29

Yale School of Management Hedge Funds and International Opportunities and Threats William N. Goetzmann Yale School of Management

| Date post: | 20-Dec-2015 |

| Category: |

Documents |

| View: | 218 times |

| Download: | 1 times |

Yale School of Management

Hedge Funds and International Opportunities and Threats

William N. Goetzmann

Yale School of Management

Yale School of Management

Two Parts

Example of opportunity Corporate governance Sentiment

Example of threat Blame and the Asian currency crisis

Yale School of Management

Modeling and Measuring Russian Corporate Governance:

The Case of Russian Preferred and Common Shares

William N. Goetzmann

Matthew Spiegel

Andrey Ukhov

Yale School of Management

Barriers to Efficiency

Expectations process flawed. Unreasonable expectations Poor information about benefits

The comparison process is flawed Market prices not observed or accurate

The trading process is flawed. Insider information vs. liquidity Recorded prices are inaccurate.

Yale School of Management

The Average Ratio of Common to Preferred Price Equally Weighted Index

0

1

2

3

4

5

6

7

8

Aug

-97

Oct

-97

Dec

-97

Feb

-98

Apr

-98

Jun-

98

Aug

-98

Oct

-98

Dec

-98

Feb

-99

Apr

-99

Jun-

99

Aug

-99

Oct

-99

Dec

-99

Feb

-00

Apr

-00

Jun-

00

Aug

-00

Oct

-00

Dec

-00

Feb

-01

Apr

-01

Jun-

01

Aug

-01

Oct

-01

Dec

-01

Feb

-02

Apr

-02

Jun-

02

Aug

-02

Oct

-02

Dec

-02

Feb

-03

Apr

-03

Date

Rat

io o

f C

om

mo

n t

o P

refe

rred

Sh

are

Pri

ces

Big 8 ALL

Yale School of Management

Stylized facts about Russian Preferred Shares

Minimum dividend set equal to a fraction of the firm’s earnings. Typically 10%.

Minimum dividend must at least equal that paid to the common shareholders.

Protection against splits, and similar actions.

Yale School of Management

The Puzzle

Why do Russian preferred shares typically sell for substantially less than the common?

The preferred are guaranteed cash flows at least equal to the common.

The preferred are guaranteed at least 10% of the firm’s profits.

The preferred get the legal right to vote.

Yale School of Management

Voting

Preferred shareholders are allowed to vote on: . . . modifications or amendments to the Charter may

affect the rights and interests of the first issue Preferred Stock owners . . . the decision has to be ratified by those owning two thirds of the Preferred Stock . . . Surgutneftegaz Charter

Other firms pool votes from the common and preferred.

Is voting really allowed?

Yale School of Management

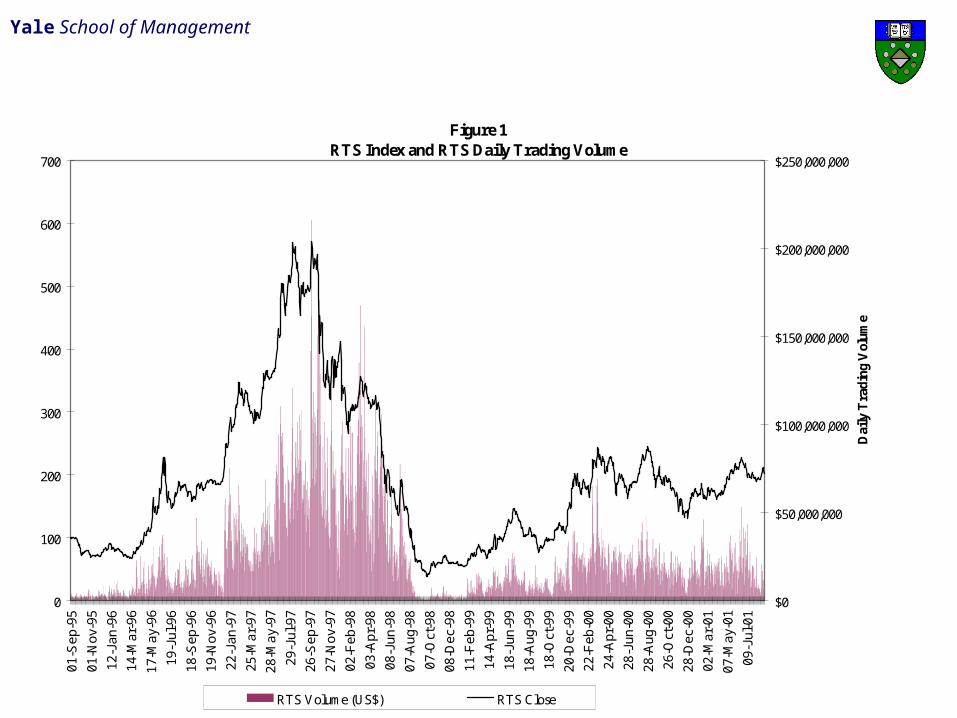

Figure 1RTS Index and RTS Daily Trading Volume

0

100

200

300

400

500

600

700

01-S

ep-9

5

01-N

ov-9

5

12-J

an-9

6

14-M

ar-9

6

17-M

ay-9

6

19-J

ul-9

6

18-S

ep-9

6

19-N

ov-9

6

22-J

an-9

7

25-M

ar-9

7

28-M

ay-9

7

29-J

ul-9

7

26-S

ep-9

7

27-N

ov-9

7

02-F

eb-9

8

03-A

pr-9

8

08-J

un-9

8

07-A

ug-9

8

07-O

ct-9

8

08-D

ec-9

8

11-F

eb-9

9

14-A

pr-9

9

18-J

un-9

9

18-A

ug-9

9

18-O

ct-9

9

20-D

ec-9

9

22-F

eb-0

0

24-A

pr-0

0

28-J

un-0

0

28-A

ug-0

0

26-O

ct-0

0

28-D

ec-0

0

02-M

ar-0

1

07-M

ay-0

1

09-J

ul-0

1

$0

$50,000,000

$100,000,000

$150,000,000

$200,000,000

$250,000,000

Dai

ly T

radi

ng V

olum

e

RTS Volume (US$) RTS Close

Yale School of Management

Can Corporate Governance Explain the Price Discrepancy?

Paper builds three simple models of expropriation and calculates the parameters needed to explain the current observed price discrepancies.

Two cash flow perpetual growth models, with a constant discount rate.

One relative return model.

Yale School of Management

Model 1: Value Expropriation

At some date T the common will take some fraction α of the preferred’s value.

Free parameters: r = interest rateα = level of expropriationg = growth rateT = expropriation date.

Fix r and α to reasonable values and then see if reasonable values of g and T will fit the data.

Yale School of Management

Values of T and g Implied by Prices of Common and Preferred Shares

Expropriation level: 75%r = real rate, g(rowth rate) in %, T

(expropriation date) years

LKOH RTKM SNGS

r 2000 2002 2000 2002 2000 2002

5% [g]

[T]

[2]

[14]

[-4]

[6]

[4]

[6]

[3]

[14]

[4]

[19]

[4]

[56]

15% [g]

[T]

[12]

[16]

[6]

[7]

[14]

[6]

[13]

[15]

[14]

[21]

[14]

[61]

Yale School of Management

Conclusions

No reasonable assumptions justify the spread. Is Russia a place where “reasonable”

assumptions make sense? Was this an opportunity for a convergence

trade? What factors should be considered?

Yale School of Management

Threats: Background

Speculators in global marketsSoros’ 1992 “attack”1997 Asian crisis1998 IMF study

Small group of funds with leverage attacking. Herding Positive feedback -- momentum

Yale School of Management

Possible? Likely?

Hedge fund scale vs. financial institutionsCo-ordination vs. concealmentPositive feedback?

Tech bubble stocks/large investors

Yale School of Management

BGP paper

Focus on a set of major funds Monthly data. Estimate exposures through time. Examine returns around crisis.

Some weekly data for two funds. Provides better estimates.

Yale School of Management

Funds and Capitalization, 9/1993 through 9/1997

Company 9/93 Capital 9/94 Capital 9/95 Capital 9/96 Capital 9/97 CapitalCapital International $414,851,451 $889,557,779 $889,557,779 $1,281,490,551 $2,098,790,487

$77,475,986 $188,000,000 $188,000,000 $521,000,000 $1,030,000,000 NA $2,100,000,000 $2,100,000,000 $2,471,369,347 $3,173,802,345

Tiger Management Corp. $3,207,000,000 $3,867,000,000 $3,867,000,000 $4,096,585,000 $7,109,416,846Orbis Investment Mgmt Ltd $586,086,439 $616,622,417 $616,622,417 $826,700,000 $1,122,579,613Orbis Investment Mgmt Ltd $626,514,397 $724,830,691 $724,830,691 $899,500,000 $1,039,465,999

Soros Fund Management NA $1,397,535,723 $1,397,535,723 $1,661,300,000 $2,026,600,000Soros Fund Management NA $3,803,764,764 $3,803,764,764 $4,528,400,000 $5,882,800,000

Soros Fund Management NA $1,259,245,119 $1,259,245,119 $1,567,900,000 $1,544,200,000Swiss Bank Corporation NA $828,724,170 $828,724,170 $1,848,500,000 $2,379,200,000

$4,911,928,273 $21,918,252,844 $15,675,280,664 $21,442,320,671 $29,467,860,414

Yale School of Management

Estimation

Rolling correlationsChanging frequencyWhat assets/currencies?

Yale School of Management

Fund Performance

Return 9/93 -10/97

June

July

August

Septem

ber

October

Emerging Markets Fund 8.13% 0.87% 1.59% 1.08% 1.88% 1.25%Everest Capital Int'l Ltd 18.21% 0.87% 0.87% 2.41% -2.10% 3.82%Haussman Holdings NV 12.54% 2.41% 0.87% 0.87% 10.98% 5.85%

Jaguar Fund NV 22.42% -2.10% 10.98% 0.87% 0.87% -4.29%

Orbis Global Equity Fund 13.72% 3.82% 5.85% -4.29% 0.87% 0.87%Orbis Optimal Equity Fund 6.65% 1.06% -1.67% 2.81% 0.27% 0.87%Quantum Emerging Growth 19.97% 5.65% 10.29% -6.72% 2.00% -11.77%

Quasar International Fund 11.25% 2.35% 9.17% -5.88% 0.45% -15.11%Quota Fund NV 43.50% 4.25% 13.62% -8.17% -3.86% -15.74%

Swiss Bank Currency Portfolio 13.92% -2.52% 0.38% 4.11% 1.46% 0.72%

Ringgit/Dollar Return -0.10% -0.47% -4.21% -10.17% NA

Yale School of Management

04/14/95

06/16/95 08/18/95 10/20/95 12/22/95 02/23/96 04/26/96 06/28/96 08/30/96 11/01/96 01/03/97 03/07/97 05/09/97 07/11/97 09/12/97 11/14/97

-15

-10

-5

0

5

Estimated Exposure Coefficie

nt

0.6 5

0.7

0.7 5

0.8

0.8 5

0.9

0.9 5

1

1.0 5

As ia n Ba s k e t

J a pa n

Ge rma ny

Brita in

Me x ic o

ring g it In de x

M anager 1: Exposures to M ul t i pl e Currenci es1 2 we e k ro llin g c oe ffic ie n ts

Yale School of Management

Managers

1994Jan

1994Apr

1994Jul

1994Oct

1995Jan

1995Apr

1995Jul

1995Oct

1996Jan

1996Apr

1996Jul

1996Oct

1997Jan

1997Apr

1997Jul

1997Oct

-40

-20

01

02

0Quantum.Emerging.Growth

Estimated 4 Month Exposure to Asia Basket

1994Jan

1994Apr

1994Jul

1994Oct

1995Jan

1995Apr

1995Jul

1995Oct

1996Jan

1996Apr

1996Jul

1996Oct

1997Jan

1997Apr

1997Jul

1997Oct

-20

02

04

0

Quasar.International.Fund

Estimated 4 Month Exposure to Asia Basket

Yale School of Management

Managers

1994Jan

1994Apr

1994Jul

1994Oct

1995Jan

1995Apr

1995Jul

1995Oct

1996Jan

1996Apr

1996Jul

1996Oct

1997Jan

1997Apr

1997Jul

1997Oct

-60

-40

-20

02

0Quota.Fund.NV

Estimated 4 Month Exposure to Asia Basket

1994Jan

1994Apr

1994Jul

1994Oct

1995Jan

1995Apr

1995Jul

1995Oct

1996Jan

1996Apr

1996Jul

1996Oct

1997Jan

1997Apr

1997Jul

1997Oct

-10

01

02

03

0

Currency.Portfolio.Ltd

Estimated 4 Month Exposure to Asia Basket

Yale School of Management

Fund & Hsieh Study

Larger number of funds: 19Style analysis identified macro-managers

Macro Trend Emerging Market

More events

Yale School of Management

October 1987

-40-30-20-10

0102030405060

Ret

urn

for

the

Mon

th

9/1/1987

Hedge Funds in Sample

Yale School of Management

1992 European Rate Mechanism Crisis

-10

0

10

20

30

Macro Macro Macro Macro Macro Macro Macro Macro Macro

Macro Macro Macro trend trend trend EM unclass unclass

unclass unclass unclass unclass

Yale School of Management

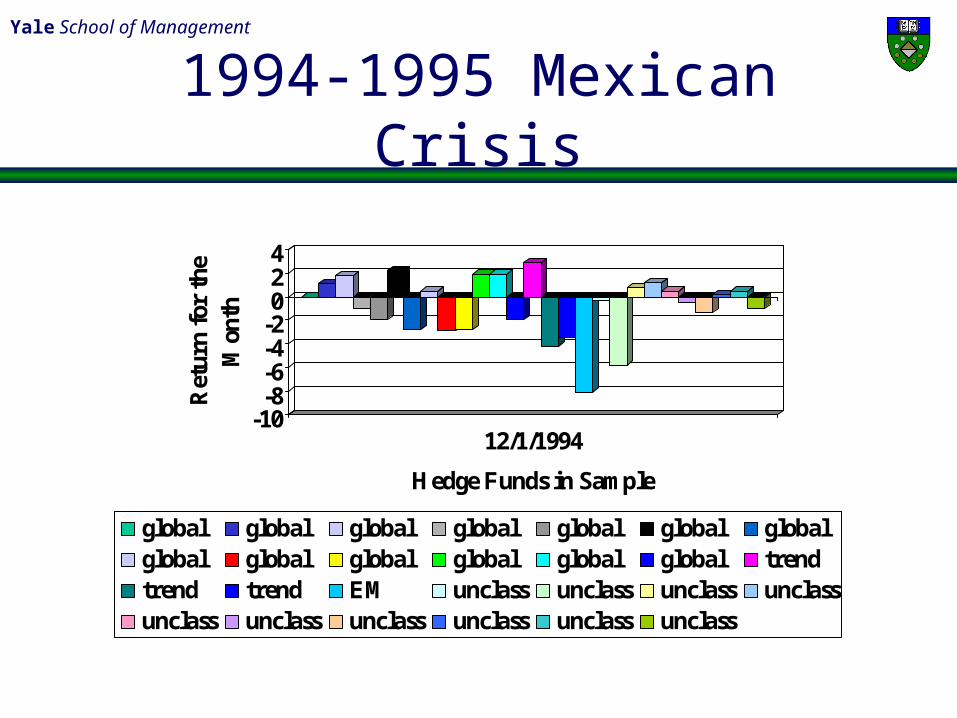

1994-1995 Mexican Crisis

-10-8-6-4-2024

Ret

urn

for

the

Mon

th

12/1/1994

Hedge Funds in Sample

global global global global global global globalglobal global global global global global trendtrend trend EM unclass unclass unclass unclassunclass unclass unclass unclass unclass unclass

Yale School of Management

Yale School of Management

According to F&S…

“Hedge funds never had more than $6 Billion short position in Asia currencies”

Was this enough?Small compared to banks: $36 billion net

outflow.

Yale School of Management

Current/Future Issues

“Manipulation” of voting rights?Short-selling as a threat?Foreign investor governance “arbitrage”Nature of arbitrage in expectations