171

ALTERNATIVES FOR POWER GENERATION IN THE GREATER MEKONG SUB-REGION Volume 6: Socialist Republic of Viet Nam Power Sector Scenarios Final 31 March 2016

| Date post: | 29-Jan-2017 |

| Category: |

Documents |

| Upload: | duongtuong |

| View: | 225 times |

| Download: | 2 times |

ALTERNATIVES FOR POWER GENERATION IN THE GREATER MEKONG SUB-REGION

Volume6:

SocialistRepublicofVietNamPowerSectorScenarios

Final

31 March 2016

FINAL

IntelligentEnergySystems IESREF:5973 ii

DisclaimerThis report has been prepared by Intelligent Energy Systems Pty Ltd (IES) andMekongEconomics (MKE) in relation toprovisionofservices toWorldWideFundforNature(WWF).Thisreportissuppliedingoodfaithandreflectstheknowledge,expertiseandexperienceof IESandMKE. Inconducting theresearchandanalysisforthisreportIESandMKEhaveendeavouredtousewhatitconsidersisthebestinformation available at the date of publication. IES and MKE make norepresentationsorwarrantiesastotheaccuracyoftheassumptionsorestimatesonwhichtheforecastsandcalculationsarebased.

IESandMKEmakenorepresentationorwarrantythatanycalculation,projection,assumption or estimate contained in this report should or will be achieved. Thereliance that the Recipient places upon the calculations and projections in thisreportisamatterfortheRecipient’sowncommercialjudgementandIESacceptsnoresponsibilitywhatsoeverforanylossoccasionedbyanypersonactingorrefrainingfromactionasaresultofrelianceonthisreport.

FINAL

IntelligentEnergySystems IESREF:5973 iii

AcronymsAD AnaerobicDigestion

ADB AsianDevelopmentBank

AGL AboveGroundLevel

ASEAN AssociationofSoutheastAsianNations

ASES AdvancedSustainableEnergySector

BAU BusinessAsUsual

BCM/Bcm BillionCubicMetres

BNEF BloombergNewEnergyFinance

BOT Build-Own-Transfer

BP BritishPetroleum

BST BulkSupplyTariff

BTU/Btu BritishThermalUnit

CAA CommercialArrangementArea

CAGR CompoundAnnualGrowthRate

CAPEX CapitalExpenditure

CCGT CombinedCycleGasTurbine

CCS CarbonCaptureandStorage

CENER NationalRenewableEnergyCentre

CHP CombinedHeatandPower

CIEMOT CentrodeInvestigacionesEnergeticasMedioambientalesyTecnológicas

COD CommercialOperationsDate

CSP ConcentratedSolarPower

DNI DirectNormalIrradiation

DR DemandResponse

DSM DemandSideManagement

DTU TechnicalUniversityofDenmark

EE EnergyEfficiency

FINAL

IntelligentEnergySystems IESREF:5973 iv

EIA EnergyInformationAdministration

EPTC ElectricPowerTradingCompany

ERAV ElectricityRegulatoryAuthorityofVietNam

EVN ElectricityofVietNam

FOB FreeonBoard

FOM FixedOperatingandMaintenance

GDE GeneralDirectorateforEnergy

GDP GrossDomesticProduct

GHI GlobalHorizontalIrradiance

GMS GreaterMekongSubregion

GT GasTurbine

HV HighVoltage

ICT InformationandCommunicationTechnology

IDAE InstitutoparalaDiversificaciónyAhorrodelaEnergía

IEA InternationalEnergyAgency

IES IntelligentEnergySystemsPtyLtd

IPP IndependentPowerProducer

IRENA InternationalRenewableEnergyAgency

LCOE OverallLevelisedCostofElectricity

LNG LiquefiedNaturalGas

LPG LiquefiedPetroleumGas

MKE MekongEconomics

MMCM MillionCubicMetres

MOIT MinistryofIndustryandTrade

MOU MemorandumofUnderstanding

MTPA MillionTonnesPerAnnum

MV MediumVoltage

NASA NationalAeronauticsandSpaceAdministration(theUnitedStates)

NLDC NationalLoadDispatchCentre

FINAL

IntelligentEnergySystems IESREF:5973 v

NPT NationalPowerTransmissionCorporation

NPV NetPresentValue

NREL NationalRenewableEnergyLaboratory(theUnitedStates)

OECD OrganisationforEconomicCo-operationandDevelopment

OPEC OrganisationofthePetroleumExportingCountries

OPEX OperationalExpenditure

PC PowerCorporation

PDP PowerDevelopmentPlan

PDR People’sDemocraticRepublic(ofLaos)

PPA PowerPurchaseAgreements

PRC People’sRepublicofChina

PV Photovoltaic

PVGas GasTradingCorporationunderPVN

PVPower PowerCorporationunderPVN

PVN PetroVietnam-VietNamNationalOilandGasGroup

RE RenewableEnergy

REVN RenewableEnergyofVietNamJointStockCompany

ROR RunofRiver

RPR ReservestoProductionRatio

SB SingleBuyer

SCADA/EMS SupervisoryControlandDataAcquisition/EnergyManagementSystem

SES SustainableEnergySector

SMO SystemandMarketOperator

ST SteamTurbine

SWERA SolarandWindEnergyResourceAssessment

SWH SolarWaterHeating

TCF/Tcf TrillionCubicFeet

TKV VietNamNationalCoalandMineralIndustryGroup

TNO TransmissionNetworkOperator

FINAL

IntelligentEnergySystems IESREF:5973 vi

TOE TonneofOilEquivalent

UN UnitedNations

US UnitedStates

USAID UnitedStatesAgencyforInternationalDevelopment

USD UnitedStatesDollar

VCGM VietNamCompetitiveGenerationMarket

VINACOMIN VietNamNationalCoalandMineralIndustryGroup

VOM VariableOperatingandMaintenance

VWEM VietNamWholesaleElectricityMarket

WBG WorldBankGroup

WEO WorldEnergyOutlook

WWF WorldWideFundforNature

WWF-GMPO

WWF–GreaterMekongProgrammeOffice

FINAL

IntelligentEnergySystems IESREF:5973 vii

TableofContents1 Introduction 9

1.1 ReportStructure 92 Background:VietNam’sElectricitySector 11

2.1 IndustryStructure 112.2 PowerSystem 132.3 InstalledCapacityandReserveMargin 142.4 ElectricityDemand 172.5 GenerationSupply 192.6 ImportsandExports 21

3 DevelopmentOptionsforVietNam’sElectricitySector 223.1 Overview 223.2 DomesticandImportedCoalResources 253.3 NaturalGasResources 273.5 HydroPower 323.10OceanEnergy 513.11RenewableEnergyPotentialandDiversity 51

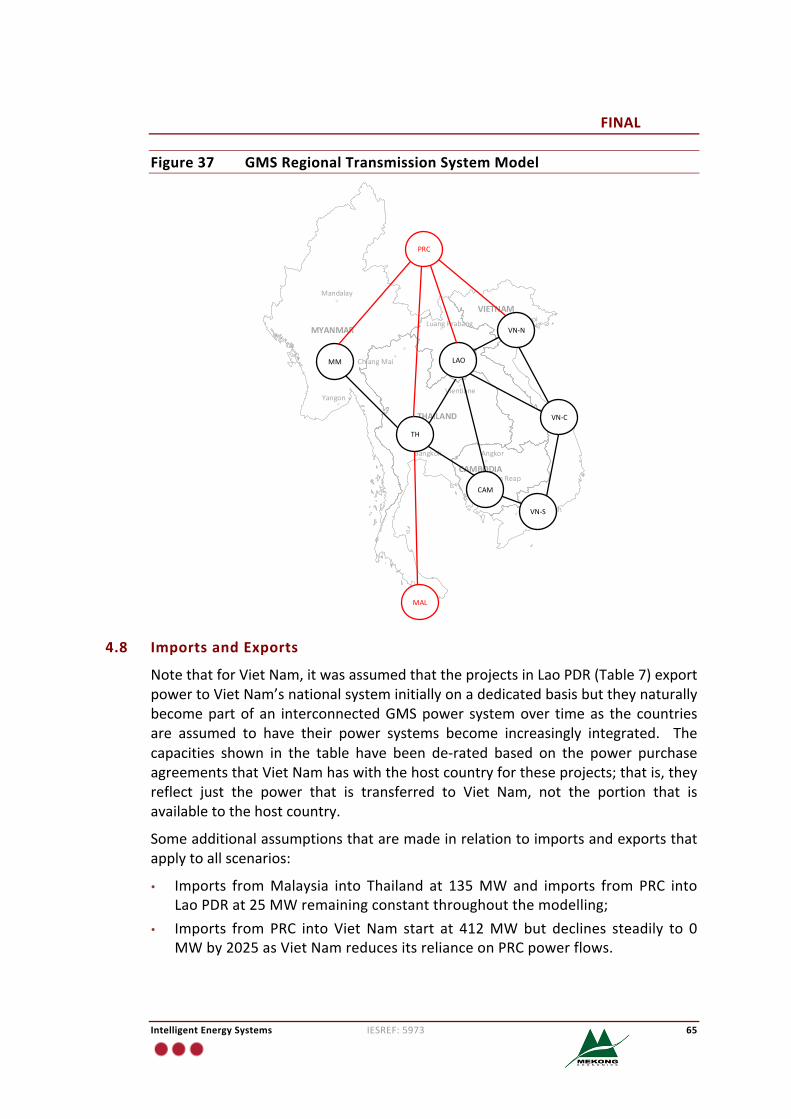

4 VietNamDevelopmentScenarios 534.1 Scenarios 534.2 TechnologyCostAssumptions 564.3 FuelPricingOutlook 594.4 VietNamRealGDPGrowthOutlook 604.5 PopulationGrowth 614.6 CommittedGenerationProjectsinBAU,SESandASESScenarios 614.7 RegionalTransmissionSystemIntegration 644.8 ImportsandExports 654.9 Technical-EconomicPowerSystemModelling 66

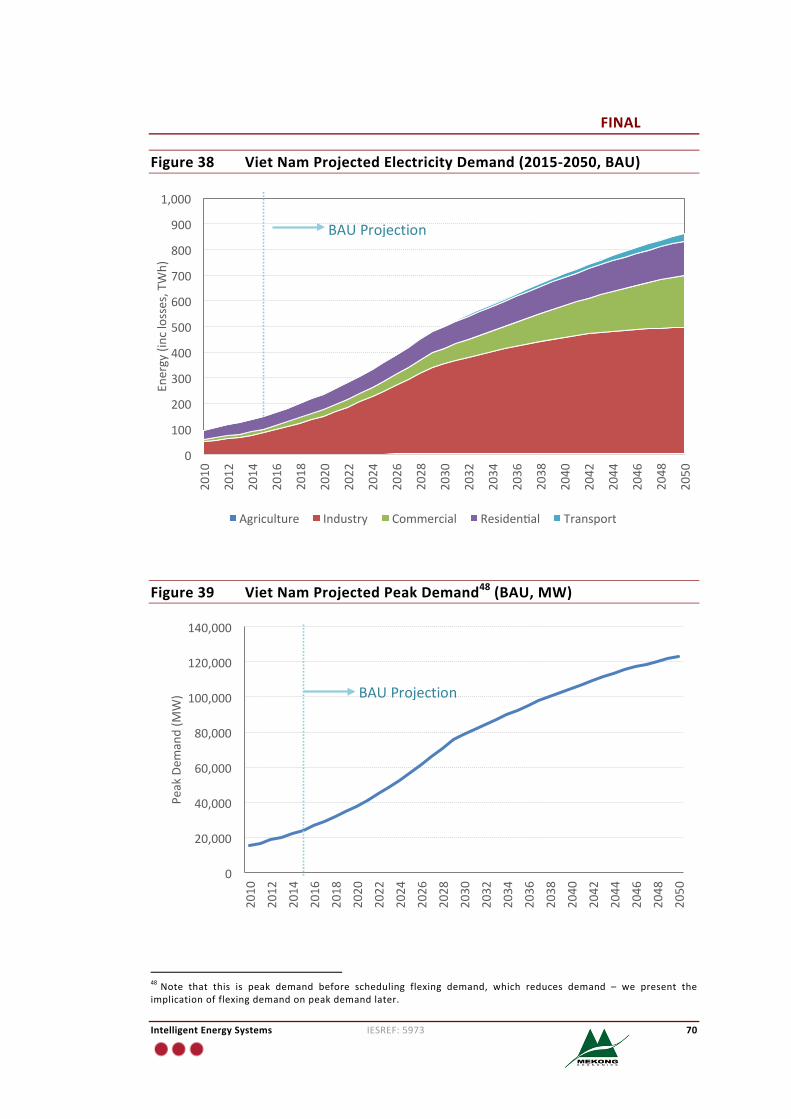

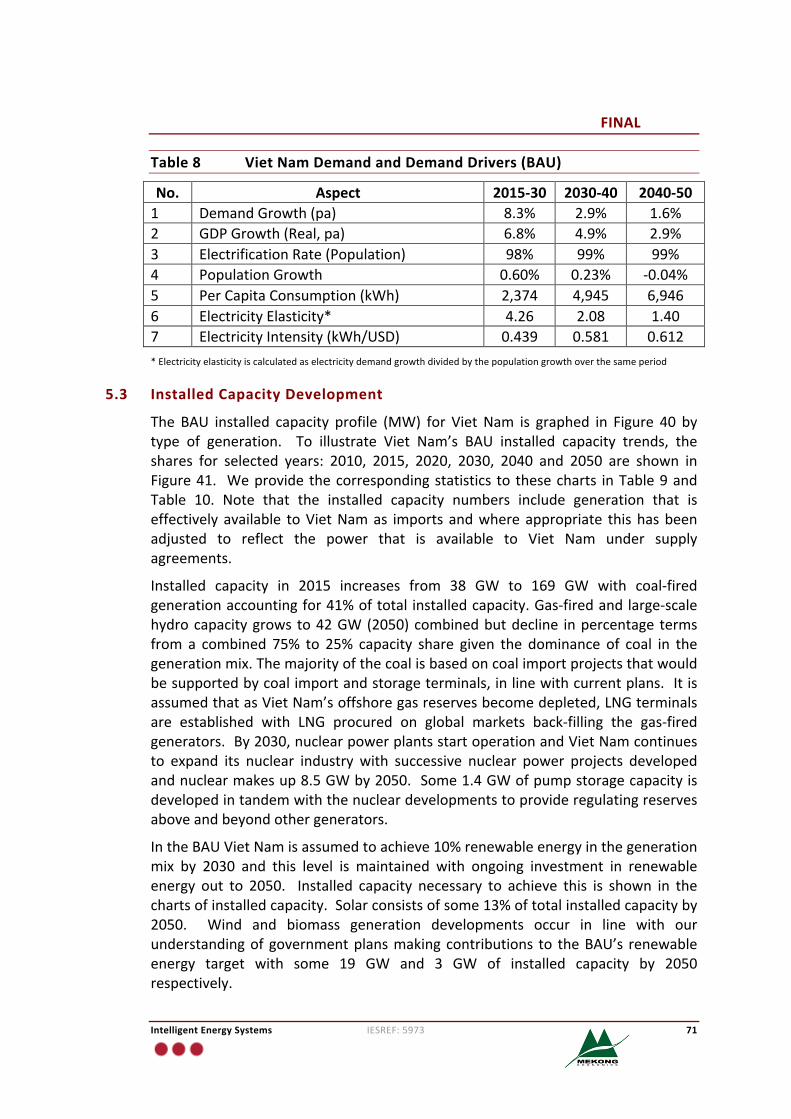

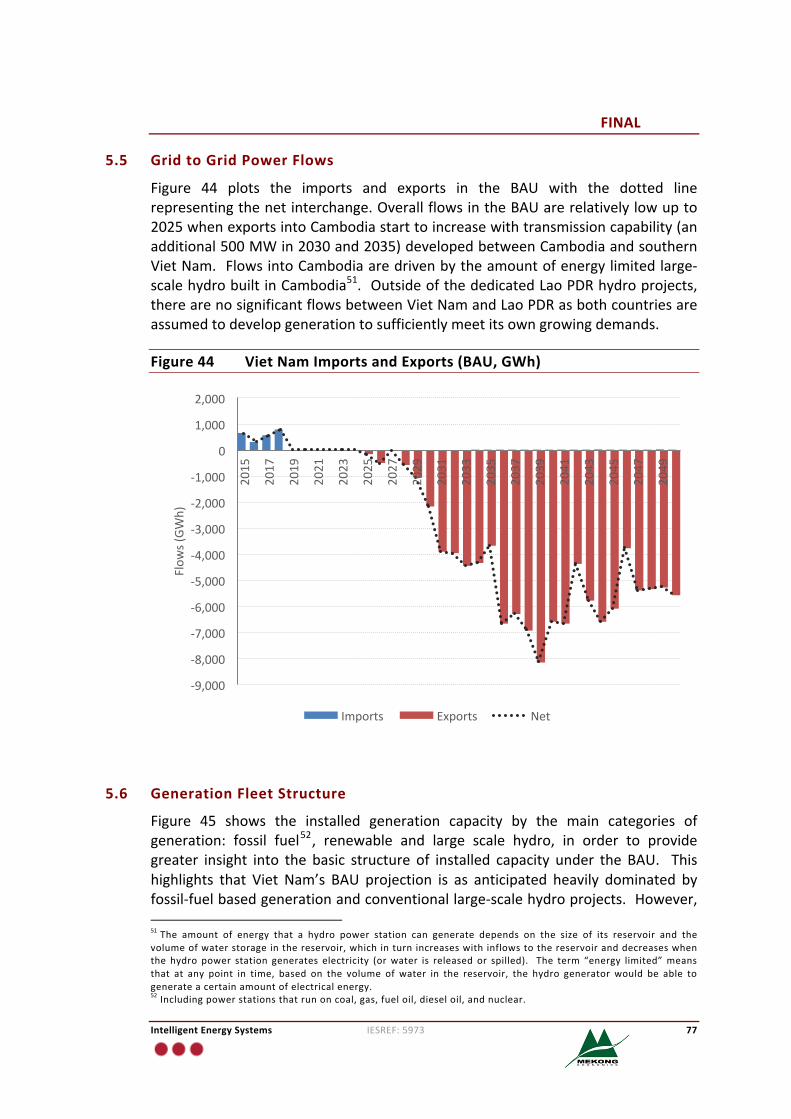

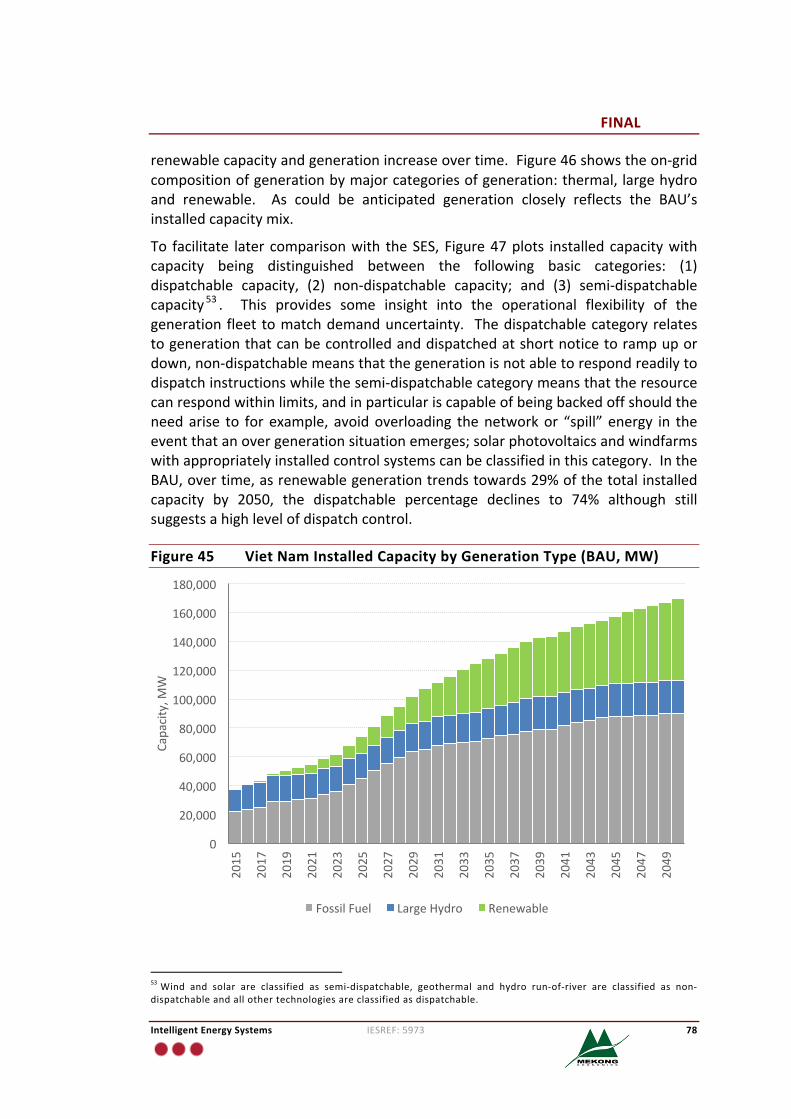

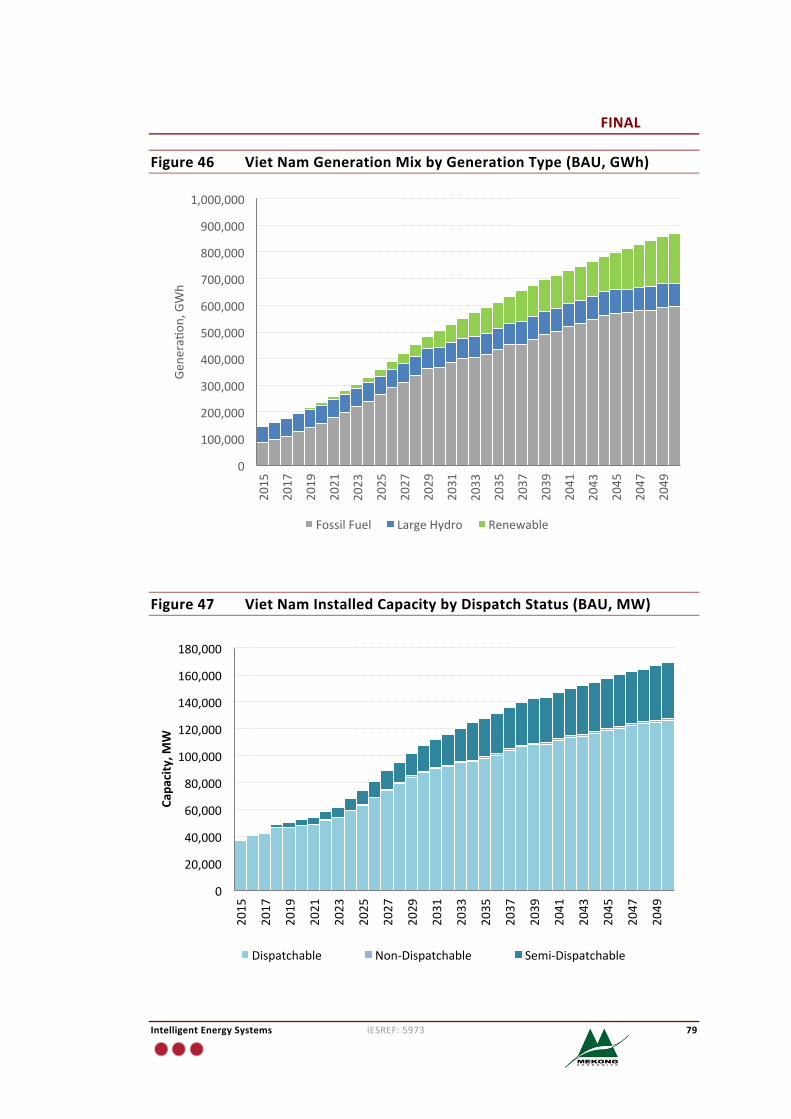

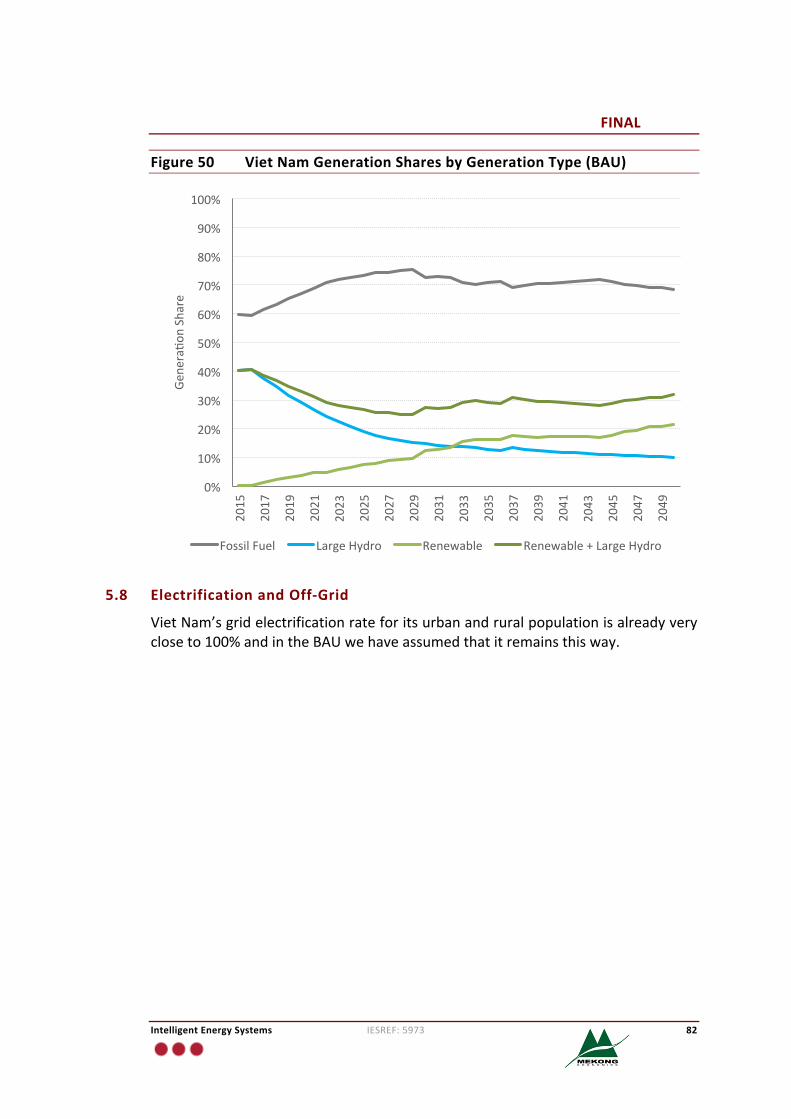

5 BusinessasUsualScenario 685.1 BusinessasUsualScenario 685.2 ProjectedDemandGrowth 695.3 InstalledCapacityDevelopment 715.4 ProjectedGenerationMix 745.5 GridtoGridPowerFlows 775.6 GenerationFleetStructure 775.7 ReserveMarginandGenerationTrends 805.8 ElectrificationandOff-Grid 82

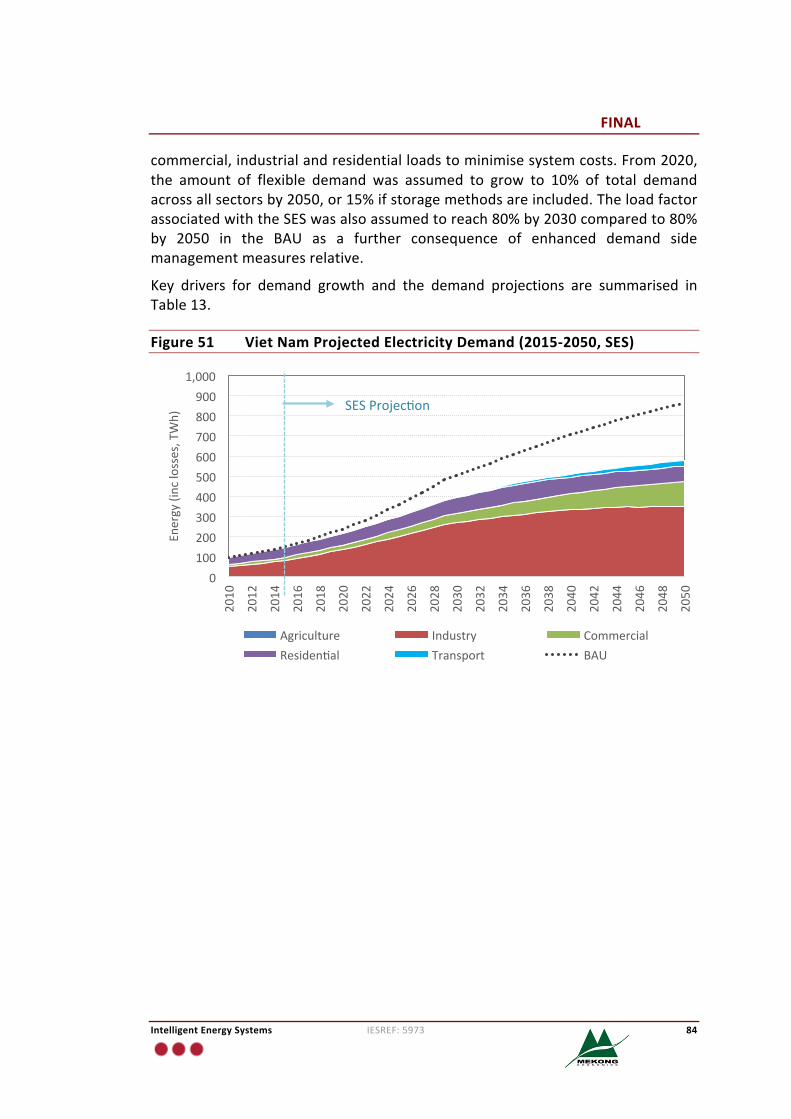

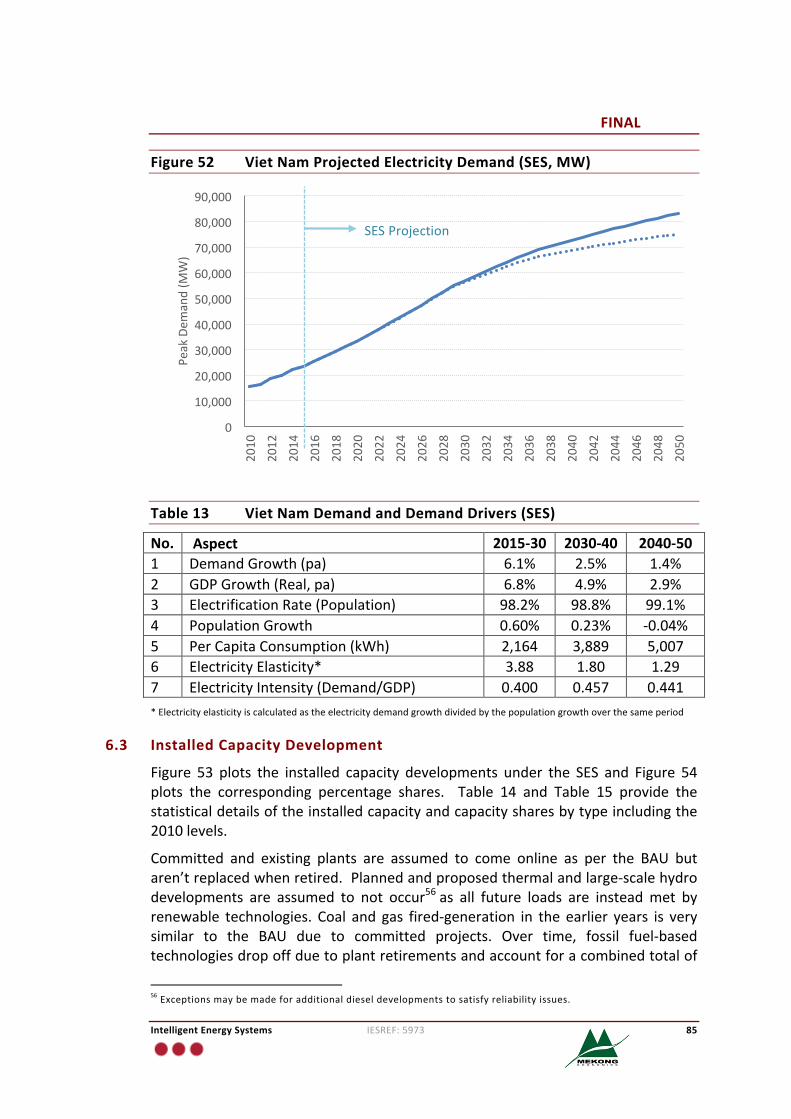

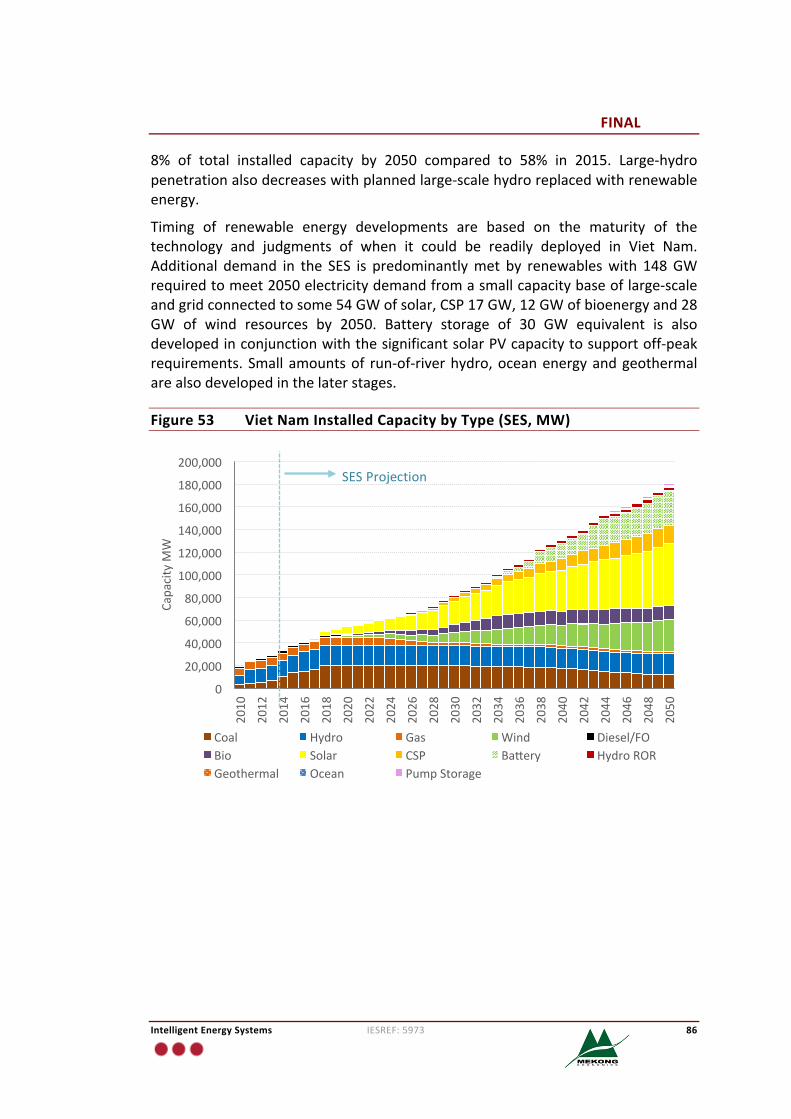

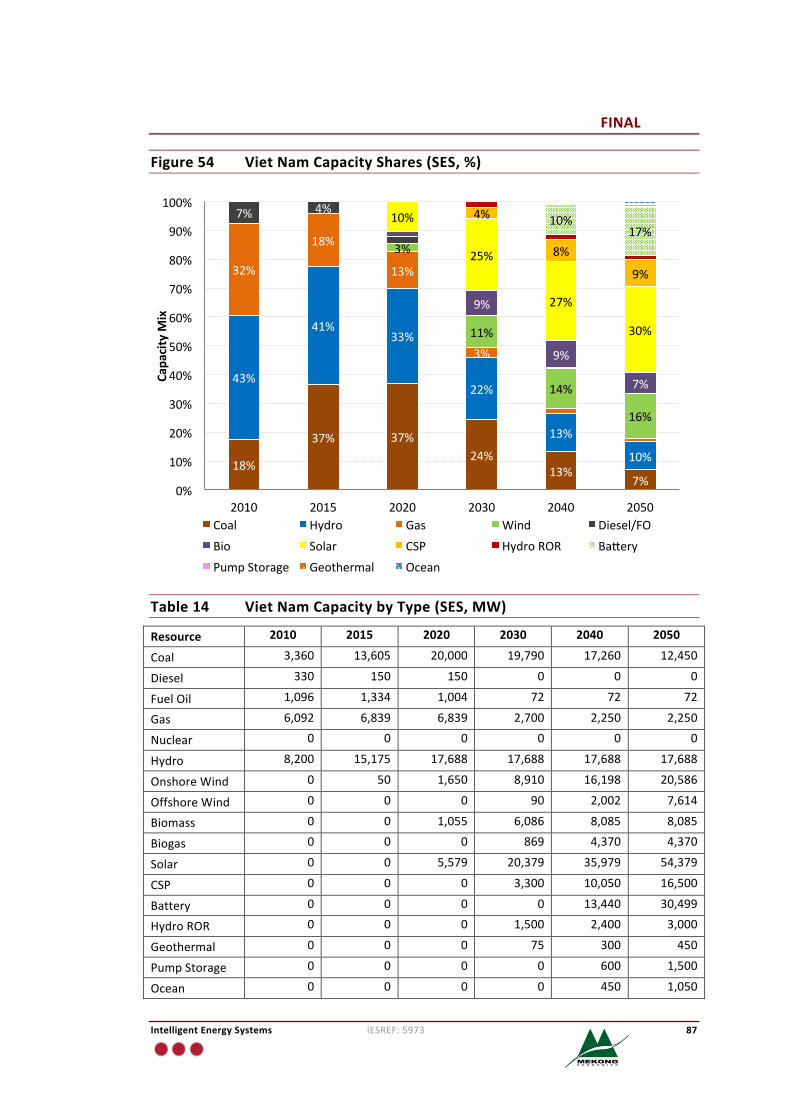

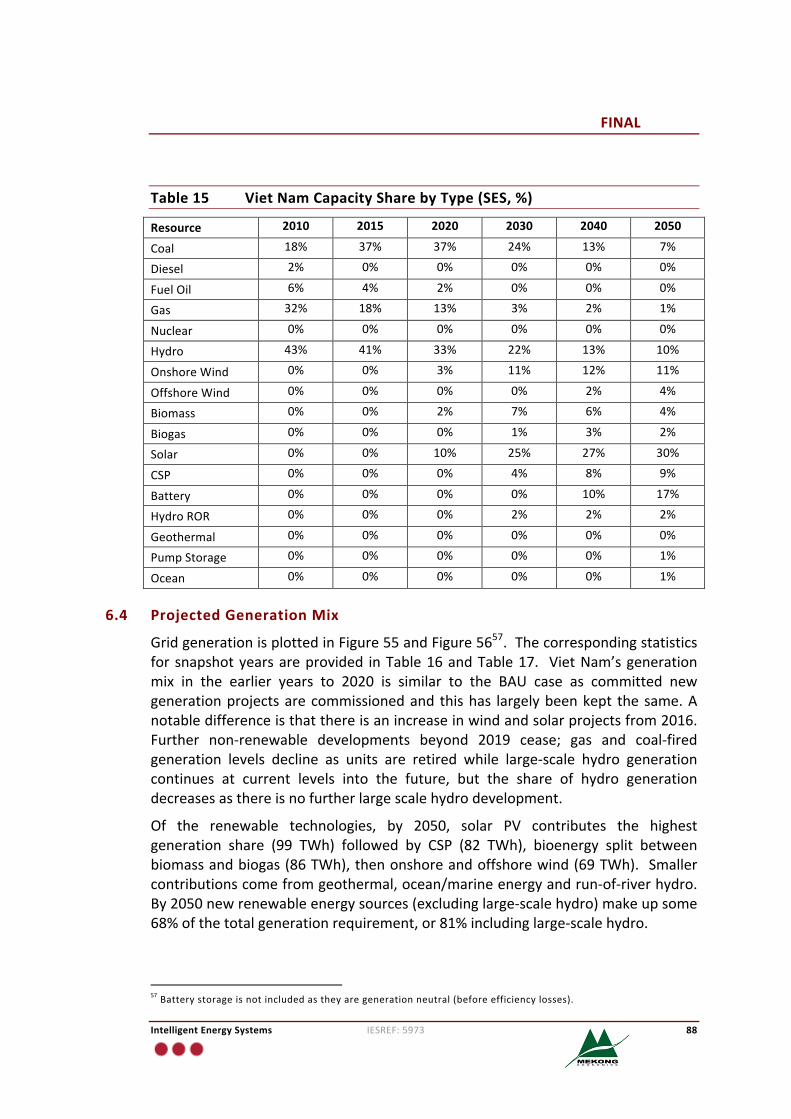

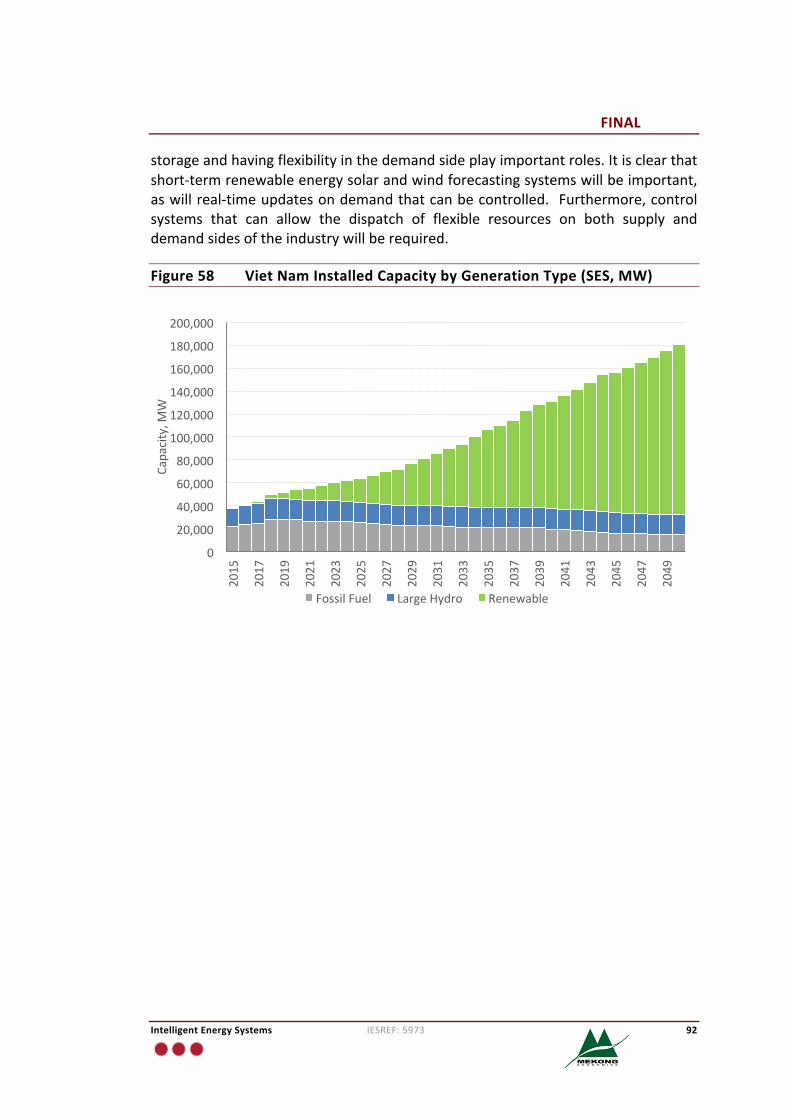

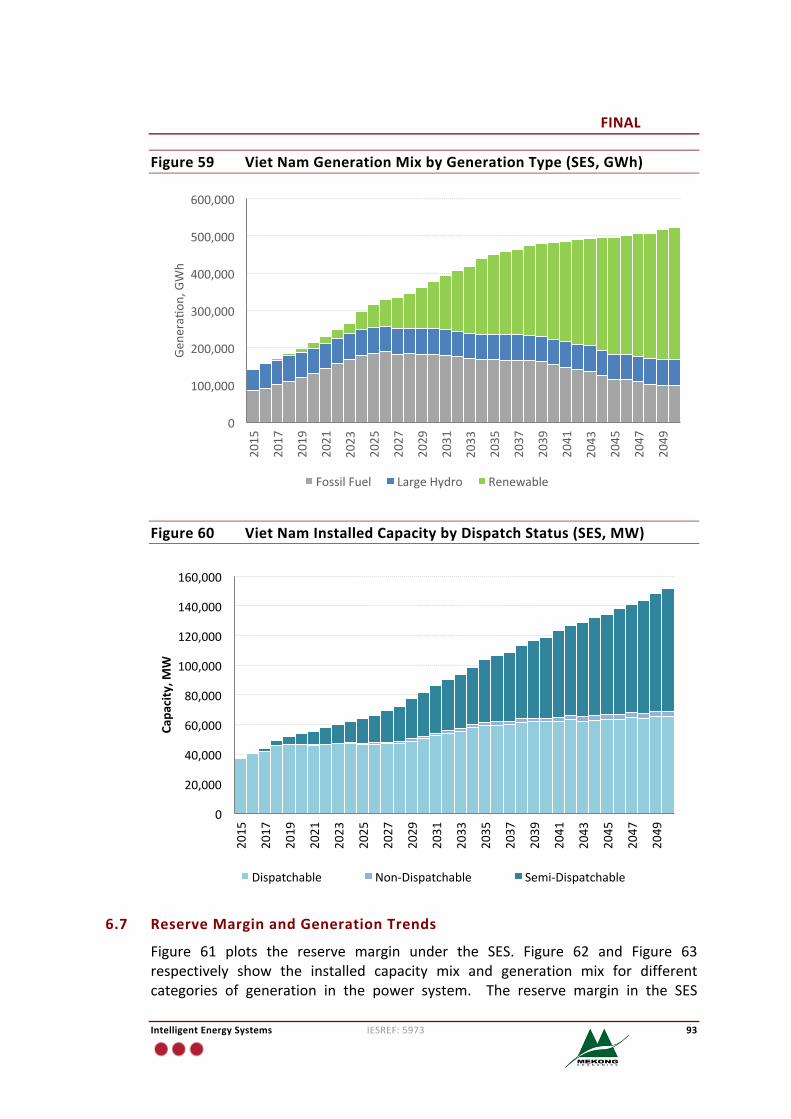

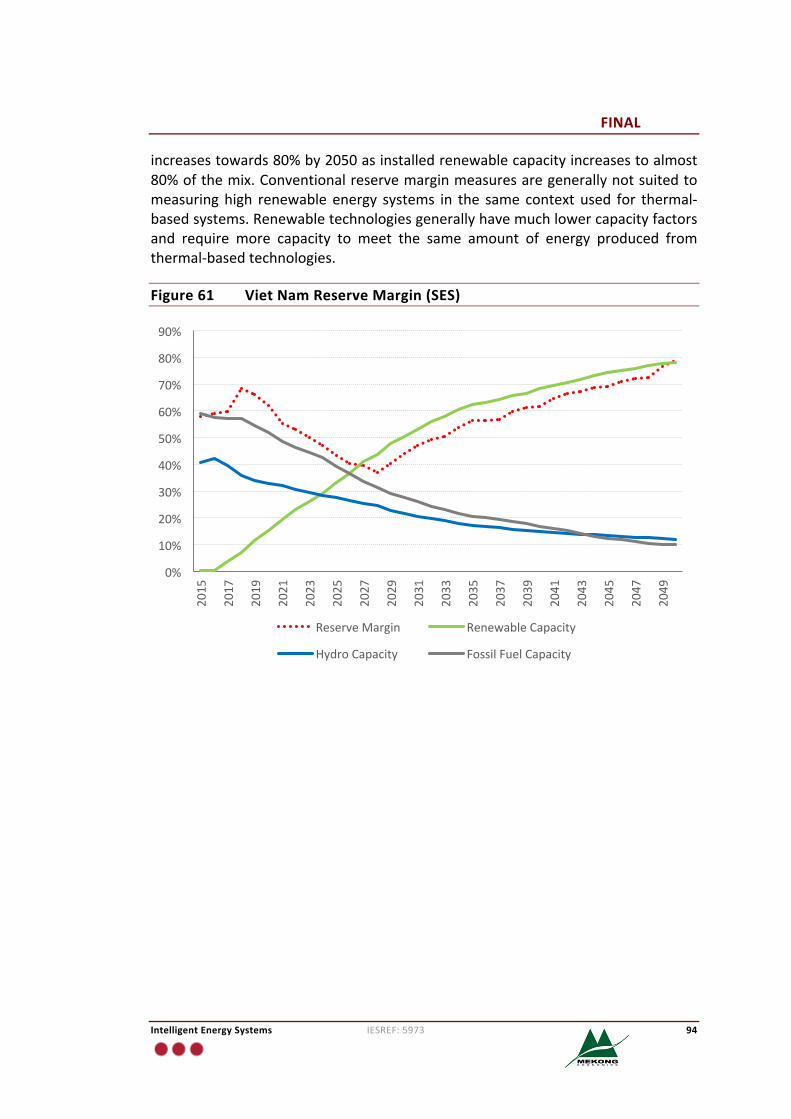

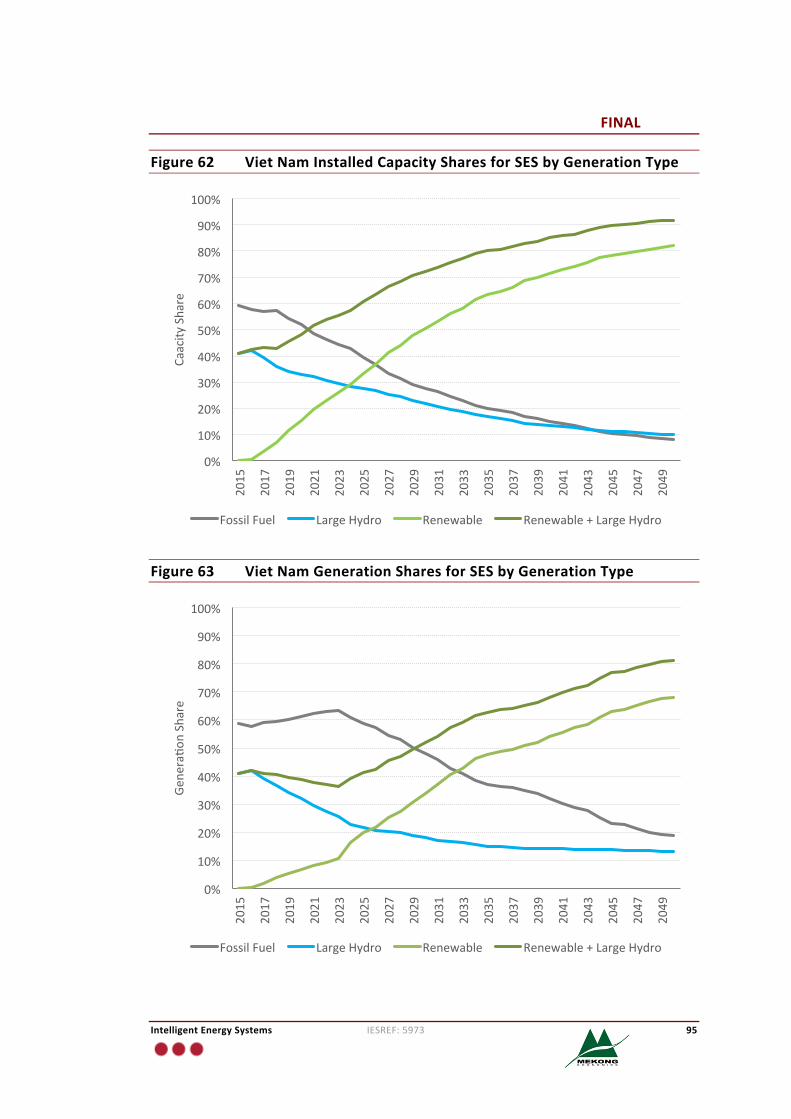

6 SustainableEnergySectorScenario 836.1 SustainableEnergySectorScenario 836.2 ProjectedDemandGrowth 836.3 InstalledCapacityDevelopment 856.4 ProjectedGenerationMix 886.5 GridtoGridPowerFlows 916.6 GenerationFleetStructure 916.7 ReserveMarginandGenerationTrends 936.8 ElectrificationandOff-Grid 96

FINAL

IntelligentEnergySystems IESREF:5973 viii

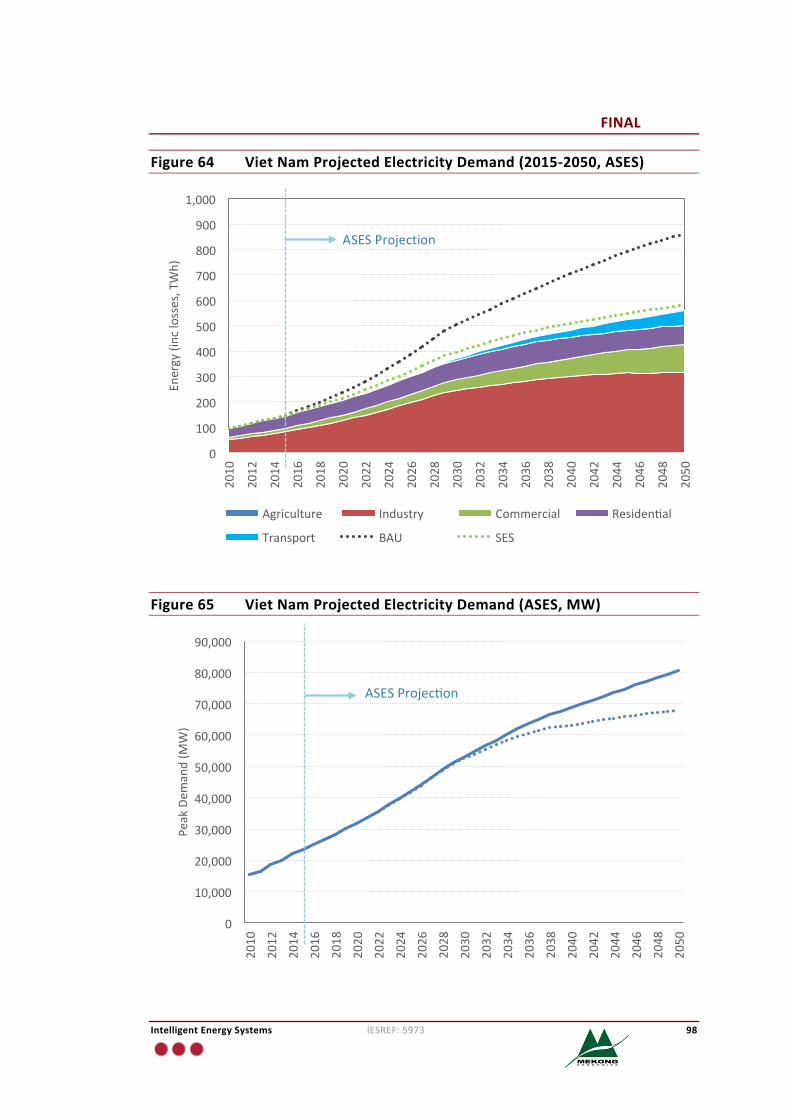

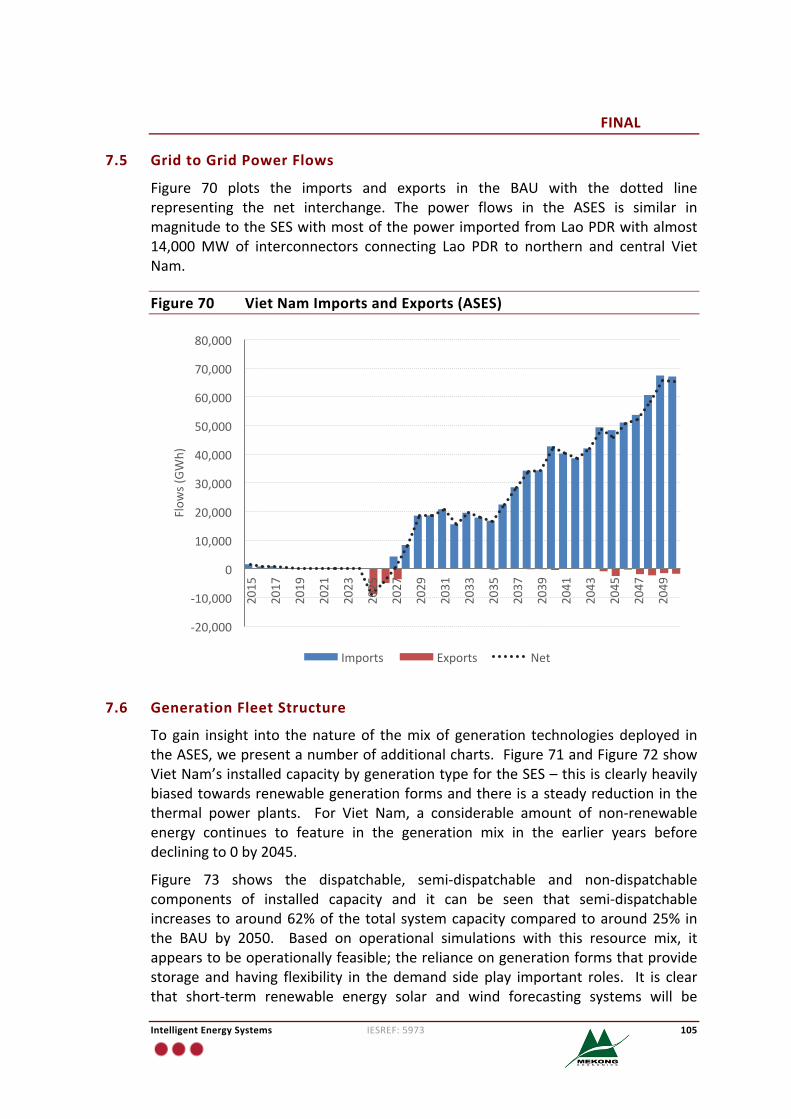

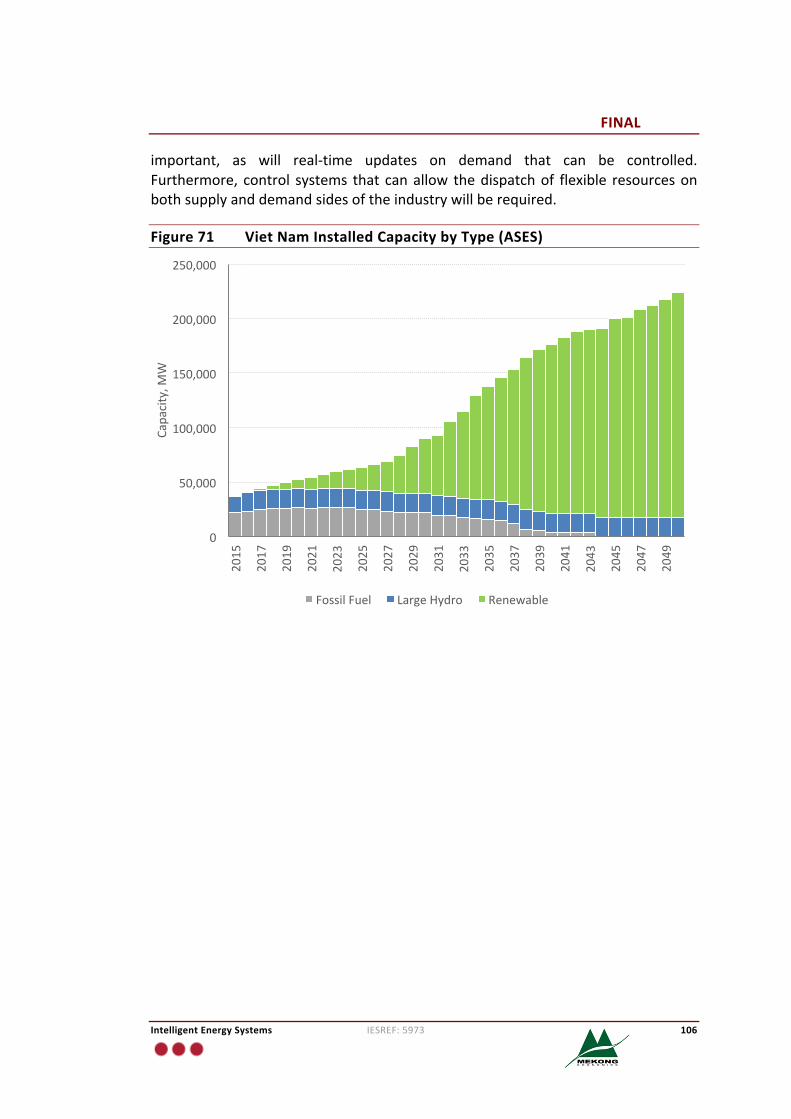

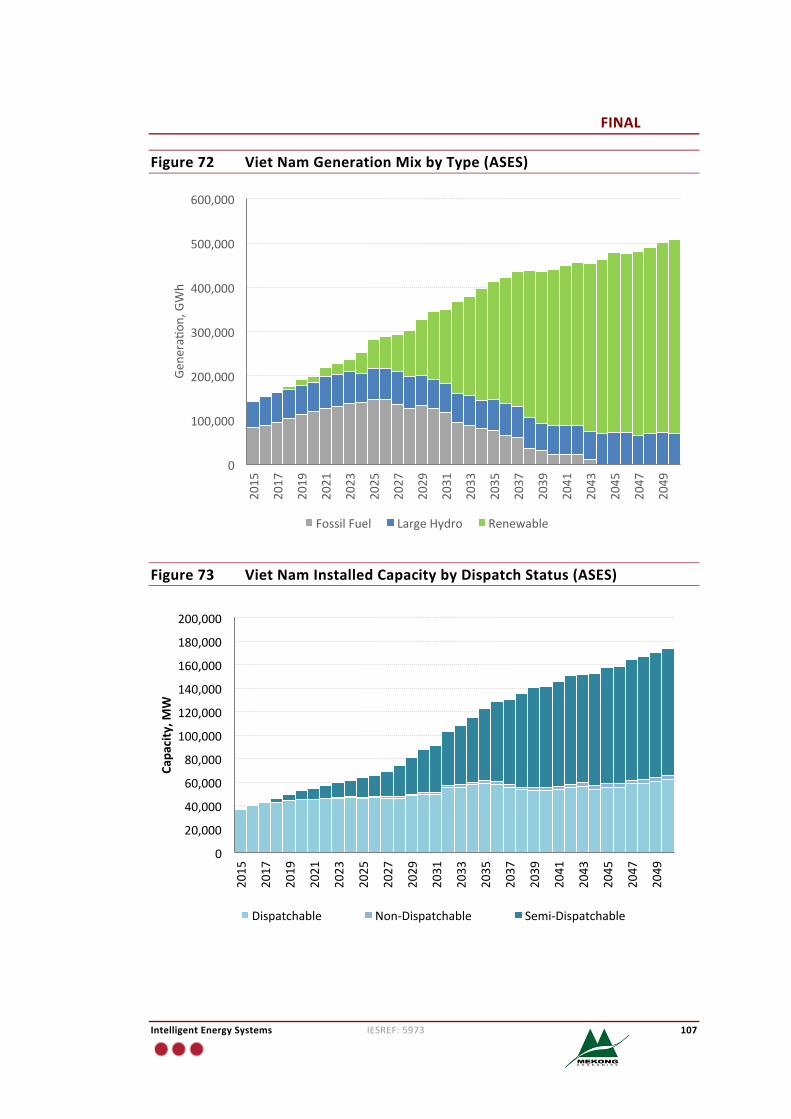

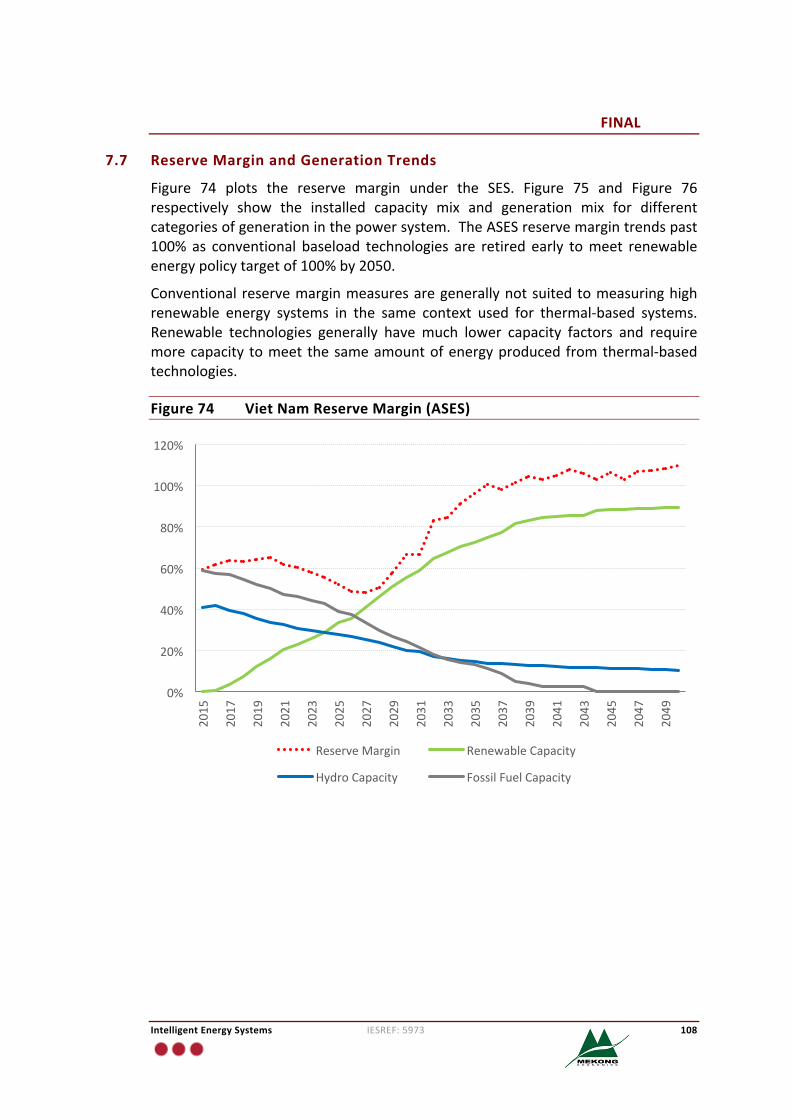

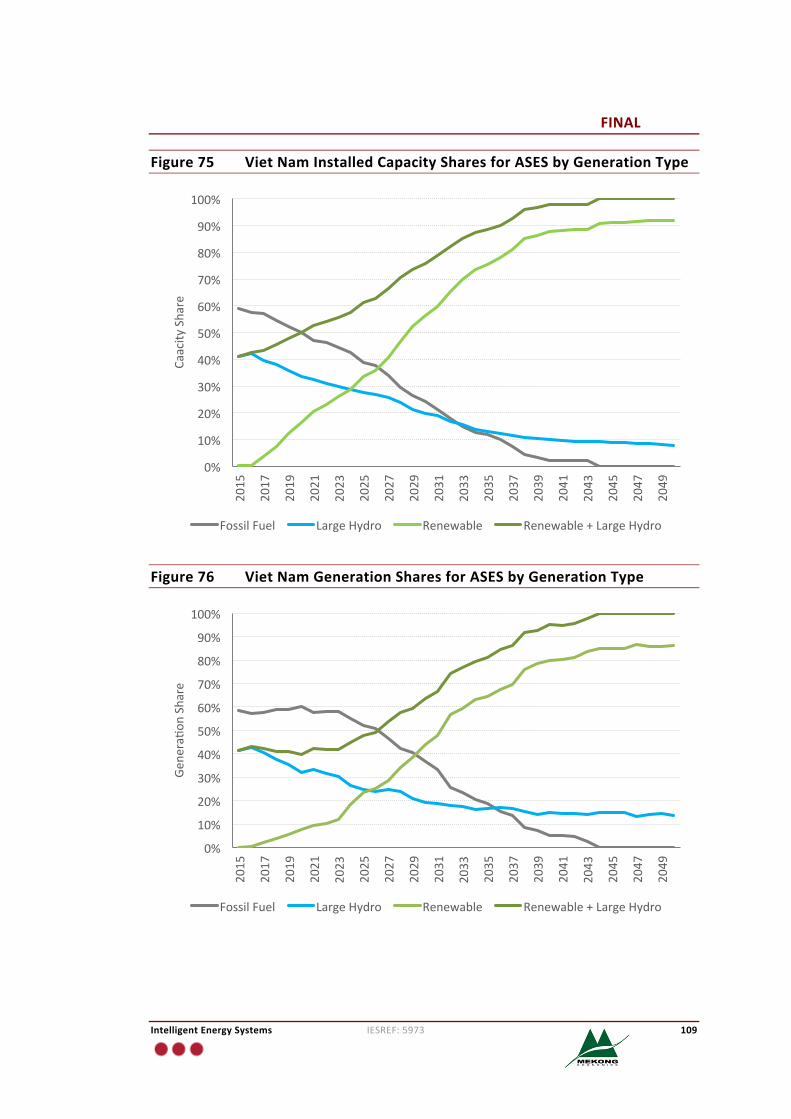

7 AdvancedSustainableEnergySectorScenario 977.1 AdvancedSustainableEnergySectorScenario 977.2 ProjectedDemandGrowth 977.3 InstalledCapacityDevelopment 997.4 ProjectedGenerationMix 1027.5 GridtoGridPowerFlows 1057.6 GenerationFleetStructure 1057.7 ReserveMarginandGenerationTrends 1087.8 ElectrificationandOff-Grid 110

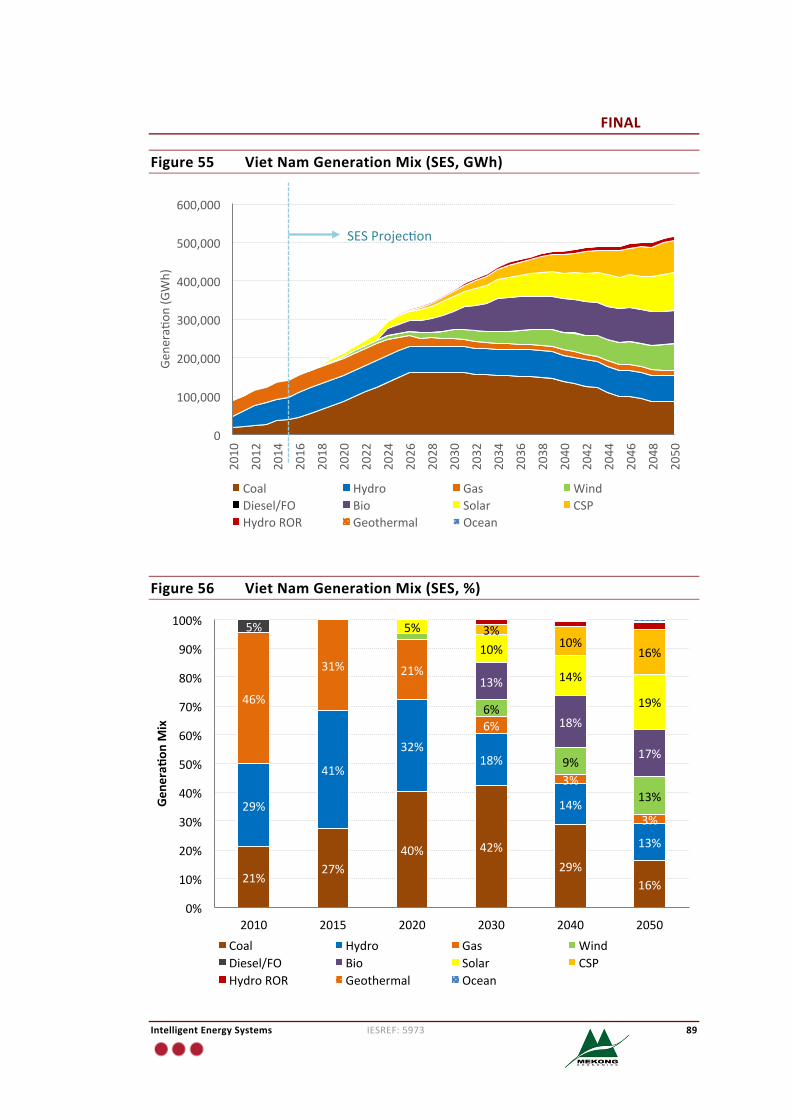

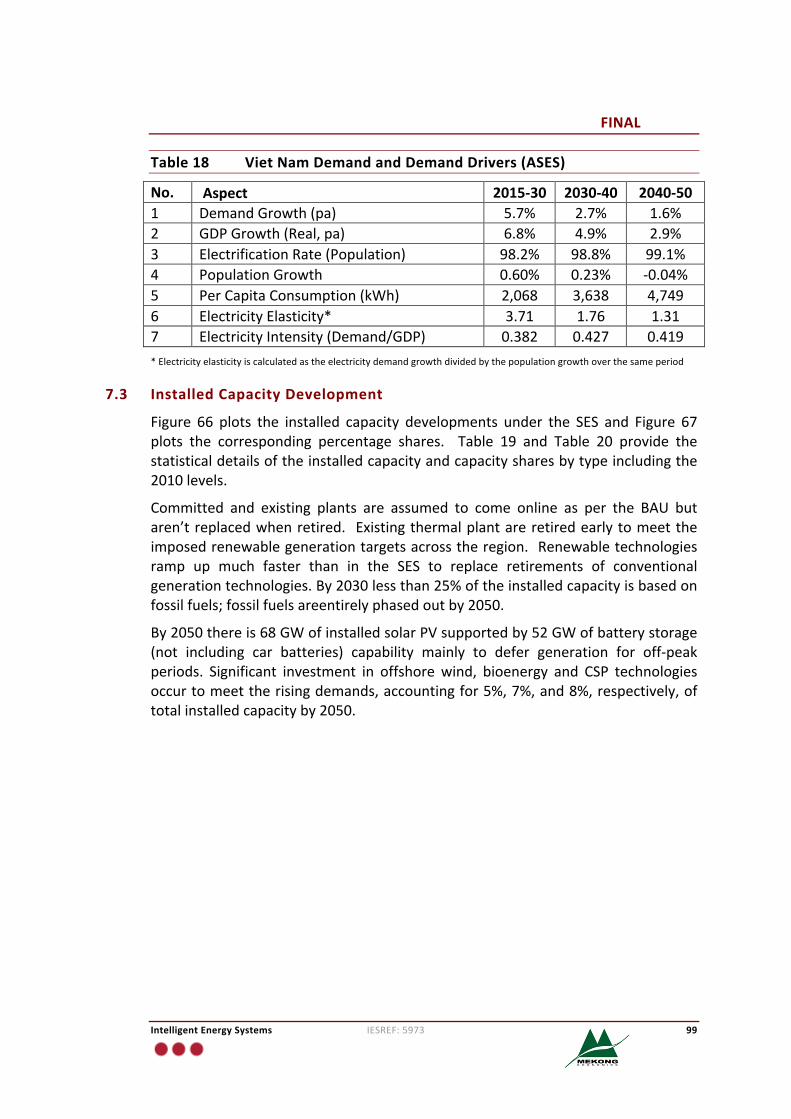

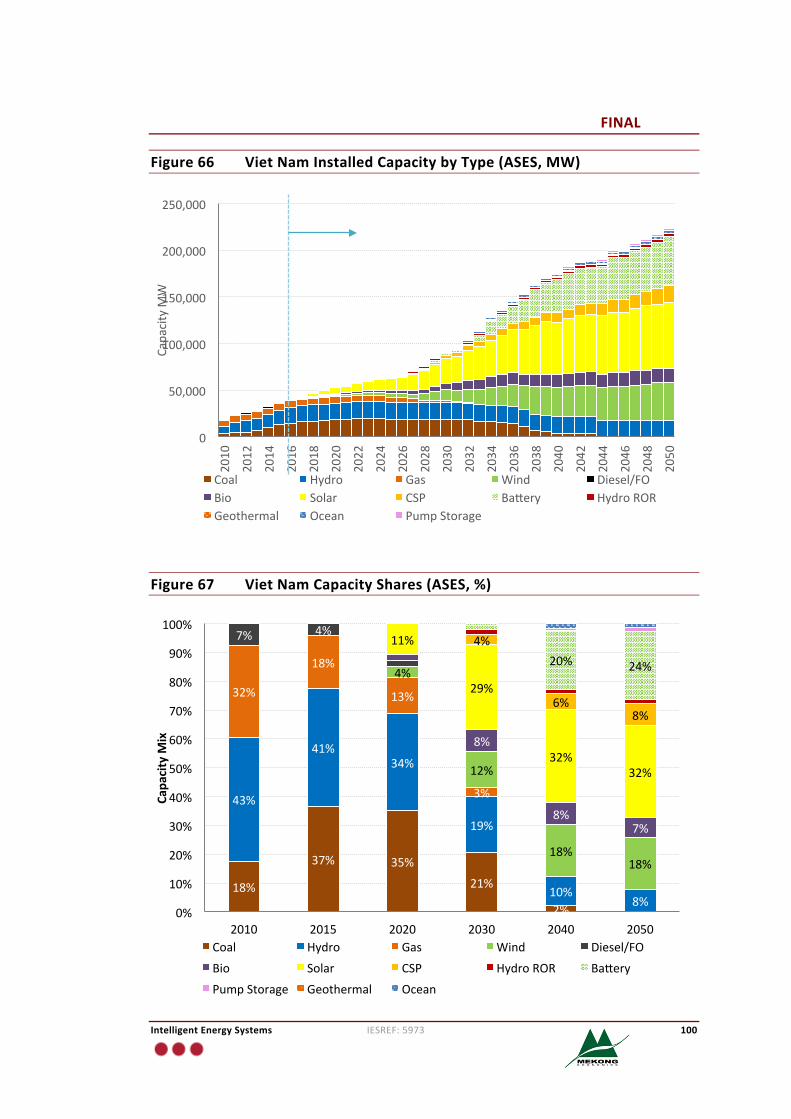

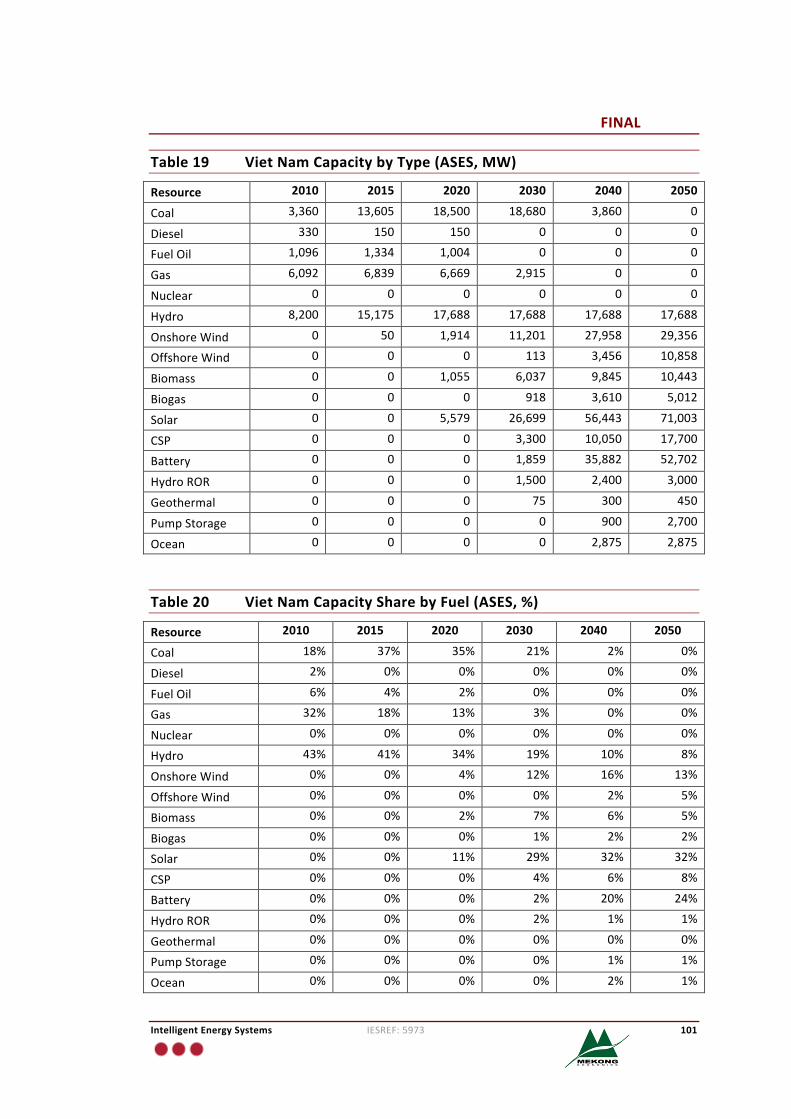

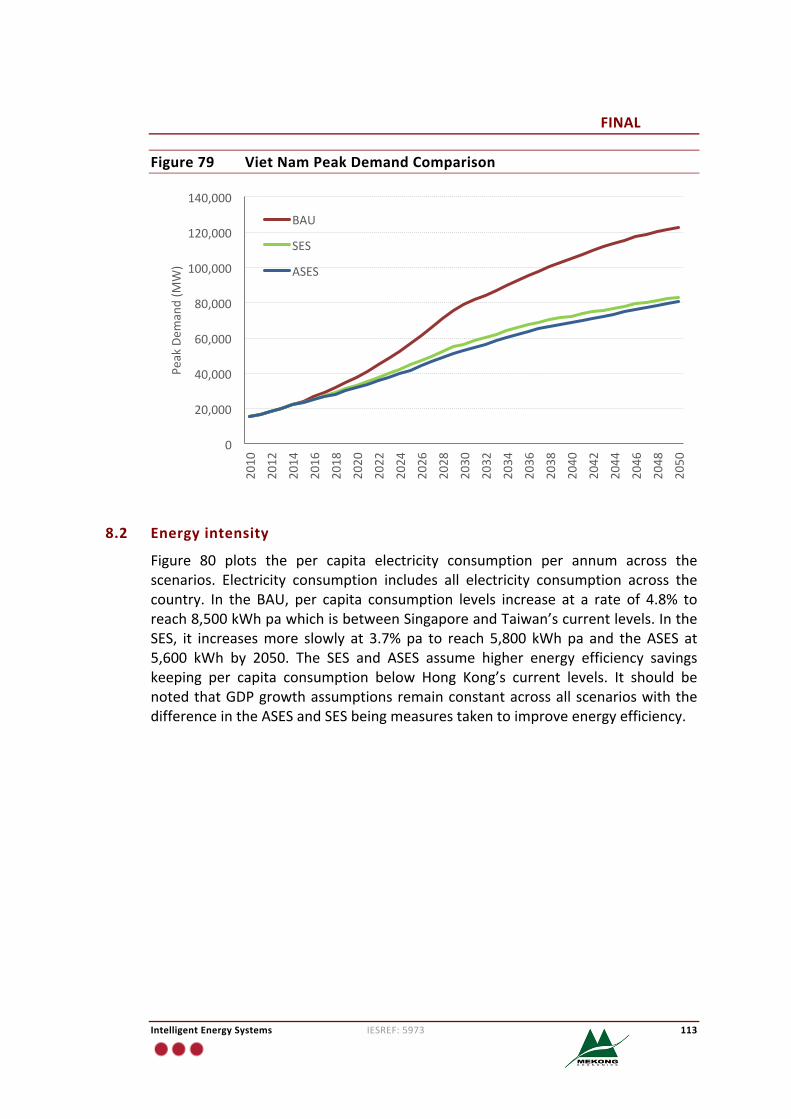

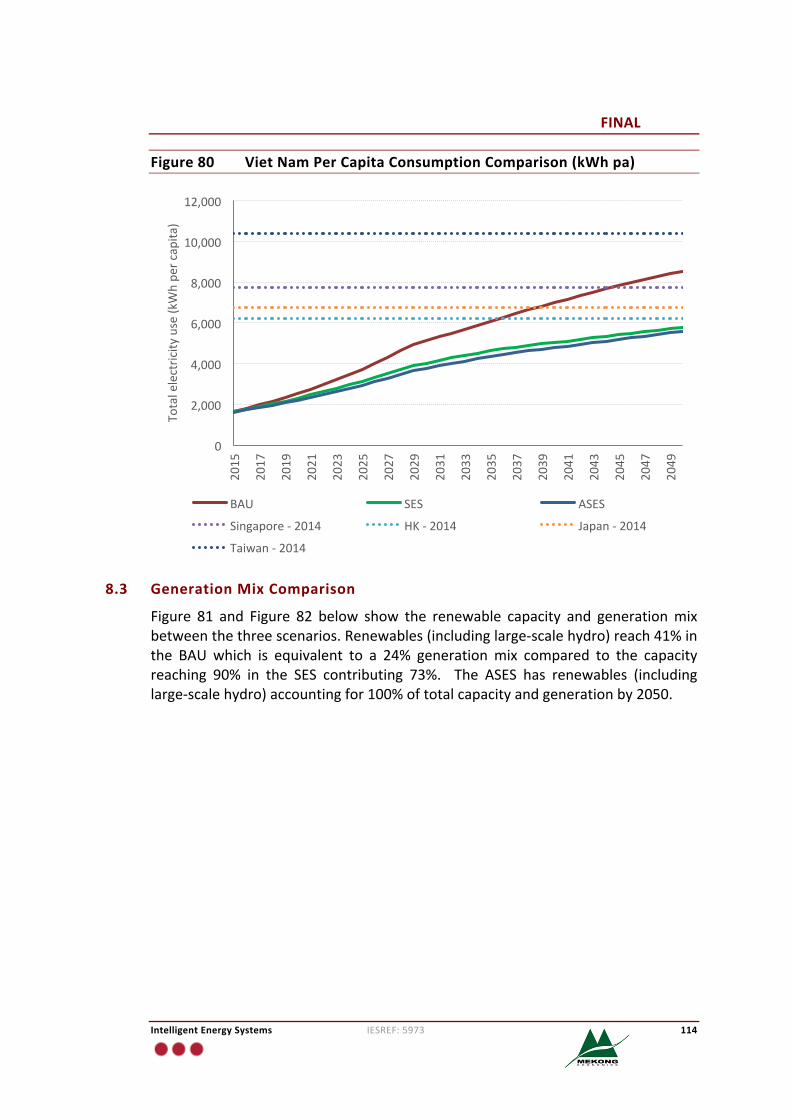

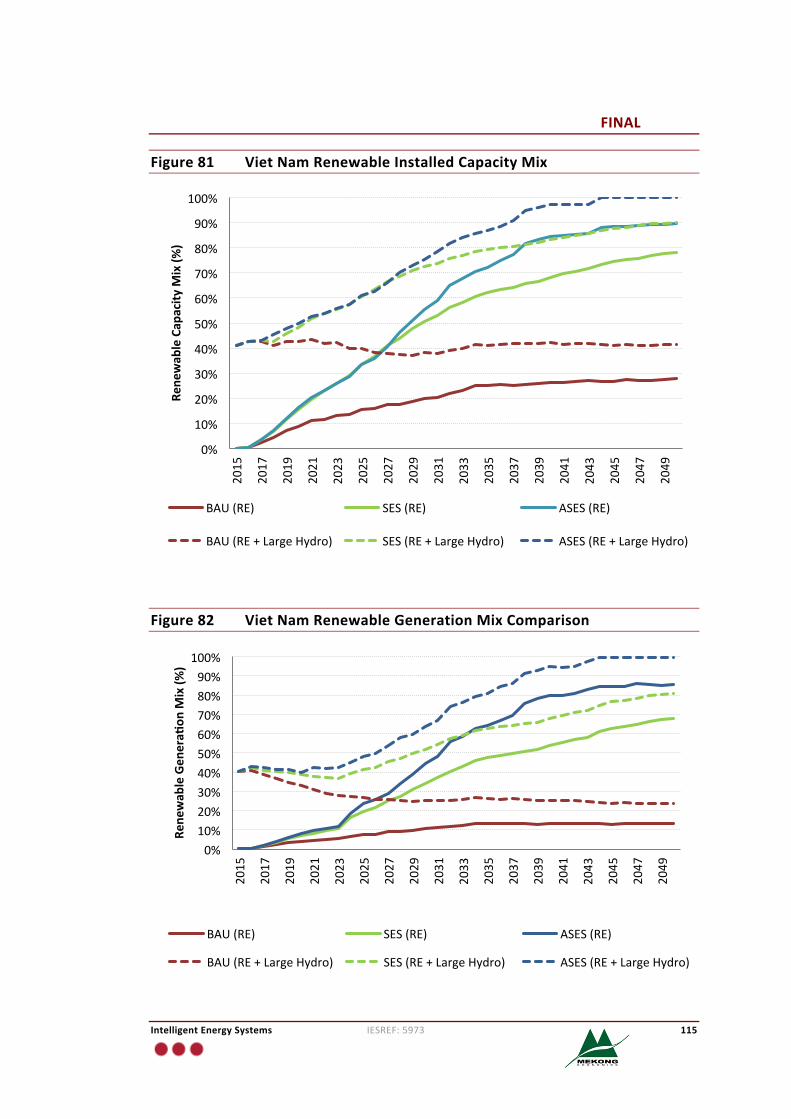

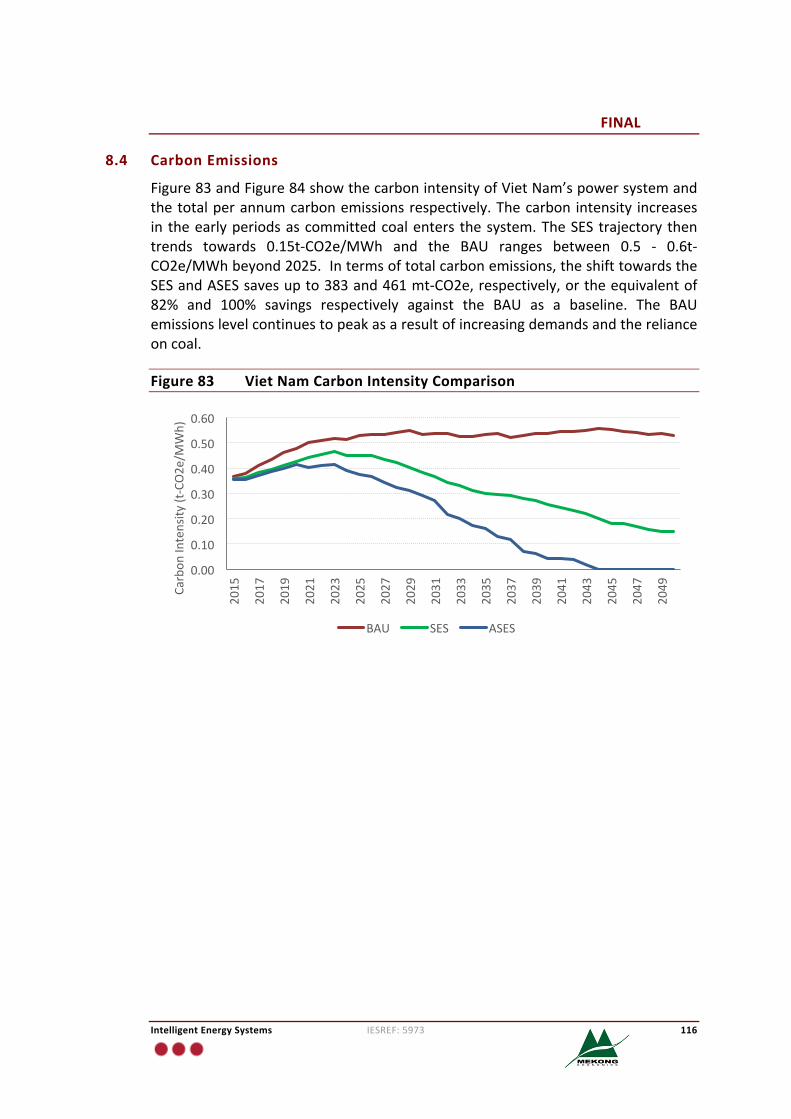

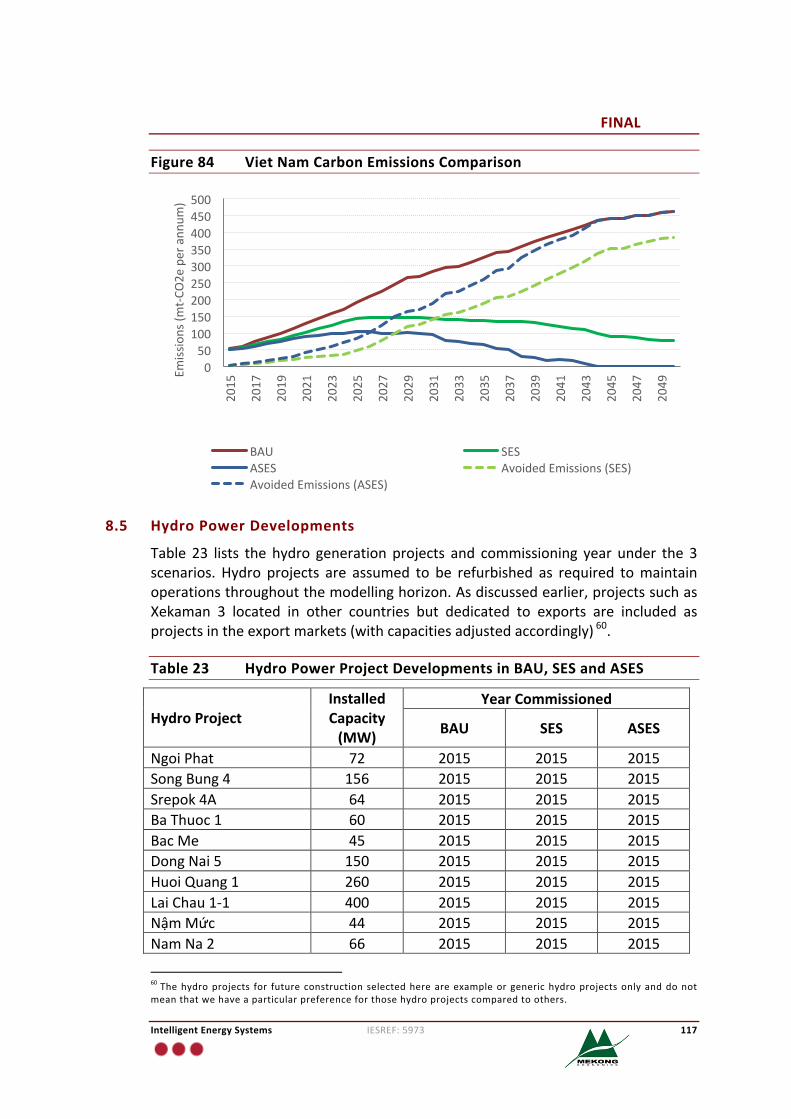

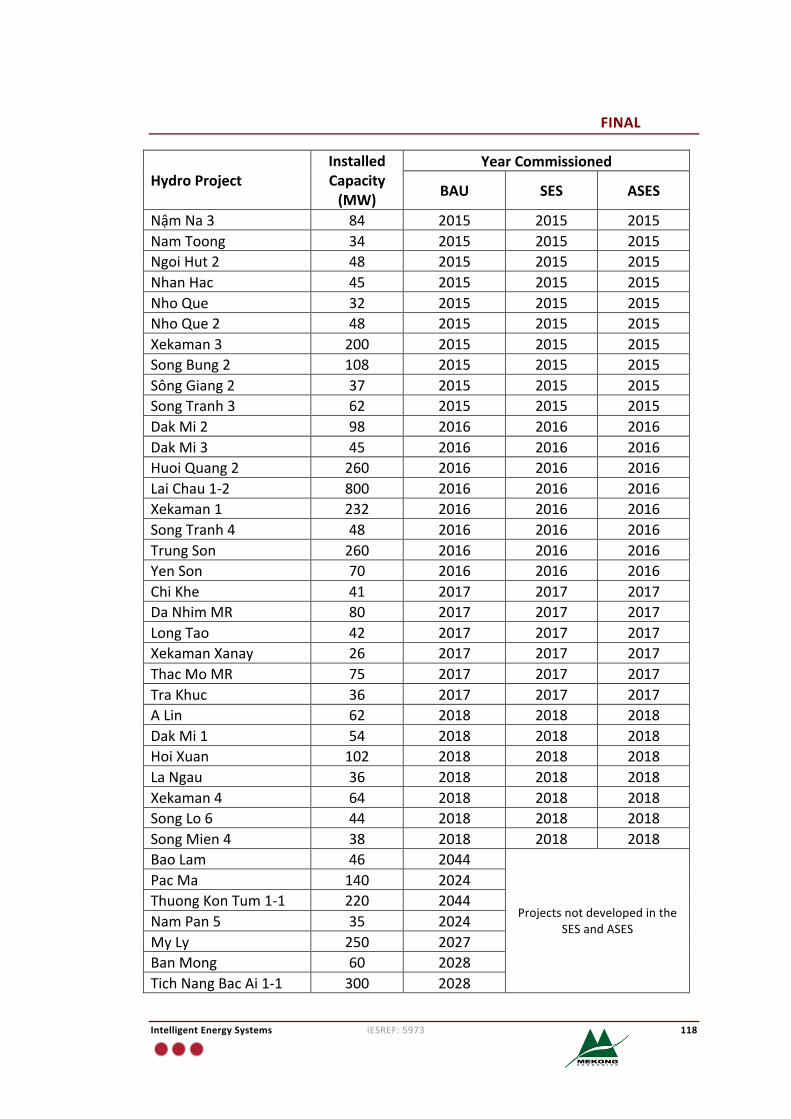

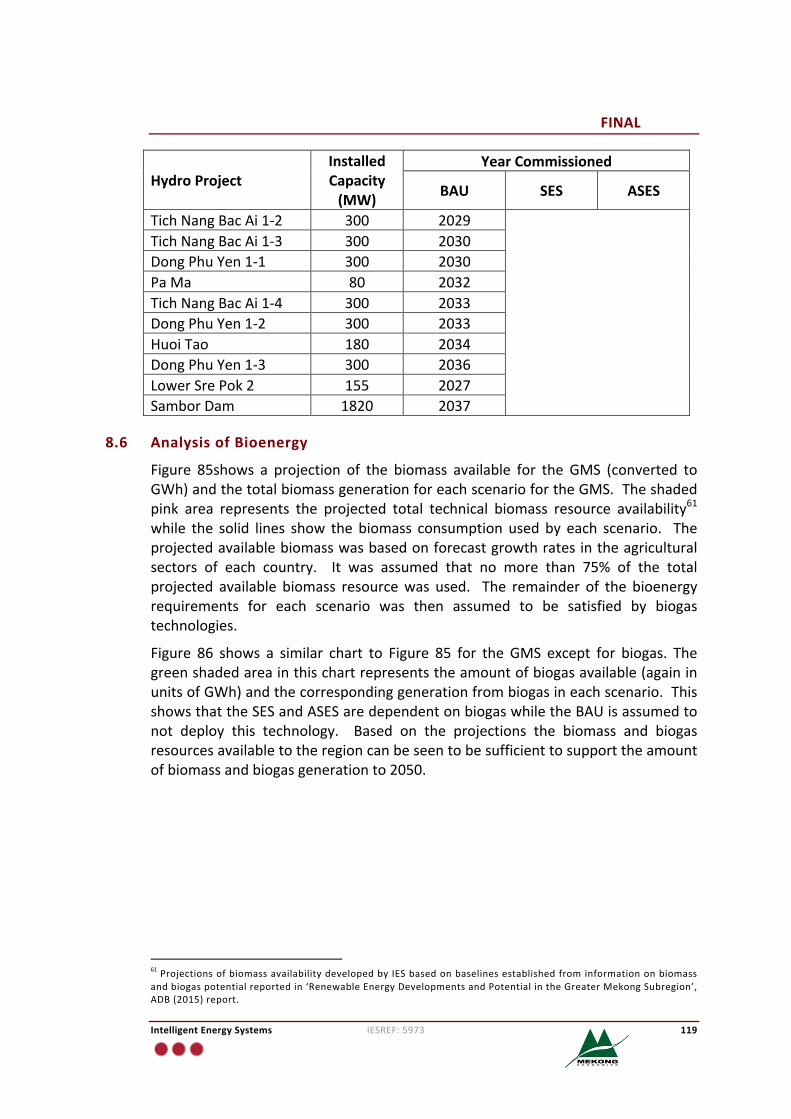

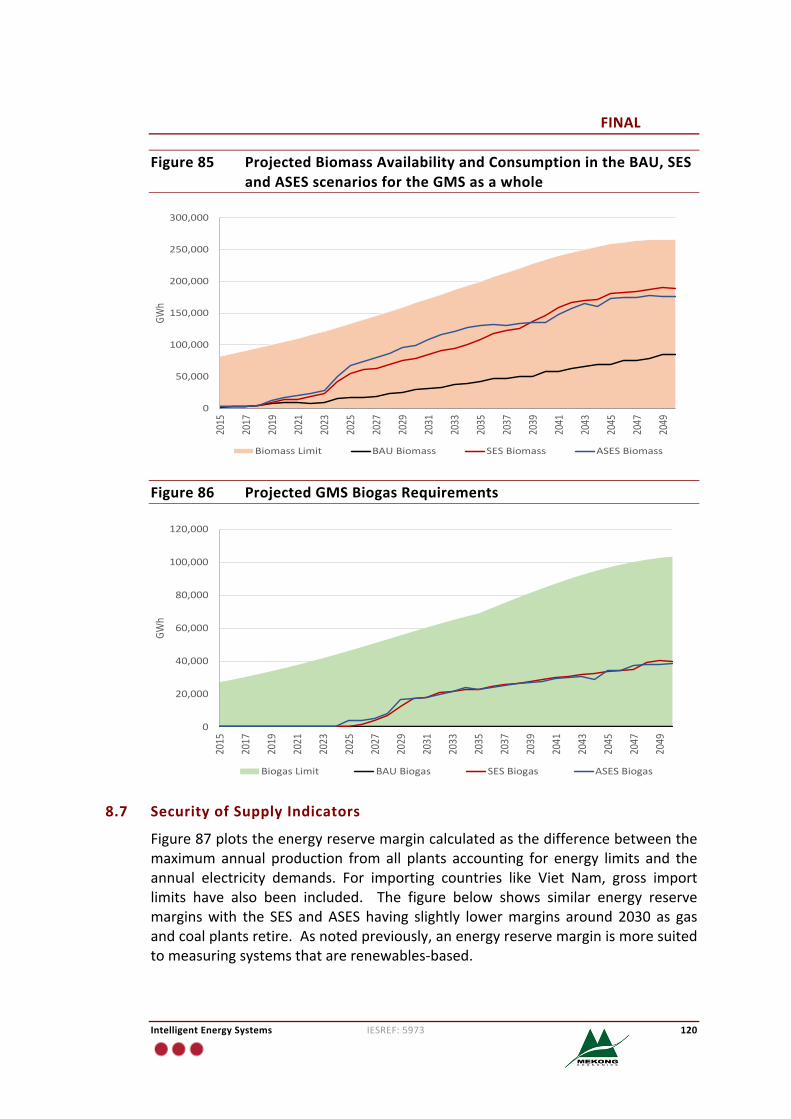

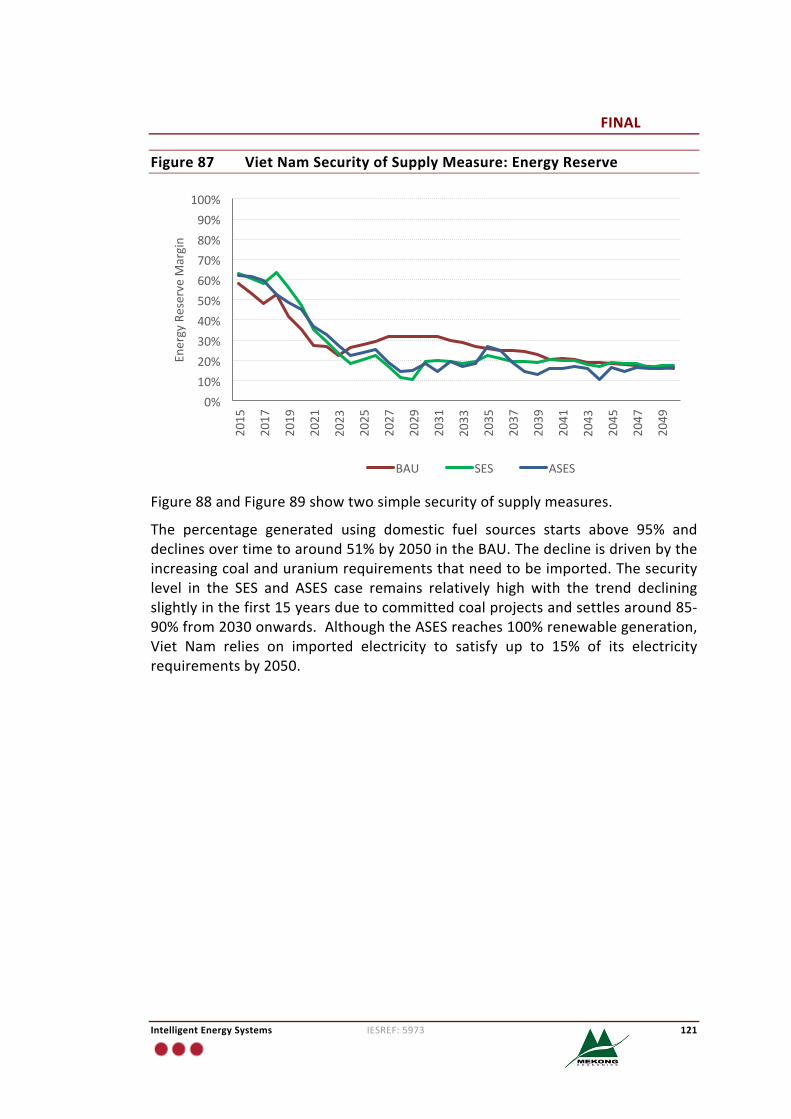

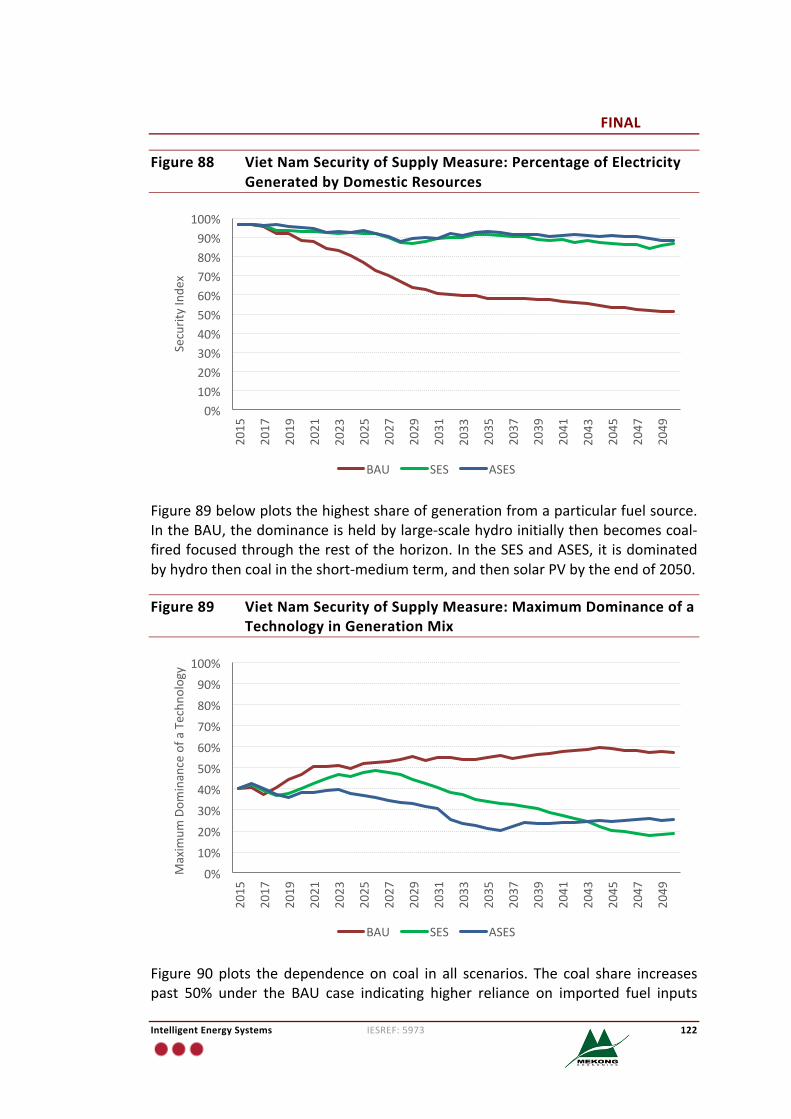

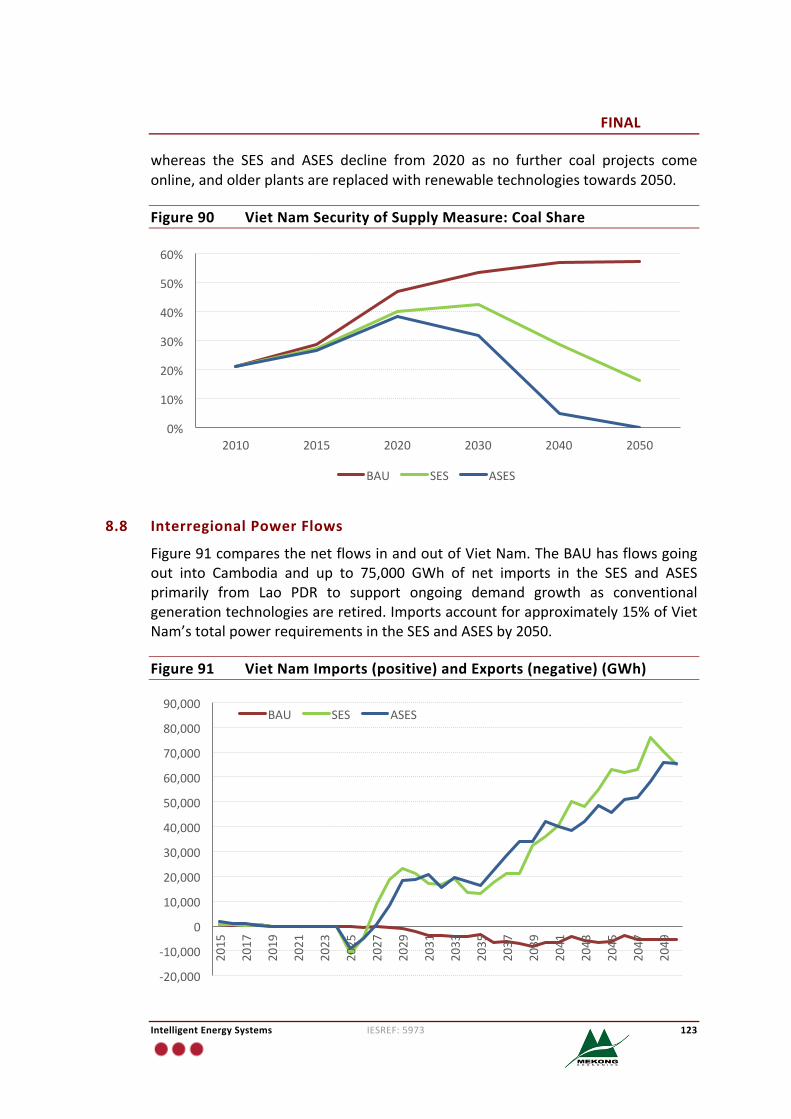

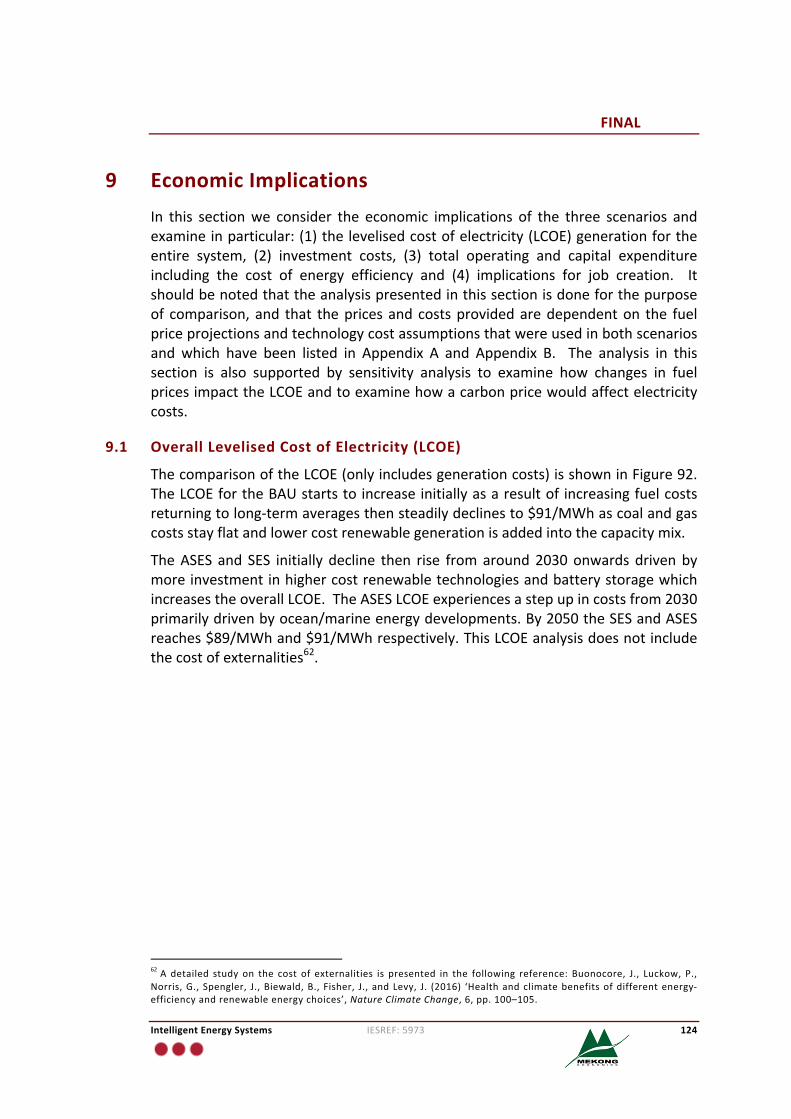

8 AnalysisofScenarios 1118.1 EnergyandPeakDemand 1118.2 Energyintensity 1138.3 GenerationMixComparison 1148.4 CarbonEmissions 1168.5 HydroPowerDevelopments 1178.6 AnalysisofBioenergy 1198.7 SecurityofSupplyIndicators 1208.8 InterregionalPowerFlows 123

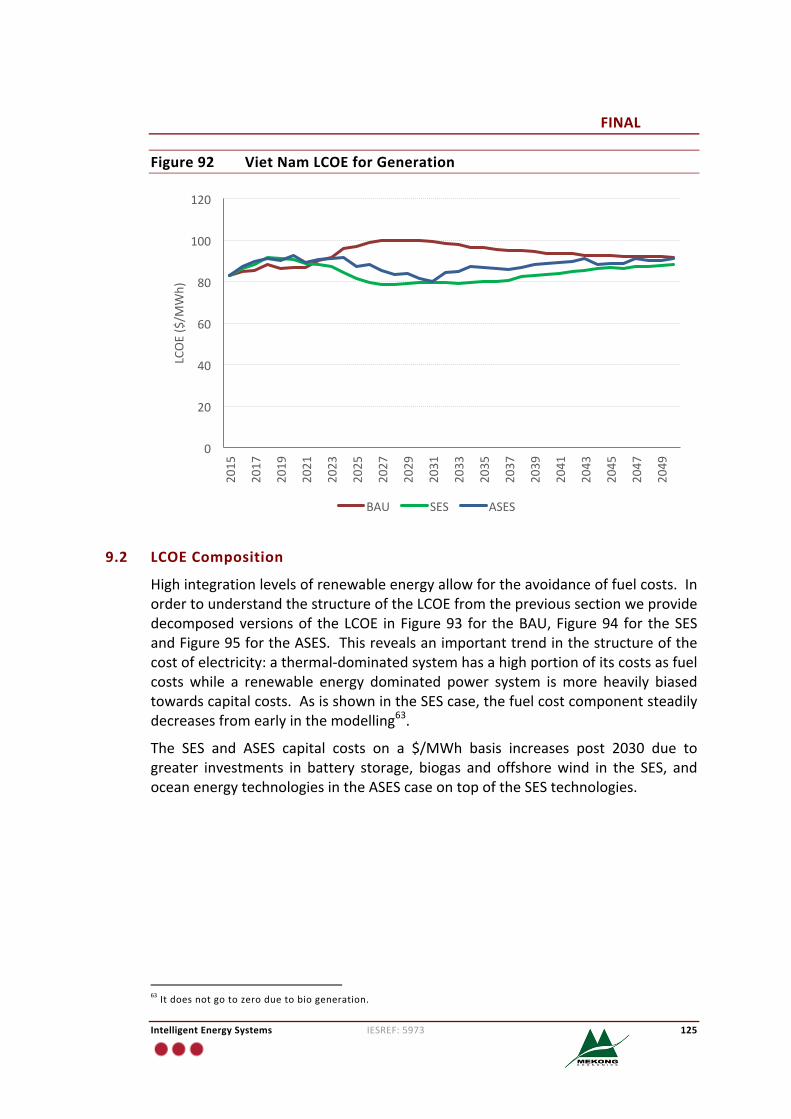

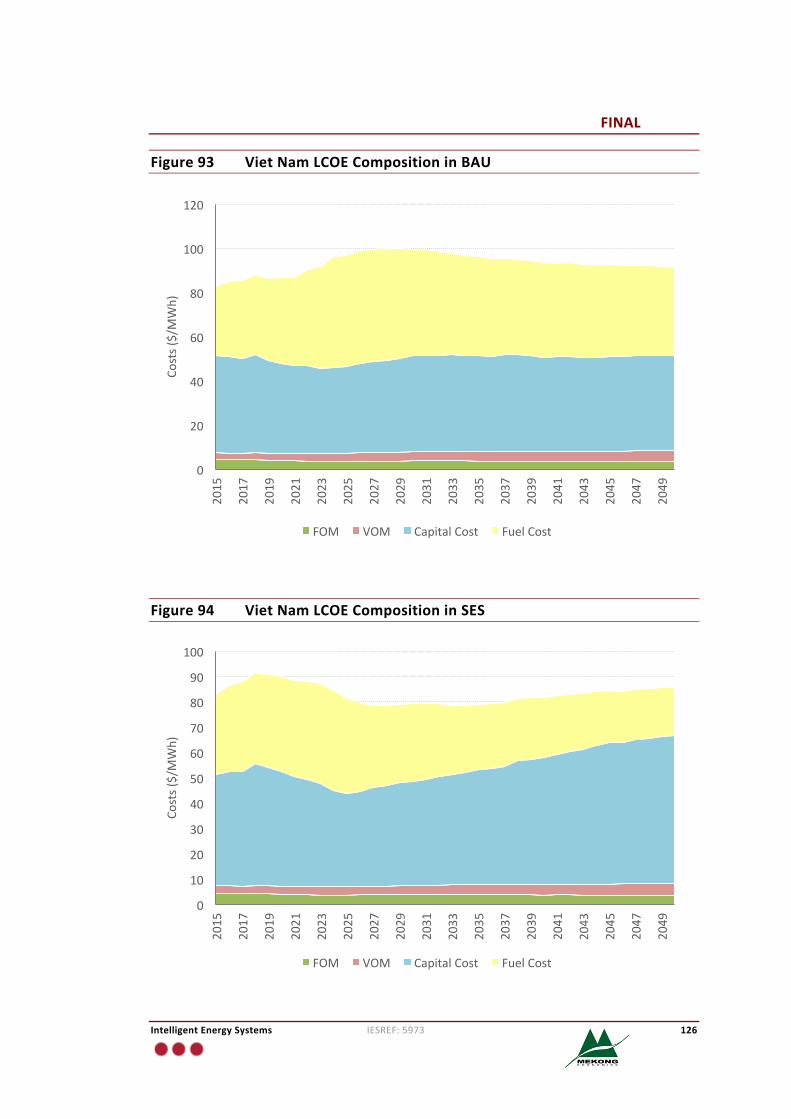

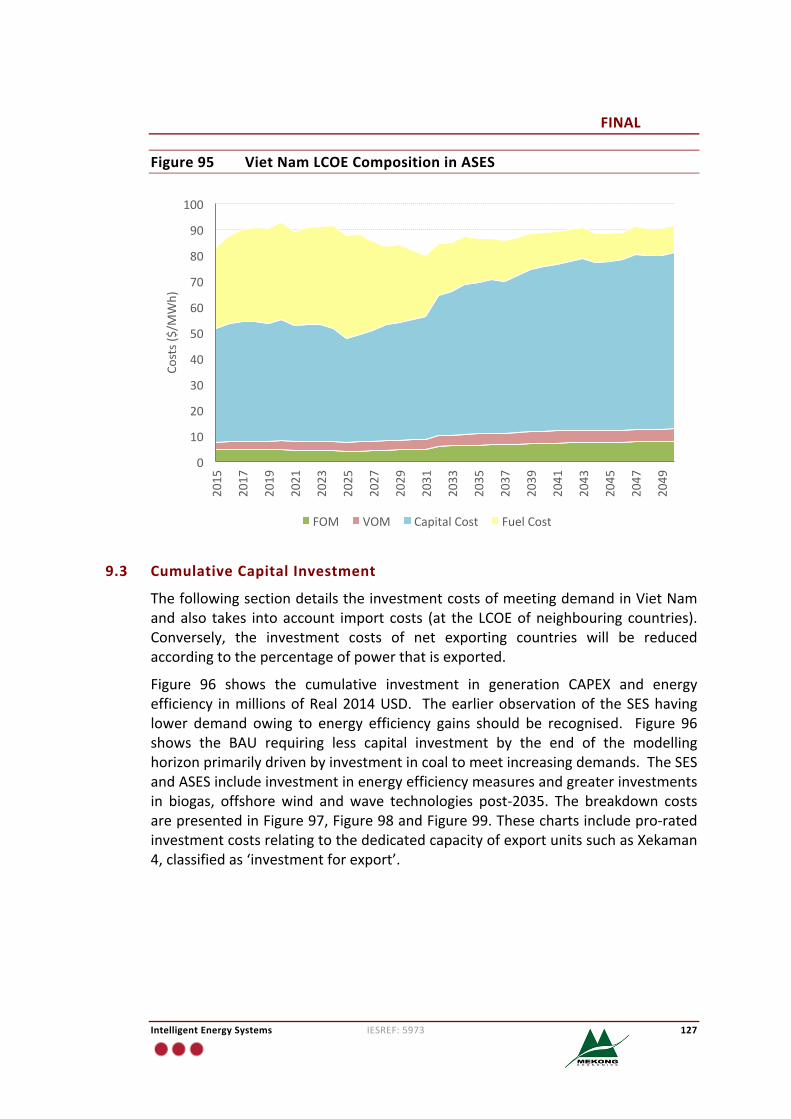

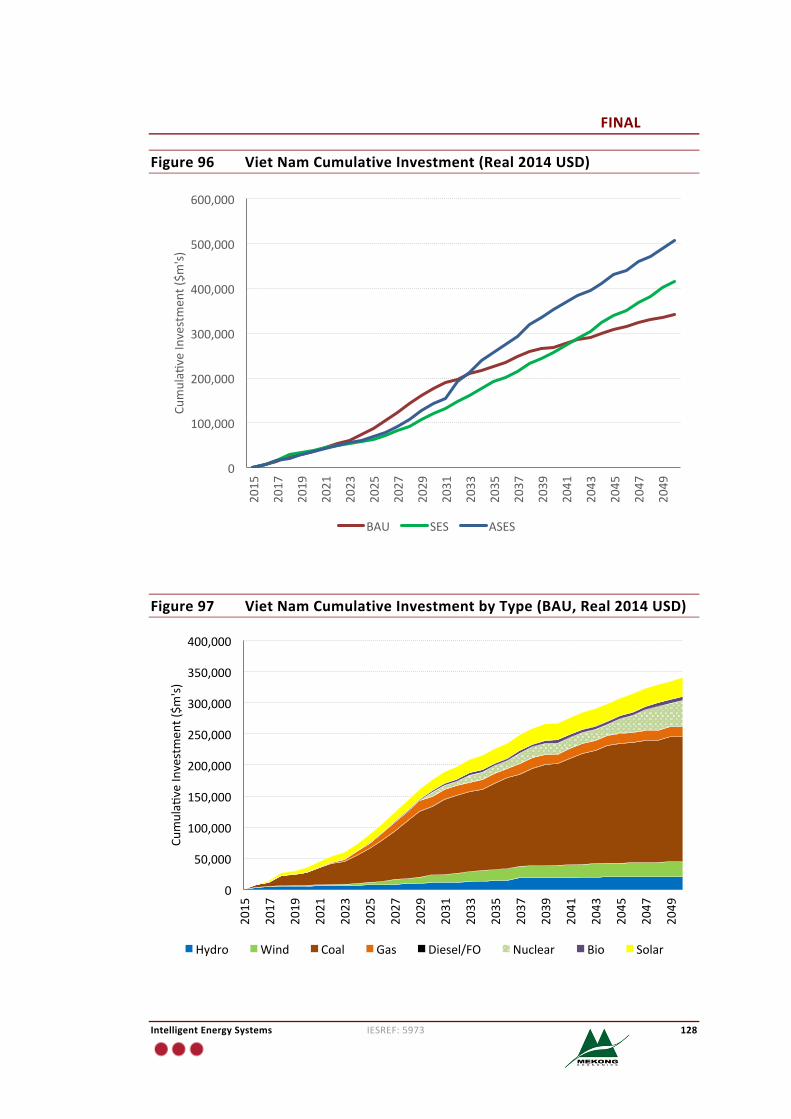

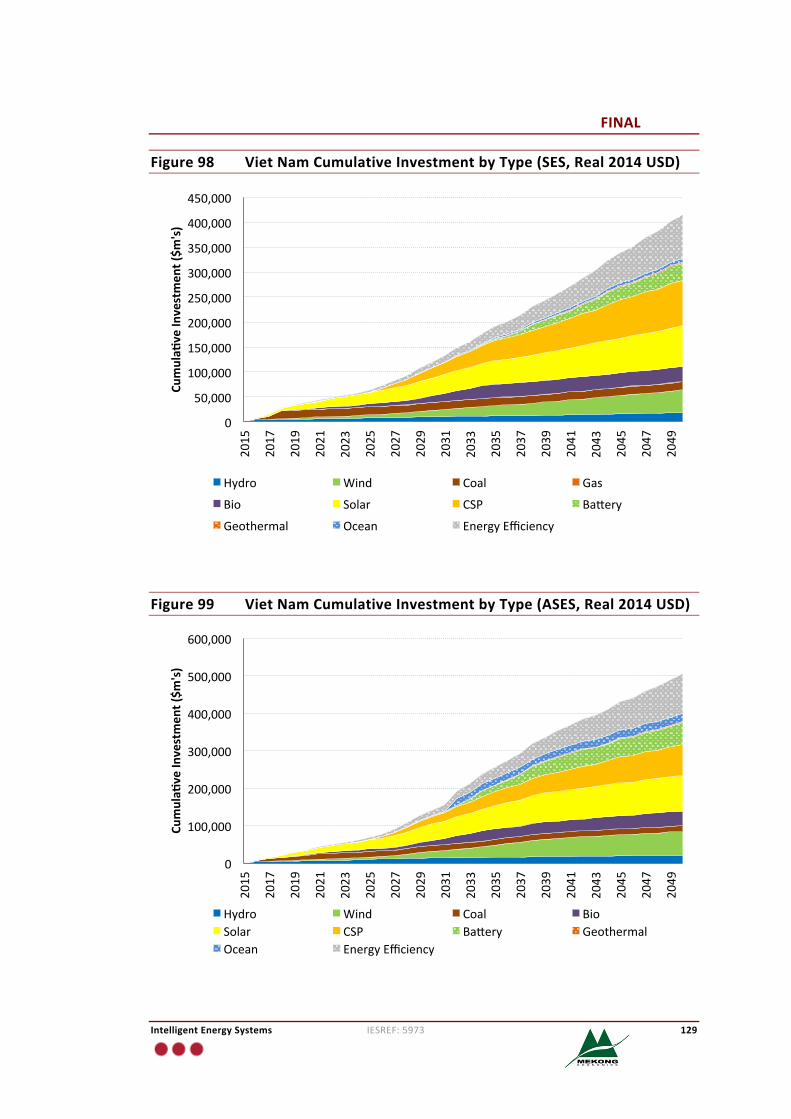

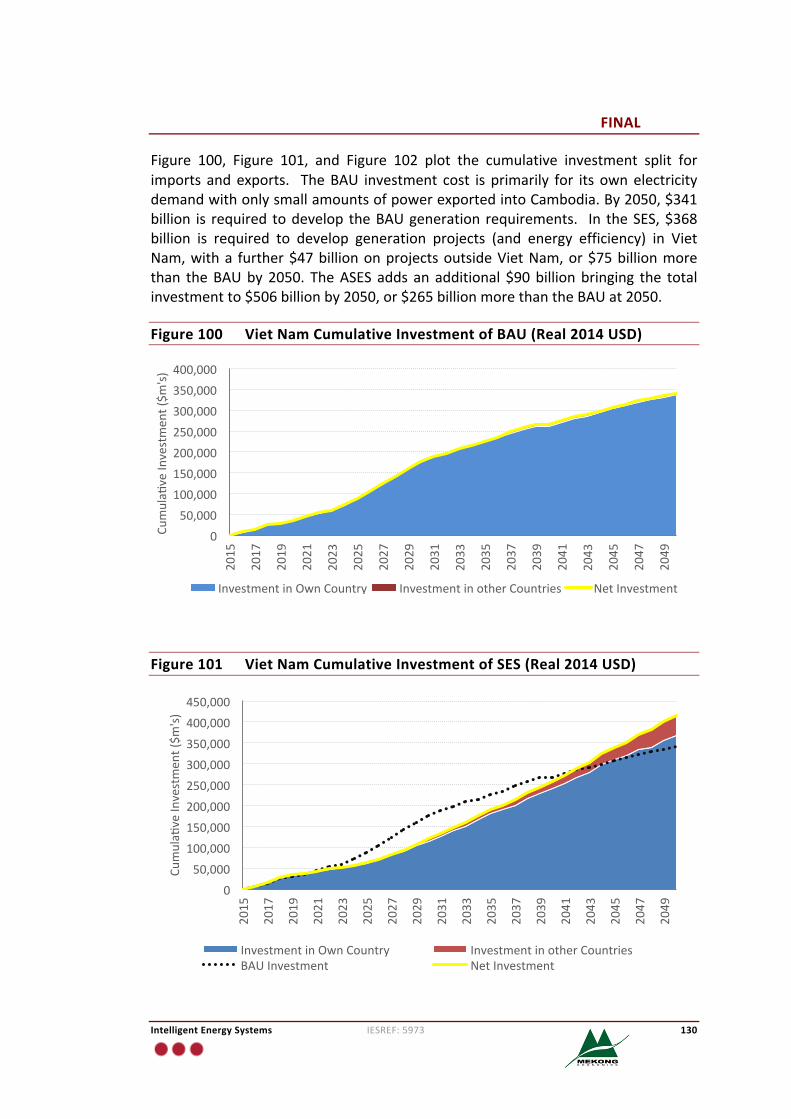

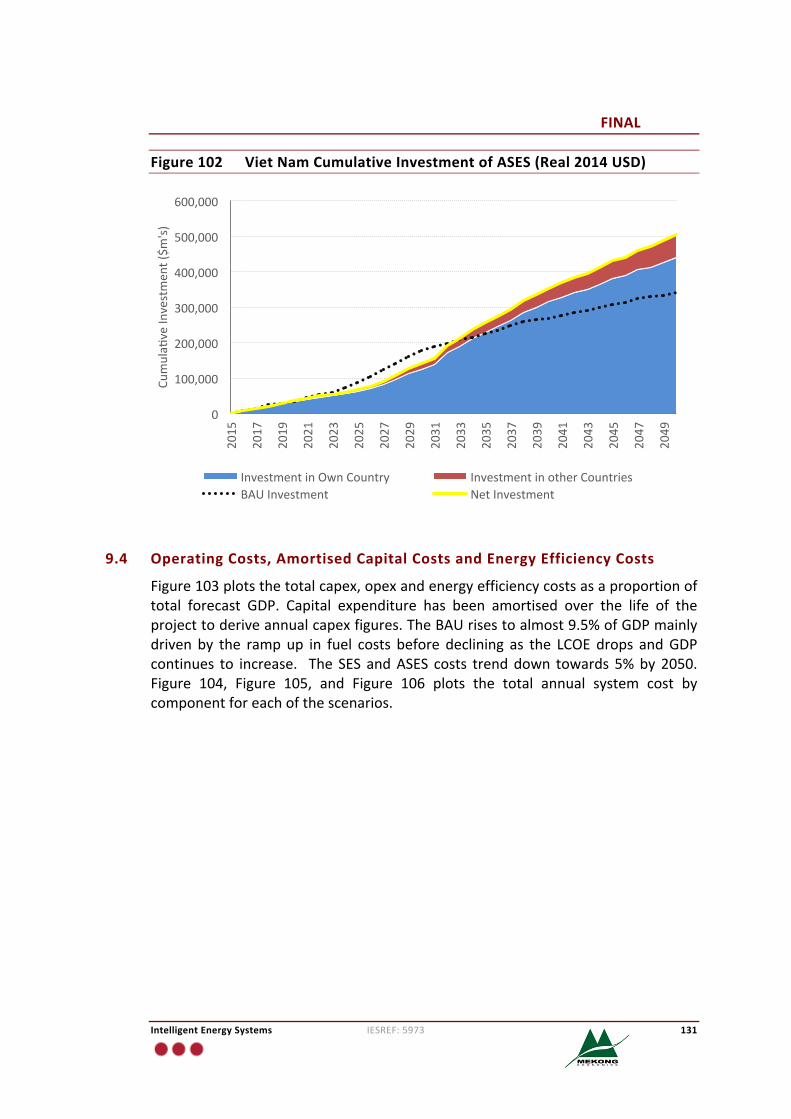

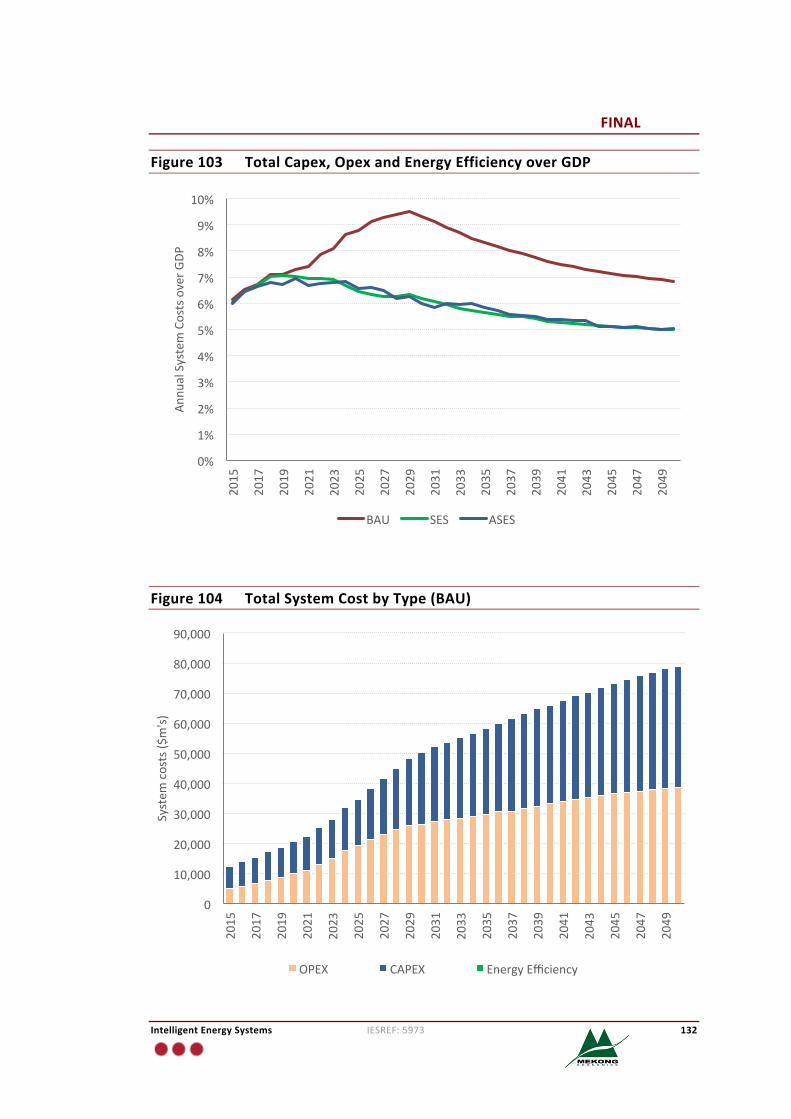

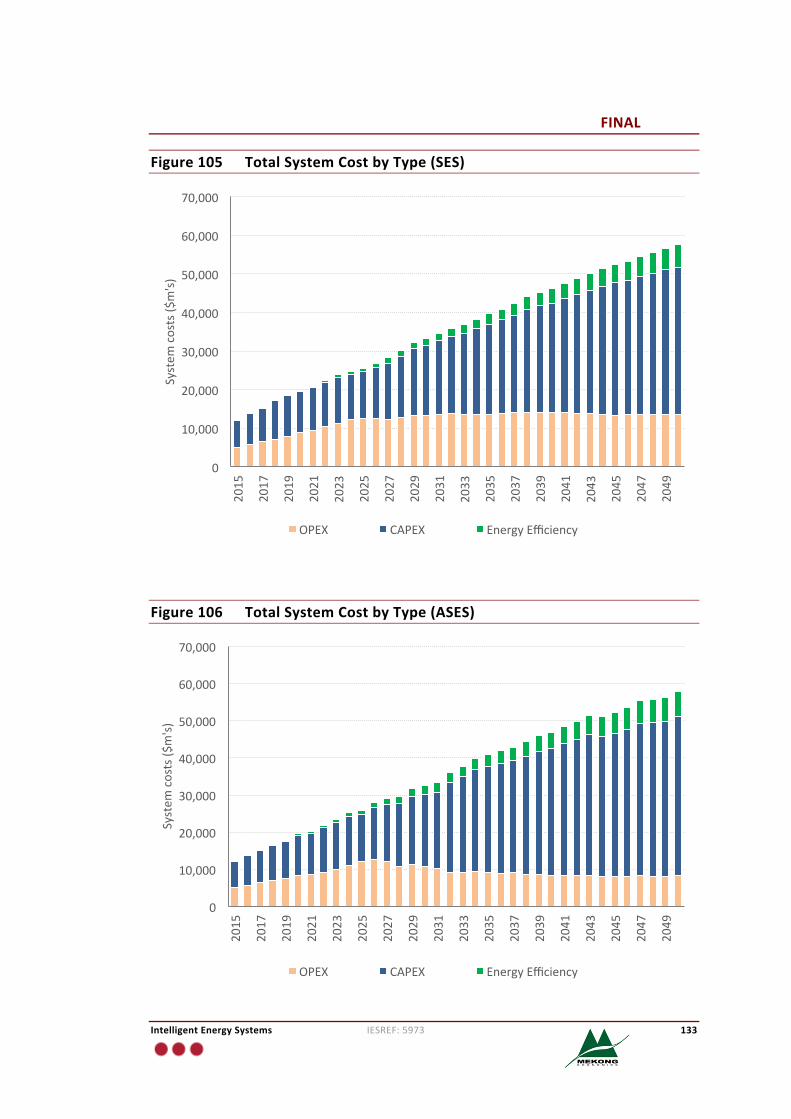

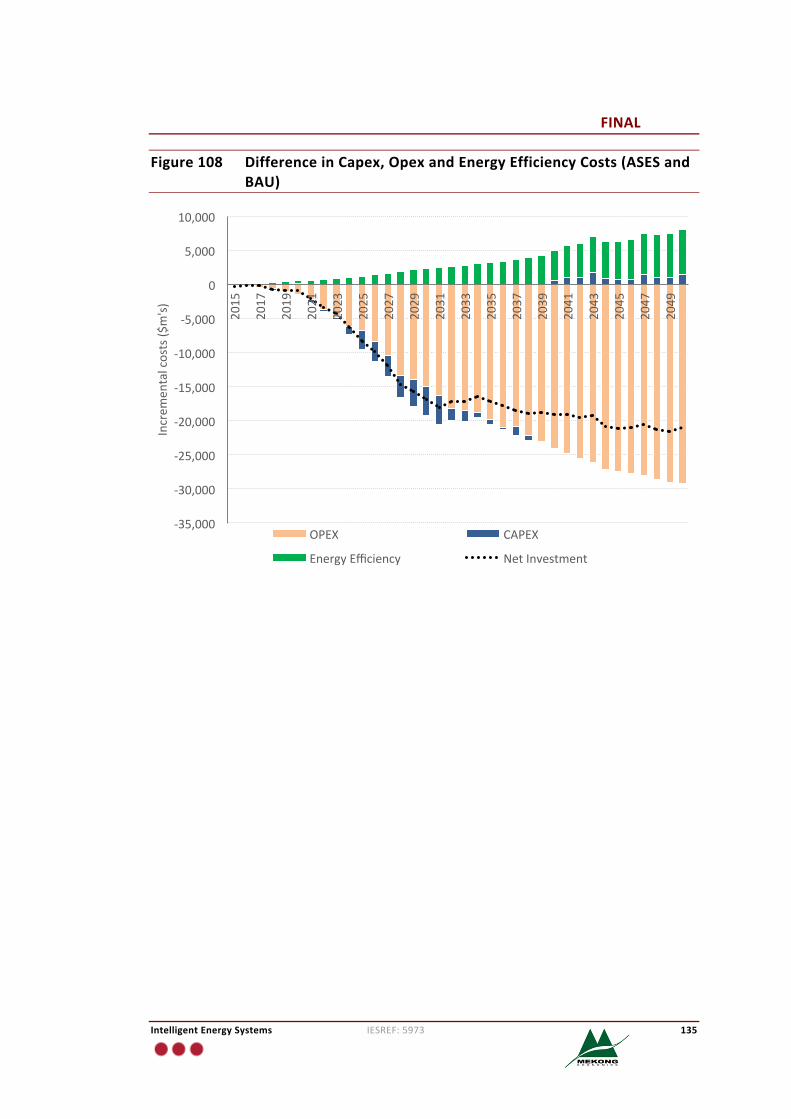

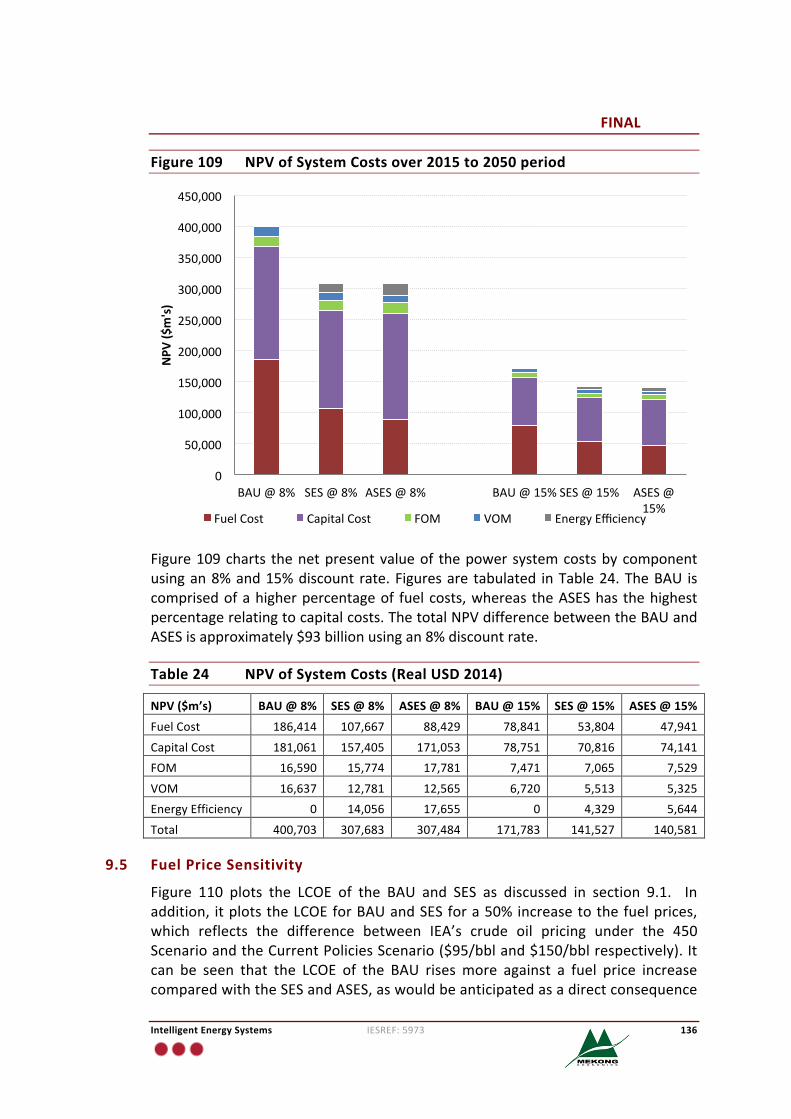

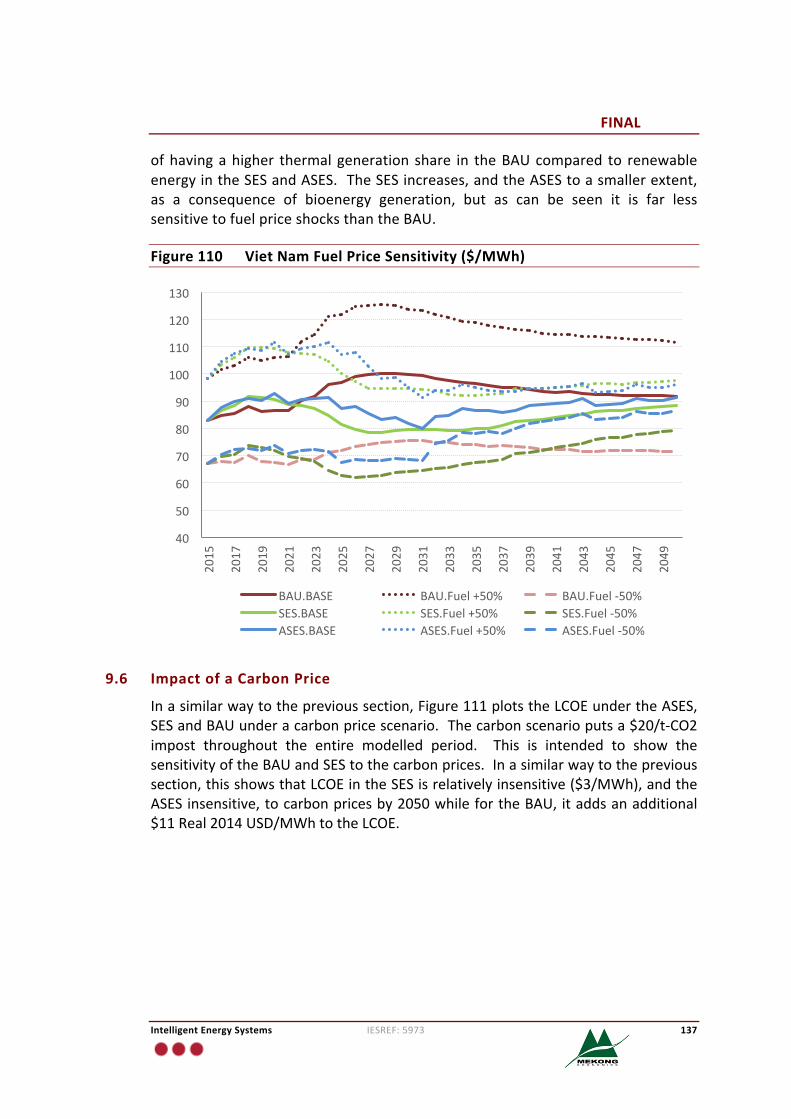

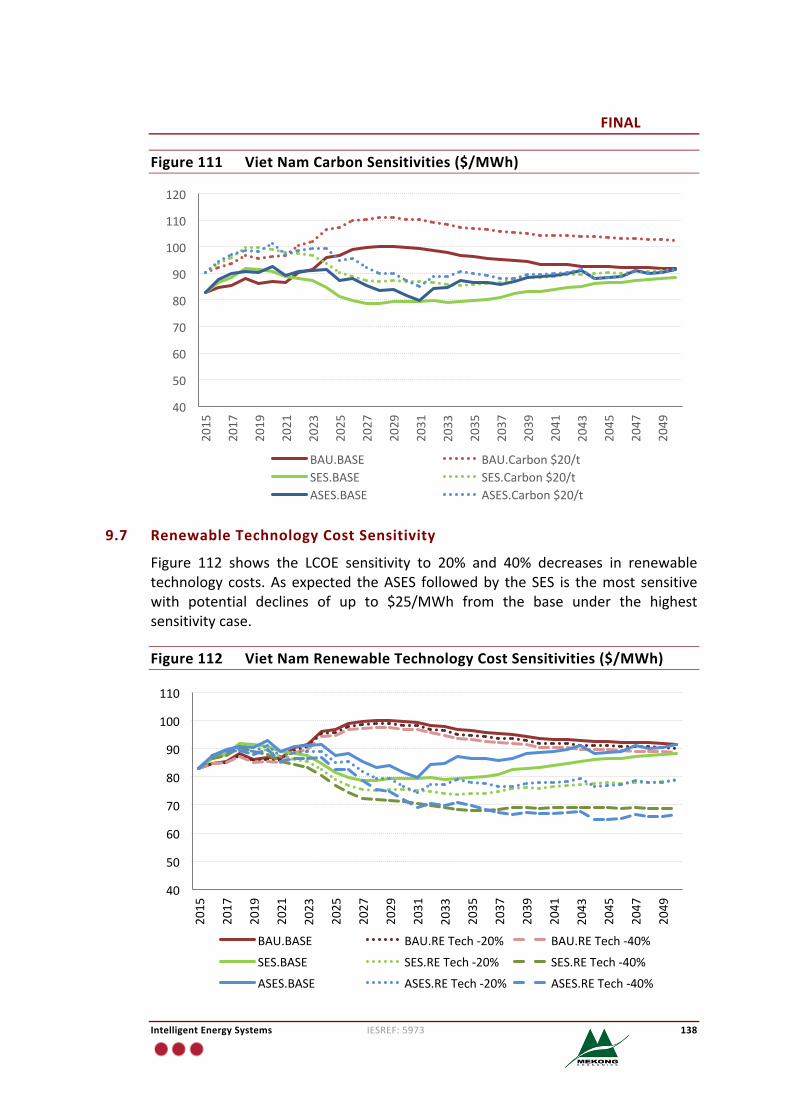

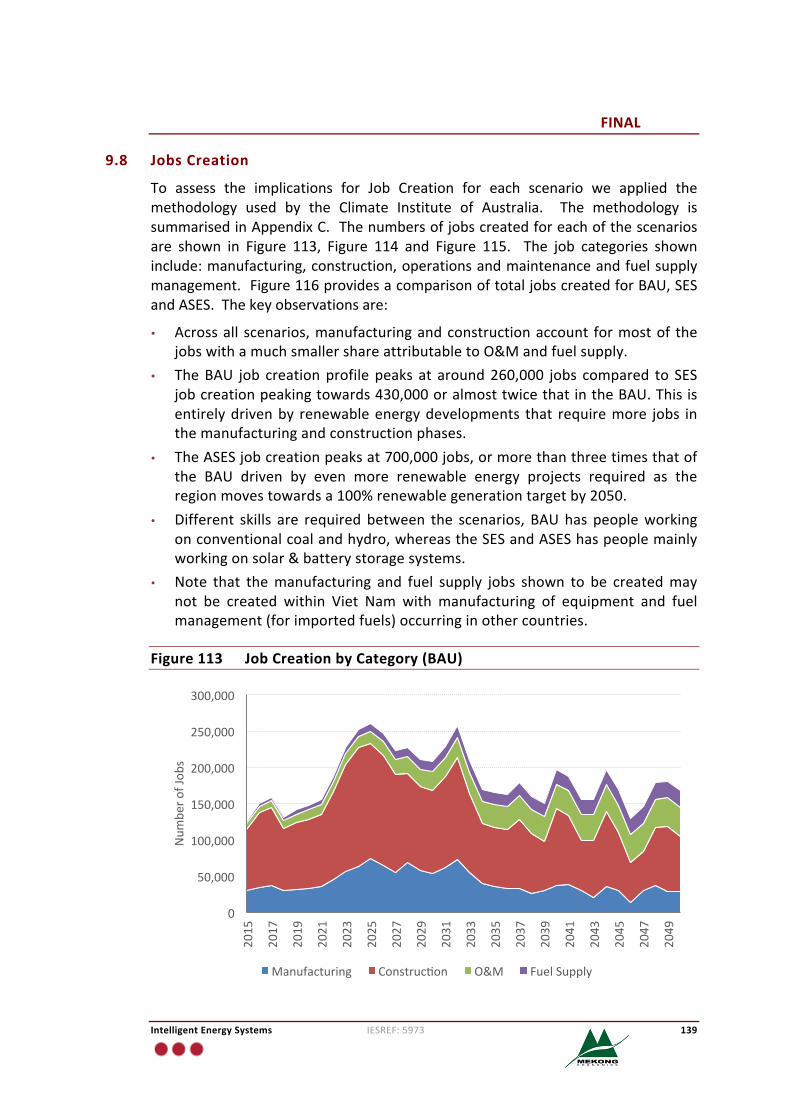

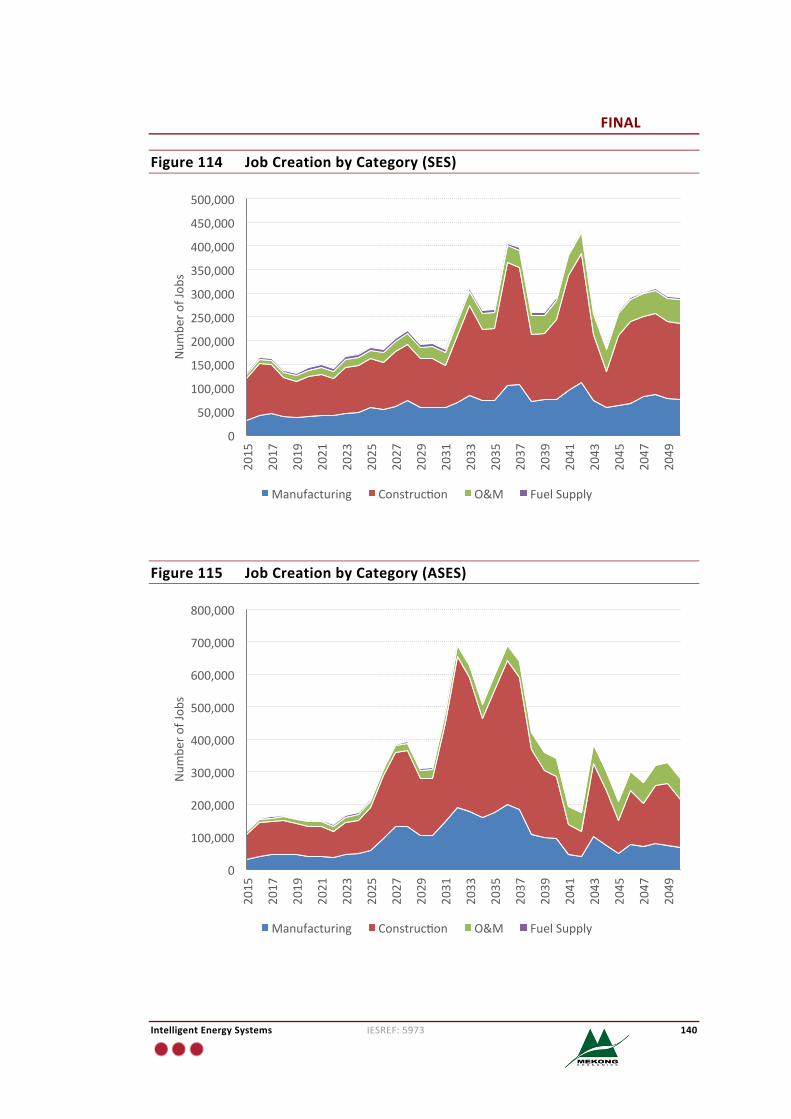

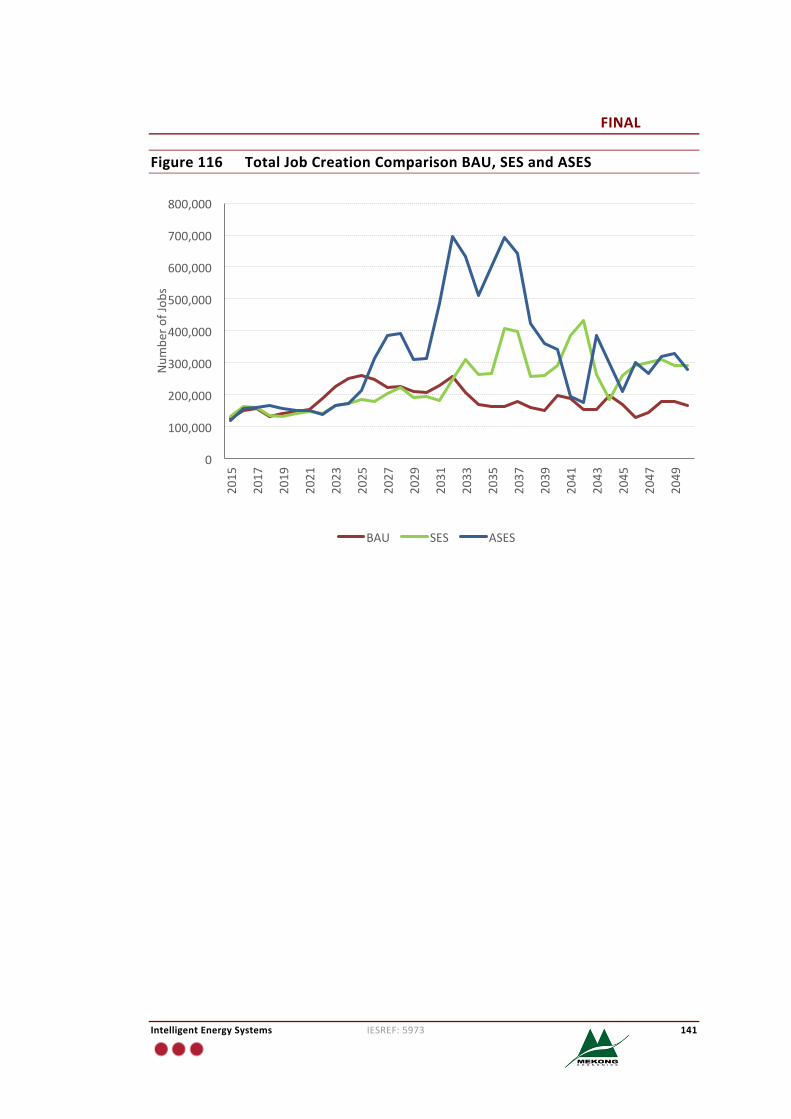

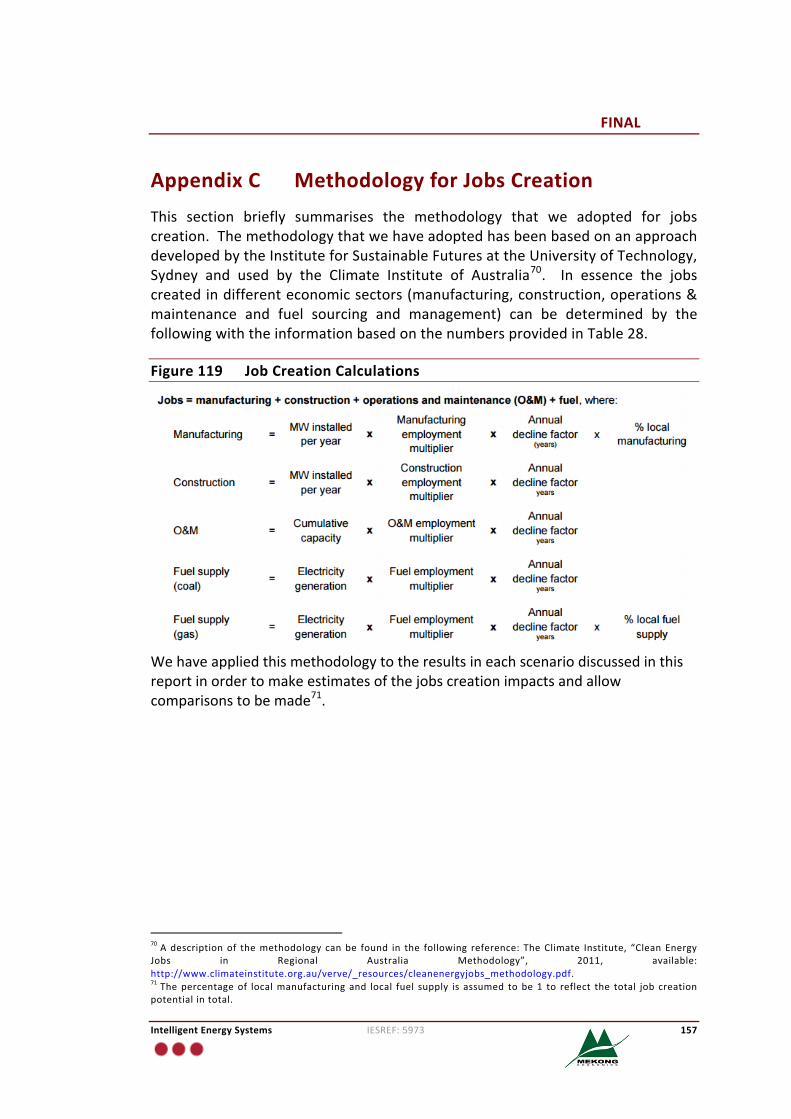

9 EconomicImplications 1249.1 OverallLevelisedCostofElectricity(LCOE) 1249.2 LCOEComposition 1259.3 CumulativeCapitalInvestment 1279.4 OperatingCosts,AmortisedCapitalCostsandEnergyEfficiencyCosts 1319.5 FuelPriceSensitivity 1369.6 ImpactofaCarbonPrice 1379.7 RenewableTechnologyCostSensitivity 1389.8 JobsCreation 139

10 Conclusions 14210.1ComparisonofScenarios 14410.2EconomicImplications 14510.3IdentifiedBarriersfortheSESandASES 14610.4Recommendations 149

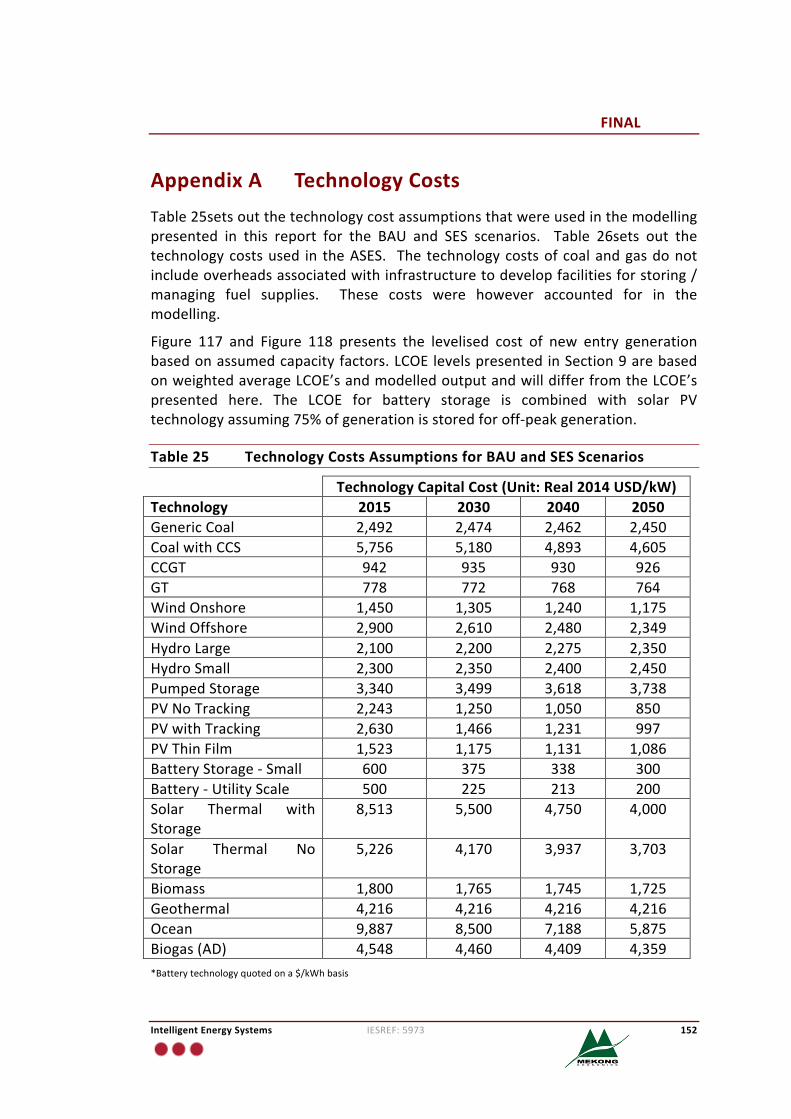

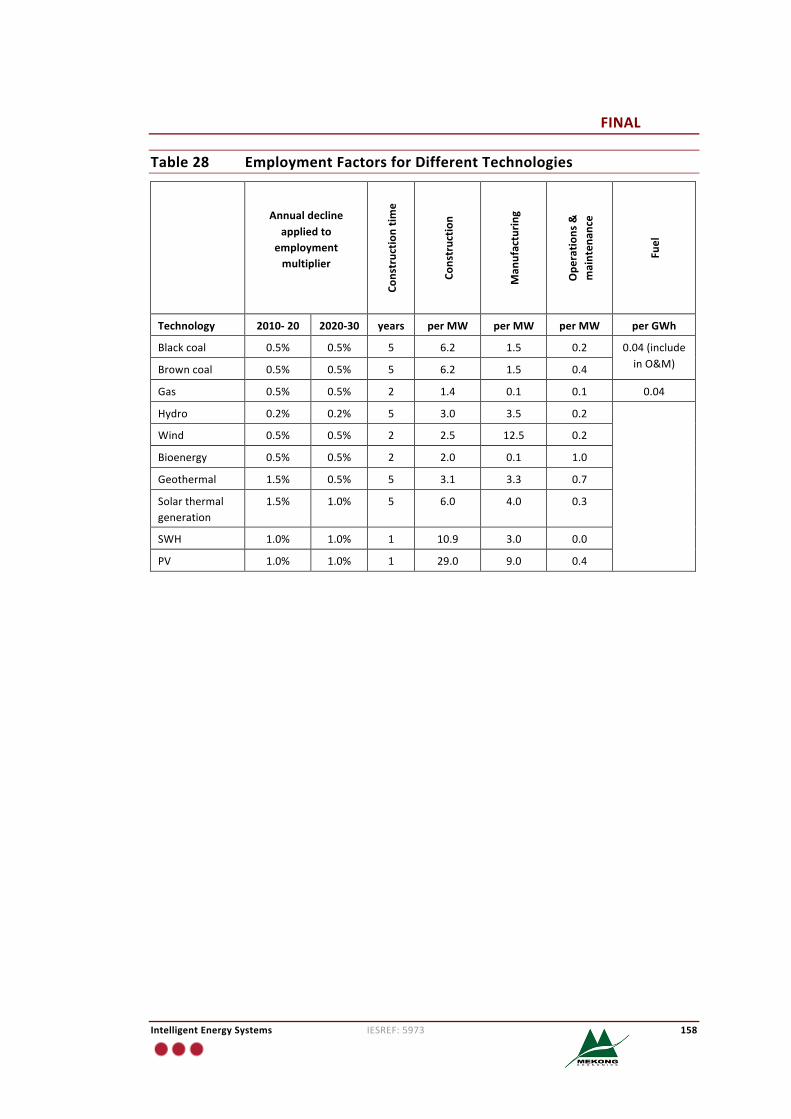

AppendixA TechnologyCosts 152AppendixB FuelPrices 156AppendixC MethodologyforJobsCreation 157AppendixD VietNamWindResourceMaps 159

D.1 WindSpeedMaps 159D.2 WindPowerDensityMaps 163

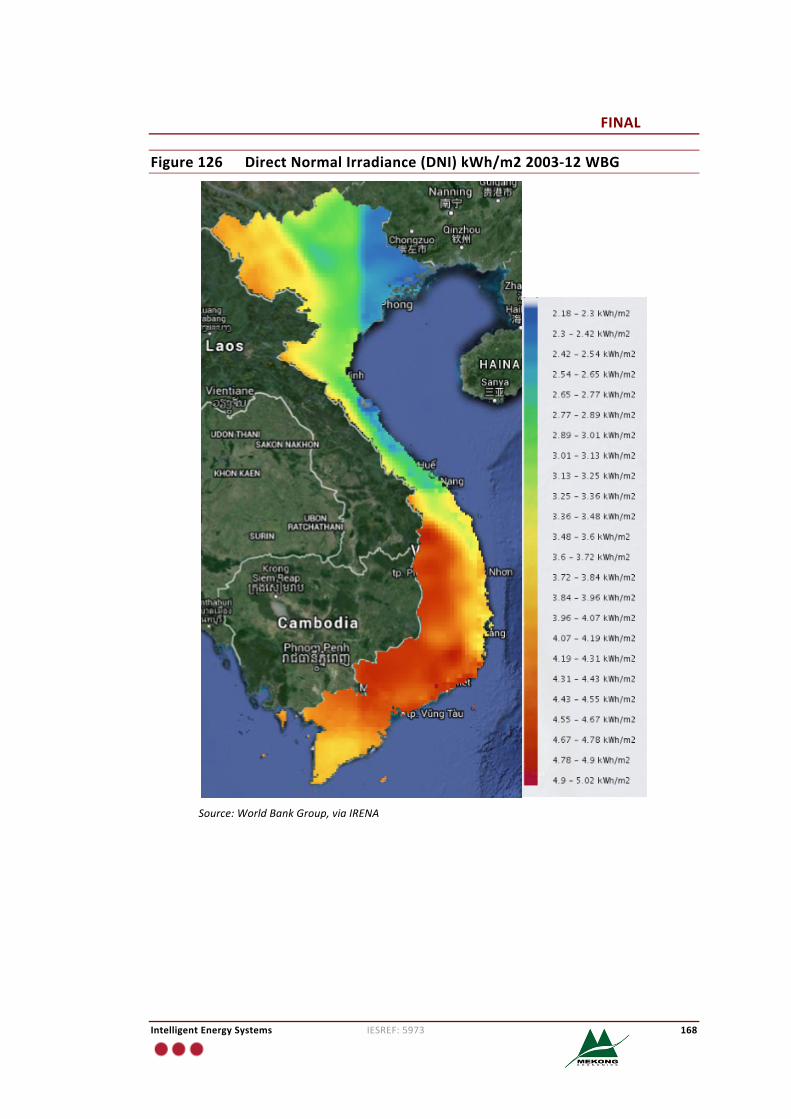

AppendixE VietNamSolarResourceMaps 166E.1 GlobalHorizontalIrradianceandDirectNormalIrradiance 166E.2 ConcentratingSolarPower(CSP)Potential 169

FINAL

IntelligentEnergySystems IESREF:5973 9

1 IntroductionIntelligent Energy Systems Pty Ltd (“IES”) and Mekong Economics (“MKE”) wereretained by WWF – Greater Mekong Programme Office (“WWF-GMPO”) toundertakeaprojectcalled“Produceacomprehensivereportoutliningalternativesfor power generation in the Greater Mekong Sub-region”. This was to developscenarios for the countries of the GreaterMekong Sub-region (GMS) that are asconsistentaspossiblewiththeWWF’sGlobalEnergyVisiontothePowerSectorsofall GreaterMekong Subregion countries. The objectives ofWWF’s vision are: (i)contributetoreductionofglobalgreenhouseemissions(cutby>80%of1990levelsby2050);(ii)reducedependencyonunsustainablehydroandnuclear;(iii)enhanceenergyaccess; (iv) takeadvantageofnewtechnologiesandsolutions; (v)enhancepower sector planning frameworks for the region:multi-stakeholder participatoryprocess;and(vi)developenhancementsforenergypolicyframeworks.

Thepurposeofthisreportistoprovidedetailedcountry-leveldescriptionsofthreescenariosforthepowersectoroftheSocialistRepublicofVietNam(VietNam):

• BusinessasUsual (BAU)powergenerationdevelopmentpathwhich isbasedoncurrentpowerplanningpractices,currentpolicyobjectives;

• Sustainable Energy Sector (SES) scenario, where measures are taken tomaximally deploy renewable energy 1 and energy efficiency measures toachieveanear-100%renewableenergypowersector;and

• Advanced Sustainable Energy Sector (ASES) scenario,which assumes amorerapid advancement and deployment of new and renewable technologies ascomparedtotheSES.

The scenarios were based on public data, independent assessments of resourcepotentials, information obtained from published reports and power systemmodellingoftheGMSregionfortheperiod2015to2050.

1.1 ReportStructure

Thisreporthasbeenorganisedinthefollowingway:

• Section2setsoutrecentoutcomesforVietNam’selectricityindustry;• Section3summarisesthemaindevelopmentoptionscoveringbothrenewable

energyandfossilfuels;• Section4providesabriefsummaryofthescenariosthatweremodelledanda

summaryoftheassumptionsincommon;• Section5setsoutthekeyresultsforthebusinessasusualscenario;

1Proposed but not committed fossil fuel based projects are not developed. Committed and existing fossil fuelbasedprojectsareretiredattheendoftheir lifetimeandnotreplacedwithotherfossil fuelprojects. A leastcostcombinationofrenewableenergygenerationisdevelopedtomeetdemand.

FINAL

IntelligentEnergySystems IESREF:5973 10

• Section6setsoutthekeyresultsforthesustainableenergysectorscenario;• Section7 sets out the key results for an advanced sustainable energy sector

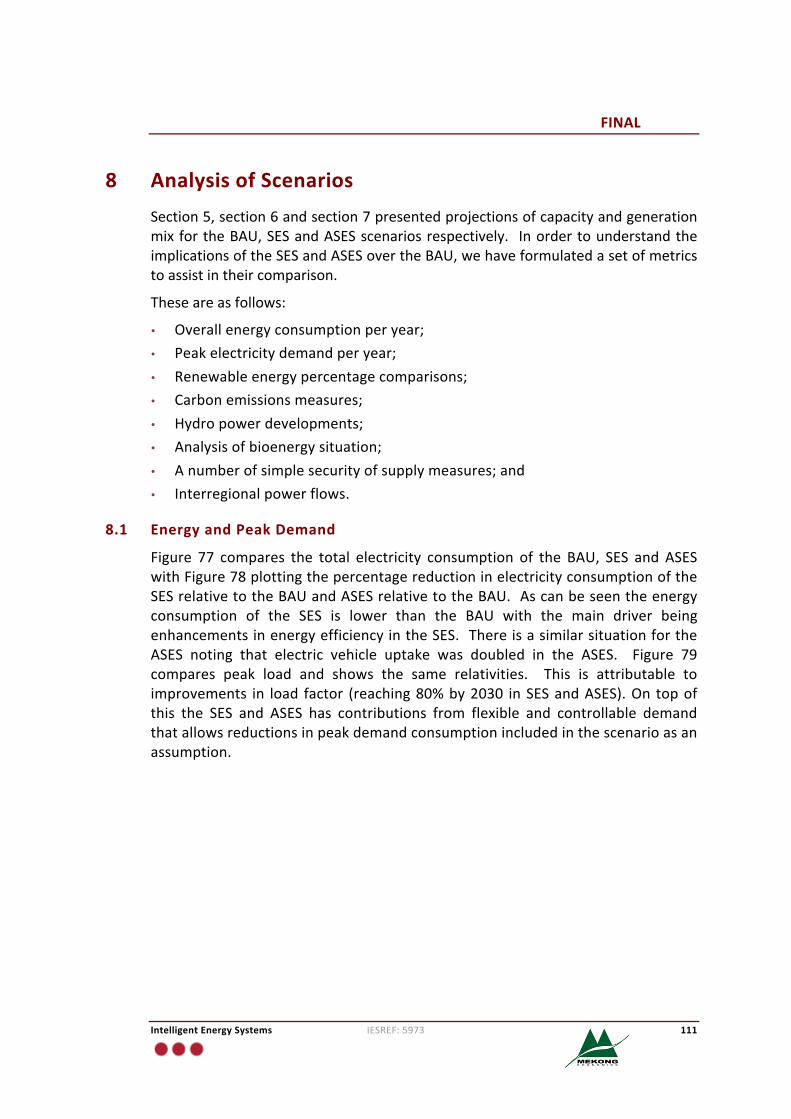

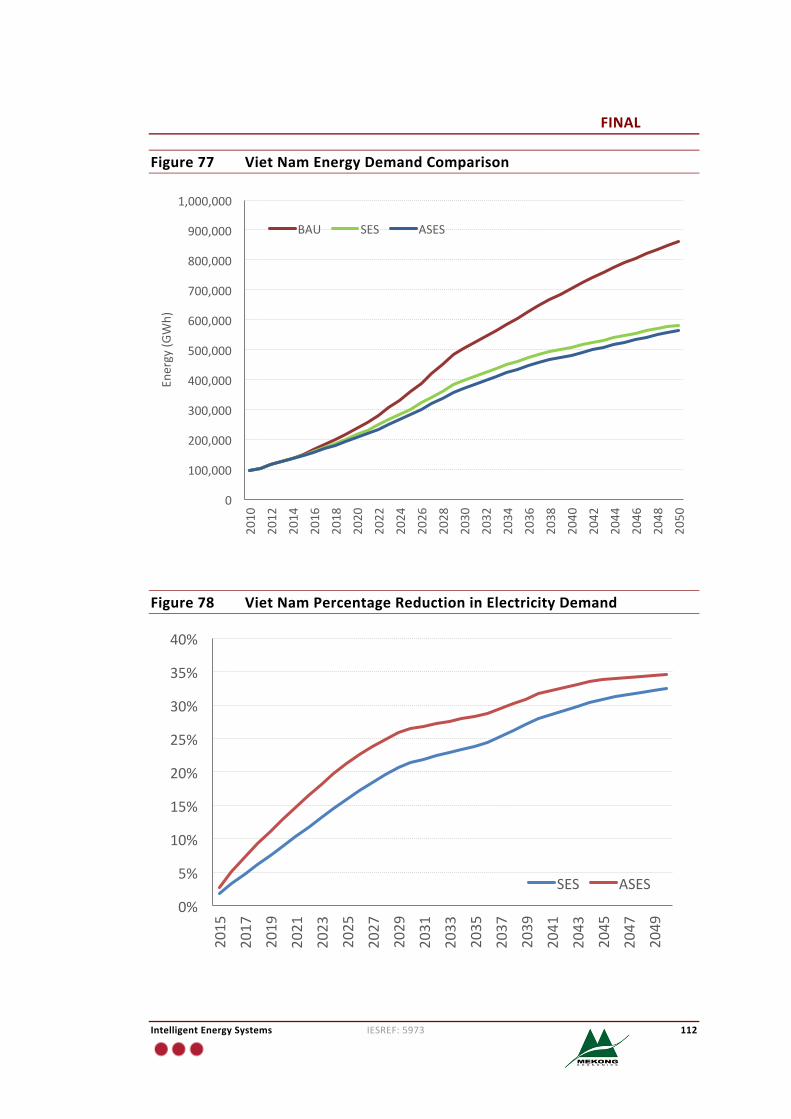

scenario;• Section 8 provides comparative analysis of the three scenarios basedon the

computationofanumberofsimplemetricsthatfacilitatecomparison;• Section9providesanalysisoftheeconomicimplicationsofthescenarios;and• Section10providesthemainconclusionsfromthemodelling.

Thefollowingappendicesprovidesomeadditionalinformationforthescenarios:

• AppendixAcontainsthetechnologycostassumptionsthatwereused;• AppendixBprovidesthefuelpriceprojectionsthatwereused;• AppendixC setsout informationused toestimate jobscreationpotential for

eachscenario.• AppendixDsetsoutanumberofwindresourcemaps;and• AppendixEsetsoutseveralsolarresourcemaps.

Note thatunlessotherwisenoted,all currency in the report isReal2014UnitedStates Dollars (USD). All projections presented in this report commence in theyear2015.

FINAL

IntelligentEnergySystems IESREF:5973 11

2 Background:VietNam’sElectricitySector

2.1 IndustryStructure

Viet Nam’s electricity industry has been undergoing restructuring since 2005 andthisisaprocessthatisongoing.

Restructuring Viet Nam’s electricity sector startedwith the establishment of VietNamElectricity(EVN)asaholdingcompanyin2006. EVNanditssubsidiaries(thePCs)havesinceplayedadominantrole intheelectricity industry. EVN’sactivitiescovermost aspects in Viet Nam’s electricity sector: generation, transmission, theroleof thesinglewholesalebuyer,distribution,andsellingbeingmanagedbyfivePCs.Asof2013,EVNheldmajorityownershipofapproximately61%oftheinstalledgeneratingcapacitydirectlyandthroughitssubsidiaries2.

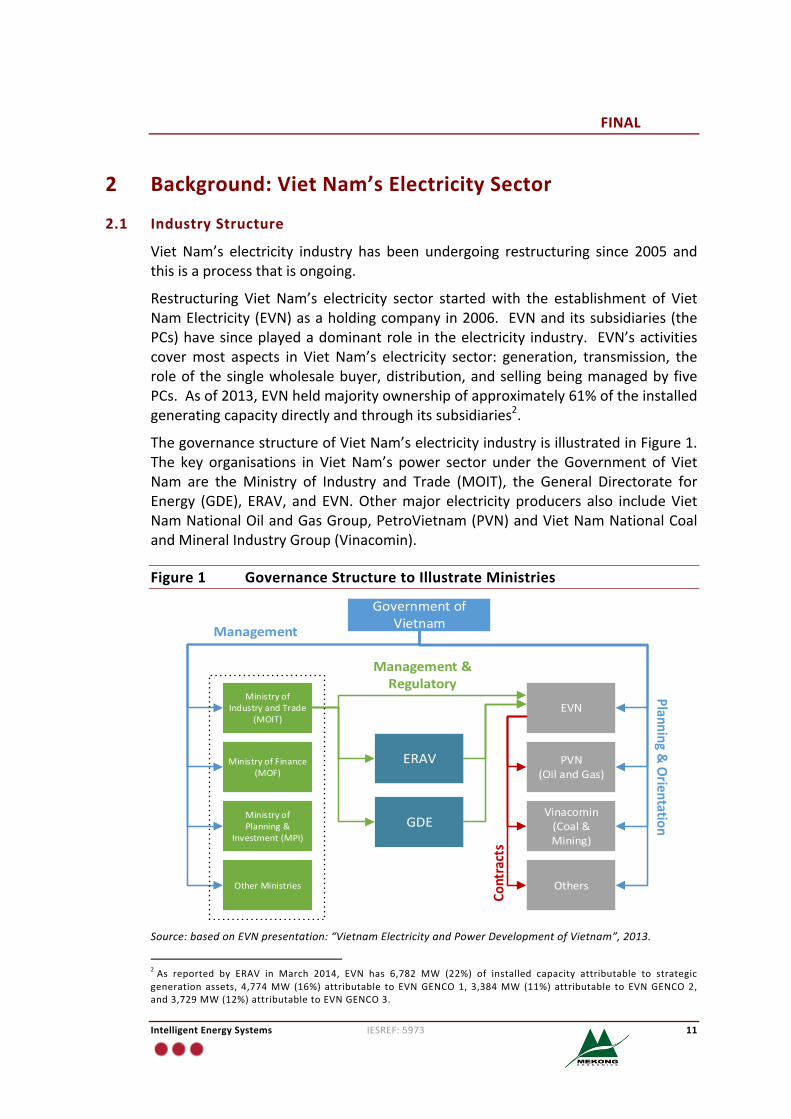

ThegovernancestructureofVietNam’selectricityindustryisillustratedinFigure1.The key organisations in VietNam’s power sector under theGovernment of VietNam are theMinistry of Industry and Trade (MOIT), the General Directorate forEnergy (GDE), ERAV, and EVN.Othermajor electricity producers also includeVietNamNationalOilandGasGroup,PetroVietnam(PVN)andVietNamNationalCoalandMineralIndustryGroup(Vinacomin).

Figure1 GovernanceStructuretoIllustrateMinistries

GovernmentofVietnam

MinistryofIndustryandTrade

(MOIT)

MinistryofFinance(MOF)

MinistryofPlanning&

Investment(MPI)

OtherMinistries

ERAV

GDE

EVN

PVN(OilandGas)

Vinacomin(Coal&Mining)

Others

Management

Planning&Orientation

Management&Regulatory

Contracts

Source:basedonEVNpresentation:“VietnamElectricityandPowerDevelopmentofVietnam”,2013.

2As reported by ERAV in March 2014, EVN has 6,782 MW (22%) of installed capacity attributable to strategicgeneration assets, 4,774MW (16%) attributable to EVNGENCO1, 3,384MW (11%) attributable to EVNGENCO2,and3,729MW(12%)attributabletoEVNGENCO3.

FINAL

IntelligentEnergySystems IESREF:5973 12

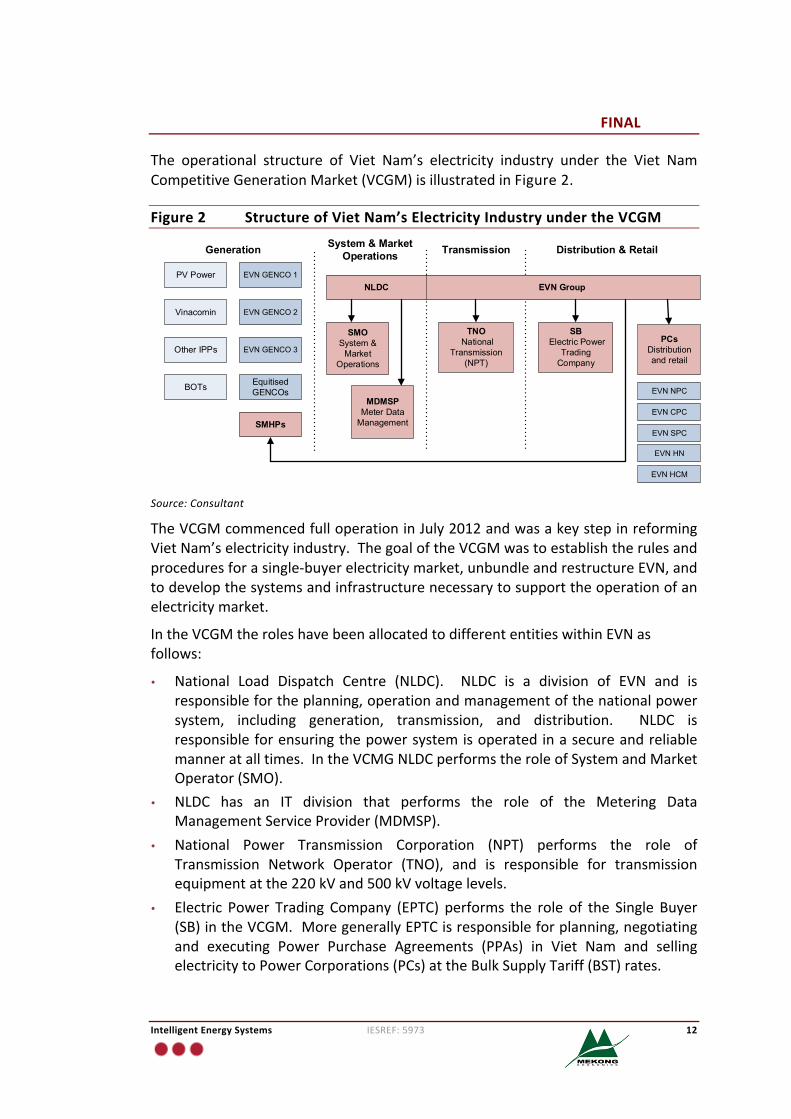

The operational structure of Viet Nam’s electricity industry under the Viet NamCompetitiveGenerationMarket(VCGM)isillustratedinFigure2.

Figure2 StructureofVietNam’sElectricityIndustryundertheVCGM

Source:Consultant

TheVCGMcommencedfulloperationinJuly2012andwasakeystepinreformingVietNam’selectricityindustry.ThegoaloftheVCGMwastoestablishtherulesandproceduresforasingle-buyerelectricitymarket,unbundleandrestructureEVN,andtodevelopthesystemsandinfrastructurenecessarytosupporttheoperationofanelectricitymarket.

IntheVCGMtheroleshavebeenallocatedtodifferententitieswithinEVNasfollows:

• National Load Dispatch Centre (NLDC). NLDC is a division of EVN and isresponsiblefortheplanning,operationandmanagementofthenationalpowersystem, including generation, transmission, and distribution. NLDC isresponsibleforensuringthepowersystemisoperatedinasecureandreliablemanneratalltimes.IntheVCMGNLDCperformstheroleofSystemandMarketOperator(SMO).

• NLDC has an IT division that performs the role of the Metering DataManagementServiceProvider(MDMSP).

• National Power Transmission Corporation (NPT) performs the role ofTransmission Network Operator (TNO), and is responsible for transmissionequipmentatthe220kVand500kVvoltagelevels.

• Electric Power Trading Company (EPTC) performs the role of the Single Buyer(SB)intheVCGM.MoregenerallyEPTCisresponsibleforplanning,negotiatingand executing Power Purchase Agreements (PPAs) in Viet Nam and sellingelectricitytoPowerCorporations(PCs)attheBulkSupplyTariff(BST)rates.

BOTs

PV Power

Vinacomin

Other IPPs

Equitised GENCOs

SMHPs

EVN GENCO 1

EVN GENCO 2

EVN GENCO 3

Generation System & Market Operations Distribution & Retail

TNO National

Transmission (NPT)

SB Electric Power

Trading Company

PCsDistribution and retail

MDMSPMeter Data

Management

EVN Group

Transmission

SMOSystem &

Market Operations

NLDC

EVN NPC

EVN CPC

EVN SPC

EVN HN

EVN HCM

FINAL

IntelligentEnergySystems IESREF:5973 13

• ThefivePCsaredistributionandretailcompanies. TheypurchasepowerfromEPTC at the BST and sell electricity to their customers at regulated uniformtariffs.

ThereareplanstotransitiontheVCGMtowardstheVietNamWholesaleElectricityMarket (VWEM) by 2019, which would involve having PC’s being responsible formanaging theirownpowerpurchases, rather than theSBand takingmeasures tomaximisethedirectparticipationofallgeneratorsinthewholesalemarket.

2.2 PowerSystem

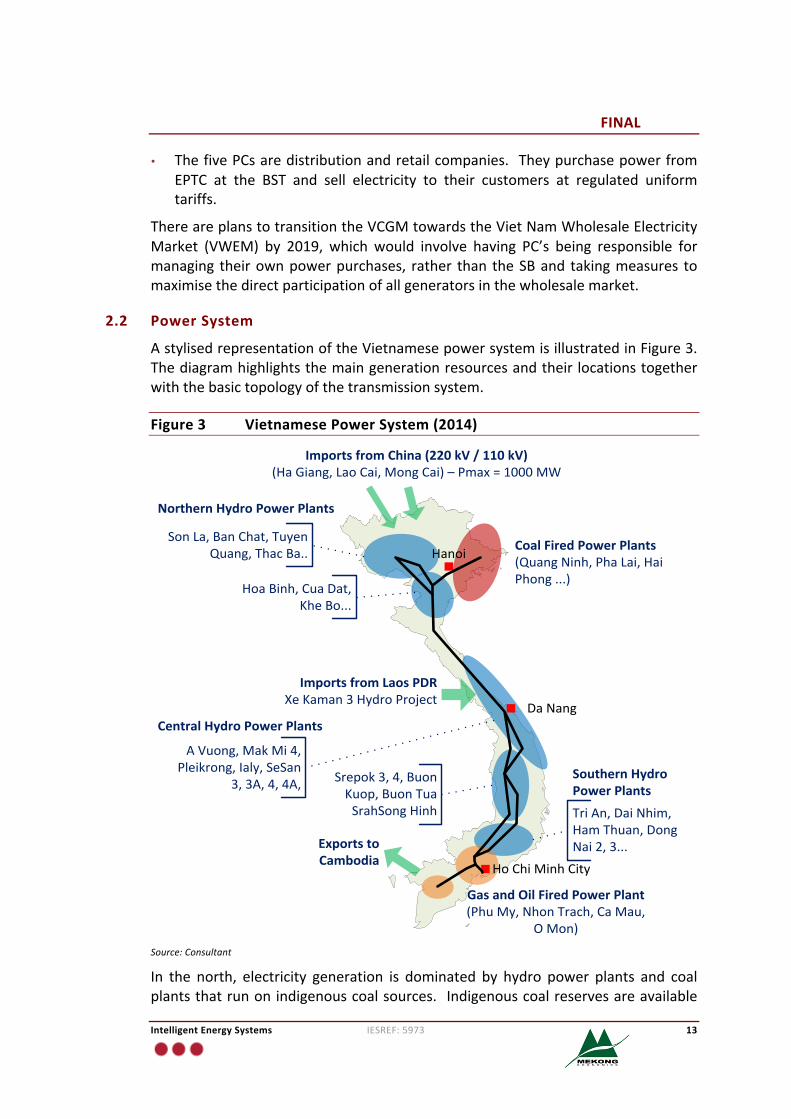

AstylisedrepresentationoftheVietnamesepowersystemisillustratedinFigure3.Thediagramhighlightsthemaingenerationresourcesandtheirlocationstogetherwiththebasictopologyofthetransmissionsystem.

Figure3 VietnamesePowerSystem(2014)

Hanoi

DaNang

HoChiMinhCity

CoalFiredPowerPlants(QuangNinh,PhaLai,HaiPhong...)

NorthernHydroPowerPlants

ImportsfromChina(220kV/110kV)(HaGiang,LaoCai,MongCai)–Pmax=1000MW

GasandOilFiredPowerPlant(PhuMy,NhonTrach,CaMau,

OMon)

ImportsfromLaosPDRXeKaman3HydroProject

ExportstoCambodia

SonLa,BanChat,TuyenQuang,ThacBa..

HoaBinh,CuaDat,KheBo...

CentralHydroPowerPlants

AVuong,MakMi4,Pleikrong,Ialy,SeSan

3,3A,4,4A,

TriAn,DaiNhim,HamThuan,DongNai2,3...

SouthernHydroPowerPlants

Srepok3,4,BuonKuop,BuonTuaSrahSongHinh

Source:Consultant

In the north, electricity generation is dominated by hydro power plants and coalplantsthatrunonindigenouscoalsources. Indigenouscoalreservesareavailable

FINAL

IntelligentEnergySystems IESREF:5973 14

mainly inthenortheastregion(QuangNinhProvince)andarebeingexploitedforpowergeneration.Likewisethereservoirsforthehydrosgenerallylieinriverbasinsin the northwest, particularly in the red river system. Apart from electricitygeneration the large reservoirs within the Red river system are used for floodmitigationintheRedriverdelta. Inthenorth,therearealsopower importsfromPeople’s Republic of China (PRC), although thenational systemsofVietNamandPRCareelectricallyisolated.

Thecentral regionofVietNam isalmostentirelydominatedbyhydrogeneration.The central region is considered to consist of two main subregions: the eastcoastlandandthesouth-westhighlands.Thecoastalsubregionisanarrowstripoflandwhich consists of a numberof separatebasins. There is considerablehydropotentialdue to thegradientof the rivers inmountainousareas thatareclose tothecoastline.Thesouth-westhighlandshaveanumberofMekongtributariesthatflowtowardsthewesternborderofthecountry.

Thesouthern region isdominatedbyhydro,CombinedCycleGasTurbines (CCGT)andSteamTurbines(ST).TheCCGTsincludingPhuMyComplex,NhonTrach,BaRiaandCaMauandrunonnaturalgasthatistransportedfromanumberofoffshorefields.ThemainriversystemsinthesouthregionincludetheDongNaiRiverBasinwith significant potential for hydro power generation and to the west of it, thedownstream Mekong Delta (only 5% of the entire Mekong basin). This poseschallengesforfloodmitigationinthedelta.

Itisnotedthat,underthegovernment’sstrategytodiversifydifferenttechnologiesacross the regions, coalpowerplantshavebeenplannedandconstructed for thecentralandsouthernregions,withseveralgeneratorsalreadycommissioned,withrecentlytheVinhTancoalthermalcomplexinBinhThuanprovince(South),DuyenHaicoalthermalcomplex inTraVinhprovince(South)andVungAngcoalthermalgeneration complex in Ha Tinh province (Centre). In addition, the first nuclearpowerplantsmaybeconstructedinNinhThuanprovince(Centre).

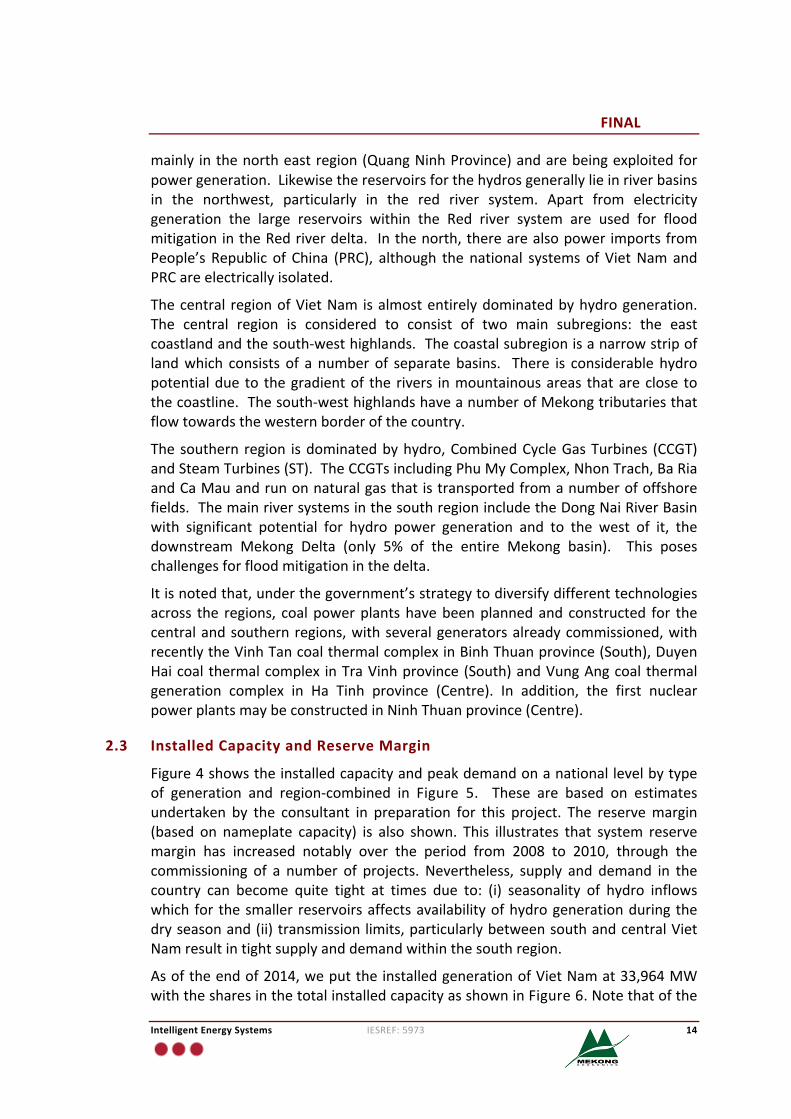

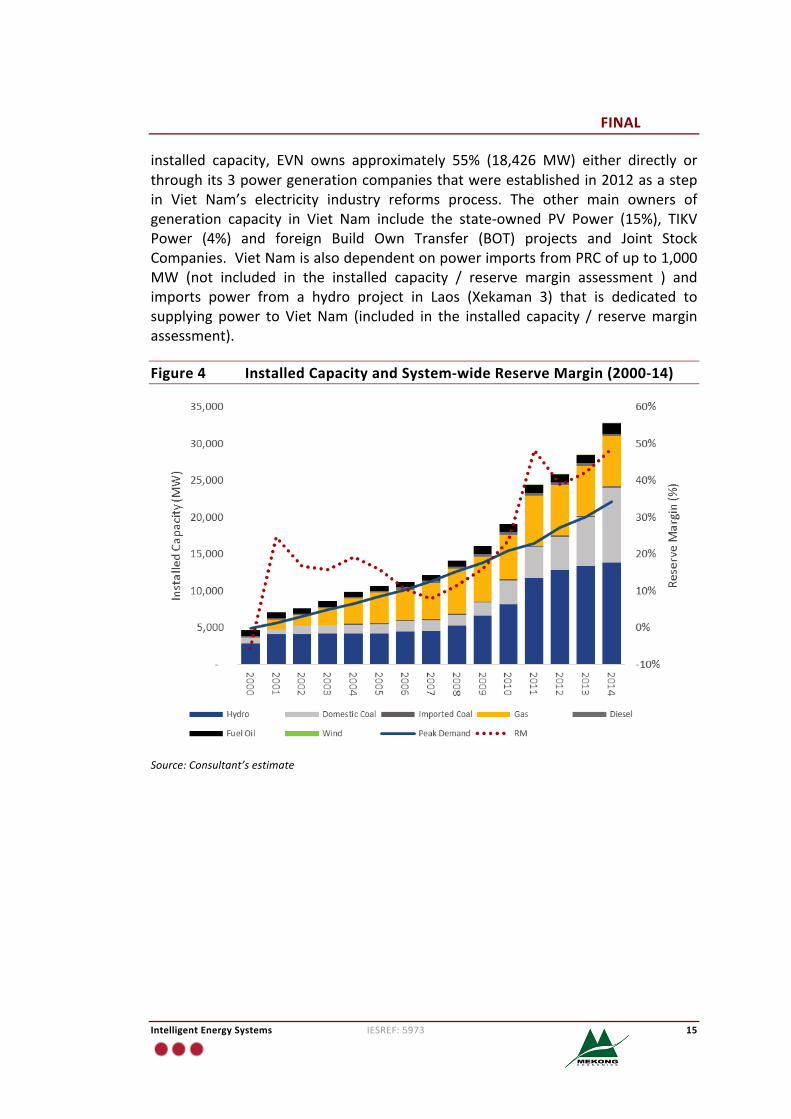

2.3 InstalledCapacityandReserveMargin

Figure4showstheinstalledcapacityandpeakdemandonanationallevelbytypeof generation and region-combined in Figure 5. These are based on estimatesundertaken by the consultant in preparation for this project. The reservemargin(based on nameplate capacity) is also shown. This illustrates that system reservemargin has increased notably over the period from 2008 to 2010, through thecommissioning of a number of projects. Nevertheless, supply and demand in thecountry can become quite tight at times due to: (i) seasonality of hydro inflowswhich for thesmaller reservoirsaffectsavailabilityofhydrogenerationduringthedryseasonand(ii)transmissionlimits,particularlybetweensouthandcentralVietNamresultintightsupplyanddemandwithinthesouthregion.

Asoftheendof2014,weputtheinstalledgenerationofVietNamat33,964MWwiththesharesinthetotalinstalledcapacityasshowninFigure6.Notethatofthe

FINAL

IntelligentEnergySystems IESREF:5973 15

installed capacity, EVN owns approximately 55% (18,426 MW) either directly orthroughits3powergenerationcompaniesthatwereestablishedin2012asastepin Viet Nam’s electricity industry reforms process. The other main owners ofgeneration capacity in Viet Nam include the state-owned PV Power (15%), TIKVPower (4%) and foreign Build Own Transfer (BOT) projects and Joint StockCompanies.VietNamisalsodependentonpowerimportsfromPRCofupto1,000MW (not included in the installed capacity / reserve margin assessment ) andimports power from a hydro project in Laos (Xekaman 3) that is dedicated tosupplying power to VietNam (included in the installed capacity / reservemarginassessment).

Figure4 InstalledCapacityandSystem-wideReserveMargin(2000-14)

Source:Consultant’sestimate

FINAL

IntelligentEnergySystems IESREF:5973 16

Figure5 InstalledCapacity(byRegion)andSystem-wideReserveMargin

Source:Consultant’sestimate

Figure6 CapacityBreakdownbyType(2014)

Source:Consultant’sestimate

FINAL

IntelligentEnergySystems IESREF:5973 17

2.4 ElectricityDemand

2.4.1 System-WideandRegionalDemandTrends

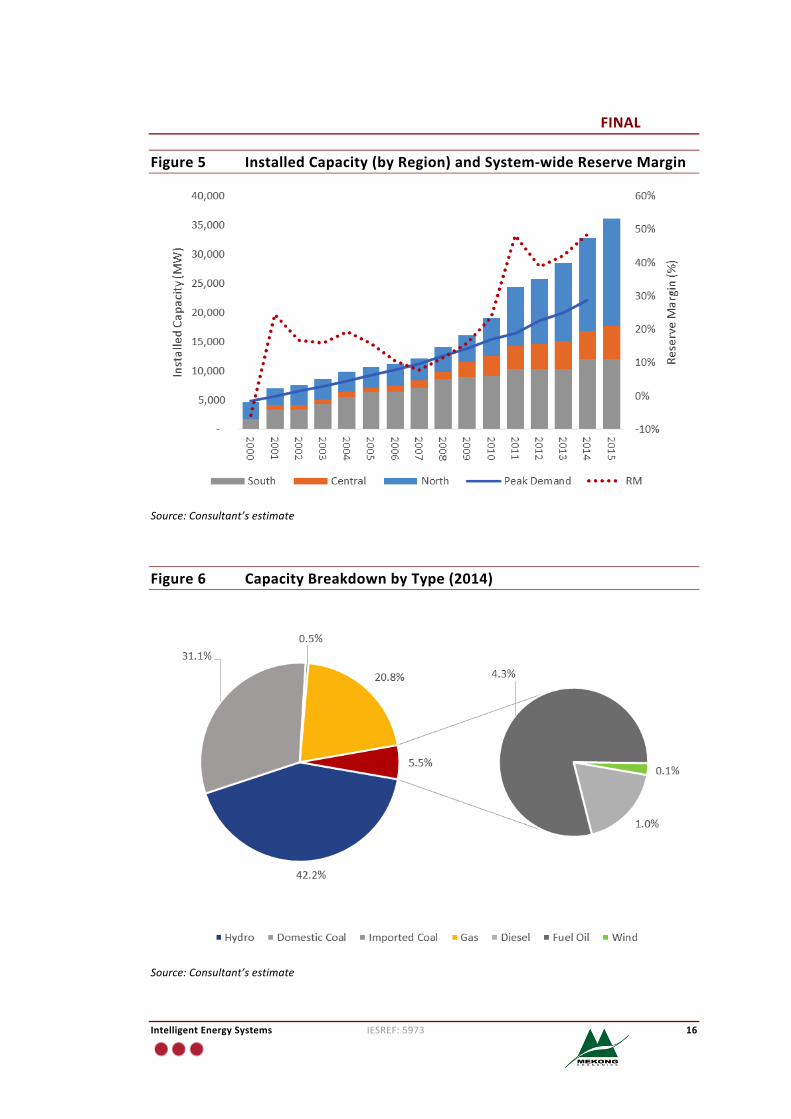

Figure 7 showsmaximum (peak) demand on a national level and total electricitydemand. Over the past 10 years national energy demand has had a compoundannual growth rate (CAGR) of 12.7% and for peak demand CAGR of 10.2%.Regionally, demand in the south of Viet Nam has grown themost rapidly in therecentpast,althoughwhenCAGRsareconsideredfortheperiod2004to2013,the“long-term” regional growth rates are: North region at 14.0%, south region at13.5%,andcentralregionat12.0%. Theseareveryhighratesofdemandgrowth.Peakdemandineachregionhasexhibitedasimilartrend.

Figure7 PeakDemandandEnergyProduction(2000-14)

Source:ERAV

2.4.2 ElectricitySales(GridConnected)

EconomicdevelopmentinVietNamhasdrivenstronggrowthinelectricitydemand,whichreflectsrapidindustrialisation,anexpansionofbusinessandservicesandalsorisinghouseholdconsumptioninlinewithrisinglivingstandards;forexample,from1995to2010thepercapitaconsumptionroseduringthesameperiodfromsome156kWh toabout900kWh. Figure8 shows thenational electricity sales for theperiod 2000 to 2013 and the associated year-on-year growth rates, which haveaveragedaround12%overtheperiod2009-13.

FINAL

IntelligentEnergySystems IESREF:5973 18

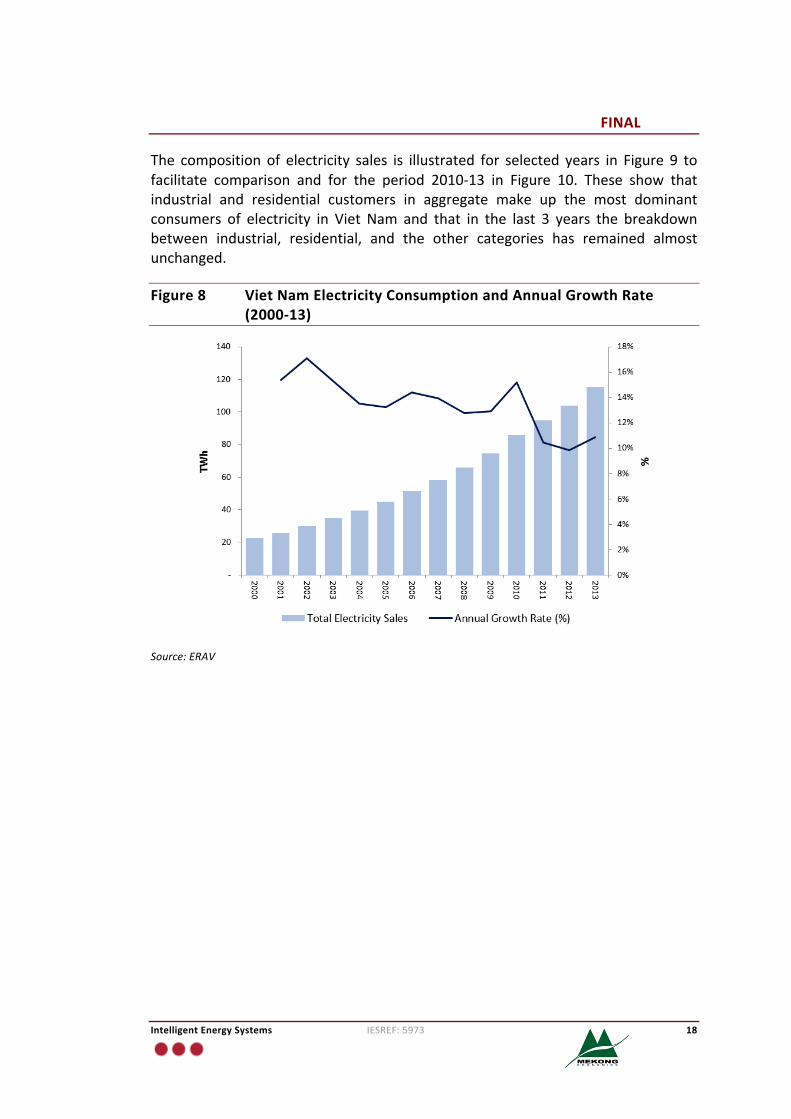

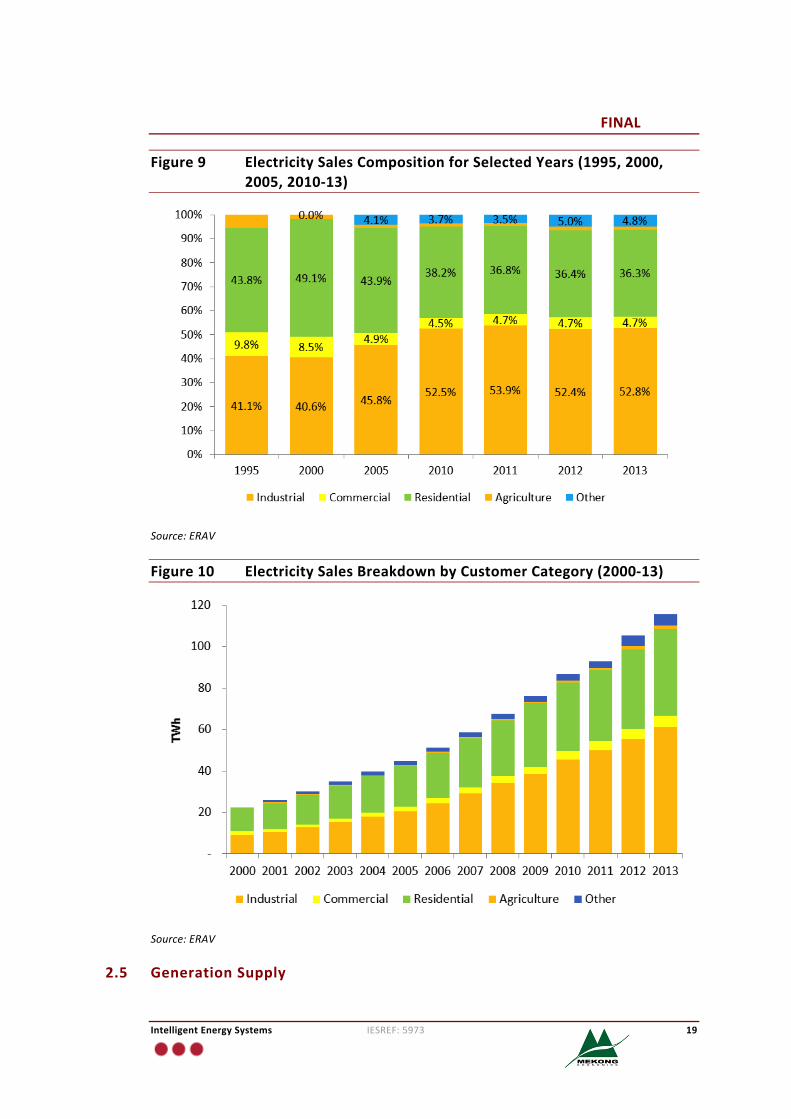

The composition of electricity sales is illustrated for selected years in Figure 9 tofacilitate comparison and for the period 2010-13 in Figure 10. These show thatindustrial and residential customers in aggregate make up the most dominantconsumers of electricity in Viet Nam and that in the last 3 years the breakdownbetween industrial, residential, and the other categories has remained almostunchanged.

Figure8 VietNamElectricityConsumptionandAnnualGrowthRate(2000-13)

Source:ERAV

FINAL

IntelligentEnergySystems IESREF:5973 19

Figure9 ElectricitySalesCompositionforSelectedYears(1995,2000,2005,2010-13)

Source:ERAV

Figure10 ElectricitySalesBreakdownbyCustomerCategory(2000-13)

Source:ERAV

2.5 GenerationSupply

FINAL

IntelligentEnergySystems IESREF:5973 20

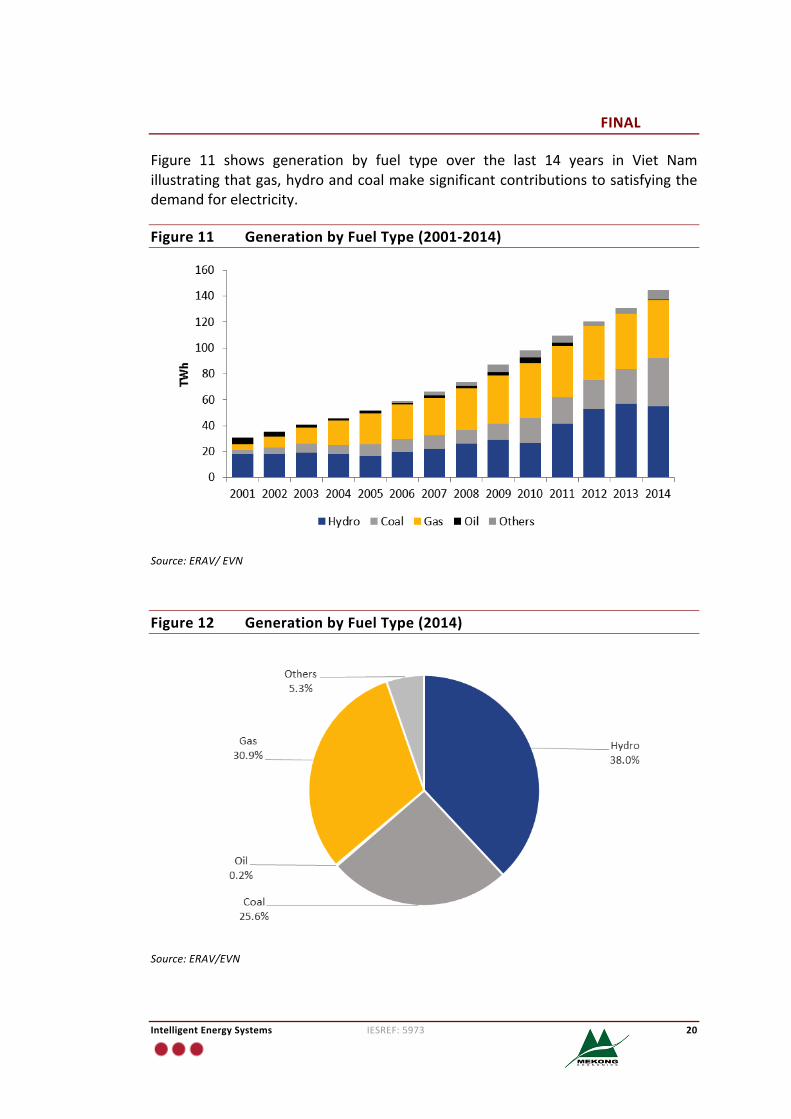

Figure 11 shows generation by fuel type over the last 14 years in Viet Namillustratingthatgas,hydroandcoalmakesignificantcontributionstosatisfyingthedemandforelectricity.

Figure11 GenerationbyFuelType(2001-2014)

Source:ERAV/EVN

Figure12 GenerationbyFuelType(2014)

Source:ERAV/EVN

FINAL

IntelligentEnergySystems IESREF:5973 21

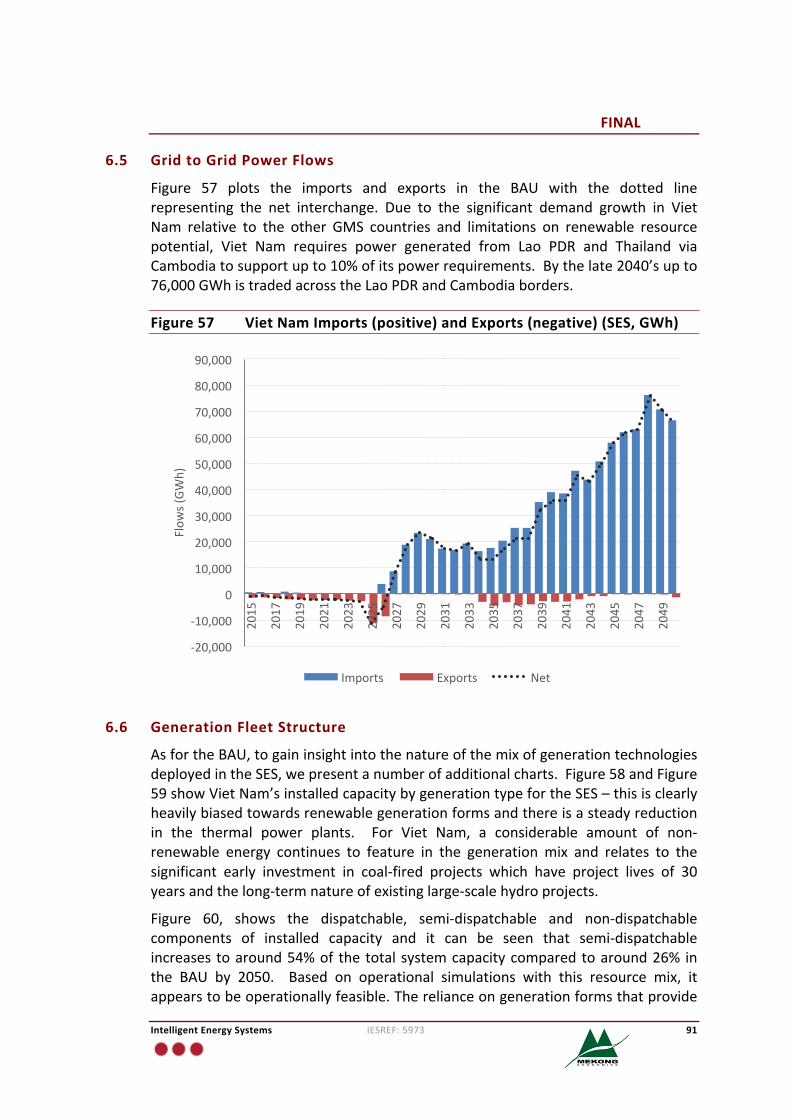

2.6 ImportsandExports

Anumber of small load centres in VietNam’s north are effectively suppliedwithpower imports fromPRC. VietNamalso receives power imports froma recentlycommissionedhydroprojectinLaos(Xekaman3)andVietNam’sgridisconnectedtoCambodiatoprovideexportstothecountry.Asummaryofthecurrentsituationasof2013is:

• Importsofaround3.61TWh3onaveragefromPRCintheNorth;

• Imports fromXeKaman3hydroproject fromLaosPDR in the central region:and

• Exportsofaround1.22TWhonaveragetoCambodia,intheSouth.

2.6.1 ImportsfromPRC

Power imports fromPRC commenced in 2004 via two110KV lines and later two220kV lines. The combinedmaximumcapacityof these interconnections is1,000MW. The annual imported amount is around 3.6 TWh on average but has beengenerally declining from 5.6 TWh in 2010 to 1.8 TWh in 2015 (estimated). Theexisting purchase agreements (for ten year duration) are expected to end after2015. Note that the Chinese grid and Vietnamese grids are not electricallyconnected; loads in the north are switched from being connected to theVietnamesenationalsystemtotheChinesegrid.

AtpresentthefollowingtransmissionlinesimportpowerfromPRCtoVietNam:

• 220kVtransmissionlinefromHaGiang;

• 220kVtransmissionlinefromLaoCai;

• 110kVtransmissionlinefromHaGiang;and

• 110kVtransmissionlinefromMongCai.

2.6.2 ImportsfromLaoPDR

Xe Kaman 3 Hydropower project is located in Laos PDR and is dedicated toexporting power to Viet Nam’s transmission system. The 250 MW project wasmostly financedbytheGovernmentofVietNam. Theprojectstartedcommercialoperation in 2013. It has a power purchase agreement in placewith EVN and isoperatedbyNLDCaccordingtofixedgenerationschedules.

2.6.3 ExportstoCambodia

VietNamexportspowertoCambodiaviaa220kVChauDo–Takeotransmissionline.In2013,VietNamexportedsome1.34TWhtothecountry.

3Reportedtobe2.46TWhin2014.

FINAL

IntelligentEnergySystems IESREF:5973 22

3 DevelopmentOptionsforVietNam’sElectricitySector

3.1 Overview

As with a number of other countries in the region Viet Nam's economy hasexperiencedsignificantgrowthwhichhasbeenaccompaniedbyveryhighratesofelectricitydemandgrowth.Evenwithaslightsofteningintheeconomicoutlookforthe country in the last year, basic analysis shows that electricity demand growthratesinthecountrywillberelativelyhighintotheneartermfuture.Thisismoresothe case given long-term strategic plans by the Government to focus ontransitioning the economy towards onewhere the industrial sector plays a largerrolethanatpresent.Accompanyingeconomicgrowthhasbeenanincreaseinthelivingstandards,whichhastranslatedintoincreasinglevelsofhouseholdelectricityconsumption, particularly in urban areas. These trends have put pressure on theexisting infrastructure including distribution networks, transmission networks andgeneration facilities to ensure a stable and reliable flow of electrical energy isprovidedtoendusers.

Viet Nam is endowed with a diverse set of primary energy resources, includingdomesticcoal,offshorenaturalgasreserves,biomass,biogas,solar,largeandsmall-scale hydro, onshore and offshore wind, geothermal, and marine-basedtechnologiessuchastidalandwave.Whileeachoftheseresourceshasitsownsetof challenges, they provide the basis for developing a range of possibledevelopmentpaths for the country's electricity industry. A summaryof themainresourcedevelopmentoptionsavailabletoVietNamisasfollows:

• Domesticcoal.Therearereservesofligniteandsub-bituminousgradesofcoalwith reserves located mainly around the red river basin around Quang Ninhprovinceinthenortheastofthecountry.Themajorityofthecoal-firedpowerstationsinVietNamexploitthesereserves. Estimatesofreservesizessuggestthatfurtherexploitationispossible,althoughapartfromtheexternalitiessuchasgreenhousegasemissionsand localpollution,thenortheast locationofthereserves is not ideally located given the structure of Viet Nam's transmissionsystem,thefactthatmanycoalplant inthisareaarealready inplaceandthegradeofcoalbeinginthelowerendoftherangeofwhatistypicallypreferredfor coal based generation. Domestic transportation networks (via sea or rail)for domestic coal havebeen contemplated, butwith domestic coal prices fortheelectricitysectorbeing regulated tocome into linewith internationalcoalprices,theeconomicsofsuchinfrastructureinvestmentsagainstinvestmentinfacilitiestoimporthigherqualitycoalatlocationsalongthecoastline,makethisunlikely.

• Imported coal. Viet Nam has a coastline that spans some 3260 km whichprovidesanumberofsitesthatwouldallowforthedevelopmentofcoalimportandstorage facilities to supportcoalprojectsat locations thatareconvenient

FINAL

IntelligentEnergySystems IESREF:5973 23

given the transmission network structure and location of load centres. Anumber of such facilities are already under development and there are plansunder the last power plan to continue to expand and grow these facilities insupportof coal importprojects thatwould likely sourcehighgrade coal fromcoalsuppliersinIndonesiaand/orAustralia.

• Offshore natural gas reserves. VietNam is estimated tohave some617Bcm(21.8 Tcf) of proved reserves, or around 52% of the total proved natural gasreserves of the GMS. Gas reserves have been found in five of the sevenoffshorebasins4: SongHong,PhuKhanh,NamConSon,Cuu LongandMalay-ThoChu.TheNamConSonandCuuLongbasinsareexploitedtosupplygastothe PhuMy complex, Ba Ria, andNhon Trach. Off the south coast, the PM3fieldintheMalay-ThoChubasinisalsoinproductionandsuppliesgastotheCaMaucomplex. FurtherdevelopmentsofVietNam’soffshoregas reserveshasbeencontemplated,withthemostprospectivebeing:

− Furtherdevelopmentofthesouth-westregion.OffshoreBlocksB,52/97,48/95, could support significant natural gas power generation projects inthesouthofVietNam,andinparticular,topupgastotheCaMaucomplexand allow further development of the OMon complex. PetroVietnam iscurrently working with recent joint venture partners Murphy Oil andExxonMobiltodevelopthesefields;and

− North-eastregion.Offshoreoilandgasfieldshavebeenidentifiedoffthenortheastcoastlinewithextensivesurveyingandexplorationstillongoing.Astheinvestmentintheinfrastructuretosupportdevelopmentofthisfieldissignificant,thisisconsideredtobealonger-termoptionfordevelopment.

• LNG.ThemostrecentGasDevelopmentPlanandPowerDevelopmentPlan7(PDP7) to have been approved by the government include plans for an LNGregasificationterminalsitedinthecentralprovinceofBinhThuan(nearHoChiMinhCity)withacapacityof3MTPA.However,thedevelopmentoftheLNGterminalhasbeendelayedanditappearsunlikelythatanLNGimportterminalwouldbeinoperationbefore2020.

• NuclearPower.Aspartofalong-termenergysecuritystrategyVietNamhasbeenenhancingtheirnuclearpowerknowledgeandcapability. VietNamhasinplaceagreementswithRussiaandJapantobuildnuclearpowerprojectsof2400MWand2000MWrespectively5;bothplannedtobeconstructedintheNinh Thuan province. Nuclear power features in Viet Nam’s powerdevelopmentplans,althoughthedatesoffirstgenerationfromnuclearpowerremainsuncertainwithtighteningsafetyrequirementsandunforeseendelaysoccurringinadvancingthedeploymentofthistechnologyinVietNam.

4 “BCC Contract Signed for Billion Gas Pipeline Project,” PetroVietnam, March 11, 2010,http://english.pvn.vn/?portal=news&page=detail&category_id=11&id=3278.5WorldNuclearAssociation,www.world-nuclear.org/info/Country-Profiles/Countries-T-Z/Vietnam,October2015.

FINAL

IntelligentEnergySystems IESREF:5973 24

• LargeHydro.Around38%ofVietNam’selectricityiscurrentlygeneratedbyarangeoflargereservoirsandinsomecasescascadedhydropowerstationsthatare locatedthroughoutthecountry.Thelargestreservoirs,HoaBinhandSonLa,arelocatedinthenorthwestofthecountry,althoughtherearesignificantstorageslocatedinthecentralandsouthregionsaswell. VietNamisabletogainthebenefitsofdiversity inhydrologicalconditionsacrossmanyseparateriversystemswithnotablediversityininflowsacrossnorth,centralandsouthregions.However,VietNamhas largelyexploitedallof the large scalehydroconsideredtobeeconomicallyfeasible;furtherdevelopmentbeyondwhathasbeenexploitedtodateandwhatisunderconstructionnowisnotconsideredanoption.

• Small, mini, and micro hydro. Viet Nam has untapped small scale hydropotential. In recent years, there has been a lot of small hydropowerdevelopmentinVietNamwiththenumberofprojectsgoingfromabout141in2006(167MW)toabout156(622MW)by2009,andsome226projects(1635MW) by 2014. Some 1943MW of capacity is now under construction, andsome236projects (with total capacityof2019MW)under study. However,concerns have been raised on small hydro projects in the country based onconsiderations of the low levels of efficiency achieved from some projectsrelativetotheenvironmentalexternalities.

• Pumped storage hydro. Viet Nam does not presently have any pumpedstorage hydro plant in operation. However, feasibility studies have beencarriedoutandshowthatpumpedstoragepowerplantsmaybefeasiblewiththe south and central regions offering the most favourable geographicalconditions.

• Onshore and offshore wind. Viet Nam is considered to have moderate togood onshore wind energy potential, with the best locations in Viet NamrecordingreasonablewindspeedsthroughouttheyearexceptforthemonthsofApril,MayandSeptember.Mostoftheonshorewindpotentialisalongthecountry’ssouthcentralandcentralcoastalareas,andanumberoflocationsinthe mountainous areas in the central region. The greatest onshore windpotential that has been measured is in Binh Thuan province. A limitedamountofdataisreportedinrelationtooffshorewindpotentialinVietNam,however,itappearsthatVietNamhaspotentialforoffshorewindwithalittleunder half the sites having been tested being rated as ”good” or better foroffshore.

• Solar Energy. Viet Nam is considered to have very high potential for thedevelopment of solar energy resources. A number of studies have beenconductedtoassessthepotential,themostrecentanddetailedofwhichwasastudyentitled:“MapsofSolarResourceandPotentialinVietnam”,publishedinJanuary2015.ThiswasundertakenbytheMOITandaSpanishConsortiumconsisting of Centro de Investigaciones Energeticas Medioambientales yTecnológicas (CIEMOT), National Renewable Energy Centre (CENER) and

FINAL

IntelligentEnergySystems IESREF:5973 25

Instituto para la Diversificación y Ahorro de la Energía (IDAE). This broadlyshowsthatbasedonGHIandDNImeasurementsthereissubstantialpotentialfor solar photovoltaic deployment throughout the country, with the greatestpotential identifiedinthesoutheast,centralhighlands,MekongRiverDelta,allcoastalareasandthenortheast. ThestudyalsoconcludesthatbasedonDNImeasurements, there is substantial potential for concentrated solar power(CSP) based technologies, with the greatest potential in the central regions,highlandsandsoutheastofVietNam.

• Geothermal. Presently there are no geothermal power plants in Viet Nam.However,basedonsurveysandstudiescarriedoutoverthelastfewdecadesongeothermal energy resources, the country is recognised to have a limitedamountof geothermalpotentialwith some300MW to400MWhavingbeenidentifiedtodate.

• Bio Generation (Biomass and biogas). As an agricultural country, VietNamhas significant potential for power generation from biomass and biogassources.Typical forms includewoodenergy,cropwasteandresidues,animalwaste,urbanwasteandotherorganicwaste.SustainableexploitationcapacityofbiomassforenergyproductioninVietNamisestimatedatabout150milliontonsper year6,withoverall powergenerationpotential of around11-15GWfrombiomassand4-5GWfrombiogas.

• PowerImports.VietNamhasbeenactiveinpursuingopportunitiesforpowerimport from neighbouring countries. Since 2004 the country has importedpowerfromPRCandatdifferenttimestherehasbeendiscussionofincreasingpower imports fromPRC,althoughmore recently thisoptionseemsunlikely.VietNamhasbeeninvolvedinthejointdevelopmentofhydroprojectsinLaoPDRwhicharededicatedunder25yearPPAstosupplyingtheiroutputtoVietNam.TherehasbeendiscussionofsimilarprojectsinCambodiawithMOUsinplace for a number of hydro projects, although these are longer-termprospectsandarenotconsideredtobecommitted.

3.2 DomesticandImportedCoalResources

3.2.1 DomesticCoal

VietNamisacountrywithacomparativeadvantageinthecoalsectorwhichcomesfromthecountry’srelativelyabundantcoalreserves.ByJanuary2011,theresultsofinvestigationsindicatedthatVietNamhascoalreservesofaround48.7billiontons,ofwhich,some39.35billiontons,liebeneaththeRedRiverbasininanareaofsize2000 km2. The Northeast of Viet Nam possesses the second largest coal depositwithreservesestimatedtobearound8.83billiontons.TheNortheastisthelargestminingarea inthecountrybecause it iscurrentlynotfeasibletoexploitcoalfrom

6 http://ievn.com.vn/tin-tuc/Tong-quan-ve-hien-trang-va-xu-huong-cua-thi-truong-nang-luong-tai-tao-cua-Viet-Nam-5-999.aspx

FINAL

IntelligentEnergySystems IESREF:5973 26

the Red River basin, as deposits lie some 150-2,500 meters undergroundnecessitating large investmentandmodernminingtechnologies thatarecurrentlynot available in Viet Nam. In addition, the Red River deposit has complicatedhydrogeologicalfeaturesandislocatedinapopulousarea.AssuchcoalproductionismainlycarriedoutintheNortheastofthecountry.

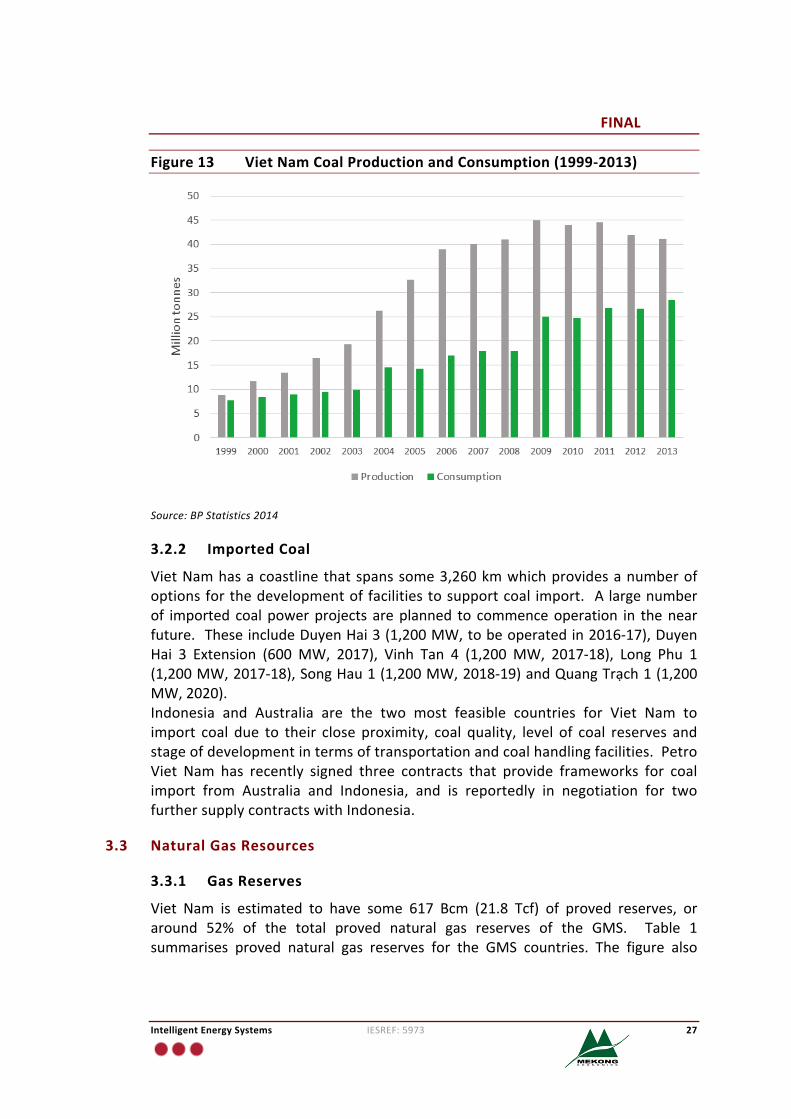

As of 2012, Viet Nam is the 17th coal producer in the world. Figure 13 providesstatisticsoncoalproductionandcoalconsumption. It indicatescoalproduction inVietNamhasincreasedrapidlyfrom11.6Mt/yin2001to44.5Mt/yin2011.Thelarge increase in production is duemainly to increases in coal exports, althoughdomesticconsumptionhasalsoincreasedsignificantlyfrom2009,driveninpartbythe commissioningof coal plants in thenorth. Coal reserves fromVietNamhavealmostentirelybeenproduced inthe formofanthracite,sourcedfromVinacominminesandusedinindustry,theelectricitysector,andsoldasexports.

VietNamNationalCoalMineralIndustriesHoldingCorporationLimited(Vinacomin)isthemajorcoalproducerinVietNam,accountingfor95%ofthenation’stotalcoalproduction.Thecorporationhas5bigopen-castmineswiththecapacityofover2milliontons/year,15otheropen-castmineswiththecapacityof100-700thousandtons/yearandsomewiththecapacityoflessthan100thousandtons/year.

Coaldemand isexpected togrowataround5.3%annually,duemainly togreateranticipateduseintheelectricitygenerationsector.ItisexpectedthatcoalexportswillreduceasMOITintroducespoliciesforutilisingVietNam’scoalproductionforinternal consumptiononly. A furtherextensionof thispolicycouldoccur ifMOITrecommends that the country stops exporting coal, in order to secure additionalsupplies fordomesticuse intheelectricitygeneration industry. BusinessasUsualprojections for 2030 suggest coal supply reaching some 65million tonswith coaldemandbeingaround110to150milliontons.UnderBusinessasUsualprojectionsVietNamwillneedtoimportcoalfrom2017withimportvolumesneedingtorisetomakeupexpectedshortfallsindomesticsupply.

Domesticcoalprices for theelectricitysectorhavebeenregulatedandsubsidisedbutcoalpricinghasbeenslowlyfreedtothepointwherethedomesticcoalpricesfor power generation purposes will in the shorter-term be similar to prices ofimportedcoal.

FINAL

IntelligentEnergySystems IESREF:5973 27

Figure13 VietNamCoalProductionandConsumption(1999-2013)

Source:BPStatistics2014

3.2.2 ImportedCoal

VietNamhasacoastlinethatspanssome3,260kmwhichprovidesanumberofoptionsforthedevelopmentoffacilitiestosupportcoal import. Alargenumberof imported coalpowerprojects areplanned to commenceoperation in thenearfuture.TheseincludeDuyenHai3(1,200MW,tobeoperatedin2016-17),DuyenHai 3 Extension (600 MW, 2017), Vinh Tan 4 (1,200 MW, 2017-18), Long Phu 1(1,200MW,2017-18),SongHau1(1,200MW,2018-19)andQuangTrạch1(1,200MW,2020).Indonesia and Australia are the two most feasible countries for Viet Nam toimport coal due to their close proximity, coal quality, level of coal reserves andstageofdevelopmentintermsoftransportationandcoalhandlingfacilities.PetroViet Nam has recently signed three contracts that provide frameworks for coalimport from Australia and Indonesia, and is reportedly in negotiation for twofurthersupplycontractswithIndonesia.

3.3 NaturalGasResources

3.3.1 GasReserves

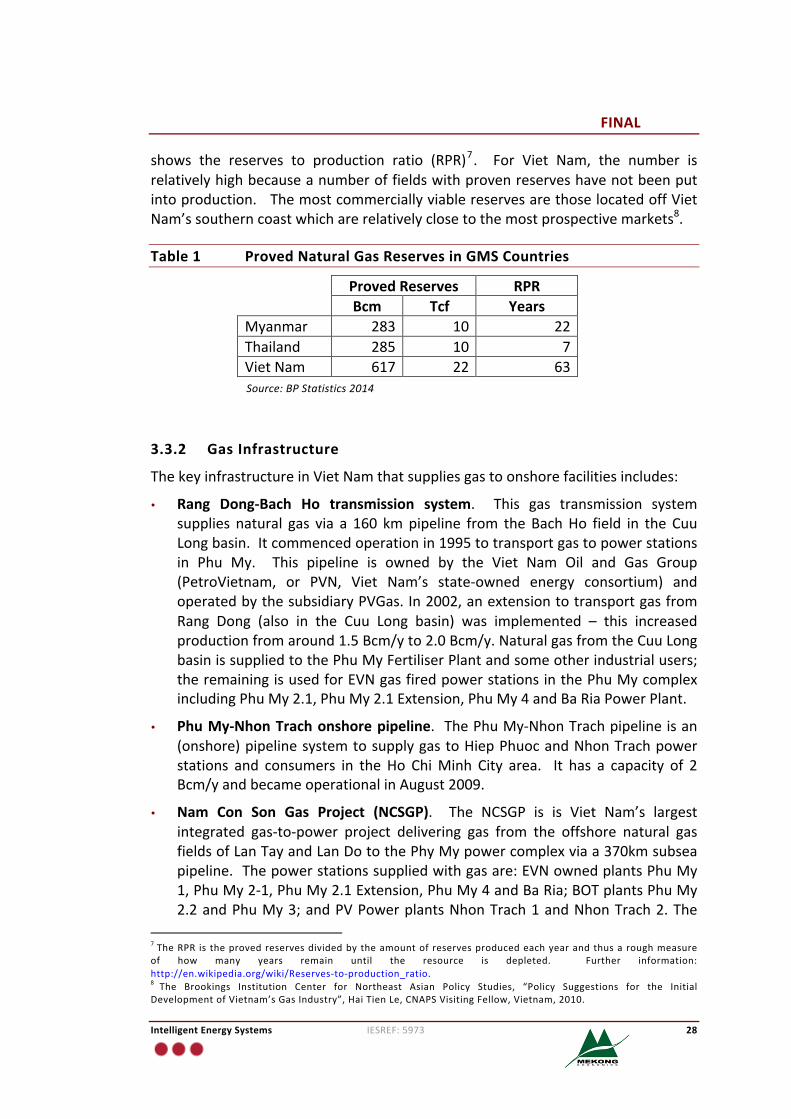

Viet Nam is estimated to have some 617 Bcm (21.8 Tcf) of proved reserves, oraround 52% of the total proved natural gas reserves of the GMS. Table 1summarises proved natural gas reserves for the GMS countries. The figure also

FINAL

IntelligentEnergySystems IESREF:5973 28

shows the reserves to production ratio (RPR)7. For Viet Nam, the number isrelativelyhighbecauseanumberoffieldswithprovenreserveshavenotbeenputintoproduction.ThemostcommerciallyviablereservesarethoselocatedoffVietNam’ssoutherncoastwhicharerelativelyclosetothemostprospectivemarkets8.

Table1 ProvedNaturalGasReservesinGMSCountries

ProvedReserves RPRBcm Tcf Years

Myanmar 283 10 22Thailand 285 10 7VietNam 617 22 63Source:BPStatistics2014

3.3.2 GasInfrastructure

ThekeyinfrastructureinVietNamthatsuppliesgastoonshorefacilitiesincludes:

• Rang Dong-Bach Ho transmission system. This gas transmission systemsupplies natural gas via a 160 kmpipeline from the BachHo field in the CuuLongbasin.Itcommencedoperationin1995totransportgastopowerstationsin Phu My. This pipeline is owned by the Viet Nam Oil and Gas Group(PetroVietnam, or PVN, Viet Nam’s state-owned energy consortium) andoperatedbythesubsidiaryPVGas.In2002,anextensiontotransportgasfromRang Dong (also in the Cuu Long basin) was implemented – this increasedproductionfromaround1.5Bcm/yto2.0Bcm/y.NaturalgasfromtheCuuLongbasinissuppliedtothePhuMyFertiliserPlantandsomeotherindustrialusers;theremainingisusedforEVNgasfiredpowerstationsinthePhuMycomplexincludingPhuMy2.1,PhuMy2.1Extension,PhuMy4andBaRiaPowerPlant.

• PhuMy-NhonTrachonshorepipeline. ThePhuMy-NhonTrachpipelineisan(onshore)pipelinesystemtosupplygastoHiepPhuocandNhonTrachpowerstations and consumers in the Ho ChiMinh City area. It has a capacity of 2Bcm/yandbecameoperationalinAugust2009.

• Nam Con Son Gas Project (NCSGP). The NCSGP is is Viet Nam’s largestintegrated gas-to-power project delivering gas from the offshore natural gasfieldsofLanTayandLanDotothePhyMypowercomplexviaa370kmsubseapipeline.Thepowerstationssuppliedwithgasare:EVNownedplantsPhuMy1,PhuMy2-1,PhuMy2.1Extension,PhuMy4andBaRia;BOTplantsPhuMy2.2andPhuMy3;andPVPowerplantsNhonTrach1andNhonTrach2.The

7TheRPR istheprovedreservesdividedbytheamountofreservesproducedeachyearandthusaroughmeasureof how many years remain until the resource is depleted. Further information:http://en.wikipedia.org/wiki/Reserves-to-production_ratio.8 The Brookings Institution Center for Northeast Asian Policy Studies, “Policy Suggestions for the InitialDevelopmentofVietnam’sGasIndustry”,HaiTienLe,CNAPSVisitingFellow,Vietnam,2010.

FINAL

IntelligentEnergySystems IESREF:5973 29

LanTay/LanDofieldsreportedlyholdsome2Tcfofgasreserveswithoutputfrom the field said to be some 530mmcf/d (193Bcf/y). The project startedoperation in 2003. The project is operated by a consortium comprisingPetroVietnam(51%),BP(32.67%)andConocoPhilips(16.33%).BPoperatedthepipelinefromitsestablishment in2003until2008,when itwastransferredtoPVN. In the future, this pipelinemay be used to transport natural gas fromotherfieldswithintheNamConSonbasinonshore;andtosupplygastousersinPhuMy,DongNai,andHoChiMinhCity.

• PM3-Ca Mau pipeline9 . Commissioned in 2007, the PM3-Ca Mau pipelinesupplies gas from thePM3 /Block46 fields to the1,500MWCaMaupowercomplex.ThepipelinewascompletedunderthePM3CommercialArrangementArea(CAA)atthesoutherntipofVietNamandnationalproductionsurpassedBcmwith the transportation of natural gas fromBlock PM3 CAA and the CaiNuoc field – an offshore area administered jointly with Malaysia. Gas istransported to theCaMau1and2power stations,which consumearound2Bcmperyear.IntheCaMaugasdistributionstation,thereisafuturetie-infortheCaMaufertilizerplantwhichconsumesaround500MMCMofgasperyear,as well as other users in Ca Mau province. The pipeline system is fundedcompletely by PVN; PVGas operates this pipeline system on behalf ofPetroVietnam.

3.3.3 PastProductionandConsumption

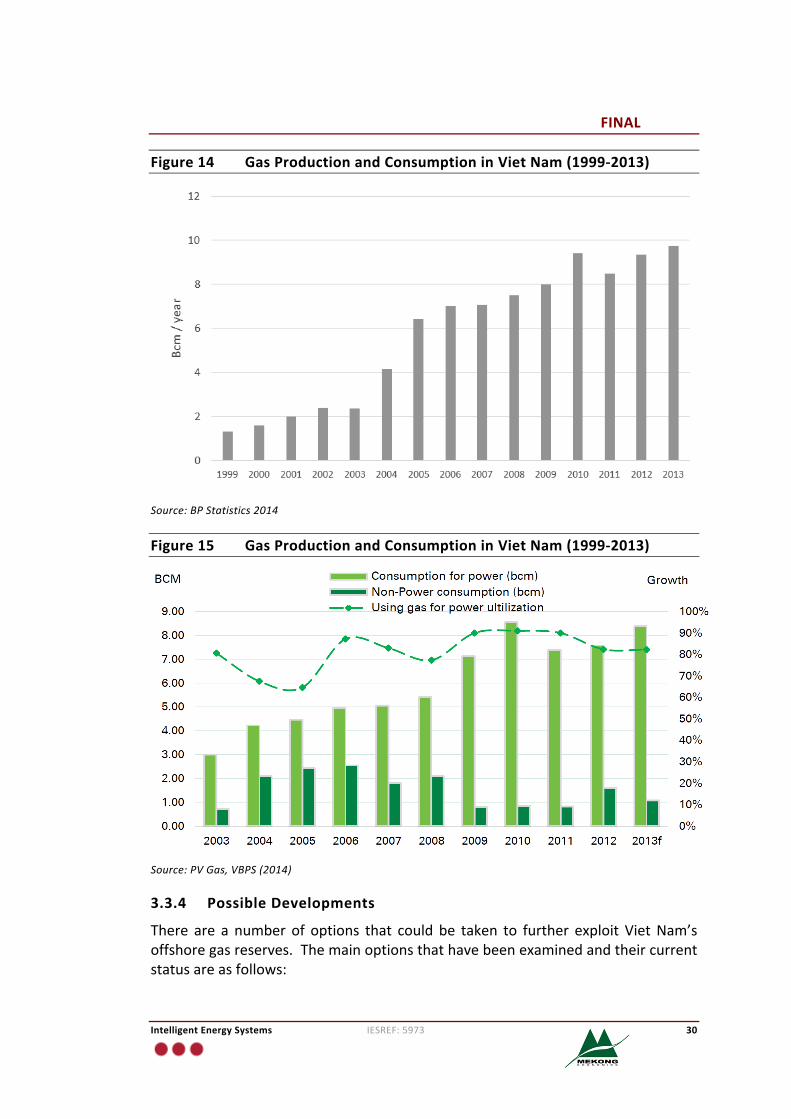

Being a coastal country, Viet Nam has several hundred thousand squarekilometresofcontinentalshelfinwhichseventertiarybasinshavebeenidentified.Gasreserveshavebeenfoundinfiveofthesevenoffshorebasins:SongHong,PhuKhanh,NamConSon,CuuLongandMalay-ThoChu.Figure14showsthetrendingasproductioninVietNam(allgasproducedisconsumedwithinVietNam).Gasproductionisobservedtohaverampedupsince2003andagainin2007coincidingwiththecommissioningoftheNamConSonGasProjectandtheCaMaupipelinedevelopments.

Figure 15 shows the gas consumption trend for the period 1999 to 2013 asreportedbyPVGasin2014.Around85%ofnaturalgasconsumptionisattributableto power generation, 10% for fertilizer production, and the rest provided to lowpressuregasnetworksorasLPGtoindustrialconsumers.Currentgassupplyisonlysatisfying 60% of the demand for gas for VietNam’s power demand, 30% of thedemandforfertilizerfeedstocksand60%ofthedemandforLPG10.

9 The Brookings Institution Center for Northeast Asian Policy Studies, “Policy Suggestions for the InitialDevelopmentofVietnam’sGasIndustry”,HaiTienLe,CNAPSVisitingFellow,Vietnam,2010.10Around half of Vietnam’s LPG demand is satisfied by domestic production, with the remainder imported fromChina,Australia,UnitedArabEmiratesandothers.

FINAL

IntelligentEnergySystems IESREF:5973 30

Figure14 GasProductionandConsumptioninVietNam(1999-2013)

Source:BPStatistics2014

Figure15 GasProductionandConsumptioninVietNam(1999-2013)

Source:PVGas,VBPS(2014)

3.3.4 PossibleDevelopments

There are a number of options that could be taken to further exploit VietNam’soffshoregasreserves.Themainoptionsthathavebeenexaminedandtheircurrentstatusareasfollows:

FINAL

IntelligentEnergySystems IESREF:5973 31

• FurtherDevelopmentof the South-WestRegion. Therehasbeenpromisingexploration of South West offshore Block B, 52/97, 48/95, in the pastconsiderationwasgiventodevelopingapipelinetobebuiltfromthesefieldstosupplytheplannedOMonComplexandbackfilltheCaMauComplex.Thiswouldhaveinvolvedtheconstructionofa500kmpipelinetoOMonintheCanTho province. However, in 2014 these plans were abandoned by fielddeveloper, PetroVietnam and Chevron citing an inability to agree on gasofftake prices and development plans. This ended with PetroVietnampurchasing Chevon’s stake in the field and pursuing other joint venturepartners.

• Developments in the North-East Region. Some offshore oil and gas fieldshavebeenidentifiedoffthenortheastcoastline,althoughextensivesurveyingandexplorationoftheregionisstillongoing.Investmentintheinfrastructurenecessary tosupportdevelopmentofoffshoregaspipelines isunderstoodtonot presently be viable, but in the future, if energy supplies to Viet Namremaintight,gasinthisregionmaybedeveloped.

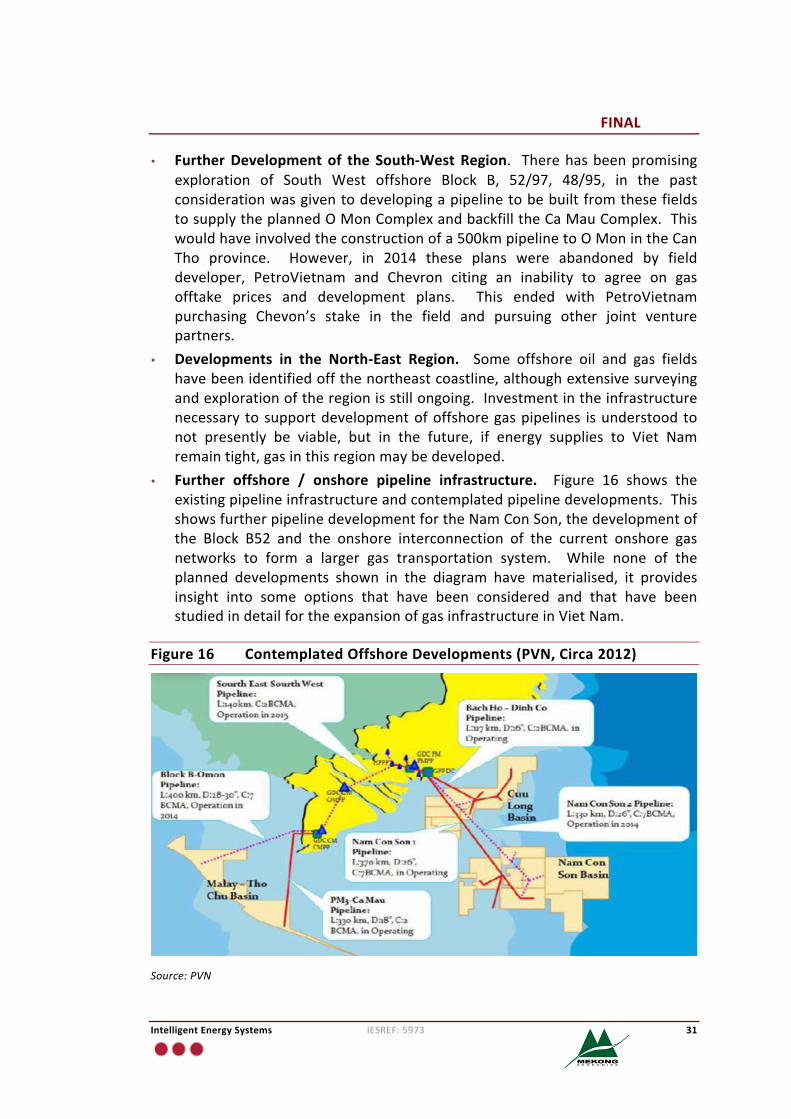

• Further offshore / onshore pipeline infrastructure. Figure 16 shows theexistingpipelineinfrastructureandcontemplatedpipelinedevelopments.ThisshowsfurtherpipelinedevelopmentfortheNamConSon,thedevelopmentofthe Block B52 and the onshore interconnection of the current onshore gasnetworks to form a larger gas transportation system. While none of theplanned developments shown in the diagram have materialised, it providesinsight into some options that have been considered and that have beenstudiedindetailfortheexpansionofgasinfrastructureinVietNam.

Figure16 ContemplatedOffshoreDevelopments(PVN,Circa2012)

Source:PVN

FINAL

IntelligentEnergySystems IESREF:5973 32

3.3.5 LNGImport

ThemostrecentGasDevelopmentPlanandPowerDevelopmentPlan7(PDP7)tohave been approved by the government include plans for an LNG regasificationterminalsited inSonMy inthecentralprovinceofBinhThuan(nearHoChiMinhCity)withacapacityof3MTPA,withanoption todoubleor triple its capacityasneeded. However, thedevelopmentof theLNGterminalhasbeendelayedand itseemsunlikelythatVietNamwoulddevelopanLNGimportterminalbefore2020.MostlikelyLNGimportsourceswouldbeAustraliaandQatargiventheproductioncapabilityofthesecountries.

ApartfromanLNGterminalbeingsituationinBinhThuanprovince,otherlocationsthathavebeenconsideredinclude:LachNguyeninHaiPhong,MyGianginKhanhHoaprovince,andaterminalinCaMautosupportbackfillingtheCaMaucomplex.

3.4 NuclearPower

In January2006, thePrimeMinister ofVietNam signeddecisionNo.01-2006-QD-TTgontheapprovalofthestrategytoapplynuclearenergyforpeacefulpurposesby 2020. The intent is to build and develop a nuclear technology industry. Thestrategy in place envisaged the commencement of the first nuclear power plantprojectinVietNamby2020.

In2009,theNationalAssemblydecidedthefirstnuclearpowerplantof2,000MWcapacity would be built in the Ninh Thuan province. The investigation andconstructionworkhas since thenbegunbut the expected commencementof theplant’s operationwas pushed back until 2024 due to additional unforeseenworkcomponents and tightened safety requirements as part of the fallout from theFukushima crisis. The second plant, Ninh Thuan 2, has been scheduled to beconstructedinthesamelocationandoperatingfrom2025.

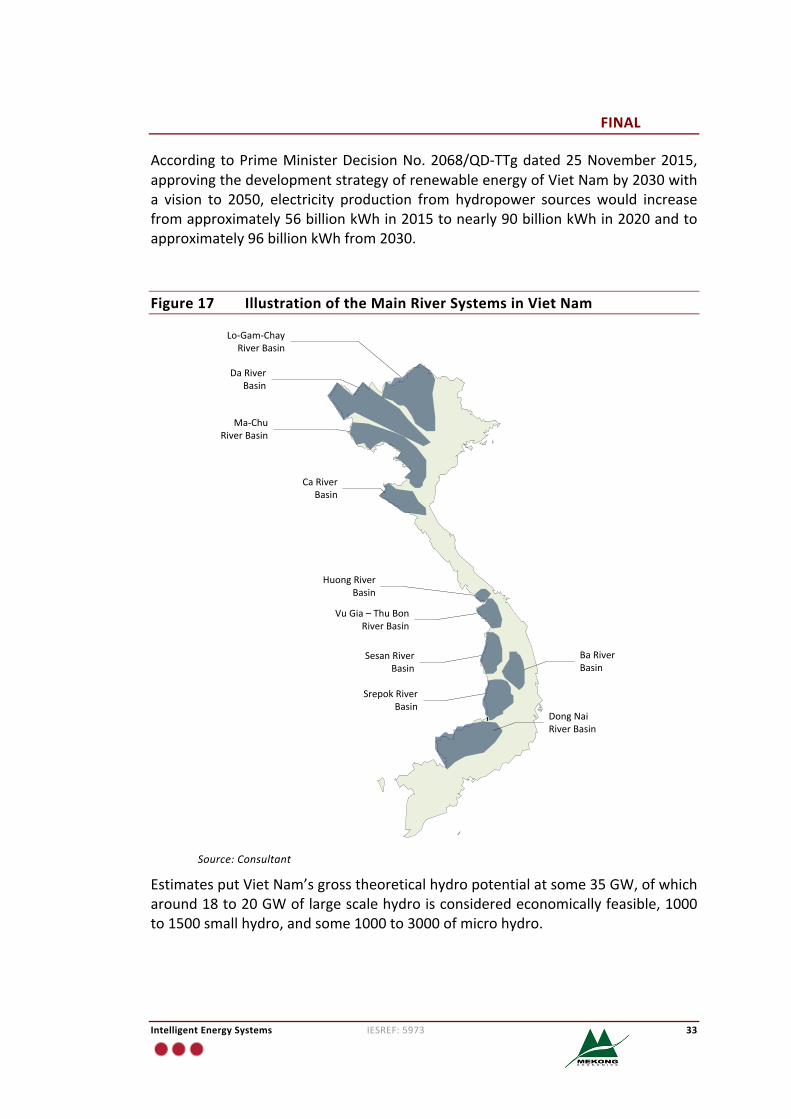

3.5 HydroPower

VietNamhas high potential for hydro power. The country has some2,360 riversandstreamsofthatexceed10km.ThemainriversystemsareillustratedinFigure17. The Red River system in the north comprises theDa and Lo-Gam-Chay riverbasins,theMekongriverdeltaisinthesouth.Inthecentralregion,therearemanyriverbasins,includingtheMaRiver,CaRiverinthenorthcentralarea,VuGia–ThuBon River in the central area, Sesan River and Srepok Rivers are in the centralhighlandsandtheBaRiverisinthecoastalarea.TheDongNaiRiverbasinisinthesouth.

In 2013, hydro power accounted for 47.5% of the country’s total 30,473 MWinstalled generating capacity. In 2014, hydropowerproductionwas59,479millionkWh, accounting for 41.41% total electricity supply. Currently, the Son Lahydropowerplantisthelargestpowerplantwith2,400MWinstalledcapacity.

FINAL

IntelligentEnergySystems IESREF:5973 33

According toPrimeMinisterDecisionNo.2068/QD-TTgdated25November2015,approvingthedevelopmentstrategyofrenewableenergyofVietNamby2030witha vision to 2050, electricity production from hydropower sourceswould increasefromapproximately56billionkWhin2015tonearly90billionkWhin2020andtoapproximately96billionkWhfrom2030.

Figure17 IllustrationoftheMainRiverSystemsinVietNam

Source:Consultant

EstimatesputVietNam’sgrosstheoreticalhydropotentialatsome35GW,ofwhicharound18to20GWoflargescalehydroisconsideredeconomicallyfeasible,1000to1500smallhydro,andsome1000to3000ofmicrohydro.

Lo-Gam-ChayRiverBasin

DaRiverBasin

Ma-ChuRiverBasin

CaRiverBasin

HuongRiverBasin

VuGia–ThuBonRiverBasin

SesanRiverBasin

SrepokRiverBasin

BaRiverBasin

DongNaiRiverBasin

FINAL

IntelligentEnergySystems IESREF:5973 34

3.5.1 LargeScaleHydro

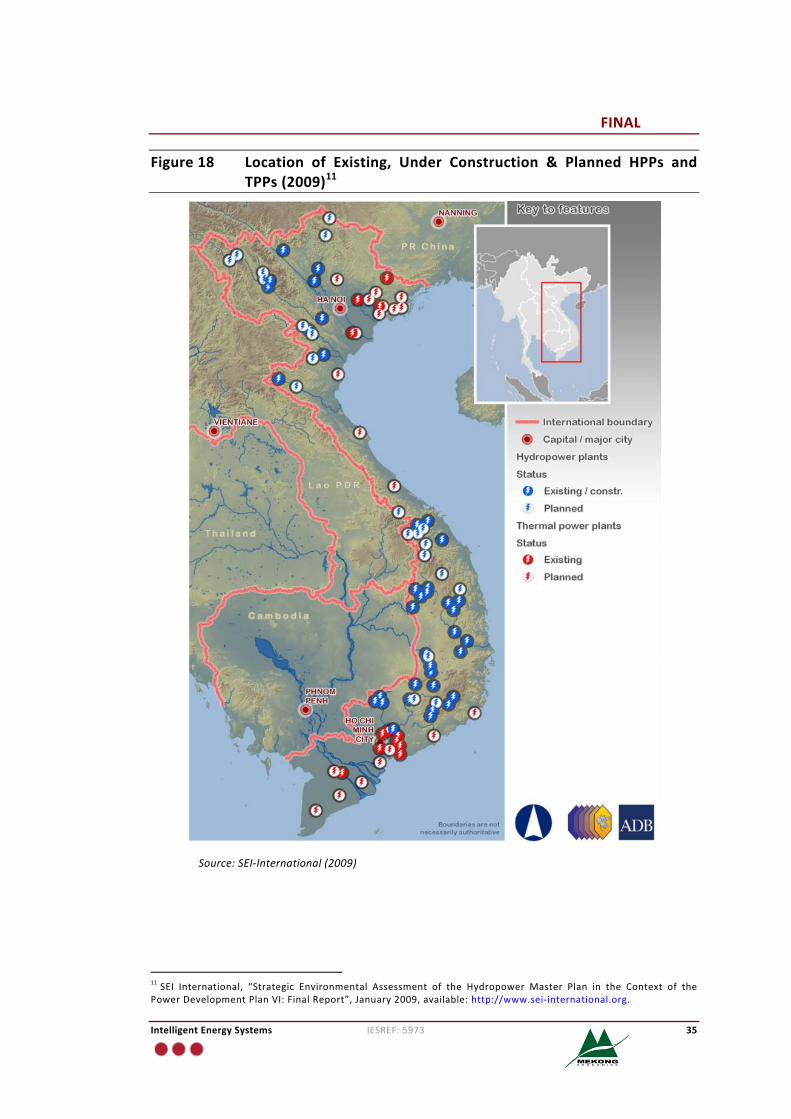

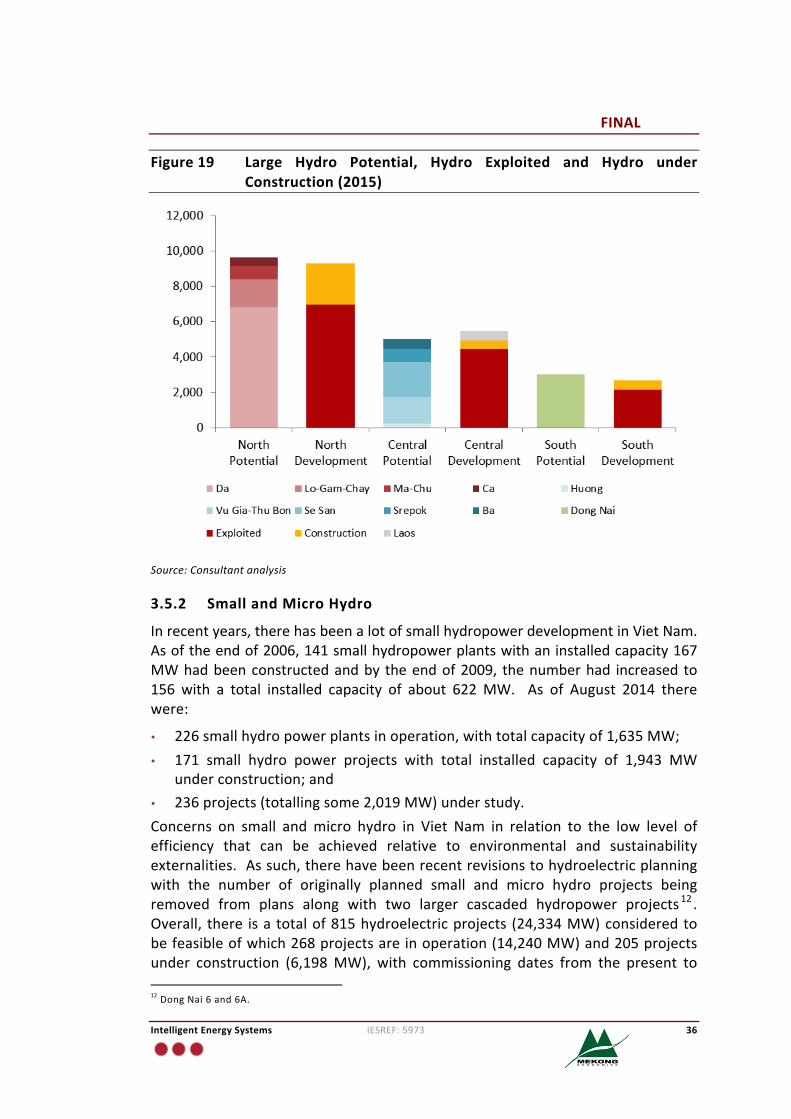

Mosthydroelectricreserveswithcapacityinexcessof50MWhavebeenexploitedinVietNamorareunderdevelopment.Figure18providesabasicoverviewofthelocation of existing and planned hydro developments in Viet Nam. A chart tocomparethepotentials(forlargescalehydro)comparedwithhydrocapacitythathas been developed or that is under construction is shown in Figure 19. Thisillustrates quite clearly that all large scale hydro potential in Viet Nam isessentially exploited and in the case of the central region there has beenexploitation of hydro power potential in neighbouring Laos. Thus future hydrodevelopmentis likelytobedrivenbytwoforms:(1) importsfromhydroprojectsdevelopedinneighbouringcountries,and(2)smallhydroelectricplantsdevelopedinthemoreremoteregions.

FINAL

IntelligentEnergySystems IESREF:5973 35

Figure18 Location of Existing, Under Construction & Planned HPPs andTPPs(2009)11

Source:SEI-International(2009)

11SEI International, “Strategic Environmental Assessment of the Hydropower Master Plan in the Context of thePowerDevelopmentPlanVI:FinalReport”,January2009,available:http://www.sei-international.org.

FINAL

IntelligentEnergySystems IESREF:5973 36

Figure19 Large Hydro Potential, Hydro Exploited and Hydro underConstruction(2015)

Source:Consultantanalysis

3.5.2 SmallandMicroHydro

Inrecentyears,therehasbeenalotofsmallhydropowerdevelopmentinVietNam.Asoftheendof2006,141smallhydropowerplantswithaninstalledcapacity167MWhadbeenconstructedandby theendof2009, thenumberhad increased to156 with a total installed capacity of about 622MW. As of August 2014 therewere:

• 226smallhydropowerplantsinoperation,withtotalcapacityof1,635MW;• 171 small hydro power projects with total installed capacity of 1,943 MW

underconstruction;and• 236projects(totallingsome2,019MW)understudy.Concerns on small andmicro hydro in Viet Nam in relation to the low level ofefficiency that can be achieved relative to environmental and sustainabilityexternalities.Assuch,therehavebeenrecentrevisionstohydroelectricplanningwith the number of originally planned small and micro hydro projects beingremoved from plans along with two larger cascaded hydropower projects 12 .Overall, there isatotalof815hydroelectricprojects (24,334MW)consideredtobefeasibleofwhich268projectsareinoperation(14,240MW)and205projectsunder construction (6,198MW), with commissioning dates from the present to12DongNai6and6A.

FINAL

IntelligentEnergySystems IESREF:5973 37

2017.

3.5.3 PumpedStorageHydro

VietNamdoesnotpresentlyhaveanypumpedstoragehydroplant inoperation.However,feasibilitystudieshavebeencarriedoutandshowthatpumpedstoragepowerplantsmaybefeasiblewiththesouthandcentralregionsofferingthemostfavourable geographical conditions. Pumped storagehydroplants do feature ingovernmentplansfortheelectricityindustry.TheNationalMasterPlanforpowerdevelopmentforthe2011-2020periodwiththe vision to 2030 has included five pumped storage hydro plants to beconstructed between 2019 and 2030. These projects include Bac Ai 1 (4 x 300MW),DongPhuYen(4x300MW),DonDuong(4x300MW),NinhSon(4x300MW)andaPumpedStorageHydroplantintheNorth(3x300MW).According to the latest Prime Minister’s Decision No. 2068/QD-TTg dated 25November2015,approvingthedevelopmentstrategyofrenewableenergyofVietNamby2030withavisionto2050,pumpstoragehydroinstalledcapacityshouldtarget2,400MWby2030to8,000MWby2050.

3.6 WindPower

Viet Nam is considered to have moderate to good wind energy potential.However, likemany other developing countries, the potential ofwind power inViet Nam has not yet been quantified in detail. In 2011, the World Banksupported theMinistry of Industry and Trade to reconstruct theWindResourceAtlasofVietNam.Basedon this study, theyestimateda totalof10,000MWofonshore wind capacity could be theoretically exploited at surfaces with 80 mheightandwithwindspeedsover6m/s.

However, more recent studies have indicated that onshore wind potential inVietnam is considerably higher,with estimates as high as almost 27 GWMW13.According to the latest Prime Minister’s Decision No. 2068/QD-TTg dated 25November2015,approvingthedevelopmentstrategyofrenewableenergyofVietNamby2030withavisionto2050,totalelectricityproductionfromwindpowerwouldincreasefrom180millionkWhin2015toabout2.5billionkWhin2020(1%share),approximately16billionkWh in2030 (2.7%)andabout53billionkWh in2050(5%).

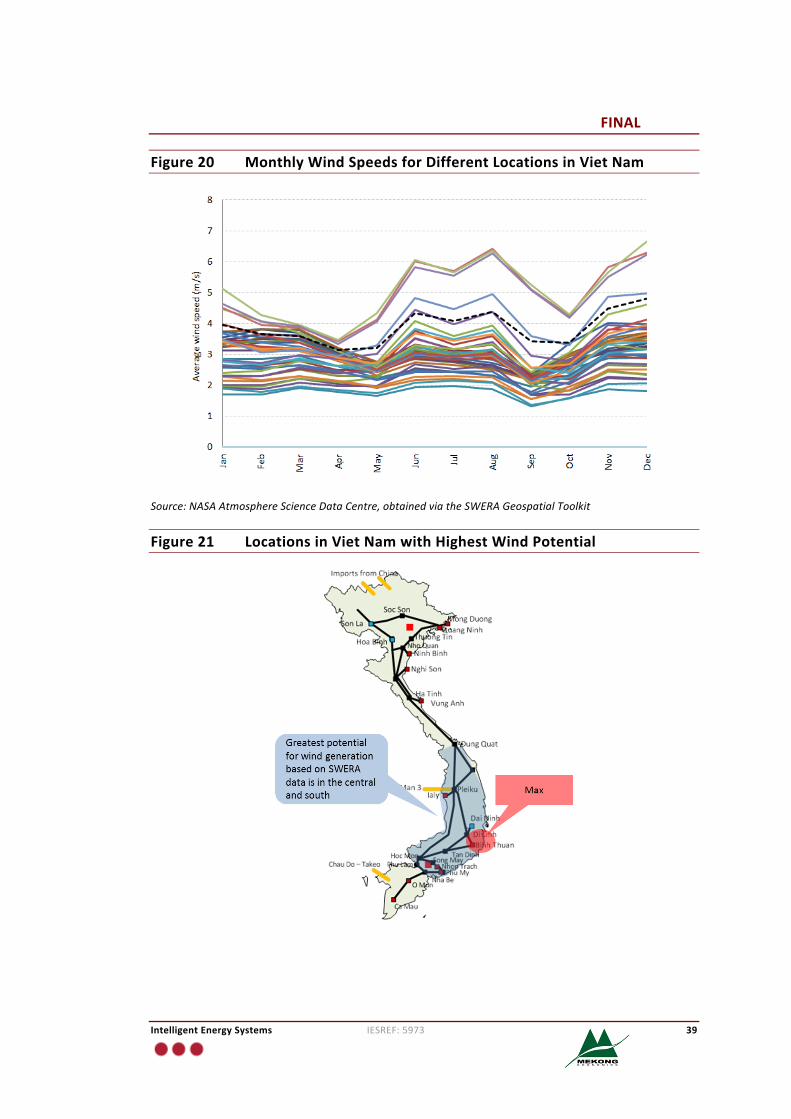

Figure20showsmonthlywindspeedmeasurementsforallregionsinVietNamasreportedbyNASAAtmosphereScienceDataCentreofeachregioninVietNamwiththedashedlinerepresentingtheaveragespeedofthetop7squareprofiles(above5.2m/s).ThisgraphshowsthatmanylocationsinVietNamrecordreasonablewindspeeds throughout the year except for April, May and September. When theselocationsareshadedoverthemapofVietNam,asillustratedinFigure21,wecan

13Forexample:26,673MWissuggestedbyADB(2015)

FINAL

IntelligentEnergySystems IESREF:5973 38

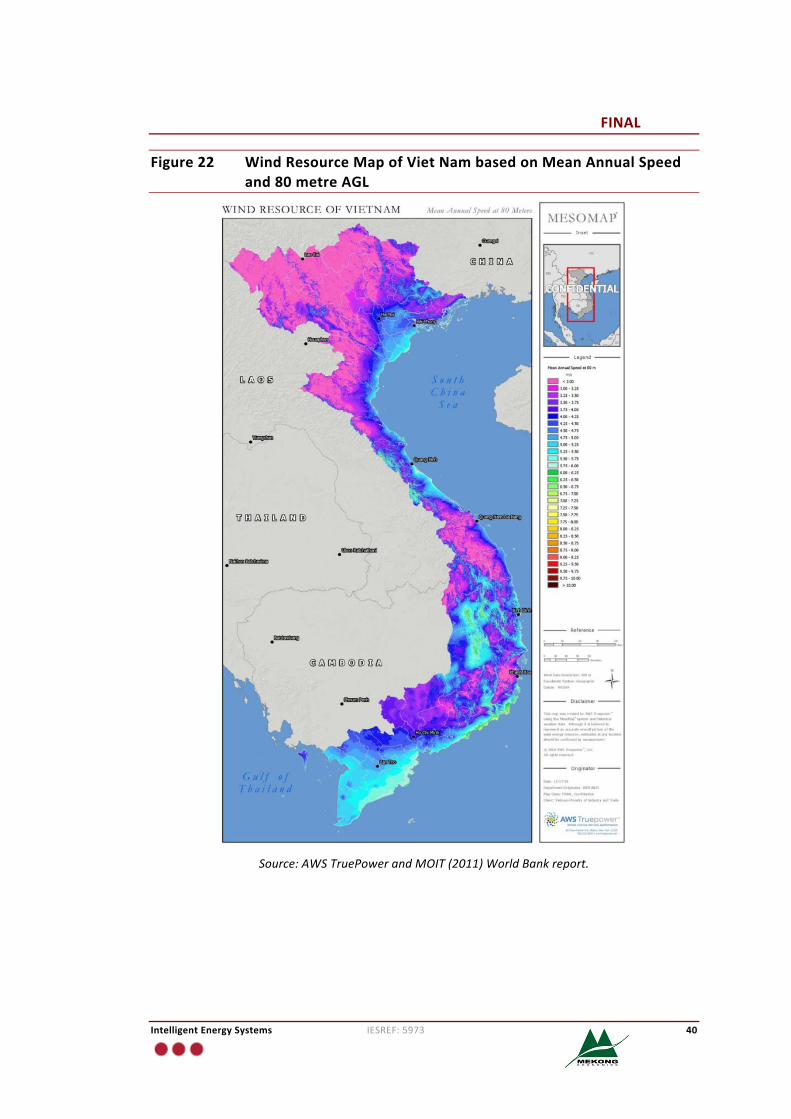

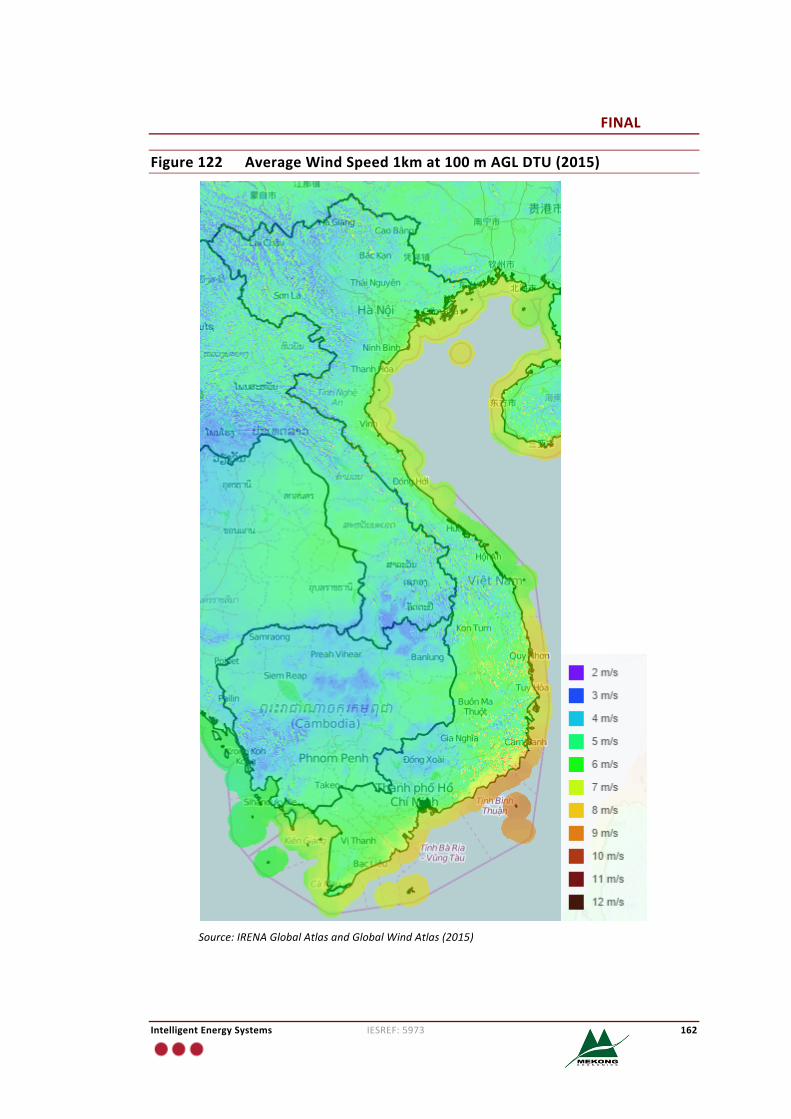

seethatinthemainthelocationsarealongthecountry’ssouthcentralandcentralcoastal areas. Figure 22 plots awind resourcemap from the AWS TrueEnergy /MOITandWorldBankstudyconductedin2011forheightsof80metres.ThisalsoprovidesfurtherindicationofthelocationsforthebestwindpowerpotentialinVietNamandhighlightstheareasofthecountry(coastalandmountainousparts)wherewind speeds are in excess of 6m/s. The greatest wind potential that has beenmeasuredisinBinhThuanprovince.

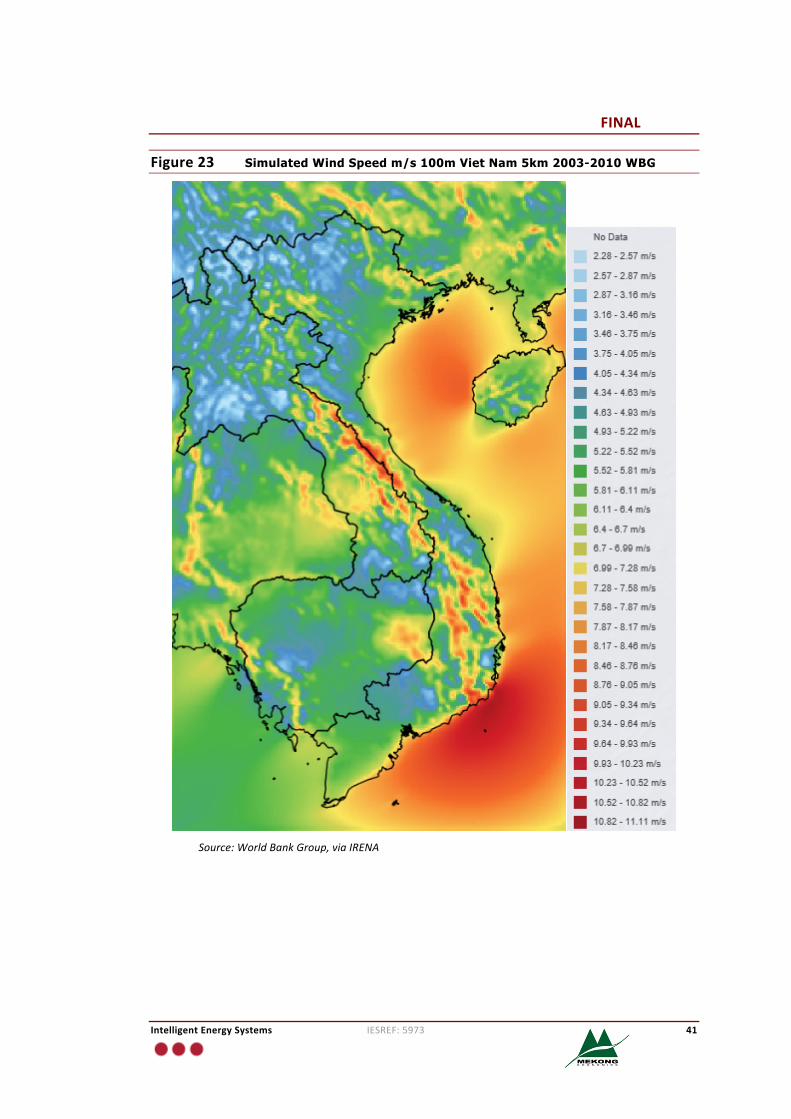

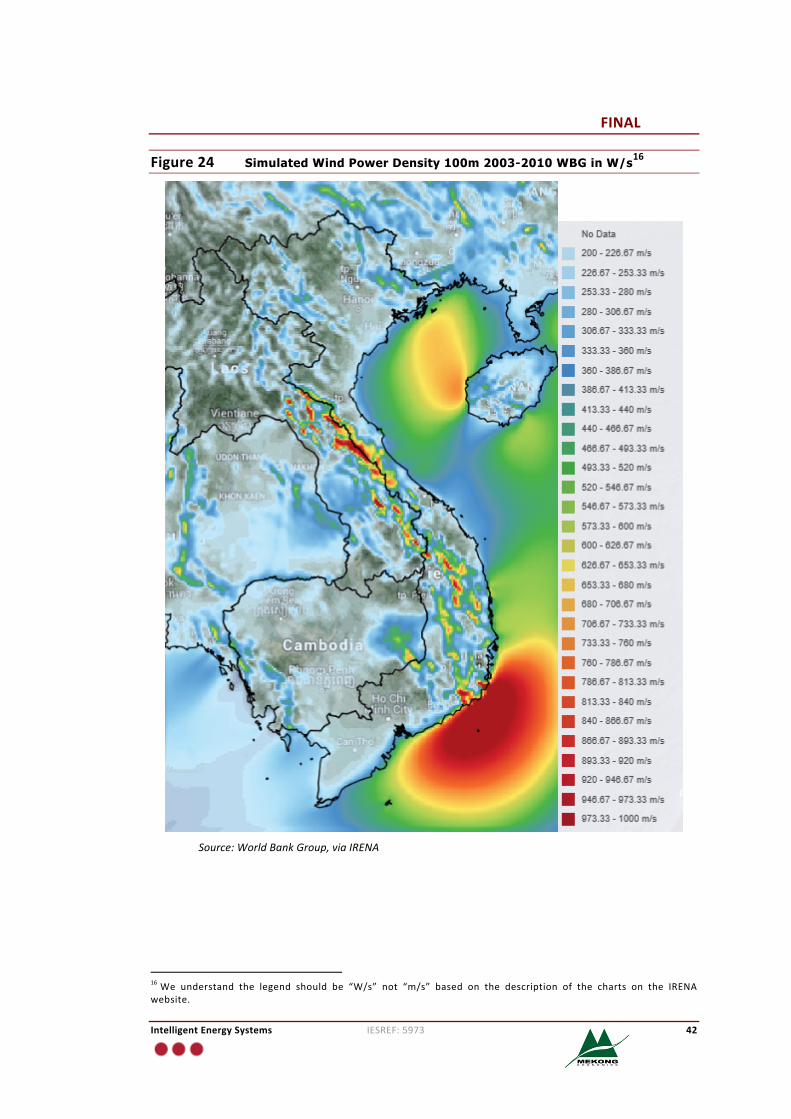

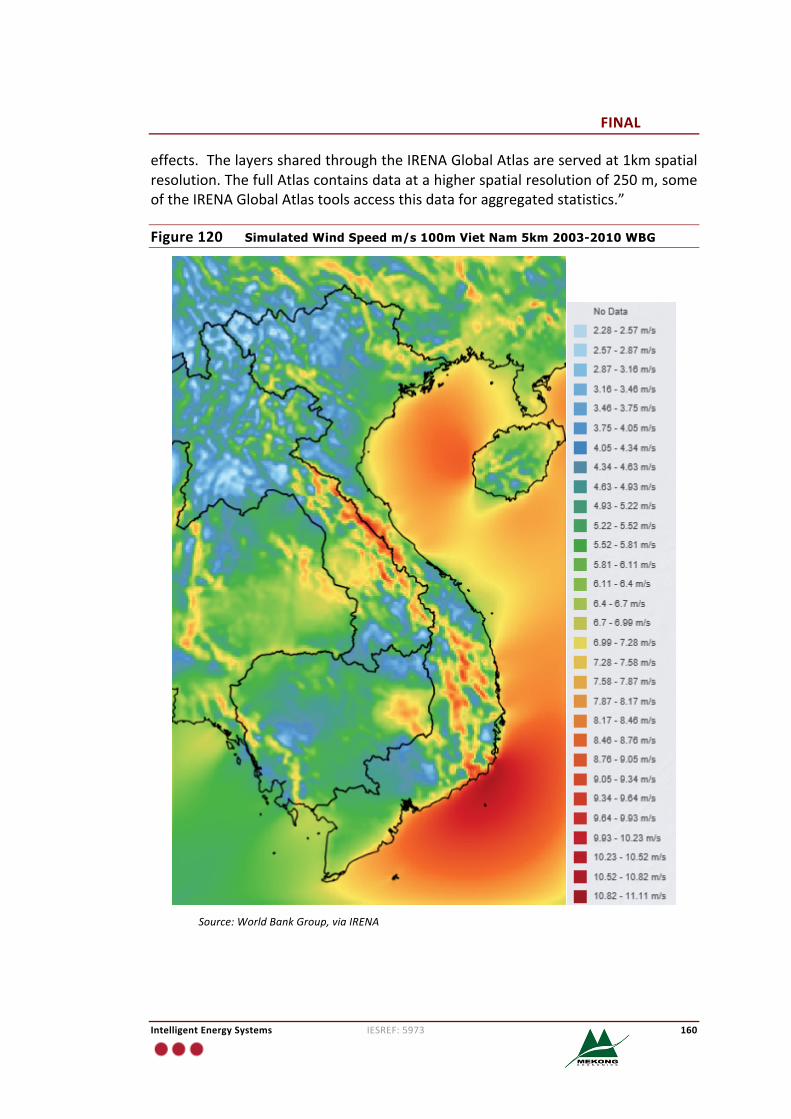

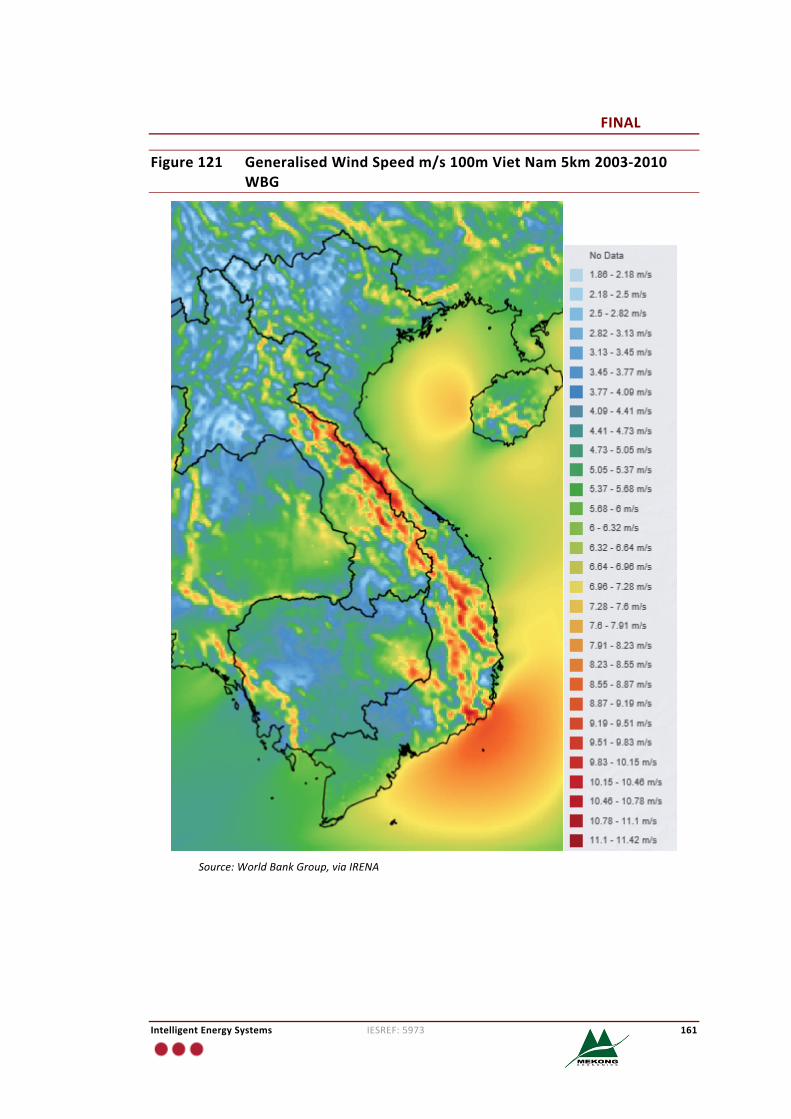

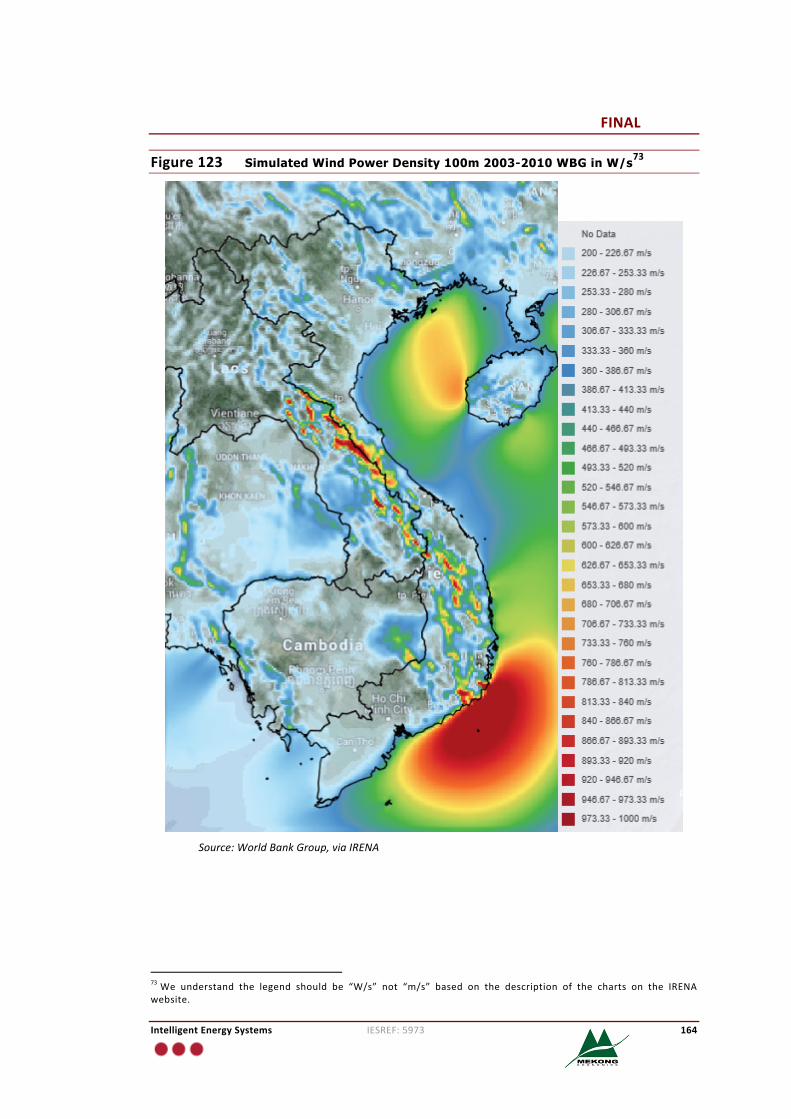

Further insight into geographical dispersion of wind power in Viet Nam can beassessedbasedonhighresolutionmapsofsimulatedwindpotentialaspresentedinFigure23andthecorrespondingwindpowerdensityinFigure24.Thefirstpresentssimulated wind speeds based on a set of measurements at 100m above groundlevel takenover2003-10andthesecondshowsthecorrespondingpowerdensity.These were based on information sourced from IRENA’s website 14 . Furtherinformationandadditionalplotsareprovided inAppendixD. Thechartsarewellcorrelated with the other sources we have plotted and show that there issubstantialoffshorewindpotentialalongthesouthcoastofthecountry.

Different reportshave indicated that since2007VietNamhasplannedup to50windpowerprojects.However,manyof theseprojectshavenotprogresseddueto various difficulties and barriers. Amajority of the previously registeredwindfarms have no plan for construction or had the permit revoked due to delay inimplementation. According to MOIT data, the country currently has only threeprojects in operation with combined capacity of 52 MW. The first projectgeneratingelectricitytothegridfrom2012isTuyPhongwindfarm,developedbyRenewableEnergyofVietNamJointStockCompany(REVN)inBinhThuandistrict.Theexisting capacity is 30MW,whichwill beexpanded to120MW in thenextstage. The otherwind farms include a 100MW (62 [email protected])project located inaMekongDeltaprovinceofBac Lieu (inoperation since2013andscaledupovertimeto100MWby2016),anda6MWoff-gridprojectinPhuQuyIsland,alsoofBinhThuanprovince.

A limitedamountofdata is reportedby InstituteofEnergy inrelationtooffshorewind resources at a height of 10m for 11 islands and at a height of 60m for twoislands. The information is limited,but itappearsthatVietNamhaspotential foroffshorewindwith a little underhalf the siteshavingbeen testedbeing rated as”good”orbetterforoffshore.

14Referto:http://irena.masdar.ac.ae/.15Source:http://www.power-technology.com/projects/bac-lieu-offshore-wind-farm/.

FINAL

IntelligentEnergySystems IESREF:5973 39

Figure20 MonthlyWindSpeedsforDifferentLocationsinVietNam

Source:NASAAtmosphereScienceDataCentre,obtainedviatheSWERAGeospatialToolkit

Figure21 LocationsinVietNamwithHighestWindPotential

FINAL

IntelligentEnergySystems IESREF:5973 40

Figure22 WindResourceMapofVietNambasedonMeanAnnualSpeedand80metreAGL

Source:AWSTruePowerandMOIT(2011)WorldBankreport.

FINAL

IntelligentEnergySystems IESREF:5973 41

Figure23 Simulated Wind Speed m/s 100m Viet Nam 5km 2003-2010 WBG

Source:WorldBankGroup,viaIRENA

FINAL

IntelligentEnergySystems IESREF:5973 42

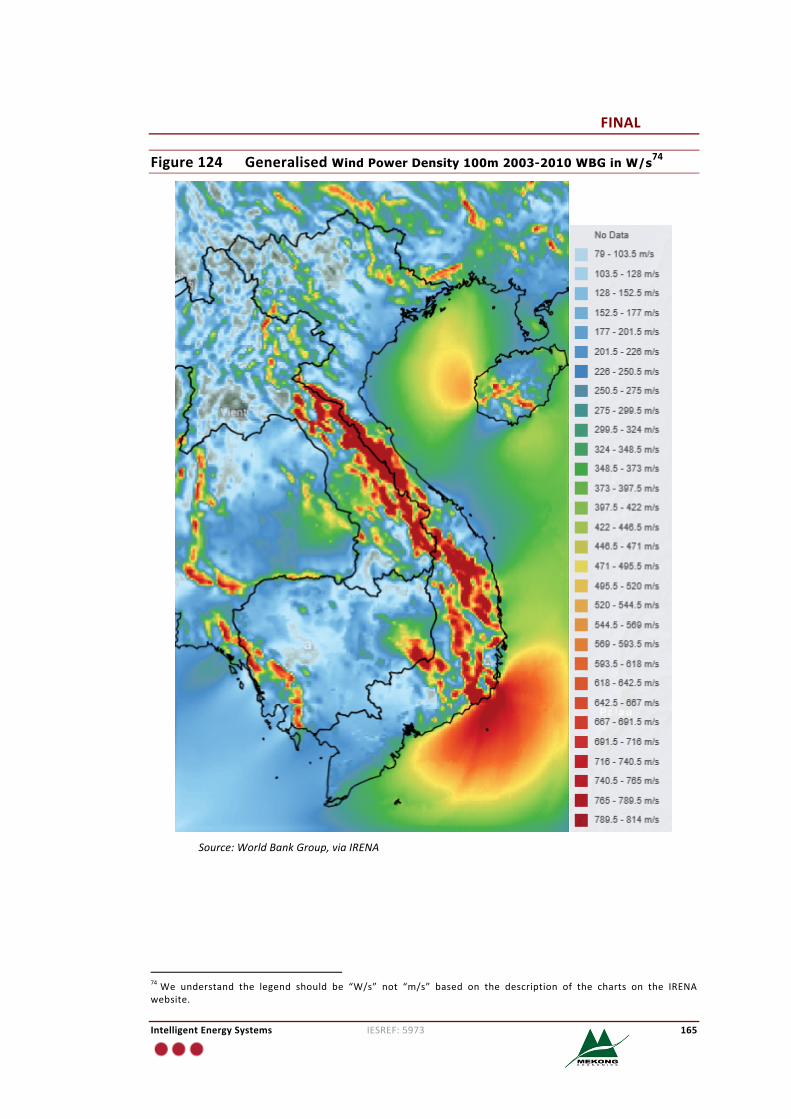

Figure24 Simulated Wind Power Density 100m 2003-2010 WBG in W/s16

Source:WorldBankGroup,viaIRENA

16We understand the legend should be “W/s” not “m/s” based on the description of the charts on the IRENAwebsite.

FINAL

IntelligentEnergySystems IESREF:5973 43

3.7 SolarPower

Viet Nam is considered to have high potential for the development of solarenergy.Thecountryhas13weatherstationstomeasureradiation,andover170weatherstationsdistributedovermostof theprovinces tomeasure thenumberofhoursofsunshine.Thenumberofhoursofsunshinerangesfrom1,300to2,900hoursperyear,dependingonthestationtendsto increasegradually fromnorthto south. The total installed capacity of solar PV in Viet Nam until 2014 wasapproximately4MWp.

According to the latest Prime Minister’s Decision No. 2068/QD-TTg dated 25November2015,approvingthedevelopmentstrategyofrenewableenergyofVietNamby2030withavisionto2050,totalelectricityproductionfromsolarpowerwould increase from 10 million kWh in 2015 to 1.4 billion kWh in 2020 (0.5%share), about 35.4 billion kWh in 2030 (6%) and about 210 billion kWh in 2050(20%).

A number of studies have been conducted on assessing the potential, themostrecentanddetailedofwhichwasa studyentitled: “Mapsof SolarResourceandPotential in Viet Nam”, published in January 2015. This was undertaken by theMOIT and a Spanish Consortium consisting of Centro de InvestigacionesEnergeticas Medioambientales y Tecnológicas (CIEMAT), National RenewableEnergyCentre(CENER)andInstitutoparalaDiversificaciónyAhorrodelaEnergía(IDAE).

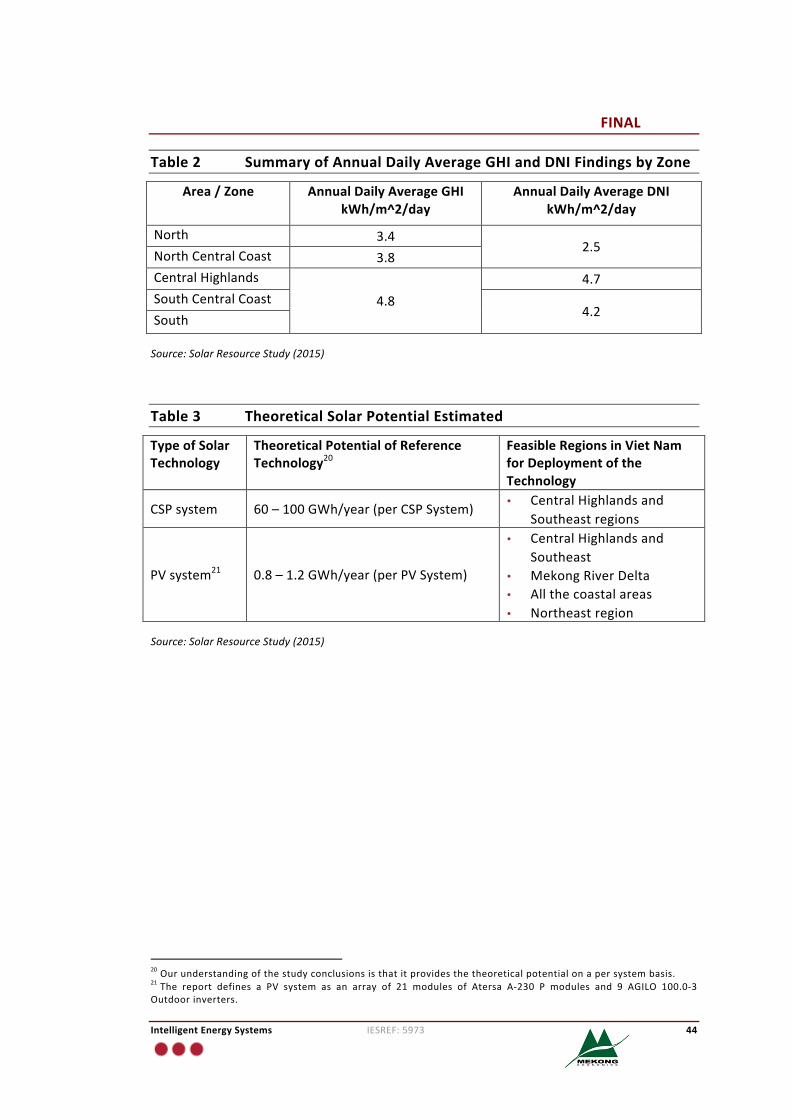

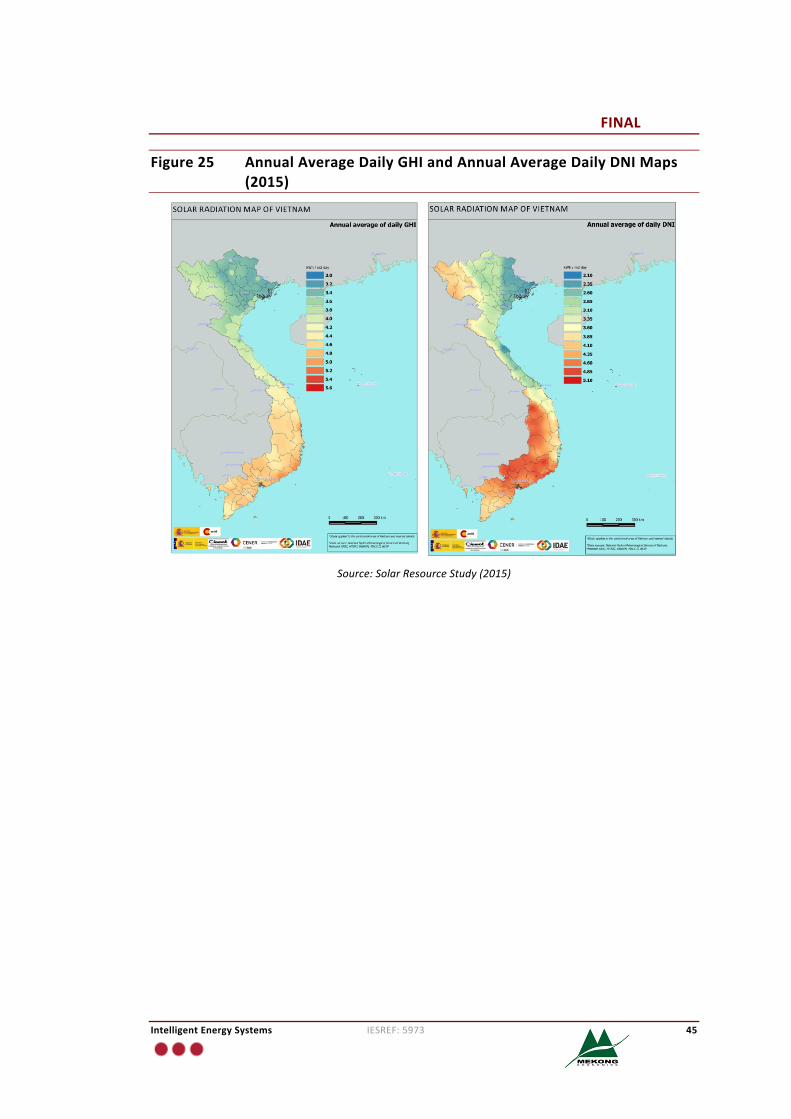

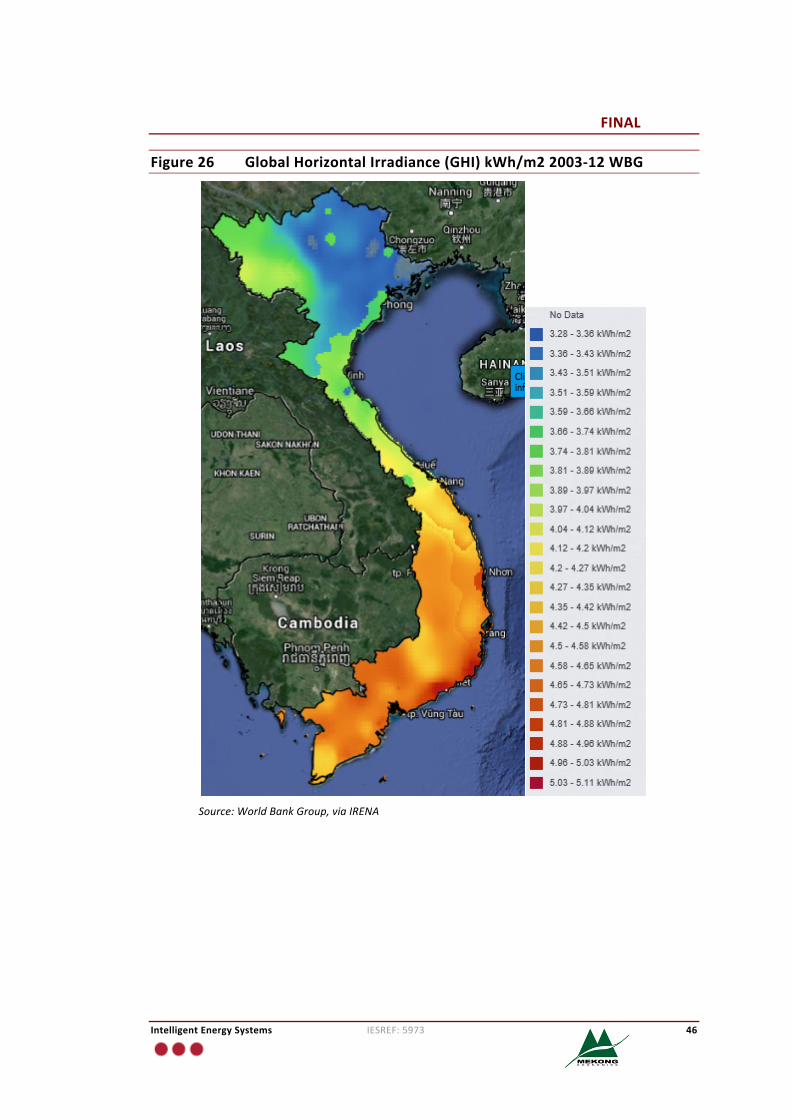

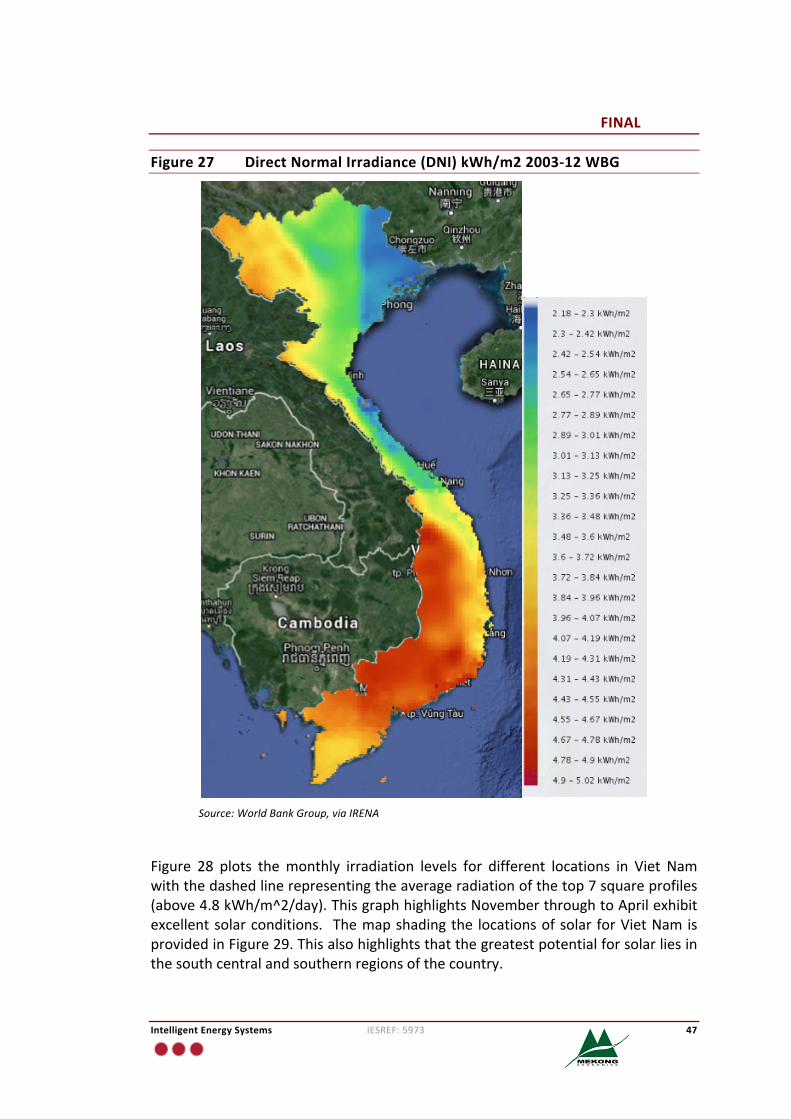

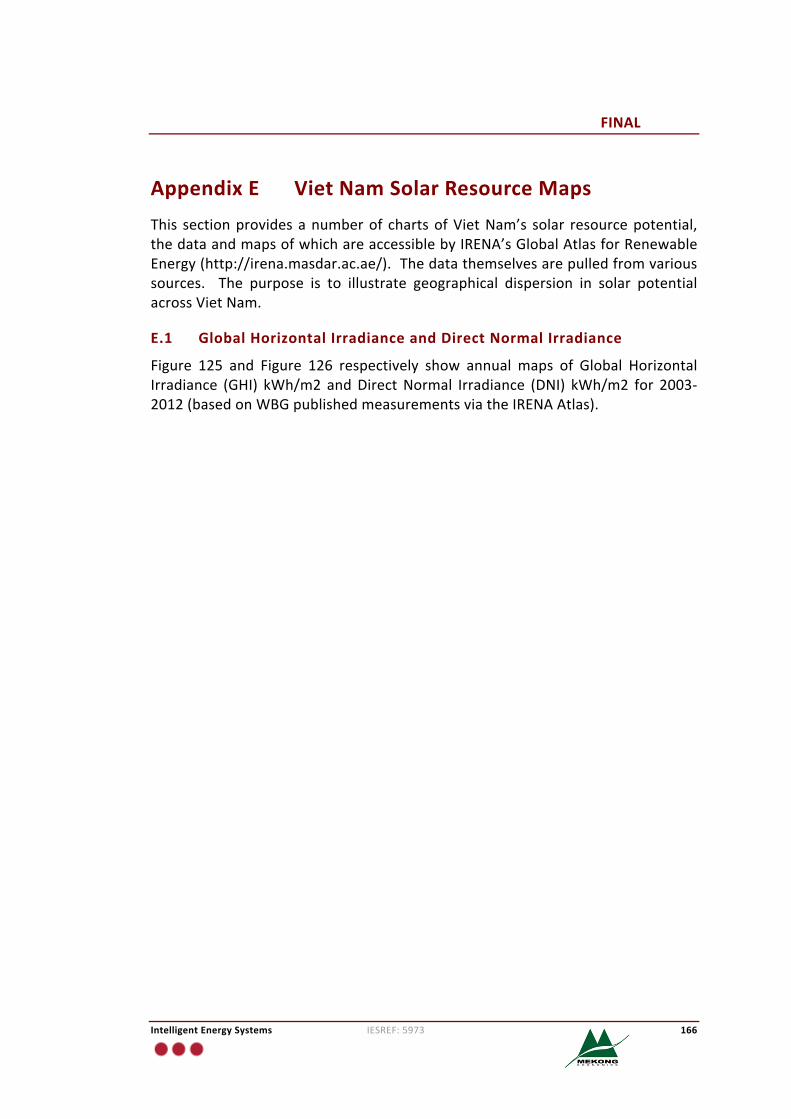

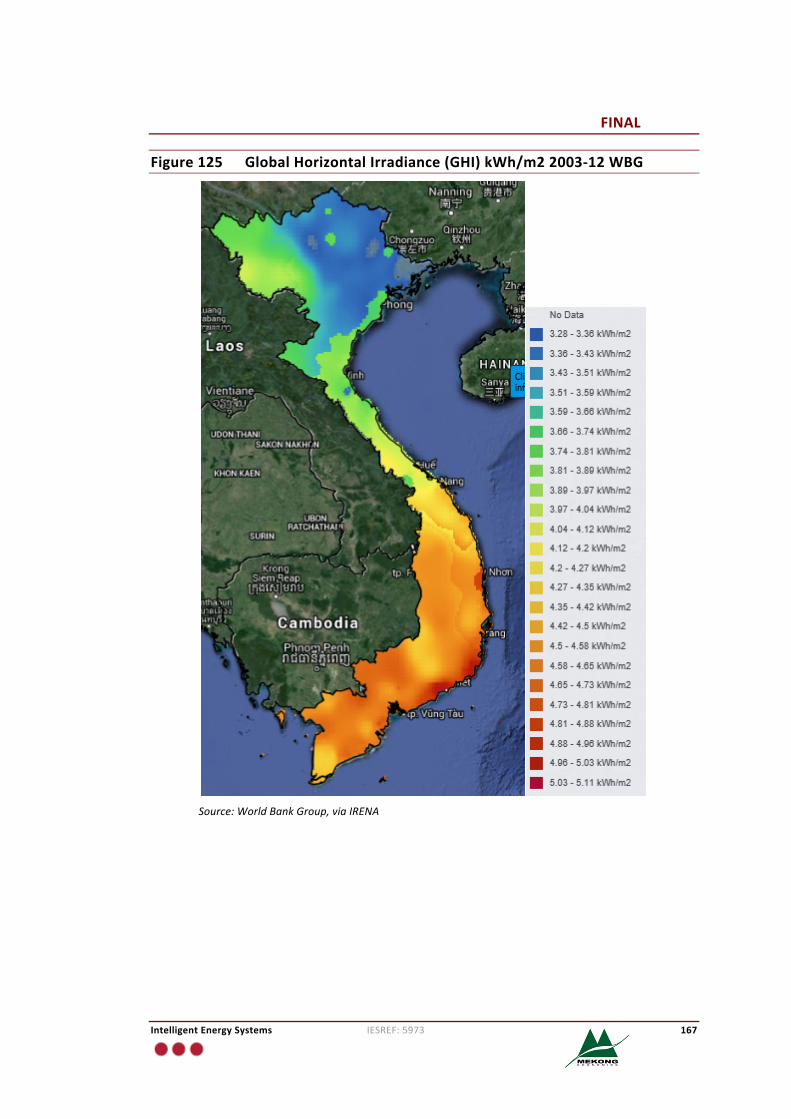

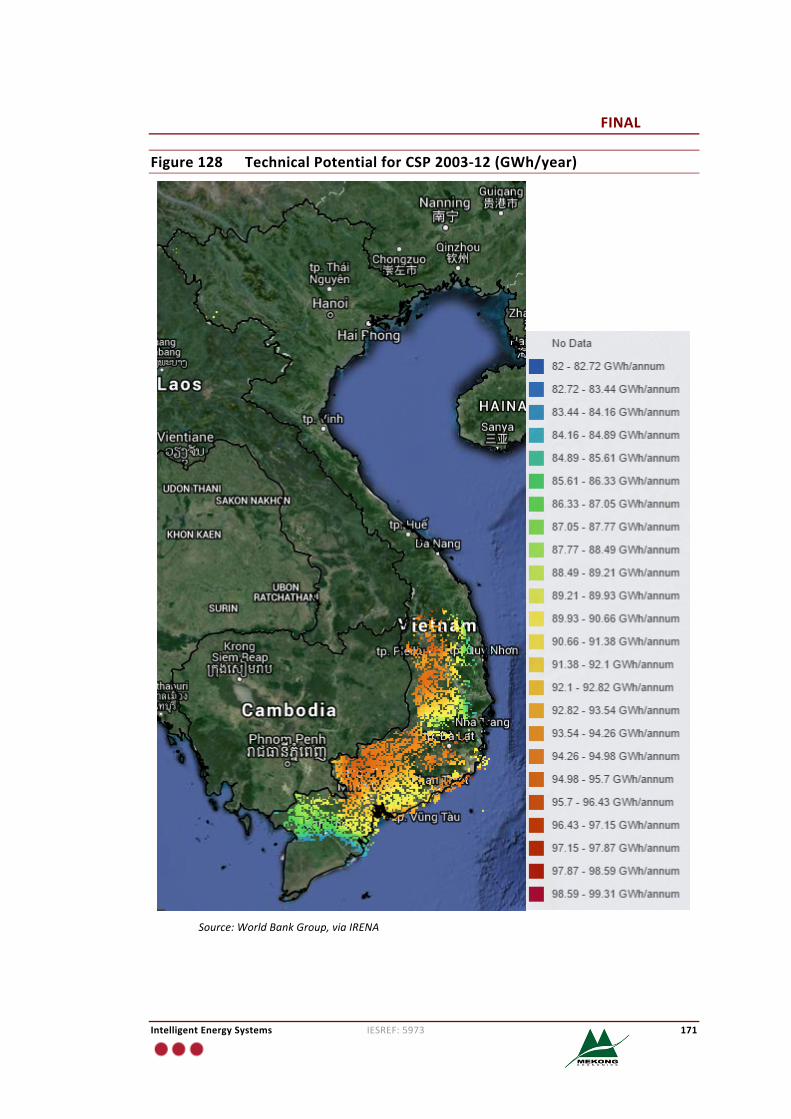

Figure25,Figure26andFigure27showsolarresourcemapsofannualaverageofdailyGlobalHorizontal Insolation (GHI)17andDirectNormal Insolation (DNI)18; thefirst illustrates the solar irradiation map for 2015 data, while the latter arerespectivelyGHIandDNImapsfor thebasedonannualdata for theperiod2003-1219. Table 2 summarises the findings of the Spanish Consortium’s study inrelationtothedailyaverageGlobalHorizontalInsolation(GHI)andDirectNormalInsolation (DNI) findings by zone. GHI provides an indication for flat-panelphotovoltaic (PV) potential while DNI provides the potential for concentratedsolarpower(CSP).ThetheoreticalpotentialforCSPandPVsystemsisprovidedinthestudyandtheareaswhereitcouldbedeployedaresetoutinTable3.

17GHIissolarradiationmeasuredwithaninstrumentmountedhorizontallysothatitseesthewholesky(effectivelyitisthedirectinsolationplusanydiffuseradiationthatoccursfromthescatteringoflight).18DNI is solar radiation solar radiation that comes directly from the sun,withminimal attenuation by the Earth’satmosphereorobstacles.19Maps were plotted using IRENA’s freeware tool here: http://irena.masdar.ac.ae/ and they are based onWorldBankGroup(WBG)data.

FINAL

IntelligentEnergySystems IESREF:5973 44

Table2 SummaryofAnnualDailyAverageGHIandDNIFindingsbyZone

Area/Zone AnnualDailyAverageGHIkWh/m^2/day

AnnualDailyAverageDNIkWh/m^2/day

North 3.42.5

NorthCentralCoast 3.8CentralHighlands

4.84.7

SouthCentralCoast4.2South

Source:SolarResourceStudy(2015)

Table3 TheoreticalSolarPotentialEstimated

TypeofSolarTechnology

TheoreticalPotentialofReferenceTechnology20

FeasibleRegionsinVietNamforDeploymentoftheTechnology

CSPsystem 60–100GWh/year(perCSPSystem) • CentralHighlandsandSoutheastregions

PVsystem21 0.8–1.2GWh/year(perPVSystem)

• CentralHighlandsandSoutheast

• MekongRiverDelta• Allthecoastalareas• Northeastregion

Source:SolarResourceStudy(2015)

20Ourunderstandingofthestudyconclusionsisthatitprovidesthetheoreticalpotentialonapersystembasis.21The report defines a PV system as an array of 21 modules of Atersa A-230 P modules and 9 AGILO 100.0-3Outdoorinverters.

FINAL

IntelligentEnergySystems IESREF:5973 45

Figure25 AnnualAverageDailyGHIandAnnualAverageDailyDNIMaps(2015)

Source:SolarResourceStudy(2015)

FINAL

IntelligentEnergySystems IESREF:5973 46

Figure26 GlobalHorizontalIrradiance(GHI)kWh/m22003-12WBG

Source:WorldBankGroup,viaIRENA

FINAL

IntelligentEnergySystems IESREF:5973 47

Figure27 DirectNormalIrradiance(DNI)kWh/m22003-12WBG

Source:WorldBankGroup,viaIRENA

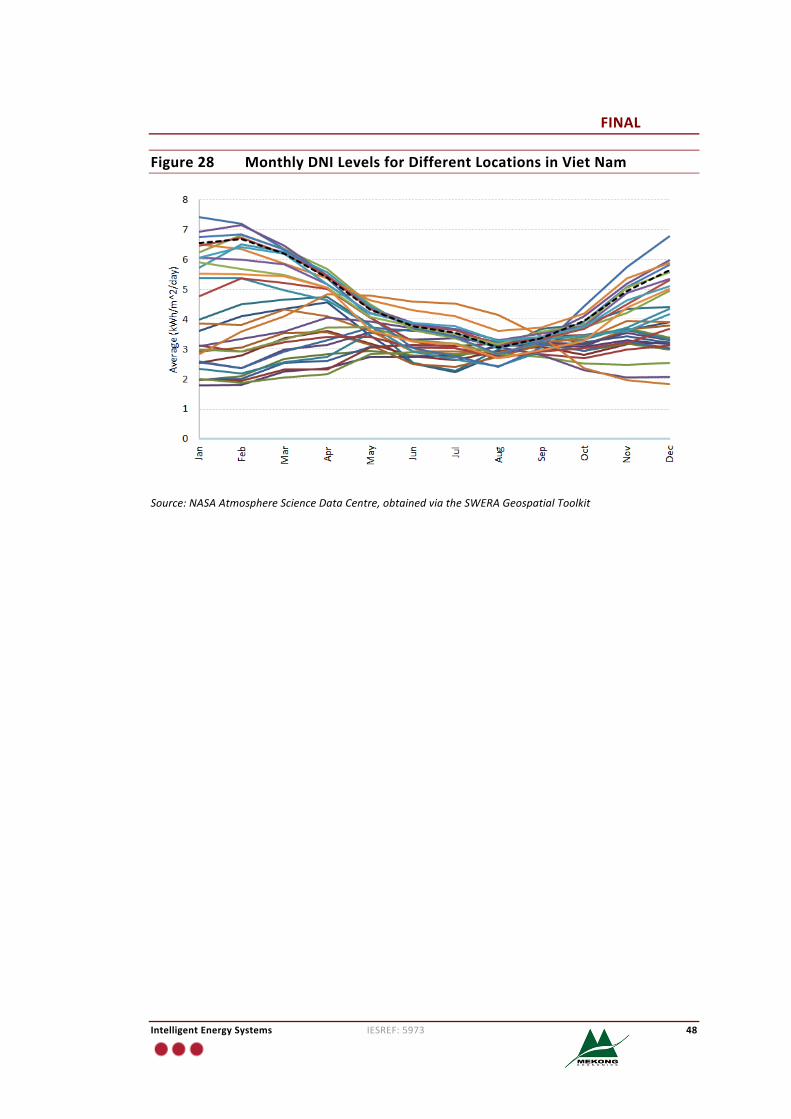

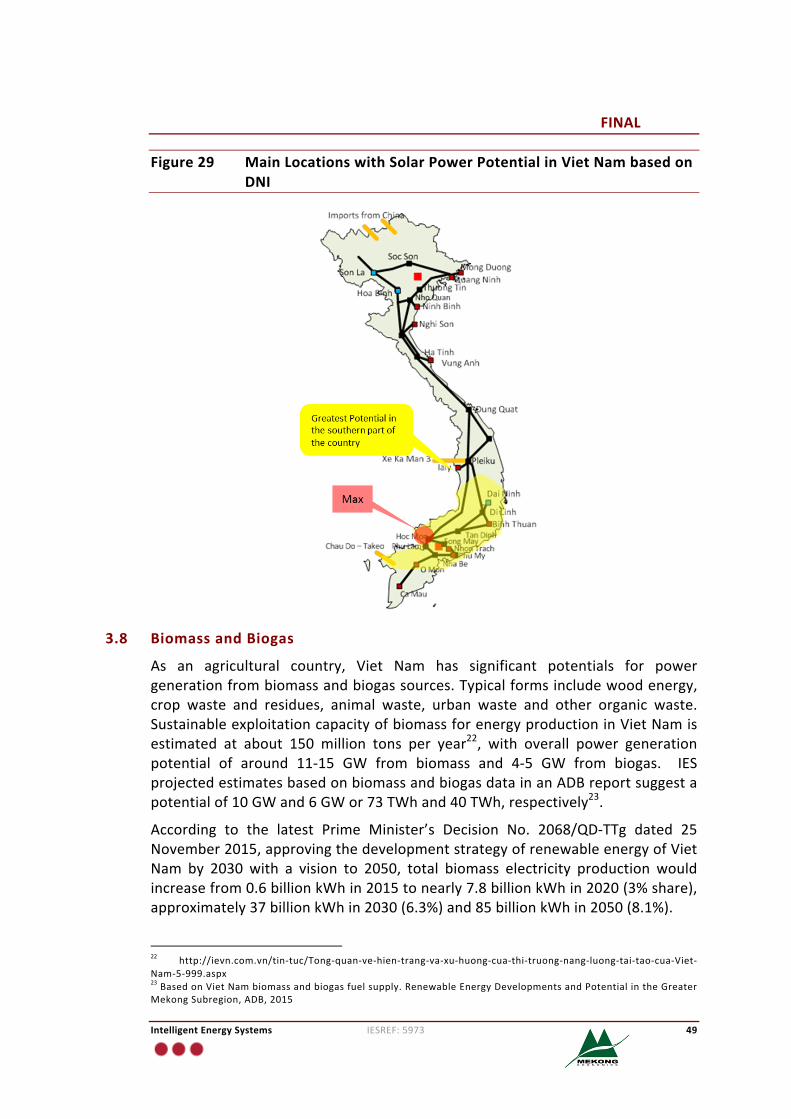

Figure 28 plots themonthly irradiation levels for different locations in Viet Namwiththedashedlinerepresentingtheaverageradiationofthetop7squareprofiles(above4.8kWh/m^2/day).ThisgraphhighlightsNovemberthroughtoAprilexhibitexcellentsolarconditions. Themapshadingthe locationsofsolar forVietNamisprovidedinFigure29.Thisalsohighlightsthatthegreatestpotentialforsolarliesinthesouthcentralandsouthernregionsofthecountry.

FINAL

IntelligentEnergySystems IESREF:5973 48

Figure28 MonthlyDNILevelsforDifferentLocationsinVietNam

Source:NASAAtmosphereScienceDataCentre,obtainedviatheSWERAGeospatialToolkit

FINAL

IntelligentEnergySystems IESREF:5973 49

Figure29 MainLocationswithSolarPowerPotentialinVietNambasedonDNI

3.8 BiomassandBiogas

As an agricultural country, Viet Nam has significant potentials for powergenerationfrombiomassandbiogassources.Typicalformsincludewoodenergy,crop waste and residues, animal waste, urban waste and other organic waste.SustainableexploitationcapacityofbiomassforenergyproductioninVietNamisestimated at about 150 million tons per year22, with overall power generationpotential of around 11-15 GW from biomass and 4-5 GW from biogas. IESprojectedestimatesbasedonbiomassandbiogasdatainanADBreportsuggestapotentialof10GWand6GWor73TWhand40TWh,respectively23.

According to the latest Prime Minister’s Decision No. 2068/QD-TTg dated 25November2015,approvingthedevelopmentstrategyofrenewableenergyofVietNam by 2030 with a vision to 2050, total biomass electricity production wouldincreasefrom0.6billionkWhin2015tonearly7.8billionkWhin2020(3%share),approximately37billionkWhin2030(6.3%)and85billionkWhin2050(8.1%).

22 http://ievn.com.vn/tin-tuc/Tong-quan-ve-hien-trang-va-xu-huong-cua-thi-truong-nang-luong-tai-tao-cua-Viet-Nam-5-999.aspx23BasedonVietNambiomassandbiogasfuelsupply.RenewableEnergyDevelopmentsandPotentialintheGreaterMekongSubregion,ADB,2015

FINAL

IntelligentEnergySystems IESREF:5973 50

Bagassehasbeenused forcombinedheatandpower (CHP)production inabout40 sugar mills in Viet Nam for a long time. By 2009, the total installed powercapacityofallCHPsystemswasaround150MW.In2007,sugarmillsinVietNamhave processed 9.4 million tons of sugar cane producing 2.8 million tons ofbagasse(495kTOE).However,only70-80%ofthisamount(i.e.2.1milliontonsor370kTOE)wasusedforheatandpowergeneration.Thisamountofbagassecouldgeneratemorethan300GWhofelectricityperyear.

Biogas energy was introduced into Viet Nam in the early 1960s. Many biogasdigester models were developed and widely disseminated by various localresearch and development institutions. At present, more than 200,000 biogasplants have been constructed in Viet Nam. Most operating biogas plants arefamily-sized with a digester capacity of 5 m3 to 20 m3. Biogas produced fromthese biogas plants is mainly used as fuel for cooking and lighting in thehouseholds.Thetotalbiogasproductionfromtheoperatingbiogasplantscouldbeestimatedat120millionm3,whichcontributedabout2.1millionGJ(50kTOE)tothetotalenergybalanceofVietNam.

To provide support for investors, the Vietnamese Government has recentlyestablishedthelevelsoffeedintariffsforbiomasspowergenerationprojectsandprojectssolidwaste.Theestablishedpricesforthebuyerare5.8UScents/kWhfor biomass sources, 10.05 US cents / kWh for generation sources on directly-burntsolidand7.28UScents/kWhforprojectsusingcombustiongascollectedfromthesolidwastelandfill.

3.9 GeothermalEnergy

Presently therearenogeothermalpowerplants inVietNam.However,basedonsurveys and studies carried out over the last few decades on geothermal energyresources, the country is recognised to have a limited amount of geothermalpotential.Estimatessuggestthereisthepotentialforbetween300MWto400MWwiththefollowingareas/regionsbeingidentifiedastheprimecandidates:• A 1993 study “Study and Assessment of Geothermal Potential from Quang

Nam – Da Nang to Ba Ria – Vung Tau” (Institute of Geology andMinerals),identified6potentialsites:(i)Bang,(ii)TuBong,(iii)HoiVan,(iv)DanhThanh,(v)MoDuc,and(vi)NghiaThang;

• A study in 1996, “Assessment of Geothermal Potential in Northern CentralRegion” (also carriedoutby the InstituteofGeology), refined someof thesefindings;

• ORMAT in coordination with EVN undertook a pre-feasibility study and it isunderstoodthatthefindingsleadtothemapplyinginApril2012foralicensetobuild5geothermalenergyplants inLeThuy (QuangBinh),MoDuc,NghiaThang(QuangNgai),HoiVan(BinhDinh)andTuiBong(KhanhHoa)withtotalcapacityofthegeneratorsintherangefrom150to200MW;

FINAL

IntelligentEnergySystems IESREF:5973 51

• VietNamGeothermal Energy Corp is also reportedlyworkingwithOrmat asthemajortechnicalpartnerfortwoprojects inMoDucandTuNghiadistrict,QuangNgaiprovincewithadesignedcapacityeachbeing18.7MW;and

• In 2013, Quang Tri Province granted investment certificate and constructionpermit for a geothermal energy plantwith a capacity of 25MWat Dakrongand according to press, the project’s price tag has been stated as US$46.3million.

3.10 OceanEnergy

VietNam’s3,200kmcoastlineandthousandsofislandspresentsignificantpotentialforwaveandtidal-basedenergytechnologies. Thecountryisestimatedtohaveatidal energy potential of around 1,753 GWh per year andwave energy potentialbetween40–411kW/mlocatedaroundBinhThuanandcentralVietNam24. Thegovernmenthas includedoceanenergyaspartof itsVietNamMarineStrategyto202025.

3.11 RenewableEnergyPotentialandDiversity

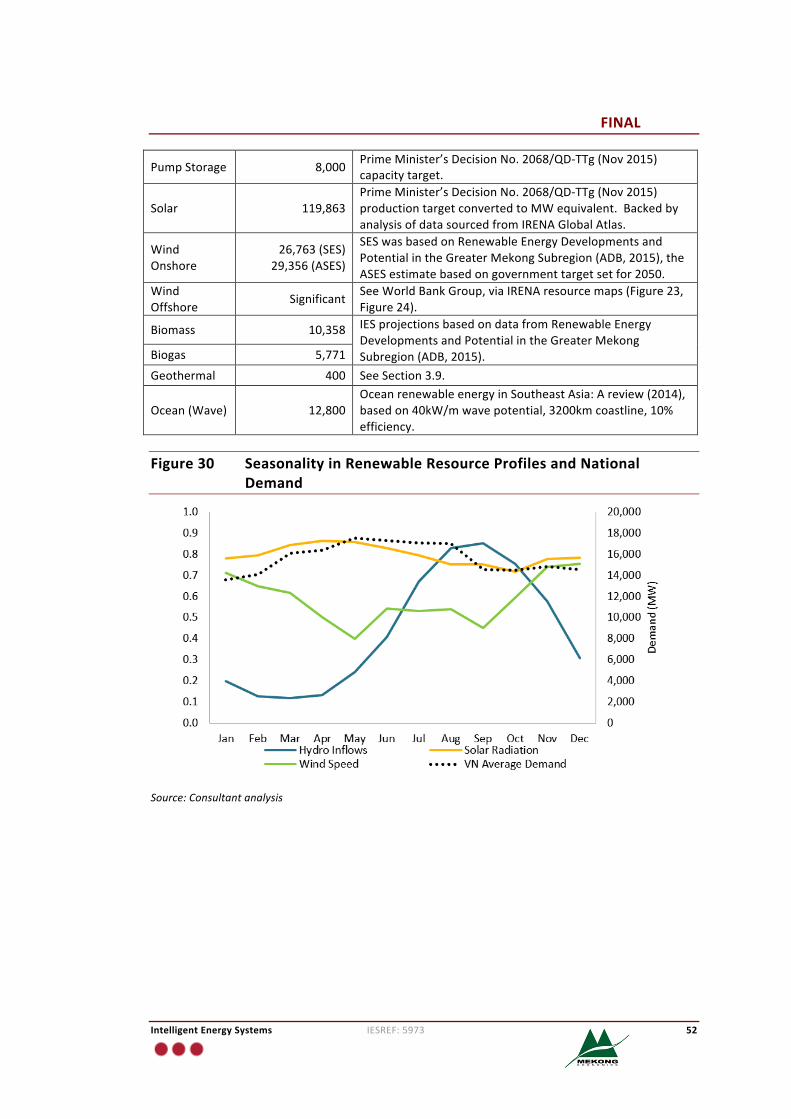

In summary, the renewableenergypotential forVietNam isprovided inTable4.Thenumberspresentedherehavebeendrawnfrommultiplesourcesandinformedby analysis of IRENAGlobal Atlas data. Figure 30 shows on amonthly basis thenormalised hydro inflows, solar radiation and wind speeds respectively for thenorth,centralandsouthregions.Thisallowsseasonalvariationintheavailabilityofsolar,wind,hydroanditscoincidencewithaveragemonthlydemandprofilestobeobservedatthenationallevel.Itshouldbenotedthatthekeyissueinthechartsiscorrelation but not amplitude, and furthermore, that the hydro inflows fall intoreservoirs,somewithsignificantamountofstorage,whichenablessmoothingoutgeneration throughout the year (within the limits of the storage capacity of thereservoirs), thus there is some scope for the role / operation of hydro powerstations tochange inVietNamtoaccommodatehigh levelsof renewableenergy.These charts show that there is some natural seasonal / monthly diversificationbetween resources: wind speeds tend to be high as the wet season ends, solarradiation tends to reach a peak as wind speeds become lower. They not onlyhighlightseasonaldiversificationamongthesolar,hydroandwindtechnologies;inVietNamthereisalsodiversificationbetweenthemainregions.

Table4 Summary of Estimated Renewable Energy Potential (CompiledfromVariousSourcesandAnalysis)

VietNam Potential(MW) Sourceandcomments

Hydro(Large) Morethan30,000 IESanalysis,seeFigure19.

Hydro(Small) 24,334 IESanalysis,seeSection3.5.2.

24OceanrenewableenergyinSoutheastAsia:Areview(Quirapas,Lin,Abundo,Brahim,Santos,2014)25Referto:http://english.vietnamnet.vn/fms/special-reports/144832/vietnam-and-the-marine-strategy.html

FINAL

IntelligentEnergySystems IESREF:5973 52

PumpStorage 8,000 PrimeMinister’sDecisionNo.2068/QD-TTg(Nov2015)capacitytarget.

Solar 119,863PrimeMinister’sDecisionNo.2068/QD-TTg(Nov2015)productiontargetconvertedtoMWequivalent.BackedbyanalysisofdatasourcedfromIRENAGlobalAtlas.

WindOnshore

26,763(SES)29,356(ASES)

SESwasbasedonRenewableEnergyDevelopmentsandPotentialintheGreaterMekongSubregion(ADB,2015),theASESestimatebasedongovernmenttargetsetfor2050.

WindOffshore

Significant SeeWorldBankGroup,viaIRENAresourcemaps(Figure23,Figure24).

Biomass 10,358 IESprojectionsbasedondatafromRenewableEnergyDevelopmentsandPotentialintheGreaterMekongSubregion(ADB,2015).Biogas 5,771

Geothermal 400 SeeSection3.9.

Ocean(Wave) 12,800OceanrenewableenergyinSoutheastAsia:Areview(2014),basedon40kW/mwavepotential,3200kmcoastline,10%efficiency.

Figure30 SeasonalityinRenewableResourceProfilesandNationalDemand

Source:Consultantanalysis

FINAL

IntelligentEnergySystems IESREF:5973 53

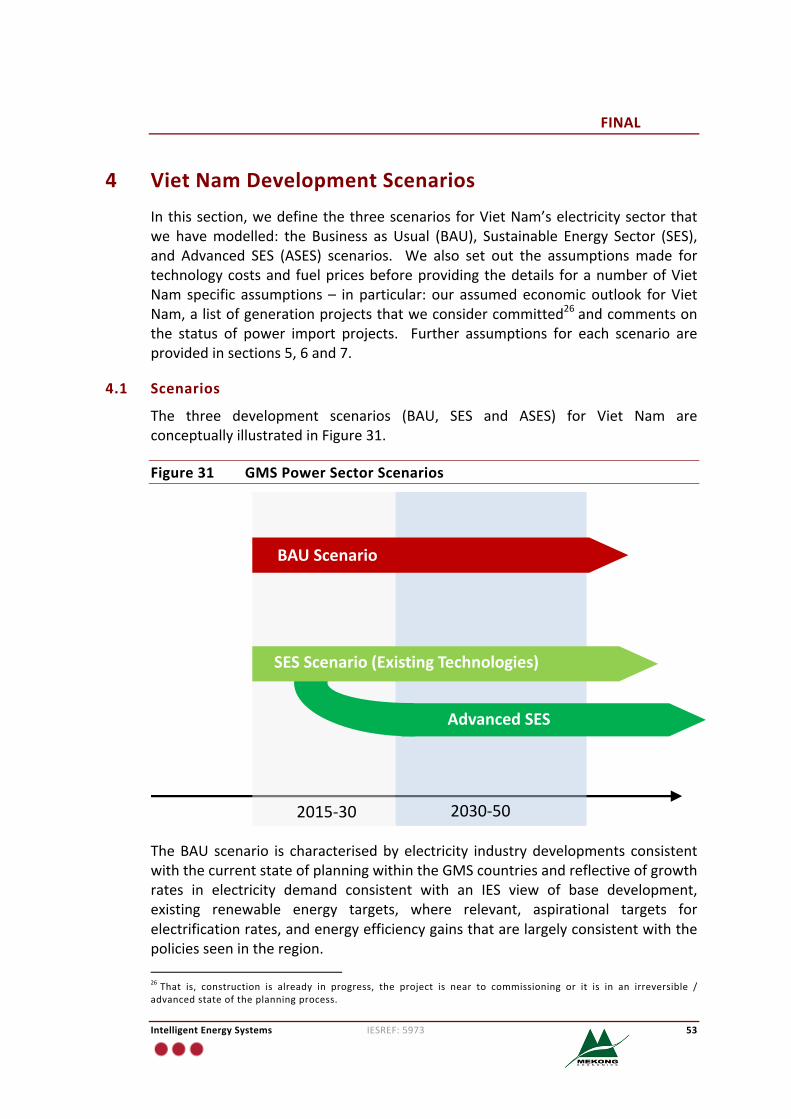

4 VietNamDevelopmentScenariosInthissection,wedefinethethreescenariosforVietNam’selectricitysectorthatwe havemodelled: the Business as Usual (BAU), Sustainable Energy Sector (SES),and Advanced SES (ASES) scenarios. We also set out the assumptionsmade fortechnologycostsand fuelpricesbeforeprovidingthedetails foranumberofVietNam specific assumptions– inparticular: our assumedeconomicoutlook forVietNam,alistofgenerationprojectsthatweconsidercommitted26andcommentsonthe status of power import projects. Further assumptions for each scenario areprovidedinsections5,6and7.

4.1 Scenarios

The three development scenarios (BAU, SES and ASES) for Viet Nam areconceptuallyillustratedinFigure31.

Figure31 GMSPowerSectorScenarios

TheBAU scenario is characterisedbyelectricity industrydevelopments consistentwiththecurrentstateofplanningwithintheGMScountriesandreflectiveofgrowthrates in electricity demand consistent with an IES view of base development,existing renewable energy targets, where relevant, aspirational targets forelectrificationrates,andenergyefficiencygainsthatarelargelyconsistentwiththepoliciesseenintheregion.26That is, construction is already in progress, the project is near to commissioning or it is in an irreversible /advancedstateoftheplanningprocess.

2015-30 2030-50

AdvancedSES

BAUScenario

SESScenario(ExistingTechnologies)

FINAL

IntelligentEnergySystems IESREF:5973 54

Incontrast,theSESseekstotransitionelectricitydemandtowardsthebestpracticebenchmarksofotherdevelopedcountries in termsofenergyefficiency,maximisetherenewableenergydevelopment,ceasethedevelopmentoffossilfuelresources,and make sustainable and prudent use of undeveloped conventional hydroresources.Whererelevant,itleveragesadvancesinoff-gridtechnologiestoprovideaccesstoelectricity toremotecommunities. TheSEStakesadvantageofexisting,technicallyprovenandcommerciallyviablerenewableenergytechnologies.

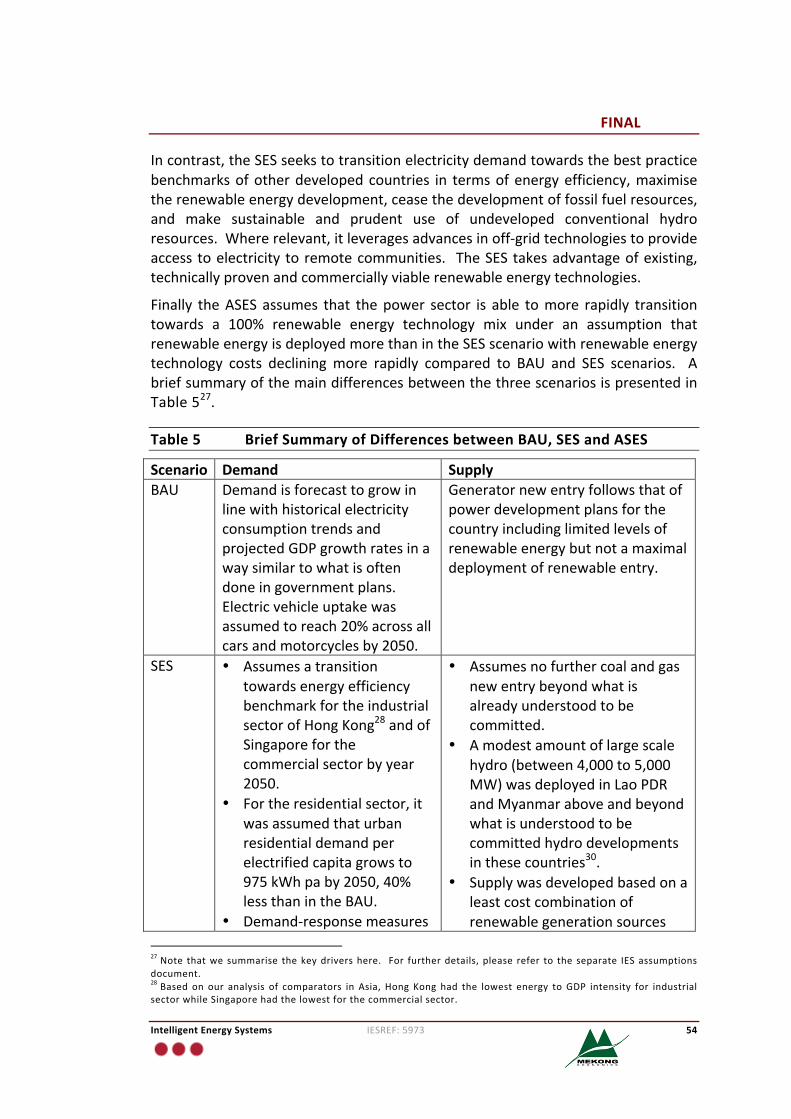

Finally theASES assumes that thepower sector is able tomore rapidly transitiontowards a 100% renewable energy technology mix under an assumption thatrenewableenergyisdeployedmorethanintheSESscenariowithrenewableenergytechnology costs decliningmore rapidly compared to BAU and SES scenarios. AbriefsummaryofthemaindifferencesbetweenthethreescenariosispresentedinTable527.

Table5 BriefSummaryofDifferencesbetweenBAU,SESandASES

Scenario Demand SupplyBAU Demandisforecasttogrowin

linewithhistoricalelectricityconsumptiontrendsandprojectedGDPgrowthratesinawaysimilartowhatisoftendoneingovernmentplans.Electricvehicleuptakewasassumedtoreach20%acrossallcarsandmotorcyclesby2050.

Generatornewentryfollowsthatofpowerdevelopmentplansforthecountryincludinglimitedlevelsofrenewableenergybutnotamaximaldeploymentofrenewableentry.

SES • AssumesatransitiontowardsenergyefficiencybenchmarkfortheindustrialsectorofHongKong28andofSingaporeforthecommercialsectorbyyear2050.

• Fortheresidentialsector,itwasassumedthaturbanresidentialdemandperelectrifiedcapitagrowsto975kWhpaby2050,40%lessthanintheBAU.

• Demand-responsemeasures

• Assumesnofurthercoalandgasnewentrybeyondwhatisalreadyunderstoodtobecommitted.

• Amodestamountoflargescalehydro(between4,000to5,000MW)wasdeployedinLaoPDRandMyanmaraboveandbeyondwhatisunderstoodtobecommittedhydrodevelopmentsinthesecountries30.

• Supplywasdevelopedbasedonaleastcostcombinationofrenewablegenerationsources

27Note thatwe summarise thekeydrivershere. For furtherdetails,please refer to the separate IESassumptionsdocument.28Based on our analysis of comparators in Asia, Hong Kong had the lowest energy to GDP intensity for industrialsectorwhileSingaporehadthelowestforthecommercialsector.

FINAL

IntelligentEnergySystems IESREF:5973 55

Scenario Demand Supplyassumedtobephasedinfrom2021withsome15%ofdemandbeingflexible29by2050.

• SlowerelectrificationratesforthenationalgridsinCambodiaandMyanmarcomparedtotheBAU,butdeploymentofoff-gridsolutionsthatachievesimilarlevelsofelectricityaccess.

• Mini-grids(off-gridnetworks)areassumedtoconnecttothenationalsysteminthelonger-term.

• ElectricvehicleuptakeaspertheBAU.

limitedbyestimatesofpotentialratesofdeploymentandjudgmentsinonwhentechnologieswouldbefeasibleforimplementationtodeliverapowersystemwiththesamelevelofreliabilityastheBAU.

• Technologiesusedinclude:solarphotovoltaics,biomass,biogasandmunicipalwasteplants,CSPwithstorage,onshoreandoffshorewind,utilityscalebatteries,geothermalandoceanenergy.

• TransmissionlimitsbetweenregionswereupgradedasrequiredtosupportpowersectordevelopmentintheGMSasanintegratedwhole,andthetransmissionplanallowedtobedifferentcomparedtothetransmissionplanoftheBAU.

ASES TheASESdemandassumptionsaredoneasasensitivitytotheSES:• Anadditional10%energyefficiencyappliedtotheSESdemands(excludingtransport).

• Flexibledemandassumedtoreach25%by2050.

• Uptakeofelectricvehiclesdoubledby2050.

ASESsupplyassumptionswerealsoimplementedasasensitivitytotheSES,withthefollowingmaindifferences:• AllowratesofrenewableenergydeploymenttobemorerapidcomparedtotheBAUandSES.

• Technologycostreductionswereacceleratedforrenewableenergytechnologies.

• Implementamorerapidprogrammeofretirementsforfossilfuelbasedpowerstations.

• Energypolicytargetsof70%renewablegenerationby2030,90%by2040and100%by2050acrosstheregionareinplace.

30ThisisimportanttoallcountriesbecausetheGMSismodelledasaninterconnectedregion.29Flexible demand is demand that can be rescheduled at short notice andwould be implemented by a variety ofsmartgridanddemandresponsetechnologies.

FINAL

IntelligentEnergySystems IESREF:5973 56

Scenario Demand Supply• Assumethattechnical/operationalissueswithpowersystemoperationandcontrolforaveryhighlevelofrenewableenergyareaddressed31.

4.2 TechnologyCostAssumptions

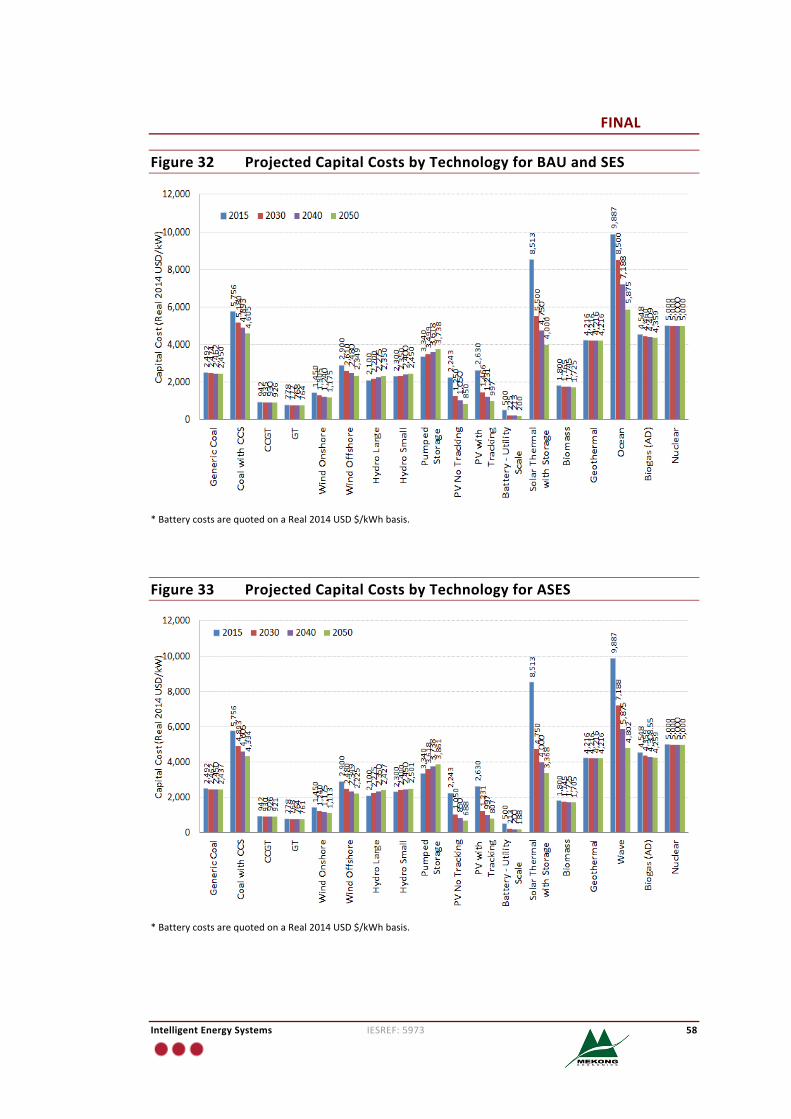

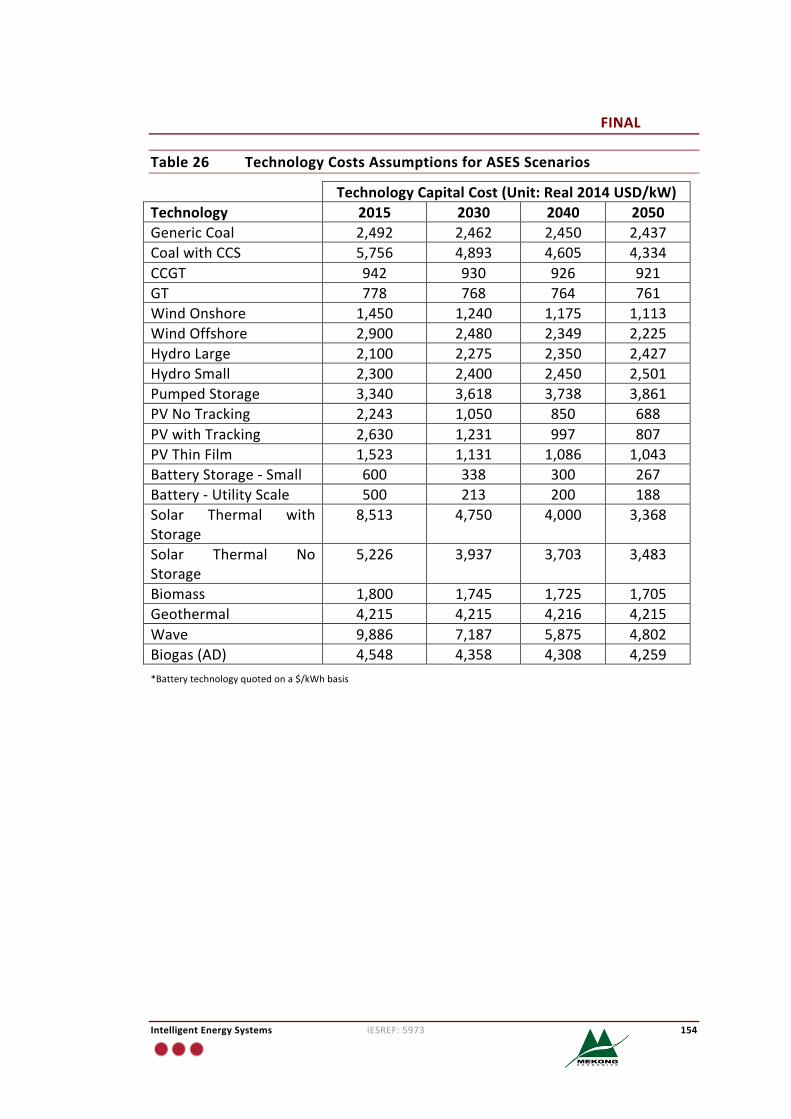

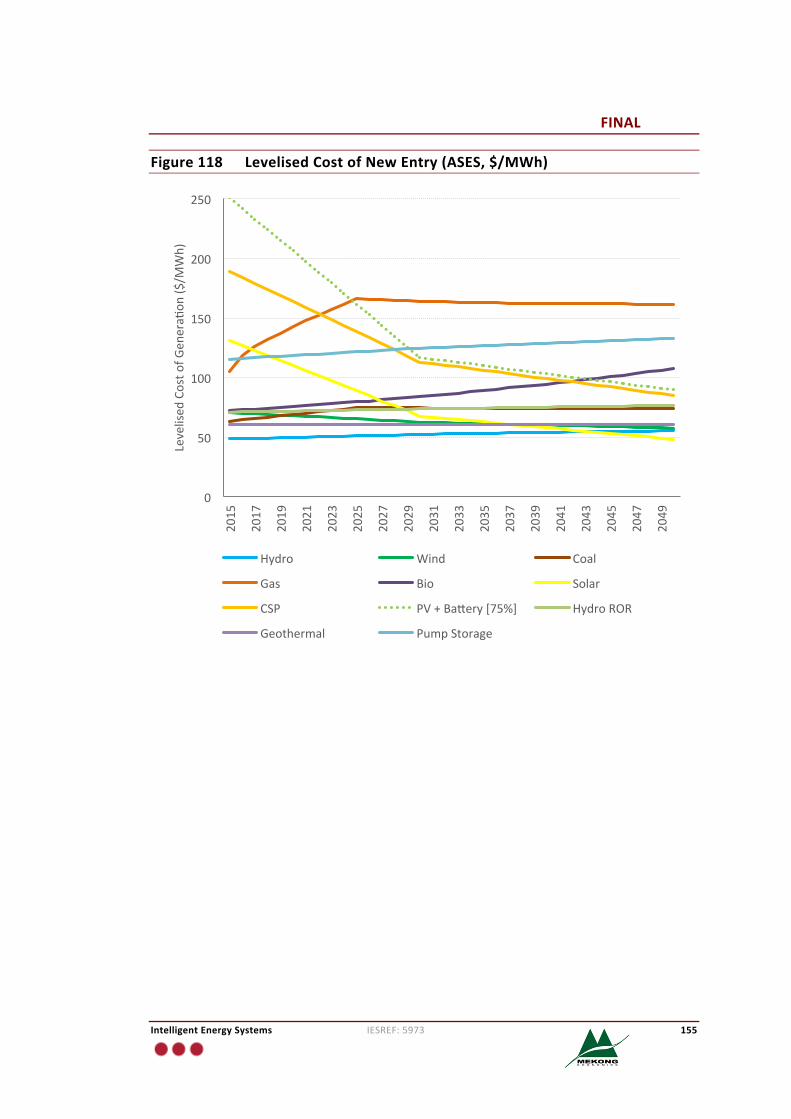

Technology capital cost estimates from a variety of sources were collected andnormalised tobeona consistentanduniformbasis32. Mid-pointswere taken foreachtechnologythatisrelevanttotheGMSregion.Thedatapointscollatedreflectovernight, turnkey engineering procurement construction capital costs and areexclusive of fixed operating and maintenance costs, variable operating andmaintenancecostsandfuelcosts. Thecapitalcostsbytechnologyassumedinthestudy are presented in Figure 32for the BAU and SES scenarios. For the ASESscenario,weassumedthatthetechnologycostsofrenewabletechnologiesdeclinemorerapidly.ThesetechnologycostassumptionsarelistedinFigure33.Notethatthetechnologycapitalcostshavenot includedlandcosts,transmissionequipmentcosts,nordecommissioningcostsandarequotedonaRealUSD2014basis.

CommentsonthevarioustechnologiesarediscussedbelowinrelationtotheBAUandSEStechnologycosts:

• Conventional thermal technology costs areassumed todecreaseat a rateof0.05%pa citingmaturation of the technologieswith no significant scope forcostimprovement.

• Onshorewindcostswerebasedon thecurrent installedpricesseen inChinaand Indiawith future costs decreasing at a rate of 0.6% pa. Future offshorewind costs were developed by applying the current percentage differencebetweencurrentonshoreandoffshorecapitalcostsforallfutureyears.

• Largeandsmall-scalehydrocostsareassumedtoincreaseovertimereflectingeasyandmorecost-efficienthydroopportunitiesbeingdeveloped inthefirstinstance. IRENA reported no cost improvements for hydro over the periodfrom 2010 to 2014. Adjustments are made in the case of Lao PDR andMyanmarwheresignificanthydroresourcesaredevelopedintheBAUcase33.

31Inparticular:(1)sufficientreal-timemonitoringforbothsupplyanddemandsideoftheindustry,(2)appropriateforecasting for solar and wind and centralised real-time control systems in place to manage a more distributedsupplyside,storagesandflexibledemandresources,and(3)powersystemsdesignedtobeabletomanagevoltage,frequency and stability issues that may arise from having a power system that is dominated an asynchronoustechnologies.32WestandardisedonReal2014USDwithalltechnologiescostsnormalisedtoreflectturnkeycapitalcosts.33Capitalcostsforlargescalehydroprojectsareassumedtoincreaseto$3,000/kWby2050consistentwithhavingthemosteconomicallyfeasiblehydroresourcesdevelopedaheadoflesseconomicallyfeasibleresources.

FINAL

IntelligentEnergySystems IESREF:5973 57