27

www.sage-growth.com What’s an IPA To Do? Prepared for IPN Sage Growth Partners October 22, 2014

| Date post: | 15-Jul-2015 |

| Category: |

Healthcare |

| Upload: | sage-growth-partners |

| View: | 109 times |

| Download: | 0 times |

www.sage-growth.com

What’s an IPA To Do? Prepared for IPN Sage Growth Partners October 22, 2014

www.sage-growth.com

About Us

www.sage-growth.com

A Growing Client Roster

www.sage-growth.com

Hypothesis: Health Care Will be Disrupted

There is an overwhelming confluence of

interests, incen6ves, and macro-‐environmental forces that will disrupt the industry and drive

real change – Payment model redesign will be a core catalyst for

change

4

www.sage-growth.com

A Step Further

• Even if no net-‐new, domes6c U.S. HC is a $1T arbitrage opportunity – and its largely in facili6es, specialists, transi6ons, and chronic care management

• Health care will experience its industrial revolu6on – Transparency – Standards – Focus on efficiency

• In an industrial model – community organizers/entrepreneurs (PCPs) are very well suited to assume the mantle of leadership

• The garage is coming to health care • Incen6ves are aligned between payers and enlightened providers beOer

then ever – economics and ACA are driving payers to shiQ risk

5

www.sage-growth.com

Lots of QuesOons

• The role of physicians – especially independents • The role of hospitals and health systems • The role of subs6tutes • The pace of migra6on to VBP • The pace of provider/payer convergence

• WHAT IS THE IPA TO DO?

6

www.sage-growth.com

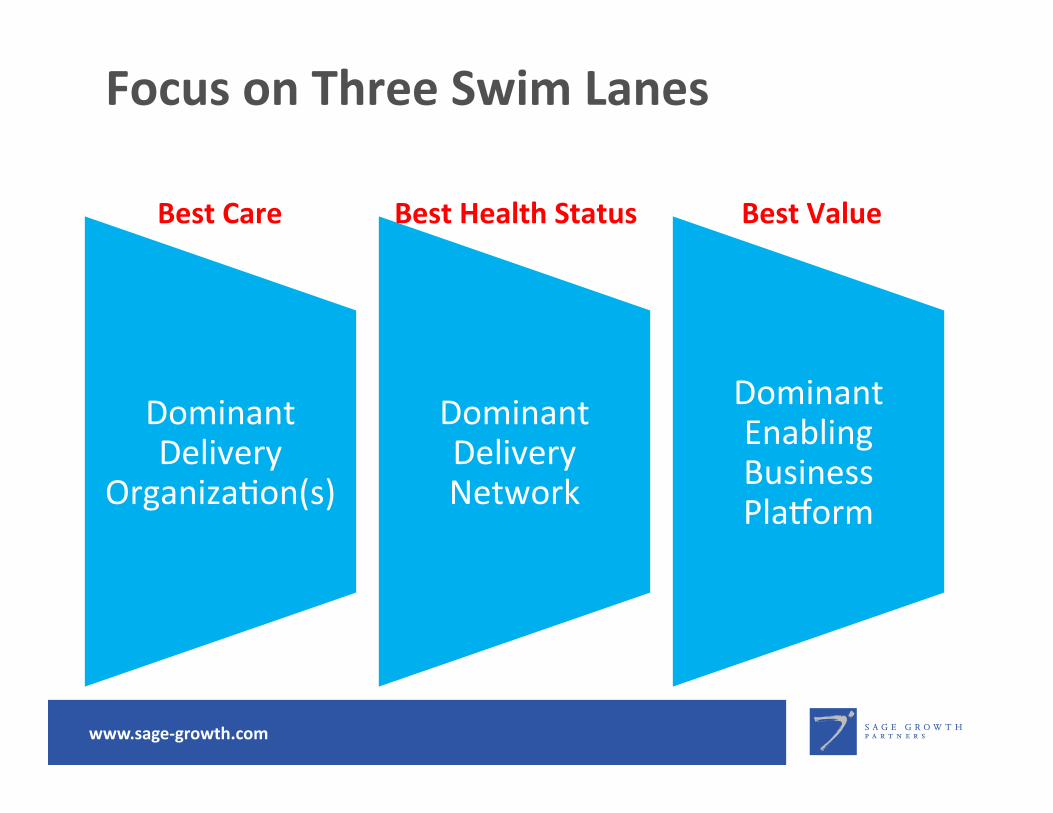

Focus on Three Swim Lanes

Best Care

Dominant Delivery

Organiza6on(s)

Dominant Delivery Network

Dominant Enabling Business PlaZorm

Best Health Status Best Value

www.sage-growth.com

THE EVIDENCE

8

www.sage-growth.com

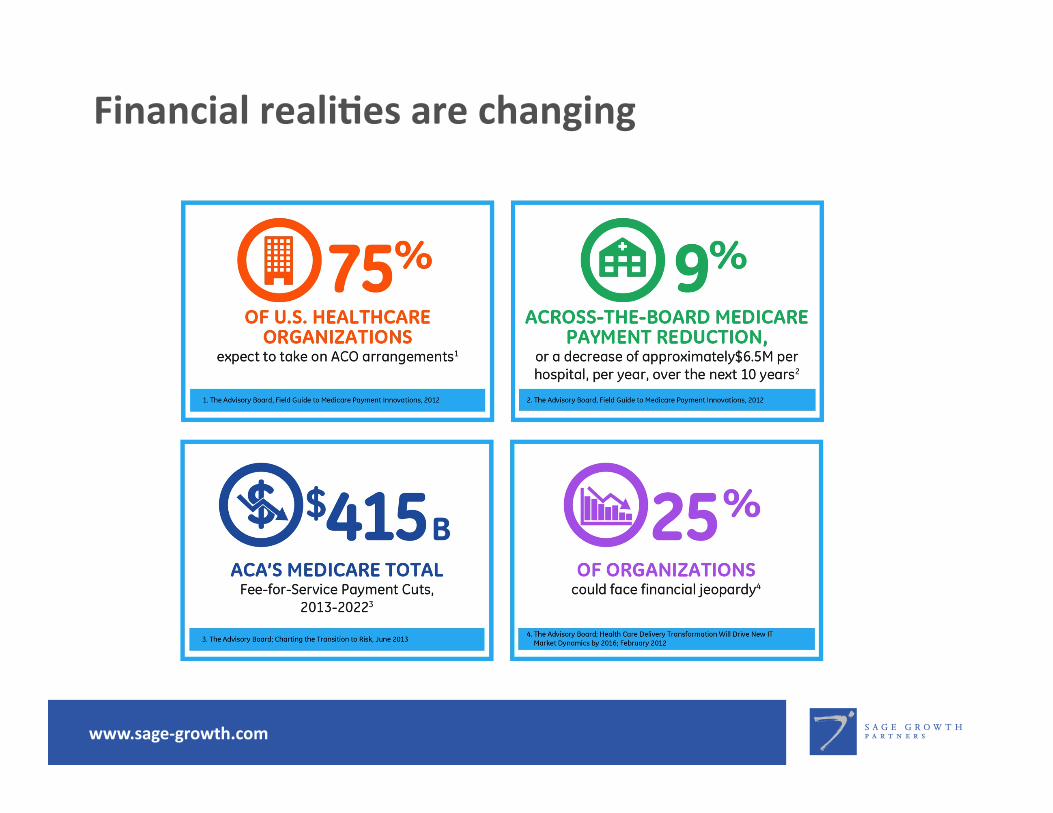

Financial realiOes are changing

www.sage-growth.com

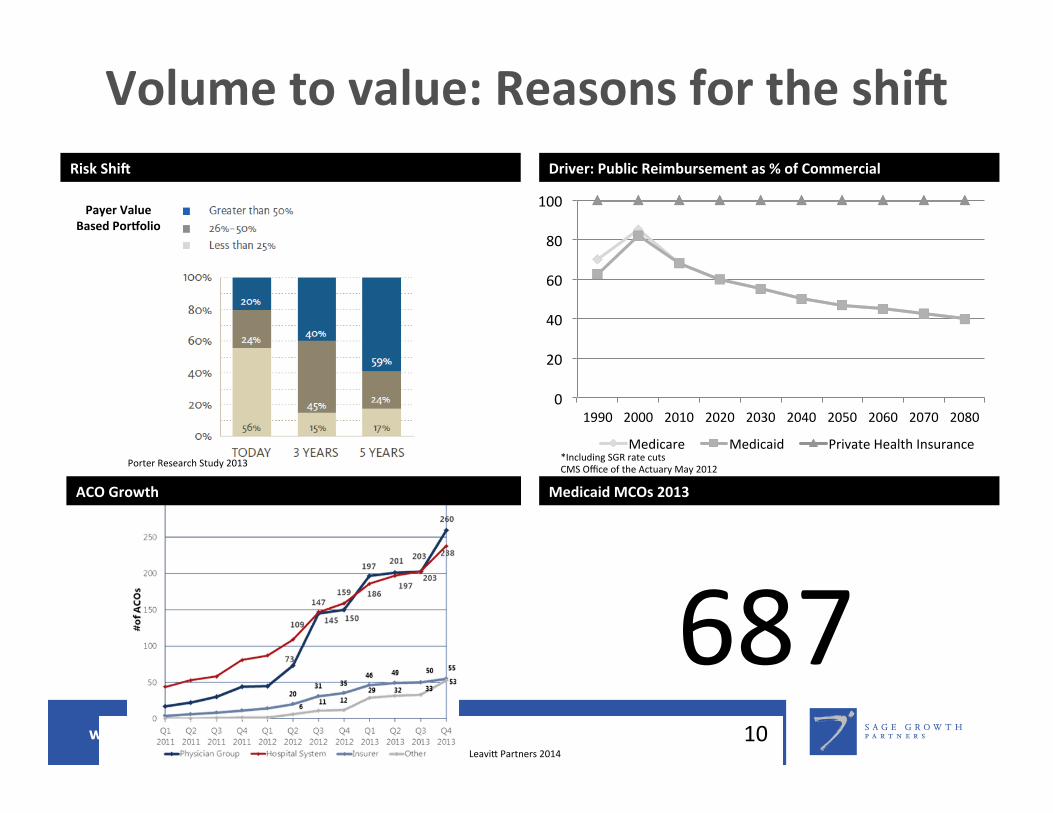

Volume to value: Reasons for the shiT

10

Risk ShiT

Payer Value Based PorVolio

0

20

40

60

80

100

1990 2000 2010 2020 2030 2040 2050 2060 2070 2080

Medicare Medicaid Private Health Insurance

Driver: Public Reimbursement as % of Commercial

ACO Growth

687 Medicaid MCOs 2013

Porter Research Study 2013 *Including SGR rate cuts CMS Office of the Actuary May 2012

LeaviO Partners 2014

www.sage-growth.com

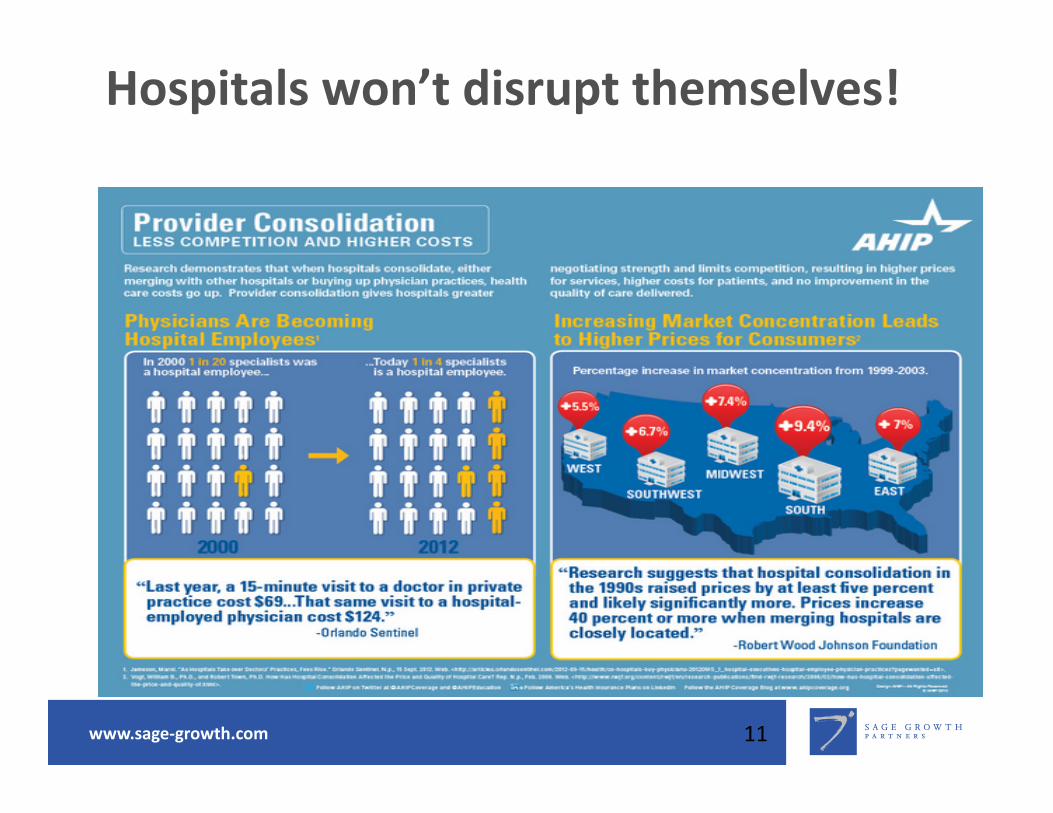

Hospitals won’t disrupt themselves!

11

www.sage-growth.com

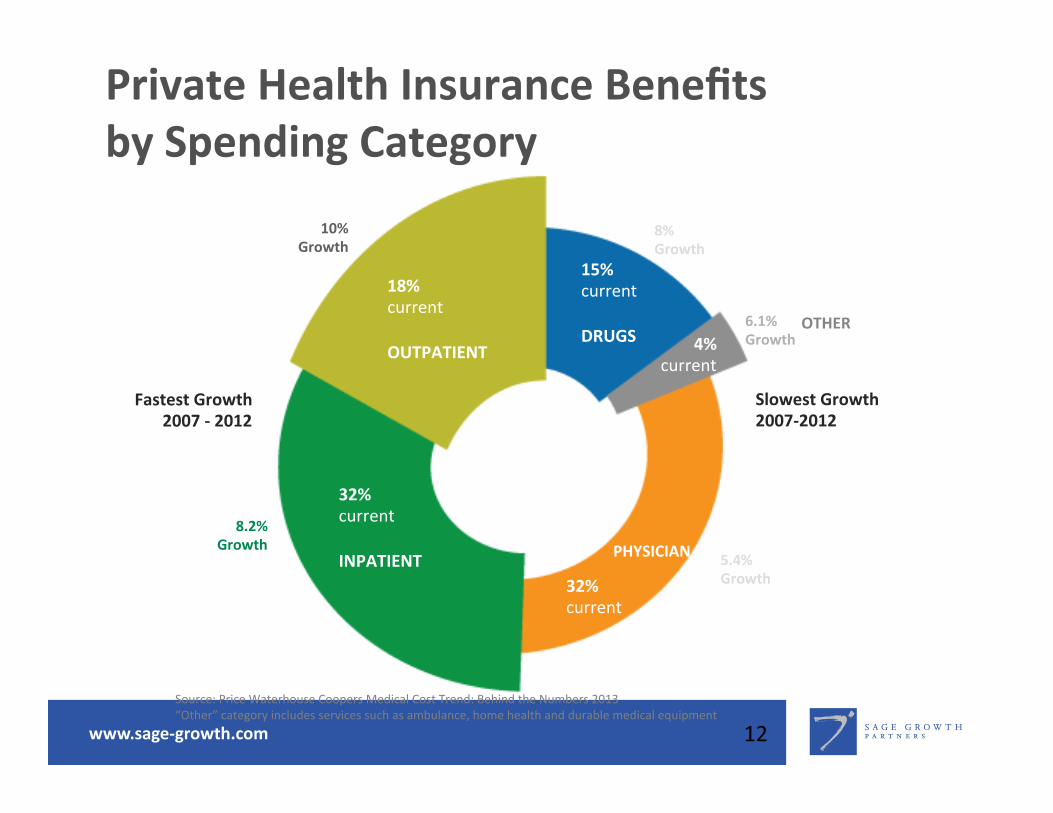

Private Health Insurance Benefits by Spending Category

12

18% current OUTPATIENT

32% current INPATIENT

32% current

PHYSICIAN

4% current

OTHER

15% current DRUGS

Fastest Growth 2007 -‐ 2012

Slowest Growth 2007-‐2012

8.2% Growth

10% Growth

8% Growth

6.1% Growth

5.4% Growth

Source: Price Waterhouse Coopers Medical Cost Trend: Behind the Numbers 2013 “Other” category includes services such as ambulance, home health and durable medical equipment

www.sage-growth.com

The (really) lean health plan

13

www.sage-growth.com

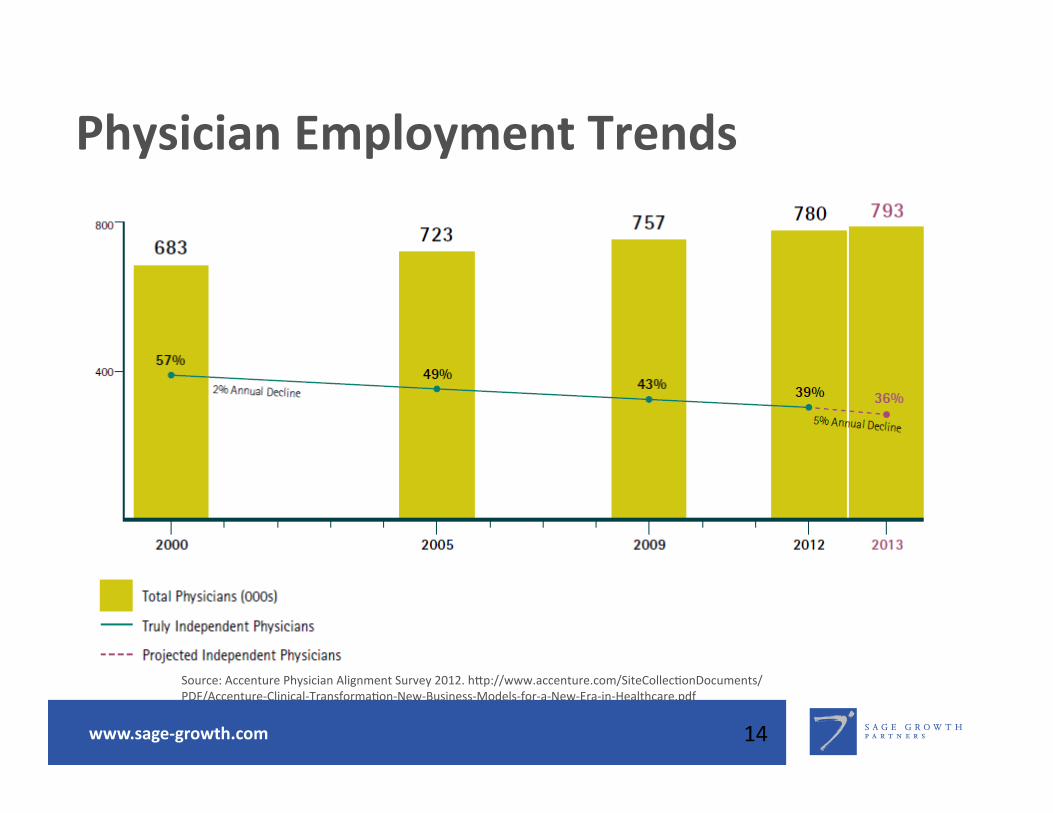

Physician Employment Trends

14

Source: Accenture Physician Alignment Survey 2012. hOp://www.accenture.com/SiteCollec6onDocuments/PDF/Accenture-‐Clinical-‐Transforma6on-‐New-‐Business-‐Models-‐for-‐a-‐New-‐Era-‐in-‐Healthcare.pdf

www.sage-growth.com

Sustainable?

• Hospitals lose on average $176,463 per physician on owned physician prac6ces

• The longer a hospital owns physician groups, the higher the likelihood it is losing money on them.

• The more physicians a hospital employs, the more likely they incur losses

• 78% of hospitals are paying physicians non-‐produc6vity incen6ves (pa6ent sa6sfac6on, clinical quality, and ci6zenship), expected to rise to 94% in 3 years

15

Sources: MGMA 2013 Cost Survey All mul6-‐specialty groups, hospital-‐owned and Report: Hospital-‐owned prac6ces lose up to $100K per doc each year – FiercePrac6ceManagement

www.sage-growth.com

New reality High performing provider organizaOons must manage risk

• Market forces driving a heightened need for financial accountability

• Insurers seeking to transfer the financial risk of clinical service

• The risk-‐transference taking the form of payment-‐for-‐value arrangements

• Entrepreneurial provider-‐sponsored organiza6ons are well posi6oned

• Organiza6ons may lack technology and solu6ons infrastructure to transform their business models

www.sage-growth.com

Where are you? Are you ready?

www.sage-growth.com

NEW (?) PAYMENT MODELS

www.sage-growth.com

IncenOves Drive (bad) Behavior

19

www.sage-growth.com

Why VBP?

• Purchasers are demanding more accountability around quality and cost

• Medicare and Medicaid need the “stop loss” • Its a way to take and grow share • It allows a focus on “industrial improvement”

• Its working in key markets • Its driving quality outcomes

20

www.sage-growth.com

The Impact of Truly Independent PCPs

21

www.sage-growth.com

BUILDING CAPABILITIES TO ADDRESS MARKET NEEDS

www.sage-growth.com

CITI research1 Framework for managing populaOon health

1Source: Popula6on Health Management-‐Hill’s Handbook to the Next Decade in Healthcare Technology, 14 May 2013

www.sage-growth.com

What’s an IPA to Do? NOT MUTUALLY EXCLUSIVE

24

Dominant Delivery

Organiza6on(s)

Dominant Delivery Network

Dominant Enabling Business PlaZorm

www.sage-growth.com

If It Were My IPA, I’d be thinking about…

• PopulaOon Health – let’s define – needs to be CORE – AOribu6on/iden6fica6on – Surveillance – Risk assessment – Risk stra6fica6on – what’s our triangle look like? – Gap assessment – Coordinate/drive interven6ons

• On-‐ramps for providers – especially PCPs – Running through walls to enhance/aggregate primary care

– Build a new economic model – “the era of 3x” – Employment op6ons – Find the entrepreneurs

25

www.sage-growth.com

If It Were My IPA, I’d be thinking about…

• Aggressively courOng Payers/Purchasers (Insurers, TPA/ASO, Employers, Unions, Purchasing Groups) – Make something different happen – Get out and talk early and oQen – Don’t make assump6ons and don’t ignore purchasers

• Embracing transparency wholeheartedly – Prices, Costs, Quality

• Don’t forget the infrastructure – And plan the Ecosystem – IT, Rev Cycle, Messaging, CDS, PH, PI, Retail, remote monitoring, etc. etc. etc.

• Capital Partners – be creaOve

26

www.sage-growth.com

Contact: Sage Growth Partners 3500 Boston Street, Suite 435 Bal3more, Maryland 21224 410.534.1161