March 2010 Wind Power, an Economic Option for Egypt? Yasser Sherif – Environics Based on : Clean Energy Investment in Developing Countries: Wind Power In Egypt IISD, Oct. 2009 (El Sobki, M. - Wooders, P. - Sherif, Y.) http://www.iisd.org/pdf/bali_2_copenhagen_egypt_wind.pdf

Transcript

March 2010

Wind Power, an Economic Option for Egypt?

Yasser Sherif – Environics

Based on :Clean Energy Investment in Developing Countries: Wind Power In Egypt

IISD, Oct. 2009 (El Sobki, M. - Wooders, P. - Sherif, Y.)

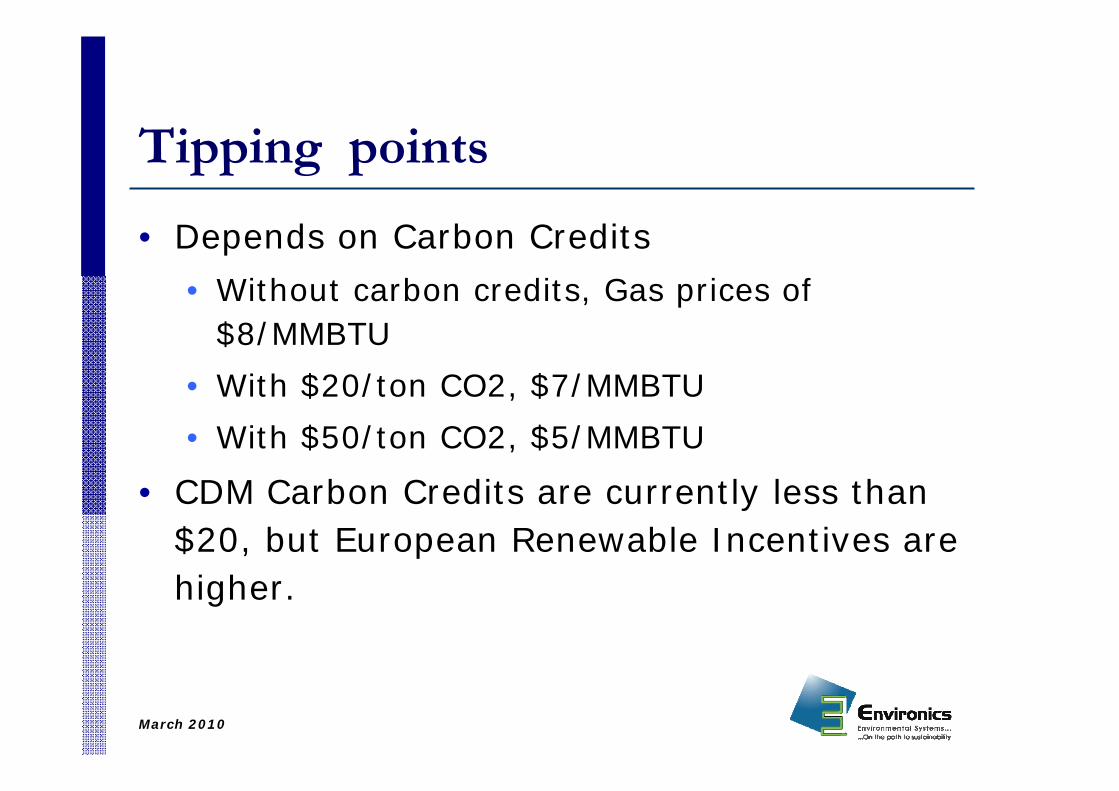

• Wind Resources are sufficiently mapped• Potential is clear but not effectively tapped• Government announcement of ambitious

plans• Large scale implementation needs step

change to private sector mode

March 2010

Satisfactory Developments

• First competitive bid is underway• Feed-in tariff, currently studied• First Private Development to satisfy own need

on track• Resident representatives of international

companies, visits of business development managers

• Local manufacturing capacity is being built claimed to potentially decrease capital costs by up to 25%

March 2010

Financial Viability

• There is no shortage of potential investors• A competitive bidding approach, or a

reasonable ROI insured through the FIT, should make financial sense to investors

• Not for transmission companies, though• NREA currently sells at lower than economic

generation costs, but the planned Renewable Energy Fund should fill this gap

March 2010

Is Support Economically justified?

• Should be an ECONOMIC option for Egypt as a whole?

• Electricity is the service provided• Natural Gas is the primary energy source

potentially displaced by Wind Power• On which 90% of thermal electricity relies • 63% of local consumption by Electricity sector

• Combined Cycle Generation is the rising technology of choice

March 2010

Generating Capacity, 1980-2006

0

5000

10000

15000

20000

25000

1980 1985 1990 1995 2000 2005

Cap

acity

(MW

)

CombinedCycle GasTurbineGas Turbine

Steam Turbine

Hydro

Source: EEHC annual reports

March 2010

Economic Value of Natural Gas• Known to be subsidized and to residential

users ($ 0.5 to 1.5MMBTU) as well as to power generation

• Planned to be for $3/MMBTU for energy intensive industries, $ 1.66 to non-energy intensive industries, and 1.25 for others (PM Decrees in 2007/2008)

• The right reference is obviously not the Costs of production but rather the alternative uses ( at the margin) of Natural Gas not consumed by electricity generation

March 2010

Potential uses of Natural Gas

• At the Margin• Local market for energy• Export (L.N.G or pipelines)• Feed Stock to Petrochemical Industry

• Export as L.N.G is the short term potential alternative use, as existing Capacity not fully utilized

• Take cost of liquefaction into account ($1-1.5/MMBTU based on local plant capital and operation costs)

March 2010

World Market Prices

• There is no single figure • No published figures for LNG export contracts• Figures reported to have been as low as

$2/MMBTU for some older contracts and reached $3-4.5/MMBTU for more recent ones.

• But opportunity Costs are related to future rather than historical prices.

March 2010

Volatile Market PricesMarch 2008- March 2009 March 2009- March 2010

Source: US Nymex-Henry Hub; 2009, 2010

March 2010

Wind & Natural Gas CCGTLevelised Cost Comparison

Wind GasDiscount Rate 10% 10%Economic Lifetime 20 20 years

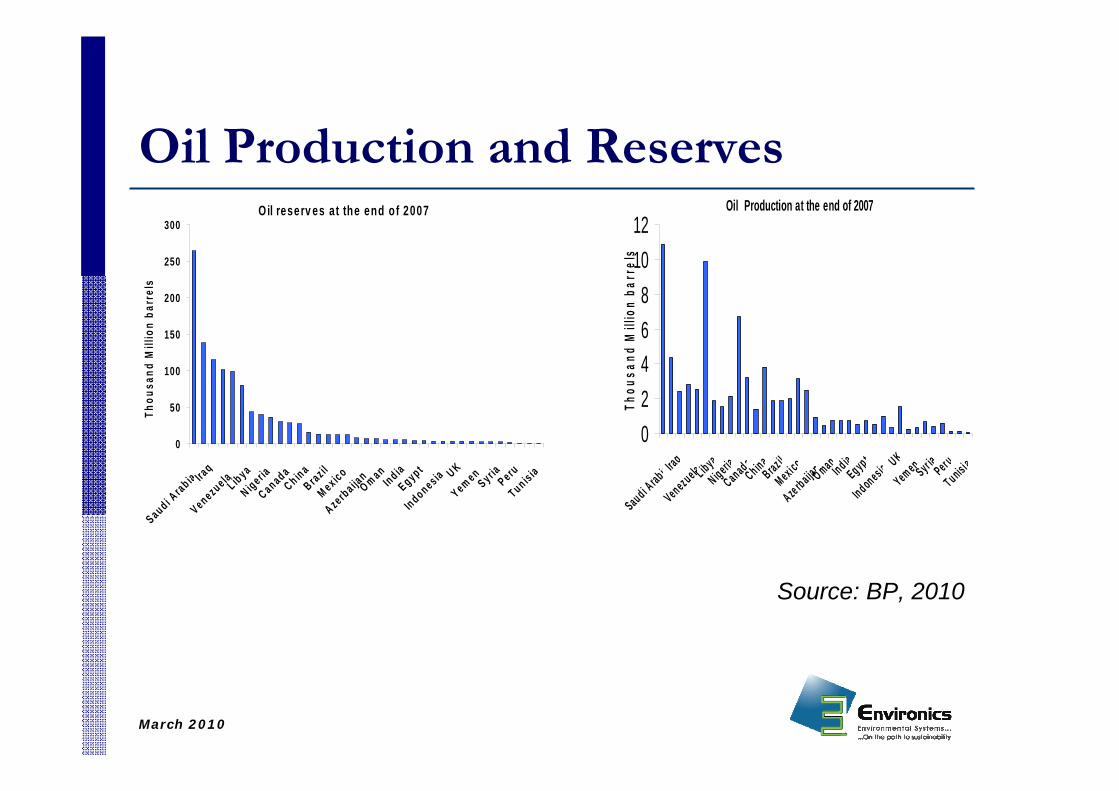

• Oil Production/Reserves Ratio: 0.06 (compared to World Average of 0.02)

• NG Production/ Reserves Ratio:0.028 (compared to World Average of 0.01)

• As opposed to Oil, Natural Gas Production Expected to double in 2030 while demand for Electricity should triple.

• If trend continues, almost all Natural Gas produced should go to power generation

March 2010

A Change in Perspective

• Given the recent, and potential future, price shocks…. And a thinning local resource buffer

• The life of Egypt’s non-renewable resources has to be expanded

• The question becomes not WHETHER to develop wind resources but HOW to improve the economics of its development• Tap on European Renewable Incentives ?• Reduce capital costs ? Local Manufacturing?• ….Raise the REAL opportunity cost of NG ?