qHelpful comments on earlier drafts were provided by Olivier Blanchard, Ricardo Caballero, StijnClaessens, Douglas Diamond, Stephanie Flanders, Mary Kwak, Rafael La Porta, Don Lessard,Richard Locke, Florencio Lopez-de-Silanes, Stewart Myers, Andrei Shleifer, Ed Steinfeld, Scott Stern,Ksenia Yudaeva, Luigi Zingales, three anonymous referees, and seminar participants at the NBERcorporate "nance workshop, the Stockholm School of Economics, and the Federal Reserve Bank ofChicago. Florencio Lopez-de-Silanes kindly provided access to unpublished data. Konstantina Drakouliand Matthew Utterback were very helpful research assistants. Generous support was provided by theMIT Entrepreneurship Center and the Russian}European Centre for Economic Policy (RECEP).

*Corresponding author. Tel.: #1-617-253-8412; fax: #1-617-253-2660.

E-mail address: [email protected] (S. Johnson).

Journal of Financial Economics 58 (2000) 141}186

Corporate governance in the Asian "nancialcrisisq

Simon Johnson!,*, Peter Boone", Alasdair Breach#,Eric Friedman$

!Sloan School of Management, Massachusetts Institute of Technology, Cambridge, MA 02142, USA"Brunswick UBS Warburg, 52/4 Kosmodamianskaya Nab., Moscow, Russian Federation

#Goldman Sachs, 22/13 Voznesensky Pereulok, Moscow, Russian Federation$Department of Economics, Rutgers University, New Brunswick, NJ 08903, USA

Received 4 February 1999; received in revised form 19 October 1999

Abstract

The `Asian Crisisa of 1997}98 a!ected all the `emerging marketsa open to capital#ows. Measures of corporate governance, particularly the e!ectiveness of protection forminority shareholders, explain the extent of exchange rate depreciation and stock marketdecline better than do standard macroeconomic measures. A possible explanation is thatin countries with weak corporate governance, worse economic prospects result in moreexpropriation by managers and thus a larger fall in asset prices. ( 2000 Elsevier ScienceS.A. All rights reserved.

JEL classixcation: G18; G38; K22

Keywords: Corporate governance; Investor protection; Financial crisis

FINEC=1093=KG Shankar=Venkatachala=BG

0304-405X/00/$ - see front matter ( 2000 Elsevier Science S.A. All rights reserved.PII: S 0 3 0 4 - 4 0 5 X ( 0 0 ) 0 0 0 6 9 - 6

1. Introduction

What caused the large exchange rate depreciations and stock market declinesin some Asian countries during 1997}98? The three main explanations for the`Asian crisisa emphasize macroeconomic and banking issues. The standardWashington view attributes the Asian crisis to inappropriate macroeconomicpolicy during the 1990s, made worse by inept management of the initial depre-ciation in 1997 (Greenspan, 1998; Corsetti et al., 1998). In contrast, Radelet andSachs (1998a, b) and Wade and Veneroso (1998) argue that the crisis began witha mild panic that had no real foundation and was made serious only by IMFpressure to increase interest rates and to close down banks. Krugman (1998)presents a third theory based on international bank behavior, arguing there wasa `Pangloss equilibriuma that caused a bubble in asset prices. In his view, theAsian panics had their origins in implicit (and implausible) guarantees o!ered bygovernments and believed by investors.

These explanations agree that for some reason, perhaps unrelated to economicfundamentals, there was a loss of con"dence by domestic and foreign investors inall emerging markets. This led to a fall in capital in#ows and an increase in capitalout#ows that triggered, in some cases, a very large nominal depreciation anda stock market crash. At the same time, these explanations do not address exactlywhy this loss of con"dence had such large e!ects on the exchange rate and stockmarket in some emerging market countries but not in others.

This paper presents evidence that the weakness of legal institutions forcorporate governance had an important e!ect on the extent of depreciations andstock market declines in the Asian crisis. By `corporate governancea we meanthe e!ectiveness of mechanisms that minimize agency con#icts involving man-agers, with particular emphasis on the legal mechanisms that prevent theexpropriation of minority shareholders (see Shleifer and Vishny, 1997a). Thetheoretical explanation is simple and quite complementary to the usual macro-economic arguments. If expropriation by managers increases when the expectedrate of return on investment falls, then an adverse shock to investor con"dencewill lead to increased expropriation as well as lower capital in#ow and greaterattempted capital out#ow for a country. These, in turn, will translate into lowerstock prices and a depreciated exchange rate. In the case of the Asian crisis, we"nd that corporate governance provides at least as convincing an explanationfor the extent of exchange rate depreciation and stock market decline as any orall of the usual macroeconomic arguments.

The Bangkok Bank of Commerce is a well-documented example of expropri-ation by managers that worsened as the bank's "nancial troubles deepened.

As the losses mounted, Thai authorities say, more and more money was movedo!shore, much of it through a now-defunct Russian bank2 [It] came to looklike straight siphoning (The Wall Street Journal, May 10, 1999, p. A6.)

Finec=1093=KGM=VVC

142 S. Johnson et al. / Journal of Financial Economics 58 (2000) 141}186

The experience of creditors in Hong Kong who lent to "rms doing business inmainland China is similar } Hong Kong-based company liquidators are notable to recover assets of Chinese companies that default on loans (Wall StreetJournal, August 25, 1999, p. A14.) More generally, very few debt defaults fromthe Asian crisis of 1997}98 have resulted in investors receiving any liquidationvalue. The Economist (January 30, 1999, p. 59) reports that `despite the creationlast year of a bankruptcy law in Indonesia where there had been none before, itis still virtually impossible to force a defaulted debtor into liquidation (the fewcreditors that have tried are still tangled up in legal appeals).aDuring the crisis,Korean minority shareholders protested the transfer of resources out of large"rms, including Samsung Electronics and SK Telecom. Most collapses of banksand "rms in Russia after the devaluation of August 1998 were associated withcomplete expropriation; creditors and minority shareholders got nothing(Troika Dialog, 1999). Table 1 summarizes the details of leading allegations ofexpropriation in countries a!ected by the Asian crisis. Note that in many ofthese cases, controlling shareholders did not need to break any local laws inorder to expropriate from investors.

In most of these instances, management was able to transfer cash and otherassets out of a company with outside investors, perhaps to pay the manage-ment's personal debts, to shore up another company with di!erent shareholders,or to go straight into a foreign bank account. The fact that management in mostemerging markets is also the controlling shareholder makes these transferseasier to achieve. The downturns in these countries have been associated withsigni"cantly more expropriation of cash and tangible assets by managers.

Our results highlight the importance of the legal protection a!orded creditorsand minority shareholders and are closely linked to the recent "ndings of LaPorta et al. (1997, 1998, 1999b), hereafter referred to as LLSV. These authorsshow that the extent to which creditor and minority shareholder rights areprotected explains a great deal of the variation in how "rms are funded andowned across countries. In particular, LLSV (1997) provide evidence froma sample of 49 countries that weak shareholder rights and poor enforcementlead to underdeveloped stock markets. Here we show that weak enforcement ofshareholder rights has "rst-order importance in determining the extent ofexchange rate depreciation and stock market collapse in 1997}98.

Related ideas have been expressed by Yellen (1998), Rajan and Zingales (1998),and Caballero and Krishnamurthy (1998). Yellen argues that `a &relationships'model of capital allocation is extraordinarily susceptible to a deterioration inperceptions about the quality of investment decisions.a Rajan and Zingalesexplain the problems that can occur when a relationship-based "nancial system isopened up to capital in#ows. Caballero and Krishnamurthy emphasize theunderinvestment in appropriate collateral that occurs due to incentive problems.

Section 2 presents the assumptions and implications of our model. Section 3explains our sources and data on exchange rate depreciation and stock market

Finec=1093=KGM=VVC

S. Johnson et al. / Journal of Financial Economics 58 (2000) 141}186 143

Tab

le1

Alle

ged

inci

den

tsofst

ealing

inth

eA

sian"nan

cial

crisis.!

Com

pany

Cou

ntr

yD

ate

Alleg

edin

ciden

t

Ban

gkok

Ban

kof

Com

mer

ceThai

land

1996}97

Ban

km

anag

ers

mov

edm

one

yto

o!sh

ore

com

pan

ies

unde

rth

eir

contr

ol.

United

Eng

inee

rs(M

alay

sia)

Bhd

Mal

aysia

1997}98

United

Eng

inee

rsba

iled

out

its"nan

cial

lytr

oub

led

par

ent,

Ren

ong

Bhd,

by

acqu

irin

ga

33%

stak

eat

anar

ti"ci

ally

high

price

.

Mal

aysia

Air

Sys

tem

Bhd.

Mal

aysia

1998

The

chai

rman

used

com

pan

yfu

nds

tore

tire

per

sonal

deb

ts.

PT

Ban

kBal

iIn

don

esia

1997}98

Man

ager

sdi

vert

edfu

nds

inord

erto"na

nce

apol

itic

alpa

rty.

Sinar

Mas

Gro

up

Indon

esia

1997}98

Gro

up

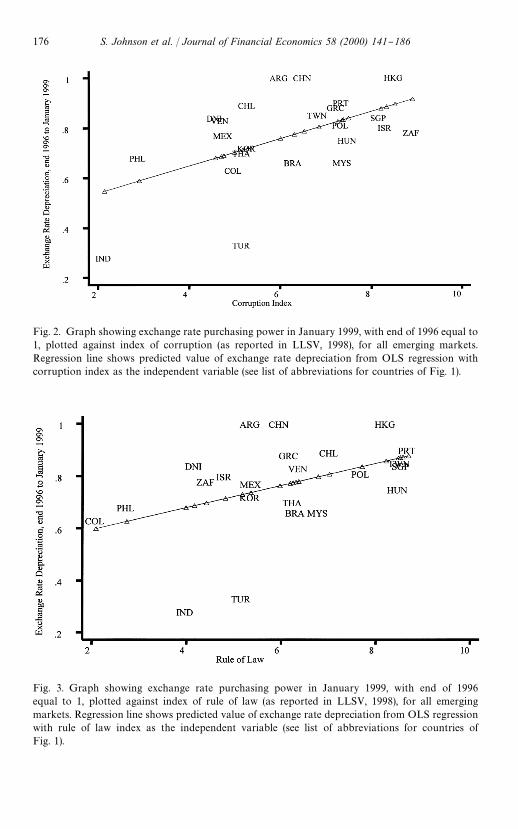

man

ager

str

ansfer

red

fore

ign

exch

ange

loss

esfrom

am

anufa

cturing

com

-pa

nyto

agr

oup-

contr

olle

dban

k,e!

ective

lyex

pro

priat

ing

the

ban

k's

cred

itor

san

dm

inor

ity

shar

ehol

der

s.

Guan

gdong

Inte

rnat

ional

Tru

st&

Inve

stm

entC

oH

ong

Kon

g/C

hina

1998}99

Ass

etsth

athad

been

ple

dge

das

colla

tera

ldisap

pear

edfrom

the

com

pan

yw

hen

itw

ent

bank

rupt

.

Siu-F

ung

Cer

amic

sC

oH

ong

Kon

g/C

hina

1998}99

Ass

etsth

athad

been

ple

dge

das

colla

tera

ldisap

pear

edfrom

the

com

pan

yw

hen

itw

ent

bank

rupt

.

Toko

ban

kR

ussia

1998}99

Cre

ditors

who

may

hav

ebe

enlink

edto

ban

km

anag

ers

took

cont

rolofth

eba

nkan

dits

rem

ainin

gas

sets

follo

win

gde

fault.Fore

ign

cred

itor

sgo

tnoth

ing.

Men

atep

Russ

ia19

98Follo

win

gM

enat

ep's

ban

kru

ptcy

,m

anag

ers

tran

sfer

red

ala

rge

num

ber

of

re-

gion

albra

nch

esto

anoth

erban

kth

eyco

ntr

olle

d.

AO

Yuk

os

Russ

ia19

98}99

Man

ager

str

ansfer

red

Yuko

s's

mos

tva

luab

lepe

trole

um-p

rodu

cing

prop

erties

too!

shore

com

pan

ies

they

contr

olle

d.

Unex

imba

nk

Russ

ia19

99Follo

win

gU

nex

imban

k's

ban

kru

ptcy

,m

anag

ers

move

dpro"ta

ble

cred

it-c

ard

proce

ssin

gan

dcu

stodi

alope

rations

toan

oth

erban

k.

Sam

sung

Ele

ctro

nic

sC

o.

Kore

a19

97}98

Man

ager

sus

edca

shfrom

Sam

sung

Ele

ctro

nics

tosu

pport

other

mem

ber

softh

eSa

msu

nggr

oup

(not

ably

Sam

sung

Moto

rs)th

atw

ere

losing

mon

ey.

Hyu

nda

iK

ore

a19

98}99

Man

ager

sofa

Hyu

nda

i-co

ntr

olle

din

vest

men

tfu

ndch

annel

led

mone

yfrom

reta

ilin

vest

ors

tolo

ss-m

akin

g"rm

sin

the

Hyu

ndai

group

.

!Sourc

es:f

orW

allS

tree

tJo

urn

al,M

ay7,

1999

,p.A

1;A

pril

17,1

998,

p.A

12;S

epte

mbe

r21

,199

9,p.

A1;

Augu

st25

,199

9,p.A

14;A

pril

4,19

99,p

.A1;

Apr

il8,

1999

,p.A

14.The

Eco

nom

ist,

Mar

ch27

,199

9an

dSe

ptem

ber

11,1

999.

Finec=1093=KGM=VVC

144 S. Johnson et al. / Journal of Financial Economics 58 (2000) 141}186

1A referee has pointed out that we could cast the model in terms of general agency problems formanagers (e.g., shirking). Our results apply directly to any managerial agency problems that becomeworse in an economic downturn. Note that many forms of stealing are actually legal in countrieswith weak legal environments (Johnson et al., 2000).

declines during the Asian crisis. Section 4 brie#y assesses the ability of standardmacroeconomic measures to explain the magnitude of depreciation in 1997}98.Section 5 shows that measures of corporate governance provide a better ex-planation for the extent of exchange rate depreciation, and Section 6 assessesboth macroeconomic and corporate governance explanations for stock marketperformance in 1997}98. Section 7 concludes by evaluating the relative strengthof corporate governance and macroeconomic explanations for what happenedin the Asian crisis.

2. Stealing and speculative attacks

2.1. A simple static model

Consider the following simple model, which is related to LLSV (1999b)although they assume a di!erent timing for expropriation relative to investment.As in Jensen and Meckling (1976), the con#ict of interest is between insiders(managers) and outsiders (equity owners in our simple model). The managerowns share a of the "rm and outsiders own share 1!a. Retained earnings aredenoted by I. The manager steals S*0 of retained earnings and obtains utilityof S from them. We use `stealinga as shorthand for more general forms ofexpropriation by managers.

Stealing is costly and the manager expects to lose C(S)"(S2/2k) when hesteals because, for example, other people need to be paid o! and there is someprobability that the manager will be caught and punished. A higher value ofk } representing, in this case, weaker corporate governance rules or a weakerlegal system or both } means that it is less costly to steal. Thus, the value ofstealing, S!C(S), is concave in S. The marginal value of stealing falls as theamount stolen increases because it becomes harder to steal as the absoluteamount of theft increases; the stealing becomes more obvious and easier fora court to stop.1

The manager invests what he does not steal in a project that earns a gross rateof return R, which is greater than one, and from which he obtains the share a ofpro"ts. The manager's optimization problem is given by

MaxS;(S; R, k, a)"Max[aR(I!S)#S!(S2/2k)],

and the optimal amount of theft, SH, is found by solving

L;/LS"1!(SH/k)!aR"0,

Finec=1093=KGM=VVC

S. Johnson et al. / Journal of Financial Economics 58 (2000) 141}186 145

which yields

SH(R, k, a)"k(1!aR).

We assume that the parameter values are such that the manager will not attemptto steal more than the total amount of retained earnings, or SH(R, k, a))I. Thissimpli"es the analysis by avoiding a corner solution, without changing the maininsights.

The manager equalizes the marginal cost and marginal bene"t of stealing.Because the manager owns a of the "rm, he has an incentive to invest at leastsome of the "rm's cash rather than to steal it all. As a rises, the equilibriumamount of stealing falls. As k rises, the amount of stealing in equilibrium rises. Ifa'1/R, the manager's stealing is `negativea, meaning the manager puts in someof his own money into the "rm, perhaps to keep the "rm alive and enjoy`positivea stealing in the future (Friedman and Johnson, 1999). For our pur-poses, we assume that a is low enough that the manager chooses to steal.Alternatively, we could assume that the manager is credit constrained. In thisstatic model, assuming that the manager never steals less than zero does notsubstantially alter the analysis.

Di!erentiating the optimal stealing equation with respect to R gives

(LSH/LR)"!ak.

An increase in the rate of return on the invested resources reduces the amount ofstealing because it raises the marginal opportunity cost of the stolen resources.

A larger a means LSH/LR is more negative. If the manager owns more of the"rm, then a given increase in the return on investment convinces him to put moreresources into the investment project and, therefore, to steal less. Conversely, if themanager owns more but the return on investment declines, then he steals more.

A larger value of k means that LSH/LR is more negative. A lower cost ofstealing (higher k) both raises the equilibrium value of stealing and makesstealing more responsive to changes in the rate of return on investment. This isbecause higher k both shifts up the stealing function and makes it less concave(i.e., the returns to stealing do not decrease so strongly.)

The outside investor receives share (1!a) of the returns from the funds thatare actually invested in the "rm. The expected value of the equity in the "rm istherefore

P"R(I!k(1!aR)),

where P is the equity value of the "rm. This is the value of all the equity held byboth outsiders and managers, which equals the total value of the "rm minus thevalue of stealing.

Di!erentiating with respect to R gives the `absolute responsiveness,a

o!"LP/LR"I!k#2Rka,

Finec=1093=KGM=VVC

146 S. Johnson et al. / Journal of Financial Economics 58 (2000) 141}186

2 In order to make the main point, we have presented a simpli"ed model that ignores generalequilibrium e!ects. Assuming a is exogenous, the expected return for an outside investor variesbetween countries that have a di!erent value of k. In equilibrium this would not occur becauseoutside investors would want to invest more in the country with a higher return. A complete modelwould include these general equilibrium e!ects.

3Di!erentiating absolute responsiveness with respect to k gives:

Lo!/Lk"L2P/LRLk"(!LS/Lk)#[!R(L2S/LRLk)].

The "rst term is always negative: a higher value of k increases the absolute level of stealing. But thesecond term is positive }when k is higher, a given change in R induces a smaller change in the level ofstealing (due to the convex stealing costs). When the second term is relatively large in absolute terms,i.e., when R is high, then L2P/LRLk will be positive.

which is the sensitivity of "rm value to changes in R. This is always positivebecause we have assumed that the optimal level of stealing is less than I. Themaximum value of stealing, given by the "rst-order condition when aR is zero, isk. We have already assumed that there cannot be `negativea stealing, so k)I,and thus is su$cient to ensure that o

!'0.

There are two e!ects of a higher R. The "rst, direct e!ect is to raise theexpected payo! and thus increase the amount that the investor is willing to putinto the "rm. Holding the level of stealing constant, the direct e!ect shows thatthe value of the "rm rises. The second, indirect e!ect works because higherreturns from investment reduce the optimal level of stealing, so LS*/LR(0.Lower stealing also raises the expected payo! for outside investors and increasesthe value of the "rm.2

What is the e!ect on LP/LR of changing the penalty for managerial theft, k?The e!ect on the absolute responsiveness is

Lo!/Lk"2Ra!1.

For low values of aR, such that Ra(1/2, a higher value of k (a lower penalty)implies a fall in LP/LR. For high values of aR, however, a higher value ofk implies an increase in LP/LR. The intuition for this result is that when aR issmall the manager is already stealing a great deal, so P is already low in absoluteterms and thus further changes in R do not induce much additional theft.3

However, we can obtain an unambiguous prediction for the relative respon-siveness,

o3"(LP/LR)/P"(I!k(1!aR)#Rka)/R(I!k(1!aR)),

which is the sensitivity of "rm value in percentage terms. The derivative of thischange with respect to k is

Lo3/Lk"Ia/(I!k#Rka)2'0.

This e!ect is positive regardless of the value of a. Note that the relation betweenabsolute and relative responsiveness is

L(o!)/Lk"L(Po

3)/Lk"P[Lo

3/Lk]#[LP/Lk](o

3).

Finec=1093=KGM=VVC

S. Johnson et al. / Journal of Financial Economics 58 (2000) 141}186 147

The "rst term is positive. The second term contains LP/Lk, which is negative.A higher value of k (i.e., a weaker legal environment) implies that (LP/LR)/Pincreases, so that the value of the "rm, P, becomes more sensitive in percentageterms to a change in the rate of return, R. The same result holds if we allow "rmsto borrow debt as well as issue equity. However, the presence of debt impliesa range of values for R within which a lower value of R actually means lessstealing because the manager steals less (or even transfers funds into the "rm ifthat is possible) in order to enable the "rm to service its debt and thereforepreserve the possibility of future stealing. If R falls su$ciently low, however, thenthe manager will choose to loot the "rm and it will go out of existence. In thedata, therefore, we will look at percentage changes in "rms' values.

2.2. Implications for the exchange rate

Our model so far has dealt exclusively with the e!ect of a loss of con"dence onthe value of a single "rm. Aggregating similar "rms to create an economy-widecollapse of "rms' values is straightforward. We can also reasonably assume thatforeign investors and many domestic investors care about returns in dollars. Wethen have the result that a fall in R, which is now a loss of con"dence aboutreturns in dollars, can trigger a fall in "rms' values in dollars (i.e., the value of thestock market in dollar terms). Note that "rms' values could fall sharply, even ifthere is not much actual stealing, because the value of "rms' to outsiders isdetermined by expected expropriation.

But will such a collapse of "rms' values occur alongside an exchange ratecollapse? Theoretically, a sharp fall in stock prices need not a!ect the exchangerate. Outside investors can choose to bring more capital into the country if, forexample, they are more patient than domestic investors. The exchange rate onlydepreciates if the loss of con"dence about R also triggers a fall in capital in#owsor larger capital out#ows. Greenspan (1998, p. 3) explains the depreciation spiraland its spread across countries as follows: `The loss of con"dence can triggerrapid and disruptive changes in the pattern of "nance, which, in turn feeds backon exchange rates and asset prices. Moreover, investor concerns that weak-nesses revealed in one economy may be present in others that are similarlystructured means that the loss of con"dence can be quickly spread to othercountries.a In fact, if the foreign exchange market is forward looking, the mereprospect of a reduction in net capital in#ows should be enough to cause animmediate depreciation.

There are "ve reasons why a loss of con"dence can cause the net capital in#owto fall and why this fall can be larger when corporate governance is weaker.First, when the expected return to outside investors is lower, investing ina country is less attractive. Outside investors receive less because the actualreturns on investment projects are lower and because managers steal more. Fora given level of expected risk, lower expected returns tend to reduce the net

Finec=1093=KGM=VVC

148 S. Johnson et al. / Journal of Financial Economics 58 (2000) 141}186

capital in#ow to a particular country. In a full model, if investors learn that theexpected return in a country is lower, while risk is unchanged or has even increased,their preference for assets in this country will be reduced. This is one reason whymany global investment funds cut their positions in emerging markets in 1997}98(see International Organization of Securities Commissions (1998)). Weaker corpo-rate governance means lower short-term expected returns or more risk or both.

Second, there are important agency-related reasons why traders who havejust lost a great deal of money cannot immediately invest more in a country,even if they believe that the expected returns are high. Shleifer and Vishny(1997b) develop a model in which traders cannot persuade their "nancialbackers that they should be allowed to invest more, because having lost moneymay indicate that the trader has bad judgment: `The seemingly perverse behav-ior of taking money away from an arbitrageur after noise trader sentimentdeepens, i.e., precisely when his expected return is greatest, is a rational responseto the problem of trying to infer the arbitrageur's (unobserved) ability and futureopportunities jointly from past returnsa, (p. 41.) In reaction to a fall in assetprices, "nancial backers might insist that the trader cut his or her position ina country even further. Shleifer and Vishny (1997b) make this argument forhedge funds involved in arbitrage, but the same argument can be applied tolarge international banks lending to countries. As these investors pull theirmoney out, the exchange rate depreciates.

Third, there could be particular institutional reasons why commercial banksrefuse to roll over their loans. This might be due to regulatory rules andprocedures that limit a bank's `value at riska (Cornelius, 1999). When prices fallin a market, the value-at-risk models used by international banks can generatethe direct requirement that the bank reduce its exposure to that country(Folkerts-Landau and Garber, 1998.) Unless the borrower defaults when theloans are not rolled over, this constitutes a capital out#ow. Even if the borrowerdefaults, there will still be a reduction in new capital in#ow. The details ofvalue-at-risk models vary, but a bigger fall in asset prices, due to worse corpo-rate governance, can plausibly trigger a larger reduction in the bank's invest-ment position in all the assets of that country.

The fourth reason that a loss of con"dence can trigger a decline in net capitalin#ow is that when managers choose to steal more of the corporate cash, theymight take the money outside the country. For this to happen, managers mustcare about their returns in foreign currency terms, perhaps because they havepersonal expenses in dollars or because they feel that local-currency-denominated assets, such as bank deposits, are not the right place to keep theproceeds of what they have stolen (e.g., because they want to avoid taxes.)Weaker corporate governance means that more is stolen for a given reduction inexpected R, leading to more capital #ight and deeper currency depreciation.

Finally, as an important complement to the previous four explanations, theremight be no safe haven for investors in local-currency-denominated assets.

Finec=1093=KGM=VVC

S. Johnson et al. / Journal of Financial Economics 58 (2000) 141}186 149

Management of local commercial banks can also engage in theft, raising theprobability that these banks will default. The government could guarantee bankdeposits but in most emerging markets there is a signi"cant risk that thegovernment will default. In fact, in some emerging market countries, such asIndonesia and Thailand, there was no liquid market for government securities at thetime of the crisis. In the view of many investors during the Asian crisis, theprobability of government default went up as the value of "rms and tax receiptswent down. The only government that actually defaulted on domestic currency debtduring the crisis was Russia, but a number of other governments appear to havecome close. Thus, when the value of "rms began to fall in each emerging marketcountry, both domestic and foreign investors tried to withdraw their money from alldomestic-currency-denominated assets, leading to greater capital out#ows for coun-tries with weaker corporate governance. Note that there can be a net capitalout#ow even if foreign investors remain con"dent. A loss of con"dence in local-currency-denominated assets by domestic investors can be just as damaging.

These arguments suggest that the extent of exchange rate depreciation can bea!ected by corporate governance institutions. As long as a larger fall in "rms'values means that investors are less inclined to buy their securities, then capitalcan #ow out of the country. The evidence in fact shows a sharp reduction incapital in#ows to emerging markets after July 1997, turning into capital out-#ows by September (Brunswick Warburg, 1999). The World Bank (1999,pp. 25}26) estimates that capital out#ows from emerging markets increased by$80 million between 1996 and 1997. We do not have precise estimates of capital#ows, including capital #ight, by country. Net capital in#ows to emergingeconomies peaked at $330 billion in 1996 but fell to less than half that in theAsian crisis (Goldman Sachs, Emerging Markets Quarterly, July 1999, p. 3).

2.3. Corporate governance and volatility

In our model, there need not be any actual expropriation by managers whiletimes are good, for example when aR*1. Typically, in most emerging marketsa is above 0.3 (i.e., much higher than is usual in the U.S.), so a reasonablyoptimistic expectation for R might be enough to remove the incentive formanagerial theft. Detailed examination of insider ownership in some emergingmarkets is in La Porta et al. (1999) and LLSV (1999b), who "nd, for example,that the median cash #ow rights (in companies where insiders control more than20% of the votes) are 41% in Argentina, 26% in Korea, 28% in Hong Kong,34% in Mexico, 20% in Israel, and 31% in Singapore. This suggests that the`institutionsa that protect investors' rights are not important as long as growthlasts, because managers do not want to steal. It may even be possible to attracta great deal of outside capital during a period when the economy expands. Butwhen growth prospects decline, the lack of good corporate governance becomesimportant. Without e!ective shareholder protection, a mild shock can entail

Finec=1093=KGM=VVC

150 S. Johnson et al. / Journal of Financial Economics 58 (2000) 141}186

a large increase in stealing, which in turn causes a large depreciation. This explains,for example, how a country can grow rapidly even if its institutions are #awed.Prime Minister Mahathir of Malaysia argues that rapid growth implies that theinstitutions are good: `We were growing at the rate of more than 8% a year foralmost ten years. You must give us credit for knowing how to run the countrya (TheFar Eastern Economic Review, July 2, 1998, p. 15.) However, our model showsthat institutions matter most when an economy experiences a downturn.

According to this argument, a country can grow rapidly for an inde"nite periodeven if it has weak protection for shareholder rights. But weak institutions of thiskind make a country vulnerable, in the sense that a small negative shock to expectedfuture earnings can have a large e!ect on the economy. If this theory is correct,institutions a!ect volatility, speci"cally the size of the decline in asset values andexchange rates when there is an adverse shock to expected future earnings.

Our argument suggests two empirical issues to investigate. First, across countrieswhere there is some initial loss of con"dence, does the exchange rate depreciatemore when corporate governance is weaker? We deal with this in Section 5. Oursimple model is silent on whether de facto or de jure shareholder and creditor rightsmatter more. We can test these alternatives by examining which kinds of rights weremore important in determining the extent of exchange rate depreciation in 1997}98.Second, the model predicts that countries with poor corporate governance shouldalso have weaker ex post stock market performance if we include the 1997}98 crisis.We examine the evidence on this point in Section 6.

3. Data

3.1. Measuring the crisis

Our basic sample is 25 emerging markets: Argentina, Brazil, Chile, China,Colombia, the Czech Republic, Greece, Hong Kong, Hungary, India, Indonesia,Israel, Korea, Malaysia, Mexico, Philippines, Poland, Portugal, Russia, Sin-gapore, Thailand, Turkey, Taiwan, South Africa, and Venezuela. The list in-cludes six countries from Latin America, four from Eastern Europe, ten fromAsia, plus Greece and Portugal in Europe, Turkey and Israel in the Middle East,and South Africa. There is no universally accepted de"nition of the `emergingmarketsa involved in the Asian crisis, but our sample of 25 includes almost allthe countries regarded as `emerginga by the International Finance Corporation,The Economist, J.P. Morgan, Goldman Sachs, and Flemings Research. This isthe set of developing countries with relatively large "nancial markets andrelatively open capital accounts.

According to the IFC (Emerging Markets Factbook 1997, p. 334), at the end of1996 there was completely free entry and exit of capital (with regard to listedstocks) in 12 of our countries: Argentina, Brazil, the Czech Republic, Greece,

Finec=1093=KGM=VVC

S. Johnson et al. / Journal of Financial Economics 58 (2000) 141}186 151

Hungary, Malaysia, Mexico, Poland, Portugal, Russia, South Africa, and Tur-key. There was also `relatively free entrya and free exit in Chile, Korea,Thailand, and Venezuela. There was `relatively free entrya and `some restric-tionsa on exit in Indonesia. Formally, there was free entry and exit only forspecial classes of shares in China and the Philippines, although the anecdotalevidence suggests that these capital controls have only really been e!ective inChina. Only authorized investors were allowed into Colombia and India, butfree exit was allowed. The tightest market access, according to the IFC measure,was in Taiwan, where only authorized investors were allowed in and there were`some restrictionsa on the repatriation of income and capital. The IFC did notclassify Hong Kong, Israel, and Singapore.

We follow the literature on the Asian crisis by regarding the extent of thenominal exchange rate depreciation as the key variable to be explained. Speci"-cally, our most important dependent variable is the change in the nominalexchange rate from the end of 1996 to January 1999. We take the end of 1996 asthe starting point and measure the change in purchasing power over the nexttwo years of currencies relative to the U.S. dollar. If the exchange rate depreci-ates from 2,500 to 10,000 to the dollar (as with the Indonesian rupiah), it has lostthree-quarters of its purchasing power (i.e. four times as many rupiah are neededto buy one dollar). Alternatively, its purchasing power now is one-quarter of itsformer level and this country would score 0.25 in our index of change inpurchasing power. Table 2 shows the exchange rates and change in purchasingpower of exchange rates for alternative ending points for the 25 countries in oursample.

The crisis clearly began in summer 1997 with the initial devaluation ofThailand. However, there is no agreement on when the crisis ended. There werebasically four phases: fall 1997, when the major problems were in Asia and a fewcountries in Latin America; spring 1998, when the crisis is perceived to havespread to Russia and Brazil; summer 1998, when Russia devalued; and fall 1998,when Brazil struggled against devaluation. The crisis from Brazil's point of viewcontinued at least through the eventual devaluation in January 1999, althoughby this time most of the Asian countries were starting to recover (and theirexchange rates were actually appreciating). All our regressions use mid-January1999 as the ending point. None of our results are a!ected by including orexcluding Brazil's January 1999 devaluation, and we also perform similarregression results using March 1998, July 1998, September 1998, November1998, and April 1999 as alternative ending points. Table 2 presents the rawexchange rate data for these alternative dates. We report these robustnesschecks in more detail as we move through the analysis.

For stock markets, we use the International Finance Corporation's InvestableIndex (published in the IFC's 1998 and 1999 Emerging Markets Factbook andupdated daily in the Financial Times) which measures stock market returns fora selected set of companies in U.S. dollars. This index includes the largest and

Finec=1093=KGM=VVC

152 S. Johnson et al. / Journal of Financial Economics 58 (2000) 141}186

most liquid stocks in each market. Using the IFC's Investable Index reduces theusual problem whereby posted prices in illiquid markets are not real transactionprices. Table 3 reports the value of this IFC index at the end of 1998 and at itslowest point in 1998, assuming that the value for each country was equal to 100at the end of 1996. The IFC does not report an index for Hong Kong orSingapore, so we use the standard Hang Seng Stock Index and Straits TimesStock Index respectively, converted into U.S. dollars.

Some countries begin to show de"nite signs of economic recovery in thesecond half of 1998, just as other countries are experiencing the full e!ects of thecrisis. For example, the Korean index we use reaches a low point of 23.6 at theend of September, but recovers to 53.1 by the end of the year. In our mainregressions we therefore look at the lowest point in the stock market during1998 to measure how far the market falls as a result of the crisis. We also checkour results using the end of 1998 as an alternative end point.

In terms of the model, our empirical tests assume that R and a are constantacross countries. We test whether k, as measured by corporate governancevariables, has an independent impact. This assumption is reasonable to a "rstapproximation because the anecdotal evidence suggests there was a similarshock across all emerging markets. Most of the essays in Hunter et al. (1999)argue or assume that there was a similar shock of some kind across all emergingmarkets (see also Biers, 1998). We do not know if the size of this initial shock tocon"dence was exactly the same in all countries, but the evidence indicates boththat the initial loss of con"dence was small and that, at least in fall 1997, almostevery emerging market was a!ected (International Monetary Fund, 1997.) It ispossible that the shock was larger in countries with weaker institutions forreasons that are unrelated to institutions. However, there is no evidence of sucha pattern to the shock. The anecdotal evidence suggests that there was a smallloss of investor con"dence that began in Thailand, spread through Asia, andthen suddenly included other emerging markets, marked by a surprising sell-o!in Hong Kong from October 1997. By November 1997 there had been somesmall loss of con"dence or questioning of future prospects in almost all emergingmarkets.

3.2. Measuring economic conditions

To measure prior economic conditions we use standard macroeconomicaggregates (the raw data are in Table 3). We use the versions of these datapublished by two investment banks, J.P. Morgan (Emerging Markets: EconomicIndicators, Dec. 5, 1997) and Goldman Sachs (Emerging Markets Biweekly, Dec.10, 1997). Both of these organizations build their databases using the availableinformation from national statistical o$ces and international organizations,most notably the IMF and the World Bank, but they also put a great deal ofe!ort into ensuring that the data are comparable across countries. In addition,

Finec=1093=KGM=VVC

S. Johnson et al. / Journal of Financial Economics 58 (2000) 141}186 153

Tab

le2

Ext

ent

ofex

chan

gera

tede

pre

ciat

ion

inem

ergi

ngm

arket

s,19

97}99

.!

Purc

hasing

pow

erofcu

rren

cyExc

han

gera

tes

Mar

ch19

98/

end

1996

July

1998

/en

d19

96

Sept

1998

/en

d19

96

Nov

1998

/en

d19

96

Jan

1999

/en

d19

96

Apr

1999

/en

d19

96End-

1996

Mar

ch-

98Ju

ly-

98Se

ptem

ber

-98

Nov.

1998

Janu

ary- 99

Apr

il- 99

Arg

entina

1.00

1.00

1.00

1.00

1.00

1.00

0.99

981

11

11

1Bra

zil

0.92

0.90

0.88

0.87

0.66

0.63

1.04

1.13

1.16

1.18

1.19

1.58

1.66

Chi

le0.

940.

900.

900.

920.

890.

8942

4.35

453

471

473

462

478

479

Chi

na

1.00

1.00

1.00

1.00

1.00

1.00

8.30

8.28

8.28

8.28

8.28

8.28

8.28

Colo

mbia

0.74

0.74

0.67

0.64

0.63

0.63

1,00

61,

354

1,35

21,

498

1,56

71,

595

1,59

4C

zech

0.80

0.83

0.89

0.93

0.88

0.78

27.2

334

32.9

30.5

29.4

31.1

35G

reec

e0.

860.

810.

840.

880.

880.

8224

6.71

287

306

295

280

279

300

Hong

Kon

g1.

001.

001.

001.

001.

001.

007.

737.

747.

757.

757.

747.

757.

75H

ung

ary

0.77

0.73

0.73

0.75

0.75

0.69

161.

6520

922

022

221

521

623

4In

dia

0.91

0.85

0.84

0.85

0.84

0.84

35.8

339

.542

.242

.642

.342

.542

.8In

dones

ia0.

240.

160.

200.

270.

280.

272,

363

9,65

014

,500

11,7

008,

850

8,47

58,

625

Isra

el0.

910.

890.

850.

760.

800.

813.

253.

583.

663.

834.

294.

054.

03K

ore

a0.

540.

620.

620.

640.

720.

7084

5.50

1565

1371

1362

1312

1167

1214

Mex

ico

0.92

0.88

0.76

0.79

0.77

0.83

7.87

8.58

8.93

10.3

89.

9410

.17

9.51

Mal

aysia

0.66

0.61

0.66

0.66

0.66

0.66

2.53

3.81

4.15

3.8

3.8

3.8

3.8

Phili

ppi

nes

0.66

0.64

0.60

0.67

0.68

0.69

26.3

039

.841

.443

.939

.438

.438

.2Pola

nd0.

820.

820.

790.

830.

810.

722.

863.

483.

493.

623.

433.

533.

98Port

ugal

0.83

0.83

0.88

.0.

900.

8215

5.25

186

186

177

173.

417

3.43

189.

2

Finec=1093=KGM=VVC

154 S. Johnson et al. / Journal of Financial Economics 58 (2000) 141}186

Rus

sia

0.93

0.93

0.33

0.36

0.24

0.22

5.59

66

1715

.63

23.2

25.8

Singa

pore

0.86

0.83

0.81

0.87

0.84

0.83

1.41

1.64

1.69

1.74

1.62

1.68

1.69

Thai

land

0.58

0.61

0.63

0.70

0.70

0.68

25.6

444

.442

.141

36.6

36.5

37.6

Turk

ey0.

470.

410.

390.

380.

330.

2910

9,09

523

2,15

526

7,53

027

6,40

029

0,12

032

9,00

037

9,28

0Tai

wan

0.86

0.80

0.79

0.85

0.85

0.84

27.5

032

34.4

34.6

32.5

32.3

32.9

Ven

ezue

la0.

920.

860.

810.

840.

830.

8147

6.26

519

555

587

567

571

589

South

Afric

a0.

950.

780.

750.

840.

780.

774.

684.

936.

016.

245.

576

6.08

!Sou

rces

(1)The

Eco

nom

ist

for

Mar

ch19

98,Ju

ly19

98,Sep

tem

ber

1998

,N

ovem

ber

1998

,Ja

nua

ry19

99,a

nd

April19

99M

arch

exch

ange

rate

sar

eM

arch

4ofea

chye

ar(fr

omThe

Eco

nom

ist,

Mar

ch7t

h,19

98)

July

exch

ange

rate

sar

eJu

ly1

(fro

mThe

Eco

nom

ist,

July

4th,1

998)

Sept

ember

exch

ange

rate

sar

eSep

tem

ber

9th

(from

The

Eco

nom

ist,

Sep

tem

ber

12th

,19

98)

Nove

mber

exch

ange

rate

sar

eN

ovem

ber

4th

(from

The

Eco

nom

ist,

Nov

embe

r7t

h,1

998;

this

issu

edid

not

repo

rta

rate

for

Por

tuga

l);t

he

Nov

embe

r19

98ex

chan

gera

tefo

rP

ortu

galis

from

the

Inte

rnat

iona

lF

inan

ceC

orpora

tion's

Em

ergi

ngM

arket

sD

atab

ase

(199

9).

Janu

ary

1999

exch

ange

rate

sar

eJa

nuar

y20

th(fr

omThe

Eco

nom

ist,

Janua

ry23

rd,19

99);

Por

tuga

lis

from

the

Wal

lSt

reet

Jour

nal,

Janu

ary

28A

pril19

99ex

chan

gera

tes

are

Apr

il21

st(fro

mThe

Eco

nom

ist,

April24

th,1

999)

;Por

tuga

lis

from

the

Fin

anci

alTim

esA

pril

23(2

)IF

C19

98,p.

32fo

ren

dof19

96(T

heIF

Cdo

esno

tre

port

anex

chan

gera

tefo

rH

ong

Kon

gan

dSin

gapo

re;t

hese

are

from

The

Eco

nom

ist,

Janu

ary

2nd,

1999

)The"rs

tsix

colu

mns

show

the

chan

gein

purc

has

ing

pow

erofth

ecu

rren

cy,ta

king

the

end

of19

96as

equal

toone.

Chan

gein

purc

hasing

pow

eris

calc

ula

ted

asth

eex

chan

gera

teat

the

end

of19

96div

ided

by

the

exch

ange

rate

in19

98or

1999

.The

exch

ange

rate

atth

een

dof

1996

isgi

ven

inth

ese

venth

colu

mn.

Exc

han

gera

tes

for

1998

and

1999

are

inth

e8t

h}14

thco

lum

ns.

All

exch

ange

rate

sar

elo

calcu

rren

cyunits

per

U.S

.dolla

r.The

sam

ple

isth

e25`e

mer

ging

mar

ket

s,a

asvi

ewed

byin

tern

atio

nal

inve

stor

s.Thes

ear

ere

lative

lyla

rge

dev

elop

ing

countr

ies

open

toca

pital#ow

s.W

eus

eth

ese

tofc

ountr

ies

clas

si"ed

asem

ergi

ng

mar

kets

by

The

Eco

nom

ist(a

lthou

ghP

ortu

galw

asdro

pped

from

this

group

in19

98),

J.P.M

org

an,

and

Gold

man

Sach

s.

Finec=1093=KGM=VVC

S. Johnson et al. / Journal of Financial Economics 58 (2000) 141}186 155

Tab

le3

Dat

aus

edin

regr

ession

s.!

Mac

roec

onom

icva

riab

les

Gov

ernm

ent

budg

etba

lance

asa

Per

cent

1996

Bro

adm

oney

grow

th,

%per

annu

m,

1996

Curr

ent

acco

unt

asa

per

cent

ofG

DP

,19

96

Tota

lre

serv

es,

billi

ons

ofU

Sdolla

rsat

the

end

of19

96

Import

cove

rage

,m

onth

sof

import

s,at

the

end

of19

96

Tota

lfo

reig

ndeb

t,m

illio

ns

of

US

dolla

rs,

atth

een

dof

1996

Fore

ign

debtas

aper

centof

expo

rts,

for

1996

Sho

rt-ter

mde

btan

dam

ortiza

tion

asa

per

cent

ofre

serv

es,

for

1996

Inte

rest

paym

ents

asa

perc

ent

ofex

port

s,fo

r19

96

Ext

ernal

debt-

GD

Pra

tio,

end

of

1996

Arg

entina

!2.

019

.8!

1.3

18.1

5.8

105,

388

311

111

18.6

0.35

Bra

zil

!3.

928

.9!

3.3

60.1

5.7

194,

046

296

148

20.6

0.26

Chi

le2.

223

.6!

3.3

14.8

8.7

24,4

4911

432

6.5

0.34

Chi

na

!0.

925

.30.

910

7.0

8.8

150,

541

7039

2.6

0.18

Colo

mbia

!1.

121

.0!

5.4

9.6

6.3

26,8

9816

062

13.7

0.31

Cze

ch!

0.1

9.2

!8.

012

.43.

420

,412

6062

6.0

0.39

Gre

ece

!7.

413

.3!

3.7

17.5

5.8

55,3

3621

916

83.

70.

37H

ong

Kon

g1.

318

.31.

963

.83.

949

1,10

014

4n.

a.n.

a.2.

2H

ung

ary

!3.

320

.9!

3.2

9.8

3.5

27,6

4699

6310

.70.

64In

dia

!5.

016

.5!

1.1

20.2

5.2

95,7

9717

293

10.1

0.27

Indo

nes

ia0.

029

.6!

3.4

18.3

4.6

121,

374

198

152

11.7

0.53

Isra

el!

4.3

25.0

!7.

011

.43.

147

,600

231

n.a.

190.

504

Kore

a!

1.8

16.2

!4.

733

.21.

510

6,92

267

377

3.6

0.22

Mex

ico

0.4

30.5

!0.

619

.42.

116

9,67

512

224

211

.70.

51M

alay

sia

!0.

520

.6!

6.3

27.0

2.6

38,5

5338

742.

40.

39

Finec=1093=KGM=VVC

156 S. Johnson et al. / Journal of Financial Economics 58 (2000) 141}186

Phili

ppi

nes

!0.

215

.8!

4.5

10.0

2.1

56,6

1611

719

46.

60.

68Pola

nd

!2.

529

.0!

1.0

17.8

5.3

41,6

2810

314

4.2

0.31

Port

ugal

!2.

35.

6!

1.4

21.9

5.7

65,0

1025

5n.

a.16

.30.

607

Rus

sia

!7.

833

.72.

111

.33.

112

3,11

712

912

27.

30.

27Si

nga

pore

7.0

9.8

15.2

76.8

6.0

288,

500

188

n.a.

n.a.

3.00

Thai

land

1.5

16.6

!4.

337

.74.

498

,368

124

134

3.5

0.65

Turk

ey!

8.2

120.

5!

2.4

16.5

3.5

79,7

4715

219

78.

70.

43Tai

wan

!8.

77.

84.

088

.06.

942

,797

3037

1.4

0.15

Ven

ezue

la1.

448

.313

.111

.88.

834

,037

120

648.

30.

39So

uth

Afric

a!

5.6

13.6

!1.

60.

91.

532

,927

8918

86.

70.

26

Sourc

eJP

Morg

anan

dse

ebe

low

Gol

dm

anSa

chs

and

see

belo

w

JPM

org

anan

dse

ebe

low

JPM

org

anan

dse

ebe

low

JPM

org

anan

dse

ebe

low

JPM

org

anan

dse

ebe

low

JPM

org

anan

dse

ebe

low

JPM

org

anJP

Morg

anan

dse

ebe

low

JPM

orga

nan

dse

ebe

low

Coun

trie

sm

issing

Non

eN

one

Non

eN

one

Non

eN

one

Non

eIs

rael

Hong

Kon

gN

one

Por

tuga

lSin

gapo

reH

ong

Kon

gSi

ngap

ore

Sam

ple

size

2525

2525

2525

2521

2325

Finec=1093=KGM=VVC

S. Johnson et al. / Journal of Financial Economics 58 (2000) 141}186 157

Tab

le3

(con

tinu

ed) C

orpo

rate

gove

rnan

ceva

riab

les

Judic

ial

e$ci

ency

Corr

uption

Rule

of

law

Enfo

rcea

ble

min

ority

shar

edhol

der

righ

ts

Ant

i-di

rect

ors

righ

tsC

reditors

righ

ts

Acc

ounting

stan

dar

ds,

1990

Arg

entina

6.0

6.0

5.4

3.0

41

45Bra

zil

5.8

6.3

6.3

3.0

31

54C

hile

7.3

5.3

7.0

3.5

52

52C

hina

n.a.

6.5

6.0

n.a.

n.a.

n.a.

n.a.

Colo

mbia

7.3

5.0

2.1

n.a.

30

50C

zech

n.a.

n.a.

n.a.

2.0

n.a.

n.a.

n.a.

Gre

ece

7.0

7.3

6.2

n.a.

21

55H

ong

Kon

g10

.08.

58.

23.

05

469

Hung

ary

n.a.

7.5

8.5

3.0

n.a

.n.a

.n.

a.In

dia

8.0

4.6

4.2

2.0

54

57In

dones

ia2.

52.

14.

01.

02

4n.

a.Is

rael

10.0

8.3

4.8

3.0

34

64K

ore

a6.

05.

35.

41.

02

362

Mex

ico

6.0

4.8

5.4

3.0

10

60M

alay

sia

9.0

7.4

6.8

2.0

44

76

Finec=1093=KGM=VVC

158 S. Johnson et al. / Journal of Financial Economics 58 (2000) 141}186

Phili

ppi

nes

4.8

2.9

2.7

3.0

30

65Pola

nd

n.a.

7.4

7.7

4.0

n.a

.n.a

.n.

a.Port

ugal

5.5

7.4

8.7

n.a.

31

36R

uss

ian.

a.n.a

.n.a

.2.

0n.a

.n.a

.n.

a.Si

nga

pore

10.0

8.2

8.6

4.0

44

78Thai

land

3.3

5.2

6.3

2.0

23

64Turk

ey4.

05.

25.

22.

02

251

Tai

wan

6.8

6.9

8.5

3.0

32

65V

enez

uela

6.5

4.7

6.4

n.a.

1n.

a.40

South

Afric

a6.

08.

94.

42.

55

370

Sourc

eL

LSV

"19

98LL

SV19

98LLSV

1998

Fle

min

gsLL

SV19

98LLSV

1998

LLSV

1998

Coun

trie

sm

issing

Chi

na

Cze

chC

zech

Rep

ublic

Chi

na

Chin

aC

hin

aC

hina

Cze

chR

ussia

Rus

sia

Colo

mbi

aC

zech

Rep

ubl

icC

zech

Rep

ublic

Cze

chR

epub

licH

ung

ary

Gre

ece

Hung

ary

Hung

ary

Hung

ary

Pola

nd

Por

tuga

lPola

nd

Pola

ndPola

nd

Rus

sia

Ven

ezue

laR

ussia

Russ

iaR

ussia

Ven

ezue

laIn

dones

ia

Sam

ple

size

2023

2320

2019

19

Finec=1093=KGM=VVC

S. Johnson et al. / Journal of Financial Economics 58 (2000) 141}186 159

Tab

le3

(con

tinu

ed)

IFC

inve

stab

lein

dex

inat

low

est

poin

tin

1998

(with

end

of19

96"

100)

IFC

inve

stab

lein

dex

aten

dof

1998

(with

end

of19

96"

100)

Mont

hin

whic

hIF

Cin

vest

able

inde

xre

ached

low

estpoin

tin

1998

Arg

entina

68.9

83.9

Aug

ust

Bra

zil

69.4

69.4

Sept

ember

Chi

le62

.472

.8A

ugus

tC

hina

29.0

35.5

Aug

ust

Colo

mbia

51.6

69.4

Oct

obe

rC

zech

59.4

72.3

Augu

stIn

dia

75.0

81.5

Nove

mber

Gre

ece

124.

925

5.5

Janu

ary

Hong

Kon

g41

.147

.8Se

ptem

ber

Hung

ary

103.

914

2.6

Sept

ember

Indo

nes

ia8.

519

.0Se

ptem

ber

Isra

el94

.710

2.2

Oct

ober

Kore

a30

.668

.7Se

ptem

ber

Mex

ico

73.7

90.5

Augu

stM

alay

sia

12.8

26.3

Augu

stPhili

ppi

nes

22.7

41.9

Augu

stPola

nd

63.3

71.5

Augu

stPort

ugal

158.

819

9.8

Sept

ember

Russ

ian.

a.n.

a.Se

ptem

ber

Singa

pore

40.8

61.2

Sept

ember

Thai

land

14.3

28.5

Augu

stTurk

ey90

.798

.4O

ctobe

rTai

wan

66.3

75.6

Augu

stV

enez

uela

37.5

62.3

Aug

ust

South

Afric

a49

.760

.0A

ugus

t

Finec=1093=KGM=VVC

160 S. Johnson et al. / Journal of Financial Economics 58 (2000) 141}186

Sourc

eIF

C#

1999

IFC

1999

IFC

1999

Coun

trie

sm

issing

Rus

sia

Rus

sia

Sam

ple

size

2424

!Add

itio

nalnu

mbe

rsto"ll

gaps

(at

reco

mm

endat

ion

ofre

fere

e)ar

efrom

:Fisca

lde"ci

tin

Isra

el,P

ortu

gal,

and

Ven

ezue

la(fr

omW

orld

Ban

k,19

99)

Bro

adm

oney

grow

thin

Gre

ece,

Isra

el,a

ndP

ortu

gal(fr

om

Wor

ldBan

k,19

99)

Cur

rentac

coun

tin

Isra

elan

dPort

uga

l(fr

omW

orld

Ban

k,19

99)

Tota

lre

serv

esin

Isra

elan

dP

ortg

ual

(from

Wor

ldB

ank,

1999

)Im

port

cove

rage

inIs

rael

,P

ortu

gal,

and

Sin

gapo

re(fr

om

World

Ban

k,19

99);

dat

afo

rH

ong

Kong

calc

ula

ted

from

Pol

itic

alR

isk

Ser

vice

s(1

999)

,w

ww

.cou

ntr

ydat

a.co

m.

Tota

lfo

reig

ndeb

tfo

rH

ong

Kon

g,Is

rael

and

Singa

por

e(fr

om

Gol

dm

anSac

hs19

99);

dat

afo

rPor

tuga

lfrom

Polit

ical

Risk

Ser

vice

s(1

999)

,w

ww

.cou

ntr

ydat

a.co

m.

Fore

ign

deb

tas

aper

centof

expor

tsfo

rH

ong

Kong

and

Sin

gapor

e(fr

om

Gol

dman

Sach

sE

mer

ging

Mar

ket

sQ

uar

terly,

July

1999

);dat

afo

rP

ort

uga

lan

dIs

rael

from

Polit

ical

Risk

Ser

vice

s(1

999)

,w

ww

.cou

ntr

ydat

a.co

m.

Inte

rest

pay

men

tsas

aper

cent

ofex

port

sfo

rIs

rael

from

Pol

itic

alR

isk

Ser

vice

s19

99Ext

ernal

Deb

t-G

DP

ratio

forH

ong

Kong

and

Sin

gapore

(from

Gol

dm

anSa

chs,

Em

ergi

ngM

arke

tsQ

uart

erly

,199

9);d

ata

forIs

rael

and

Por

tuga

lfrom

Polit

ical

Risk

Ser

vice

s(1

999)

,w

ww

.cou

ntr

ydat

a.co

m.

Note

that

the

info

rmat

ion

onde

bt/ex

por

tsan

din

tere

stpay

men

ts/e

xport

san

ddeb

t/G

DP

for

Hong

Kong

and

Singa

pore

isfo

rea

rly

1999

Var

iable

de"nitio

nsnot

give

nin

colu

mn

head

ings

Judic

ialE$

cien

cy,T

able

1in

LLSV

(199

8)de

scribe

sth

isva

riab

leas

follow

s.A

sses

smen

toft

he`e$

cien

cyan

din

tegr

ity

oft

hele

gale

nvironm

entas

ita!

ects

busines

s,par

ticu

larly

fore

ign"rm

sapr

odu

ced

byth

eco

untr

y-risk

rating

agen

cyB

usin

ess

Inte

rnat

iona

lC

orpor

atio

n.It`m

aybe

taken

tore

pres

entin

vest

ors'as

sess

men

tsofc

ond

itio

nsin

the

countr

yin

que

stio

n.aA

vera

gebet

wee

n19

80an

d19

83.S

cale

from

0to

10,w

ith

low

ersc

ores

[mea

nin

g]lo

wer

e$ci

ency

leve

ls.

Cor

ruption

The

dat

afo

rC

hina,

Hun

gary

,Pol

and

are

not

inLL

SV(1

998)

but

wer

epro

vide

dby

Lope

z-de-

Sila

nes

(199

8).T

able

1in

LLSV

(199

8)de

scribe

sth

isva

riab

leas

follow

s.IC

R's

asse

ssm

entofth

eco

rrup

tion

ingo

vern

men

t.Low

ersc

ores

indic

ate

that`h

igh

gove

rnm

ento$

cial

sar

elik

ely

todem

and

spec

ialpa

ymen

tsa

and

`ille

gal

pay

men

tsar

ege

nera

llyex

pec

ted

thro

ugh

out

low

erle

vels

ofgo

vern

men

tain

the

form

of`b

ribes

conne

cted

with

import

and

expo

rtlic

ense

s,ex

chan

geco

ntro

ls,t

axas

sess

men

t,po

licy

pro

tect

ion,o

rlo

ans.a

Ave

rage

ofth

em

ont

hs

ofA

prilan

dO

ctobe

rof

the

mont

hly

inde

xbet

wee

n19

82an

d19

95.S

cale

from

0to

10,w

ith

low

ersc

ore

sfo

rhi

gher

leve

lsof

corr

upt

ion.(W

e[L

LSV

]ch

ange

dth

esc

ale

from

its

orig

inal

range

goin

gfrom

0to

6.)

Finec=1093=KGM=VVC

S. Johnson et al. / Journal of Financial Economics 58 (2000) 141}186 161

Tab

le3

Footnot

e(c

ontinu

ed)

Rul

eofl

aw.

The

dat

afo

rC

hin

a,H

unga

ry,P

olan

dw

ereag

ain

provi

ded

by

Lop

ez-d

e-Si

lane

s.Tab

le1

inLLSV

(199

8)des

crib

esth

isva

riab

leas

follo

ws.

Ass

essm

ent

ofth

ela

wan

dor

der

trad

itio

nin

the

count

rypro

duce

dby

the

countr

y-risk

rating

agen

cyIn

tern

atio

nal

Coun

try

Risk

(IC

R).

Ave

rage

ofth

em

ont

hs

ofA

pril

and

Oct

obe

rofth

em

onth

lyin

dex

bet

wee

n19

82an

d19

95.

Scal

efrom

0to

10,w

ith

low

ersc

ores

for

less

trad

itio

nfo

rla

wan

dor

der

.(W

e[L

LSV

]ch

ange

dth

esc

ale

from

its

orig

inal

rang

ego

ing

from

0to

6.)

Ant

i-direc

tor

righ

ts.

Tab

le1

inL

LSV

(199

8)des

crib

esth

isva

riab

leas

follo

ws.

An

index

aggr

egat

ing

the

shar

ehold

errigh

tsw

hich

we

label

edas`y

anti-d

irec

torrigh

ts.a

The

inde

xis

form

edby

addin

g1

when

:(1)

the

countr

yal

low

ssh

areh

older

sto

mai

lthei

rpro

xyvo

teto

the"rm

;(2)

shar

ehol

der

sar

eno

tre

quired

todep

ositth

eirsh

ares

priorto

the

Gen

eral

Shar

ehold

ers'

Mee

ting;

(3)

cum

ula

tive

voting

orpro

por

tion

alre

pres

enta

tion

ofm

inorities

inth

ebo

ard

ofdirec

tors

isal

low

ed;(

4)an

oppr

esse

dm

inorities

mec

han

ism

isin

pla

ce;(

5)th

em

inim

um

perc

enta

geof

shar

eca

pita

ltha

ten

titles

ash

areh

old

erto

call

foran

Ext

raor

dinar

yShar

ehol

ders'M

eeting

isle

ssth

anoreq

ualt

o10

per

cent

(the

sam

ple

med

ian)

;or

(6)sh

areh

olde

rshav

epre

empt

ive

righ

tsth

atca

nonly

be

wai

ved

bya

shar

ehol

ders'vo

te.The

inde

xra

nges

from

0to

6.

Cre

ditor

righ

ts.

Tab

le1

inL

LSV

(199

8)de

scribe

sth

isva

riab

leas

follow

s.A

nin

dex

aggr

egat

ing

di!

eren

tcr

editor

righ

ts.T

he

index

isfo

rmed

by

addi

ng

1w

hen

(1)t

he

count

ryim

pose

sre

strict

ions,

such

ascr

editors'co

nsen

tor

min

imum

divi

den

dsto"le

forre

org

aniz

atio

n;(2

)sec

ure

dcr

editors

are

able

toga

inpo

sses

sion

ofth

eirse

curity

once

the

reor

ganiz

atio

npe

tition

hasbee

nap

prove

d(n

oau

tom

atic

stay

);(3

)se

cure

dcr

editors

are

ranked"rs

tin

the

distr

ibution

ofth

epr

ocee

ds

that

resu

ltfrom

the

dispo

sition

ofth

eas

sets

of

aban

kru

pt"rm

;and

(4)t

he

deb

tordoe

snotre

tain

the

adm

inistr

atio

nof

itspro

per

type

ndi

ng

the

reso

lution

oft

here

org

aniz

atio

n.T

he

index

rang

esfrom

zero

tofo

ur.

Acc

ounting

stan

dar

ds.

Tab

le1

inL

LSV

(199

8)des

crib

esth

isva

riab

leas

follo

ws.

Inde

xcr

eate

dby

exam

inin

gan

dra

ting

com

panie

s'19

90an

nua

lre

port

son

thei

rin

clusion

or

om

ission

of90

item

s.Thes

eitem

sfa

llin

tose

ven

cate

gories

(gen

eral

info

rmat

ion,

inco

me

stat

emen

ts,b

alan

cesh

eets

,fun

ds#ow

stat

emen

t,ac

coun

ting

stan

dard

s,st

ock

dat

a,an

dsp

ecia

litem

s.)A

min

imum

ofth

ree

com

panie

sin

each

coun

try

wer

est

udie

d.The

com

pan

iesre

pre

sent

acr

ossse

ctio

nofv

ario

usin

dust

rygr

oup

s;in

dus

tria

lcom

panie

sre

pres

ente

d70

perc

ent,

and"nan

cial

com

panie

sre

pre

sente

dth

ere

mai

nin

g30

perc

ent.

"LLSV

1998

isLa

Port

a,Lop

ez-d

e-Sila

nes

,Sh

leife

ran

dV

ishny

(199

8).

#IF

C19

99is

the

Inte

rnat

ional

Fin

ance

Corp

orat

ion'

s(1

999)

Em

ergi

ngM

arke

tF

actb

ook.

Finec=1093=KGM=VVC

162 S. Johnson et al. / Journal of Financial Economics 58 (2000) 141}186

using these sources helps us examine whether information actually available tothe "nancial markets before the crisis is useful in predicting the exchange rate.Following the suggestion of a referee, we "ll gaps in these data using numbersfrom the World Bank and the IMF (details are in Table 3).

3.3. Measuring institutions