APPRAISAL REPORT MARKET VALUE APPRAISAL OF HOHOKAM 10 BUSINESS CENTER AT 4425, 4445, 4535, AND 4555 EAST ELWOOD STREET, PHOENIX, ARIZONA PREPARED FOR ARIZONA DEPARTMENT OF TRANSPORTATION 1801 WEST JEFFERSON STREET, SUITE 120, MD 102M, PHOENIX, ARIZONA, 85007 ATTN: MR. TIMOTHY F. O'CONNELL, JR. RIGHT OF WAY PROJECT MANAGEMENT SECTION, REVIEW APPRAISER PARCEL: L-C-047 PROLOGIS OWNER: ADOT EFFECTIVE DATE: DECEMBER 19, 2017 MFVS FILE NO. 17365 PREPARED BY WENDELL L. MONTANDON, MAI AND R. JOHN MCDONALD, MAI OF MONTANDON FARLEY VALUATION SERVICES 1440 EAST MISSOURI AVENUE, SUITE C-100 PHOENIX, ARIZONA 85014

Transcript

APPRAISAL REPORT

MARKET VALUE APPRAISAL

OF HOHOKAM 10 BUSINESS CENTER

AT 4425, 4445, 4535, AND 4555 EAST

ELWOOD STREET,

PHOENIX, ARIZONA

PREPARED FOR

ARIZONA DEPARTMENT OF TRANSPORTATION

1801 WEST JEFFERSON STREET, SUITE 120, MD 102M,

PHOENIX, ARIZONA, 85007

ATTN: MR. TIMOTHY F. O'CONNELL, JR.

RIGHT OF WAY PROJECT MANAGEMENT SECTION, REVIEW APPRAISER

PARCEL: L-C-047 PROLOGIS

OWNER: ADOT

EFFECTIVE DATE: DECEMBER 19, 2017

MFVS FILE NO. 17365

PREPARED BY

WENDELL L. MONTANDON, MAI

AND

R. JOHN MCDONALD, MAI

OF

MONTANDON FARLEY VALUATION SERVICES

1440 EAST MISSOURI AVENUE, SUITE C-100

PHOENIX, ARIZONA 85014

WENDELL L. MONTANDON, MAI 1440 EAST MISSOURI AVENUE DENNIS L. FARLEY JR., MAI R. JOHN McDONALD, MAI SUITE C-100 SARA CABIRAC

PETER MENGHINI PHOENIX, ARIZONA 85014 LISA ANDREWS

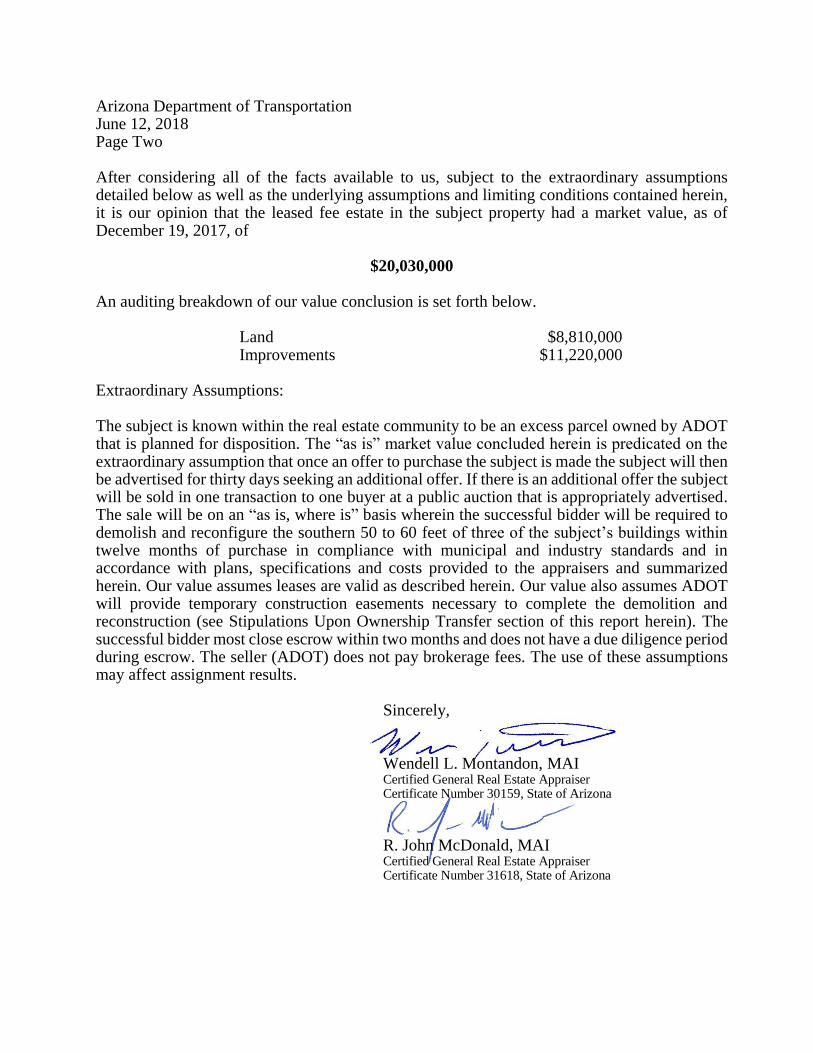

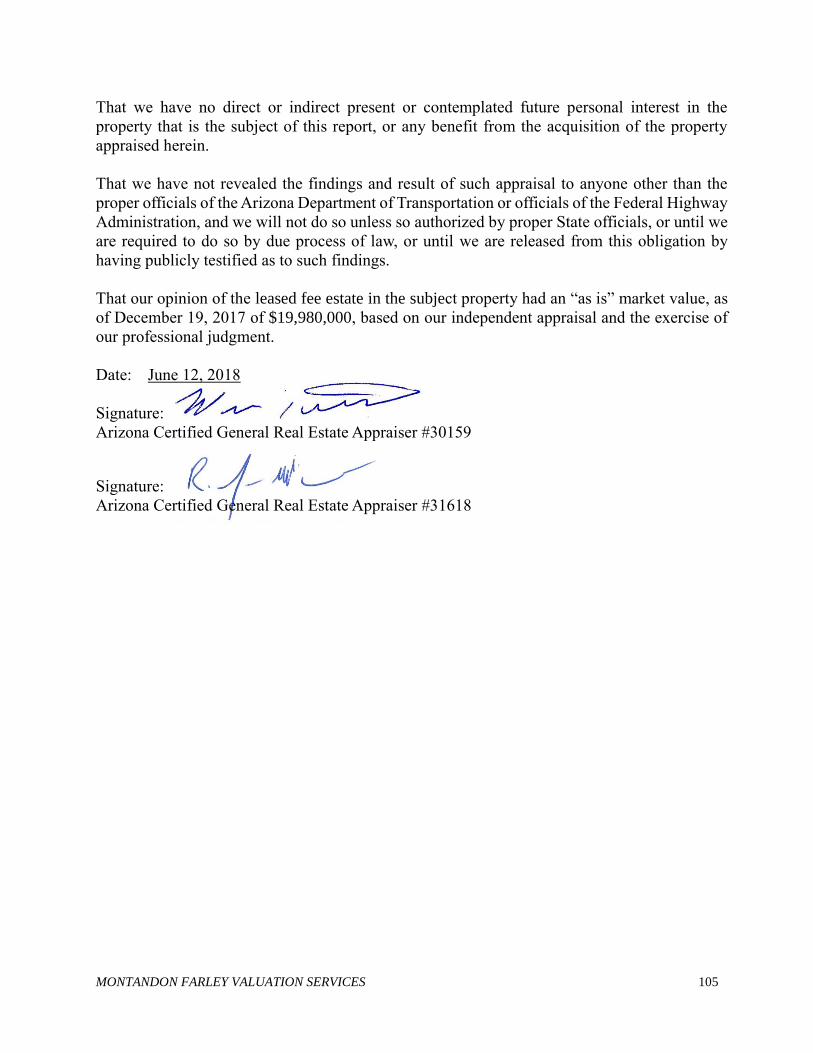

Arizona Department of Transportation June 12, 2018 Page Two After considering all of the facts available to us, subject to the extraordinary assumptions detailed below as well as the underlying assumptions and limiting conditions contained herein, it is our opinion that the leased fee estate in the subject property had a market value, as of December 19, 2017, of

$20,030,000 An auditing breakdown of our value conclusion is set forth below. Land $8,810,000 Improvements $11,220,000 Extraordinary Assumptions: The subject is known within the real estate community to be an excess parcel owned by ADOT that is planned for disposition. The “as is” market value concluded herein is predicated on the extraordinary assumption that once an offer to purchase the subject is made the subject will then be advertised for thirty days seeking an additional offer. If there is an additional offer the subject will be sold in one transaction to one buyer at a public auction that is appropriately advertised. The sale will be on an “as is, where is” basis wherein the successful bidder will be required to demolish and reconfigure the southern 50 to 60 feet of three of the subject’s buildings within twelve months of purchase in compliance with municipal and industry standards and in accordance with plans, specifications and costs provided to the appraisers and summarized herein. Our value assumes leases are valid as described herein. Our value also assumes ADOT will provide temporary construction easements necessary to complete the demolition and reconstruction (see Stipulations Upon Ownership Transfer section of this report herein). The successful bidder most close escrow within two months and does not have a due diligence period during escrow. The seller (ADOT) does not pay brokerage fees. The use of these assumptions may affect assignment results. Sincerely, Wendell L. Montandon, MAI Certified General Real Estate Appraiser Certificate Number 30159, State of Arizona

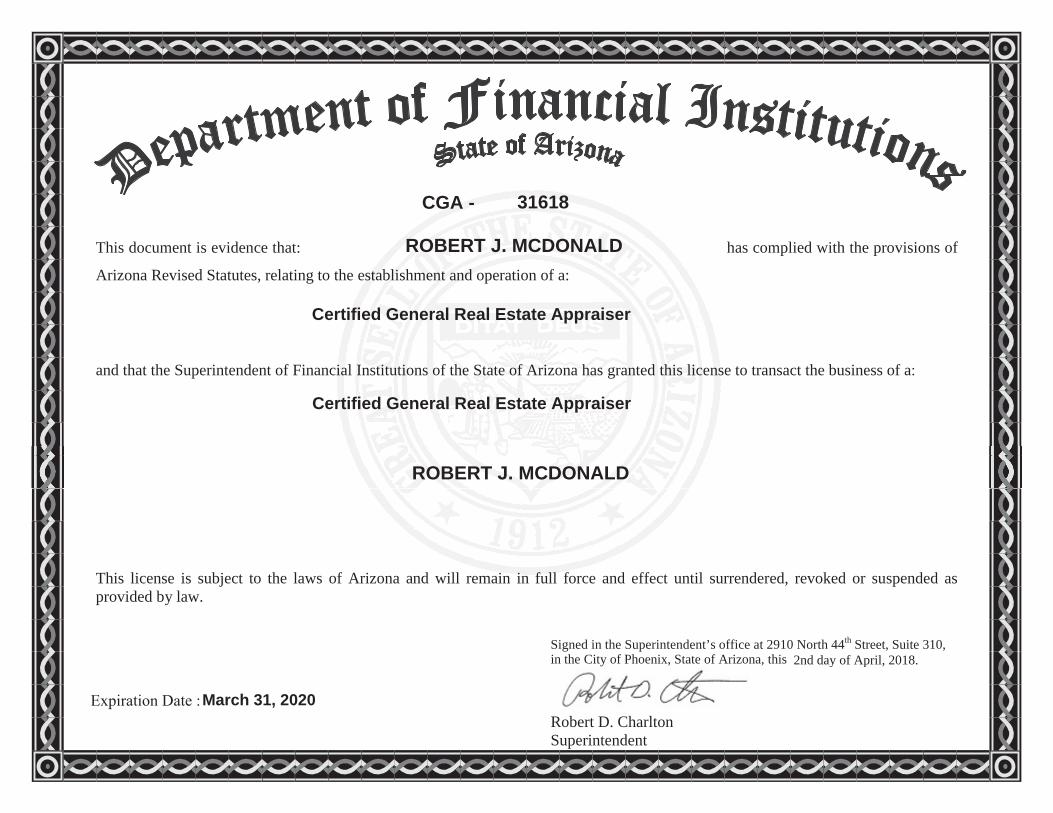

R. John McDonald, MAI Certified General Real Estate Appraiser Certificate Number 31618, State of Arizona

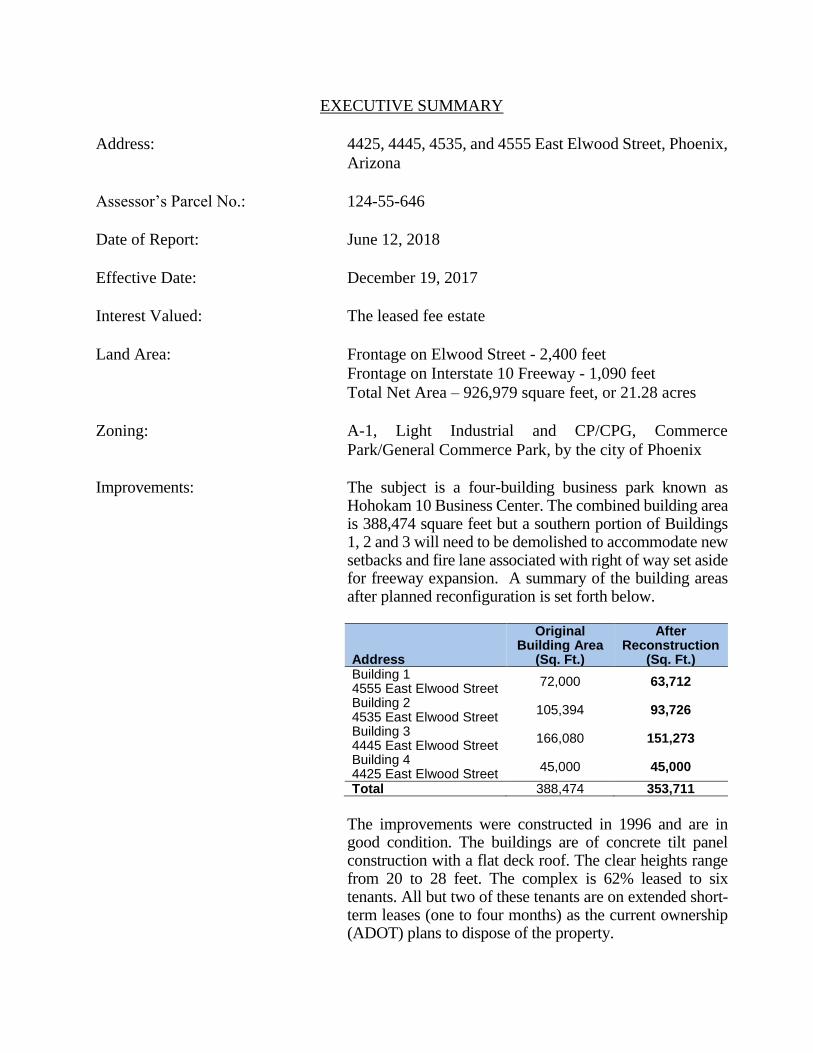

EXECUTIVE SUMMARY

Address: 4425, 4445, 4535, and 4555 East Elwood Street, Phoenix,

Arizona

Assessor’s Parcel No.: 124-55-646

Date of Report: June 12, 2018

Effective Date: December 19, 2017

Interest Valued: The leased fee estate

Land Area: Frontage on Elwood Street - 2,400 feet

Frontage on Interstate 10 Freeway - 1,090 feet

Total Net Area – 926,979 square feet, or 21.28 acres

Zoning: A-1, Light Industrial and CP/CPG, Commerce

Park/General Commerce Park, by the city of Phoenix

Improvements: The subject is a four-building business park known as

Hohokam 10 Business Center. The combined building area is 388,474 square feet but a southern portion of Buildings 1, 2 and 3 will need to be demolished to accommodate new setbacks and fire lane associated with right of way set aside for freeway expansion. A summary of the building areas after planned reconfiguration is set forth below.

Address

Original Building Area

(Sq. Ft.)

After Reconstruction

(Sq. Ft.) Building 1 4555 East Elwood Street

72,000 63,712

Building 2 4535 East Elwood Street

105,394 93,726

Building 3 4445 East Elwood Street

166,080 151,273

Building 4 4425 East Elwood Street

45,000 45,000

Total 388,474 353,711

The improvements were constructed in 1996 and are in

good condition. The buildings are of concrete tilt panel construction with a flat deck roof. The clear heights range from 20 to 28 feet. The complex is 62% leased to six tenants. All but two of these tenants are on extended short-term leases (one to four months) as the current ownership (ADOT) plans to dispose of the property.

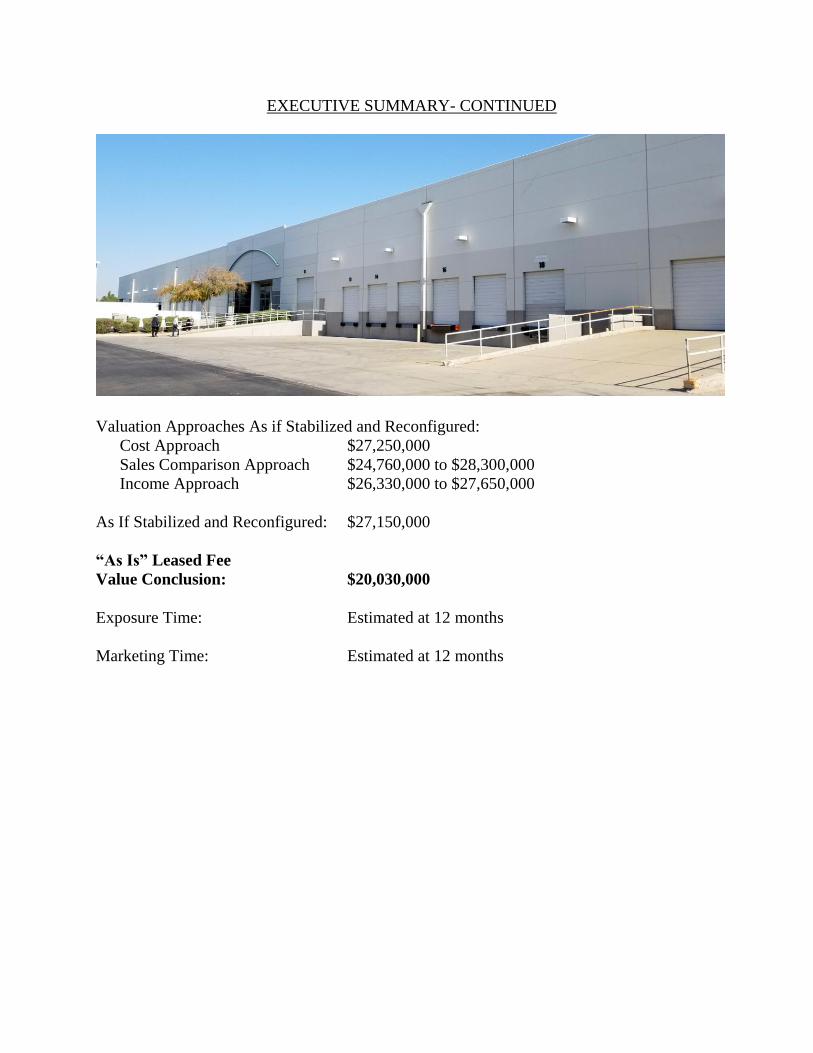

EXECUTIVE SUMMARY- CONTINUED

Valuation Approaches As if Stabilized and Reconfigured:

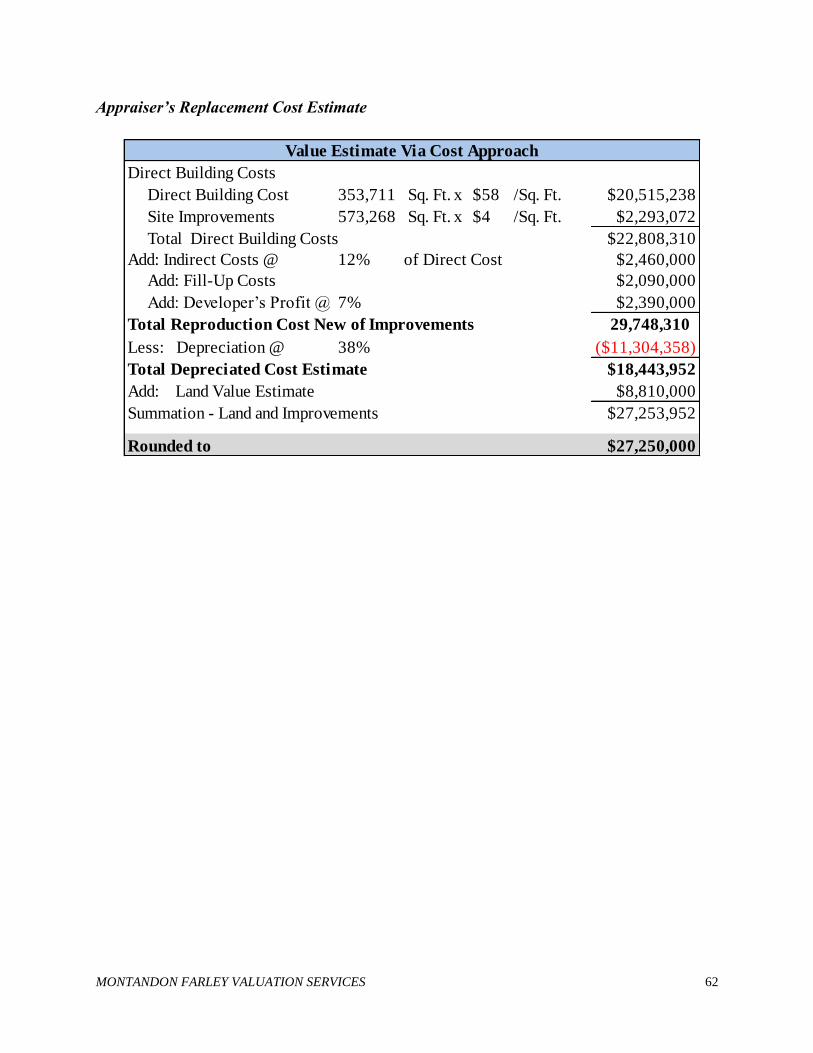

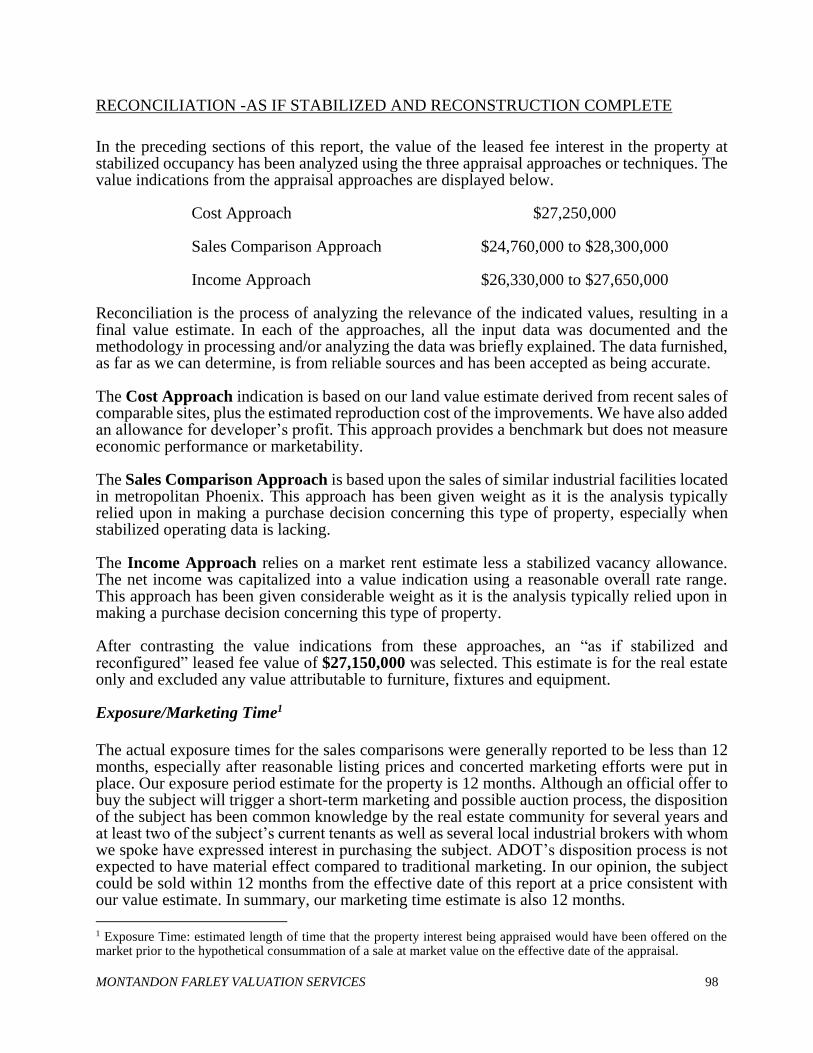

Cost Approach $27,250,000

Sales Comparison Approach $24,760,000 to $28,300,000

Income Approach $26,330,000 to $27,650,000

As If Stabilized and Reconfigured: $27,150,000

“As Is” Leased Fee

Value Conclusion: $20,030,000

Exposure Time: Estimated at 12 months

Marketing Time: Estimated at 12 months

TABLE OF CONTENTS

PREFACE

LETTER OF TRANSMITTAL

EXECUTIVE SUMMARY

TABLE OF CONTENTS

PURPOSE OF THE APPRAISAL ................................................................................................... 1

INTENDED USER AND USE ......................................................................................................... 1

The purpose of this appraisal report is to provide the appraiser’s best estimate of the market

value, as of December 19, 2017, of the leased fee estate in the property at 4425, 4445, 4535, and

4555 East Elwood Street, in Phoenix, Arizona. The current owner, Arizona Department of

Transportation, intends to dispose of the property but will retain the southern 60 to 75 feet that

for freeway right of way expansion. The subject property excludes this retained right of way and

the south 50 to 60 feet of the subject’s Buildings 1, 2 and 3 will require demolition and

reconstruction with a new configuration due to fire lane and setback requirement associated with

the new right of way line. These obligations are considered in the “as is” leased fee value of the

property.

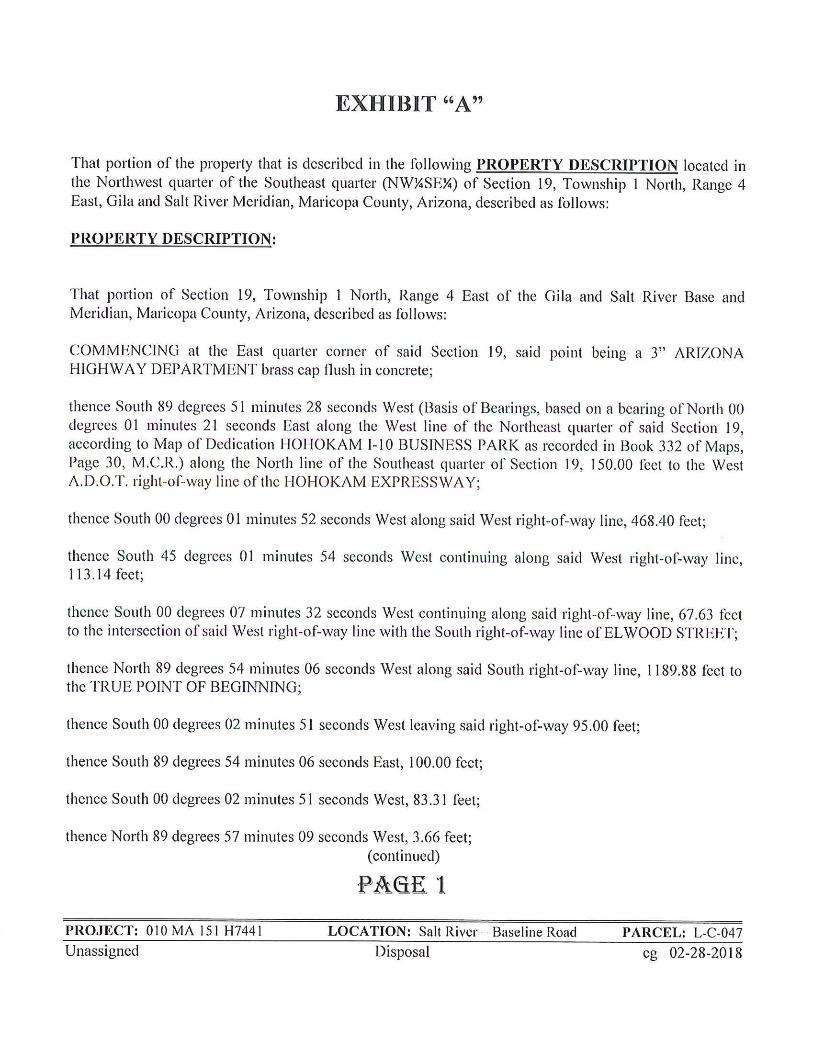

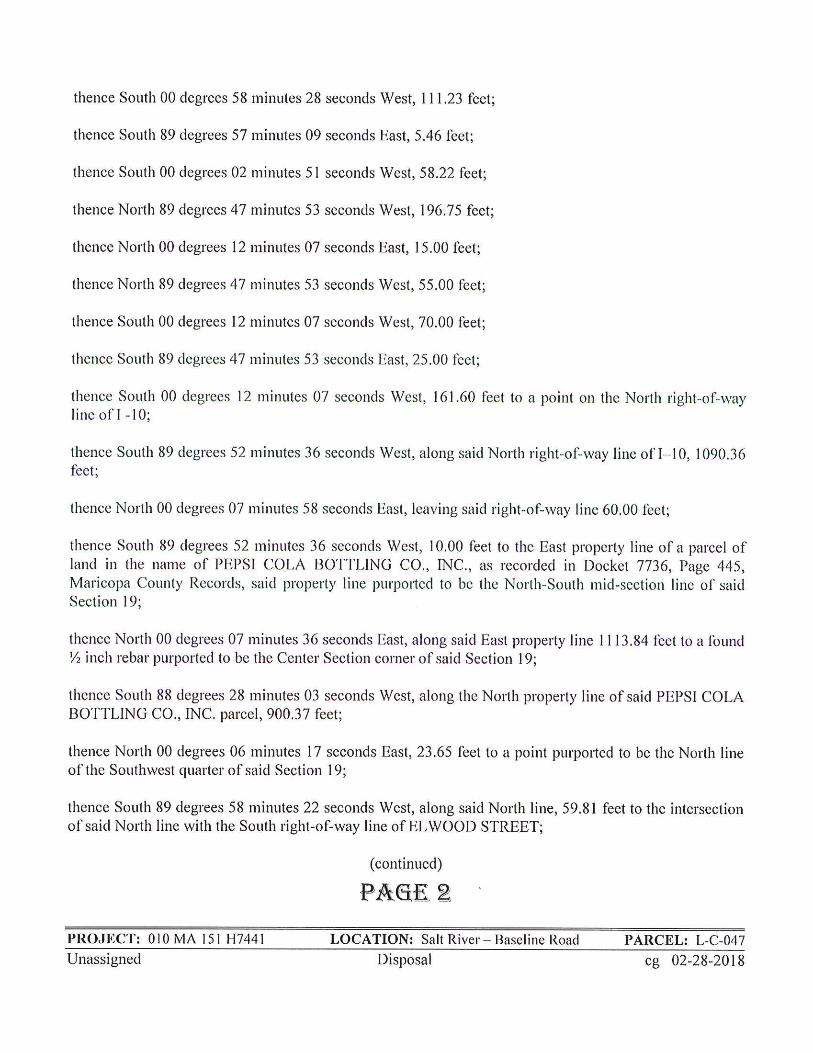

The legal description of the property is set forth is set forth in the addenda to this report.

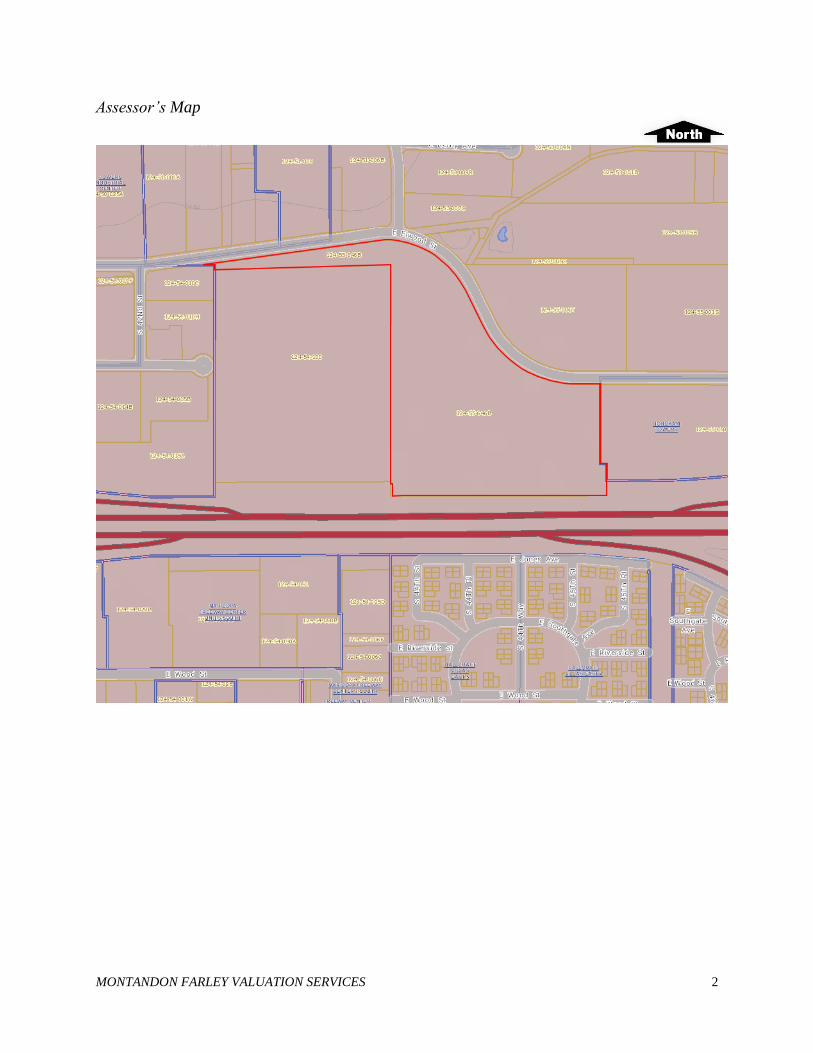

The property is also identified as Maricopa County Assessor’s parcel 124-55-646. A copy of the

Assessor’s plat, with the subject outlined, is included on the following page.

INTENDED USER AND USE

This report is intended for use only by Arizona Department of Transportation (ADOT) and the

Federal Highway Administration (FHWA) for use in assisting in decisions regarding the

disposition of the property. Use of this report by others, or for any other use, is not intended by

the appraisers.

MONTANDON FARLEY VALUATION SERVICES 2

Assessor’s Map

MONTANDON FARLEY VALUATION SERVICES 3

DEFINITIONS

Market Value, pursuant to Arizona Revised Statute 28-7091, is as follows: “…Market Value’ means the most probable price estimated in terms of cash in

United States dollars or comparable market financial arrangements that the property

would bring if exposed for sale in the open market, with reasonable time allowed in

which to find a purchaser, buying with knowledge of all of the uses and purposes to

which it was adapted and for which it was capable.”.1 Market value “As Is” is defined as: The estimate of the market value of real property in its current physical condition,

use, and zoning as of the appraisal date. (Proposed Interagency Appraisal and Evaluation Guidelines, OCC-4810-33-P 20%)2

Fee simple estate is defined as: Absolute ownership unencumbered by any other interest or estate, subject only to

the limitations imposed by the governmental powers of taxation, eminent domain, police power, and escheat.3

Leased fee estate is defined as: A freehold (ownership interest) where the possessory interest has been granted to

another party by creation of a contractual landlord-tenant relationship (i.e., a lease).4

Hypothetical Condition is defined as:

A condition, directly related to a specific assignment, which is contrary to what is known

by the appraiser to exist on the effective date of the assignment results, but is used for

the purpose of analysis.5

Extraordinary Assumption is defined as:

An assumption, directly related to a specific assignment, as of the effective date of the

assignment results, which, if found to be false, could alter the appraiser’s opinions or

conclusions.6

1 Page 21 – R/W Appraisal Standards and Specifications 2 The Dictionary of Real Estate Appraisal, Fifth Edition, Appraisal Institute, (Chicago, Illinois: 2010) 3 The Dictionary of Real Estate Appraisal, Fifth Edition, Appraisal Institute, (Chicago, Illinois: 2010), p. 78. 4 The Dictionary of Real Estate Appraisal, Fifth Edition, Appraisal Institute, (Chicago, Illinois: 2010) 5 USPAP 2012/13; Definitions, p. U-3 6 USPAP 2012/13; Definitions, p. U-3

MONTANDON FARLEY VALUATION SERVICES 4

SCOPE OF WORK

The scope of the appraisal required investigating sufficient data, relative to the subject, to derive

an opinion of value. The depth of the analysis was intended to be appropriate in relation to the

significance of the appraisal problem. We made a physical visit to the property on December

19, 2017 and have also gathered information on the neighborhood to determine its physical

features and recent development patterns. A search of public records was completed to ascertain

the current and historical assessment and ownership data regarding the property. The data

sources used to gather information for this report include, but are not limited to, the following:

• Planning and Zoning Department of Phoenix

• Maricopa County Assessor’s, Treasurer’s and Recorder’s websites

• CoStar Comps database

• Internal database

We have researched recent sales of land and improved industrial properties in the subject market

area. The most pertinent sales discovered have been analyzed in the Cost and Sales Comparison

Approaches. We have also gathered rental information on similar space in the market area for

use in the Income Approach. The indications from these three approaches have been reconciled

to a final value.

The subject’s current physical and legal condition, its background and history were researched

with all due diligence expected of professional real estate appraisers in the course of performing

appraisal services. The appraisers have attempted to analyze the property as seen through the

eyes of the hypothetical “most probable” buyer. The market area was examined to determine

existing and proposed inventory, demand and the marketability of properties comparable to the

subject.

This Appraisal Report is intended to comply with the reporting requirements set forth under

Standards Rule 2-2(a) of the Uniform Standards of Professional Appraisal Practice for an

Appraisal Report and the Federal Highway Administration (FHWA) Uniform Act, 49 CFR Part

24. The depth of discussion contained in this report is specific to the needs of the client and for

the intended use stated within this report.

MONTANDON FARLEY VALUATION SERVICES 5

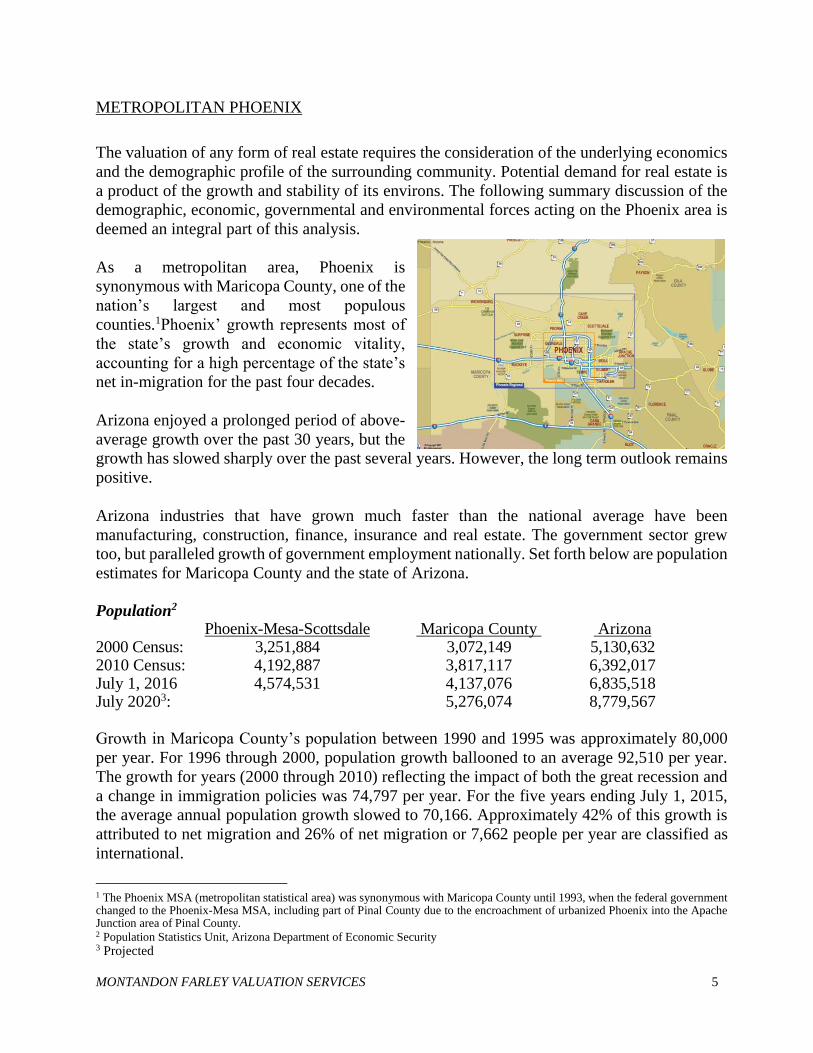

METROPOLITAN PHOENIX

The valuation of any form of real estate requires the consideration of the underlying economics

and the demographic profile of the surrounding community. Potential demand for real estate is

a product of the growth and stability of its environs. The following summary discussion of the

demographic, economic, governmental and environmental forces acting on the Phoenix area is

deemed an integral part of this analysis.

As a metropolitan area, Phoenix is

synonymous with Maricopa County, one of the

nation’s largest and most populous

counties.1Phoenix’ growth represents most of

the state’s growth and economic vitality,

accounting for a high percentage of the state’s

net in-migration for the past four decades.

Arizona enjoyed a prolonged period of above-

average growth over the past 30 years, but the

growth has slowed sharply over the past several years. However, the long term outlook remains

positive.

Arizona industries that have grown much faster than the national average have been

manufacturing, construction, finance, insurance and real estate. The government sector grew

too, but paralleled growth of government employment nationally. Set forth below are population

estimates for Maricopa County and the state of Arizona.

Population2 Phoenix-Mesa-Scottsdale Maricopa County Arizona 2000 Census: 3,251,884 3,072,149 5,130,632 2010 Census: 4,192,887 3,817,117 6,392,017 July 1, 2016 4,574,531 4,137,076 6,835,518 July 20203: 5,276,074 8,779,567 Growth in Maricopa County’s population between 1990 and 1995 was approximately 80,000

per year. For 1996 through 2000, population growth ballooned to an average 92,510 per year.

The growth for years (2000 through 2010) reflecting the impact of both the great recession and

a change in immigration policies was 74,797 per year. For the five years ending July 1, 2015,

the average annual population growth slowed to 70,166. Approximately 42% of this growth is

attributed to net migration and 26% of net migration or 7,662 people per year are classified as

international.

1 The Phoenix MSA (metropolitan statistical area) was synonymous with Maricopa County until 1993, when the federal government changed to the Phoenix-Mesa MSA, including part of Pinal County due to the encroachment of urbanized Phoenix into the Apache Junction area of Pinal County. 2 Population Statistics Unit, Arizona Department of Economic Security 3 Projected

MONTANDON FARLEY VALUATION SERVICES 6

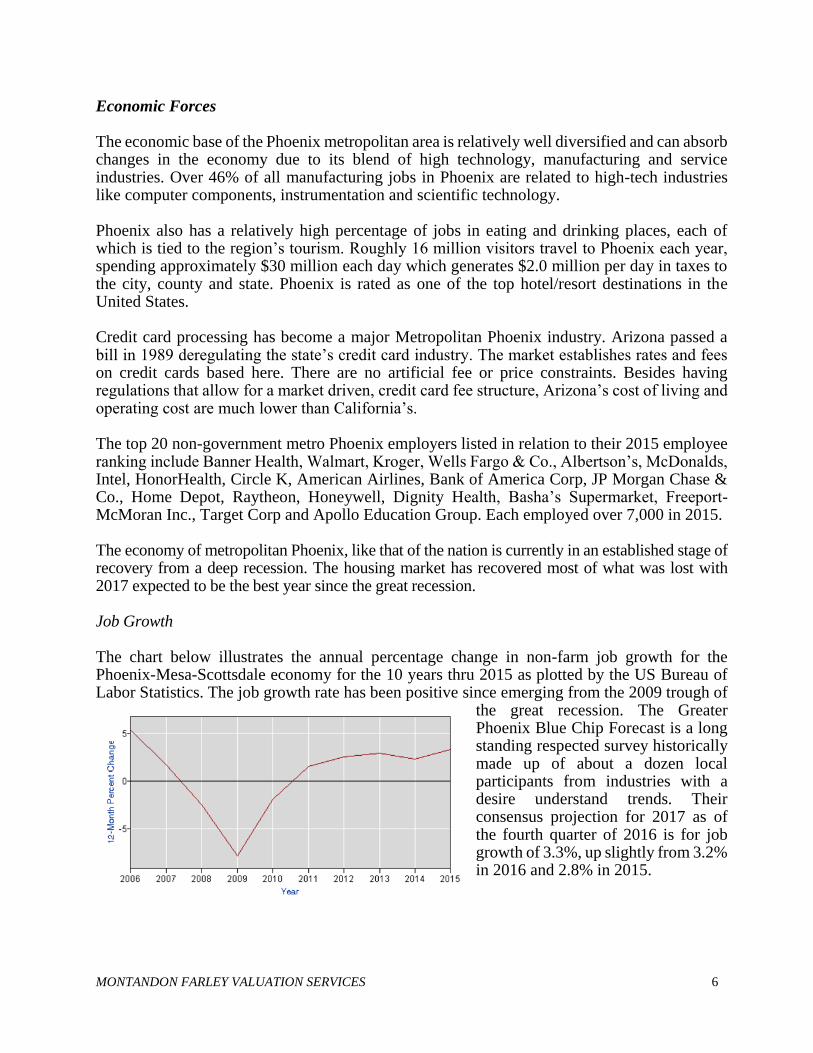

Economic Forces The economic base of the Phoenix metropolitan area is relatively well diversified and can absorb changes in the economy due to its blend of high technology, manufacturing and service industries. Over 46% of all manufacturing jobs in Phoenix are related to high-tech industries like computer components, instrumentation and scientific technology. Phoenix also has a relatively high percentage of jobs in eating and drinking places, each of which is tied to the region’s tourism. Roughly 16 million visitors travel to Phoenix each year, spending approximately $30 million each day which generates $2.0 million per day in taxes to the city, county and state. Phoenix is rated as one of the top hotel/resort destinations in the United States. Credit card processing has become a major Metropolitan Phoenix industry. Arizona passed a bill in 1989 deregulating the state’s credit card industry. The market establishes rates and fees on credit cards based here. There are no artificial fee or price constraints. Besides having regulations that allow for a market driven, credit card fee structure, Arizona’s cost of living and operating cost are much lower than California’s. The top 20 non-government metro Phoenix employers listed in relation to their 2015 employee ranking include Banner Health, Walmart, Kroger, Wells Fargo & Co., Albertson’s, McDonalds, Intel, HonorHealth, Circle K, American Airlines, Bank of America Corp, JP Morgan Chase & Co., Home Depot, Raytheon, Honeywell, Dignity Health, Basha’s Supermarket, Freeport-McMoran Inc., Target Corp and Apollo Education Group. Each employed over 7,000 in 2015. The economy of metropolitan Phoenix, like that of the nation is currently in an established stage of recovery from a deep recession. The housing market has recovered most of what was lost with 2017 expected to be the best year since the great recession. Job Growth The chart below illustrates the annual percentage change in non-farm job growth for the Phoenix-Mesa-Scottsdale economy for the 10 years thru 2015 as plotted by the US Bureau of Labor Statistics. The job growth rate has been positive since emerging from the 2009 trough of

the great recession. The Greater Phoenix Blue Chip Forecast is a long standing respected survey historically made up of about a dozen local participants from industries with a desire understand trends. Their consensus projection for 2017 as of the fourth quarter of 2016 is for job growth of 3.3%, up slightly from 3.2% in 2016 and 2.8% in 2015.

MONTANDON FARLEY VALUATION SERVICES 7

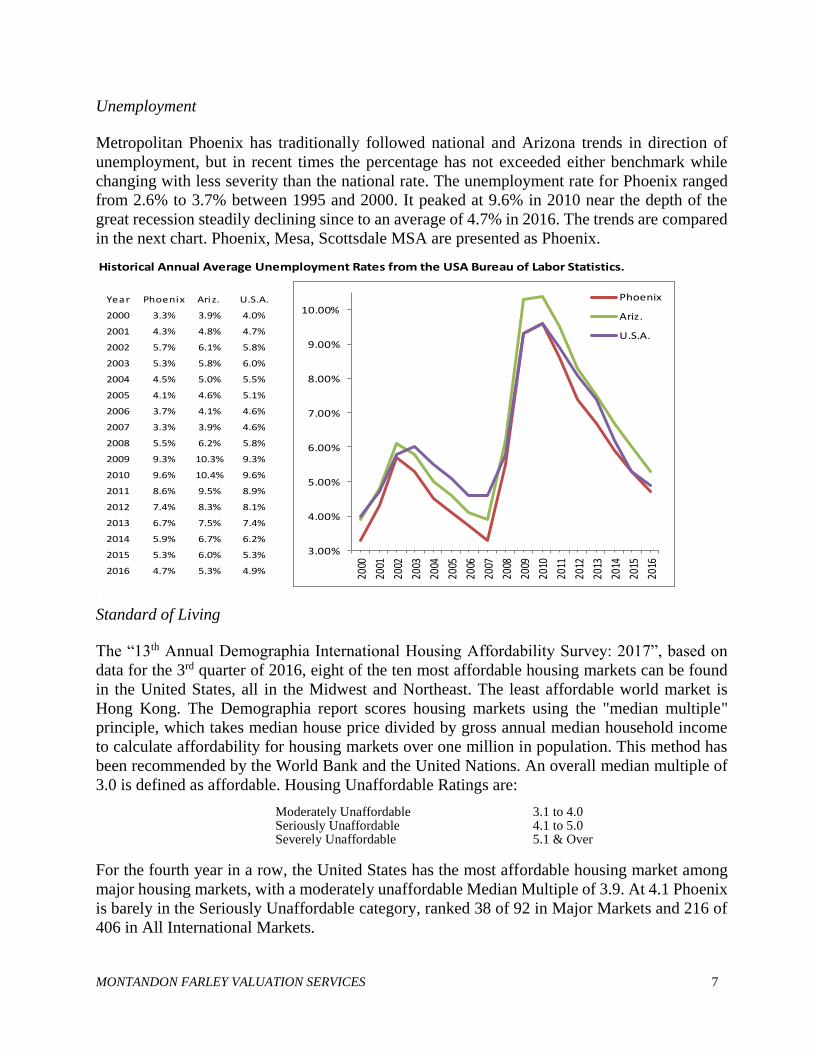

Unemployment Metropolitan Phoenix has traditionally followed national and Arizona trends in direction of

unemployment, but in recent times the percentage has not exceeded either benchmark while

changing with less severity than the national rate. The unemployment rate for Phoenix ranged

from 2.6% to 3.7% between 1995 and 2000. It peaked at 9.6% in 2010 near the depth of the

great recession steadily declining since to an average of 4.7% in 2016. The trends are compared

in the next chart. Phoenix, Mesa, Scottsdale MSA are presented as Phoenix.

Historical Annual Average Unemployment Rates from the USA Bureau of Labor Statistics.

Year Phoenix Ariz. U.S.A.

2000 3.3% 3.9% 4.0%

2001 4.3% 4.8% 4.7%

2002 5.7% 6.1% 5.8%

2003 5.3% 5.8% 6.0%

2004 4.5% 5.0% 5.5%

2005 4.1% 4.6% 5.1%

2006 3.7% 4.1% 4.6%

2007 3.3% 3.9% 4.6%

2008 5.5% 6.2% 5.8%

2009 9.3% 10.3% 9.3%

2010 9.6% 10.4% 9.6%

2011 8.6% 9.5% 8.9%

2012 7.4% 8.3% 8.1%

2013 6.7% 7.5% 7.4%

2014 5.9% 6.7% 6.2%

2015 5.3% 6.0% 5.3%

2016 4.7% 5.3% 4.9%

3.00%

4.00%

5.00%

6.00%

7.00%

8.00%

9.00%

10.00%

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

Phoenix

Ariz.

U.S.A.

Standard of Living The “13th Annual Demographia International Housing Affordability Survey: 2017”, based on

data for the 3rd quarter of 2016, eight of the ten most affordable housing markets can be found

in the United States, all in the Midwest and Northeast. The least affordable world market is

Hong Kong. The Demographia report scores housing markets using the "median multiple"

principle, which takes median house price divided by gross annual median household income

to calculate affordability for housing markets over one million in population. This method has

been recommended by the World Bank and the United Nations. An overall median multiple of

3.0 is defined as affordable. Housing Unaffordable Ratings are:

Moderately Unaffordable 3.1 to 4.0 Seriously Unaffordable 4.1 to 5.0 Severely Unaffordable 5.1 & Over

For the fourth year in a row, the United States has the most affordable housing market among

major housing markets, with a moderately unaffordable Median Multiple of 3.9. At 4.1 Phoenix

is barely in the Seriously Unaffordable category, ranked 38 of 92 in Major Markets and 216 of

406 in All International Markets.

MONTANDON FARLEY VALUATION SERVICES 8

Governmental Forces The city of Phoenix government is a city council form, with a mayor and a city manager. This

form is the most common among the larger communities in the metropolitan area. Most of the

major issues facing Metropolitan Phoenix city governments relate to problems caused by rapid

growth, such as: air and ground water pollution, freeway construction, annexations and urban

sprawl, preserving residential neighborhoods, ensuring an adequate water supply, flood control

and mass transit alternatives. Transportation

The Regional Transportation Authority was created in 1985. In October of 1985 voters approved

a half-cent sales tax increase to fund right-of-way acquisition and freeway thru 2005. Public-

transit was implemented in 2000 expanding bus and light rail service. In 2004 voters extended

the half cent county sales tax. In November of 2014, voters renewed the tax through 2025 by

approval of Proposition 400. In August 2015 voters approved Proposition 104, increasing the

state sales tax by 0.3 percent. The increase will pay for tripling of light rail miles, expanded bus

service, street re-pavement and transit infrastructure improvements.

Natural Resources National forests and some of the country’s largest county and city parks/preserves provide an

abundance of outdoor activities. Most of Phoenix’ growth, as well as its tourist industry, is

attributable to its climate, scenery and recreational opportunities. The area’s mild winter climate,

proximity to several major southwest cities, and the availability of water and developable land

has enabled the Phoenix area to become one of the fastest growing metropolitan areas in the

country.

The Phoenix area is characterized by a dry climate with a wide range between minimum and

maximum temperatures. June and July are the hottest months with an average maximum

temperature of 106.4F. December is the coldest month with an average minimum temperature

of 42.8F. February and March provide the most ideal temperatures and are the peak tourist

months. The average annual minimum temperature is 63.1F while the average maximum

temperature is 86.9F. Annual precipitation averages 8.4 inches.

Water is a precious commodity in the desert, but Phoenix has sufficient supplies to support its

continued growth. As more agriculture is eliminated, the net demand for water decreases even

with the burgeoning growth in population. One acre of typical residential growth requires about

one-third of the water of one acre of agricultural land.

Conclusion The Phoenix economy is relatively diverse, relying primarily on service, trade, manufacturing

and government sectors as major employers. The near-term outlook for the individual real estate

sectors and the economy as a whole is for slow steady growth.

MONTANDON FARLEY VALUATION SERVICES 9

Metropolitan Phoenix Map

MONTANDON FARLEY VALUATION SERVICES 10

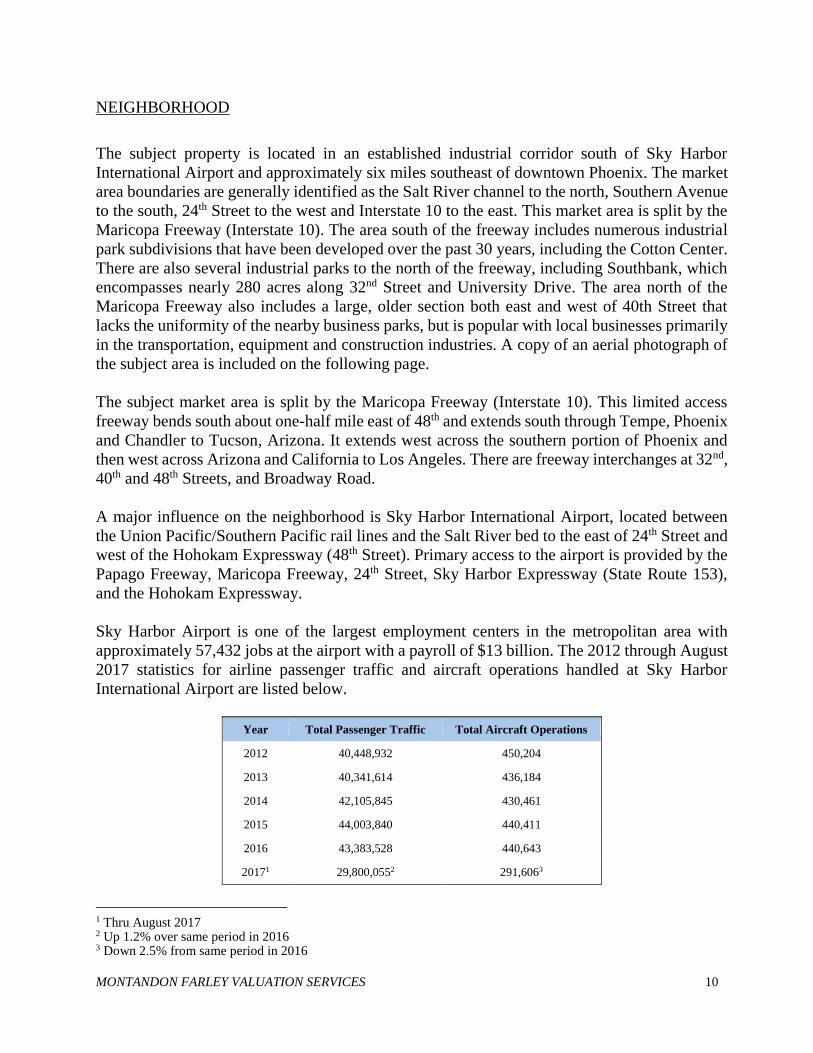

NEIGHBORHOOD

The subject property is located in an established industrial corridor south of Sky Harbor

International Airport and approximately six miles southeast of downtown Phoenix. The market

area boundaries are generally identified as the Salt River channel to the north, Southern Avenue

to the south, 24th Street to the west and Interstate 10 to the east. This market area is split by the

Maricopa Freeway (Interstate 10). The area south of the freeway includes numerous industrial

park subdivisions that have been developed over the past 30 years, including the Cotton Center.

There are also several industrial parks to the north of the freeway, including Southbank, which

encompasses nearly 280 acres along 32nd Street and University Drive. The area north of the

Maricopa Freeway also includes a large, older section both east and west of 40th Street that

lacks the uniformity of the nearby business parks, but is popular with local businesses primarily

in the transportation, equipment and construction industries. A copy of an aerial photograph of

the subject area is included on the following page.

The subject market area is split by the Maricopa Freeway (Interstate 10). This limited access

freeway bends south about one-half mile east of 48th and extends south through Tempe, Phoenix

and Chandler to Tucson, Arizona. It extends west across the southern portion of Phoenix and

then west across Arizona and California to Los Angeles. There are freeway interchanges at 32nd,

40th and 48th Streets, and Broadway Road.

A major influence on the neighborhood is Sky Harbor International Airport, located between

the Union Pacific/Southern Pacific rail lines and the Salt River bed to the east of 24th Street and

west of the Hohokam Expressway (48th Street). Primary access to the airport is provided by the

Sky Harbor Airport is one of the largest employment centers in the metropolitan area with

approximately 57,432 jobs at the airport with a payroll of $13 billion. The 2012 through August

2017 statistics for airline passenger traffic and aircraft operations handled at Sky Harbor

International Airport are listed below.

Year Total Passenger Traffic Total Aircraft Operations

2012 40,448,932 450,204

2013 40,341,614 436,184

2014 42,105,845 430,461

2015 44,003,840 440,411

2016 43,383,528 440,643

20171 29,800,0552 291,6063

1 Thru August 2017 2 Up 1.2% over same period in 2016 3 Down 2.5% from same period in 2016

MONTANDON FARLEY VALUATION SERVICES 11

Aerial Photograph

MONTANDON FARLEY VALUATION SERVICES 12

The major development to the north of the Interstate 10 freeway in this market area is Southbank.

This 280-acre business park is situated between Interstate 10 (Maricopa Freeway) on the south

and the Salt River on the north, east and west of University Drive. Southbank was developed in

the mid 1980’s by Denro Limited of Phoenix and was planned for over one million square feet

of industrial, office and retail development. The business park is now approximately 85 percent

developed. The majority of the development is in the subdivision's north section, including a

variety of hotels and flex industrial buildings. The hotels include a 163-room Radisson Hotel, a

114 room Holiday Inn Express, a 101 room Extended Stay America motel, and a 93 room Hilton

Garden Inn. Some of the industrial projects include Hewson Southbank, a five-building,

110,318-square-foot office and light industrial complex; the 160,000-square-foot Arizona

Design Center; the Corporate Center at Southbank, a 224,408-square-foot office building; the

100,000-square-foot former Century Bank office building; and a 122,608-square-foot, multi-

tenant, back-office building. In addition, Colonial Development has constructed a 179,910

square foot project. This is the first speculative project built in Southbank in the past ten years.

The Colonial Center at Southbank includes five buildings ranging in size from 31,383 to 45,557

square feet which were completed in 2007.

The dominant recent development to the south of the freeway is Cotton Center. This developing

business park contains approximately 281 gross acres and is bounded on the east by 48th Street,

on the west by 40th Street, on the north by Broadway Road and on the south by Roeser Road.

This property was formerly an experimental cotton farm that was owned and operated by the

University of Arizona – hence the Cotton Center project name. The property was sold via a

sealed-bid auction in September 1997 for $40,000,000, or about $3.28 per square foot without

infrastructure or offsite improvements. Marketing of Cotton Center as sites for a variety of

business park uses began in mid-1998 and a variety of national and regional developers such as

Opus West, The Koll Company, Douglas Allred Company and Carlson Real Estate Company have

built projects within the Cotton Center. The project is sold out and nearly all the lots have been

developed.

MONTANDON FARLEY VALUATION SERVICES 13

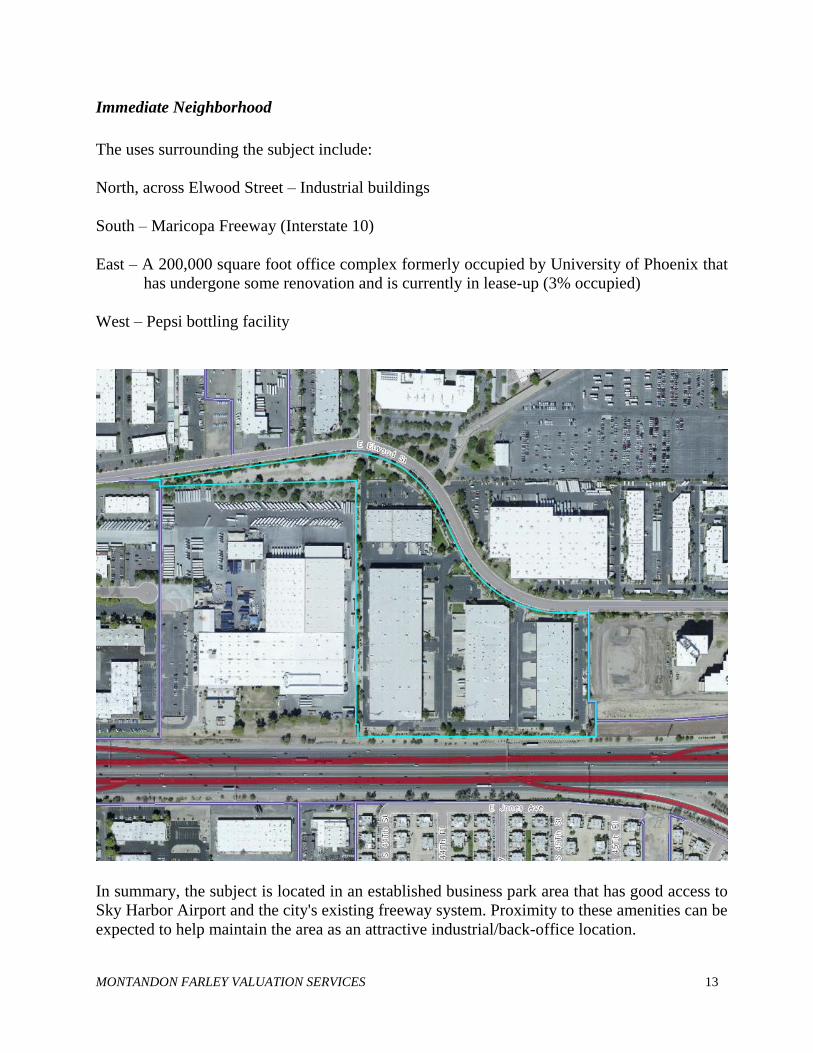

Immediate Neighborhood

The uses surrounding the subject include:

North, across Elwood Street – Industrial buildings

South – Maricopa Freeway (Interstate 10)

East – A 200,000 square foot office complex formerly occupied by University of Phoenix that

has undergone some renovation and is currently in lease-up (3% occupied)

West – Pepsi bottling facility

In summary, the subject is located in an established business park area that has good access to

Sky Harbor Airport and the city's existing freeway system. Proximity to these amenities can be

expected to help maintain the area as an attractive industrial/back-office location.

MONTANDON FARLEY VALUATION SERVICES 14

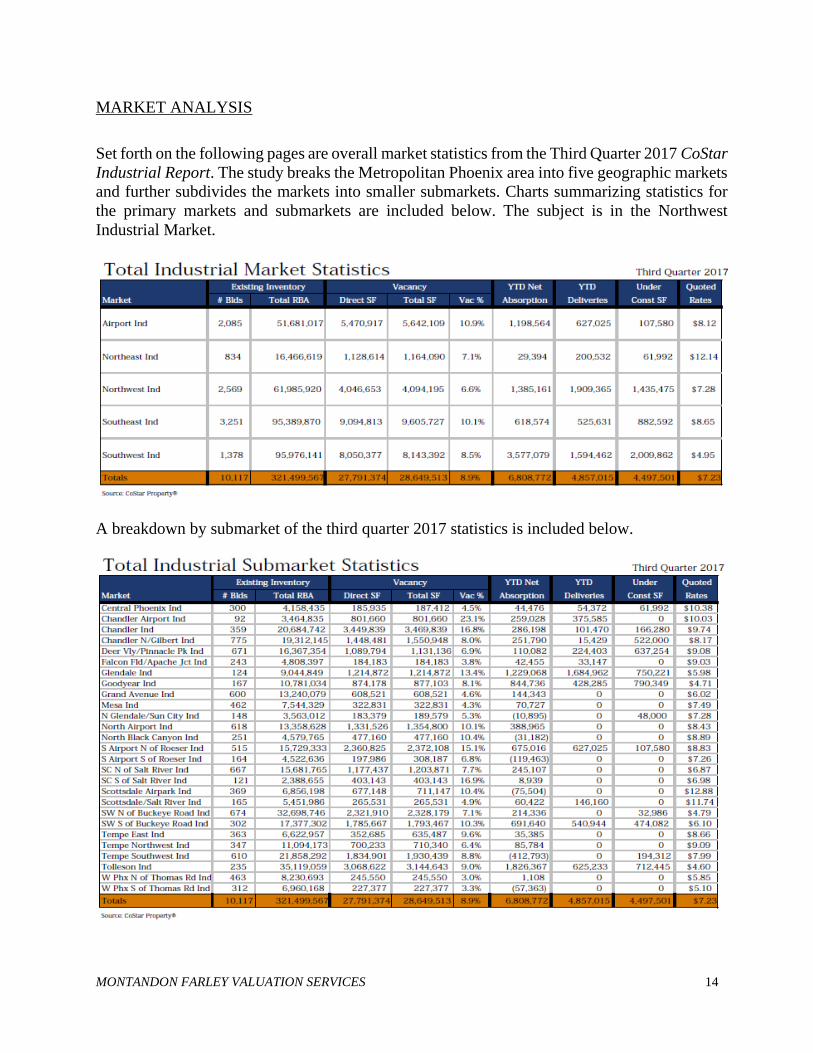

MARKET ANALYSIS

Set forth on the following pages are overall market statistics from the Third Quarter 2017 CoStar

Industrial Report. The study breaks the Metropolitan Phoenix area into five geographic markets

and further subdivides the markets into smaller submarkets. Charts summarizing statistics for

the primary markets and submarkets are included below. The subject is in the Northwest

Industrial Market.

A breakdown by submarket of the third quarter 2017 statistics is included below.

MONTANDON FARLEY VALUATION SERVICES 15

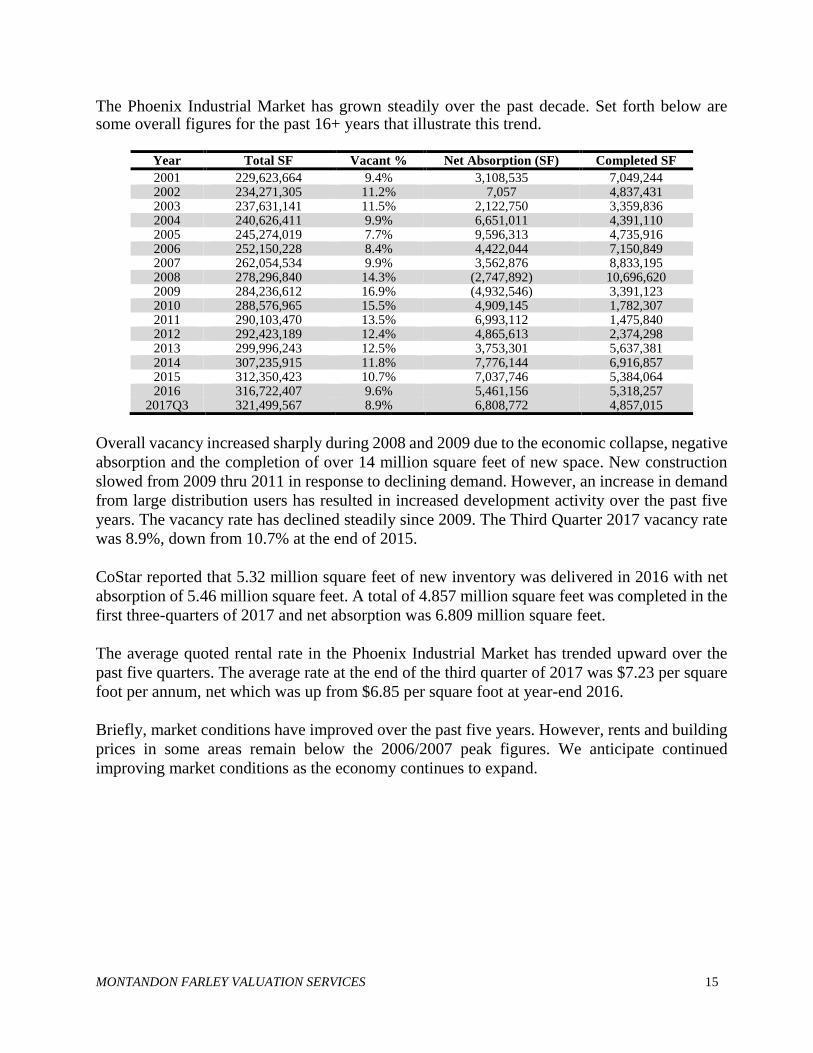

The Phoenix Industrial Market has grown steadily over the past decade. Set forth below are some overall figures for the past 16+ years that illustrate this trend.

Year Total SF Vacant % Net Absorption (SF) Completed SF

Overall vacancy increased sharply during 2008 and 2009 due to the economic collapse, negative

absorption and the completion of over 14 million square feet of new space. New construction

slowed from 2009 thru 2011 in response to declining demand. However, an increase in demand

from large distribution users has resulted in increased development activity over the past five

years. The vacancy rate has declined steadily since 2009. The Third Quarter 2017 vacancy rate

was 8.9%, down from 10.7% at the end of 2015.

CoStar reported that 5.32 million square feet of new inventory was delivered in 2016 with net

absorption of 5.46 million square feet. A total of 4.857 million square feet was completed in the

first three-quarters of 2017 and net absorption was 6.809 million square feet.

The average quoted rental rate in the Phoenix Industrial Market has trended upward over the

past five quarters. The average rate at the end of the third quarter of 2017 was $7.23 per square

foot per annum, net which was up from $6.85 per square foot at year-end 2016.

Briefly, market conditions have improved over the past five years. However, rents and building

prices in some areas remain below the 2006/2007 peak figures. We anticipate continued

improving market conditions as the economy continues to expand.

MONTANDON FARLEY VALUATION SERVICES 16

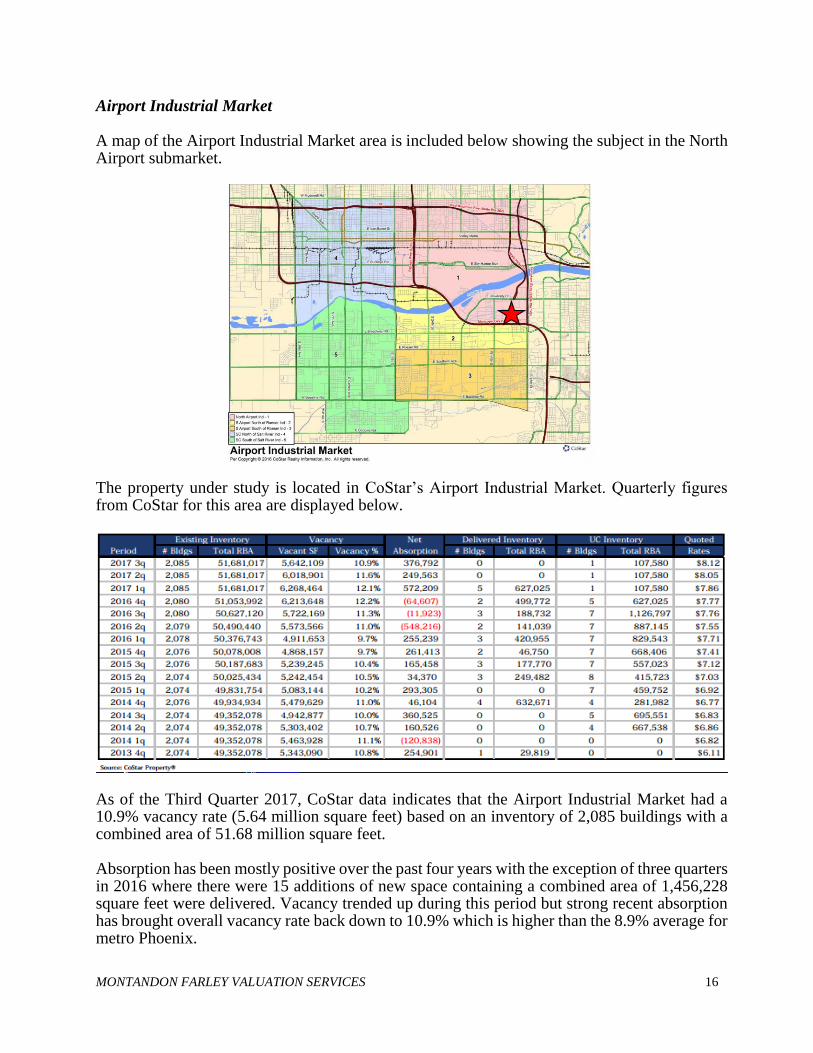

Airport Industrial Market A map of the Airport Industrial Market area is included below showing the subject in the North Airport submarket.

The property under study is located in CoStar’s Airport Industrial Market. Quarterly figures from CoStar for this area are displayed below.

As of the Third Quarter 2017, CoStar data indicates that the Airport Industrial Market had a 10.9% vacancy rate (5.64 million square feet) based on an inventory of 2,085 buildings with a combined area of 51.68 million square feet. Absorption has been mostly positive over the past four years with the exception of three quarters in 2016 where there were 15 additions of new space containing a combined area of 1,456,228 square feet were delivered. Vacancy trended up during this period but strong recent absorption has brought overall vacancy rate back down to 10.9% which is higher than the 8.9% average for metro Phoenix.

MONTANDON FARLEY VALUATION SERVICES 17

CoStar data indicate that average quoted rental rates have trended upward over the past four years which is due to the completion of new space. There is currently one building of 108,694 square feet currently under construction in this market area.

After a surge in speculative construction activity in this market area during 2016 conditions

continue to be competitive for the near term given the amount of new space. Brokers report

projects with freeway exposure are in the highest demand with average lease rates up over the

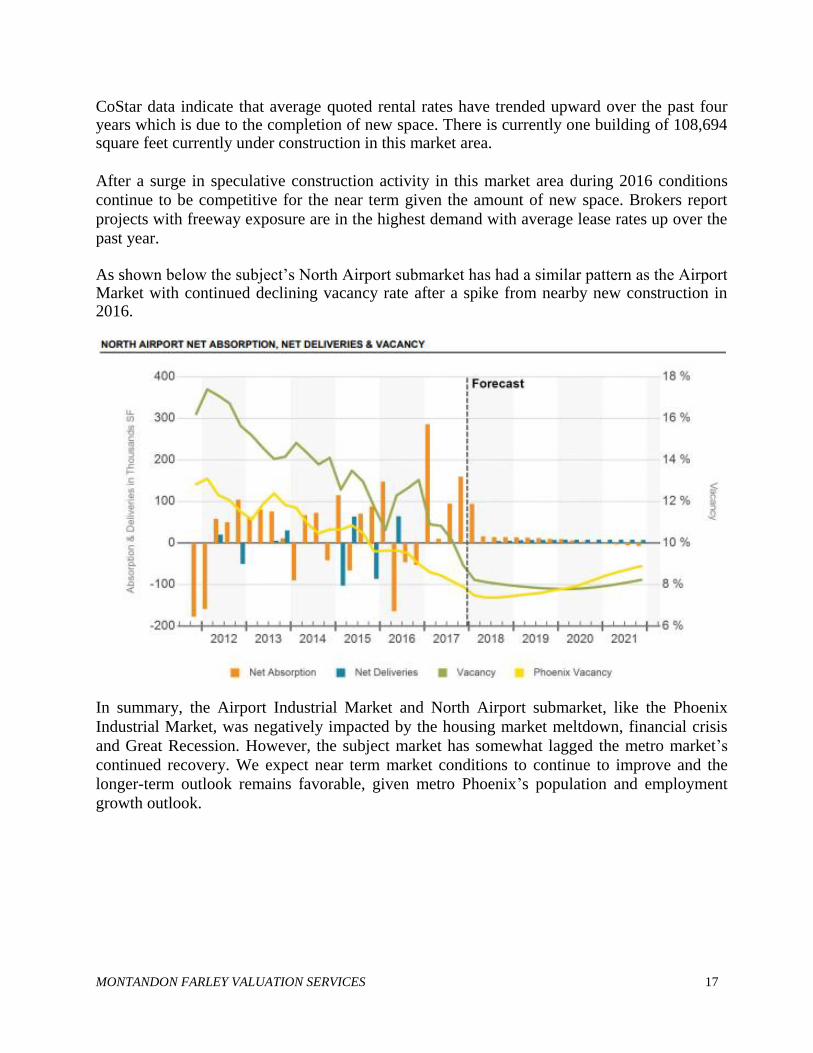

past year. As shown below the subject’s North Airport submarket has had a similar pattern as the Airport Market with continued declining vacancy rate after a spike from nearby new construction in 2016.

In summary, the Airport Industrial Market and North Airport submarket, like the Phoenix

Industrial Market, was negatively impacted by the housing market meltdown, financial crisis

and Great Recession. However, the subject market has somewhat lagged the metro market’s

continued recovery. We expect near term market conditions to continue to improve and the

longer-term outlook remains favorable, given metro Phoenix’s population and employment

growth outlook.

MONTANDON FARLEY VALUATION SERVICES 18

PROPERTY DATA

Property History:

The owner of record is

Arizona Department of Transportation (ADOT)

Due to proposed expansion of Interstate 10, ADOT acquired the property via condemnation in

January 2011 along with an office building adjacent east (since demolished) that is not part of

the subject. Market conditions have improved since the acquisition. ADOT intends to dispose

of the property but will retain the southern 60 to 75 feet for freeway expansion. The subject

property excludes this southern 60 to 75 feet that will utilized for freeway right of way. The new

right of way at the subject eliminates previously existing driveway/fire lane. In order to

accommodate fire lane and set back requirements the south 50 to 60 feet of the subject’s

Buildings 1, 2 and 3 will need to be demolished and reconstructed with a new configuration

(less building area) that complies with legal and practical requirements. We are unaware of any

recent attempts to market the property or of any unsolicited offers to purchase. However, ADOT

intends to dispose of the property and reportedly has had interest from prospective buyers.

Accordingly, ADOT expects more than one formal offer triggering a public auction for the

subject in the near future.

Site Data:

Area: The site has 2,400 feet of frontage on Elwood Street, 1,090 of frontage on Interstate 10 Freeway and contains 926,979 square feet, or 21.28 acres.

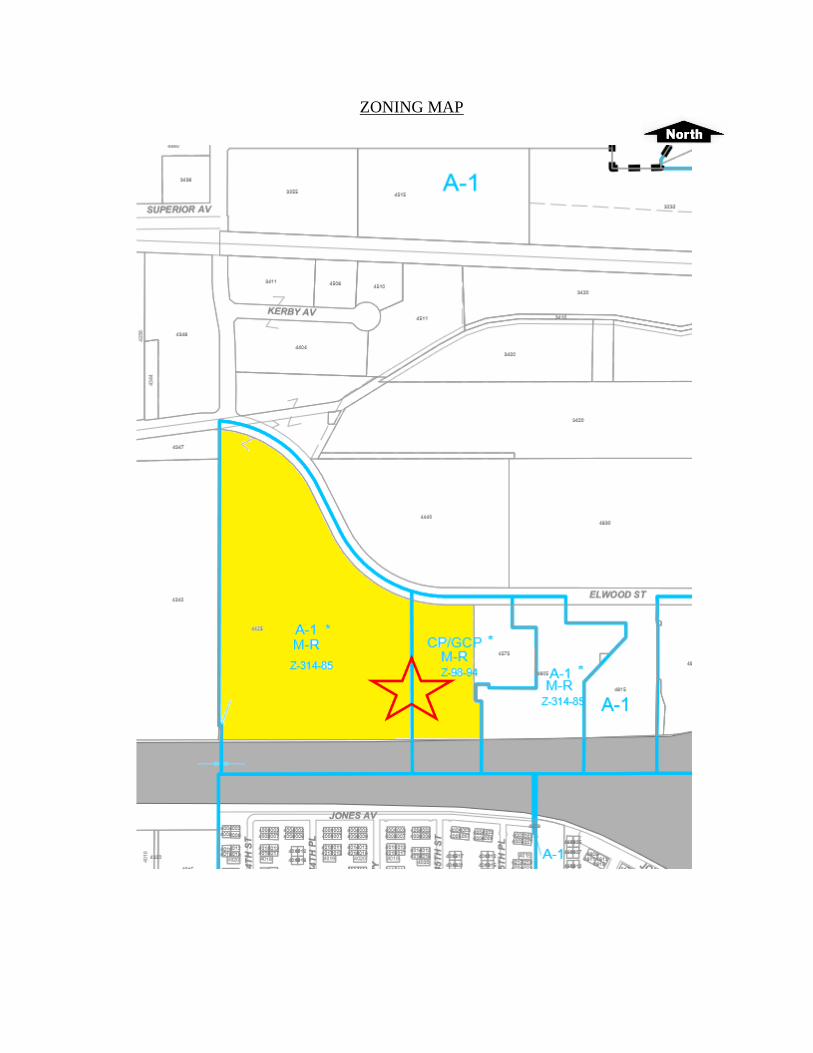

Zoning:

The eastern portion of the property is zoned CP/GCP, Commerce Park/General Commerce Park,

and the western portion is zoned, A-1, Light Industrial, by the City of Phoenix. The CP/GCP,

Commerce Park/General Commerce Park district is designed for commerce, service and

employment activities to serve the needs of the community presenting a desirable appearance

toward public streets and not offensive to nearby commercial or residential uses. The General

Commerce Park Option allows a broad range of manufacturing, warehousing, distribution and

support retail sales/services. Permitted uses include offices of all types, research labs,

medical/dental labs, pharmacy, restaurants, churches, motels, hotels, and public buildings. The

A-1, Light Industrial zoning district is designed to serve the needs of the community for

industrial activity not offensive to nearby commercial and residential uses. Permitted uses in the

A-1 district include manufacturing, storage yards and all non-residential uses permitted in the

RE-24, R-3, R-4, R-5, C-1, C-2 and C-3 districts. The existing industrial project is to the best of

our knowledge a legal, conforming use. A zoning map is included in the addendum.

MONTANDON FARLEY VALUATION SERVICES 19

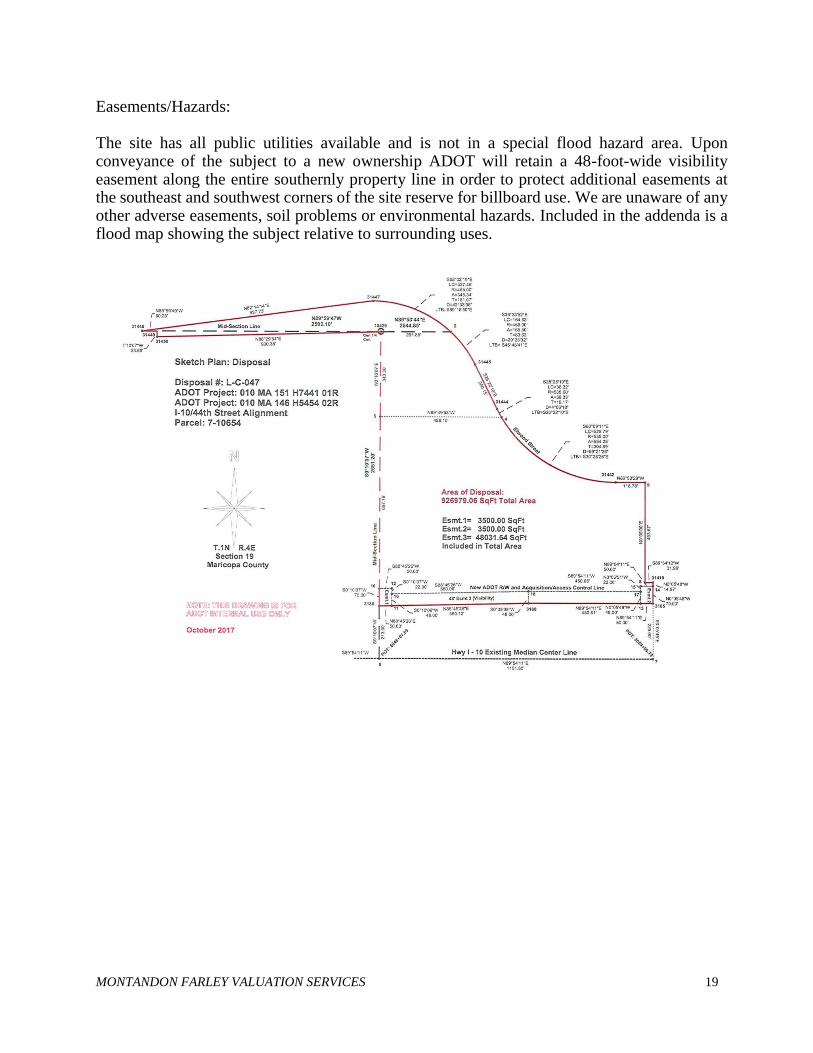

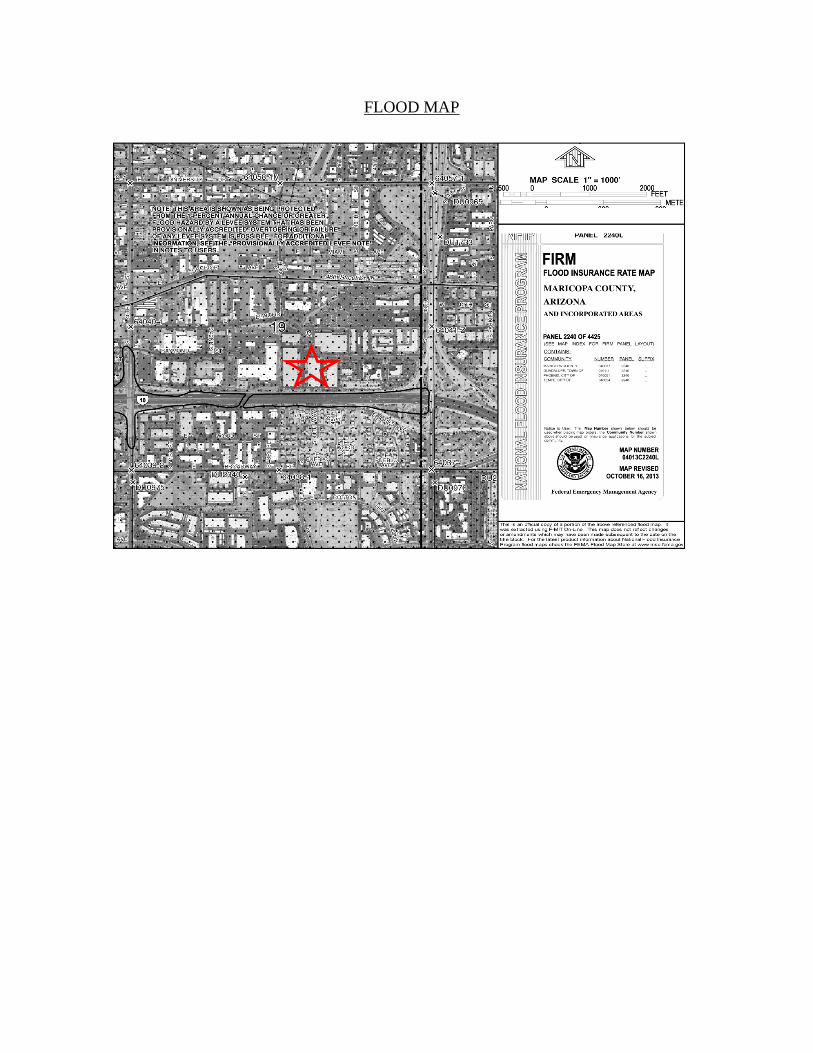

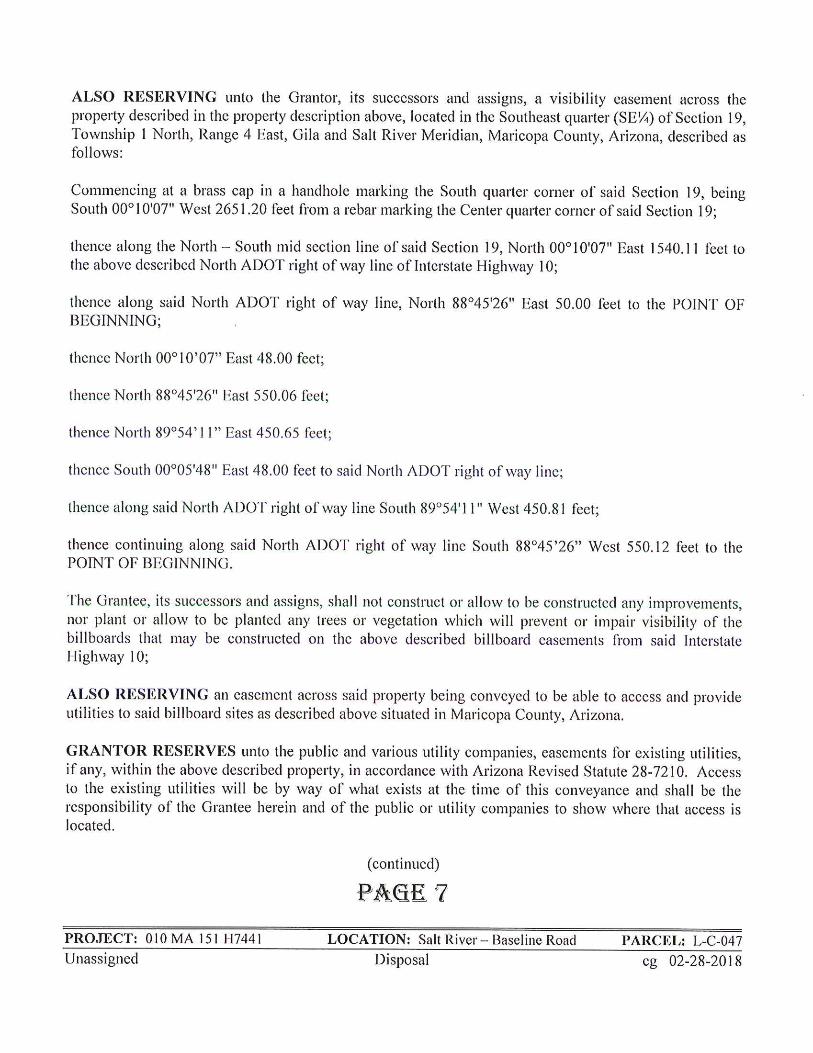

Easements/Hazards: The site has all public utilities available and is not in a special flood hazard area. Upon conveyance of the subject to a new ownership ADOT will retain a 48-foot-wide visibility easement along the entire southernly property line in order to protect additional easements at the southeast and southwest corners of the site reserve for billboard use. We are unaware of any other adverse easements, soil problems or environmental hazards. Included in the addenda is a flood map showing the subject relative to surrounding uses.

MONTANDON FARLEY VALUATION SERVICES 20

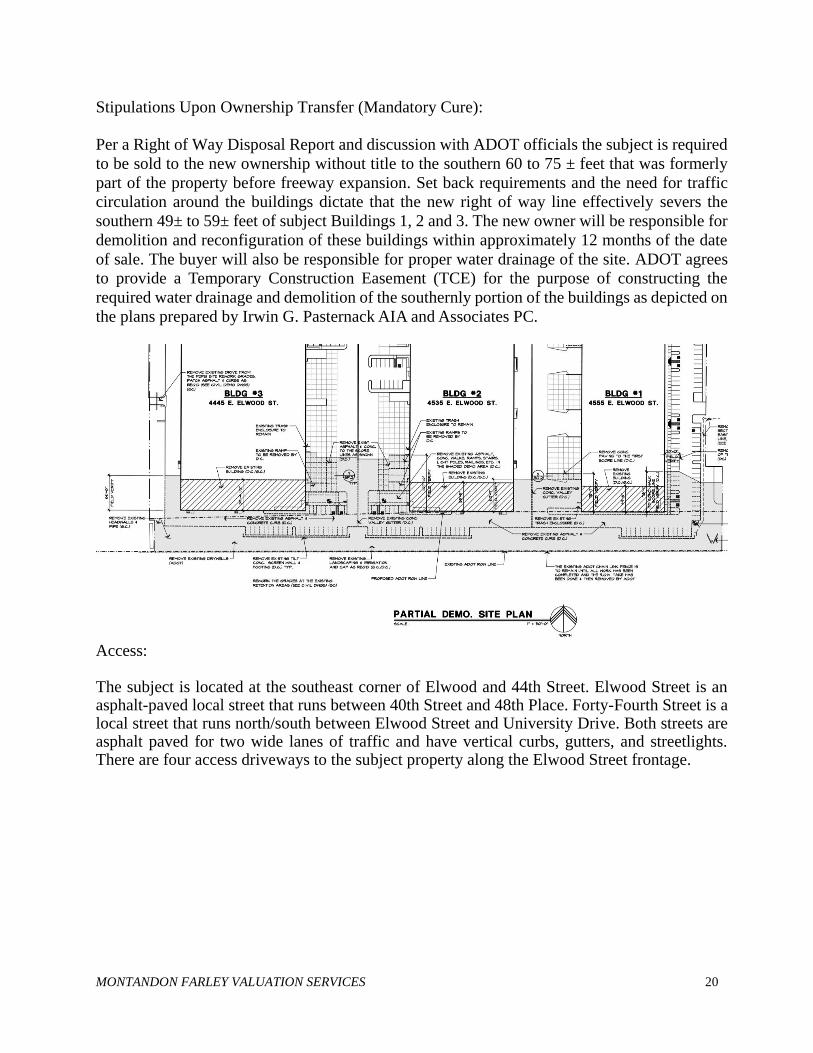

Stipulations Upon Ownership Transfer (Mandatory Cure): Per a Right of Way Disposal Report and discussion with ADOT officials the subject is required

to be sold to the new ownership without title to the southern 60 to 75 ± feet that was formerly

part of the property before freeway expansion. Set back requirements and the need for traffic

circulation around the buildings dictate that the new right of way line effectively severs the

southern 49± to 59± feet of subject Buildings 1, 2 and 3. The new owner will be responsible for

demolition and reconfiguration of these buildings within approximately 12 months of the date

of sale. The buyer will also be responsible for proper water drainage of the site. ADOT agrees

to provide a Temporary Construction Easement (TCE) for the purpose of constructing the

required water drainage and demolition of the southernly portion of the buildings as depicted on

the plans prepared by Irwin G. Pasternack AIA and Associates PC.

Access: The subject is located at the southeast corner of Elwood and 44th Street. Elwood Street is an asphalt-paved local street that runs between 40th Street and 48th Place. Forty-Fourth Street is a local street that runs north/south between Elwood Street and University Drive. Both streets are asphalt paved for two wide lanes of traffic and have vertical curbs, gutters, and streetlights. There are four access driveways to the subject property along the Elwood Street frontage.

MONTANDON FARLEY VALUATION SERVICES 21

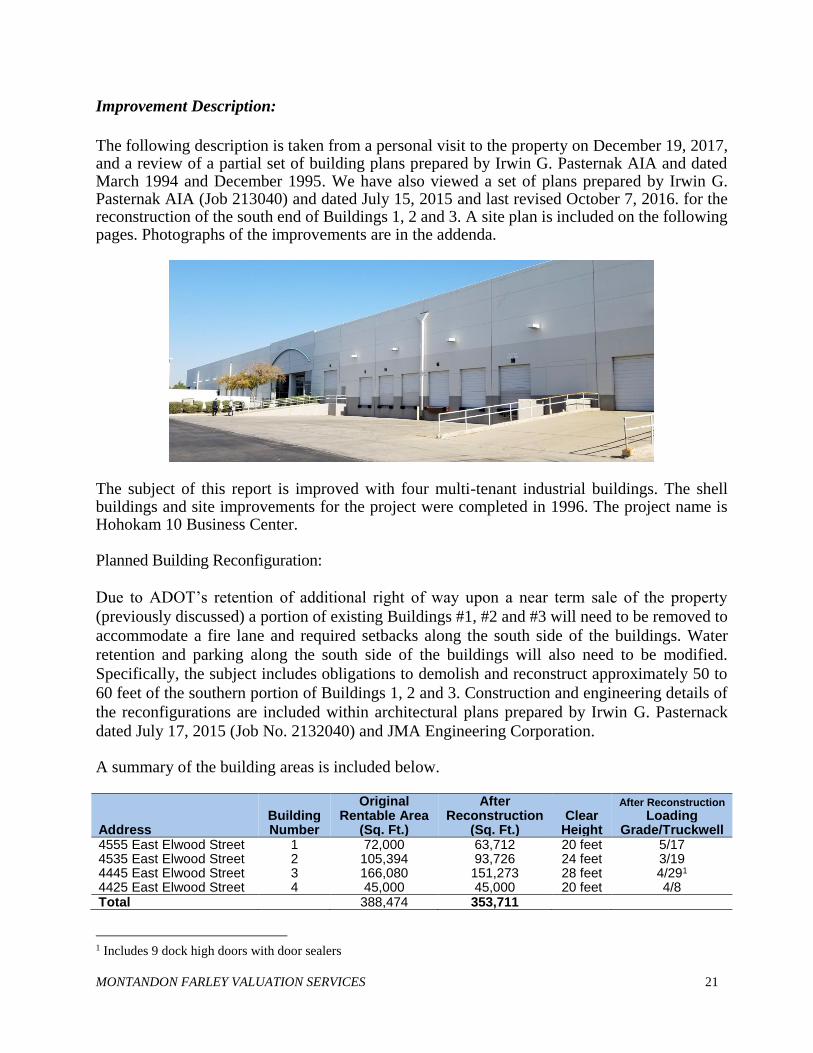

Improvement Description:

The following description is taken from a personal visit to the property on December 19, 2017, and a review of a partial set of building plans prepared by Irwin G. Pasternak AIA and dated March 1994 and December 1995. We have also viewed a set of plans prepared by Irwin G. Pasternak AIA (Job 213040) and dated July 15, 2015 and last revised October 7, 2016. for the reconstruction of the south end of Buildings 1, 2 and 3. A site plan is included on the following pages. Photographs of the improvements are in the addenda.

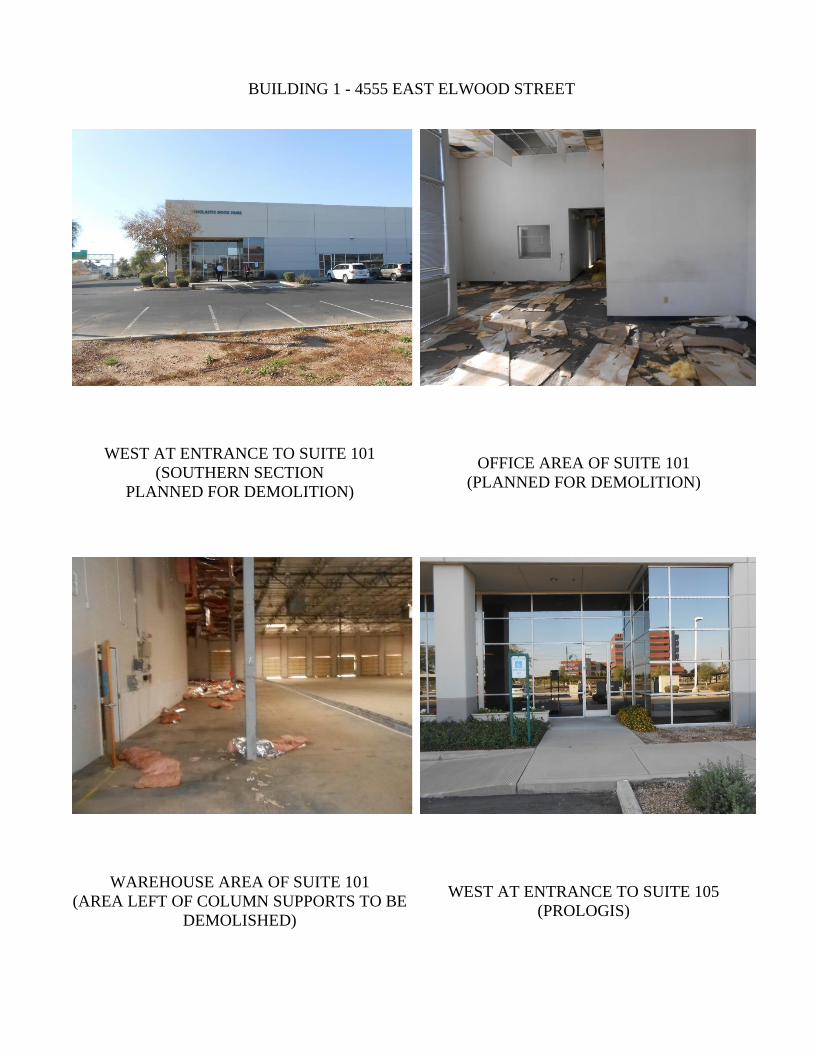

The subject of this report is improved with four multi-tenant industrial buildings. The shell buildings and site improvements for the project were completed in 1996. The project name is Hohokam 10 Business Center. Planned Building Reconfiguration: Due to ADOT’s retention of additional right of way upon a near term sale of the property

(previously discussed) a portion of existing Buildings #1, #2 and #3 will need to be removed to

accommodate a fire lane and required setbacks along the south side of the buildings. Water

retention and parking along the south side of the buildings will also need to be modified.

Specifically, the subject includes obligations to demolish and reconstruct approximately 50 to

60 feet of the southern portion of Buildings 1, 2 and 3. Construction and engineering details of

the reconfigurations are included within architectural plans prepared by Irwin G. Pasternack

dated July 17, 2015 (Job No. 2132040) and JMA Engineering Corporation. A summary of the building areas is included below.

Address Building Number

Original Rentable Area

(Sq. Ft.)

After Reconstruction

(Sq. Ft.) Clear

Height

After Reconstruction

Loading Grade/Truckwell

4555 East Elwood Street 1 72,000 63,712 20 feet 5/17 4535 East Elwood Street 2 105,394 93,726 24 feet 3/19 4445 East Elwood Street 3 166,080 151,273 28 feet 4/291 4425 East Elwood Street 4 45,000 45,000 20 feet 4/8 Total 388,474 353,711

1 Includes 9 dock high doors with door sealers

MONTANDON FARLEY VALUATION SERVICES 22

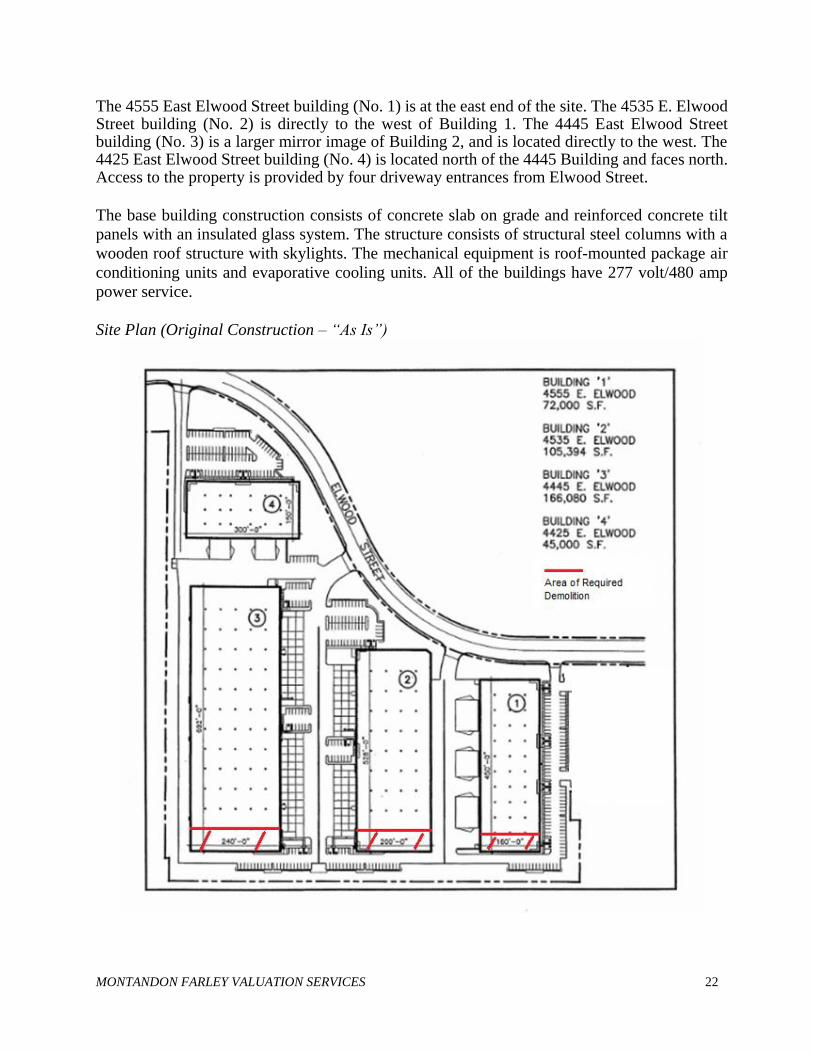

The 4555 East Elwood Street building (No. 1) is at the east end of the site. The 4535 E. Elwood Street building (No. 2) is directly to the west of Building 1. The 4445 East Elwood Street building (No. 3) is a larger mirror image of Building 2, and is located directly to the west. The 4425 East Elwood Street building (No. 4) is located north of the 4445 Building and faces north. Access to the property is provided by four driveway entrances from Elwood Street.

The base building construction consists of concrete slab on grade and reinforced concrete tilt

panels with an insulated glass system. The structure consists of structural steel columns with a

wooden roof structure with skylights. The mechanical equipment is roof-mounted package air

conditioning units and evaporative cooling units. All of the buildings have 277 volt/480 amp

power service.

Site Plan (Original Construction – “As Is”)

MONTANDON FARLEY VALUATION SERVICES 23

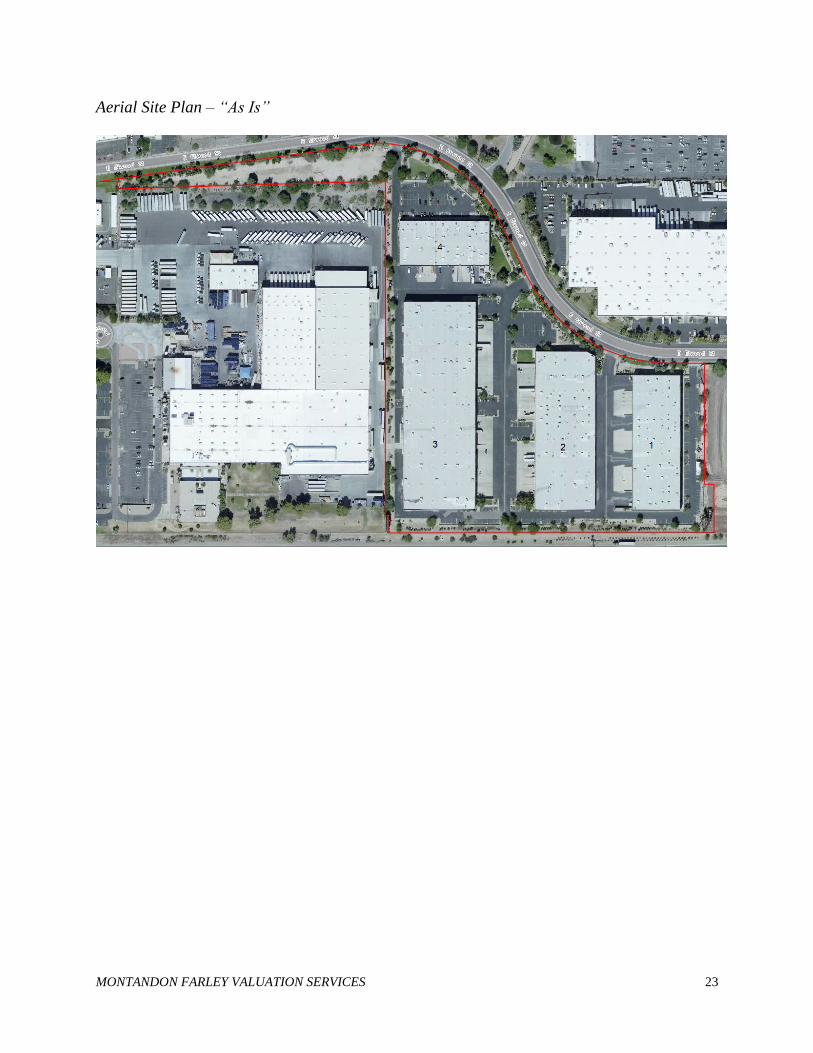

Aerial Site Plan – “As Is”

MONTANDON FARLEY VALUATION SERVICES 24

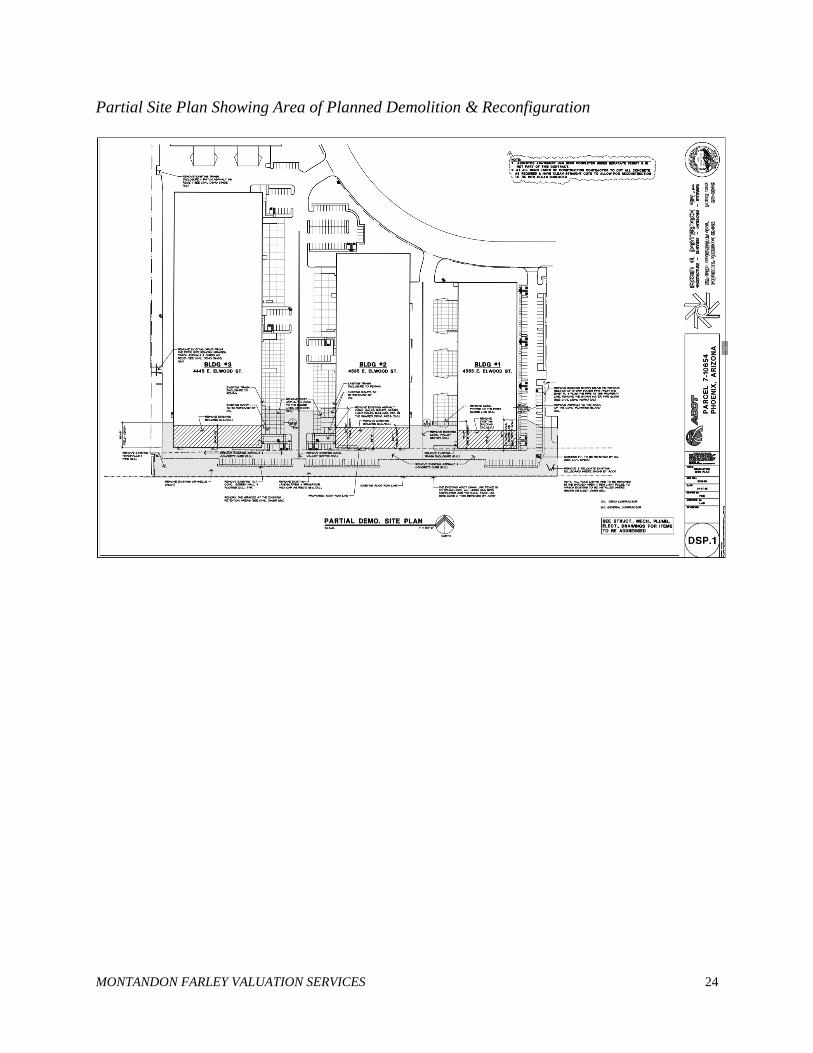

Partial Site Plan Showing Area of Planned Demolition & Reconfiguration

MONTANDON FARLEY VALUATION SERVICES 25

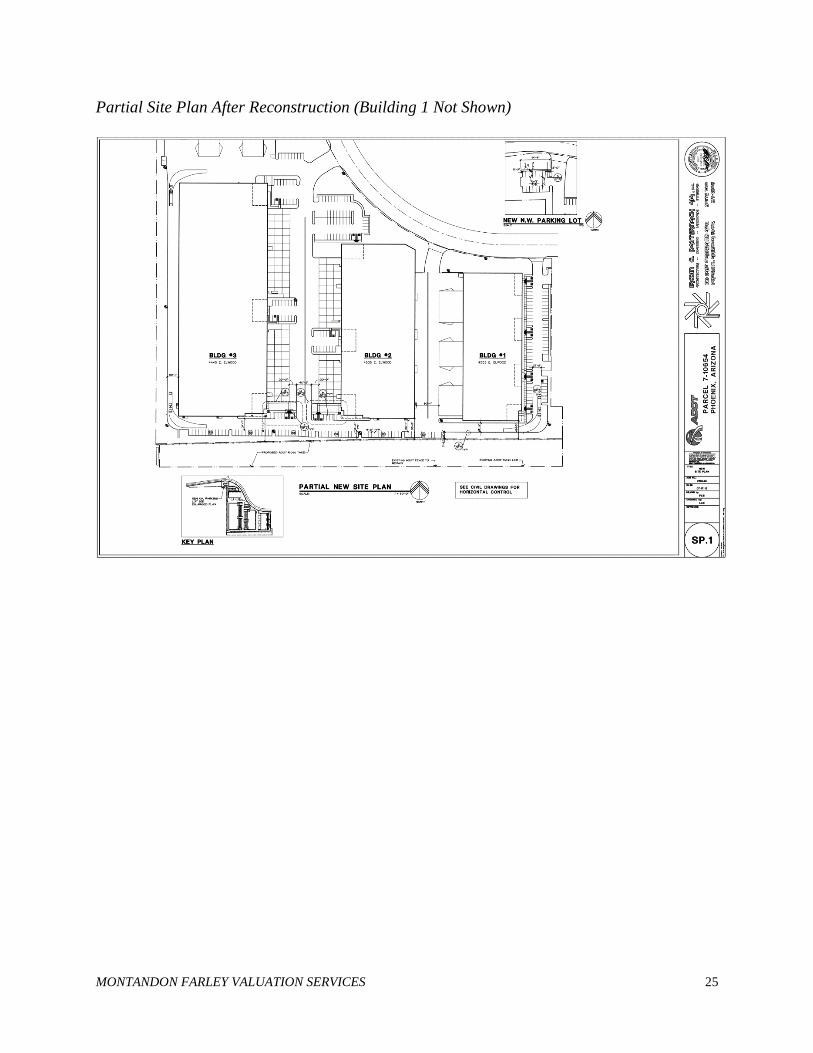

Partial Site Plan After Reconstruction (Building 1 Not Shown)

MONTANDON FARLEY VALUATION SERVICES 26

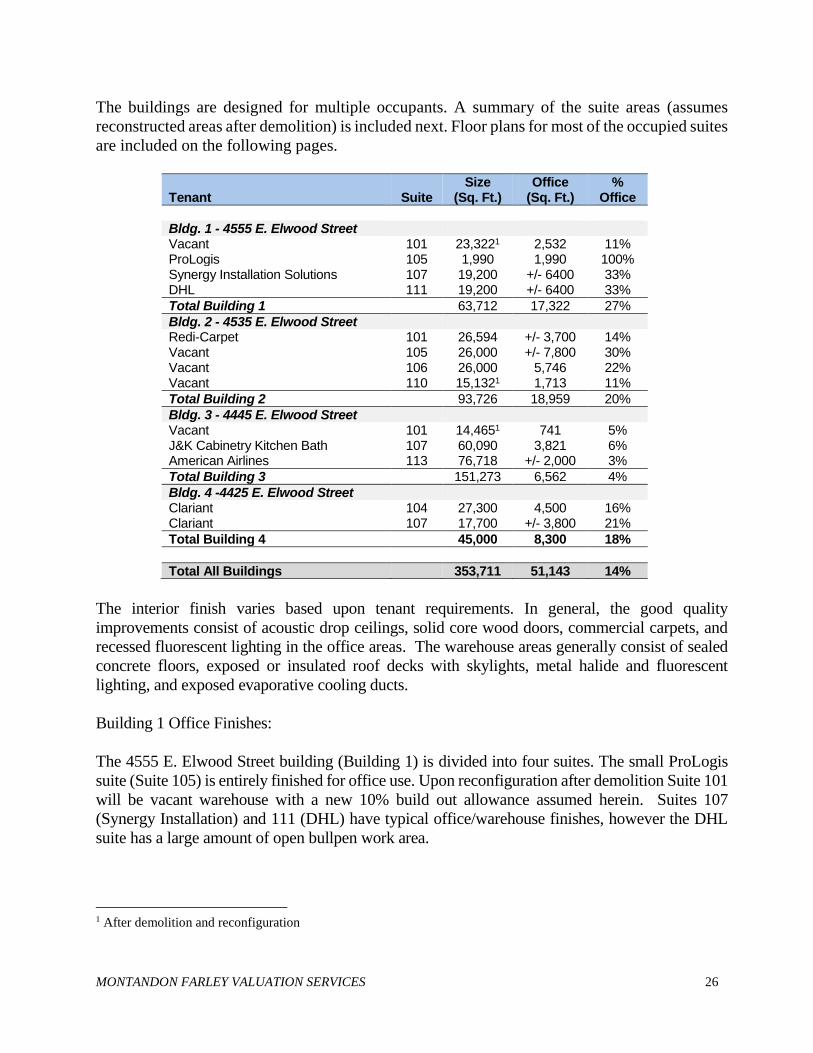

The buildings are designed for multiple occupants. A summary of the suite areas (assumes

reconstructed areas after demolition) is included next. Floor plans for most of the occupied suites

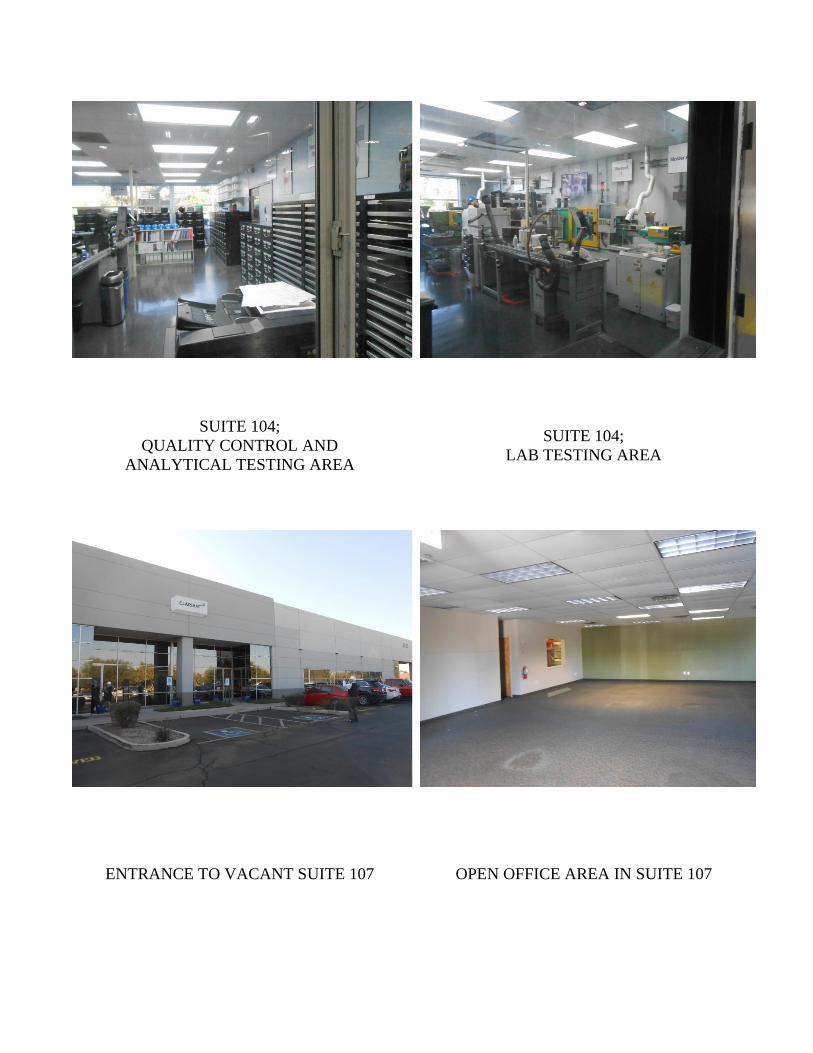

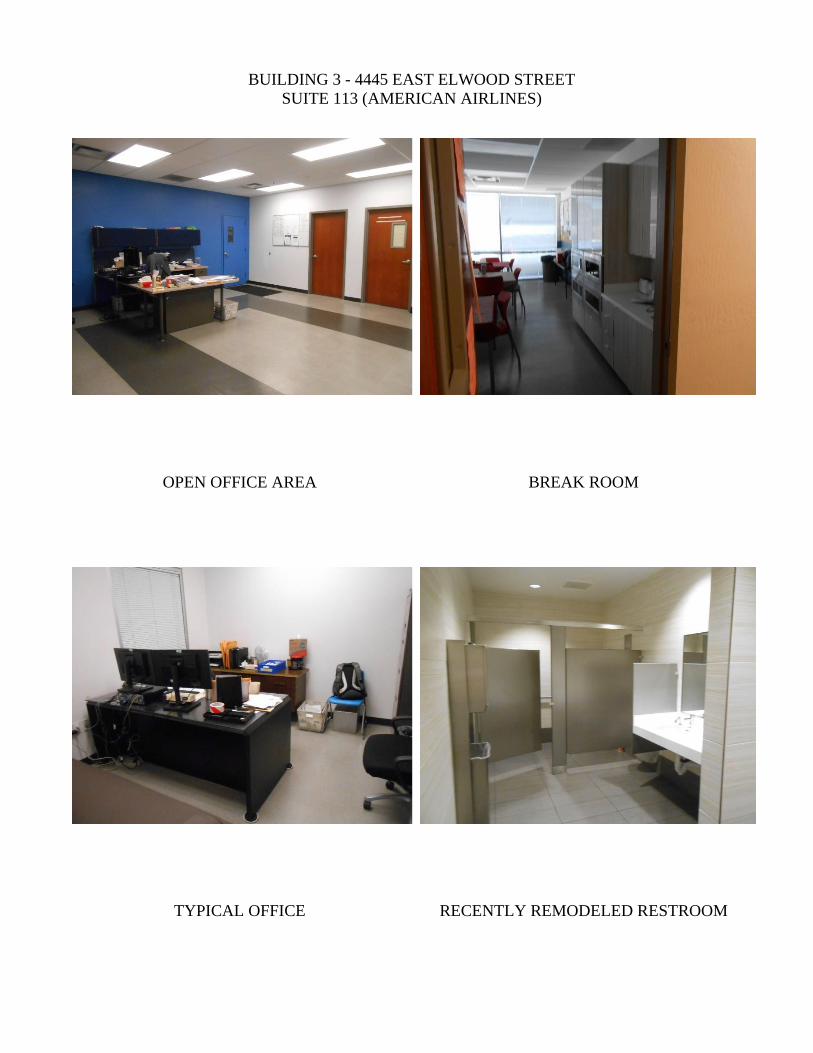

Bldg. 3 - 4445 E. Elwood Street Vacant 101 14,4651 741 5% J&K Cabinetry Kitchen Bath 107 60,090 3,821 6% American Airlines 113 76,718 +/- 2,000 3%

Total Building 3 151,273 6,562 4%

Bldg. 4 -4425 E. Elwood Street Clariant 104 27,300 4,500 16% Clariant 107 17,700 +/- 3,800 21%

Total Building 4 45,000 8,300 18%

Total All Buildings 353,711 51,143 14%

The interior finish varies based upon tenant requirements. In general, the good quality

improvements consist of acoustic drop ceilings, solid core wood doors, commercial carpets, and

recessed fluorescent lighting in the office areas. The warehouse areas generally consist of sealed

concrete floors, exposed or insulated roof decks with skylights, metal halide and fluorescent

lighting, and exposed evaporative cooling ducts.

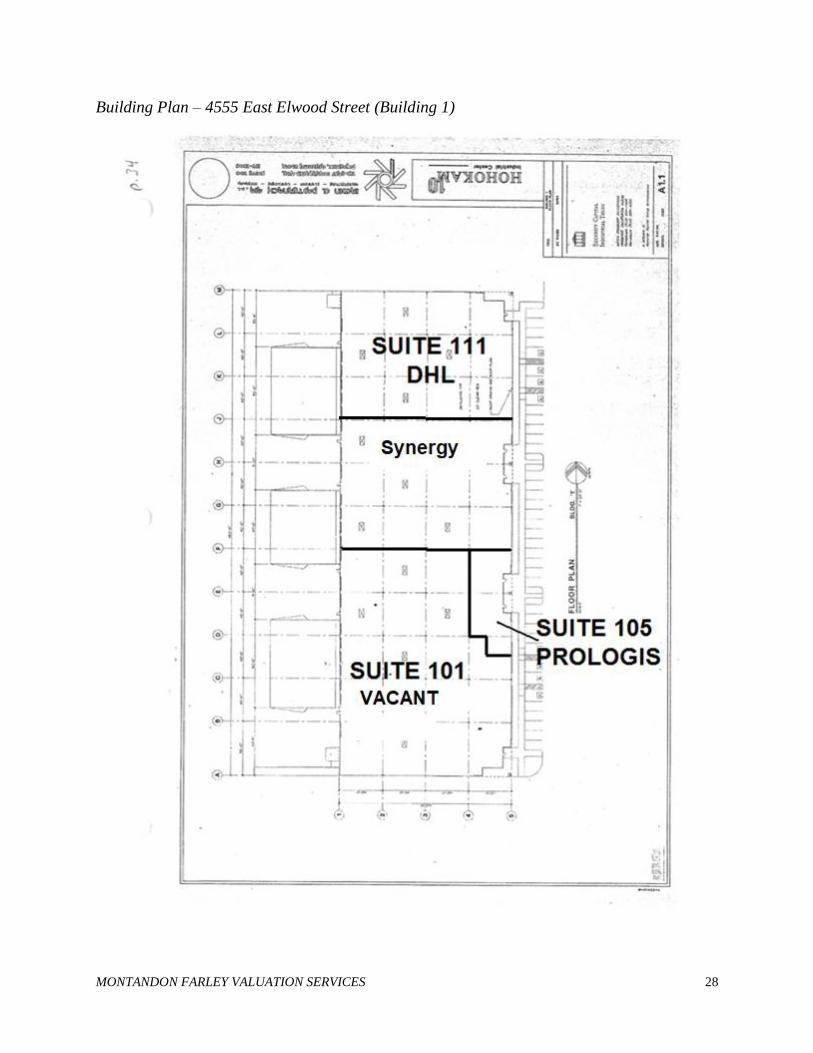

Building 1 Office Finishes:

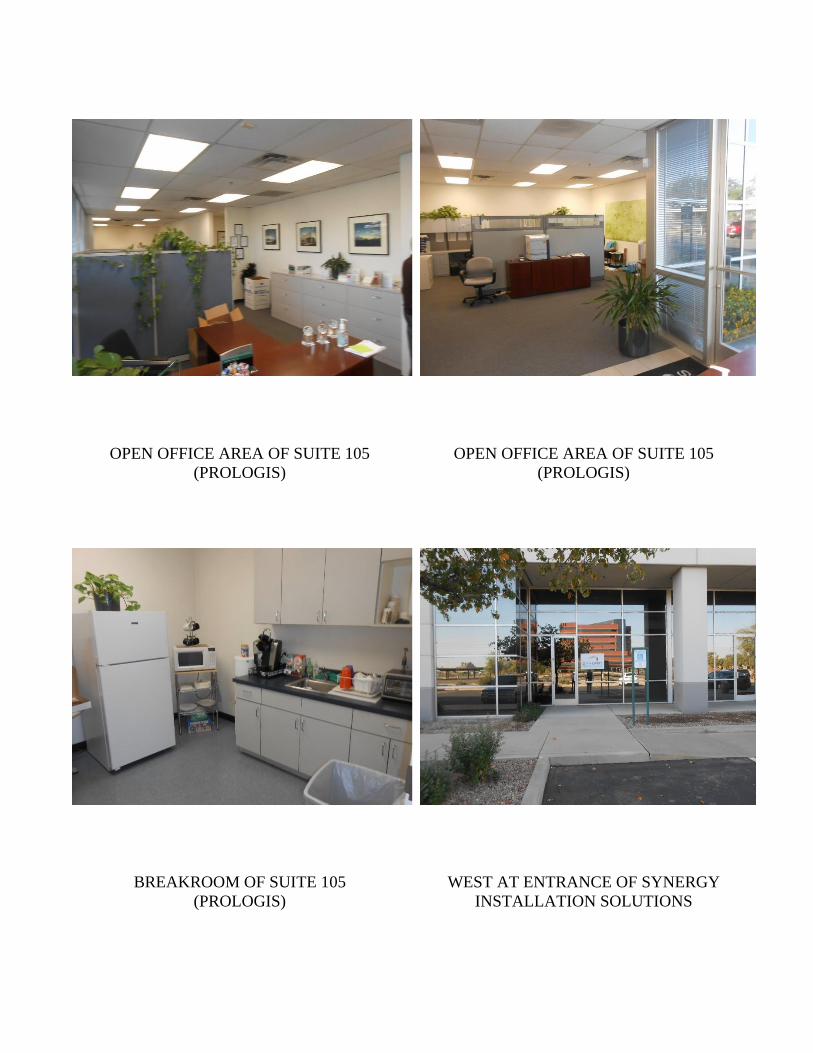

The 4555 E. Elwood Street building (Building 1) is divided into four suites. The small ProLogis

suite (Suite 105) is entirely finished for office use. Upon reconfiguration after demolition Suite 101

will be vacant warehouse with a new 10% build out allowance assumed herein. Suites 107

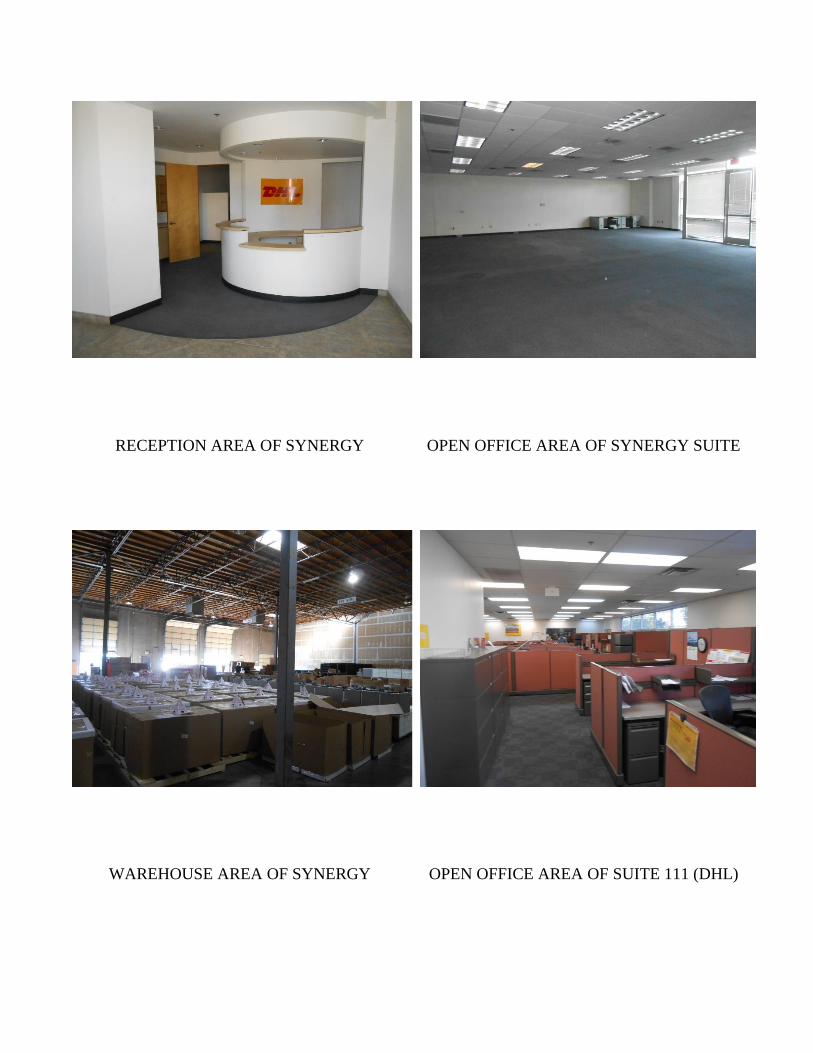

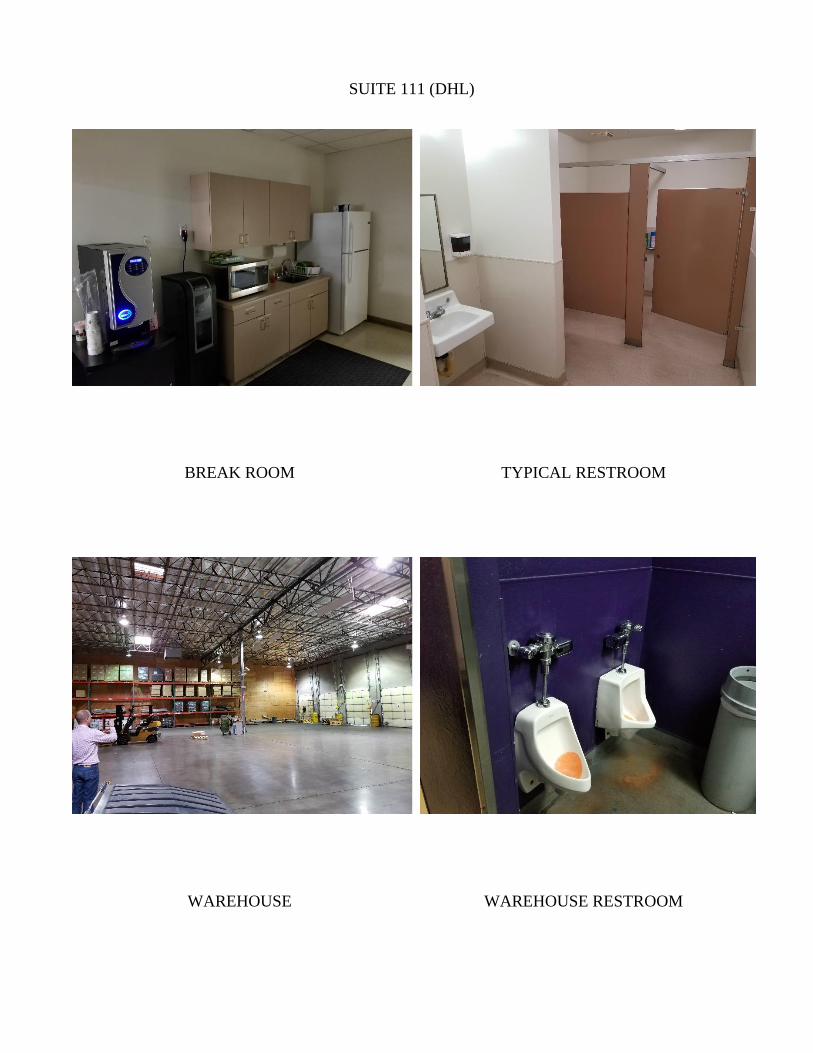

(Synergy Installation) and 111 (DHL) have typical office/warehouse finishes, however the DHL

suite has a large amount of open bullpen work area.

1 After demolition and reconfiguration

MONTANDON FARLEY VALUATION SERVICES 27

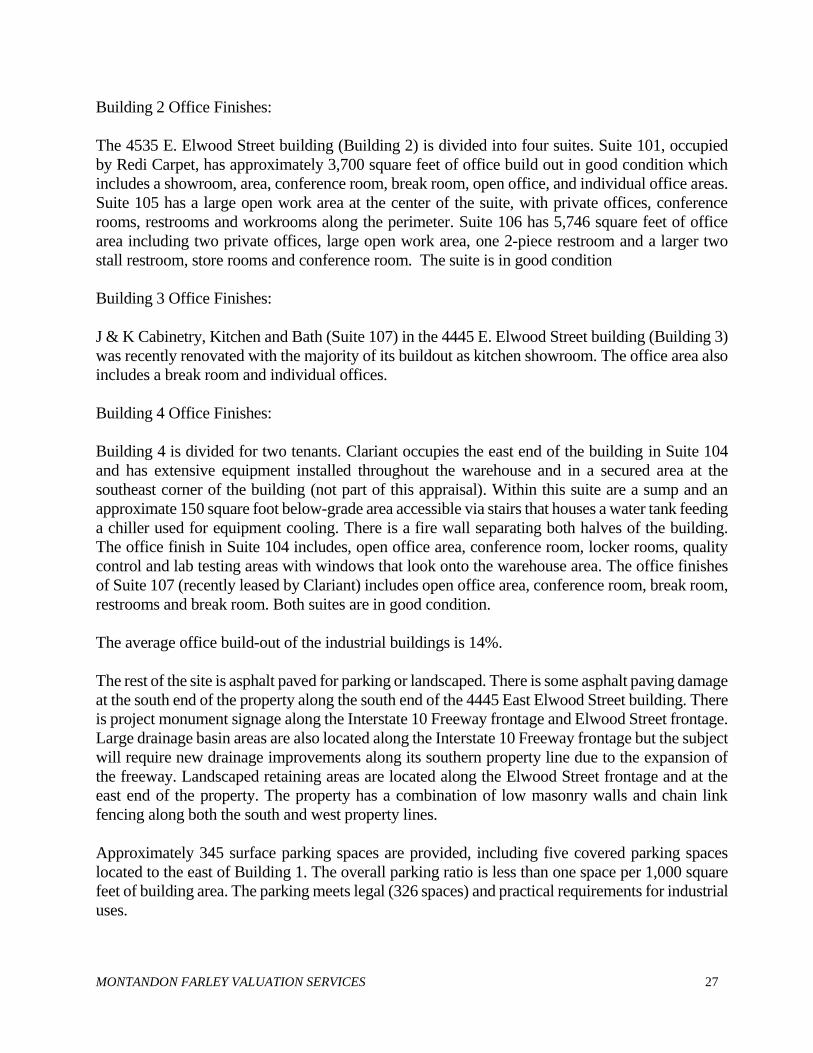

Building 2 Office Finishes:

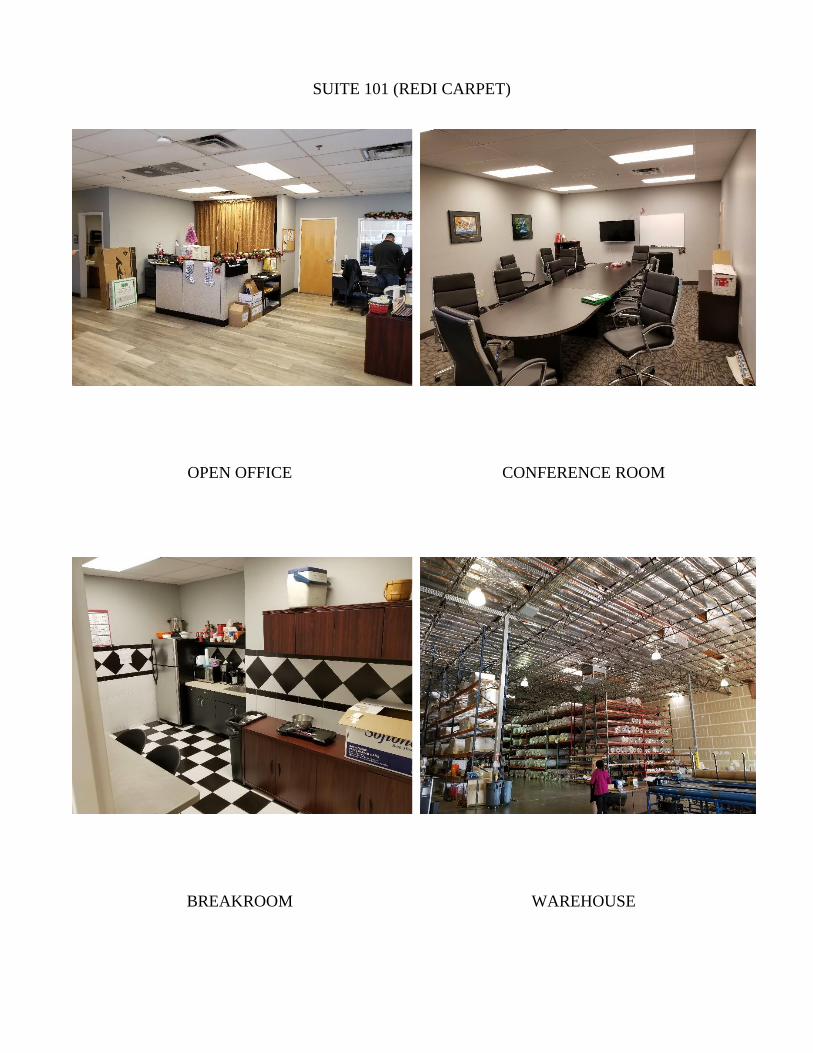

The 4535 E. Elwood Street building (Building 2) is divided into four suites. Suite 101, occupied

by Redi Carpet, has approximately 3,700 square feet of office build out in good condition which

includes a showroom, area, conference room, break room, open office, and individual office areas.

Suite 105 has a large open work area at the center of the suite, with private offices, conference

rooms, restrooms and workrooms along the perimeter. Suite 106 has 5,746 square feet of office

area including two private offices, large open work area, one 2-piece restroom and a larger two

stall restroom, store rooms and conference room. The suite is in good condition

Building 3 Office Finishes:

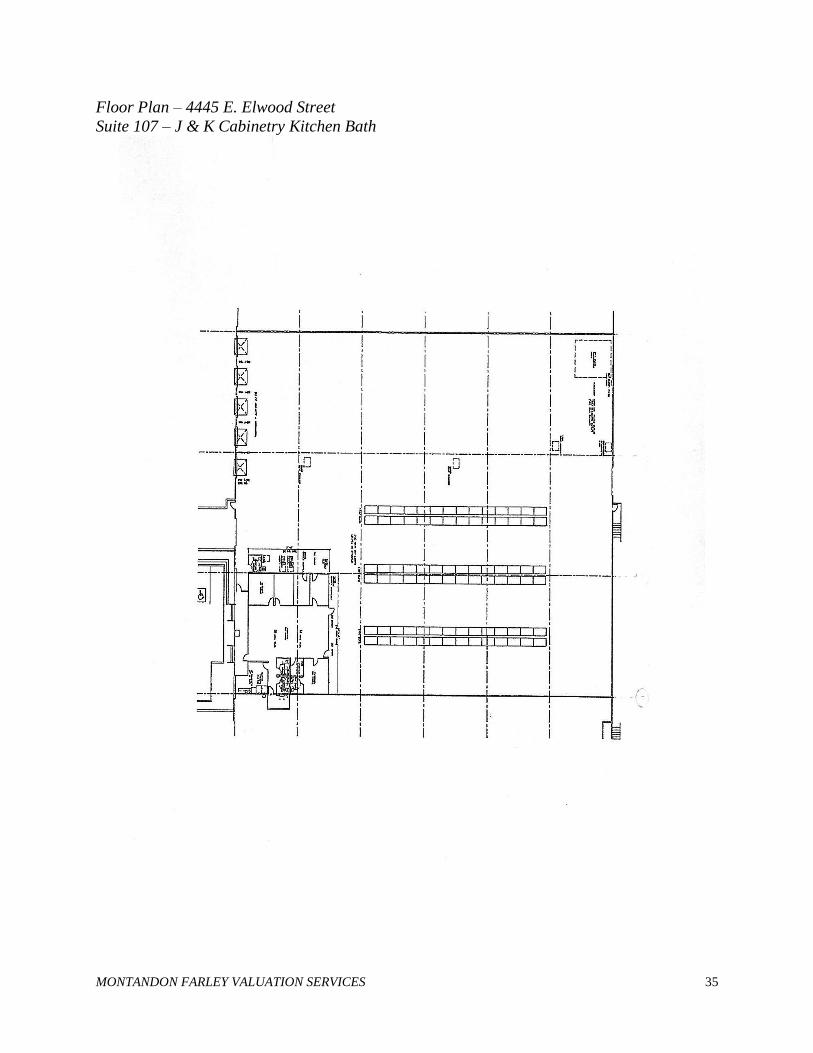

J & K Cabinetry, Kitchen and Bath (Suite 107) in the 4445 E. Elwood Street building (Building 3)

was recently renovated with the majority of its buildout as kitchen showroom. The office area also

includes a break room and individual offices.

Building 4 Office Finishes:

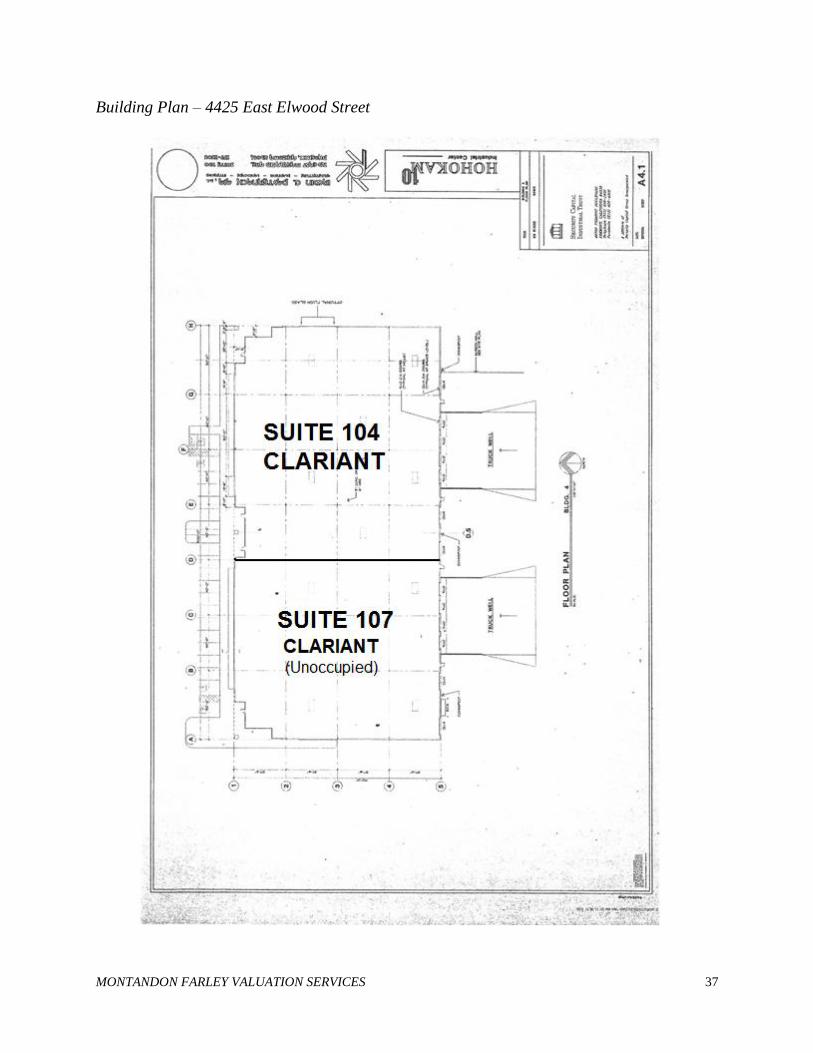

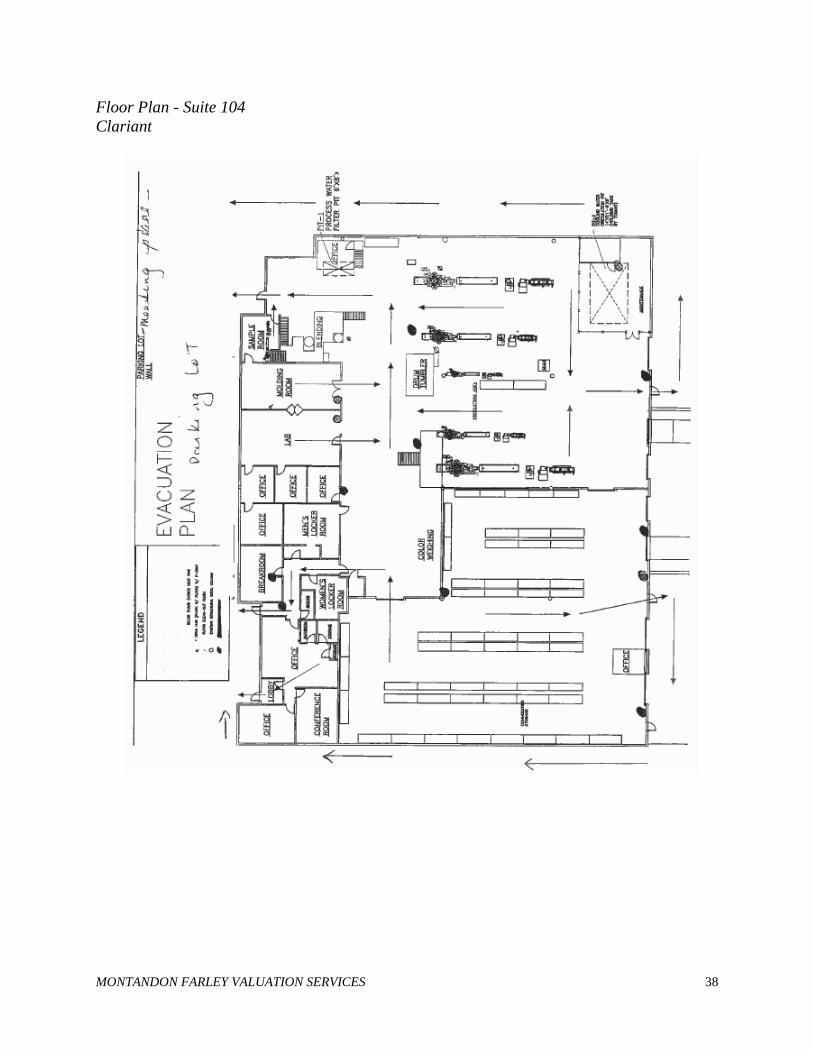

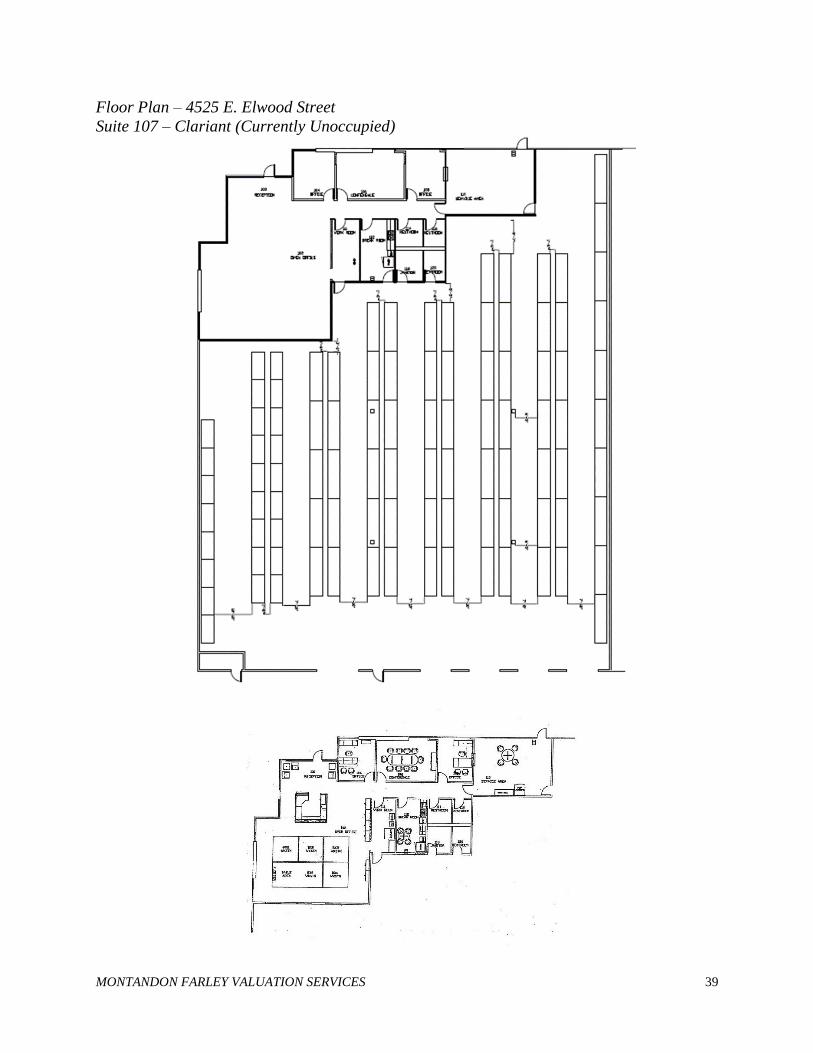

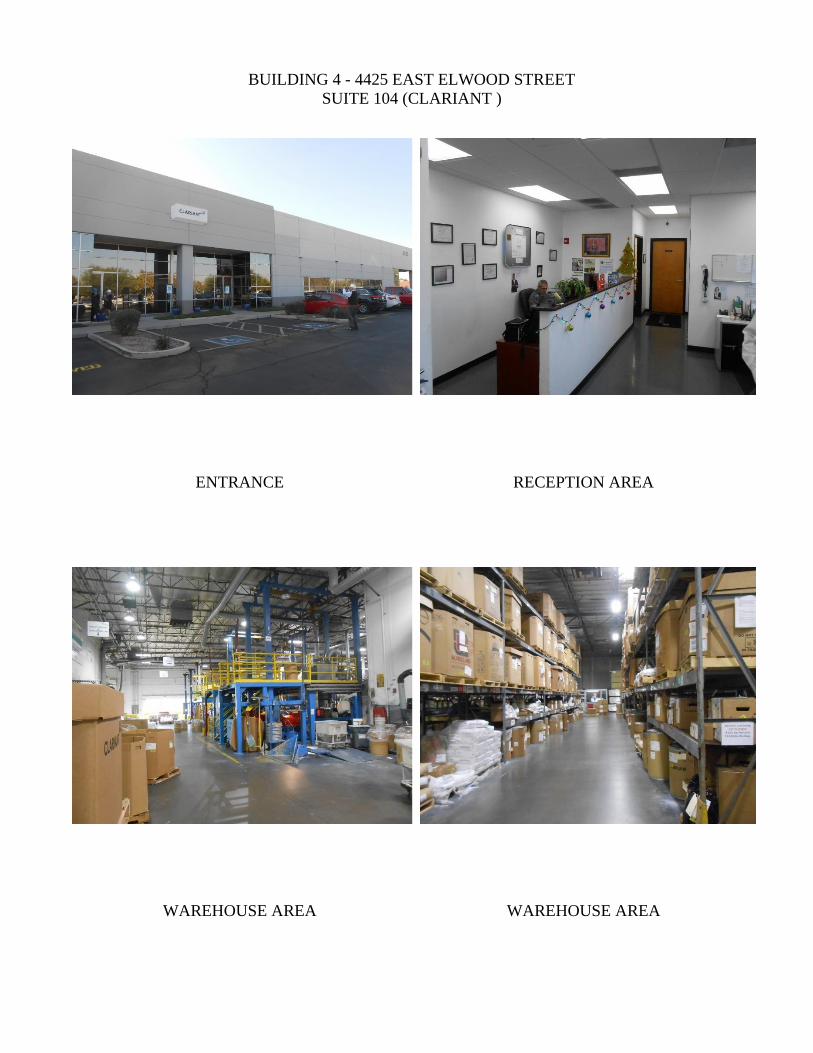

Building 4 is divided for two tenants. Clariant occupies the east end of the building in Suite 104

and has extensive equipment installed throughout the warehouse and in a secured area at the

southeast corner of the building (not part of this appraisal). Within this suite are a sump and an

approximate 150 square foot below-grade area accessible via stairs that houses a water tank feeding

a chiller used for equipment cooling. There is a fire wall separating both halves of the building.

The office finish in Suite 104 includes, open office area, conference room, locker rooms, quality

control and lab testing areas with windows that look onto the warehouse area. The office finishes

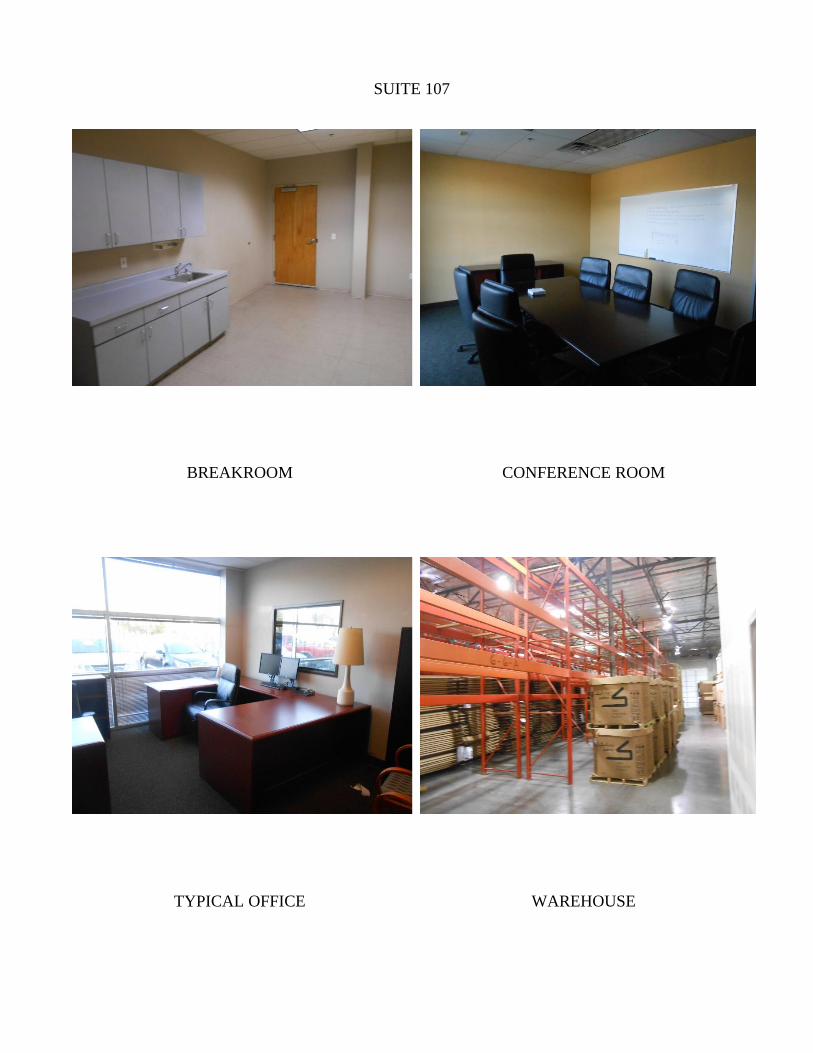

of Suite 107 (recently leased by Clariant) includes open office area, conference room, break room,

restrooms and break room. Both suites are in good condition.

The average office build-out of the industrial buildings is 14%.

The rest of the site is asphalt paved for parking or landscaped. There is some asphalt paving damage

at the south end of the property along the south end of the 4445 East Elwood Street building. There

is project monument signage along the Interstate 10 Freeway frontage and Elwood Street frontage.

Large drainage basin areas are also located along the Interstate 10 Freeway frontage but the subject

will require new drainage improvements along its southern property line due to the expansion of

the freeway. Landscaped retaining areas are located along the Elwood Street frontage and at the

east end of the property. The property has a combination of low masonry walls and chain link

fencing along both the south and west property lines.

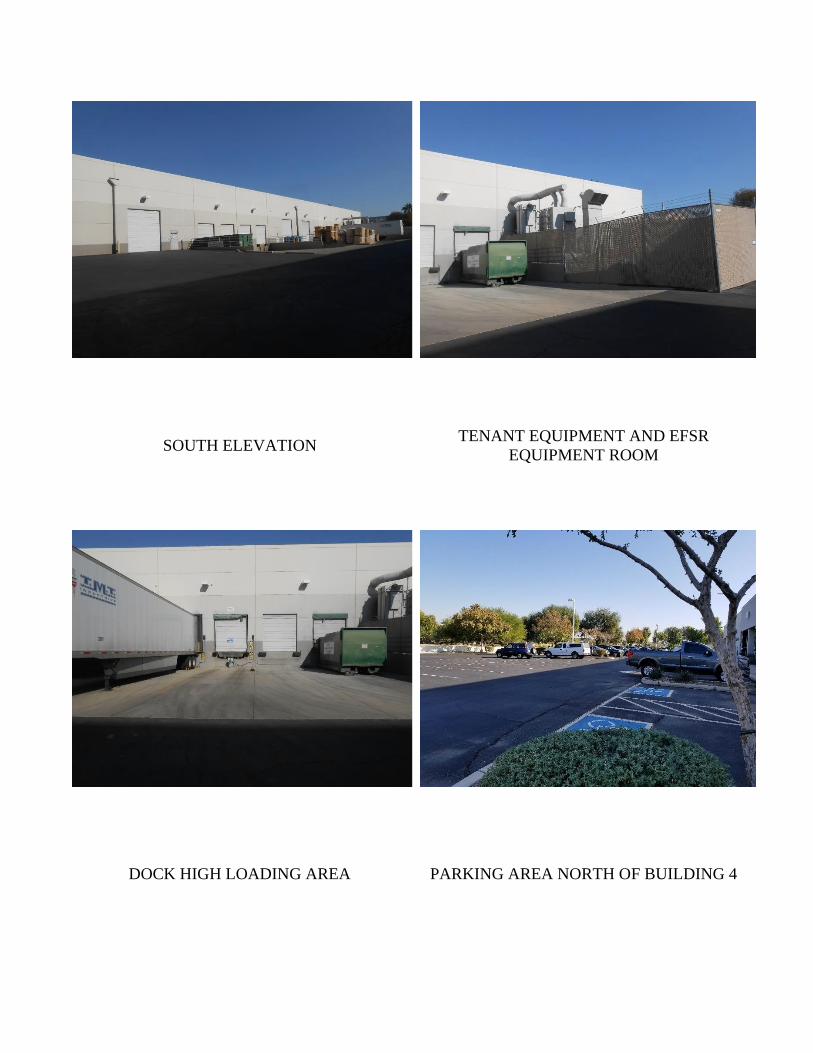

Approximately 345 surface parking spaces are provided, including five covered parking spaces

located to the east of Building 1. The overall parking ratio is less than one space per 1,000 square

feet of building area. The parking meets legal (326 spaces) and practical requirements for industrial

uses.

MONTANDON FARLEY VALUATION SERVICES 28

Building Plan – 4555 East Elwood Street (Building 1)

MONTANDON FARLEY VALUATION SERVICES 29

Floor Plan – 4555 E. Elwood Street

Suite 111 – DHL

MONTANDON FARLEY VALUATION SERVICES 30

Building Plan – 4535 East Elwood Street (Building 2)

MONTANDON FARLEY VALUATION SERVICES 31

Floor Plan – 4535 E. Elwood Street

Suite 101 – Redi-Carpet Office Area

MONTANDON FARLEY VALUATION SERVICES 32

Floor Plan – 4535 East Elwood Street

Suite 105 – Vacant

MONTANDON FARLEY VALUATION SERVICES 33

Floor Plan – 4535 E. Elwood Street

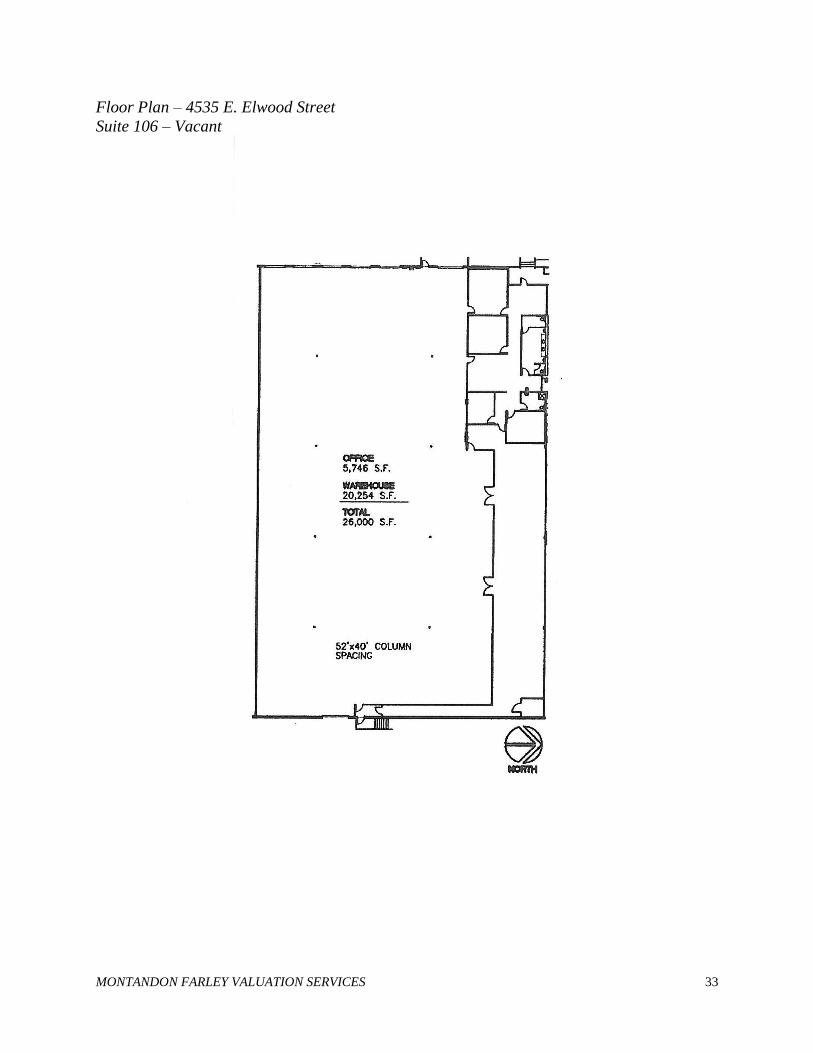

Suite 106 – Vacant

MONTANDON FARLEY VALUATION SERVICES 34

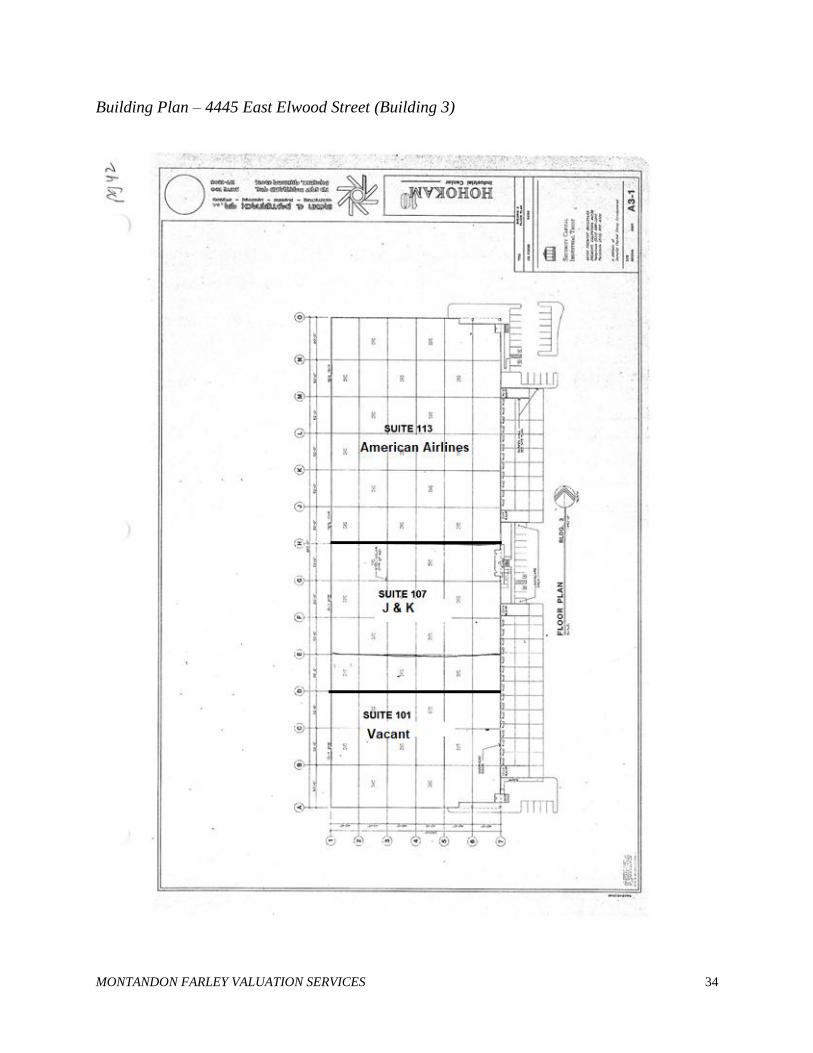

Building Plan – 4445 East Elwood Street (Building 3)

MONTANDON FARLEY VALUATION SERVICES 35

Floor Plan – 4445 E. Elwood Street

Suite 107 – J & K Cabinetry Kitchen Bath

MONTANDON FARLEY VALUATION SERVICES 36

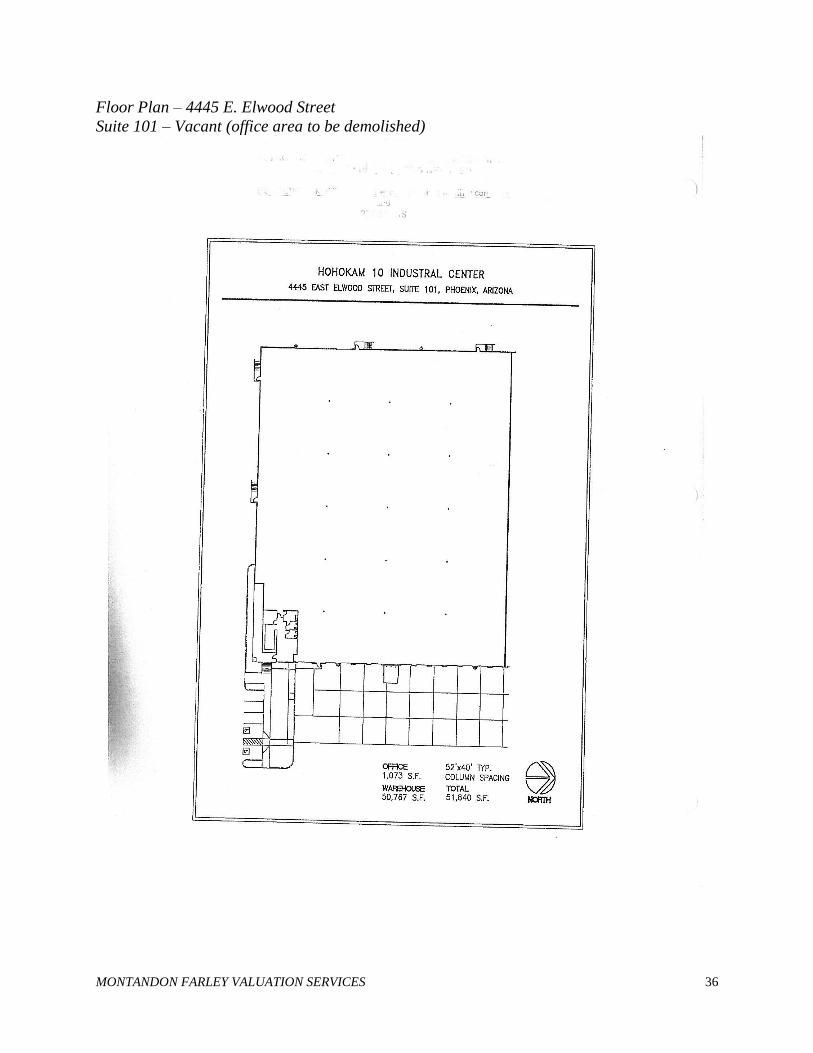

Floor Plan – 4445 E. Elwood Street

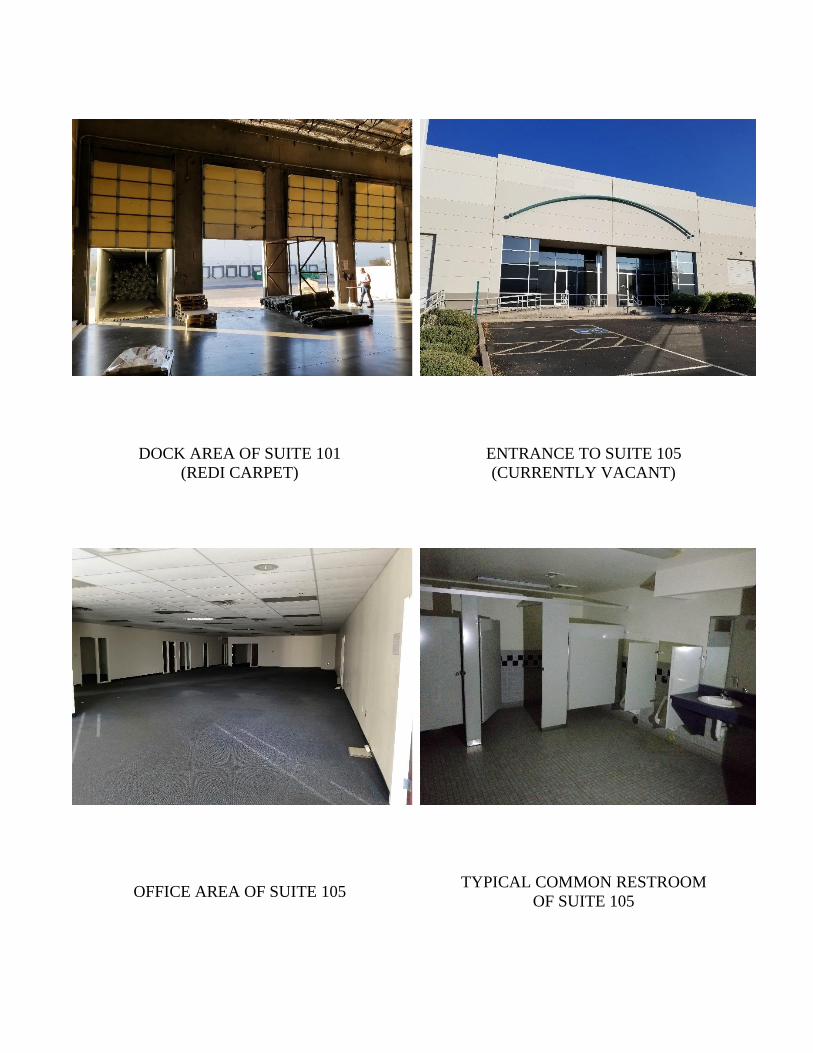

Suite 101 – Vacant (office area to be demolished)

MONTANDON FARLEY VALUATION SERVICES 37

Building Plan – 4425 East Elwood Street

MONTANDON FARLEY VALUATION SERVICES 38

Floor Plan - Suite 104

Clariant

MONTANDON FARLEY VALUATION SERVICES 39

Floor Plan – 4525 E. Elwood Street

Suite 107 – Clariant (Currently Unoccupied)

MONTANDON FARLEY VALUATION SERVICES 40

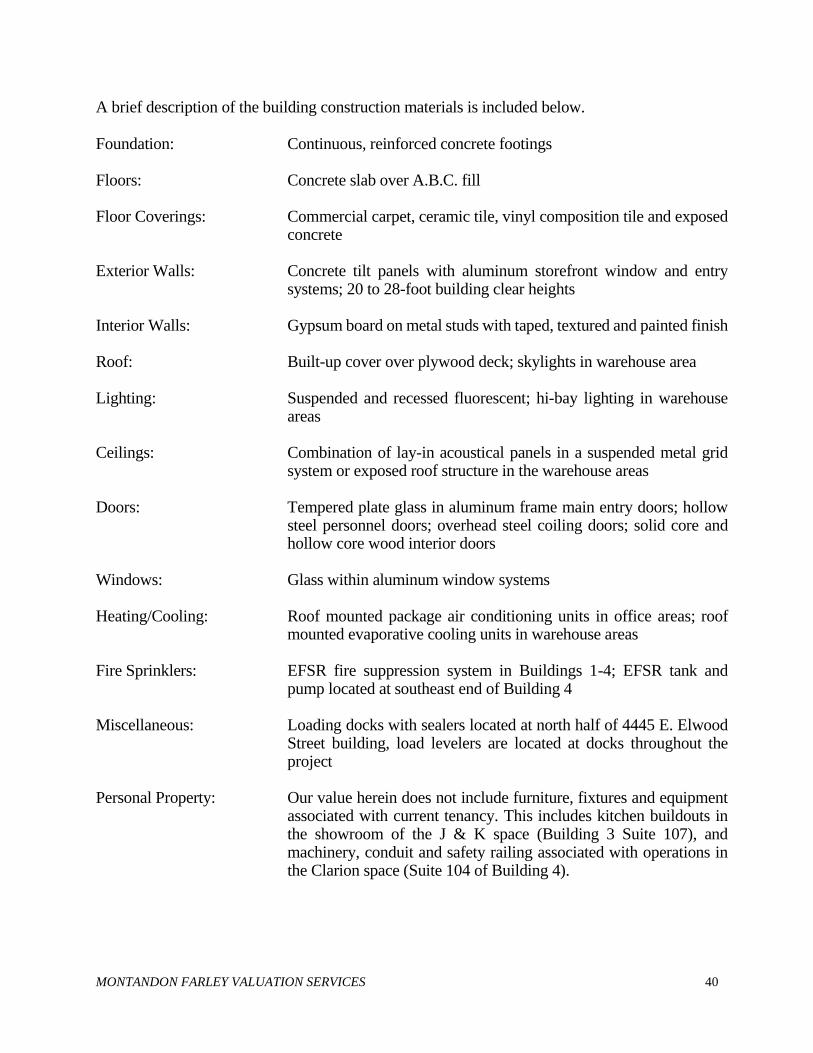

A brief description of the building construction materials is included below. Foundation: Continuous, reinforced concrete footings Floors: Concrete slab over A.B.C. fill Floor Coverings: Commercial carpet, ceramic tile, vinyl composition tile and exposed

concrete Exterior Walls: Concrete tilt panels with aluminum storefront window and entry

systems; 20 to 28-foot building clear heights Interior Walls: Gypsum board on metal studs with taped, textured and painted finish Roof: Built-up cover over plywood deck; skylights in warehouse area Lighting: Suspended and recessed fluorescent; hi-bay lighting in warehouse

areas Ceilings: Combination of lay-in acoustical panels in a suspended metal grid

system or exposed roof structure in the warehouse areas Doors: Tempered plate glass in aluminum frame main entry doors; hollow

Windows: Glass within aluminum window systems Heating/Cooling: Roof mounted package air conditioning units in office areas; roof

mounted evaporative cooling units in warehouse areas Fire Sprinklers: EFSR fire suppression system in Buildings 1-4; EFSR tank and

pump located at southeast end of Building 4 Miscellaneous: Loading docks with sealers located at north half of 4445 E. Elwood

Street building, load levelers are located at docks throughout the project

Personal Property: Our value herein does not include furniture, fixtures and equipment

associated with current tenancy. This includes kitchen buildouts in the showroom of the J & K space (Building 3 Suite 107), and machinery, conduit and safety railing associated with operations in the Clarion space (Suite 104 of Building 4).

MONTANDON FARLEY VALUATION SERVICES 41

Except for roofing in the areas of planned demolition, which were adversely affected by asbestos

abatement in the past causing leaks, the roofs are reported to be in good condition. During our site

visit we noted water dripping from the northeast corner of the warehouse ceiling in Suite 106 of

Building 2 and noted some cracking in asphalt pavement in several along the southern driveways

and parking. The planned reconfiguration will eliminate the roof leaks at the southern end of

Buildings 1, 2 and 3 as well as provide new driveways along the southern portion of the buildings.

We have concluded that the cost to correct minor maintenance/repair issues that remain after

reconfiguration could be covered in the normal annual operating budget for the property. In

summary, the improvements are in good condition with no significant deferred maintenance

expected upon completion of reconstruction of the southern portion of buildings planned for

reconfiguration.

Based on the information available to us, it is our opinion the improvements are a legal

conforming use of the site.

We have estimated the average effective age of the improvements at 17 years and their remaining

economic life at 28 years. The layout of the project is efficient, allows tenant flexibility, and there

is sufficient onsite parking.

Environmental Assessment

We have not had the benefit of a Phase 1 environmental report and are unqualified to conduct

this type of study. Our inspection of the property did not reveal any obvious potential hazards.

We have assumed for the purposes of this report that the property is free of any environmental

hazards that may exceed EPA standards or could have an adverse impact on the value of the real

estate.

Americans with Disabilities Act

The landmark Americans with Disabilities Act (ADA) enacted on July 26, 1990, provides

comprehensive civil rights protection to individuals with disabilities in the areas of employment,

public accommodations, state and local government services and telecommunications. The

ADA generally became effective on January 26, 1992 and affects public accommodations such

parks, private schools and day care centers. Private clubs and religious organizations are exempt.

There are three basic areas to the act including: employment, public accommodations and

transportation.

The subject was constructed after the enactment of ADA; therefore, the building must comply

with the Americans with Disabilities Act of January 1990. We have assumed for the purposes

of this report that the project is in compliance with ADA standards. If an independent study

indicates that there are major violations of the act that could affect the value of the property, we

reserve the right to amend our final conclusion.

MONTANDON FARLEY VALUATION SERVICES 42

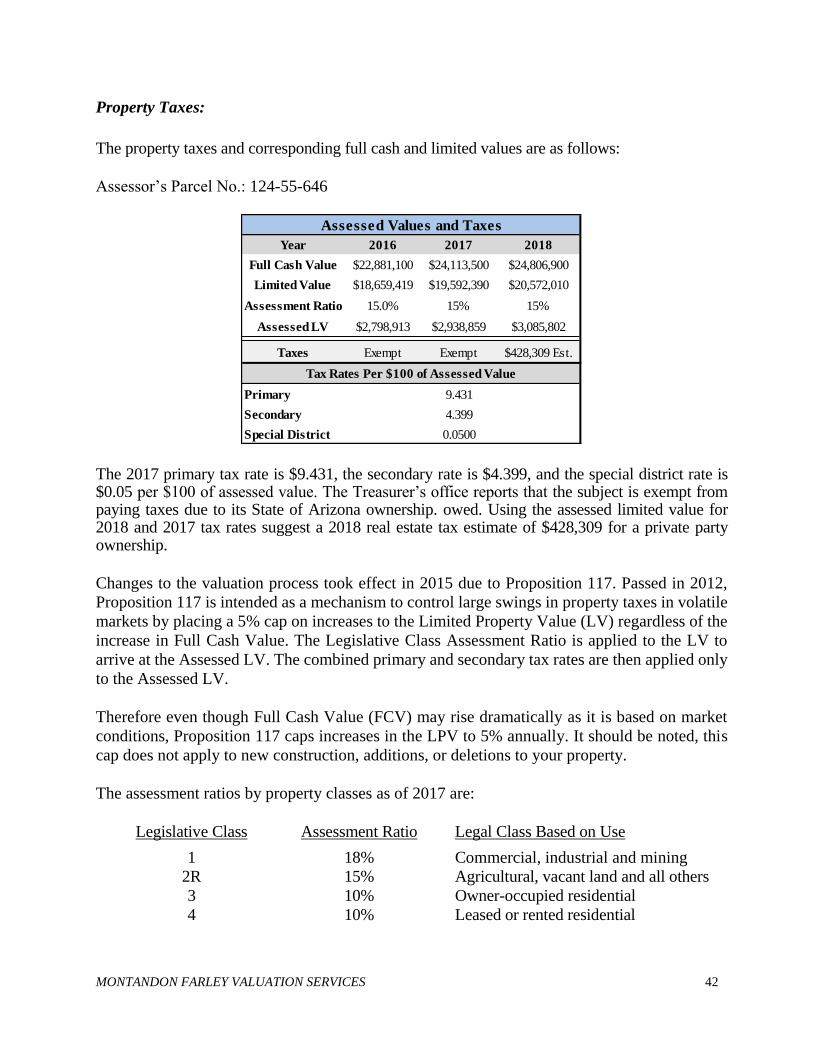

Property Taxes:

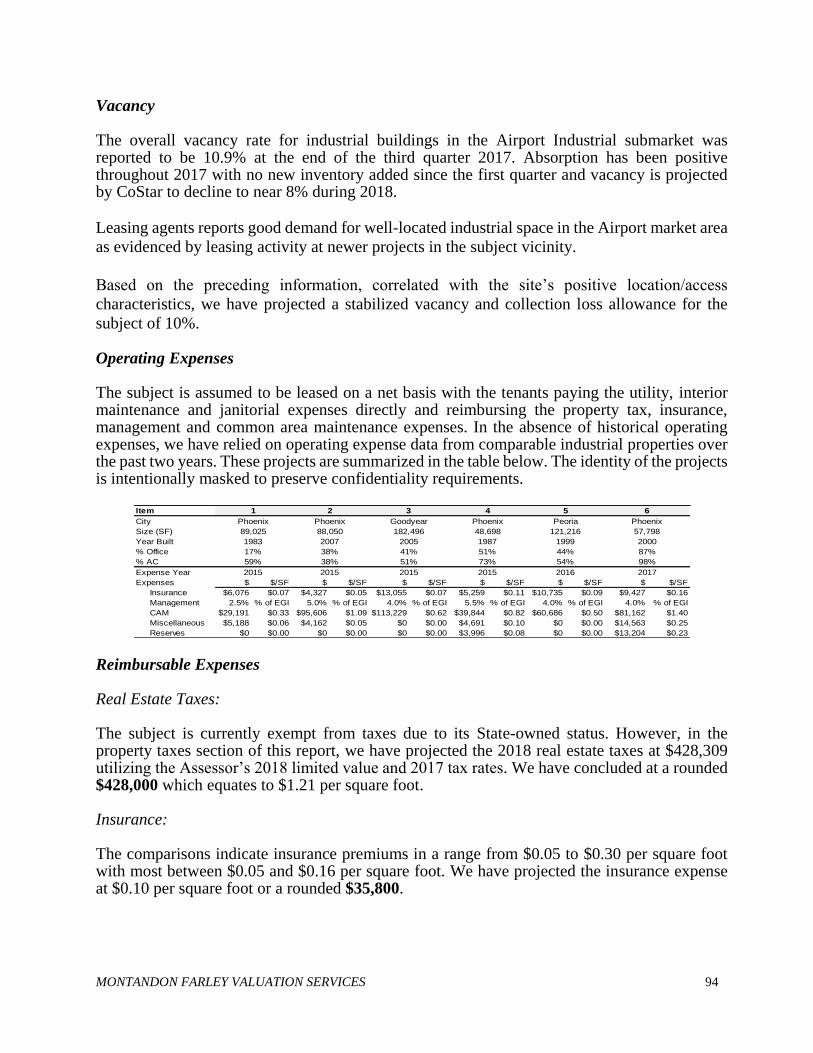

The property taxes and corresponding full cash and limited values are as follows:

Assessor’s Parcel No.: 124-55-646

The 2017 primary tax rate is $9.431, the secondary rate is $4.399, and the special district rate is $0.05 per $100 of assessed value. The Treasurer’s office reports that the subject is exempt from paying taxes due to its State of Arizona ownership. owed. Using the assessed limited value for 2018 and 2017 tax rates suggest a 2018 real estate tax estimate of $428,309 for a private party ownership.

Changes to the valuation process took effect in 2015 due to Proposition 117. Passed in 2012,

Proposition 117 is intended as a mechanism to control large swings in property taxes in volatile

markets by placing a 5% cap on increases to the Limited Property Value (LV) regardless of the

increase in Full Cash Value. The Legislative Class Assessment Ratio is applied to the LV to

arrive at the Assessed LV. The combined primary and secondary tax rates are then applied only

to the Assessed LV.

Therefore even though Full Cash Value (FCV) may rise dramatically as it is based on market

conditions, Proposition 117 caps increases in the LPV to 5% annually. It should be noted, this

cap does not apply to new construction, additions, or deletions to your property.

The assessment ratios by property classes as of 2017 are:

Legislative Class Assessment Ratio Legal Class Based on Use

1 18% Commercial, industrial and mining

2R 15% Agricultural, vacant land and all others

3 10% Owner-occupied residential

4 10% Leased or rented residential

Year 2016 2017 2018

Full Cash Value $22,881,100 $24,113,500 $24,806,900

Limited Value $18,659,419 $19,592,390 $20,572,010

Assessment Ratio 15.0% 15% 15%

Assessed LV $2,798,913 $2,938,859 $3,085,802

Taxes Exempt Exempt $428,309 Est.

Primary 9.431

Secondary 4.399

Special District 0.0500

Assessed Values and Taxes

Tax Rates Per $100 of Assessed Value

MONTANDON FARLEY VALUATION SERVICES 43

HIGHEST AND BEST USE

In the most recent edition of The Appraisal of Real Estate, the Appraisal Institute, defines

highest and best use as:

The reasonably probable and legal use of vacant land or an improved property,

which is physically possible, appropriately supported, financially feasible, and

that results in the highest value.

To estimate highest and best use, four elements are considered:

1. Legally Permissible - Of the possible uses, which uses are permitted by

zoning and deed restrictions?

2. Physically Possible - What uses are physically possible?

3. Financially Feasible - Which possible and permissible uses will produce a

net return to the owner of the site?

4. Maximally Productive - Among the feasible uses, which use will produce

the highest net return or the highest present value?

The highest and best use must be legal and probable, not speculative or conjectural. A demand

for the use must exist and it must yield the highest net return to the land for the longest period.

The highest and best use of the land as if vacant and available for use may be different from the

highest and best use of the improved property. This may be true when the improvement is not

an appropriate use, but it makes a contribution to the total property value in excess of the value

of the site. Therefore, to arrive at an estimate of highest and best use, the subject was analyzed

1) as though the site were vacant and available for development, and 2) as presently improved.

MONTANDON FARLEY VALUATION SERVICES 44

As If Vacant

Legally Permissible

The sites’ legally permissible uses are governed by the city of Phoenix A-1 and CP/GCP zoning classifications. This classification allows a mixture of industrial uses, including commerce, service and employment activities. The General Commerce Park Option allows a broad range of manufacturing, warehousing, distribution and support retail sales/services. We are unaware of any unusual easements or restrictions that could impact the value of the property. Physically Possible

The subject site has frontage on Elwood Street and abuts the Maricopa Freeway (Interstate 10). It contains 926,979 square feet, or 21.28 acres. All public utilities are available to the site, it is accessible from arterial streets and is developable from a terrain standpoint. Virtually any urban improvement is physically possible on the site, limited only by size. Financially Feasible/ Maximally Productive

The property is located in an established industrial corridor that is bisected by Interstate 10 and is just south of Sky Harbor Airport. The subject’s zoning, proximity to major transportation routes and location in an established industrial area indicate that industrial development is the most likely use of the property. Rents have are generally below the levels necessary to economically support new speculative office development although some build-to-suite office use may be possible. The industrial sector in the subject area is stable with positive absorption and declining vacancy. Rents have approached the levels necessary to economically support some new speculative development. However, larger projects typically require some anchor tenant commitment. In light of the preceding, it is our opinion that the highest and best use of the property as if vacant is for industrial development upon securing a large tenant commitment.

As Improved

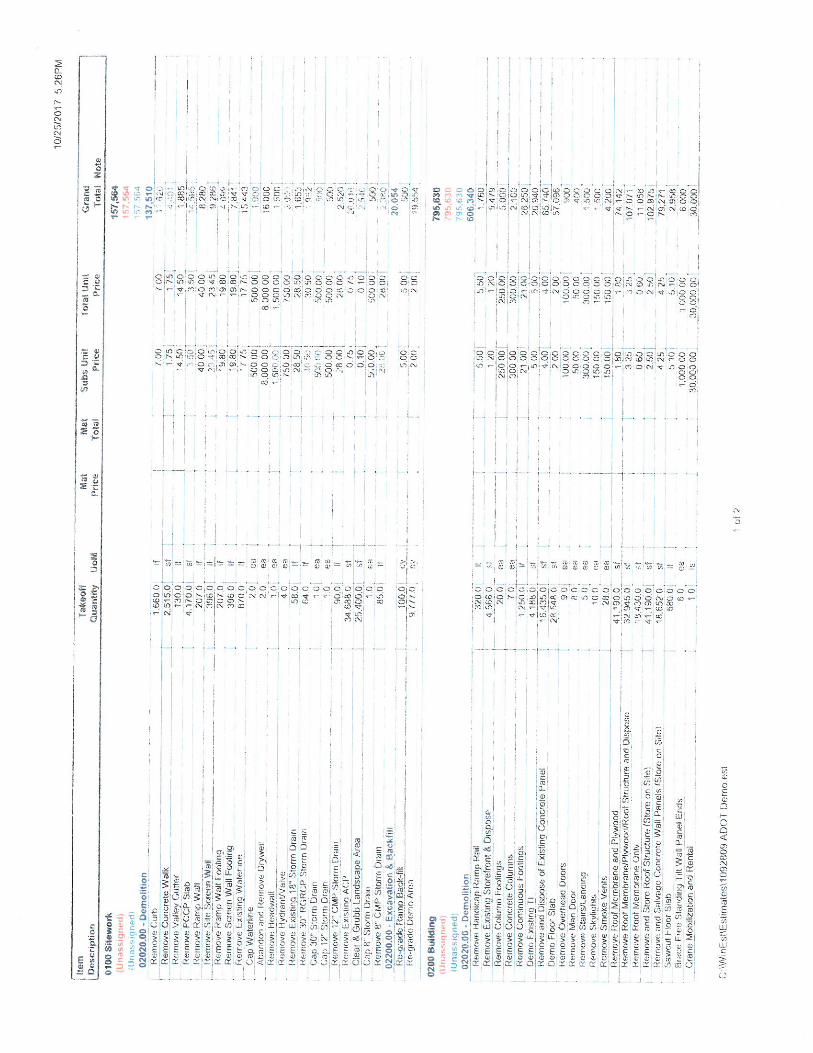

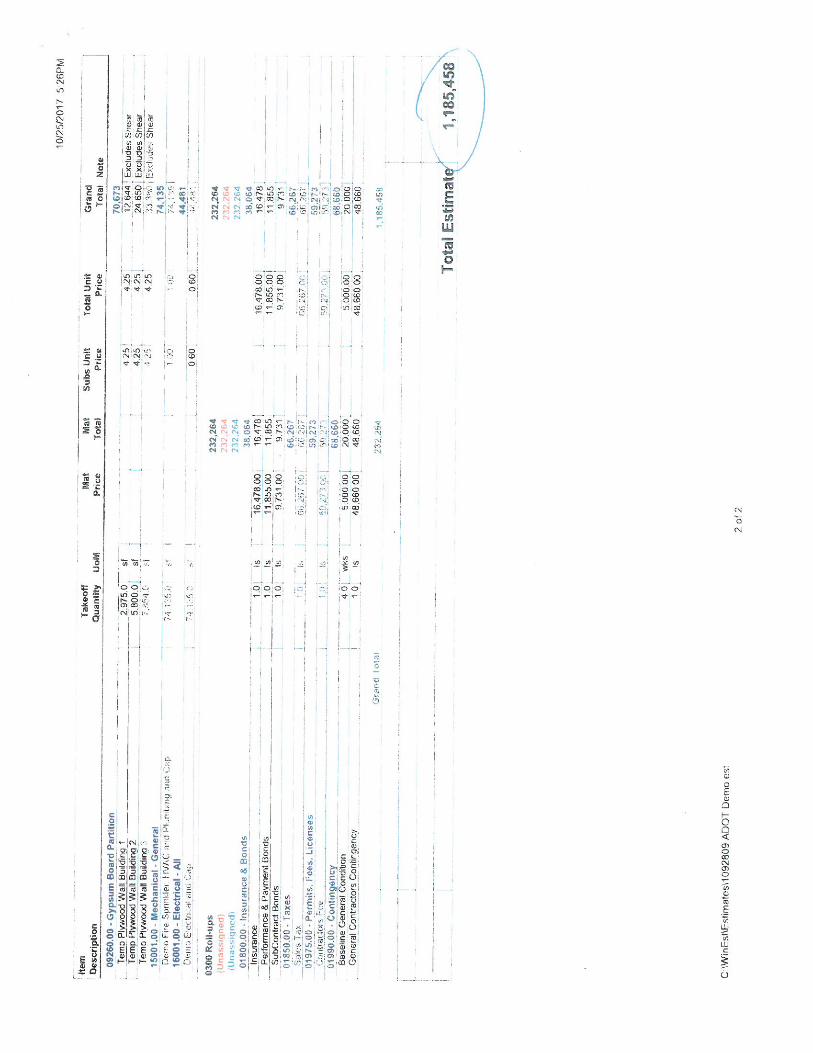

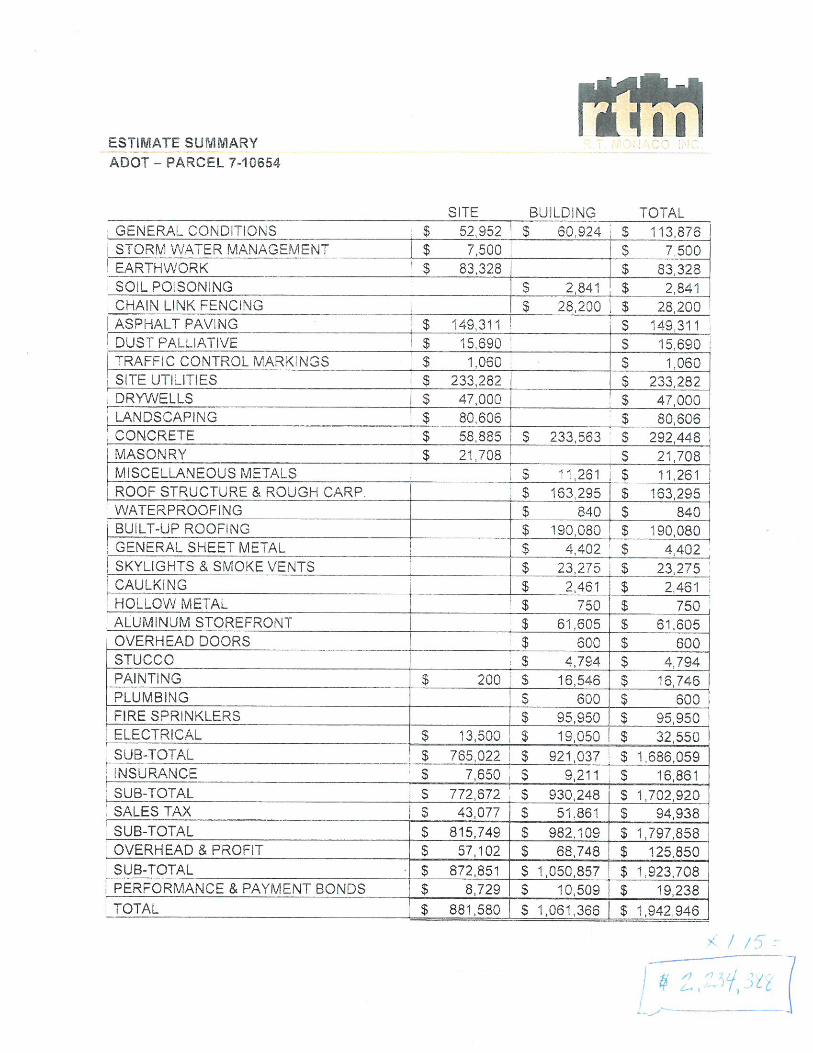

The site is currently improved with a five-building industrial complex which contains a total building area of 388,474 square feet. However, fire lane and setback requirements due to new right of way lines for freeway expansion obligate the subject to demolish approximately 50 to 60 feet the southern portion of Buildings 1, 2 and 3. After reconstruction of exposed area the building area and reconfiguration of parking, drainage and driveway along the south property line at a cost estimated herein of $3,200,000 the subject will have a rentable total building area of 353,711 square feet. The value of the property with the project in place greatly exceeds the cost to cure and value of the land only. In our opinion, the existing industrial development is the highest and best use of the property “as improved”.

MONTANDON FARLEY VALUATION SERVICES 45

VALUE AS IF RECONSTRUCTED TO ACCOMMODATE RIGHT

OF WAY & AT STABILIZED OCCUPANCY

Appraisal Process Methodology:

In order to arrive at an “as is” value for the subject we have first valued the subject under the

hypothetical condition that areas affected by the acquisition have had reconstruction completed

as of the effective date of this report and that the subject has been filled up to stabilized

occupancy projected herein. Later in this report costs to reconfigure the buildings and construct

new fire lanes, parking and driveway to accommodate setback related to the new right of way

for freeway expansion are deducted from our value as if complete value along with deductions

for fill-up costs to achieve stabilized occupancy. These deductions which included a profit

allowance provide the basis of our “as is” value conclusion later in this report.

The following section of this report assumes the subject has had all demolition and

reconstruction work complete to accommodate right of way for freeway expansion.

MONTANDON FARLEY VALUATION SERVICES 46

VALUATION APPROACHES

The estimation of a real property’s market value involves a systematic process in which the

problem is defined; the work necessary to solve the problem is planned; and the data required is

acquired, classified, analyzed and interpreted into an estimate of value. In this process, three

basic approaches, when applicable, are used by the appraisers: the Cost, Sales Comparison and

Income Approaches. The value estimates, as indicated by the direct approaches, are then

reconciled into a final estimate, of the property’s value based on the appropriateness of each

approach, the accuracy of the data and the quantity and the quality of the evidence. When one or

more of these approaches is not applicable in the appraisal process, justification is presented.

COST APPROACH

The Cost Approach is based on the premise that the value of a property can be derived by adding

the estimated value of the land to the current cost of constructing a reproduction or replacement

for the improvements and then subtracting the amount of depreciation (i.e., deterioration and

obsolescence) in the structures from all causes.

LAND SALES COMPARISON APPROACH

Set forth on the following pages are the land comparables that have been considered in

estimating the “as is” market value of the site on a direct comparison basis. A summary and map

of the comparables follow the detailed data.

MONTANDON FARLEY VALUATION SERVICES 47

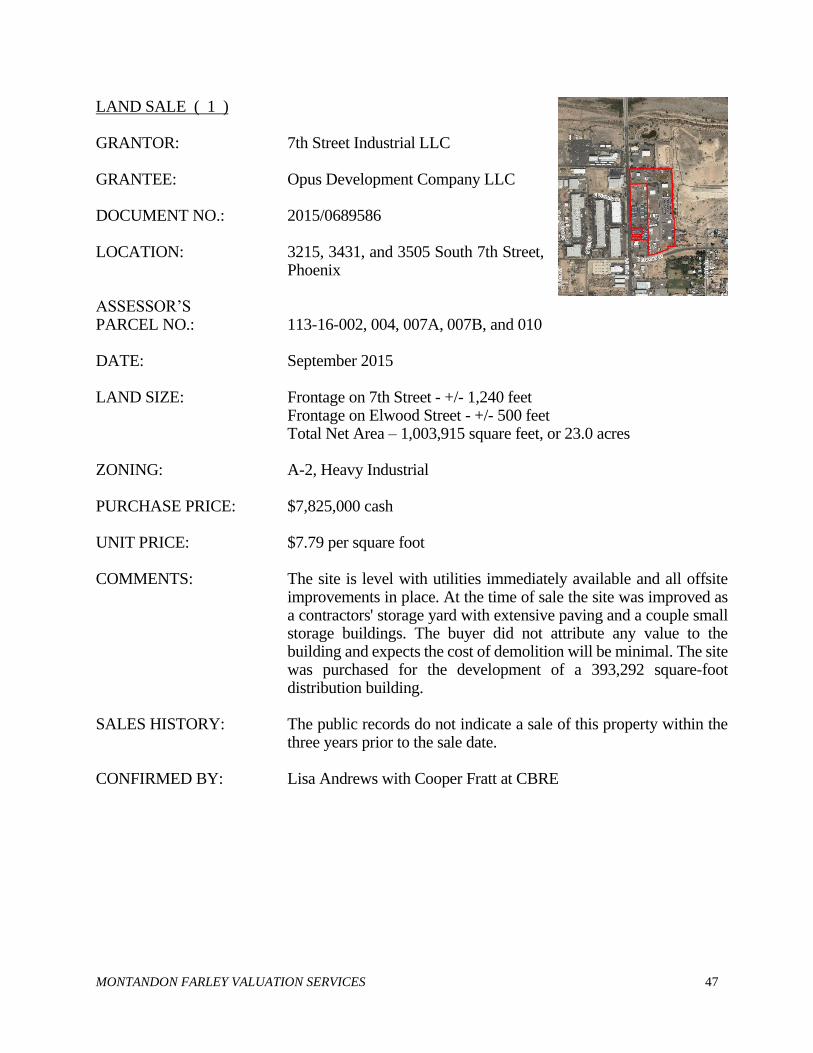

LAND SALE ( 1 ) GRANTOR: 7th Street Industrial LLC GRANTEE: Opus Development Company LLC DOCUMENT NO.: 2015/0689586 LOCATION: 3215, 3431, and 3505 South 7th Street,

Phoenix ASSESSOR’S PARCEL NO.: 113-16-002, 004, 007A, 007B, and 010 DATE: September 2015 LAND SIZE: Frontage on 7th Street - +/- 1,240 feet Frontage on Elwood Street - +/- 500 feet Total Net Area – 1,003,915 square feet, or 23.0 acres ZONING: A-2, Heavy Industrial PURCHASE PRICE: $7,825,000 cash UNIT PRICE: $7.79 per square foot COMMENTS: The site is level with utilities immediately available and all offsite

improvements in place. At the time of sale the site was improved as a contractors' storage yard with extensive paving and a couple small storage buildings. The buyer did not attribute any value to the building and expects the cost of demolition will be minimal. The site was purchased for the development of a 393,292 square-foot distribution building.

SALES HISTORY: The public records do not indicate a sale of this property within the

three years prior to the sale date. CONFIRMED BY: Lisa Andrews with Cooper Fratt at CBRE

MONTANDON FARLEY VALUATION SERVICES 48

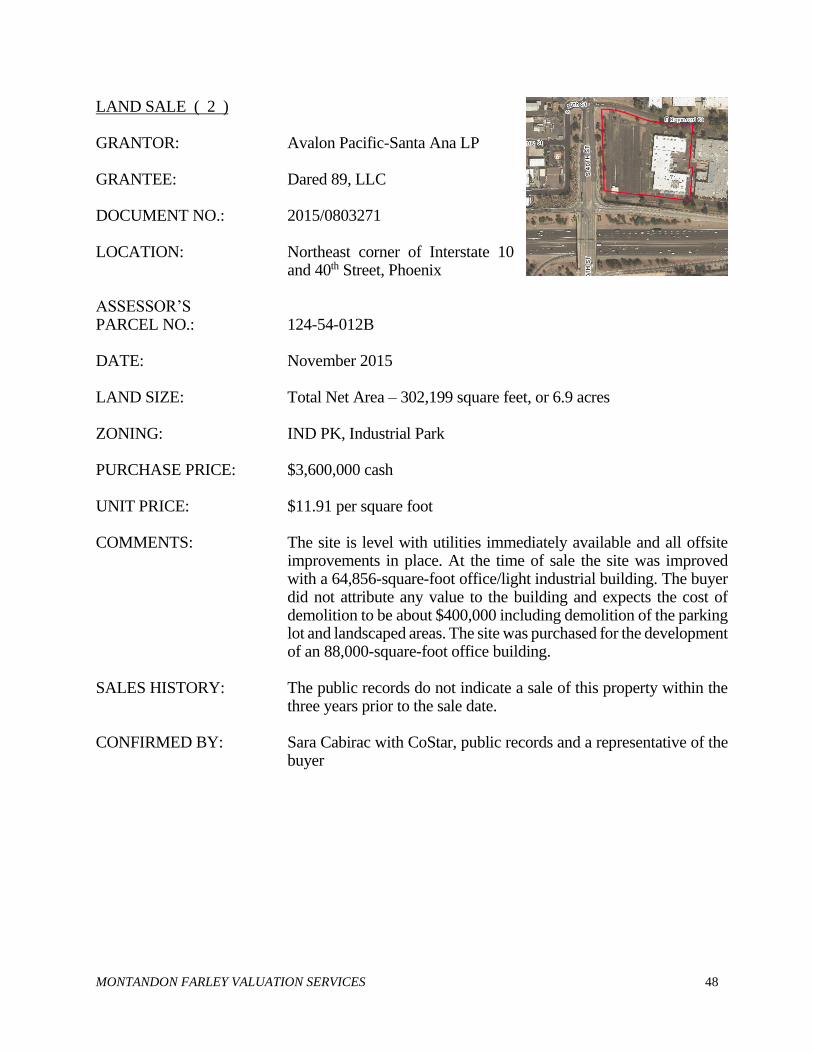

LAND SALE ( 2 ) GRANTOR: Avalon Pacific-Santa Ana LP GRANTEE: Dared 89, LLC DOCUMENT NO.: 2015/0803271 LOCATION: Northeast corner of Interstate 10

and 40th Street, Phoenix ASSESSOR’S PARCEL NO.: 124-54-012B DATE: November 2015 LAND SIZE: Total Net Area – 302,199 square feet, or 6.9 acres ZONING: IND PK, Industrial Park PURCHASE PRICE: $3,600,000 cash UNIT PRICE: $11.91 per square foot COMMENTS: The site is level with utilities immediately available and all offsite

improvements in place. At the time of sale the site was improved with a 64,856-square-foot office/light industrial building. The buyer did not attribute any value to the building and expects the cost of demolition to be about $400,000 including demolition of the parking lot and landscaped areas. The site was purchased for the development of an 88,000-square-foot office building.

SALES HISTORY: The public records do not indicate a sale of this property within the

three years prior to the sale date. CONFIRMED BY: Sara Cabirac with CoStar, public records and a representative of the

buyer

MONTANDON FARLEY VALUATION SERVICES 49

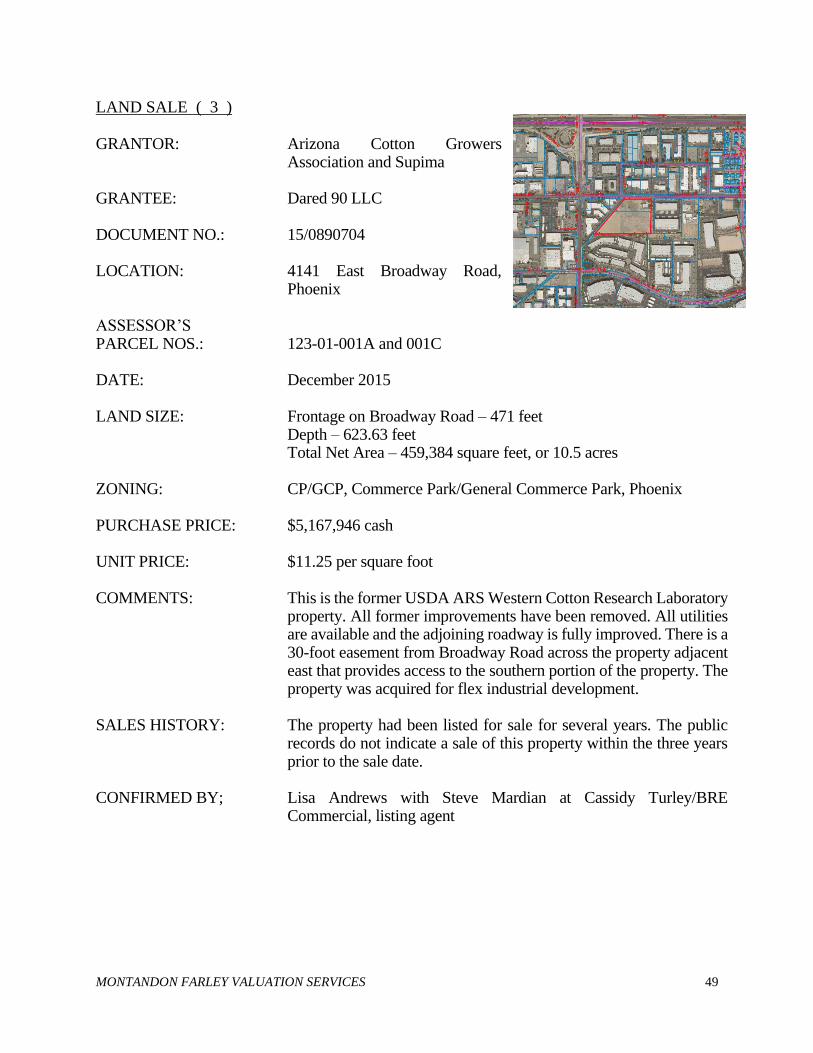

LAND SALE ( 3 ) GRANTOR: Arizona Cotton Growers

Association and Supima GRANTEE: Dared 90 LLC DOCUMENT NO.: 15/0890704 LOCATION: 4141 East Broadway Road,

Phoenix ASSESSOR’S PARCEL NOS.: 123-01-001A and 001C DATE: December 2015 LAND SIZE: Frontage on Broadway Road – 471 feet Depth – 623.63 feet Total Net Area – 459,384 square feet, or 10.5 acres ZONING: CP/GCP, Commerce Park/General Commerce Park, Phoenix PURCHASE PRICE: $5,167,946 cash UNIT PRICE: $11.25 per square foot COMMENTS: This is the former USDA ARS Western Cotton Research Laboratory

property. All former improvements have been removed. All utilities are available and the adjoining roadway is fully improved. There is a 30-foot easement from Broadway Road across the property adjacent east that provides access to the southern portion of the property. The property was acquired for flex industrial development.

SALES HISTORY: The property had been listed for sale for several years. The public

records do not indicate a sale of this property within the three years prior to the sale date.

CONFIRMED BY; Lisa Andrews with Steve Mardian at Cassidy Turley/BRE

Commercial, listing agent

MONTANDON FARLEY VALUATION SERVICES 50

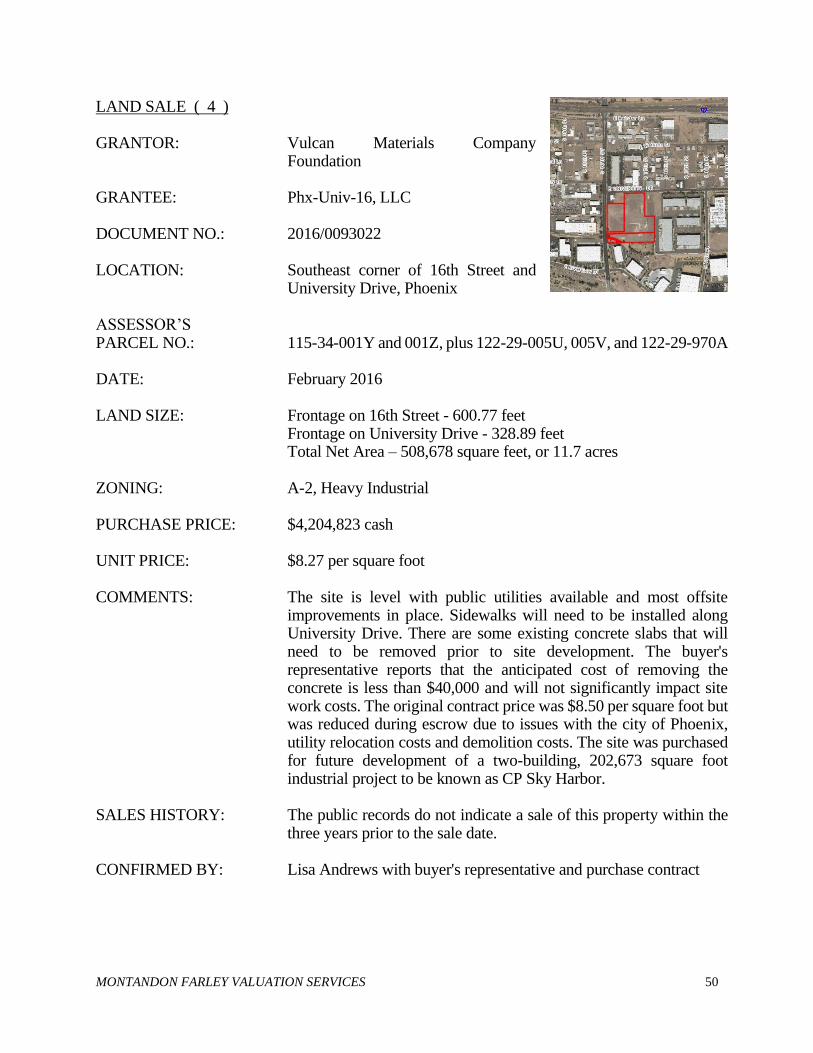

LAND SALE ( 4 ) GRANTOR: Vulcan Materials Company

Foundation GRANTEE: Phx-Univ-16, LLC DOCUMENT NO.: 2016/0093022 LOCATION: Southeast corner of 16th Street and

University Drive, Phoenix ASSESSOR’S PARCEL NO.: 115-34-001Y and 001Z, plus 122-29-005U, 005V, and 122-29-970A DATE: February 2016 LAND SIZE: Frontage on 16th Street - 600.77 feet Frontage on University Drive - 328.89 feet Total Net Area – 508,678 square feet, or 11.7 acres ZONING: A-2, Heavy Industrial PURCHASE PRICE: $4,204,823 cash UNIT PRICE: $8.27 per square foot COMMENTS: The site is level with public utilities available and most offsite

improvements in place. Sidewalks will need to be installed along University Drive. There are some existing concrete slabs that will need to be removed prior to site development. The buyer's representative reports that the anticipated cost of removing the concrete is less than $40,000 and will not significantly impact site work costs. The original contract price was $8.50 per square foot but was reduced during escrow due to issues with the city of Phoenix, utility relocation costs and demolition costs. The site was purchased for future development of a two-building, 202,673 square foot industrial project to be known as CP Sky Harbor.

SALES HISTORY: The public records do not indicate a sale of this property within the

three years prior to the sale date. CONFIRMED BY: Lisa Andrews with buyer's representative and purchase contract

MONTANDON FARLEY VALUATION SERVICES 51

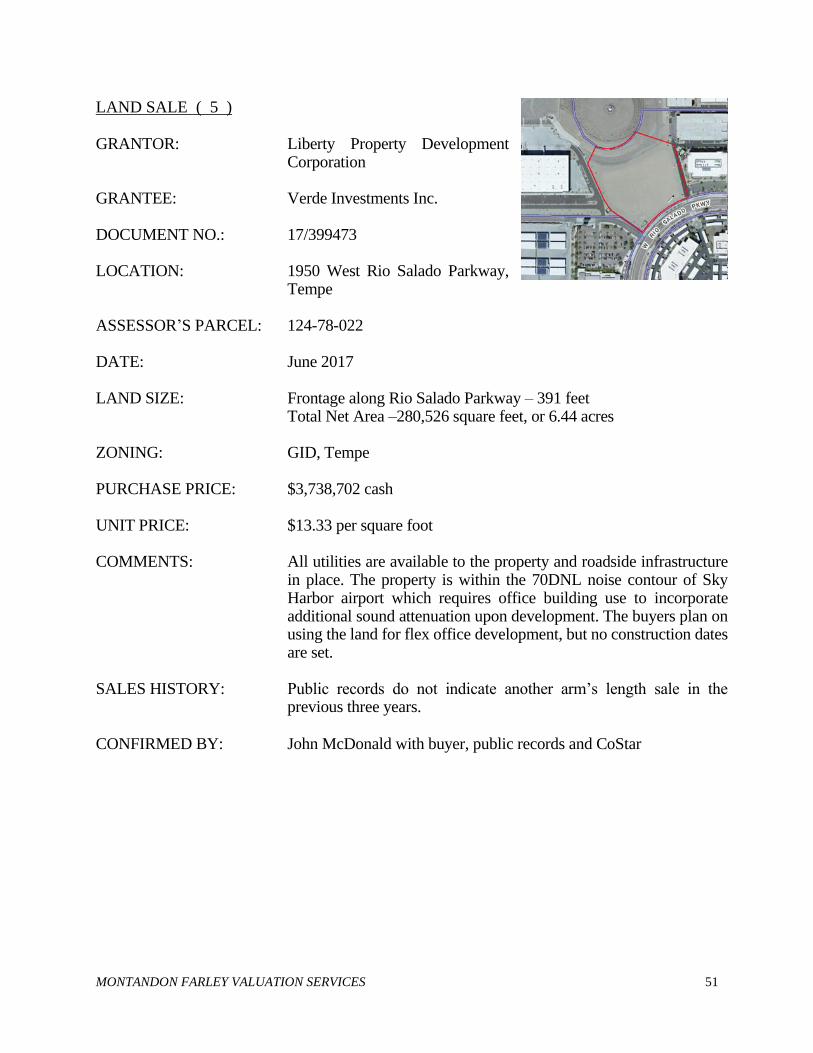

LAND SALE ( 5 ) GRANTOR: Liberty Property Development

Corporation GRANTEE: Verde Investments Inc. DOCUMENT NO.: 17/399473 LOCATION: 1950 West Rio Salado Parkway,

Tempe ASSESSOR’S PARCEL: 124-78-022 DATE: June 2017 LAND SIZE: Frontage along Rio Salado Parkway – 391 feet Total Net Area –280,526 square feet, or 6.44 acres ZONING: GID, Tempe PURCHASE PRICE: $3,738,702 cash UNIT PRICE: $13.33 per square foot COMMENTS: All utilities are available to the property and roadside infrastructure

in place. The property is within the 70DNL noise contour of Sky Harbor airport which requires office building use to incorporate additional sound attenuation upon development. The buyers plan on using the land for flex office development, but no construction dates are set.

SALES HISTORY: Public records do not indicate another arm’s length sale in the

previous three years. CONFIRMED BY: John McDonald with buyer, public records and CoStar

MONTANDON FARLEY VALUATION SERVICES 52

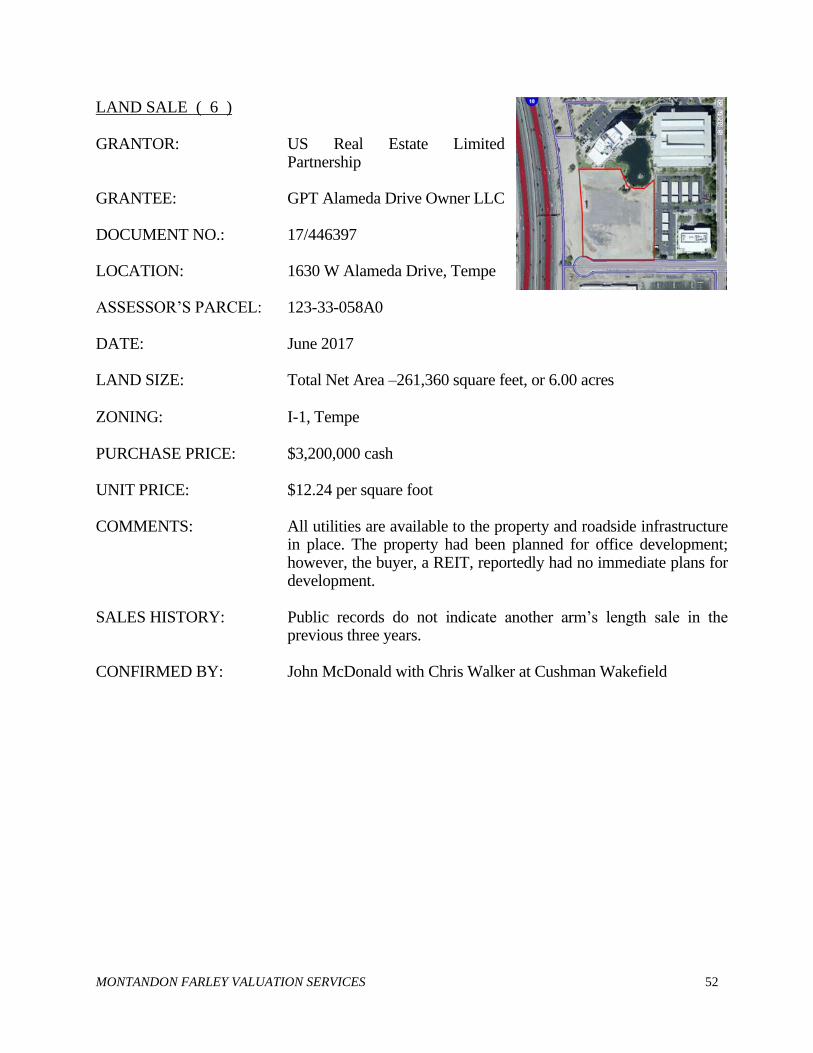

LAND SALE ( 6 ) GRANTOR: US Real Estate Limited

Partnership GRANTEE: GPT Alameda Drive Owner LLC DOCUMENT NO.: 17/446397 LOCATION: 1630 W Alameda Drive, Tempe ASSESSOR’S PARCEL: 123-33-058A0 DATE: June 2017 LAND SIZE: Total Net Area –261,360 square feet, or 6.00 acres ZONING: I-1, Tempe PURCHASE PRICE: $3,200,000 cash UNIT PRICE: $12.24 per square foot COMMENTS: All utilities are available to the property and roadside infrastructure

in place. The property had been planned for office development; however, the buyer, a REIT, reportedly had no immediate plans for development.

SALES HISTORY: Public records do not indicate another arm’s length sale in the

previous three years. CONFIRMED BY: John McDonald with Chris Walker at Cushman Wakefield

MONTANDON FARLEY VALUATION SERVICES 53

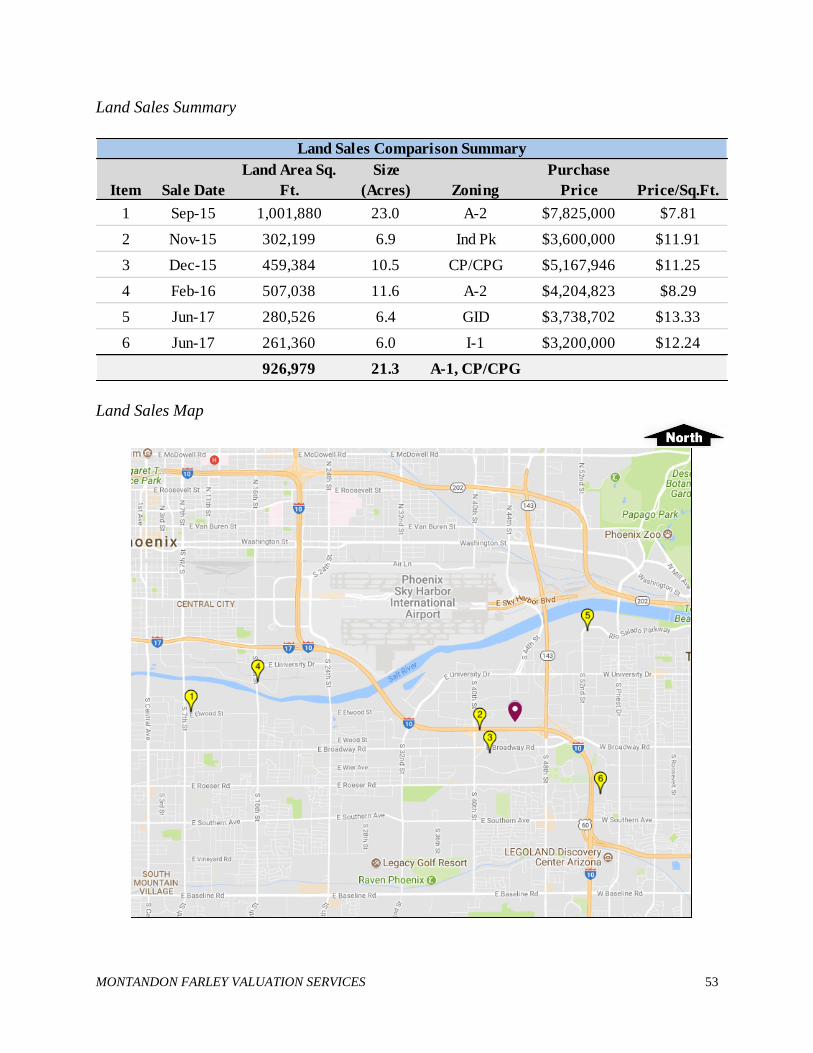

Land Sales Summary

Item Sale Date

Land Area Sq.

Ft.

Size

(Acres) Zoning

Purchase

Price Price/Sq.Ft.

1 Sep-15 1,001,880 23.0 A-2 $7,825,000 $7.81

2 Nov-15 302,199 6.9 Ind Pk $3,600,000 $11.91

3 Dec-15 459,384 10.5 CP/CPG $5,167,946 $11.25

4 Feb-16 507,038 11.6 A-2 $4,204,823 $8.29

5 Jun-17 280,526 6.4 GID $3,738,702 $13.33

6 Jun-17 261,360 6.0 I-1 $3,200,000 $12.24

926,979 21.3 A-1, CP/CPG

Land Sales Comparison Summary

Land Sales Map

MONTANDON FARLEY VALUATION SERVICES 54

Adjustment Analysis

The unit of comparison used in this approach is the price-per-square-foot-of-land-area. The sales have been compared to the subject property with respect to the following items. 1) Property Rights Conveyed 2) Financing (Cash Equivalency) 3) Conditions of Sale 4) Expenditures made immediately after purchase 5) Market Conditions (Time) 6) Location 7) Physical Characteristics 8) Economic Characteristics 9) Use (Zoning) A grid illustrating the adjustments to the individual sales follows the discussion. Property Rights Conveyed

The interest being valued in this section of the report is that of the fee simple estate. None of the sales involve ground leases; therefore, no adjustments are necessary. Financing

The sales were cash transactions and do not require adjustment for comparison purposes. Conditions of Sale

Adjustments for conditions of sale are made when the buyer or seller had atypical motivations. In our opinion, no adjustments to the sales are deemed necessary. Expenditures Made Immediately After Purchase Sale 2 was improved with an existing office/light industrial building that the buyer planned to demolish at a projected cost of about $400,000 or a rounded 10% of its value. We have adjusted the comparison upward for this factor. No other adjustments are necessary. Market Conditions

The sales comparisons have occurred over the past two and one-quarter years. Our discussions with industrial brokers familiar with the subject area report that property values have been increased since late 2015 but have remained relatively stable over the past nine months. We have adjusted Sales 1 through 4 upward for improved market conditions since their late 2015 and early 2016 sale dates.

MONTANDON FARLEY VALUATION SERVICES 55

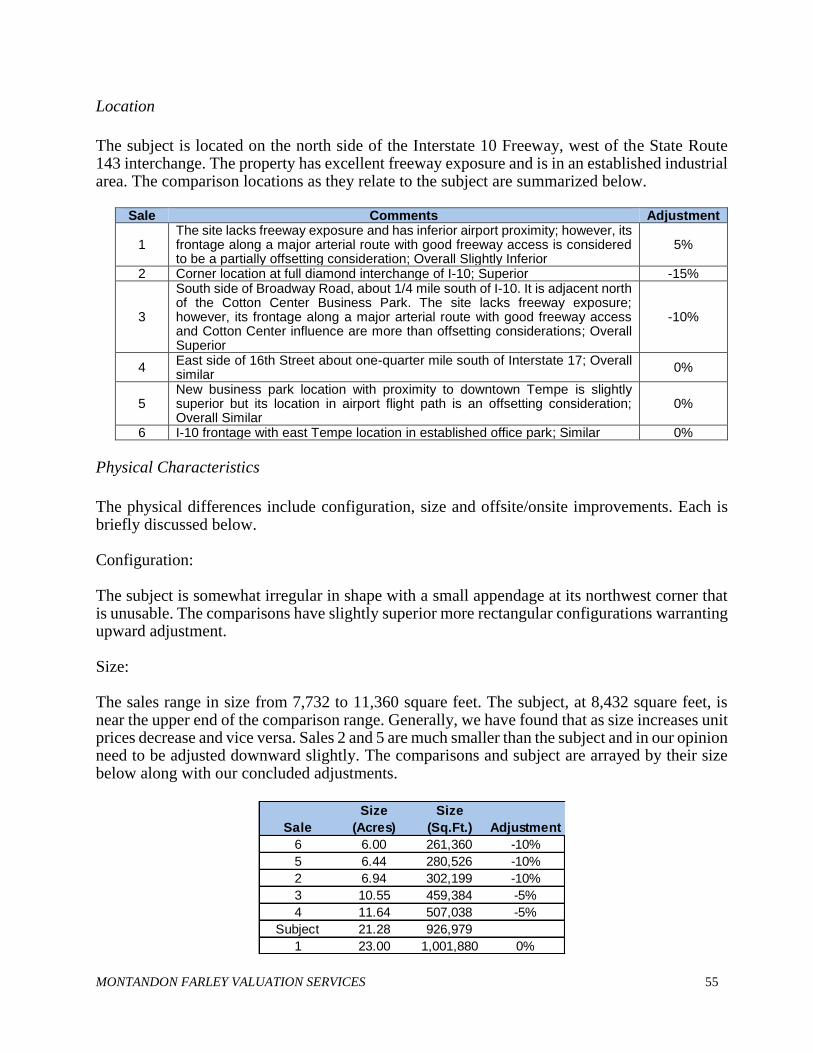

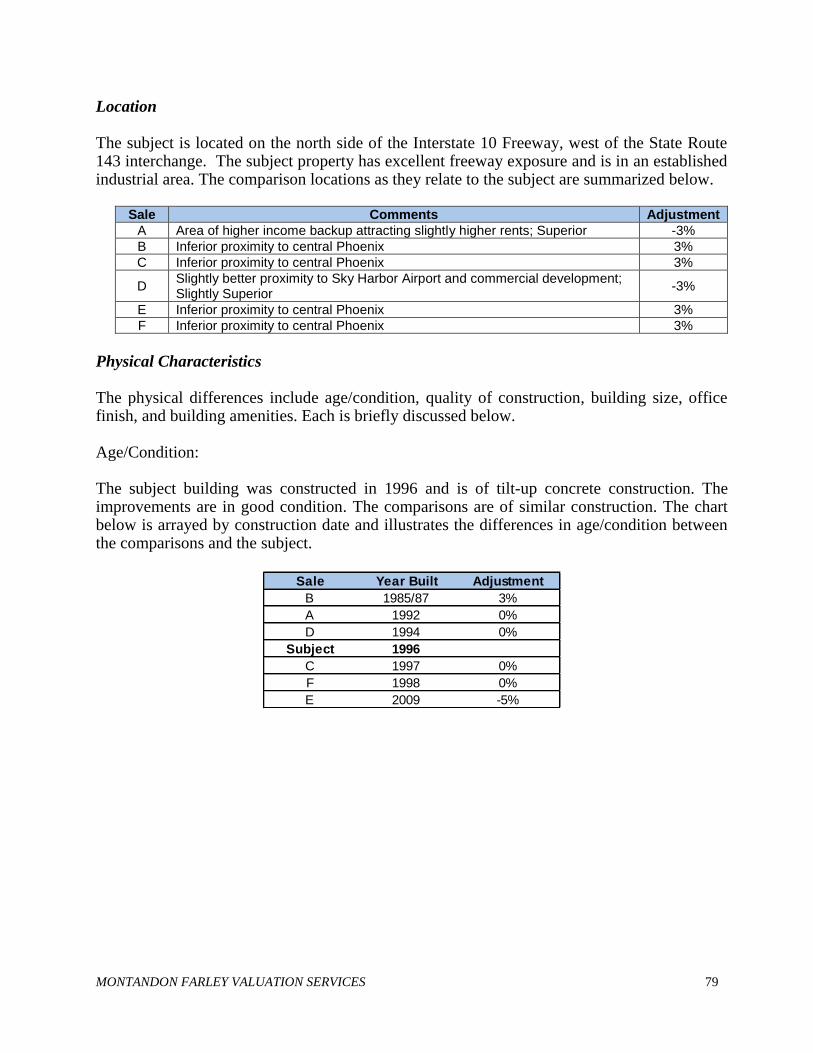

Location

The subject is located on the north side of the Interstate 10 Freeway, west of the State Route 143 interchange. The property has excellent freeway exposure and is in an established industrial area. The comparison locations as they relate to the subject are summarized below.

Sale Comments Adjustment

1 The site lacks freeway exposure and has inferior airport proximity; however, its frontage along a major arterial route with good freeway access is considered to be a partially offsetting consideration; Overall Slightly Inferior

5%

2 Corner location at full diamond interchange of I-10; Superior -15%

3

South side of Broadway Road, about 1/4 mile south of I-10. It is adjacent north of the Cotton Center Business Park. The site lacks freeway exposure; however, its frontage along a major arterial route with good freeway access and Cotton Center influence are more than offsetting considerations; Overall Superior

-10%

4 East side of 16th Street about one-quarter mile south of Interstate 17; Overall similar

0%

5 New business park location with proximity to downtown Tempe is slightly superior but its location in airport flight path is an offsetting consideration; Overall Similar

0%

6 I-10 frontage with east Tempe location in established office park; Similar 0%

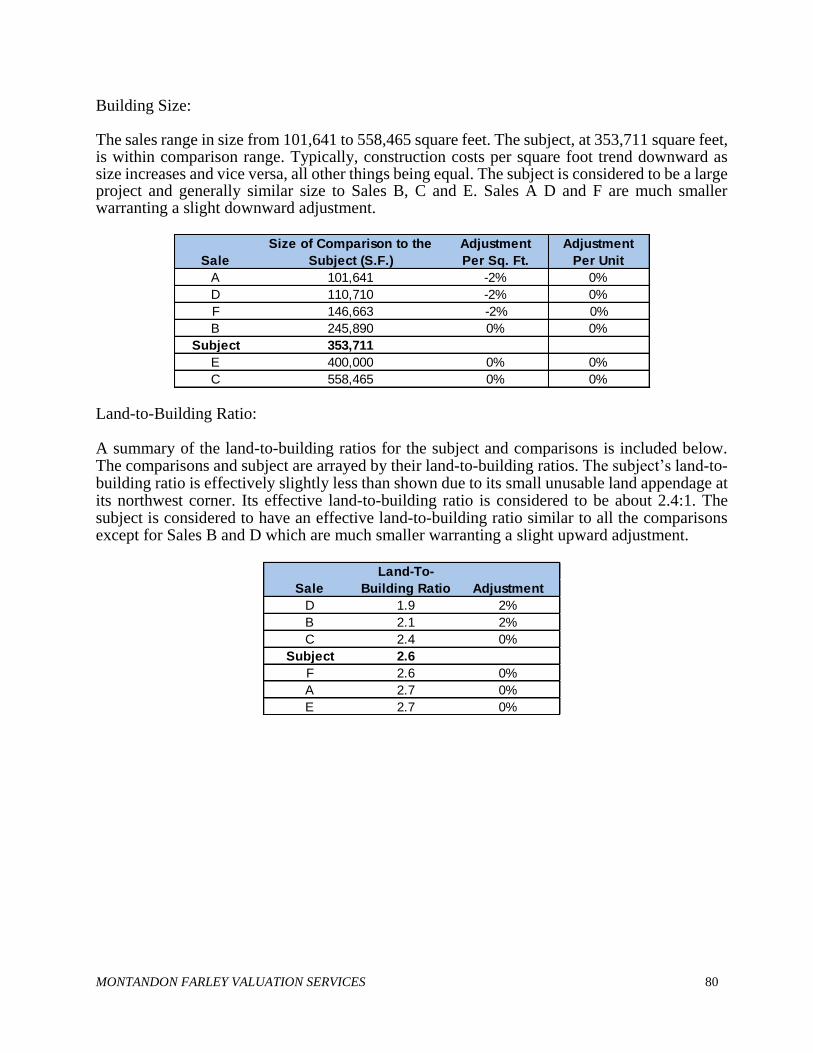

Physical Characteristics

The physical differences include configuration, size and offsite/onsite improvements. Each is briefly discussed below. Configuration: The subject is somewhat irregular in shape with a small appendage at its northwest corner that is unusable. The comparisons have slightly superior more rectangular configurations warranting upward adjustment. Size: The sales range in size from 7,732 to 11,360 square feet. The subject, at 8,432 square feet, is near the upper end of the comparison range. Generally, we have found that as size increases unit prices decrease and vice versa. Sales 2 and 5 are much smaller than the subject and in our opinion need to be adjusted downward slightly. The comparisons and subject are arrayed by their size below along with our concluded adjustments.

Sale

Size

(Acres)

Size

(Sq.Ft.) Adjustment

6 6.00 261,360 -10%

5 6.44 280,526 -10%

2 6.94 302,199 -10%

3 10.55 459,384 -5%

4 11.64 507,038 -5%

Subject 21.28 926,979

1 23.00 1,001,880 0%

MONTANDON FARLEY VALUATION SERVICES 56

Offsite/Onsite improvements:

The subject has all utilities to the site and all roadside infrastructure in place. Except for Sale 4

all the comparisons are similar with utilities and roadside infrastructure in place. Sale 4 will

require the installation of concrete sidewalks along its University Drive frontage (335± feet). In

addition, there are some existing concrete slabs on the site that must be removed although the

buyer representative reported that the cost of removal was less than $40,000 and didn’t

significantly impact the site development costs. Upward adjustments for the on and offsite costs

associated with Sales 4 warrant upward adjustment.

Economic Characteristics

No adjustments are deemed necessary for economic characteristics.

Use (Zoning)

No adjustments are deemed necessary for use potential.

MONTANDON FARLEY VALUATION SERVICES 57

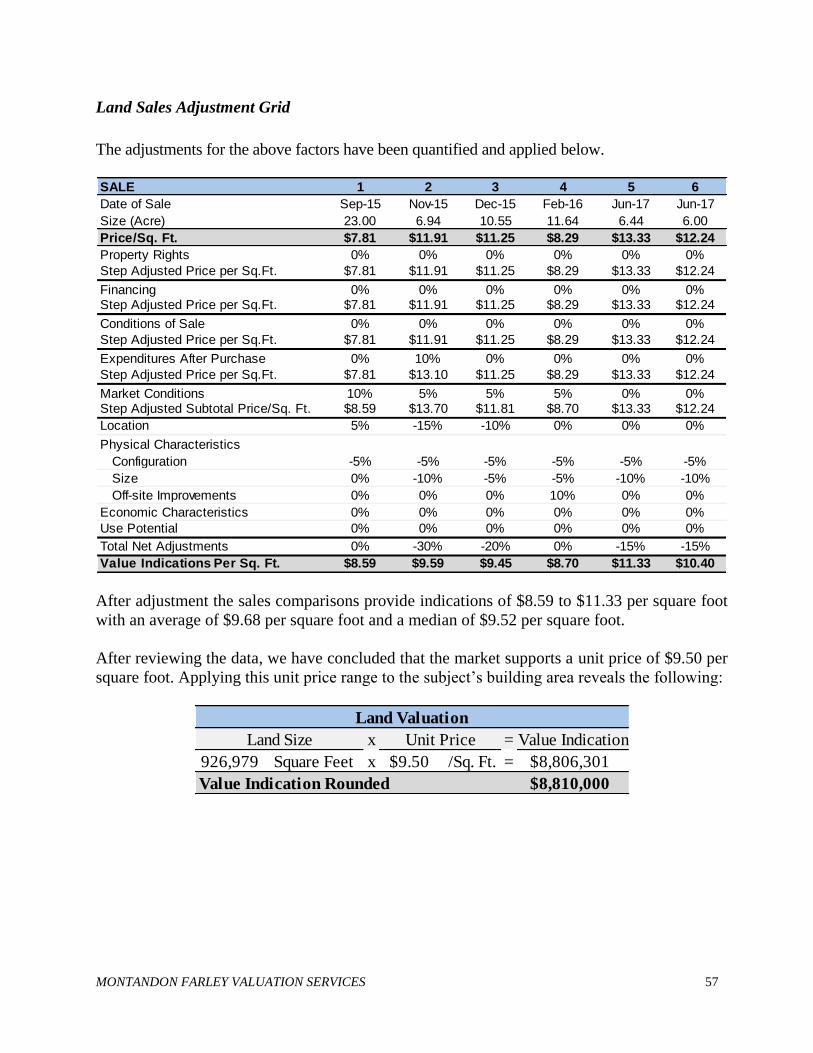

Land Sales Adjustment Grid

The adjustments for the above factors have been quantified and applied below.

SALE 1 2 3 4 5 6

Date of Sale Sep-15 Nov-15 Dec-15 Feb-16 Jun-17 Jun-17

Size (Acre) 23.00 6.94 10.55 11.64 6.44 6.00

Price/Sq. Ft. $7.81 $11.91 $11.25 $8.29 $13.33 $12.24

Value Indications Per Sq. Ft. $8.59 $9.59 $9.45 $8.70 $11.33 $10.40 After adjustment the sales comparisons provide indications of $8.59 to $11.33 per square foot

with an average of $9.68 per square foot and a median of $9.52 per square foot.

After reviewing the data, we have concluded that the market supports a unit price of $9.50 per

square foot. Applying this unit price range to the subject’s building area reveals the following:

x = Value Indication

926,979 Square Feet x $9.50 /Sq. Ft. = $8,806,301

Value Indication Rounded $8,810,000

Unit Price

Land Valuation

Land Size

MONTANDON FARLEY VALUATION SERVICES 58

Replacement Cost of the Improvements Replacement cost1 is defined as: The estimated cost to construct, at current prices as of the effective appraisal date, a

substitute for the building being appraised, using modern materials and current standards, design, and layout.

Direct Costs In order to estimate the reasonableness of the developer’s costs budget and to estimate the cost new of the proposed subject improvements, we have considered the Marshall Valuation Service cost manual, published by Marshall & Swift, which is an authoritative construction cost publication commonly used by cost estimators and real estate appraisers. Cost estimates within this publication are averages of final costs, including architect fees, contractor’s overhead and profit, (sales tax, permit fees, insurance during construction, interest on interim construction financing, etc.) The estimated cost of the building, using this source, is discussed next. In order estimate a direct cost estimate we have considered several recent cost comparisons. Two specific comparisons are discussed on the following page. Comparison No. 1: In early 2016 we reviewed the construction budget for a two-building 203,000-square-foot industrial project planned for an 11.6-acre site along the Interstate 10 corridor. The buildings will be of concrete tilt panel construction, have about 7% office build out and feature an interior clear height of 28 to 32 feet. There will be 61 dock high loading doors and 8 grade level doors. The interior was expected to include a modest amount of office area with the remaining space being evaporative cooled warehouse area. The direct cost of the improvements is budgeted at approximately $53.00 per square foot, including an average tenant improvement allowance of $10.89 per square foot. The buildings had a lesser amount of office build out than the subject warranting a slight upward adjustment. A higher direct cost is indicated for the subject. Comparison No. 2: We reviewed the construction budget for a two-building 215,000-square-foot industrial project that was constructed in late 2016 on a 14.5-acre site along the Interstate 10 corridor. The buildings are of concrete tilt panel construction and feature an interior clear height of 32 feet. They have 54 dock high loading doors and 8 grade level doors. The interior was expected to include a modest amount of office area with the remaining space being evaporative cooled warehouse area. The direct cost of the improvements was budgeted at approximately $58.50 per square foot, including a tenant improvement allowance of $12.50 per square foot.

1 The Dictionary of Real Estate Appraisal, Fifth Edition, Appraisal Institute, (Chicago, Illinois: 2010), p. 168.

MONTANDON FARLEY VALUATION SERVICES 59

The buildings had a slightly lesser percentage of office build out than the subject warranting a

slight upward adjustment. However, this comparison’s greater clear height is an offsetting

consideration.

We have also considered the Marshall Valuation Service cost manual, which is an authoritative

construction cost publication. Cost estimates within this publication are averages of final costs,

including architect fees, contractor’s overhead and profit, (sales tax, permit fees, insurance

during construction, interest on interim construction financing, etc.).

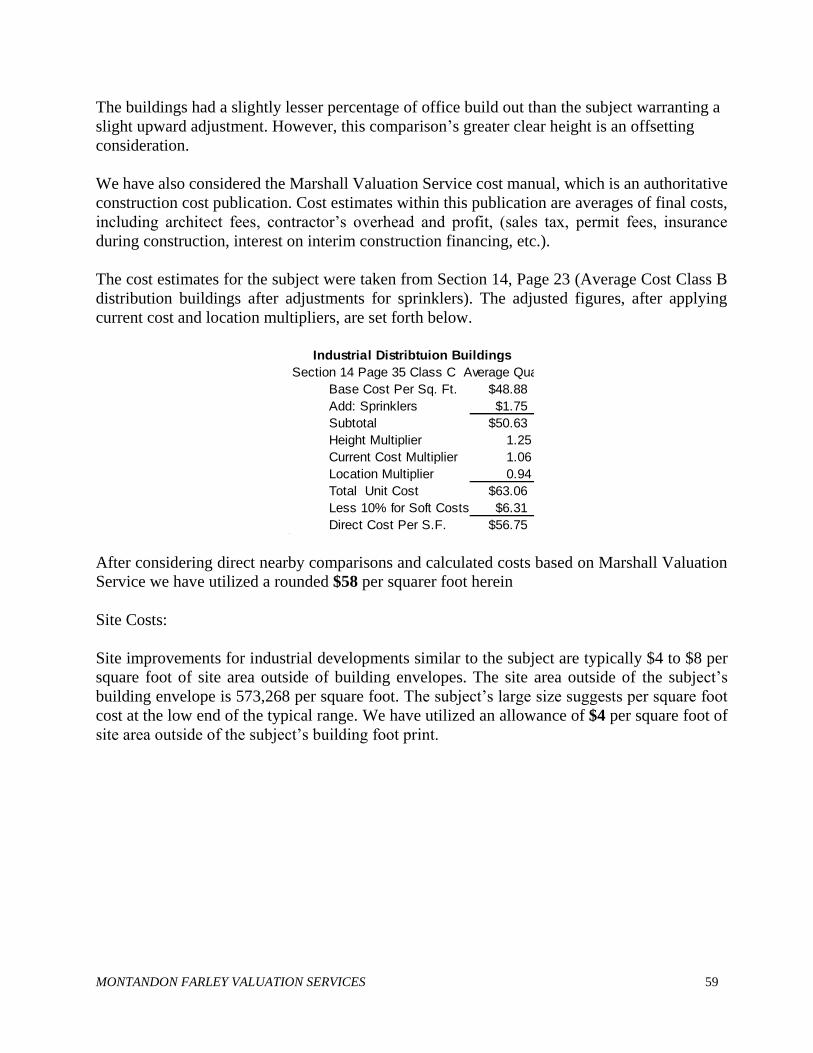

The cost estimates for the subject were taken from Section 14, Page 23 (Average Cost Class B

distribution buildings after adjustments for sprinklers). The adjusted figures, after applying

current cost and location multipliers, are set forth below.

Section 14 Page 35 Class C Average Quality

Base Cost Per Sq. Ft. $48.88

Add: Sprinklers $1.75

Subtotal $50.63