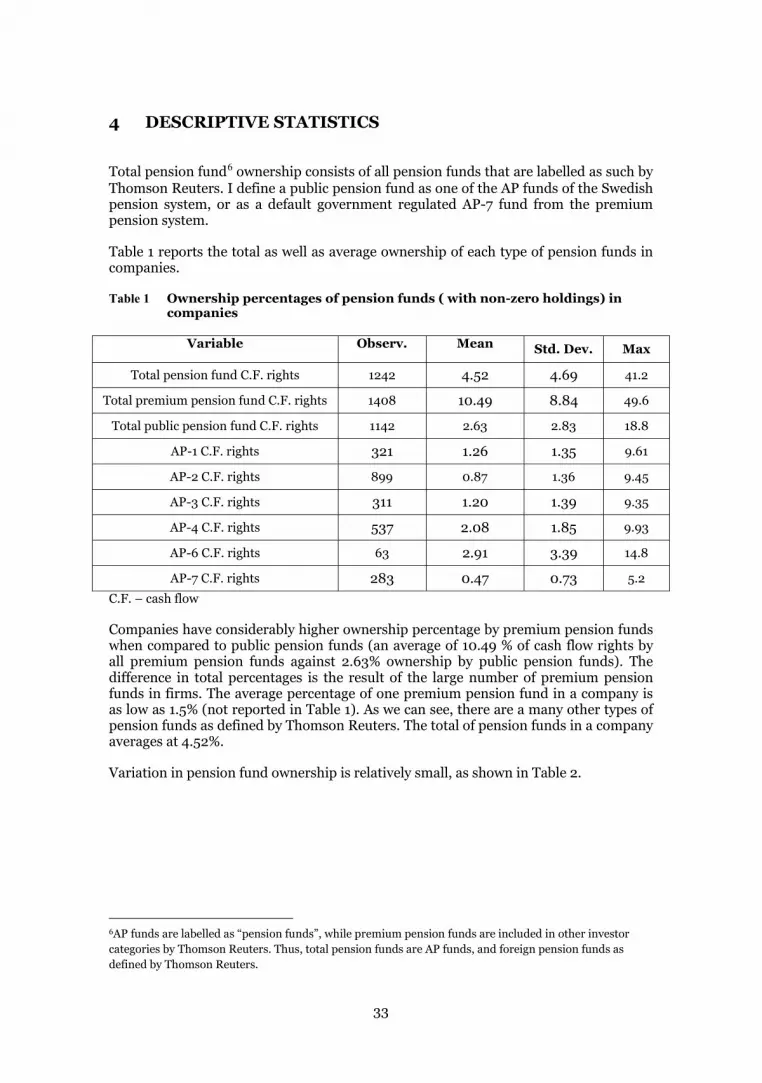

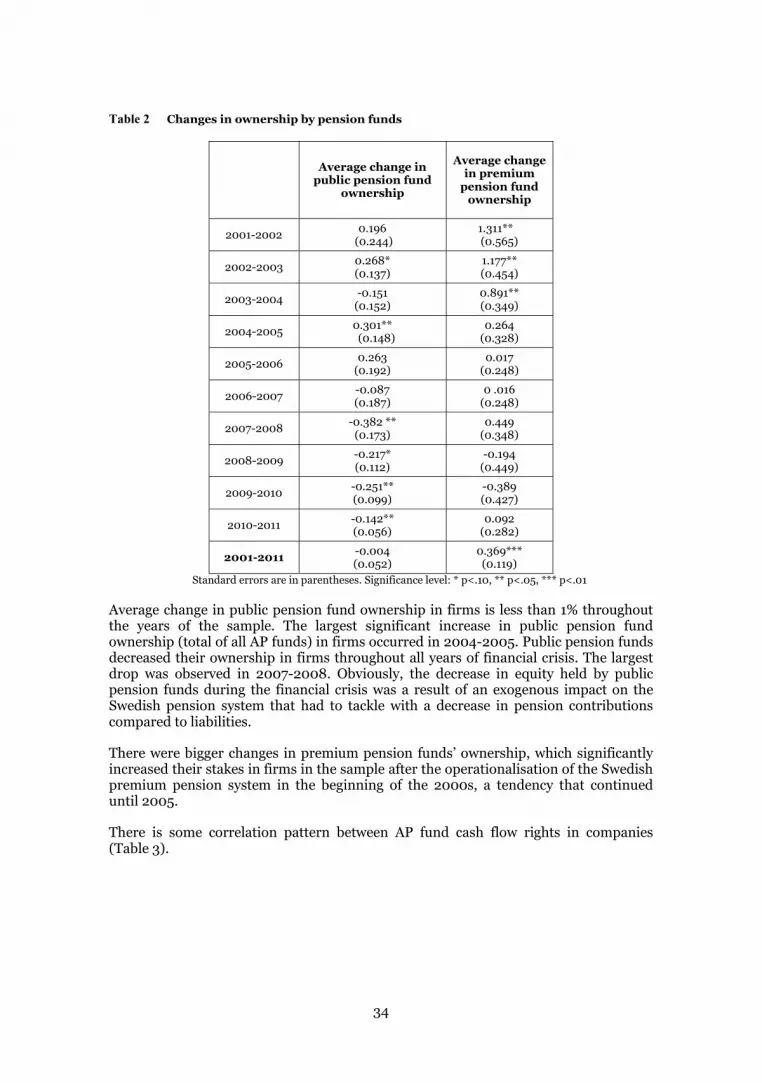

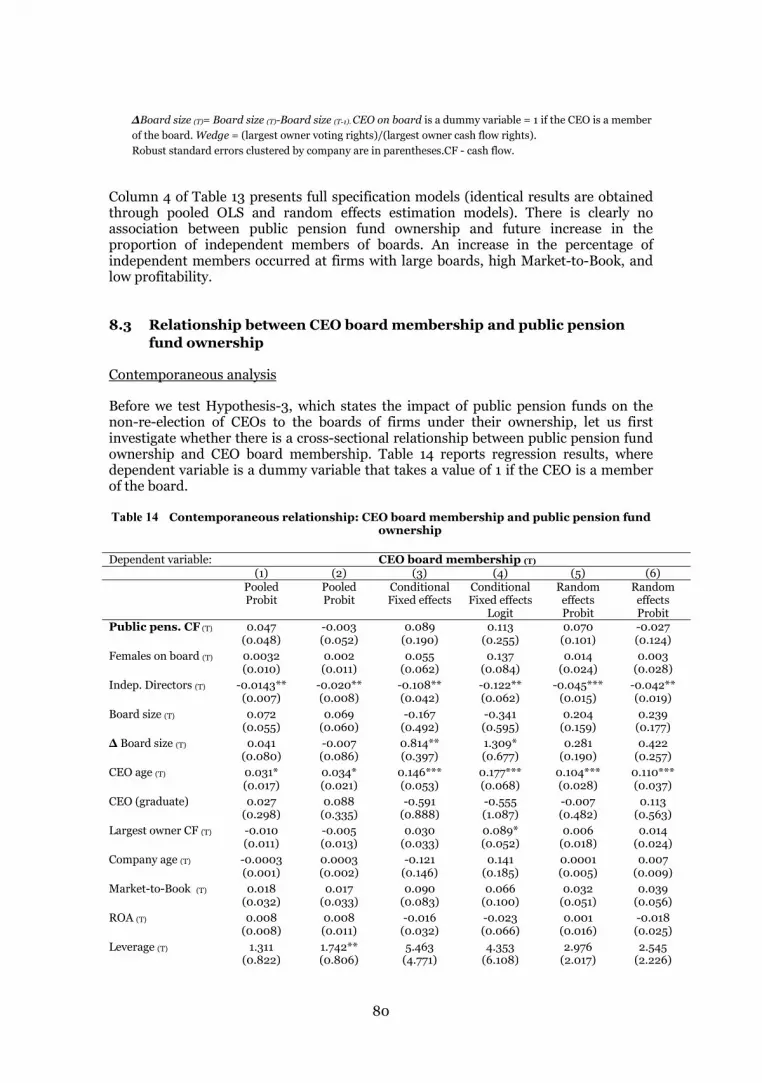

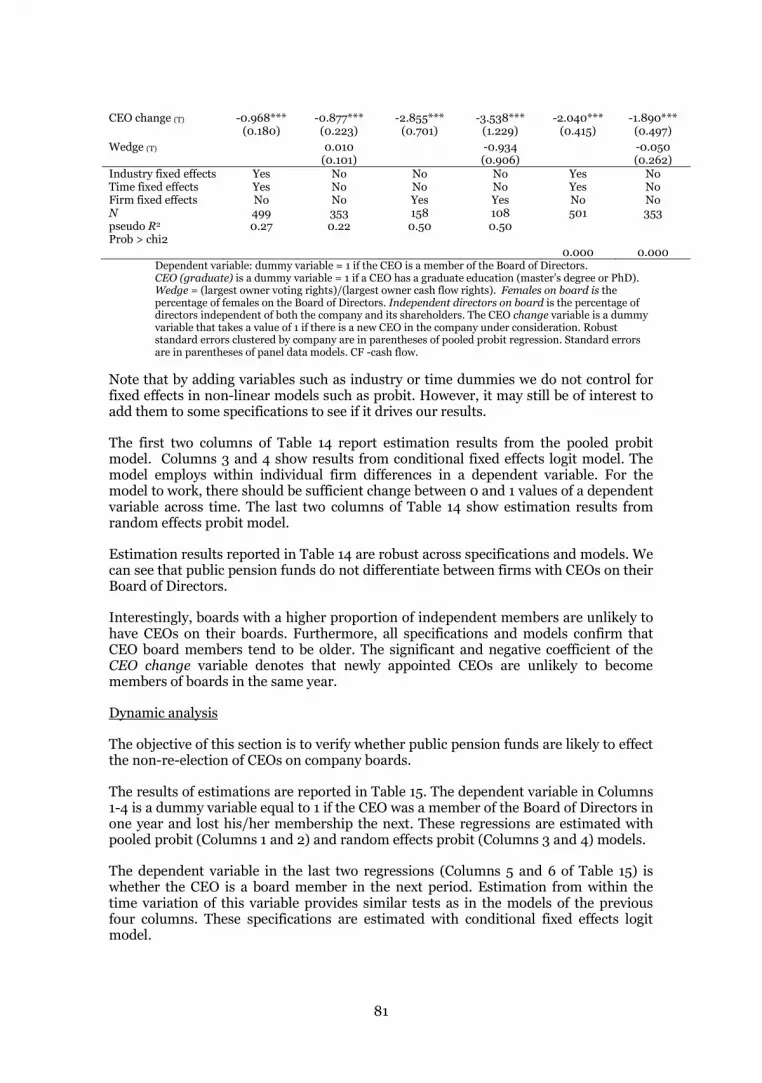

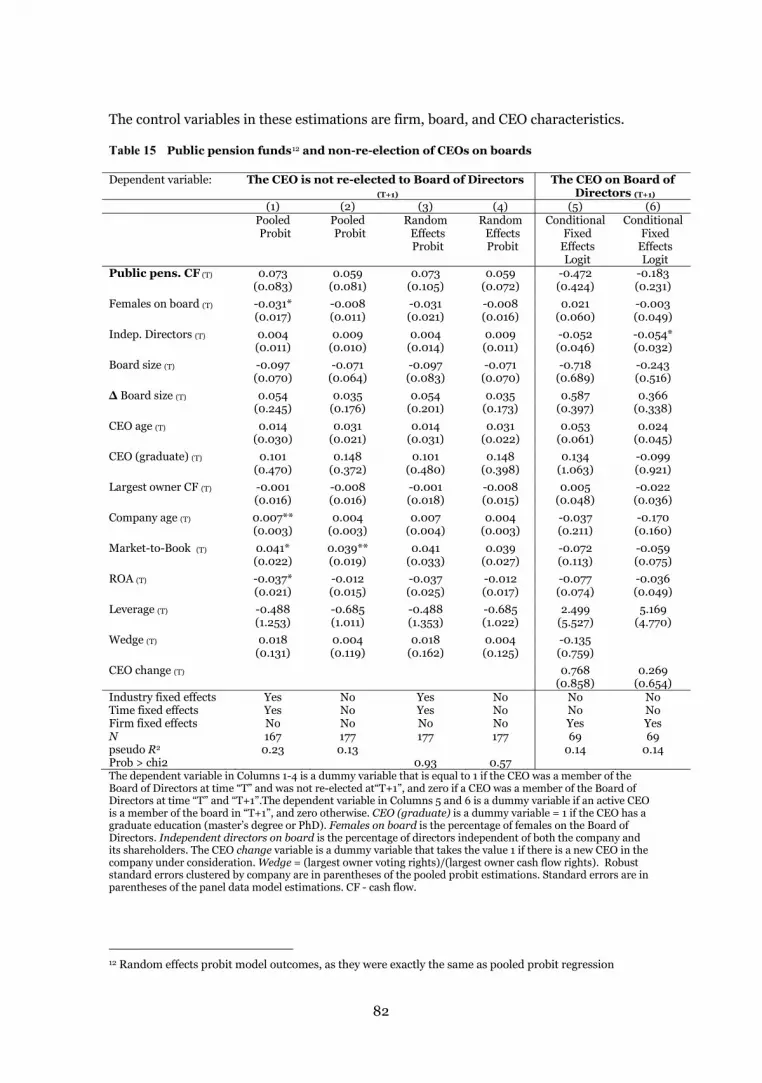

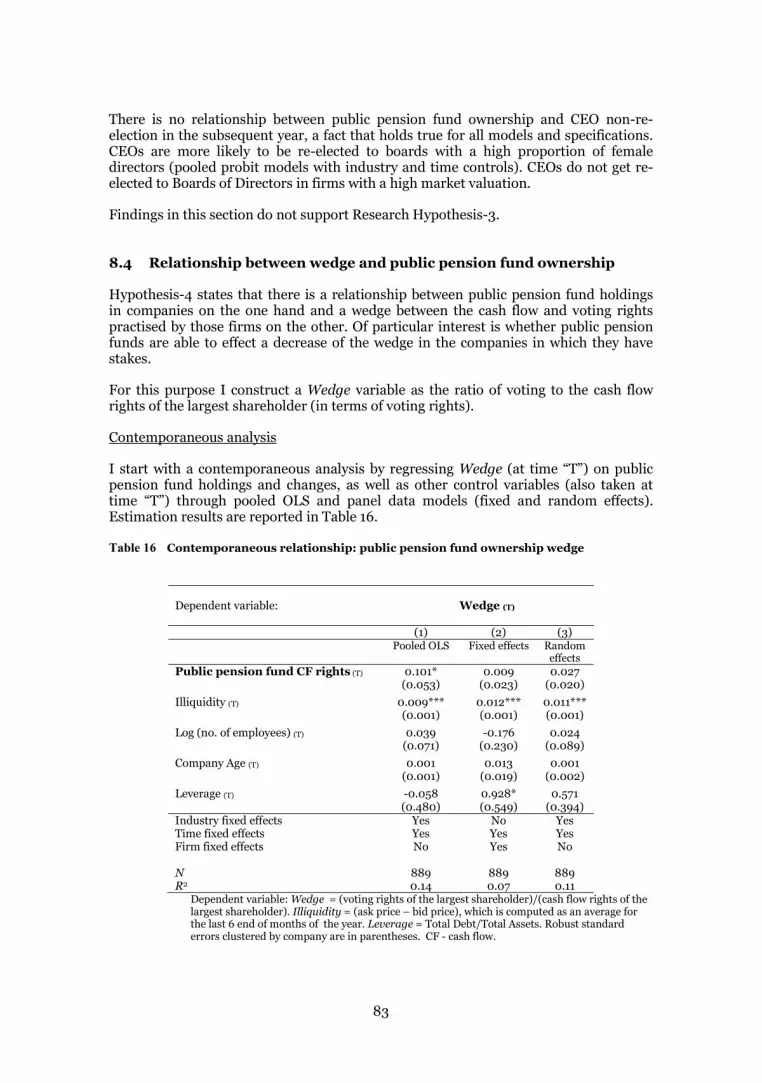

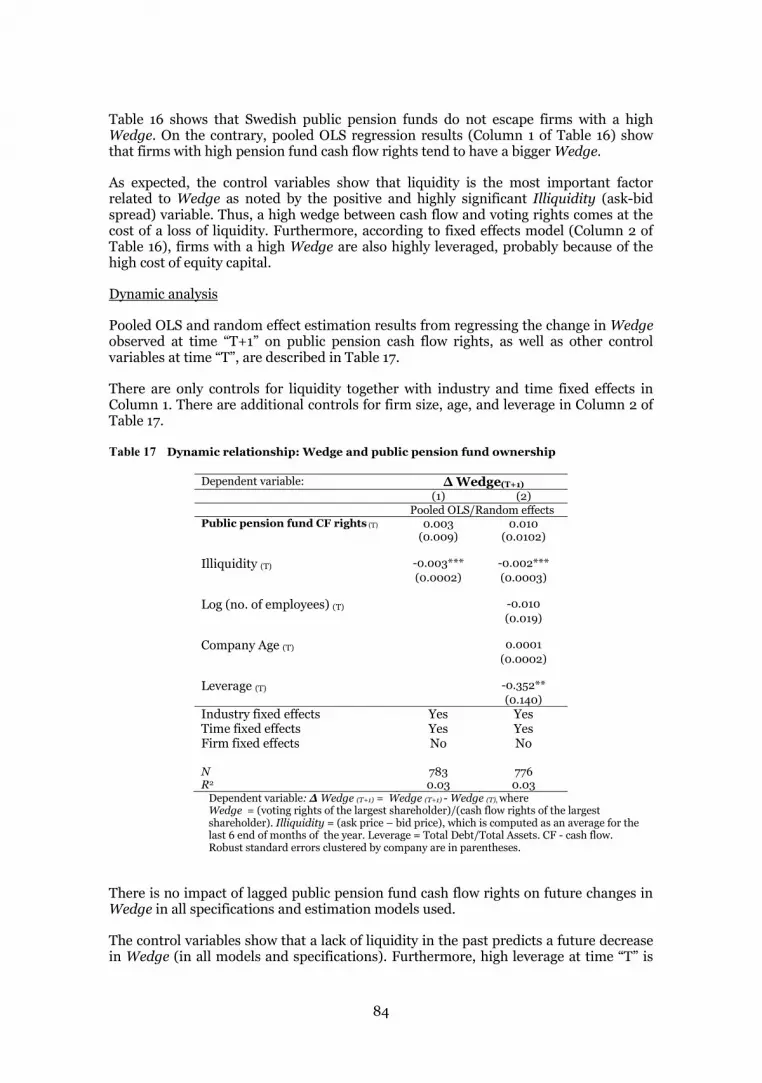

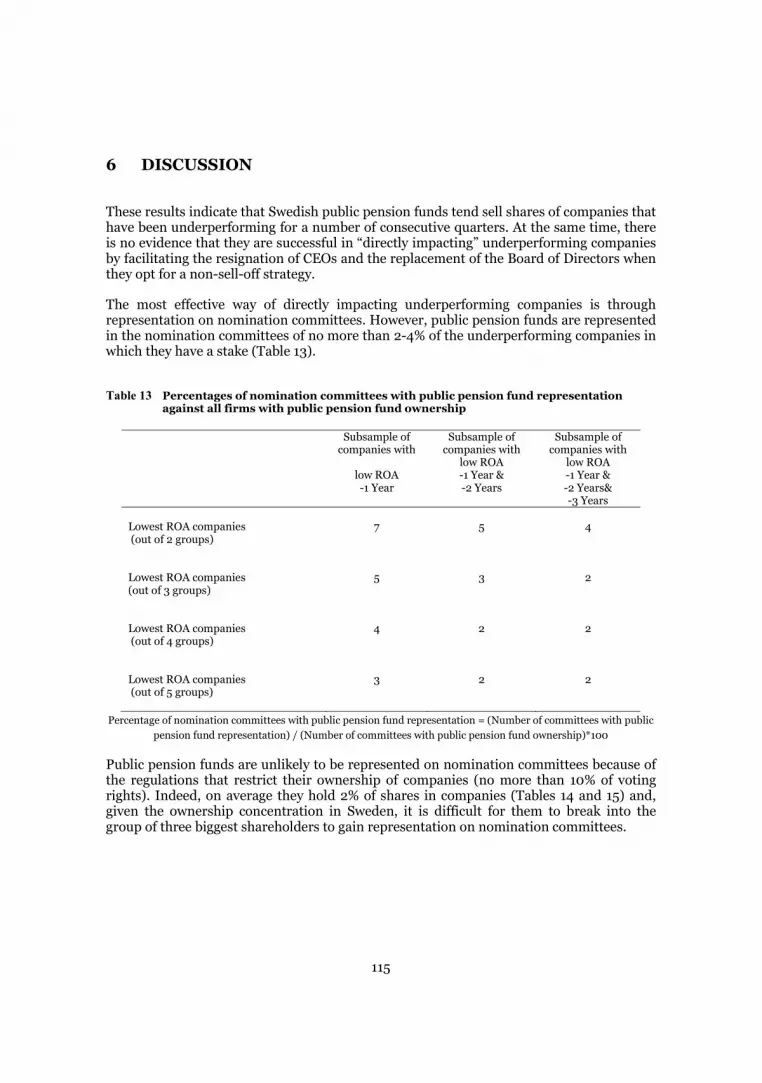

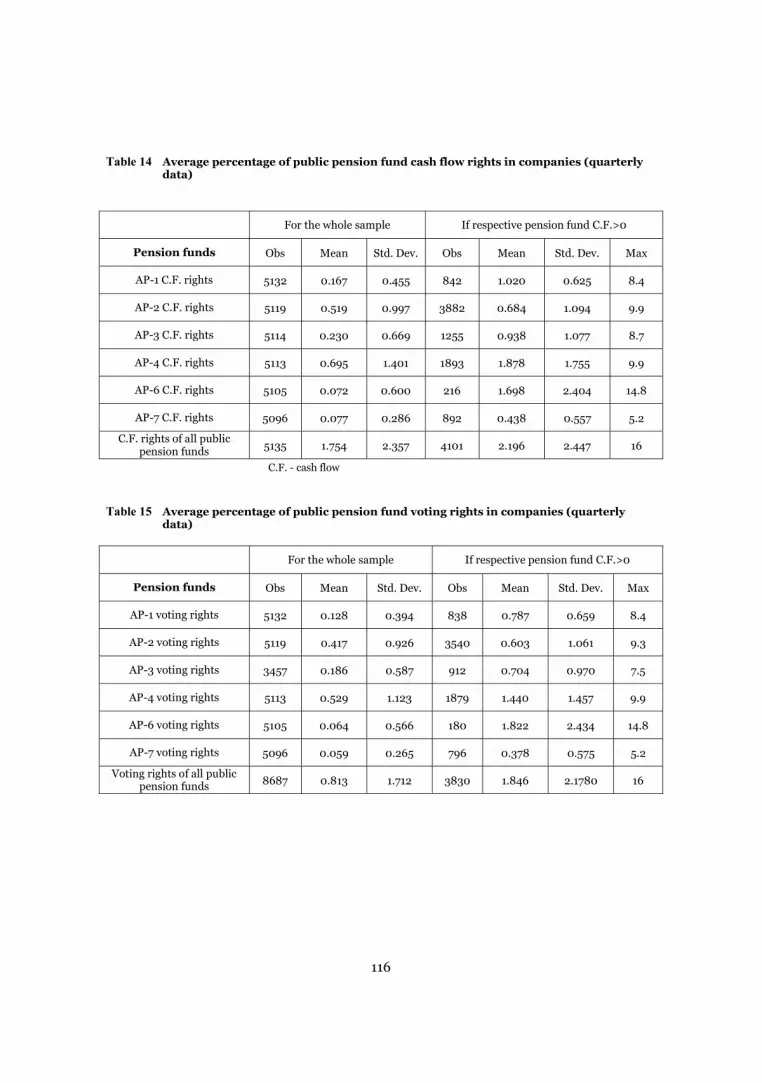

169

| Date post: | 10-Nov-2023 |

| Category: |

Documents |

| Upload: | khangminh22 |

| View: | 0 times |

| Download: | 0 times |

NAUFAL ALIMOV – INSTITUTIONAL INVESTORS AS SHAREHOLDERS

INSTITUTIONAL INVESTORS AS SHAREHOLDERSTHE CASE OF PENSION FUNDS

NAUFAL ALIMOV

EKONOMI OCH SAMHÄLLE ECONOMICS AND SOCIETY

308

NAUFAL ALIMOV

INSTITUTIONAL INVESTORS AS SHAREHOLDERS: THE CASE OF PENSION FUNDS

Institutional ownership in publicly listed companies has grown rapidly in recent decades. It is claimed that insti-tutional investors are well-suited for active involvement in firms’ corporate governance, because they are managed by professional managers who can utilise information bet-ter than lay investors. However, efficient governance may not be in the best interest of asset managers employed by institutional investors. The final role of institutional investors in corporate governance therefore remains an empirical question. In this dissertation, I empirically investigate the role of

public pension funds in firms’ governance, using the data from the Swedish pension system, which was reformed at the turn of the millennium. This data was chosen because Swedish public pension funds have the same history and mandates, and are expected to compete with each other. The thesis consists of four essays. In the first two, I inves-

tigate whether Swedish pension fund ownership is related to firms’ market valuation and corporate governance qual-ity. In paper three, I analyse whether these funds prefer to impact or exit underperforming firms. In the final paper, I examine whether there are similarities in the composition of the Swedish public pension funds’ domestic equity port-folios, and whether these funds adopt similar strategies in selling and buying shares of Swedish listed companies.I find that there is a contemporaneous positive relation-

ship between firms’ market valuation and public pension

fund ownership. The evidence suggests that this relation-ship is a result of public pension funds’ preference for in-vesting in firms the market values highly. My results show that public pension fund ownership in

companies is not associated with better corporate gover-nance. I find no evidence that these funds effect the diver-sification of boards by increasing the proportion of wom-en, foreigners, or directors of various ages. Furthermore, Swedish public pension funds have not been successful in promoting independent directors, securing the non-re-election of an active CEO to the Board of Directors, and reducing the wedge between cash flow and voting rights in listed firms.The analysis indicates that public pension funds tend

to sell their shares of underperforming companies, rather than facilitate the dismissal of the CEO or the Board of Di-rectors. In the final paper, I find that there has been a relatively

high degree of similarity in the domestic equity portfolios of the Swedish public pension funds. My analysis also shows that these funds have timed their purchases and sales of company shares in approximately the same way. These findings are probably the result of the constraints of a small and illiquid market for individual shares and the Swedish pension system’s stringent investment rules.

HANKEN

SCHOOL OF ECONOMICS

HELSINKI

ARKADIANKATU 22, P.O. BOX 479

00101 HELSINKI, FINLAND

TEL +358 (0)9 431 331. FAX +358 (0)9 431 33 333

VAASA

KIRJASTONKATU 16, P.O. BOX 287

65101 VAASA, FINLAND

TEL +358 (0)6 3533 700. FAX +358 (0)6 3533 703

HANKEN.FI/DHANKEN

ISBN 978-952-232-327-9 (printed)

ISBN 978-952-232-328-6 (PDF)

ISSN-L 0424-7256

ISSN 0424-7256 (printed)

ISSN 2242-699X (PDF)

JUVENES PRINT, HELSINKI

Ekonomi och samhälle Economics and Society

Skrifter utgivna vid Svenska handelshögskolan Publications of the Hanken School of Economics

No 308

Naufal Alimov

Institutional Investors as Shareholders

The Case of Pension Funds

Helsinki 2016 <

Institutional investors as shareholders: The case of pension funds

Key words: Institutional investor, pension funds, corporate governance, competition

© Hanken School of Economics & Naufal Alimov, 2016

Naufal Alimov Hanken School of Economics Department of Economics P.O.Box 479, 00101 Helsinki, Finland

Hanken School of Economics ISBN 978-952-232-327-9 (printed) ISBN 978-952-232-328-6 (PDF) ISSN-L 0424-7256 ISSN 0424-7256 (printed) ISSN 2242-699X (PDF)

Juvenes Print – Suomen Yliopistopaino Oy, Helsinki 2016

i

ACKNOWLEDGEMENTS

I am finally at the end of my PhD studies’ long journey. I had no clear idea of what to expect when I arrived in Finland with my wife and son some years ago. The journey had its ups and downs – learning contemporary research techniques during course work, financial difficulties, and an extended quest to find myself as a researcher. It took me a long time to understand that a PhD study is actually a process of transformation on the journey to becoming an unbiased researcher.

First, I would like to express my sincerest gratitude to my supervisor, Professor Tom Berglund, who was much more than my doctoral degree supervisor. He has constantly challenged my way of thinking, inspired me towards better research, and contributed immensely to my formation as a personality. His help in finding solutions for my various problems made my family’s life in Finland run more smoothly. I will always remember our exciting discussions at lunches and other shared activities. He laid out the fundamentals for my future career!

I am extremely grateful to my thesis supervisor, Professor Martin Holmen, for his patience in reading my drafts and providing me with valuable comments and suggestions for improvement. He has encouraged and supported me throughout the process of my dissertation project.

I would like express my gratitude to my pre-examiners, Professor Johan Eklund and, especially, Professor Harley E. Ryan Jr., who have carefully read through my dissertation, and made excellent comments. Their thoughts and suggestions assisted me in taking my analyses further, and have resulted in an improved manuscript.

I am grateful to the participants of the Economics Department’s seminars for their insightful comments. I would especially like to thank Professor Rune Stenbacka, who reviewed my manuscript and gave valuable suggestions for improvement during our follow-up meeting.

I greatly enjoyed participating with presentations and listening to other researchers’ presentations during our small group seminars. I therefore wish to thank Tom Berglund, Laura Arranz Aperte, Robert Gillanders, Olga Neselevska, Jyri Kinnunen, Praveen Malla, Minna Martikainen, Benjamin Maury, Henrik Keinonen, Jonas Spohr, Jakob Strorå, Pontus Troberg, and Tuomas Takalo.

I have benefited greatly from participating in presentations at the annual Nordic Corporate Governance workshops (Stockholm, Copenhagen, and Helsinki). I value the constructive comments of Dr Sophie Nachemson-Ekwall, Professor Per-Olof Bjuggren, and Dr Conny Overland, who reviewed the papers included in this dissertation.

I am also grateful to the participants of the annual PhD workshop organised by the Hanken Centre for Corporate Governance. I would like to thank specially appointed faculty: Professor Ulf Jakobsson, Dr Daniel Wieberg, and Dr Tor Brunzell, who made comments and suggestions that considerably improved my research papers.

I would like to thank participants of GSF/FDPE Winter Research Workshop in Finance (Helsinki), especially Dr Mikko Leppämäki for comments on my research project.

ii

Professor Runer Stenbacka, Dr Staffan Ringbom, and Professor Topi Miettinen, who were the heads of the Economics Department of Hanken of the period of my PhD studies, have helped me with a number of important issues. I am very grateful to them.

I am grateful to Helen Malmsten, the secretary of Hanken’s Department of Economics for her assistance.

I wish to thank Hanken’s Department of Economics and the Centre for Corporate Governance for providing me with office space.

I would like to thank Rupert Moreton, who did an excellent job proofreading the text of this dissertation.

I am thankful to SIS Ägarservice AB, and personally to Sven-Ivan Sundqvist for providing me with excellent ownership data on Swedish listed companies.

I am grateful for the financial support of the Hanken Foundation, the Finnish Cultural Foundation, the Marcus Wallenberg Foundation, Suomen Arvopaperimarkkinoiden Edistämissäätiö, and the Oskar Öflund Foundation.

I am grateful to my local friends Laura Arranz Aperte, Praveen Malla, Olga Neslevska, and Frans Saxen; Sascha and Natia Gokiely, who were further away in Germany; and other friends still further away in Uzbekistan for their encouragement.

I would also like to express my deepest gratitude to my wife, Rano Niyazmuradova, and sons, Timur and Dariy, for their constant support and understanding. I am especially grateful to Rano, who has always been supportive during this important phase in our family’s life. It has not been an easy path together, especially given that our younger son, Dariy, was born in the course of my studies. I would also like to express my gratitude to my mother-in-law, Gulchekha Nugmanova, for her care and help in realising the commencement of my studies in Finland. My thanks also go to my parents, sisters Mashxura and Mahchekhra, and all my other close relatives for their love, which comforted and energised me in my studies.

iii

EXECUTIVE SUMMARY

The role of institutional investors in corporate governance is the main focus of this thesis. It has been argued that institutional investors, which have become more important in capital markets in recent decades, promote value maximisation in companies by protecting the best interests of shareholders. However, asset managers employed by institutional investors may pursue their own interests rather than their employers’. To prevent this, competition between asset managers may be a solution. The evidence concerning the actual outcome of this kind of competition is still scant. The new Swedish pension system provides a “natural experiment”1 in a competitive structure between pension funds. Of particular interest is whether this competition- based structure has produced the active corporate governance involvement that has been advocated as one of the ways to enhance fund performance. If large institutions owning sizable blocks of shares in companies actually contribute to their improved governance, detailed data from the new Swedish pension system should be ideal in identifying that type of impact.

This study helps us understand institutional owners’ capacity and incentives to be active in corporate governance within a competitive framework. Its results should be of interest to people involved in regulating or managing pension funds, and also to officials working on corporate governance regulations.2

Four papers are included in this doctoral dissertation. Below, I outline the main findings of these papers sequentially:

“Market valuation of firms and public pension fund ownership”.

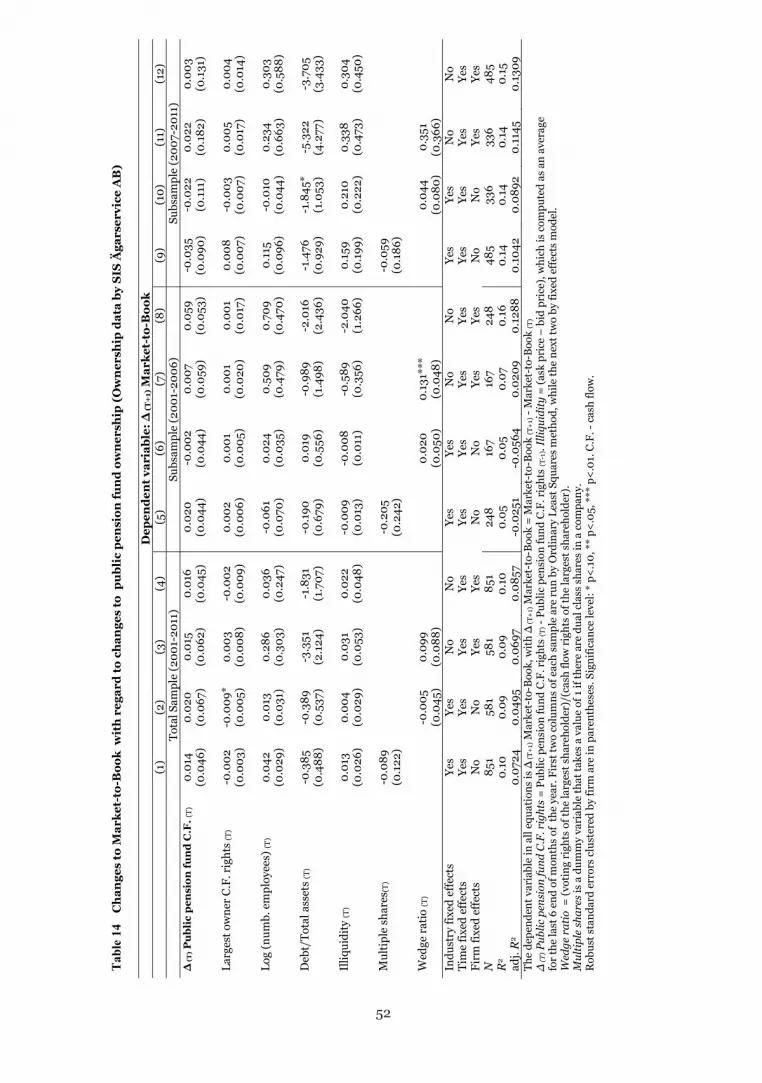

In this paper I study the relationship between public pension fund ownership and firms’ market valuation. Consistent with earlier findings, I find a positive correlation. However, public pension funds tend to increase their holdings in firms after an increase in the market valuation of these firms, whereas there is no relationship between change in pension fund ownership and future change in the market value of these firms. I conclude that the positive correlation between public pension fund ownership and the market valuation of firms in Sweden is the result of public pension funds investing in equity that commands a high price in the stock market, rather than the result of an ability to improve corporate performance.

“Corporate governance by Swedish public pension funds”.

In this paper, I explore the direct relationship between public pension fund ownership and the quality of corporate governance in firms. I find no evidence of public pension funds facilitating the diversification of company boards by increasing the proportion of women, foreigners, or directors of various ages. Furthermore, public pension funds were unsuccessful in promoting independent directors, securing the non-re-election of an active CEO to the Board of Directors, and in reducing the wedge between cash flow and voting rights in listed firms.

1 See Giannetti & Laeven (2009) 2 As mentioned in policy recommendations by Jakobsson & Korkeamaki (2014).

iv

“Public pension funds as shareholders and firm performance”.

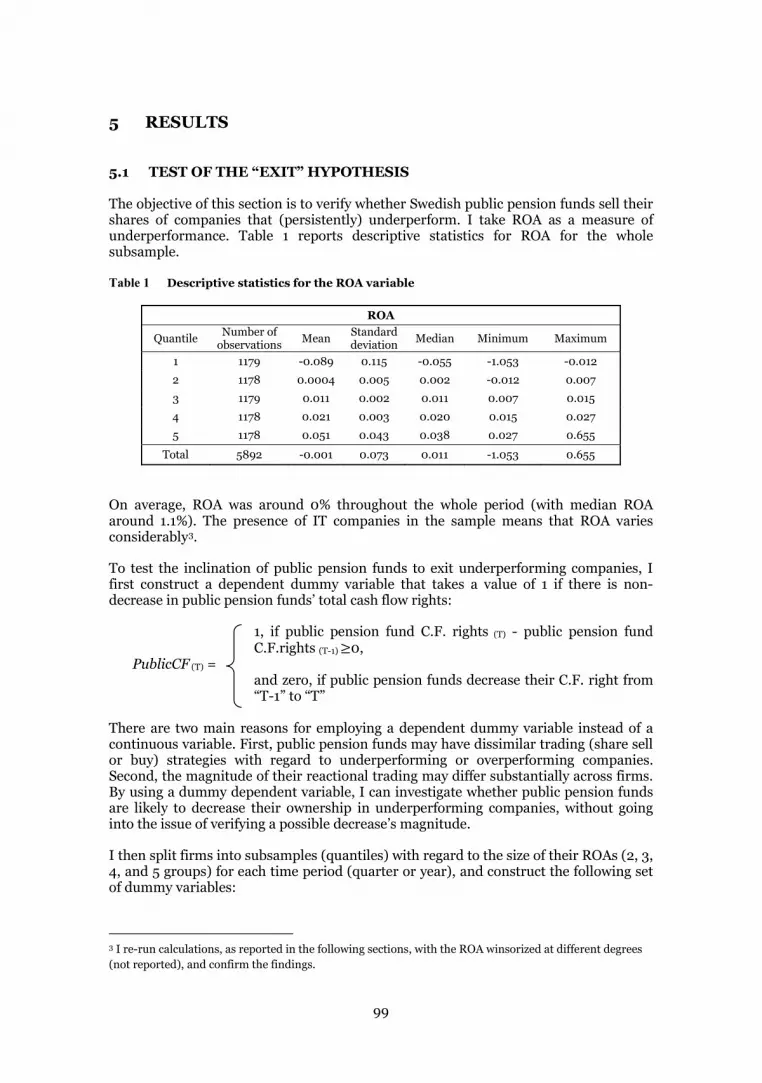

The main question addressed in this study is whether Swedish public pension funds are likely to impact a company in their portfolios, directly or indirectly, when they are dissatisfied with its performance, or to “vote with their feet” instead. Thus, the goal of the study is to test two different hypotheses for active portfolio management by these funds: “exit”- that is, sell shares of a low performance company, or “impact” - that is, contribute actively to the dismissal of underperforming CEOs and Boards of Directors.

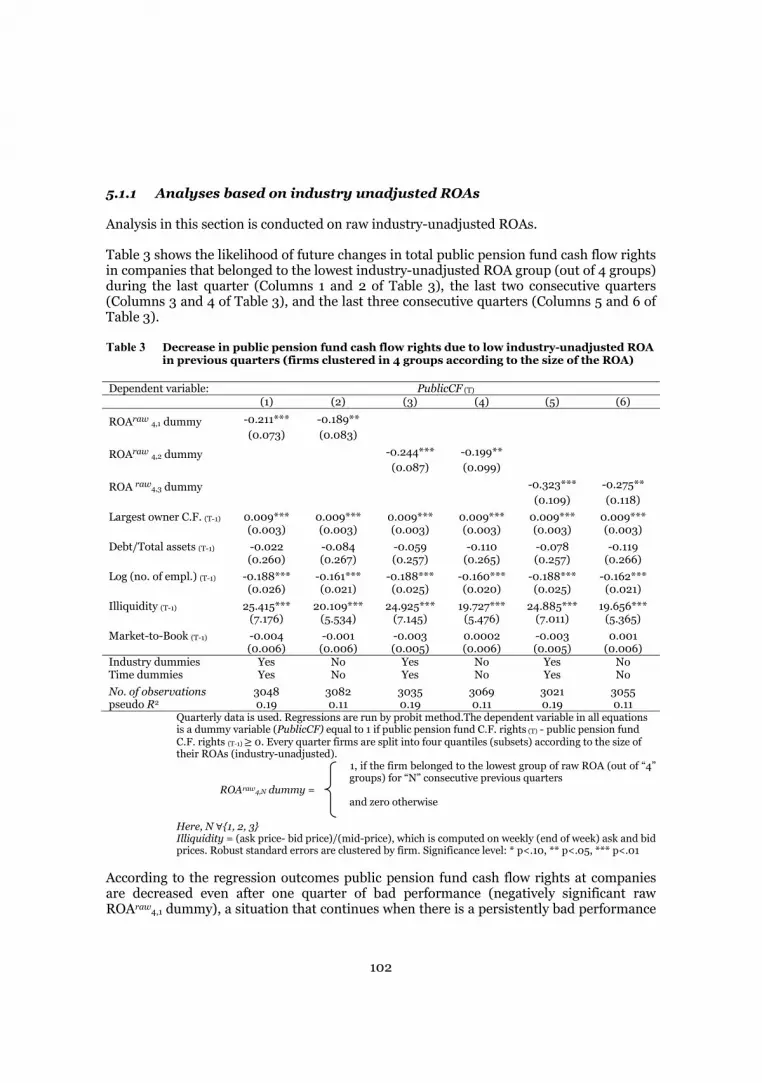

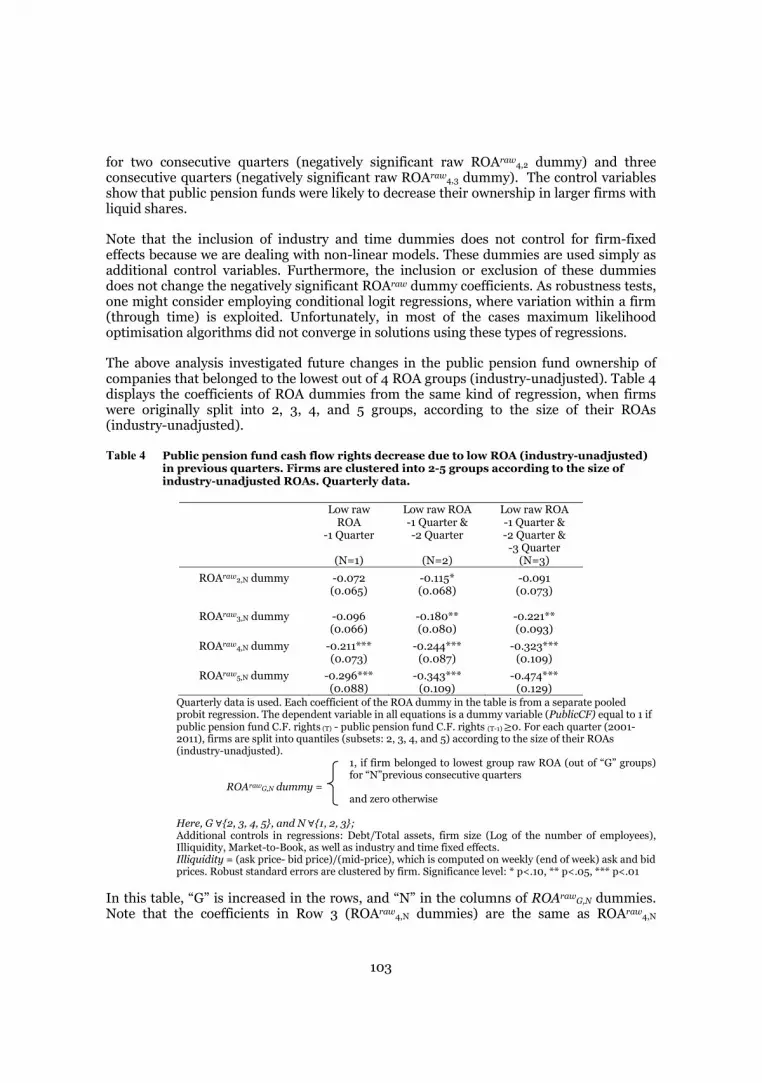

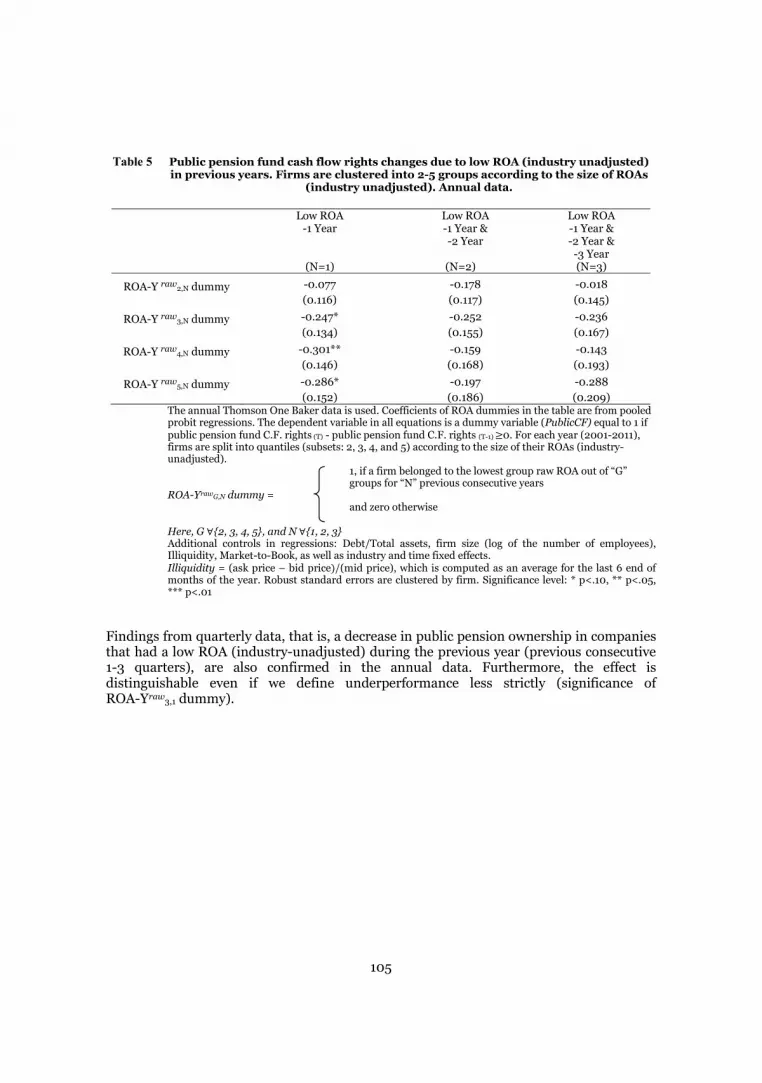

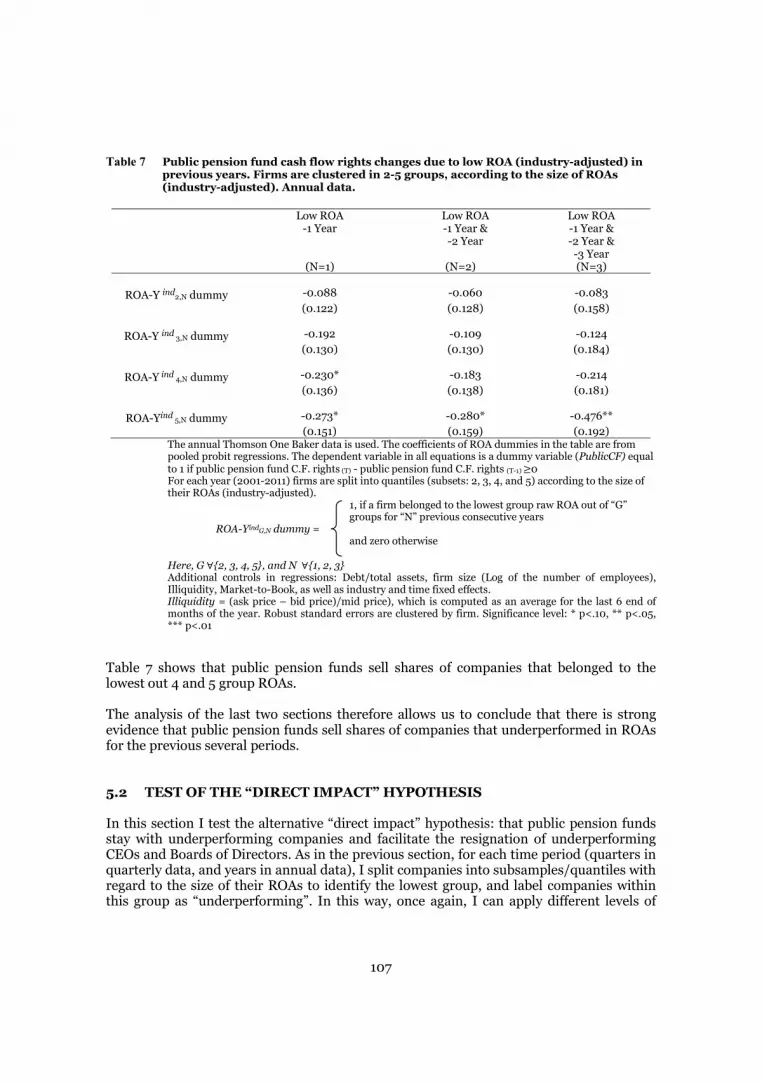

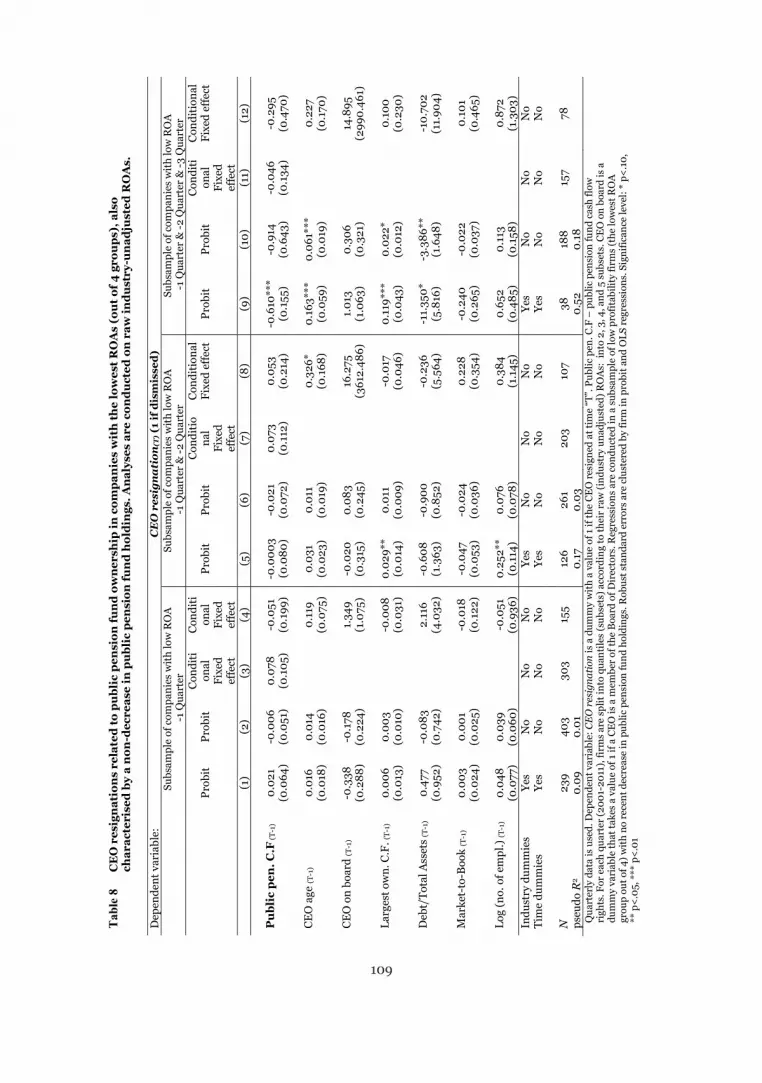

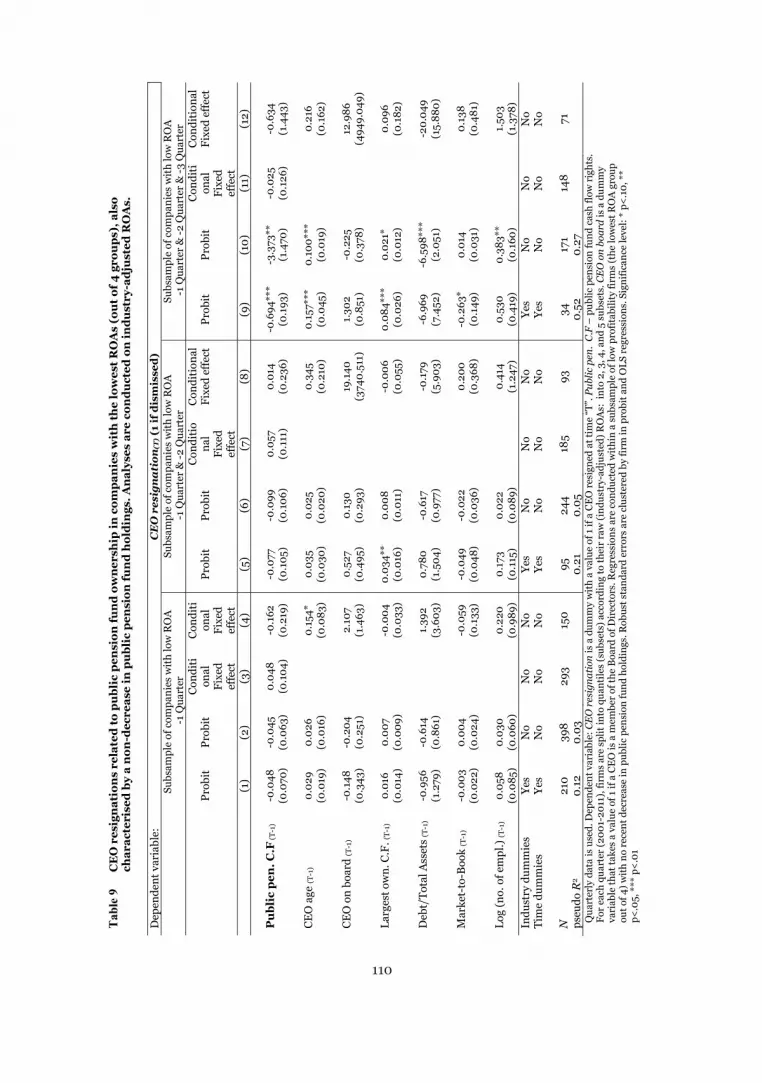

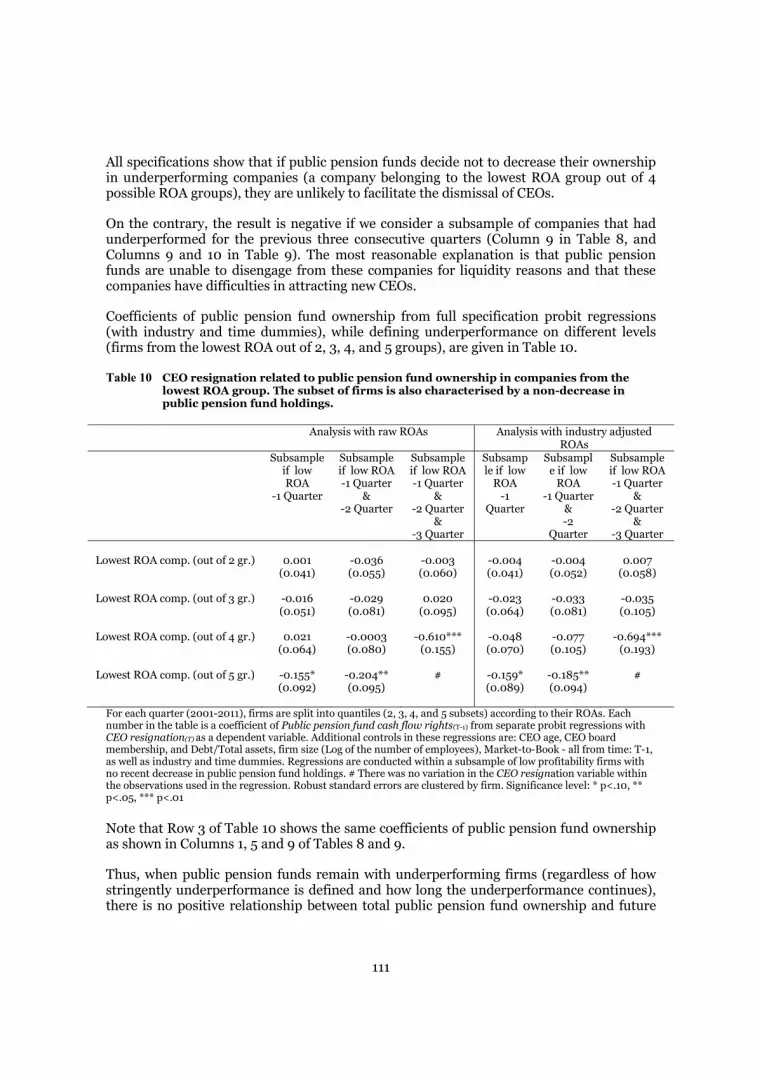

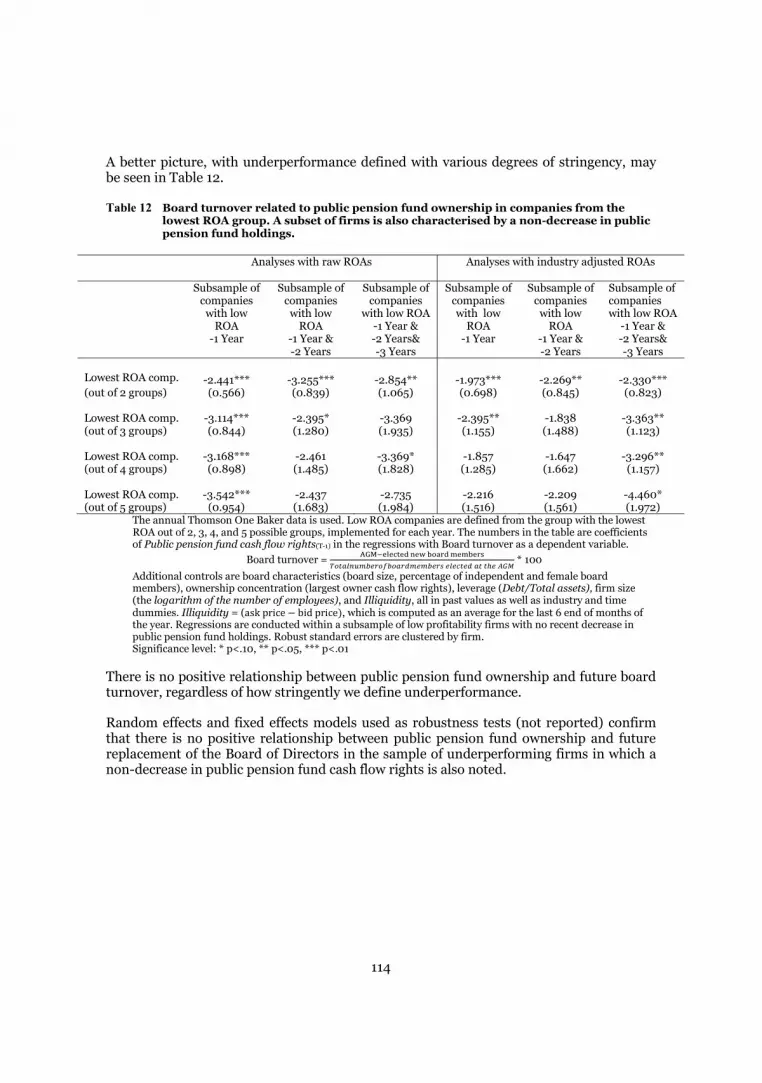

I find that ownership by public pension funds significantly decreases if a company belongs to the subsample with the lowest ROA (out of 2,3,4,5 groups) during 1 to 3 previous consecutive quarters. However, I do not find a significant relationship between public pension fund ownership and the dismissal of CEOs or a Board of Directors in companies belonging to the low ROA subsample in the course of several past periods.

Thus, the findings in this study indicate that Swedish public pension funds tend to sell their shares of underperforming companies rather than facilitate the dismissal of the CEO or the Board of Directors.

“Competition as a driving force among institutional investors. The case of Swedish pension funds”.

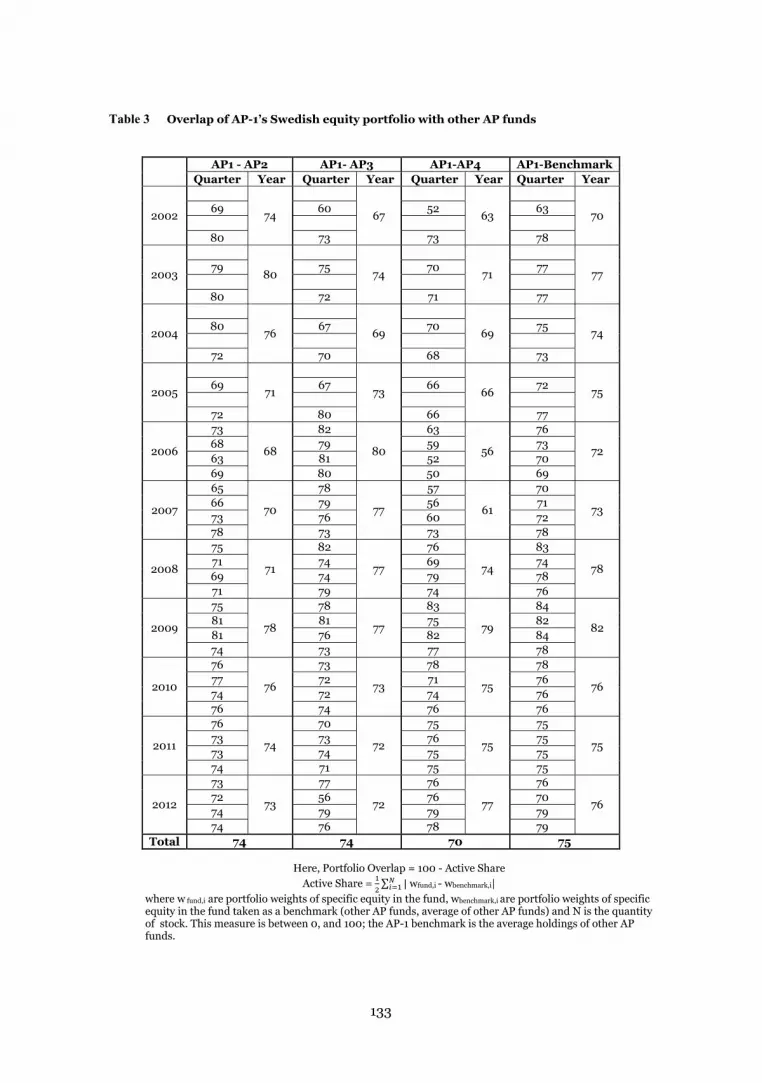

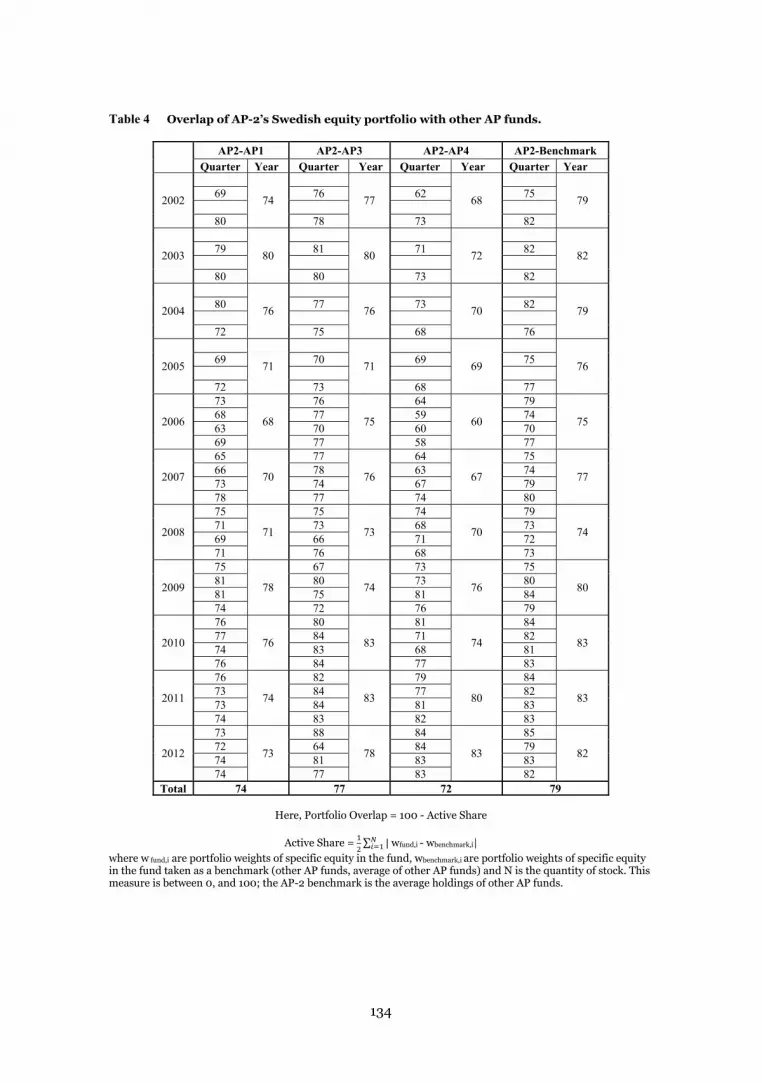

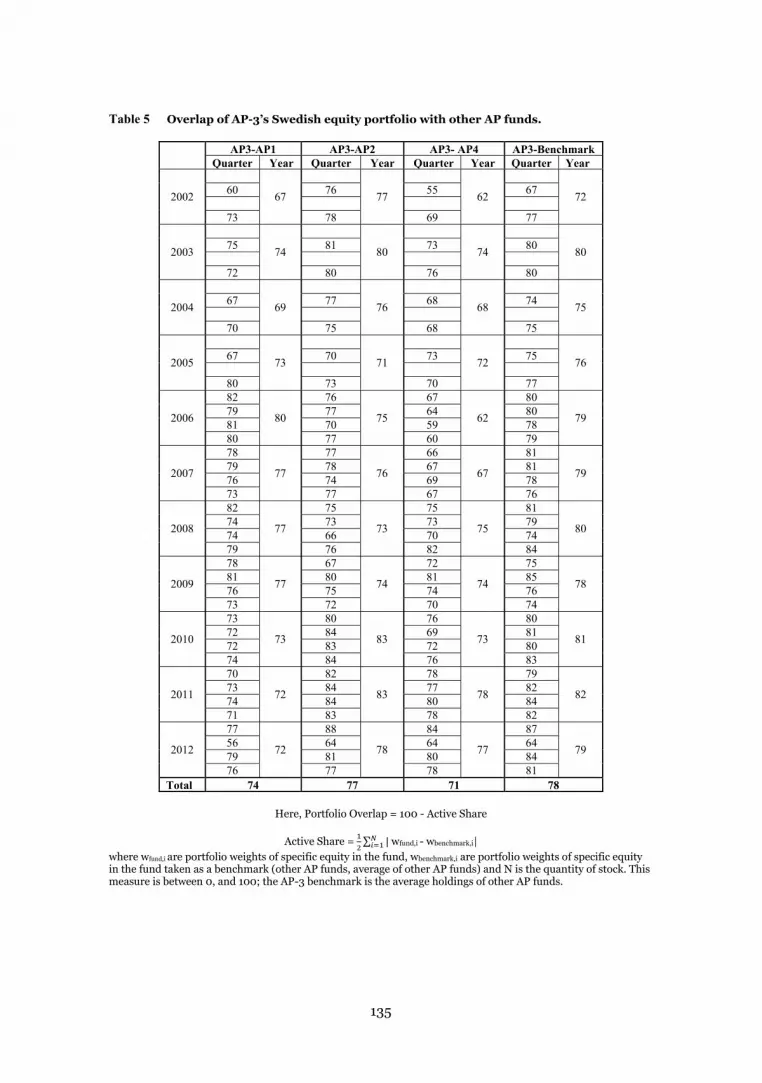

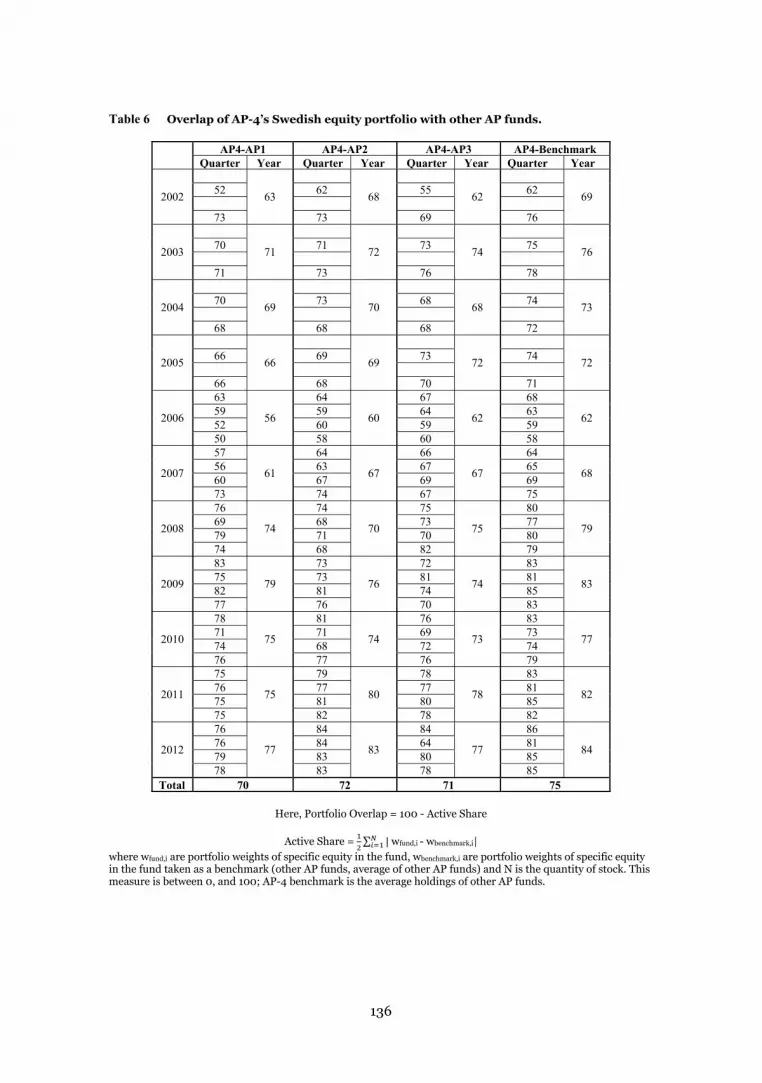

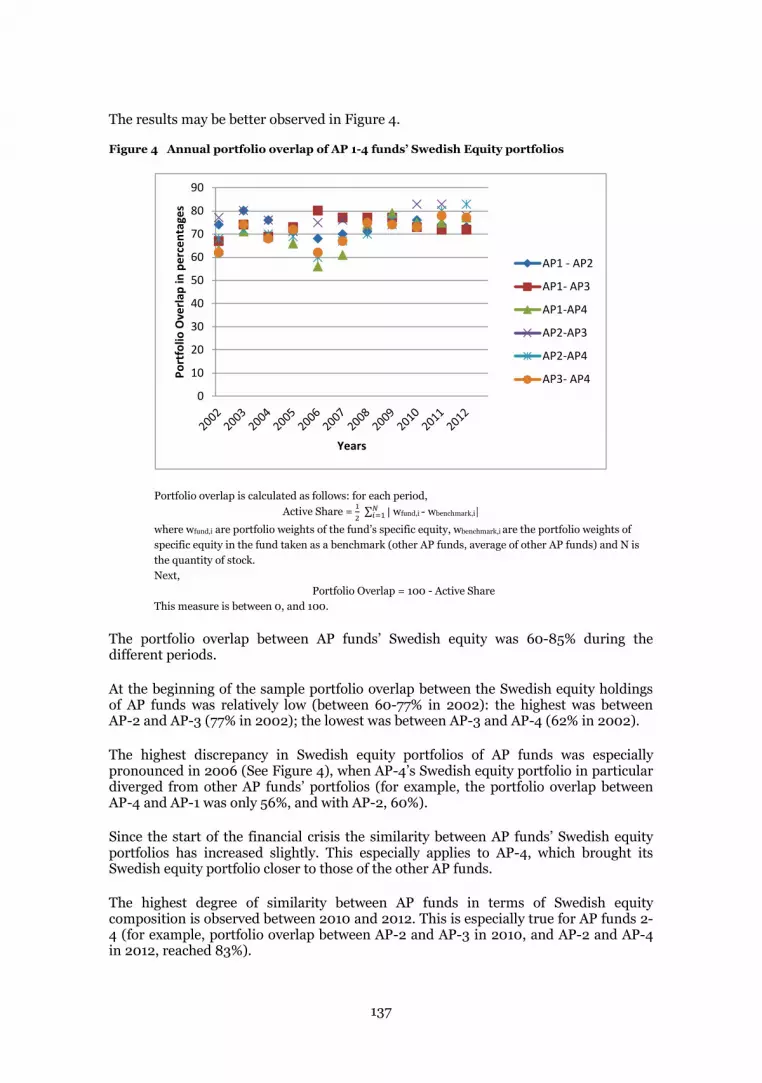

In the final paper I investigate the consequences of having several public pension funds (AP buffer funds) with similar mandates. The main justification for such a structure, when the system was created was to encourage competition between funds. I employ Active Share measure proposed by Petajisto (2013) and Cremers & Petajisto (2009) to evaluate the extent to which Swedish equity portfolios of AP buffer funds overlapped in the years 2001-2012. According to this measure there is a 60-85% overlap of Swedish equity portfolios of AP buffer funds over the sample period (with stronger portfolio convergence between buffer funds after the start of the financial crisis in 2008).

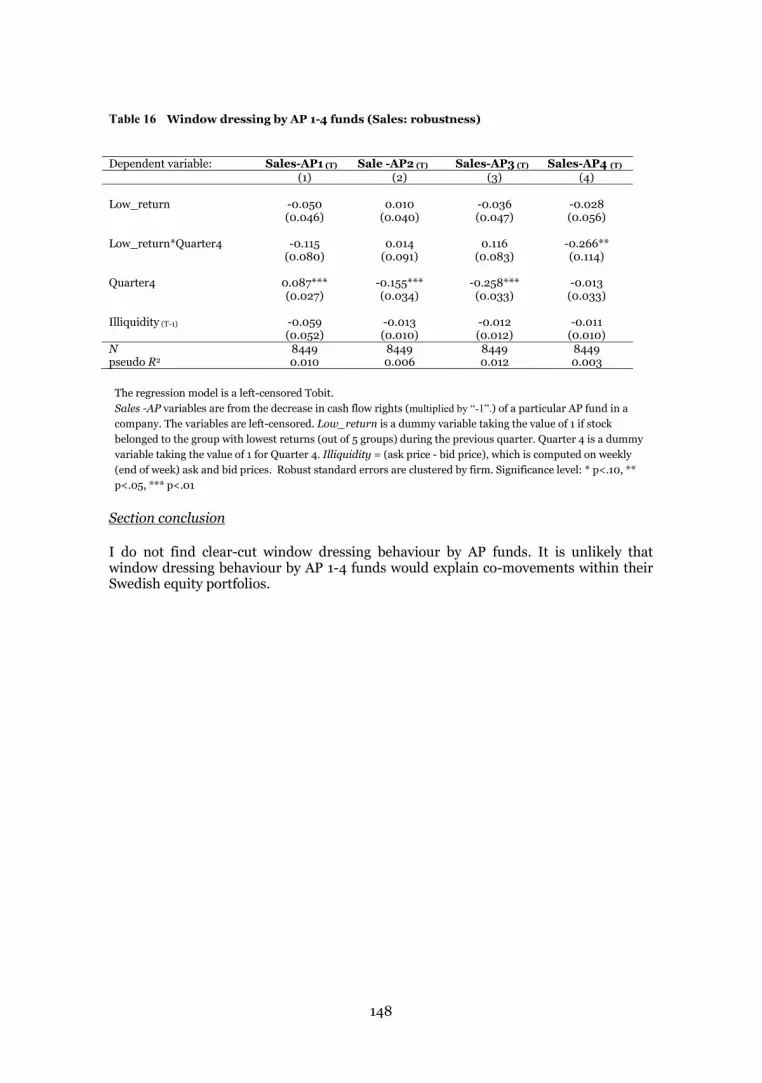

In further analysis I find that there are co-movements in domestic share trades of AP buffer funds. I find no evidence that co-movements are due to “window dressing”.

v

References

Cremers M., Petajisto A., 2009, “How Active Is Your Fund Manager? A New Measure That Predicts Performance”, Review of Financial Studies, 22(9) pp.3329-3365

Giannetti M., Laeven L., 2009, “Pension reform, ownership structure, and corporate governance: Evidence from a natural experiment”, The Review of Financial Studies v 22 n 10, pp. 4091-4127

Jakobsson U., Korekeamaki, 2014, “Ownership and governance of large Finnish firms”, Prime Minister's Office Reports, 6/2014

Petajisto A., 2013, “Active Share and Mutual Fund Performance”, Financial Analysts Journal, 69(4) pp. 73-93

vi

CONTENTS

Chapter I: Introduction

1 BACKGROUND ................................................................................................... 1

2 THE ROLE OF INSTITUTIONAL INVESTORS IN CORPORATE GOVERNANCE ................................................................................................... 3

2.1 Advantages and disadvantages of institutional ownership .................... 3

2.2 Institutional investors within a legal-institutional framework .............. 4

2.3 Institutional investors: monitor or "vote with the feet"? ........................ 5

2.4 Along the path of institutional shareholder activism ............................. 6

2.5 Institutional "voting with the feet" ........................................................ 8

2.6 Major trends in institutional investor activism ...................................... 9

2.7 Literature summary .............................................................................. 10

3 THE SWEDISH CORPORATE GOVERNANCE ............................................... 11

4 THE SWEDISH PENSION SYSTEM................................................................. 13

4.1 Features of the reformed Swedish pension system .............................. 13

4.1.1 Income pension ...................................................................... 14

4.1.2 Premium Pension ................................................................... 15

4.2 Expected changes in the system............................................................ 16

5 THE MAIN THESIS CONCLUSIONS ............................................................... 17

REFERENCES ................................................................................................................. 19

Chapter II: Essays

1 Market valuation of firms and public pension fund ownership ........................ 27

2 Corporate governance by Swedish public pension funds ................................. 56

3 Public pension funds as shareholders and firm performance .......................... 91

4 Competition as a driving force among institutional investors. The case of Swedish pension funds .................................................................................... 121

CHAPTER I: INTRODUCTION

“From a broader perspective corporate governance is socially valuable because it will contribute to efficient use of scarce resources in society, that is, achieves a distribution of some scarce resources that is superior to the solution that would arise without properly functioning corporate governance. The scarce resources that corporate governance targets is managerial talent. A good governance system thus makes the best use of available managerial talent.” (Berglund, 2014)

1

1 BACKGROUND

Economists have long known that value maximisation within the existing legal framework is beneficial for societies at large. This is consistent with shareholder value maximisation. Nevertheless, in publicly held companies with dispersed ownership executives may well act in their own interests at the expense of shareholders, as shareholders are unable to observe the decisions executives may make, or refrain from making. This is referred to as an agency problem3, and it is the purpose of corporate governance to address it. The goal is to safeguard value maximisation by monitoring management and seeking to align the interests of a company’s managers with those of its shareholders.

Since the Second World War institutional investors have become gradually more important in the global capital markets. A crucial question is whether these institutional investors should and can be effective in improving the corporate governance of firms in which they acquire significant blocks of shares.

Some researchers have argued that institutional investors can alleviate the agency problem between shareholders and company managers (Black, 1992; Black & Coffee, 1994). Others point out that institutional investors are themselves subject to agency problems, which reduces their usefulness in exercising this role (Allen, 2001; Menkhoff, 2002; Kahl & Gorton, 1999; Lakonishok et al., 1992).

Regulation proposed by well-meaning political decision makers may not be helpful in addressing these problems. Excessive regulation and legal barriers may instead preclude the active role of institutional investors in firms’ governance (Gillan & Starks, 2003; Rose, 2007; Aggarwal et al., 2011; Black, 1992; Jara-Bertin et al., 2012).

A potential solution may be found in competition between asset managers. Mutual monitoring by competing managers might stimulate better fund management by institutional investors. Competition between fund managers might also lead to more active corporate governance involvement, since significant ownership in a company that experiences a visible corporate governance scandal will reduce the fund’s portfolio return (Brown et al., 1996; Agarwal et al., 2004; Chevalier & Elison, 1999).

Empirical research in this area is hampered by the fact that the issues are quite complex. Each country has a unique setting of formal and informal structures, which makes comparisons difficult, since the differences observed may be the result of a number of factors contributing to country heterogeneity.

One way to tackle such problems is to look for “natural experiments”, that can show if one feasible solution is better than another. The desirability of “natural experiments” in the context of institutional oversight has been eloquently stated by Black & Coffee (1994):

“We cannot run the legal experiment of changing our laws to facilitate institutional oversight of corporate managers and observe how the institutions act. Still less can we go back sixty years or more, change our laws then, and see how the institutions would act if they had grown up in a different legal and political environment. In similar settings, however, social scientists have long used ‘natural experiments’ to gain insight into how a particular legal rule affects behavior across otherwise similar societies.” (Black & Coffee, 1994, pp. 2000)

3 Adam Smith was already aware of this problem as can be seen in his “Wealth of Nations”, published in 1776.

2

In its pension reform finalized at the turn of millennium, Sweden has provided us with a unique “natural experiment” (Giannetti & Laeven, 2009). As a result of the reform, several public pension funds (AP funds) were created with the same starting point and the same mandates. The main objective of creating these multiple public pension funds was to stimulate competition between them (Björkmo & Lundbergh, 2010).

The objective of this study is to investigate whether the competitive institutional framework created in Sweden by pension reform has indeed been effective in stimulating competition between pension funds, and whether it has had an impact on their corporate governance involvement. In particular, I study whether Swedish pension fund ownership is related to (1) firms’ market valuation; (2) firms’ corporate governance quality; and (3) impact vs. exit for underperforming firms. I also study whether there are similarities in the composition of domestic equity portfolios of the Swedish public pension funds, and whether these funds tend to have similar sell and buy strategies in these particular portfolios.

3

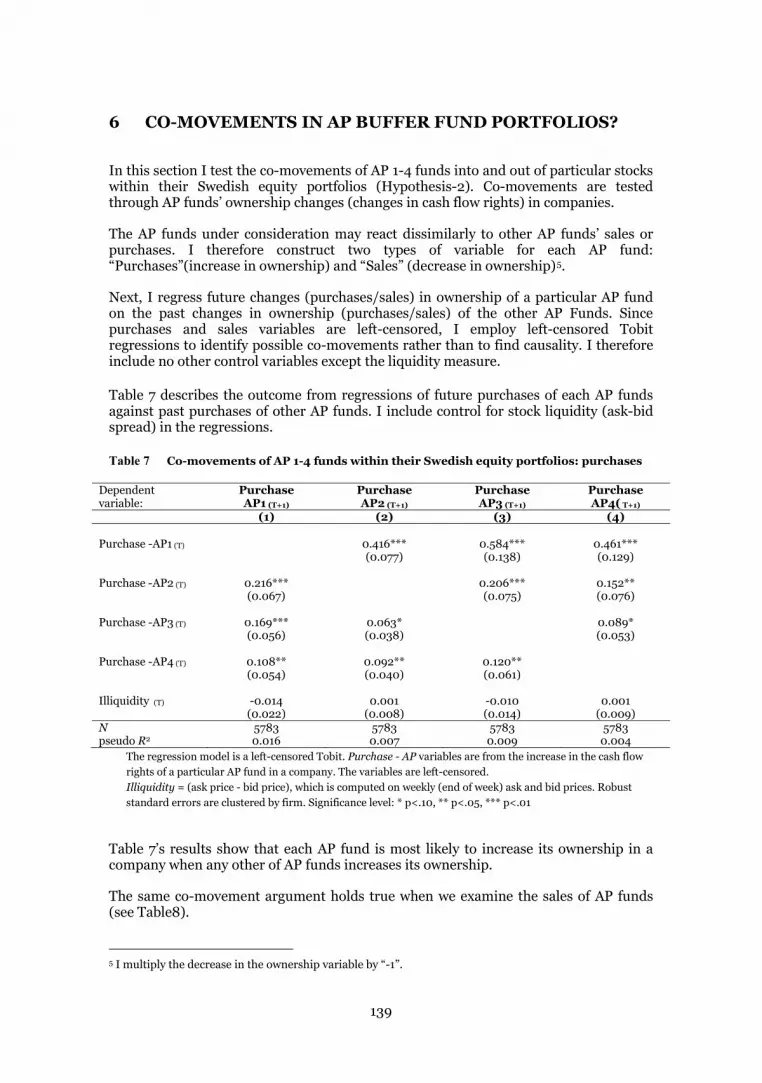

2 THE ROLE OF INSTITUTIONAL INVESTORS IN CORPORATE GOVERNANCE

2.1 Advantages and disadvantages of institutional ownership

Institutional investors are organisations that invest money on behalf of their beneficiaries. This definition suggests there are at least the following types of institutional investors: mutual funds, pension funds, endowment funds, insurance companies, banks, private equity funds, hedge funds, and venture capital funds. The main objective of these investors is to create value for their beneficiaries.

The role of institutional investors in corporate governance has been debated extensively, especially since the late 1980s, when pension funds, emerged as big players in capital markets. It has been argued that institutional shareholders should exploit their advantages over individual investors in disciplining management to pursue shareholders’ interests (Clark & Hebb, 2004; Black, 1992; Black & Coffee, 1994).

While recognising the existence of heterogeneous types of institutional investors, several common advantages of institutional ownership have been identified (Menkhoff, 2002; Black, 1992): (1) institutional investors are managed by professionals, who can utilise information better than lay investors; (2) the cost of management is lower for institutional investors, because they can exploit economies of scale; and (3) they have an interest in ensuring better protection of minority shareholder rights, because their actions are constantly under public scrutiny.

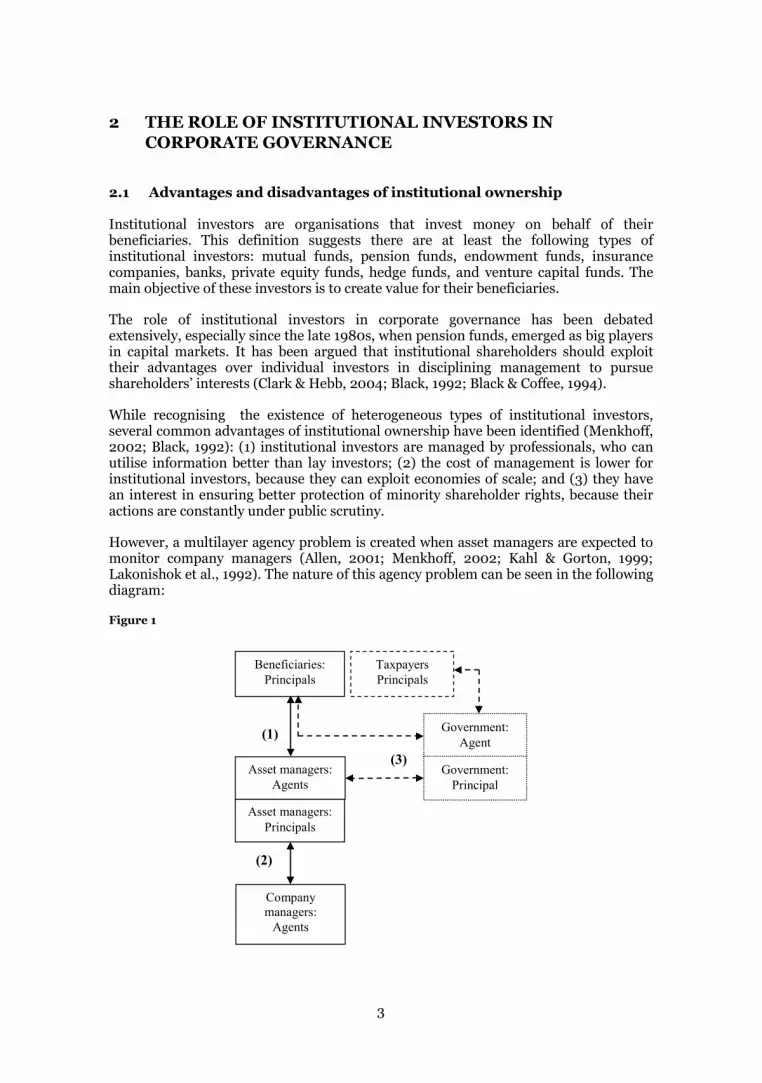

However, a multilayer agency problem is created when asset managers are expected to monitor company managers (Allen, 2001; Menkhoff, 2002; Kahl & Gorton, 1999; Lakonishok et al., 1992). The nature of this agency problem can be seen in the following diagram:

Figure 1

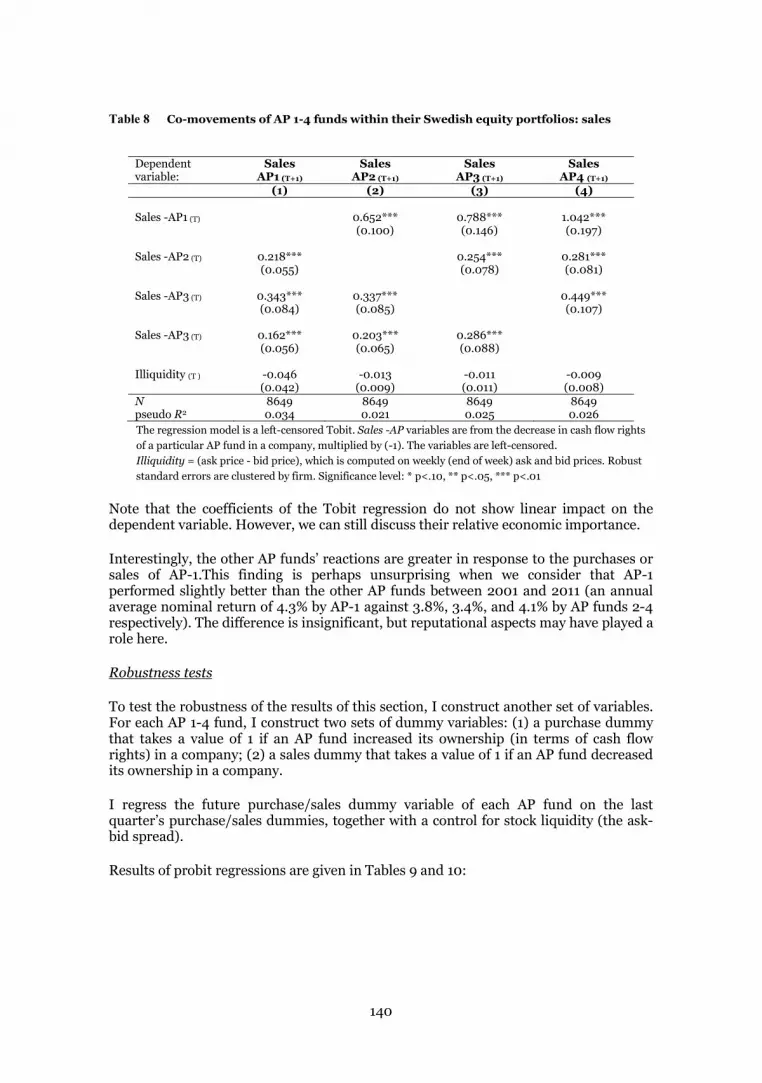

(1)

(2)

(3)

Beneficiaries: Principals

Asset managers: Agents

Government: Agent

Government: Principal

Asset managers: Principals

Company managers:

Agents

Taxpayers Principals

4

An agency problem will exist between (1) beneficiaries and asset managers, and in the next step (2) between asset managers and managers of the firms in which the fund is invested. Conflicts of interest may arise in both links of the chain. Beneficiaries want the long-term value of their funds to be maximised (taking risk appropriately into account). Asset managers are concerned with their reputation (Chevalier & Elison, 1999), which may make them overly risk-averse. In addition, if asset managers are evaluated against predetermined benchmarks on a short-term basis, they may opt for short-term investments. Company managers, in the last link of the chain, may be tempted to expropriate company resources if they are not properly monitored.

The problem becomes even more complicated when the government is the intermediary between beneficiaries and asset managers, as shown on the right hand side (3) of Figue-1 (this is especially the case with public pension funds). Here, the government is the agent of the beneficiaries to the extent that they are taxpayers, but also of other taxpayers. At the same time the government is the asset managers’ principal. Government representatives employed to monitor asset managers are concerned with their career prospects (Lakonishok et al., 1992), and political considerations will therefore play a substantial role. In some cases, there may be a conflict of interest between fund beneficiaries and taxpayers in general.4

Different types of institutional investors are subject to intrinsic agency problems to various degrees. Thus, the layers of agency problems are more complex for public pension funds than for private activist hedge funds or private equity funds. It is therefore erroneous to expect different types of institutional investors in governance of firms to exercise a homogeneous role (Berglund & Alimov, 2015).

The severity of asymmetric information between company managers and investors is another dimension in determining the suitability of a particular type of institutional investor for the “monitoring role”. There have been attempts to relate institutional ownership to asymmetric information (El-Gazzar, 1998; Boemer & Kelley, 2009; Huyghebaert & Hulle, 2004; Gibson et al., 2004). It is usually claimed that institutional investors reduce asymmetric information, as there is a positive relationship between institutional ownership and the severity of asymmetric information. However, the causality may run in reverse: institutional investors may prefer to invest in firms with low asymmetric information to reduce the likelihood their holdings producing unpleasant surprises.

Given the complexity of the different factors involved, the final outcome of institutions’ role in corporate governance is difficult to foresee, and remains largely an empirical question.

2.2 Institutional investors within legal-institutional framework

Institutional investors are subject to a given legal and institutional framework. Their degree of involvement in corporate governance also depends on the nature of their investment strategies and their investment horizons, as well as on their interaction with the market for corporate control, with large shareholders, with employees, and with other company stakeholders (Gillan & Starks, 2003; Jara-Bertin et al., 2012; Aggarwal et al., 2011). 4 Localization decision of an investment could produce this type of a conflict. Beneficiaries as shareholders could benefit from a liberal subsidy provided by the state while taxpayers in general, who will pay the bill, would lose.

5

The legal and institutional framework limits constraints on the extent to which institutional investors are involved in corporate governance (Gillan & Starks, 2003; Jara-Bertin et al., 2012; Aggarwal et al., 2011; Celik & Isaksson, 2013). According to Black & Coffee (1994) overregulation has limited corporate governance involvement and favoured a simple exit strategy practiced by institutional investors in US corporations.

Jara-Bertin et al. (2012) emphasise the differences in the roles undertaken by institutional investors in common and civil law countries. They find a positive relationship between firm value and ownership concentration by institutional investors in civil law countries, and a negative one in common law countries. The authors explanation is that ownership is dispersed in common law countries, and even at low levels of ownership institutional shareholders are able to have an impact on corporate governance. Excessive ownership concentration in this environment, results in undesirable entrenchment. The authors also claim that in civil law countries, where ownership is concentrated, institutional investors can challenge dominant shareholders only when they have sufficient influence.

Institutional investors are also seen as important because they tend to promote best practice in corporate governance in countries with low corporate governance standards (Aggarwal et al., 2011; Ferreira & Matos, 2008; Ferreira et al., 2010; Tihanyi et al., 2003).

According to Aggarwal et al. (2011) institutional ownership drives change in firms’ governance, with reverse causality not holding true. According to the authors foreign investors especially improve firms’ governance in countries with weak shareholder protection, while it is domestic institutional investors that advocate better governance in the US.

The findings of Aggarwal et al. (2011) are supported by Ferreira et al. (2010), who find more M&As in firms with a high proportion of foreign institutional investors, especially in countries with weak corporate governance standards.

Chung & Zhang (2011) and Bushee et al. (2014), on the other hand, find empirical evidence for institutional investors preferring stocks of companies with good corporate governance. Chung & Zhang (2011) conclude that institutional investors are inclined to invest in firms with good corporate governance because of their fiduciary responsibilities, and because the shares of such companies are also more liquid. Furthermore, according to Ferreira & Matos (2008), institutional investors invest in countries with high disclosure standards.

2.3 Institutional investors: monitor or “vote with the feet”?

The main objective of institutional investors is to create value for their beneficiaries. This suggests that they should take the least costly way to achieve a given increase in the gross value of their asset portfolio. When they are dissatisfied with the performance of a company in their portfolios, institutional investors have a number of options: (1) “vote with their feet” - sell company shares; (2) “voice” - hold their shares and try to impact companies’ governance; (3) hold their shares, and do nothing (Gillan & Starks, 2003). In severe cases managers can also be brought to court on the initiative of institutional investors (Cheng et al., 2010). The preferred strategy taken by different institutional investors remains an empirical question.

6

It is claimed that monitoring by institutional investors depends on whether their investments in the companies are short-term or long-term (Bushee, 1998; Bushee, 2001; Elyasiania et al., 2010; Chen et al., 2007).

According to Bushee (1998, 2001) short-term institutional investors (with high portfolio turnover) are unlikely to monitor companies. Bushee (1998) investigates the role of institutional shareholders in companies, in which the tension between achieving earnings targets and R&D expenditure is particularly high. He finds that in companies where the proportion of short-term institutional investors is comparatively high, managers are likely to increase earnings at the expense of R&D expenditure. Moreover, Bushee (2001) finds that institutional investors such as banks, with strict fiduciary responsibilities, and those with high turnover and diverse portfolios prefer to invest in companies with high near-term earnings, even at the expense of long-term shareholder value.

Elyasiania et al. (2010) argue that institutional investors with a long-term horizon can reduce agency costs and decrease information risk by pressing the managers to disclose private information. The authors argue that managers monitored by long-term investors are likely to avoid myopic behaviour. Managers who attract long-term investors build their reputations especially in debt markets, and thus reduce the cost of the debt incurred by their firm. In line with these arguments, the authors find a negative relationship between institutional ownership and the cost of debt.

Chen et al. (2007) claim that independent institutional investors with a long-term concentrated ownership are likely to be engaged in monitoring. Their findings indicate that ownership by this type of institutional investor is positively associated with post-merger firm performance measured by stock returns, accounting profitability measures, and analyst earnings forecasts. Moreover, they find that such investors do not trade for short-term profit, and exit firms that are likely to make very bad bids. The authors suggest that the exit action taken by these investors puts further pressure on managers and strengthens impact monitoring.

Furthermore, a number of studies suggest that, “pressure-resistant” institutional investors that have no business relationship with companies (such as public pension funds or mutual funds) in contrast to “pressure sensitive” ones (such as banks, insurance companies, trusts, and private pension funds), are less subject to management influence, and hence more likely to be monitors (Ferreira and Matos, 2008; Cornett et al., 2007; Bhattacharya & Graham, 2007; Gianneti & Laeven, 2009; Aggarwal et al., 2011; Almazan et al., 2005; Brickley et al., 1988; Woidtke, 2002; Chen et al., 2007).

2.4 Along the path of institutional shareholder activism

Early evidence on institutional shareholder activism comes from the activities of major US public pension funds, such as CalPERS - California Public Employees’ Retirement System - during the 1980s and 1990s (Smith, 1996; Duggal & Millar, 1999; Wahal, 1996; Nesbitt, 1994; Wu, 2004; Woidtke, 2002; Prevost & Rao, 2000). These funds targeted underperforming firms and initiated shareholder proxy proposals. Market reaction to the announcements of the activities of US public pension funds is not usually found to be significantly positive (Del Guercio & Hawkins, 1999; Duggal & Millar, 1999; Wahal, 1996). Shareholder proposals in targeted firms were followed by

7

changes in corporate governance structure, but failed to improve corporate performance (Del Guercio & Hawkins 1999; Prevost & Rao, 2000).

Prevost & Rao (2000) claim that public pension fund proposals in targeted firms may serve as a signal to the market, and that such firms’ management is unlikely to cooperate and prevent the submission of a proposal. This is the argument they give for finding short and long-term deterioration of firm performance in stock price returns and accounting measures after the submission of a shareholder proposal by a public pension fund.

Wu (2004) makes a similar argument that, on announcing the poor corporate governance of firms, US public pension funds, and in particular CalPERS, influenced public opinion and damaged the reputation of the management and directors of those companies during the late 1980s and mid 1990s. As a result, the targeted companies reduced the proportion of insider directors, CEO dismissal became more likely, and CEO dismissal-performance sensitivity increased.

Crutchley et al. (1998) and Nelson (2006) note that shareholder activism by US public pension funds declined in the late 1990s, reflected in lower returns to buy and hold strategies of targeted firms.

The evidence on institutional shareholder activism from other countries is not conclusive either. Faccio & Lasfer (2000) investigate occupational pension funds in the UK, and claim that monitoring by these funds is ineffective. Their findings suggest that UK occupational pension funds target small firms for the most part, and fail to improve corporate governance of firms under their ownership. Such funds have therefore underperformed when compared to industry or a benchmark.

Becht et al. (2007) arrive at an opposite conclusion in investigating shareholder activism by the Hermes UK focus fund. They find that the fund was successful in beating the benchmark through private engagement with firms’ managers. According to the investigators shareholder activism by the fund resulted in corporate restructuring, changes in boards, improved firm performance, and increased cash payouts to shareholders. 5

Rose (2007) investigates Danish data from the turn of the millennium. He shows that equity ownership by the largest institutional investors is associated with companies’ negative performance, while financial institutions such as banks and insurance companies have a positive impact on company performance.

Giannetti & Laeven (2009) investigate similar data as the present study does6 - namely Swedish data after the pension reform finalised at the turn of the millennium. They find a positive relationship between ownership by public pension funds as well as large independent private pension funds and firm valuation. They also find that an increase in public pension fund ownership is related to an additional control premium.

According to Carleton et al. (1998) the lack of a consistent relationship between institutional investor shareholder activism and changes in the governance practised by firms observed in the literature may be due to the fact that institutional shareholders’ 5 However, it is worth noting that the Hermes UK focus fund is organised as a partnership (as is usually the case in private equity funds). 6 The difference here is in time periods. Giannetti & Laeven (2009) consider the period before the financial crisis (2000-2005). In this project I explore a longer period (2001-2012)

8

advocacy for changes in firms is done for the most part by private negotiation, as in the case of TIAA-CREF – one of the biggest US pension funds, which they investigate. The importance of institutional investors’ behind-the-scenes activity is also confirmed by McCahery et al. (2015), who survey institutional activism around the world.

To test the “monitoring hypothesis” researchers have explored institutional ownership against a number of dimensions such as M&As, executive compensation (Almazan et al., 2005; Hartzell & Starks, 2003), earnings management (Chung et al., 2002), and corporate payouts (Grinstein & Michaely, 2005; Scott, 2014; Qayyum et al., 2015; Han et al., 1999).

Qiu (2006) claims that public pensions funds prevent value-reducing acquisitions more than other types of institutional investors, especially in firms with high agency costs. Qiu further argues that firms with high public pension fund ownership perform better having acquired other firms.

Hartzell & Starks (2003) relate institutional ownership to executive compensation. They find that institutional investors have an impact on executive compensation structures, and that institutional ownership is positively related to pay-for-performance sensitivity and negatively to the level of an executive management’s compensation. Almazan et al. (2005) model, and subsequently find empirical support for the theory that “potentially active” institutional investors such as investment advisers and investment companies, unlike banks or insurance companies, have an impact on pay-for-performance sensitivity.

Chung et al. (2002) claim that institutional investors monitor the accounting choices of company managers and inhibit their opportunistic earnings management. In examining discretionary accounting accruals, the authors find that managers in firms with high institutional ownership are less likely to smooth earnings to suit their own preferences by shifting profits from one year to another.

Institutional investors may also alleviate the agency problem by ensuring that managers share profits with shareholders, especially in firms with high free cash flow and low investment opportunities (Jensen, 1986). There have been a number of empirical studies that investigate the relationship between institutional ownership and corporate payouts7 (Grinstein & Michaely, 2005; Scott, 2014; Qayyum et al., 2015). The evidence for this is also mixed. For example, Grinstein & Michaely (2005) find little evidence that institutional investors increase payouts, while Scott (2014) and Qayyum et al. (2015) come to the opposite conclusion. Scott (2014) finds that institutional investors’ ownership in firms with high free cash flow and poor investment opportunities is positively related to corporate payouts, which confirms the monitoring hypothesis. Similarly, Qayyum et al. (2015) argue that institutional investors are likely to be engaged in monitoring and facilitate higher payout at companies weighted relatively highly in their portfolios.

2.5 Institutional ‘voting with the feet’

According to Kahn & Winton (1998) decisions to trade in company shares and decisions to actively intervene are endogenous. They claim that institutional investors are likely to intervene (involve themselves in shareholder activism) if such an action will give them information advantages over uninformed traders in their subsequent trades on 7 Dividend payouts and stock repurchases.

9

private information. According to the authors the likelihood of intervention depends not only on the size of institutional holdings, but also on firm characteristics.

Admati & Pfleiderer (2009) argue that legal barriers, liquidity concerns, agency costs, and free rider problems discourage institutional investors from exerting their “voice” at companies. They show that the ability to exit (potential threat) based on private information by institutional investors has an impact on decisions made by company managers.

Parrino et al. (2003) find empirical evidence for the disciplining effect of institutional investors voting with their feet. They investigate US companies in the 1980s and early 1990s and find that informed investors subject to the prudent man rule exited underperforming firms one year before forced CEO turnover, which obviously depressed prices. The authors conclude that the exit of institutional owners affected boards’ decision to fire underperforming CEOs.

Helwege et al. (2012) argue that the disciplining effect of voting with the feet by institutional investors has diminished over time. The authors relate “voting with the feet” against “voice” implemented by institutional investors to forced CEO turnover over two subsamples, 1982–1994 and 1995–2006. The authors confirm the findings of Parrino et al. (2003) for only the first sub-period – the negative relationship between change in institutional ownership and future CEO dismissal. In further analysis they find that in spite of the fact that “voice” by activist institutional investors is correlated to forced CEO turnover during the entire period, this does not explain the recent upward trend in CEO dismissals.

2.6 Major trends in institutional investor activism

Institutional investors such as hedge funds, private equity funds, and venture capital funds have been more closely related to corporate restructuring in recent decades (Wright et al., 2009; Kaplan & Stromberg, 2009; Harris et al., 2015; Klein & Zur, 2009; Brav et al., 2008; Bebchuk et al. 2015; Brav et al. ,2015).

Corporate restructuring through leveraged buyouts by private equity institutions has become increasingly important as a governance mechanism8 (Wright et al., 2009; Kaplan & Stromberg, 2009; Harris et al., 2015). As Jensen (1989) argues, leveraged buyout organisations, while using debt rather than equity as a major source of capital, have “proper” incentives for value creation. In a normal buyout transaction a private equity fund acquires the majority control of a company and restructures it to enhance its accounting profitability and efficiency (Wright et al., 2009; Kaplan & Stromberg, 2009). Value creation is achieved by the dissemination of best practice by skilled private equity fund managers.

Governance intervention by venture capital firms is also noteworthy. While investing in young and emerging firms, venture capital funds, unlike private equity funds, do not gain major control of companies. Harris et al. (2015) show that the venture capital market has been more active in North America than in Europe. Furthermore, the

8 There have been two waves in leveraged buyouts in recent decades. The first wave peaked during the 1980s, the second in the mid-2000s (Acharya et al., 2013; Wright et al., 2009; Kaplan & Stromberg, 2009; Harris et al., 2015). Buyout activities were hindered by the junk bond crisis that occurred during the early 1990s and the financial crisis that started in 2007.

10

authors find that the difference between the best and the worst funds in terms of value creation is more pronounced in venture than in buyout funds.

There is also evidence that hedge funds exploit their shareholdings in restructuring companies under their ownership (Klein & Zur, 2009; Brav et al., 2008; Bebchuk et al. 2015; Brav et al., 2015). In general, there is a positive market reaction to news of hedge fund intervention (Klein & Zur, 2009; Brav et al., 2008). According to Brav et al. (2008) hedge fund targeted firms experience higher CEO turnover and better operating performance. Klein & Zur (2009) claim that hedge funds also solve the free cash flow problem (Jensen, 1986), while other types of institutional activists, such as private equity funds and venture capital funds, demand change in companies’ operational strategies. Bebchuk et al. (2015) and Brav et al. (2015) also claim that intervention by hedge funds does not damage long-term shareholder value.

2.7 Literature summary

Institutional investors are part of a multilayer agency problem. The ability of ultimate beneficiaries to make asset managers accountable for funds’ performance is an important characteristic that differentiates types of institutional investors. Different types of institutions will cater to demands from investors that differ in their capacity to monitor asset managers. Institutions that cater to less sophisticated investors are better off by a pre-commitment to invest only in assets with a relatively low degree of investment asymmetry. Standardised systems run by less expensive personnel will allow these institutions to stay competitive. However, more sophisticated investors, who are able to assess the likely impact of strategic choices by firms, will have an advantage in picking asset managers who are strongly incentivised to find undervalued assets. These managers are allowed to invest in assets that are subject to substantial information asymmetry.9 Empirical findings reported for different types of institutions are mostly in line with this view. For example, equity funds and activist hedge funds that cater to more sophisticated investors more than other types of institutional investors, are those that have been largely involved in corporate restructuring.

Ownership engagement by institutional investors that are subject to severe potential agency problems is the most likely explanation of the mixed findings in the literature concerning the corporate governance involvement by institutional investors.10 An important additional issue is whether institutional investors with weak engagement by the ultimate beneficiaries can be induced to act in the interests of these beneficiaries by additional mechanisms. Competition between the AP funds in the Swedish system should provide such a mechanism. The actual role of this competition and its consequences to corporate governance are thus worthy of a proper investigation. The Swedish pension reform finalised at the turn of the millennium is an example of encouraging competition between otherwise heavily regulated institutional investors – the pension funds. In this study I also examine the evidence concerning the consequences of this additional mechanism.

9 For a more detailed discussion of this, see Berglund & Alimov (2015). 10 This is, for example, the case for pension funds, as discussed in previous sections.

11

3 THE SWEDISH CORPORATE GOVERNANCE

Corporate governance in Sweden is regulated by the Companies Act (2005), the Swedish Corporate Governance Code (SCGC)11, and generally accepted practice (Lekvall et al., 2014). The SCGC applies mostly to listed companies and relies on the “comply or explain” principle. Since the turn of the millennium, the number of listed companies in Sweden12 has ranged between 250 and 300.

Swedish corporate governance shares features with other Nordic countries (Finland, Denmark, and Norway). These features constitute the Nordic Corporate Governance Model (NCGM), which is considered an alternative to the Anglo-Saxon model (Lekvall et al., 2014). The model’s distinguishing characteristic is that the largest shareholders have dominant positions in companies stemming from their ownership and corporate governance structures. They take long-term responsibility for the companies, and this is generally accepted by other shareholders and society (Lekvall, 2009).

Swedish companies are noted for their high concentration of ownership. In 2014, about 67% of Swedish listed companies had at least one shareholder, with about 20% of voting rights, whereas in 17 % of companies there was a shareholder who held at least 50% of voting rights (Lekvall et al., 2014). The positions of the largest shareholders are strengthened by companies’ practice of dual class shares. More than half of the Swedish listed companies have multiple class shares.

Both the Companies Act and the SCGC require that Swedish companies have three main governing bodies: the General Shareholders’ Meeting, the Board of Directors, and the CEO. The Shareholders’ Meeting is the highest decision-making body. The Nomination Committee, which consists mainly of the largest shareholders (with at least one member independent of the company’s largest shareholders), proposes candidates for the Board of Directors and their remuneration to the Shareholders’ Meeting.

The Board of Directors consists primarily of non-executives, and only one person from management (usually the CEO) may be a member of the board. A majority of directors should be independent of the company (at least two persons should also be independent of the largest shareholders). Boards may also include employee representatives (up to three persons in large companies). In practice, unions do not always choose to take up their right to representation on Boards of Directors, which may be due to the costs associated with such membership (Berglund & Holmen, 2013).

At the same time the Swedish corporate governance model, like the NCGM in general, is characterised by good protection of minority shareholders, which discourages the largest shareholders from extracting private benefits at the expense of other shareholders (Holmen & Knopf, 2004; Lekvall, 2009; Lekvall et al., 2014).

Corporate governance in general evolves over time, and this is no less the case in Sweden. The role of foreign investors has increased dramatically since the 1990s, when Sweden became a member of the EU. Deregulation and social reforms have resulted in a rapid increase in the institutional share of capital markets in recent decades in

11 The Swedish Corporate Governance Code was introduced in 2005 and amended in 2008, 2010, and 2015. 12 Nasdaq Stockholm, and Nordic Growth Market

12

Sweden. In the 1950s the share of institutional investors in capital markets was close to zero. Today, institutional investors hold about 85% of Swedish market capitalisation (Lekvall et al. 2014). These forces have contributed to a decline in power in the hands of the largest shareholders, but they have not been sufficient to cause a convergence towards the Anglo-Saxon model, which is characterised by dispersed ownership and management control (Henrekson & Jakobsson, 2012).

With this increase in institutional ownership in Swedish companies, it remains an open question as to what role they can play in the governance of firms in which they have substantial stakes. In this study I focus on Swedish pension funds, and explore several dimensions of their corporate governance involvement.

13

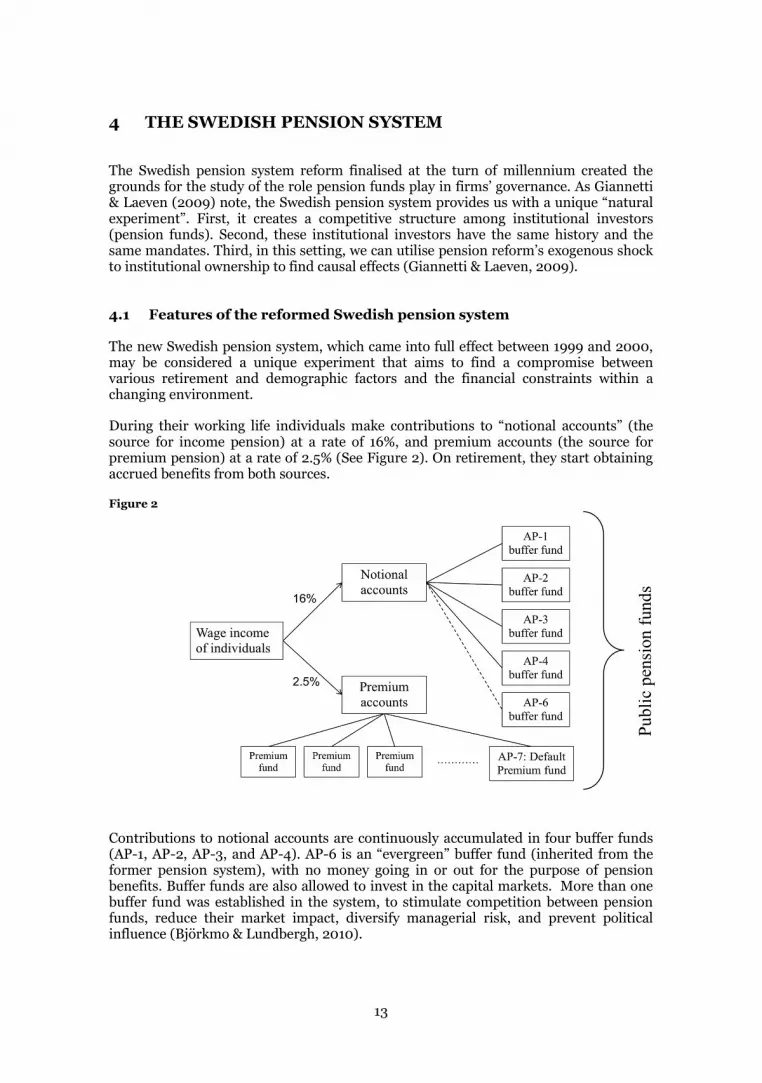

4 THE SWEDISH PENSION SYSTEM

The Swedish pension system reform finalised at the turn of millennium created the grounds for the study of the role pension funds play in firms’ governance. As Giannetti & Laeven (2009) note, the Swedish pension system provides us with a unique “natural experiment”. First, it creates a competitive structure among institutional investors (pension funds). Second, these institutional investors have the same history and the same mandates. Third, in this setting, we can utilise pension reform’s exogenous shock to institutional ownership to find causal effects (Giannetti & Laeven, 2009).

4.1 Features of the reformed Swedish pension system

The new Swedish pension system, which came into full effect between 1999 and 2000, may be considered a unique experiment that aims to find a compromise between various retirement and demographic factors and the financial constraints within a changing environment.

During their working life individuals make contributions to “notional accounts” (the source for income pension) at a rate of 16%, and premium accounts (the source for premium pension) at a rate of 2.5% (See Figure 2). On retirement, they start obtaining accrued benefits from both sources.

Figure 2

Contributions to notional accounts are continuously accumulated in four buffer funds (AP-1, AP-2, AP-3, and AP-4). AP-6 is an “evergreen” buffer fund (inherited from the former pension system), with no money going in or out for the purpose of pension benefits. Buffer funds are also allowed to invest in the capital markets. More than one buffer fund was established in the system, to stimulate competition between pension funds, reduce their market impact, diversify managerial risk, and prevent political influence (Björkmo & Lundbergh, 2010).

Publ

ic p

ensi

on fu

nds

14

Individuals are allowed to manage their contributions into the premium pension part and allocate their money to up to 5 funds (premium pension funds) accredited by the Premium Pension Authority. Premium pension funds, in turn, invest money in the capital markets. There are now more than 800 pension funds within the Swedish premium pension system. When not managed actively, premium pension money is directed to a government-managed default AP-7 fund.

4.1.1 Income pension

The Swedish income pension system is often called a Notional Defined Contribution system, and has the following features:

Pension rights are collected in “notional accounts” throughout individuals’ working life with a defined contribution rate of 16%.

Pension rights in “notional accounts” are adjusted annually according to the average income index.

On retirement, pensions are calculated in accordance with life expectancy.

Flexible retirement is allowed, but those who retire earlier automatically receive fewer benefits.

There is a residence-based guarantee pension for low income retirees.

Funds in “notional accounts” are directed towards AP 1-4 funds in equal amounts. Pension benefits are paid out from AP 1-4 funds.13 If total liabilities exceed total pension contributions, then an automated balancing mechanism is triggered, and “notional accounts” are adjusted upwards less than country’s average wage growth.

Thus, the main objective of buffer funds (AP-1, AP-2, AP-3, and AP-4) is to stabilise the system, when differences arise between fixed pension contributions and benefits (which vary depending on demographic factors such as life expectancy and individuals’ age of retirement). The buffer funds allocate resources in the capital markets.

Governance and management of AP buffer funds is based on the Swedish National Pension Insurance Funds Act (SFS 2000:192). Boards of Directors of AP buffer funds are appointed by the government. They consist of nine members (including two representatives nominated by organisations representing employee interests, and another two representing employer interests).

As stated in the act, AP funds should manage their funds to achieve the highest possible return at the lowest possible risk in the best interest of the retirement pension insurance.

The following investment rules apply to AP 1-4 funds:

Investments should be mostly in stock exchange-listed assets (not more than 5% in unlisted assets).

13 The system is therefore still formally pay-as-you-go

15

Each fund may hold not more than 10% of the voting rights of a listed company.

Not more than 2% of the market value of shares listed on the Swedish stock exchange should be held.

At least 10 % of a fund’s assets are to be managed by external management.

A maximum of 40% of each fund’s assets may be exposed to currency risk.

At least 30% of assets should be invested in debt instruments with low liquidity risk.

4.1.2 Premium Pension

The premium pension system is governed by the Premium Pension Authority (PPM) which manages individual premium accounts, enters into agreement with funds wishing to participate, provides information on fund share values, and acts as a “clearinghouse”. Having contributed 2.5% of their income to premium accounts, individuals may self-regulate their portfolios by allocating their money to a number of funds available in the system. The following rules apply to such activity:

Individuals may choose up to 5 funds out of about 800.

Individuals may change their choice as many times as they wish.

If they do not choose a fund, their premium contributions are invested into the default Premium Savings Fund (Premiersparfonden) – AP-7.

Once individuals have chosen a fund, they may not switch to the Premium Savings Fund.

The total return of the Premium Savings Fund should be at least equal to, and the risk lower than the average of all actively chosen funds.

The Premium Savings Fund is managed by internal as well as external managers.

After the age of 61, individuals’ accumulated premium funds are converted to annuities. Annuities may be withdrawn in full or in ¼, ½, ¾ parts at a time.

AP-7 is required to manage assets for the benefit of savers, and to hold shares with no more than 5% of voting rights in a single company (Swedish National Pension Insurance Funds Act, 2000). Unlike other AP funds, AP-7 is inhibited in the exercise of its voting rights.14 Nevertheless, it is stated that AP-7 is involved in firms’ governance:

“By working closely with other institutional investors, without being part of any formal coalition or group, we can take an active part in board nomination processes. We can engage in dialogue with senior company officers and can attend shareholder meetings without voting. In the case of

14 But it can do so if investment cannot be satisfied in another manner (Swedish National Pension Insurance Funds Act, 2000);

16

foreign investees, we are allowed to vote at company meetings and to participate in public debate.” (AP 7, 2015)

In this study AP buffer funds (AP-1, AP-2, AP-3, and AP-4), the AP-6 fund, and the government-regulated AP-7 fund from the premium pension system are labelled as “public pension funds”, while funds accredited within the premium pension system are labelled as "premium pension funds".

4.2 Expected changes in the system

Since its establishment, there has been extensive criticism of the system. The system has been criticised for being overregulated. The rationale for having more than one buffer fund in the system has also been heavily questioned. Thus there have been calls to merge the AP funds (see for example, Fowler, 2011; Carter, 2010).

Criticism was strongest following a review of AP funds by a team (Buffer Capital Inquiry - Buffertkapitalsutredningen) led by Mats Langensjö, appointed by the Swedish Finance Ministry, and the Swedish Pension Group in 2011.

The investigators (Buffertkapitalsutredningen, 2012) criticise the investment rules as too restrictive, and propose to replace them with a Prudent Person Rule and stricter monitoring. At the same time they argue that separate funds do not take a unified responsibility over buffer capital in the pension system. They therefore suggest the establishment of an independent board to supervise AP funds that would set performance objectives, and undertake monitoring of all AP funds.

Recently, there has been a discussion in Sweden as to whether the Buffer Capital Inquiry group proposals should be adopted (See for example, White, 2015; Williams, 2015a, Williams, 2015b). Indeed, the New AP fund regulation (Finansdepartementet, 2015) has been proposed15. The following changes in the system have been suggested: (1) merge the AP-2 fund with AP-6 (which is a private equity fund inherited from the former system); (2) eliminate one of the remaining AP buffer funds from the system; (3) replace investment rules with Prudent Person Rule; (4) create a Supervisory Board (the National Pension Fund Board); (5) the evaluate performance of AP funds against a single reference portfolio.

The debate is ongoing, and political consensus has yet to be reached.

15 In December 2015, deputy finance minister Per Bolund announced that reforms of AP fund system as stated in the New AP fund regulation (Finansdepartementet, 2015) would be cancelled.

17

5 THE MAIN THESIS CONCLUSIONS

The Swedish pension reform finalised at the turn of the millennium created a competitive framework for pension funds. Competition was thought to boost the performance of pension funds, and their active involvement in corporate governance. Indeed, Swedish pension funds claim that they are active in the corporate governance of firms under their ownership.

The results of my thesis project indicate that there is a contemporaneous positive relationship between firms’ market valuation and public pension fund ownership. Giannetti & Laeven (2009) claim that such a positive relationship arises from Swedish public pension funds improving the quality of firms’ corporate governance. My analysis shows that the relationship arises from public pension funds investing in firms that are highly valued by the market, rather than from public pension funds driving the market value of firms.

In the next paper in my thesis I find that public pension funds are unlikely to intensify the diversification of company boards (through increasing proportion of females, foreigners, or directors of various ages); nor are they likely to promote independent directors, or prevent the re-election of active CEOs to the Boards of Directors of companies they own.

Underperforming companies in portfolios held by public pension funds are the subject of my analysis in the next chapter of the thesis. Indeed, these were the companies that needed the corporate governance intervention the most. I find that public pension funds sell shares of companies that have underperformed several previous consecutive quarters. However, I do not find evidence for public pension funds facilitating the dismissal of CEOs and Boards of Directors when they do not sell shares of underperforming companies.

My results indicate that Swedish public pension funds have not brought changes to the corporate governance of firms under their ownership. A principal reason for these findings may lie in the strict investment rules that limit pension funds’ control of particular companies. The overall picture that emerges is that regulation compels pension funds to diversify their portfolios, to guarantee a low risk for the pension buffer capital, while there is a public pressure on these funds to be active in the corporate governance of the firms in which they invest. However, investment rules have limited the rewards from successful engagement in individual firms’ governance, while costs are largely fixed in the form of resources required to form an expert judgment. It has been much cheaper for the funds to sell shares of underperforming companies, making it possible to meet performance objectives on an annual basis, and to keep up with other pension funds in the system (especially when it comes to public evaluations).

As previous results suggest that competition between pension funds has not contributed to their corporate governance involvement, in the next paper I investigate whether there is indeed proper competition between them. I find that there has been a relatively high degree of similarity in domestic equity portfolios of the Swedish public pension funds. Further analysis shows that these funds have timed their purchases and sales of company shares in roughly the same way. These findings do not necessarily support a claim that competition has failed, it may rather be an outcome of constraints caused by small and illiquid market for individual shares and too restrictive investment rules in the Swedish pension system.

18

The pension system created by the Swedish pension reform provides excellent evidence that it is difficult to match detailed regulation and active corporate governance involvement by institutional investors. After all, the main objective of institutional investors is to ensure the best long term return on investments for their beneficiaries. Forcing them to be active in corporate governance may simply force them to take on costs that do not result in benefits that fully compensate for these costs.

Finally, one may speculate that less stringent investment rules and more performance based incentive schemes for portfolio managers might have produced more efficient competition and better performance in the Swedish pension system. A closer examination of the relationship between incentives, management turnover and performance of the Swedish pension funds is a relevant question for future research.

19

REFERENCES

Acharya V., Gottschalg O, Hahn M., Kehoe C., 2013, “Corporate governance and value creation: Evidence from private equity”, Review of Financial Studies 26, pp.368–402

Admati A., Pfleiderer, P., 2009, “The 'Wall Street Walk' and shareholder activism: exit as a form of voice”, Review of Financial Studies 22, pp. 2645–2685

Aggarwal R., Erel I., Ferreira M., Matos P., 2011, “Does governance travel around the world? Evidence from institutional investors”, Journal of Financial Economics 100 (2011), pp. 154–181

Allen F., 2001, “Do financial institutions matter?”, The Journal of Finance, Vol. LVI, No. 4, pp. 1165–1175

Almazan A., Hartzell J., Starks L., 2005, “Active Institutional Shareholders and Costs of Monitoring: Evidence from Executive Compensation”, Financial Management, 34, pp. 5–34

Barber, B. M., 2007. “Monitoring the monitor: Evaluating CalPERS’ shareholder activism”, Journal of Investing 16, pp. 66–80.

Bebchuk L., Brav A., Jiang W., 2015, “The Long-Term Effects of Hedge Fund Activism”, Columbia Law Review, Vol. 115, 2015, pp. 1085-1156

Becht M., Franks J., Mayers C., Rossi S., 2007, “Returns to shareholder activism: Evidence from a clinical study of the Hermes UK focus fund”, Review of Financial Studies, 22(8), pp. 3039–3129.

Berglund T., 2014, “Corporate Governance and Optimal Transparency”, in J Forssbaeck & L Oxelheim (eds), The Oxford Handbook of Economic and Institutional Transparency. Oxford University Press, Oxford, pp. 359-371.

Berglund T., Alimov N., 2015, “Institutional Shareholders and Corporate Governance: A Survey”, Hanken Working paper

Berglund T., Holmen M., 2013, “Why Employees Choose to be Represented on Corporate Boards”, manuscript Centre for Finance, University of Gothenburg, and Hanken School of Economics. Available at: http://www.gu.se/digitalAssets/1495/1495049_holmen_berglund_cgir_version.pdf, Accessed on August 30, 2016

Bhattacharya P., Graham M., 2007, “Institutional Ownership and Firm Performance: Evidence from Finland”, Accounting, Finance, Financial Planning and Insurance Series 2007_01, Faculty of Business and Law, School of Accounting, Economics and Finance

20

Björkmo M., Lundbergh S., 2010, “Restructuring Sweden’s AP Funds for Scale and Global Impact”, Rotman International Journal of Pension Management, Volume 3 • Issue 1 Spring 2010

Black B., 1992, “Agents Watching Agents: The Promise of Institutional Investor Voice”, UCLA Law Review, Vol. 39, pp. 811-89

Black B., Coffee J., 1994, “Hail Britannia? Institutional investor behavior under limited regulation”, Michigan Law Review 92, pp. 1997-2087.

Boehmer E., Kelley, E.2009, “Institutional Investors and the Informational Efficiency of Prices”, Review of Financial Studies 22, pp. 3563-3594

Brav A., Jiang W., Kim H., 2015, “The Real Effects of Hedge Fund Activism: Productivity, Asset Allocation, and Labor Outcomes”, Working paper, Available at SSRN: http://ssrn.com/abstract=2022904 orhttp://dx.doi.org/10.2139/ssrn.2022904

Brav A., Wei J., Frank P., Randall T., 2008, “Hedge fund activism, corporate governance, and firm performance”, Journal of Finance 63, pp. 1729–1775

Brickley J., Lease R., Smith C., 1988, “Ownership Structure and Voting on Antitakeover Amendments”, Journal of Financial Economics 20, pp. 267-292

Brown K., Harlow W., Starks L., 1996, “Of Tournaments and Temptations: An Analysis of Managerial Incentives in the Mutual Fund Industry”, The Journal of Finance, Vol. 51, No. 1 (Mar., 1996), pp. 85-110

Bushee, B.J., 1998, “The influence of institutional investors on myopic R&D investment behavior”, The Accounting Review, Vol. 73, No. 3 pp. 305-333

Bushee B., 2001, “Do Institutional Investors Prefer Near-Term Earnings over Long-Run Value?”, Contemporary Accounting Research, 18, pp. 207–246

Bushee B., Carter M., Gerakos J., 2014, “Institutional Investor Preferences for Corporate Governance Mechanisms”, Journal of Management Accounting Research, Vol. 26, No. 2, pp. 123 - 149

Carleton W., Nelson J., Weisbach M., 1998, “The influence of institutions on corporate governance through private negotiations: Evidence from TIAA-CREF”, The Journal of Finance, Vol. 53, No. 4, pp. 1335–1362

Çelik S., Isaksson M., 2013, “Institutional Investors as Owners: Who Are They and What Do They Do?”, OECD Corporate Governance Working Papers, No. 11,

Chemmanur T., He S., Hu G., 2009, “The Role of Institutional Investors in Seasoned Equity Offerings”, Journal of Financial Economics (JFE), Vol. 94, No. 3, pp. 384-411

21

Chen X., Harford J., Li K., 2007, “Monitoring: Which institutions matter?”, Journal of Financial Economics 86, pp. 279–305

Cheng C., Huang H., Li Y., Lobo G., 2010, “Institutional Monitoring Through Shareholder Litigation”, Journal of Financial Economics, Vol. 95, pp. 356-383, 2010

Chevalier J., Ellison G., 1999, “Career Concerns of Mutual Fund Managers”, Quarterly Journal of Economics, Vol. 114, no. 2 (May 1999), pp. 389-432

Chung K., Zhang H., 2011, “Corporate governance and institutional ownership”, Journal of Financial and Quantitative Analysis", 46 (1), pp. 247–273.

Chung R., Firth M., Kim J., 2002, “Institutional monitoring and opportunistic earnings management”, Journal of Corporate Finance 8, pp. 29–48

Clark G, Hebb T. 2004, “Pension Fund Corporate Engagement: The Fifth Stage of Capitalism”, Industrial Relations, Vol. 59 (1) pp. 142–171

Cornett M., Marcus A., Saunders A., Tehranian H., 2007, “The impact of institutional ownership on corporate governance performance”, Journal of Banking & Finance 31, pp. 1771-1794

Cremers M., Petajisto A., 2009, “How Active Is Your Fund Manager? A New Measure That Predicts Performance”, Review of Financial Studies, 22(9) pp.3329-3365

Crutchley C., Hudson C., Jensen M., 1998, “The Shareholder Wealth Effects of CalPERS' Activism”, Financial Services Review, Vol. 7 No 1. pp. 1-10

Del Guercio D., Hawkins J., 1999, “The motivation and impact of pension fund activism”, Journal of Financial Economics, Volume 52, Issue 3, June 1999, pp. 293–340

Del Guercio D., Cole L., Woidtke T., 2008, “Do Boards Pay Attention When Institutional Investor Activists 'Just Vote No'?”, Journal of Financial Economics (JFE), Vol. 90, pp. 84-103.

Demiralp I., D'Mello R., Schlingemann F., Subramaniam V., 2011, “Are there Monitoring Benefits to Institutional Ownership? Evidence from Seasoned Equity Offerings”, Journal of Corporate Finance 17, pp.1340-1359.

Duggal R., Millar J., 1999, “Institutional ownership and firm performance: The case of bidder returns”, Journal of Corporate Finance 5, pp. 103-117

El- Gazzar S., 1998, “Predisclosure information and institutional ownership: A cross-sectional examination of market regulations during earnings announcement periods”, The Accounting Review, Vol. 73, No. 1 pp. 119-129

22

Elyasiania E., Jiab J., Maoa C., 2010, “Institutional ownership stability and the cost of debt”, Journal of Financial Markets 13, pp. 475–500

Faccio M., Lasfer A., 2000, “Do occupational pension funds monitor companies in which they hold large stakes?”, Journal of Corporate Finance 6, pp. 71-110

Ferreira M., Matos P., 2008, “The colors of investors’ money: The role of institutional investors around the world”, Journal of Financial Economics, Volume 88, Issue 3, pp. 499–533

Ferreira, M., Massa, M., Matos, P., 2010, "Shareholders at the gate? institutional investors and cross-border mergers and acquisitions", Review of Financial Studies 23, pp. 601–644

Fong K., Gallagher D., Gardner P., Swan P., 2011, “Follow the leader: fund managers trading in signal-strength sequence”, Accounting & Finance, 51, pp. 684–710

Giannetti M., Laeven L., 2009, “Pension reform, ownership structure, and corporate governance: Evidence from a natural experiment”, The Review of Financial Studies v 22 n 10, pp. 4091-4127

Gibson S., Safieddine A., Sonti R., 2004, “Smart investment by smart money: Evidence from seasoned equity offerings”, Journal of Financial Economics 72, pp. 581-604

Gillan S., Starks L., 2000, “Corporate governance proposals and shareholder activism: the role of institutional investors”, Journal of Financial Economics 57, pp. 275-305

Gillan S., Starks L., 2003, “Corporate Governance, Corporate Ownership, and the Role of Institutional Investors: A Global Perspective”, Journal of Applied Finance 13, pp. 4-22

Gillan S., Starks L., 2007, “The Evolution of Shareholder Activism in the United States”, Journal of Applied Corporate Finance, 19, pp. 55–73

Gopalan R., 2008, “Institutional Stock Sales and Takeovers: The Disciplinary Role of Voting with Your Feet”, Working paper, Available at SSRN: http://ssrn.com/abstract=891515 or http://dx.doi.org/10.2139/ssrn.891515

Graves S., Waddock, 1994, “Institutional owners and corporate social performance”, Academy of Management Journal, 1994, Vol. 37, No.4, pp. 1034-1046

Grinstein Y., Michaely R., 2005, “Institutional Holdings and Payout Policy”, The Journal of Finance, Vol. LX, No. 3, June 2005, pp. 1389-1426.

Han K., Lee S., Suk D., 1999, “Institutional shareholders and dividends”, Journal of Financial and Strategic Decisions, Vol. 12, No. 1, pp. 53-62

23

Harris R., Jenkinson T., Kaplan, S, 2015, “How Do Private Equity Investments Perform Compared to Public Equity?”, forthcoming Journal of Investment Management

Hartzell J., Starks L., 2003, “Institutional investors and executive compensation”, Journal of Finance 58, pp. 2351–2374

Helwege J., Intintoli V., Zhang, 2012, “Voting with their feet or activism? Institutional investors’ impact on CEO turnover”, Journal of Corporate Finance 18, pp. 22–37

Henrekson M., Jakobsson U., 2012, “The Swedish Corporate Control Model: Convergence, Persistence or Decline?” Corporate Governance: An International Review, Vol. 20, Issue 2, pp. 212-227, 2012.

Holmen M., Knopf J., 2004, “Minority Shareholder Protections and the Private Benefits of Control for Swedish Mergers”, Journal of Financial and Quantitative Analysis, 39, pp. 167-191

Huyghebaert N., Hulle C., 2004, “The role of institutional investors in corporate finance”, Tijdschrift voor Economie en Management, Vol. XLIX, 4, pp. 689-726

Jara-Bertin M., Lopez-Iturriaga F., Lopez-de-Foronda O., 2012, “Does the influence of institutional investors depend on the institutional framework? An international analysis”, Applied Economics - Vol. 44, No. 3, pp. 265 - 278

Jensen, M., 1986, “Agency cost free cash flow, corporate finance, and takeovers”, American Economic Review, 76(2), pp. 323–329

Jensen, M. 1989, “Eclipse of the public corporation”, Harvard Business Review, Sept.–Oct. pp. 61–74

Kahl M., Gorton G., 1999, “Blockholder Identity, Equity Ownership Structures, and Hostile Takeovers”, NBER Working Paper No. w7123. Available at SSRN: http://ssrn.com/abstract=165132

Kahn C., Winton A., 1998, “Ownership Structure, Speculation, and Shareholder Intervention”, The Journal of Finance, 53, pp. 99–129

Kaplan S., Stromberg P., 2009, “Leveraged Buyouts and Private Equity”, Journal of Economic Perspectives, 23(1), pp. 121-46.

Klein A., Zur E., 2009, “Entrepreneurial Shareholder Activism: Hedge Funds and Other Private Investors”, The Journal of Finance, VOL. LXIV, NO. 1, pp. 187-229

Lakonishok J., Shleifer A, Vishny R., Hart O., Perry G., 1992, “The structure and performance of the money management industry”, Brookings Papers on Economic Activity. Microeconomics, pp. 339-391.

24