35

WHATEVER THE CHALLENGE CPC ANNUAL REPORT 2009

32 H Mourad St., Giza P.O. Box 42 Giza, Egypt

Tel: +(202) 3570 7739 - 3570 7694 Fax: +(202) 3570 7716

www.cpg.com.eg

WH

ATE

VE

R T

HE

CH

ALL

EN

GE

C

PC

AN

NU

AL

RE

PO

RT

2009

Concept and Design Designframe corp www.designframe.netPrinting RAIDY

Overview 1 Highlights 10 Chairman’s Statement 22 Board of Directors 24 Executive Management 26 Financial Review 28

During times of global financial turmoil, any industry can expect to struggle.

Those who have what it takes will not only survive but also thrive.

When one business line is adversely affected, with diversification and strategic integration

we are assured others will fill their gaps.

When strategies and versatility work together we are able to better manage

changing market demands.

When our more than 30-year track record of overcoming challenges is coupled with a magnitude of operational resources

ONLY THEN WE CAN CLAIM THAT WE WILL sTanD soliD

IN ANY TURBULENCE

Having strength in assets enables us to produce more for further growth. We will continue to grow annually.

1999 our total LTA was EGP 330 Million.

2000 we increased our LTA by 5%.

2001 we increased our LTA by 4%.

2002 we increased our LTA by 11% compared to 2001.

2004 we started to grow again and take wider steps with almost 13% increase in LTA.

2005 we had a slow down in growth with only 4% increase in LTA.

330347361402432

1,024

487504893

1,1 341,293

2008 we had a 11% increase compared to 2007.

2009 we had a 14% increase compared to 2008.

2007 we continued growing our LTA by 15%.

Growth in long-Term assets

2003 we increased our LTA by 8%.

2006 our Long-Term Assets received a massive increase of 77%.

1110

1312

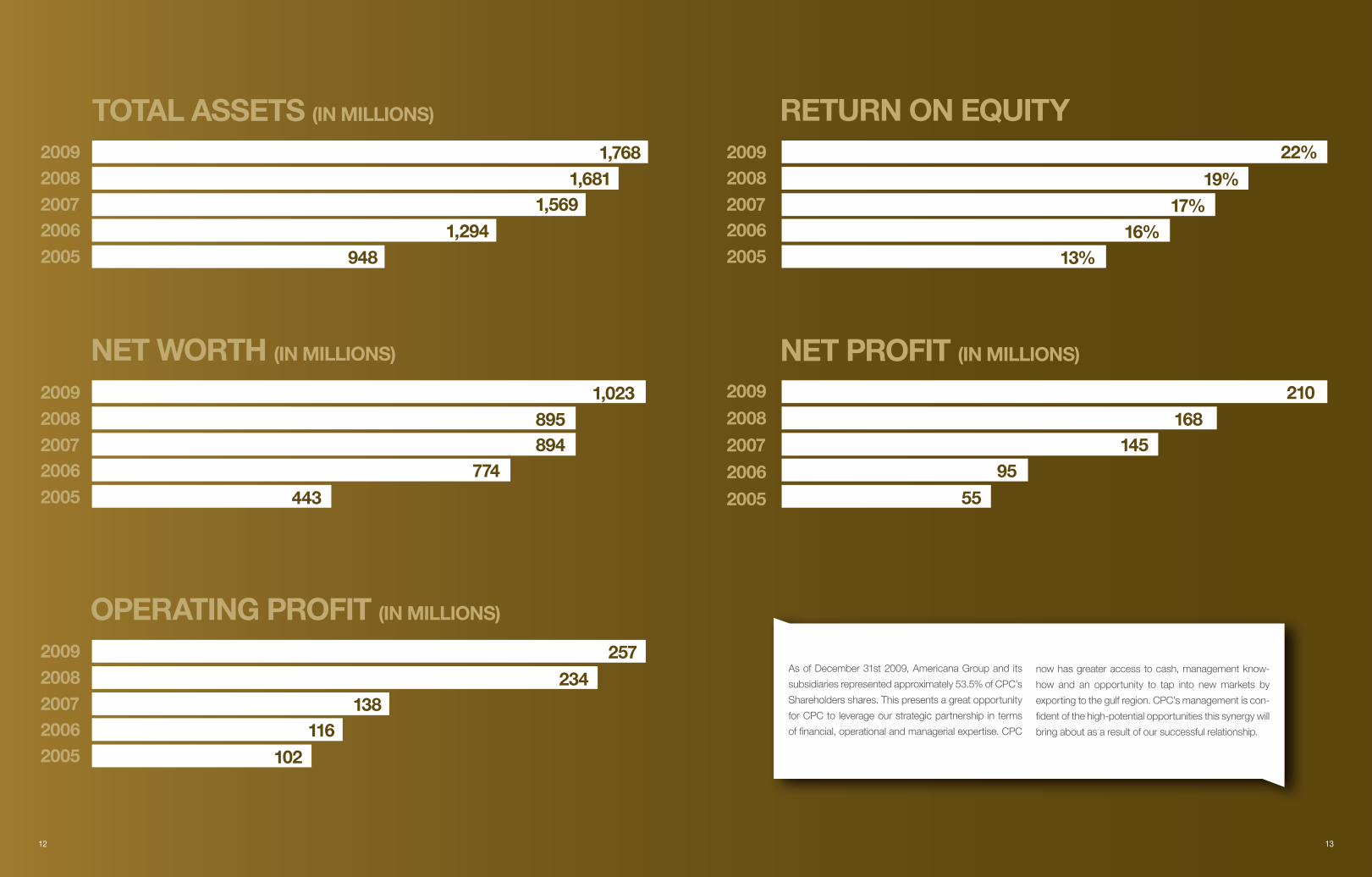

ToTal asseTs (in millions) reTurn on equiTy

As of December 31st 2009, Americana Group and its

subsidiaries represented approximately 53.5% of CPC’s

Shareholders shares. This presents a great opportunity

for CPC to leverage our strategic partnership in terms

of financial, operational and managerial expertise. CPC

now has greater access to cash, management know-

how and an opportunity to tap into new markets by

exporting to the gulf region. CPC’s management is con-

fident of the high-potential opportunities this synergy will

bring about as a result of our successful relationship.

2009

948

2009

2006

1,681

20062007 1,569 20072008

1,294

2008

2005

1,768

2005

oPeraTinG ProFiT (in millions)

2009

200620072008

2005

neT WorTh (in millions)

2005

1,023

2006

8952007 8942008

774

2009

443

neT ProFiT (in millions)

2009

2008

2007

2006

2005

210168

14595

55

257

234138

116102

13%

19%17%

16%

22%

15

ToTal accumulaTeD ProFiT over The lasT 10 years

920,185,000eGP

cPc had a good year during such global financial turmoil and we are

even more confident about our future.

14

1716

year in review

In 2009 Koki encountered several challenges. Although we

succeeded in making money in the broiler sector, once we

sold Koki to the slaughterer it was considered highly priced,

so we prevented the slaughterer from achieving a satisfactory

markup due to the increase in cost of raw material this year.

Our main competition in the frozen chicken market lies in the

frozen imported chicken from Brazil and other countries, which

are penetrating our markets at a high rate. Consequently, and

in order to bypass the fight for shelf space in the supermarkets

and hypermarkets, we have created our own outlets, which are

branded as KOKI shops in addition to introducing a new KOKI

package. And, by adding the chilled chicken to our product line

we are able to expand and diversify the chicken business other

than only providing frozen products to providing chilled prod-

ucts as well. CPC is now the preferred supplier to numerous

international fast food chains and hotel chains including KFC,

Pizza Hut, Domino’s Pizza, Burger King, Marriott, Sheraton and

Hyatt Regency. Koki is also the certified supplier for the Egyp-

tian army and the US Department of Defense in the Middle East.

KoKi

CPC holds the position as one of the most successful Egyp-

tian companies within the food and beverage industries, based

on rankings conducted by the Egyptian business magazine

“Business Today”.

qualiTaTive hiGhliGhTs

Net total assets at the group are valued at EGP 1.8 billion,

growing by 87% starting 31-12-2005 until 31-12-2009. Mean-

while, net profit increased by 279% during the same period.

The feed business is also growing at a rapid pace. Currently,

67% is being sold in open market, while the rest is serving our

poultry integrated sectors.

quanTiTaTive hiGhliGhTs

CPC commissioned their first extrusion production facility to

produce full fat Soy Bean meal. Those meals add more value

for nutrition and quality of our feed.

FeeD nuTriTion

Since December 2007, we have acquired several smaller

competitors in the broilers division thus further strengthening

our position in the market, making us the biggest and most

influential key player in the Egyptian boilers market. We imple-

ment world-class standards in bio-safety, bio-security, and

workforce training.

Broilers

Our farms’ production is complemented by our hatchery op-

eration. The total hatcheries’ capacity before expansion ac-

counted for 86 mm hatching eggs that yielded a production

of 69 mm one-day-old broiler chicks. After our expansion

project, our hatcheries can now hold up to 109 mm hatching

eggs to produce 88 mm one-day-old broiler chicks. With this

growing capacity, we expect our market share to increase,

as we satisfy more demand.

haTcheries

Our Starch and Glucose factory has undergone wide scale

renovations in the form of fully upgrading these facilities in col-

laboration with the World Bank. The upgrade was performed

in 3 phases. The first stage concentrated on improving Starch

and Glucose derivatives, which we implemented successfully.

In the second stage we upgraded the starch factory. During

the third stage, we will be upgrading the glucose factory. After

the completion of this project work, we will have undergone a

complete facility renovation.

sTarch anD Glucose

2008 was the first operational year for our new slaughter-

house. This operation performed well during the year as we

tripled its processing capacity. The tactic used in managing

this new slaughterhouse relied heavily on the chickens’ mar-

ket price and their availability in the market. In order to maxi-

mize our returns we adjusted our slaughterhouse production

levels depending on current market demand.

neW slauGhTer-house

We are constantly developing new products. Since we are

able to anticipate our products market cycle, new products

are constantly being offered in the market regardless of eco-

nomic conditions. These new products are currently in the

research and development stage and we are confident of

their potential success.

neW ProDucTs

We adopted a continuous testing process that ensures

optimal nutritional value of our products. In 2009 all our tech-

nical ratios increased, the yield percentage in our hatcheries

increased and our feed conversion improved.

TesTinG

inTernal saFeGuarDinGCORPORATE GOvERNANCE

Good corporate governance is the key to a company’s

success. It involves a corporation’s commitment to op-

erating with a strict code of conduct. CPC’s corporate

governance ensures that we are operating with a high

level of integrity.

We adopt policies that emphasize accountability,

fairness and transparency.

This is reflected in having the majority of our board

members as non-executive committee members,

and informing an audit committee that supports the

board in fulfilling its role. The audit committee abides

by a set of policies that represent CPC’s Audit Com-

mittee Charter, one which the committee reviews and

assesses annually.

The audit committee is empowered with the authority

to conduct or authorize investigations into any matters

within its scope of responsibilities. These responsibili-

ties entail reviewing significant accounting and reporting

issues and examine their impact on the financial state-

ments, overseeing the internal and external audit proc-

esses - ensuring that efforts are coordinated and audit

resources are utilized effectively -, verifying company’s

compliance with laws and regulations, as well as other

reporting responsibilities.

In addition to our ongoing concern to increase sharehold-

ers’ value and equity, we commit ourselves to building,

developing and enriching the community where we op-

erate. CPC takes an active role in positively contributing

to the local community by undertaking several initiatives

which aim to improve the community’s well-being and

social welfare. An example of this is El-Saff area located

on the eastern side of the Nile river bank. El-Saff was an

unprivileged area with minimal employment opportunities.

CPC’s newly established operations facilities have re-

vived the economic and industrial development of that

area, offering job opportunities for its residents.

We also work with social institutions such as

orphanages. We offer them many benefits, encourage

them to work in teams and to develop their skills. We col-

laborate with them to produce the uniforms of our work-

ers and employees in laboratories, factories and farms.

Further, CPC has a wide range of educational pro-

grams offering summer training, PHD degree and Mas-

ter’s degree programs and scholarships. Other initiatives

include assisting the Ministry of Agriculture, allowing

them to use CPC’s faculties and farms and finance the

Research & Development activities and projects. We

also collaborate with the Egyptian Ministry of Agriculture

to develop testing farms. CPC plans to continuously

pursue its goal in community development.

aDDinG value To our communiTyCORPORATE SOCIAL RESPONSIBILITY

18 19

21

for the freshest chicken from Koki Shop

Koki shops distribute fresh not frozen chicken, making CPC a pioneer in selling fresh chicken. The product is then processed and sent to the market to guarantee its freshness and nutritional value. There are currently 18 Koki shop outlets, 2 of which are located inside the slaughterhouses in Nobareya & 10th of Ramadan, 15 outlets in Cairo and 1 outlet in Marina, Northern coast for the summer season.

19585Call

20

23

excellence is within our reach, but perfection is still to come; this will need tools that we have and others

that we still have to acquire through hard work.

We aspire that CPC will be able to gain inter-

national recognition and accreditation and fare

about in new orbits higher than the present do-

mestic markets in which we excel many of our

competitors. “I aspire to witness CPC brand

name as a super brand in many countries in Eu-

rope, Middle East and Africa.”

First, I would like to congratulate all of the CPC

family members for their exceptional work and

excellent results they achieved in fiscal year 2009;

because of the hard work and professional man-

agement, CPC has started to reap the benefits of

the managerial and logistic support from its part-

ners and main shareholders’ (AMERICANA). This

was clearly reflected in the remarkable increase in

benefits of last year.

chairman’s statement

2524

Dr. Hans NagelBoard

Member

>>

Mr. Sayed Nassef Board

Member

>>

Mr. Adel Al-AlfiBoard

Member

>>

Mr. Ayman Laz

Board Member

>>

Mr. Ahmed Al Khayat

Vice Chairman & Managing

Director

>>

Eng. Tarek Tawfik

Managing Director

>>

Mr. Moataz Al-AlfiBoard

Member

>>

Professor Mamdouh SharafeldinChairman

>>

Mr.Mahmoud

Al Affifi Board

Member

>>

Board of Directors

2726

Dr. Nabil DarwishGrandparent Division

Managing Director

Mr. Mostafa RashedCairo Poultry

Processing Division Chairman

Mr. Mohamed TahaChief Financial

Officer

Mr. Bas Zuidberg Supply Chain Officer

Dr. Fernando Parra Technical Director

Mr. Ayman RoushdyHR Director

Eng. Basem Aboul Wafa

Projects Director

Mr. Ahmed Al Khayat Vice Chairman &

Managing Director

Eng. Tarek TawfikManaging Director

Mr. Hazem ZayedAsst. Managing

Director – Corporate Finance & Business

Development

Mr. Adel Al-AlfiGeneral Manager

>> >>

>>

>>

>>

>>

>> >>

>>

>>

>>

executive management

2928

auditor’s report

To the shareholders of cairo Poultry company “an egyptian joint stock company”

report on the Financial statements

We have audited the accompanying consolidated financial

statements of Cairo Poultry Company S.A.E, which com-

prise the consolidated balance sheet as at 31 December

2009 , and the related consolidated statements of income,

changes in shareholders’ equity, and cash flow for the year

then ended, and a summary of significant accounting poli-

cies and other explanatory notes.

management’s responsibility for the Financial statements

These consolidated financial statements are the responsibility

of Company’s management. Management is responsible for

the preparation and fair presentation of these consolidated fi-

nancial statements in accordance with the Egyptian Accounting

Standards and in the light of the prevailing Egyptian laws, man-

agement responsibility includes, designing, implementing and

maintaining internal control relevant to the preparation and

fair presentation of consolidated financial statements that are

free from material misstatement, whether due to fraud or error

management responsibility also includes selecting and apply-

ing appropriate accounting policies and making accounting

estimates that are reasonable in the circumstances.

auditor’s responsibility

Our responsibility is to express an opinion on these consoli-

dated financial statements based on our audit. Except as de-

scribed below, We conducted our audit in accordance with

the Egyptian Standards on Auditing and in the light of the

prevailing Egyptian laws. Those standards require that we

comply with ethical requirements and plan and perform the

audit to obtain reasonable assurance whether the consolidat-

ed financial statements are free from material misstatement.

An audit involves performing procedures to obtain audit evi-

dence about the amounts and disclosures in the consolidated

financial statements. The procedures selected depend on

the auditor’s judgment, including the assessment of the risks

of material misstatement of the consolidated financial state-

ments, whether due to fraud or error. In making those risk as-

sessments, the auditor considers internal control relevant to

the entity’s preparation and fair presentation of the consoli-

dated financial statements in order to design audit procedures

that are appropriate in the circumstances, but not for the

purpose of expressing an opinion on the effectiveness of the

entity’s internal control. An audit also includes evaluating the

appropriateness of accounting policies used and the reason-

ableness of accounting estimates made by management, as

well as evaluating the overall presentation of the consolidated

financial statements.

We believe that the audit evidence we have obtained is suf-

ficient and appropriate to provide a basis for our audit opinion

on the consolidated financial statements.

Basis for Qualified Opinion

The consolidated financial statements include assets,

liabilities, revenues and expenses refers to subsidiaries that

were audited by other auditors amounted to L.E 521 175 192,

L.E 193 968 212, L.E 949 379 337 and L.E 781 464 907 with

a percentage of 21.54 %, 19.66 %, 31.02 %, and 28.94 %

KPmG hazem hassanPublic accounts & consultant

nasr abou elabasPublic accountsFinancial review

30 31

respectively to total consolidated assets, liabilities, expenses

and revenues as at 31 December 2009. Against 18.55 %,

16.53 %, 30.12 % and 29.93 % respectively to total consoli-

dated assets, liabilities, expenses and consolidated revenues

as at 31 December 2008, So we couldn’t determine whether

there is an important adjustments to be made of the value of

these assets, liabilities, expenses and revenues recorded in

the consolidated financial statements to be relevant in accor-

dance with Egyptian Accounting Standards.

In our opinion, except for the effects of such adjustments,

if any, as might have been determined to be necessary

had we audited the financial statements of such subsidiary

companies referred to in paragraph above, the consolidated

financial statements referred to above present fairly, in all

material respects, the consolidated financial position of the

group as at 31,December 2009 and the results of its opera-

tions and its cash flows for the financial year then ended, in

accordance with Egyptian Accounting Standards and rel-

evant Egyptian laws and regulations that related to prepare

this consolidated financial statements.

report on other legal and regulatory requirements

The Company maintains proper books of account, which

include all that is required by law and by the statutes of

the Company, the consolidated financial statements are in

agreement thereto.

The financial information included in the Board of

Directors’ report, prepared in accordance with Law No. 159

of 1981 and its executive regulations, is in agreement with

the Company’s books of account.

Cairo, 20 January 2010

KPmG hazem hassanPublic accounts & consultant

nasr abou elabasPublic accounts

cairo Poultry company(An Egyptian Joint Stock Company)Consolidated Statement of financial positionAs at 31 December 2009

The notes from (1) to (38) are an integral part of these consolidated financial statements.

note no. 31/12/2009 le(amended)

31/12/2008 le

non-currenT asseTs Property, Plant and equipment (7) 810 620 162 709 927 510Breeders (8) 59 041 209 47 929 924Plant Wealth (9) 10 479 229 -Projects under construction (10) 100 522 199 118 424 199Other financial investments (11) 1 202 500 1 202 500Investments in associate companies (12) 88 638 353 105 743 568Other investments (13) 213 602 734 141 853 047Payment for purchase of investment (14) 8 540 000 8 540 000Total non-current assets 1 292 646 386 1 133 620 748currenT asseTsInventories (15) 286 623 432 322 887 093Trade receivables & other debit balances (16) 104 201 361 132 241 305Due from related parties (34-1) 68 384 756 53 161 469Other financial investments (17) - 11 388 405Cash and cash equivalent (18) 16 063 534 27 386 971Total current assets 475 273 083 547 065 243currenT liaBiliTiesProvision for Contingency (19) 21 160 530 6 762 390Provision for claims (20) 34 196 287 26 675 336Banks-credit facilities (21) 112 467 144 353 672 896Banks-overdrafts 74 442 790 142 179 057Trade payables & other credit balances (22) 130 778 749 117 430 248Due to related parties (34-2) 4 789 877 3 198 965Long term loans - current portion (25) 37 802 016 63 514 006Total current liabilities 415 637 393 713 432 898Working capital 59 635 690 ( 166 367 655)Total investment 1 352 282 076 967 253 093Financed as follows:shareholDers’ equiTyIssued & paid - up capital (23) 145 152 000 145 152 000Reserves 247 284 332 229 592 791Special reserve- change in value of investments available for sale (24) 134 291 839 62 542 153Revaluation surplus 46 820 572 53 990 980Retained earnings 227 372 608 223 159 511Parent company’s share in profits of treasury stocks sale 196 446 196 446Net profit for the year 205 365 585 163 031 500 Total equity attributable to the shareholders of the parent company 1 006 483 382 877 665 381minority interest 16 214 241 16 730 191 Total shareholders’ equity 1 022 697 623 894 395 572non-currenT liaBiliTiesLong term loans (25) 295 127 774 38 935 279Deferred tax liabilities (26-1) 20 270 890 16 225 864Long term notes payable 9 190 391 14 494 306Deferred sales tax installments 4 990 141 3 202 072Other long term liabilities 5 257 -Total non-current liabilities 329 584 453 72 857 521Total shareholders’ equity and non-current liabilities 1 352 282 076 967 253 093

Chief Financial Officer

Acc/ Mohamed Taha

General manager

Mr. Adel Al-Alfi

managing Director

Eng/ Tarek Tawfik

chairman

Professor/ Mamdouh Abdelwahab Sharafeldin

32 33

cairo Poultry company(An Egyptian Joint Stock Company)Consolidated Income statementfor the financial year ended 31 December, 2009

note no.

The year ended 31/12/2009

le

amendedThe year ended

31/12/2008le

Net sales 1 935 108 702 1 962 315 356

Cost of sales (1 550 109 193) (1 615 775 664)

Gross profit 384 999 509 346 539 692

Selling & distribution expenses (57 635 688) (62 075 029)

General & administrative expenses (27) (50 818 193) (46 817 705)

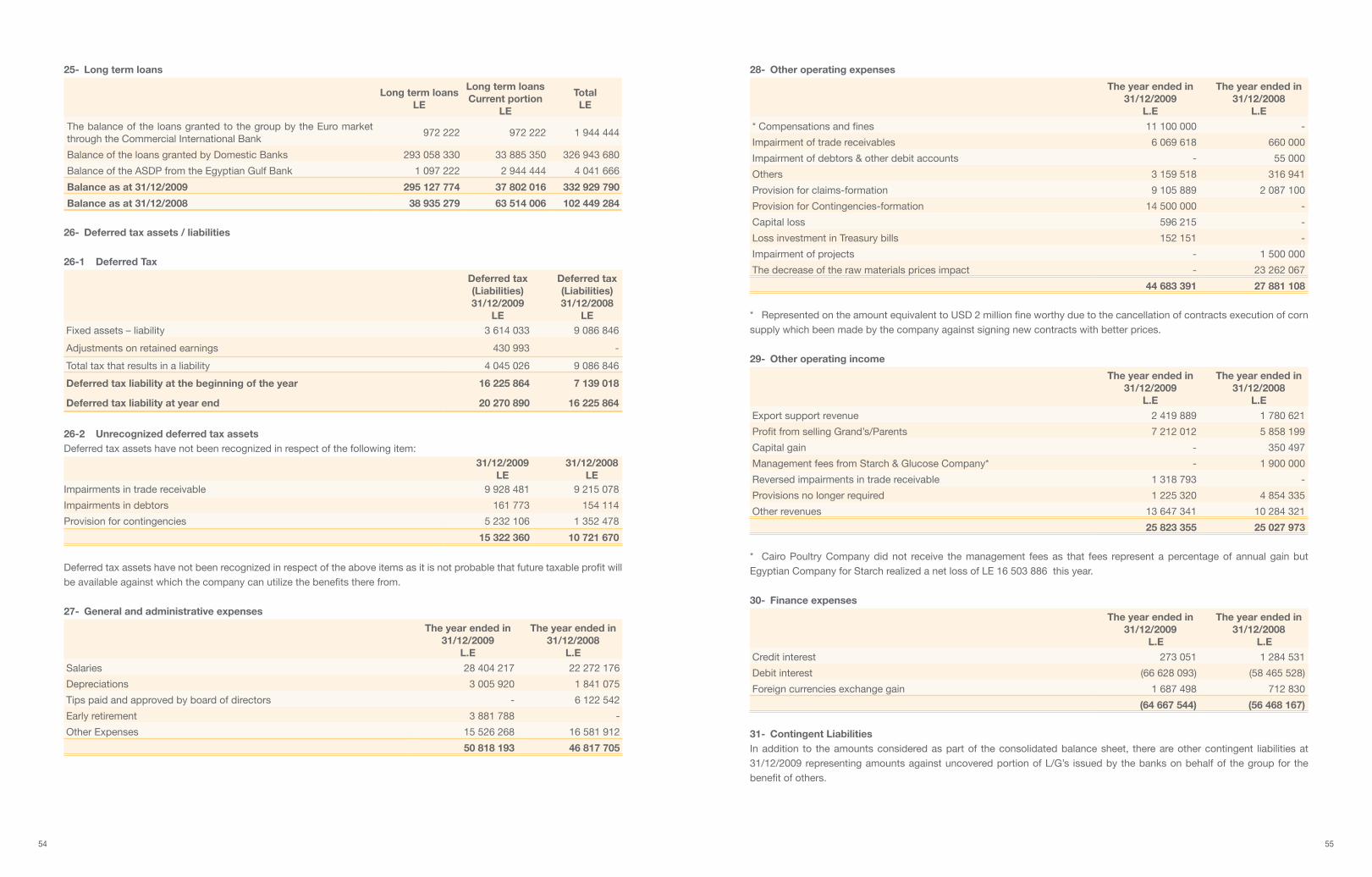

Other operating expense (28) (44 683 391) (27 881 108)

Board of directors remuneration (898 000) (319 464)

Other operating revenues (29) 25 823 355 25 027 973

Profit from operations 256 787 592 234 474 359

Revenue from investments available for sale 3 494 450 2 409 931

The group’s share in the net profit of associate companies (12) 990 478 5 619 979

Profit from sale of investments available for sale 23 949 185 2 093 626

Finance interest and expense (30) (64 667 544) (56 468 167)

Net profit for the year before income tax 220 554 161 188 129 728

Income tax (6 867 240) (11 423 656)

Deferred tax (26-1) (3 614 033) (9 086 846)

Net profit after income tax 210 072 888 167 619 226

Distributed as followsParent company’s share in profit 205 365 585 163 031 500

Non controlling interest share in profit 4 707 303 (4 587 726)

210 072 888 167 619 226

Earning per share for the year (LE/Share) (36) 2.34 1.79

* The notes from (1) to (38) are an integral part of these consolidated financial statements.

Des

crip

tio

nn

ote

n

o.

sha

re c

apit

al

ler

eser

ves

le

sp

ecia

l res

erve

s ev

alua

tio

n d

iffer

-en

ces

of

avai

lab

le f

or

sale

inve

stm

ents

le

re-

eval

uati

on

surp

lus

le

ret

aine

d

ear

ning

s

le

Par

ent

com

pan

y’s

shar

e in

pro

fits

o

f tr

easu

ry

sto

cks

sale

le

Net

Pro

fit

for

the

year

le

Tota

l le

Bal

ance

as

at 3

1/12

/200

7 7

2 57

6 00

022

6 76

7 21

4 1

63 6

27 7

7053

990

980

216

495

383

196

446

146

333

062

879

986

855

Div

iden

ds

for

the

year

200

7-

2 82

5 57

7-

-7

465

999

-(1

46 3

33 0

62)

(136

041

486

)

Incr

ease

in s

hare

cap

ital

72 5

76 0

00-

--

--

-72

576

000

Ava

ilab

le fo

r sa

le fi

nanc

ial i

nves

tmen

t ev

alua

tion

diff

eren

ces

--

(101

085

617

)-

--

-(1

01 0

85 6

17)

Net

pro

fit fo

r th

e ye

ar-

--

--

-16

3 39

8 97

116

3 39

8 97

1

Bal

ance

as

at 3

1/12

/200

8 b

efor

e am

end

men

t14

5 15

2 00

0 2

29 5

92 7

91 6

2 54

2 15

3 5

3 99

0 98

0 2

23 9

61 3

82 1

96 4

46 1

63 3

98 9

71 8

78 8

34 7

23

Ad

just

men

t-

--

-(8

01 8

71)

-(3

67 4

71)

(1 1

69 3

42)

Bal

ance

as

at 3

1/12

/200

8 (a

fter

am

end

ed)

145

152

000

229

592

791

62

542

153

53

990

980

223

159

511

196

446

163

031

500

877

665

381

Div

iden

ds

for

the

year

200

8-

17

691

541

--

4 2

13 0

97-

(163

031

500

)(1

41 1

26 8

62)

Ava

ilab

le fo

r sa

le fi

nanc

ial i

nves

tmen

t ev

alua

tion

diff

eren

ces

(24)

--

71

749

686

--

--

71

749

686

Re-

eval

uatio

n su

rplu

s-

--

(7 1

70 4

08)

--

-(7

170

408

)

Net

pro

fit fo

r th

e ye

ar-

--

--

- 2

05 3

65 5

85 2

05 3

65 5

85

Bal

ance

as

at 3

1/12

/200

9 1

45 1

52 0

00 2

47 2

84 3

32 1

34 2

91 8

39 4

6 82

0 57

2 2

27 3

72 6

08 1

96 4

46 2

05 3

65 5

851

006

483

382

cai

ro P

oul

try

co

mp

any

(An

Egy

ptia

n Jo

int

Sto

ck C

omp

any)

Con

solid

ated

sta

tem

ents

cha

nges

in s

hare

hold

ers’

eq

uity

(Am

end

ed)

for

the

finan

cial

yea

r en

ded

31

Dec

emb

er, 2

009

* T

hese

ad

just

men

ts r

epre

sent

ed in

the

diff

eren

ce b

etw

een

grou

p’s

sha

re in

the

net

con

solid

ated

ass

ets

and

net

unc

onso

lidat

ed a

sset

s of

the

Egy

ptia

n C

omp

any

for

Sta

rch

&

G

luco

se a

s of

31/

12/2

008.

* T

he n

otes

from

(1) t

o (3

8) a

re a

n in

tegr

al p

art

of t

hese

con

solid

ated

fina

ncia

l sta

tem

ents

.

34 35

note no.

The year ended31/12/2009

le

The year ended31/12/2008

le

cash FloWs From oPeraTinG acTiviTies

Net profit for the year before income tax and minority interest in profits 220 554 161 188 129 728

aDjusTmenTs To reconcile neT ProFiT For The year To neT cash

FloWs From oPeraTinG acTiviTies:

Depreciation of fixed assets (7) 59 962 912 45 852 023

Depreciation of plant wealth 207 649 -

Capital loss 596 215 ( 350 497)

Amortization of breeders (8) 109 547 715 80 970 022

Profits from sale of breeders (7 212 012) ( 5 858 199)

Profits from sale of financial investments (23 949 185) -

Impairment in trade receivables and other debit balances - formed 6 069 618 715 000

Impairment in trade receivables and other debit balances - no longer required (2 344 113) ( 1 854 335)

Impairment in inventories - formed (28) - 23 262 067

Impairment in projects under construction - formed - 1 500 000

The group’s share in the net profits of associates companies ( 990 478) ( 5 619 979)

Provision for Contingencies - formed 14 500 000 -

Provision for Contingencies - no longer required - ( 3 000 000)

Provision of claims - formed (28) 9 105 889 2 087 100

Provision of claims- no longer required ( 200 000) -

Management fees of The Egyptian Company for Starch & Glucose - ( 1 900 000)

Investments revenue (3 494 450) ( 2 409 931)

Credit interests (30) ( 273 051) ( 1 284 531)

Finance interests & expense (30) 66 628 093 58 465 528

448 708 963 378 703 996

chanGes in WorKinG caPiTal

Decrease (increase) in inventories 36 263 661 ( 85 260 436)

Decrease in trade receivables & other debit balances 24 314 439 6 609 451

(Decrease) in trade payables & other credit balances ( 30 784 177) ( 27 943 619)

(Increase) decrease in due from related parties ( 15 223 287) 48 465 268

Increase in due to related parties 1 590 912 2 625 006

Provisions - utilized ( 1 754 432) ( 3 227 207)

Financial interests paid ( 66 628 093) ( 58 465 528)

Net cash flows generated from operating activities 396 487 986 261 506 931

cairo Poultry company(An Egyptian Joint Stock Company)Consolidated Statement of Cash Flowsfor the financial year ended 31 December, 2009

cairo Poultry company(An Egyptian Joint Stock Company)Consolidated Statement of Cash Flowsfor the financial year ended 31 December, 2009

note no.

The year ended31/12/2009

le

The year ended31/12/2008

le

cash FloWs From invesTinG acTiviTies

Proceeds from sale of fixed assets 4 169 740 762 250

Payments for acquisition of fixed assets & projects under constructions ( 158 206 397) ( 248 304 257)

Payments for purchase of Poultry breeders ( 138 505 527) ( 104 737 417)

Proceeds from sale of Poultry breeders 25 058 539 24 708 114

Proceeds from sale of treasury stocks 11 388 405 11 577 346

Proceeds from sale of financial investments 29 260 074 ( 11 624 835)

Payments for purchase of financial investments - ( 14 636 357)

Collected interests 273 051 1 284 531

Collected investments revenue 3 494 450 2 409 931

Dividends received from the associate companies 5 013 337 5 675 735

Net cash flow used in investing activities (218 054 328) (332 884 959)

cash FloWs From FinancinG acTiviTies

Settlements of banks - credit facilities ( 241 205 752) ( 52 596 233)

Proceeds from loans 230 480 505 12 003 987

Decrease in minority interest ( 5 223 253) -

Cash dividends paid for shareholders ( 108 864 000) ( 36 288 000)

Net cash flows used in financing activities (124 812 500) (76 880 246)

net (Decrease) increase in cash & cash equivalents during the year 53 621 158 (148 258 274)

cash and cash equivalents at the beginning of the year (115 393 262) 32 865 012

cash and cash equivalents at the end of the year (18/1) (61 772 104) (115 393 262)

* The notes from (1) to (38) are an integral part of these consolidated financial statements.

36 37

cairo Poultry company Notes to consolidated financial statements for financial year ended 31 December 2009

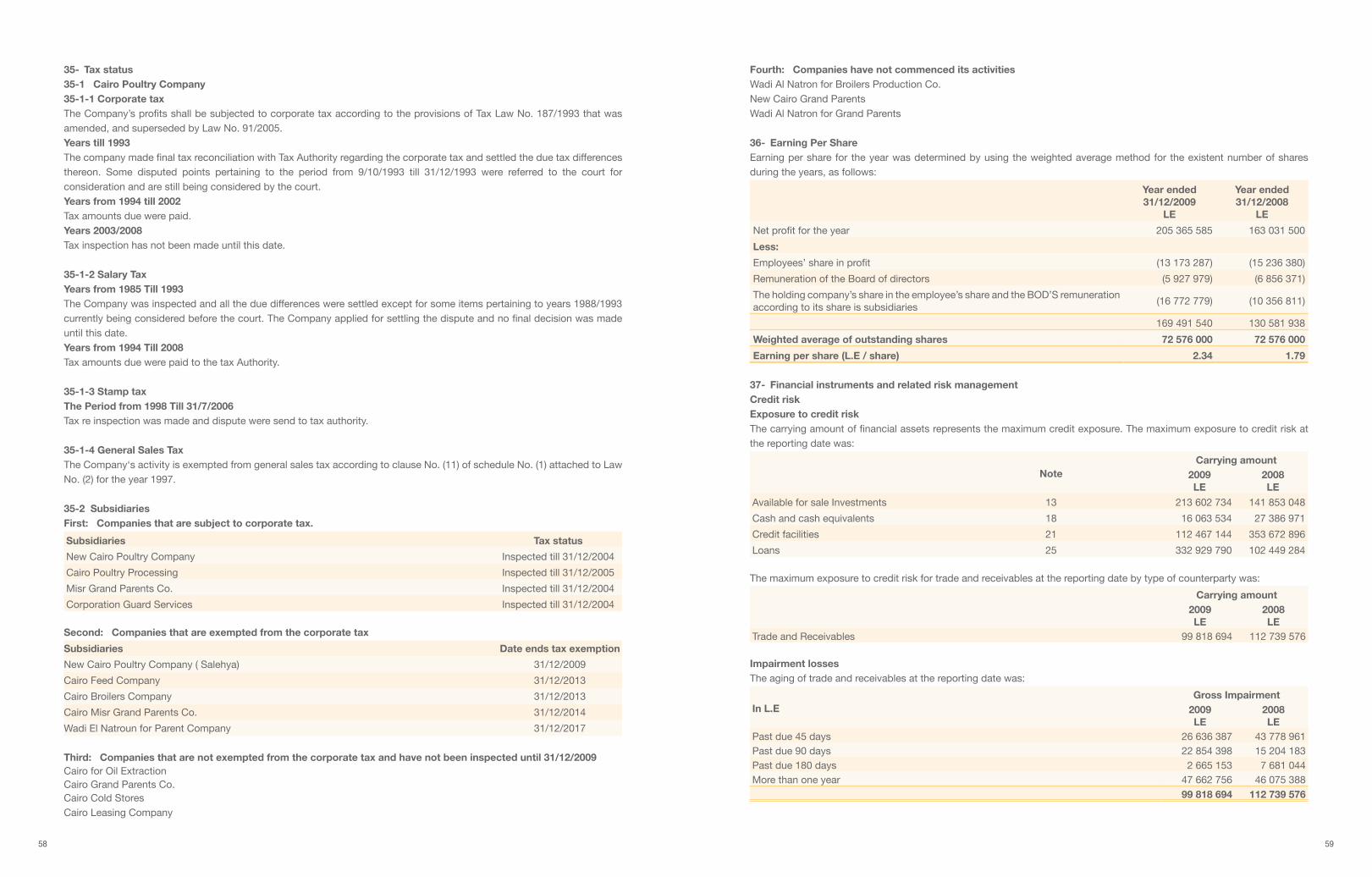

1- company’s & subsidiaries’ background Cairo Poultry Company – An Egyptian Joint Stock Company – was established in year 1977 according to the provisions of Investment Law No. 230 of 1989.

The Company was registered under the commercial register on 26/7/1977 No. 42444, The Company’s life was extended to be 25 Years starting from 19/7/2002.The Company is a subsidiary to the Kuwait Food Company.Company location : 32 Mourad st. –Giza – Egypt .Chairman of the board Prof. Dr. / Mamdouh Sharafeldin.

The company’s purposeThe Company’s objective is represented in producing, raising chicks and producing life stock fodder, mix preliminary ingredients and producing hatching eggs and participating in similar projects domestically and overseas.

registration in the stock exchangeThe Company is listed in the formal table (1) of Cairo and Alexandria Stock Exchanges.

2- Basis of preparation2-1 statement of complianceThe financial statements have been prepared in accordance with Egyptian Accounting Standards (“EAS”), and in compliance with applicable Egyptian laws and regulations.The financial statements were approved by the Company’s Board of Directors in its meeting held on 17/1/2010 for issuance.

2-2 Basis of measurementThe consolidated financial statements have been prepared on the historical cost basis except for the following:• Semi-Finished production ( Chicks at the fatten station at fair value)• Available for sale investmentsThe methods used to measure fair values are discussed further in note 4.

2-3 Functional and presentation currencyThese consolidated financial statements are presented in Egyptian pound, which is the Company’s and its subsidiaries functional currency.

2-4 use of estimates and judgmentsThe preparation of financial statements in conformity with Egyptian Accounting Standards requires management to make judgments, estimates and assumptions that affect the application of accounting policies and the reported amounts of assets, liabilities, income and expenses. Actual results may differ from these estimates.

Estimates and underlying assumptions are reviewed on an ongoing basis. Revisions to accounting estimates are recognized in the period in which the estimate is revised and in any future periods affected.

Information about significant areas of estimation uncertainty and critical judgments in applying accounting policies that have the most significant effect on the amounts recognized. In the financial statements is included in the following notes:• Note(3-1): Business combination. • Note(7): Property, plant and equipment.• Note(15): Inventories.• Note(16-1): trade receivables and other debit balances.• Note(31): Provisions and Contingent liabilities.• Note(26-1): deferred tax.

3- Significant accounting policiesThe accounting policies set out below have been applied consistently to all periods presented in these consolidated financial statements.

3-1 Basis of consolidationsubsidiary companiesSubsidiaries are those enterprises controlled by the Company. Control exists when the Company has the power, to govern the financial and operating policies of an enterprise so as to obtain benefits from its activities. And when evaluating this power we have to take in consideration the present and possible voting rights in the consolidated financial statements’ date. And the subsidiaries’ financial statements will be consolidated in the consolidated financial statements from the acquisition date till the holding company loses its power.

associatesAssociates are those entities in which the Group has significant influence, but not control, over the financial and operating policies. Associates are accounted for using the equity method. The consolidated financial statements include the Group’s share of the income and expenses of equity accounted investees, after adjustments to align the accounting policies with those of the Group, from the date that significant influence or joint control commences until the date that significant influence or joint control ceases. When the Group’s share of losses exceeds its interest in an equity accounted investee, the carrying amount of that interest (including any long-term investments) is reduced to nil and the recognition of further losses is discontinued except to the extent that the Group has an obligation or has made payments on behalf of the investee.

Transactions eliminated on consolidation Intra-group balances, and any unrealized income and expenses arising from intra-group transactions, are eliminated in preparing the consolidated financial statements. Unrealized gains arising from transactions with equity accounted investees are eliminated against the investment to the extent of the Group’s interest in the investee. Unrealized losses are eliminated in the same way as unrealized gains, but only to the extent that there is no evidence of impairment.

3-2 Foreign currency Foreign currency transactionsTransactions in foreign currencies (other than functional and presentation currency the Egyptian Pound) are translated to the functional currency at exchange rates at the dates of the transactions. Monetary assets and liabilities denominated in foreign currencies at the reporting date are retranslated to the functional currency at the exchange rate at that date. Non-monetary assets and liabilities denominated in foreign currencies that are measured at fair value are retranslated to the functional currency at the exchange rate at the date that the fair value was determined. Foreign currency differences arising on retranslation are recognized in profit or loss, except for differences arising on the retranslation of available-for-sale equity instruments.

3-3 Financial instruments3-3-1 Non-derivative financial instrumentsNon-derivative financial instruments comprise investments in equity and debt securities, trade and other receivables, cash and cash equivalents, loans and borrowings, and trade and other payables.

Non-derivative financial instruments are recognized initially at fair value plus directly attributable transaction costs. Cash and cash equivalents comprise cash balances and call deposits. Bank overdrafts that are repayable on demand and

form an integral part of the Company’s cash management are included as a component of cash and cash equivalents for the purpose of the statement of cash flows.

Accounting for finance income and expense is discussed in note (3-18).

3-3-2 available-for-sale investments Equity securities held for sale are classified as current assets and are recognized at fair value. Gain or loss are recognized in the income statement.Equity securities and certain debt securities are classified as available-for-sale financial assets are measured at fair value (except for investments which are unlisted in stock exchange),gain or loss are directly recognized in equity. When an

38 39

investment is derecognized, the cumulative gain or loss in equity is transferred to income statement except for impairment losses. Equity securities which are unlisted in stock exchange are recognized at cost less impairment.

3-4 Property, plant and equipmenta- recognition and measurementItems of property, plant and equipment are measured at cost less accumulated depreciation and accumulated impairment losses (note: 7).

Cost includes expenditures that are directly attributable to the acquisition of the asset. The cost of self-constructed assets includes the cost of materials and direct labor, any other costs directly attributable to bringing the asset to a working condition for their intended use, and the costs of dismantling and removing the items and restoring the site on which they are located.

When parts of an item of property, plant and equipment have different useful lives, they are accounted for as separate items (major components) of property, plant and equipment.

Purchased software that is integral to the functionality of the related equipment is capitalized as part of that equipment.Borrowing costs related to the acquisition, construction or productions of qualifying assets are recognized in profit or loss as incurred.Gains and losses on disposal of an item of property, plant and equipment are determined by comparing the proceeds from

disposal with the carrying amount of property, plant and equipment and are recognized net within “other income” in profit or loss.

B- subsequent costsThe cost of replacing part of an item of property, plant and equipment is recognized in the carrying amount of the item if it is probable that the future economic benefits embodied within the part will flow to the Company and its cost can be measured reliably. The carrying amount of the replaced part is derecognized. The costs of the day-to-day servicing of property, plant and equipment are recognized in profit or loss as incurred.

c- DepreciationDepreciation is recognized in profit or loss on a straight-line basis over the estimated useful lives of each part of an item of property, plant and equipment. Land is not depreciated. The estimated useful lives for the current and comparative periods are as follows:

3-5 GrantsGranted assets gained by group companies from grantee are recorded after deduction the cost of purchasing till reaches the book value for the assets, the grants are recorded as revenue at consolidated income statement during the estimated life time for the asset with reducing the annual depreciation burden.

3-6 BreedersThe grand Parent Poultry (related to the Misr Grand Parents Company, Cairo Grand Parents Company, Cairo Misr Grand Parents) are recorded at its net book value less the accumulated depreciation at the consolidated balance sheet date. The depreciation is computed according to the average of hatching eggs production during the productive period which is the standard applicable international ratios related to the race that the company acquire (due to the absence of an active market to determine a reliable price).

3-7 Projects under constructionExpenditures incurred on purchasing and constructing fixed assets are initially recorded in projects under construction until the asset is completed and becomes ready for use. Upon the completion of the assets, all related costs are transferred to fixed assets. Projects under construction are measured at cost less accumulated impairment losses (note: 3-14). No depreciation is charged until the project is completed and transferred to fixed assets.

Description estimated useful lives (years)

Buildings & constructions 10 - 40

Machinery and equipment 7 - 14

Motor vehicles & transportation means 5

Tools & equipment 5

Furniture and office equipment 3 - 8

3-8 Plant life stockAll the expenditures of planting olive trees that have been capitalized as fixed assets in the balance sheet under the plant life stock item after reaching the marginal production, and to be depreciated on 50 years according to its nature.

3-9 GoodwillGoodwill is initially measured at its cost , being the excess of the cost of the business combination over the Group’s interest in the net fair value of identifiable assets, liabilities and contingent liabilities. After initial recognition, the group measures acquired goodwill at cost less impairment losses. Recognized goodwill impairment losses are not subsequently reversed.

3-10 inventoriesInventories of raw materials, packing materials and spare parts are measured at the lower of cost and net realizable value. Net realizable value is the estimated selling price, in the ordinary course of business, less the estimated costs of completion and selling expenses.

The cost of inventory determined as follows:Raw materials and packing materials is determined at cost according to first in First out method.Spare parts and supplies at cost are determined according to weighted average method.The work in progress (Chicks in batteries) at fair value determined by career’s specialists after deducting estimated cost of sales, the increase or decrease in fair value are recorded to income statement – if any – according to the sales price weighted to percentage of compilation of the chicks.Finished goods of (Fodders and frozen breeders) are measured at the lower of manufacturing cost or net realizable value. The manufacturing cost comprises raw materials, direct labor, and cost includes an appropriate share of overheads based on normal operating capacity.

3-11 Plant life stock ( land reclamation) All the expenditures of planting olive trees that have not reached the marginal production yet included in the projects in progress until reach that stage are capitalized as fixed assets in the consolidated balance sheet under the plant life stock item.

3-12 Trade receivables and other debit balancesTrade accounts receivable with age from one day to 365 days are recognized by the invoiced value net of an estimate of the uncollectible amount which is made when collection of the full amount is no longer probable. Also, the balance of trade accounts receivable and debtors should be impaired by the determined value of bad debts. Debtors and other debit balances are stated at their nominal value less the impairment in its value.

3-13 creditors and other credit balancesCreditors and other credit balances are stated at their cost.

3-14 impairmentFinancial assetsA financial asset is assessed at each reporting date to determine whether there is any objective evidence that it is impaired. A financial asset is considered to be impaired if objective evidence indicates that one or more events have had a negative effect on the estimated future cash flows of that asset.An impairment loss in respect of a financial asset measured at amortized cost is calculated as the difference between its carrying amount, and the present value of the estimated future cash flows discounted at the original effective interest rate. An impairment loss in respect of an available-for-sale financial asset is calculated by reference to its fair value.Individually significant financial assets are tested for impairment on an individual basis. The remaining financial assets are assessed collectively in groups that share similar credit risk characteristics.All impairment losses are recognized in profit or loss. Any cumulative loss in respect of an available-for-sale financial asset recognized previously in equity is transferred to profit or loss.An impairment loss is reversed if the reversal can be related objectively to an event occurring after the impairment loss was recognized. For financial assets measured at amortized cost and available-for-sale financial assets that are debt securities,

40 41

the reversal is recognized in profit or loss. For available-for-sale financial assets that are equity securities, the reversal is recognized directly in equity.

Non-financial assets The carrying amounts of the Company’s non-financial assets, other than, inventories and deferred tax assets are reviewed at each reporting date to determine whether there is any indication of impairment. If any such indication exists, then the asset’s recoverable amount is estimated. For intangible assets that have indefinite lives or that is not yet available for use.The recoverable amount of an asset or cash-generating unit is the greater of its value in use and its fair value less costs to sell. In assessing value in use, the estimated future cash flows are discounted to their present value using a pre-tax discount rate that reflects current market assessments of the time value of money and the risks specific to the asset. An impairment loss is recognized if the carrying amount of an asset or its cash-generating unit exceeds its estimated recoverable amount. Impairment losses are recognized in profit or loss.An impairment loss is reversed if there has been a change in the estimates used to determine the recoverable amount. An impairment loss is reversed only to the extent that the asset’s carrying amount does not exceed the carrying amount that would have been determined, net of depreciation or amortization, if no impairment loss had been recognized.

3-15 Defined contribution plansThe Company contributes to the government social insurance system for the benefits of its employees according to the social insurance Law No. 79 of 1975 and its amendments, the Company’s contributions are recognized in income statement using the accrual basis of accounting. The company’s obligation in respect of employees’ pensions is confined to the amount of aforementioned contributions.

3-16 ProvisionsA provision is recognized if, as a result of a past event, the Company has a present legal or constructive obligation that can be estimated reliably, and it is probable that an outflow of economic benefits will be required to settle the obligation. Provisions are determined by discounting the expected future cash flows at a pre-tax rate that reflects current market assessments of the time value of money and the risks specific to the liability.

3-17 revenue recognitionRevenue from the sale of goods is measured at the fair value of the consideration received or receivable, net of returns, trade discounts and volume rebates. Revenue is recognized when the significant risks and rewards of ownership have been transferred to the buyer, recovery of the consideration is probable, the associated costs and possible return of goods can be estimated reliably.Investment revenue are recorded when the shareholders have the right of dividends that provided by the associates and available for sale investments at the financial period that dividends are approved by general assembly of the invested companies.

3-18 Finance income and expensesFinance income comprises interest income on funds invested Interest income is recognized as it accrues in profit or loss, using the effective interest method. Finance expenses comprise interest expense on borrowings using the effective interest method. Foreign currency gains and losses are reported on a net basis.

3-19 income taxIncome tax on profit or loss for the year comprises current and deferred tax. Income tax is recognized in the income statement except to the extent that it relates to items recognized directly on equity, in which case it is recognized in equity. Current tax is the expected tax payable on the taxable income for the year, using tax rates enacted or substantially enacted at the balance sheet date, and any adjustment to tax payable in respect of previous years.

3-20 Deferred taxDeferred tax is recognized using the balance sheet method, providing for temporary differences between the carrying amounts of assets and liabilities for financial reporting purposes and the amounts used for taxation purposes. The amount of deferred tax provided is based on the expected manner of realization or settlement of the carrying amount of assets and liabilities,

using tax rates enacted or substantively enacted at the consolidated balance sheet date. A deferred tax asset is recognized only to the extent that it is probable that future taxable profits will be available against which the asset can be utilized. Deferred tax assets are reduced to the extent that it is no longer probable that the related tax benefit will be realized.

3-21 Borrowing costsBorrowings are recognized initially at the proceeds received, net of transaction costs incurred. Borrowings are subsequently stated at amortized cost using the effective interest rate basis; any difference between proceeds (net of transaction costs) and the redemption value is recognized in the income statement over the period of the borrowings.

3-22 segmentation reportsEach sector of the companies’ activity segments considers as a unit that contributes in providing variant products different that the other activities (Activity segments) and each unit have risks and utilities different than the other unit exist on the company according to its activity.

3-23 earnings per shareThe Company presents basic earnings per share (EPS) data for its ordinary shares. Basic EPS is calculated by dividing the profit or loss attributable to ordinary shareholders of the Company by the weighted average number of ordinary shares outstanding during the period.

3-24 legal reserveAccording to the Companies Law requirements and the statutes of the Company, 5% of the annual net profit transferred to a legal reserve until the accumulated reserve reaches 50% of the issued share capital. The reserve is un-distributable; however, it can be used to increase the share capital or to offset losses. If the reserve falls below the defined level (50% of the issued share capital), than the Company is required to resume setting aside 5% of the annual profit until it reaches 50% of the issued share capital.

3-25 Cash flow statementThe cash flow statement is prepared using the indirect method.

3-26 Key sources of estimation uncertaintyimpairment of Trade and other receivables balancesAn estimate of the collectable amount of trade receivables is made when collection of the full amount is no longer probable. This estimation is performed on an individual basis.

At the consolidated financial statements date, gross trade receivables and other debit balances were L.E 154 652 625 and the impairment in trade receivables and other debit balances value was L.E 50 451 269. Any difference between the amounts actually collected, in future periods, and the amounts currently expected to be collected will be recognized in the consolidated income statement.

Write down of inventoriesInventories are held at lower of cost and net realizable value. When inventories become old or obsolete, an estimate is made of their net realizable value. For individually significant amounts this estimation is performed on an individual basis.

At the consolidated financial statement date, gross inventories were L.E 286 623 432, Any difference between the amounts actually realized in future periods and the amounts expected to be recovered will be recognized in the consolidated income statement.

4- Determination of fair valueA number of the Company’s accounting policies and disclosures require the determination of fair value, for both financial and non- financial assets and liabilities. Fair values have been determined for measurement and/or disclosure purposes based on the following methods. Where applicable, further information about the assumptions made in determining fair values is disclosed in the notes concerning that asset or liability.

42 43

4-1 Work in process (chicks in batteries)With fair value determined by specialist opinion.

4-2 available for sale investmentsCurrent available for sale investments are evaluated in active market with its market value.

5- Financial risk management overviewThe Group has exposure to the following risks from its use of financial instruments:• Credit risk• Liquidity risk • Market risk.

This note presents information about the Company’s exposure to each of the above risks, the Company’s objectives, policies and processes for measuring and managing risk, and the Company’s management of capital. Further quantitative disclosures are included throughout these financial statements.

The Board of Directors has overall responsibility for the establishment and oversight of the Company’s risk management framework. The Board is responsible for developing and monitoring the Company’s risk management policies.

The Company’s risk management policies are established to identify and analyze the risks faced by the Company, to set appropriate risk limits and controls, and to monitor risks and adherence to limits. Risk management policies and systems are reviewed regularly to reflect changes in market conditions and the Company’s activities. The Company, through its training and management standards and procedures, aims to develop a disciplined and constructive control environment in which all employees understand their roles and obligations.

The Company’s Board oversees how management monitors compliance with the Company’s risk management policies and procedures, and reviews the adequacy of the risk management framework in relation to the risks faced by the Company. The Company’s Board is assisted in its oversight role by Internal Audit. Internal Audit undertakes both regular and ad hoc reviews of risk management controls and procedures, the results of which are reported to the management.

credit risk Credit risk is the risk of financial loss to the Company if a customer or counterparty to a financial instrument fails to meet its contractual obligations, and arises principally from the Company’s receivables from customers and investment securities.

Trade and other receivablesThe Company’s exposure to credit risk is influenced mainly by the individual characteristics of each customer. The demographics of the Company’s customer base, including the default risk of the industry and country, in which customers operate, has less of an influence on credit risk. Credit risk is considered limited due to the Company’s policy that points to dealing with a different customers sector and changing the Company’s policy to cash sales.

The Board of Directors has established a credit policy under which each new customer is analyzed individually for creditworthiness before the Company’s standard payment and delivery terms and conditions are offered. The Company’s review includes external ratings, when available, and in some cases bank references. Purchase limits are established for each customer, which represents the maximum open amount without requiring approval from the management; these limits are reviewed quarterly. Customers that fail to meet the Company’s benchmark creditworthiness may transact with the Company only on a prepayment basis.

Most of the Company’s customers have been transacting with the Company for many years, and losses have occurred infrequently. In monitoring customer credit risk, customers are grouped according to their credit characteristics, including whether they are an individual or legal entity, whether they are a wholesale, retail or end-user customer, geographic location, industry, aging profile, maturity and existence of previous financial difficulties. Trade and other receivables relate mainly to the Company’s wholesale customers. Customers that are graded as “high risk” are placed on a restricted customer list and monitored by the Management, and future sales are made on a prepayment basis.

Goods are sold subject to retention of title clauses, so that in the event of non-payment the Company may have a secured claim. The Company does not require collateral in respect of trade and other receivables. The Company establishes an

allowance for impairment that represents its estimate of incurred losses in respect of trade and other receivables and investments. The main components of this allowance are a specific loss component that relates to individually significant exposures, and a collective loss component established for groups of similar assets in respect of losses that have been incurred but not yet identified. The collective loss allowance is determined based on historical data that considered an estimation made by the Company related to Receivables, other debit balances and investments.

liquidity riskLiquidity risk is the risk that the Company will not be able to meet its financial obligations as they fall due. The Company’s approach to managing liquidity is to ensure, as far as possible, that it will always have sufficient liquidity to meet its liabilities when due, under both normal and stressed conditions, without incurring unacceptable losses or risking damage to the Company’s reputation.

The Company uses activity-based costing to cost its products and services, which assists it in monitoring cash flow requirements and optimizing its cash return on investments. Typically the company ensures that it has sufficient cash on demand to meet expected operational expenses for a period of 60 days, including the servicing of financial obligations; this excludes the potential impact of extreme circumstances that cannot reasonably be predicted, such as natural disasters. In addition, the Company maintains the following lines of credit: • Credit facility amounted to L.E 112 467 144 the interest incurred is paid at the interest rate between 9% and 10 % for Facilities in Egyptian pound and at the interest rate between 1 % and 2.5% over the Libor rate for US Dollars facilities.

market risk Market risk is the risk that changes in market prices, such as foreign exchange rates, interest rates and equity prices will affect the Company’s income or the value of its holdings of financial instruments. The objective of market risk management is to manage and control market risk exposures within acceptable parameters, while optimizing the return. The Company buys and sells derivatives, and also incurs financial liabilities, in order to manage market risks. All such transactions are carried out within the guidelines set by the Management.

currency riskThe Company is exposed to currency risk on sales, purchases and borrowings that are denominated in a currency other than the respective functional currencies of the Company, primarily the U.S. Dollars (USD).

The Company uses forward exchange contracts to hedge its currency risk, most with a maturity of less than one year from the reporting date. When necessary, forward exchange contracts are rolled over at maturity.

In respect of other monetary assets and liabilities denominated in foreign currencies, the Company ensures that its net exposure is kept to an acceptable level by buying or selling foreign currencies at spot rates when necessary to address short-term imbalances.

interest rate riskThe Company adopts a policy of ensuring that most of its exposure to changes in interest rates on borrowings is on a fixed rate basis.

capital managementThe Board’s policy is to maintain a strong capital base so as to maintain investor, creditor and market confidence and

to sustain future development of the business. The Board of Directors monitors the return on capital, which the Company defines as net operating income divided by total shareholders’ equity, excluding non-redeemable preference shares. The Board of Directors also monitors the level of dividends to ordinary shareholders.

There were no changes in the Group’s approach to capital management during the year. The Company is not subject to externally imposed capital requirements.

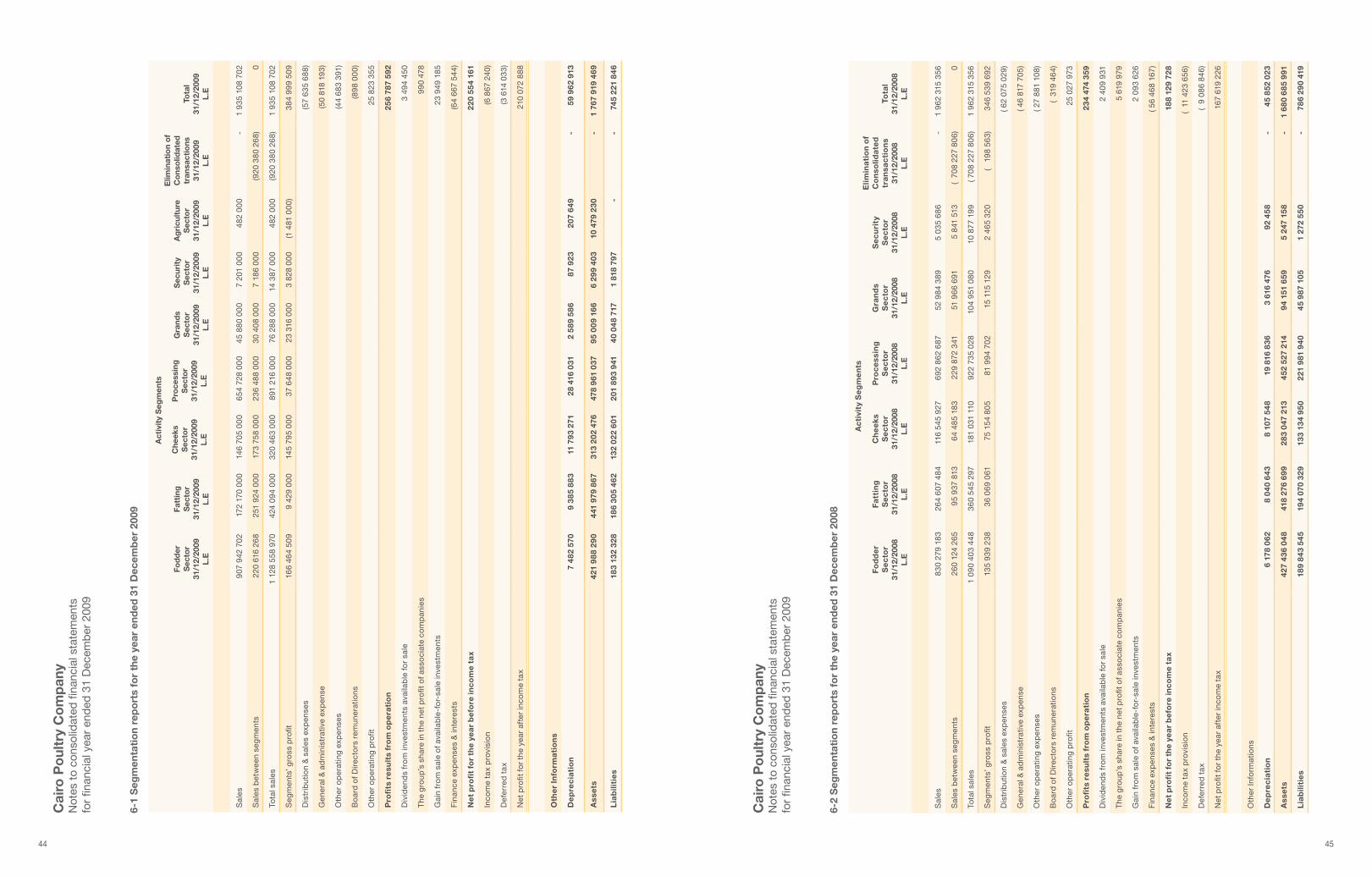

6- segmentation reportsThe segmentation reports was prepared on activity segments basis, the primary report for the activity segments was prepared in accordance with organizational and managerial chart of the company and its subsidiaries. Activities segmentations results include a direct participation unit in each sector activity. The primary report for activity segmentations:A revenue details according to activity segmentations were as follows:

44 45

cai

ro P

oul

try

co

mp

any

N

otes

to

cons

olid

ated

fina

ncia

l sta

tem

ents

fo

r fin

anci

al y

ear

end

ed 3

1 D

ecem

ber

200

9

Fod

der

sec

tor

31/1

2/20

09l.

e

Fatt

ing

sec

tor

31/1

2/20

09l.

e

act

ivit

y s

egm

ents

Gra

nds

sec

tor

31/1

2/20

09l.

e

sec

urit

ys

ecto

r31

/12/

2009

l.e

ag

ricu

ltur

es

ecto

r31

/12/

2009

l.e

elim

inat

ion

of

co

nso

lidat

edtr

ansa

ctio

ns31

/12/

2009

l.e

Tota

l31

/12/

2009

l.e

che

eks

sec

tor

31/1

2/20

09l.

e

Pro

cess

ing

sec

tor

31/1

2/20

09l.

e

Sal

es 9

07 9

42 7

02

172

170

00

0 1

46 7

05 0

00

654

728

00

0 4

5 88

0 0

00

7 2

01 0

00

482

00

0-

1 93

5 10

8 70

2

Sal

es b

etw

een

seg

men

ts 2

20 6

16 2

68

251

924

00

0 1

73 7

58 0

00

236

488

00

0 3

0 40

8 0

00

7 1

86 0

00

(920

380

268

)

0

Tota

l sal

es1

128

558

970

424

094

00

0 3

20 4

63 0

00

891

216

00

0 7

6 28

8 0

00

14

387

00

0 4

82 0

00

(920

380

268

)1

935

108

702

Seg

men

ts’ g

ross

pro

fit 1

66 4

64 5

09

9 4

29 0

00

145

795

00

0 3

7 64

8 0

00

23

316

00

0 3

828

00

0(1

481

00

0) 3

84 9

99

509

Dis

trib

utio

n &

sal

es e

xpen

ses

(57

635

688)

Gen

eral

& a

dm

inis

trat

ive

exp

ense

(50

818

193)

Oth

er o

per

atin

g ex

pen

ses

(44

683

391)

Bo

ard

of D

irec

tors

rem

uner

atio

ns(8

98 0

00)

Oth

er o

per

atin

g p

rofit

25

823

355

Pro

fits

re

sult

s fr

om

op

era

tio

n 2

56 7

87 5

92

Div

iden

ds

fro

m in

vest

men

ts a

vaila

ble

fo

r sa

le 3

494

450

The

gro

up’s

sha

re in

the

net

pro

fit o

f ass

oci

ate

com

pan

ies

99

0 47

8

Gai

n fr

om

sal

e o

f ava

ilab

le-f

or-

sale

inve

stm

ents

23

949

185

Fin

ance

exp

ense

s &

inte

rest

s(6

4 6

67 5

44)

Net

pro

fit

for

the

yea

r b

efo

re in

co

me

tax

220

55

4 16

1

Inco

me

tax

pro

visi

on

(6 8

67 2

40)

Def

erre

d t

ax(3

614

033

)

Net

pro

fit f

or

the

year

aft

er in

com

e ta

x 2

10 0

72 8

88

oth

er

info

rma

tio

ns

De

pre

cia

tio

n 7

482

570

9

38

5 8

83

11

793

271

28

416

031

2 5

89 5

86

87

923

207

649

- 5

9 9

62 9

13

ass

ets

421

98

8 29

0 4

41 9

79 8

67

313

202

476

4

78 9

61 0

37

95

00

9 16

6 6

299

403

1

0 47

9 23

0-

1 76

7 91

9 46

9

lia

bili

tie

s 1

83

132

328

186

305

462

1

32 0

22 6

01

201

893

941

4

0 04

8 71

7 1

818

797

-

- 7

45

221

846

6-1

seg

men

tati

on

rep

ort

s fo

r th

e ye

ar e

nded

31

Dec

emb

er 2

009

Fo

dd

er

se

cto

r31

/12/

2008

l.e

Fatt

ing

se

cto

r31

/12/

2008

l.e

ac

tivi

ty s

eg

me

nts

Gra

nd

ss

ec

tor

31/1

2/20

08l.

e

se

cu

rity

se

cto

r31

/12/

2008

l.e

elim

ina

tio

n o

fc

on

solid

ate

dtr

an

sac

tio

ns

31/1

2/20

08l.

e

Tota

l31

/12/

2008

l.e

ch

eek

ss

ec

tor

31/1

2/20

08l.

e

Pro

ce

ssin

gs

ec

tor

31/1

2/20

08l.

e

Sal

es 8

30 2

79 1

83

264

607

484

1

16 5

45 9

27

692

862

687

5

2 98

4 38

9 5

035

686

-

1 9

62 3

15 3

56

Sal

es b

etw

een

seg

men

ts 2

60 1

24 2

65

95

937

813

64

485

183

229

872

341

5

1 9

66

691

5 8

41 5

13

( 70

8 22

7 80

6)

0

Tota

l sal

es1

09

0 40

3 44

8 3

60 5

45 2

97 1

81 0

31 1

10 9

22 7

35 0

28 1

04 9

51 0

80 1

0 87

7 19

9( 7

08 2

27 8

06)

1 9

62 3

15 3

56

Seg

men

ts’ g

ross

pro

fit 1

35 9

39 2

38 3

6 0

69 0

61

75

154

805

81

994

702

15

115

129

2 4

65 3

20(

198

563

) 3

46 5

39 6

92

Dis

trib

utio

n &

sal

es e

xpen

ses

( 62

075

029)

Gen

eral

& a

dm

inis

trat

ive

exp

ense

( 46

817

705)

Oth

er o

per

atin

g ex

pen

ses

( 27

881

108)

Bo

ard

of D

irec

tors

rem

uner

atio

ns(

319

464)

Oth

er o

per

atin

g p

rofit

25

027

973

Pro

fits

re

sult

s fr

om

op

era

tio

n 2

34

474

359

Div

iden

ds

fro

m in

vest

men

ts a

vaila

ble

fo

r sa

le 2

40

9 93

1

The

gro

up’s

sha

re in

the

net

pro

fit o

f ass

oci

ate

com

pan

ies

5 6

19 9

79

Gai

n fr

om

sal

e o

f ava

ilab

le-f

or-

sale

inve

stm

ents

2 0

93 6

26

Fin

ance

exp

ense

s &

inte

rest

s( 5

6 46

8 16

7)

Net

pro

fit

for

the

yea

r b

efo

re in

co

me

tax

18

8 12

9 72

8

Inco

me

tax

pro

visi

on

( 11

423

656

)

Def

erre

d t

ax(

9 08

6 84

6)

Net

pro

fit f

or

the

year

aft

er in

com

e ta

x 1

67 6

19 2

26

Oth

er In

form

atio

ns

De

pre

cia

tio

n 6

178

062

8

040

64

3 8

107

54

8 1

9 81

6 8

36

3 6

16 4

76

92

45

8-

45

852

023

ass

ets

427

436

04

8 4

18 2

76 6

99

28

3 04

7 21

3 4

52 5

27 2

14

94

151

659

5 2

47 1

58

-1

68

0 6

85

991

lia

bili

tie

s 1

89 8

43

545

1

94 0

70 3

29

133

13

4 95

0 2

21 9

81 9

40

45

987

105

1

272

550

-

78

6 29

0 41

9

cai

ro P

oul

try

co

mp

any

N

otes

to

cons

olid

ated

fina

ncia

l sta

tem

ents

fo

r fin

anci

al y

ear

end

ed 3

1 D

ecem

ber

200

9

6-2

seg

men

tati

on

rep

ort

s fo

r th

e ye

ar e

nded

31

Dec

emb

er 2

008

46 47

7-1 The cost of land – related to New Cairo poultry Company – includes the sum of LE 232 295, L.E 65 000 represents the value of 5 Acres and 7 Karat, 985 square meter respectively. It was registered during this year. Based upon the final measurement of the land area, total area becomes 3 Acres and 7 Karats.

7-2 The following represents the fixed assets items which were purchased through the group companies based on initial selling contracts, the necessary regulatory procedures for registering and transferring its possession under the company’s name are currently under progress :-

leLand 54 604 384Building & Construction 23 209 976

77 814 360

7-3 The machinery and equipment balance includes LE 10 934 739, representing in the cost for acquiring a treatment line for solid wastes purposes (Cairo processing company), this amount was partially financed by the Ministry of Environment (The project of controlling the industrial pollution- financed by the World Bank-). The amount of LE 1 108 279 equal to 20% of total finance represents a non-refundable grant. Based on the accounting policy no. (3-5), the value of this grant was deducted from cost value of the said treatment line.

7-4 The building caption includes the amount of L.E 2 247 812 represents total finance cost capitalized to this caption until the balance sheet date.

7-5 The machinery and equipment caption includes the amount of L.E 2 972 379 represents total finance cost capitalized to this caption until the balance sheet date.

8- Breeders31/12/2009

le31/12/2008

le

costBeginning of the year 272 621 939 196 767 961

Additions for the year 138 505 527 104 737 417

Disposals for the year (Breeders – grand parents & raising expenses)

( 39 193 032) (28 883 439)

At year end 371 934 434 272 621 939

accumulated amortization Beginning of the year 224 692 015 153 755 517

Amortization for the year 109 547 715 80 970 022

Disposals amortization ( 21 346 505) (10 033 524)

At year end 312 893 225 224 692 015

net book value as at 31 December 2009 59 041 209 47 929 924

9- Plant Wealth31/12/2009

le31/12/2008

lecost as at 1 jan 2009Transfer from project for the year 10 686 878 -Cost at 31 December 2009 10 686 878 -less

Wealth amortization 207 649 -Net book value as at 31 December 2009 10 479 229 -

10- Projects under construction31/12/2009

le31/12/2008

le

Buildings & construction in progress 55 115 044 45 502 573Machinery & Equipment under installation 29 642 933 20 155 732Advance payments for fixed assets acquisition 11 629 367 25 711 467L/Cs for purchasing fixed assets 4 134 855 15 824 946Plant life stock – land reclamation - 11 229 481

100 522 199 118 424 199

cai

ro P

oul

try

co

mp

any

N

otes

to

cons

olid

ated

fina

ncia

l sta

tem

ents

fo

r fin

anci

al y

ear

end

ed 3

1 D

ecem

ber

200

9 la

nd

s l

.eB

uild

ing

sl

.e

mac

hin

ery

&e

qu

ipm

en

tl

.e

ve

hic

les

& m

ean

s o

f tr

an

spo

rta

tio

nl

.e

Too

ls a

nd

eq

uip

me

nt

l.e

Furn

itu

re &

offi

ce

sup

plie

sl

.eTo

tal

l.e

Co

st a

s at

1 J

anua