Page 1

Visit UMT online at www.umtweb.edu© South-Western 2004Survey of Accounting, 2/e

1 of 31Chapter 12,

ACCT125

ACCOUNTING ACCOUNTING FUNDAMENTALS FOR FUNDAMENTALS FOR

MANAGERSMANAGERS

University of Management and Technology1901 North Fort Myer Drive

Arlington, VA 22209Voice: (703) 516-0035 Fax: (703) 516-0985

Website: www.umtweb.edu

Page 2

2 of 31Visit UMT online at www.umtweb.eduChapter 12,

ACCT125

Task Force Clip Art Task Force Clip Art included in this electronic included in this electronic presentation is used with presentation is used with

the permission of New the permission of New Vision Technology of Vision Technology of

Nepean Ontario, Canada.Nepean Ontario, Canada.

Page 3

Visit UMT online at www.umtweb.edu© South-Western 2004Survey of Accounting, 2/e

3 of 31Chapter 12,

ACCT125

Chapter 12Chapter 12

Differential Analysis and Differential Analysis and Product PricingProduct Pricing

Page 4

4 of 31Visit UMT online at www.umtweb.eduChapter 12,

ACCT125

After studying this After studying this chapter, you should chapter, you should

be able to:be able to:

After studying this After studying this chapter, you should chapter, you should

be able to:be able to:

ContinuedContinuedContinuedContinued

Learning ObjectivesLearning Objectives

1. Prepare a differential analysis report for decisions involvingLeasing or selling equipment.

Discontinuing an unprofitable segment.

Manufacturing or purchasing a needed part.

Replacing usable fixed assets.

Processing further or selling an intermediate product.

Accepting additional business at a special price.

Page 5

5 of 31Visit UMT online at www.umtweb.eduChapter 12,

ACCT125

Learning ObjectivesLearning Objectives

2. Determine the selling price of a product using the total cost concept.

3. Calculate the relative profitability of products in bottleneck production environments.

Page 6

6 of 31Visit UMT online at www.umtweb.eduChapter 12,

ACCT125

1Prepare a differential analysis report.

Learning ObjectiveLearning Objective

Page 7

7 of 31Visit UMT online at www.umtweb.eduChapter 12,

ACCT125

Differential AnalysisDifferential Analysis

1. Leasing or selling equipment

2. Discontinuing an unprofitable segment

3. Manufacturing or purchasing a needed part

4. Replacing usable fixed assets

5. Processing further or selling an intermediate product

6. Accepting additional business at a special price

Differential analysis is used for analyzing:

Page 8

8 of 31Visit UMT online at www.umtweb.eduChapter 12,

ACCT125

Proposal to Lease or Sell EquipmentJune 22, 2006

Differential revenue from alternatives:Revenue from lease $160,000Revenue from sales 100,000 Differential revenue from lease $60,000

Differential cost of alternatives:Repairs, insurance, taxesa $ 35,000Commission expense on sale 6,000 Differential cost of lease 29,000

Net differential income from leasing $31,000

Page 9

9 of 31Visit UMT online at www.umtweb.eduChapter 12,

ACCT125

Proposal to Lease or Sell EquipmentJune 22, 2006

Revenue from lease $160,000 Revenue from sales 100,000 Repairs, insurance, taxes (35,000)Commission expense on sale (6,000)

Totals $125,000 $94,000

Lease Sell

This alternative format separates the two options into columns. The net benefit is the same.

This alternative format separates the two options into columns. The net benefit is the same.

Page 10

10 of 31Visit UMT online at www.umtweb.eduChapter 12,

ACCT125

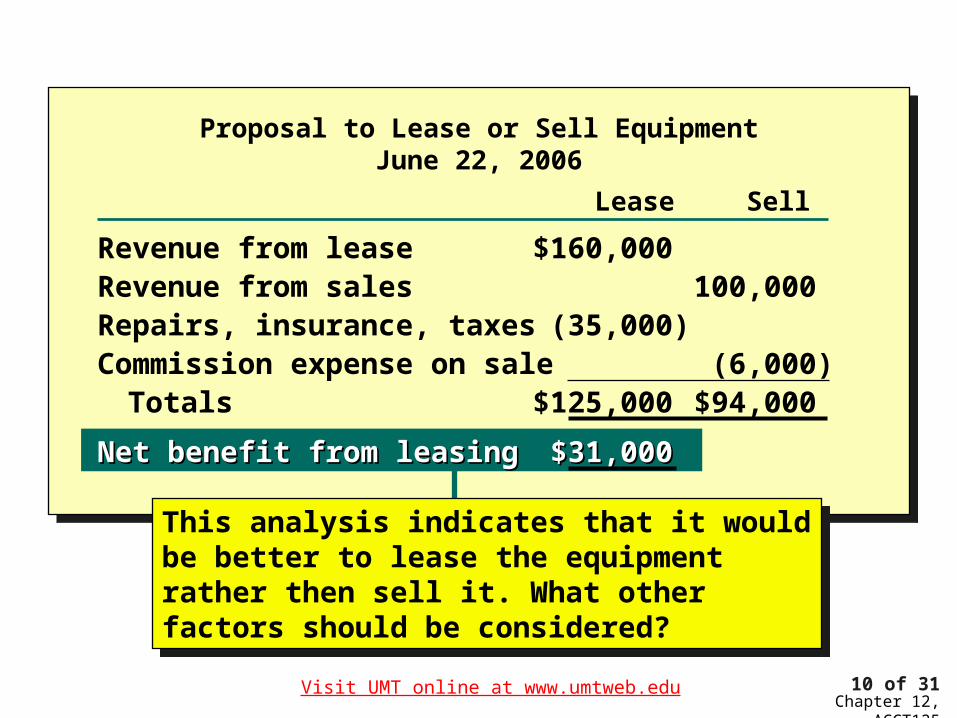

Proposal to Lease or Sell EquipmentJune 22, 2006

Lease Sell

Revenue from lease $160,000 Revenue from sales 100,000 Repairs, insurance, taxes (35,000)Commission expense on sale (6,000)

Totals $125,000 $94,000

Net benefit from leasingNet benefit from leasing $31,000 $31,000

This analysis indicates that it would be better to lease the equipment rather then sell it. What other factors should be considered?

This analysis indicates that it would be better to lease the equipment rather then sell it. What other factors should be considered?

Page 11

11 of 31Visit UMT online at www.umtweb.eduChapter 12,

ACCT125

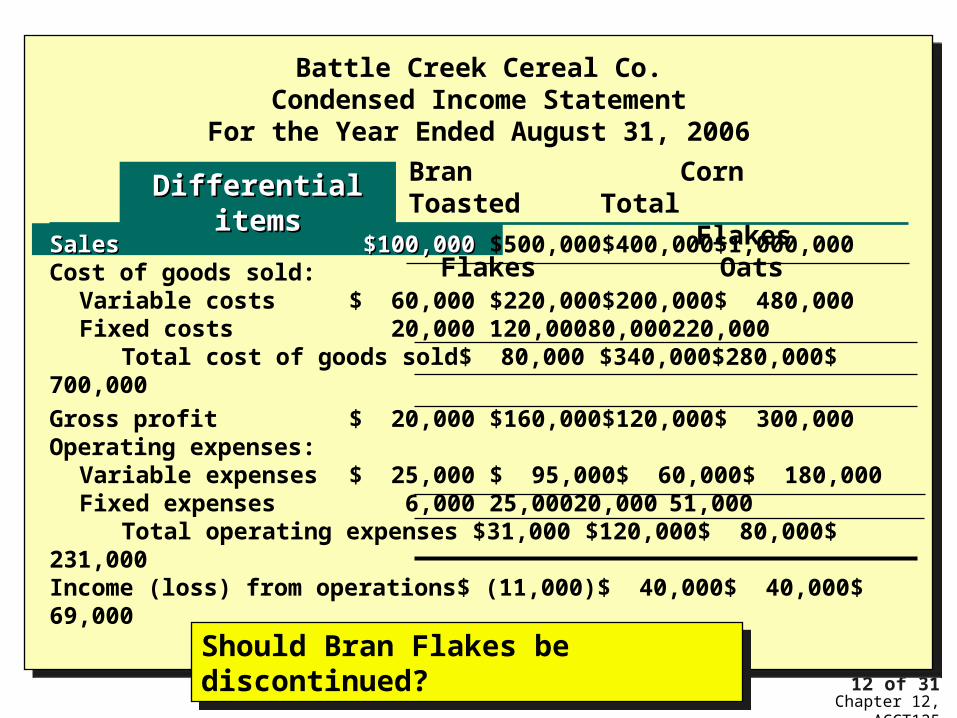

Battle Creek Cereal Co.Condensed Income Statement

For the Year Ended August 31, 2006

Bran Corn Toasted Total Flakes Flakes

OatsSales $100,000 $500,000 $400,000 $1,000,000Cost of goods sold:

Variable costs $ 60,000 $220,000 $200,000 $ 480,000Fixed costs 20,000 120,000 80,000 220,000 Total cost of goods sold $ 80,000 $340,000 $280,000 $ 700,000

Gross profit $ 20,000 $160,000 $120,000 $ 300,000Operating expenses:

Variable expenses $ 25,000 $ 95,000 $ 60,000 $ 180,000Fixed expenses 6,000 25,000 20,000 51,000 Total operating expenses $ 31,000 $120,000 $ 80,000 $ 231,000

Income (loss) from operations$ (11,000) $ 40,000 $ 40,000 $ 69,000

Should Bran Flakes be discontinued?Should Bran Flakes be discontinued?

Page 12

12 of 31Visit UMT online at www.umtweb.eduChapter 12,

ACCT125

Battle Creek Cereal Co.Condensed Income Statement

For the Year Ended August 31, 2006

Bran Corn Toasted Total Flakes Flakes

Oats

Differential itemsDifferential items

SalesSales $100,000$100,000 $500,000 $400,000 $1,000,000Cost of goods sold:

Variable costs $ 60,000 $220,000 $200,000 $ 480,000Fixed costs 20,000 120,000 80,000 220,000 Total cost of goods sold $ 80,000 $340,000 $280,000 $ 700,000

Gross profit $ 20,000 $160,000 $120,000 $ 300,000Operating expenses:

Variable expenses $ 25,000 $ 95,000 $ 60,000 $ 180,000Fixed expenses 6,000 25,000 20,000 51,000 Total operating expenses $ 31,000 $120,000 $ 80,000 $ 231,000

Income (loss) from operations$ (11,000) $ 40,000 $ 40,000 $ 69,000

Should Bran Flakes be discontinued?Should Bran Flakes be discontinued?

Page 13

13 of 31Visit UMT online at www.umtweb.eduChapter 12,

ACCT125

Battle Creek Cereal Co.Condensed Income Statement

For the Year Ended August 31, 2006

Bran Corn Toasted Total Flakes Flakes

Oats

Differential itemsDifferential items

SalesSales $100,000$100,000 $500,000 $400,000 $1,000,000Cost of goods sold:

Variable costsVariable costs $ 60,000$ 60,000 $220,000 $200,000 $ 480,000Fixed costs 20,000 120,000 80,000 220,000 Total cost of goods sold $ 80,000 $340,000 $280,000 $ 700,000

Gross profit $ 20,000 $160,000 $120,000 $ 300,000Operating expenses:

Variable expenses $ 25,000 $ 95,000 $ 60,000 $ 180,000Fixed expenses 6,000 25,000 20,000 51,000 Total operating expenses $ 31,000 $120,000 $ 80,000 $ 231,000

Income (loss) from operations$ (11,000) $ 40,000 $ 40,000 $ 69,000

Should Bran Flakes be discontinued?Should Bran Flakes be discontinued?

Page 14

14 of 31Visit UMT online at www.umtweb.eduChapter 12,

ACCT125

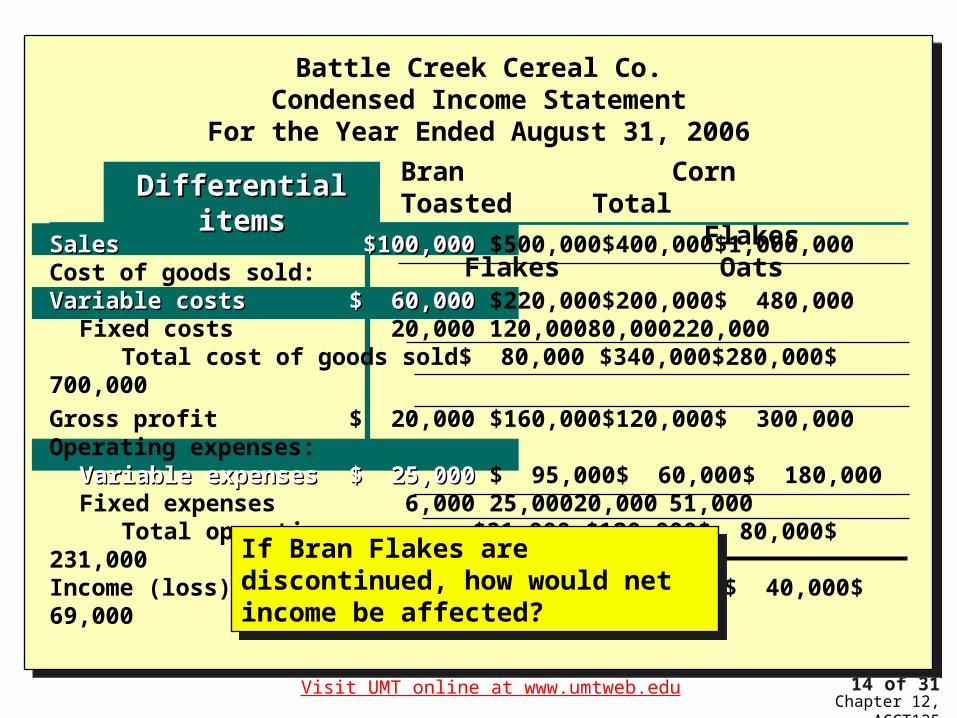

Battle Creek Cereal Co.Condensed Income Statement

For the Year Ended August 31, 2006

Bran Corn Toasted Total Flakes Flakes

Oats

Differential itemsDifferential items

SalesSales $100,000$100,000 $500,000 $400,000 $1,000,000Cost of goods sold: Variable costsVariable costs $ 60,000$ 60,000 $220,000 $200,000 $ 480,000

Fixed costs 20,000 120,000 80,000 220,000 Total cost of goods sold $ 80,000 $340,000 $280,000 $ 700,000

Gross profit $ 20,000 $160,000 $120,000 $ 300,000Operating expenses:

Variable expensesVariable expenses $ 25,000 $ 25,000 $ 95,000 $ 60,000 $ 180,000Fixed expenses 6,000 25,000 20,000 51,000 Total operating expenses $ 31,000 $120,000 $ 80,000 $ 231,000

Income (loss) from operations$ (11,000) $ 40,000 $ 40,000 $ 69,000If Bran Flakes are discontinued, how would net income be affected?

If Bran Flakes are discontinued, how would net income be affected?

Page 15

15 of 31Visit UMT online at www.umtweb.eduChapter 12,

ACCT125

Battle Creek Cereal Co.Condensed Income Statement

For the Year Ended August 31, 2006

Differential itemsDifferential items Bran Corn Toasted Total Flakes Flakes

OatsSalesSales $100,000$100,000 $500,000 $400,000 $1,000,000Cost of goods sold: Variable costsVariable costs $ 60,000$ 60,000 $220,000 $200,000 $ 480,000

Fixed costs 20,000 120,000 80,000 220,000 Total cost of goods sold $ 80,000 $340,000 $280,000 $ 700,000

Gross profit $ 20,000 $160,000 $120,000 $ 300,000Operating expenses:

Variable expensesVariable expenses $ 25,000 $ 25,000 $ 95,000 $ 60,000 $ 180,000Fixed expenses 6,000 25,000 20,000 51,000 Total operating expenses $ 31,000 $120,000 $ 80,000 $ 231,000

Income (loss) from operations$ (11,000) $ 40,000 $ 40,000 $ 69,000If Bran Flakes are discontinued, $15,000 of net income will be lost and overall net income would be reduced to $54,000.

If Bran Flakes are discontinued, $15,000 of net income will be lost and overall net income would be reduced to $54,000.

Page 16

16 of 31Visit UMT online at www.umtweb.eduChapter 12,

ACCT125

Annual variable costs—present $225,000Annual variable costs—new equip. 150,000Annual differential decrease in cost $ 75,000Number of years applicable x 5Total differential decrease in cost $375,000Proceeds from sale of present equipment 25,000 $400,000Cost of new equipment 250,000Net differential decrease in cost, 5-years $150,000

Annual net differential—new equipment $ 30,000

Proposal to Replace EquipmentNovember 28, 2006

Page 17

17 of 31Visit UMT online at www.umtweb.eduChapter 12,

ACCT125

Proposal to Replace EquipmentNovember 28, 2006

Present NewEquipment Equipment

This analysis indicates that it would be better to replace the existing equipment. What other factors should be considered?

This analysis indicates that it would be better to replace the existing equipment. What other factors should be considered?

Annual variable costs $ 225,000 $150,000 Number of years applicable x 5 x 5 Total variable costs $1,125,000 $750,000 Cost of new equipment 250,000 Less proceeds from sale (25,000) Total costs $1,125,000 $975,000

Net total benefit to replace $150,000 Net annual benefit to replaceNet annual benefit to replace $ 30,000 $ 30,000

Page 18

18 of 31Visit UMT online at www.umtweb.eduChapter 12,

ACCT125

Differential revenue from further processing per batch:Revenue from sale of gasoline [(4,000 gallons - 800 gallons evaporation) x $1.25] $4,000Revenue from sale of kerosene (4,000 gallons x $0.80) 3,200

Differential revenue $800Differential cost per batch:

Additional cost of producing gasoline 650Differential income from further processing gasoline per batch $150

Proposal to Process Kerosene FurtherOctober 1, 2006

Page 19

19 of 31Visit UMT online at www.umtweb.eduChapter 12,

ACCT125

Determine the selling price of a product using the total cost concept.2

Learning ObjectiveLearning Objective

Page 20

20 of 31Visit UMT online at www.umtweb.eduChapter 12,

ACCT125

Setting Normal Product Selling PricesSetting Normal Product Selling Prices

1. Demand-based methods

2. Competition-based methods

1. Total cost concept

2. Product cost concept

3. Variable cost concept

Cost-Plus MethodsCost-Plus Methods

Market MethodsMarket Methods

Page 21

21 of 31Visit UMT online at www.umtweb.eduChapter 12,

ACCT125

Per Unit TotalCost Cost

Cost Structure Example (100,000 units)Cost Structure Example (100,000 units)

Variable Costs:Direct materials $ 3.00 $ 300,000Direct labor 10.00 1,000,000Factory overhead 1.50 150,000Selling and admin. 1.50 150,000

Fixed Costs:Factory overhead .50 50,000Selling and admin. .20 20,000

Total costs $16.70 $1,670,000

Product costs $15.00 $1,500,000

Variable costs $16.00 $1,600,000

Page 22

22 of 31Visit UMT online at www.umtweb.eduChapter 12,

ACCT125

Per Unit TotalCost Cost

Cost Structure Example (100,000 units)Cost Structure Example (100,000 units)

Variable Costs:Direct materials $ 3.00 $ 300,000Direct labor 10.00 1,000,000Factory overhead 1.50 150,000Selling and admin. 1.50 150,000

Fixed Costs:Factory overhead .50 50,000Selling and admin. .20 20,000

Total costs $16.70 $1,670,000

Product costs $15.00 $1,500,000

Variable costs $16.00 $1,600,000

Page 23

23 of 31Visit UMT online at www.umtweb.eduChapter 12,

ACCT125

Per Unit TotalCost Cost

Cost Structure Example (100,000 units)Cost Structure Example (100,000 units)

Variable Costs:Direct materials $ 3.00 $ 300,000Direct labor 10.00 1,000,000Factory overhead 1.50 150,000Selling and admin. 1.50 150,000

Fixed Costs:Factory overhead .50 50,000Selling and admin. .20 20,000

Total costs $16.70 $1,670,000

Product costs $15.00 $1,500,000

Variable costs $16.00 $1,600,000

Page 24

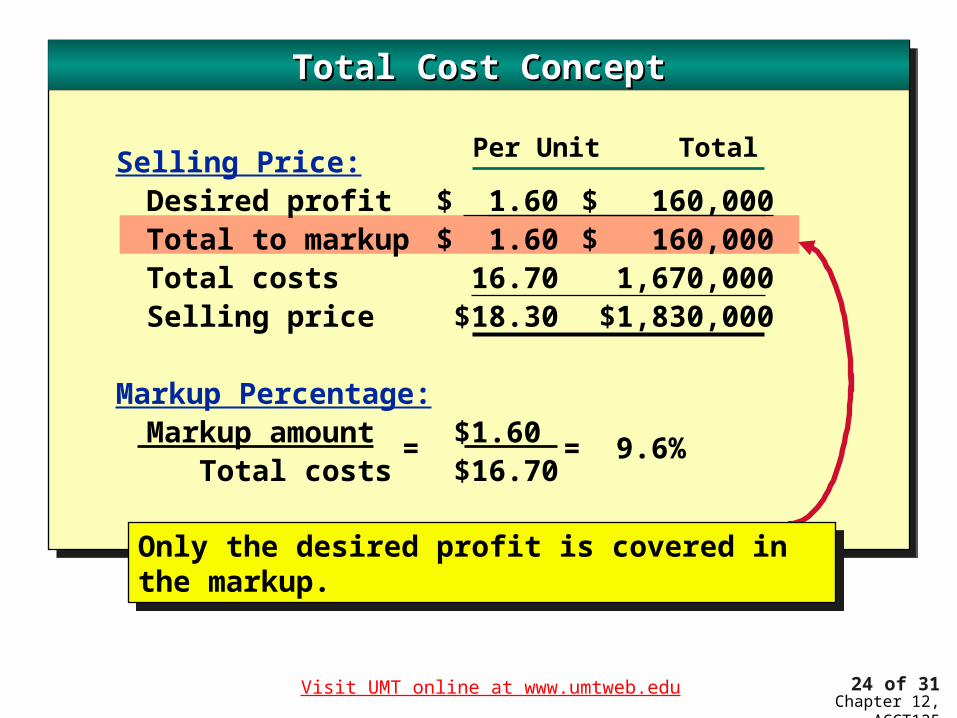

24 of 31Visit UMT online at www.umtweb.eduChapter 12,

ACCT125

Selling Price:Desired profit $ 1.60 $ 160,000Total to markup $ 1.60 $ 160,000Total costs 16.70 1,670,000 Selling price $18.30 $1,830,000

Markup Percentage:Markup amount $1.60 Total costs $16.70

Per Unit Total

Total Cost ConceptTotal Cost Concept

= 9.6%

Only the desired profit is covered in the markup.Only the desired profit is covered in the markup.

=

Page 25

25 of 31Visit UMT online at www.umtweb.eduChapter 12,

ACCT125

Per Unit TotalSelling Price:Desired profit $ 1.60 $ 160,000Total to markup $ 1.60 $ 160,000Total costs 16.70 1,670,000 Selling price $18.30 $1,830,000

Markup Percentage:Markup amount $1.60 Total costs $16.70

Total Cost ConceptTotal Cost Concept

= 9.6%

Markup on total costMarkup on total cost

=

Page 26

26 of 31Visit UMT online at www.umtweb.eduChapter 12,

ACCT125

Calculate the relative profitability of products in bottleneck production environments.3

Learning ObjectiveLearning Objective

Page 27

27 of 31Visit UMT online at www.umtweb.eduChapter 12,

ACCT125

Products—Unit Analysis Small Medium Large

Wrench Wrench Wrench

Sales price $130 $140 $160

Variable cost 40 40 40

Contribution margin $ 90 $100 $120

Profitability Under Production BottlenecksProfitability Under Production Bottlenecks

The process is currently operating at full capacity and is a production bottleneck.

The process is currently operating at full capacity and is a production bottleneck.

Page 28

28 of 31Visit UMT online at www.umtweb.eduChapter 12,

ACCT125

Sales price $130 $140 $160

Variable cost 40 40 40

Contribution margin $ 90 $100 $120

Bottleneck hours 1 4 8

Products—Unit Analysis Small Medium Large

Wrench Wrench Wrench

Profitability Under Production BottlenecksProfitability Under Production Bottlenecks

The number of hours per unit for each product.The number of hours per unit for each product.

Page 29

29 of 31Visit UMT online at www.umtweb.eduChapter 12,

ACCT125

Products—Unit Analysis Small Medium Large

Wrench Wrench Wrench

Profitability Under Production BottlenecksProfitability Under Production Bottlenecks

Contribution after dividing by the bottleneck hours.Contribution after dividing by the bottleneck hours.

Sales price $130 $140 $160

Variable cost 40 40 40

Contribution margin $ 90 $100 $120

Bottleneck hours 1 4 8

Bottleneck contribution $ 90 $ 25 $ 15

Page 30

30 of 31Visit UMT online at www.umtweb.eduChapter 12,

ACCT125

Products—Unit Analysis Small Medium Large

Wrench Wrench Wrench

Sales price $130 $140 $160

Variable cost 40 40 40

Contribution margin $ 90 $100 $120

Bottleneck hours 1 4 8

Bottleneck contribution $ 90 $ 25 $ 15

Profitability Under Production BottlenecksProfitability Under Production Bottlenecks

What price for Product C would equate its profitability to Product A?

What price for Product C would equate its profitability to Product A?

Page 31

31 of 31Visit UMT online at www.umtweb.eduChapter 12,

ACCT125

Products—Unit Analysis Small Medium Large

Wrench Wrench Wrench

Sales price $130 $140 $160 $760

Variable cost 40 40 40 40

Contribution margin $ 90 $100 $120 $720

Bottleneck hours 1 4 8 8

Bottleneck contribution $ 90 $ 25 $ 15 $ 90

Profitability Under Production BottlenecksProfitability Under Production Bottlenecks

A price of $760 will provide the same contribution as Product A.

A price of $760 will provide the same contribution as Product A.