24

www.german-renewable-energy.com Project Development Programme East Africa Rwanda’s Solar Energy Market Target Market Analysis www.renewables-made-in-germany.com

www.german-renewable-energy.com

www.german-renewable-energy.com

Project Development Programme East Africa

Rwanda’s Solar Energy Market

Target Market Analysis

www.renewables-made-in-germany.com

www.german-renewable-energy.com

Target Market Analysis

Rwanda’s Solar Energy Market

www.german-renewable-energy.com

Authors

Integrated Energy Solutions (IES):

Mark Hankins

Anjali Saini

Paul Kirai

December 2009

Editor

Deutsche Gesellschaft für Technische

Zusammenarbeit (GTZ) GmbH

On behalf of the

German Federal Ministry

of Economics and Technology (BMWi)

Contact

Deutsche Gesellschaft für Technische Zusammenarbeit (GTZ) GmbH

Potsdamer Platz 10, 10785 Berlin, Germany

Fax: +49 (0)30 408 190 22 253

Email: [email protected]

Web: www.gtz.de/projektentwicklungsprogramm

Web: www.exportinitiative.bmwi.de

This Target Market Analysis is part of the Project Development Programme (PDP) East Africa. PDP East Africa is implemented

by the Deutsche Gesellschaft für Technische Zusammenarbeit (GTZ) on behalf of the German Federal Ministry of Economics

and Technology (BMWi) in context of the Export Initiative Renewable Energies. More information about the PDP and about

renewable energy markets in East Africa: www.gtz.de/projektentwicklungsprogramm

This publication, including all its information, is protected by copyright. GTZ cannot be liable for any material or immaterial

damages caused directly or indirectly by the use or disuse of parts. Any use that is not expressly permitted under copyright

legislation requires the prior consent of GTZ.

All contents were created with the utmost care and in good faith. GTZ assumes no responsibility for the accuracy, timeliness,

completeness or quality of the information provided.

Target Market Analysis: Rwanda’s Solar Energy Market V

Content

1 STATUS QUO OF THE SOLAR ENERGY SECTOR ............................................................... 1

1.1 Brief Solar Sector Overview .................................................................................................................. 1

1.2 Major Market Segments ....................................................................................................................... 1

1.3 Local Capacities .................................................................................................................................... 4

2 MARKET POTENTIALS ............................................................................................................. 5

2.1 Overall Sector Outlook ......................................................................................................................... 5 2.1.1 Public Sector Market........................................................................................................................... 6 2.1.2 Private Sector PV ................................................................................................................................ 8

2.2 Undeveloped Market Opportunities ..................................................................................................... 9 2.2.1 Solar Water Heating (SWH) ................................................................................................................ 9 2.2.2 Grid-Connected Solar PV .................................................................................................................... 9

3 SOLAR-SPECIFIC REGULATION AND FRAMEWORK .................................................... 10

3.1 Policies and Regulations ..................................................................................................................... 10

3.2 Applicable Public Sector Support / Financing Mechanisms and Sources ............................................. 11

4 BUSINESS PARTNERS AND COMPETITORS .................................................................... 12

4.1 Overview of Key Solar Market Players ................................................................................................ 12

4.2 Overview of Major and/or Most Emblematic Projects ........................................................................ 14 4.2.1 Public Sector PV Investments ........................................................................................................... 14 4.2.2 Kigali Solair ........................................................................................................................................ 14

Target Market Analysis: Rwanda’s Solar Energy Market VI

List of Tables

Table 1: A Summary of Current Solar PV Market Activities in Rwanda ................................................................... 1

Table 2: MININFRA Solar Energy Related Budget 2009 ......................................................................................... 6

Table 3: Indicative ICT and PV System Procurements, 2008 Budget by MINEDU 2008 ........................................ 7

Table 4: The SHS Market in Rwanda ...................................................................................................................... 8

Table 5: Importing Companies of Rwanda's Solar Market .....................................................................................12

Table 6: Consultants; NGO's and Non-Government Projects ................................................................................13

Table 7: Government and Public Sector Projects ..................................................................................................13

Currency

1 USD = RWF 575 (May 2010)

1 € = RWF 708 (May 2010)

Measurement

W Watt Wp Watt peak Wh Watt hour

kW Kilowatt kWp Kilowatt peak kWh Kilowatt hour

MW Megawatt MWp Megawatt peak MWh Megawatt hour

GW Gigawatt GWp Gigawatt peak GWh Gigawatt hour

Target Market Analysis: Rwanda’s Solar Energy Market VII

List of Acronyms

ACDM Atelier Central de Maintenance

a-Si Amorphous Silicon

BBS Battery Based System

BTC Belgian Technical Cooperation

BTS Base Stations

BOS Balance of System (Components of PV Systems)

CDC Centre for Disease Control

CRS Catholic Relief Services

EGPAF Elisabeth Glaser Pediatric AIDS Foundation

ERC Electricity Regulatory Commission

FHI Family Health International

GEF Global Environment Facility

GLE Great Lakes Energy

HC Health Centre

ICAP International Centre for AIDS Care and Treatment Programmes

ICT Information and Communication Technology

JICA Japan International Cooperation Agency

LED Light Emitting Diode

MINIEDU Ministry of Education

MININFRA Ministry of Infrastructure

MTS Modern Technology Services

NGO Non-Governmental Organisation

PEPFAR President’s Emergency Plan for AIDS

PIH Partners in Health

PPA Power Purchase Agreement

PPP Purchasing Power Parity

PV Photovoltaic

PVMTI Photovoltaic Market Transformation Initiative

SELF Solar Electric Light Fund

SHS Solar Home System

SWH Solar Water System

UNDP United Nations Development Programme

USAID United States Agency for International Development

x-Si Chrystalline Silicon

Target Market Analysis: Rwanda’s Solar Energy Market VIII

Summary

Rwanda is a densely populated, small country with a relatively low average income. Its small solar

market was less than 60 kWp/annum in 2008 and total installed capacity is estimated to be below 1

MWp.

Solar power in Rwanda is mainly a procurement market for government and NGO institutional

systems though there is an increasing demand for solar home systems. In 2008, Kigali Solair (up to

now the largest solar PV project in Sub-Saharan Africa), injected 250 kW to the grid and plans are to

expand to 1 MW. But still there remains no renewable energy feed-in tariff.

Rwanda is well-positioned to serve as an export market within the Great Lakes region. Since it is

based mostly on procurement, current demand is extremely unpredictable and irregular. The future

outlook however seems promising. High electricity prices, combined with some favourable policy

indicate future opportunities in the solar water heater industry and also in the grid-connected solar PV

market towards 2015. The government’s solar energy related budget 2009 allocated USD 1.72 million,

excluding project-related work, the majority will be spend for a strategic study of renewable energy.

Target Market Analysis: Rwanda’s Solar Energy Market 1

1 Status Quo of the Solar Energy Sector

1.1 Brief Solar Sector Overview

Rwanda receives an annual solar radiation of 5.2 Wh/m

2/day. This represents a good potential for

solar PV development. Like most countries in the region, solar radiation is considerably variable, and

months in the cloudy season have average irradiation levels of below 4.5 Wh/m2/day.

A combination of high electricity and fuel prices, and a growing economy, as well as export

opportunities into the Democratic Republic of the Congo (DRC), should increase the overall demand

for solar PV equipment in Rwanda. However, due to the small size of the country, the medium to long-

term off-grid opportunities will gradually decrease as the grid network is enlarged and coverage made

denser. Despite of the high cost for electricity in Rwanda (USD 0.21 kWh), the solar PV market is still

undeveloped. Current demand for PV is below 60 kWp/annum and total installed capacity is estimated

to be below 1 MWp.

The current installed capacity of Rwanda’s energy sector amounts more than 85 MW, however, the

country needs a total of at least 100 MW to meet present demand and sustain its economic growth. In

Rwanda has a net deficit of power with a national electrification rate of 8 % and a rural electrification

rate of 1 %. There is a government target to double the electrification rate, increasing connections to

16 % of the population (equal to 200,000 connections) up from the current 100,000 customers by

2012 at a cost of USD 400 million.

Government and NGO programmes, electrification targets for rural health, educational facilities, and

government administrative offices are the key drivers of the Rwandan solar energy market. While the

demand for solar home systems appears limited, there has been a recent growth in this sector due to

an increasing (but still small) middle-income community. The Rwandan Government is working with

partners such as the European Union, the World Bank and the Belgium Government to install solar PV

in public health centres, schools and government administration facilities in the rural areas. Their total

installation target is approximately 200 kWp in solar PV installations commencing in 2009.

Rwanda is also home to the “largest single solar installation” in Africa - the “Kigali Solair” solar power

plant - that generates 250 kW and feeds into the national electricity grid. The plant was funded by the

German municipal power company Stadtwerke Mainz and installed by the German company Juwi in

2008.

1.2 Major Market Segments

There are several active market segments in the solar PV market, elaborated below and in Table 1:

Table 1: A Summary of Current Solar PV Market Activities in Rwanda

Solar PV technology Size of

opportunity

Estimated kWp

installed/year (2008)

Notes

Government administrative

centres

>0.4 MWp ±15 kW Good government contacts

required

Government clinics and schools >1 MWp ±40 kW World Bank, EU, Belgium

NGO & NGO health sector >0.3 MWp <±5 kWp PEPFAR

Solar Home System >4 MWp N/A Low rural spending power

TOTAL >6 MWp >50kWp

Target Market Analysis: Rwanda’s Solar Energy Market 2

Government programmes

The Rwandan Government has an excellent relationship with donors and relies on donor support for

budget support and infrastructure development. It issues tenders for the installation of solar PV in

schools, health centres and clinics, as well as administrative centres (sector offices). Relationships

with key donors, including the European Union, the World Bank, the US Government (through the

United States Agency for International Development (USAID) and the President’s Emergency Plan for

AIDS (PEPFAR)) and the Belgian Government, will enable Rwanda to aggressively pursue – and in all

likelihood achieve – a high level of electrification of government institutions.

Administrative centres. There are 145 such sector offices currently un-electrified. Out of the

total 496 centres, 86 run on diesel generators and 116 on solar PV. The central government

issues three to four tenders per year1. District governments contract directly with the

contractor and public tenders are not always announced.

Health centres and schools. The World Bank, the European Union and Belgian Technical

Cooperation (BTC) will be funding solar electrification of government health centres and

schools over the next five years. The objective is to cover all non-electrified institutions. These

procurements may cumulatively be larger than 200 kWp.

Non-Government organisation procurements

In addition to the government programmes, various donor-led programmes to electrify Health Centres

in Rwanda are under way. PEPFAR/USAID, which spent over USD 120 million in Rwanda in 2008, is

supporting programmes to electrify the hundred plus health centres that proving anti-retroviral, HIV

testing and counselling services.

Implementing partners (who manage programme, and purchase energy systems) include the Catholic

Relief Services (CRS), Partners in Health, Intra Health, International Centre for AIDS Care and

Treatment Programmes (ICAP), and Family Health International (FHI), EGPAF and Columbia

University. Together they have installed a few tens of kW of PV over the last three years. In the future,

battery backups with inverter systems will also make up a large part of this growing demand.

The implementing partners carry out the above contracts. Each partner carries out tenders according

to their own process, and these processes differ considerably. For example, Columbia University

purchased all of its equipment in the US through a US NGO, while CRS and FHI both purchase

equipment on the local market. USAID and PEPFAR may complete a larger procurement project in

the near future.

Solar Home Systems (SHS)

Solar home systems will be an important sector for future growth in PV. Presently, most of the likely

customers include middle class customers with homes in off-grid rural areas including teachers,

business people, church leaders and NGOs. Only one company called Modern Technology Services

(MTS) (see section 4) is aggressively exploiting this market at present.

Great Lakes export opportunities

Because Kigali is strategically located to serve consumer needs of eastern Congo (Goma, Kivu),

Burundi and parts of Uganda, many business people sell products into these regions from Kigali. Solar

PV providers consistently mentioned that they serve these markets, and that they make up a

significant portion of their business.

1 Tenders are issues by district agencies. Quality of tender documents is mixed and there is a lack of quality

design work and specification in tender documents.

Target Market Analysis: Rwanda’s Solar Energy Market 3

Predominate operator models

The Rwandan solar PV market is an early-stage market of small players that is poorly integrated into

the global and regional solar energy industry. Six to eight companies compete in the market, but only

two of them sell over 15 kW per year (see section 4). In general, companies are involved in PV as a

side-business. The PV business was better developed before the genocide, but, as with other sectors,

demand collapsed during 1993/94 and did not pick up again until ten years after the war. Total

“normal” demand for PV is unlikely to be more than 60 kW per year, but an increasing number of large

projects have made this number grow quickly and it is likely that there is a substantial “invisible” /

under the counter market. As with other countries in early stages of PV development, much of the

business is channeled through the donor sector, and some local companies have poor access to

these projects. In 2008, over 30 % of the total demand was in a single procurement by a donor agent

that avoided taxes and duties.

PV and balance of system (BOS) prices are much higher than in other parts of the region. Module

costs well over USD 10 per watt are common. PV system components such as batteries are also very

highly priced. This means fully installed systems often cost over USD 20 per watt. Equipment is

sourced from Europe and Asia; solar companies tend to be linked with European partners.

The high price regime favors a contracted approach to sales rather than over the counter. Only two

companies were able to provide price lists. High prices are caused by high duties2, lack of competition

and lack of availability of components on the market, and the consequent need to source individual

purchases rather than buy in volume or stock. It is interesting to note that, despite increasing activity in

Rwanda’s PV demand since 2007, there is little interest in the market among the large (i.e. Kenyan)

regional players. This has to do with the fact that local Rwandan companies do not actively seek to

lower prices or become more competitive (i.e. by seeking out lower prices), as their customers

(donors) have previously been willing to pay high prices and there is little competition.

Only two companies displayed a strong linkage with PV companies outside of the country (see section

4). Many dealers were not conversant with recent developments in PV and inverters – technologies

that change almost monthly. As well, rather than taking an educative approach to customers, some

dealers “mystify” the technology, making it seem like something that the layman customer would not

be able to understand.

Companies maintain very little stock, instead relying on tenders and projects to gain business. In this

regard, solar PV is like a contracting business. Equipment is procured after the deal is made and little

is kept in stock. One or two companies (MTS, SECAM) are more customer-oriented than others (a

favorable trend). But in general all companies rely on clients that come back, such as NGOs,

churches, the military or projects and are willing to pay premium prices. Very few companies are

attempting to build volumes by supplying to agents.

Some companies complain that multilateral and government tenders are not conducted transparently

and that the donor-controlled aspects of the market make it difficult to participate. Some companies

interviewed do not participate in tenders any more because of the time consuming nature of bid

preparation and the lack of “fair” evaluation of tenders. Surveys carried out by this consultant have

found that many government-tendered systems are installed without proper design or specification

work. One of the problems is that “government” tenders are put together by District officials, Ministry of

Health officials, and the military or other government departments. There is no accepted methodology

for designing and procuring PV systems.

2 Duties amounted to over 60 % of the cost of systems until they were recently removed. However, dealers

complained that customs officials were unaware of the removal of duties and still charged them.

Target Market Analysis: Rwanda’s Solar Energy Market 4

1.3 Local Capacities

There are five to six players active in the Rwandan solar energy sector, and they are the primary

repositories of solar energy skills (as well as a number of independent contractors). These include

SECAM, Modern Technical Services (MTS), Davis & Shirtliff, Great Lakes Energy, EPS Renewable

and the Solar Electric Light Fund (SELF)3 (see section 4 for more information). In addition, the Kigali

Institute of Technology has conducted basic solar training courses with SELF. As well, the Atelier

Central de Maintenance (ACDM, the Maintenance workshop for the Ministry of Health) plays a role in

maintenance of health equipment, though it does not have well-developed solar energy expertise. It

does have qualified technicians at district level who can easily be trained to maintain PV systems.

There is also some regional expertise in solar energy in smaller towns. For example, Family Health

International (FHI) – who are one of the main players in electrification of PEPFAR health centres –

have a small network of solar PV technicians.

Rwandan solar energy companies are just beginning to build up capacities. Their products are rather

expensive (over USD 20/Wp), and there is limited capacity to design and deliver sophisticated PV

systems and battery backups. Furthermore, other groups that might provide technical service, such as

the Atelier Central de Maintenance (ACDM) in the Ministry of Health or the Ministry of Infrastructure

(MININFRA), are over-stretched and poorly equipped to provide services4. Nevertheless, as described

below, some groups have recently provided capacity building services in the country.

Training programmes have been conducted sporadically be a variety of players in the past ten years.

Unfortunately, there is no coordinated repository of trained PV technicians, and as yet there is no

accepted code of practice or curriculum for PV in the country in university or among technician

practitioners. Some of the classes carried out include:

PEPFAR-sponsored classes to develop local knowledge to maintain the solar PV and health

centre energy systems. The Atelier Central de Maintenance (ACDM) was involved in these

classes.

SELF/Kigali Institute of Science and Technology classes on basic solar PV. SELF also trained

a dozen technicians to install sophisticated hybrid PV-generator systems as part of its

Columbia University work.

The Centre for Disease Control (CDC) is collaborating with Toluene University of Columbia for

development of capacity for energy management and maintenance of the solar PV systems in

the health centres.

The Japan International Cooperation Agency (JICA) is supporting a college with the Ministry

of Education (MINIEDU) to train solar technicians.

Stadtwerke Mainz, the German company that installed the grid-connected system trained a

network of regional PV technicians.

The EU solar programme of the MININFRA plans to train technicians.

Bidders for various government solar PV contracts are required to include a component for

training of technicians.

3 SELF does not maintain a local office but has contracted with PEPFAR partners to install dozens of institutional

systems. It has conducted several training programmes to install large health centre systems. 4 Although ACDM is designated as the provider of maintenance service for health care centres, it has only two

vehicles and less than 25 staff who must provide all maintenance skills for the entire country’s health sector.

Target Market Analysis: Rwanda’s Solar Energy Market 5

Strengths and weaknesses of local capacities

All the local companies have limited capacity to install large scale projects. For example, MTS, Davis

& Shirtliff, and SECAM are dealers for other types of goods and services including diesel generators,

pumps and general hardware.

Several large tenders have been announced for sectors (i.e. the Global Fund tender for the health

sector). As mentioned previously, PV experts do usually not design such tenders and the system

designs are not adequate for international companies to bid on. There is a critical lack of capacity to

design, specify and prepare procurement documents for PV systems among government and project

staff. This means that is it often impossible for professional PV suppliers to prepare bids, as the

documents on which their bids are based do not enable proper sizing and elaboration of systems.

Therefore companies often win them without experience in PV technology.

In other cases, government tenders are often announced in small tranches on regional levels to be

handled by small local companies. Well-connected small contractors, not necessarily importers-

suppliers, often win such contracts. Many of them do not have fulltime technicians – let alone

engineers. They contract technicians on an as-needed basis.

Complaints of poor installation as a result of bad workmanship or components are common. There is a

task force in the MININFRA to establish some basic standards for solar PV equipment and installation.

An international NGO is set to start producing PV modules from second quality silicon wafers and to

sell them in the local market at discounted prices. This is expected to build local capacity in basic

production and assembly of PV modules, which could extend to better installation practice.

2 Market Potentials

2.1 Overall Sector Outlook

The overall outlook for solar in Rwanda is that the government and donor projects will continue to

dominate the market in the short and medium term. Demand by private sector for solar products

remains limited, but may become an important niche market.

There are over one million households in Rwanda, out of which only 8 % have access to grid

electricity, with most connections in the main cities (Kigali alone accounts for nearly 75 % of total

electricity consumption). Electrogaz is the country’s only power generation and distribution company.

It has an installed domestic capacity of about 27 MW that is barely sufficient to cover half of its peak

demand. The other half is imported from Rusizi - a consortium of the electric utilities of the Democratic

Republic of the Congo (DRC), Rwanda, and Burundi. Electricity sales have been growing at a rate of

about 7 % p.a. on average since 1997. Supply constraints kept sales artificially low.

In 2008, the Kigali Solair solar PV plant fed 250 kW into the grid. Another 4.5 MW has been connected

from the initial phase of the Lake Kivu methane gas project. Even then, the utility is faced with a

generation deficit and still has to rely on thermal generation to meet peak demand.

Target Market Analysis: Rwanda’s Solar Energy Market 6

2.1.1 Public Sector Market

The government plans to increase grid connection to 16 % by 2012 at a cost of USD 400 million. This

will require a combination of expanded grid extension and new power generation. By the year 2020,

the grid coverage is projected to reach 35 %.

In the past ten years, several hundred kWp of solar has been installed off-grid in Rwanda, mainly in

health care centres, schools and administration buildings. The planned government budget

expenditures for solar energy in 2009 (which do not include projects) are summarised in Table 2.

Table 2: MININFRA Solar Energy Related Budget 2009

Project Amount (RWF) USD

Rural electrification with solar energy 250,000,000 450,500

Access to energy in rural areas 130,000,000 234,000

Strategic study/renewable energies 575,000,000 1,036,000

Total 955,000,000 1,720,000

Current tenders and projects:

European Commission (EC) programmes at MININFRA. The project will spend 7 million Euros

over the next five years on solar electrification of at least 350 institutions – ranging from

schools, health care centres and administration offices with 1.5 – 2.5 KW each. The

programme will be implemented by the private sector through tenders by the Ministry.

Belgian Technical Cooperation (BTC). This programme aims to electrify 60 health care

centers with a budget of 1.5 million Euros in its first phase from 2009-2010. It is targeting

about 1 kWp per health care centre.

The World Bank is currently supporting a major rural electrification initiative in Rwanda. It is

expected to provide the government rural electrification programmes with considerable

resources, a significant portion of which will be renewable and PV.

Government administration: The energy supply of the 496 government offices is as follows:

146 centrally supplied by Electrogaz

205 supplied by:

Solar PV (116)

Diesel generators (86)

Micro hydro (3)

145 un-electrified

From the above, more than 230 government sector offices (including diesel operated ones) will

potentially be supplied, through government procurements, by solar PV with a requirement of as much

as 300 kWp.

Health care sector

Out of the 528 health care centres in rural areas, 50 % have been electrified (with grid connections,

generators or solar). Around 300 private health care centres currently lack electricity. A programme

administered by the government in collaboration with partners and NGOs aims to electrify all rural

health care centres in the country. In 2009, the UN Global Fund for AIDS issued a tender for 34 health

facilities, while the Belgian Technical Cooperation (BTC) programme covers another 60.

Target Market Analysis: Rwanda’s Solar Energy Market 7

Projects will be done mainly through tenders where the government invites eligible firms to bid for the

contracts5. As mentioned previously, a major area of concern has been the tender specifications,

supervision and quality of installation.

Education sector

A decision by the government to include English as an official language will most likely lead to an

increase in electronic broadcasting and information communication technology (ICT) applications

which could stimulate the demand for solar PV – especially in rural areas. Rwanda is rated highly

among African countries with regards to ICT adoption, and this could also spur the growth of PV

market as many NGOs and homes acquire computers and telecommunication/entertainment devices.

There are plans by the government – through the Ministry of Education (MINEDU) to have ICT in all

schools in the country. This is another major driver for PV development in Rwanda. The total Ministry

of Education budget for solar PV to promote ICT in 2008 was RWF 1,350,000,000 (Table 3).

Table 3: Indicative ICT and PV System Procurements, 2008 Budget by MINEDU 2008

Type of school Amount RWF USD

Primary school 500,000,000 901,000

Junior secondary school 400,000,000 721,000

Upper secondary education 400,000,000 721,000

Teacher training and colleges of education 50,000,000 90,100

TOTAL 1,350,000,000 2,433,100

Recommendations to German enterprises

Work closely with existing traders. Seek those that maintain good government contacts and

that have a track record of completing contracts for the government (see section 4 for

company lists).

Develop networks of local agents and installers (it may be helpful to seek graduates of

previous programmes). Provide in-service training.

Understand the procurement procedures of the government.

Ensure that the local agent understands your equipment and is equipped with a suitable

amount of spares.

When funds originate from a donor, make an effort to communicate your company’s desire to

participate in any tender with both the government and the donor.

5 Companies interested in these programmes should contact the Ministry of Infrastructure, the Ministry of Health

or the relevant donors supporting the projects.

Target Market Analysis: Rwanda’s Solar Energy Market 8

2.1.2 Private Sector PV

Solar Home Systems (SHS)

The limiting factor for the deployment of SHS sector is the extremely low purchasing power of rural

populations. With a purchasing power parity (PPP), adjusted per-capita income of USD 1,206 (161 out

of 177 total countries), not many rural consumers can afford solar systems in Rwanda. However, the

economy has been growing moderately and is expected to spur demand for solar home systems.

Extension of mobile phone coverage will increase the need for phone charging possibilities around the

country. As well, expansion of television coverage will lead to an increase in the number of private

television sets and also spur the solar home market.

Growth in the SHS sector is slow but encouraging with at least three companies actively marketing

their products. Given the low-income level of the country, this report estimates that less than 10 % of

the total off-grid rural population (1.7 million un-electrified) would have an interest in a 10-50 Wp PV

system and another 30-40 % would be interested in a micro system. Table 4 provides a basic model

for this market:

Table 4: The SHS Market in Rwanda

Type of solar home systems Size of system

(Wp)

Estimated % of

households buying

Total number Size of market

(kWp)

No System 0 55.0% 944,690 -

Micro Systems 2 35.0% 601,166 1,202

One Light & Radio 10 7.3% 124,527 1,245

Two light and radio system 20 2.0% 34,352 687

Four light system or higher 50 0.5% 8,588 429

Larger systems (inverter or

hybrid)

150 0.3% 4,294 644

TOTAL 100.0% 1,717,618 4,208 kWp

Telecommunication

The telecommunications sector has not been – and will not be – a major client though the

government/donors have subsidised the use of solar energy in a couple of base stations (BTS) in

remote areas to enable mobile coverage. There would be the opportunity to extend the coverage of

mobile phones if the mobile phone companies made use of more solar PV.

At least one major dealer of PV in Kigali has recognized this opportunity and is developing a solution

for mobile phone companies. As in other East African countries, a small market for PV-powered phone

charging devices is likely to develop.

Recommendations to German enterprises

Work closely with existing traders. Select traders that have experience selling goods into the

consumer and private market (see section 4).

Develop networks of local agents and installers (it may be helpful to seek graduates of

previous programmes). Provide service training.

Develop a marketing strategy for rural households, NGOs and other groups.

Ensure that the local agent understands your equipment and is equipped with a suitable

amount of spares.

Connect your Rwandan agent with other players in the East African market with which you are

associated.

Target Market Analysis: Rwanda’s Solar Energy Market 9

2.2 Undeveloped Market Opportunities

2.2.1 Solar Water Heating (SWH)

Many households, hotels and institutions in Kigali use electricity to heat water. Given current tariff

rates this amounts to costs close to USD 100 per month and boiler. The use of electricity for water

heating is extremely expensive, and is often the most expensive part of a business’ or household’s

electricity bill.

At present, there are only a few providers of solar water heaters (SWH) in the country, and the market

is only in its early stages. Prices for SWH are extremely high and few players trade aggressively in

this market. The two primary markets are private households and tourism. Assuming 15 % of the

existing electrical connections have a boiler, the base potential market is about 15,000 households

and commercial establishments. Government legislation will require new buildings to include SWHs in

their design. This will provide impetus to the development of the SWH market.

Recommendations to German enterprises

Approach large hotels, developers, urban-based customers, NGOs, health sector supporters

and finance agencies.

Monitor government solar water heating programmes and legislation closely. This is best done

through use of partner companies.

Meet with government and donors to discuss how SWH programmes can be rolled out. Note

that energy legislation is primarily made in MININFRA.

Advertise in the media stressing how investments in solar pay back quickly. Any advertising

campaign would best be planned with a local partner.

Develop partnerships with companies that are familiar with the tourism and housing industry

(not necessarily solar PV companies). These include contractors, architects, service

providers, etc.

2.2.2 Grid-Connected Solar PV

Grid connected PV is not considered in existing government policy. As mentioned below, high level

interest in grid connected solar is not explicitly mentioned. Hydro, diesel generation, regional

interconnection and methane-fired generation are the current major focus for national power supply.

Three things make the prospect of grid connected PV perhaps more interesting in Rwanda than in

other parts of Africa:

Rwanda already has experience with Africa’s currently largest grid connected PV system.

Electricity prices are among the highest in Africa and Rwanda has a major shortfall of

electricity. At USD 0.21, grid parity is not far away.

Unlike other countries in the region, the power sector in Rwanda is managed in a transparent

manner and with government incentives it would be fairly easy for a project to be developed.

Interest in grid-connected systems would likely be higher from consumers (who could combine

systems with power backups and off-set power prices) than from the power company. Note that peak

power demand occurs in the evening, not during the day, so Electrogaz would be unlikely to pay a

premium for PV power.6 Government dispensations in favor of grid connection would be required. In

6 The initial 250 kWp solar array outside Kigali was installed chiefly as a demonstration, and proper long-term

price agreements were not reached.

Target Market Analysis: Rwanda’s Solar Energy Market 10

order for this to happen, there would have to be development of financial, technical and legal

protocols that are independently supported. However, currently there is no signal to believe that the

government would be broadly supportive of any initiative.

3 Solar-Specific Regulation and Framework

3.1 Policies and Regulations

Rwanda is well-known for being a leader in governance in the region since the genocide, and as such,

it has attracted significant amounts of donor support during the last 15 years. Much of this support is

targeted at the energy sector. As well, the government is aggressively pursuing rural electrification

strategies which include Renewable Energy components. What is missing is a strong internal capacity

to develop and build appropriate energy policy regimes. Given the urgency of the energy problems

faced, the lack of skilled manpower and the lack of finances, it is not surprising that there is not a well-

developed solar energy policy. For better or for worse, much of the policy development in Renewable

Energy occurs on an “ad hoc” basis, often as a result of donor advice.

The government is focused on rural development, poverty alleviation and creation of business

opportunities. As such, its energy policy is designed to support these overarching goals.7

The national energy policy objectives are to ensure availability of reliable and affordable energy

supplies and their use in a rational and sustainable manner in order to support national development

goals. The national energy policy, therefore, aims to establish an efficient energy production,

procurement, transportation, distribution and end-use systems in an environmentally sound and

sustainable manner.

In the 2004 Energy Policy, solar energy is only mentioned broadly as a “potential” source of energy,

and as a part of its strategy to electrify off-grid areas. Rwanda does not have the budget to invest

heavily in Renewable Energy outside of its immediate development targets (and donors who provide a

large portion of government support limit expenditures to immediate priorities).

Unlike other countries in the region, Rwanda has neither a stand alone electricity regulator or rural

electrification agency. Other government departments (within MININFRA) play this role. The key

government institutions involved in renewable energy policy making and procurement include:

The Ministry of Infrastructure (MININFRA): The Ministry is responsible for the build up of

national energy infrastructure. Rural energy is part of this mandate, however, staffing and

funding requirements restrict what MININFRA is able to effectively do. The MININFRA views

its role in the off-grid energy sector to include training, strategy development, development of

technical specifications for energy equipment, recommendation of strategies for the

development of the private sector and follow up work on the above.

Ministry of Health: This Ministry is actively involved in procurement of solar equipment for

remote health care centres.

Government policy to promote rural electricity access is primarily based on the extension of the

Electrogaz network as the most cost effective means. However it recognises that where customers

are not clustered close enough for grid service, solar PV, generators or hydro power may be offered

through private suppliers.

7 Rwanda Government Energy Policy 2004.

Target Market Analysis: Rwanda’s Solar Energy Market 11

For long term costs and environmental reasons, the government is developing large scale PV

procurements for rural administration, health and education facilities. Priority action number four of the

energy policy is the only place where solar energy is specifically mentioned as part of implementable -

government programmes. The government, in theory, also supports commercial sales of solar PV to

off-grid private sector customers and households. Theoretically, the government has removed duties

and taxes on solar equipment. However, in a 2008 study, companies complained that customs agents

still charged duties on solar equipment.

So far Rwanda has not developed Renewable Energy feed-in tariffs, despite the implementation of a

250 kWp grid-connected project (which was given a spill contract by Electrogaz). As mentioned

above, grid connected solar power is not a priority, as the government is focused on building up base

load supply at low costs in order to be able to meet peak demand.

The government recognises that demand side management can play a role in reducing peak

electricity demand, as well as in lowering energy costs for consumers. To this end, they are promoting

compact fluorescent lamps and solar water heaters (to replace electric boilers). The building code8

was recently revised so that it requires new buildings to install solar water heaters and is likely to

activate development of the solar water heating market.

3.2 Applicable Public Sector Support /

Financing Mechanisms and Sources

Except for the procurements mentioned in section 2, no direct public sector support or financing

mechanisms are available through government programmes for solar. Government involvement is

mainly in the form of government tenders and contracts.

Nevertheless, the government has removed all taxes on solar equipment, which should have an

impact on pricing.

8 Discussions with Naceur Hammami, Ministry of Infrastructure Energy Expert

Target Market Analysis: Rwanda’s Solar Energy Market 12

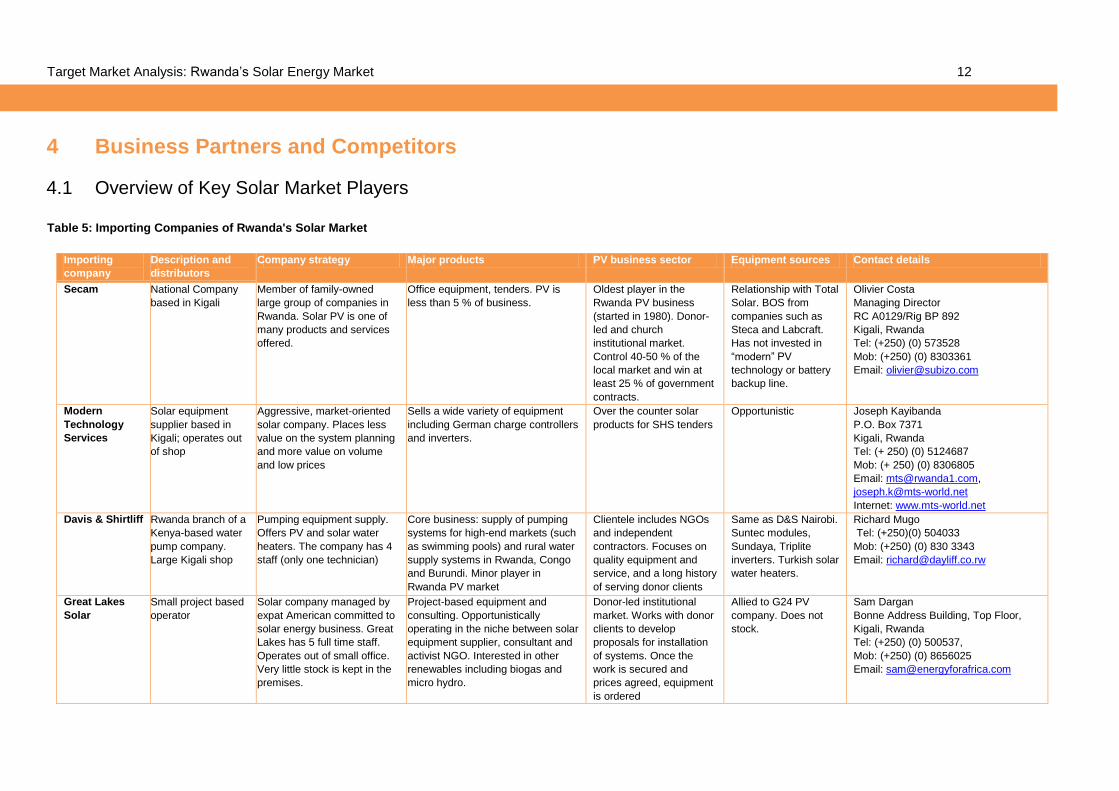

4 Business Partners and Competitors

4.1 Overview of Key Solar Market Players

Table 5: Importing Companies of Rwanda's Solar Market

Importing

company

Description and

distributors

Company strategy Major products PV business sector Equipment sources Contact details

Secam National Company

based in Kigali

Member of family-owned

large group of companies in

Rwanda. Solar PV is one of

many products and services

offered.

Office equipment, tenders. PV is

less than 5 % of business.

Oldest player in the

Rwanda PV business

(started in 1980). Donor-

led and church

institutional market.

Control 40-50 % of the

local market and win at

least 25 % of government

contracts.

Relationship with Total

Solar. BOS from

companies such as

Steca and Labcraft.

Has not invested in

“modern” PV

technology or battery

backup line.

Olivier Costa

Managing Director

RC A0129/Rig BP 892

Kigali, Rwanda

Tel: (+250) (0) 573528

Mob: (+250) (0) 8303361

Email: [email protected]

Modern

Technology

Services

Solar equipment

supplier based in

Kigali; operates out

of shop

Aggressive, market-oriented

solar company. Places less

value on the system planning

and more value on volume

and low prices

Sells a wide variety of equipment

including German charge controllers

and inverters.

Over the counter solar

products for SHS tenders

Opportunistic Joseph Kayibanda

P.O. Box 7371

Kigali, Rwanda

Tel: (+ 250) (0) 5124687

Mob: (+ 250) (0) 8306805

Email: [email protected],

Internet: www.mts-world.net

Davis & Shirtliff Rwanda branch of a

Kenya-based water

pump company.

Large Kigali shop

Pumping equipment supply.

Offers PV and solar water

heaters. The company has 4

staff (only one technician)

Core business: supply of pumping

systems for high-end markets (such

as swimming pools) and rural water

supply systems in Rwanda, Congo

and Burundi. Minor player in

Rwanda PV market

Clientele includes NGOs

and independent

contractors. Focuses on

quality equipment and

service, and a long history

of serving donor clients

Same as D&S Nairobi.

Suntec modules,

Sundaya, Triplite

inverters. Turkish solar

water heaters.

Richard Mugo

Tel: (+250)(0) 504033

Mob: (+250) (0) 830 3343

Email: [email protected]

Great Lakes

Solar

Small project based

operator

Solar company managed by

expat American committed to

solar energy business. Great

Lakes has 5 full time staff.

Operates out of small office.

Very little stock is kept in the

premises.

Project-based equipment and

consulting. Opportunistically

operating in the niche between solar

equipment supplier, consultant and

activist NGO. Interested in other

renewables including biogas and

micro hydro.

Donor-led institutional

market. Works with donor

clients to develop

proposals for installation

of systems. Once the

work is secured and

prices agreed, equipment

is ordered

Allied to G24 PV

company. Does not

stock.

Sam Dargan

Bonne Address Building, Top Floor,

Kigali, Rwanda

Tel: (+250) (0) 500537,

Mob: (+250) (0) 8656025

Email: [email protected]

Target Market Analysis: Rwanda’s Solar Energy Market 13

SOS Energie Kigali based solar

energy contractor

and solar water

heater assembler

5-year-old business operated

as a side-business out of a

separate auto-repair

business, Garage Sebalex

SAPL

Supplies by order, and maintains no

supply or storefront. Contracts with

Rwandan military and donors

Experienced solar system

designer and sub-

contracts a team of six

electricians, three

engineers and two

plumbers. He was trained

by the ex-head of

SECAM.

Supplies equipment

from French

companies such as

Total Energie

Sebastien Houben

Managing Director

PO Box 417, Av. de la Justice

Kigali, Rwanda

Tel: (+250) (0) 576060,

Mob: (+250) (0) 8301780

Email: [email protected],

Table 6: Consultants; NGO's and Non-Government Projects

Full name Role in sector Activities Procurements (types of

equipment/services)

Volume kWp or USD Plans in immediate

future

Contact details

PEPFAR/

Centers for

Disease Control

Health sector

project

Involved in control of HIV/

AIDS. Strengthening of

health sector institutions

Occasional purchase of energy

equipment

USD100's of K per year Not known Mary Hadley

Mob: (+250) (0) 830 2140

Email: [email protected]

Table 7: Government and Public Sector Projects

Full name Role in sector Activities Procurements (types of

equipment/services)

Volume kWp or USD Plans in immediate

future

Contact details

Ministry of

Infrastructure

Energy sector

policy and

leadership

Development of energy

projects

Health, education and military

sector purchase of solar equipment

Large procurements

planned

Not known Naceur Hammami, Alexis Karani

BP 24

Kigali, Rwanda

Email: [email protected],

BTC-CTB

Belgian

Technical

Cooperation

Energy

infrastructure

support

Launching project to install

PV systems in 30 clinics

around the country

PV equipment supply for clinics Estimated 3 million Euros Project being

developed

Erik Van Malderen

Rue Député Kayuku, 41, B.P. 6089

KigaIi, Rwanda

Tel: (+ 250) (0) 500267,

Mob: (+250) (0) 8305107

Email: [email protected]

World Bank Energy Unit,

Africa Region

Supporting Rwandan

Government in design of

rural energy projects

Procurement through Government

of Rwanda

Not known Project being

developed

Erik Fernstrom

Tel: (+250) (0) 591318, 5396318

Email: [email protected]

Target Market Analysis: Rwanda’s Solar Energy Market 14

4.2 Overview of Major and/or Most Emblematic Projects

4.2.1 Public Sector PV Investments

PV installations in the public rural institutions are the most significant projects in Rwanda. These are

government led initiatives and are expected to dominate the market for a while until the solar home

market develops and the private institutions take up solar. Projects are at various stages of

development. Interested players should contact the Ministry of Infrastructure (see section 4.1).

Projects include the following:

Ministry of Infrastructure / BTC installation of solar powered clinics. BTC has made

available three million Euros for the installation of about 30 solar powered clinics in the

country. The project is in a late stage of development (see BTC contact for more information).

Ministry of Infrastructure school and clinic power projects. With support from the World

Bank and the European Commission, the Rwandan Government plans to provide electric

power to all schools and clinics in the country in the next ten years. Those regions that cannot

be met by grid power will have energy systems provided by PV and/or generators. The project

is currently being developed. Contact the Ministry of Infrastructure for more information.

4.2.2 Kigali Solair

“Kigali Solair” is a PV plant built by Stadtwerke Mainz (a German municipal power company) at the

outskirts of Kigali in 2008. It feeds 250 kW into the national grid. The project builders hope to expand

this to 1 MW – but no timeframe has been given. The feed-in tariff offered by Electrogaz is said to be

too low to cover capital and operation costs of the plant.

Target Market Analysis: Rwanda’s Solar Energy Market 15

References

Common Development Fund (CDF): Annual Report (2008).

http://www.cdf.gov.rw/reports.html#rpt/ (July 2010).

EAC Strategy to ScaleUp Access to Modern Energy Services: Rwanda Country Report (2008)

http://www.eac.int/energy/index.php?option=com_docman&task=doc_download&gid=65&Itemid=

70 (July 2010).

GTZ (2009): Business Guide Ruanda, Eschborn.

Kigali Solair:

http://mininfra.gov.rw/index.php?option=com_content&task=view&id=204&Itemid=343,

http://www.energie-fuer-afrika.de/projekte/details/projekt/3-kigali-solaire.html (July 2010).

Ministry of Infrastructure: http://mininfra.gov.rw/ (July 2010).

Rwanda’s Energy Sector Strategy:

http://mininfra.gov.rw/index.php?option=com_content&task=view&id=110&Itemid=138 (July

2010).

This publication is available free of charge as part of the public relations work of the Federal

Ministry of Economics and Technology, and may not be sold. It may not be used by political parties

or campaigners or electoral assistants during an election for the purposes of campaigning. In

particular, it is forbidden to distribute this publication at campaign events or at information stands

run by political parties or to insert, overprint, or affix partisan information or advertising. It is also

forbidden to pass it on to third parties for the purposes of electoral campaigning. lrrespective of

when, in what way, and in what quantity this publication reached the recipient, it may not be used

even when an election is not approaching in a way that might be understood as suggesting a bias

in the federal government in favour of individual political groupings.

![Pioneer Pdp 434cmx Pdp 43mxe1 s [ET]](https://static.documents.pub/doc/80x56/55cf8eae550346703b948a48/pioneer-pdp-434cmx-pdp-43mxe1-s-et.jpg)