8/4/2019 Forecasting 2008

http://slidepdf.com/reader/full/forecasting-2008 1/67

Demand Forecasting

• Four Fundamental Approaches• Time Series „„„

– General Concepts – Evaluating Forecasts – How ‗good‘ is it? – Forecasting Methods (Stationary) Š

• Cumulative Mean Š• Naïve Forecast ŠŠ„ŠŠŠŠ• Moving Average• Exponential Smoothing

– Forecasting Methods (Trends & Seasonality)• OLS Regression• Holt‘s Method• Exponential Method for Seasonal Data• Winter‘s Model Other Models

8/4/2019 Forecasting 2008

http://slidepdf.com/reader/full/forecasting-2008 2/67

Demand Forecasting

• Forecasting is difficult – especially for the future• Forecasts are always wrong• The less aggregated, the lower the accuracy• The longer the time horizon, the lower the accuracy

• The past is usually a pretty good place to start• Everything exhibits seasonality of some sort• A good forecast is not just a number – it should include a

range, description of distribution, etc.• Any analytical method should be supplemented by

external information• A forecast for one function in a company might not beuseful to another function (Sales to Mkt to Mfg to Trans)

8/4/2019 Forecasting 2008

http://slidepdf.com/reader/full/forecasting-2008 3/67

Four Fundamental Approaches

Subjective – Judgmental

• Sales force surveys• Delphi techniques• Jury of experts

– Experimental

• Customer surveys• Focus group sessions• Test Marketing

Objective – Causal / Relational

• Econometric Models• Leading Indicators• Input-Output Models

– Time Series

• ―Black Box‖ Approach • Uses past to predict

the future

8/4/2019 Forecasting 2008

http://slidepdf.com/reader/full/forecasting-2008 4/67

Time Series Concepts

1. Time Series – Regular & recurring basis to forecast2. Stationarity – Values hover around a mean3. Trend- Persistent movement in one direction4. Seasonality – Movement periodic to calendar

5. Cycle – Periodic movement not tied to calendar6. Pattern + Noise – Predictable and random components of aTime Series forecast

7. Generating Process –Equation that creates TS8. Accuracy and Bias – Closeness to actual vs Persistent

tendency to over or under predict9. Fit versus Forecast – Tradeoff between accuracy to past

forecast to usefulness of predictability10. Forecast Optimality – Error is equal to the random noise

8/4/2019 Forecasting 2008

http://slidepdf.com/reader/full/forecasting-2008 5/67

8/4/2019 Forecasting 2008

http://slidepdf.com/reader/full/forecasting-2008 6/67

Demand Forecasting

• Generate the large number of short-term, SKUlevel, locally dis-aggregated demand forecastsrequired for production, logistics, and sales to

operate successfully. „• Focus on: ŠŠŠŠŠ – Forecasting product demand – Mature products (not new product releases)

– Short time horizon (weeks, months, quarters, year) – Use of models to assist in the forecast – Cases where demand of items is independent

8/4/2019 Forecasting 2008

http://slidepdf.com/reader/full/forecasting-2008 7/67

Historical Data

0 50

100 150 200 250 300 350 400

0 10 20 30 40 50

Forecasting Terminology

Initialization ExPostForecast

Forecast

Historical Data

8/4/2019 Forecasting 2008

http://slidepdf.com/reader/full/forecasting-2008 8/67

―We are now looking at a future from here, and thefuture we were looking at in February now includessome of our past, and we can incorporate the past

into our forecast. 1993, the first half, which is nowthe past and was the future when we issued our firstforecast, is now over‖

Laura D‘Andrea Tyson, Head of the President‘s Council of Economic Advisors, quoted in November of 1993 in the Chicago Tribune , explaining why the Administration reduced its projectionsof economic growth to 2 percent from the 3.1percent it predicted inFebruary.

Forecasting Terminology

8/4/2019 Forecasting 2008

http://slidepdf.com/reader/full/forecasting-2008 9/67

Forecasting Problem

• Suppose your fraternity/sorority houseconsumed the following number of cases ofbeer for the last 6 weekends: 8, 5, 7, 3, 6, 9

0

1

23

4

5

6

7

8

9

10

0 1 2 3 4 5 6 7

Week

C a s e s

• How many casesdo you think yourfraternity / sorority

will consume thisweekend?

8/4/2019 Forecasting 2008

http://slidepdf.com/reader/full/forecasting-2008 10/67

0 1 2 3 4 5 6 7 8 9 10

0 1 2 3 4 5 6 7 8 Week

C a s e s

Forecasting:Simple Moving Average Method

• Using a three period moving average, wewould get the following forecast:

63

963F

8/4/2019 Forecasting 2008

http://slidepdf.com/reader/full/forecasting-2008 11/67

0 1 2 3 4 5 6 7 8 9 10

0 1 2 3 4 5 6 7 8 Week

C a s e s

Forecasting:Simple Moving Average Method

• What if we used a two period moving average?

5.72

96F

8/4/2019 Forecasting 2008

http://slidepdf.com/reader/full/forecasting-2008 12/67

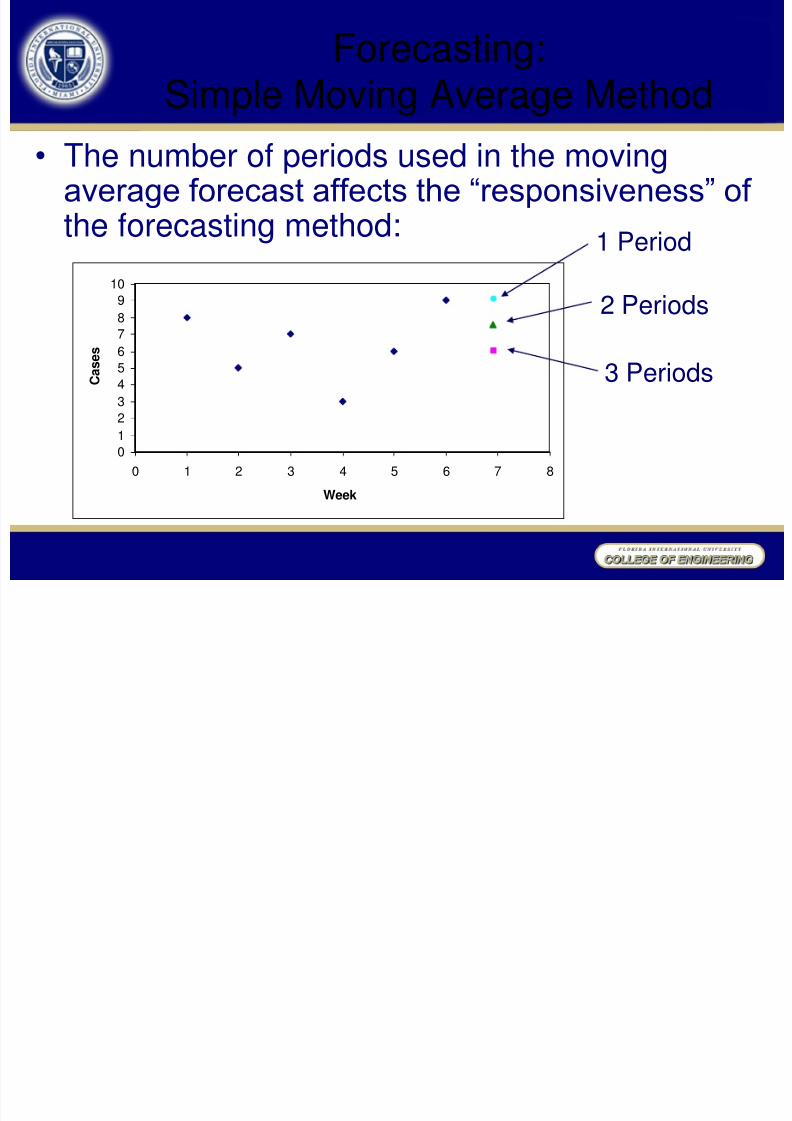

• The number of periods used in the movingaverage forecast affects the ―responsiveness‖ of the forecasting method:

0 1 2 3 4 5 6 7 8 9 10

0 1 2 3 4 5 6 7 8 Week

C a s e s

Forecasting:Simple Moving Average Method

2 Periods

3 Periods

1 Period

8/4/2019 Forecasting 2008

http://slidepdf.com/reader/full/forecasting-2008 13/67

t A(t) F(t)1 8

2 5

3 7

4 3 6.67

5 6 5

6 9 5.33

7 68 6

9 6

10 6

Forecasting Terminology

• Applying this terminology to our problemusing the Moving Average forecast:

Initialization

ExPostForecast

Forecast

ModelEvaluation

8/4/2019 Forecasting 2008

http://slidepdf.com/reader/full/forecasting-2008 14/67

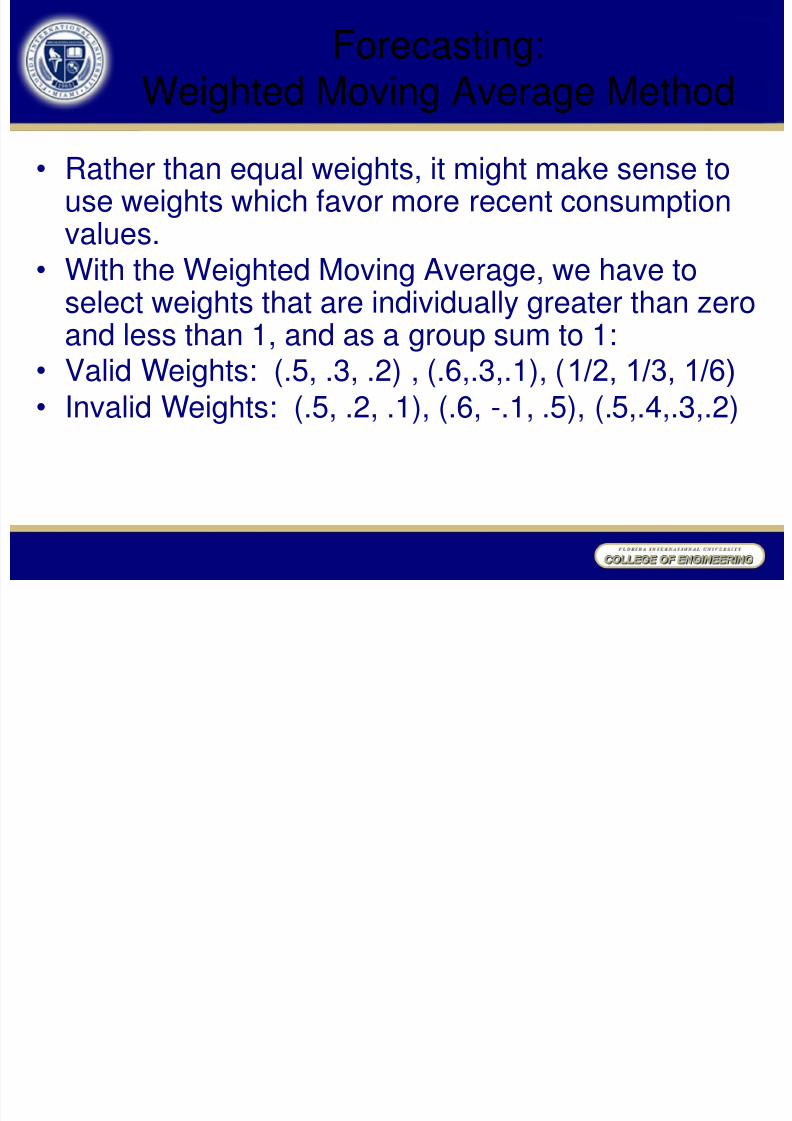

• Rather than equal weights, it might make sense touse weights which favor more recent consumptionvalues.

• With the Weighted Moving Average, we have toselect weights that are individually greater than zeroand less than 1, and as a group sum to 1:

• Valid Weights: (.5, .3, .2) , (.6,.3,.1), (1/2, 1/3, 1/6)

• Invalid Weights: (.5, .2, .1), (.6, -.1, .5), (.5,.4,.3,.2)

Forecasting:Weighted Moving Average Method

8/4/2019 Forecasting 2008

http://slidepdf.com/reader/full/forecasting-2008 15/67

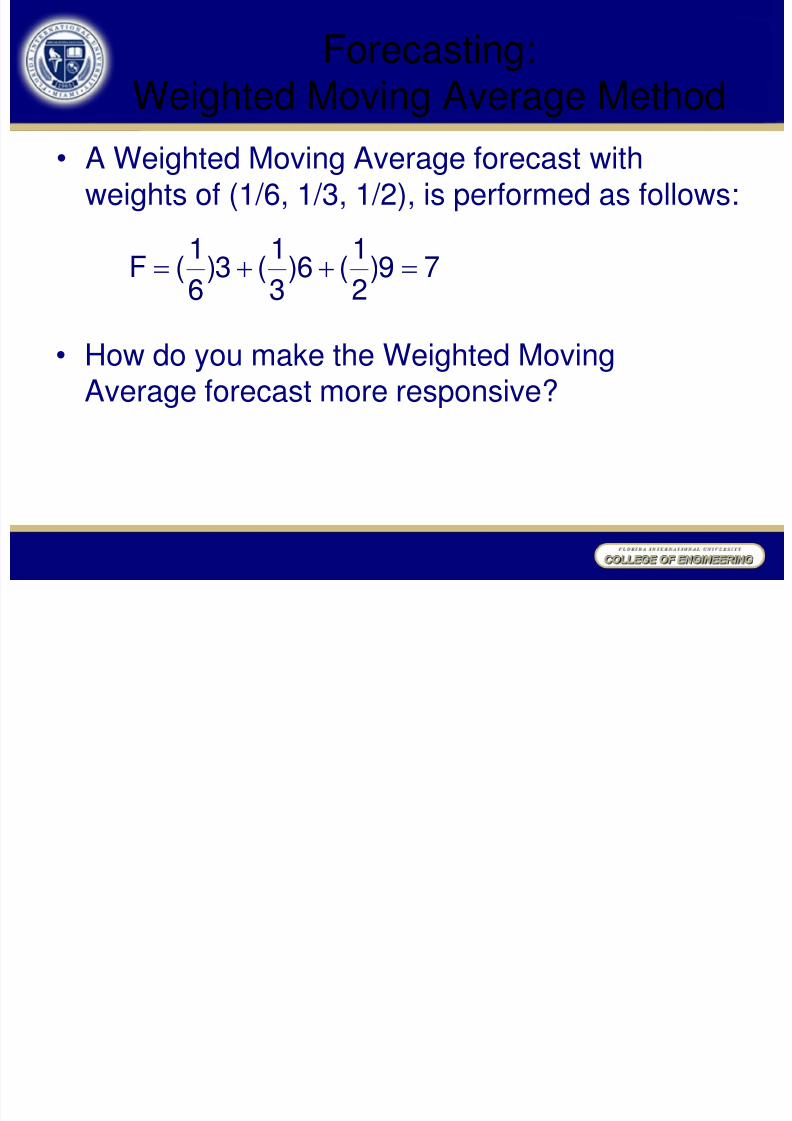

Forecasting:Weighted Moving Average Method

• A Weighted Moving Average forecast withweights of (1/6, 1/3, 1/2), is performed as follows:

• How do you make the Weighted MovingAverage forecast more responsive?

79)2

1

(6)3

1

(3)6

1

(F

8/4/2019 Forecasting 2008

http://slidepdf.com/reader/full/forecasting-2008 16/67

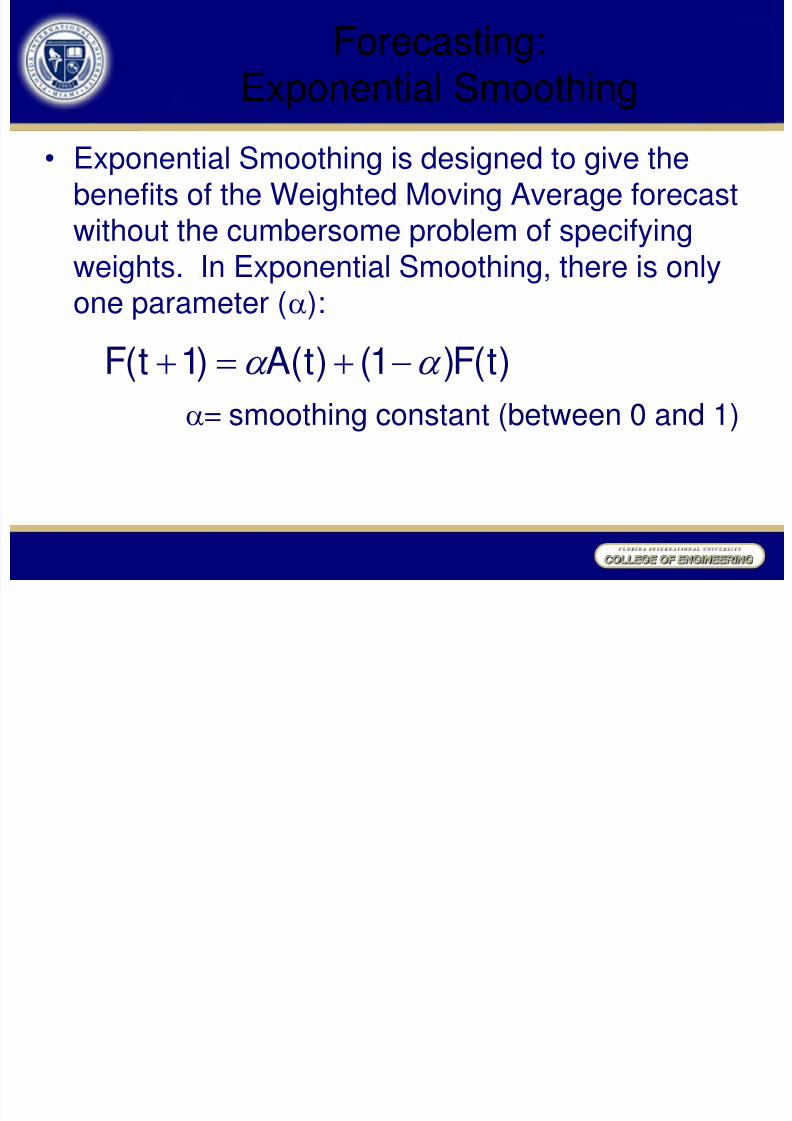

• Exponential Smoothing is designed to give thebenefits of the Weighted Moving Average forecastwithout the cumbersome problem of specifying

weights. In Exponential Smoothing, there is onlyone parameter ():

= smoothing constant (between 0 and 1)

Forecasting:Exponential Smoothing

)t(F)1()t(A)1t(F

8/4/2019 Forecasting 2008

http://slidepdf.com/reader/full/forecasting-2008 17/67

Initialization:•

• )2(F)1()2(A)3(F

)1(A)2(F

Forecasting:Exponential Smoothing

)2(F)1()2(A)3(F

2 / )]2(A)1(A[)2(F

8/4/2019 Forecasting 2008

http://slidepdf.com/reader/full/forecasting-2008 18/67

t A(t) F(t)

1 8

2 5 6.5

3 7 5.9

4 3 6.34

5 6 5

6 9 5.4

7 6.84

8 6.84

9 6.84

10 6.84

Forecasting:Exponential Smoothing

• Using = 0.4,

Initialization

ExPostForecast

Forecast

8/4/2019 Forecasting 2008

http://slidepdf.com/reader/full/forecasting-2008 19/67

Forecasting:Exponential Smoothing

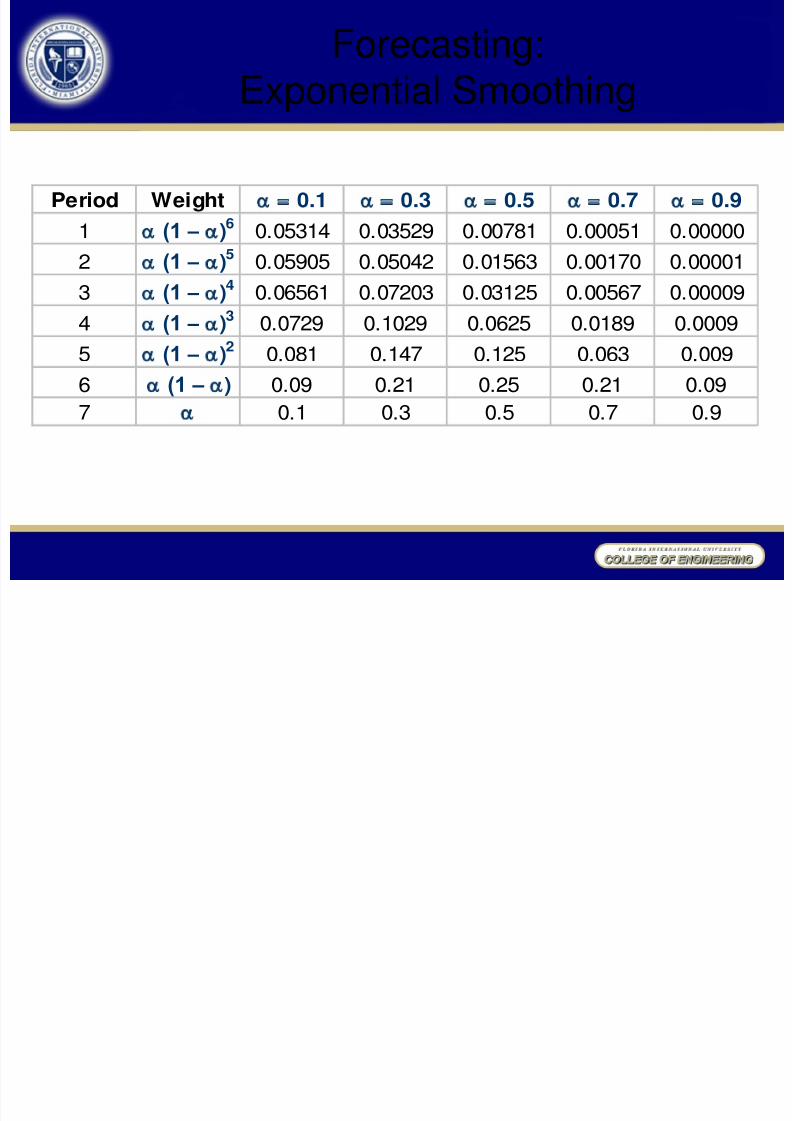

Period Weight 0.1 0.3 0.5 0.7 0.9

1 (1 – )6

0.05314 0.03529 0.00781 0.00051 0.00000

2 (1 – )5

0.05905 0.05042 0.01563 0.00170 0.00001

3 (1 – )4 0.06561 0.07203 0.03125 0.00567 0.00009

4 (1 – )3 0.0729 0.1029 0.0625 0.0189 0.0009

5 (1 – )2

0.081 0.147 0.125 0.063 0.009

6 (1 – ) 0.09 0.21 0.25 0.21 0.09

7 0.1 0.3 0.5 0.7 0.9

8/4/2019 Forecasting 2008

http://slidepdf.com/reader/full/forecasting-2008 20/67

Forecasting:Exponential Smoothing

0 0.1 0.2 0.3 0.4 0.5 0.6 0.7 0.8 0.9

1

1 2 3 4 5 6 7 Period

W e i g h t

= 0.1 = 0.3 = 0.5 = 0.7 = 0.9

8/4/2019 Forecasting 2008

http://slidepdf.com/reader/full/forecasting-2008 21/67

Outliers (eloping point)

Exp Exp

t A(t) = 0.3 = 0.7

1 8

2 5 6.50 6.50

3 6 6.05 5.454 3 6.04 5.84

5 4 5.12 3.85

6 15 4.79 3.96

7 7.85 11.69

8 7.85 11.699 7.85 11.69

10 7.85 11.69

0

2

4

6

8

10

12

14

16

1 2 3 4 5 6 7 8 9 10

Outlier

8/4/2019 Forecasting 2008

http://slidepdf.com/reader/full/forecasting-2008 22/67

Data with Trends

01

2

3

4

5

67

8

9

10

0 1 2 3 4 5 6 7

8/4/2019 Forecasting 2008

http://slidepdf.com/reader/full/forecasting-2008 23/67

0 1 2

3 4 5 6 7 8 9

10

1 2 3 4 5 6 7

A(t)

Data with Trends

= 0.3 = 0.5 = 0.7 = 0.9

8/4/2019 Forecasting 2008

http://slidepdf.com/reader/full/forecasting-2008 24/67

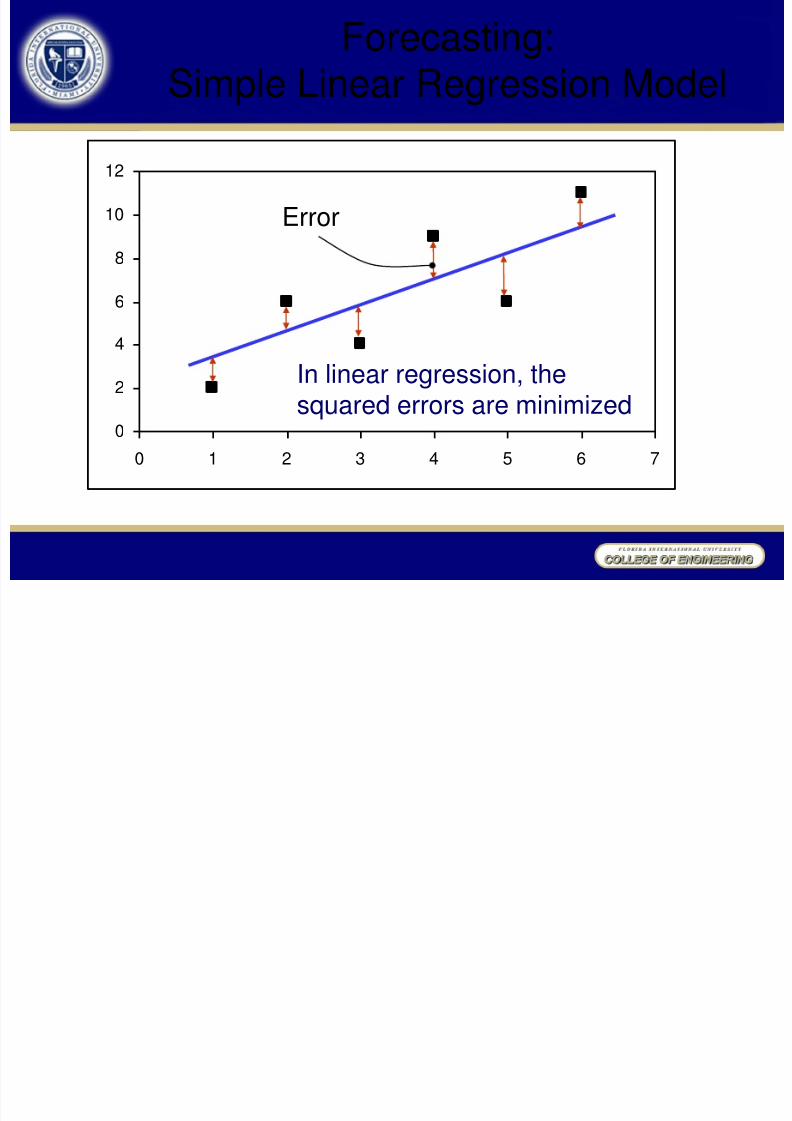

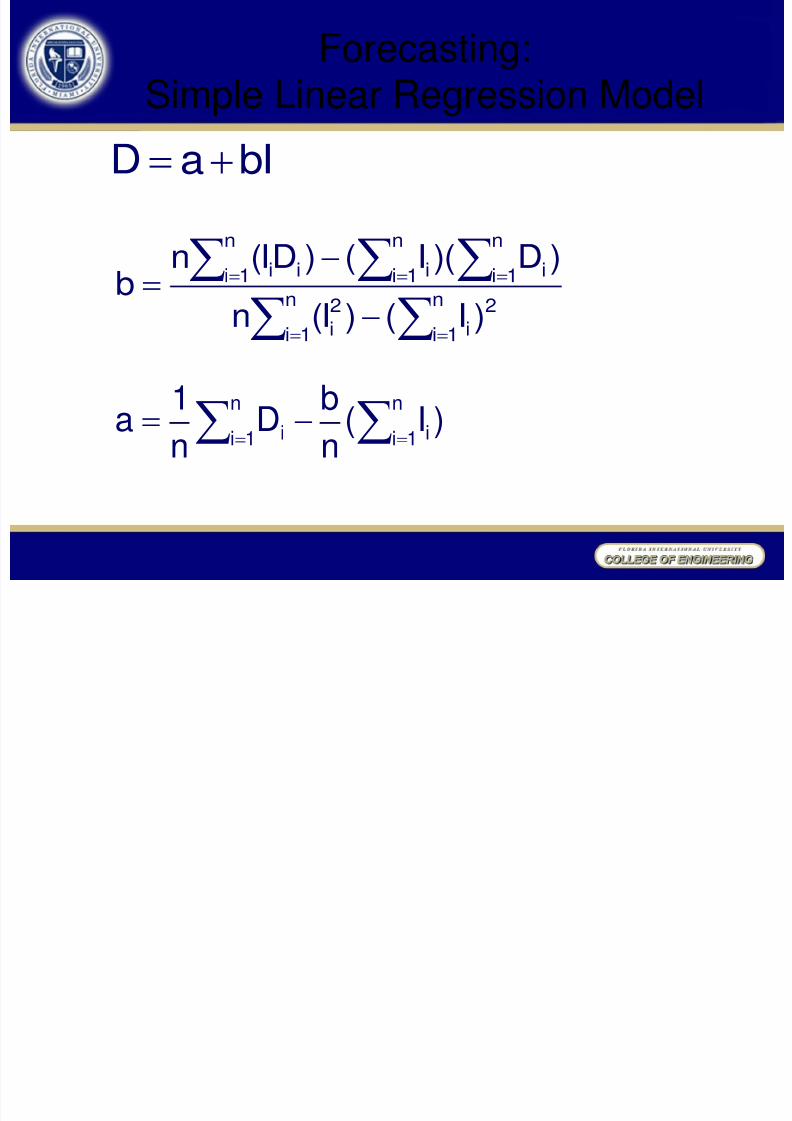

Forecasting:Simple Linear Regression Model

Simple linear regressioncan be used to forecastdata with trends

D is the regressed forecast value or dependentvariable in the model, a is the intercept value of theregression line, and b is the slope of the regressionline.

a

bIaD

D

0 1 2 3 4 5 I

b

8/4/2019 Forecasting 2008

http://slidepdf.com/reader/full/forecasting-2008 25/67

0

2

4

6

8

10

12

0 1 2 3 4 5 6 7

Forecasting:Simple Linear Regression Model

In linear regression, the

squared errors are minimized

Error

8/4/2019 Forecasting 2008

http://slidepdf.com/reader/full/forecasting-2008 26/67

Forecasting:Simple Linear Regression Model

n

1i

n

1i

2

i

2

i

n

1i

n

1i

n

1i iiii

)I()I(n

)D)(I()DI(nb

bIaD

n

1in

1i ii )I(nbD

n1a

8/4/2019 Forecasting 2008

http://slidepdf.com/reader/full/forecasting-2008 27/67

0 50

100 150 200 250

0 2 4 6 8 10 12 14 16

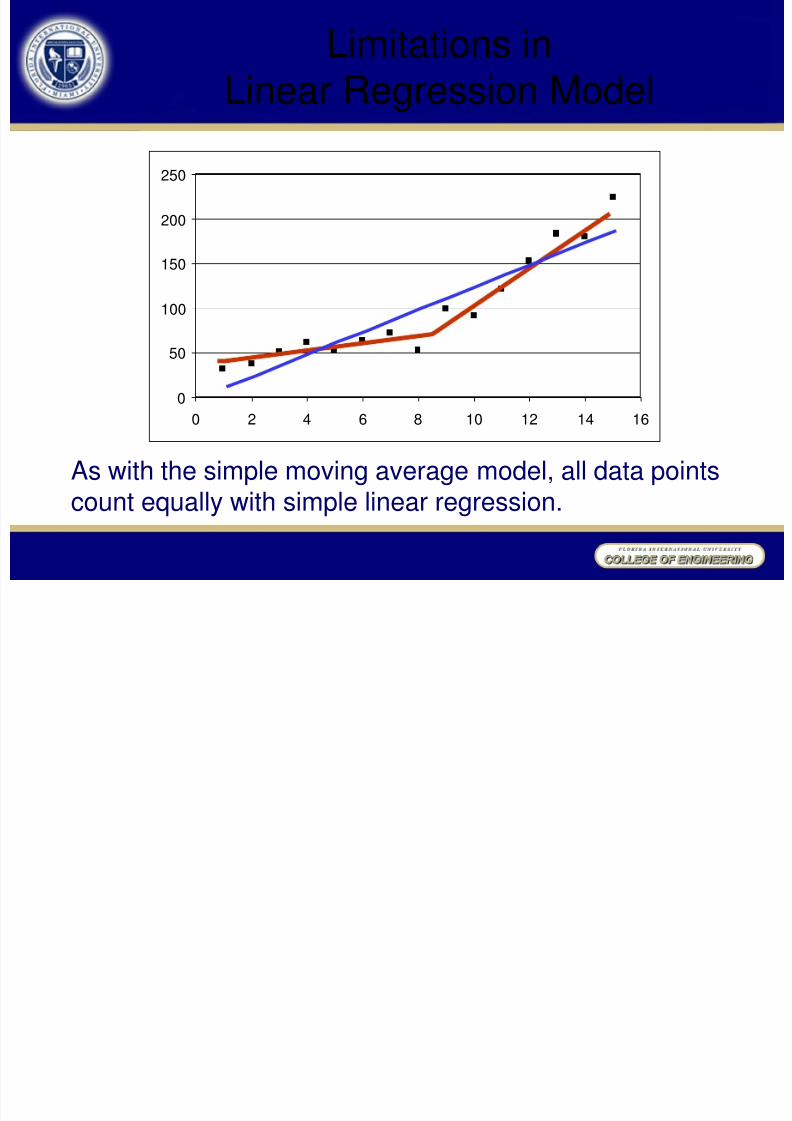

Limitations inLinear Regression Model

As with the simple moving average model, all data pointscount equally with simple linear regression.

8/4/2019 Forecasting 2008

http://slidepdf.com/reader/full/forecasting-2008 28/67

Forecasting:Holt‘s Trend Model

• To forecast data with trends, we can usean exponential smoothing model withtrend, frequently known as Holt‘s model:

L(t) = A(t) + (1- ) F(t) T(t) = [L(t) - L(t-1) ] + (1- ) T(t-1)

F(t+1) = L(t) + T(t)• We could use linear regression to initialize

the model

8/4/2019 Forecasting 2008

http://slidepdf.com/reader/full/forecasting-2008 29/67

Holt‘s Trend Model: Initialization

t A(t)

1 32

2 38

3 50

4 61

5 526 63

7 72

8 53

9 99

10 92

11 12112 153

13 183

14 179

15 224

First, we‘ll initialize the model: x y x2 xy

1 32 1 32

2 38 4 76

3 50 9 150

4 61 16 244Sum 30 502

Average 2.5 45.25

5.20)(9.9)(2.5-45.3=xb-y=a

9.95

5.49

)5.2(430

.5)4(45.25)(2-502=

)xn(-x

)x)(yn(-xy=b

222

L(4) = 20.5+4(9.9)=60.1T(4) = 9.9

8/4/2019 Forecasting 2008

http://slidepdf.com/reader/full/forecasting-2008 30/67

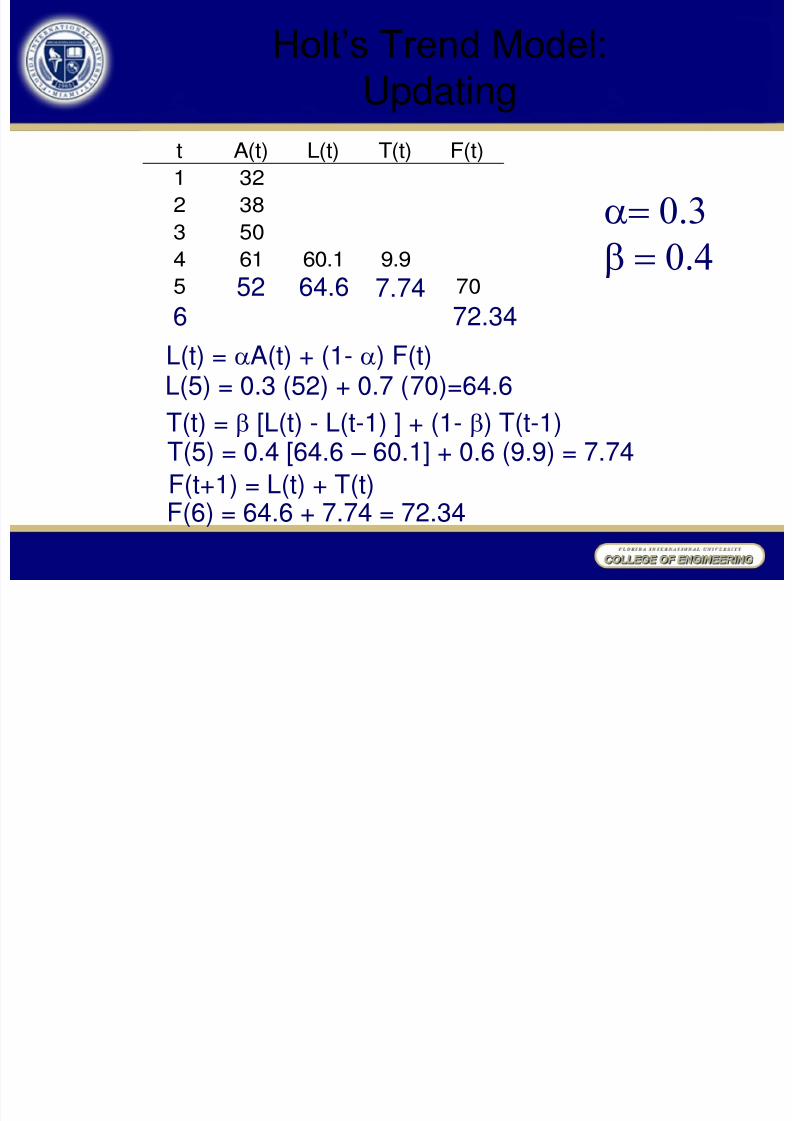

Holt‘s Trend Model: Updating

t A(t) L(t) T(t) F(t)

1 32

2 38

3 50

4 61 60.1 9.9

5 7052

L(t) = A(t) + (1- ) F(t)

0.3

0.4

L(5) = 0.3 (52) + 0.7 (70)=64.6

T(t) = [L(t) - L(t-1) ] + (1- ) T(t-1)T(5) = 0.4 [64.6 – 60.1] + 0.6 (9.9) = 7.74F(t+1) = L(t) + T(t)F(6) = 64.6 + 7.74 = 72.34

64.6 7.7472.346

8/4/2019 Forecasting 2008

http://slidepdf.com/reader/full/forecasting-2008 31/67

t A(t) L(t) T(t) F(t)

1 32

2 38

3 50

4 61 60.1 9.9

5 52 64.60 7.74 70

6 72.34

Holt‘s Trend Model: Updating

63

0.3

0.4

L(6) = 0.3 (63) + 0.7 (72.34)=69.54T(6) = 0.4 [69.54 – 64.60] + 0.6 (7.74) = 6.62

F(7) = 69.54 + 6.62 = 76.16

69.54 6.6276.167 72

8/4/2019 Forecasting 2008

http://slidepdf.com/reader/full/forecasting-2008 32/67

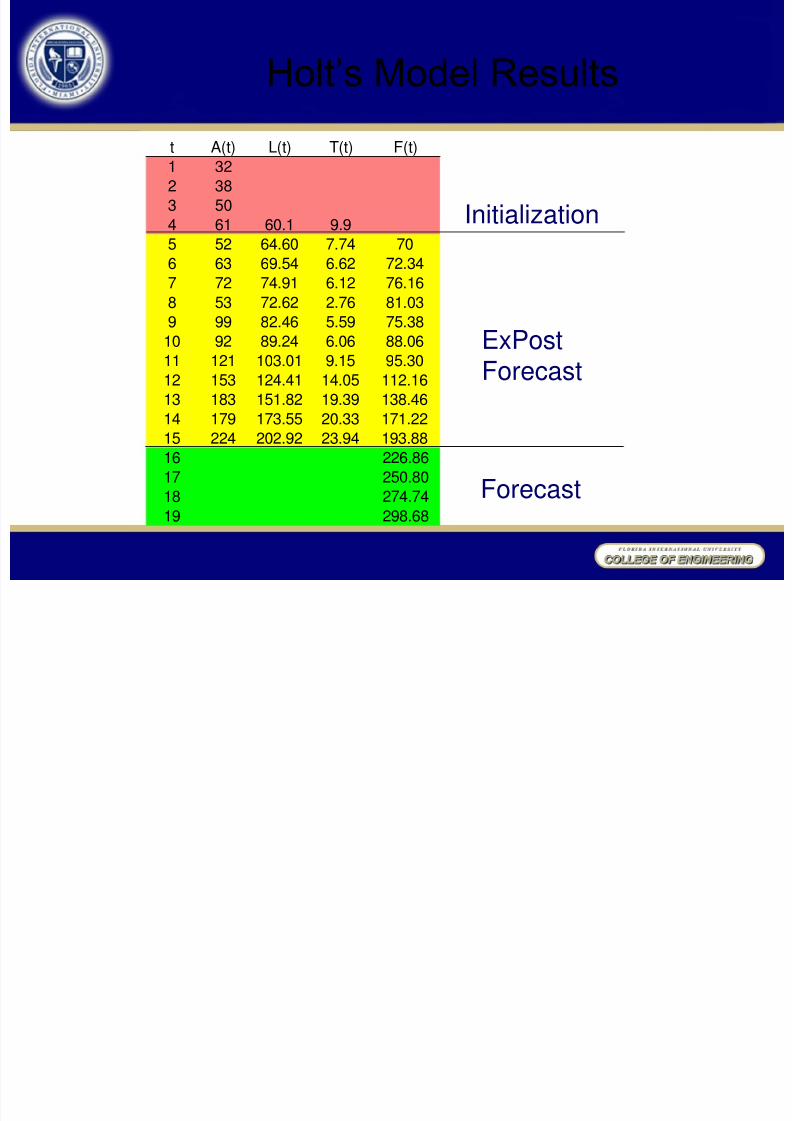

Holt‘s Model Results

t A(t) L(t) T(t) F(t)

1 32

2 38

3 50

4 61 60.1 9.9

5 52 64.60 7.74 70

6 63 69.54 6.62 72.34

7 72 74.91 6.12 76.16

8 53 72.62 2.76 81.03

9 99 82.46 5.59 75.38

10 92 89.24 6.06 88.06

11 121 103.01 9.15 95.30

12 153 124.41 14.05 112.16

13 183 151.82 19.39 138.46

14 179 173.55 20.33 171.22

15 224 202.92 23.94 193.88

16 226.86

17 250.80

18 274.74

19 298.68

Initialization

ExPostForecast

Forecast

8/4/2019 Forecasting 2008

http://slidepdf.com/reader/full/forecasting-2008 33/67

Regression

0 50

100 150 200 250 300 350

0 5 10 15 20

Initialization ExPost Forecast Forecast

Holt‘s Model Results

8/4/2019 Forecasting 2008

http://slidepdf.com/reader/full/forecasting-2008 34/67

Forecasting: Seasonal Model (No Trend)

0

5

10

15

20

25

30

35

40

45

50

S p r i n g 2

0 0 3

S u m m

e r 2 0

0 3

F a l l 2

0 0 3

W i n t

e r 2 0 0 3

S p r i n g 2

0 0 4

S u m m

e r 2 0

0 4

F a l l 2

0 0 4

W i n t

e r 2 0 0 4

S p r i n g 2

0 0 5

S u m m

e r 2 0

0 5

F a l l 2

0 0 5

W i n t

e r 2 0 0 5

A(t)

2003 Spring 16

Summer 27

Fall 39Winter 22

2004 Spring 16

Summer 26

Fall 43

Winter 23

2005 Spring 14Summer 29

Fall 41

Winter 22

8/4/2019 Forecasting 2008

http://slidepdf.com/reader/full/forecasting-2008 35/67

L(t) = A(t) / S(t-p) + (1- ) L(t-1)

S(t) = g [A(t) / L(t)] + (1- g) S(t-p)

Seasonal Model Formulas

p is the number of periods in a season

Quarterly data: p = 4Monthly data: p = 12

F(t+1) = L(t) * S(t+1-p)

8/4/2019 Forecasting 2008

http://slidepdf.com/reader/full/forecasting-2008 36/67

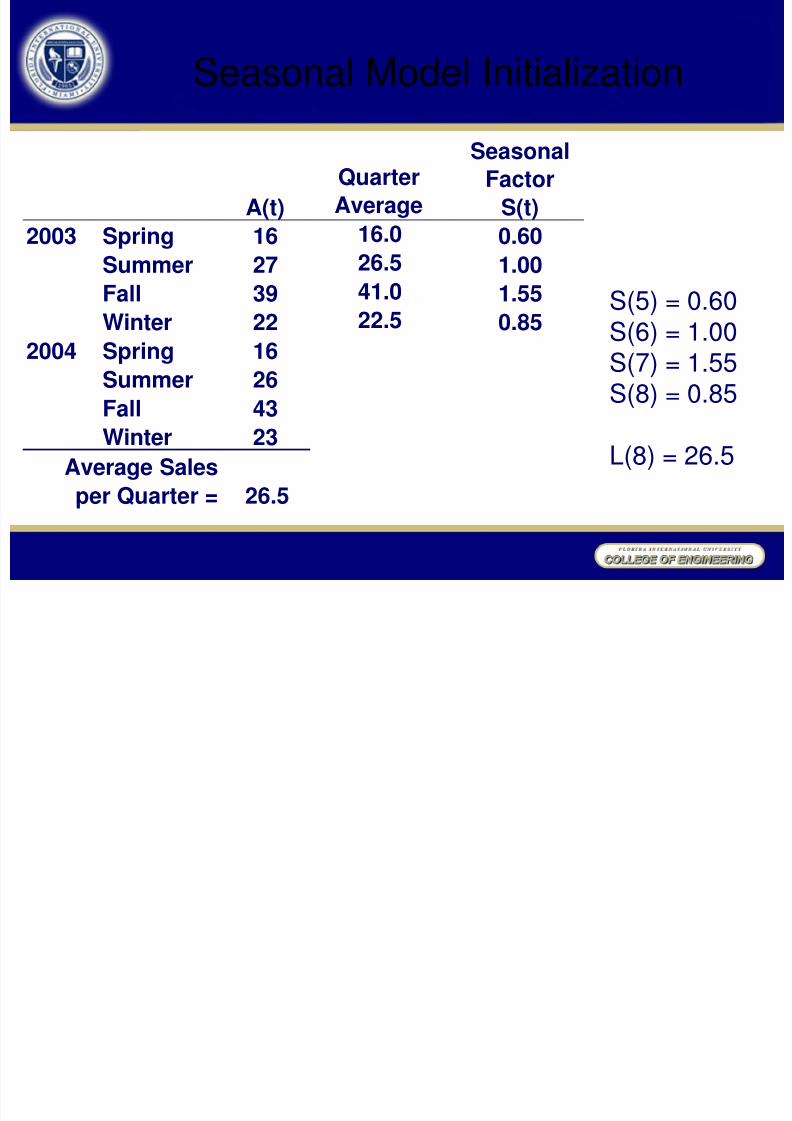

Seasonal Model Initialization

S(5) = 0.60S(6) = 1.00S(7) = 1.55S(8) = 0.85

L(8) = 26.5

Quarter Average

16.0 26.5 41.0 22.5

Seasonal Factor

S(t) 0.60 1.00

1.55 0.85

Average Sales per Quarter = 26.5

A(t) 2003 Spring 16

Summer

27

Fall 39 Winter 22

2004 Spring 16 Summer 26 Fall 43 Winter 23

8/4/2019 Forecasting 2008

http://slidepdf.com/reader/full/forecasting-2008 37/67

Seasonal Model Forecasting

g 0.3

0.4

26.71 1.03 25.18 26.62 1.55 41.32 25.18 0.59 16.00 2005 Spring 14

Summer 29 Fall 41 Winter 22 26.34 0.84 22.60 2006 Spring Summer Fall Winter

15.53 27.02 40.69 22.25

A(t) L(t) Seasonal

Factor S(t) F(t)

2004 Spring 16 0.60 Summer 26 1.00 Fall 43 1.55 Winter 23 26.50 0.85

8/4/2019 Forecasting 2008

http://slidepdf.com/reader/full/forecasting-2008 38/67

0 5

10 15 20 25 30 35 40 45 50

0 2 4 6 8 10 12 14 16

Seasonal Model Forecasting

8/4/2019 Forecasting 2008

http://slidepdf.com/reader/full/forecasting-2008 39/67

Forecasting: Winter‘s Model for Data

with Trend and Seasonal Components

L(t) = A(t) / S(t-p) + (1- )[L(t-1)+T(t-1)]

T(t) = [L(t) - L(t-1)] + (1- ) T(t-1)

S(t) = g [A(t) / L(t)] + (1- g) S(t-p)

F(t+1) = [L(t) + T(t)] S(t+1-p)

8/4/2019 Forecasting 2008

http://slidepdf.com/reader/full/forecasting-2008 40/67

Seasonal-Trend ModelDecomposition

• To initialize Winter‘s Model, we will use

Decomposition Forecasting, which itselfcan be used to make forecasts.

8/4/2019 Forecasting 2008

http://slidepdf.com/reader/full/forecasting-2008 41/67

41

Decomposition Forecasting

• There are two ways to decompose forecastdata with trend and seasonal components:

– Use regression to get the trend, use the trendline to get seasonal factors

– Use averaging to get seasonal factors, ―de-seasonalize‖ the data, then use regression to

get the trend.

8/4/2019 Forecasting 2008

http://slidepdf.com/reader/full/forecasting-2008 42/67

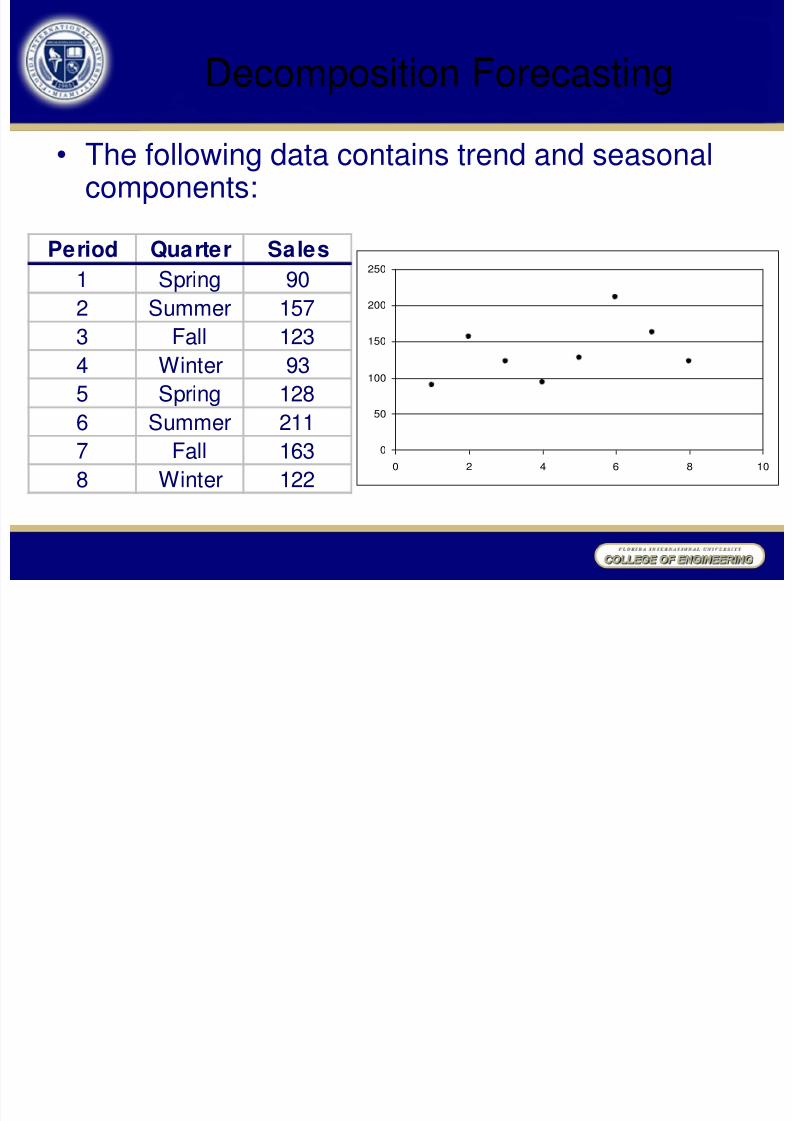

Decomposition Forecasting

• The following data contains trend and seasonalcomponents:

0

50

100

150

200

250

0 2 4 6 8 10

Period Quarter Sales

1 Spring 902 Summer 157

3 Fall 123

4 Winter 93

5 Spring 128

6 Summer 211

7 Fall 163

8 Winter 122

8/4/2019 Forecasting 2008

http://slidepdf.com/reader/full/forecasting-2008 43/67

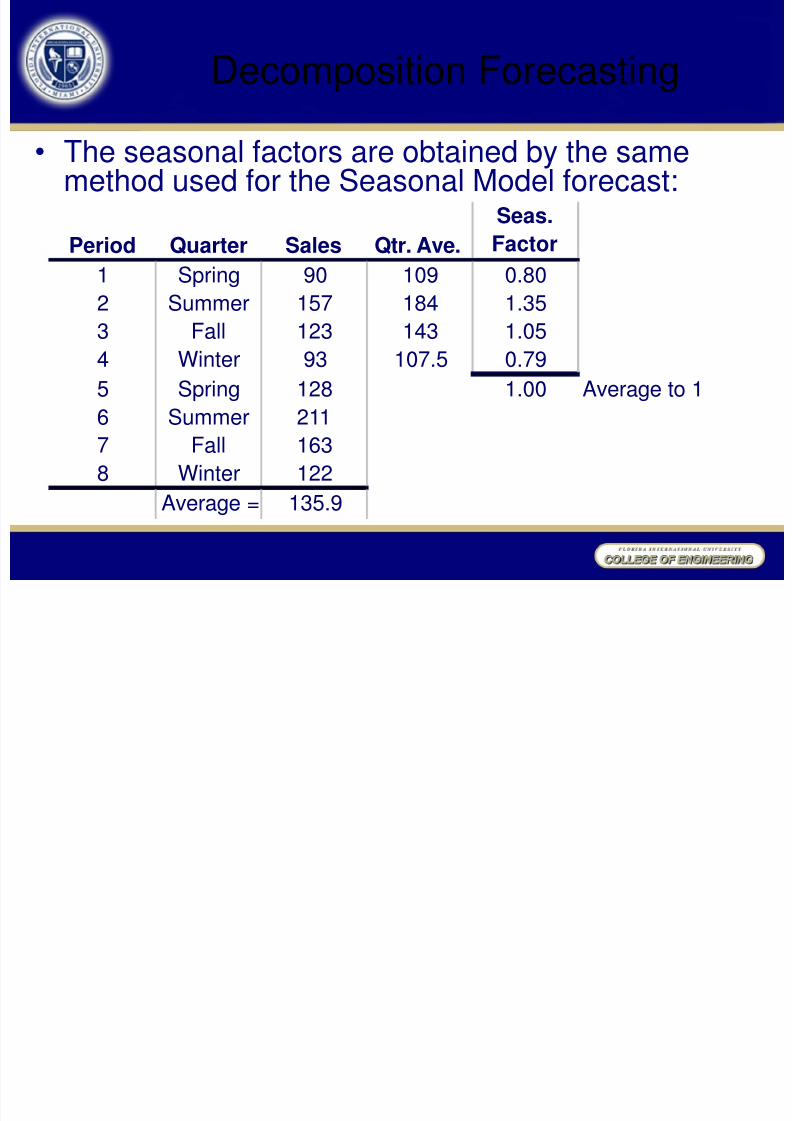

Decomposition Forecasting

• The seasonal factors are obtained by the samemethod used for the Seasonal Model forecast:

Period Quarter Sales 1 Spring 90 2 Summer 157 3 Fall 123 4 Winter 93 5 Spring 128 6 Summer 211 7 Fall 163 8 Winter 122

Average = 135.9

Average to 1

Qtr. Ave. 109 184 143

107.5

Seas.

Factor 0.80 1.35 1.05 0.79 1.00

8/4/2019 Forecasting 2008

http://slidepdf.com/reader/full/forecasting-2008 44/67

Decomposition Forecasting

• With the seasonal factors, the data can be de-seasonalized by dividing the data by the seasonalfactors:

Deseasonalized Data

100.0

110.0

120.0

130.0

140.0

150.0

160.0

170.0

0 2 4 6 8 10

Sales

Seas.

Factor

Deseas.

Data90 0.80 112.2

157 1.35 115.9

123 1.05 116.9

93 0.79 117.5

128 0.80 159.6211 1.35 155.8

163 1.05 154.9

122 0.79 154.2

Regression on the De-seasonalizeddata will give the trend

Decomposition Forecasting

8/4/2019 Forecasting 2008

http://slidepdf.com/reader/full/forecasting-2008 45/67

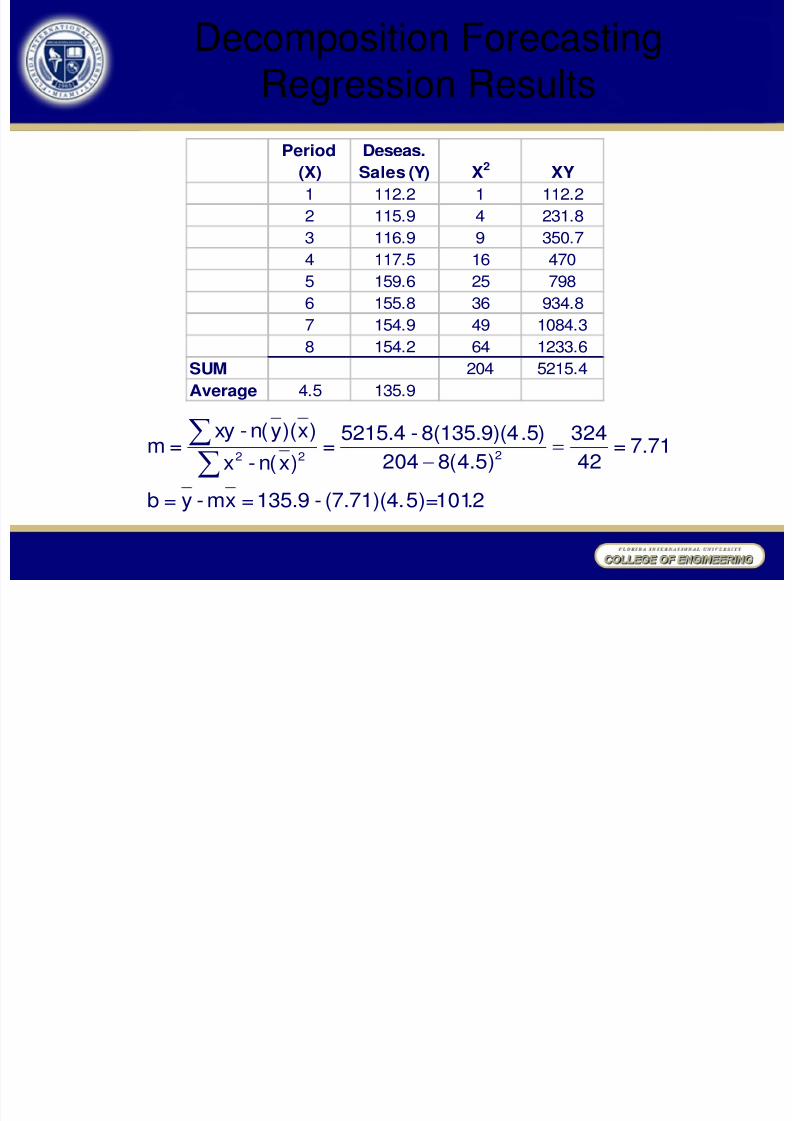

Decomposition ForecastingRegression Results

Period

(X)

Deseas.

Sales (Y) X2 XY

1 112.2 1 112.2

2 115.9 4 231.8

3 116.9 9 350.7

4 117.5 16 470

5 159.6 25 7986 155.8 36 934.8

7 154.9 49 1084.3

8 154.2 64 1233.6

SUM 204 5215.4

Average 4.5 135.9

2.101)=5(7.71)(4.-135.9=xm-y=b

7.71=42

324

)5.4(8204

.5)8(135.9)(4-5215.4=

)xn(-x

)x)(yn(-xy=m

222

8/4/2019 Forecasting 2008

http://slidepdf.com/reader/full/forecasting-2008 46/67

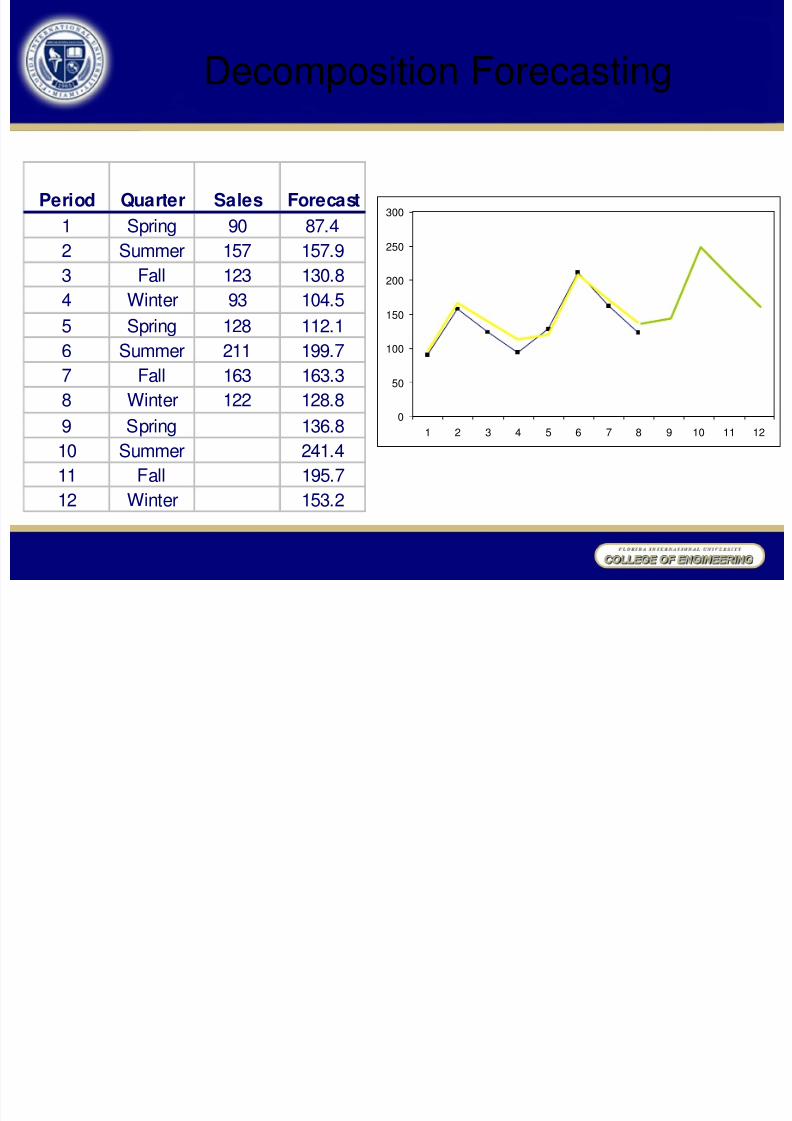

Decomposition Forecast

• Regression on the de-seasonalized dataproduces the following results: – Slope (m) = 7.71 – Intercept (b) = 101.2

• Forecasts can be performed using thefollowing equation – [mx + b](seasonal factor)

8/4/2019 Forecasting 2008

http://slidepdf.com/reader/full/forecasting-2008 47/67

0

50 100 150 200

250 300

1 2 3 4 5 6 7 8 9 10 11 12

Decomposition Forecasting

Period Quarter Sales Forecast

1 Spring 90 87.4

2 Summer 157 157.9

3 Fall 123 130.84 Winter 93 104.5

5 Spring 128 112.1

6 Summer 211 199.7

7 Fall 163 163.3

8 Winter 122 128.8

9 Spring 136.8

10 Summer 241.4

11 Fall 195.7

12 Winter 153.2

8/4/2019 Forecasting 2008

http://slidepdf.com/reader/full/forecasting-2008 48/67

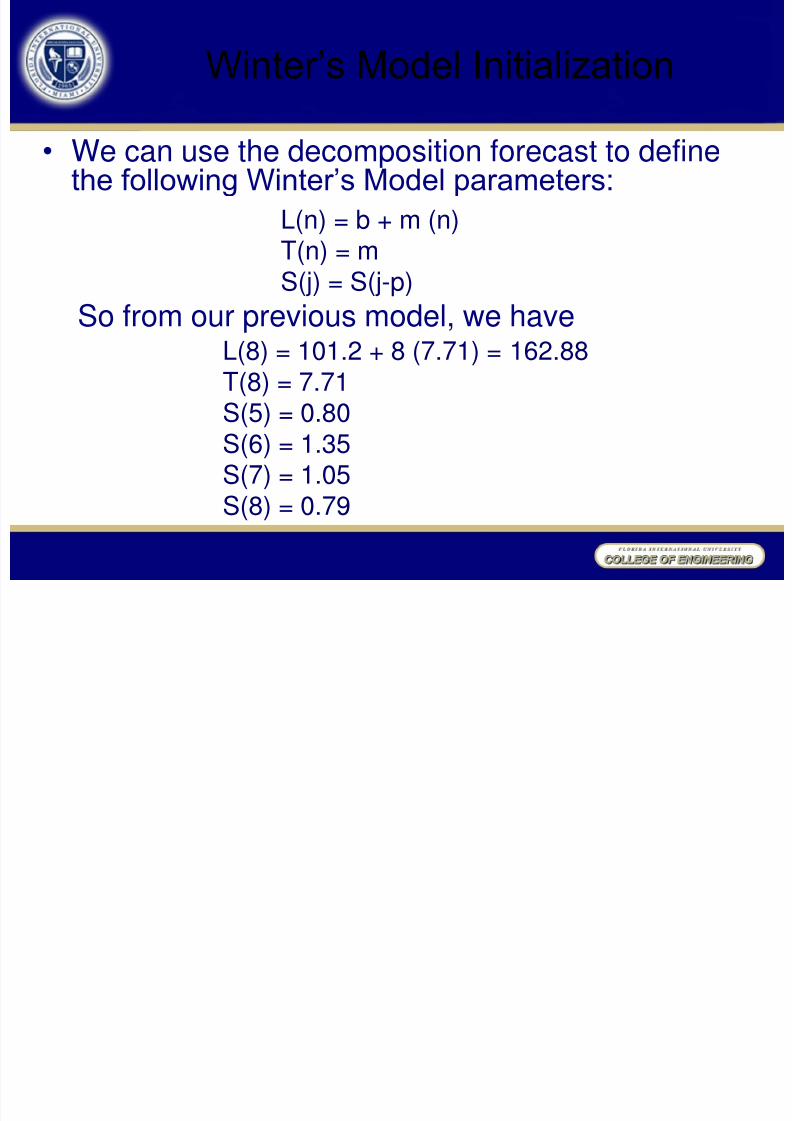

Winter‘s Model Initialization

• We can use the decomposition forecast to definethe following Winter‘s Model parameters:

L(n) = b + m (n)T(n) = m

S(j) = S(j-p)

L(8) = 101.2 + 8 (7.71) = 162.88T(8) = 7.71

S(5) = 0.80S(6) = 1.35S(7) = 1.05S(8) = 0.79

So from our previous model, we have

8/4/2019 Forecasting 2008

http://slidepdf.com/reader/full/forecasting-2008 49/67

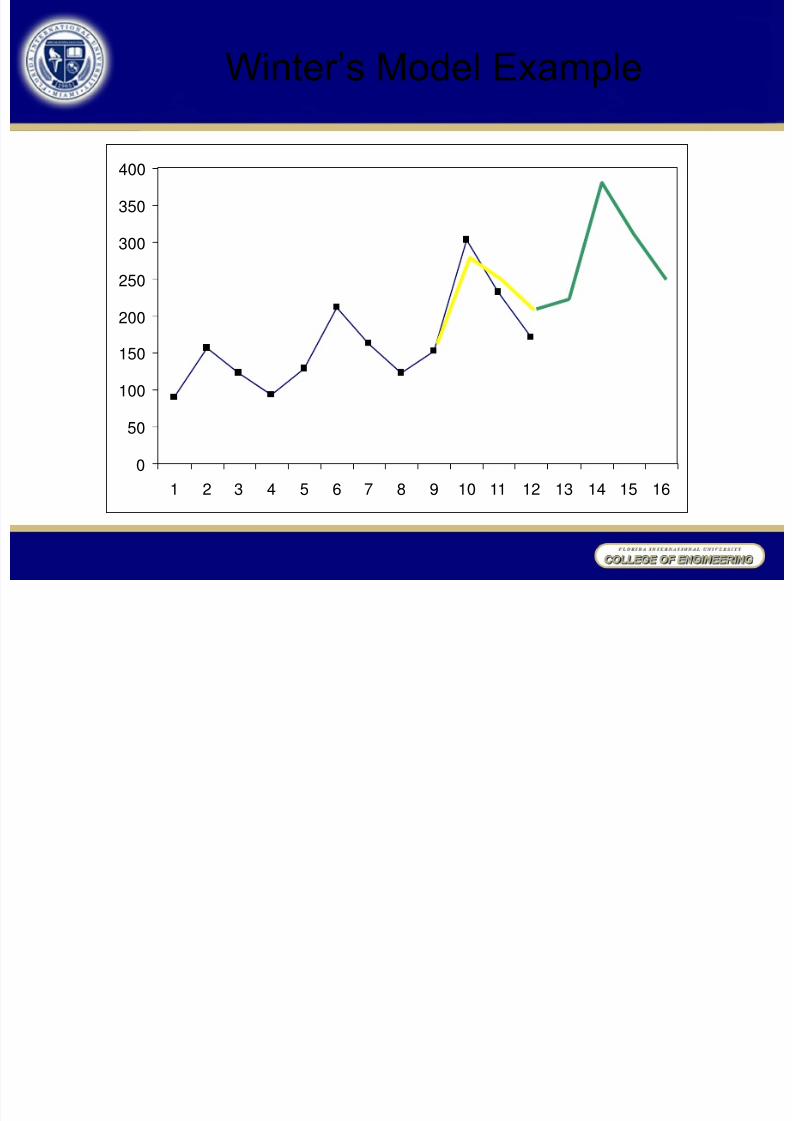

Winter‘s Model Example

176.41 10.04 0.81 136.47 197.85 14.60 1.39 251.71 215.00 15.62 1.06 223.07

9 Spring 152 10 Summer 303 11 Fall 232 12 Winter 171 226.37 13.92 0.78 182.19 13 Spring 14 Summer 15 Fall 16 Winter

195.19 352.41 283.09 220.87

= 0.3 = 0.4 g = 0.2 Period Quarter Sales L(t) T(t) S(t) F(t)

1 Spring 90 2 Summer 157 3 Fall 123 4 Winter 93 5

Spring

128

0.8

6 Summer 211 1.35 7 Fall 162 1.05 8 Winter 122 162.88 7.71 0.79

8/4/2019 Forecasting 2008

http://slidepdf.com/reader/full/forecasting-2008 50/67

0 50

100 150 200 250 300 350 400

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16

Winter‘s Model Example

8/4/2019 Forecasting 2008

http://slidepdf.com/reader/full/forecasting-2008 51/67

Evaluating Forecasts

―Trust, but Verify‖ Ronald W. Reagan

• Computer software gives us the ability to mess up

more data on a greater scale more efficiently• While software like SAP can automatically selectmodels and model parameters for a set of data,and usually does so correctly, when the data is

important, a human should review the modelresults• One of the best tools is the human eye

8/4/2019 Forecasting 2008

http://slidepdf.com/reader/full/forecasting-2008 52/67

0 10 20 30 40 50 60

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15

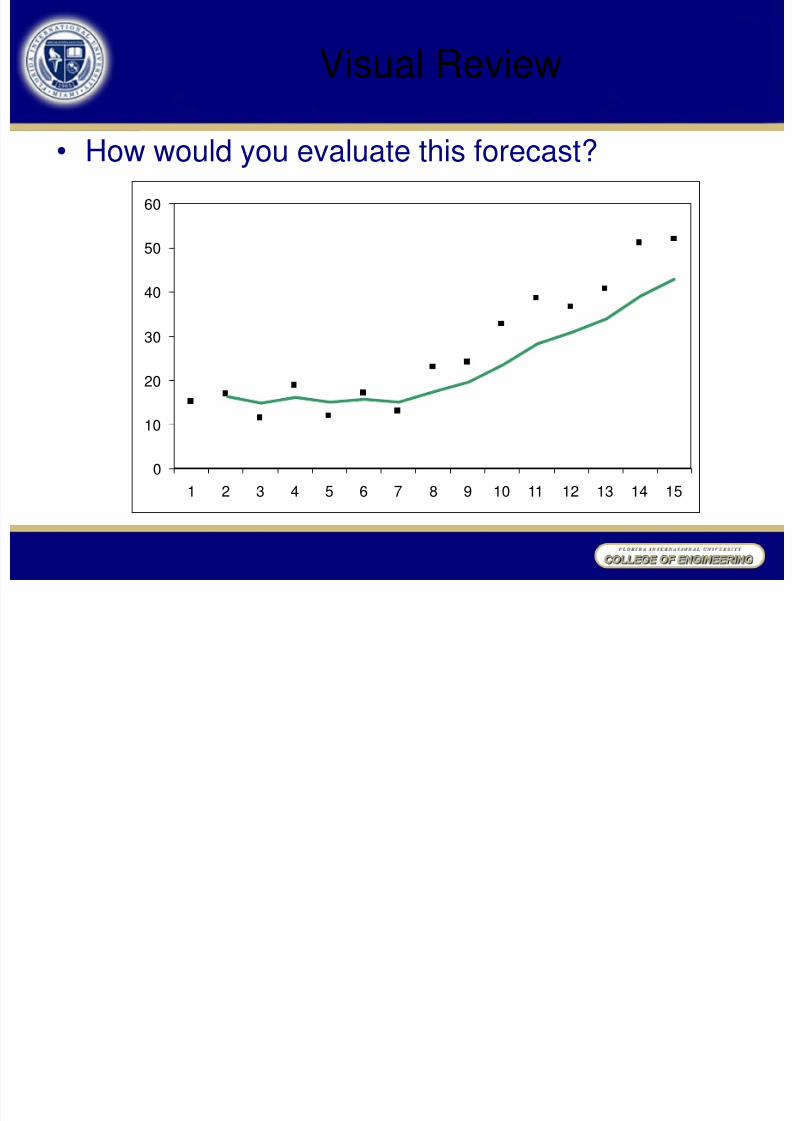

Visual Review

• How would you evaluate this forecast?

8/4/2019 Forecasting 2008

http://slidepdf.com/reader/full/forecasting-2008 53/67

0 50

100 150 200 250 300 350 400

0 10 20 30 40 50

Forecast Evaluation

Initialization ExPostForecast

Forecast

Where Forecast is EvaluatedDo not includeinitialization datain evaluation

8/4/2019 Forecasting 2008

http://slidepdf.com/reader/full/forecasting-2008 54/67

8/4/2019 Forecasting 2008

http://slidepdf.com/reader/full/forecasting-2008 55/67

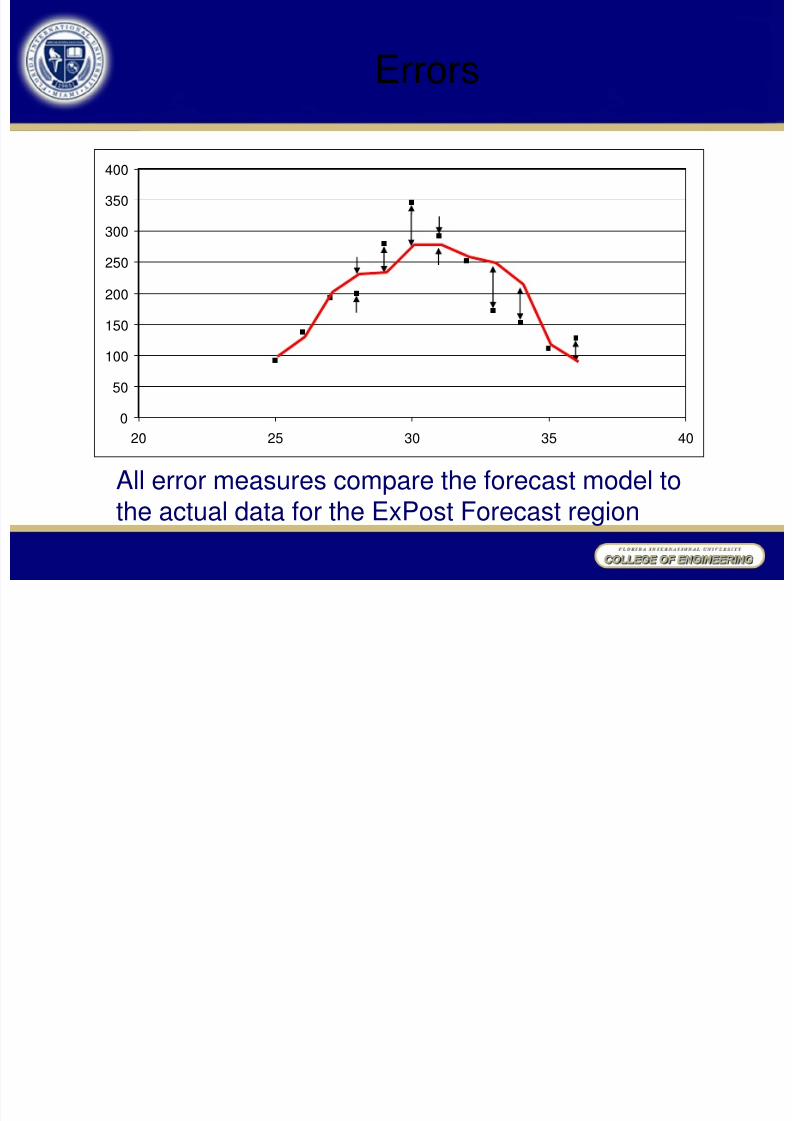

Errors Measure

All error measures are based on the comparison of forecastvalues to actual values in the ExPost Forecast region—do notinclude data from initialization.

t F(t) A(t)Error

F(t) - A(t) | F(t) - A(t) |

25 95 91 4 4

26 125 137 -12 12

27 197 193 4 4

28 227 199 28 28

29 230 278 -48 48

30 274 344 -70 70

31 274 291 -17 17

32 255 250 5 5

33 244 171 73 73

34 211 152 59 59

35 114 111 3 3

36 85 127 -42 42Sum -13 365

8/4/2019 Forecasting 2008

http://slidepdf.com/reader/full/forecasting-2008 56/67

Bias and MAD

t F(t) A(t)Error

F(t) - A(t) | F(t) - A(t) |

25 95 91 4 4

26 125 137 -12 12

35 114 111 3 336 85 127 -42 42

Sum -13 365

08.1

12

13

n

)t( A )t(FBias

42.3012

365

n

)t( A )t(FMAD

8/4/2019 Forecasting 2008

http://slidepdf.com/reader/full/forecasting-2008 57/67

• Bias tells us whether we have a tendency to over-or under-forecast. If our forecasts are ―in themiddle‖ of the data, then the errors should beequally positive and negative, and should sum to 0.

• MAD (Mean Absolute Deviation) is the averageerror, ignoring whether the error is positive ornegative.

• Errors are bad, and the closer to zero an error is,

the better the forecast is likely to be.• Error measures tell how well the method worked inthe ExPost forecast region. How well the forecastwill work in the future is uncertain.

Bias and MAD

8/4/2019 Forecasting 2008

http://slidepdf.com/reader/full/forecasting-2008 58/67

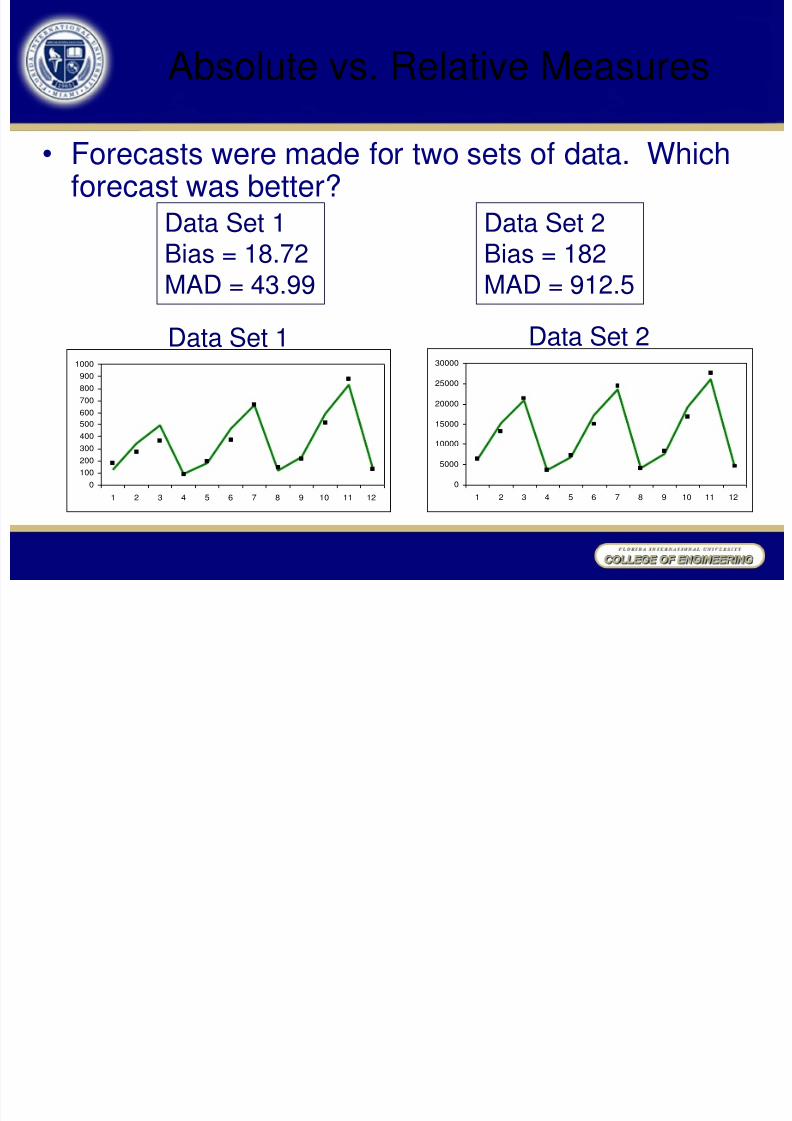

Absolute vs. Relative Measures

• Forecasts were made for two sets of data. Whichforecast was better?

Data Set 1Bias = 18.72

MAD = 43.99

Data Set 2Bias = 182

MAD = 912.5

0

100

200

300

400

500

600

700

800

900

1000

1 2 3 4 5 6 7 8 9 10 11 12

Data Set 1 Data Set 2

0

5000

10000

15000

20000

25000

30000

1 2 3 4 5 6 7 8 9 10 11 12

8/4/2019 Forecasting 2008

http://slidepdf.com/reader/full/forecasting-2008 59/67

MPE and MAPE

• When the numbers in a data set are larger inmagnitude, then the error measures are likely tobe large as well, even though the fit might not be

as ―good‖. • Mean Percentage Error (MPE) and MeanAbsolute Percentage Error (MAPE) are relativeforms of the Bias and MAD, respectively.

• MPE and MAPE can be used to compareforecasts for different sets of data.

8/4/2019 Forecasting 2008

http://slidepdf.com/reader/full/forecasting-2008 60/67

MPE and MAPE

• Mean Percentage Error (MPE)

n

)t( A

)t( A )t(F

MPE

n

)t( A

)t( A )t(F

MAPE

• Mean Absolute Percentage Error (MAPE)

8/4/2019 Forecasting 2008

http://slidepdf.com/reader/full/forecasting-2008 61/67

MPE and MAPE

Data Set 1

148.012

774.1MAPE

037.012446.0MPE

t A(t) F(t)

F(t) - A(t)

A(t)

| F(t) - A(t) |

A(t)

9 177 125.4 -0.292 0.292

10 275 338.85 0.232 0.232

11 363 493.2 0.359 0.35912 91 89.1 -0.021 0.021

13 194 176 -0.093 0.093

14 376 463.05 0.232 0.232

15 659 658.8 0.000 0.000

16 146 116.7 -0.201 0.201

17 219 226.6 0.035 0.03518 514 587.25 0.143 0.143

19 875 824.4 -0.058 0.058

20 130 144.3 0.110 0.110

0.446 1.774

8/4/2019 Forecasting 2008

http://slidepdf.com/reader/full/forecasting-2008 62/67

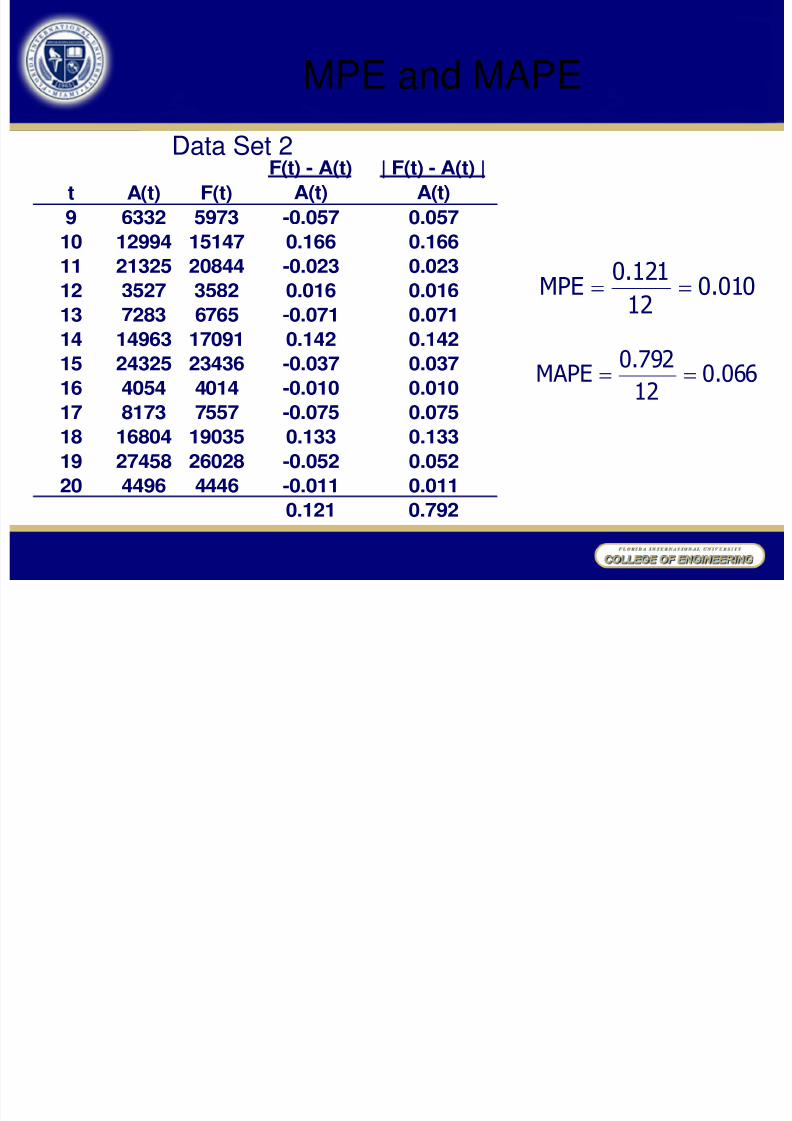

MPE and MAPE

Data Set 2

066.012

792.0MAPE

010.012121.0MPE

t A(t) F(t)

F(t) - A(t)

A(t)

| F(t) - A(t) |

A(t)

9 6332 5973 -0.057 0.057

10 12994 15147 0.166 0.166

11 21325 20844 -0.023 0.023

12 3527 3582 0.016 0.016

13 7283 6765 -0.071 0.071

14 14963 17091 0.142 0.142

15 24325 23436 -0.037 0.037

16 4054 4014 -0.010 0.010

17 8173 7557 -0.075 0.07518 16804 19035 0.133 0.133

19 27458 26028 -0.052 0.052

20 4496 4446 -0.011 0.011

0.121 0.792

8/4/2019 Forecasting 2008

http://slidepdf.com/reader/full/forecasting-2008 63/67

MPE and MAPE

Data Set 2

066.012

792.0MAPE

010.012

121.0MPE

148.012774.1MAPE

037.012

446.0MPE

Data Set 1

0

100

200

300

400500

600

700

800

900

1000

1 2 3 4 5 6 7 8 9 10 11 12

0

5000

10000

15000

20000

25000

30000

1 2 3 4 5 6 7 8 9 10 11 12

8/4/2019 Forecasting 2008

http://slidepdf.com/reader/full/forecasting-2008 64/67

0 10 20 30 40 50 60

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15

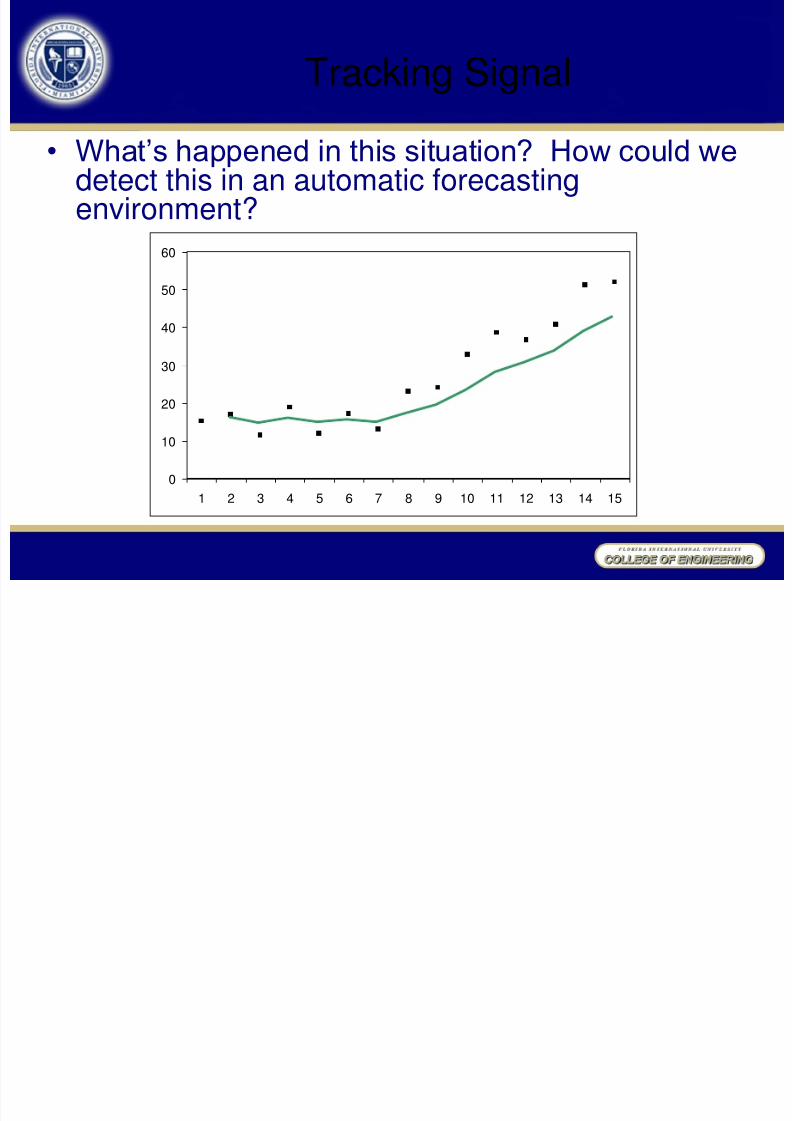

Tracking Signal

• What‘s happened in this situation? How could wedetect this in an automatic forecastingenvironment?

8/4/2019 Forecasting 2008

http://slidepdf.com/reader/full/forecasting-2008 65/67

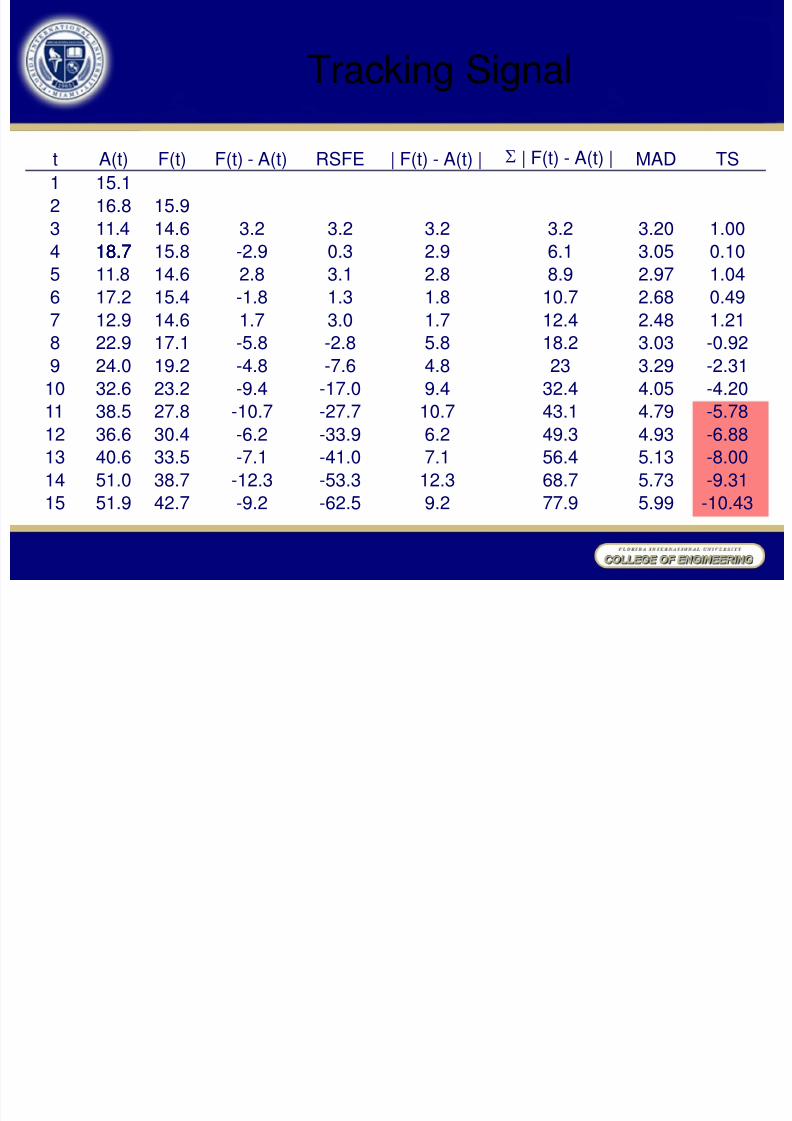

Tracking Signal

• The tracking signal can be calculated after each actualsales value is recorded. The tracking signal iscalculated as:

n

)t( A )t(F

)t( A )t(F

)t(MAD

RSFE)t(TS

• The tracking signal is a relative measure, like MPE

and MAPE, so it can be compared to a set value(typically 4 or 5) to identify when forecastingparameters and/or models need to be changed.

8/4/2019 Forecasting 2008

http://slidepdf.com/reader/full/forecasting-2008 66/67

Tracking Signal

t A(t) F(t) F(t) - A(t) RSFE | F(t) - A(t) | S | F(t) - A(t) | MAD TS 1 15.1 2 16.8 15.9 3 11.4 14.6 3.2 3.2 3.2 3.2 3.20 1.00 4 18.7 15.8 -2.9 0.3 2.9 6.1 3.05 0.10 5

11.8

14.6

2.8

3.1

2.8

8.9

2.97

1.04

6 17.2 15.4 -1.8 1.3 1.8 10.7 2.68 0.49 7 12.9 14.6 1.7 3.0 1.7 12.4 2.48 1.21 8 22.9 17.1 -5.8 -2.8 5.8 18.2 3.03 -0.92 9 24.0 19.2 -4.8 -7.6 4.8 23 3.29 -2.31

10 32.6 23.2 -9.4 -17.0 9.4 32.4 4.05 -4.20 11

38.5

27.8

-10.7

-27.7

10.7

43.1

4.79

-5.78

12 36.6 30.4 -6.2 -33.9 6.2 49.3 4.93 -6.88 13 40.6 33.5 -7.1 -41.0 7.1 56.4 5.13 -8.00 14 51.0 38.7 -12.3 -53.3 12.3 68.7 5.73 -9.31 15 51.9 42.7 -9.2 -62.5 9.2 77.9 5.99 -10.43

18.7 18.7

8/4/2019 Forecasting 2008

http://slidepdf.com/reader/full/forecasting-2008 67/67

0 10 20 30 40

50 60

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15

Tracking Signal

TS = -5.78