Employer Webinar

Copyright 2010

866.390.1871

This Employer Webinar Series program is presented by Spencer Fane Britt & Browne LLP

in conjunction with United Benefit Advisors

Kansas City Omaha Overland ParkSt. Louis Jefferson City www.spencerfane.com

www.UBAbenefits.com

This Employer Webinar Series program is presented by Spencer Fane Britt & Browne LLP

in conjunction with United Benefit Advisors

Copyright 2010

Health Care Reform Update

Presented by

Julia M. Vander WeeleRobert A. Browning

Copyright 2010

Focus of This Update

Provisions effective in 2011 (or earlier) Provisions affecting all plans, including

“grandfathered” plans

Provisions affecting only non-grandfathered plans

Guidance re: “grandfathered” plans Changes causing loss of “grandfathered” status

Other regulatory guidance issued since Health Care Reform legislation was enacted

Copyright 2010

Provisions Applicable toAll Plans

Effective for plan years beginning on or after 9-23-10:

No lifetime dollar limits on “essential health benefits”

Restricted annual limits on “essential health benefits” (until 2014)

No preexisting condition exclusions may be applied to children under age 19

Prohibition will be extended to adults in 2014

Copyright 2010

Provisions Applicable toAll Plans

Effective for plan years beginning on or after 9-23-10: No rescission of coverage allowed, except for

fraud or intentional misrepresentation (in violation of specific plan terms)

Dependent coverage (if offered) must continue through 26th birthday, even if child marries Tax exclusion is extended to end of calendar year in

which child attains age 26 (effective 3-30-10) Until 2014, grandfathered plans may terminate

coverage if child becomes eligible for other employer-provided health coverage

Copyright 2010

Provisions Applicable toAll Plans

Effective for plan years beginning on or after 1-1-2011: Insured plans will be subject to minimum

medical-loss ratios: Based on percentage of premium income

spent on clinical services and activities to improve health care quality

At least 85% in large group market At least 80% in small group market Any “excess” profits must be rebated to

participants

Copyright 2010

Provisions Applicable toAll Plans

Beginning in 2011, employer must report on Form W-2 the total value of employer-provided health coverage

Excludes HSA or FSA contributions Applies to W-2s issued in early 2012 (for 2011)

Employers with more than 200 full-time employees must implement automatic enrollment of all new full-time employees

Subject to employee opt-out Effective date is still to be determined

Copyright 2010

Provisions Applicable toAll Plans

Beginning January 1, 2011, health FSAs, HSAs, HRAs and Archer MSAs cannot reimburse expenses for OTC drugs (other than insulin) unless the drug is prescribed by a physician

Effective in 2011, the excise tax on non-medical distributions from HSAs is increased from 10% to 20%

Copyright 2010

Additional Requirements for Non-Grandfathered Plans

Effective for plan years beginning on or after 9-23-10: Must permit enrollee to designate any network

physician as his or her primary care physician (same rule applies to pediatricians)

May not require pre-authorization or referral for female to visit OB-GYN

Emergency care (if offered) must be covered without preauthorization and as though provided in-network

Expanded claims and appeals procedures

Copyright 2010

Additional Requirements forNon-Grandfathered Plans

Effective for plan years beginning on or after September 23, 2010: Must cover certain preventive services without

cost-sharing Fully insured plans must comply with

nondiscrimination requirements of Code Section 105(h) These are the same rules to which self-funded plans

are already subject However, the consequences of noncompliance fall on

the plan (in the form of a $100 daily penalty), rather than the highly compensated individual (in the form of taxable benefits)

Copyright 2010

Additional Requirements forNon-Grandfathered Plans

Effective when HHS issues implementing regulations (which is to be done by 3-23-12), plan must provide annual reports to HHS and participants (during open enrollment) of steps taken to improve quality of care – e.g.: Wellness programs

Effective case management

Preventing readmissions

Copyright 2010

Guidance Issued to Date

Tri-agency request for information re: medical loss ratio provisions – April 14

IRS Notice re: tax treatment of coverage for children under age 27 – April 27

Tri-agency regulations re: extension of dependent coverage to age 26 – May 13

Tri-agency regulations re: status as “grandfathered” plan – June 17

Copyright 2010

Guidance to Date (cont.)

Tri-agency regulations re: pre-existing conditions, lifetime/annual limits, rescissions, and patient protections – June 28

Tri-agency regulations re: preventive health services – July 19

Tri-agency regulations re: internal claims/appeals, external review – July 23

Copyright 2010

Grandfathered Plans

Definition – Health plan in effect on 3-23-10

Grandfathered status is not lost because new employees are covered, or because covered employees add dependents

Statute was not clear on whether adding current employees, benefit changes, or plan mergers will undermine grandfathered status

Special rules for collectively bargained plans

Copyright 2010

Grandfathered Plans

Determination of grandfathered status is made separately with respect to each benefit package made available under a group health plan

One benefit package might retain grandfathered status while the other benefit package loses grandfathered status

Copyright 2010

Grandfather Plans – Adding New Employees

Regulations clarify that plan retains grandfathered status with respect to new employees (whether newly hired or newly enrolled) and their families

Anti-abuse rules Principal purpose of merger or acquisition must

not be to cover new individuals under grandfathered plan

Transferred employees (must have bona fide employment-based reason for transfer, other than cost)

Copyright 2010

Loss of Grandfathered Status

Change in insurers (but not TPAs) Elimination of all or substantially all benefits to

diagnose or treat a particular condition Increase in fixed cost-sharing requirements

Fixed amounts (e.g., deductibles) cannot be increased more than medical inflation plus 15 percentage points

Co-pays cannot be increased more than the greater of 1) medical inflation plus 15 percentage points, or 2) $5, increased by medical inflation

Any increase in percentage cost-sharing requirement (e.g., coinsurance)

Copyright 2010

Loss of Grandfather Status

Changes to employer contributions If contribution rate based on cost of coverage,

decrease in contribution toward the cost of any tier of coverage by more than 5 percentage points

Total cost of coverage is equivalent to COBRA cost

If contribution rate is based on formula (e.g., hours worked), decrease in contribution rate by more than 5 percent

Copyright 2010

Loss of Grandfather Status

Imposition of new or modified annual limit Addition of any annual limit (if no lifetime

or annual limit before) Adoption of an annual limit that is lower

than previous lifetime limit (if no annual limit before)

Decrease in annual limit (if annual limit before)

Copyright 2010

Loss of Grandfather Status

Changes that are okay: Changes to premiums (other than employer cost-sharing

percentage) Changes to comply with law (federal or state) Changing TPA

Changes that are okay (for now): Changes to plan structure (e.g., from insured to self-

insured) Changes in provider network Changes to prescription drug formulary Other substantial change to overall benefit design

Copyright 2010

Transition Rules

Changes adopted prior to March 23, 2010 are still grandfathered, even if effective later

Changes adopted between March 23, 2010, and issuance of regulations - good faith efforts to comply with a reasonable interpretation of statutory requirements will be taken into account

Grace period to revoke or modify changes adopted prior to regulations

Copyright 2010

Disclosure of Grandfathered Status

Must include statement in all plan materials provided to participants describing benefits that the plan believes it is a grandfathered health plan

Must provide contact information for questions and complaints

Model notice available Plan must retain records demonstrating

terms of plan that were in effect on March 23, 2010

Copyright 2010

Collectively Bargained Plans

General Rule – Retain grandfathered status until at least the expiration of the last CBA that was in effect on 3-23-10 Applies only to insured plans Plan may be voluntarily amended to comply with selected

new requirements without accelerating overall compliance date

Essentially permits insured plan to change insurers during the term of the CBA without losing grandfathered status

On expiration of final CBA, plan will retain grandfathered status until lost under rules in effect at that time

Does not delay the effective date of requirements otherwise applicable to grandfathered plans

Copyright 2010

Dependent Coverage Mandate

If plan makes coverage available to dependent children, such coverage must be available until child’s 26th birthday: Even if the child is married

Regardless of student status

Even if child does not reside with parents

Even if child is not financially dependent on parents

State insurance laws that require coverage beyond age 26 are still applicable

Copyright 2010

Dependent Coverage Mandate -Definition of “Child”

“Child” is not defined in the regulations, but Internal Revenue Code defines “child” as: Son or daughter Stepson or stepdaughter Lawful foster child A child legally adopted by or placed for adoption

with the employee “Child” does not include the spouse or

children of an employee’s adult child (i.e., the employee’s son-in-law, daughter-in-law, or grandchildren)

Copyright 2010

Cost and Terms of Dependent Coverage

Regulations restrict employers’ ability to charge for extended dependent coverage

Employer’s contribution structure for other dependents must be extended to adult children now covered under the mandate (can’t charge more for “adult” children)

Neither contributions nor benefit eligibility can vary based on a child’s age

Copyright 2010

Cost and Terms of Dependent Coverage (cont.)

Tiered or per dependent contributions are permitted (if applied uniformly)

Employers may have to enroll and cover additional dependents under current family contribution rates, or they may consider adopting new contribution structures, such as charging per dependent, regardless of age

Adult child surcharge not allowed Benefit options cannot be age-restricted

Copyright 2010

Dependent Coverage and COBRA

Dependent coverage must be extended to qualified beneficiaries under COBRA Former employee on COBRA would have the

same right to add an adult child up to age 26 as would a similarly situated active employee

Children who have aged out of a plan and now have COBRA continuation coverage must be given the opportunity to enroll as a dependent of an active employee Child who later loses eligibility due to a

qualifying event will then have another opportunity to elect COBRA

Copyright 2010

Special Enrollment Opportunity re: Dependent Coverage

Encompasses all children under age 26 who have lost coverage due to aging out of the plan’s previous eligibility provisions, and those originally denied coverage or ineligible due to age

If a child is eligible under these new rules, a parent not currently enrolled must be given an opportunity to enroll as well

Copyright 2010

Special Enrollment Period re: Dependent Coverage

Mandatory 30-day opportunity to enroll no later than the first day of the first plan year beginning on or after September 23, 2010 Coverage must start no later than that date, even if the

request for coverage is made after that date

Can use open enrollment period, provided special notice is furnished and children are given at least 30 days to enroll Employers planning a shorter enrollment period for their

next open enrollment may wish to alter their strategy and provide at least 30 days for all coverage elections to avoid the need for a separate enrollment process

Copyright 2010

Notice of Dependent Coverage Enrollment Period

Plans must provide written notice of the opportunity to enroll an eligible “child”

A prominent notice must be given (by the plan or an insurer) to the employee on behalf of the child, and may be included with other enrollment materials The enrollment right must offer all benefit

packages available to similarly situated children under 26

Parents may switch to a benefit package option for which a child is eligible

Copyright 2010

Dependent Coverage – Tax Treatment

Prior to Health Care Reform, employers could provide non-taxable health care coverage and/or medical expense reimbursements only to: Employees (including retirees);

Spouses (as defined under DOMA); and

“Dependents,” as defined in Code Section 152 (i.e., “Tax Code Dependents)

Copyright 2010

Tax Code “Dependent”

Under Code Section 152, “dependent” includes a “qualifying child”

A “qualifying child” must: Be a “child” (as defined in earlier slide);

Live with taxpayer for over ½ the year;

Not provide over ½ of own support; and

Be under 19 for entire year, or a full time student who is under 24 for entire year

Copyright 2010

Taxation of Dependent Coverage

Health Care Reform extends the exclusion from income to: Any “child” of the employee who, as of

the end of the taxable year, has not attained age 27

Applies to health plans (including premiums paid via 125 plan), health FSAs, and HRAs (but not HSAs)

Applies to coverage/reimbursements provided on or after March 30, 2010

Copyright 2010

Dependent Coverage and Cafeteria Plans

Exclusion from income applies to: Premiums for coverage of children < 27 paid

with pre-tax employee contributions Reimbursement of medical care expense of

children < 27 through a health FSA

Mid-year “change in status” events may include a child who is <27: Becoming newly eligible for coverage; or Becoming eligible for coverage beyond the date

child would have otherwise lost coverage

Copyright 2010

Dependent Coverage and Cafeteria Plans

125 plans may need to be amended to allow payment of premiums for, or reimbursement of expenses for, a child <27 who is not a Tax Code Dependent

Transition rule allows plan to allow employees to make contributions (for such expenses) immediately, so long as plan is amended by Dec. 31, 2010

Copyright 2010

Dependent Coverage Mandate vs. Tax Exclusion

Different Effective Dates: Coverage Mandate: 1st plan year after Sept. 23,

2010 (i.e., 2011 for calendar year plans)

Tax Change: March 30, 2010

Different Age Limit Coverage Mandate: Until child’s 26th birthday

Tax Change: Thru 12/31 after 26th birthday

Options for voluntary non-taxable coverage: Early implementation (during 2010)

Coverage through end of year child turns 26

Copyright 2010

Lifetime/Annual Limits

“Essential benefits” include at least the following (subject to regulatory guidance): Ambulatory patient services Emergency services Hospitalization Maternity and newborn care Mental health and substance abuse disorder services Prescription drugs Rehabilitative services and devices Laboratory services Preventive and wellness services and chronic disease

management Pediatric services, including oral and vision care

Copyright 2010

Restricted Annual Limits

With respect to benefits that are not essential health benefits, plan may impose annual or lifetime limits on specific covered benefits

Departments will take into account good faith efforts to comply with reasonable interpretation of the term “essential health benefits” but definition must be applied consistently

Exclusion of all benefits for a condition is not a lifetime or annual limit

Copyright 2010

Restricted Annual Limits

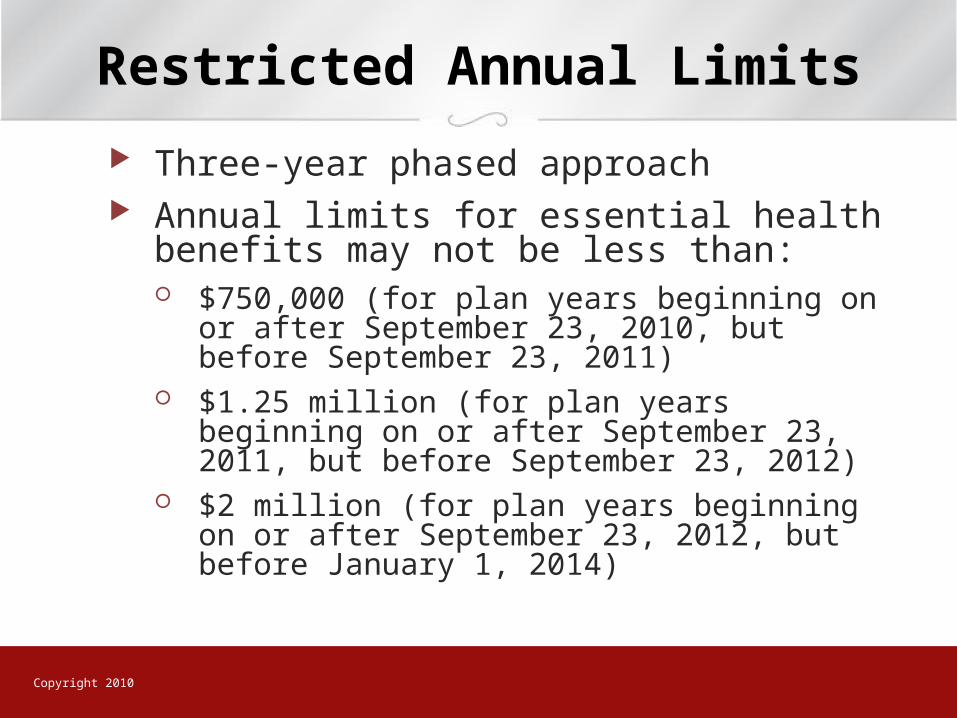

Three-year phased approach Annual limits for essential health benefits

may not be less than: $750,000 (for plan years beginning on or after

September 23, 2010, but before September 23, 2011)

$1.25 million (for plan years beginning on or after September 23, 2011, but before September 23, 2012)

$2 million (for plan years beginning on or after September 23, 2012, but before January 1, 2014)

Copyright 2010

Applicability to HRAs

When HRA integrated with other group health plan coverage (that complies with annual limit restrictions), combined coverage will satisfy requirements

Stand-alone HRA is subject to restricted annual limit requirements

Copyright 2010

Limited Benefit Plans

HHS to establish program under which “mini-med” plans may be excused from complying with restricted annual limit requirements if compliance would result in a significant decrease in access to benefits or a significant increase in premiums

Scope and application process unknown

Copyright 2010

Notice of Lifetime Limit

Individual who previously reached lifetime limit must be notified that lifetime limit no longer applies (if otherwise still eligible)

Must include opportunity to re-enroll in any benefit package

Copyright 2010

Rescissions

May not rescind coverage, except for fraud or intentional misrepresentation

Rescission = cancellation or discontinuance of coverage that has retroactive effect (unless attributable to a failure to pay required premium)

30-day advance notice of rescission required

Copyright 2010

Patient Protections

Choice of any participating and available primary care provider

Notice required – model notice available; must be included in SPD

Regular plan provisions or exclusions relating to pediatric care or OB/GYN care may still apply

Copyright 2010

Emergency Services

Cost-sharing requirements: Co-payment and coinsurance cannot

exceed cost-sharing requirements that would be imposed for in-network services

“Reasonable” amount must be paid before patient responsible for balance billing amount

Copyright 2010

Emergency Services

Plan must cover out-of-network emergency services in amount equal to greatest of: Negotiated in-network amount

In-network cost-sharing provisions

Medicare rate

Copyright 2010

Claims and Appeals Procedures

Applicable only to non-grandfathered plans Even non-ERISA plans will be subject to

existing ERISA regulations (which the DOL plans to strengthen)

Recent regulations apply the following additional requirements: Rules will apply to coverage “rescissions”

Deadline for notifying of ruling on “urgent care claim” will be only 24 hours (versus current 72 hours)

Copyright 2010

Claims and Appeals Procedures

Must disclose additional evidence considered, as well as any new rationale

Must take steps to avoid conflicts of interest by decision makers

Expanded notice rules, including communications in foreign languages

Strict compliance standard will apply (no more “substantial compliance” or “de minimis error” defenses)

Copyright 2010

Claims and Appeals Procedures

Plans must offer external appeal process Insured plans must comply with state-law rules

(if consistent with NAIC model act) Self-funded plans must comply with federal

standards (to be announced) Coverage must be continued during appeal

of a “concurrent care claim” Generally effective for plan years beginning

on or after 9-23-10 (but all state-law external appeal standards are deemed to comply through 7-1-11)

Copyright 2010

Preventive Care Services

Non-grandfathered plans must provide benefits for the following categories of preventive care services: Evidence-based, recommended items or services

carrying a rating of “A” or “B” by the U.S. Preventive Services Task Force;

Immunizations included in the CDC’s Immunization Schedules; and

Evidence-informed, preventive care and screenings supported by the Health Research and Services Administration

Copyright 2010

Preventive Care Services

Benefits must be provided without cost-sharing (deductibles, copays, or coinsurance)

But may limit to in-network providers (or charge more for out-of-network) and apply cost-sharing to other preventive services

And may apply reasonable medical management techniques (so long as not inconsistent with recommended frequencies)

Copyright 2010

Preventive Care Services

Treatment of concurrent office visits: May still charge for separately billed

office visits

And may charge for office visit if primary purpose of visit was not for preventive services

But may not bill for office visit if primary purpose was preventive services

Copyright 2010

Short-Term Incentives for Expansionof Coverage

High Risk Pools for Long-Term Uninsured Established by state or federal governments

Eligibility conditioned on having a preexisting condition and being without health coverage for at least six months

Program is already in effect; set to expire on 1-1-14, when preexisting condition clauses are prohibited

Insurer or self-funded plan must reimburse pool if found to have encouraged individual to disenroll

Copyright 2010

Short-Term Incentives for Expansionof Coverage

Tax Credit for Small Employers Beginning in 2010, small employers (under 25

FTEs, with average annual wages of less than $50,000) may receive a credit of up to 35% of employer contributions for health coverage Employer must pay at least 50% of total premium After 2010, employer must pay uniform percentage of

premium for all employees To receive full credit, employer must have 10 or

fewer FTEs and average annual wages of less than $25,000

In 2014, maximum credit increases to 50%

Copyright 2010

Short-Term Incentives for Expansionof Coverage

Early Retiree Reinsurance Program Program will reimburse “eligible plans” for certain

claims paid on behalf of early retirees (age 55-64) To be an “eligible plan,” a plan (insured or self-

funded) must use procedures designed to generate cost-savings for participants with chronic and high-cost conditions (defined as a condition likely to result in annual claims by one participant of $15,000 or more)

For 2010, program will reimburse 80% of claims between $15,000 and $90,000; dollar amounts will be adjusted for inflation in later years

Copyright 2010

Short-Term Incentives for Expansionof Coverage

Reimbursements may be used either to offset insurance premiums (employer or retiree) or to reduce retirees’ cost-sharing requirements

However, reimbursements may not be used as employer’s general revenue (must prove “maintenance of effort”)

Program ends on 1-1-14 (or sooner, if $5 billion funding amount is exhausted)

Copyright 2010

Penalties for Noncompliance

Generally subject to excise tax of $100 per day per affected participant (under Code Section 4980D)

Penalty for unintentional violations is capped at lesser of $500,000 or 10% of employer’s annual health care costs

Most provisions are also enforceable under ERISA or Public Health Service Act

Certain requirements (e.g., auto enrollment and notification concerning Exchanges) are subject to FLSA penalties

Tax-reporting requirements are subject to reporting penalties

Employer Webinar

Copyright 2010

866.390.1871