© 2016 IHS Markit. All Rights Reserved. © 2016 IHS Markit. All Rights Reserved.

Global Energy Markets & Alberta Leveraging the Alberta legacy to attract new waves of petrochemical industry investment

BUILDING ALBERTA'S INNOVATION AND INVESTMENT 18th Annual Stakeholder Luncheon Thursday, January 19, 2017 Edmonton, Alberta, Canada

Mark Eramo, VP Global Business Development Oil / Midstream / Downstream & Chemicals Houston, TX [email protected]

© 2016 IHS Markit

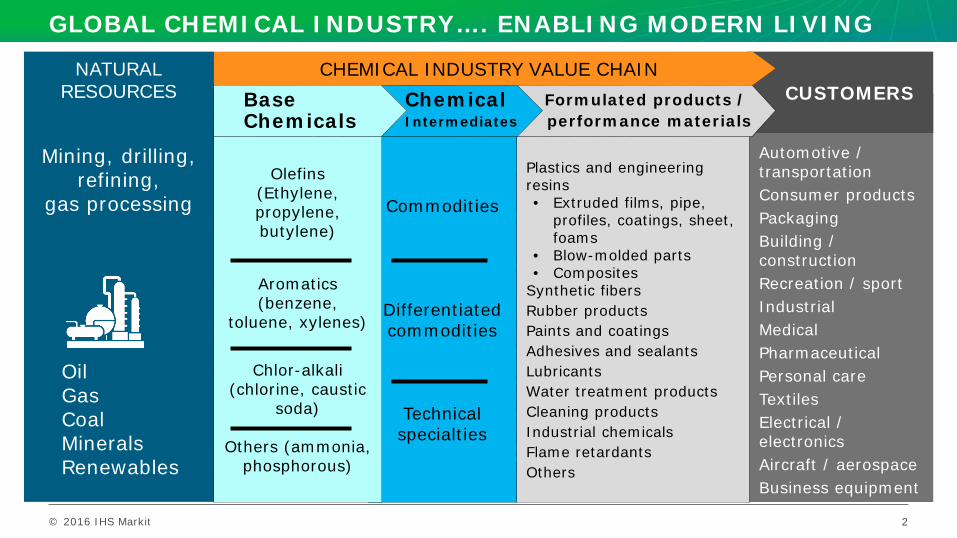

Automotive / transportation Consumer products Packaging Building / construction Recreation / sport Industrial Medical Pharmaceutical Personal care Textiles Electrical / electronics Aircraft / aerospace Business equipment

GLOBAL CHEMICAL INDUSTRY…. ENABLING MODERN LIVING

CUSTOMERS CHEMICAL INDUSTRY VALUE CHAIN NATURAL

RESOURCES

Mining, drilling, refining,

gas processing

Oil Gas Coal Minerals Renewables

Plastics and engineering resins • Extruded films, pipe,

profiles, coatings, sheet, foams

• Blow-molded parts • Composites

Synthetic fibers Rubber products Paints and coatings Adhesives and sealants Lubricants Water treatment products Cleaning products Industrial chemicals Flame retardants Others

Formulated products / performance materials

Commodities

Differentiated commodities

Technical specialties

Chemical Intermediates

Olefins (Ethylene, propylene, butylene)

Aromatics (benzene,

toluene, xylenes)

Chlor-alkali

(chlorine, caustic soda)

Others (ammonia,

phosphorous)

Base Chemicals

2

© 2016 IHS Markit

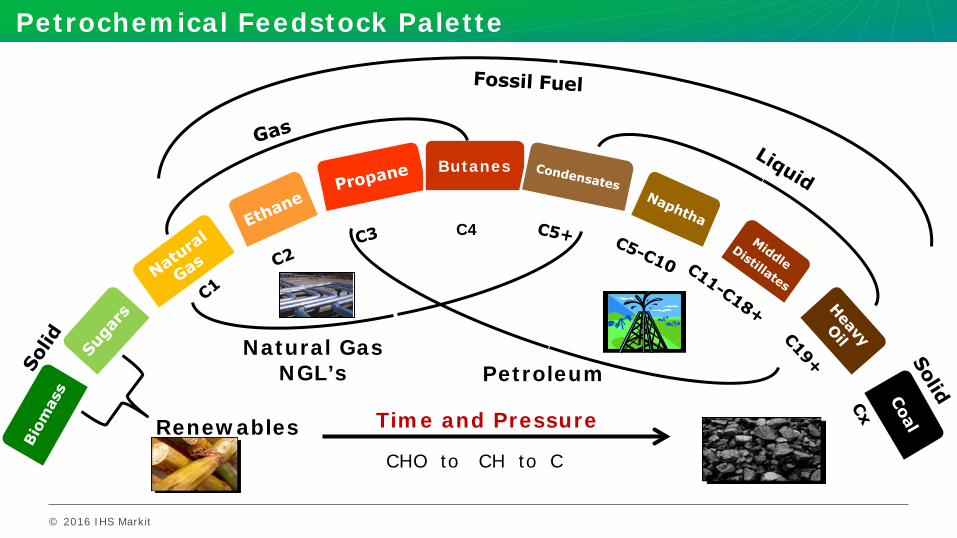

Petrochemical Feedstock Palette

Butanes

Renewables Time and Pressure

CHO to CH to C

Natural Gas NGL’s Petroleum

C4

© 2016 IHS Markit

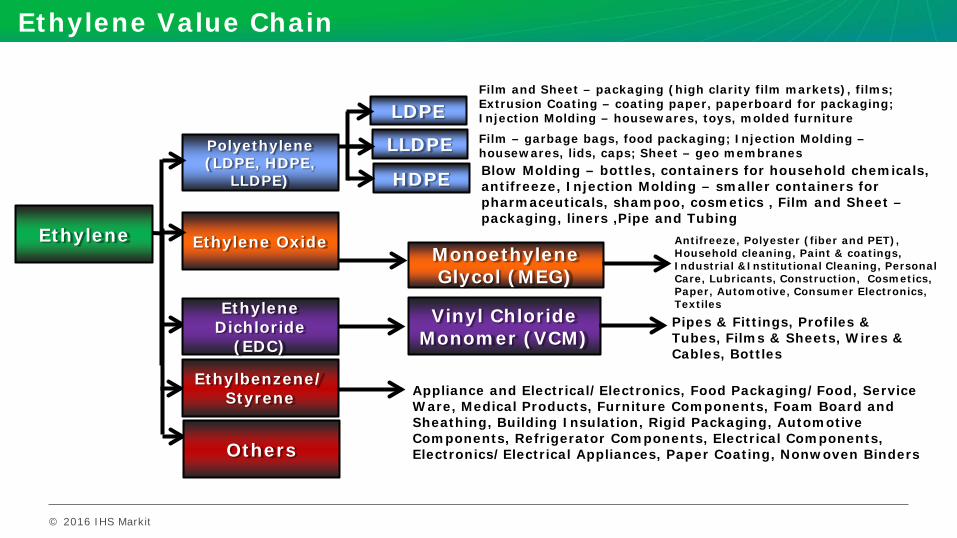

Ethylene Value Chain

Polyethylene (LDPE, HDPE,

LLDPE)

Monoethylene Glycol (MEG)

Ethylene Oxide Ethylene

Ethylbenzene/ Styrene

Others

Antifreeze, Polyester (fiber and PET), Household cleaning, Paint & coatings, Industrial &Institutional Cleaning, Personal Care, Lubricants, Construction, Cosmetics, Paper, Automotive, Consumer Electronics, Textiles Ethylene

Dichloride (EDC)

Vinyl Chloride Monomer (VCM)

Pipes & Fittings, Profiles & Tubes, Films & Sheets, Wires & Cables, Bottles

Appliance and Electrical/Electronics, Food Packaging/Food, Service Ware, Medical Products, Furniture Components, Foam Board and Sheathing, Building Insulation, Rigid Packaging, Automotive Components, Refrigerator Components, Electrical Components, Electronics/Electrical Appliances, Paper Coating, Nonwoven Binders

LLDPE

LDPE

HDPE

Film and Sheet – packaging (high clarity film markets), films; Extrusion Coating – coating paper, paperboard for packaging; Injection Molding – housewares, toys, molded furniture Film – garbage bags, food packaging; Injection Molding – housewares, lids, caps; Sheet – geo membranes Blow Molding – bottles, containers for household chemicals, antifreeze, Injection Molding – smaller containers for pharmaceuticals, shampoo, cosmetics , Film and Sheet – packaging, liners ,Pipe and Tubing

© 2016 IHS Markit

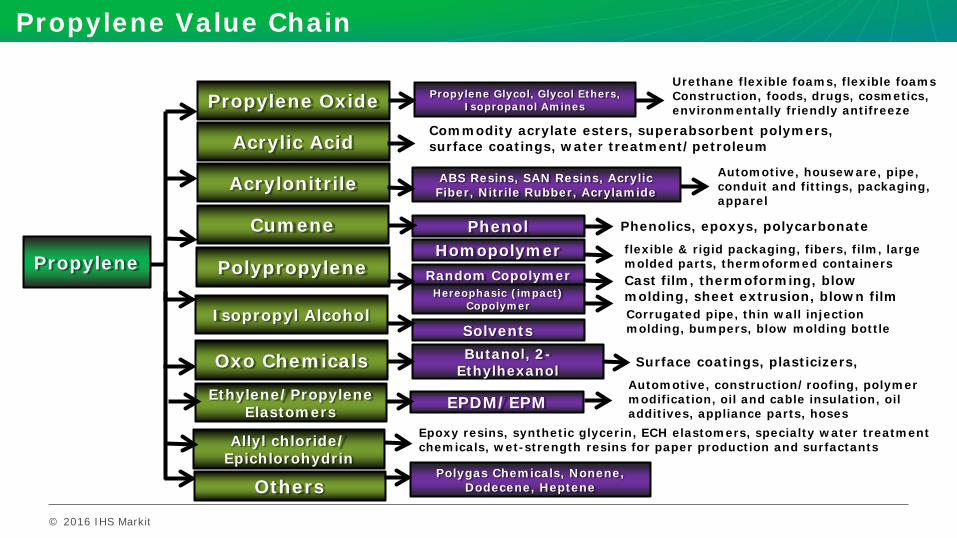

Propylene Value Chain

Propylene Oxide

Acrylonitrile

Acrylic Acid

Propylene

Cumene

Polypropylene Random Copolymer

Oxo Chemicals

Isopropyl Alcohol

Ethylene/Propylene Elastomers

Homopolymer

Hereophasic (impact) Copolymer

flexible & rigid packaging, fibers, film, large molded parts, thermoformed containers Cast film, thermoforming, blow molding, sheet extrusion, blown film Corrugated pipe, thin wall injection molding, bumpers, blow molding bottle

Phenol Phenolics, epoxys, polycarbonate

ABS Resins, SAN Resins, Acrylic Fiber, Nitrile Rubber, Acrylamide

Propylene Glycol, Glycol Ethers, Isopropanol Amines

Solvents Butanol, 2-

Ethylhexanol

EPDM/EPM

Others Polygas Chemicals, Nonene,

Dodecene, Heptene

Urethane flexible foams, flexible foams Construction, foods, drugs, cosmetics, environmentally friendly antifreeze

Commodity acrylate esters, superabsorbent polymers, surface coatings, water treatment/petroleum

Automotive, houseware, pipe, conduit and fittings, packaging, apparel

Surface coatings, plasticizers, Automotive, construction/roofing, polymer modification, oil and cable insulation, oil additives, appliance parts, hoses

Allyl chloride/ Epichlorohydrin

Epoxy resins, synthetic glycerin, ECH elastomers, specialty water treatment chemicals, wet-strength resins for paper production and surfactants

© 2016 IHS Markit

Energy & Economic Fundamentals Impact Investment Decisions

• Energy trends impact regional competitiveness and profitability

• Advantaged investments in North America, Middle East and China see lower margins in low crude oil market. “Advantaged” companies are focused on operational efficiencies in the current environment.

• Economy and energy assumptions drive key investment decisions of location, feedstock, technology, scale…

• Uncertainty results in delayed approvals; when combined with steady growth leads to tighter market conditions in basic chemical value-chains

• Crude oil (energy) “at the extremes” impacts demand for chemicals and plastics. On the high end, it can “destroy” demand and on the low end it can stimulate demand. Creates variability in the forecast.

6

© 2016 IHS Markit

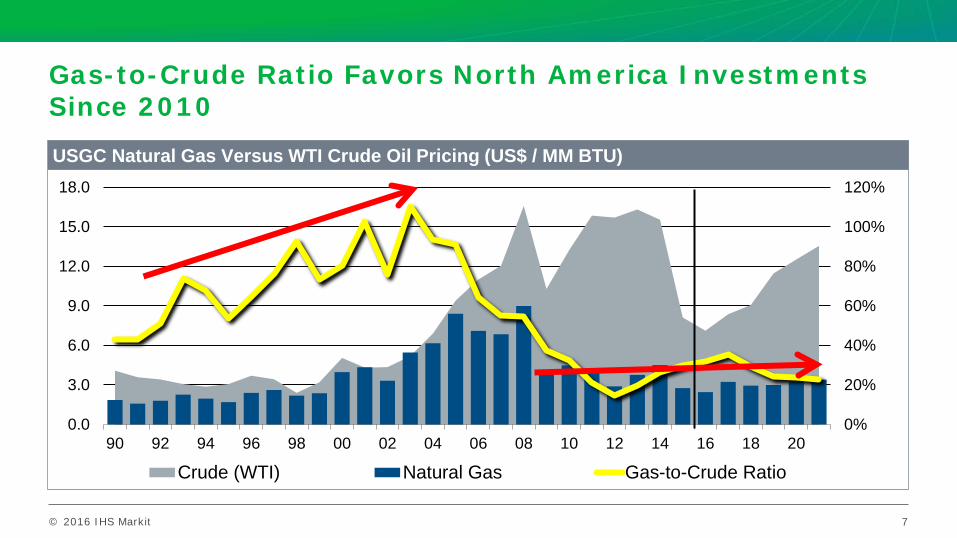

Gas-to-Crude Ratio Favors North America Investments Since 2010

0%

20%

40%

60%

80%

100%

120%

0.0

3.0

6.0

9.0

12.0

15.0

18.0

90 92 94 96 98 00 02 04 06 08 10 12 14 16 18 20

Crude (WTI) Natural Gas Gas-to-Crude Ratio

USGC Natural Gas Versus WTI Crude Oil Pricing (US$ / MM BTU)

Source: IHS

Gas

-to-C

rude

7

© 2016 IHS Markit

Impact of Changing Energy Dynamics On Regional Chemical Capacity Additions

-30%

0%

30%

60%

90%

120%

-10

0

10

20

30

40

91 93 95 97 99 01 03 05 07 09 11 13 15 17 19 21

Gas

-to

-Cru

de

Oil

BTU

Rat

io,

%

Mill

ion

Met

ric

Ton

s

China Asia Less China (with India)Middle East North AmericaWest Europe Gas-To-Crude BTU Ratio, %

Annual Change - Total Basic Chemicals Capacity: Ethylene, Propylene, Methanol, Benzene, Paraxylene, Chlorine

8

© 2016 IHS Markit

Investment Decisions, Made Years In Advance, Consider Many Factors Beyond Energy & Economy

9

Investment Drivers/Assumptions:

• Crude oil/energy price trends • Global economic growth • Geo-political considerations • North American energy market • State of industry profit cycle • China structural changes • Non-conventional technology • Sustainability • Levels of integration • Regional CAPEX differentials • Logistics investments • Evolving Technology and Impact on

Consumer Products & Markets

Braskem-Idesa Ethylene/PE Plant Nanchital, Veracruz, Mexico

Start-Up: June 2016

© 2016 IHS Markit

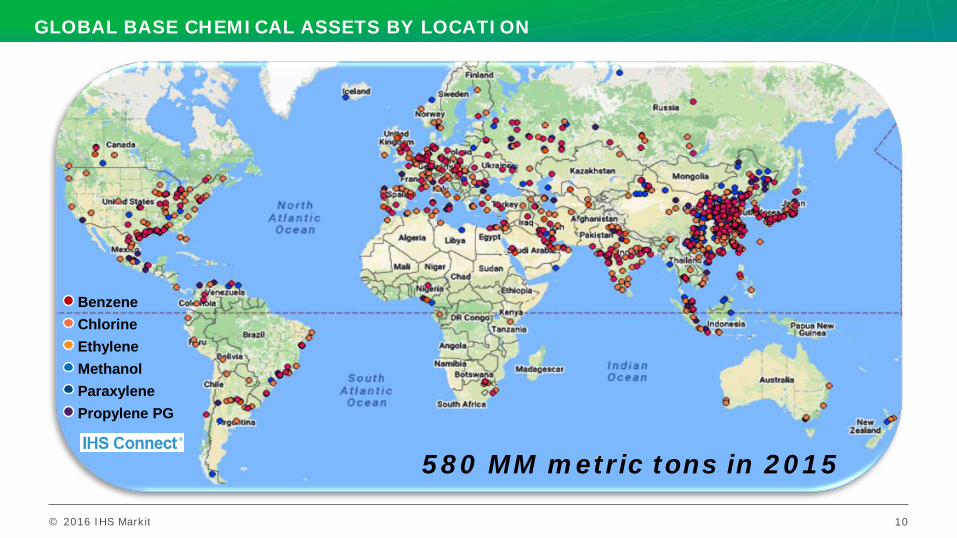

GLOBAL BASE CHEMICAL ASSETS BY LOCATION

10

Benzene Chlorine Ethylene Methanol Paraxylene Propylene PG

580 MM metric tons in 2015

© 2016 IHS Markit

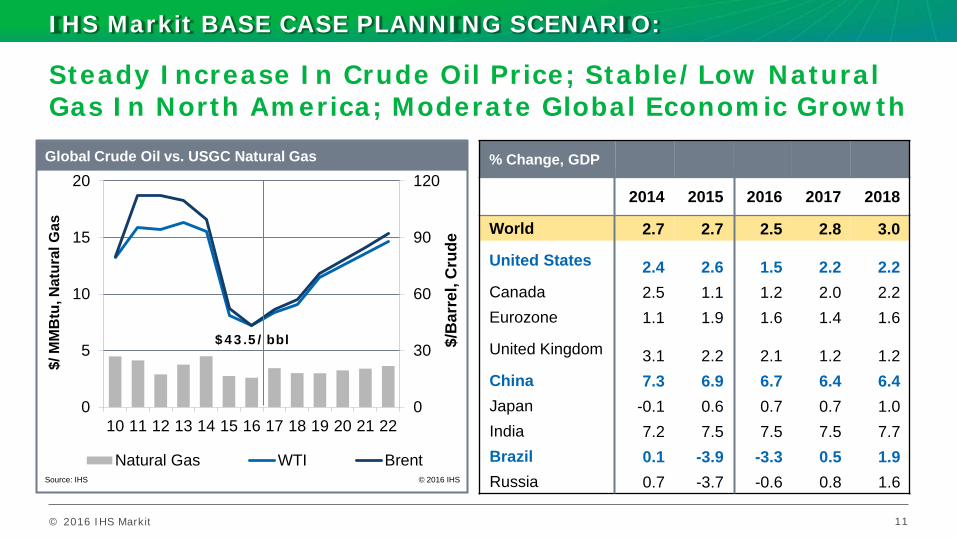

Steady Increase In Crude Oil Price; Stable/Low Natural Gas In North America; Moderate Global Economic Growth

11

% Change, GDP

2014 2015 2016 2017 2018

World 2.7 2.7 2.5 2.8 3.0

United States 2.4 2.6 1.5 2.2 2.2 Canada 2.5 1.1 1.2 2.0 2.2 Eurozone 1.1 1.9 1.6 1.4 1.6

United Kingdom 3.1 2.2 2.1 1.2 1.2 China 7.3 6.9 6.7 6.4 6.4 Japan -0.1 0.6 0.7 0.7 1.0 India 7.2 7.5 7.5 7.5 7.7 Brazil 0.1 -3.9 -3.3 0.5 1.9 Russia 0.7 -3.7 -0.6 0.8 1.6

0

30

60

90

120

0

5

10

15

20

10 11 12 13 14 15 16 17 18 19 20 21 22

Crude Oil vs. Natural Gas

Natural Gas WTI Brent

Global Crude Oil vs. USGC Natural Gas

Source: IHS © 2016 IHS

$/B

arre

l, C

rude

$/ M

MB

tu, N

atur

al G

as

$43.5/bbl

IHS Markit BASE CASE PLANNING SCENARIO:

© 2016 IHS Markit

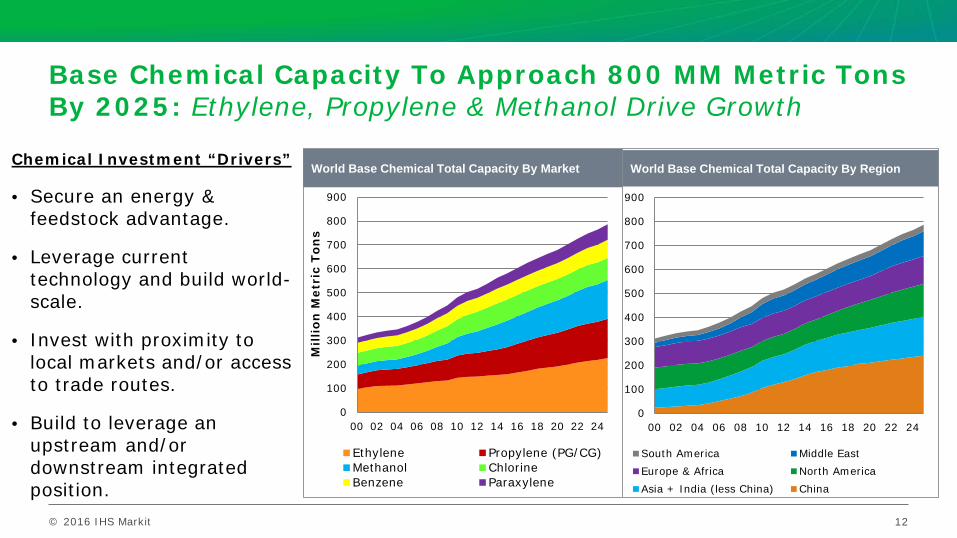

Base Chemical Capacity To Approach 800 MM Metric Tons By 2025: Ethylene, Propylene & Methanol Drive Growth

Chemical Investment “Drivers”

• Secure an energy & feedstock advantage.

• Leverage current technology and build world-scale.

• Invest with proximity to local markets and/or access to trade routes.

• Build to leverage an upstream and/or downstream integrated position.

0

100

200

300

400

500

600

700

800

900

00 02 04 06 08 10 12 14 16 18 20 22 24

Mil

lion

Met

ric

Ton

s

Ethylene Propylene (PG/CG)Methanol ChlorineBenzene Paraxylene

World Base Chemical Total Capacity By Market

12

0

100

200

300

400

500

600

700

800

900

00 02 04 06 08 10 12 14 16 18 20 22 24

South America Middle EastEurope & Africa North AmericaAsia + India (less China) China

World Base Chemical Total Capacity By Region

© 2016 IHS Markit

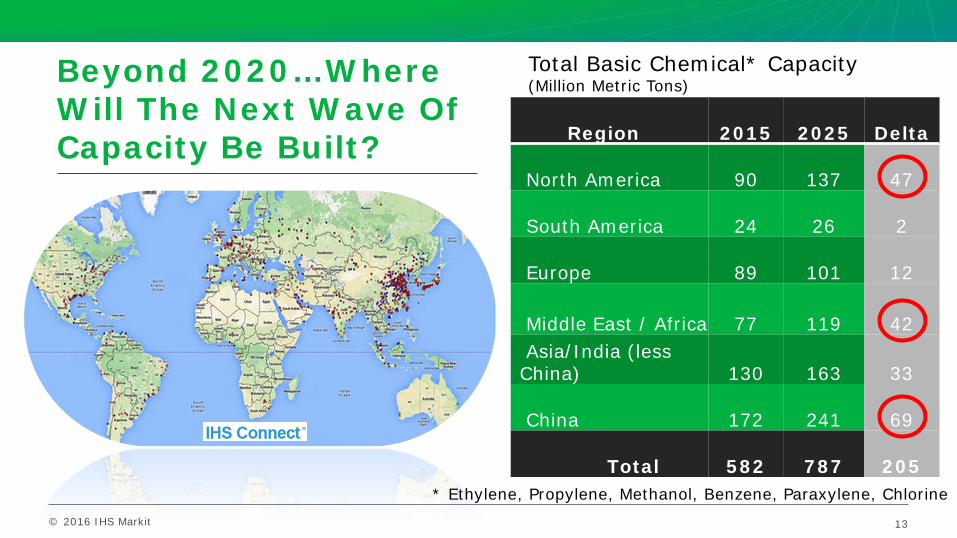

Beyond 2020…Where Will The Next Wave Of Capacity Be Built? Region 2015 2025 Delta

North America

90

137

47

South America

24

26 2

Europe

89

101

12

Middle East / Africa

77

119

42 Asia/India (less China)

130

163

33

China

172

241

69

Total

582

787

205

Total Basic Chemical* Capacity (Million Metric Tons)

* Ethylene, Propylene, Methanol, Benzene, Paraxylene, Chlorine

13

© 2016 IHS Markit

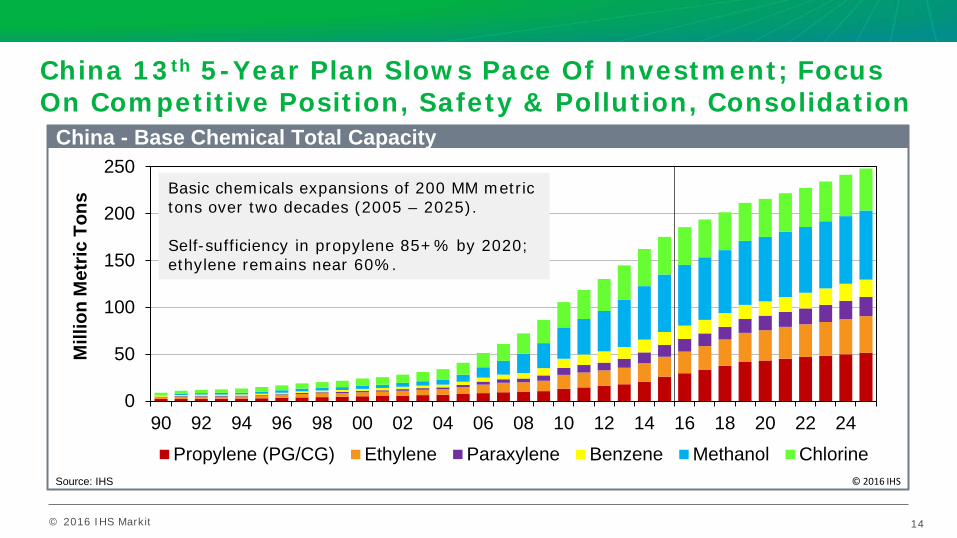

China 13th 5-Year Plan Slows Pace Of Investment; Focus On Competitive Position, Safety & Pollution, Consolidation

0

50

100

150

200

250

90 92 94 96 98 00 02 04 06 08 10 12 14 16 18 20 22 24

Propylene (PG/CG) Ethylene Paraxylene Benzene Methanol Chlorine

China - Base Chemical Total Capacity

Source: IHS © 2016 IHS

Mill

ion

Met

ric T

ons

14

Basic chemicals expansions of 200 MM metric tons over two decades (2005 – 2025). Self-sufficiency in propylene 85+% by 2020; ethylene remains near 60%.

14

© 2016 IHS Markit

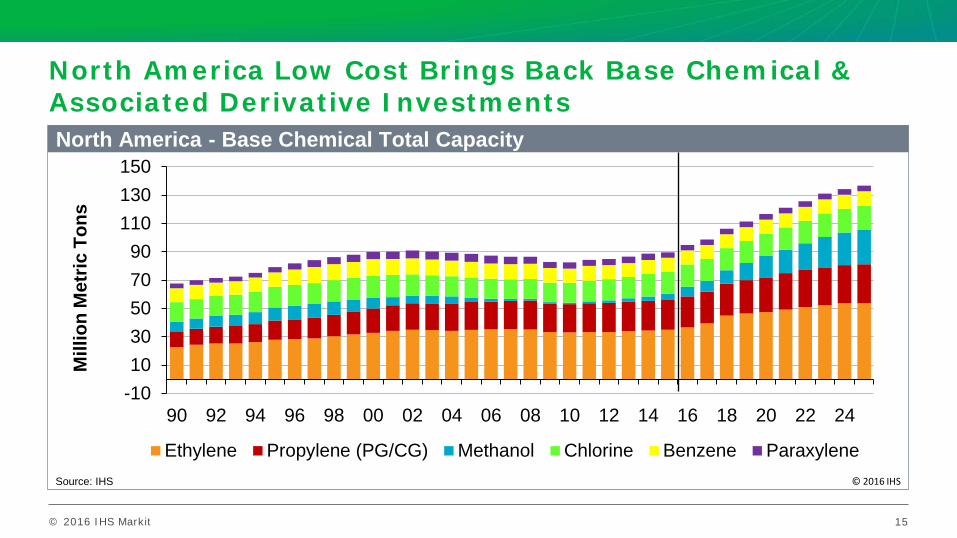

North America Low Cost Brings Back Base Chemical & Associated Derivative Investments

-101030507090

110130150

90 92 94 96 98 00 02 04 06 08 10 12 14 16 18 20 22 24

Ethylene Propylene (PG/CG) Methanol Chlorine Benzene Paraxylene

North America - Base Chemical Total Capacity

Source: IHS © 2016 IHS

Mill

ion

Met

ric T

ons

15

© 2016 IHS Markit

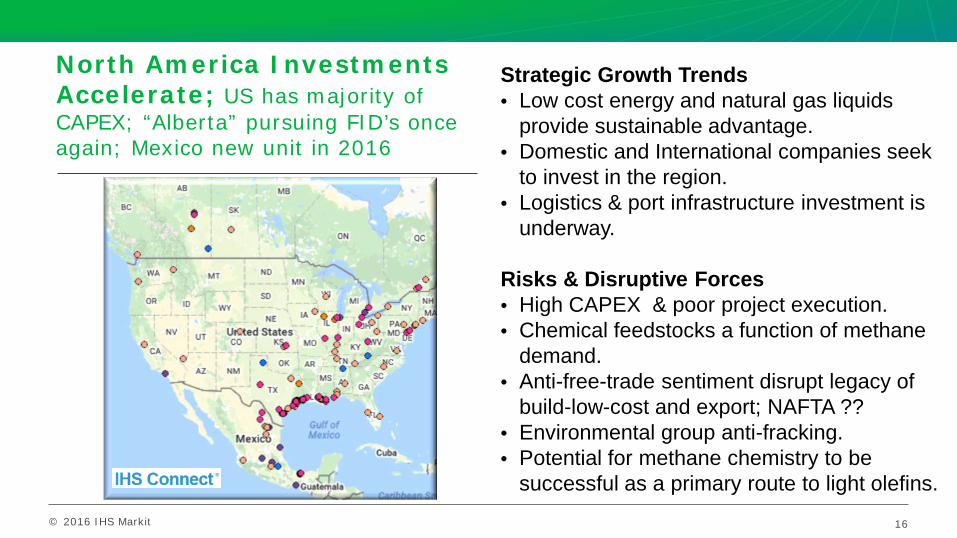

North America Investments Accelerate; US has majority of CAPEX; “Alberta” pursuing FID’s once again; Mexico new unit in 2016

Strategic Growth Trends • Low cost energy and natural gas liquids

provide sustainable advantage. • Domestic and International companies seek

to invest in the region. • Logistics & port infrastructure investment is

underway. Risks & Disruptive Forces • High CAPEX & poor project execution. • Chemical feedstocks a function of methane

demand. • Anti-free-trade sentiment disrupt legacy of

build-low-cost and export; NAFTA ?? • Environmental group anti-fracking. • Potential for methane chemistry to be

successful as a primary route to light olefins.

16

© 2016 IHS Markit

Propylene

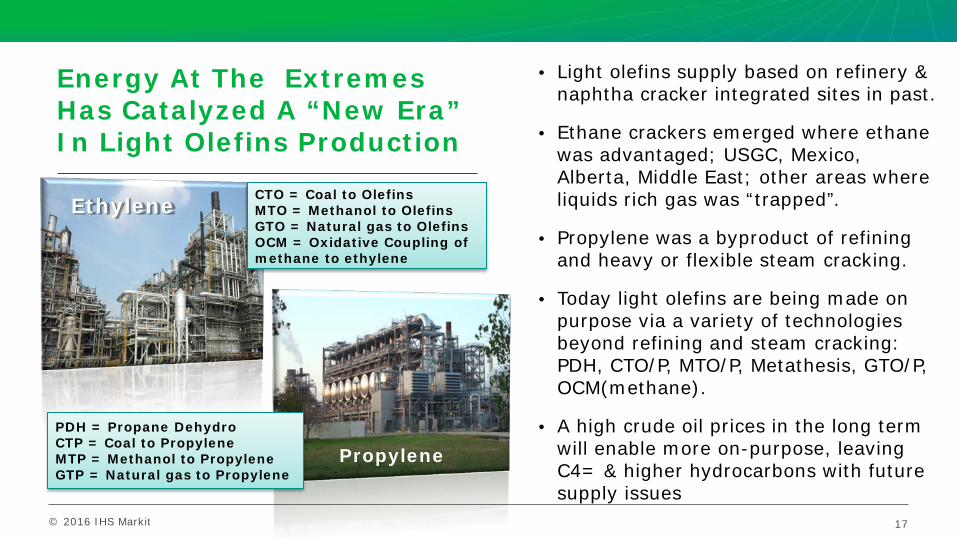

Energy At The Extremes Has Catalyzed A “New Era” In Light Olefins Production

17

• Light olefins supply based on refinery & naphtha cracker integrated sites in past.

• Ethane crackers emerged where ethane was advantaged; USGC, Mexico, Alberta, Middle East; other areas where liquids rich gas was “trapped”.

• Propylene was a byproduct of refining and heavy or flexible steam cracking.

• Today light olefins are being made on purpose via a variety of technologies beyond refining and steam cracking: PDH, CTO/P, MTO/P, Metathesis, GTO/P, OCM(methane).

• A high crude oil prices in the long term will enable more on-purpose, leaving C4= & higher hydrocarbons with future supply issues

Ethylene CTO = Coal to Olefins MTO = Methanol to Olefins GTO = Natural gas to Olefins OCM = Oxidative Coupling of methane to ethylene

PDH = Propane Dehydro CTP = Coal to Propylene MTP = Methanol to Propylene GTP = Natural gas to Propylene

© 2016 IHS Markit

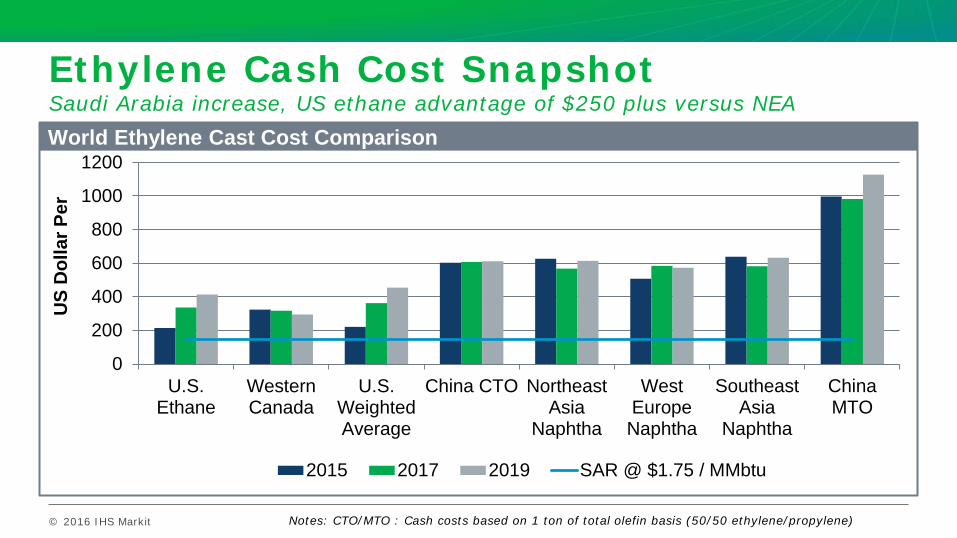

Ethylene Cash Cost Snapshot Saudi Arabia increase, US ethane advantage of $250 plus versus NEA

0

200

400

600

800

1000

1200

U.S.Ethane

WesternCanada

U.S.WeightedAverage

China CTO NortheastAsia

Naphtha

WestEuropeNaphtha

SoutheastAsia

Naphtha

ChinaMTO

2015 2017 2019 SAR @ $1.75 / MMbtu

World Ethylene Cast Cost Comparison

US

Dol

lar P

er

Notes: CTO/MTO : Cash costs based on 1 ton of total olefin basis (50/50 ethylene/propylene)

© 2016 IHS Markit

Ethylene Market Key Issues

19

• New Ethylene Capacity: delayed start up timing of all “first wave” US ethylene units. Pushed out and/or removed MTO, CTO) in China

• Build-cycle Disruption: under investing new capacity during 2020-21 period; supporting margin “up-cycle” .

• Effective Global Operating Rates: expected high over the next 5 years assuming steady economic growth, current new-build profile, unplanned outages.

• Naphtha crackers: required to balance demand; increasing cash cost combined with need for naphtha cracking, push ethylene prices higher.

© 2016 IHS Markit

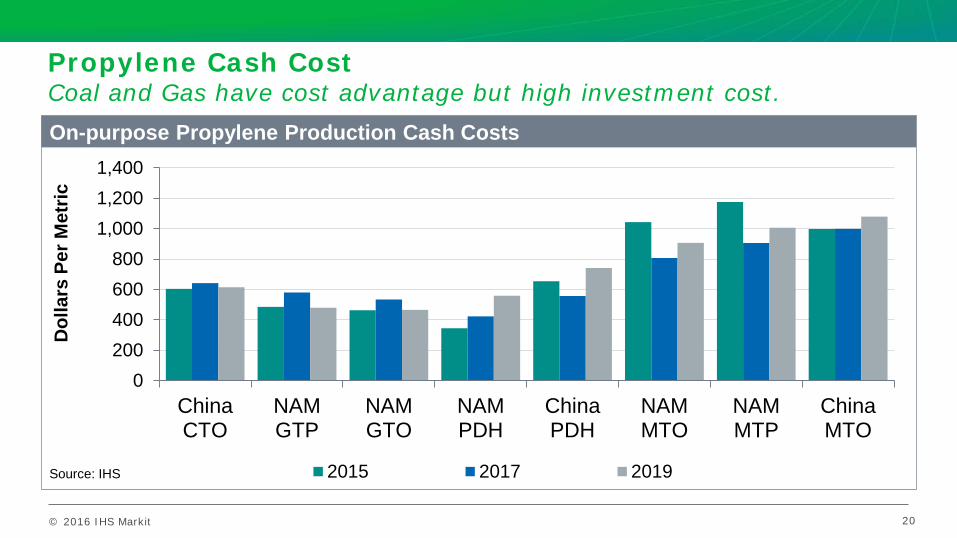

Propylene Cash Cost Coal and Gas have cost advantage but high investment cost.

20

0200400600800

1,0001,2001,400

ChinaCTO

NAMGTP

NAMGTO

NAMPDH

ChinaPDH

NAMMTO

NAMMTP

ChinaMTO

2015 2017 2019

On-purpose Propylene Production Cash Costs

Source: IHS

Dol

lars

Per

Met

ric

© 2016 IHS Markit

Propylene Market Key Issues

Propylene Requires On-Purpose Investment: margins for incremental supply will have to support new investments On-Purpose Technology Will Vary: dependent on regional feedstock advantage - PDH in U.S., Middle East, and Asia along with coal to olefins in China; Chinese PDH units based on propane imports that compete into fuels market. MTP is high cost. Build phase is delayed: investment in North American on-purpose propylene production delayed as questions over energy and the economy persist; “GTP under study”. Regional imbalance causes price volatility: overcapacity in propylene will cause major price shifts regionally but balance out over time. US monomer balance is long, derivatives are tighter. Low prices stimulate demand: propylene demand growth is seeing strength due to ample low cost supplies.

21

© 2016 IHS Markit © 2016 IHS Markit. All Rights Reserved.

Global Energy Markets & Alberta Leveraging the Alberta legacy to attract new waves of petrochemical industry investment

BUILDING ALBERTA'S INNOVATION AND INVESTMENT 18th Annual Stakeholder Luncheon Thursday, January 19, 2017 Edmonton, Alberta, Canada

Mark Eramo, VP Global Business Development Oil / Midstream / Downstream & Chemicals Houston, TX [email protected]

THANK YOU !!