www.dw-1.com Russian Oilfield Services “a $23 billion market by 2011” London Home Counties Branch – 25 th June 2007 Steve Robertson Assistant Director, Manager Oil & Gas Rod Westwood Analyst, Oil & Gas

Transcript

www.dw-1.com

Russian Oilfield Services “a $23 billion market by 2011”

London Home Counties Branch – 25th June 2007

Steve RobertsonAssistant Director, Manager Oil & Gas

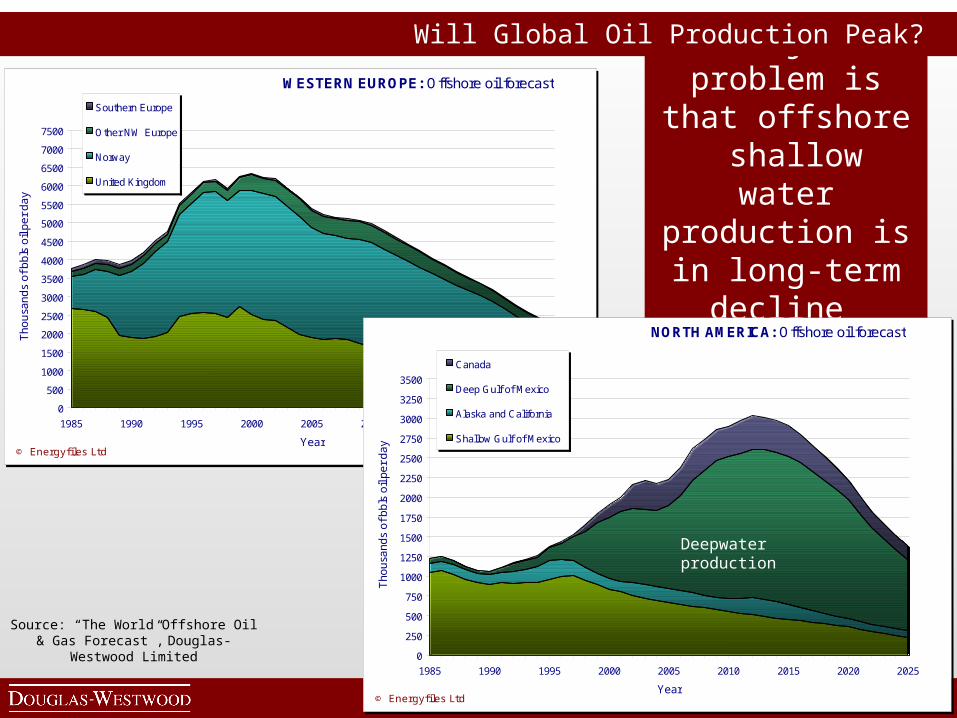

Demand – EIA forecast 118 million barrels per day by 2030

www.dw-1.com

• “The peak oil theory is flawed…..production is more likely to trace an undulating plateau that will last for a decade or more beyond 2030” Review of CERA report, Oil & Gas Journal Nov 27th, 2006

• “production will plateau at above 118 million b/d…..in 2031” Prof. H. R. Linden, Oil & Gas Journal Nov 27 th, 2006

• “CERA’s report contends that it is not reservoir constraints but aboveground factors such as geopolitics, conflict, economics, and

technology that will dictate future oil supply.” Review of CERA report, Oil & Gas Journal Nov 27th, 2006

Global oil reserves are not the issue. The key issue is our ability to produce them.

Longer term….limits of supply could come into play

• An oil supply peak? • Massive increases in oil prices could

result until alternatives are found• How long might that take? Some

think 20 years!

Near term…. Political influences could support prices

• OPEC gains influence over another 1.4 mm bpd via Angola

• Underpinning? The Saudi Arabian economy needs $45 oil

• OPEC would like $60 target price?• Oil supplies look set to remain

tight, supporting prices

www.dw-1.com

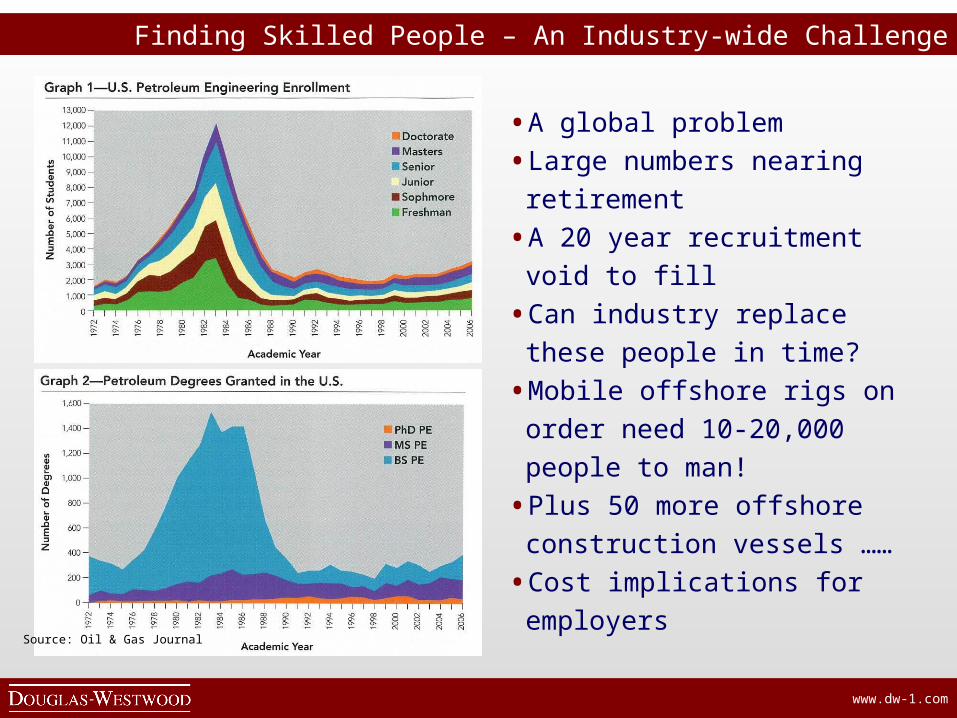

• A global problem

• Large numbers nearing retirement

• A 20 year recruitment void to fill

• Can industry replace these

people in time?

• Mobile offshore rigs on order

need 10-20,000 people to man!

• Plus 50 more offshore

construction vessels ……

• Cost implications for employers

Source: Oil & Gas Journal

Finding Skilled People – An Industry-wide Challenge

www.dw-1.com

•Arctic

•HPHT

•H2S

•Deepwater

•Politically unstable

The Easy Oil has been Found – the future?...Harsh Environments

www.dw-1.com

Oil & Gas Industry Cost Escalation

www.dw-1.com

Source: Lehman Brothers survey of 325 oil & gas companies E&P spend, 2006

0

50

100

150

200

250

300

350

Dec-04 Jun-05 Dec-05 Jun-06 Dec-06 07e

E&

P S

pend

($b

illion

s)

Oil Producers’ Equipment Expenditure

• Worldwide expenditure increasing year on year, $267 billion expenditure in 2006• Survey excludes some big spending state NOCs (e.g. Saudi Aramco)• Oil co. budgets based on oil price of $55.50 & gas $6.70 • “Companies would only reduce spend if oil prices fell to $42”• Investment decision threshold “in $20’s range”

www.dw-1.com

• A major power shift is underway

• 75% of oil reserves now held by NOCs

• Only 4% now controlled by the oil majors

• NOCs need technology & need the know-how

(But do they need / trust the oil majors?)

• NOCs are cooperating with each other

• NOCs governments want local content

“National oil companies will lead the 2007 increase in international spending with the largest spending growth among the Russian oil companies” Lehman Bros. Dec ’06 Survey

The Rise of the NOCs

www.dw-1.com

• Gazprom holds 16% of the world’s

gas reserves

• 2/3rd of Gazprom revenues are

from gas exports ($39 billion)

• Jan 1, 2006, supplies cut to

Ukraine (and parts of Europe)

• Jan 1 2007, doubles gas price to

Belarus & Georgia

• Wants to set up a “gas OPEC”?

• Jan 8 2007, Russia halts oil

exports via Belarus (to Europe!)

• “A giant aware of its power”

Sources: ISN Security Watch, 10 July 2006

Financial Times, 14 & 15 December 2006

Houston Chronicle, 8 Jan 2006

The Russian NOCs

www.dw-1.com

Source: Douglas-Westwood

0.0 0.1 0.2 0.3 0.4 0.5 0.6 0.7 0.8 0.9 1.0

Kazakhstan

Algeria

Mexico

Nigeria

India

Iran

Venezuela

China

Canada

Russia

USA

Index Relative to USA

2005

2010

Russia ranks third overall in the world for onshore expenditure throughout 2001-2005 and will continue to hold this position until 2010.

Although not included in this analysis, Saudi Arabia ranks second in the world for total onshore expenditure.

Onshore expenditure in Russia is increasing year on year compared with the US index.

Strong growth can be expected in Kazakhstan as this country continues to develop.

Russian Expenditure Comparison

www.dw-1.com

Douglas-Westwood Overview

Macro-economic trends

Russian regional overview

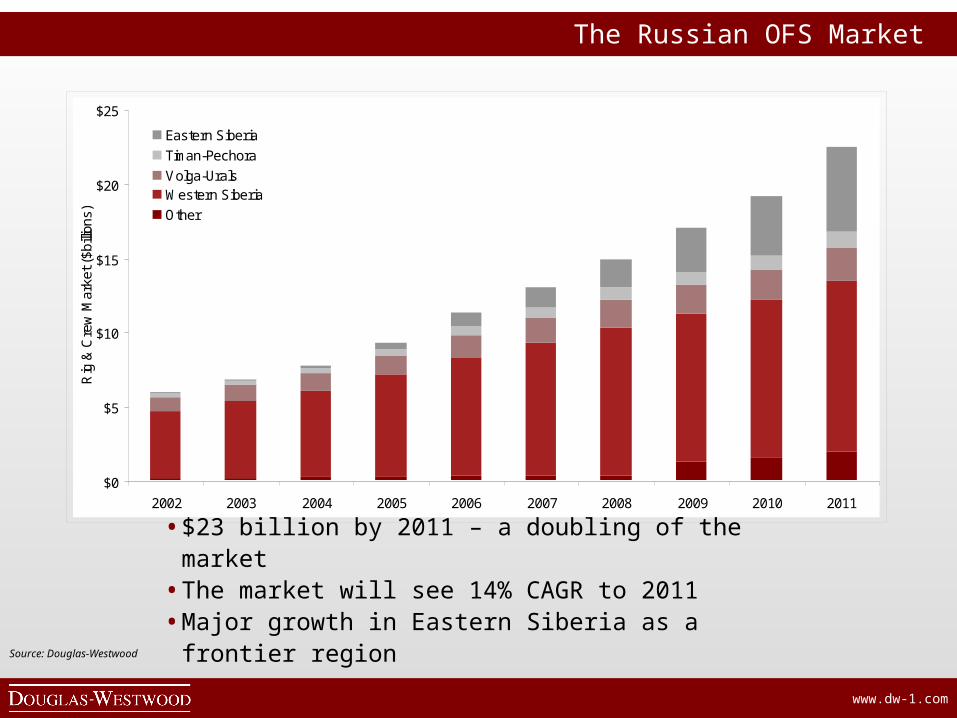

The Russian OFS Market

Conclusions

www.dw-1.com

Russian Oil Production

0

1

2

3

4

5

6

7

8

9

1019

30

1935

1940

1945

1950

1955

1960

1965

1970

1975

1980

1985

1990

1995

2000

2005

2010

2015

2020

2025

2030

2035

2040

2045

2050

Ann

ual O

il &

Gas

Pro

duct

ion

(billi

on b

oe)

Gas

Oil

• Production recovered since post-Soviet trough

• Major drilling & workover efforts – recent gains in production forecast to continue through to 2035

• Gas to play increasingly prominent role

www.dw-1.com

Russian Oil & Gas Production

Western Siberia

0

1

2

3

4

5

6

7

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Tot

al O

nsho

re P

rodu

ctio

n (b

nboe

)

Gas

Oil

• Mature region• Accounts for 60% of production• Samotlor (Russia’s largest oilfield)

peaked at 3.5 mboe/day and is now in decline

www.dw-1.com

Russian Oil Production

0

100

200

300

400

500

600

700

800

900

1,000

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Tot

al O

nsho

re P

rodu

ctio

n (m

mbo

e)

Gas

Oil

Volga Urals

• Most mature Russian region• Major EOR efforts underway• Romashkino oilfield now in decline

www.dw-1.com

Russian Oil Production

0

50

100

150

200

250

300

350

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Tot

al O

nsho

re P

rodu

ctio

n (m

mbo

e)

Gas

Oil

Timan-Pechora• Mainly a post-Soviet region• Strong growth forecast• Holds 8% of Russian reserves

www.dw-1.com

Russian Oil Production

0

50

100

150

200

250

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Tot

al O

nsho

re P

rodu

ctio

n (m

mbo

e)

Gas

Oil

Eastern Siberia

• A region in its infancy• Strong growth forecast• Lack of infrastructure in place• ‘Difficult’ geology – impact on cost• A major future OFS opportunity

www.dw-1.com

Douglas-Westwood Overview

Macro-economic trends

Russian regional overview

The Russian OFS Market

Conclusions

www.dw-1.com

Methodology – Challenges relating to Data Access

• Very little public-domain data• Small independent companies have very little public visibility• Few requirements to record information, companies now moving to western

business practices (but slowly!)• Reluctance of operators to release data, particularly with regards pricing• No rig count exists for Russia• Inactive rig cannibalisation

• Face-to-face meetings with major operators and drilling contractors• Evaluation and appraisal of Russian sources (e.g. Ministry information)• Sense-checking on multiple levels• Input and feedback from DWL’s due-diligence experience

Ch

alle

ng

esW

ork

aro

un

ds

www.dw-1.com

.

In-House Service Company

Oil Major

SpecialistSubsidiary

SpecialistSubsidiary

SpecialistSubsidiary

State Bodies

Service Teams

Development of the Russian OFS Industry

Soviet Post-Soviet

IndependentIndependentIndependent

www.dw-1.com

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Indigenous

Western

In-House

Source: Douglas-Westwood

Development of the Russian OFS Industry

Development of the Russian OFS Industry

www.dw-1.com

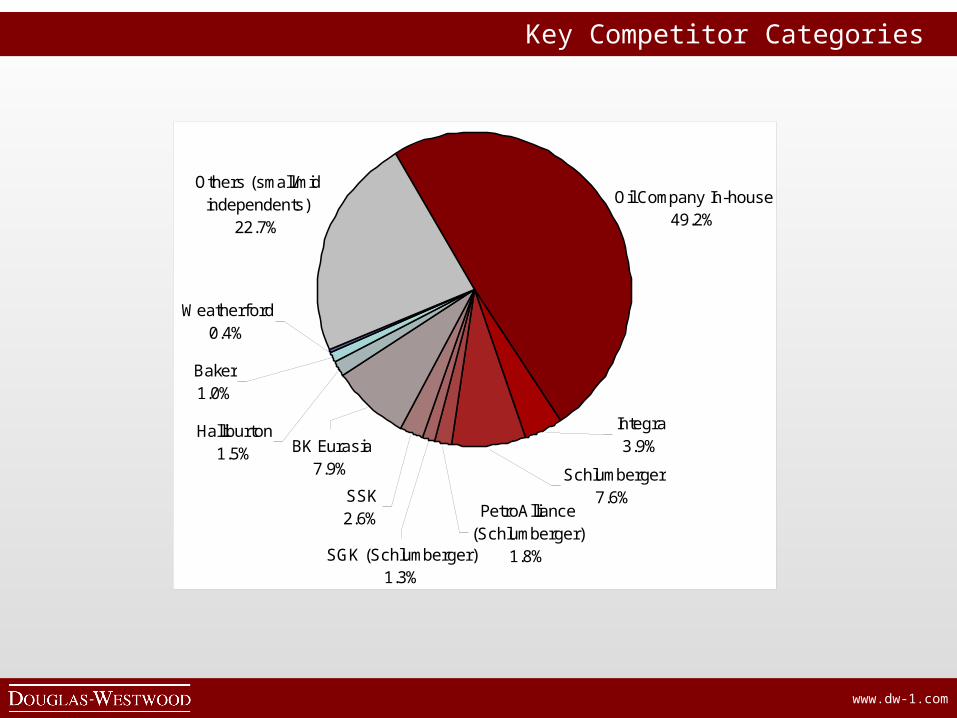

SSK2.6%

Integra3.9%

Schlumberger7.6%

PetroAlliance (Schlumberger)

1.8%SGK (Schlumberger)1.3%

BK Eurasia7.9%

Halliburton1.5%

Baker1.0%

Weatherford0.4%

Others (small/mid independents)

22.7%

Oil Company In-house49.2%

Key Competitor Categories

www.dw-1.com

Qua

lity,

Tec

hno

logy

Price

Russian independent service providers

Russian oil company in-house & affiliates

International service providers

SSK

Key Competitor Categories

www.dw-1.com

Decrease in Downhole Pressure

Maturing Regions

Increase inSand Production

Increase inWater-Cut

ProductionDecrease

TechnologyPush

3D

Se

ism

ic

Art

ifici

al L

ift

San

d C

ontr

ol

Inte

llig

en

t C

om

ple

tions

Dire

ctio

nal

Dri

lling

Hyd

rau

lic F

ract

urin

g

Wat

er

Co

ntr

ol

Res

erv

oir

En

gin

ee

rin

g

Production Increase

Increasing Technology Requirements

• Russian technology is fit-for-purpose• Westerners bring advanced tooling,

downhole technology, EOR methods and project management