Globalisation and the Knowledge Economy – the Case of Ireland

Andrew McDowell

Chief Economist

October 2006

2

MAY 1997MAY 1997

►

1988 1997 2004

The Development of the Irish Economy

3

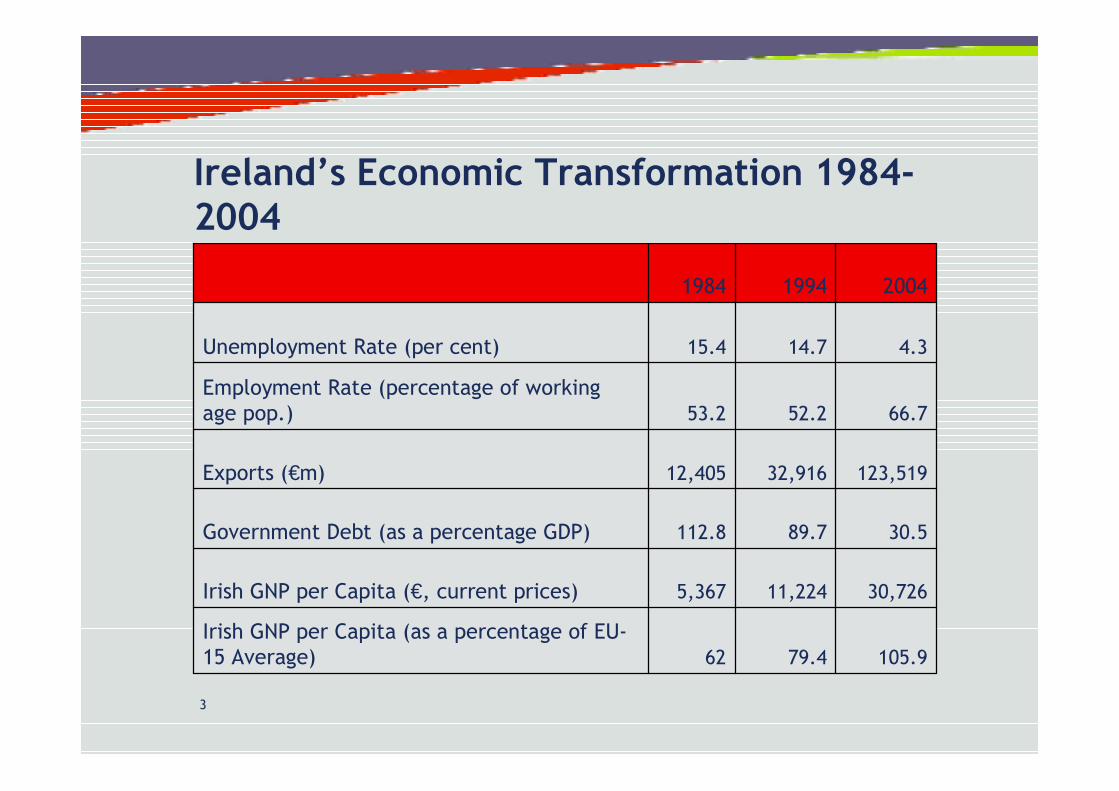

Ireland’s Economic Transformation 1984-2004

105.979.462Irish GNP per Capita (as a percentage of EU-15 Average)

30,72611,2245,367Irish GNP per Capita (€, current prices)

30.589.7112.8Government Debt (as a percentage GDP)

123,51932,91612,405Exports (€m)

66.752.253.2Employment Rate (percentage of working age pop.)

4.314.715.4Unemployment Rate (per cent)

200419941984

4

The Global Economic Landscape is Changing More Rapidly than Ever Before

► Increasing share of services in output and employment, and declining roles of manufacturing and agriculture

► Growing importance of knowledge flows as a driver of economic growth

► Greater foreign ownership► Greater people mobility (skilled and unskilled)► Offshoring

5

The Global Economic Landscape is Changing More Rapidly than Ever Before

► How are these trends affecting Ireland, and how is Irish economic policy responding?

6

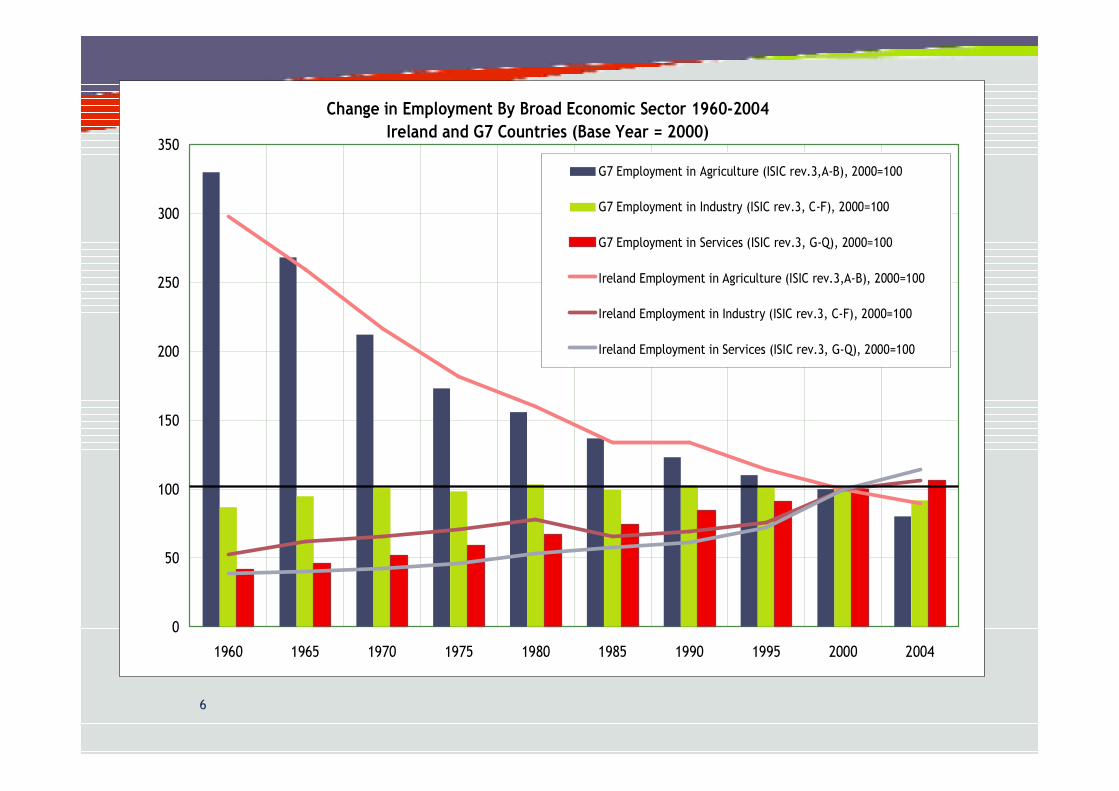

Change in Employment By Broad Economic Sector 1960-2004 Ireland and G7 Countries (Base Year = 2000)

0

50

100

150

200

250

300

350

1960 1965 1970 1975 1980 1985 1990 1995 2000 2004

Thou

sand

s

G7 Employment in Agriculture (ISIC rev.3,A-B), 2000=100

G7 Employment in Industry (ISIC rev.3, C-F), 2000=100

G7 Employment in Services (ISIC rev.3, G-Q), 2000=100

Ireland Employment in Agriculture (ISIC rev.3,A-B), 2000=100

Ireland Employment in Industry (ISIC rev.3, C-F), 2000=100

Ireland Employment in Services (ISIC rev.3, G-Q), 2000=100

7

8

Manufacturing Employment – 1995/2005Select OECD Economies

Share of Manufacturing as % of Total Employment - 1995, 2005*

40.58%

30.06%

26.27%

23.42%

20.88%

16.78%

13.21%

10.11%11.30%

25.84% 25.17%

18.63% 18.00%

27.25%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

Czech Rep. Poland Hungary Korea Switzerland Ireland USA

1995 2005*

9

Employment (000s) within Manufacturing, 1995-2005

0 5000 10000 15000 20000 25000 30000 35000 40000 45000 50000

Food& Beverages; Tobacco

Textiles/Leather

Wood/Paper

Chemicals

Materials & Minerals

Electricial Machinery & Euipment

Modern Machinery

Medical, & Optical Instruments

Transport equipment

Manufacturing N.E.C

Number of Employees (000s)

1995 Q4 2000 Q4 2005 Q3

10

Services – Export Performance

Growth in Services and Merchandise Exports (1998-2005) Base Year = 1998

0

50

100

150

200

250

300

350

400

1998 1999 2000 2001 2002 2003 2004 2005

Merchandise

Services

11

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005

Services M erchandise

Ireland’s Global Market Share

12

1.20%

1.23%

1.17%

1.49%

2.63%

2.26%

0.21%

0.49%

2.01%

4.78%

0.12%

0.30%

0.40%

0.55%

2.15%

4.34%

1.05%

0.12%

0.66%

0.80%

1.40%

4.10%

0% 1% 2% 3% 4% 5% 6%

Total Merchandise

Total Services

Fuels and Mining

Textiles

Transportation Services

Travel Services

Machinery

Food

Office and Telecom

Other Services

Chemicals

Ranked by 2005 World Market Share

2005

2000

Ireland’s Global Market Share

13

3.15.35.45.6

7.88.08.9

10.612.3

15.015.1

19.520.321.0

31.834.1

63.091.1

102.6

0 20 40 60 80 100 120

JapanItalyUS

KoreaGermany

FranceNetherlands

OECDPolandFinland

SpainNew Zealand

UKSwitzerland

SwedenDenmarkHungary

IrelandSingapore

Number of Greenfield Projects by Destination (per million of population)

FDI Greenfield Projects

14

Export Performance by Ownership

Irish Manufacturing Exports (Agency Assisted Companies) 1995-2004

0

10

20

30

40

50

60

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004

€ Bi

llion

s

Indigenous Foreign Owned Companies

15

Irish FDI Outflows as a % of OECD Outflows

0.0%0.2%0.4%0.6%0.8%1.0%1.2%1.4%1.6%1.8%2.0%

1999 2000 2001 2002 2003 2004 2005Per

cent

age

of O

EC

D FD

I out

flow

s

Ireland FDI Outflow as % OECD FDI Outflow s

16

4.3

-0.2

1.8

3.1

-0.2

0.5

9.4

-0.5

4.2 4.1

-1.0

0.7

-2

0

2

4

6

8

10

Ireland Northern Ireland EU 15 US NEU 10 Japan

Mig

rant

s pe

r 1,0

00 o

f pop

ulat

ion

1995-1999 2000-2004

People Mobility

17

Emerging Policy Developments / Challenges

► Industrial policy►Research/ innovation policy►Fiscal/tax policy►Labour market policy►Regional policy/land and infrastructure planning►Education and training

18

Industrial Policy

► Continued pro-active / well resourced / highly skilled industrial development agencies

► Manufacturing – no special policy supports► FDI – no backlash after 2000 downturn► New EU state aid disciplines – gradual shift to

environmental/ R&D /skills supports► Mobile R&D investments - IDA/SFI partnership ► Smaller indigenous industry – policy emphasis on export

promotion, mgt. development, risk capital market development and R&D supports

► Outsourcing – policy neutral approach – some “soft support” for ODI for market development

19

Research / Innovation Policy

►Science Foundation Ireland►Creation of “4th level” education system -

doubling of PhD graduates by 2013►New university codes for management of IP

from publicly funded research►Coherence between research funding priorities

and industrial strategy►SME and services innovation policy?►Universities and applied research?

20

Fiscal Policy

►Global competition demands both higher spending on physical/ knowledge infrastructure and social supports and competitive tax rates• Greater pressure for public sector efficiencies• New financing models for infrastructure (user charges)• Shift from direct to indirect taxes (VAT, property)

►Corporate tax competition►Taxation of R&D and intellectual property►Extension of tax treaty network

21

Labour Market Policy

►Economic restructuring• Current forecasts suggest absolute declines in

employment only for farm workers and plant and machinery operators – natural demographic churn

► Immigration• Open access to new EU Members since 2004• New “green card” system for skilled non-EU migrants

►Hiring and firing• New protections against dislocation by immigrants• Social welfare replacement rates remain low• Application of Danish flexicurity model to Ireland?

22

Regional Policy / Land Planning

►Clustering of high-skilled jobs in urban areas► Increasing importance of creating attractive

metropolitan areas – social/cultural/ recreational infrastructure

►Rapidly rising urban land prices►More integrated land/transport planning►National Spatial Strategy►Rural economy? Continued direct and indirect

subsidies for agriculture, tourism, fisheries

23

Education and Training

►Education• Need to address polarisation of education outcomes• Need to complement academic system of education

with vocational stream• Growing demand for graduates – 65% of school leavers

to go on to higher education• Increasing emphasis on “soft generic” skills –

communications, team-working, conceptual

►Upskilling• National Training Fund• SkillNets

24

Responding to Change

“When the pace of change on the outside exceeds the pace of change on the inside then the end is in sight”

………………….Jack Welsh