17

When you are on your own: economic integration and financial literacy Miryam Hazán, MATT

| Date post: | 16-Dec-2015 |

| Category: |

Documents |

| Upload: | joanna-armstrong |

| View: | 217 times |

| Download: | 0 times |

When you are on your

own: economic

integration and financial

literacy

Miryam Hazán, MATT

Outline

Models of integration and what it means for you

Starting from disadvantage

How immigration reform will change the situation

We are still on our own: financial literacy a survival skill and a road to success

Models of integration

Integration is related to how immigrants absorb the values of their host society (economic, social, political) engage, and navigate the system. When there are not major differences with mainstream society in terms of access to rights and opportunities it is possible to argue that immigrants are integrated

Models of integration

Integration does not proceeds in the same way in every place.

Soysal (1994) distinguished the following models of integration which relate to the type of polity (institutions) immigrants encounter:

• Statist, corporatist, fragmental, and liberal

Models of integration

Statist: state authority is highly centralized, state plays an active role in integrating immigrants

Corporatist: corporate groups (occupational, ethnic, religious and others) play an important role as the source of action and authority. Immigrants need to subscribe to these wider organizations to gain legitimacy and access to rights. These groups take an active responsibility in integrating immigrants

Fragmental: state is weak and has limited interactions with society. Groups based ancestral or religious origin or others which are inaccessible to outsiders play a major role. Integration is very difficult.

Liberal: Source of action and authority is the individual. Authority is more fragmented and local authorities and voluntary organizations play a more active role. The individual is responsible for its integration

You are on your own (US…Texas)

This is bad and good:

You get less support than you might get in other places…which may make the integration process slower and more difficult

but it also brings out the entrepreneurial spirit…reflected for example in the activities of HTAs, which raise funds to support communities of origin

Starting from disadvantage

When you are on your own disadvantage is a problem. From the outset, immigrants are at a disadvantage with respect to the native population because of limited knowledge. But the situation is not equal for all of them.

Mexican immigrants who account for 29% of the foreign born population face the most challenging situation (followed by Central Americans).

Compared with other immigrant groups they are younger, less educated and less likely to speak English well (Pew Hispanic Center, 2012).

Only 23% are citizens compared with 52% from all other countries

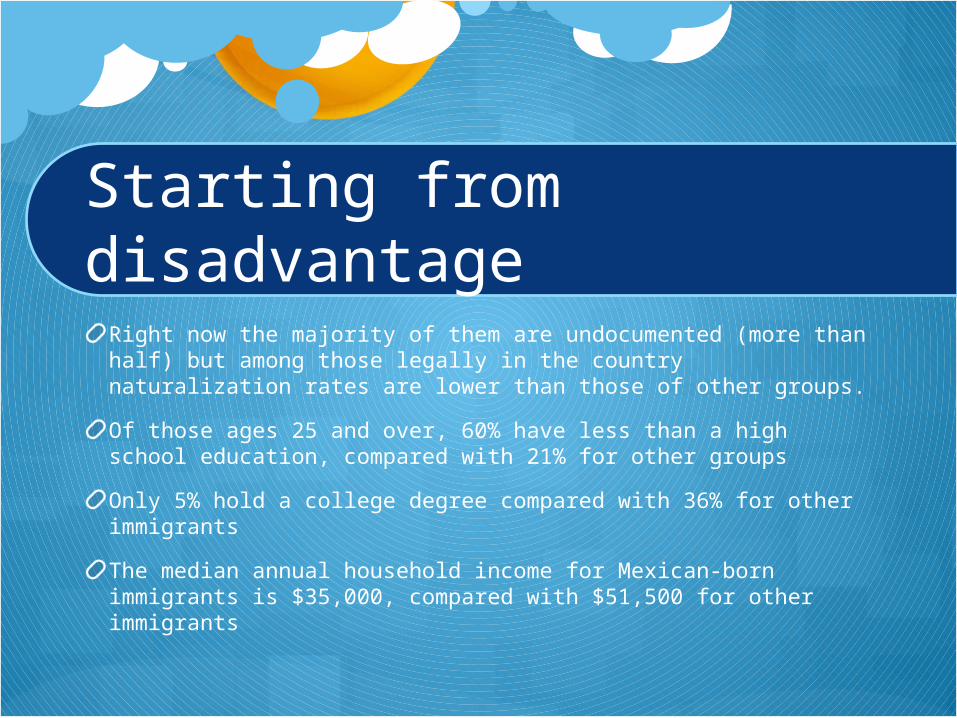

Starting from disadvantage

Right now the majority of them are undocumented (more than half) but among those legally in the country naturalization rates are lower than those of other groups.

Of those ages 25 and over, 60% have less than a high school education, compared with 21% for other groups

Only 5% hold a college degree compared with 36% for other immigrants

The median annual household income for Mexican-born immigrants is $35,000, compared with $51,500 for other immigrants

Starting from disadvantage

Lower income is a reflection of employment profile: 23 % of Mexicans work in the construction, agriculture or mining industries, compared with 6% for other groups

Only 10% of Mexicans work in management, professional and related jobs, compared with 41% of immigrants from other countries

They are somewhat less likely than other groups to be homeowners (46% of households vs 55%)

Starting from disadvantage

A disproportionate percentage (33% to 44%) of Latinos in the U.S. are unbanked (they do not maintain a checking or savings account). Recent immigrants are even more likely to be unbanked. Over half of all Mexican immigrants lack bank accounts and 75% of Mexican remittance senders are unbanked (Stookey, 2006 and, ecommlink, 2009, Huffington Post April 2013)

Starting from disadvantage

Yes, they are entrepreneurial: 18 % of all small business owners in the U.S. are immigrants, and there are more small business owners from Mexico than from any other country (12%). But that is only because Mexicans are the largest immigrant group. For instance, the Fiscal Policy Institute argues that they are less likely than other groups to own small businesses, in great part because of their legal status. Other groups are disproportionately represented for their size. Highest share: Greeks, Palestinians, Israelis, Syrians, Lebanese, Jordanians, Italians, Koreans, South Africans…..

Access to legal status will bring change

For their size Mexicans could do better, and it does not have to do with education only: though better educated migrants are more likely to be business owners, the majority of small business owners, like the majority of their U.S born counterparts do not have a college degree (56%)…Which implies, by the way, that not only educated migrants matter…

It all starts with access to rights, and opportunities which bring social mobility, and access to the resources and information to start a business… or consider a more promising job or career

Legal status matters

Though many consider the amnesty to have failed (from the enforcement perspective), different studies of immigrants that benefited from IRCA in 1986 show that legalization allowed them to earn higher wages and get better jobs

A study by Rob Parral et al (2011) showed that between 1990 and 2006 their educational attainment increased substantially, their poverty rates decreased dramatically, and their levels of homeownership improved a great deal

Immigration reform: the basics

This time legalization, and access to citizenship will take longer… if it finally passes in Congress

The new immigration bill introduced by the gang of eight, only grants them access to the residence after 10 years, and to citizenship after 13 years, and this is contingent on border security.

This will imply that the benefits of legalization will take longer to manifest, especially because they will also be excluded from welfare and health benefits

We are still on our own: financial literacy

But the new bill provides for the creation of an Office of New Americans taskforce and additional integration initiatives, efforts will probably be focused more on teaching them English and civic skills, but it also opens the space of financial literacy…

Financial literacy a survival skill

Those who might benefit the most from legalization are also those who are the most likely to be unbanked. To initiate a normal life in the U.S. these immigrants need to gain basic financial knowledge: how to open checking and savings accounts, how to make a budget, what strategic choices they can make to save for the future (retirement) to send remittances, to get loans to buy a house, and send their kids to university…

Financial literacy: a road to success

Gaining those skills will not only allow immigrants to improve their life prospects and better integrate into their host country.

It will also yield more tax revenue, more consumer buyer power, and more jobs (they will have a better chance to express their entrepreneurial spirit )

It will make them more capable of contributing to the development of their country of origin as well…