1 www.coalimp.org.uk World Coal and the Imperative for CCS Nigel Yaxley Royal Society of Chemistry 24 th March 2010 World Coal and the Imperative for CCS World coal demand and supply growth Reserves and resources Coking demand and steel production World traded market IEA world energy outlook Policy developments Europe and UK Conclusions RSC Symposium 24th March 2010 2

Transcript

1

www.coalimp.org.uk

World Coal andthe Imperativefor CCS

Nigel YaxleyRoyal Society of Chemistry

24th March 2010

World Coal and theImperative for CCS

World coal demand and supply growthReserves and resourcesCoking demand and steel productionWorld traded marketIEA world energy outlookPolicy developments Europe and UKConclusions

RSC Symposium24th March 2010

2

2

Source: BP Statistical Review

Coal – the world’s fastestgrowing energy source

RSC Symposium24th March 2010

3

Coal production growtheven continued in 2009

0

1000

2000

3000

4000

5000

6000

7000

Mil

lion

To

nnes

Coking Coal

Steam Coal

RSC Symposium24th March 2010

4

Source: IEA Coal Information 2009

3

0

500

1000

1500

2000

2500

3000

Mill

ion

Tonn

es

2007 2008

2008 Total 5.85 billion tonnes hard coal

China dwarfs otherproducers…

RSC Symposium24th March 2010

5

Source: IEA Coal Information 2009

…and drives hard coalproduction growth…

RSC Symposium24th March 2010

6

0

1000

2000

3000

4000

5000

6000

7000

2003 2004 2005 2006 2007 2008

Mill

ion

Tonn

es

Others

Ukraine

Colombia

Poland

Kazakhstan

South Africa

Indonesia

Russia

Australia

India

United States

PR of China

Source: IEA Coal Information 2009

4

0

100

200

300

400

500

600

2003 2004 2005 2006 2007 2008

Mill

ion

Tonn

es

India

Australia

Russia

Indonesia

South Africa

Kazakhstan

Poland

Colombia

Ukraine

RSC Symposium24th March 2010

…but second tier producersalso show interesting trends

7

Source: IEA Coal Information 2009

EU remains world’s 3rdlargest coal consumer…

0.0

500.0

1000.0

1500.0

2000.0

2500.0

PR of China UnitedStates

EU27 India Russia Japan South Africa Others

Mill

ion

Tonn

esCo

alEq

uiva

lent

World CoalConsumption 2008(including lignite)

RSC Symposium24th March 2010

8

Source: IEA Coal Information 2009

5

EU IndigenousHard Coal, 122.6,

28%

EU IndigenousLignite, 133.2,

30%

Imported HardCoal, 181.4, 42%

Almost 60% of EU’s coalsupply is indigenous

2008 MtceBased onEstimatedCalorific Values

RSC Symposium24th March 2010

9

Source: EURACOAL

Reserves andResources Reserves – proven and can be recovered at

current prices with current technology Different sources and methodologies

WEC/BP/BGR Assessment of ‘economically recoverable’ is

difficult 728 billion tonnes hard coal (+269 Bn t lignite)

Resources – demonstrated quantities thatmight be recoverable in the future plusgeologically possible but not demonstrated Over 15 trillion tonnes hard coal (+4 Tn t lignite)

“Resources” are particularly relevant forunderground coal gasification

RSC Symposium24th March 2010

10

6

Reserves of coal are evenlydistributed around the globe

N. America120/10/8

Africa22/17/13

MiddleEast0/102/68

Europe18/2/5

FSU107/17/51 Asia Pacific

138/6/14

S. & Cent.America

7/18/7

(billion tonnes oil equivalent)coal / oil / gas

Global EnergyReserves 2008

Source: BP StatisticalReview of World Energy 2009

RSC Symposium24th March 2010

The top five countries have80% of proven reserves…

0

50

100

150

200

250

Bil

lion

Ton

ne

s

Source: BGR - Bundesanstalt für Geowissenschaften und Rohstoffe

12

7

0

1000

2000

3000

4000

5000

6000

7000

Billi

on

Tonn

es

Reserves ResourcesRSC Symposium24th March 2010

…and USA, China and Russiahave 90% of resources…

Source: BGR

13

0

50

100

150

200

250

300

350

400

450

500

Billion

To

nnes

Reserves ResourcesRSC Symposium24th March 2010

Changing the axis highlightslarge resources in the UK

Source: BGR

14

8

Coking Demand andSteel ProductionRemember coal is not just for electricity

production!Coking coal demand in 2009 was around

800 million tonnesEssential component in steel-makingUse is concentrated in rapidly growing

economiesMust not be forgotten in climate change

mitigationMeasures in old economies may simply

drive production elsewhere – “carbonleakage”

RSC Symposium24th March 2010

15

Coal in China powers morethan just electricity…

57%

8%

24%

3%8%

ElectricityCokingIndustryResidentialOthers

RSC Symposium24th March 2010

16

Source: IEA Coal Information 2009

9

China568

Japan88

Russia60

United States58

India57

South Korea49

Germany33

Ukraine30

Brazil27

Turkey25 Others

227

Million Tonnes

…with China also dominantin world steel production

RSC Symposium24th March 2010

17

Source: World Steel Association

Chinese steel productionwithstood the recession

RSC Symposium24th March 2010

18

0

200

400

600

800

1,000

1,200

1,400

1,600

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

Mill

ion

Tonn

es

Others

Turkey

Brazil

Ukraine

Germany

South Korea

India

United States

Russia

Japan

China

Source: World Steel Association

10

World Traded Market

Most coal demand in the world is metfrom indigenous supply

Around 15% is tradedDifferent players have dominated the

international coal marketBut this is changingWorld markets in 2009 saw a net

increase of 100 million tonnes inChinese demand

RSC Symposium24th March 2010

19

445492

532 575 607 606 615

191180

197

204226 243 231

0

100

200

300

400

500

600

700

800

900

2003 2004 2005 2006 2007 2008 2009 Est

Mill

ion

Tonn

es

Coking Coal

Steam Coal

RSC Symposium24th March 2010

World seaborne hard coaltrade stalled in 2009

20

Source: IEA Coal Information 2009

11

…but Asia/Pacific tradecontinued to grow

RSC Symposium24th March 2010

21

Source: Verein der KohlenImporteure

0

10

20

30

40

50

60

70

80

90

100

Mil

lio

nT

on

nes

Steam Coal Demand UK Production

RSC Symposium24th March 2010

UK has become a majorcoal importer…

Source – DECC

22

12

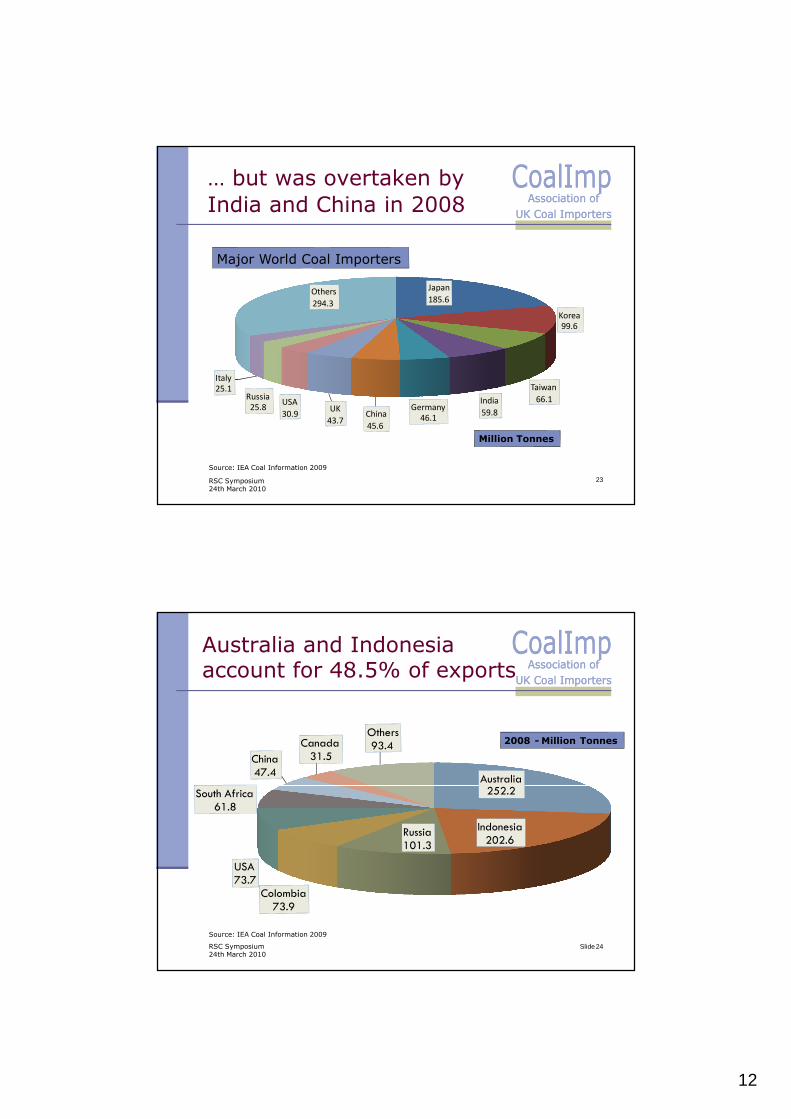

… but was overtaken byIndia and China in 2008

RSC Symposium24th March 2010

Japan185.6

Korea99.6

Taiwan66.1India

59.8Germany46.1China

45.6

UK43.7

USA30.9

Russia25.8

Italy25.1

Others294.3

Million Tonnes

Major World Coal Importers

23

Source: IEA Coal Information 2009

Australia252.2

Indonesia202.6

Russia101.3

Colombia73.9

USA73.7

South Africa61.8

China47.4

Canada31.5

Others93.4 2008 - Million Tonnes

Australia and Indonesiaaccount for 48.5% of exports

RSC Symposium24th March 2010

Slide24

Source: IEA Coal Information 2009

13

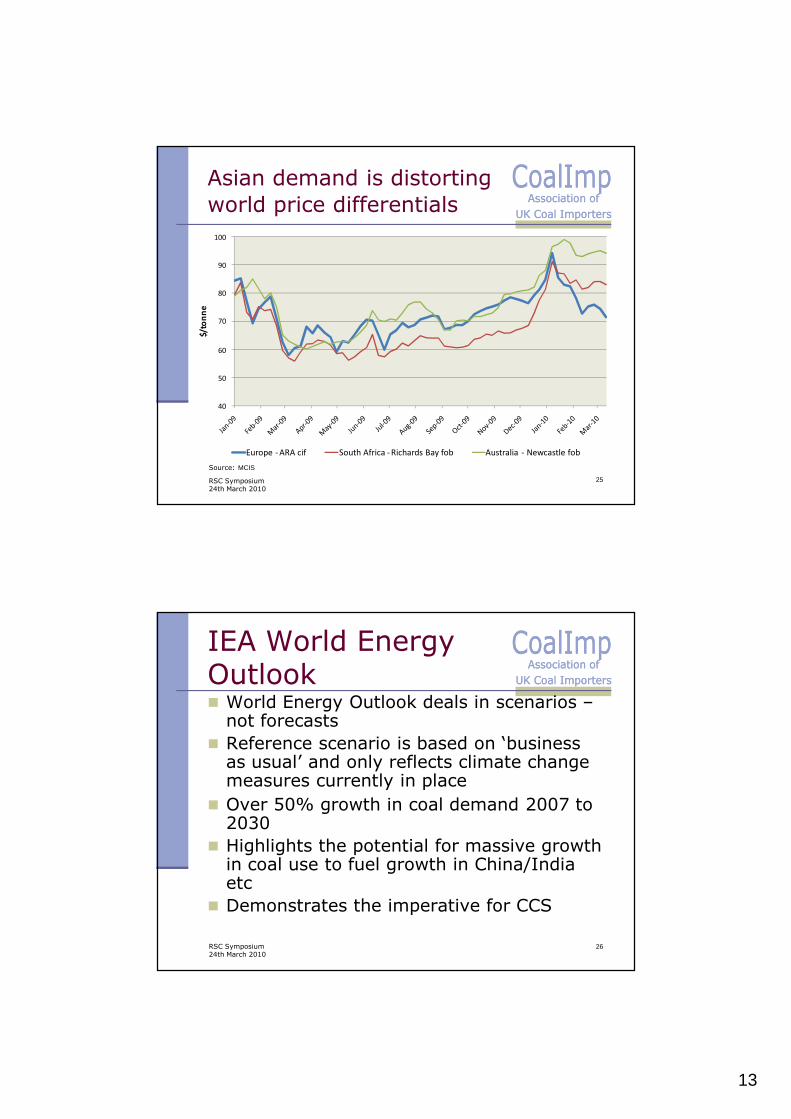

40

50

60

70

80

90

100

$/to

nne

Europe - ARA cif South Africa - Richards Bay fob Australia - Newcastle fob

Asian demand is distortingworld price differentials

RSC Symposium24th March 2010

25

Source: MCIS

IEA World EnergyOutlookWorld Energy Outlook deals in scenarios –

not forecastsReference scenario is based on ‘business

as usual’ and only reflects climate changemeasures currently in place

Over 50% growth in coal demand 2007 to2030

Highlights the potential for massive growthin coal use to fuel growth in China/Indiaetc

Demonstrates the imperative for CCS

RSC Symposium24th March 2010

26

14

IEA Reference Scenarioshows continued growth

RSC Symposium24th March 2010

27

EU

India

China

Others

0

500

1,000

1,500

2,000

2,500

3,000

3,500

20072015

2030

472

401

334

346 436837

1,847.00

2,633.00

3,424.00

1,883.00 1,998.002,386.00

Mill

ion

Tonn

esCo

alEq

uiva

lent

Source: IEA World Energy Outlook 2009

Policy Developments

15

IEA CCS roadmap sets thechallenge

Without CCSoverall costs toreduce emissionsto 2005 levels by2050increase by70%

Roadmap envisions100 projectsglobally by 2020and over 3000projects by 2050

RSC Symposium24th March 2010

29

EU attempts to kick-startCCS funding

EU Council has agreed12 CCSdemonstrations by2015

Economic Recoverypackage €1 billion for 6 projects

(including Hatfield) Funding from EUETS

300 Million EUAs fromNew Entrant Reserve

Further fundingneeded frommembers states

RSC Symposium24th March 2010

30

16

UK policy emerges

Financial support for upto four commercial-scaleCCS demonstrations

No new coal without CCSon a defined part of itscapacity

Requirement to retrofitCCS to full capacitywithin five years of CCSbeing judged technicallyand economically proven- planned on the basisthat CCS will be provenby 2020

Annual LuncheonMeeting 16thMarch 2010

31

…but progress is slow

Five months on… And little new emerges “CCS incentive able to

support full retrofit by2025”

Funding for up to fourprojects subsequentlyconfirmed

Energy bill passesthrough parliament

But the competitionruns on

Annual LuncheonMeeting 16thMarch 2010

32

17

CCS Industrial Strategywas launched last week

CCS – a massive industrialgrowth opportunity for the UK

Coal is the most abundantworldwide energy resourcebut it is also the mostpolluting, so there is nosolution to climate changewithout CCS

Yorkshire and Humber is wellplaced to see the benefitsfrom the jobs that investmentin CCS can bring, otherregions will too

For the UK economy as awhole these benefits could beworth up to £6.5 billion ayear, sustaining jobs for up to100,000 people, by 2030

RSC Symposium24th March 2010

33

…and the Conservativeslaunched their policy

A Conservative Government willput UK CCS back on track: Bring the current CCS

competition to a rapidconclusion

Expand the demonstrationprogramme to at least fourfacilities

We will ensure that CCSpipelines are planned andlocated where the greatestcapacity for growth can beprovided

Preference to fund the CCSdemonstrations from EUEmissions Trading Systemreceipts, but would adopt theCCS levy in the current EnergyBill to avoid further delays

RSC Symposium24th March 2010

34

18

Conclusions Coal is the world’s fastest growing energy source Reserves are widespread and resources are

massive – long term potential for UCG Coal is also required for steel production – key for

rapidly developing economies IEA ‘business as usual’ scenario shows 50%

growth in coal by 2030 Highlights the imperative for CCS EU/UK policy is enthusiastic about CCS -but

progress is slow “Global leadership” from Europe and USA is surely

![[Smart Grid Market Research] Coal: Closer Look at CCS (Part 3 of 3), May 2012](https://static.documents.pub/doc/80x56/5414023c8d7f7294698b47d3/smart-grid-market-research-coal-closer-look-at-ccs-part-3-of-3-may-2012.jpg)