would increase DoD admin-istrative costs. There would be one-time startup costs associated with creating a DoD FRET direct payment capability. We believe, however, that this approach would result in net savings in administrative effort and costs, especially if DoD adopted a centralized mechanism to pay FRET instead of having administrative burden spread across multiple program offices. This approach would also increase visibility of DoD FRET payments, eliminating the opacity of the current arrangement.

In Option 3, DoD would make an annual payment (perhaps indexed for inflation) to the HTF unrelated to annual DoD vehicle purchases or refurbishments. This approach would eliminate FRET-related OEM administrative and working capital costs while increasing sta-bility in HTF funding. It would also eliminate DoD incentive problems discussed earlier. This approach would also, however, make the annual DoD payment to HTF obligatory, and one DoD could not reduce even if it were to buy or refurbish no vehicles in a given year. Also, DoD would have to negotiate the annual payment with the Department of Transportation and how it might be adjusted over time.

Figure 4.1 modifies Figure 1.1 to show how these options would work. Under any of these options, DoD would pay a tax-free price to the OEM. Under Options 2 and 3, DoD would separately make FRET payments to the HTF.

1 One SME suggested that DoD would have greater incentive than OEMs currently have to push for FRET exemptions, i.e., to exempt more vehicles or components of vehicles from the 12-percent tax. As noted in IRS Publication 510, the taxable basis for a vehicle should not include amounts charged for machinery or equipment that do not contribute to the highway-transportation function of the vehicle. The SME suggested that, in recent years, OEMs have not been aggressive in trying to reduce vehicles’ taxable bases. A reader of an earlier draft of this report wondered why the MRAP was ever subject to the FRET, considering it not to be a highway-appropriate vehicle. Because the FRET is a reimbursable CLIN, an OEM may not currently have much incentive to push for a vehicle-level FRET basis reduction. Of course, DoD fighting for reduced tax bases on its vehicles would increase government administrative costs and, if successful, would adversely affect the HTF.

Options for Reform 21

Figure 4.1A Graphical Depiction of FRET Reform Options

RAND RR1635-4.1

OEM

IRS/Treasury

HTF

DoD

Trucks

$ for trucksPrice without FRET

Options 2 and 3include DoDpayments to the HTF

23

CHAPTER FIVE

Conclusions

The fact that OEMs make FRET payments on applicable vehicles that they sell to the DoD is counterintuitive. This is a right-pocket-to-left-pocket transfer within the federal government, except one that encumbers OEMs, increasing their costs.

There may be scope for DoD to reduce its FRET bill through management changes. Most directly, OEMs need to be informed when a FRET-eligible vehicle’s first usage is outside of the United States, rendering that vehicle tax-exempt. An OEM with access to a reimburs-able CLIN will pay FRET and charge the CLIN unless provided with clear documentation of vehicle export. SMEs expressed concern that FRET has been paid unnecessarily on exported vehicles, though we have not found evidence of this phenomenon being widespread in recent years.

There may also be scope for savings if DoD wrote separate contracts for vehicles being sold to the National Guard. However, this prospective management reform faces a tradeoff in that doing so would increase DoD and OEM contracting costs. The volume and dollar value of National Guard vehicle purchases may or may not justify such an approach.

Some improvements to FRET processes have occurred over the years. In particular, the reimbursable CLIN reforms starting in the early 1990s all but ended large-scale litigation related to FRET on DoD vehicles. Hallock (2001) notes a litany of very costly court cases in the 1980s and 1990s related to DoD FRET, but such litigation has since largely ceased. We surmise that the reimbursable CLIN approach reduced total indirect costs, even inclusive of elevated OEM working capital costs.

If DoD wishes to pursue reform options such as those discussed in Chapter Four, the most direct way to do so would be through the legislative process, i.e., convincing Congress to include such a reform in annual defense-related legislation. Indeed, DoD could only pursue Options 2 and 3, entailing direct payments to the HTF rather than through vehicle OEMs, through legislation.

A second, nonlegislative path to pursuing Option 1, DoD exemption from FRET pay-ments, would be to seek regulatory relief from the Department of the Treasury. 26 U.S. Code Section 4293 gives the Secretary of the Treasury authority to exempt from taxes items pur-chased “for the exclusive use of the United States, if he determines that the imposition of such taxes with respect to such articles or services, or class of articles or services will cause substan-tial burden or expense which can be avoided by granting tax exemption and that full benefit of such exemption, if granted, will accrue to the United States.” Unfortunately, there is no objective test on whether the current indirect costs of the FRET are “substantial.” We conclude that indirect costs of the FRET are real, but it is a subjective judgment on whether they are substantial.

25

APPENDIX A

An Indifference Curve–Based Portrayal of U.S. Department of Defense Vehicle Choice

In Chapter One, we noted that the FRET may distort DoD decisionmaking. In this appendix, we present an indifference curve–based exposition of how the imposition of the FRET on spe-cific types of vehicles could potentially change, or distort, DoD decisions.

In Figure A.1, we present a line showing different prices the DoD might pay for vehicles as a function of gross vehicle weight (GVW) rating. Not surprisingly, the price line in Figure A.1 is upward sloping, i.e., a larger vehicle will cost more, other things being equal. (In fact, price rising linearly with GVW is not important. It is only important, and eminently plausible, that price increases with GVW.)

We might then expect DoD to choose the vehicle that puts it on the most favorable indif-ference curve, a curve we label I* in Figure A.2. DoD indifference curves in this formulation are upward sloping, i.e., DoD is willing to pay more for a heavier truck. Of course, when DoD pays more for a heavier truck, it receives fewer other items it may wish to purchase. Hence, a given indifference curve connects points with heavier trucks and higher prices (i.e., DoD has

Figure A.1 Vehicle Price Rises with Gross Vehicle Weight

Pric

e to

Do

D

Gross vehicle weight

RAND RR1635-A.1

26 Understanding and Assessing the Costs of the Federal Retail Excise Tax

less funding for other things) with points with lighter trucks and lower prices (i.e., DoD has more funding for other things).

In Figure A.2, DoD would prefer to be on indifference curve IH, but IH is not attainable from vehicle vendors. Vehicles that large are not available at such a low price (below the price line). Indifference curve IL, meanwhile, is inferior. The DoD could spend less or get a larger truck than the options on IL. At the tangent point between indifference curve I* and the price line, the DoD buys a vehicle with weight W* for price P*. This is the DoD’s optimal choice in this simple construct.

Next, we introduce a vehicle tax, but we suppose that the tax is only assessed on vehicles above a threshold weight, WT. As shown in Figure A.3, up to weight WT, the price line is the same as in Figure A.1. For vehicles with weight WT and above, however, the price line jumps to a higher level, reflecting the fact that the tax is assessed only on vehicles at or above that threshold weight.

If WT is greater than W*, DoD could buy the same truck it chose in Figure A.2 and not pay any FRET. If, however, WT is less than or equal to W*, indifference curve I* is no longer feasible, as shown in Figure A.4.

Instead, as Figure A.4 illustrates, the most favorable and feasible indifference curve would be I-. In this case, I- intersects at a weight just below WT, i.e., the largest possible tax-free truck.

In a case such as that portrayed in Figure A.4, the tax has distorted DoD decisionmaking. W* was the optimal choice but, in the presence of the tax, the smaller truck (with weight just below WT) is chosen instead.

The tax need not distort DoD decisionmaking. If DoD indifference curves were suffi-ciently vertical (inelastic with respect to vehicle weight), the vehicle weight choice might not

Figure A.2DoD Chooses Its Most Favorable Point on the Price Line

Pric

e to

Do

D

Gross vehicle weight

W*

RAND RR1635-A.2

P*

ILPrice line

I*

IH

An Indifference Curve–Based Portrayal of U.S. Department of Defense Vehicle Choice 27

Figure A.3Vehicle Prices Jump for Vehicles Above the Threshold Weight

RAND RR1635-A.3

Pri

ce t

o D

oD

Gross vehicle weight

Price line with tax

WT

Old price line

Figure A.4Vehicle FRET Could Induce DoD to Purchase a Smaller Vehicle

RAND RR1635-A.4

Pric

e to

Do

D

Gross vehicle weight

Price line with tax

I−I*

W*WT

Old price line

28 Understanding and Assessing the Costs of the Federal Retail Excise Tax

change, i.e., DoD would simply pay the higher, tax-inclusive price. If, for instance, DoD had an immutable requirement for a 35,000-pound vehicle, its indifference curve would simply be a vertical line at that weight. But this illustration shows that imposition of the vehicle tax could change DoD decisions in the presence of demand elasticity. In particular, there is a strong temptation to purchase a vehicle whose weight is just below the taxable threshold. Buying such a truck instead of a larger, taxable truck would represent a decision distortion induced by the tax.

Tax-induced distortion could arise in other ways. Suppose, for instance, that an acquisi-tion official was given a fixed annual budget. The imposition of the tax could force the official to buy fewer vehicles per year, either extending the program’s acquisition period or resulting in fewer vehicles being purchased (if there was an externally imposed cap on total program spending).

To the extent that different decisions are made from what would have happened absent FRET, an indirect or social cost of FRET has been incurred.

29

APPENDIX B

Challenges in Collection and Tabulation of FRET’s Direct Costs to the U.S. Department of Defense

In Chapter Two, we present estimates of the direct costs of the FRET to DoD. Those estimates were based on data provided to RAND by U.S. Army Tank-automotive and Armaments Com-mand (TACOM) and Program Executive Officer (PEO) Land Systems and the U.S. Marine Corps, the lead program offices for ground vehicles. Our tabulations, however, are incomplete. In particular, there are systems on which we know FRET was paid, but for which we have not received tabulations by fiscal year.

As an alternative to the TACOM and PEO Land Systems–provided cost estimates, we explored using the Federal Procurement Data System–Next Generation (FPDS-NG) and Army procurement data to estimate FRET payments. As we note below, however, FPDS-NG data are too aggregate for our purposes, i.e., recorded payments combine the FRET with other payments. Army procurement data considerably overestimate FRET payments because such data offer no way to identify tax-free vehicles, e.g., vehicles whose first usage is overseas.

As discussed in Chapter One, whether a vehicle is subject to the FRET depends on char-acteristics such as its highway capability and gross weight. The baseline FRET rate is 12 per-cent of the retail-unit price (noninclusive of the tax). FRET payments reside as a separate reimbursable CLIN within program contracts. In theory, therefore, it would seem straightfor-ward to sum FRET payments across contracts. In practice, inconsistency in eligibility, con-tract changes over time, and the lack of a consolidated data source with CLIN-level detail make summing FRET payments problematic. Accurate data at the program level are available through individual contracting offices, though tracking historical costs for multiple programs would require a large time commitment and assistance from a large number of personnel.

Defining the Tactical Wheeled Vehicle and Trailer Fleet

We developed a list of Army and U.S. Marine Corps vehicles and trailers that have been sub-ject to the FRET (see Table B.1). The list we originally received from MIBP, our client, did not include the MRAP and the Medium Mine Protected Vehicle (MMPV, the three-axle vari-ant of the MRAP), but U.S. Marine Corps SMEs told us that FRET had been paid on those vehicles as well. We also found contract data corroborating FRET payments on some MRAPs. We subsequently received data on some MRAP FRET payments. During interviews, litera-ture searches, and analysis of FPDS-NG data, we also found evidence of FRET payments for additional vehicles such as the U.S. Marine Corps P-19 Airport Rescue Firefighting (ARFF) truck and the U.S. Marine Corps MK970 semi-trailer refueler. We never received, however,

30 Understanding and Assessing the Costs of the Federal Retail Excise Tax

tabulations of FRET payments associated with these vehicles (though these are much smaller fleets than the FHTV and FMTV that dominate Figure 2.2). While Table B.1 lists a number of programs, each program may have multiple variants and configurations, only some of which may be subject to FRET. We reiterate Klecha’s (1996) observation that it is very difficult to determine with absolute certainty whether a vehicle is subject to FRET.

Alternative Data Sources

Figures 2.1 and 2.2 come from data originally tabulated by TACOM and PEO Land Systems. These data appear to be the most thorough and validated tabulation of FRET-related direct costs available. Our interviews at U.S. Marine Corps headquarters, Quantico, Virginia, also found that FRET had been paid on MRAPs. The TACOM and PEO Land Systems data we received did not include any tabulation of FRET paid on MRAPs, but we subsequently received a tabulation by fiscal year of FRET paid on Navistar MRAPs, which we then included

Table B.1U.S. Department of Defense FRET-Eligible Vehicles and Trailers

Service Family Vehicle Description

Army Medium Tactical Vehicles FMTV Family of Medium Tactical Vehicles

Army Heavy Tactical Vehicles HEMTT Heavy Expanded Mobility Tactical Truck

Army Heavy Tactical Vehicles HETS Heavy Equipment Transporter System

Army Heavy Tactical Vehicles Line Haul M915A5 Line Haul Tractor

Army Heavy Tactical Vehicles M800/M900 trailers Line haul trailers and fuel tankers

Army Heavy Tactical Vehicles HEMAT Heavy Expanded Mobile Ammunition Trailer

Army Heavy Tactical Vehicles HEWATT HEMTT-based Water Tender

Army Heavy Tactical Vehicles CBT Common Bridge Transporter

Army Heavy Tactical Vehicles TFFT Tactical Firefighting Truck

Army Heavy Tactical Vehicles FWTD Fifth Wheel Towing Device

Army MMPV Medium Mine Protected Vehicle

Army, U.S. Marine Corps

MRAP Mine Resistant Ambush Protected

U.S. Marine Corps, Navy

Medium Tactical Vehicles MTVR Medium Tactical Vehicle Replacement

U.S. Marine Corps

Heavy Tactical Vehicles LVSR Logistics Vehicle System Replacement

U.S. Marine Corps

MK970 Semi-Trailer Refueler

U.S. Marine Corps

P-19 ARFF Airport Rescue Firefighting Truck

NOTE: The italicized MMPV, MK970, and P-19 ARFF are not included in Chapter Two’s FRET payment cost tabulations.

Challenges in Collection and Tabulation of FRET’s Direct Costs to the U.S. Department of Defense 31

in Figures 2.1 and 2.2. We did not receive FRET tabulations by fiscal year for other MRAP manufacturers.1

Federal Procurement Data System–Next Generation

We explored USASPENDING.GOV, a publicly accessible and searchable website mandated by the Federal Funding Accountability and Transparency Act of 2006, as a prospective alterna-tive data source. The website pulls information from the FPDS-NG, a data set tabulating all prime recipient contract transactions over $3,000. We explored FPDS-NG using the FMTV as a pilot test. We found the FRET mentioned in several FMTV contract descriptions, but most of these transactions include the FRET only as a component of a larger dollar-value sum. FPDS-NG, in other words, can verify that some FRET was paid for with a weapon system, but it does not always indicate how much FRET was paid.

A key issue in using FPDS-NG is the level of detail entered in the contract requirement description field. Some transactions are very clear and contain only changes in cost due to the FRET, i.e., one can tally FRET payments associated with these transactions. Other FPDS-NG records, however, contain multiple action items per transaction without any breakouts or levels of detail. As a result, we were unable to generate a coherent estimate of FMTV-generated FRET payments from FPDS-NG.

Army Procurement Data

We also explored Army procurement data in order to estimate FRET payments. A procure-ment record indicates total procurement spending (inclusive of the FRET), so one might esti-mate FRET payments by multiplying total procurement spending by (0.12/1.12). Such an estimate would overestimate FRET payments because vehicles sent overseas are not subject to the FRET. Nevertheless, we experimented with estimating such an upper bound on FRET payments.

The basic information required would be the total procurement quantity and the retail, tax-inclusive unit price for each family of vehicles. To gain insight into procurement quantities by fiscal year, we reviewed Army Financial Management Procurement Justification Books for Tactical & Support Vehicles. These justification books are publicly available on a web site spon-sored by the Assistant Secretary of the Army for Financial Management and Comptroller.2 The data are organized by Budget Line Item Numbers and Specification Serial Numbers. Procure-ment quantities and total costs are reported by fiscal year. Our estimated FRET payments are therefore about 10.7 percent (0.12/1.12) of total reported costs, those total costs being inclusive of FRET payments.

Figure B.1 compares estimated FMTV FRET payments using the Army procurement data approach to those reported by TACOM and PEO Land Systems.

It is not a coincidence that the two data sources are especially divergent in FY 2007 and FY 2008, two years in which a large number of new FMTVs were sent directly abroad and, hence, were tax-free. The estimates are close in FY 2009 and subsequent years when fewer new vehicles were sent directly abroad.

1 We received information that BAE Systems paid approximately $10 million in FRET on its MRAPs, but we do not know in which years. Of course, adding $10 million in total to Figures 2.1 and 2.2 would not meaningfully change those displays.2 Assistant Secretary of the Army for Financial Management and Comptroller, “Army Financial Management: Budget Materials,” website, last modified October 20, 2014.

32 Understanding and Assessing the Costs of the Federal Retail Excise Tax

We conclude from Figure B.1 that program office–provided FRET tabulations differ considerably from the procurement data–generated estimates. The procurement data are not a good replacement for the program-office tabulations, especially when a large number of vehicles are sent abroad.

Table B.2 summarizes different data sources and our views as to their applicability.

Figure B.1Different Estimates of Army FMTV FRET Payments

RAND RR1635-B.1

Esti

mat

ed A

rmy

FRET

pay

men

ts(t

hen

-yea

r $m

illio

ns)

2007 2008 2009 2010 2011 2012 2013 2014 20150

50

100

150

200

250

300

350

Fiscal year

Army procurement data

TACOM and PEO land systems

Table B.2Prospective Data Sources to Estimate FRET Payments

Data Source Description Comment

TACOM and PEO Land Systems

Tabulation of FRET payments back to FY 2003

MRAP, a few other programs missing

FPDS-NG Publicly available enumeration of government contracts

FRET payments are not consistently separated from other types of spending

Army procurement data A year-by-year tally of Army procurement quantities and costs

FRET payments are overestimated because data do not segregate tax-free vehicles

33

APPENDIX C

Finances of the Highway Trust Fund

DoD vehicle FRET payments go to the HTF. Table C.1 compares our estimates of DoD FRET payments to overall HTF truck retail tax proceeds and total HTF proceeds. The HTF derives revenue from truck retail taxes (of which DoD vehicle FRET payments are a portion), but in much larger part from fuel tax revenues.

A long-standing principle in highway finance has been “users pay,” i.e., the people who pay taxes to fund highways are those who benefit from the highways (U.S. Government Account-ability Office, 2015). The truck retail tax (of which DoD FRET is a portion) is an excise tax on the purchase of large trucks, justified by the greater wear and subsequent maintenance burden that large vehicles impose on highways. Fuel tax revenues, the greatest category of HTF revenues, come from an 18.4 cents-per-gallon tax on the purchase of gasoline and diesel fuel. The operator of a large vehicle pays the HTF both up front through the FRET at the time of vehicle purchase and on an ongoing basis as fuel is purchased. Because the FRET is calculated as a percentage of a vehicle’s sale price, its revenues increase as a vehicle’s price increases, i.e., it is effectively indexed for inflation, but the fuel tax of 18.4 cents per gallon is unrelated to the current price of gasoline or diesel fuel.

FRET and fuel taxes are due even if a given vehicle rarely operates on public highways. Klecha (1996), Hallock (2001), and many of the SMEs we interviewed emphasized how few miles, compared to commercial vehicles, DoD FRET-eligible vehicles incur on public high-

Table C.1Highway Trust Fund Revenue Sources, FYs 2006–2012

Fiscal Year

Estimated DoD Vehicle FRET

Payments (then-year $millions)

Total HTF Truck Retail Tax

Revenue (then-year $millions)

DoD FRET Percentage

of HTF Truck Retail Tax Revenue

HTF Fuel Tax Revenue

(then-year $millions)

Total HTF Revenue

(then-year $millions)

DoD FRET Percentage of Total HTF

Revenue

2006 45 3,619 1.23 34,574 40,109 0.11

2007 219 3,809 5.76 35,551 40,853 0.54

2008 358 1,446 24.73 35,858 37,423 0.96

2009 204 1,890 10.82 33,950 35,981 0.57

2010 268 1,562 17.17 33,973 35,537 0.75

2011 240 2,417 9.94 34,788 36,884 0.65

2012 93 3,855 2.41 35,327 40,146 0.23

SOURCES: Authors’ tabulations and U.S. Department of the Treasury, 2015.

34 Understanding and Assessing the Costs of the Federal Retail Excise Tax

ways. Hallock (2001) estimated that a typical Army truck might drive 25,000 miles on public highways over its lifetime while a typical commercial truck would drive nearly 300,000 miles on public highways over its lifetime. Similarly, while car owners do not pay an up-front vehicle excise tax, they pay the fuel excise tax on every gallon of fuel purchased, irrespective of how frequently they operate their cars on federal highways.

The Defense Logistics Agency receives a rebate from the IRS for tax-included fuel pur-chases for DoD vehicles that do not drive on highways. Many in DoD have suggested that DoD should similarly receive a rebate for or exemption from vehicle FRET payments.

DoD vehicle FRET payments have never represented more than one percent of overall HTF revenue, but they were a sizable fraction of the total truck retail tax proceeds in 2008 when overall truck retail tax proceeds plummeted. The HTF’s truck retail tax revenues have been quite volatile with a sharp downturn, presumably tied to the overall economy, from 2008 through 2010. The 2008 DoD vehicle FRET payment surge proved to be desirably counter-cyclical for the HTF, i.e., DoD vehicle FRET payments increased just as commercial vehicle FRET payments decreased.

The HTF’s primary revenue source, fuel tax revenue, has been quite stable in nominal terms, but has degraded with inflation and has not kept pace with the costs associated with building and maintaining highways. Federal motor fuel tax rates have remained at 18.4 cents per gallon since 1993, resulting in an inflation-adjusted tax rate of 11.5 cents (measured in 1993 dollars) today. Drivers of passenger vehicles with average fuel efficiency currently pay about $96 per year in federal fuel taxes (U.S. Government Accountability Office, 2015). This figure is likely to decrease as vehicles become more fuel-efficient, even though the costs of building and maintaining highways are likely to increase with inflation (Lewis, undated.). A proposed rule to tighten fuel economy standards would gradually decrease fuel consumption, reducing HTF revenues from the fuel tax by 21 percent by 2040 (Dinan and Austin, 2012). The long-term structural issues for the fuel-tax component of HTF financing make it more challenging to exempt DoD vehicles from the FRET.

Perhaps not surprisingly, in light of these HTF financial difficulties, since 2008 lawmak-ers have supplemented tax revenue for the HTF with $65 billion from the U.S. Treasury Gen-eral Fund (Kile, 2015). Of course, such use of general funds contradicts the principle that the HTF be financed by highway users.

35

References

Assistant Secretary of the Army for Financial Management and Comptroller, “Army Financial Management: Budget Materials,” website, last modified October 20, 2014. As of February 22, 2016: http://www.asafm.army.mil/offices/BU/BudgetMat.aspx?OfficeCode=1200

Damodaran, Aswath, “Cost of Capital by Sector (US),” updated January 2015. As of December 28, 2015: http://pages.stern.nyu.edu/~adamodar/New_Home_Page/datafile/wacc.htm

Day, Chris, “Exemption of Federal Retail Excise Tax on Military Vehicles” briefing, Department of Defense, Manufacturing and Industrial Base Policy (MIBP), November 21, 2014.

Dinan, Terry, and David Austin, “How Would Proposed Fuel Economy Standards Affect The Highway Trust Fund?” Congressional Budget Office, May 2012. As of January 2, 2016: https://www.cbo.gov/sites/default/files/112th-congress-2011-2012/reports/05-02-CAFE_brief.pdf

Hallock, Harry P., A DoD Conundrum: The Handling of Federal Retail Excise Tax on the Army’s Medium & Heavy Truck Fleet, Monterey, Calif.: Naval Postgraduate School, June 2001. As of January 12, 2016: https://calhoun.nps.edu/bitstream/handle/10945/10826/Mar01_Hallock.pdf?sequence=1&isAllowed=y

Internal Revenue Service, U.S. Department of the Treasury, Letter to Oshkosh Truck Company, TIN 39-0520270, Index No. 4051.00-00, December 19, 1990.

———, Excise Taxes (Including Fuel Tax Credits and Refunds), Publication 510, revised January 2016. As of March 5, 2016: https://www.irs.gov/pub/irs-pdf/p510.pdf

IRS—See Internal Revenue Service.

Kile, Joseph, “The Status of the Highway Trust Fund and Options for Paying for Highway Spending,” testimony before the Committee on Finance, United States Senate, June 18, 2015. As of January 2, 2016: https://www.cbo.gov/sites/default/files/114th-congress-2015-2016/reports/ 50297-TransportationTestimony-Senate.pdf

Klecha, John E., “More Than Just One Pocket to Another: Federal Excise Taxation of Military Medium and Heavy Trucks,” Warren, Mich.: U.S. Army Tank-automotive and Armaments Command, August 21, 1996.

———, “Opinion as to the Applicability of Federal Retail Excise Tax to Used Vehicles Inducted into Army Reset Programs after Being Returned to the United States by the Army from OCONUS Locations,” Memorandum of Law to Mr. Vince Faggioli, Command Counsel, Headquarters, U.S. Army Materiel Command, January 31, 2011.

Lewis, John, “Understanding the Highway Trust Fund,” United States House of Representatives, undated. As of January 2, 2016: https://johnlewis.house.gov/legislative-work/issues/transportation/understanding-highway-trust-fund

Office of Management and Budget, Circular A-94 Appendix C, November 2015. As of January 29, 2016: https://www.whitehouse.gov/omb/circulars_a094/a94_appx-c

Oshkosh Defense, “Medium Tactical Vehicle Replacement (MTVR),” web page, 2016. As of September 1, 2016: https://oshkoshdefense.com/vehicles/mtvr/#overview

36 Understanding and Assessing the Costs of the Federal Retail Excise Tax

Seltzer, David R., “Federal Income Tax Compliance Costs: A Case Study of Hewlett-Packard Company,” National Tax Journal, Vol. 50, No. 3, September 1997, pp. 487–493. As of January 12, 2016: http://www.ntanet.org/NTJ/50/3/ntj-v50n03p487-93-federal-income-tax-compliance.pdf

Slemrod, Joel B., and Varsha Venkatesh, “The Income Tax Compliance Cost of Large and Mid-Size Businesses,” University of Michigan, Ross School of Business Working Paper No. 914, September 2002. As of December 24, 2015: http://ssrn.com/abstract=913056