96

A Survey Of Private Label Fashion, Food, And Storewide Brands By Melanie Shreffler Editor, Research Alert WOMEN'S RETAIL BRAND AWARENESS

A Survey OfPrivate Label Fashion, Food,

And Storewide Brands

By Melanie Shreffler Editor, Research Alert

WOMEN'SRETAIL BRANDAWARENESS

LICENSE AGREEMENT

By opening or accessing this PDF file, you are entering into the following legally binding license agreement (or, if you obtained this file directly through our website, the following reiterates the terms of the license agreement to which you already have agreed): In return for the license fee you pay, you and your employees are entitled to download the PDF to your personal computer workstations, and to maintain a backup copy for storage. You may print out copies of the document, and route them within your company. You may post the PDF to your secure corporate intranet for internal use only. You may incorporate reasonable portions of the content into your company's PowerPoint presentations, reports or the like.

The PDF may NOT be re-distributed, forwarded, uploaded to the Internet or in any other way shared outside your company without prior written permission of the publisher. Neither the PDF nor the print copies may be given to those outside your company. You will make your employees aware of the terms of this license agreement.

If you do not wish to be bound by these terms, you must return this PDF without accessing, opening or copying it, as described in our return policy.

Women’s Retail BrandAwareness

A Survey Of Private Label Fashion,Food, And Storewide Brands

By Melanie Shreffler

Editor, Research Alert

Additional analysis:Emily Scardino, Executive Editor, The Licensing LetterKaren Raugust, Licensing Letter Special Projects Editor

© 2009 EPM Communications, Inc.ISBN: 978-1-935521-05-1

All rights reserved. Contents may not be reproduced or reprintedby any means without prior consent of the publisher.

Ira Mayer, President & Publisher

Riva Bennett, Chief Operating Officer

Michele Khan, VP Marketing

160 Mercer St., 3rd FloorNew York, NY 10012Phone: 212-941-0099

Fax: 212-941-1622E-mail: [email protected]: www.epmcom.com

TABLE OF CONTENTS

1© Copyright 2009, EPM Communications, Inc. May not be reproduced without written consent of publisher.

Women’s Retail Brand Awareness: A Survey Of Private Label Fashion, Food, And Storewide Brands

INTRODUCTION . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .5

Identifying Brands And Their Retailers . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .5

Exhibit: Most Important Factor That Influences A Shopper’s Choice Whether Or Not ToBuy A Brand, 2009 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .5

Exhibit: Duration Brands Have Been Carried At Their Respective Retailers,Alphabetical By Brand, 2009 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .6

Exhibit: Duration Brands Have Been Carried At Their Respective Retailers, By Retailer, 2009 . . . . . . . . .7External Factors Affecting Brand Awareness . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .8

Survey Methodology . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .9

PART I: IDENTIFYING BRANDS AND THEIR RETAILERS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .11

APPAREL BRAND AWARENESS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .13

Exhibit: Apparel Brand Awareness Overall . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .15Exhibit: Women Who Know, Incorrectly Think They Know, And Are Unsure Where

Private Label Brands Are Carried, In Descending Order Of Those Who Are Correct, 2009 . . . . . . . .16Exhibit: Women Who Know, Incorrectly Think They Know, And Are Unsure Where

Private Label Brands Are Carried, In Descending Order Of Those Who Are Incorrect, 2009 . . . . . . .17Exhibit: Women Who Know, Incorrectly Think They Know, And Are Unsure Where

Private Label Brands Are Carried, In Descending Order Of Those Who Are Not Sure, 2009 . . . . . . .18Exhibit: Women’s Awareness Of Apparel Store Brands, By Age, 2009 . . . . . . . . . . . . . . . . . . . . . . . . . .19Exhibit: Women’s Awareness Of Apparel Store Brands, By Income Level, 2009 . . . . . . . . . . . . . . . . . .20Exhibit: Women’s Awareness Of Apparel Store Brands, By Marital Status, 2009 . . . . . . . . . . . . . . . . . .21Exhibit: Women’s Awareness Of Apparel Store Brands, By The

Presence Of Children In The Household, 2009 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .22

FOOD BRAND AWARENESS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .23

The Name Game . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .24

Exhibit: Women Who Know, Incorrectly Think They Know, And Are Unsure WherePrivate Label Food Brands Are Carried, 2009 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .25

Exhibit: Women’s Awareness of Private Label Food Brands, By Income Level, 2009 . . . . . . . . . . . . . . .26Exhibit: Women’s Awareness of Private Label Food Brands,

By The Presence Of Children In The Household, 2009 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .27Exhibit: Women’s Awareness of Food Private Label Brands, By Age, 2009 . . . . . . . . . . . . . . . . . . . . . .28Exhibit: Women’s Awareness of Private Label Food Brands, By Marital Status, 2009 . . . . . . . . . . . . . .29

STOREWIDE BRAND AWARENESS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .31

Exhibit: Women Who Know, Incorrectly Think They Know, And Are Unsure WherePrivate Label Storewide Brands Are Carried, 2009 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .33

© Copyright 2009, EPM Communications, Inc. May not be reproduced without written consent of publisher.

2

Exhibit: Women’s Awareness Of Storewide Brands, By Age, 2009 . . . . . . . . . . . . . . . . . . . . . . . . . . . . .34Exhibit: Women’s Awareness Of Storewide Brands, By Presence Of

Children In The Household, 2009 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .35Exhibit: Women’s Awareness Of Storewide Brands, By Income Level, 2009 . . . . . . . . . . . . . . . . . . . . .36Exhibit: Women’s Awareness Of Storewide Brands, By Marital Status, 2009 . . . . . . . . . . . . . . . . . . . . .37

PART II: EXTERNAL FACTORS AFFECTING BRAND AWARENESS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .39

FREQUENCY . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .41

Exhibit: Awareness Of Wal-Mart Store Brands Based On Frequency Of Shopping Wal-Mart, 2009 . . . .43Exhibit: Awareness Of Target Store Brands Based On Frequency Of Shopping Target, 2009 . . . . . . . . .44Exhibit: Awareness Of Kohl’s Store Brands Based On Frequency Of Shopping Kohl’s, 2009 . . . . . . . . .45Exhibit: Awareness Of Sears Store Brands Based On Frequency Of Shopping Sears, 2009 . . . . . . . . . .46Exhibit: Awareness Of Kmart Store Brands Based On Frequency Of Shopping Kmart, 2009 . . . . . . . . .47Exhibit: Awareness Of Macy’s Store Brands Based On Frequency Of Shopping Macy’s, 2009 . . . . . . . .48Exhibit: Awareness Of JC Penney Store Brands Based On Frequency Of Shopping JC Penney, 2009 . . .49

DESTINATION BRANDS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .51

Exclusive Brands . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .51

Exhibit: Women Who Say A Brand’s Presence At A Store Makes It ADestination For Them, By Age, 2009 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .53

Exhibit: Women Who Say A Brand’s Presence At A Store Makes It A Destination For Them,By Income, 2009 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .54

Exhibit: Apparel Brand Awareness Among Women Who Say A Brand’s Presence At A StoreMakes It A Destination For Them, 2009 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .55

Exhibit: Food Brand Awareness Among Women Who Say A Brand’s Presence At A StoreMakes It A Destination For Them, 2009 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .56

Exhibit: Storewide Brand Awareness Among Women Who Say A Brand’s Presence At A StoreMakes It A Destination For Them, 2009 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .57

Exhibit: How Brand Exclusivity Affects Women’s Habits, Spending, AndStore Recommendations, 2009 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .58

Exhibit: Brand Exclusivity’s Effect On Shopping Habits,By Shopper’s Belief That Brands Make A Store A Destination, 2009 . . . . . . . . . . . . . . . . . . . . . . . .59

Exhibit: How Brand Exclusivity Affects Shoppers’ Habits, Spending, AndRecommendations, By Age, 2009 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .60

Exhibit: How Brand Exclusivity Affects Shoppers’ Habits, Spending, And Recommendations,By Income, 2009 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .61

Exhibit: How Brand Exclusivity Affects Shoppers’ Habits, Spending, And Recommendations,By Marital Status, 2009 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .62

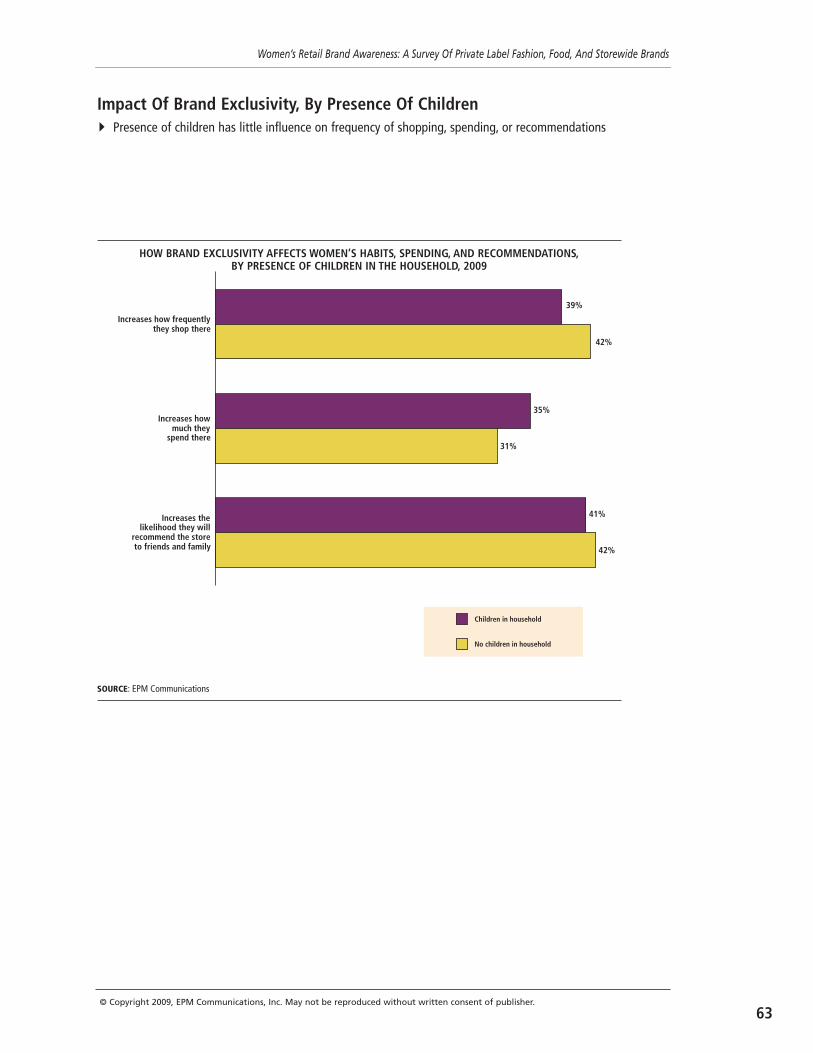

Exhibit: How Brand Exclusivity Affects Shoppers’ Habits, Spending, And Recommendations,By Presence Of Children In The Household . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .63

MEDIA EFFECT ON AWARENESS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .65

Age Distinction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .65

Marital Status . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .65

Income . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .66

Retailer Recall . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .66

Exhibit: Medium By Which Women First Learned About Private LabelApparel And Storewide Brands, 2009 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .67

Exhibit: How Women First Learned About Apparel Brands, By Age, 2009 . . . . . . . . . . . . . . . . . . . . . . .68

Women’s Retail Brand Awareness: A Survey Of Private Label Fashion, Food, And Storewide Brands

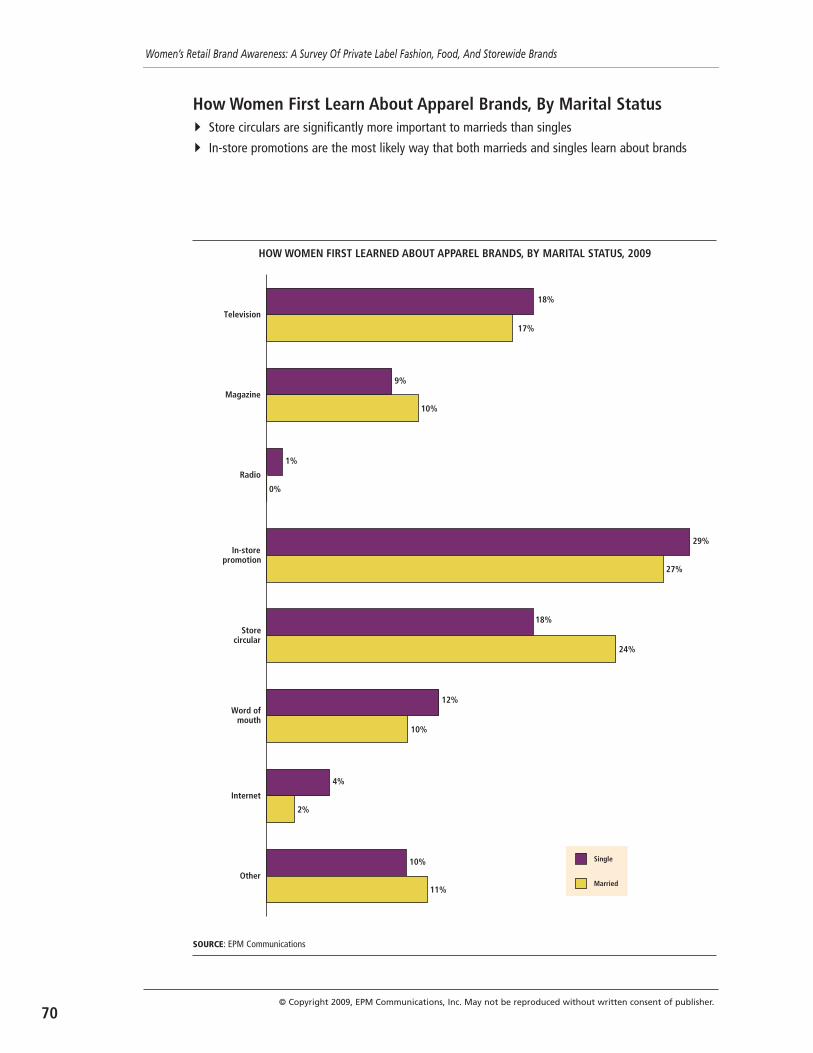

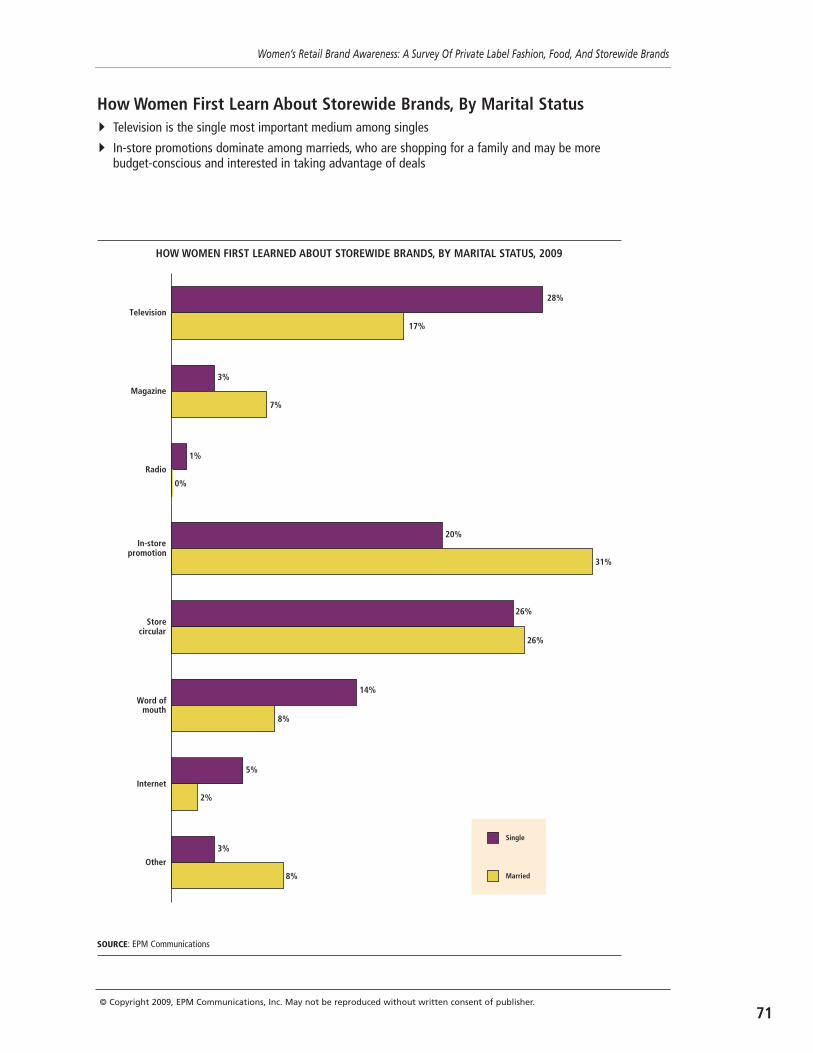

Exhibit: How Women First Learned About Storewide Brands, By Age, 2009 . . . . . . . . . . . . . . . . . . . . .69Exhibit: How Women First Learned About Apparel Brands, By Marital Status, 2009 . . . . . . . . . . . . . . .70Exhibit: How Women First Learned About Storewide Brands, By Marital Status, 2009 . . . . . . . . . . . . .71Exhibit: How Women First Learned About Apparel Brands,

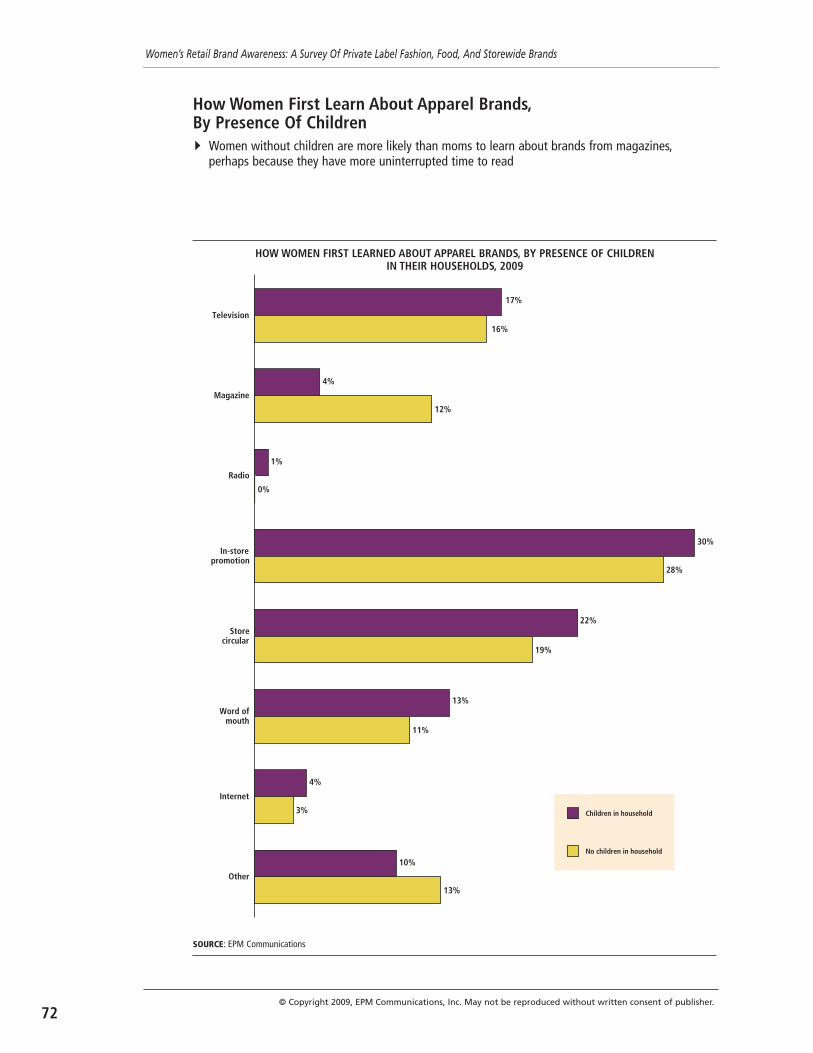

By Presence Of Children In Their Households, 2009 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .72Exhibit: How Women First Learned About Storewide Brands,

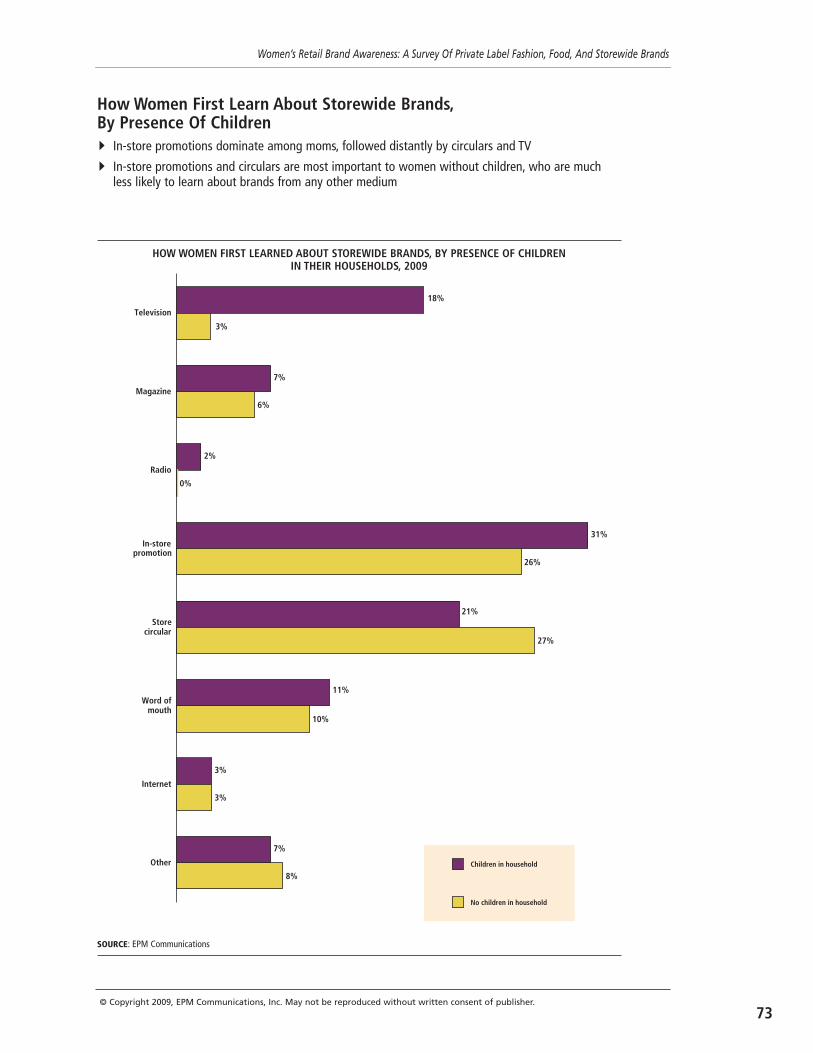

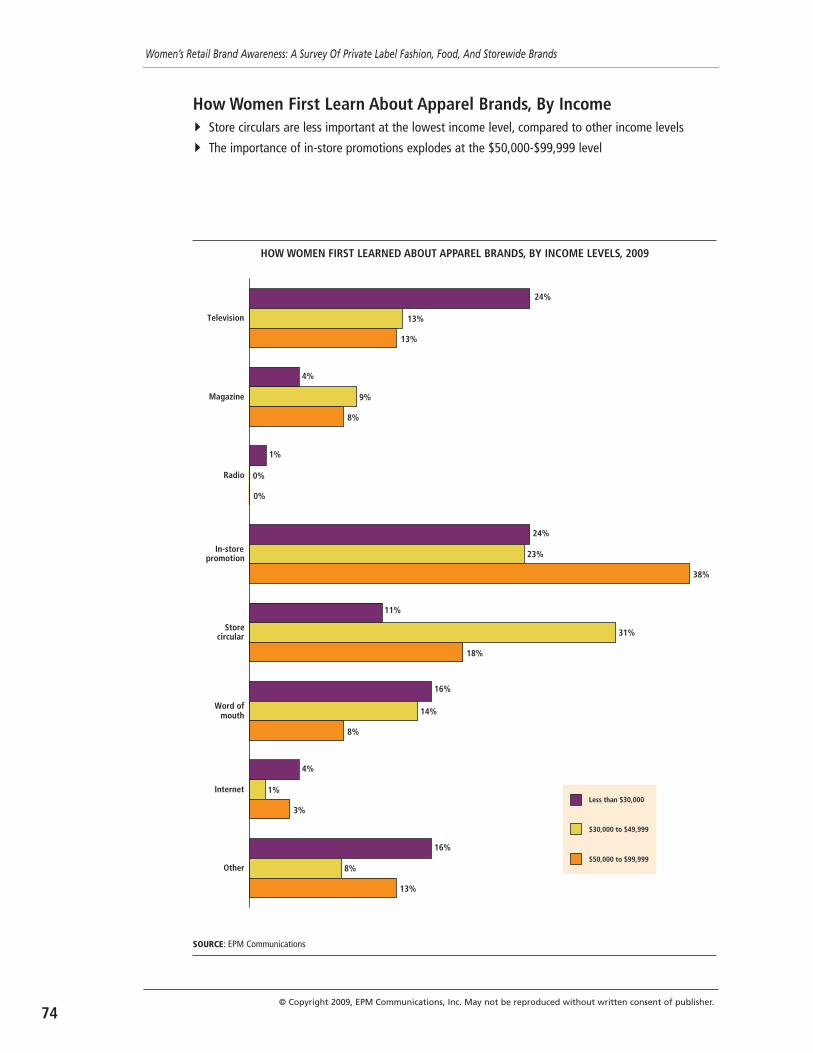

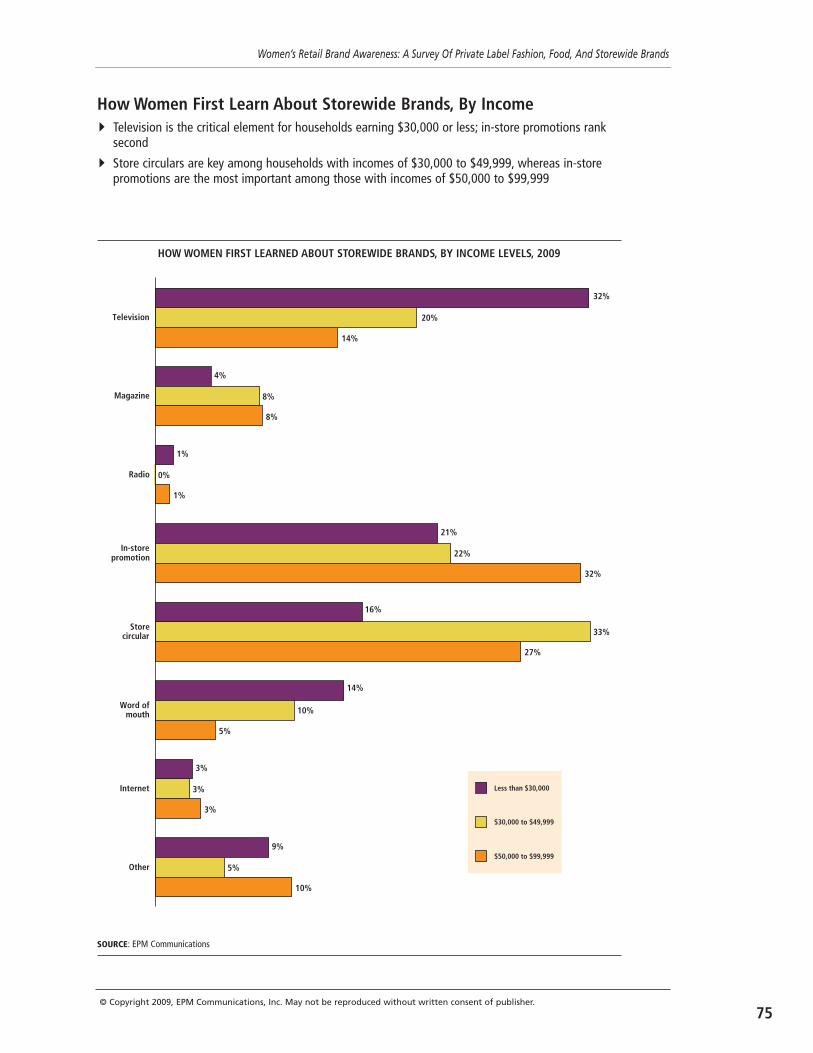

By Presence Of Children In Their Households, 2009 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .73Exhibit: How Women First Learned About Apparel Brands, By Income Levels, 2009 . . . . . . . . . . . . . . .74Exhibit: How Women First Learned About Storewide Brands, By Income Levels, 2009 . . . . . . . . . . . . .75Exhibit: How Women First Learned About Brands Compared To Those Who

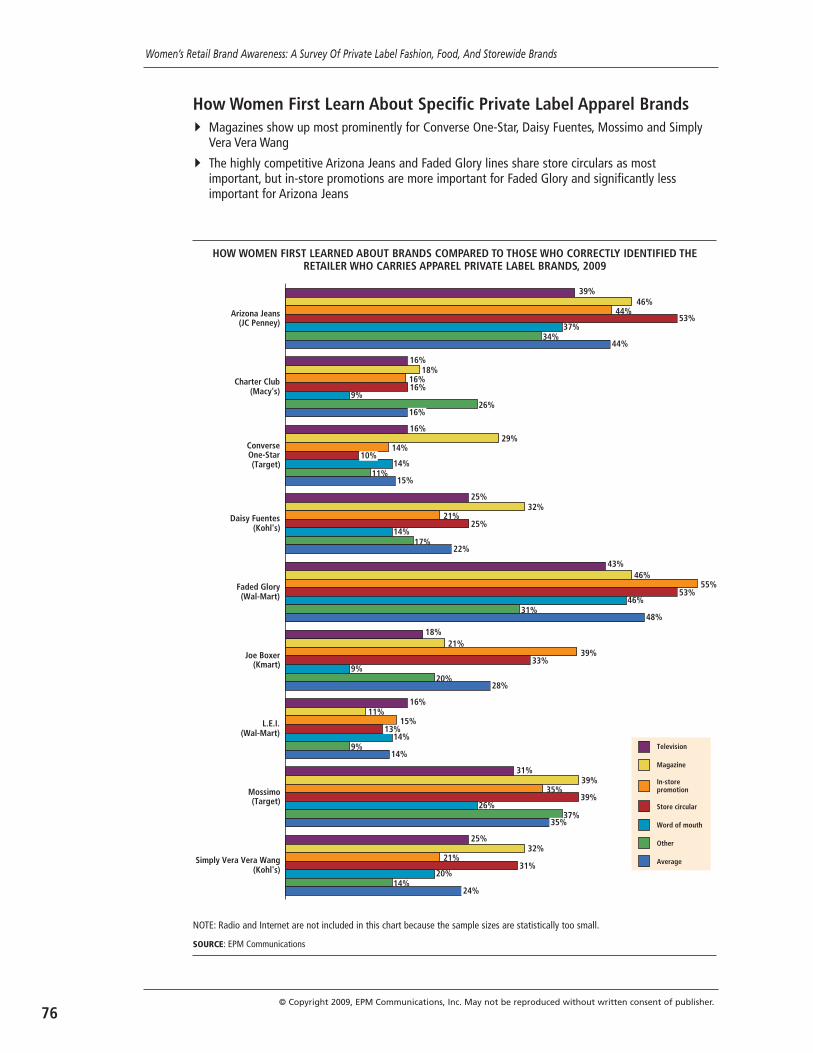

Correctly Identified The Retailer Who Carries Apparel Private Label Brands, 2009 . . . . . . . . . . . . .76Exhibit: How Women First Learned About Brands Compared To Those Who

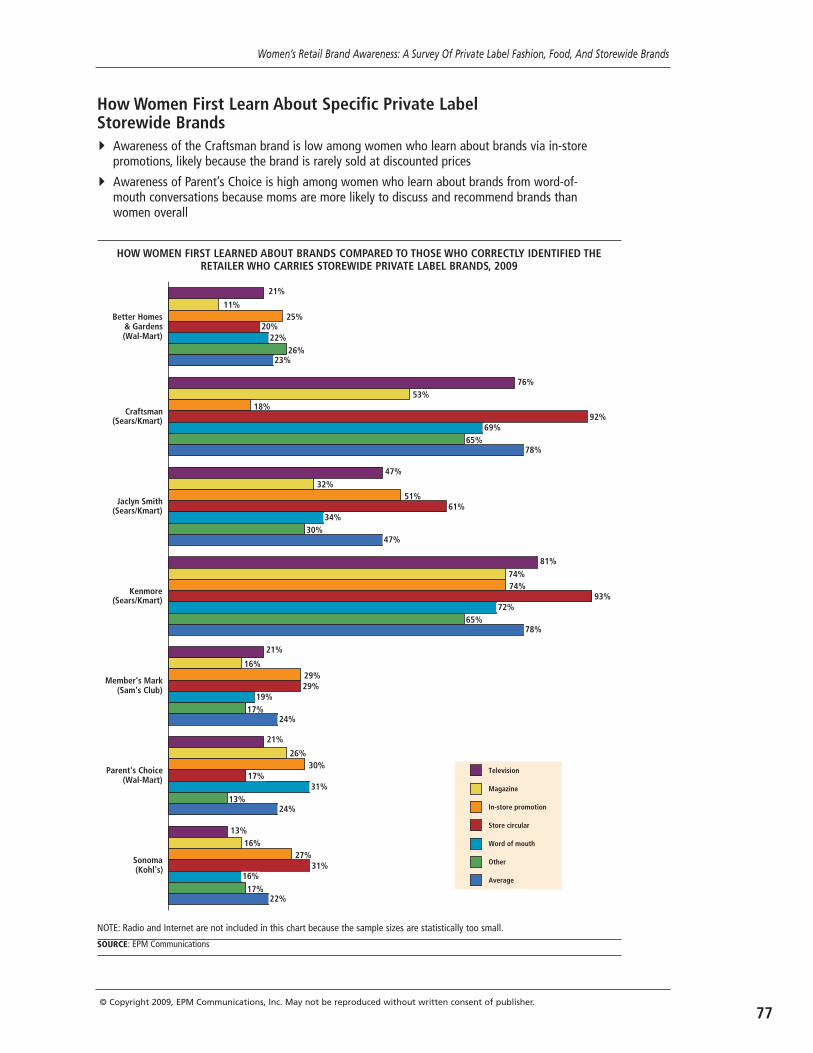

Correctly Identified The Retailer Who Carries Storewide Private Label Brands, 2009 . . . . . . . . . . . .77

LICENSED VS. NON-LICENSED BRANDS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .79

Differences Among Retailers . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .79

Exhibit: Women’s Awareness Of Wal-Mart Private Label And Licensed Brands, 2009 . . . . . . . . . . . . . .83Exhibit: Women’s Awareness Of Target Private Label And Licensed Brands, 2009 . . . . . . . . . . . . . . . . .84Exhibit: Women’s Awareness Of Macy’s Private Label And Licensed Brands, 2009 . . . . . . . . . . . . . . . .85Exhibit: Women’s Awareness Of Kohl’s Private Label And Licensed Brands, 2009 . . . . . . . . . . . . . . . . .86Exhibit: Women’s Awareness Of Sears Private Label And Licensed Brands, 2009 . . . . . . . . . . . . . . . . .87Exhibit: Women’s Awareness Of JC Penney Private Label And Licensed Brands, 2009 . . . . . . . . . . . . .88

ABOUT EPM COMMUNICATIONS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .89

Women’s Retail Brand Awareness: A Survey Of Private Label Fashion, Food, And Storewide Brands

© Copyright 2009, EPM Communications, Inc. May not be reproduced without written consent of publisher.

3

Sales of private label brands are experi-encing strong growth in both unit and dollarsales according to several researchers —including the Private Label Manufacturer’sAssociation, Nielsen, and InformationResources Inc., to name just a few — but doconsumers know what they are buying? Inthis proprietary survey from EPM Communi-cations, publisher of RESEARCH ALERT, THE

LICENSING LETTER, and MARKETING TO WOMEN,we examine how well consumers know 46private label brands available at 20 retailers(see chart, p. 6), and the factors that influ-ence their brand awareness.

We included brands displaying a widerange of products, marketing efforts, andlongevity. Some direct-to-retail powerhouses(such as Martha Stewart) were not includedbecause their lines are in transition from oneretailer to another, or because they havemultiple exclusive lines at different retailers.

The women in this survey are not luxuryshoppers or fashionistas; they representmainstream America and have incomes thatclosely match the income breakdowns of theU.S. Census Bureau’s 2008 American Commu-nity Survey.

Two in 10 women (20%) can correctlyidentify the retailers that carry the brands inthis survey. The same proportion (20%)incorrectly identify the retailer. Three timesas many women (60%) are not sure who car-ries the brands.

Identifying Brands AndTheir Retailers

Sales of private label goods have taken offin recent years not only because manufactur-ers have put more effort into offering moreattractive packaging and labeling, but alsobecause a majority of consumers who have

tried them have deemed them as good asnational brands. In addition, consumers whomay have been reluctant to buy private labelbrands were driven to try them during therecession as they explored ways to savemoney. Private label products are an easyway for shoppers to trade down to lessexpensive items while still meeting theireveryday needs.

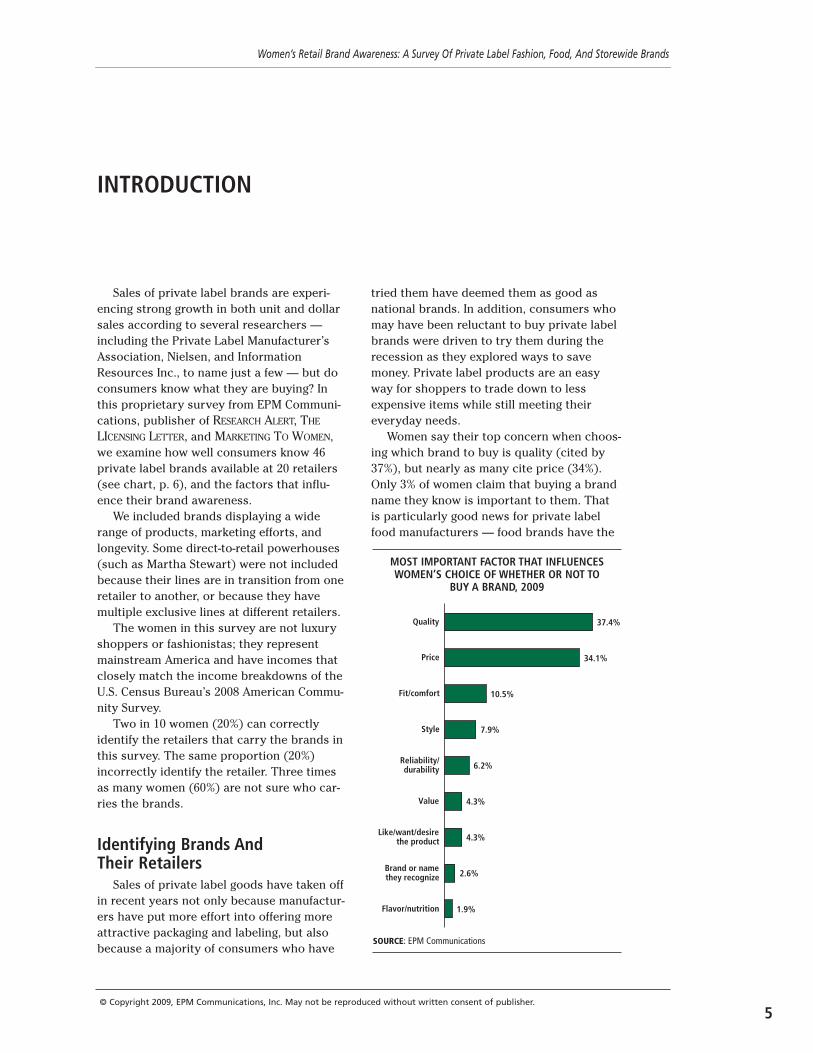

Women say their top concern when choos-ing which brand to buy is quality (cited by37%), but nearly as many cite price (34%).Only 3% of women claim that buying a brandname they know is important to them. Thatis particularly good news for private labelfood manufacturers — food brands have the

Flavor/nutrition

Brand or namethey recognize

Like/want/desirethe product

Value

Reliability/durability

Style

Fit/comfort

Price

Quality 37.4%

34.1%

10.5%

7.9%

6.2%

4.3%

4.3%

2.6%

1.9%

MOST IMPORTANT FACTOR THAT INFLUENCESWOMEN’S CHOICE OF WHETHER OR NOT TO

BUY A BRAND, 2009

SOURCE: EPM Communications

INTRODUCTION

5© Copyright 2009, EPM Communications, Inc. May not be reproduced without written consent of publisher.

Women’s Retail Brand Awareness: A Survey Of Private Label Fashion, Food, And Storewide Brands

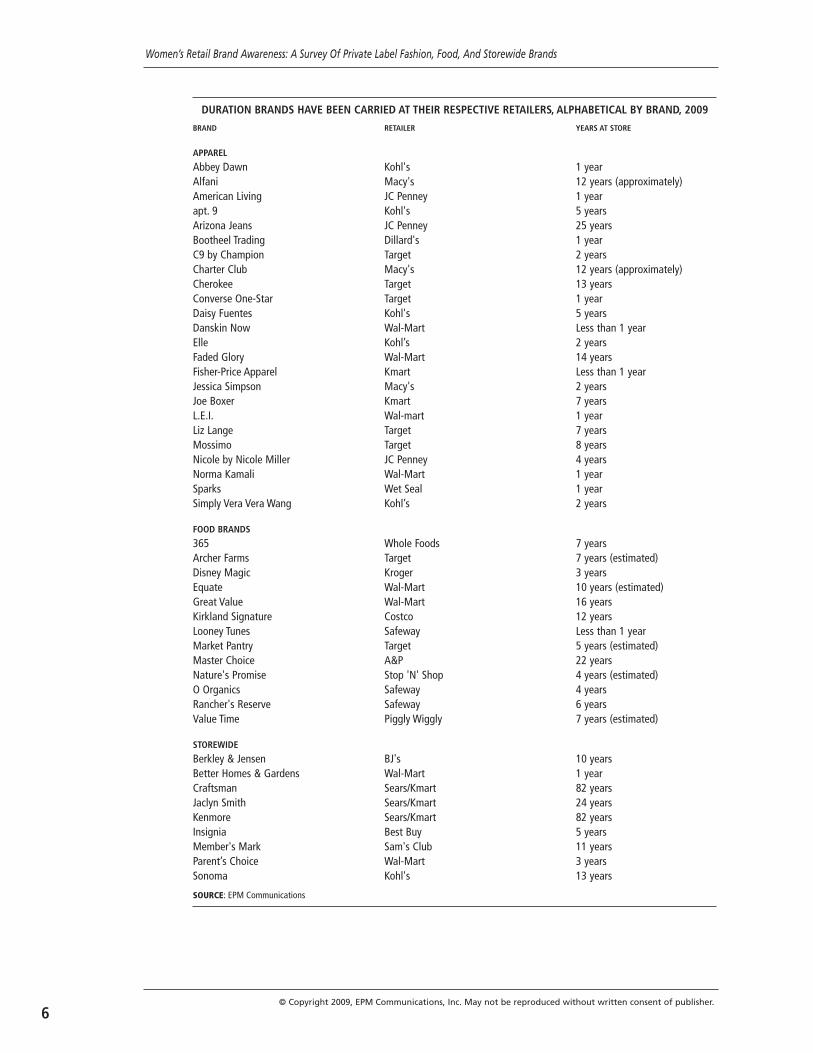

DURATION BRANDS HAVE BEEN CARRIED AT THEIR RESPECTIVE RETAILERS, ALPHABETICAL BY BRAND, 2009

BRAND RETAILER YEARS AT STORE

APPAREL

Abbey Dawn Kohl's 1 yearAlfani Macy's 12 years (approximately)American Living JC Penney 1 yearapt. 9 Kohl's 5 yearsArizona Jeans JC Penney 25 yearsBootheel Trading Dillard's 1 yearC9 by Champion Target 2 yearsCharter Club Macy's 12 years (approximately)Cherokee Target 13 yearsConverse One-Star Target 1 yearDaisy Fuentes Kohl's 5 yearsDanskin Now Wal-Mart Less than 1 yearElle Kohl’s 2 yearsFaded Glory Wal-Mart 14 yearsFisher-Price Apparel Kmart Less than 1 yearJessica Simpson Macy's 2 yearsJoe Boxer Kmart 7 yearsL.E.I. Wal-mart 1 yearLiz Lange Target 7 yearsMossimo Target 8 yearsNicole by Nicole Miller JC Penney 4 yearsNorma Kamali Wal-Mart 1 yearSparks Wet Seal 1 yearSimply Vera Vera Wang Kohl’s 2 years

FOOD BRANDS

365 Whole Foods 7 yearsArcher Farms Target 7 years (estimated)Disney Magic Kroger 3 yearsEquate Wal-Mart 10 years (estimated)Great Value Wal-Mart 16 yearsKirkland Signature Costco 12 yearsLooney Tunes Safeway Less than 1 yearMarket Pantry Target 5 years (estimated)Master Choice A&P 22 yearsNature's Promise Stop 'N' Shop 4 years (estimated)O Organics Safeway 4 yearsRancher's Reserve Safeway 6 yearsValue Time Piggly Wiggly 7 years (estimated)

STOREWIDE

Berkley & Jensen BJ's 10 yearsBetter Homes & Gardens Wal-Mart 1 yearCraftsman Sears/Kmart 82 yearsJaclyn Smith Sears/Kmart 24 yearsKenmore Sears/Kmart 82 yearsInsignia Best Buy 5 yearsMember's Mark Sam's Club 11 yearsParent’s Choice Wal-Mart 3 yearsSonoma Kohl's 13 years

SOURCE: EPM Communications

Women’s Retail Brand Awareness: A Survey Of Private Label Fashion, Food, And Storewide Brands

6© Copyright 2009, EPM Communications, Inc. May not be reproduced without written consent of publisher.

Women’s Retail Brand Awareness: A Survey Of Private Label Fashion, Food, And Storewide Brands

© Copyright 2009, EPM Communications, Inc. May not be reproduced without written consent of publisher.

7

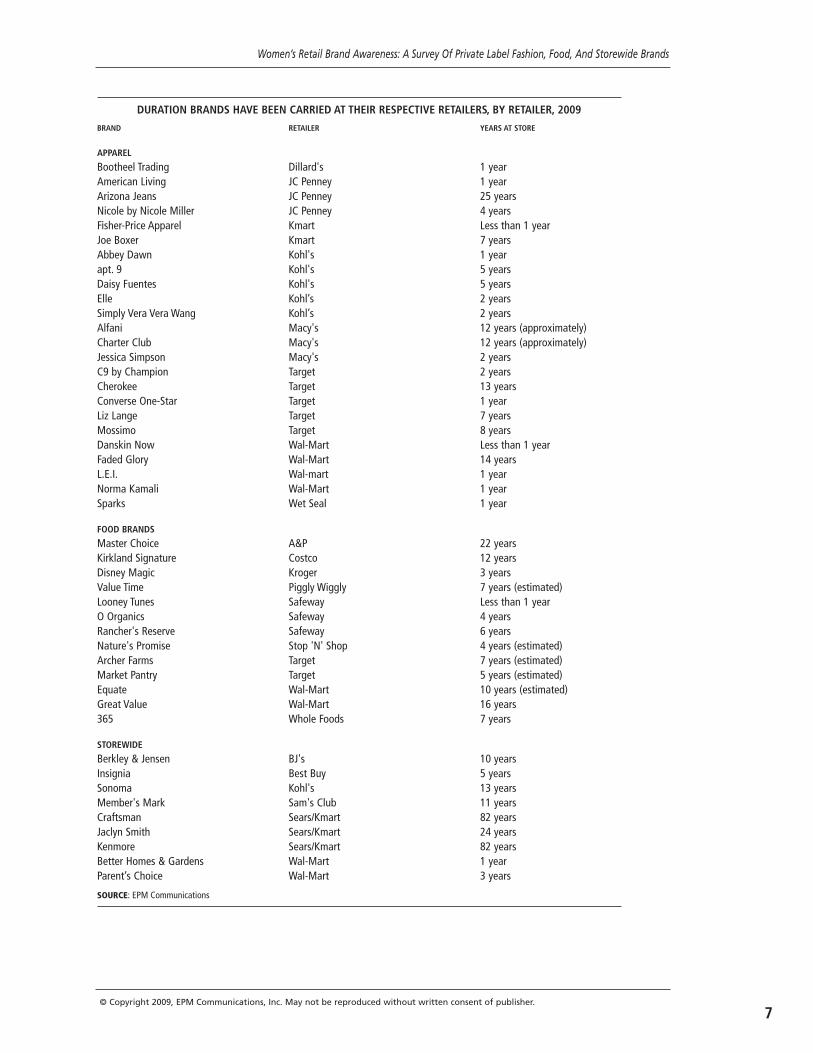

DURATION BRANDS HAVE BEEN CARRIED AT THEIR RESPECTIVE RETAILERS, BY RETAILER, 2009

BRAND RETAILER YEARS AT STORE

APPAREL

Bootheel Trading Dillard's 1 yearAmerican Living JC Penney 1 yearArizona Jeans JC Penney 25 yearsNicole by Nicole Miller JC Penney 4 yearsFisher-Price Apparel Kmart Less than 1 yearJoe Boxer Kmart 7 yearsAbbey Dawn Kohl's 1 yearapt. 9 Kohl's 5 yearsDaisy Fuentes Kohl's 5 yearsElle Kohl’s 2 yearsSimply Vera Vera Wang Kohl’s 2 yearsAlfani Macy's 12 years (approximately)Charter Club Macy's 12 years (approximately)Jessica Simpson Macy's 2 yearsC9 by Champion Target 2 yearsCherokee Target 13 yearsConverse One-Star Target 1 yearLiz Lange Target 7 yearsMossimo Target 8 yearsDanskin Now Wal-Mart Less than 1 yearFaded Glory Wal-Mart 14 yearsL.E.I. Wal-mart 1 yearNorma Kamali Wal-Mart 1 yearSparks Wet Seal 1 year

FOOD BRANDS

Master Choice A&P 22 yearsKirkland Signature Costco 12 yearsDisney Magic Kroger 3 yearsValue Time Piggly Wiggly 7 years (estimated)Looney Tunes Safeway Less than 1 yearO Organics Safeway 4 yearsRancher's Reserve Safeway 6 yearsNature's Promise Stop 'N' Shop 4 years (estimated)Archer Farms Target 7 years (estimated)Market Pantry Target 5 years (estimated)Equate Wal-Mart 10 years (estimated)Great Value Wal-Mart 16 years365 Whole Foods 7 years

STOREWIDE

Berkley & Jensen BJ's 10 yearsInsignia Best Buy 5 yearsSonoma Kohl's 13 yearsMember's Mark Sam's Club 11 yearsCraftsman Sears/Kmart 82 yearsJaclyn Smith Sears/Kmart 24 yearsKenmore Sears/Kmart 82 yearsBetter Homes & Gardens Wal-Mart 1 yearParent’s Choice Wal-Mart 3 years

SOURCE: EPM Communications

Women’s Retail Brand Awareness: A Survey Of Private Label Fashion, Food, And Storewide Brands

lowest level of awareness (17%) among thecategories studied.

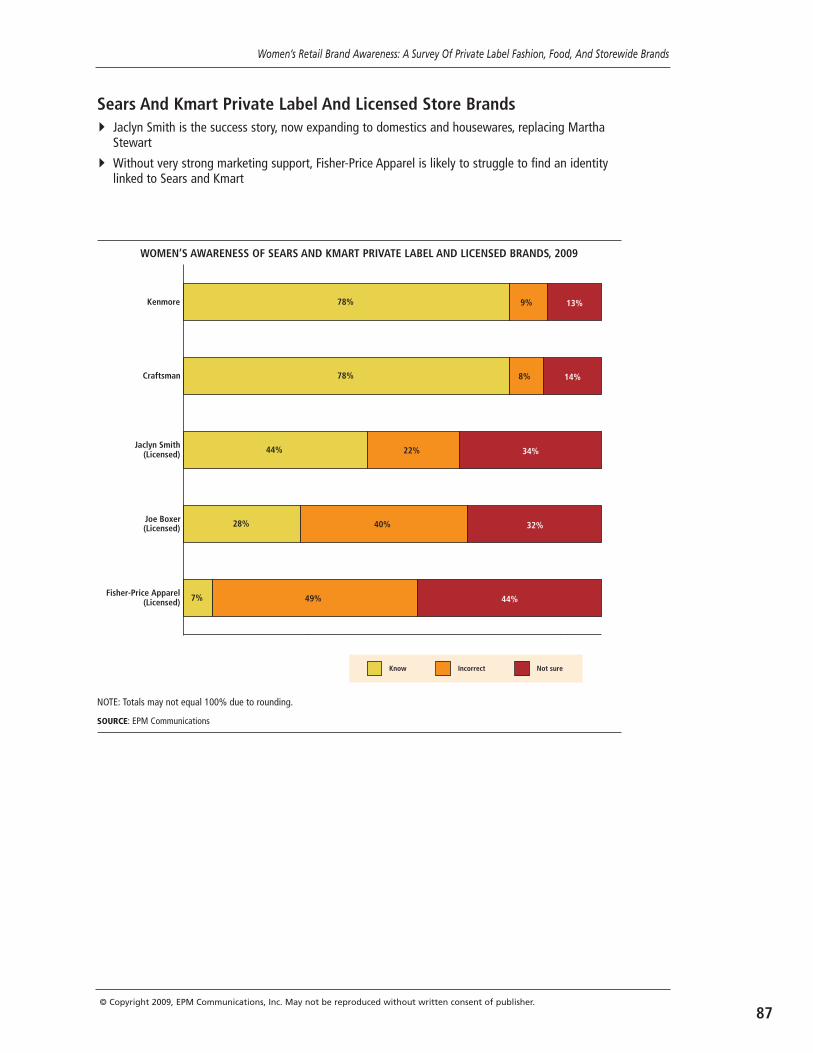

Storewide brands enjoy the highest levelsof awareness among women shoppers (31%).More than three quarters (78%) know theSears/Kmart brands Kenmore and Craftsman— women know tools as well as appliances!Both benefit from being long establishedbrands (82 years each).

Brand longevity positively influencesawareness, as evidenced by brands that topthis survey. Among apparel labels, the threebest-known brands have been in existencefor eight to 25 years; among food brands,seven to 16 years; and among storewidebrands, 24 to 82 years.

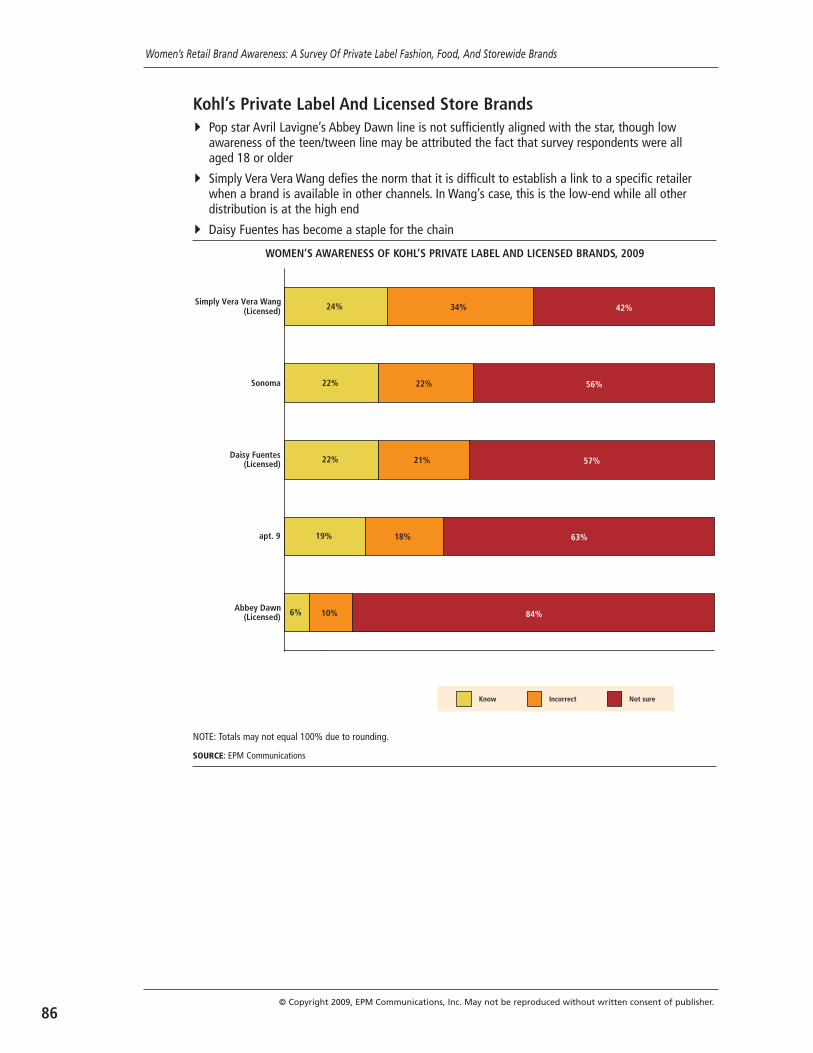

However, some relatively young brands,such as the Better Homes & Gardens label atWal-Mart, have rapidly established strongawareness by leveraging their well-knownnames. Celebrity apparel brands have hadsimilar success, but it is key that theyinclude the celebrity name in the brandname; those that do not fail to reap the bene-fit. For example, Kohl’s Abbey Dawn labelfrom Avril Lavigne scores low despite thepop star appearing in the brand’s advertisingpush. (Admittedly, this survey was adminis-tered only to women 18 years and older; Lav-igne’s line may be better known amongyounger girls.

External Factors AffectingBrand Awareness

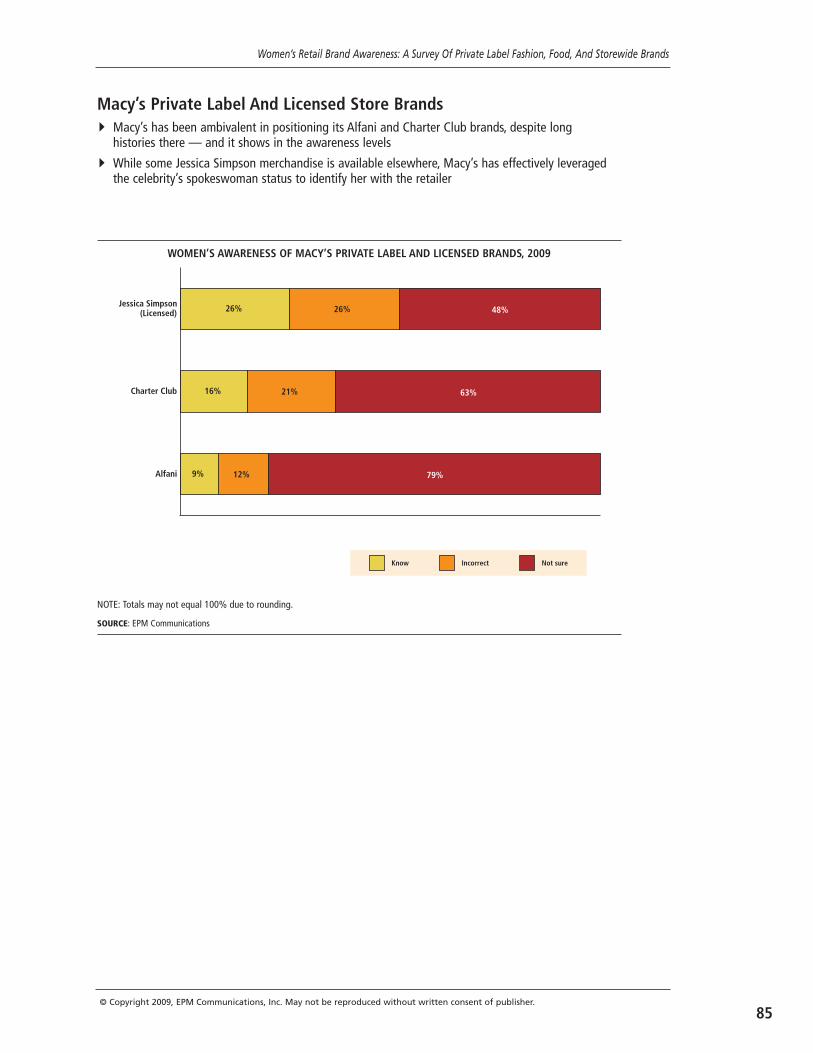

The frequency with which women shop ishighly correlated to how likely they are toknow brands. In general, the more often theyshop a store, the more likely they are toknow the brands that store carries. Amongthe notable exceptions is Jessica Simpson atMacy’s; women are equally likely to know thebrand regardless of how often they shopMacy’s. Simpson was prominently featured inthe retailer’s widespread holiday campaign in2008, which likely boosted awareness amongall women.

Nearly a third of women (31%) say that abrand’s exclusive presence at a store makesit a destination for them when they shop.The younger the women, the more likely theyare to say brands bring them to stores.

Exclusive brands are not only beneficial ingenerating foot traffic to the store, but also

drive sales: 33% of women are likely to spendmore at a store that carries a favorite brandexclusively.

Brand names are key, even among non-“name brand” products. When consumersassociate a retailer with a particular position,they tend to associate brands that referencethat position with that retailer. For example,women think Safeway’s O Organics is sold atWhole Foods because they know that WholeFoods focuses on offering organic and natu-ral products. Women also think that budget-friendly extensions of designer brands, suchas Simply Vera Vera Wang, are available athigher-end department stores Dillard’s orMacy’s, rather than at mid-tier retailer Kohl’s,by nature of the designer name attached tothe brand.

The word “parent” in Wal-Mart’s Parent’sChoice brand explains women’s relativelyhigh awareness (24%) of the three-year-oldbrand. It benefits from being marketed tomoms who are more likely than women ingeneral to discuss and share productreviews. In fact, women who learn aboutbrands via word-of-mouth are more likely toknow Parent’s Choice than women who learnabout brands in other ways.

Wal-Mart, whose historic positioning hasbeen based on low prices, has also cooptedthe word “value.” Women largely ascribe Pig-gly Wiggly’s Value Time brand to Wal-Mart.

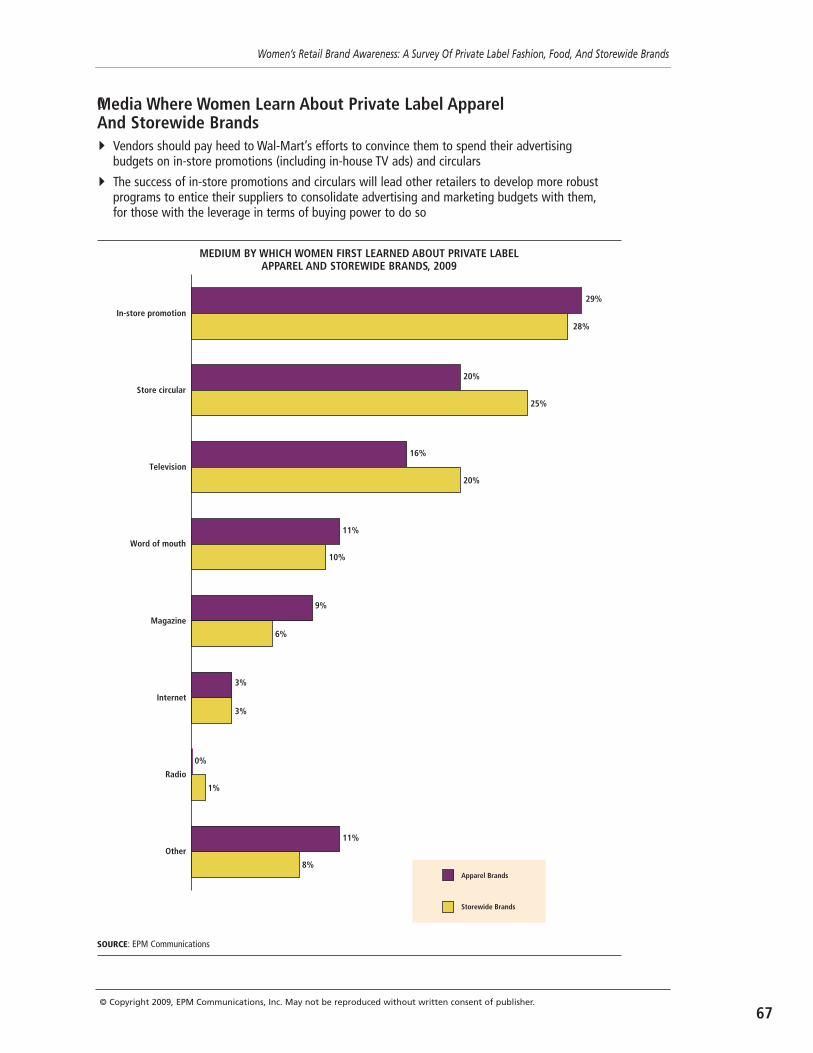

Women are more likely to first learn aboutbrands via store circulars and in-store pro-motions than they are to learn about themthrough television, magazines, radio, andInternet combined.

The way in which they discover brandshas an impact on their brand awareness.Women who learn about brands via in-storepromotions and circulars are more likelythan women overall to know storewidebrands. Those who learn about brands viamagazines are more likely than women over-all to know licensed apparel lines, such asKohl’s Daisy Fuentes or Target’s Mossimo.

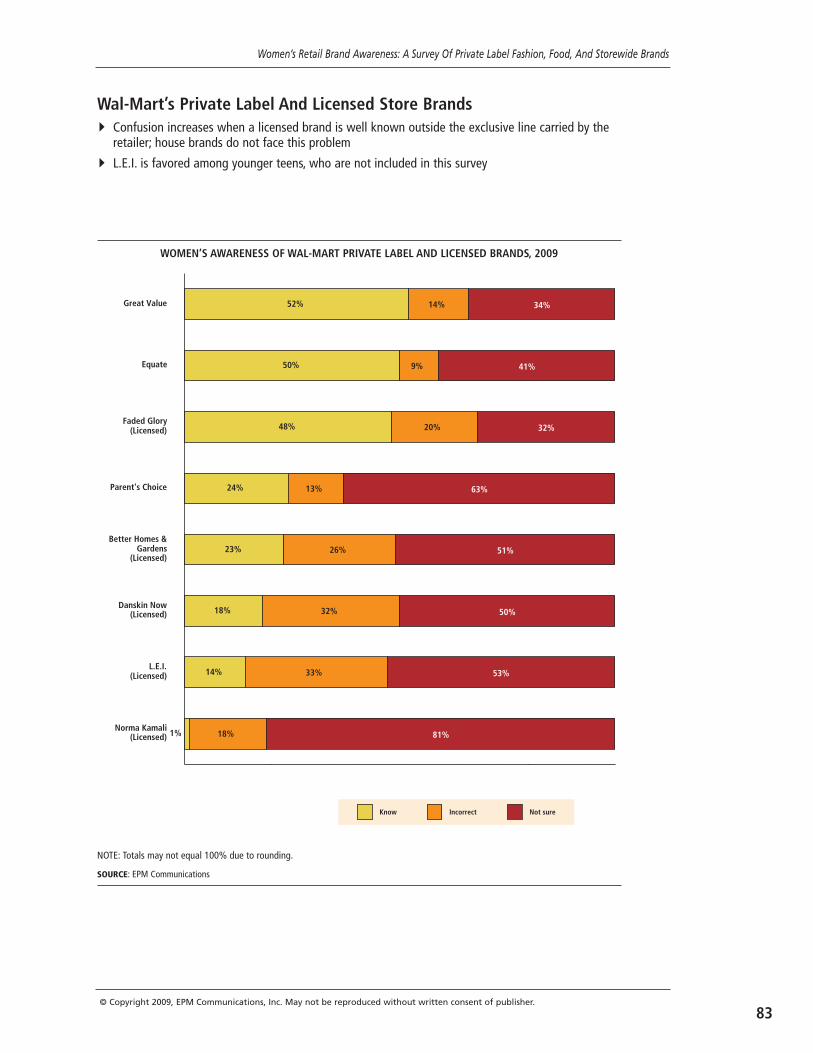

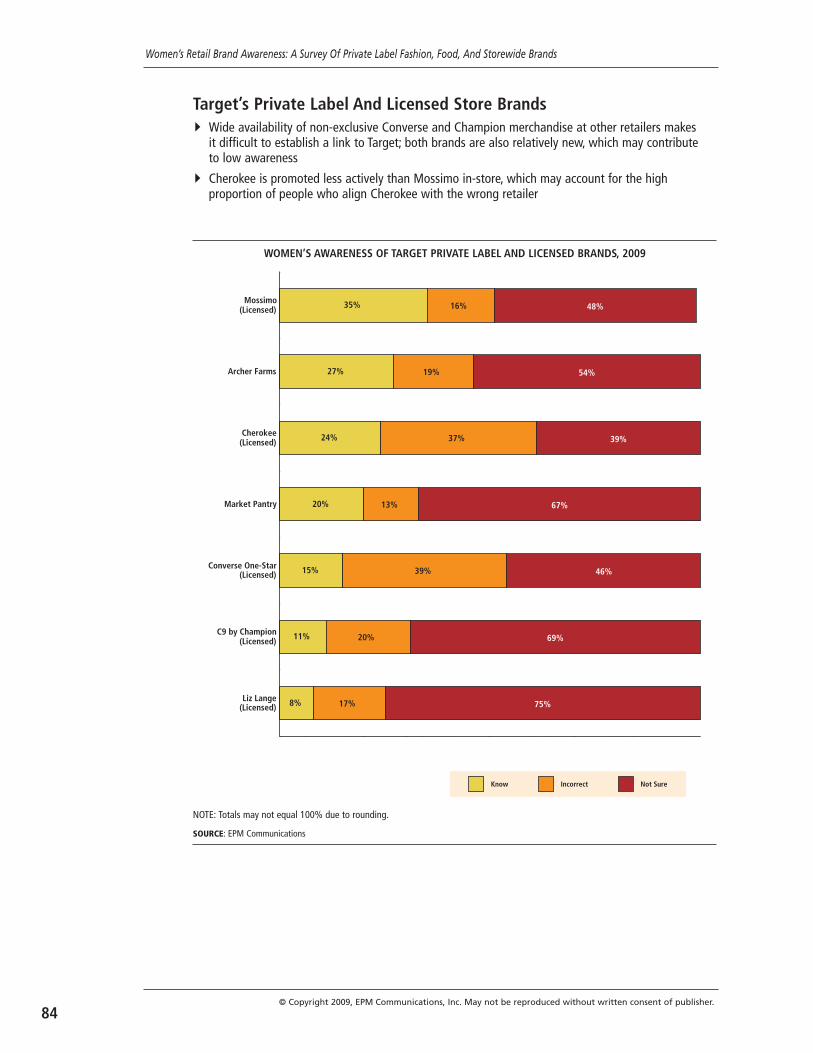

Licensed brands face an additional set ofchallenges to build awareness — only 17% ofwomen correctly identify retailers of thelicensed brands included in this survey.Women are confused about where to findexclusively licensed extensions of nationalbrands (Target’s C9 by Champion and Wal-Mart’s Danskin Now, for example). The chal-

8© Copyright 2009, EPM Communications, Inc. May not be reproduced without written consent of publisher.

lenge is compounded at some retailers. Forexample, Wal-Mart’s price-conscious shopperis more likely to know the store’s privatelabel offerings than its more-expensivelicensed brands. On the other hand, womenwho shop Target, which caters to a trendierclientele, are more likely to know the store’slicensed brands than its store brands.

Survey MethodologyThe Women’s Retail Brand Awareness

research was conducted online by EPM Com-munications. Data was collected October 19-20, 2009 from 305 women aged 18+ whoreside in the U.S. concerning their knowledgeand opinions of 46 private label and licensedbrands and 20 retailers.

Women’s Retail Brand Awareness: A Survey Of Private Label Fashion, Food, And Storewide Brands

© Copyright 2009, EPM Communications, Inc. May not be reproduced without written consent of publisher.

9

PART I:IDENTIFYING BRANDSAND THEIR RETAILERS

Women’s Retail Brand Awareness: A Survey Of Private Label Fashion, Food, And Storewide Brands

© Copyright 2009, EPM Communications, Inc. May not be reproduced without written consent of publisher.

11

APPAREL BRAND AWARENESS

13© Copyright 2009, EPM Communications, Inc. May not be reproduced without written consent of publisher.

Women’s Retail Brand Awareness: A Survey Of Private Label Fashion, Food, And Storewide Brands

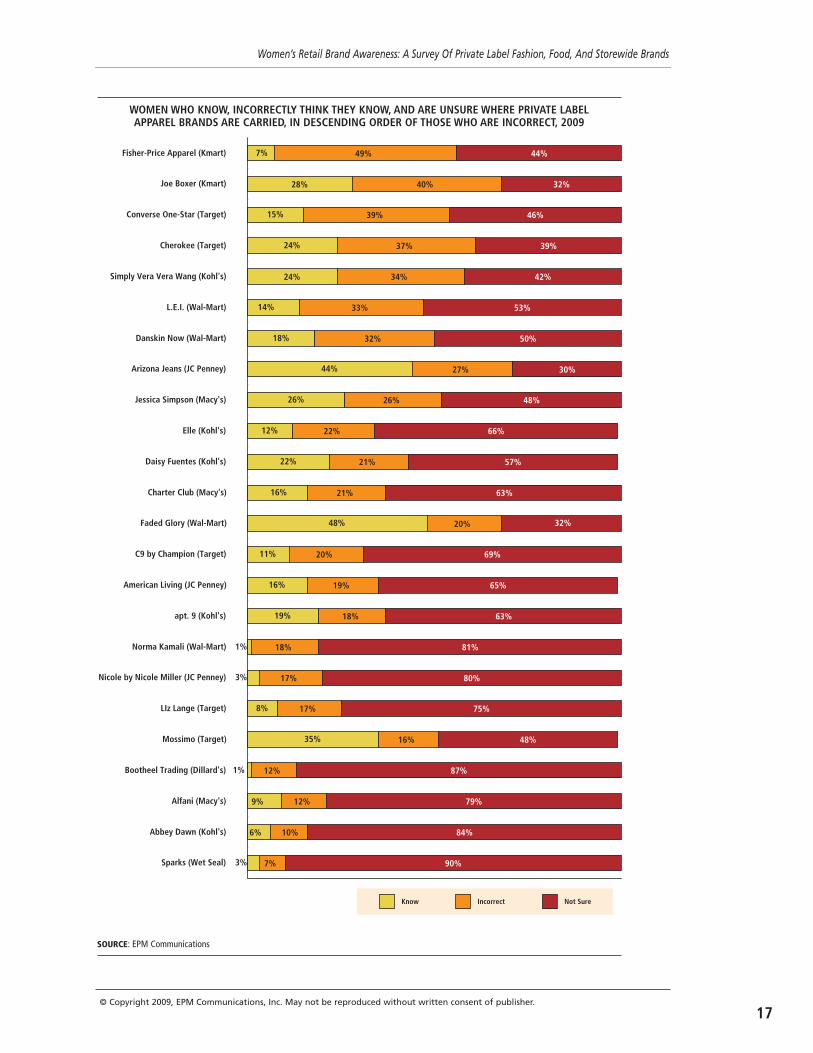

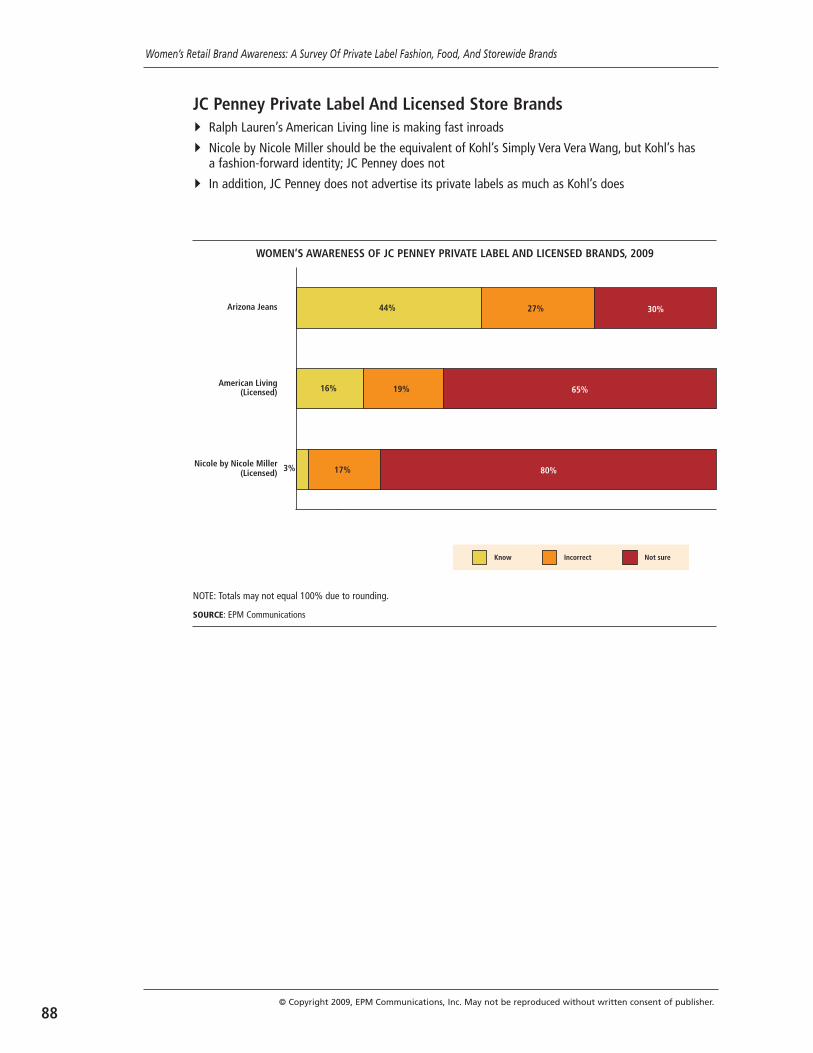

None of the 24 apparel brands surveyedachieve 50% awareness among women shop-pers. Nearly half (48%) correctly identify Fad-ed Glory as a Wal-Mart brand, 44% knowArizona Jeans is available at JC Penney, and35% know Mossimo is carried at Target. Noother brands can boast even 30% awareness.

Among some of the better-known brands(Joe Boxer and Cherokee, for example), anequally large proportion of consumers incor-rectly think they are carried at other retail-ers.

The recent push to offer designer-brandapparel at affordable prices has not necessar-ily benefited retailers. While 24% of womenknow Kohl’s Simply Vera Vera Wang brand,34% of them incorrectly assume it is sold athigher-end retailers Macy’s or Dillard’s. Thesame fate befalls Wal-Mart’s Norma Kamalilabel — only 1% of women know it is exclu-sive to Wal-Mart, compared to 10% whobelieve it is sold at Macy’s or Dillard’s.

The dramatic difference in women’sknowledge of the designer labels Simply VeraVera Wang and Norma Kamali can be attrib-uted to the retailers’ treatments of thebrands. Norma Kamali is less critical to Wal-Mart’s bottom line because it sells numerousmerchandise categories, and gets less pro-motion in-store and in advertising. On theother hand, Simply Vera Vera Wang is a keyline in Kohl’s mix and is widely advertised todraw consumers into the store.

Many women are not aware of Macy’sCharter Club and Alfani brands, both ofwhich have been around for more than adozen years and take up substantial floorspace in the store. It is probable that womendo not make a trip to Macy’s in search ofthese brands but buy them when they finditems that suit their needs.

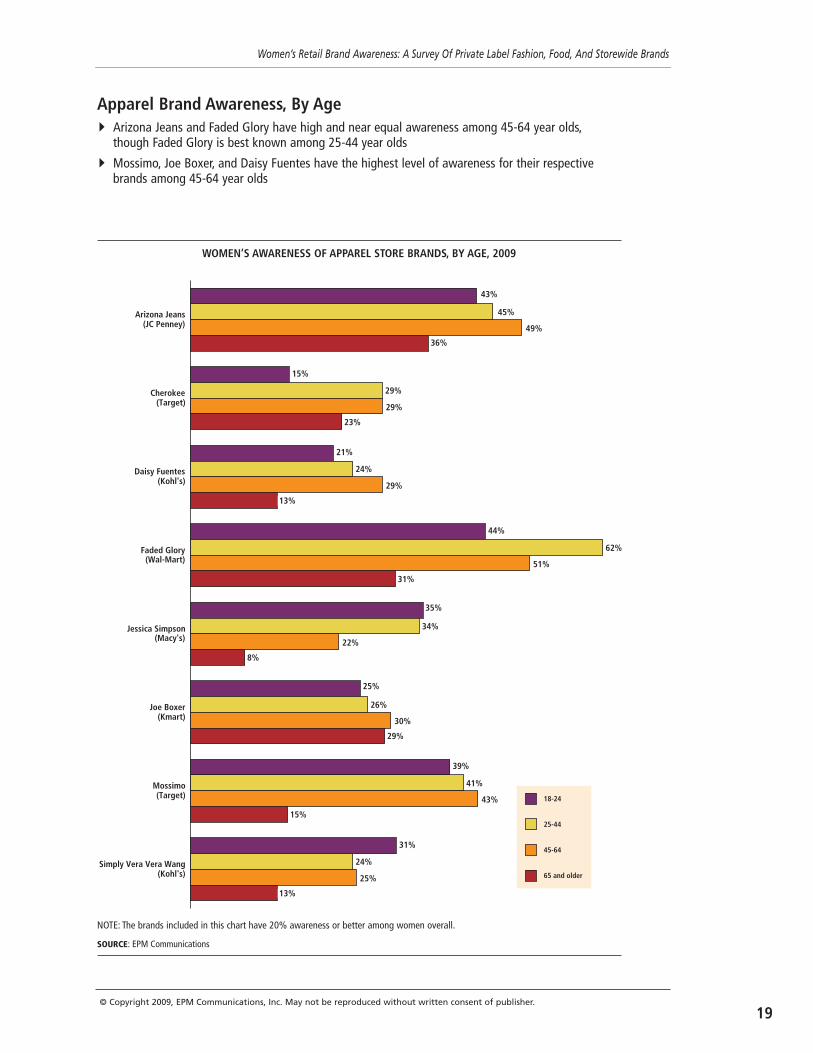

Awareness of celebrity brands amongwomen typically mirrors that celebrity’s pop-ularity among different age groups. For exam-ple, women aged 18-24 (35%) are more likelythan those aged 65 and older (8%) to identifyMacy’s Jessica Simpson brand. Women aged25-44 (24%) and 45-64 (29%) are more likelythan 18-24 year olds (21%) to know Kohl’ssells the Daisy Fuentes brand.

Similarly, young women are more likely toconnect Kohl’s with Simply Vera Vera Wangthan older women who tend to be less con-cerned about designer labels.

Middle-aged women are a key Wal-Martdemographic, so it is no surprise that thestore’s brands are best known among thoseshoppers. However, the retailer can stand toimprove in some areas — while its storebrands are well known, few women are awareof its licensed apparel.

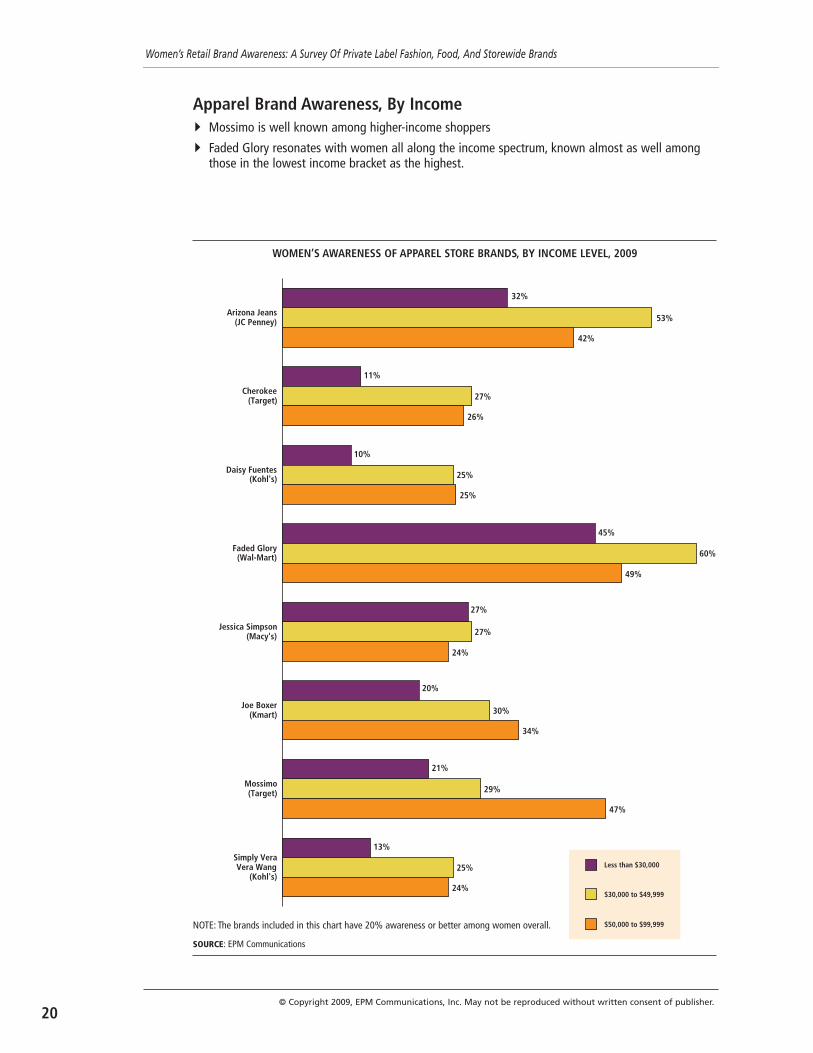

In general, women with annual householdincomes higher than $30,000 are more likelythan those with incomes lower than $30,000to be aware of apparel brands, even thosecarried at lower-end retailers, such as Kmartand Wal-Mart. One exception is the JessicaSimpson brand. The brand has receivedextensive promotion via television, which isthe medium that resonates most stronglywith women with lower incomes (see thechapter on media’s effect on brand aware-ness).

Moms have a significantly higher aware-ness of apparel brands carried at Wal-Martand Target than do women without children.The two stores cater to time-pressed momswho delight in one-stop shopping in whichthey can fill their pantries and their closetswithout having to haul their kids in and outof the car while visiting multiple stores.

Apparel Brand Awareness Overall (see charts pages 16-18)� Faded Glory and Arizona Jeans have superior awareness, and few associate them with the wrong

stores

� Kmart’s Fisher-Price Apparel, which is very new, is associated with the wrong store seven times asoften as with the right one. The omnipresence of the core brand at other stores means Kmart willhave to market the brand heavily before consumers associate it as a store brand exclusive to thechain

� The same may be true for Converse One-Star, Danskin Now, and Simply Vera Vera Wang

� Joe Boxer’s history as a national brand — despite being exclusive at Kmart for more than 7 years— may similarly explain the large number of people who associate it with other retailers

� Target has done an effective job for Mossimo, but Cherokee has not achieved comparable aware-ness; L.E.I.’s position at Wal-Mart may also be vulnerable, though Taylor Swift’s exclusive pres-ence as the spokeswoman for the brand at Wal-Mart and the addition of exclusive dresses to theline, if properly leveraged, will help build up the label

15© Copyright 2009, EPM Communications, Inc. May not be reproduced without written consent of publisher.

Women’s Retail Brand Awareness: A Survey Of Private Label Fashion, Food, And Storewide Brands

© Copyright 2009, EPM Communications, Inc. May not be reproduced without written consent of publisher.

16

Women’s Retail Brand Awareness: A Survey Of Private Label Fashion, Food, And Storewide Brands

Bootheel Trading (Dillard's)

Norma Kamali (Wal-Mart)

Sparks (Wet Seal)

Nicole by Nicole Miller (JC Penney)

Abbey Dawn (Kohl's)

Fisher-Price Apparel (Kmart)

LIz Lange (Target)

Alfani (Macy's)

C9 by Champion (Target)

Elle (Kohl's)

L.E.I. (Wal-Mart)

Converse One-Star (Target)

American Living (JC Penney)

Charter Club (Macy's)

Danskin Now (Wal-Mart)

apt. 9 (Kohl's)

Daisy Fuentes (Kohl's)

Simply Vera Vera Wang (Kohl's)

Cherokee (Target)

Jessica Simpson (Macy's)

Joe Boxer (Kmart)

Mossimo (Target)

Arizona Jeans (JC Penney)

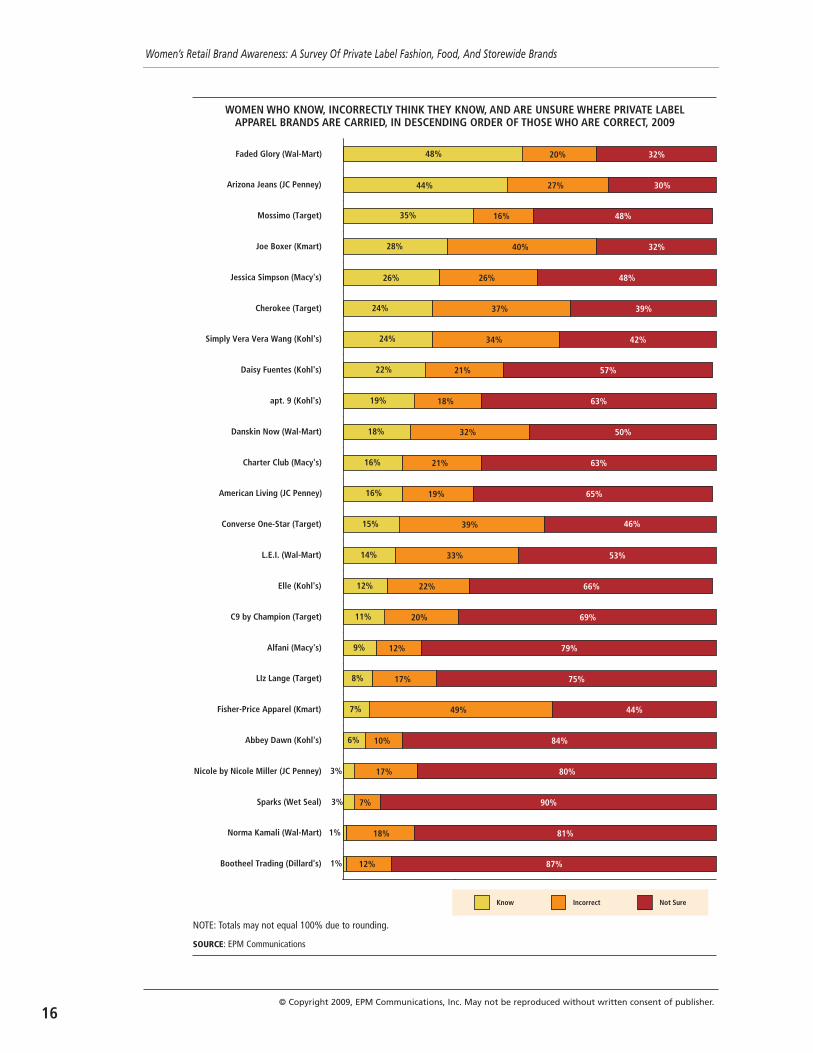

Faded Glory (Wal-Mart) 48% 20% 32%

44% 27% 30%

35% 16% 48%

28% 40% 32%

26% 26% 48%

24% 37% 39%

24% 34% 42%

22% 21% 57%

19% 18% 63%

18% 32% 50%

16% 21% 63%

16% 19% 65%

15% 39% 46%

14% 33% 53%

12% 22% 66%

11% 20% 69%

9% 12% 79%

8% 17% 75%

7% 49% 44%

6% 10% 84%

3% 17% 80%

3% 7% 90%

1% 18% 81%

1% 12% 87%

Know Incorrect Not Sure

WOMEN WHO KNOW, INCORRECTLY THINK THEY KNOW, AND ARE UNSURE WHERE PRIVATE LABELAPPAREL BRANDS ARE CARRIED, IN DESCENDING ORDER OF THOSE WHO ARE CORRECT, 2009

NOTE: Totals may not equal 100% due to rounding.

SOURCE: EPM Communications

Sparks (Wet Seal)

Abbey Dawn (Kohl's)

Alfani (Macy's)

Bootheel Trading (Dillard's)

Mossimo (Target)

LIz Lange (Target)

Nicole by Nicole Miller (JC Penney)

Norma Kamali (Wal-Mart)

apt. 9 (Kohl's)

American Living (JC Penney)

C9 by Champion (Target)

Faded Glory (Wal-Mart)

Charter Club (Macy's)

Daisy Fuentes (Kohl's)

Elle (Kohl's)

Jessica Simpson (Macy's)

Arizona Jeans (JC Penney)

Danskin Now (Wal-Mart)

L.E.I. (Wal-Mart)

Simply Vera Vera Wang (Kohl's)

Cherokee (Target)

Converse One-Star (Target)

Joe Boxer (Kmart)

Fisher-Price Apparel (Kmart) 7% 49% 44%

28% 40% 32%

15% 39% 46%

24% 37% 39%

24% 34% 42%

14% 33% 53%

18% 32% 50%

44% 27% 30%

26% 26% 48%

12% 22% 66%

22% 21% 57%

16% 21% 63%

48% 20% 32%

11% 20% 69%

16% 19% 65%

19% 18% 63%

1% 18% 81%

3% 17% 80%

8% 17% 75%

35% 16% 48%

1% 12% 87%

9% 12% 79%

6% 10% 84%

3% 7% 90%

Know Incorrect Not Sure

SOURCE: EPM Communications

WOMEN WHO KNOW, INCORRECTLY THINK THEY KNOW, AND ARE UNSURE WHERE PRIVATE LABELAPPAREL BRANDS ARE CARRIED, IN DESCENDING ORDER OF THOSE WHO ARE INCORRECT, 2009

17© Copyright 2009, EPM Communications, Inc. May not be reproduced without written consent of publisher.

Women’s Retail Brand Awareness: A Survey Of Private Label Fashion, Food, And Storewide Brands

Women’s Retail Brand Awareness: A Survey Of Private Label Fashion, Food, And Storewide Brands

18© Copyright 2009, EPM Communications, Inc. May not be reproduced without written consent of publisher.

Arizona Jeans (JC Penney)

Faded Glory (Wal-Mart)

Joe Boxer (Kmart)

Cherokee (Target)

Simply Vera Vera Wang (Kohl's)

Fisher-Price Apparel (Kmart)

Converse One-Star (Target)

Mossimo (Target)

Jessica Simpson (Macy's)

Danskin Now (Wal-Mart)

L.E.I. (Wal-Mart)

Daisy Fuentes (Kohl's)

Charter Club (Macy's)

apt. 9 (Kohl's)

American Living (JC Penney)

Elle (Kohl's)

C9 by Champion (Target)

LIz Lange (Target)

Alfani (Macy's)

Nicole by Nicole Miller (JC Penney)

Norma Kamali (Wal-Mart)

Abbey Dawn (Kohl's)

Bootheel Trading (Dillard's)

Sparks (Wet Seal) 3% 7% 90%

1% 12% 87%

6% 10% 84%

1% 18% 81%

3% 17% 80%

9% 12% 79%

8% 17% 75%

11% 20% 69%

12% 22% 66%

16% 19% 65%

19% 18% 63%

16% 21% 63%

22% 21% 57%

14% 33% 53%

18% 32% 50%

26% 26% 48%

35% 16% 48%

15% 39% 46%

7% 49% 44%

24% 34% 42%

24% 37% 39%

28% 40% 32%

48% 20% 32%

44% 27% 30%

Know Incorrect Not Sure

SOURCE: EPM Communications

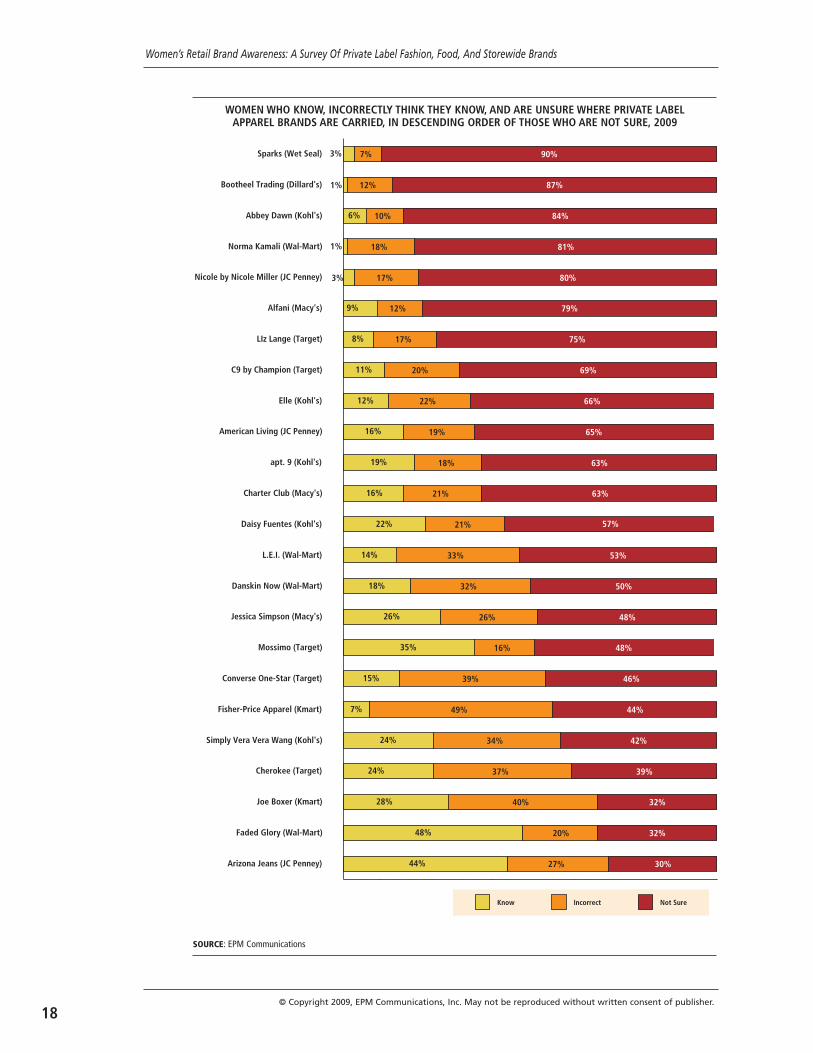

WOMEN WHO KNOW, INCORRECTLY THINK THEY KNOW, AND ARE UNSURE WHERE PRIVATE LABELAPPAREL BRANDS ARE CARRIED, IN DESCENDING ORDER OF THOSE WHO ARE NOT SURE, 2009

Simply Vera Vera Wang(Kohl's)

Mossimo(Target)

Joe Boxer(Kmart)

Jessica Simpson(Macy's)

Faded Glory(Wal-Mart)

Daisy Fuentes(Kohl's)

Cherokee(Target)

Arizona Jeans(JC Penney)

43%

45%

49%

36%

15%

29%

29%

23%

21%

24%

29%

13%

44%

62%

51%

31%

35%

34%

22%

8%

25%

26%

30%

29%

39%

41%

43%

15%

31%

24%

25%

13%

18-24

25-44

45-64

65 and older

Apparel Brand Awareness, By Age� Arizona Jeans and Faded Glory have high and near equal awareness among 45-64 year olds,

though Faded Glory is best known among 25-44 year olds

� Mossimo, Joe Boxer, and Daisy Fuentes have the highest level of awareness for their respectivebrands among 45-64 year olds

WOMEN’S AWARENESS OF APPAREL STORE BRANDS, BY AGE, 2009

NOTE: The brands included in this chart have 20% awareness or better among women overall.

SOURCE: EPM Communications

19© Copyright 2009, EPM Communications, Inc. May not be reproduced without written consent of publisher.

Women’s Retail Brand Awareness: A Survey Of Private Label Fashion, Food, And Storewide Brands

© Copyright 2009, EPM Communications, Inc. May not be reproduced without written consent of publisher.

20

Apparel Brand Awareness, By Income� Mossimo is well known among higher-income shoppers

� Faded Glory resonates with women all along the income spectrum, known almost as well amongthose in the lowest income bracket as the highest.

Women’s Retail Brand Awareness: A Survey Of Private Label Fashion, Food, And Storewide Brands

Simply VeraVera Wang

(Kohl's)

Mossimo(Target)

Joe Boxer(Kmart)

Jessica Simpson(Macy's)

Faded Glory(Wal-Mart)

Daisy Fuentes(Kohl's)

Cherokee(Target)

Arizona Jeans(JC Penney)

32%

53%

42%

11%

27%

26%

10%

25%

25%

45%

60%

49%

27%

27%

24%

20%

30%

34%

21%

29%

47%

13%

25%

24%

Less than $30,000

$30,000 to $49,999

$50,000 to $99,999

WOMEN’S AWARENESS OF APPAREL STORE BRANDS, BY INCOME LEVEL, 2009

NOTE: The brands included in this chart have 20% awareness or better among women overall.

SOURCE: EPM Communications

Women’s Retail Brand Awareness: A Survey Of Private Label Fashion, Food, And Storewide Brands

© Copyright 2009, EPM Communications, Inc. May not be reproduced without written consent of publisher.

21

Simply Vera Vera Wang(Kohl's)

Mossimo(Target)

Joe Boxer(Kmart)

Jessica Simpson(Macy's)

Faded Glory(Wal-Mart)

Daisy Fuentes(Kohl's)

Cherokee(Target)

Arizona Jeans(JC Penney)

42%

47%

20%

29%

20%

26%

43%

51%

33%

27%

28%

28%

38%

37%

28%

26%

Single

Married

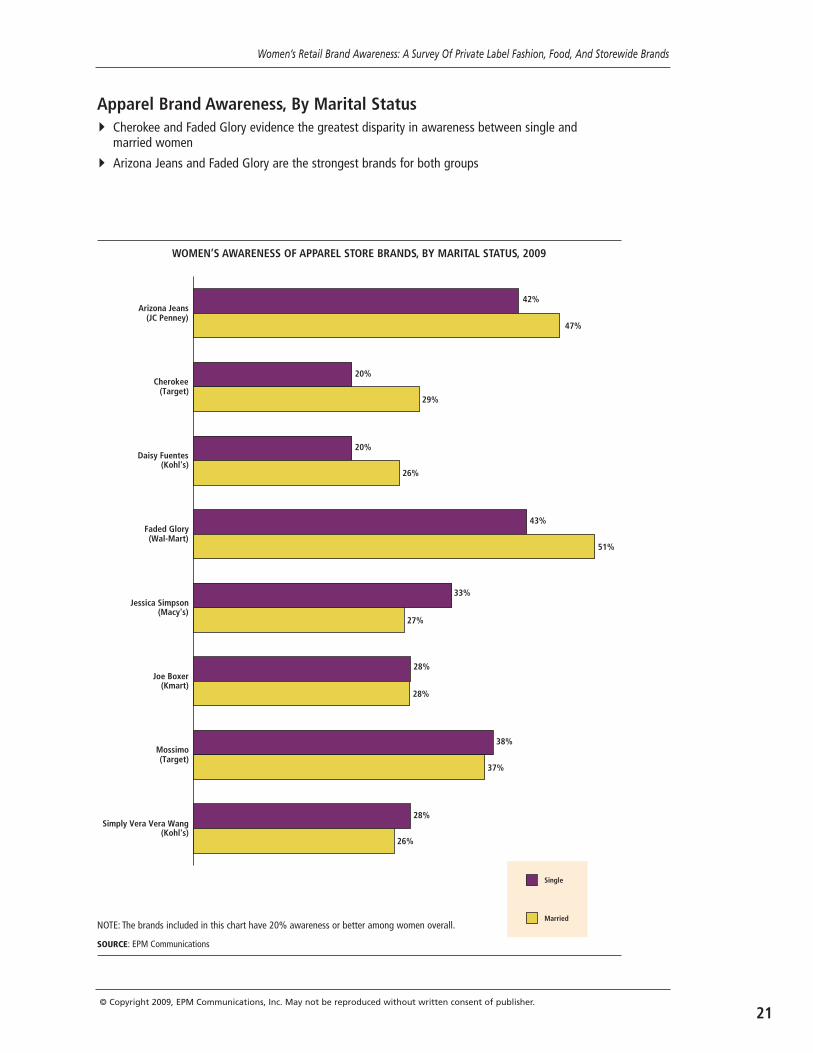

Apparel Brand Awareness, By Marital Status� Cherokee and Faded Glory evidence the greatest disparity in awareness between single and

married women

� Arizona Jeans and Faded Glory are the strongest brands for both groups

NOTE: The brands included in this chart have 20% awareness or better among women overall.

SOURCE: EPM Communications

WOMEN’S AWARENESS OF APPAREL STORE BRANDS, BY MARITAL STATUS, 2009

Simply Vera Vera Wang(Kohl's)

Mossimo(Target)

Joe Boxer(Kmart)

Jessica Simpson(Macy's)

Faded Glory(Wal-Mart)

Daisy Fuentes(Kohl's)

Cherokee(Target)

Arizona Jeans(JC Penney)

45%

43%

29%

21%

22%

23%

60%

41%

27%

25%

27%

28%

44%

30%

24%

24%Children in household

No children in household

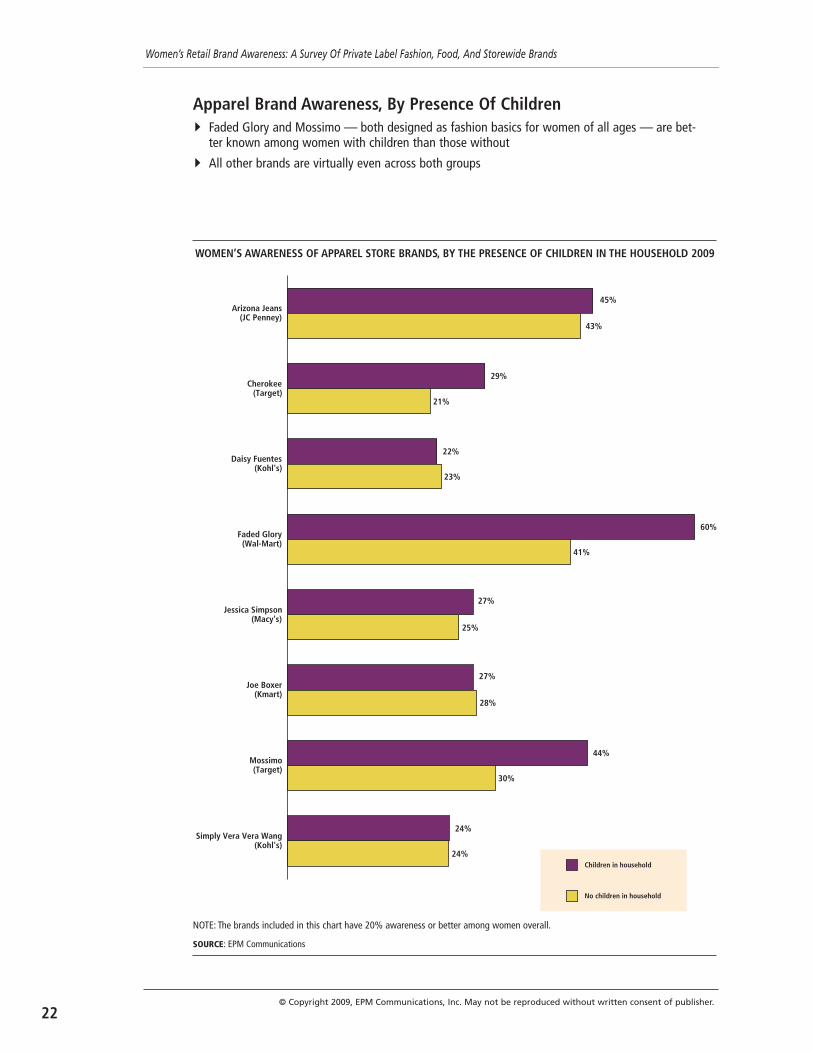

Apparel Brand Awareness, By Presence Of Children� Faded Glory and Mossimo — both designed as fashion basics for women of all ages — are bet-

ter known among women with children than those without

� All other brands are virtually even across both groups

NOTE: The brands included in this chart have 20% awareness or better among women overall.

SOURCE: EPM Communications

WOMEN’S AWARENESS OF APPAREL STORE BRANDS, BY THE PRESENCE OF CHILDREN IN THE HOUSEHOLD 2009

© Copyright 2009, EPM Communications, Inc. May not be reproduced without written consent of publisher.

22

Women’s Retail Brand Awareness: A Survey Of Private Label Fashion, Food, And Storewide Brands

Women’s Retail Brand Awareness: A Survey Of Private Label Fashion, Food, And Storewide Brands

© Copyright 2009, EPM Communications, Inc. May not be reproduced without written consent of publisher.

23

FOOD BRAND AWARENESS

In recent years, price-sensitive groceryshoppers have decided that private labelbrands are as tasty and possess the samequality as national brands. But do they knowthe private label brands they are buying? Thelow levels of awareness for such food brandssuggests they may not.

The low awareness levels for many foodbrands in this survey can be attributed tothe fact that several of the retailers — Safe-way, Stop ‘N’ Shop, Kroger, A&P, and PigglyWiggly — are regional chains, so few respon-dents may have those chains (or brands)available to them. However, even somenational chain private labels have low aware-ness, such as Whole Foods’ 365 (7%). Evenhere the awareness level is mitigated by thefact that Whole Foods has relatively fewstores, and that those who shop WholeFoods likely shop it less frequently thanthose who shop traditional grocery stores ona weekly or more basis.

It is perhaps no surprise that retail giantWal-Mart decisively wins the battle forwomen’s awareness of food brands. Wal-Martcarries the only two brands that at least halfof women identify with the store that sellsthem: Great Value (52%) and Equate (50%).The mass merchandiser draws price sensi-tive shoppers who are willing to try privatelabel brands to save money, and whichwould lead to greater awareness of thosebrands.

The Name GameWomens’ preconceived notions about

stores contribute to their errors in identify-ing which retailers carry which privatelabels.

Their impression of Whole Foods as asupermarket specializing in natural and

organic foods leads them to believe that theretailer carries Safeway’s O Organics brandand Stop ‘N’ Shop’s Nature’s Promise label. Infact, they are more likely to believe thatWhole Foods carries O Organics than theyare to correctly identify Whole Foods’ ownorganic private label, called 365. Likewise,their notion of Wal-Mart as a value-drivenretailer leads them to believe it carries PigglyWiggly’s Value Time label.

Women are also confused by licensedbrands Disney Magic and Looney Tunes.They are more likely to believe the brandsare carried at retail powerhouses Wal-Martand Target than at the regional chains thatactually carry the brands, Kroger and Safe-way. Both labels are relatively new, whichmay also be a contributing factor in their lowawareness levels.

Married, middle-aged women are morelikely than single young women to correctlyidentify which food brands are sold where.This is dictated by their lifestyles: married,middle-aged women are more likely to pre-pare meals at home for their families, where-as young single women are more likely to eatout and are, therefore, less likely to groceryshop.

Although it may seem counter-intuitivebecause women with lower incomes aremore likely to buy money-saving private labelbrands, the greater a woman’s annual house-hold income, the more likely she is to knowfood brands. Women with lower incomesfocus on price, not the name of the brandthey are buying. Women with higher incomeshave the leeway to compare brands as wellas prices.

Value Time (Piggly Wiggly)

Looney Tunes (Safeway)

Master Choice (A&P)

Disney Magic (Kroger)

Nature's Promise (Stop 'N' Shop)

365 (Whole Foods)

O Organics (Safeway)

Rancher's Reserve (Safeway)

Market Pantry (Target)

Kirkland Signature (Costco)

Archer Farms (Target)

Equate (Wal-Mart)

Great Value (Wal-Mart) 52% 14% 34%

50% 9% 41%

27% 19% 54%

27% 15% 58%

20% 13% 67%

10% 12% 78%

8% 29% 63%

7% 6% 87%

5% 26% 69%

3% 28% 69%

3% 16% 81%

1% 35% 64%

1% 23% 76%

Know Incorrect Not Sure

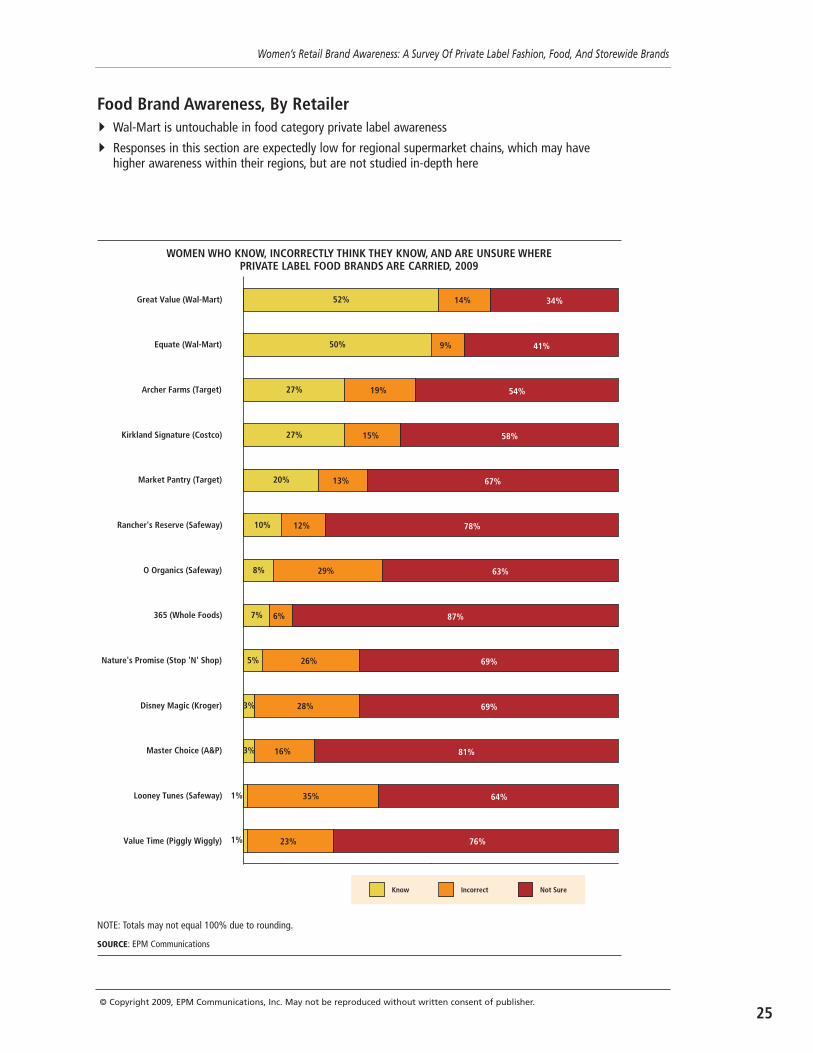

Food Brand Awareness, By Retailer� Wal-Mart is untouchable in food category private label awareness

� Responses in this section are expectedly low for regional supermarket chains, which may havehigher awareness within their regions, but are not studied in-depth here

WOMEN WHO KNOW, INCORRECTLY THINK THEY KNOW, AND ARE UNSURE WHEREPRIVATE LABEL FOOD BRANDS ARE CARRIED, 2009

NOTE: Totals may not equal 100% due to rounding.

SOURCE: EPM Communications

25© Copyright 2009, EPM Communications, Inc. May not be reproduced without written consent of publisher.

Women’s Retail Brand Awareness: A Survey Of Private Label Fashion, Food, And Storewide Brands

Market Pantry(Target)

Kirkland(Costco)

Great Value(Wal-Mart)

Equate(Wal-Mart)

Archer Farms(Target)

17%

25%

30%

45%

60%

60%

48%

53%

61%

17%

23%

33%

13%

16%

25%

Less than $30,000

$30,000 to $49,999

$50,000 to $99,999

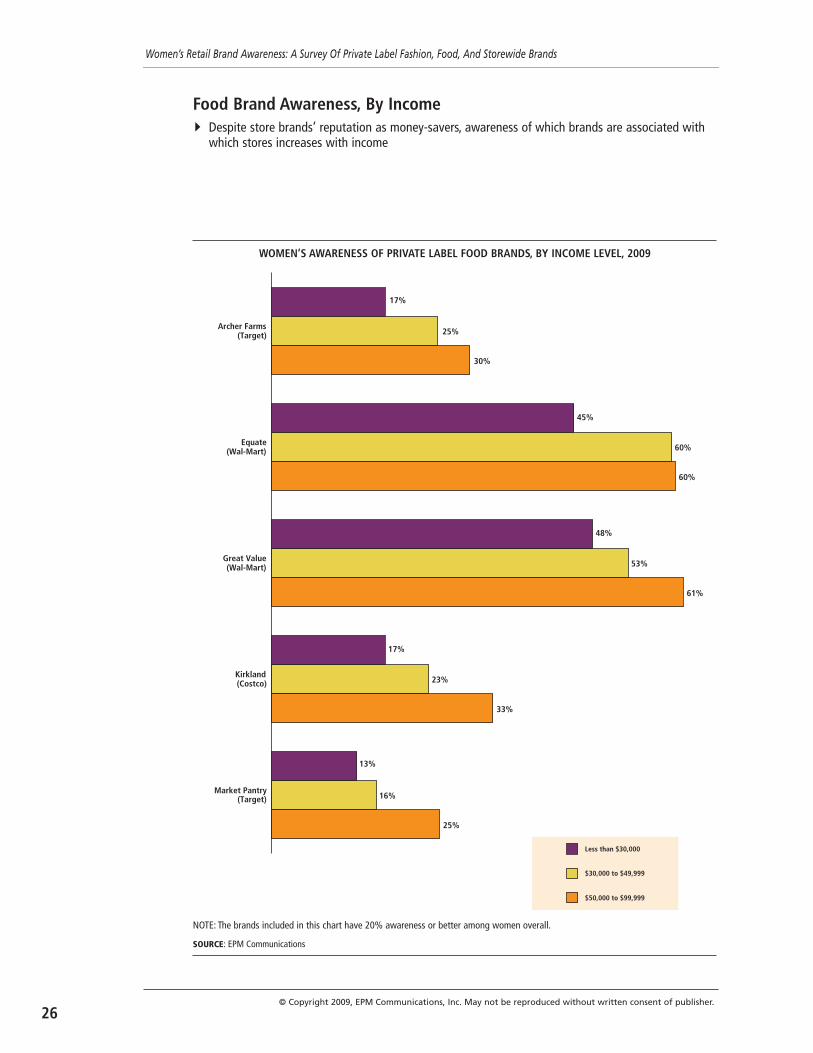

Food Brand Awareness, By Income� Despite store brands’ reputation as money-savers, awareness of which brands are associated with

which stores increases with income

NOTE: The brands included in this chart have 20% awareness or better among women overall.

SOURCE: EPM Communications

WOMEN’S AWARENESS OF PRIVATE LABEL FOOD BRANDS, BY INCOME LEVEL, 2009

© Copyright 2009, EPM Communications, Inc. May not be reproduced without written consent of publisher.

26

Women’s Retail Brand Awareness: A Survey Of Private Label Fashion, Food, And Storewide Brands

Market Pantry(Target)

Kirkland(Costco)

Great Value(Wal-Mart)

Equate(Wal-Mart)

Archer Farms(Target)

25%

28%

52%

49%

54%

51%

27%

26%

28%

15%

Children in household

No children in household

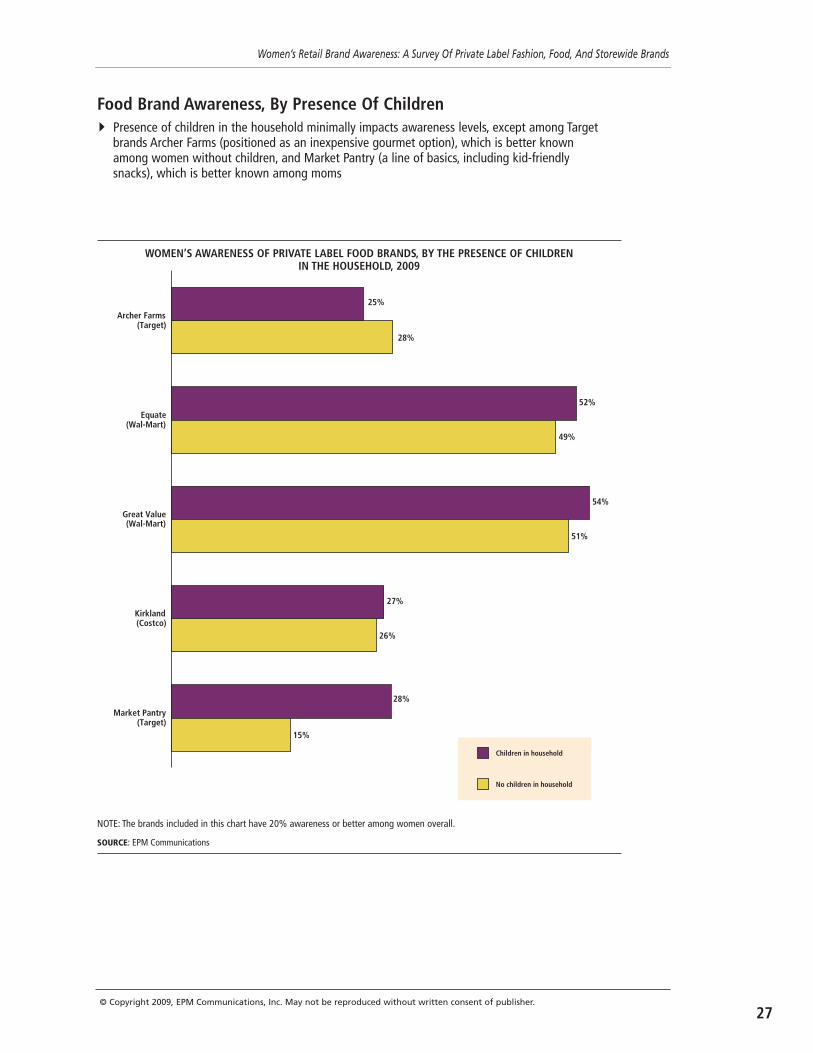

Food Brand Awareness, By Presence Of Children� Presence of children in the household minimally impacts awareness levels, except among Target

brands Archer Farms (positioned as an inexpensive gourmet option), which is better knownamong women without children, and Market Pantry (a line of basics, including kid-friendlysnacks), which is better known among moms

NOTE: The brands included in this chart have 20% awareness or better among women overall.

SOURCE: EPM Communications

WOMEN’S AWARENESS OF PRIVATE LABEL FOOD BRANDS, BY THE PRESENCE OF CHILDRENIN THE HOUSEHOLD, 2009

27© Copyright 2009, EPM Communications, Inc. May not be reproduced without written consent of publisher.

Women’s Retail Brand Awareness: A Survey Of Private Label Fashion, Food, And Storewide Brands

Market Pantry(Target)

Kirkland(Costco)

Great Value(Wal-Mart)

Equate(Wal-Mart)

Archer Farms(Target)

24%

29%

38%

15%

40%

52%

58%

50%

55%

47%

61%

44%

15%

28%

38%

26%

15%

29%

23%

10%

18-24

25-44

45-64

65 or older

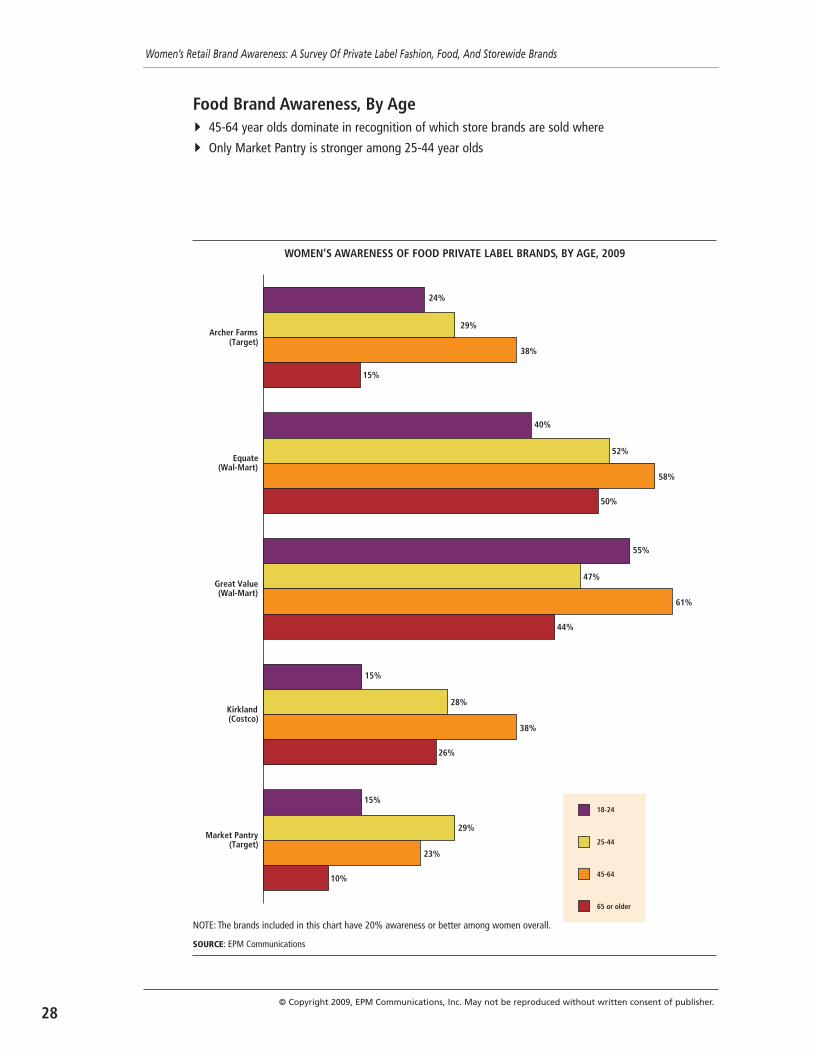

Food Brand Awareness, By Age� 45-64 year olds dominate in recognition of which store brands are sold where

� Only Market Pantry is stronger among 25-44 year olds

NOTE: The brands included in this chart have 20% awareness or better among women overall.

SOURCE: EPM Communications

WOMEN’S AWARENESS OF FOOD PRIVATE LABEL BRANDS, BY AGE, 2009

© Copyright 2009, EPM Communications, Inc. May not be reproduced without written consent of publisher.

28

Women’s Retail Brand Awareness: A Survey Of Private Label Fashion, Food, And Storewide Brands

Market Pantry(Target)

Kirkland(Costco)

Great Value(Wal-Mart)

Equate(Wal-Mart)

Archer Farms(Target)

28%

30%

42%

55%

49%

53%

20%

32%

13%

25%

Single

Married

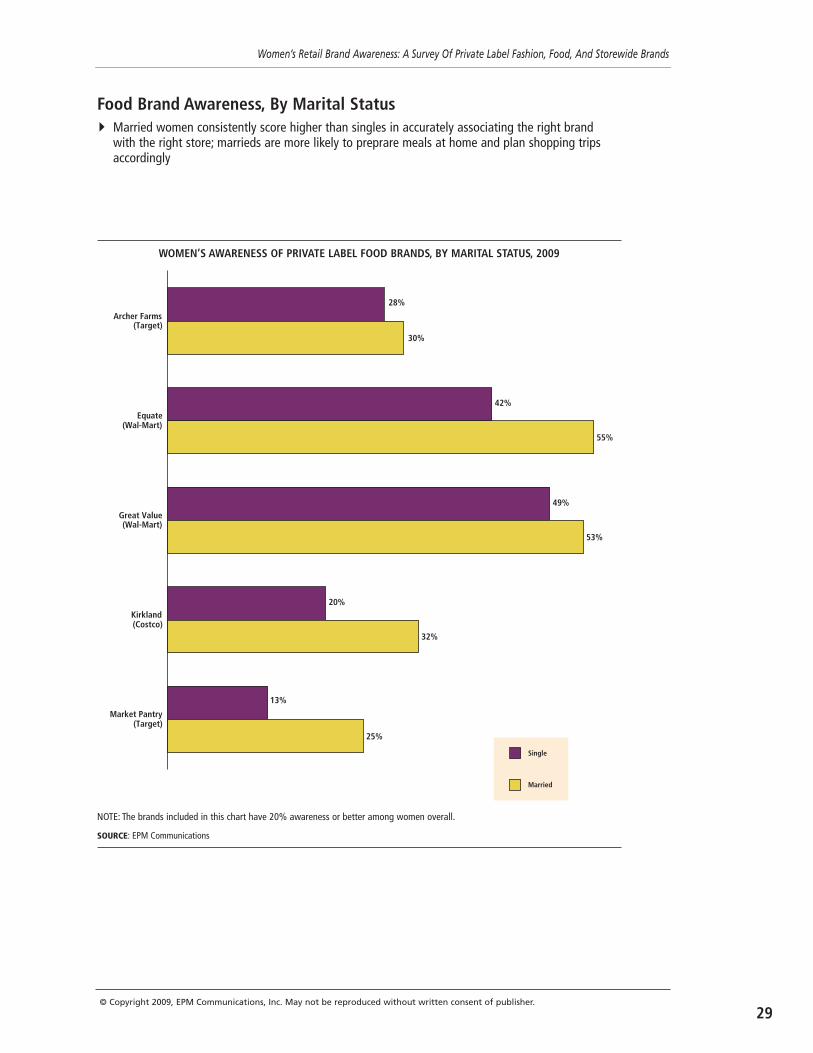

Food Brand Awareness, By Marital Status� Married women consistently score higher than singles in accurately associating the right brand

with the right store; marrieds are more likely to preprare meals at home and plan shopping tripsaccordingly

NOTE: The brands included in this chart have 20% awareness or better among women overall.

SOURCE: EPM Communications

WOMEN’S AWARENESS OF PRIVATE LABEL FOOD BRANDS, BY MARITAL STATUS, 2009

29© Copyright 2009, EPM Communications, Inc. May not be reproduced without written consent of publisher.

Women’s Retail Brand Awareness: A Survey Of Private Label Fashion, Food, And Storewide Brands

STOREWIDE BRAND AWARENESS

Women are nearly twice as likely to cor-rectly identify storewide brands (31%) asthey are to know either food or apparelbrands (17% each). However, most of thestorewide brands included in this surveyhave been in existence for more than a dozenyears, and longevity positively affects brandawareness.

The Kenmore and Craftsman brands origi-nated by Sears and now also sold at corpo-rate sister Kmart are the two oldest brandssurveyed, and have the highest awareness ofany brand in any category (78% each). Rela-tively few women incorrectly guess thebrands are carried at other retailers. Searsand Kmart promote the brands heavily in-store, via circulars, and on their websites, allof which improves awareness, according tothe survey, though there is indication thebrands don’t resonate as strongly amongyounger women — an issue the retailers willneed to address to sustain the brands goingforward.

But longevity isn’t everything. Best Buy’sInsignia brand has been in existence for 13years, with its prominence beefed up in thelast 2-3 years. But it has the lowest level ofawareness of store brands among women. Itis not heavily promoted in store circulars orvia Best Buy’s website — name brand elec-tronics are more likely to appear in thestore’s “featured brands” section of its site.

Women are able to correctly identify Wal-Mart as the retailer carrying the year-old Bet-ter Homes & Gardens brand. Its highrecognition is likely tied to its well-knownmagazine namesake.

Women aged 18-24 are less likely than old-er women to be able to identify storewidebrands. Most storewide brands are house-hold items — appliances, furniture, andhome décor — and women in this age group

generally (and single women in particular)are not likely to be setting up their ownhomes yet.

Women with children are (not surprising-ly) more likely to be aware of Wal-Mart’s Par-ent’s Choice brand, but also its Better Homes& Gardens and Kohl’s Sonoma labels. Womenin this life stage are more likely than averageto move into a larger home as their familiesexpand and have a greater need for house-wares and new décor.

Women without children are more likelythan moms to know that the Jaclyn Smithbrand is exclusive to Kmart and Sears. Thisis likely also a function of age, with the typi-cal Jaclyn Smith shopper being BabyBoomers, who are increasingly empty-nesters.

As with other categories, women withhigher household incomes are more likelythan those with annual incomes of less than$30,000 to correctly identify storewidebrands with the retailers that sell them. How-ever, low-income women are more likely thanthose in other income brackets to recognizethat Wal-Mart is home to Parent’s Choice andBetter Homes & Gardens, proving once againthat the mass merchandiser is successful inreaching low-income consumers.

31© Copyright 2009, EPM Communications, Inc. May not be reproduced without written consent of publisher.

Women’s Retail Brand Awareness: A Survey Of Private Label Fashion, Food, And Storewide Brands

Insignia (Best Buy)

Realistic (Radio Shack)

Berkley & Jensen (BJ's)

Sonoma (Kohl's)

Better Homes & Gardens (Wal-Mart)

Member's Mark (Sam's Club)

Parent's Choice (Wal-Mart)

Jaclyn Smith (Sears/Kmart)

Craftsman (Sears/Kmart)

Kenmore (Sears/Kmart) 78% 9% 13%

78% 8% 14%

47% 18% 34%

24% 13% 63%

24% 10% 66%

23% 26% 51%

22% 22% 56%

10% 7% 83%

6% 6% 88%

5% 11% 84%

Know Incorrect Not Sure

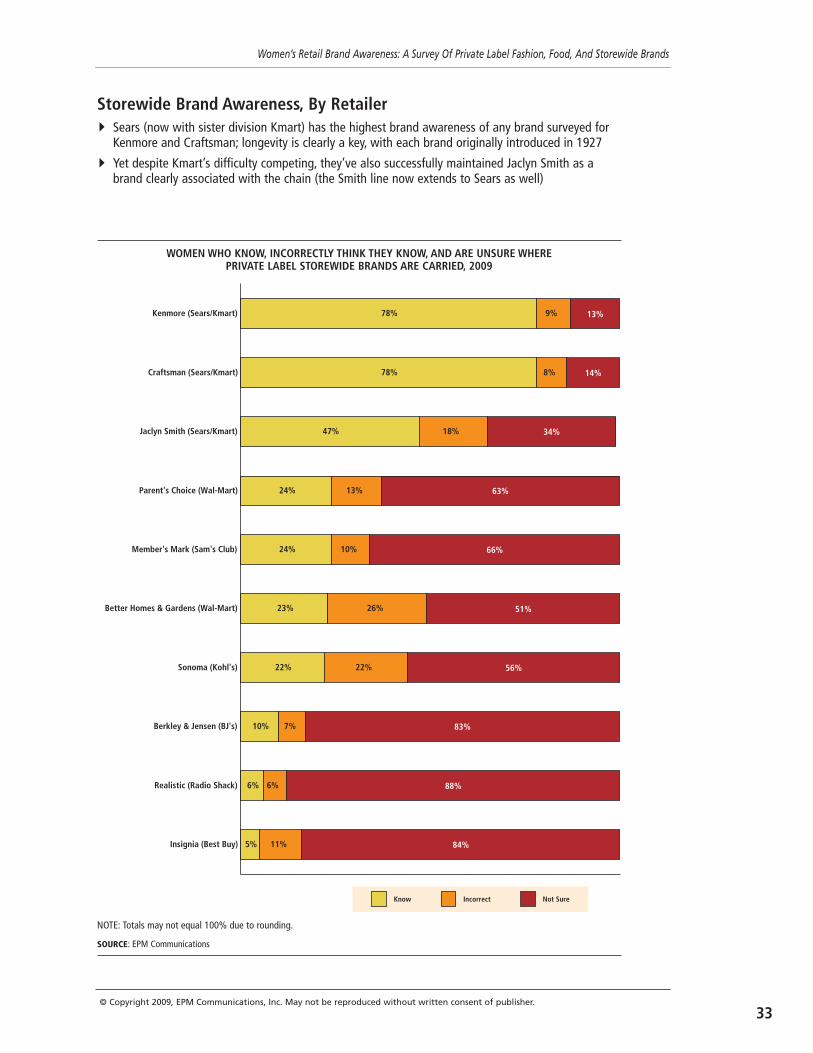

Storewide Brand Awareness, By Retailer� Sears (now with sister division Kmart) has the highest brand awareness of any brand surveyed for

Kenmore and Craftsman; longevity is clearly a key, with each brand originally introduced in 1927

� Yet despite Kmart’s difficulty competing, they’ve also successfully maintained Jaclyn Smith as abrand clearly associated with the chain (the Smith line now extends to Sears as well)

NOTE: Totals may not equal 100% due to rounding.

SOURCE: EPM Communications

WOMEN WHO KNOW, INCORRECTLY THINK THEY KNOW, AND ARE UNSURE WHEREPRIVATE LABEL STOREWIDE BRANDS ARE CARRIED, 2009

33© Copyright 2009, EPM Communications, Inc. May not be reproduced without written consent of publisher.

Women’s Retail Brand Awareness: A Survey Of Private Label Fashion, Food, And Storewide Brands

Sonoma(Kohl's)

Parent's Choice(Wal-Mart)

Member's Mark(Sam's Club)

Kenmore(Sears/Kmart)

Jaclyn Smith(Sears/Kmart)

Craftsman(Sears/Kmart)

Better Homes &Gardens (Wal-Mart)

25%

24%

26%

15%

51%

79%

92%

90%

13%

48%

74%

53%

56%

74%

90%

98%

21%

21%

34%

21%

36%

36%

17%

2%

11%

34%

30%

10%

18-24

25-44

45-64

65 and older

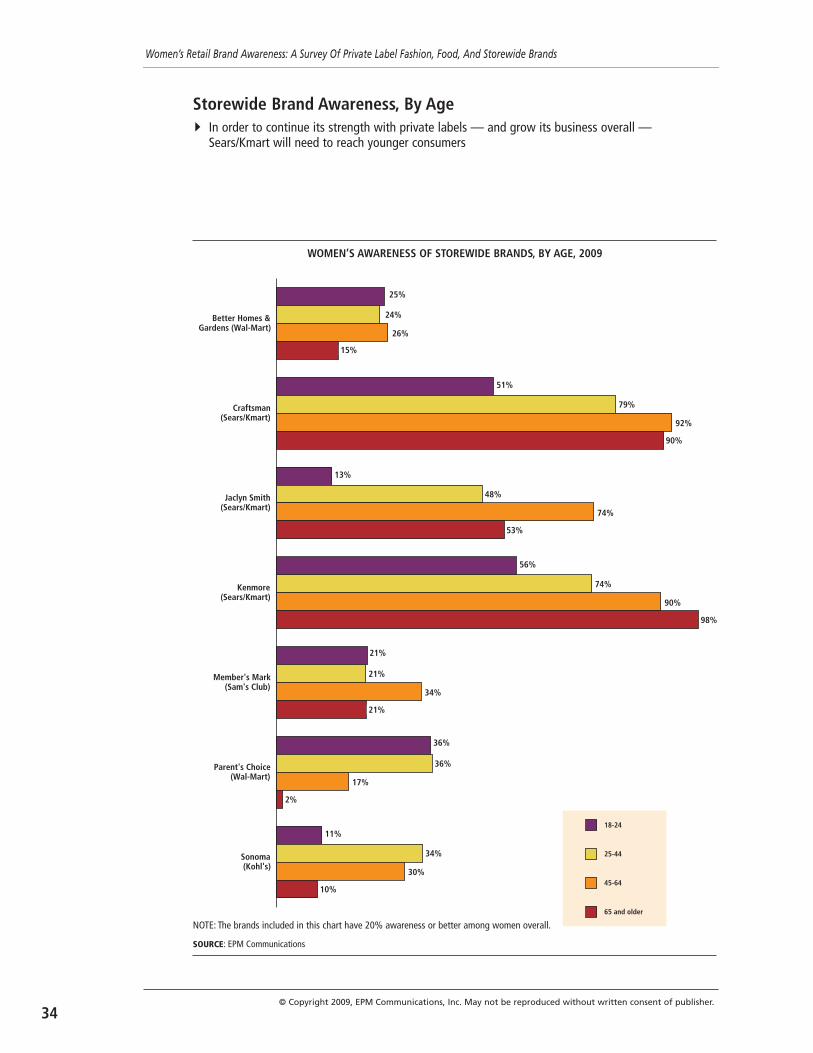

Storewide Brand Awareness, By Age� In order to continue its strength with private labels — and grow its business overall —

Sears/Kmart will need to reach younger consumers

NOTE: The brands included in this chart have 20% awareness or better among women overall.

SOURCE: EPM Communications

WOMEN’S AWARENESS OF STOREWIDE BRANDS, BY AGE, 2009

© Copyright 2009, EPM Communications, Inc. May not be reproduced without written consent of publisher.

34

Women’s Retail Brand Awareness: A Survey Of Private Label Fashion, Food, And Storewide Brands

Sonoma(Kohl's)

Parent's Choice(Wal-Mart)

Member's Mark(Sam's Club)

Kenmore(Sears/Kmart)

Jaclyn Smith(Sears/Kmart)

Craftsman(Sears/Kmart)

Better Homes &Gardens (Wal-Mart)

27%

20%

74%

81%

46%

48%

72%

82%

23%

25%

42%

14%

29%

18%Children in household

No children in household

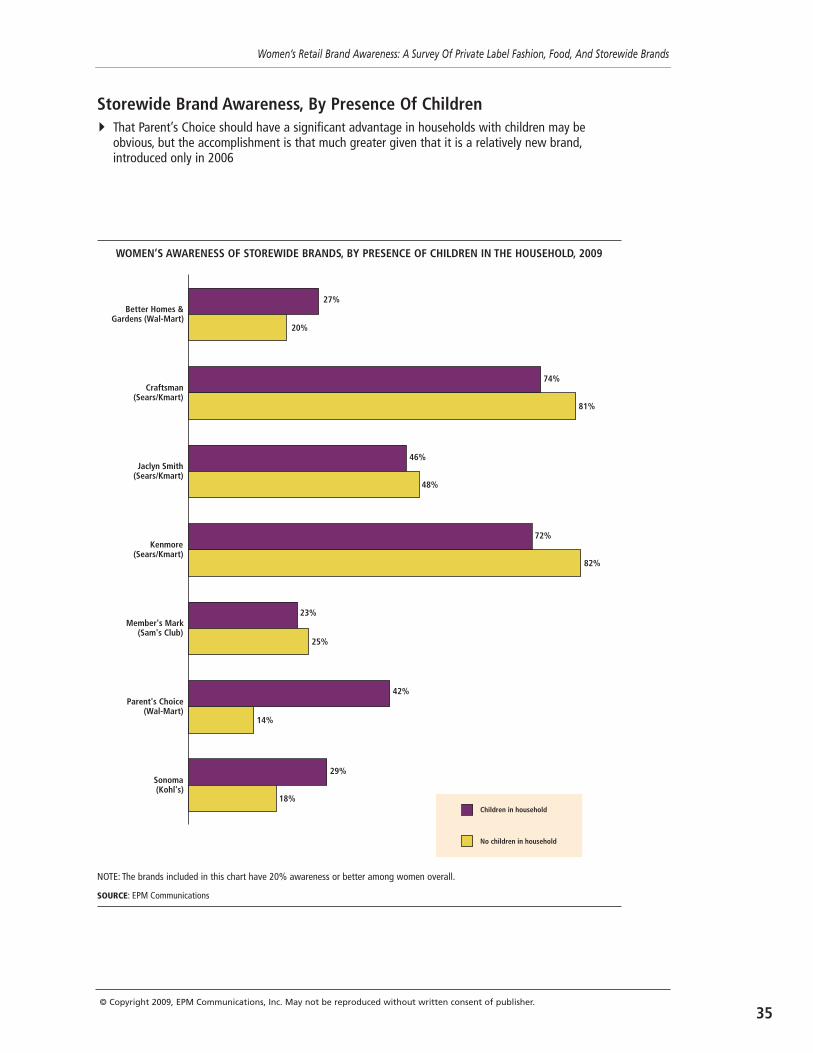

Storewide Brand Awareness, By Presence Of Children� That Parent’s Choice should have a significant advantage in households with children may be

obvious, but the accomplishment is that much greater given that it is a relatively new brand,introduced only in 2006

NOTE: The brands included in this chart have 20% awareness or better among women overall.

SOURCE: EPM Communications

WOMEN’S AWARENESS OF STOREWIDE BRANDS, BY PRESENCE OF CHILDREN IN THE HOUSEHOLD, 2009

35© Copyright 2009, EPM Communications, Inc. May not be reproduced without written consent of publisher.

Women’s Retail Brand Awareness: A Survey Of Private Label Fashion, Food, And Storewide Brands

Sonoma(Kohl's)

Parent's Choice(Wal-Mart)

Member's Mark(Sam's Club)

Kenmore(Sears/Kmart)

Jaclyn Smith(Sears/Kmart)

Craftsman(Sears/Kmart)

Better Homes &Gardens (Wal-Mart)

20%

26%

23%

56%

83%

86%

38%

58%

49%

62%

86%

82%

16%

30%

24%

28%

27%

25%

10%

27%

27%

Less than $30,000

$30,000 to $49,999

$50,000 to $99,999

NOTE: The brands included in this chart have 20% awareness or better among women overall.

SOURCE: EPM Communications

WOMEN’S AWARENESS OF STOREWIDE BRANDS, BY INCOME LEVEL, 2009

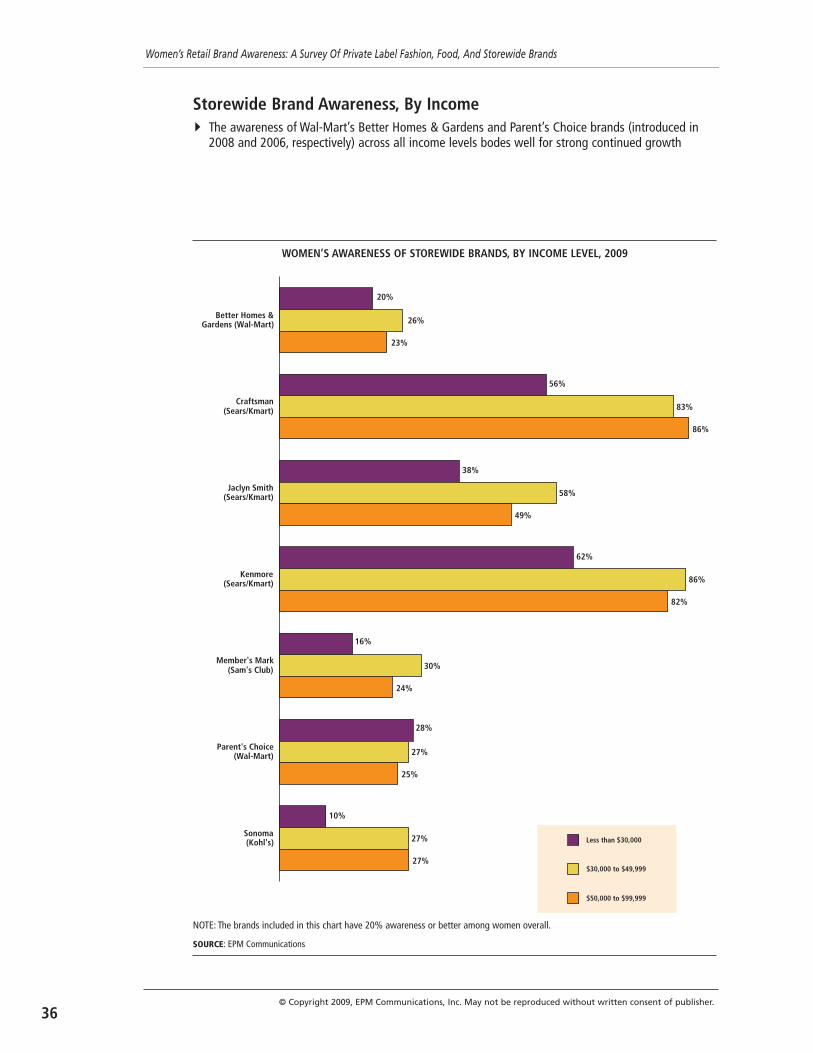

Storewide Brand Awareness, By Income� The awareness of Wal-Mart’s Better Homes & Gardens and Parent’s Choice brands (introduced in

2008 and 2006, respectively) across all income levels bodes well for strong continued growth

© Copyright 2009, EPM Communications, Inc. May not be reproduced without written consent of publisher.

36

Women’s Retail Brand Awareness: A Survey Of Private Label Fashion, Food, And Storewide Brands

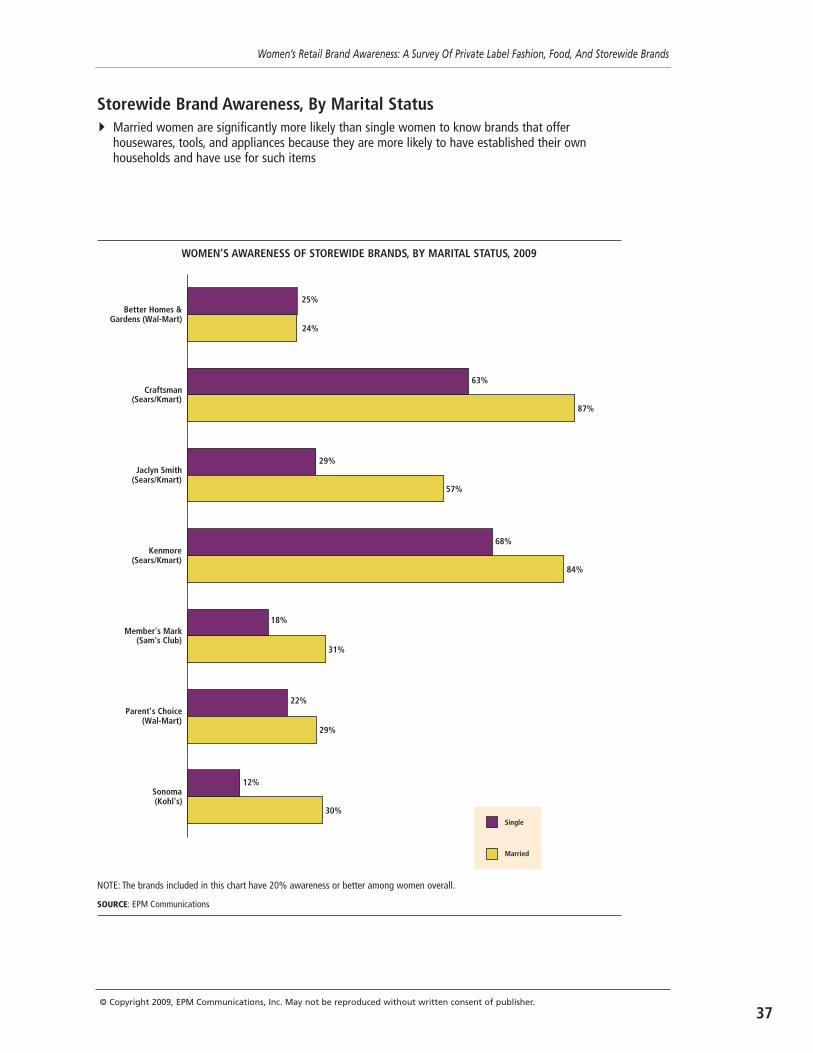

Storewide Brand Awareness, By Marital Status� Married women are significantly more likely than single women to know brands that offer

housewares, tools, and appliances because they are more likely to have established their ownhouseholds and have use for such items

Sonoma(Kohl's)

Parent's Choice(Wal-Mart)

Member's Mark(Sam's Club)

Kenmore(Sears/Kmart)

Jaclyn Smith(Sears/Kmart)

Craftsman(Sears/Kmart)

Better Homes &Gardens (Wal-Mart)

25%

24%

63%

87%

29%

57%

68%

84%

18%

31%

22%

29%

12%

30%Single

Married

NOTE: The brands included in this chart have 20% awareness or better among women overall.

SOURCE: EPM Communications

WOMEN’S AWARENESS OF STOREWIDE BRANDS, BY MARITAL STATUS, 2009

37© Copyright 2009, EPM Communications, Inc. May not be reproduced without written consent of publisher.

Women’s Retail Brand Awareness: A Survey Of Private Label Fashion, Food, And Storewide Brands

PART II:EXTERNAL FACTORSAFFECTING BRANDAWARENESS

39© Copyright 2009, EPM Communications, Inc. May not be reproduced without written consent of publisher.

Women’s Retail Brand Awareness: A Survey Of Private Label Fashion, Food, And Storewide Brands

The frequency with which women shop aretailer also significantly affects their aware-ness of that retailer’s brands. Virtually acrossthe board, the more often a woman shops aretailer, the more likely she is able to recallthat retailer’s brands. Food brands in partic-ular benefit from this trend, as women shopfor food more often than they do apparel,housewares, electronics, and other cate-gories.

In general, awareness of a brand drops bymore than a third among those who shopevery two to three months compared tothose who shop every month. It drops by60% comparing those who shop every sixmonths or less frequently to those who shopmonthly or more often.

Kohl’s, Sears, and Kmart are best at main-taining brand awareness among infrequentshoppers. For Sears and Kmart, this can beattributed to the longevity of their brands,which, as previously stated, positively influ-ences awareness. Kohl’s strong brand aware-ness among infrequent shoppers can beattributed to an extensive marketing effortfocusing on both store circulars and maga-zines.

Some exceptions to the rule that more fre-quent shoppers are more likely to knowbrands are Macy’s Jessica Simpson line andSears and Kmart’s Kenmore brand. Womenare as likely to know the Simpson brandwhether they shop Macy’s every month orevery six months. This is likely the result ofan extensive advertising campaign by Macy’sto support the brand. Kenmore is less knownamong those who shop Sears monthly, butthose shoppers are probably not looking tobuy appliances with such frequency.

Those who shop Wal-Mart every sixmonths or less frequently are more likelythan those who shop every two to three

months to know the retailer’s Better Homes& Gardens and Danskin Now lines. This is anadvantage that licensed brands have overhouse-developed brands — shoppers alreadyknow their names, which builds awarenessamong infrequent shoppers.

FREQUENCY

41© Copyright 2009, EPM Communications, Inc. May not be reproduced without written consent of publisher.

Women’s Retail Brand Awareness: A Survey Of Private Label Fashion, Food, And Storewide Brands

Norma Kamali

L.E.I.

Danskin Now

Better Homes& Gardens

Parent's Choice

Faded Glory

Equate

Great Value

64%

34%

17%

60%

49%

13%

60%

38%

17%

31%

15%

0%

28%

11%

17%

23%

6%

8%

18%

6%

4%

1%

0%

0%

At least monthly

Every 2 to 3 months

Every 6 months or so

SOURCE: EPM Communications

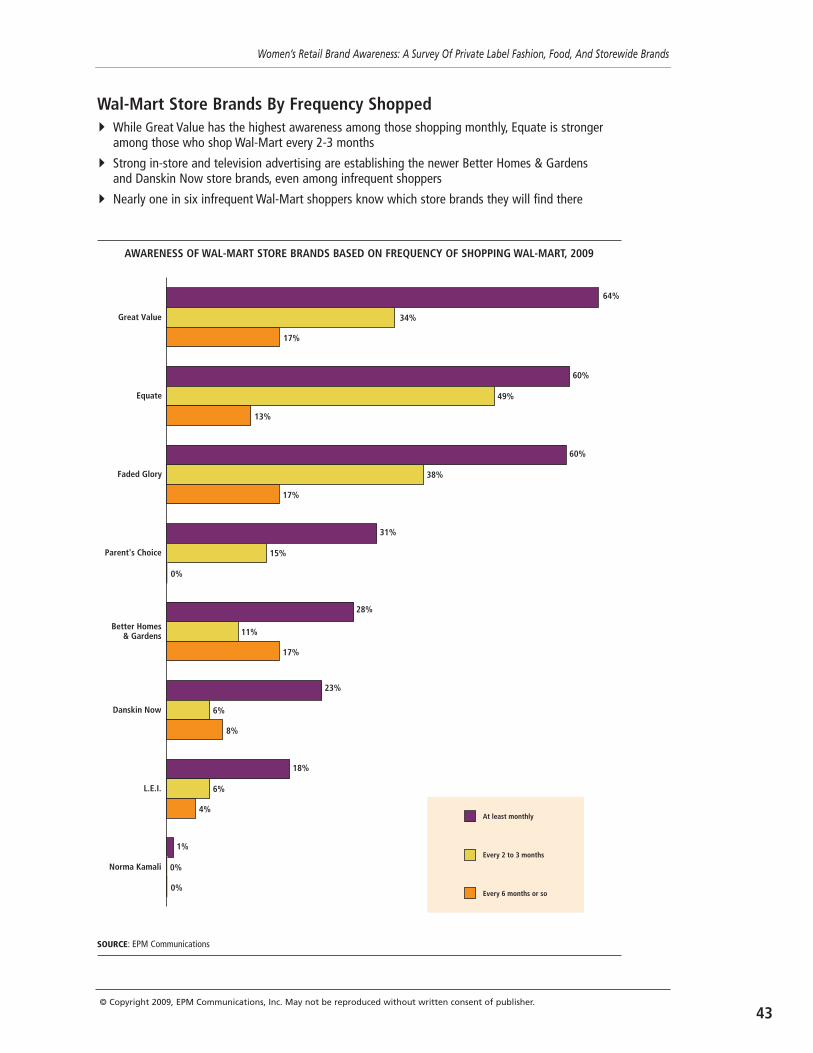

AWARENESS OF WAL-MART STORE BRANDS BASED ON FREQUENCY OF SHOPPING WAL-MART, 2009

Wal-Mart Store Brands By Frequency Shopped� While Great Value has the highest awareness among those shopping monthly, Equate is stronger

among those who shop Wal-Mart every 2-3 months

� Strong in-store and television advertising are establishing the newer Better Homes & Gardensand Danskin Now store brands, even among infrequent shoppers

� Nearly one in six infrequent Wal-Mart shoppers know which store brands they will find there

43© Copyright 2009, EPM Communications, Inc. May not be reproduced without written consent of publisher.

Women’s Retail Brand Awareness: A Survey Of Private Label Fashion, Food, And Storewide Brands

Liz Lange

C9 by Champion

Converse One-Star

Cherokee

Market Pantry

Archer Farms

Mossimo

55%

35%

21%

46%

29%

9%

41%

11%

6%

40%

21%

12%

28%

6%

6%

22%

8%

2%

16%

5%

2%

At least monthly

Every 2 to 3 months

Every 6 months or so

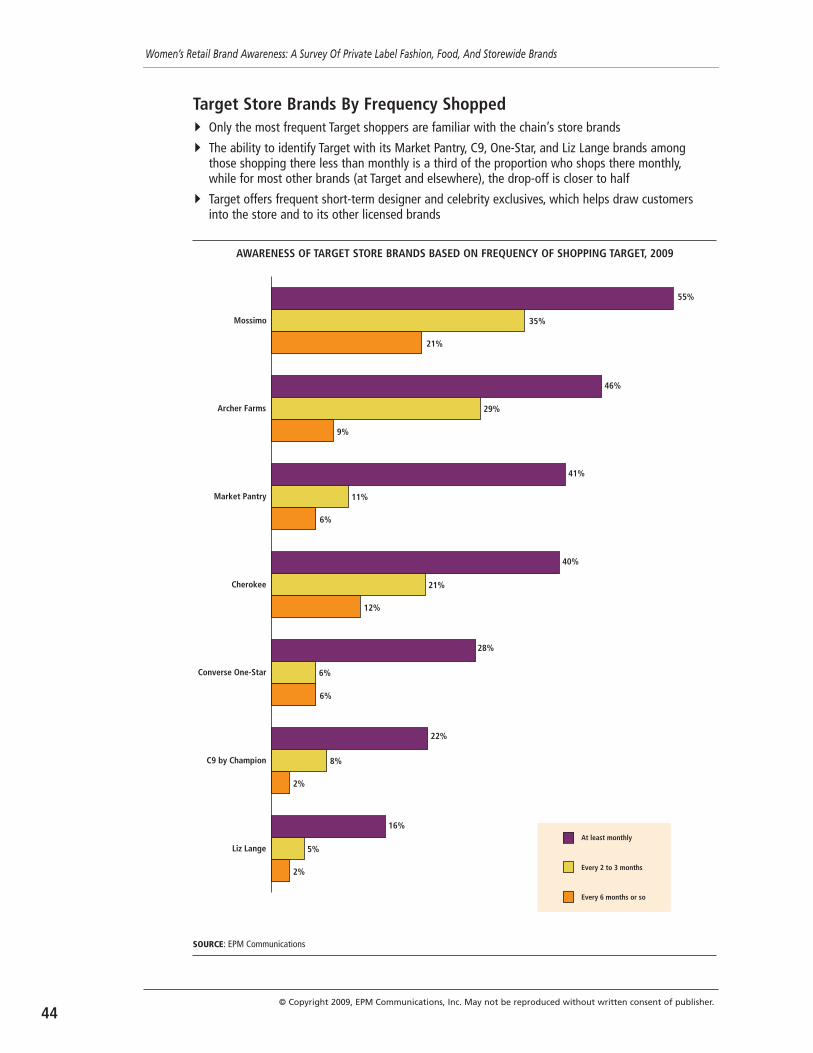

Target Store Brands By Frequency Shopped� Only the most frequent Target shoppers are familiar with the chain’s store brands

� The ability to identify Target with its Market Pantry, C9, One-Star, and Liz Lange brands amongthose shopping there less than monthly is a third of the proportion who shops there monthly,while for most other brands (at Target and elsewhere), the drop-off is closer to half

� Target offers frequent short-term designer and celebrity exclusives, which helps draw customersinto the store and to its other licensed brands

SOURCE: EPM Communications

AWARENESS OF TARGET STORE BRANDS BASED ON FREQUENCY OF SHOPPING TARGET, 2009

© Copyright 2009, EPM Communications, Inc. May not be reproduced without written consent of publisher.

44

Women’s Retail Brand Awareness: A Survey Of Private Label Fashion, Food, And Storewide Brands

Abbey Dawn

Elle

apt. 9

Daisy Fuentes

Sonoma

Simply VeraVera Wang

50%

32%

23%

47%

29%

23%

47%

27%

22%

45%

26%

13%

23%

15%

12%

12%

7%

7%

At least monthly

Every 2 to 3 months

Every 6 months or so

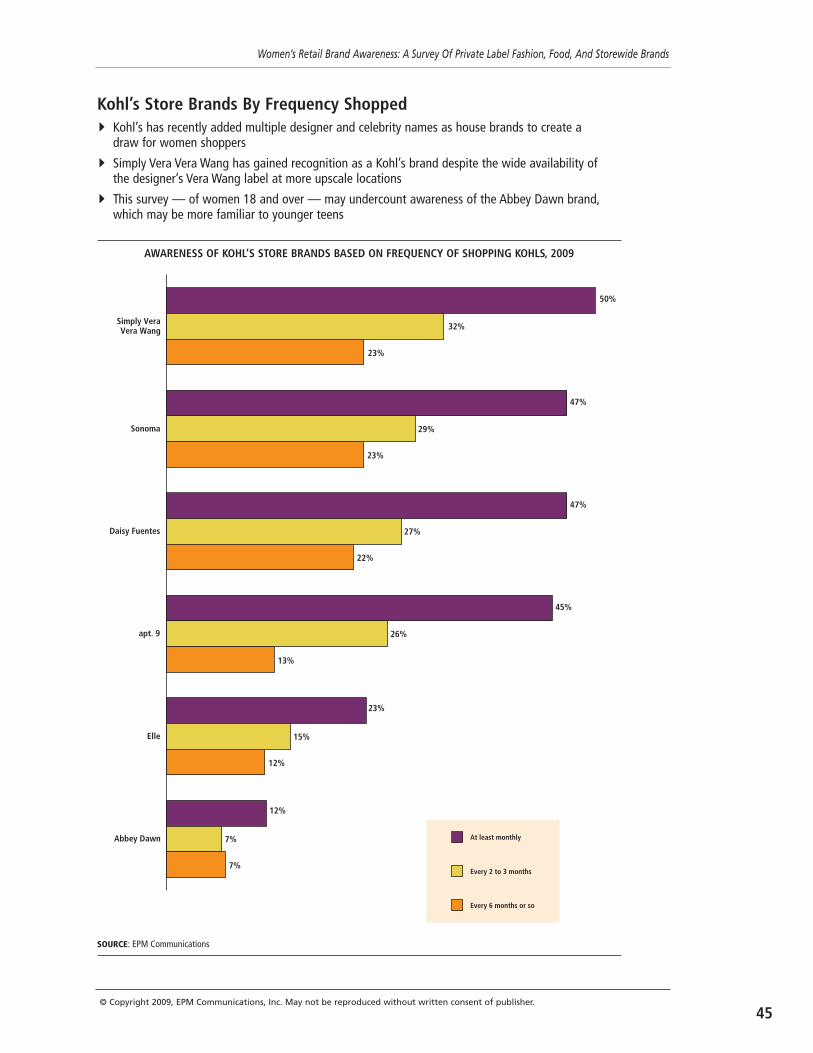

Kohl’s Store Brands By Frequency Shopped� Kohl’s has recently added multiple designer and celebrity names as house brands to create a

draw for women shoppers

� Simply Vera Vera Wang has gained recognition as a Kohl’s brand despite the wide availability ofthe designer’s Vera Wang label at more upscale locations

� This survey — of women 18 and over — may undercount awareness of the Abbey Dawn brand,which may be more familiar to younger teens

SOURCE: EPM Communications

AWARENESS OF KOHL’S STORE BRANDS BASED ON FREQUENCY OF SHOPPING KOHLS, 2009

45© Copyright 2009, EPM Communications, Inc. May not be reproduced without written consent of publisher.

Women’s Retail Brand Awareness: A Survey Of Private Label Fashion, Food, And Storewide Brands

Kenmore

Craftsman

82%

77%

82%

71%

89%

82%

At least monthly

Every 2 to 3 months

Every 6 months or so

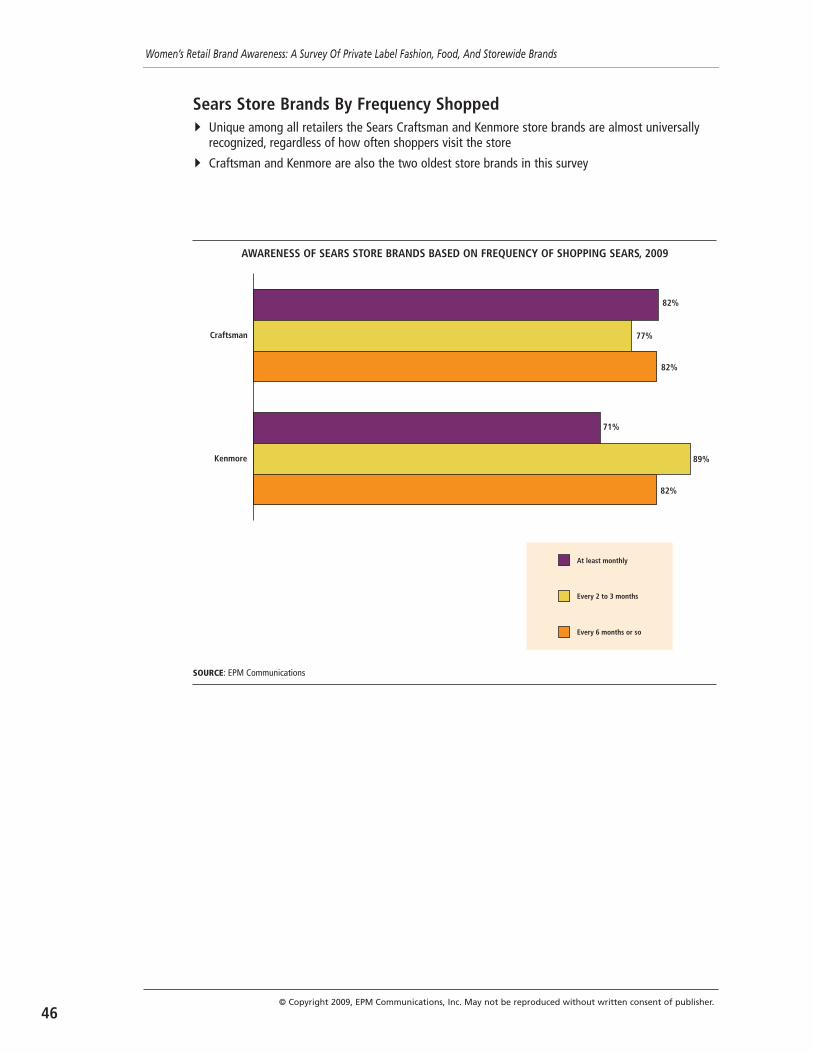

Sears Store Brands By Frequency Shopped� Unique among all retailers the Sears Craftsman and Kenmore store brands are almost universally

recognized, regardless of how often shoppers visit the store

� Craftsman and Kenmore are also the two oldest store brands in this survey

SOURCE: EPM Communications

AWARENESS OF SEARS STORE BRANDS BASED ON FREQUENCY OF SHOPPING SEARS, 2009

© Copyright 2009, EPM Communications, Inc. May not be reproduced without written consent of publisher.

46

Women’s Retail Brand Awareness: A Survey Of Private Label Fashion, Food, And Storewide Brands

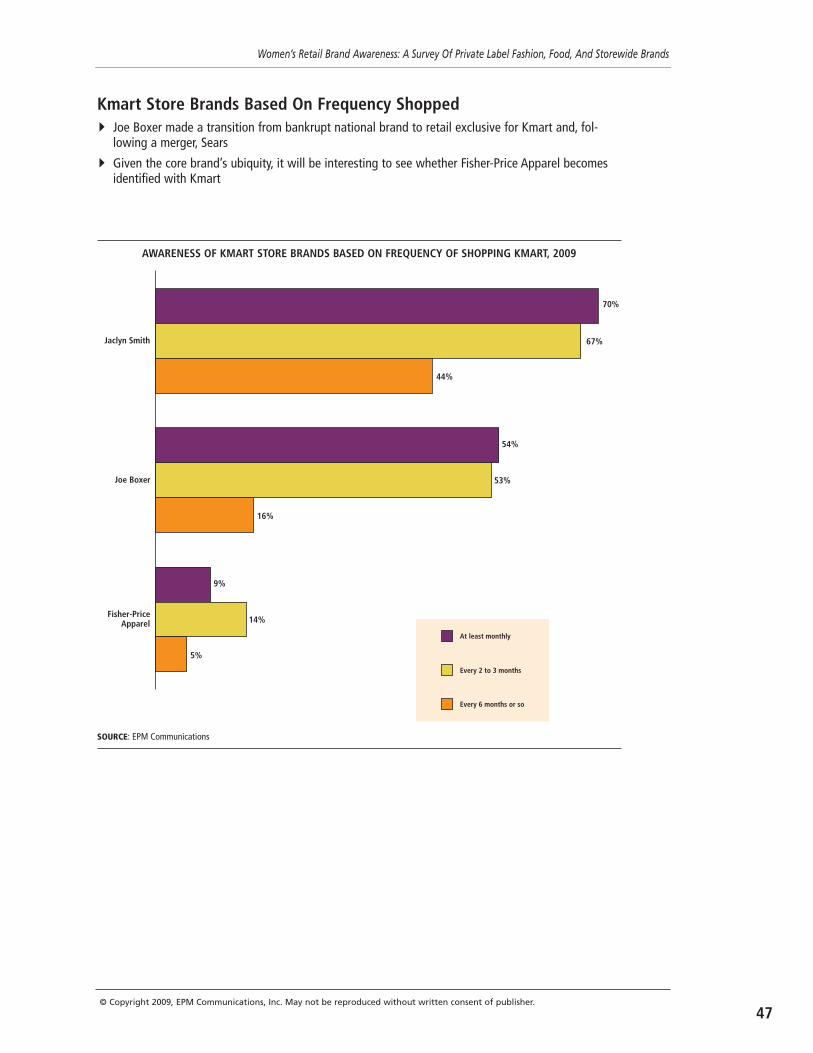

Fisher-PriceApparel

Joe Boxer

Jaclyn Smith

70%

67%

44%

54%

53%

16%

9%

14%

5%

At least monthly

Every 2 to 3 months

Every 6 months or so

Kmart Store Brands Based On Frequency Shopped� Joe Boxer made a transition from bankrupt national brand to retail exclusive for Kmart and, fol-

lowing a merger, Sears

� Given the core brand’s ubiquity, it will be interesting to see whether Fisher-Price Apparel becomesidentified with Kmart

SOURCE: EPM Communications

AWARENESS OF KMART STORE BRANDS BASED ON FREQUENCY OF SHOPPING KMART, 2009

47© Copyright 2009, EPM Communications, Inc. May not be reproduced without written consent of publisher.

Women’s Retail Brand Awareness: A Survey Of Private Label Fashion, Food, And Storewide Brands

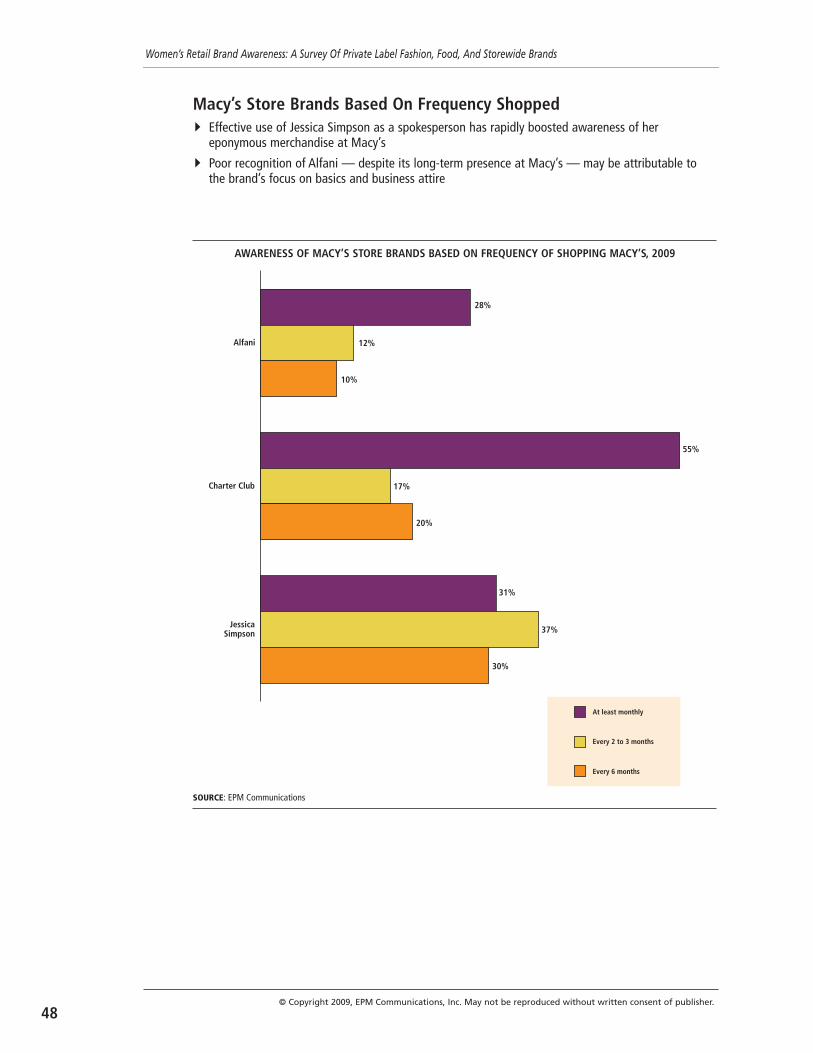

JessicaSimpson

Charter Club

Alfani

28%

12%

10%

55%

17%

20%

31%

37%

30%

At least monthly

Every 2 to 3 months

Every 6 months

Macy’s Store Brands Based On Frequency Shopped� Effective use of Jessica Simpson as a spokesperson has rapidly boosted awareness of her

eponymous merchandise at Macy’s

� Poor recognition of Alfani — despite its long-term presence at Macy’s — may be attributable tothe brand’s focus on basics and business attire

SOURCE: EPM Communications

AWARENESS OF MACY’S STORE BRANDS BASED ON FREQUENCY OF SHOPPING MACY’S, 2009

© Copyright 2009, EPM Communications, Inc. May not be reproduced without written consent of publisher.

48

Women’s Retail Brand Awareness: A Survey Of Private Label Fashion, Food, And Storewide Brands

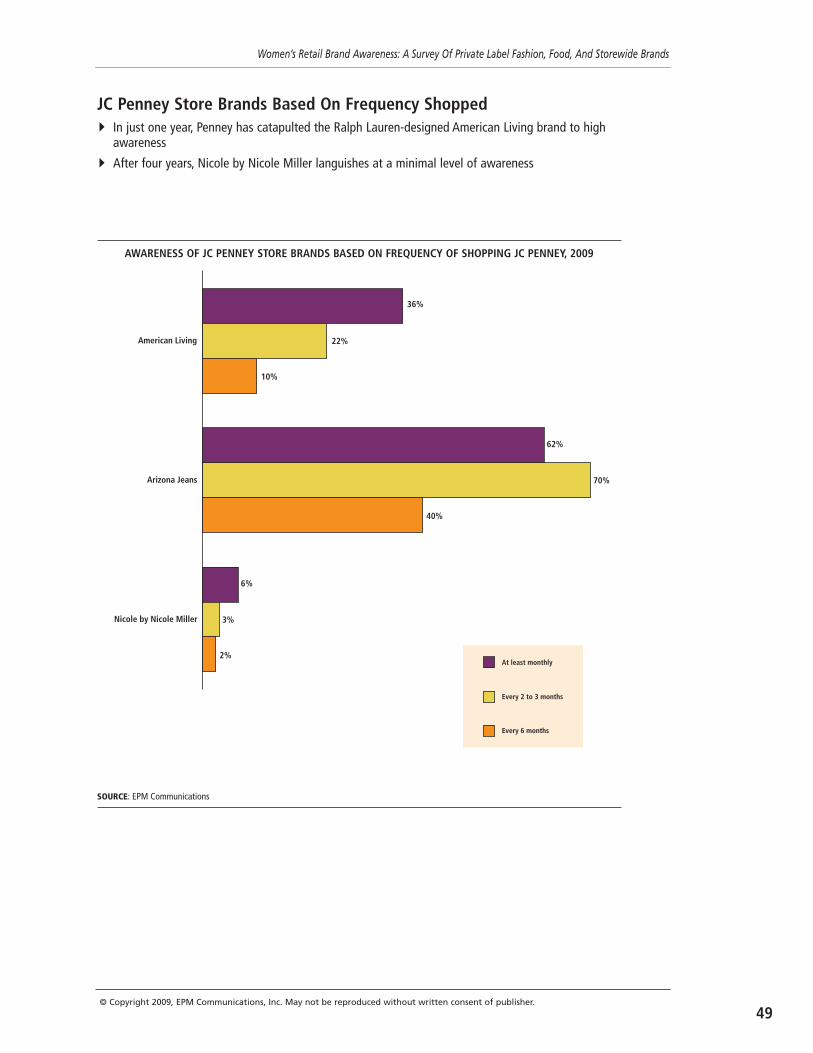

Nicole by Nicole Miller

Arizona Jeans

American Living

36%

22%

10%

62%

70%

40%

6%

3%

2%At least monthly

Every 2 to 3 months

Every 6 months

JC Penney Store Brands Based On Frequency Shopped� In just one year, Penney has catapulted the Ralph Lauren-designed American Living brand to high

awareness

� After four years, Nicole by Nicole Miller languishes at a minimal level of awareness

SOURCE: EPM Communications

AWARENESS OF JC PENNEY STORE BRANDS BASED ON FREQUENCY OF SHOPPING JC PENNEY, 2009

49© Copyright 2009, EPM Communications, Inc. May not be reproduced without written consent of publisher.

Women’s Retail Brand Awareness: A Survey Of Private Label Fashion, Food, And Storewide Brands

More than three in 10 women (31%) saythey shop a certain store because it is theonly place they can find a specific brand.

Those who say that a brand can make astore a shopping destination are more likelythan those who disagree to correctly identifythe stores that carry the brands included inthis survey, regardless of whether it is a foodbrand, apparel brand, or storewide brand.Women who say a brand does not make astore a destination more likely to knowMacy’s Alfani brand than those who say abrand makes a store a destination — the onlybrand for which this is true. (Few womenoverall know where the brand is sold.)

There are significant gaps in the ability tolink Macy’s and Jessica Simpson, Target andMossimo, and Kohl’s and Simply Vera VeraWang, suggesting that the exclusive agree-ments for those apparel brands with thoseretailers substantially impact shopper trafficto those stores. There is little difference inbrand awareness in the storewide category.

The younger a woman is, the more likelyshe is to say that a brand makes a store adestination for her. In addition, the lower herhousehold income, the more likely she is tosay brands make stores destinations.

Singletons (42%) are also more likely thanmarried women (30%) to say they shop cer-tain stores because of the brands they carry.Moms (34%) are more likely than womenwithout children (30%) to say brands drawthem to certain stores.

Exclusive BrandsBrands that are carried exclusively at one

store offer benefits to both the retailer —increased foot traffic — and vendor —increased spending. Overall, when brandsare exclusively available at one store:

� 42% of women are more likely to rec-ommend that store to their friendsand family;

� 41% say it increases the frequencywith which they shop a store; and

� 33% say they spend more at thosestores.

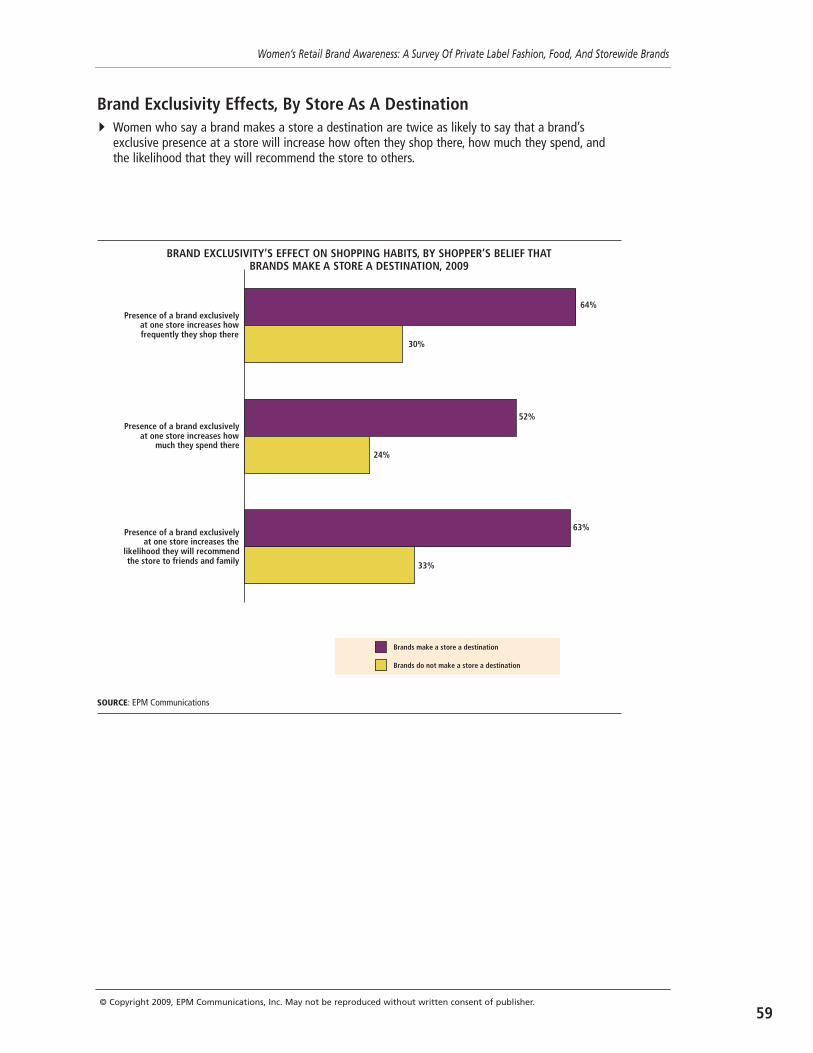

As might be expected, women who say thata brand can make a store a shopping destina-tion for them (64%) are more than twice aslikely as those who don’t (30%) to say thatbrands carried exclusively at one retailer willincrease how frequently they shop a store. Inaddition, 52% of women who claim brandsmake stores destinations say the presence ofa brand exclusively at one store increaseshow much they spend there, and 63% say itincreases the likelihood they will recommendthe store to friends and family.

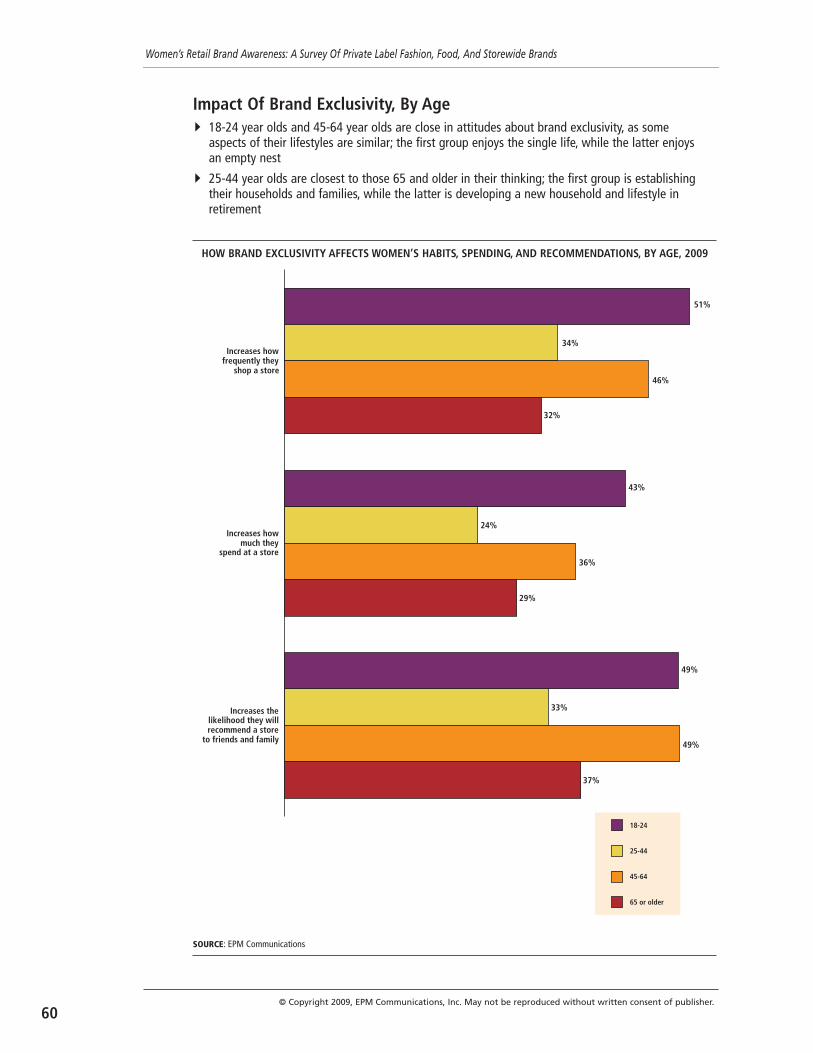

Women aged 18-24 are more likely thanolder women to say that exclusive brandsaffect their shopping habits and store recom-mendations. These young women are alsomore likely than their older counterparts tobe more brand conscious. Again, teens andtweens were not included in this survey,which may have led to higher awareness lev-els for some brands.

Interestingly, women aged 45-64 are thesecond most likely to say that exclusivebrands affect their shopping. Many BabyBoomer women have entered an empty-nestphase of life and have greater discretionaryincome to spend on themselves. Or they mayhave older children at home who are in theprocess of developing their own sense ofstyle, which rubs off on their mothers.

The least likely age group to say theirshopping habits are affected by exclusivebrands is 25-44 year olds. They are the mostlikely to have significant demands on their

DESTINATION BRANDS

51© Copyright 2009, EPM Communications, Inc. May not be reproduced without written consent of publisher.

Women’s Retail Brand Awareness: A Survey Of Private Label Fashion, Food, And Storewide Brands

© Copyright 2009, EPM Communications, Inc. May not be reproduced without written consent of publisher.

52

income — such as establishing a householdor starting a family — and are less swayed bybrands.

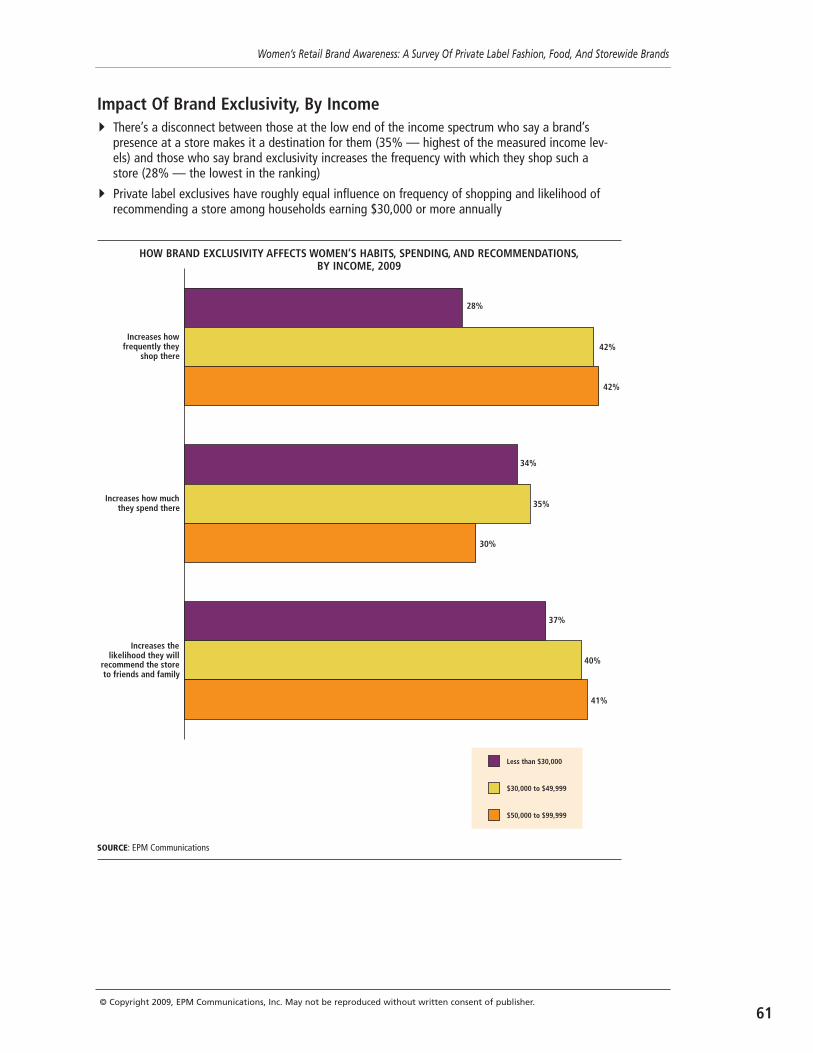

While women with the lowest householdincome are the most likely to say that abrand’s presence at a store makes it a desti-nation for their shopping, they are the leastlikely to say it increases how frequently theyshop a store. That may be because womenwith lower household incomes often avoidmaking frequent trips to a store in order tolessen the temptation to make impulse pur-chases.

However, this group is also among themost likely to say that a brand’s exclusivepresence at a store increases how much theyspend at that store.

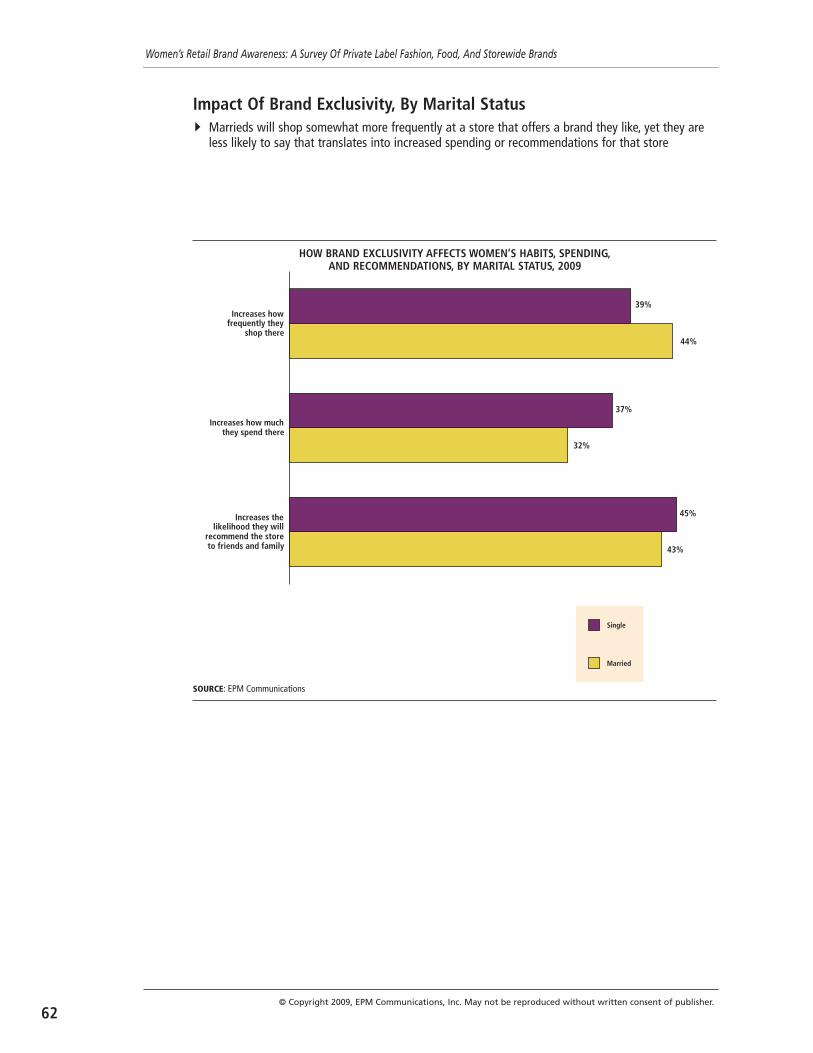

Married women (44%) are more likely thansingle women (39%) to say that a brand’sexclusive presence at a store will increasehow often they shop at a store, but singlewomen (37%) are more likely than marriedwomen (32%) to say that it will increase theamount they spend at a store. That is per-haps because single women have more dis-cretionary income to spend as they choose.

Women’s Retail Brand Awareness: A Survey Of Private Label Fashion, Food, And Storewide Brands

Women’s Retail Brand Awareness: A Survey Of Private Label Fashion, Food, And Storewide Brands

© Copyright 2009, EPM Communications, Inc. May not be reproduced without written consent of publisher.

53

65 and older

45-64

25-44

18-24 41%

32%

30%

21%

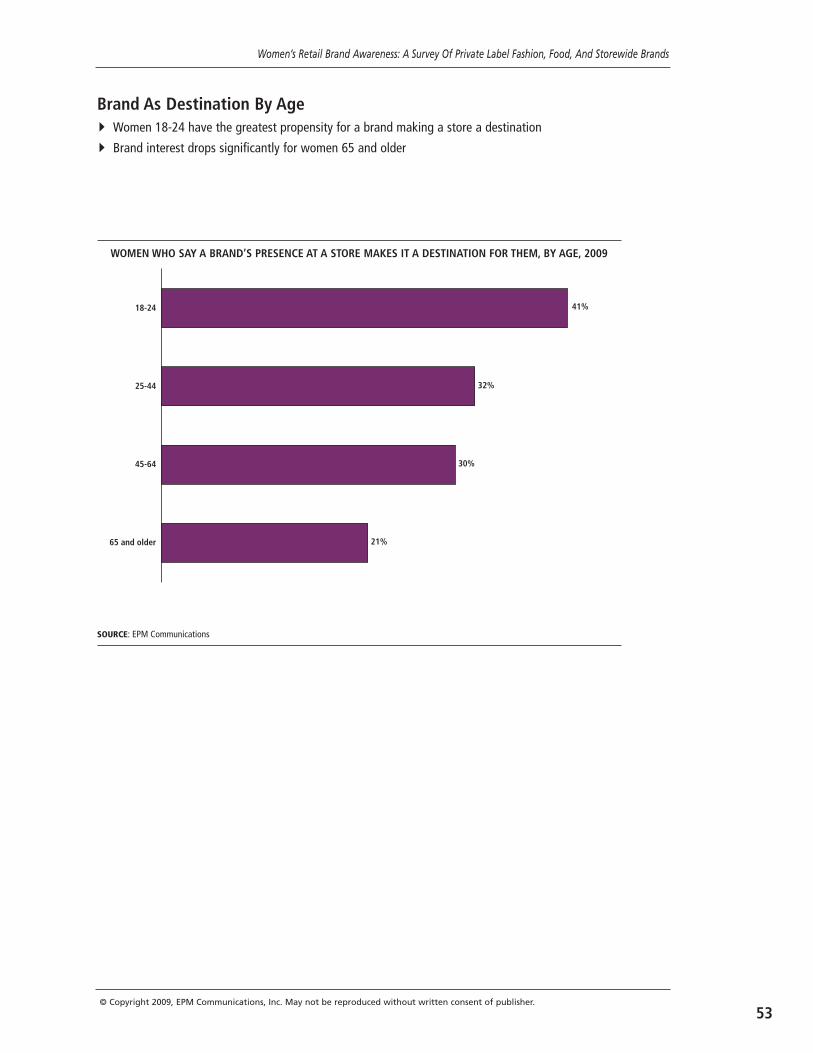

Brand As Destination By Age� Women 18-24 have the greatest propensity for a brand making a store a destination

� Brand interest drops significantly for women 65 and older

SOURCE: EPM Communications

WOMEN WHO SAY A BRAND’S PRESENCE AT A STORE MAKES IT A DESTINATION FOR THEM, BY AGE, 2009

Women’s Retail Brand Awareness: A Survey Of Private Label Fashion, Food, And Storewide Brands

54© Copyright 2009, EPM Communications, Inc. May not be reproduced without written consent of publisher.

$50,000 or $99,999

$30,000 to $49,999

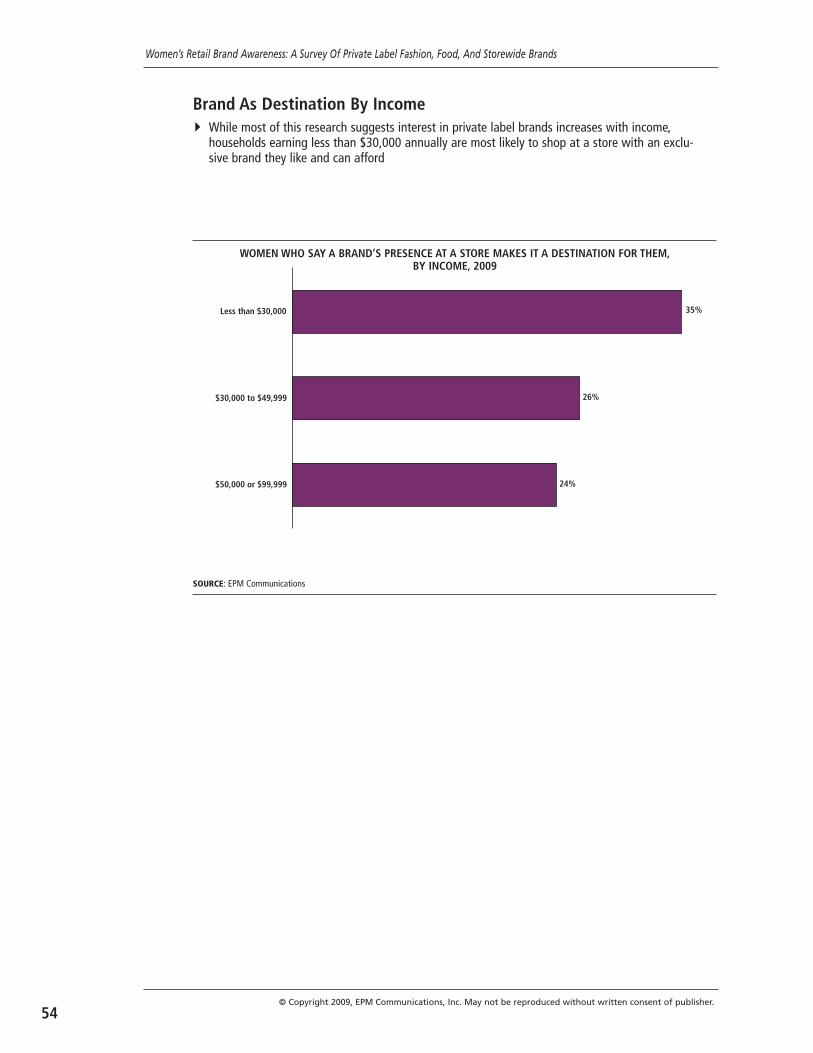

Less than $30,000 35%

26%

24%

Brand As Destination By Income� While most of this research suggests interest in private label brands increases with income,

households earning less than $30,000 annually are most likely to shop at a store with an exclu-sive brand they like and can afford

SOURCE: EPM Communications

WOMEN WHO SAY A BRAND’S PRESENCE AT A STORE MAKES IT A DESTINATION FOR THEM,BY INCOME, 2009

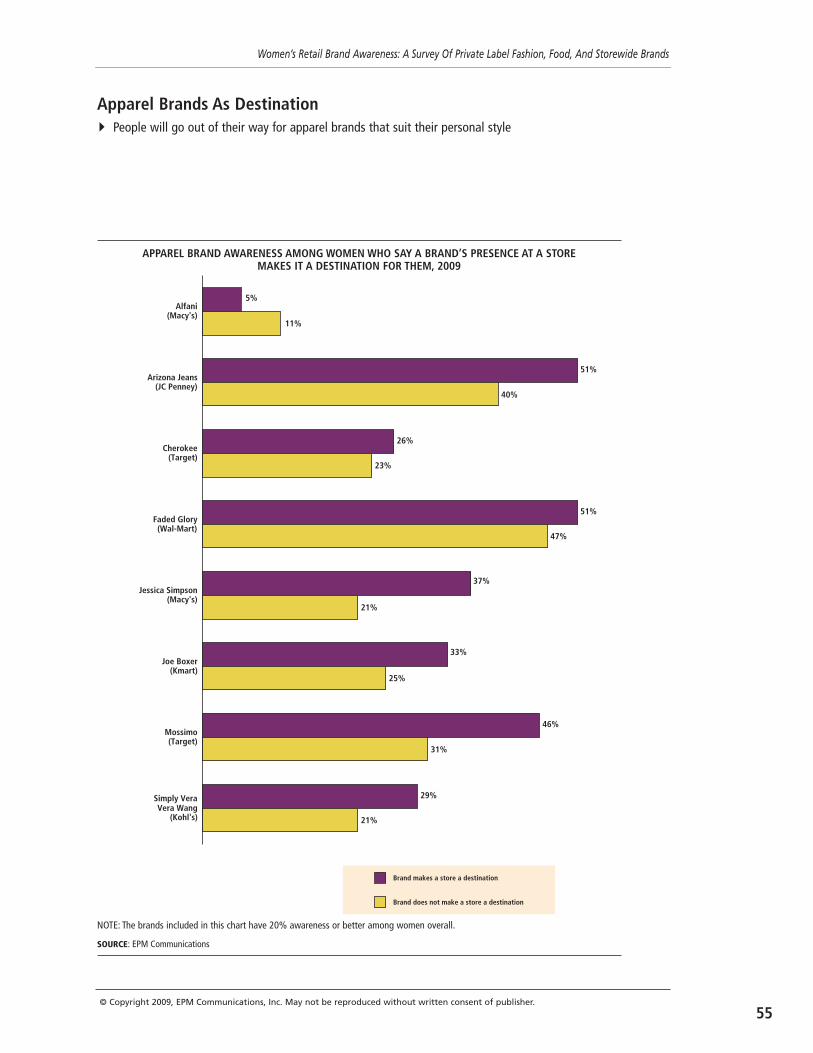

Simply VeraVera Wang

(Kohl's)

Mossimo(Target)

Joe Boxer(Kmart)

Jessica Simpson(Macy's)

Faded Glory(Wal-Mart)

Cherokee(Target)

Arizona Jeans(JC Penney)

Alfani(Macy's)

5%

11%

51%

40%

26%

23%

51%

47%

37%

21%

33%

25%

46%

31%

29%

21%

Brand makes a store a destination

Brand does not make a store a destination

Apparel Brands As Destination� People will go out of their way for apparel brands that suit their personal style

APPAREL BRAND AWARENESS AMONG WOMEN WHO SAY A BRAND’S PRESENCE AT A STOREMAKES IT A DESTINATION FOR THEM, 2009

NOTE: The brands included in this chart have 20% awareness or better among women overall.

SOURCE: EPM Communications

55© Copyright 2009, EPM Communications, Inc. May not be reproduced without written consent of publisher.

Women’s Retail Brand Awareness: A Survey Of Private Label Fashion, Food, And Storewide Brands

Market Pantry(Target)

Kirkland Signature(Costco)

Great Value(Wal-Mart)

Equate(Wal-Mart)

Archer Farms(Target)

31%

25%

52%

49%

59%

48%

29%

25%

27%

17%

Brand makes a store a destination

Brand does not make a store a destination

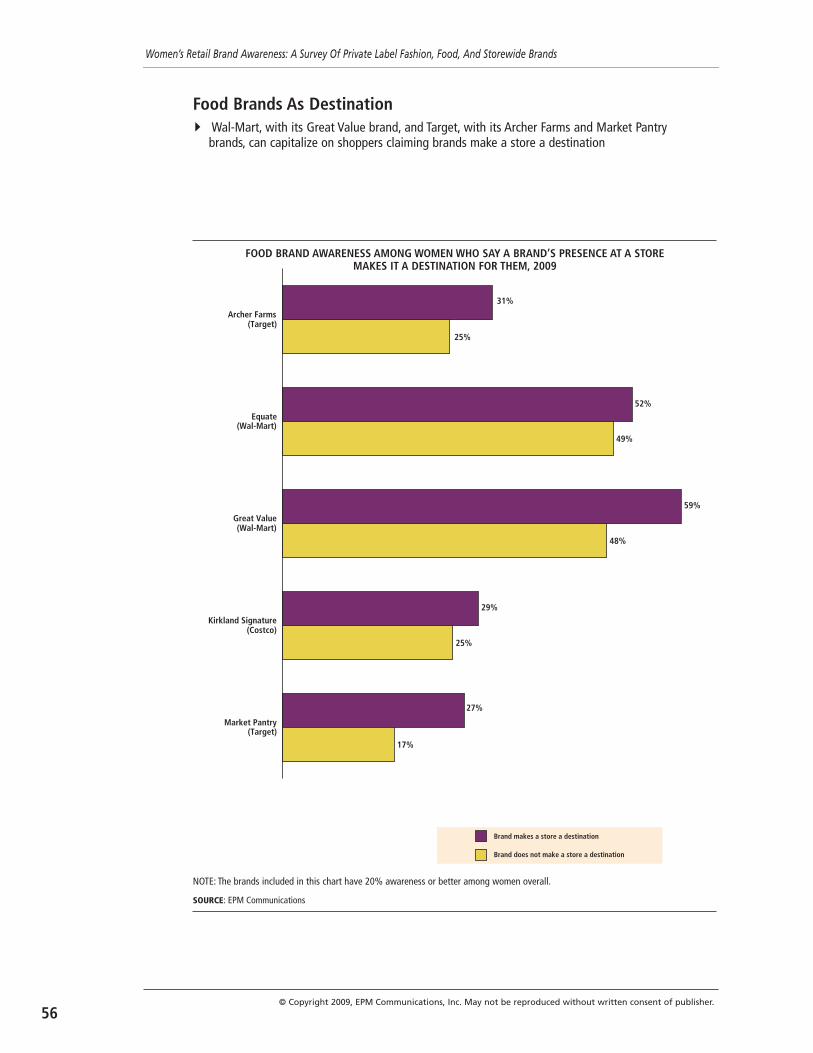

Food Brands As Destination� Wal-Mart, with its Great Value brand, and Target, with its Archer Farms and Market Pantry

brands, can capitalize on shoppers claiming brands make a store a destination

NOTE: The brands included in this chart have 20% awareness or better among women overall.

SOURCE: EPM Communications

FOOD BRAND AWARENESS AMONG WOMEN WHO SAY A BRAND’S PRESENCE AT A STOREMAKES IT A DESTINATION FOR THEM, 2009

© Copyright 2009, EPM Communications, Inc. May not be reproduced without written consent of publisher.

56

Women’s Retail Brand Awareness: A Survey Of Private Label Fashion, Food, And Storewide Brands

Sonoma(Kohl's)

Parent's Choice(Wal-Mart)

Member's Mark(Sam's Club)

Kenmore(Sears/Kmart)

Jaclyn Smith(Sears/Kmart)

Craftsman(Sears/Kmart)

Better Homes &Gardens (Wal-Mart)

26%

22%

79%

77%

49%

46%

79%

78%

28%

23%

28%

23%

23%

22%

Brand makes a store a destination

Brand does not make a store a destination

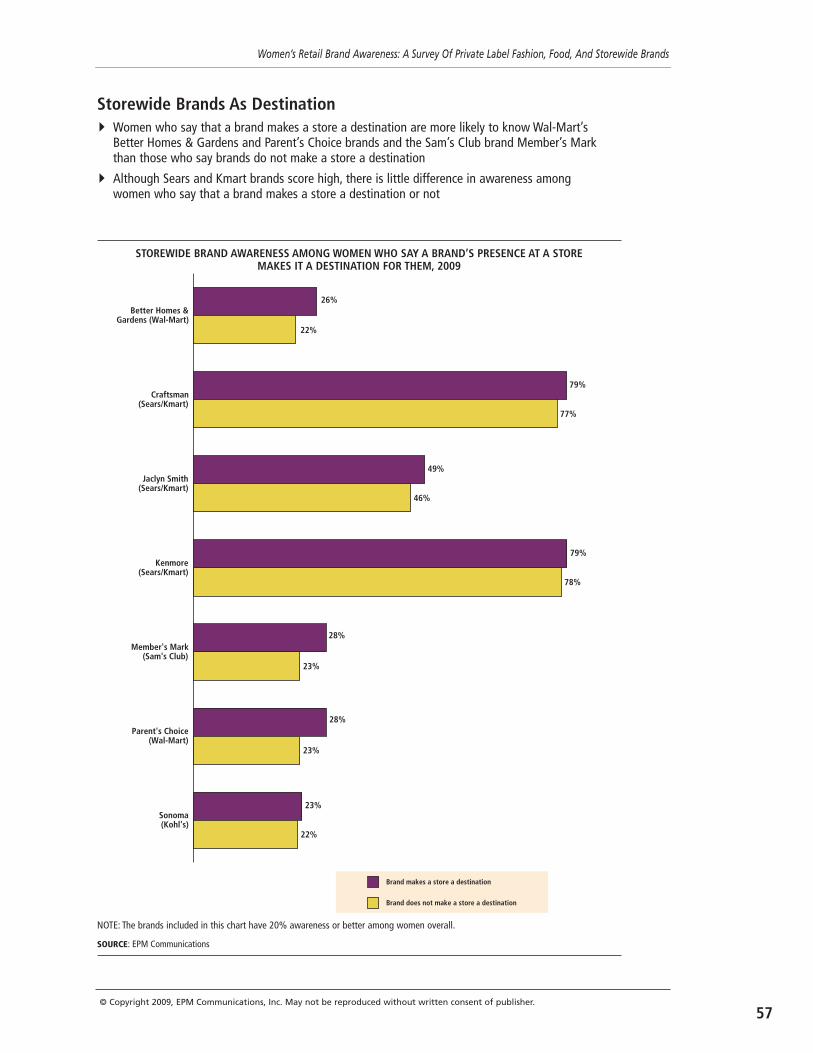

Storewide Brands As Destination� Women who say that a brand makes a store a destination are more likely to know Wal-Mart’s

Better Homes & Gardens and Parent’s Choice brands and the Sam’s Club brand Member’s Markthan those who say brands do not make a store a destination

� Although Sears and Kmart brands score high, there is little difference in awareness amongwomen who say that a brand makes a store a destination or not

STOREWIDE BRAND AWARENESS AMONG WOMEN WHO SAY A BRAND’S PRESENCE AT A STOREMAKES IT A DESTINATION FOR THEM, 2009

NOTE: The brands included in this chart have 20% awareness or better among women overall.

SOURCE: EPM Communications

57© Copyright 2009, EPM Communications, Inc. May not be reproduced without written consent of publisher.

Women’s Retail Brand Awareness: A Survey Of Private Label Fashion, Food, And Storewide Brands

Presence of a brand exclusivelyat one store increases the

likelihood they will recommendthe store to friends and family

Presence of a brand exclusivelyat one store increases

how much they spend there

Presence of a brand exclusivelyat one store increases

how frequently they shop there40.6% 34.8% 19.7% 4.9%

32.8% 37.7% 24.3% 5.2%

41.9% 35.4% 17.1% 5.6%

Agree Neutral Disagree No opinion

SOURCE: EPM Communications

HOW BRAND EXCLUSIVITY AFFECTS WOMENS’ HABITS, SPENDING, AND STORE RECOMMENDATIONS, 2009

© Copyright 2009, EPM Communications, Inc. May not be reproduced without written consent of publisher.

58

Effects Of Brand Exclusivity� More than four in 10 women say that the presence of a brand exclusively at one retailer will

increase how often they shop at that store and how likely they are to recommend it to friendsand family, however only a third say it will increase the amount they spend at the store.

Women’s Retail Brand Awareness: A Survey Of Private Label Fashion, Food, And Storewide Brands

Presence of a brand exclusivelyat one store increases the

likelihood they will recommendthe store to friends and family

Presence of a brand exclusivelyat one store increases how

much they spend there

Presence of a brand exclusivelyat one store increases howfrequently they shop there

64%

30%

52%

24%

63%

33%

Brands make a store a destination

Brands do not make a store a destination

SOURCE: EPM Communications

BRAND EXCLUSIVITY’S EFFECT ON SHOPPING HABITS, BY SHOPPER’S BELIEF THATBRANDS MAKE A STORE A DESTINATION, 2009

Brand Exclusivity Effects, By Store As A Destination� Women who say a brand makes a store a destination are twice as likely to say that a brand’s