Economic developments and the outlook for trade

AMAN UNION 6TH ANNUAL MEETING

7TH –9TH DECEMBER 2015

MUSCAT -OMAN

about ICISA

● Founded in 1928 (as ICIA)

first credit insurance association

● > 95% of private global market

● > 15% of global trade

● 55 Members

● 34 credit insurance members

● Other members:

● surety bond underwriters

● reinsurance companies

2

ICISA members

3

Association Networking

● AMAN UNION5 shared members (observers)

● ALASECE4 shared members

● BERNE UNION10 shared members

● PASA22 shared members

● SFAA8 shared members

4

types of cover

• Domestic / Export

– “Domestic” is just another country

• Commercial / Political Risk

• Whole Turnover / Single Risk Cover / XoL

• Credit Risk / Pre-Credit Risk

• Short-Term / Medium/Long Term

5

Economic imbalances

China, E.U., USA

QE: stock markets, emerging currencies

Interest rates

Commodity prices

Partnerships (e.g. TTIP)/geopolitical threats

Inflation/deflation

Sanctions

Terrorism

Migration

New global recession?

6

the current TCI market

Mismatch between risk and premium

Fraud and corruption

Neither soft or hard

Stable premium income

Rising claims

7

the current TCI market

Increased competition

Claims rising: Brazil, Canada, China, Russia, Indonesia

Insolvencies construction sector

Soft market with exceptions

Ample reinsurance capacity

Growth in Europe, MENA, Asia & N America

Trade Finance: improving, alternatives

Solvency II: implementation 2016

8

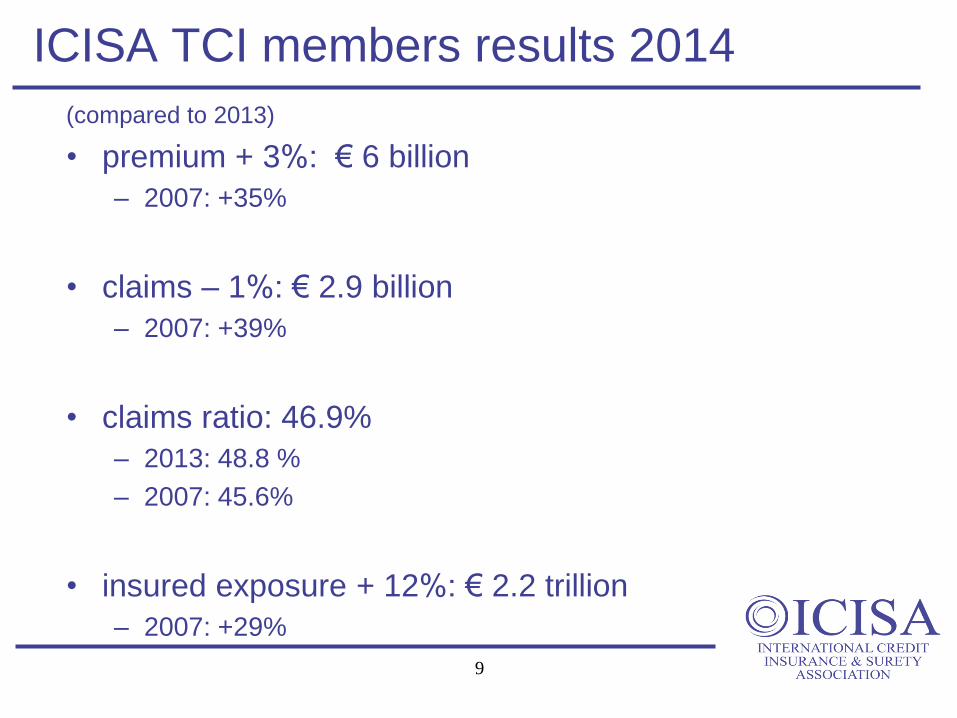

ICISA TCI members results 2014

(compared to 2013)

• premium + 3%: € 6 billion

– 2007: +35%

• claims – 1%: € 2.9 billion

– 2007: +39%

• claims ratio: 46.9%

– 2013: 48.8 %

– 2007: 45.6%

• insured exposure + 12%: € 2.2 trillion

– 2007: +29%

9

Trade credit insurance

premium, claims & claims ratio ICISA Credit Insurance Members

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Claims Ratio in %Amount in EURO

Millio

ns

Premiums

Claims

Claims Ratio in %

Trade credit insurance

Insured ExposureICISA Credit Insurance Members

0

500

1,000

1,500

2,000

2,500

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Billio

ns

Insured Exposure TradeCredit Insurance

Amount in EURO

TCI market trends - premium

56% = stable

24% = decreasing

20% = increasing

12

MENA TCI market trends - premium

60% = stable

20% = decreasing

20% = increasing

13

TCI market trends - claims

59% = stable

32% = increasing

9% = decreasing

14

MENA TCI market trends - claims

75% = stable

25% = increasing

0% = decreasing

15

market trends - insolvencies

61% = stable

29% = increasing

10% = decreasing

16

MENA market trends - insolvencies

86% = stable

14% = increasing

0% = decreasing

17

TCI current market – hard or soft?

24% = hard

43% = neither

33% = soft

18

MENA TCI current market – hard or soft?

25% = hard

75% = neither

0% = soft

19

TCI market trends next 12 months

26% = hard

41% = neither

33% = soft

20

MENA TCI market trends next 12 months

25% = hard

75% = neither

0% = soft

21

reinsurance market trends 12 months

2% = hard

24% = neither

74% = soft

22

outlook 2016 and beyond

23

concerns Trade Credit Insurance

Rising claims: Russia, Brazil, Turkey, China

Fraud: Brazil, China

Political unrest: MENA, South East Asia

Lower premium rates

Financing by banks: SMEs

Alternative financing

Construction sector

Solvency regulations (Europe, other regions)

Regulatory – protectionism - systemic

24

outlook Trade Credit Insurance

• growth in:

● Europe

● Asia

● MENA

● North America

• Markets hard/soft:

• little change expected

• Hardening markets:

● Latin America

• Softening markets:

● Europe

25

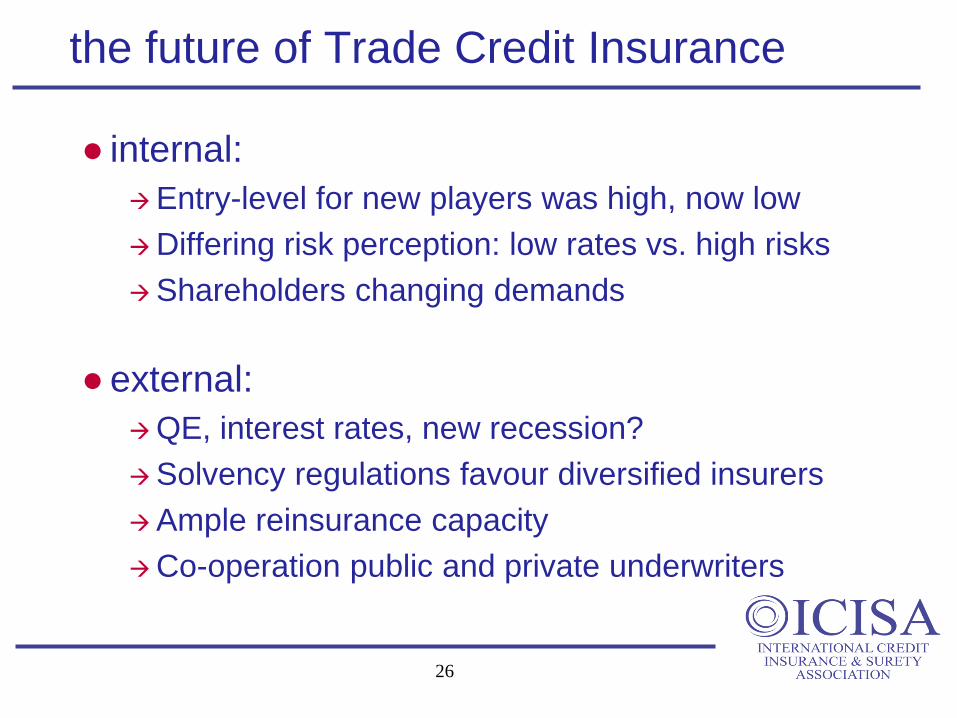

the future of Trade Credit Insurance

● internal:

Entry-level for new players was high, now low

Differing risk perception: low rates vs. high risks

Shareholders changing demands

●external:

QE, interest rates, new recession?

Solvency regulations favour diversified insurers

Ample reinsurance capacity

Co-operation public and private underwriters

26

current advocacy issues

Solvency CAT Risk

Shadow Banking/Systemic Risk

PML/LGD Study

Opening markets: India, Korea

Bankruptcy legislation

Financial information (MENA, Asia):• transparency

• group structures

• key information lacking

• quality

• reliability

• financials - consolidated financials

27

What is Surety?

• Terminology used

– Surety

– Bond

– Guarantee

• Guarantees the performance of a contract

– Construction

– Tax

– Other

Surety Risk Model

Construction

project

Beneficiary Contractor

Surety

Reinsurance

RiskIndemnity

Risk

Risk

Types of Surety Bonds

• Construction Bonds

• Customs or Tax Bonds

• Bond re concessions or licenses

• Lease Bonds

• Judicial Bonds

• Financial Bonds

• Other

The Trade Credit Insurance & Surety Academy

• Training Seminars– Basic and Advanced Training Seminars

• Trade Credit Insurance

• Surety Bond Insurance

– Participants 15 max.

• Tailor-made in-house

[email protected] www.stecis.org

31