19

U.S. Shale Gas and Tight Oil: Game-Changers for the U.S. and the World Dr. Helen Currie, Senior Economist American Association of Port Authorities Annual Conference April 6, 2016

U.S. Shale Gas and Tight Oil:

Game-Changers for the U.S. and the World

Dr. Helen Currie, Senior Economist

American Association of Port Authorities Annual Conference

April 6, 2016

Cautionary StatementThe following presentation includes forward-looking statements. All statements included in this presentation other than statements of historical fact, including, without limitation, statements regarding production forecasts, anticipated production mix, estimates of operating costs, assumptions regarding future commodity prices, planned drilling activity, potential changes in leverage, estimates of future capital expenditures, estimates of recoverable resources, projected rates of return and efficiency gains, estimates of future cost of supply, as well as projected cash flow, inventory levels and capital efficiency, business strategy and other plans and objectives for future operations, are forward-looking statements.

Forward-looking statements relating to ConocoPhillips’ operations are based on management’s current expectations, estimates, forecasts and projections about ConocoPhillips and the industries in which it operates in general. These statements are not guarantees of future performance as they involve assumptions that, while made in good faith, may prove to be incorrect, and involve risks and uncertainties that are difficult to predict. Further, many of these forward-looking statements are based upon assumptions about future events that may prove to be inaccurate. Accordingly, actual outcomes and results may differ materially from what is expressed or forecast in such forward-looking statements. Any differences could result from a variety of factors, including, but not limited to, the following: oil and gas prices; operational hazards and drilling risks; potential failure to achieve, and potential delays in achieving expected reserves or production levels from existing and future oil and gas development projects; unsuccessful exploratory activities; unexpected cost increases or technical difficulties in constructing, maintaining or modifying company facilities; international monetary conditions and exchange controls; potential liability for remedial actions under existing or future environmental regulations or from pending or future litigation; limited access to capital or significantly higher cost of capital related to illiquidity or uncertainty in the domestic or international financial markets; general domestic and international economic and political conditions, as well as changes in tax, environmental and other laws applicable to ConocoPhillips’ business; and the factors generally described in Item 1A—Risk Factors in our 2014 Annual Report on Form 10-K. We caution you not to place undue reliance on our forward-looking statements, which are only as of the date of this presentation, and we undertake no obligation to publicly update or revise any forward-looking statements, whether as a result of new information, future events or otherwise.

Use of non-GAAP financial information – This presentation may include non-GAAP financial measures, which help facilitate comparison of company operating performance across periods and with peer companies. Any non-GAAP measures included herein will be accompanied by a reconciliation to the nearest corresponding GAAP measure on our website at www.conocophillips.com/nongaap.

Cautionary Note to U.S. Investors – The SEC permits oil and gas companies, in their filings with the SEC, to disclose only proved, probable and possible reserves. We use the term "resource" in this presentation that the SEC’s guidelines prohibit us from including in filings with the SEC. U.S. investors are urged to consider closely the oil and gas disclosures in our Form 10-K and other reports and filings with the SEC. Copies are available from the SEC and from the ConocoPhillips website.

2

Outline

• U.S. unconventional oil and natural gas production renaissance: scale and scope

• Many benefits generated

1) Economic

2) Environmental

3) Energy security

• Steps to support continuation of the success story and to meet the world’s energy needs affordably

3

World-Scale Growth in U.S. Unconventional Natural Gas and Oil Production

Source: U.S. Department of Energy, Energy Information Administration (EIA)4

U.S. Natural Gas Production(Billions of cubic feet per day)

U.S. Oil Production(Million barrels per day)

Shale Gas

Non-Shale Gas

25

35

45

55

65

75

20

00

20

03

20

06

20

09

20

12

20

15

Unconventional:Shale Gas

Conventional

0

2

4

6

8

10

12

Conventional -

Lower-48, Gulf of Mexico

Tight Oil

Alaska

Natural Gas Liquids

5Map shows wells drilled in U.S. Lower 48 states since start of 20th century; well locations from U.S. Geological Survey; resource estimates based upon publically available sources and ConocoPhillips estimates

America’s "Big Four" Unconventional Fields are World-Class Discoveries

Growth in Production Restored U.S. Role as Leading Oil Producer

0

2

4

6

8

10

12

14

UnitedStates

SaudiArabia

Russia China Canada Iran UAE Iraq Kuwait Mexico

Mill

ion

Bar

rels

per

Day

Crude Oil & Condensate

NGLs

Source: Rystad Energy, May 2015 excluding U.S., EIA Petroleum Supply Monthly for U.S.

Crude, Condensate and NGLs Production for Top 10 Countries, 2014

OPEC Neutral Zone production split between Saudi Arabia and Kuwait6

Impact of Lower Market Prices: U.S. Producers Adapt and Improve

Mid-sizedE&Ps

SmallE&Ps

Source: U.S. Department of Energy, EIA Short Term Energy Outlook, March, 2016.

U.S. Natural Gas Production and Prices U.S. Crude Oil Production and Prices

5

$0

$2

$4

$6

$8

$10

$12

$14

50

55

60

65

70

75

80

Henry Hub, $/mmbtu(Right axis)

Production in Billion cubic feet per day (Left axis)

$0

$20

$40

$60

$80

$100

$120

$140

4

5

6

7

8

9

10

Production in Million barrels per day (Left axis)

Brent, $/barrel(Right axis)

7

*** 2016 and 2017 data are EIA forecasts

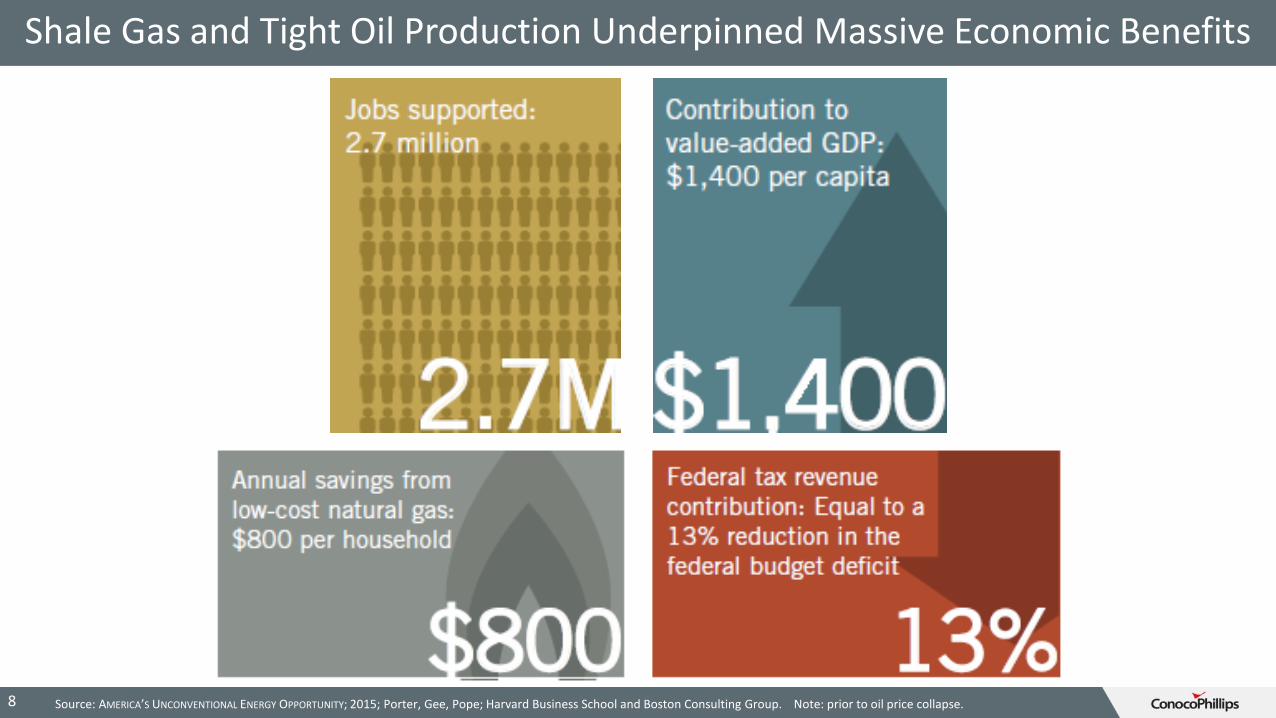

Shale Gas and Tight Oil Production Underpinned Massive Economic Benefits

8 Source: AMERICA’S UNCONVENTIONAL ENERGY OPPORTUNITY; 2015; Porter, Gee, Pope; Harvard Business School and Boston Consulting Group. Note: prior to oil price collapse.

4%

5%

6%

7%

8%

9%

10%

2007 2008 2010 2011 2013 2014 2016

U.S. Unemployment Rate

U.S. oil & gas drove 40% of U.S. GDP growth from

2008-2013*

0.9

1.0

1.1

1.2

1.3

1.4

1.5

1.6

1.7

2007 2008 2010 2011 2013 2014 2016

Oil and Gas Sector Expanded While Other Sectors LaggedIndex of Job Growth: Jan. 2007 = 1.0

Oil and Gas Sector Jobs

Total Private Sector

133

165

105103

“For every job created in oil production, three jobs are created in the

supply chain and six more in the broader

economy.”*

Sources: U.S. Bureau of Labor Statistics (Total Private Sector Jobs, NAICS 211000 and 213112) for data displayed on graphs; Quotations(*) from IHS Inc., “Unleashing the Supply Chain” released March 2015, pp. 4-5.9

Oil & Natural Gas Production Spurred U.S. Jobs and Economic Growth

10

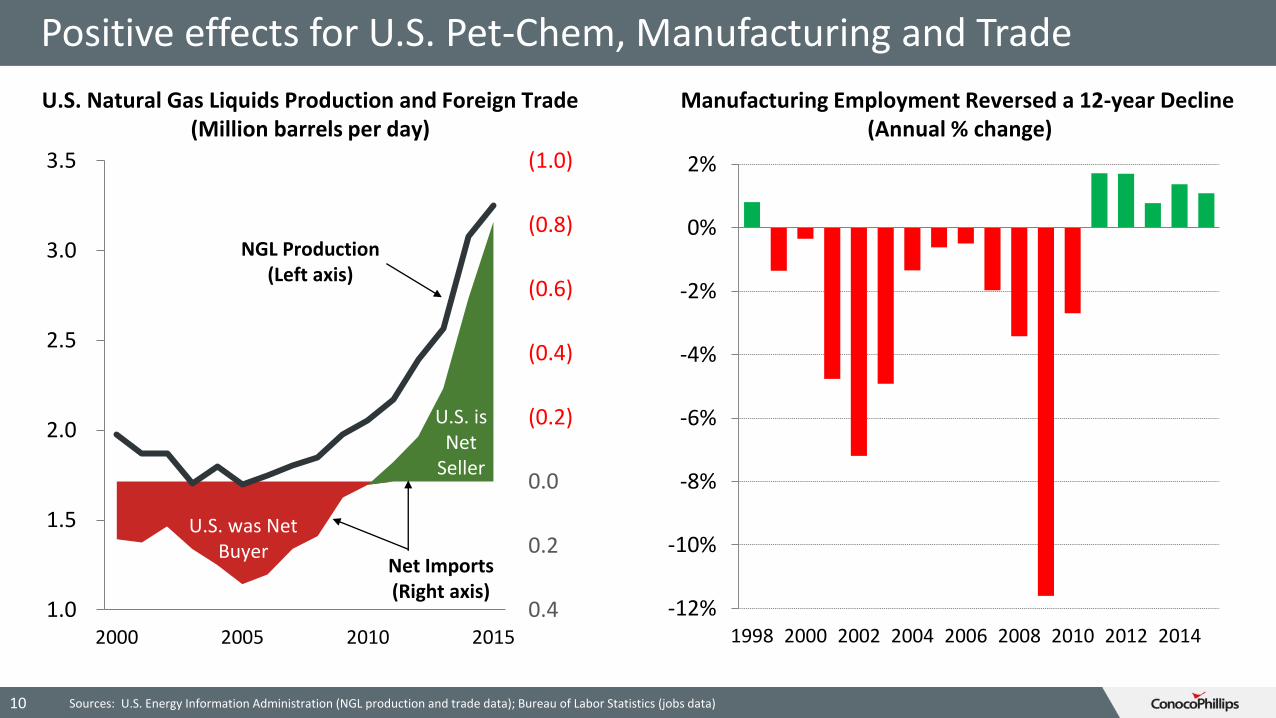

Positive effects for U.S. Pet-Chem, Manufacturing and Trade

Sources: U.S. Energy Information Administration (NGL production and trade data); Bureau of Labor Statistics (jobs data)

(1.0)

(0.8)

(0.6)

(0.4)

(0.2)

0.0

0.2

0.41.0

1.5

2.0

2.5

3.0

3.5

2000 2005 2010 2015

U.S. Natural Gas Liquids Production and Foreign Trade(Million barrels per day)

NGL Production(Left axis)

Net Imports(Right axis)

U.S. was Net Buyer

U.S. is Net

Seller

-12%

-10%

-8%

-6%

-4%

-2%

0%

2%

1998 2000 2002 2004 2006 2008 2010 2012 2014

Manufacturing Employment Reversed a 12-year Decline (Annual % change)

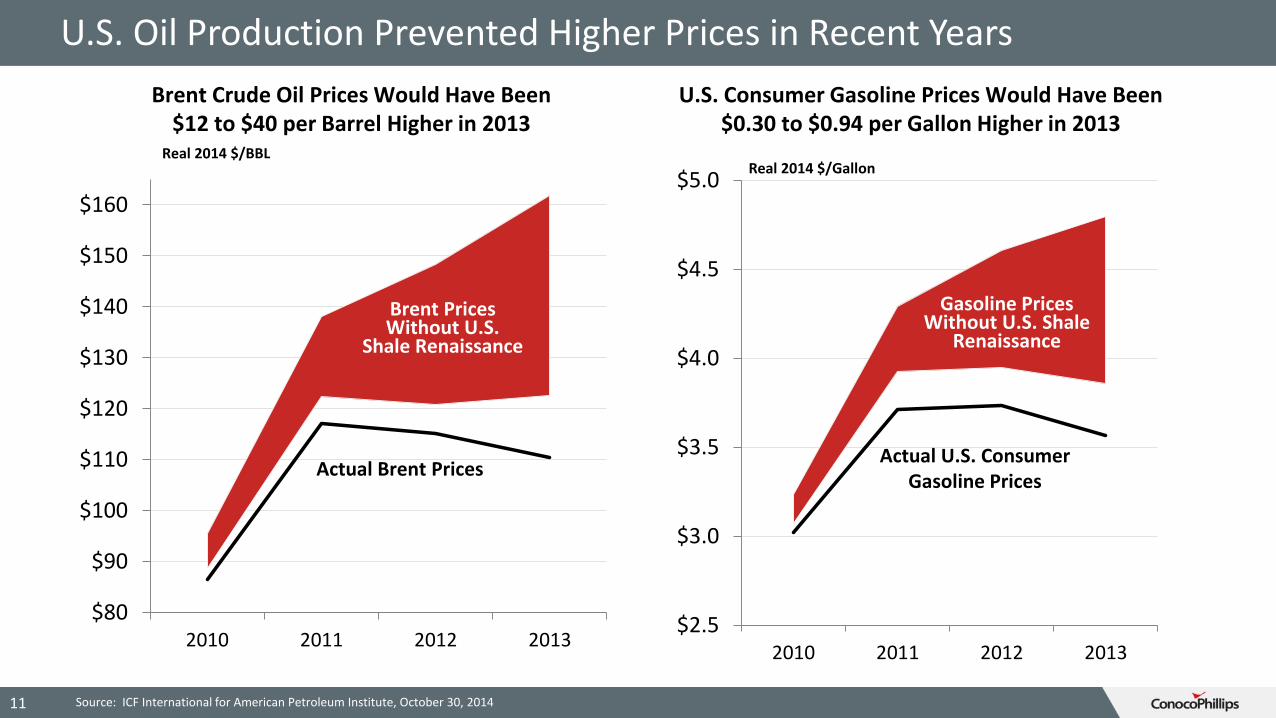

U.S. Oil Production Prevented Higher Prices in Recent Years

$80

$90

$100

$110

$120

$130

$140

$150

$160

2010 2011 2012 2013

Brent Crude Oil Prices Would Have Been$12 to $40 per Barrel Higher in 2013

Actual Brent Prices

Brent Prices Without U.S.

Shale Renaissance

Real 2014 $/BBL

$2.5

$3.0

$3.5

$4.0

$4.5

$5.0

2010 2011 2012 2013

U.S. Consumer Gasoline Prices Would Have Been $0.30 to $0.94 per Gallon Higher in 2013

Real 2014 $/Gallon

Actual U.S. Consumer Gasoline Prices

Gasoline Prices Without U.S. Shale

Renaissance

Source: ICF International for American Petroleum Institute, October 30, 2014 11

Free Trade Prevents Steep Discounts on Domestic Crude Prices

($20)

($15)

($10)

($5)

$0

$5

2000 2004 2008 2012 2016 2020

Futures 6-10-14

Futures 3-31-16

Historical

Dis

cou

nt

for

Do

mes

tic

cru

de

Pre

miu

m f

or

do

mes

tic

cru

de

12

Source: ICE, CME Group

Benchmark Crude Price DifferentialWTI – Brent ($/bbl)

• With U.S. crude production in decline, the domestic crude oil price discount is small today

• Without crude exports, seasonal discounts would have been possible even with production declining today when U.S. refineries are in steep maintenance turnarounds

• Without crude exports, the domestic crude price discount would have grown over time as the global oil price recovered and U.S. crude production growth resumed

• Crude exports are more likely to be economic when U.S. refineries are in turnaround

Critical Success Factors for U.S. Production Growth

• Legal and fiscal systems that facilitate investment

• Private property & mineral rights

• Fit for purpose regulations

• Efficient permitting process

• Large drilling fleet and service/support capabilities

• Highly developed transportation infrastructure

• Transparent market pricing

• Numerous market hubs

• Liquid Spot and Forward markets

13

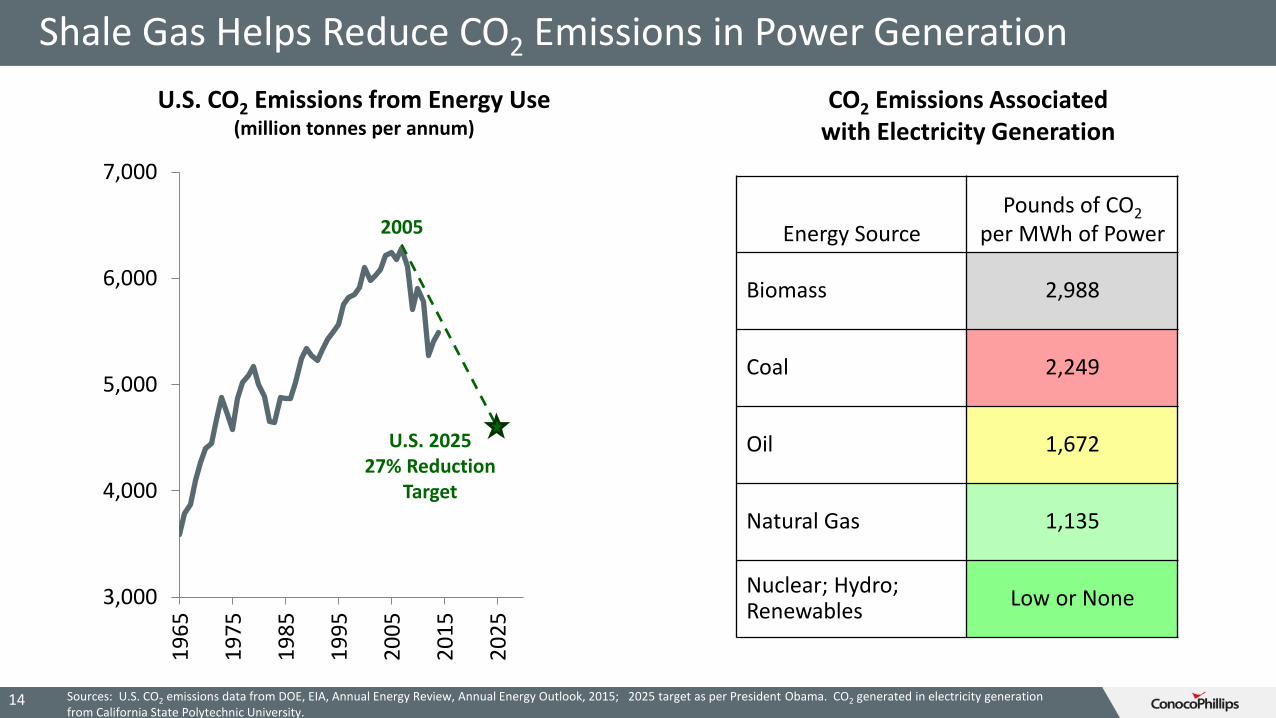

Shale Gas Helps Reduce CO2 Emissions in Power Generation

14

Energy SourcePounds of CO2

per MWh of Power

Biomass 2,988

Coal 2,249

Oil 1,672

Natural Gas 1,135

Nuclear; Hydro; Renewables

Low or None

CO2 Emissions Associatedwith Electricity Generation

3,000

4,000

5,000

6,000

7,0001

96

5

19

75

19

85

19

95

20

05

20

15

20

25

U.S. 202527% Reduction

Target

2005

U.S. CO2 Emissions from Energy Use(million tonnes per annum)

Sources: U.S. CO2 emissions data from DOE, EIA, Annual Energy Review, Annual Energy Outlook, 2015; 2025 target as per President Obama. CO2 generated in electricity generation from California State Polytechnic University.

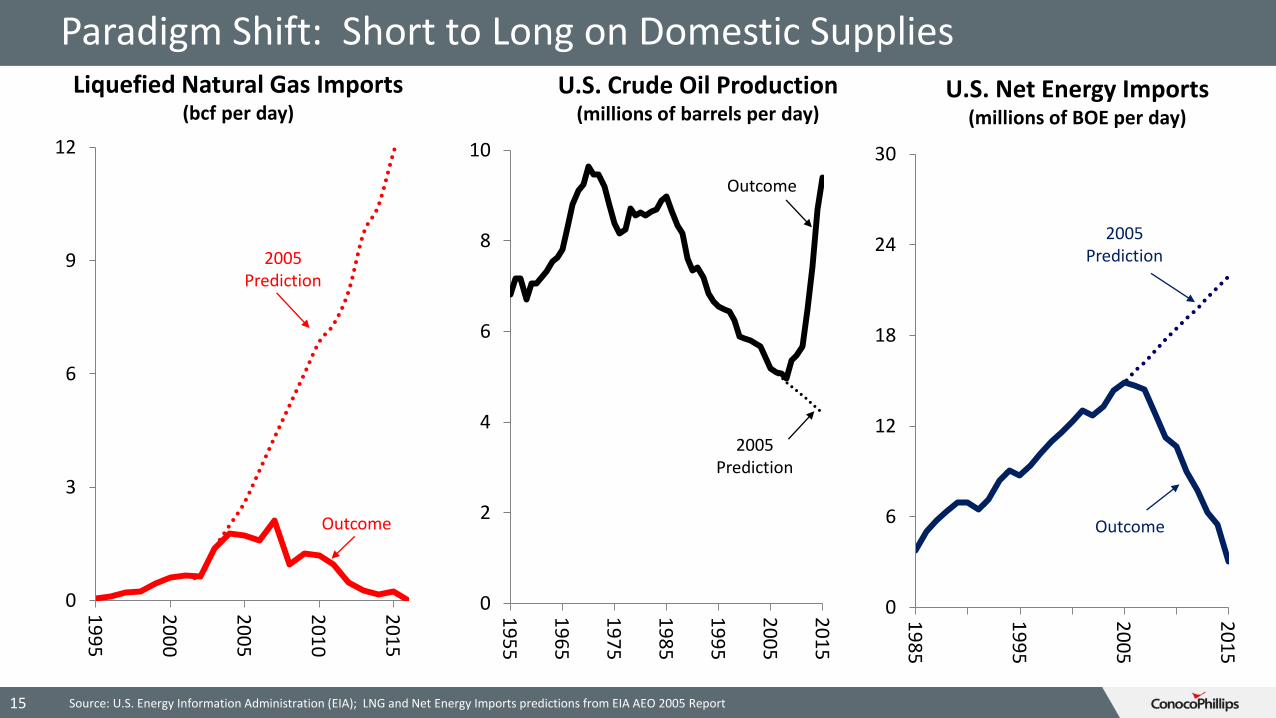

Paradigm Shift: Short to Long on Domestic Supplies

Source: U.S. Energy Information Administration (EIA); LNG and Net Energy Imports predictions from EIA AEO 2005 Report15

0

6

12

18

24

30

19

85

19

95

20

05

20

15

0

2

4

6

8

10

19

55

19

65

19

75

19

85

19

95

20

05

20

15

2005Prediction

Outcome

0

3

6

9

12

19

95

20

00

20

05

20

10

20

15

Outcome

2005Prediction

2005Prediction

Outcome

U.S. Crude Oil Production(millions of barrels per day)

Liquefied Natural Gas Imports(bcf per day)

U.S. Net Energy Imports(millions of BOE per day)

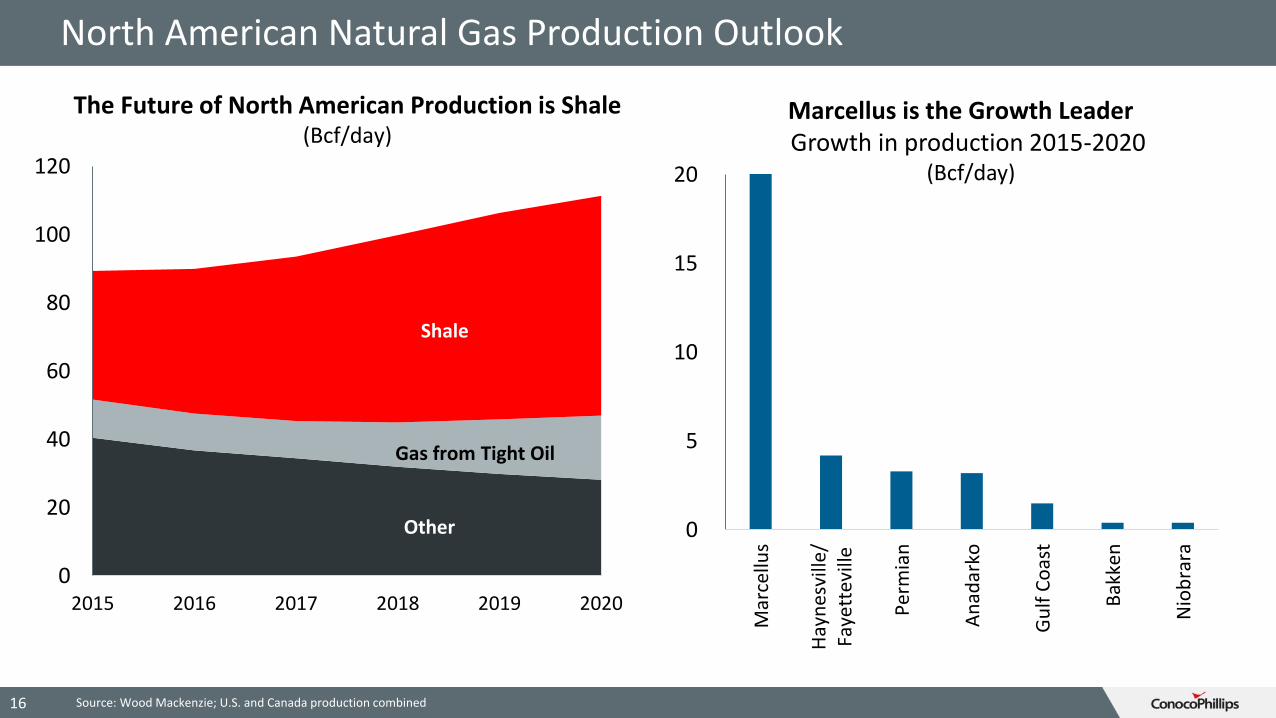

North American Natural Gas Production Outlook

Source: Wood Mackenzie; U.S. and Canada production combined16

0

20

40

60

80

100

120

2015 2016 2017 2018 2019 2020

The Future of North American Production is Shale(Bcf/day)

Shale

Other

Gas from Tight Oil

0

5

10

15

20

Mar

cellu

s

Hay

ne

svill

e/Fa

yett

evill

e

Per

mia

n

An

adar

ko

Gu

lf C

oas

t

Bak

ken

Nio

bra

ra

Marcellus is the Growth LeaderGrowth in production 2015-2020

(Bcf/day)

Affordable Shale Gas Enables LNG Exports

17

Almost 70 MTPA (9 BCFD) capacity Online by 2020

0

2

4

6

8

2016 2017 2018 2019 2020

Gulf Coast East Coast

(Bcf/day)

Sabine Pass*

Cameron

Freeport

Corpus Christi

Cove Point

U.S. Liquefaction Operational & Under Construction Today

OperationalUnder Construction

Source: Map, ConocoPhillips; Liquefaction volumes, Wood Mackenzie

Source: U.S. Department of Energy, EIA, Short Term Energy Outlook

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

2010 2011 2012 2013 2014 2015

Growth in U.S. Tight Oil Production

Increase in production since December 2009

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

2010 2011 2012 2013 2014 2015

Growth in Global Supply Disruptions

Increase in losses since 2009

(Million Barrels per Day) (Million Barrels per Day)

18

U.S. Tight Oil Production Has Helped Stabilize World Oil Supplies

Summary

• Domestic production created numerous, wide-ranging benefits across the country

o Jobs and Income growth in states with shale resources plus other regions providing service or supply-chain inputs to production

o U.S. CO2 emissions fell following increase in use of natural gas for power generation

o U.S. and global energy security enhanced by reliability and competitiveness of U.S. supplies

19

U.S. unconventional gas and oil renaissance: True Game-Changers for Global Gas and Oil Markets