1

Fullerton India Credit Company Ltd. Q3’ 18 Update

2

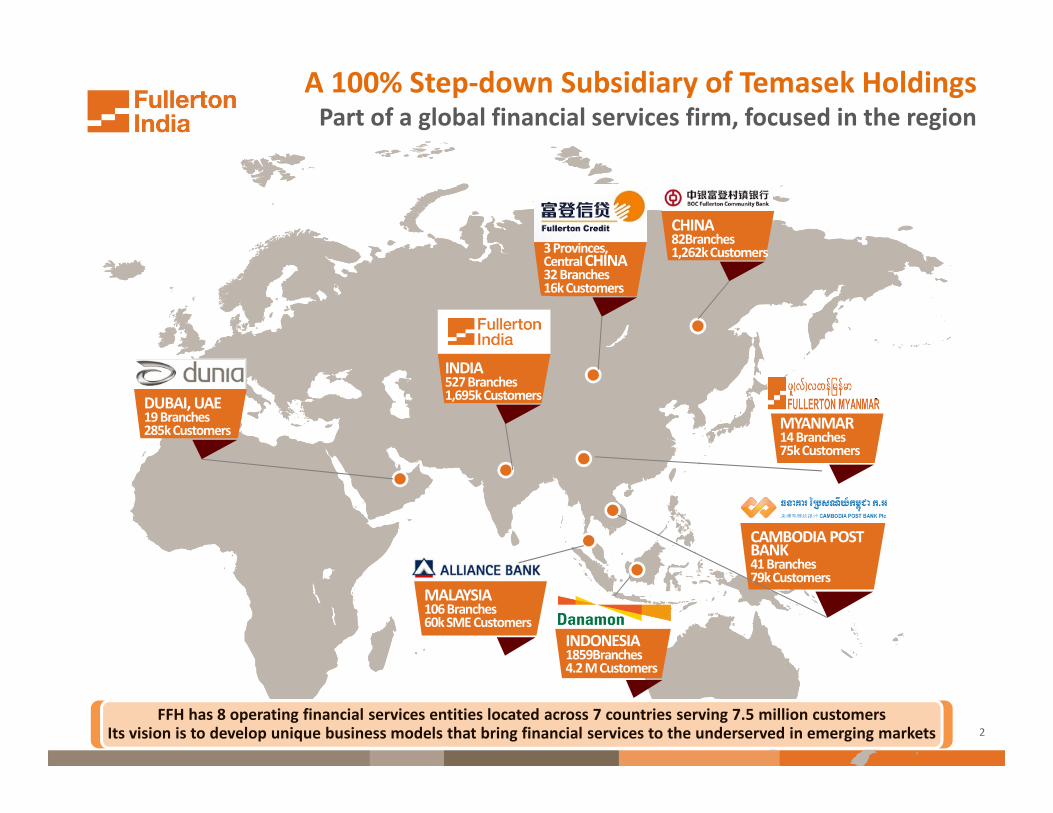

DUBAI, UAE19 Branches285k Customers

INDIA527 Branches1,695k Customers

3 Provinces,Central CHINA32 Branches16k Customers

CHINA82Branches1,262k Customers

MYANMAR14 Branches75k Customers

CAMBODIA POST BANK41 Branches79k Customers

MALAYSIA106 Branches60k SME Customers

INDONESIA1859Branches4.2 M Customers

FFH has 8 operating financial services entities located across 7 countries serving 7.5 million customersIts vision is to develop unique business models that bring financial services to the underserved in emerging markets

A 100% Step-down Subsidiary of Temasek HoldingsPart of a global financial services firm, focused in the region

3

FICCL History – Key milestones

2003FFH, parent entity of

FICCL is incorporated as a

wholly-owned subsidiary of

Temasek Holding (P) Ltd

2007/08Commercial Launch of

NBFC operations.

Pan-India presence

established.

2012/13Capital infused for growth

Rural network expanded.

Funding diversified.

2015Technology – core system

revamped.

Capital Infused for growth.

Home Finance business

launched.

2010Commercial Vehicle

business launched.

Network consolidated.

FICCL is incorporated as

a wholly-owned

subsidiary of FFH

2005

Entry into rural business.

Managed economic

downturn.

2009

Portfolio reshape

and segmental shift to

mass affluent.

LAP, SME business

re-launched.

In-sourcing of critical functions

2011

Accelerated secured

business, rural network

Operations process revamp

2014Digital deployment.

Rural franchise expanded.

Commercial Vehicles

business accelerated.

Branches exceeded 520, AUM

crossed 13,800 cr.

2016/17

FICCL:- Fullerton India Credit Company Limited, FFH:- Fullerton Financial Holding

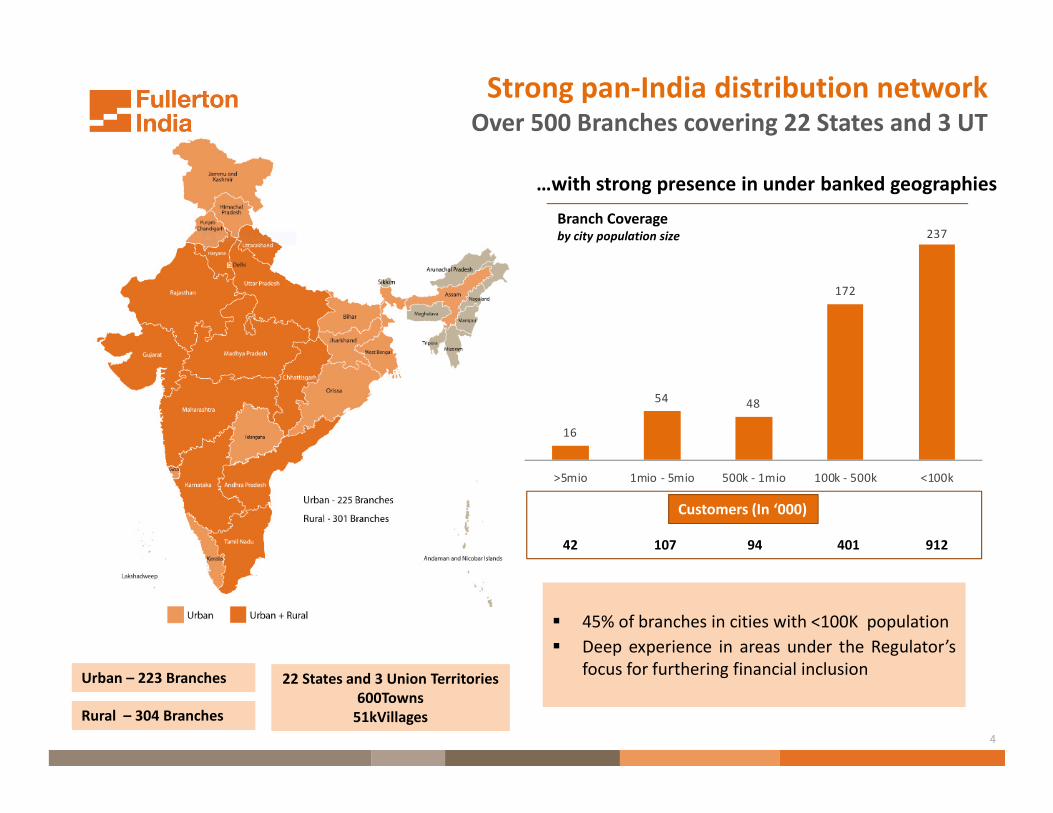

Customers (In ‘000)

40

3

Branch Coverageby city population size

…with strong presence in under banked geographies

� 45% of branches in cities with <100K population

� Deep experience in areas under the Regulator’s

focus for furthering financial inclusion

42 94107 401 912

4

13

2

1

Urban – 223 Branches

Rural – 304 Branches

22 States and 3 Union Territories

600Towns

51kVillages

Strong pan-India distribution networkOver 500 Branches covering 22 States and 3 UT

4

4

188

2

24

23

19

323

36

7

65

50

56

55

66

3

73

16

54 48

172

237

>5mio 1mio - 5mio 500k - 1mio 100k - 500k <100k

5

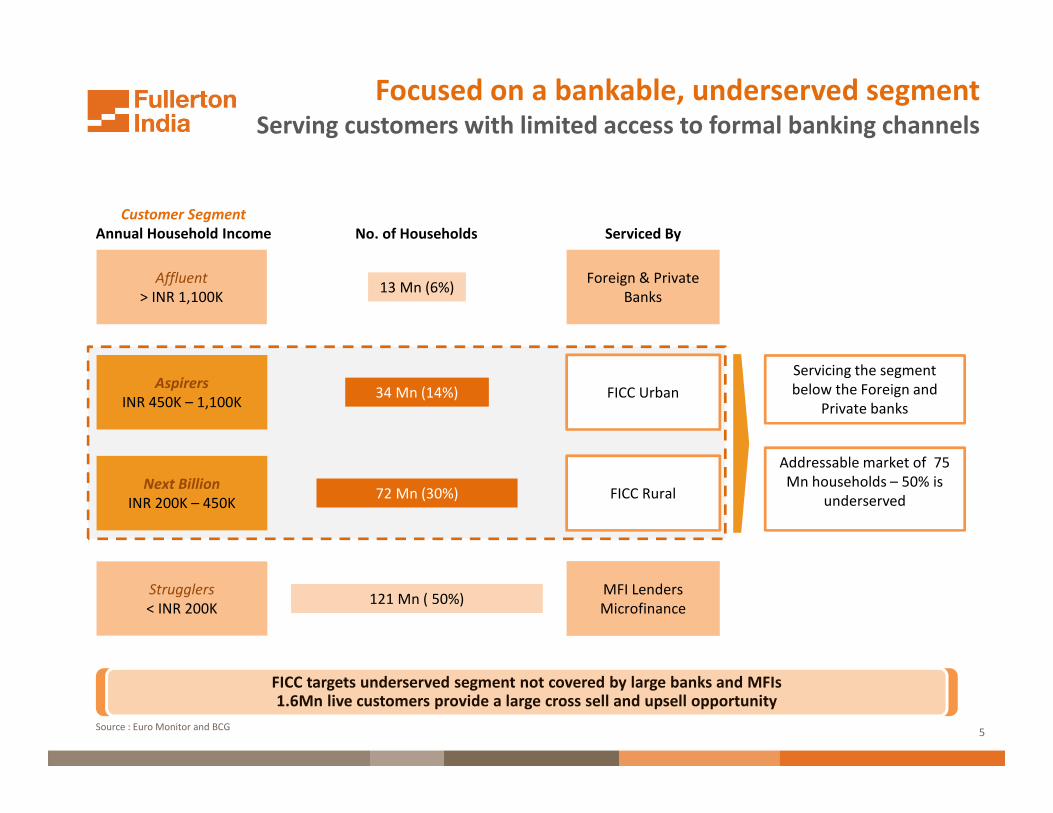

Focused on a bankable, underserved segmentServing customers with limited access to formal banking channels

Customer Segment

Annual Household Income No. of Households Serviced By

Strugglers

< INR 200K121 Mn ( 50%)

MFI Lenders

Microfinance

Affluent

> INR 1,100K13 Mn (6%)

Foreign & Private

Banks

Servicing the segment

below the Foreign and

Private banks

Addressable market of 75

Mn households – 50% is

underservedNext Billion

INR 200K – 450K

Aspirers

INR 450K – 1,100K

72 Mn (30%)

34 Mn (14%)

FICC Rural

FICC Urban

FICC targets underserved segment not covered by large banks and MFIs 1.6Mn live customers provide a large cross sell and upsell opportunity

Source : Euro Monitor and BCG

6

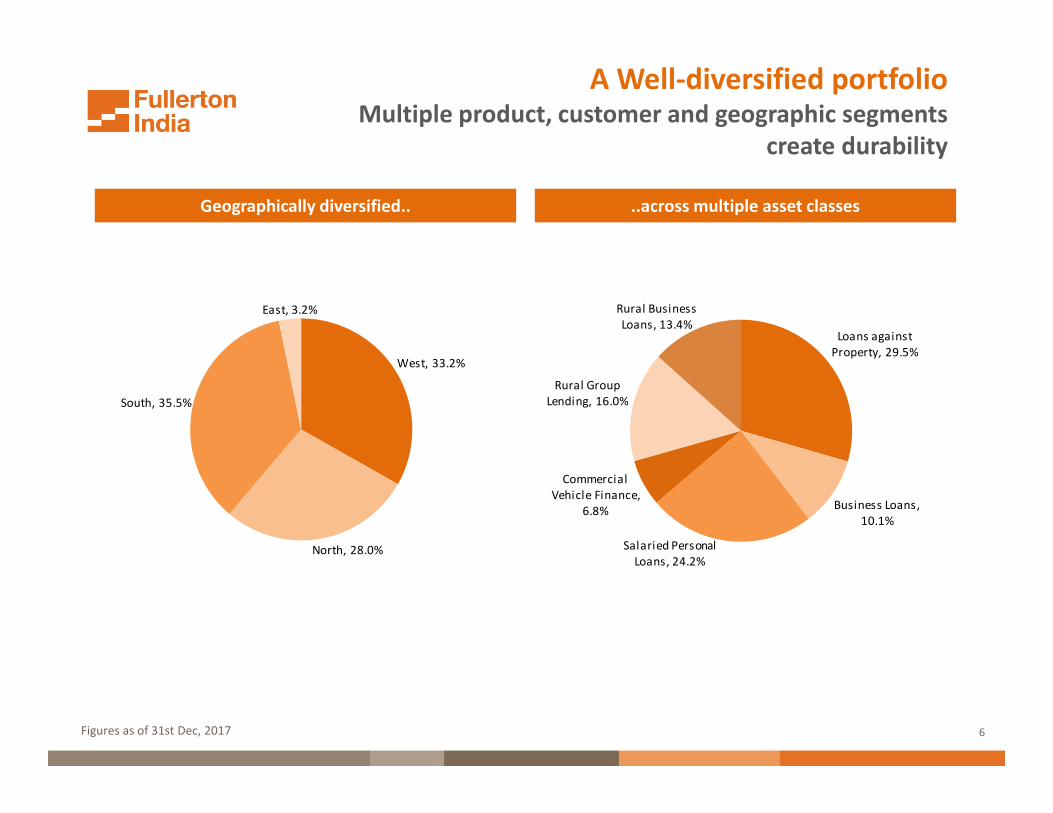

A Well-diversified portfolioMultiple product, customer and geographic segments

create durability

Geographically diversified.. ..across multiple asset classes

Figures as of 31st Dec, 2017

Loans against

Property, 29.5%

Business Loans,

10.1%

Salaried Personal

Loans, 24.2%

Commercial

Vehicle Finance,

6.8%

Rural Group

Lending, 16.0%

Rural Business

Loans, 13.4%

West, 33.2%

North, 28.0%

South, 35.5%

East, 3.2%

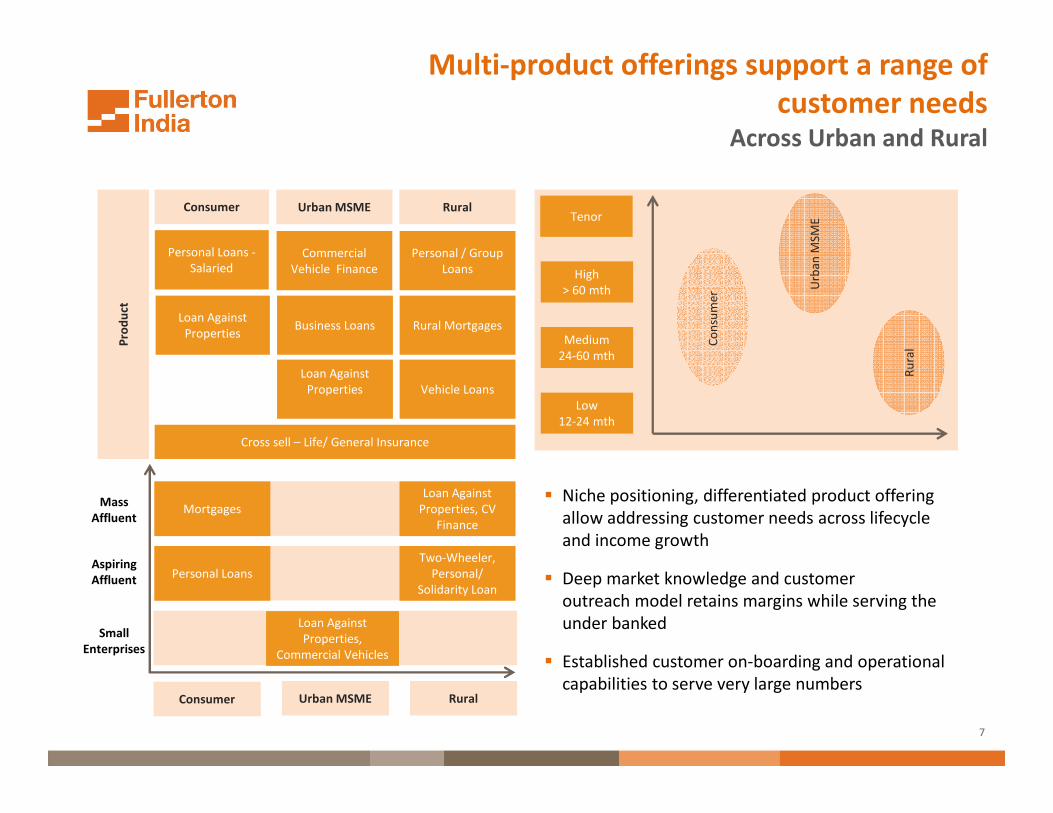

7

Multi-product offerings support a range of

customer needsAcross Urban and Rural

Pro

du

ct

Cross sell – Life/ General Insurance

Commercial

Vehicle Finance

Business Loans

Loan Against

Properties

Urban MSME

Personal / Group

Loans

Rural Mortgages

Vehicle Loans

Rural

Personal Loans -

Salaried

Loan Against

Properties

Consumer

Urban MSME RuralConsumer

Two-Wheeler,

Personal/

Solidarity Loan

Personal Loans

Loan Against

Properties,

Commercial Vehicles

Mortgages

Loan Against

Properties, CV

Finance

Mass

Affluent

Aspiring

Affluent

Small

Enterprises

Urb

an

MS

ME

Ru

ralC

on

sum

er

Tenor

High

> 60 mth

Medium

24-60 mth

Low

12-24 mth

� Niche positioning, differentiated product offering

allow addressing customer needs across lifecycle

and income growth

� Deep market knowledge and customer

outreach model retains margins while serving the

under banked

� Established customer on-boarding and operational

capabilities to serve very large numbers

8

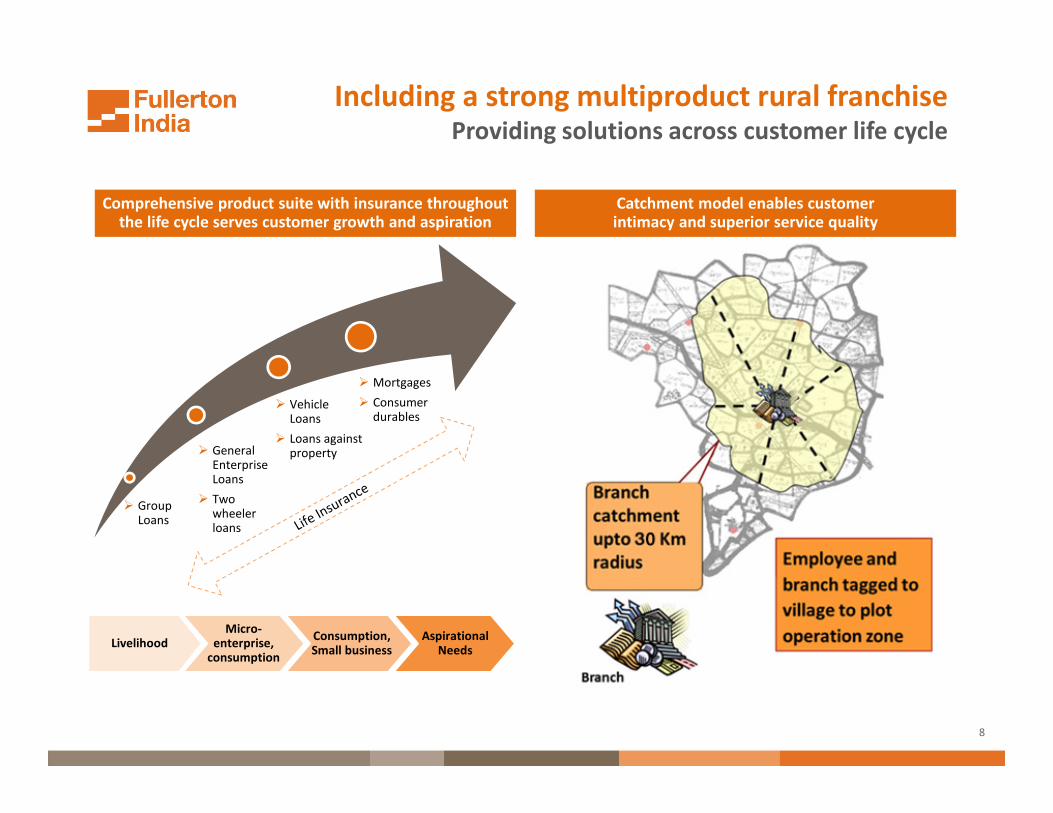

Including a strong multiproduct rural franchiseProviding solutions across customer life cycle

LivelihoodMicro-

enterprise, consumption

Consumption, Small business

Aspirational Needs

Comprehensive product suite with insurance throughout the life cycle serves customer growth and aspiration

Catchment model enables customer intimacy and superior service quality

� Group Loans

� General Enterprise Loans

� Two wheeler loans

� Vehicle Loans

� Loans against property

� Mortgages

� Consumer durables

9

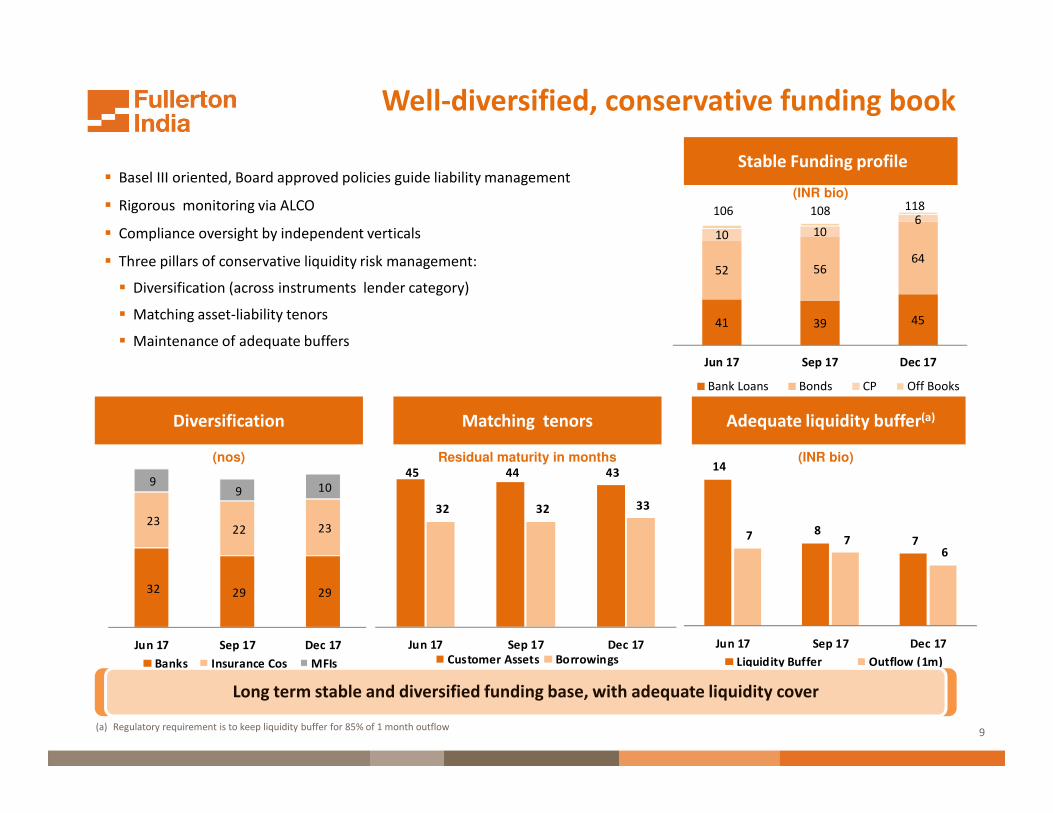

41 39 45

52 5664

10 106

Jun 17 Sep 17 Dec 17

Bank Loans Bonds CP Off Books

106 118108

14

8 7 7 7

6

Jun 17 Sep 17 Dec 17

Liquidity Buffer Outflow (1m)

Well-diversified, conservative funding book

Diversification Matching tenors Adequate liquidity buffer(a)

(nos) Residual maturity in months (INR bio)

� Basel III oriented, Board approved policies guide liability management

� Rigorous monitoring via ALCO

� Compliance oversight by independent verticals

� Three pillars of conservative liquidity risk management:

� Diversification (across instruments lender category)

� Matching asset-liability tenors

� Maintenance of adequate buffers

Long term stable and diversified funding base, with adequate liquidity cover

(a) Regulatory requirement is to keep liquidity buffer for 85% of 1 month outflow

32 29 29

23 22 23

9 9 10

Jun 17 Sep 17 Dec 17

Banks Insurance Cos MFIs

45 44 43

32 32 33

Jun 17 Sep 17 Dec 17

Customer Assets Borrowings

Stable Funding profile

(INR bio)

10

Enterprise wide, independent risk managementIntegrated approach covering entity wide risks

Overarching principles

governing Risk

Management strategy

Analytics led proactive

portfolio management

strategies

Underwriting strategies

addressing the product/

customer segment /

geographic nuances

� Risk Appetite Statement and Country Risk Assessment set the guardrails

� Assessed for ‘through the cycle’ performance and ‘stress resilience’

� Independent, integrated Operational risk and Fraud risk management

� Portfolio analytics evaluates portfolio optimisation

� PD, LGD models and risk based pricing used to guide portfolio

� Quarterly bureau scrubs flowing into early warning processes.

� Robust ‘champion-challenger’ environment to test boundaries

� Decisioning platforms based on application and behavior scorecards, fraud scoring, risk based pricing

� Supported by an automated Business Rule Engine with connectivity to bureau and fraud systems

� Judicious mix of local and centralized decisioning with robust deviation controls

� Strong collateral management – independent legal/valuation with in-house technical oversight

Collections

management driven

scientifically

� In-house tele-calling set-up with recorded lines for quick reach out to early delinquencies

� Mix of in-house (for early buckets and secured portfolios) and agencies (for late bucket and

recoveries)

� Propensity models, behavior scorecards and recovery scores for optimizing collection strategy

� Mobility solutions enabled for field staff which improves control environment significantly

Pro-active and continuous monitoring based on external environment, customer data and bureau trends

11

Operational risk managementStrong Operational Risk management culture across all key verticals

Operational and Business

Units (design and operational

effectiveness)

1st line of defense

Independent Assurance

by Internal Audit

3rd line of defense

ORMC

ROC/ Board OversightExternal

AuditorsRegulators

Operational Risk, Fraud Risk, InfoSec

and Compliance

2nd line of defense

OR framework components

Implementation/ execution

Risk Governance

framework

� Regular Operational Risk Management Committee meetings to review OR issues

� Quarterly Risk Oversight Committee meetings to assess OR profile

Policy/ Procedures� Robust Operational Risk policies and standards

� Internal Financial Controls (IFC) standards as mandated by Companies Act

Risk Identification� Comprehensive Risk library

� Regular process walkthroughs and reviews

Risk Assessment &

Measurement

� Periodic Risk Assessments

� Loss Data management

Control & Mitigation� Periodic control assessment

� Timely corrective actions

Monitoring &

Reporting

� Key Risk Indicators monitoring

� Regular reporting to ORMC and ROC

12

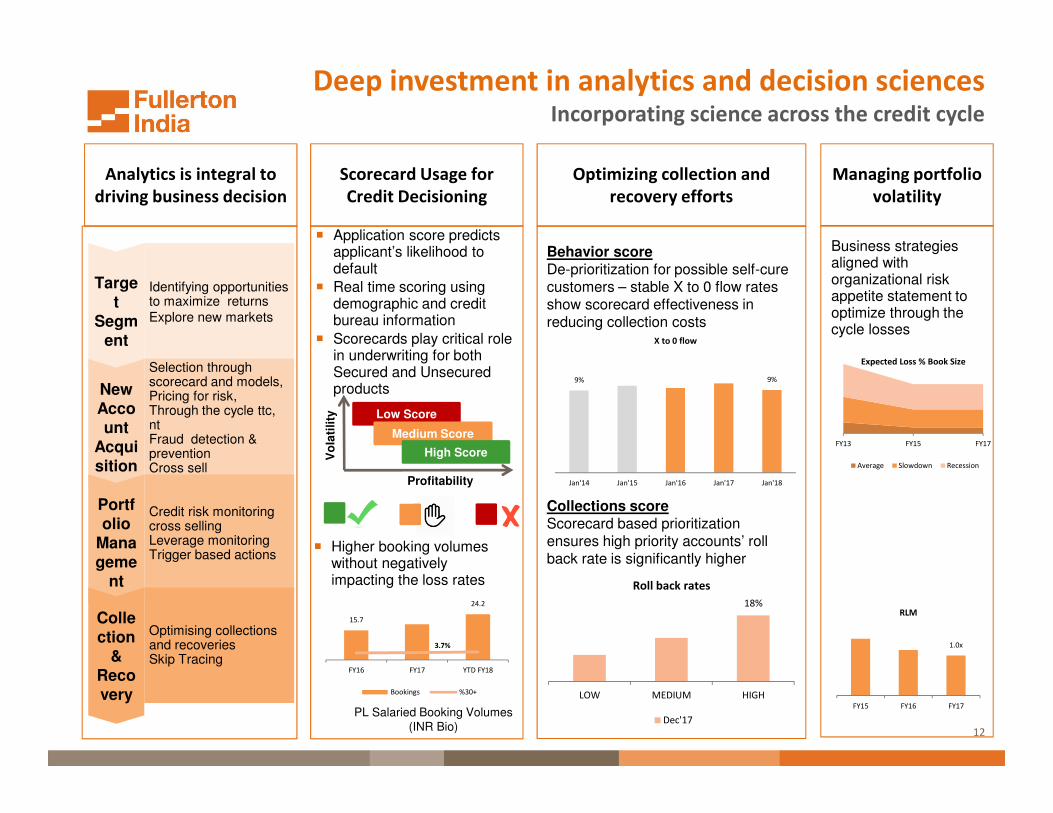

Deep investment in analytics and decision sciencesIncorporating science across the credit cycle

Analytics is integral to

driving business decision

Scorecard Usage for

Credit Decisioning

Optimizing collection and

recovery efforts

Managing portfolio

volatility

Identifying opportunities to maximize returns

Explore new markets

Selection through scorecard and models, Pricing for risk, Through the cycle ttc,ntFraud detection & preventionCross sell

Credit risk monitoring cross sellingLeverage monitoringTrigger based actions

Optimising collections and recoveriesSkip Tracing

Target

Segment

New Account

Acquisition

Portfolio

Manageme

nt

Collection

& Recovery

� Application score predicts applicant’s likelihood to default

� Real time scoring using demographic and credit bureau information

� Scorecards play critical role in underwriting for both Secured and Unsecured products

Low Score

Profitability

Vo

lati

lity

Medium Score

High Score

� Higher booking volumes without negatively impacting the loss rates

PL Salaried Booking Volumes

(INR Bio)

Behavior score De-prioritization for possible self-cure customers – stable X to 0 flow rates show scorecard effectiveness in reducing collection costs

Collections score Scorecard based prioritization ensures high priority accounts’ roll back rate is significantly higher

Business strategies aligned with organizational risk appetite statement to optimize through the cycle losses

9% 9%

Jan'14 Jan'15 Jan'16 Jan'17 Jan'18

X to 0 flow

FY13 FY15 FY17

Expected Loss % Book Size

Average Slowdown Recession

1.0x

FY15 FY16 FY17

RLM15.7

24.2

3.7%

FY16 FY17 YTD FY18

Bookings %30+

18%

LOW MEDIUM HIGH

Roll back rates

Dec'17

13

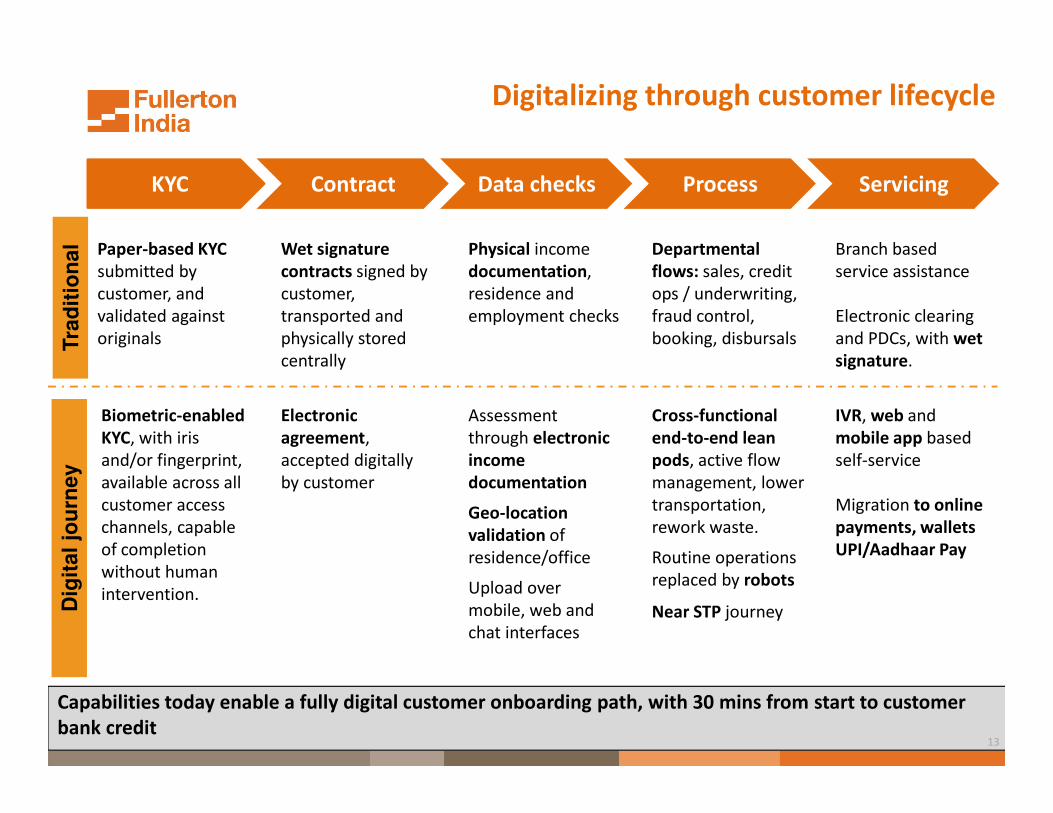

KYC Contract Data checks Process Servicing

Paper-based KYC

submitted by

customer, and

validated against

originals

Wet signature

contracts signed by

customer,

transported and

physically stored

centrally

Physical income

documentation,

residence and

employment checks

Departmental

flows: sales, credit

ops / underwriting,

fraud control,

booking, disbursals

Branch based

service assistance

Electronic clearing

and PDCs, with wet

signature.

Biometric-enabled

KYC, with iris

and/or fingerprint,

available across all

customer access

channels, capable

of completion

without human

intervention.

Electronic

agreement,

accepted digitally

by customer

Assessment

through electronic

income

documentation

Geo-location

validation of

residence/office

Upload over

mobile, web and

chat interfaces

Cross-functional

end-to-end lean

pods, active flow

management, lower

transportation,

rework waste.

Routine operations

replaced by robots

Near STP journey

IVR, web and

mobile app based

self-service

Migration to online

payments, wallets

UPI/Aadhaar Pay

Digitalizing through customer lifecycle

Capabilities today enable a fully digital customer onboarding path, with 30 mins from start to customer

bank credit

Tra

dit

ion

al

Dig

ita

l jo

urn

ey

13

14

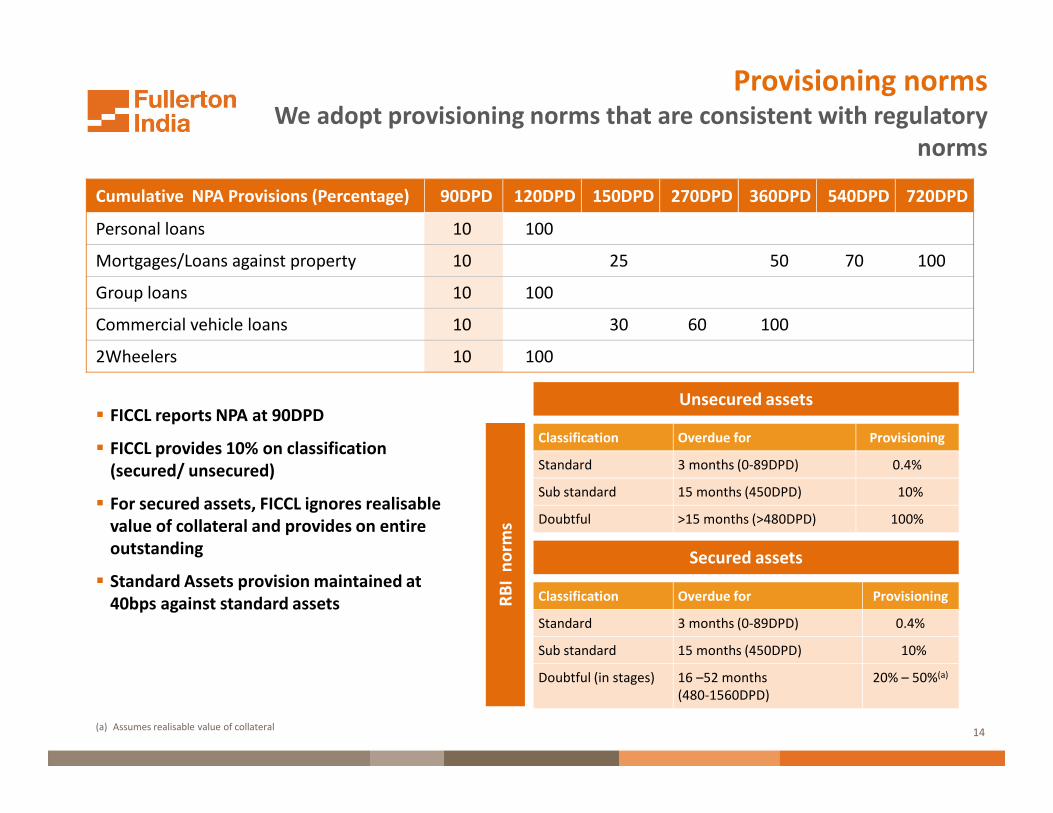

Provisioning normsWe adopt provisioning norms that are consistent with regulatory

norms

Cumulative NPA Provisions (Percentage) 90DPD 120DPD 150DPD 270DPD 360DPD 540DPD 720DPD

Personal loans 10 100

Mortgages/Loans against property 10 25 50 70 100

Group loans 10 100

Commercial vehicle loans 10 30 60 100

2Wheelers 10 100

� FICCL reports NPA at 90DPD

� FICCL provides 10% on classification

(secured/ unsecured)

� For secured assets, FICCL ignores realisable

value of collateral and provides on entire

outstanding

� Standard Assets provision maintained at

40bps against standard assets

Unsecured assets

Classification Overdue for Provisioning

Standard 3 months (0-89DPD) 0.4%

Sub standard 15 months (450DPD) 10%

Doubtful >15 months (>480DPD) 100%

Secured assets

Classification Overdue for Provisioning

Standard 3 months (0-89DPD) 0.4%

Sub standard 15 months (450DPD) 10%

Doubtful (in stages) 16 –52 months

(480-1560DPD)

20% – 50%(a)

RB

I n

orm

s

(a) Assumes realisable value of collateral

15

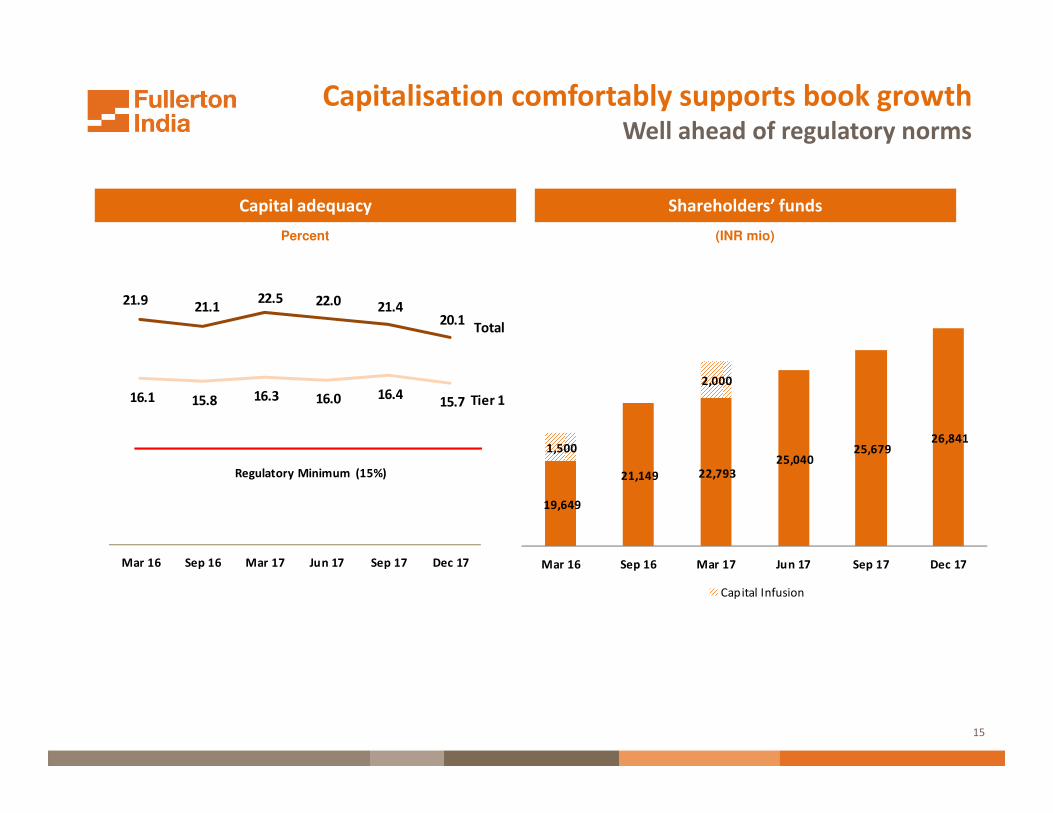

Capitalisation comfortably supports book growth Well ahead of regulatory norms

Capital adequacy Shareholders’ funds

Percent (INR mio)

16.1 15.8 16.3 16.0 16.4 15.7

21.9 21.1

22.5 22.0 21.4 20.1

Mar 16 Sep 16 Mar 17 Jun 17 Sep 17 Dec 17

Regulatory Minimum (15%)

Total

Tier 1

19,649

21,149 22,793 25,040

25,679 26,841

1,500

2,000

Mar 16 Sep 16 Mar 17 Jun 17 Sep 17 Dec 17

Capital Infusion

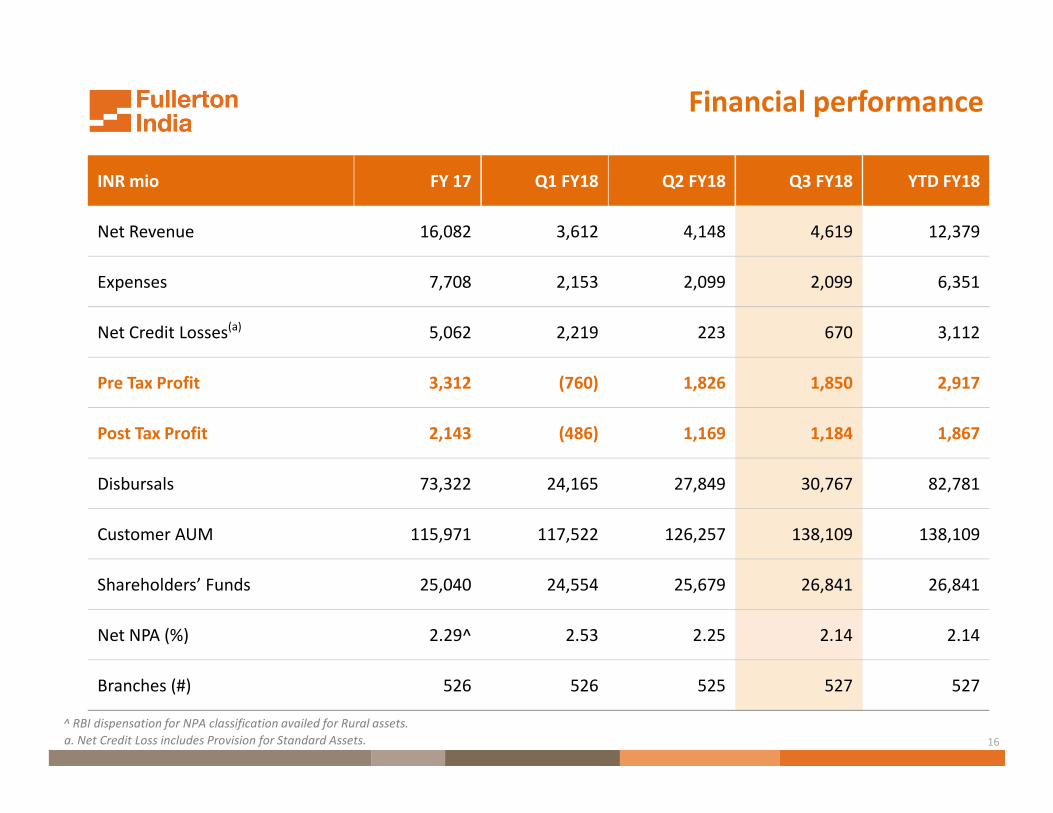

a. Net Credit Loss includes Provision for Standard Assets. 16

INR mio FY 17 Q1 FY18 Q2 FY18 Q3 FY18 YTD FY18

Net Revenue 16,082 3,612 4,148 4,619 12,379

Expenses 7,708 2,153 2,099 2,099 6,351

Net Credit Losses(a) 5,062 2,219 223 670 3,112

Pre Tax Profit 3,312 (760) 1,826 1,850 2,917

Post Tax Profit 2,143 (486) 1,169 1,184 1,867

Disbursals 73,322 24,165 27,849 30,767 82,781

Customer AUM 115,971 117,522 126,257 138,109 138,109

Shareholders’ Funds 25,040 24,554 25,679 26,841 26,841

Net NPA (%) 2.29^ 2.53 2.25 2.14 2.14

Branches (#) 526 526 525 527 527

Financial performance

^ RBI dispensation for NPA classification availed for Rural assets.

17

Strong business momentum

Disbursals (INR mio) Assets Under Management (INR mio)

13,990 13,634

24,165

27,849

30,767

Q3 FY17 Q4 FY17 Q1 FY18 Q2 FY18 Q3 FY18

121,980

115,971 117,522

126,257

138,109

Q3 FY17 Q4 FY17 Q1 FY18 Q2 FY18 Q3 FY18

18

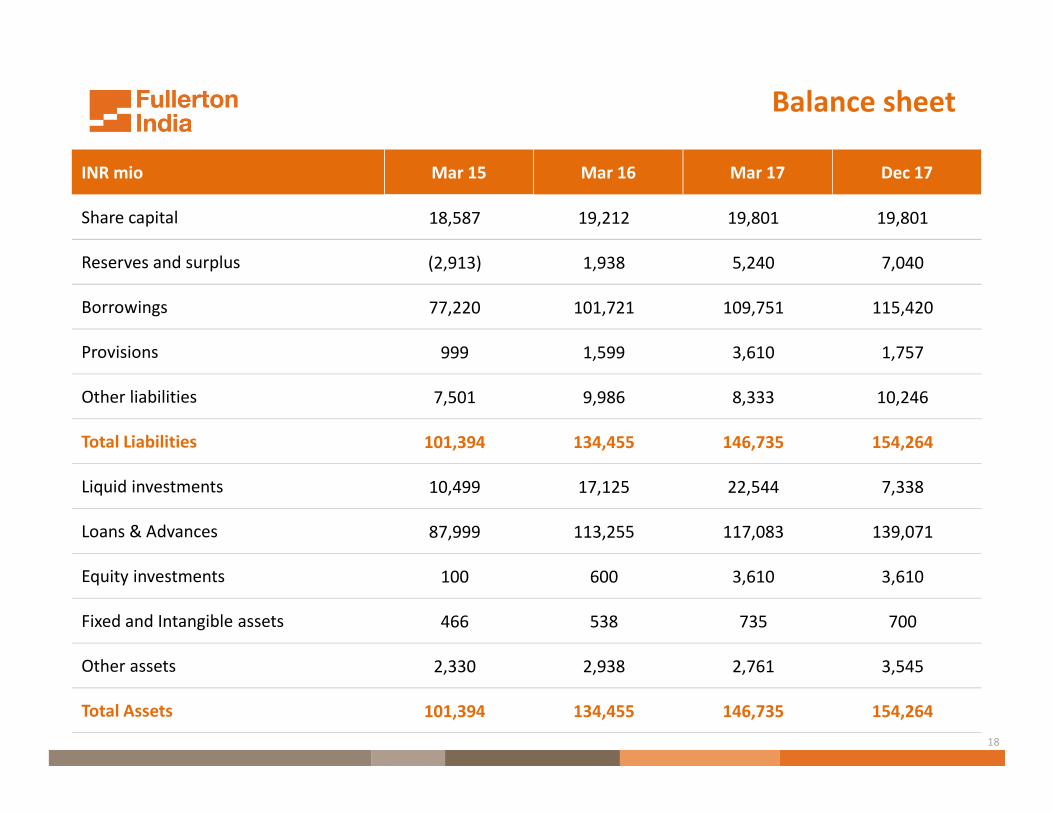

INR mio Mar 15 Mar 16 Mar 17 Dec 17

Share capital 18,587 19,212 19,801 19,801

Reserves and surplus (2,913) 1,938 5,240 7,040

Borrowings 77,220 101,721 109,751 115,420

Provisions 999 1,599 3,610 1,757

Other liabilities 7,501 9,986 8,333 10,246

Total Liabilities 101,394 134,455 146,735 154,264

Liquid investments 10,499 17,125 22,544 7,338

Loans & Advances 87,999 113,255 117,083 139,071

Equity investments 100 600 3,610 3,610

Fixed and Intangible assets 466 538 735 700

Other assets 2,330 2,938 2,761 3,545

Total Assets 101,394 134,455 146,735 154,264

Balance sheet

19

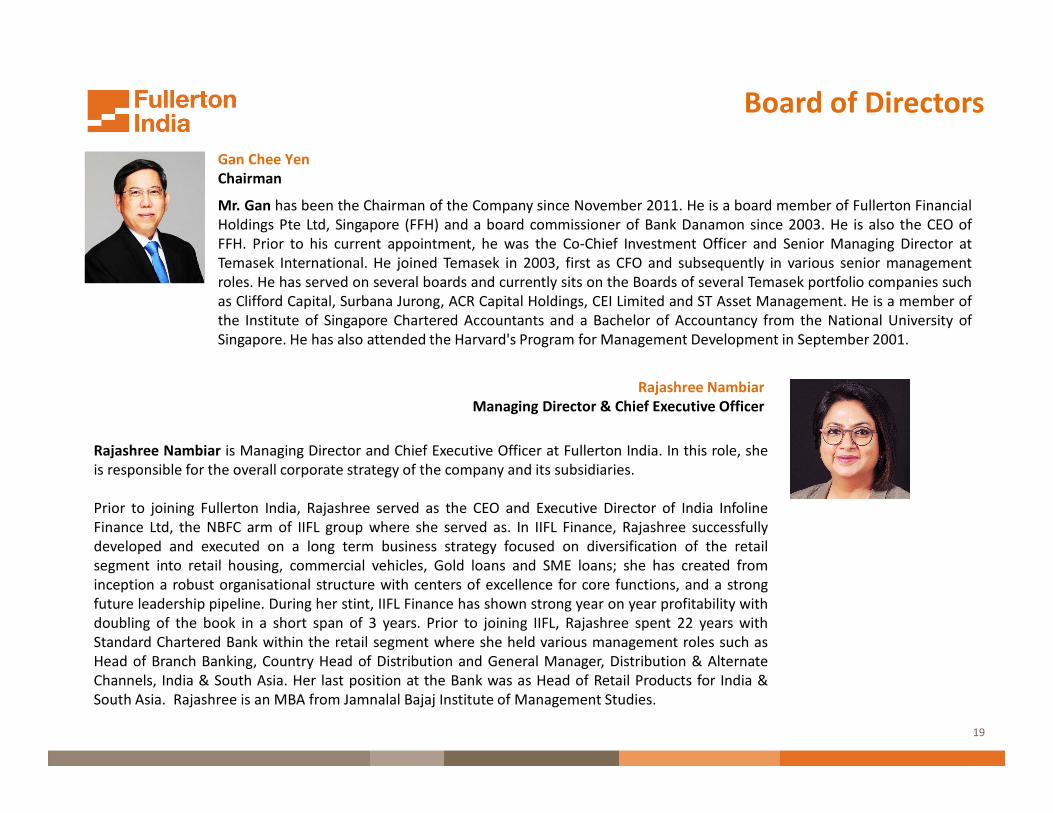

Gan Chee Yen

Chairman

Mr. Gan has been the Chairman of the Company since November 2011. He is a board member of Fullerton Financial

Holdings Pte Ltd, Singapore (FFH) and a board commissioner of Bank Danamon since 2003. He is also the CEO of

FFH. Prior to his current appointment, he was the Co-Chief Investment Officer and Senior Managing Director at

Temasek International. He joined Temasek in 2003, first as CFO and subsequently in various senior management

roles. He has served on several boards and currently sits on the Boards of several Temasek portfolio companies such

as Clifford Capital, Surbana Jurong, ACR Capital Holdings, CEI Limited and ST Asset Management. He is a member of

the Institute of Singapore Chartered Accountants and a Bachelor of Accountancy from the National University of

Singapore. He has also attended the Harvard's Program for Management Development in September 2001.

Board of Directors

Rajashree Nambiar is Managing Director and Chief Executive Officer at Fullerton India. In this role, she

is responsible for the overall corporate strategy of the company and its subsidiaries.

Prior to joining Fullerton India, Rajashree served as the CEO and Executive Director of India Infoline

Finance Ltd, the NBFC arm of IIFL group where she served as. In IIFL Finance, Rajashree successfully

developed and executed on a long term business strategy focused on diversification of the retail

segment into retail housing, commercial vehicles, Gold loans and SME loans; she has created from

inception a robust organisational structure with centers of excellence for core functions, and a strong

future leadership pipeline. During her stint, IIFL Finance has shown strong year on year profitability with

doubling of the book in a short span of 3 years. Prior to joining IIFL, Rajashree spent 22 years with

Standard Chartered Bank within the retail segment where she held various management roles such as

Head of Branch Banking, Country Head of Distribution and General Manager, Distribution & Alternate

Channels, India & South Asia. Her last position at the Bank was as Head of Retail Products for India &

South Asia. Rajashree is an MBA from Jamnalal Bajaj Institute of Management Studies.

Rajashree Nambiar

Managing Director & Chief Executive Officer

20

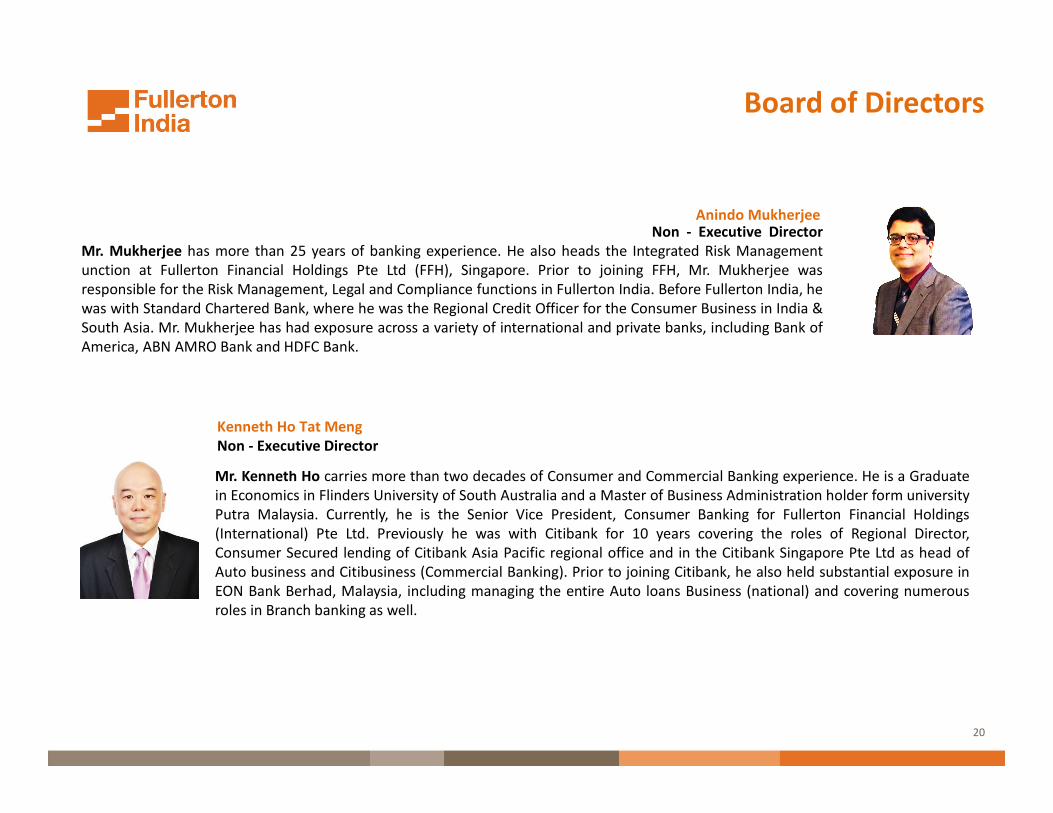

Anindo MukherjeeNon - Executive Director

Mr. Mukherjee has more than 25 years of banking experience. He also heads the Integrated Risk Management

unction at Fullerton Financial Holdings Pte Ltd (FFH), Singapore. Prior to joining FFH, Mr. Mukherjee was

responsible for the Risk Management, Legal and Compliance functions in Fullerton India. Before Fullerton India, he

was with Standard Chartered Bank, where he was the Regional Credit Officer for the Consumer Business in India &

South Asia. Mr. Mukherjee has had exposure across a variety of international and private banks, including Bank of

America, ABN AMRO Bank and HDFC Bank.

Board of Directors

Mr. Kenneth Ho carries more than two decades of Consumer and Commercial Banking experience. He is a Graduate

in Economics in Flinders University of South Australia and a Master of Business Administration holder form university

Putra Malaysia. Currently, he is the Senior Vice President, Consumer Banking for Fullerton Financial Holdings

(International) Pte Ltd. Previously he was with Citibank for 10 years covering the roles of Regional Director,

Consumer Secured lending of Citibank Asia Pacific regional office and in the Citibank Singapore Pte Ltd as head of

Auto business and Citibusiness (Commercial Banking). Prior to joining Citibank, he also held substantial exposure in

EON Bank Berhad, Malaysia, including managing the entire Auto loans Business (national) and covering numerous

roles in Branch banking as well.

Kenneth Ho Tat Meng

Non - Executive Director

21

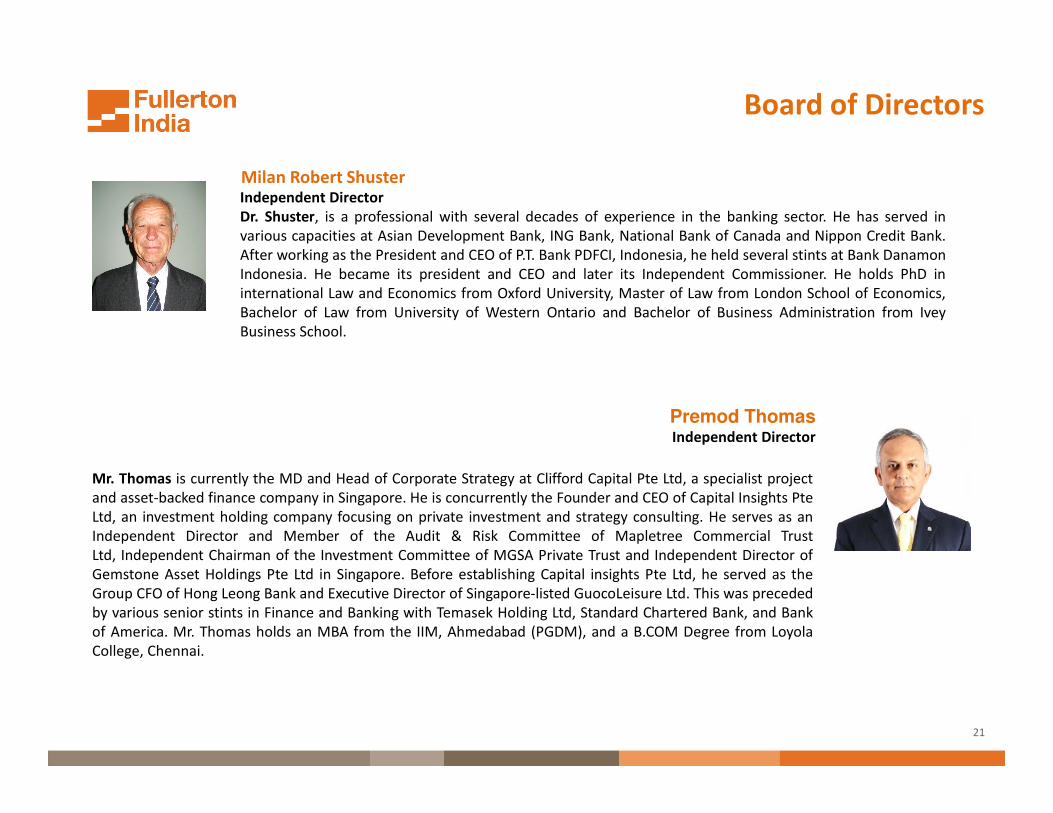

Milan Robert ShusterIndependent Director

Dr. Shuster, is a professional with several decades of experience in the banking sector. He has served in

various capacities at Asian Development Bank, ING Bank, National Bank of Canada and Nippon Credit Bank.

After working as the President and CEO of P.T. Bank PDFCI, Indonesia, he held several stints at Bank Danamon

Indonesia. He became its president and CEO and later its Independent Commissioner. He holds PhD in

international Law and Economics from Oxford University, Master of Law from London School of Economics,

Bachelor of Law from University of Western Ontario and Bachelor of Business Administration from Ivey

Business School.

Premod ThomasIndependent Director

Independent Director Mr. Thomas is currently the MD and Head of Corporate Strategy at Clifford Capital Pte Ltd, a specialist project

and asset-backed finance company in Singapore. He is concurrently the Founder and CEO of Capital Insights Pte

Ltd, an investment holding company focusing on private investment and strategy consulting. He serves as an

Independent Director and Member of the Audit & Risk Committee of Mapletree Commercial Trust

Ltd, Independent Chairman of the Investment Committee of MGSA Private Trust and Independent Director of

Gemstone Asset Holdings Pte Ltd in Singapore. Before establishing Capital insights Pte Ltd, he served as the

Group CFO of Hong Leong Bank and Executive Director of Singapore-listed GuocoLeisure Ltd. This was preceded

by various senior stints in Finance and Banking with Temasek Holding Ltd, Standard Chartered Bank, and Bank

of America. Mr. Thomas holds an MBA from the IIM, Ahmedabad (PGDM), and a B.COM Degree from Loyola

College, Chennai.

Board of Directors

22

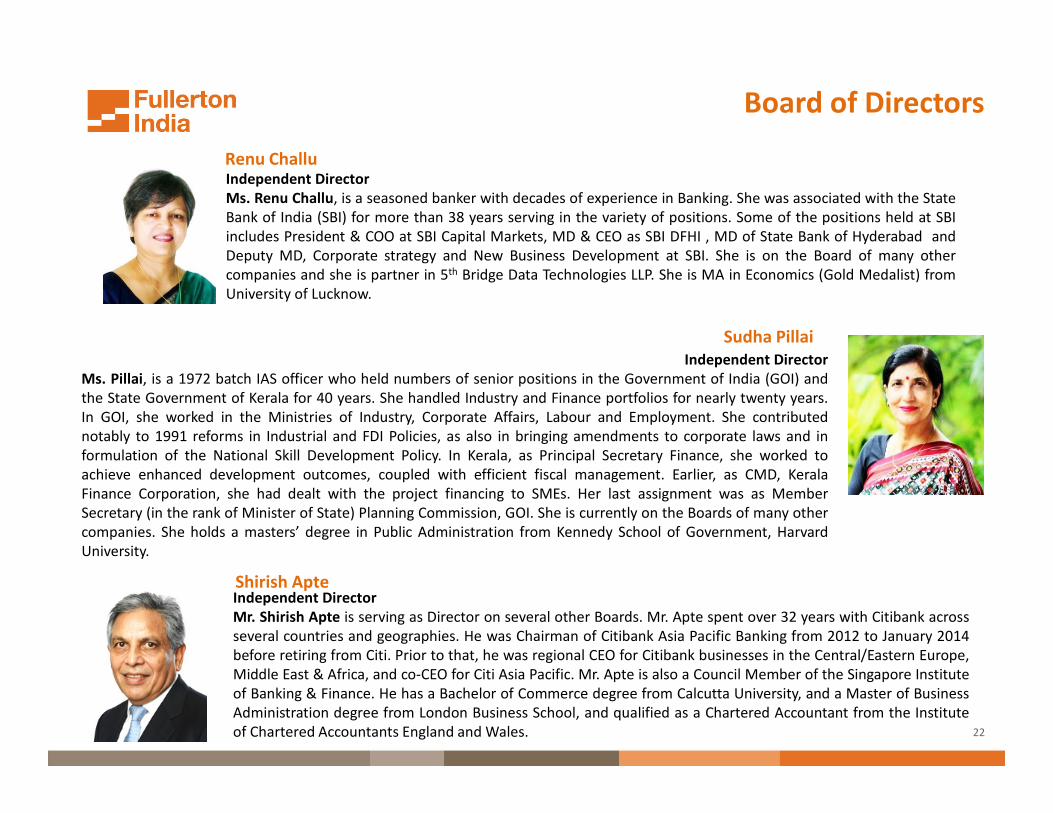

Renu ChalluIndependent Director

Ms. Renu Challu, is a seasoned banker with decades of experience in Banking. She was associated with the State

Bank of India (SBI) for more than 38 years serving in the variety of positions. Some of the positions held at SBI

includes President & COO at SBI Capital Markets, MD & CEO as SBI DFHI , MD of State Bank of Hyderabad and

Deputy MD, Corporate strategy and New Business Development at SBI. She is on the Board of many other

companies and she is partner in 5th Bridge Data Technologies LLP. She is MA in Economics (Gold Medalist) from

University of Lucknow.

Independent Director

Ms. Pillai, is a 1972 batch IAS officer who held numbers of senior positions in the Government of India (GOI) and

the State Government of Kerala for 40 years. She handled Industry and Finance portfolios for nearly twenty years.

In GOI, she worked in the Ministries of Industry, Corporate Affairs, Labour and Employment. She contributed

notably to 1991 reforms in Industrial and FDI Policies, as also in bringing amendments to corporate laws and in

formulation of the National Skill Development Policy. In Kerala, as Principal Secretary Finance, she worked to

achieve enhanced development outcomes, coupled with efficient fiscal management. Earlier, as CMD, Kerala

Finance Corporation, she had dealt with the project financing to SMEs. Her last assignment was as Member

Secretary (in the rank of Minister of State) Planning Commission, GOI. She is currently on the Boards of many other

companies. She holds a masters’ degree in Public Administration from Kennedy School of Government, Harvard

University.

Sudha Pillai

Board of Directors

Shirish ApteIndependent Director

Mr. Shirish Apte is serving as Director on several other Boards. Mr. Apte spent over 32 years with Citibank across

several countries and geographies. He was Chairman of Citibank Asia Pacific Banking from 2012 to January 2014

before retiring from Citi. Prior to that, he was regional CEO for Citibank businesses in the Central/Eastern Europe,

Middle East & Africa, and co-CEO for Citi Asia Pacific. Mr. Apte is also a Council Member of the Singapore Institute

of Banking & Finance. He has a Bachelor of Commerce degree from Calcutta University, and a Master of Business

Administration degree from London Business School, and qualified as a Chartered Accountant from the Institute

of Chartered Accountants England and Wales.

23

Leadership Team

Ajay PareekBusiness Head - Urban

Ajay is a Chartered Accountant with over 21 years' experience in audit & financial services. Starting his career with

A. F. Fergusons & Co, he moved to CitiFinancial as part of the start-up team to launch their retail finance business

in India. At CitiFinancial he handled the risk and operations functions for 3 years and later took over as a Regional

Business Head. After 8 years at CitiFinancial, he joined Fullerton India in 2005 as part of the start-up team. Ajay is

now Head of Urban Business and oversees distribution of the company's key products of Personal Loans,

Mortgages, SME and Commercial vehicle.

Vishal WadhwaBusiness Head - Rural

Vishal is the Head of Rural Business at Fullerton India. He is a Chartered Accountant from The Institute of

Chartered Accountants of India with over 20 years of varied experience in Banking and Financial Services across

Credit Cards, Consumer Banking Products, Collections and Retail Banking Operations. Vishal joined Fullerton

India in March 2012 from Tata Consultancy Services, where he headed two key functions during his tenure – as

Operations Head, facilitating client engagement and operations delivery for Commercial Bank of Qatar and as

Consumer Operations Head for India Retail. Previously, Vishal worked with Citibank N.A handling Distributions

Operations, Risk Management and Credit Operations across retail products and Branch Banking. Prior to

Citibank N.A, Vishal worked with ABN AMRO and Citigroup as East Collections Head - Cards.

24

Leadership Team

Deepak is the Chief Risk Officer and in his role he leads the overall Enterprise Risk Management across all business

verticals of Fullerton India, which includes Credit Risk, Collections, Operational Risk, Fraud Control, Legal and

Information Security functions. Prior to his appointment as the CRO, Deepak led the Internal Audit function at

Fullerton India. Deepak joined Fullerton India in 2007 as Head – Retail Collections after successful stints at Cable

Corporation, HCL Infosystems and Citibank. In his work experience of over 20 years he has handled diverse roles

including Quality Assurance, Sales and Distribution, Debt Collections, Operational Risk and Audit. On behalf of

Fullerton Financial Holdings, Singapore, Deepak has undertaken risk advisory and transformation assignments in

Mekong Development Bank, Vietnam and Fullerton Finance, Myanmar. He is an Electrical Engineer with a Masters

in Management from Jamnalal Bajaj Institute, Mumbai..

Deepak PatkarChief Risk officer

Pankaj has an overall experience of 20+ years in various capacities across finance and allied functions. He is the

Chief Financial Officer, Company Secretary and Chief Compliance Officer for Fullerton India Credit Company

Limited. In addition, he holds the position of Chief Financial Officer of Fullerton India Home Finance Company

Limited. At Fullerton, he is responsible for corporate planning, accounting, finance, taxation, compliance and

corporate governance functions. Prior to joining Fullerton in Sep 2007, Pankaj was associated with COLT Telecom

(“COLT”), an affiliate of Fidelity international, as the Financial Controller-cum-Company Secretary. He has also

been associated with GE Commercial Financial and Motherson Sumi Systems Limited in various capacities.

Pankaj is a Chartered Accountant, Company Secretary and Cost Accountant from India and Certified Public

Accountant from the State of Colorado, the USA.

Pankaj MalikChief Financial Officer

25

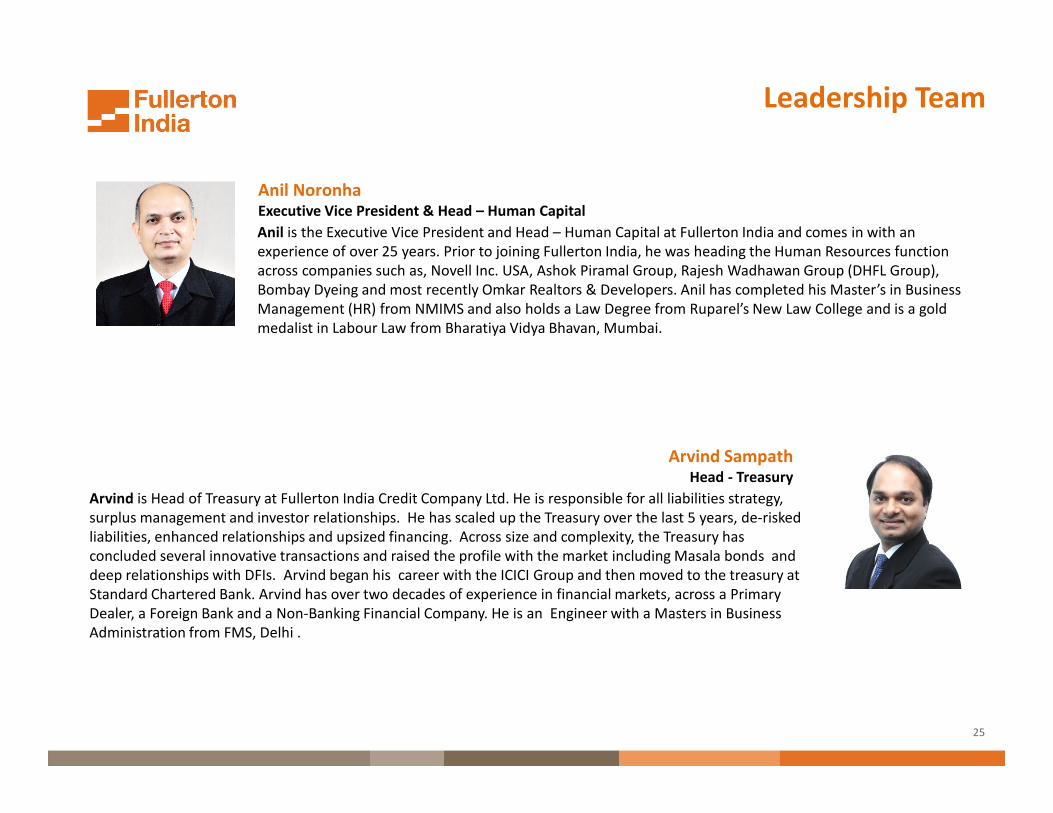

Arvind SampathHead - Treasury

Leadership Team

Anil NoronhaExecutive Vice President & Head – Human Capital

Anil is the Executive Vice President and Head – Human Capital at Fullerton India and comes in with an

experience of over 25 years. Prior to joining Fullerton India, he was heading the Human Resources function

across companies such as, Novell Inc. USA, Ashok Piramal Group, Rajesh Wadhawan Group (DHFL Group),

Bombay Dyeing and most recently Omkar Realtors & Developers. Anil has completed his Master’s in Business

Management (HR) from NMIMS and also holds a Law Degree from Ruparel’s New Law College and is a gold

medalist in Labour Law from Bharatiya Vidya Bhavan, Mumbai.

Arvind is Head of Treasury at Fullerton India Credit Company Ltd. He is responsible for all liabilities strategy,

surplus management and investor relationships. He has scaled up the Treasury over the last 5 years, de-risked

liabilities, enhanced relationships and upsized financing. Across size and complexity, the Treasury has

concluded several innovative transactions and raised the profile with the market including Masala bonds and

deep relationships with DFIs. Arvind began his career with the ICICI Group and then moved to the treasury at

Standard Chartered Bank. Arvind has over two decades of experience in financial markets, across a Primary

Dealer, a Foreign Bank and a Non-Banking Financial Company. He is an Engineer with a Masters in Business

Administration from FMS, Delhi .

26

Leadership Team

Kaushik RayGeneral Manager and Head – Operations & Customer Service

Kaushik is the Head of Operations and Customer Service for Fullerton India. He joins from Creditexchange, a

Bengaluru-based Fintech start-up, where he served as the Chief Operating Officer, responsible for setting up

the Operations, Technology, Collections, Finance and Accounts processes. Previously, Kaushik was heading the

Operations team at Fullerton India for over 6 years from 2005 to 2012. Earlier, he was part of the management

team of DLL Financial Services, a fully owned subsidiary of the Rabobank group, as head of the Operations,

Sales Support & Technology units. His other stints during his career of close to 25 years include, leading Trade

transactions processing and Contact Center operations in Citigroup, International Trade in Reliance Industries

and Corporate Loans sourcing for Summit Usha Martin Finance and Nicco Uco Financial Services. Kaushik holds

a Post Graduate diploma in Management from Xavier Institute of Management, Bhubaneswar.

Bikramjit GangulyChief Information and Digital Officer

Bikramjit has an overall experience of 14+ years in various capacities across analytics and allied functions. He is

currently the Chief Information and Digital officer for Fullerton India Credit Company Limited. At Fullerton, he is

responsible for leading the company’s digital strategy and execution as well as the information technology and

analytics functions. Prior to joining Fullerton in Mar 2012, Bikramjit was associated with Standard Chartered

Bank, heading the regional credit risk analytics unit of South Asia. He has also been associated with Fair Isaac

(“FICO”) in various capacities and has extensive experience of driving analytics driven strategies for major

financial organizations across Asia, Middle East, Latin America, Europe and Africa. Bikramjit is a Masters in

Statistics from the Indian Statistical Institute.

27

ContactFullerton India Credit Company Ltd.Floor 6, B Wing, Supreme IT Park,

Powai,

Mumbai 400 076

INDIA

Phone: +91 22 6749 1234

www.fullertonindia.com

28

Your Preferred

Financial Partner

28