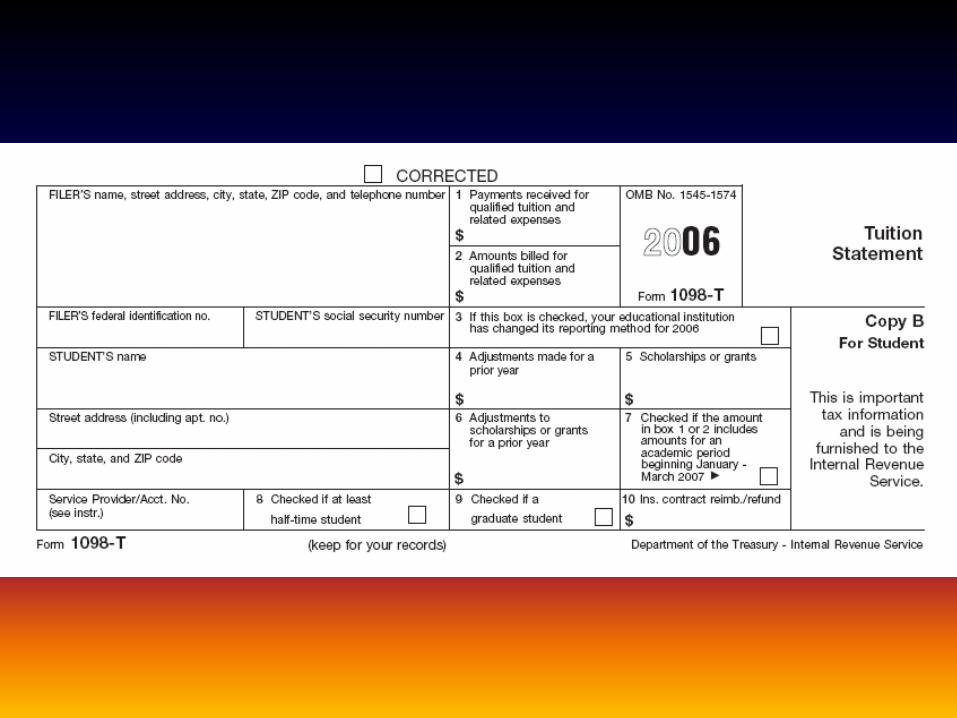

Form 1098-T Tuition Statement

Used for either Education Credit

and Tuition & Fees Adjustment

FL1 ty2006 Training

Form 1098-T

• Issued by eligible educational institution

• Not required

• Course has no academic credit

• Nonresident alien student

• Expenses waived or paid entirely with scholarships or grants

• No separate financial account ad expenses covered by arrangement with employer or governmental entity

Form1098-T

• Choice of reporting amounts received

(block 1) or amounts billed (block 2)

Form 1098-T – Block 1

• Amount of payments received for

qualified tuition and related expenses

from any source during the calendar

year.

Form 1098-T – Block 2

• Amounts billed during calendar year for

qualified tuition and related expenses

Form 1098-T – Block 3

• Indicates if method of reporting

(payments received or amounts billed)

has changed

• Written submission to IRS required

Form 1098-T - Block 4

• Adjustments made for a prior year

• Amounts reimbursed or refunded during

calendar year that relate to payments

received that were reported for any prior

year after 2002

Form 1098-T – Block 5

• Scholarships or Grants

• Amount of scholarships or grants that the

institution administered and processed

during calendar year for student’s cost of

attendance

Form 1098-T – Block 6

• Adjustments to Scholarships or grants

for a Prior Year

• Reduction of the amount of scholarships or

grants reported for any prior year after

2002

Form 1098-T – Block 7

• Checkbox for Amounts for an Academic

Period Beginning in January through

March of 2007

• Payments received or amounts billed for

expenses reported for 2006 that relate to

academic period January – March of 2007

Form 1098-T – Box 8

• Check if at Least Half-Time Student

• Standards established by Department of

Education

Form 1098-T – Block 9

• Check if a Graduate Student

• Enrolled in program leading to graduate-

level degree, graduate-level certificate, or

other recognized graduate-level

educational credential

Form 1098-T – Block 10

• Insurance Contract Reimbursements or

Refunds

• Used if institution is an insurer

• Amounts of reimbursement or refunds

shown

Instructions for Students

• Amount shown in block 1 or 2 may

represent an amount other than the

amount paid in 2006

• Student’s records are primary source to

determine amount of deduction or credit

Instructions for Tax-Aide

Counselors

• Form 1098-T alone cannot be used to

determine amount paid for qualified

tuition and related expenses